stochastic optimal control in mathematical finance

TRANSCRIPT

Jan Kallsen

Stochastic Optimal Control inMathematical Finance

CAU zu Kiel, WS 15/16, as of April 21, 2016

Contents

0 Motivation 4

I Discrete time 7

1 Recap of stochastic processes 81.1 Processes, stopping times, martingales . . . . . . . . . . . . . . . . . . . . 81.2 Stochastic integration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161.3 Conditional jump distribution . . . . . . . . . . . . . . . . . . . . . . . . . 221.4 Essential supremum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2 Dynamic Programming 27

3 Optimal Stopping 34

4 Markovian situation 40

5 Stochastic Maximum Principle 45

II Continuous time 60

6 Recap of stochastic processes 626.1 Continuous semimartingales . . . . . . . . . . . . . . . . . . . . . . . . . 62

6.1.1 Processes, stopping times, martingales . . . . . . . . . . . . . . . . 626.1.2 Brownian motion . . . . . . . . . . . . . . . . . . . . . . . . . . . 686.1.3 Quadratic variation . . . . . . . . . . . . . . . . . . . . . . . . . . 696.1.4 Square-integrable martingales . . . . . . . . . . . . . . . . . . . . 726.1.5 Stopping times . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

6.2 Stochastic integral . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 746.2.1 Differential notation . . . . . . . . . . . . . . . . . . . . . . . . . 806.2.2 Ito processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 806.2.3 Ito diffusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 816.2.4 Doléans exponential . . . . . . . . . . . . . . . . . . . . . . . . . 836.2.5 Martingale representation . . . . . . . . . . . . . . . . . . . . . . 856.2.6 Change of measure . . . . . . . . . . . . . . . . . . . . . . . . . . 85

2

CONTENTS 3

7 Dynamic programming 87

8 Optimal stopping 90

9 Markovian situation 959.1 Stochastic control . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 959.2 Optimal Stopping . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

10 Stochastic maximum principle 102

Bibliography 108

Chapter 0

Motivation

In Mathematical Finance one often faces optimization problems of various kinds, in par-ticular when it comes to choosing trading strategies with in some sense maximal utility orminimal risk. The choice of an optimal exercise time of an American option belongs to thiscategory as well. Such problems can be tackled with different methods. We distinguish twomain approaches, which are discussed both is discrete and in continuous time. As a motiva-tion we first consider the simple situation of maximizing a deterministic function of one orseveral variables.

Example 0.1 1. (Direct approach) Suppose that the goal is to maximize a function

(x, α) 7→T∑t=1

f(t, xt−1, αt) + g(xT )

over all x = (x1, . . . , xT ) ∈ (Rd)T , α = (α1, . . . , αT ) ∈ AT such that

∆xt := xt − xt−1 = δ(xt−1, αt), t = 1, . . . , T

for some given function δ : Rd × Rm → Rd. The initial value x0 ∈ Rd, the statespace of controls A ⊂ Rm and the objective functions f : 1, . . . , T×Rd×A→ R,g : Rd → R are supposed to be given. The approach in Chapters 2 and 7 below corre-sponds to finding the maximum directly, without relying on smoothness or convexityof the functions f, g, δ or on topological properties of A. Rather, the idea is to reducethe problem to a sequence of simpler optimizations in just one A-valued variable αt.

2. (Lagrange multiplier approach) Since the problem above concerns constrained opti-mization, Lagrange multiplier techniques may make sense. To this end, define theLagrange function

L(x, α, y) :=T∑t=1

f(t, xt−1, αt) + g(xT )−T∑t=1

yt(∆xt − δ(xt−1, αt))

on (Rd)T×AT×(Rd)T . The usual first-order conditions lead us to look for a candidatex? ∈ (Rd)T , α? ∈ AT , y? ∈ (Rd)T satisfying

(a) ∆x?t = δ(x?t−1, α?t ) for t = 1, . . . , T , where we set x?0 := x0,

4

5

(b) y?T = ∇g(x?T ),

(c) ∆y?t = −∇xH(t, x?t−1, α?t ) for t = 1, . . . , T, where we set H(t, ξ, a) :=

f(t, ξ, a) + y?t δ(ξ, a) and ∇xH denotes the gradient of H viewed as a functionof its second argument,

(d) α?t maximizes a 7→ H(t, x?t−1, a) on A for t = 1, . . . , T .

Provided that some convexity conditions hold, a–d) are in fact sufficient for optimalityof α?:

Lemma 0.2 Suppose that the set A is convex, ξ 7→ g(ξ), (ξ, a) 7→ H(t, ξ, a), t =1, . . . , T are concave and ξ 7→ g(ξ), ξ 7→ H(t, ξ, a), t = 1, . . . , T , a ∈ A aredifferentiable. If Conditions a–d) hold, then (x?, α?) is optimal for the problem inExample 0.1(1).

Proof. For any competitor (x, α) satisfying the constraints set h(t, ξ) :=supa∈AH(t, ξ, a). Condition d) yields h(t, x?t−1) = H(t, x?t−1, α

?t ) for t = 1, . . . , T .

We have

T∑t=1

f(t, xt−1, αt) + g(xT )−T∑t=1

f(t, x?t−1, α?t )− g(x?T )

=T∑t=1

(H(t, xt−1, αt)−H(t, x?t−1, α

?t )− y?t (∆xt −∆x?t )

)+ g(xT )− g(x?T )

≤T∑t=1

((H(t, xt−1, αt)− h(t, xt−1)) +

(h(t, xt−1)− h(t, x?t−1)

)− y?t (∆xt −∆x?t )

)+∇g(x?T )(xT − x?T )

≤T∑t=1

(∇xh(t, x?t−1)(xt−1 − x?t−1)− y?t (∆xt −∆x?t )

)+∇g(x?T )(xT − x?T ) (0.1)

=T∑t=1

(−∆y?t (xt−1 − x?t−1)− y?t (∆xt −∆x?t )

)+ y?T (xT − x?T ) (0.2)

= y?0(x0 − x?0)

= 0

where existence of ∇xh(t, x?t−1), inequality (0.1) as well as equation (0.2) followfrom Lemma 0.3 below and the concavity of g.

Under some more convexity (e.g. if δ is affine and f(t, ·, ·) is concave for t =1, . . . , T ), the Lagrange multiplier solves some dual minimisation problem. This hap-pens e.g. in the stochastic examples 5.3–5.8 in Chapter 5.

6 CHAPTER 0. MOTIVATION

The following lemma is a version of the envelope theorem which makes a statement onthe derivative of the maximum of a parametrised function.

Lemma 0.3 Let A be a convex set, f : Rd × A → R ∪ −∞ a concave function, andf(x) := supa∈A f(x, a), x ∈ Rd. Then f is concave. Suppose in addition that, for some fixedx? ∈ Rd, the optimizer a? := argmaxa∈Af(x?, a) exists and x 7→ f(x, a?) is differentiablein x?. Then f is differentiable in x? with derivative

Dif(x?) = Dif(x?, a?), i = 1, . . . , d. (0.3)

Proof. One easily verifies that f is concave. For h ∈ Rd we have

f(x? + yh) ≥ f(x? + yh, a?)

= f(x?, a?) + y

d∑i=1

Dif(x?, a?)hi + o(y)

as y ∈ R tends to 0. In view of [HUL13, Proposition I.1.1.4], concavity of f implies thatwe actually have

f(x? + yh) ≤ f(x?, a?) + yd∑i=1

Dif(x?, a?)hi

and hence differentiability of f in x? with derivative (0.3).

In the remainder of this course we consider optimization in a dynamic stochastic setup.Green parts in these notes are skipped either because they are assumed to be known (Chap-ters 1 and 6) or for lack of time. Comments are welcome, in particular if they concern errorsin this text.

Part I

Discrete time

7

Chapter 1

Recap of stochastic processes

The theory of stochastic processes deals with random functions of time as e.g. asset prices,interest rates, or trading strategies. As is true for Mathematical Finance as well, it canbe developped in both discrete and continuous time. Actual calculations are sometimeseasier and more transparent in continuous-time models, but the theory typically requiresless background in discrete time.

1.1 Processes, stopping times, martingales

The natural starting point in probability theory is a probability space (Ω,F , P ). The moreor less abstract sample space Ω stands for the possible outcomes of the random experiment.It could e.g. contain all conceivable sample paths of a stock price process. The probabilitymeasure P assigns probabilities to subsets of outcomes. For measure theoretic reasons it istypically impossible to assign probabilities to all subsets of Ω in a consistent manner. Asa way out one specifies a σ-field F , i.e. a collection of subsets of Ω which is closed undercountable set operations as e.g. ∩,∪, \, C . The probability P (F ) is defined only for eventsF ∈ F .

Random variables X are functions of the outcome ω ∈ Ω. Typically its values X(ω)are numbers but they may also be vectors or even functions, in which case X is a randomvector resp. process. We denote by E(X), Var(X) the expected value and variance of areal-valued random variable. Accordingly, E(X), Cov(X) denote the expectation vectorand covariance matrix of a random vector X .

For static random experiments one needs to consider only two states of information.Before the experiment nothing precise is known about the outcome, only probabilities andexpected values can be assigned. After the experiment the outcome is completely deter-mined. In dynamic random experiments as e.g. stock markets the situation is more involved.During the time interval of observation, some random events (e.g. yesterday’s stock returns)have already happened and can be considered as deterministic whereas others (e.g. tomor-rows’ stock returns) still belong to the unknown future. As time passes, more and moreinformation is accumulated.

This increasing knowledge is expressed mathematically in terms of a filtration F =(Ft)t≥0, i.e. an increasing sequence of sub-σ-fields of F . The collection of events Ft

stands for the observable information up to time t. The statement F ∈ Ft means that the

8

1.1. PROCESSES, STOPPING TIMES, MARTINGALES 9

random event F (e.g. F = stock return positive at time t−1) is no longer random at time t.We know for sure whether it is true or not. If our observable information is e.g. given by theevolution of the stock price, then Ft contains all events that can be expressed in terms of thestock price up to time t. The quadrupel (Ω,F ,F, P ) is called filtered probability space.We consider it to be fixed during most of the following. Often one assumes F0 = ∅,Ω,i.e. F0 is the trivial σ-field corresponding to no prior information.

As time passes, not only the observable information but also probabilities and expec-tations of future events change. E.g. our conception of the terminal stock price evolvesgradually from vague ideas to perfect knowledge. This is modelled mathematically in termsof conditional expectations. The conditional expectation E(X|Ft) of a random variable Xis its expected value given the information up to time t. As such, it is not a number but itselfa random variable which may depend on the randomness up to time t, e.g. on the stock priceup to t in the above example. Mathematically speaking, Y = E(X|Ft) is Ft-measurable,which means that Y ∈ B := ω ∈ Ω : Y (ω) ∈ B ∈ Ft for any reasonable (i.e. Borel)setB. Accordingly, the conditional probability P (F |Ft) denotes the probability of an eventF ∈ F given the information up to time t. As is true for conditional expectation, it is not anumber but an Ft-measurable random variable.

Formally, the conditional expectationE(X|Ft) is defined as the unique Ft-measurablerandom variable Y such that E(XZ) = E(Y Z) for any bounded, Ft-measurable randomvariable Z. It can also be interpreted as the best prediction of X given Ft. Indeed, ifE(X2) < ∞, then E(X|Ft) minimizes the mean squared difference E((X − Z)2) amongall Ft-measurable random variables Z. Strictly speaking, E(X|Ft) is unique only up to aset of probability 0, i.e. any two versions Y, Y satisfy P (Y 6= Y ) = 0. In this notes we donot make such fine distinctions. Equalities, inequalities etc. are always meant to hold onlyalmost surely, i.e. up to a set of probability 0.

A few rules on conditional expectations are used over and over again. E.g. we have

E(X|Ft) = E(X) (1.1)

if Ft = ∅,Ω is the trivial σ-field representing no information on random events. Moregenerally, (1.1) holds if X and Ft are stochastically independent, i.e. if

P (X ∈ B ∩ F ) = P (X ∈ B)P (F )

for any reasonable (i.e. Borel) set B and any F ∈ Ft. On the other hand we haveE(X|Ft) = X and more generally

E(XY |Ft) = XE(Y |Ft)

if X is Ft-measurable, i.e. known at time t. The law of iterated expectations tells us that

E(E(X|Ft)

∣∣Fs

)= E(X|Fs)

for s ≤ t. Almost as a corollary we have

E(E(X|Ft)

)= E(X).

Finally, the conditional expectation shares many properties of the expectation, e.g, it is linearand monotone in X and it satisfies monotone and dominated convergence, Fatou’s lemma,Jensen’s inequality etc.

10 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

Recall that the probability of a set can be expressed as expectation of an indicator func-tion via P (F ) = E(1F ). This suggests to use the relation

P (F |Ft) := E(1F |Ft) (1.2)

to define conditional probabilities in terms of conditional expectation. Of course, we wouldlike P (F |Ft) to be a probability measure when it is considered as a function of F . Thisproperty, however, is not as evident as it seems because of the null sets involved in the defi-nition of conditional expectation. We do not worry about technical details here and assumeinstead that we are given a regular conditional probability, i.e. a version of P (F |Ft)(ω)which, for any fixed ω, is a probability measure when viewed as a function of F . Such aregular version exists in all instances where it is used in this notes.

In line with (1.2) we denote by

PX|Ft(B) := P (X ∈ B|Ft) := E(1B(X)|Ft)

the conditional law of X given Ft. A useful rule states that

E(f(X, Y )|Ft) =

∫f(x, Y )PX|Ft(dx) (1.3)

for real-valued functions f and Ft-measurable random variables Y . If X is stochasticallyindependent of Ft, we have PX|Ft = PX , i.e. the conditional law of X coincides with thelaw of X . In this case, (1.3) turns into

E(f(X, Y )|Ft) =

∫f(x, Y )PX(dx) (1.4)

for Ft-measurable random variables Y .A stochastic process X = (X(t))t≥0 is a collection of random variables X(t), indexed

by time t. In this section, the time set is assumed to be N = 0, 1, 2, . . . , afterwardswe consider continuous time R+ = [0,∞). As noted earlier, a stochastic process X =(X(t))t≥0 can be interpreted as a random function of time. Indeed, X(ω, t) is a functionof t (or sequence in the current discrete case) for fixed ω. Sometimes, it is also convenientto interpret a process X as a real-valued function on the product space Ω × N or Ω × R+,respectively. In the discrete time case we use the notation

∆X(t) := X(t)−X(t− 1).

Moreover we denote by X− = (X−(t))t≥0 the process

X−(t) :=

X(t− 1) for t ≥ 1,X(0) for t = 0.

(1.5)

We will only consider processes which are consistent with the information structure, i.e.X(t) is supposed to be observable at time t. Mathematically speaking, we assume X(t) tobe Ft-measurable for any t. Such processes X are called adapted (to the filtration F).

There is in fact a minimal filtration F such that X is F-adapted. Formally, this filtrationis given by

Ft = σ(X(s) : s ≤ t), (1.6)

1.1. PROCESSES, STOPPING TIMES, MARTINGALES 11

i.e. Ft is the smallest σ-field such that all X(s), s ≤ t are Ft-measurable. Intuitively, thismeans that the only information on random events is coming from observing the process X .One calls F the filtration generated by X .

For some processes one actually needs a stronger notion of measurability than adapted-ness, namely predictability. A stochastic process X is called predictable if X(t) is knownalready one period in advance, i.e. X(t) is Ft−1-measurable. The use of this notion willbecome clearer in Section 1.2.

Example 1.1 (Random walk and geometric random walk) We call an adapted process Xrandom walk (relative to F) if the increments ∆X(t), t ≥ 1 are identically distributedand independent of Ft−1. We obtain such a process if ∆X(t), t ≥ 1 are independent andidentically distributed (i.i.d.) random variables and if the filtration F is generated by X .

Similarly, we call a positive adapted process X geometric random walk (relative to F)if the relative increments

∆X(t)

X(t− 1)=

X(t)

X(t− 1)− 1 (1.7)

are identically distributed and independent of Ft−1 for t ≥ 1. A process X is a geometricrandom walk if and only if log(X) is a random walk or, equivalently,

X(t) = exp(Y (t))

for some random walk Y . Indeed, the random variables in (1.7) are identically distributedand independent of Ft−1 if and only this holds for

∆(logX(t)) = log(X(t))− log(X(t− 1)) = log

(∆X(t)

X(t− 1)+ 1

), t ≥ 1.

Random walks and geometric random walks represent processes of constant growth inan additive or multiplicative sense, respectively. Simple asset price models are often ofgeometric random walk type.

A stopping time τ is a random variable whose values are times, i.e. are in N∪∞ in thediscrete case. Additionally one requires that τ is consistent with the information structureF. More precisely, one assumes that τ = t ∈ Ft (or equivalently τ ≤ t ∈ Ft) for anyt. Intuitively, this means that the decision to say “stop!” right now can only be based on ourcurrent information. As an example consider the first time τ when the observed stock pricehits the level 100. Even though this time is random and not known in advance, we obviouslyknow τ in the instant it occurs. The situation is different if we define τ to be the instantone period before the stock hits 100. Since we cannot look into the future, we only know τone period after it has happened. Consequently, this random variable is not a stopping time.Stopping times occur naturally in finance e.g. in the context of American options but theyalso play an important technical role in stochastic calculus.

As indicated above, the time when some adapted process first hits a given set is a stop-ping time:

Lemma 1.2 Let X be some adapted process and B a Borel set. Then

τ := inft ≥ 0 : X(t) ∈ B

is a stopping time.

12 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

Proof. By adaptedness, we have X(s) ∈ B ∈ Fs ⊂ Ft, s ≤ t and hence

τ ≤ t =t⋃

s=0

X(s) ∈ B ∈ Ft.

Occasionally, it turns out to be important to “freeze” a process at a stopping time. Forany adapted process X at any stopping time τ , the process stopped at τ is defined as

Xτ (t) := X(τ ∧ t),

where we use the notation a ∧ b := min(a, b) as usual. The stopped process Xτ remainsconstant on the level X(τ) after time τ . It is easy to see that it is adapted as well.

The concept of martingales is central to stochastic calculus and finance. A martingale(resp. submartingale, supermartingale) is an adapted process X that is integrable (in thesense that E(|X(t)|) <∞ for any t) and satisfies

E(X(t)|Fs) = X(s) (resp. ≥ X(s),≤ X(s)) (1.8)

for s ≤ t. If X is a martingale, then the best prediction for future values is the present level.If e.g. the price process of an asset is a martingale, then it is neither going up nor downon average. In that sense, it correponds to a fair game. By contrast, submartingales (resp.supermartingales) may increase (resp. decrease) on average. They correspond to favourable(resp. unfavourable) games.

The concept of a martingale is “global” in the sense that (1.8) must be satisfied for anys ≤ t. If we restrict attention to the case s = t − 1, we obtain the slightly more general“local” counterpart. A local martingale (resp. submartingale, supermartingale) is anadapted process X which satisfies E(|X(0)|) <∞, E(|X(t)||Ft−1) <∞ and

E(X(t)|Ft−1) = X(t− 1) (resp. ≥ X(t− 1),≤ X(t− 1)) (1.9)

for any t = 1, 2, . . . In discrete time the difference between martingales and local martin-gales is minor:

Lemma 1.3 Any integrable local martingale (in the sense that E(|X(t)|) <∞ for any t) isa martingale. An analogous statement holds for sub- and supermartingales.

Proof. This follows by induction from the law of iterated expectations.

Corresponding statements hold for sub-/supermartingales. Integrability in Lemma 1.3holds e.g. if X is nonnegative.

The above classes of processes are stable under stopping in the sense of the followinglemma, which has a natural economic interpretation: you cannot turn a fair game into e.g. astrictly favourable one by stopping to play at some reasonable time.

Lemma 1.4 Let τ denote a stopping time. If X is a martingale (resp. sub-/super-martingale), so is Xτ . A corresponding statement holds for local martingales and localsub-/supermartingales.

1.1. PROCESSES, STOPPING TIMES, MARTINGALES 13

Proof. We start by verifying the integrability conditions. For martingales (resp. sub-supermartingales) E(|X(t)|) < ∞ implies E(|Xτ (t)|) ≤ E(

∑ts=0 |X(s)|) < ∞. For

local martingales (resp. local sub-/supermartingales) E(|X(t)||Ft−1) <∞ yields

E(|Xτ (t)||Ft−1) ≤t∑

s=0

E(|X(s)||Ft−1)

=t∑

s=0

|X(s)|+ E(|X(t)||Ft−1) <∞.

In order to verify (1.9), observe that τ ≥ t = τ ≤ t− 1C ∈ Ft−1 implies

E(Xτ (t)1τ≥t|Ft−1) = E(X(t)1τ≥t|Ft−1)

= E(X(t)|Ft−1)1τ≥t

= X(t− 1)1τ≥t

= Xτ (t− 1)1τ≥t

(resp. ≥,≤ in the sub-/supermartingale case). For s < t we have τ = s ∈ Fs ⊂ Ft−1

and hence

E(Xτ (t)1τ=s|Ft−1) = E(X(s)1τ=s|Ft−1)

= X(s)1τ=s

= Xτ (t− 1)1τ=s.

Together we obtain

E(Xτ (t)|Ft−1) =t−1∑s=0

E(Xτ (t)1τ=s|Ft−1) + E(X(t)1τ≥t|Ft−1)

=t−1∑s=0

Xτ (t− 1)1τ=s +Xτ (t− 1)1τ≥t = Xτ (t− 1)

(resp. ≥,≤).

For later use, we note that a supermartingale with constant expectation is actually amartingale.

Lemma 1.5 If X is a supermatingale and T ≥ 0 with E(X(T )) = E(X(0)), then (1.8)holds with equality for any s ≤ t ≤ T .

Proof. The supermartingale property means that E((X(t) − X(s))1A) ≤ 0 for any s ≤ tand any A ∈ Fs. Since

0 = E(X(T ))− E(X(0))

= E(X(T )−X(t)) + E((X(t)−X(s))1A) + E((X(t)−X(s))1Ac)

+ E(X(s)−X(0))

≤ 0

14 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

for any s ≤ t ≤ T and any event A ∈ Fs, the four nonpositive summands must actually be0. This yields E((X(t)−X(s))1A) = 0 and hence the assertion.

The following technical result is used in Chapter 3.

Lemma 1.6 Let X be a supermartingale, Y a martingale, t ≤ T , and A ∈ Ft with X(t) =Y (t) on A and X(T ) ≥ Y (T ). Then X(s) = Y (s) on A for t ≤ s ≤ T . The statementremains to hold if we only requireXT−X t, Y T−Y t instead ofX, Y to be a supermartingaleresp. martingale.

Proof. FromX(s)− Y (s) ≥ E(X(T )− Y (T )|Fs) ≥ 0

andE((X(s)− Y (s))1A) ≤ E((X(t)− Y (t))1A) = 0

it follows that (X(t)− Y (t))1A = 0.

One easily verifies that an integrable random walk X is a martingale if (and only if) theincrements ∆X(t) have expectation 0. An analogous result holds for integrable geomet-ric random walks whose relative increments ∆X(t)/X(t− 1) have vanishing mean. Forthe martingale property to hold, one actually does not need the increments resp. relativeincrements of X to be identically distributed.

If ξ denotes an integrable random variable, then it naturally induces a martingale X ,namely

X(t) = E(ξ|Ft).

X is called the martingale generated by ξ. If the time horizon is finite, i.e. we considerthe time set 0, 1, . . . , T − 1, T rather then N, then any martingale is generated by somerandom variable, namely by X(T ). This ceases to be true for infinite time horizon. E.g.random walks are not generated by a single random variable unless they are constant.

Example 1.7 (Density process) A probability measure Q on (Ω,F ) is called equivalentto P (written Q ∼ P ) if the events of probability 0 are the same under P and Q. Bythe Radon-Nikodym theorem, Q has a P -density and vice versa, i.e. there are some uniquerandom variables dQ

dP, dPdQ

such that

Q(F ) = EP

(1FdQ

dP

), P (F ) = EQ

(1FdP

dQ

)for any set F ∈ F , where EP , EQ denote expectation under P and Q, respectively. P,Qare in fact equivalent if and only if such mutual densities exist, in which case we havedPdQ

= 1/dQdP

.The martingale Z generated by dQ

dPis called density process of Q, i.e. we have

Z(t) = EP

(dQ

dP

∣∣∣∣Ft

).

1.1. PROCESSES, STOPPING TIMES, MARTINGALES 15

One easily verifies that Z(t) coincides with the density of the restricted measures Q|Ft

relative to P |Ft, i.e. Z(t) is Ft-measurable and

Q(F ) = EP (1FZ(t))

holds for any event F ∈ Ft. Note further that Z and the density process Y of P relative toQ are reciprocal to each other because

Z(t) =dQ|Ft

dP |Ft

= 1/dP |Ft

dQ|Ft

= 1/Y (t).

The density process Z can be used to compute conditional expectations relative to Q.Indeed, the generalized Bayes’ rule

EQ(ξ|Ft) =EP (ξ dQ

dP|Ft)

Z(t)

holds for sufficiently integrable random variables ξ because

EQ(ξζ) = EP

(ξζdQ

dP

)= EP

(EP

(ξζdQ

dP

∣∣∣∣Ft

))= EP

(EP

(ξζ dQ

dP

Z(t)

∣∣∣∣Ft

)Z(t)

)

= EQ

(EP

(ξζ dQ

dP

Z(t)

∣∣∣∣Ft

))

= EQ

(EP (ξ dQ

dP|Ft)

Z(t)ζ

)for any bounded Ft-measurable ζ . Similarly, one shows

EQ(ξ|Fs) =EP (ξZ(t)|Fs)

Z(s)(1.10)

for s ≤ t and Ft-measurable random variables ξ.

Martingales are expected to stay on the current level on average. More general processesmay show an increasing, decreasing or possibly variable trend. This fact is expressed for-mally by a variant of Doob’s decomposition. The idea is to decompose the increment ∆X(t)of an arbitrary process into a predictable trend component ∆AX(t) and a random deviation∆MX(t) from this short time prediction.

Lemma 1.8 (canonical decomposition) Any integrable adapted process X (i.e. withE(|X(t)|) <∞ for any t) can be uniquely decomposed as

X = X(0) +MX + AX

with some martingale MX and some predictable process AX satisfying MX(0) = AX(0) =0. We call AX the compensator of X .

16 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

Proof. Define AX(t) =∑t

s=1 ∆AX(s) by ∆AX(s) := E(∆X(s)|Fs−1) and MX := X −X(0)−AX . Predictability of AX is obvious. The integrability of X implies that of AX andthus of MX . The latter is a martingale because

E(MX(t)|Ft−1) = MX(t− 1) + E(∆X(t)−∆AX(t)|Ft−1)

= MX(t− 1) + E(∆X(t)|Ft−1)− E(E(∆X(t)|Ft−1)|Ft−1)

= MX(t− 1).

Conversely, for any decomposition as in Lemma 1.8 we have

E(∆X(t)|Ft−1) = E(∆MX(t)|Ft−1) + E(∆AX(t)|Ft−1) = ∆AX(t),

which means that it coincides with the decomposition in the first part of the proof.

Note that uniqueness of the decomposition still holds if we only require MX to be alocal martingale. In this relaxed sense, it suffices to assume E(|X(t)||Ft−1) <∞ for any tin order to define the compensator AX .

IfX is a submartingale (resp. supermartingale), thenAX is increasing (resp. decreasing).This is the case commonly referred to as Doob’s decomposition. E.g. the compensator ofan integrable random walk X equals

AX(t) =t∑

s=1

E(∆X(s)|Fs−1) = tE(∆X(1)).

1.2 Stochastic integrationGains from trade in dynamic portfolios can be expressed in terms of stochastic integrals,which are nothing else than sums in discrete time.

Definition 1.9 LetX be an adapted and ϕ a predictable (or at least also an adapted) process.The stochastic integral of ϕ relative to X is the adapted process ϕ • X defined as

ϕ • X(t) :=t∑

s=1

ϕ(s)∆X(s).

If both ϕ = (ϕ1, . . . , ϕd) and X = (X1, . . . , Xd) are vector-valued processes, we defineϕ • X to be the real-valued process given by

ϕ • X(t) :=t∑

s=1

d∑i=1

ϕi(s)∆Xi(s). (1.11)

In order to motivate this definition, let us interpret X(t) as the price of a stock at time t.We invest in this stock using the trading strategy ϕ, i.e. ϕ(t) denotes the number of shareswe own at time t. Due to the price move from X(t − 1) to X(t) our wealth changes byϕ(t)(X(t)−X(t− 1)) = ϕ(t)∆X(t) in the period between t− 1 and t. Consequently, the

1.2. STOCHASTIC INTEGRATION 17

integral ϕ • X(t) stands for the cumulative gains from trade up to time t. If we invest in aportfolio of several stocks, both the trading strategy ϕ and the price process X are vectorvalued. ϕi(t) now stands for the number of shares of stock i and Xi(t) for its price. In orderto compute the total gains of the portfolio, we must sum up the gains ϕi(t)∆Xi(t) in eachsingle stock, which leads to (1.11).

For the above reasoning to make sense, one must be careful about the order in whichthings happen at time t. If ϕ(t)(X(t)−X(t− 1)) is meant to stand for the gains at time t,we obviously have to buy the portfolio ϕ(t) before prices change from X(t − 1) to X(t).Put differently, we must choose ϕ(t) already at the end of period t− 1, right after the stockprice has attained the value X(t − 1). This choice can only be based on information upto time t − 1 and in particular not on X(t), which is as yet unknown. This motivates whyone typically requires trading strategies to be predictable rather than adapted. The purelymathematical definition of ϕ • X , however, makes sense regardless of any measurabilityassumption.

The covariation process [X, Y ] of adapted processes X, Y is defined as

[X, Y ](t) :=t∑

s=1

∆X(s)∆Y (s). (1.12)

Its compensator

〈X, Y 〉(t) =t∑

s=1

E(∆X(s)∆Y (s) |Fs−1)

is called predictable covariation process if it exists. In the special case X = Y onerefers to the quadratic variation resp. predictable quadratic variation of X . If X, Yare martingales, their predictable covariation can be viewed as a dynamic analogue of thecovariance of two random variables.

We are now ready to state a few properties of stochastic integration:

Lemma 1.10 For adapted processes X, Y and predictable processes ϕ, ψ we have:

1. ϕ • X is linear in ϕ and X .

2. [X, Y ] and 〈X, Y 〉 are symmetric and linear in X and Y .

3. ψ • (ϕ • X) = (ψϕ) • X

4. [ϕ • X, Y ] = ϕ • [X, Y ]

5. 〈ϕ • X, Y 〉 = ϕ • 〈X, Y 〉 whenever the predictable covariations are defined.

6. (integration by parts)

XY = X(0)Y (0) +X− • Y + Y • X (1.13)= X(0)Y (0) +X− • Y + Y− • X + [X, Y ]

7. If X is a local martingale, so is ϕ • X .

18 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

8. If ϕ ≥ 0 andX is a local sub-/supermartingale, ϕ • X is a local sub-/supermartingaleas well.

9. Aϕ•X = ϕ • AX if the compensator AX exists in the relaxed sense following Lemma1.8.

10. If X, Y are martingales with E(|X(t)|) < ∞ and E(|Y (t)|) < ∞ for any t, theprocess XY − 〈X, Y 〉 is a martingale, i.e. 〈X, Y 〉 is the compensator of XY .

Proof.

1. This is obvious from the definition.

2. This is obvious from the definition as well.

3. This follows from

∆(ψ • (ϕ • X))(t) = ψ(t)∆(ϕ • X)(t) = ψ(t)ϕ(t)∆X(t) = ∆((ψϕ) • X)(t).

4. This follows from

∆[ϕ • X, Y ](t) = ϕ(t)∆X(t)∆Y (t) = ∆(ϕ • [X, Y ])(t).

5. Predictability of ϕ yields

∆〈ϕ • X, Y 〉(t) = E(∆(ϕ • X)(t)∆Y (t) |Ft−1)

= E(ϕ(t)∆X(t)∆Y (t) |Ft−1)

= ϕ(t)E(∆X(t)∆Y (t) |Ft−1)

= ∆(ϕ • 〈X, Y 〉)(t).

6. The first equation is

X(t)Y (t) = X(0)Y (0) +t∑

s=1

(X(s)Y (s)−X(s− 1)Y (s− 1)

)= X(0)Y (0) +

t∑s=1

(X(s− 1)(Y (s)− Y (s− 1))

)+

t∑s=1

((X(s)−X(s− 1))Y (s)

)= X(0)Y (0) +

t∑s=1

(X(s− 1)∆Y (s) + Y (s)∆X(s)

)= X(0)Y (0) +X− • Y (t) + Y • X(t).

The second follows from

Y • X(t) = Y− • X(t) + (∆Y ) • X(t) = Y− • X(t) + [X, Y ](t).

1.2. STOCHASTIC INTEGRATION 19

7. Predictability of ϕ and (1.9) yield

E(ϕ • X(t)|Ft−1) = E(ϕ • X(t− 1) + ϕ(t)(X(t)−X(t− 1))|Ft−1)

= ϕ • X(t− 1) + ϕ(t)(E(X(t)|Ft−1)−X(t− 1))

= ϕ • X(t− 1).

8. This follows along the same lines as 7.

9. This follows from 7. because ϕ • X = ϕ • MX + ϕ • AX is the canonical decompo-sition of ϕ • X .

10. This follows from statements 6 and 7.

If they make sense, the above rules also hold for vector-valued processes, e.g.

ψ • (ϕ • X) = (ψϕ) • X

if both ϕ,X are Rd-valued.Ito’s formula is probably the most important rule in continuous-time stochastic calculus.

This motivates why we state its obvious discrete-time counterpart here.

Lemma 1.11 (Ito’s formula) If X is an Rd-valued adapted process and f : Rd → R adifferentiable function, then

f(X(t)) = f(X(0)) +t∑

s=1

(f(X(s))− f(X(s− 1)))

= f(X(0)) +Df(X−) • X(t)

+t∑

s=1

(f(X(s))− f(X(s− 1))−Df(X(s− 1))>∆X(s)

)(1.14)

where Df(x) denotes the derivative or gradient of f in x.

Proof. The first statement is obvious. The second follows from the definition of thestochastic integral.

If the increments ∆X(s) are small and f is sufficiently smooth, we may use the second-order Taylor expansion

f(X(s)) = f(X(s− 1) + ∆X(s))

≈ f(X(s− 1)) + f ′(X(s− 1))∆X(s) +1

2f ′′(X(s− 1))(∆X(s))2

in the univariate case, which leads to

f(X(t)) ≈ f(X(0)) + f ′(X−) • X(t) +t∑

s=1

1

2f ′′(X(s− 1))(∆X(s))2

= f(X(0)) + f ′(X−) • X(t) +1

2f ′′(X−) • [X,X](t).

20 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

If X is vector valued, we obtain accordingly

f(X(t)) ≈ f(X(0)) +Df(X−) • X(t) +1

2

d∑i,j=1

Dijf(X−) • [Xi, Xj](t). (1.15)

Processes of multiplicative structure are called stochastic exponentials.

Definition 1.12 Let X be an adapted process. The unique adapted process Z satisfying

Z = 1 + Z− • X

is called stochastic exponential of X and it is written E (X).

The stochastic exponential can easily be motivated from a financial point of view. Supposethat 1 e earns the possibly random interest ∆Xt in period t, i.e. 1 e at time t− 1 turns into(1 + ∆Xt) e at time t. Then 1 e at time 0 run up to E (X)(t) e at time t. It is easy tocompute E (X) explicitly:

Lemma 1.13 We have

E (X)(t) =t∏

s=1

(1 + ∆X(s)),

where the product is set to 1 for t = 0.

Proof. For Z(t) =∏t

s=1(1 + ∆X(s)) we have

∆Z(t) = Z(t)− Z(t− 1) = Z(t− 1)∆X(t)

and hence

Z(t) = Z(0) +t∑

s=1

∆Z(s) = 1 +t∑

s=1

Z(s−)∆X(s) = 1 + Z− • X(t).

The previous lemma implies that the stochastic exponential of a random walk X withincrements ∆X(t) > −1 is a geometric random walk. More specifically, one can writeany geometric random walk Z alternatively in exponential or stochastic exponential form,namely

Z = eX = Z(0)E (X)

with random walks X, X , respectively. X and X are related to each other via

∆X(t) = e∆X(t) − 1 resp. ∆X(t) = log(1 + ∆X(t)).

If the increments ∆X(s) are small enough, we can use the approximation

log(1 + ∆X(s)) ≈ ∆X(s)− 1

2(∆X(s))2

1.2. STOCHASTIC INTEGRATION 21

and obtain

E (X)(t) =t∏

s=1

(1 + ∆X(s))

= exp

(t∑

s=1

log(1 + ∆X(s))

)

≈ exp

(t∑

s=1

(∆X(s)− 1

2(∆X(s))2

))

= exp

(X(t)−X(0)− 1

2[X,X](t)

).

The product of stochastic exponentials is again a stochastic exponential. Observe thesimilarity of the following result to the rule exey = ex+y for exponential functions.

Lemma 1.14 (Yor’s formula)

E (X)E (Y ) = E (X + Y + [X, Y ])

holds for any two adapted processes X, Y .

Proof. Let Z := E (X)E (Y ). Integration by parts and the other statements of Lemma 1.10yield

Z = Z(0) + E (X)− • E (Y ) + E (Y )− • E (X) + [E (X),E (Y )]

= 1 + (E (X)−E (Y )−) • Y + (E (Y )−E (X)−) • X

+ (E (X)−E (Y )−) • [X, Y ]

= 1 + Z− • (X + Y + [X, Y ]),

which implies that Z = E (X + Y + [X, Y ]).

If an adapted process Z does not attain the value 0, it can be written as

Z = Z(0)E (X)

with some unique process X satisfying X(0) = 0. This process X is naturally calledstochastic logarithm L (Z) of Z. We have

L (Z) =1

Z−• Z.

Indeed, X = 1Z−

• Z satisfies

Z−Z(0)

• X =Z−Z(0)

•

(1

Z−• Z

)=

1

Z(0)• Z =

Z

Z(0)− 1

and henceZ

Z(0)= E (X)

22 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

as claimed.Changes of the underlying probability measure play an important role in Mathematical

Finance. Since the notion of a martingale involves expectation, it is not invariant under suchmeasure changes.

Lemma 1.15 Let Q ∼ P be a probability measure with density process Z. An adaptedprocessX is aQ-martingale (resp.Q-local martingale) if and only ifXZ is a P -martingale(resp. P -local martingale).

Proof. X is a Q-local martingale if and only if

EQ(X(t)|Ft−1) = X(t− 1) (1.16)

for any t. By Bayes’ rule (1.10) the left-hand side equals E(X(t)Z(t)|Ft−1)/Z(t − 1).Hence (1.16) is equivalent to E(X(t)Z(t)|Ft−1) = X(t − 1)Z(t − 1), which is the localmartingale property of XZ relative to P . The integrability property for martingales (cf.Lemma 1.3) is shown similarly.

A martingale X may possibly show a trend under the new probability measure Q. Thistrend can be expressed in terms of predictable covariation.

Lemma 1.16 Let Q ∼ P be a probability measure with density process Z. Moreover,suppose that X is a P -martingale. If X is Q-integrable, its Q-compensator equals

〈L (Z), X〉.

Proof. Since A := 〈L (Z), X〉 = 1Z−

• 〈Z,X〉 is a predictable process and by the proofof Lemma 1.8, it suffices to show that X −X(0) − A is a Q-local martingale. By Lemma(1.15) the amounts to proving that Z(X − X(0) − A) is a P -local martingale. Integrationby parts yields

Z(X −X(0)− A) = Z− • X + (X −X(0))− • Z + [Z,X −X(0)]

− Z− • A− A • Z. (1.17)

The integrals relative to X and Z are local martingales. Moreoever,

Z− • A =Z−Z−

• 〈Z,X〉 = 〈Z,X〉

is the compensator of [Z,X] = [Z,X −X(0)], which implies that the difference is a localmartingale. Altogether the right-hand side of (1.17) is indeed a local martingale.

1.3 Conditional jump distributionFor later use we study the conditional law of the jumps of a stochastic process. We areparticularly interested in the Markovian case where this law depends only on the currentstate of the process

1.3. CONDITIONAL JUMP DISTRIBUTION 23

Definition 1.17 Let X be an adapted process with values in E ⊂ Rd. We call the mapping

KX(t, B) := P (∆X(t) ∈ B|Ft−1) := E(1B(∆X(t)) |Ft−1 ) , t = 0, . . . , T, B ⊂ E

conditional jump distribution of X . As usual, we skip the argument ω in the notation.If the conditional jump distribution depends on ω, t only through X(t − 1)(ω), i.e. if it

is of the form KX(t, B) = κ(X(t− 1), B) with some deterministic function κ, we call theprocess Markov. In this case we define the generator G of the Markov process, which isan operator mapping functions f : E → R on the like. It is defined by the equation

Gf(x) =

∫(f(x+ y)− f(x))κ(x, dy). (1.18)

Random walks have particularly simple conditional jump distributions.

Lemma 1.18 (Random walk) An adapted process X is a random walk if and only if itsconditional jump distribution is of the form

KX(t, B) = Q(B)

for some probability measure Q which does not depend on (ω, t). In this case Q is the lawof ∆X(1). In particular, random walks are Markov processes.

Proof. If X is a random walk, we have P∆X(t)|Ft−1 = P∆X(t) = P∆X(1) since ∆X(t) isindependent of Ft−1 and has the same law for all t. Conversely,

P (∆X(t) ∈ B ∩ A) = E(1B(∆X(t))1A)

=

∫E(1B(∆X(t))|Ft−1)1AdP

=

∫Q(B)1AdP

= Q(B)P (A).

for A ∈ Ft−1. For A = Ω we obtain P (∆X(t) ∈ B) = Q(B) = P (∆X(1) ∈ B). Hence∆X(t) is independent of Ft−1 and has the same law for all t.

The conditional jump distribution of a geometric random walk is also easily obtainedfrom its definition.

Example 1.19 (Geometric random walk) The jump characteristic of a geometric randomwalk X is given by

KX(t, B) = %(x ∈ Rd : X(t− 1)(x− 1) ∈ B),

where % denotes the distribution ofX(1)/X(0). In particular, it is a Markov process as well.Indeed, we have

E(1B(∆X(t)) |Ft−1 ) = E

(1B

(X(t− 1)

(X(t)

X(t− 1)− 1

))∣∣∣∣Ft−1

)=

∫1B(X(t− 1)(x− 1))%(dx)

by (1.4) and the fact that X(t)/X(t− 1) has law % and is independent of Ft−1.

24 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

For the following we define the identity process I as

I(t) := t.

The characteristics can be used to compute the compensator of an adapted process.

Lemma 1.20 (Compensator) If X is an integrable adapted process, then its compensatorAX and its conditional jump distribution KX are related to each other via

AX = aX • I

withaX(t) :=

∫xKX(t, dx).

Proof. By definition of the compensator we have

∆AX(t) = E(∆X(t)|Ft−1) =

∫xP∆X(t)|Ft−1(dx)

=

∫xKX(t, dx) = aX(t) = ∆(aX • I)(t).

Since the predictable covariation is a compensator, it can also be expressed in terms ofcompensators and conditional jump distributions.

Lemma 1.21 (Predictable covariation) The predictable covariation of adapted processesX, Y and of their martingale parts MX ,MY is given by

〈X, Y 〉 = cXY • I,

〈MX ,MY 〉 = cXY • I

with

cXY (t) :=

∫xyK(X,Y )(t, d(x, y)),

cXY (t) :=

∫xyK(X,Y )(t, d(x, y))− aX(t)aY (t)

(provided that the integrals exist).

Proof. The first statement follows similarly as Lemma 1.20 by observing that

∆〈X, Y 〉(t) = E(∆X(t)∆Y (t)|Ft−1).

The second in turn follows from the first and from Lemma 1.20 because

∆〈MX ,MY 〉(t) = E(∆MX(t)∆MY (t)|Ft−1)

= E(∆X(t)∆Y (t)|Ft−1)− E(∆X(t)|Ft−1)∆AY (t)

−∆AX(t)E(∆Y (t)|Ft−1) + ∆AX(t)∆AY (t)

= ∆〈X, Y 〉(t)−∆AX(t)∆AY (t)

=

∫xyK(X,Y )(t, d(x, y))− aX(t)aY (t).

1.4. ESSENTIAL SUPREMUM 25

Let us rephrase the integration by parts rule in terms of characteristics.

Lemma 1.22 We have

aXY (t) = X(t− 1)aY (t) + Y (t− 1)aX(t) + cXY (t)

provided that X, Y and XY are integrable adapted processes.

Proof. Computing the compensators of

XY = X(0)Y (0) +X− • Y + Y− • X + [X, Y ]

yieldsaXY • I = X(t− 1)aY • I + Y (t− 1)aX • I + cXY • I

by Lemmas 1.10(9) and 1.21. Considering increments yields the claim.

1.4 Essential supremumIn the context of optimal control we need to consider suprema of possibly uncountable manyrandom variables. To this end, let G denote a sub-σ-field of F and (Xi)i∈I a family of G -measurable random variables with values in [−∞,∞].

Definition 1.23 A G -measurable random variable Y is called essential supremum of(Xi)i∈I if Y ≥ Xi almost surely for any i ∈ I and Y ≤ Z almost surely for any G -measurable random variable Z such that Y ≤ Z almost surely for any i ∈ I . We writeY =: ess supi∈IXi.

Lemma 1.24 1. The essential supremum exists. It is almost surely unique in the sensethat any two random variables Y, Y as in Definition 1.23 coincide almost surely.

2. There is a countable subset J ⊂ I such that ess supi∈JXi = ess supi∈IXi.

Proof. By considering Xi := arctanXi instead of Xi, we may assume w.l.o.g. that the Xi

all have values in the same bounded interval.Observe that supi∈C is a G -measurable random variable for any countable subset C

of I . We denote the set of all such countable subsets of I by C . Consider a sequence(Cn)n∈N in C such that E(supi∈Cn Xi) ↑ supC∈C E(supi∈C Xi). Then C∞ := ∪n∈NCn isa countable subset of I satisfying E(supi∈C∞ Xi) = supC∈C E(supi∈C Xi). We show thatY := supi∈C∞ Xi meets the requirements of an essential supremum. Indeed, for fixed i ∈ Iwe have Y ≤ Y ∨Xi and E(Y ) = E(Y ∨Xi) < ∞, which implies that Y = Y ∨Xi andhence Xi ≤ Y almost surely.

On the other hand, we have Z ≥ Xi, i ∈ I and hence Z ≥ Y almost surely for any Z asin the definition.

The following results helps to approximate the essential supremum by a sequence ofrandom variables.

26 CHAPTER 1. RECAP OF STOCHASTIC PROCESSES

Lemma 1.25 Suppose that (Xi)i∈I has the lattice property, i.e. for any i, j ∈ I there existsk ∈ I such that Xi ∨ Xj ≤ Xk almost surely. Then there is a sequence (in)n∈N such thatXin ↑ ess supi∈IXi almost surely.

Proof. Choose a sequence (jn)n∈N such that J = jn : n ∈ N holds for the countable setJ ⊂ I in statement 2 of Lemma 1.23.

If the lattice property holds, essential supremum and expectation can be interchanged.

Lemma 1.26 Let Xi ≥ 0, i ∈ I or E(ess supi∈I |Xi|) < ∞. If (Xi)i∈I has the latticeproperty, then

E(ess supi∈IXi|H ) = ess supi∈IE(Xi|H )

for any sub-σ-field H of F .

Proof. Since E(ess supi∈IXi|H ) ≥ E(Xj|H ) a.s. for any j ∈ I , we obviously haveE(ess supi∈IXi|H ) ≥ ess supi∈IE(Xi|H ). Let (in)n∈N be a sequence as in the previouslemma. Then Xin ↑ ess supi∈IXi a.s. and monotone resp. dominated convergence implyE(Xin|H ) ↑ E(ess supi∈IXi|H ) and hence the claim.

Chapter 2

Dynamic Programming

Since we consider discrete-time stochastic control in this part, we work on a filtered proba-bility space (Ω,F ,F, P ) with filtration F = (Ft)t=0,1,...,T . For simplicity, we assume F0

to be trivial, i.e. all F0-measurable random variables are deterministic. By (1.1) this impliesE(X|F0) = E(X) for any random variable X .

Our goal is to maximize some expected reward E(u(α)) over controls α ∈ A . The setA of admissible controls is a subset of all Rm-valued adapted processes and it is assumedto be stable under bifurcation, i.e. for any stopping time τ , any event B ∈ Fτ , and anyα, α ∈ A with ατ = ατ , the process (α|τB|α) defined by

(α|τB|α)(t) := 1Bcα(t) + 1Bα(t)

is again an admissible control. Intuitively, this means that the decision how to continuemay depend on the observations so far. Moreover, we suppose that α(0) coincides for allcontrols α ∈ A . The reward is expressed by some reward function u : Ω×(Rm)0,1,...,T →R ∪ −∞. For fixed α ∈ A , we use the shorthand u(α) for the random variable ω 7→u(ω, α(ω)). The reward is meant to refer to some fixed time T ∈ N, which is expressedmathematically by the assumption that u(α) is FT -measurable for any α ∈ A .

Example 2.1 Typically, the reward function is of the form

u(α) =T∑t=1

f(t,X(α)(t− 1), α(t)) + g(X(α)(T ))

for some functions f : 1, . . . , T × Rd × Rm → R ∪ −∞, g : Rd → R ∪ −∞, andRd-valued adapted controlled processes X(α).

Definition 2.2 We call α? ∈ A optimal control if it maximizes E(u(α)) over all α ∈ A(where we set E(u(α)) := −∞ if E(u(α)−) := −∞). Moreover, the value process of theoptimization problem is the family (J(·, α))α∈A of adapted processes defined via

J(t, α) := ess supE(u(α)|Ft) : α ∈ A with αt = αt

for t ∈ [0, T ], α ∈ A .

The value process is characterized by some martingale/supermartingale property:

27

28 CHAPTER 2. DYNAMIC PROGRAMMING

Theorem 2.3 Suppose that J(0) := supα∈A E(u(α)) 6= ±∞.

1. For any admissible control α with terminal value E(u(α)) > −∞, the process(J(t, α))t∈0,...,T is a supermartingale with terminal value J(T, α) = u(α). If α?

is an optimal control, (J(t, α?))t∈0,...,T is a martingale.

2. Suppose that (J(·, α))α∈A is a family of processes such that

(a) J(0, α) coincides for all α ∈ A and is denoted as J(0),

(b) (J(t, α))t∈0,...,T is a supermartingale with terminal value J(T, α) = u(α) forany admissible control α with E(u(α)) > −∞,

(c) (J(t, α?))t∈0,...,T is a martingale for some admissible control α?.

Then α? is optimal and J(t, α?) = J(t, α?) for t = 0, . . . , T .

Proof.

1. Adaptedness and terminal value of J(·, α) are evident. In order to show the super-martingale property, let t ∈ 0, . . . , T. Stability under bifurcation implies that theset of all E(u(α)|Ft) with α ∈ A satisfying αt = αt has the lattice property. ByLemma 1.25 there exists a sequence of admissible controls αn with αtn = αt andE(u(αn)|Ft) ↑ J(t, α). For s ≤ t we have

E(E(u(αn)|Ft)|Fs) = E(u(αn)|Fs) ≤ J(s, α).

By monotone convergence we obtain the supermartingale property E(J(t, α))|Fs) ≤J(s, α).

Let α? be an optimal control. Since J(·, α?) is a supermartingale, the martingaleproperty follows from

J(0, α?) = supα∈A

E(u(α)) = E(u(α?)) = E(J(T, α?))

and Lemma 1.5.

2. The supermartingale property implies that

E(u(α)) = E(J(T, α)) ≤ J(0, α) = J(0)

for any admissible control α. Since equality holds for α?, we have that α? is optimal.By statement 1, J(·, α?) is a martingale with terminal value u(α?). Since the same istrue for J(·, α?) by assumptions 2b,c), we have J(t, α?) = E(u(α?)|Ft) = J(t, α?)for t = 0, . . . , T .

The previous theorem does not immediately lead to an optimal control but it often helps inorder to verify that some candidate control is in fact optimal.

29

Remark 2.4 1. It may happen that the supremum in the definition of the optimal value isnot a maximum, i.e. an optimal control does not exist. In this case Theorem 2.3 cannotbe applied. Sometimes this problem can be circumvented by considering a certainclosure of the set of admissible controls which does in fact contain the optimizer.

If this is not feasible, a variation of Theorem 2.3(2) without assumption 2c) may beof interest. The supermartingale property 2b) of the candidate value process ensuresthat J(0) is an upper bound of the optimal value J(0). If, for any ε > 0, one can findan admissible control α(ε) with J(0) ≤ E(J(T, α(ε))) + ε, then J(0) = J(0) and theα(ε) yield a sequence of controls approaching this optimal value.

2. The above setup allows for a straightforward extension to infinite time horizon T =∞.

As an example we consider the Merton problem to maximize expected logarithmic utilityof terminal wealth.

Example 2.5 (Logarithmic utility of terminal wealth) An investor trades in a market con-sisting of a constant bank account and a stock whose price at time t equals

S(t) = S(0)E (X)(t) = S(0)t∏

s=1

(1 + ∆X(s))

with ∆X(t) > −1. Given that ϕ(t) denotes the number of shares in the investor’s portfoliofrom time t − 1 to t, the profits from the stock investment in this period are ϕ(t)∆S(t). Ifv0 > 0 denotes the investor’s initial endowment, her wealth at any time t amounts to

Vϕ(t) := v0 +t∑

s=1

ϕ(s)∆S(s) = v0 + ϕ • S(t). (2.1)

We assume that the investor’s goal is to maximize the expected logarithmic utilityE(log(Vϕ(T ))) of wealth at time T . To this end, we assume that the stock price processS is exogenously given and the investor’s set of admissible controls is

A := ϕ predictable : Vϕ ≥ 0 and ϕ(0) = 0.

It turns out that the problem becomes more transparent if we consider the relative portfolio

π(t) := ϕ(t)S(t− 1)

Vϕ(t− 1), t = 1, . . . , T, (2.2)

i.e. the fraction of wealth invested in the stock at t− 1. Starting with v0, the stock holdingsϕ(t) and the wealth process Vϕ(t) are recovered from π via

Vϕ(t) = v0E (π • X)(t) = v0

t∏s=1

(1 + π(s)∆X(s)) (2.3)

and

ϕ(t) = π(t)Vϕ(t− 1)

S(t− 1)= π(t)

v0E (π • X)(t− 1)

S(t− 1).

30 CHAPTER 2. DYNAMIC PROGRAMMING

Indeed, (2.3) follows from

∆Vϕ(t) = ϕ(t)∆S(t) =Vϕ(t− 1)π(t)

S(t− 1)∆S(t) = Vϕ(t− 1)∆(π • X)(t).

If T = 1, a simple calculation shows that the investor should buy ϕ?(1) = π?(1)v0/S(0)shares at time 0, where the optimal fraction π?(1) maximizes the function γ 7→ E(log(1 +γ∆X(1))). We guess that the same essentially holds for multi-period markets, i.e. we as-sume that the optimal relative portfolio is obtained as the maximizer π?(ω, t) of the mapping

γ 7→ E(log(1 + γ∆X(t))|Ft−1)(ω). (2.4)

The corresponding candidate value process is

J(t, ϕ) := E

(log

(Vϕ(t)

T∏s=t+1

(1 + π?(s)∆X(s)

))∣∣∣∣∣Ft

)

= log(Vϕ(t)

)+ E

(T∑

s=t+1

log(1 + π?(s)∆X(s)

)∣∣∣∣∣Ft

). (2.5)

Observe that

E(J(t, ϕ)|Ft−1) = log(Vϕ(t− 1)

)+ E

(log

(1 +

ϕ(t)S(t− 1)

Vϕ(t− 1)∆X(t)

)∣∣∣∣∣Ft−1

)

+ E

(T∑

s=t+1

log(1 + π?(s)∆X(s)

)∣∣∣∣∣Ft−1

)≤ log

(Vϕ(t− 1)

)+ E

(log(1 + π?(t)∆X(t)

)|Ft−1

)+ E

(T∑

s=t+1

log(1 + π?(s)∆X(s)

)∣∣∣∣∣Ft−1

)= J(t− 1, ϕ)

for any t ≥ 1 and ϕ ∈ A , with equality for the candidate optimizer ϕ? satisfying ϕ?(t) =π?(t)Vϕ?(t− 1)/S(t− 1). By Theorem 2.3, we conclude that ϕ? is indeed optimal.

Note that the optimizer or, more precisely, the optimal fraction of wealth invested instock depends only on the local dynamics of the stock. This myopic property holds only forlogarithmic utility.

The following variation of Example 2.5 considers utility of consumption rather thanterminal wealth.

Example 2.6 (Logarithmic utility of consumption) In the market of the previous examplethe investor now spends c(t) currency units at any time t − 1. We assume that utility isderived from this consumption rather than terminal wealth, i.e. the goal is to maximize

E

(T∑t=1

log(c(t)) + log(Vϕ,c(T ))

)(2.6)

31

subject to the affordability constraint that the investor’s aggregate consumption cannot ex-ceed her cumulative profits:

0 ≤ Vϕ,c(t) := v0 + ϕ • S(t)−t∑

s=1

c(s).

The last term Vϕ,c(T ) in (2.6) refers to consumption of the remaining wealth at the end. Theinvestor’s set of admissible controls is

A :=

(ϕ, c) predictable : Vϕ,c ≥ 0, (ϕ, c)(0) = (0, 0).

We try to come up with a reasonable candidate (ϕ?, c?) for the optimal control. As inthe previous example, matters simplify in relative terms. We write

κ(t) =c(t)

Vϕ,c(t− 1), t = 1, . . . , T (2.7)

for the fraction of wealth that is consumed and

π(t) = ϕ(t)S(t− 1)

Vϕ,c(t− 1)− c(t)= ϕ(t)

S(t− 1)

Vϕ,c(t− 1)(1− κ(t))(2.8)

for the relative portfolio. Since wealth after consumption at time t− 1 is now Vϕ,c(t− 1)−c(t), the numerator in (2.8) had to be adjusted. Similarly to (2.3), the wealth is given by

Vϕ,c(t) = v0

t∏s=1

(1 + π(s)∆X(s))(1− κ(s)) = v0E (π • X)(t)E (−κ • I)(t) (2.9)

We guess that the same relative portfolio as in the previous example is optimal in thismodified setup, which leads to the candidate

ϕ?(t) = π?(t)V (ϕ?,c?)(t− 1)− c?(t)

S(t− 1).

Moreover, it may seem natural that the investor tries to spread consumption of wealth evenlyover time. This idea leads to κ?(t) = 1/(T + 2− t) and hence

c?(t) =V (ϕ?,c?)(t− 1)

T + 2− t

because, at time t− 1, there are T + 2− t periods are left for consumption. This candidate

32 CHAPTER 2. DYNAMIC PROGRAMMING

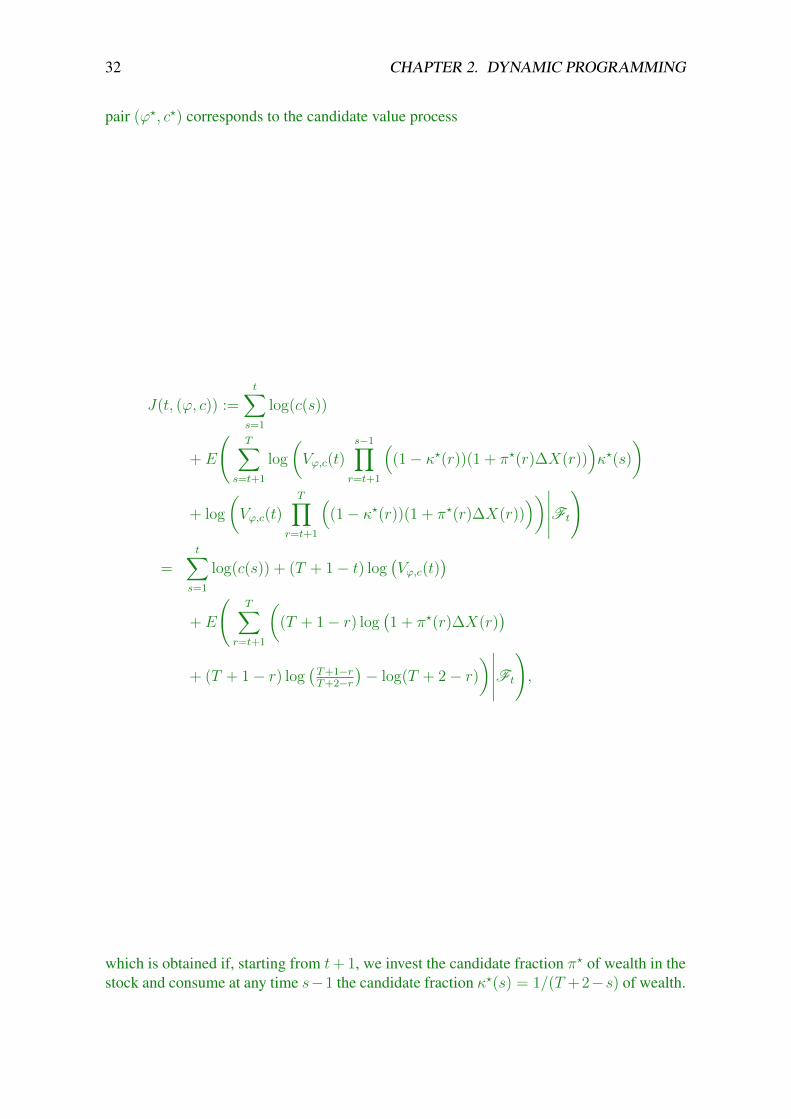

pair (ϕ?, c?) corresponds to the candidate value process

J(t, (ϕ, c)) :=t∑

s=1

log(c(s))

+ E

(T∑

s=t+1

log

(Vϕ,c(t)

s−1∏r=t+1

((1− κ?(r))(1 + π?(r)∆X(r))

)κ?(s)

)

+ log

(Vϕ,c(t)

T∏r=t+1

((1− κ?(r))(1 + π?(r)∆X(r))

))∣∣∣∣∣Ft

)

=t∑

s=1

log(c(s)) + (T + 1− t) log(Vϕ,c(t)

)+ E

(T∑

r=t+1

((T + 1− r) log

(1 + π?(r)∆X(r)

)+ (T + 1− r) log

(T+1−rT+2−r

)− log(T + 2− r)

)∣∣∣∣∣Ft

),

which is obtained if, starting from t+ 1, we invest the candidate fraction π? of wealth in thestock and consume at any time s−1 the candidate fraction κ?(s) = 1/(T +2−s) of wealth.

33

In order to verify optimality, observe that

E(J(t, (ϕ, c))|Ft−1) =t−1∑s=1

log(c(s)) + (T + 1− t) log(Vϕ,c(t− 1)

)+ (T + 1− t)E

(log(1 + π(t)∆X(t)

)∣∣∣Ft−1

)+ E

((T + 1− t) log(1− κ(t)) + log(κ(t))

∣∣Ft−1

)+ log

(Vϕ,c(t− 1)

)+ E

(T∑

s=t+1

((T + 1− s) log

(1 + π?(s)∆X(s)

)+ (T + 1− s) log

(T+1−sT+2−s

)− log(T + 2− s)

)∣∣∣∣∣Ft−1

)

≤t−1∑s=1

log(c(s)) + (T + 2− t) log(Vϕ,c(t− 1)

)+ (T + 1− t)E

(log(1 + π?(t)∆X(t)

)∣∣∣Ft−1

)+ E

((T + 1− t) log(1− 1

T+2−t)− log(T + 2− t)∣∣Ft−1

)+ E

(T∑

s=t+1

((T + 1− s) log

(1 + π?(s)∆X(s)

)+ (T + 1− s) log

(T+1−sT+2−s

)− log(T + 2− s)

)∣∣∣∣∣Ft−1

)= J(t− 1, (ϕ, c))

=t∑

s=1

log(c(s)) + (T + 1− t) log(Vϕ,c(t)

)+ E

(T∑

r=t+1

((T + 1− r) log

(1 + π?(r)∆X(r)

)+ (T + 1− r) log

(T+1−rT+2−r

)− log(T + 2− r)

)∣∣∣∣∣Ft

)

for any admissible control (ϕ, c), where π(t), κ(t) are defined as in (2.8, 2.7). Indeed, theinequality holds because π?(t) maximizes γ 7→ E(log(1+γ∆X(t))|Ft−1) and 1/(T+2−t)maximizes δ 7→ (T + 2− t) log(1− δ) + log(δ). Again, equality holds if (ϕ, c) = (ϕ?, c?).By Theorem 2.3, we conclude that (ϕ?, c?) is indeed optimal.

The optimal consumption rate changes slightly if the objective is to maximizeE(∑T

t=1 e−δ(t−1) log(ct) + e−δT log(Vϕ,c(T ))) with some impatience rate δ ≥ 0.

The two previous examples allow for a straightforward extension to d > 1 assets.

Chapter 3

Optimal Stopping

An important subclass of control problems concerns optimal stopping, i.e. given some timehorizon T and some adapted process X with E(supt∈0,...,T |X(t)|) < ∞, the goal is tomaximise the expected reward

τ 7→ E(X(τ)) (3.1)

over all stopping times τ with values in 0, . . . , T.

Remark 3.1 In the spirit of Chapter 2, a stopping time τ can be identified with the cor-responding adapted process α(t) := 1t≤τ, and hence X(τ) = X(0) + α • X(T ).Put differently, A := α predictable: α 0, 1-valued, decreasing, α(0) = 1 andu(α) := X(0) + α • X(T ) in Chapter 2 lead to the above optimal stopping problem.

Definition 3.2 The Snell envelope of X is the adapted process V defined as

V (t) := ess supE(X(τ)|Ft) : τ stopping time with values in t, t+ 1, . . . , T

. (3.2)

The Snell envelope represents the maximal expected reward if we start at time t and havenot stopped yet. The following martingale criterion may be helpful to verify the optimalityof a candidate stopping time. We will apply its continuous-time version it in two examplesin Chapter 8.

Proposition 3.3 1. Let τ be a stopping time with values in 0, . . . , T. If V is anadapted process such that V τ is a martingale, V (τ) = X(τ), and V (0) = M(0)for some martingale (or at least supermartingale) M ≥ X , then τ is optimal for (3.1)and V coincides up to time τ with the Snell envelope of Definition 3.2.

2. More generally, let τ be a stopping time with values in t, . . . , T and A ∈ Ft. IfV is an adapted process such that V τ − V t is a martingale, V (τ) = X(τ), andV (t) = M(t) onA for some martingale (or at least supermartingale)M withM ≥ Xon A, then V (s) coincides on A for t ≤ s ≤ τ with the Snell envelope of Definition3.2 and τ is optimal on A for (3.2), i.e. it maximises E(X(τ)|Ft) on A.

Proof.

1. This follows from the second statement.

34

35

2. Let s ∈ t, . . . , T. We have to show that

V (s) = ess supE(X(τ)|Fs) : τ stopping time with values in s, . . . , T

holds on s ≤ τ.“≤”: On s ≤ τ ∩ A we have

V (s) = E(V τ (T )|Fs)

= E(X(τ ∨ s)|Fs)

≤ ess supE(X(τ)|Fs) : τ stopping time with values in s, . . . , T

.

(3.3)

“≥”: Note that V τ (T ) = V (τ) = X(τ) ≤M(τ) = M τ (T ) and Lemma 1.6 yield

V τ (s) = M τ (s) ≥ E(M(τ)|Fs) ≥ E(X(τ)|Fs) (3.4)

on s ≤ τ ∩ A for any stopping time τ ≥ s.

(3.3) and (3.4) yield that τ is optimal on A. Indeed, E(X(τ)|Ft) = V (t) ≥E(X(τ)|Ft) holds for any stopping time τ ≥ s.

The following more common verification result correponds to Theorem 2.3 in the frame-work of optimal stopping.

Theorem 3.4 1. Let τ be a stopping time with values in 0, . . . , T. If V ≥ X is asupermartingale such that V τ is a martingale and V (τ) = X(τ), then τ is optimalfor (3.1) and V coincides on up to time τ with the Snell envelope of Definition 3.2.

2. More generally, let τ be a stopping time with values in t, . . . , T. If V ≥ X is anadapted process such that V − V t is a supermartingale, V τ − V t is a martingale,and V (τ) = X(τ), then V (s) coincides for s ≤ t ≤ τ with the Snell envelope ofDefinition 3.2 and τ is optimal for (3.2), i.e. it maximises E(X(τ)|Ft).

3. If τ is optimal for (3.2) and V denotes the Snell envelope, they have the properties instatement 2.

Proof.

1. This follows from the second statement.

2. This immediately follows from choosingM = V in statement 2 of Proposition 3.3 butwe give a short direct proof as well. For any competing stopping time τ with valuesin t, t+ 1, . . . , T, Lemma 1.4 yields

E(X(τ)|Ft) ≤ E(V (τ)|Ft) ≤ V (t),

with equality everywhere for τ = τ .

36 CHAPTER 3. OPTIMAL STOPPING

3. τ ≥ t, V ≥ X and adaptedness of V are obvious. It remains to be shown thatV − V t is a supermartingale, V τ − V t is a martingale, and V (τ) = X(τ). Using theidentification of Remark 3.1, we have V (t) = J(t, 1). Theorem 2.3(1) yields that Vand hence also V − V t are supermartingales. In particular, V (t) ≥ E(V (τ)|Ft). Butoptimality of τ implies

V (t) = E(X(τ)|Ft) ≤ E(V (τ)|Ft). (3.5)

Hence, equality holds in (3.5), which yields X(τ) = V (τ) as well as E(V τ (T ) −V t(T )) = 0 = V τ (0)−V t(0). The martingale property of V τ −V t follows now fromLemma 1.5.

Remark 3.5 Statement 3 in Theorem 3.4 shows that the sufficient conditions in Proposition3.3 are necessary, i.e. for the Snell envelope V there exists a martingale M as in statements1 resp. 2 of this proposition. Indeed, one may choose M := V (0) + MV if V = V (0) +MV + AV denotes the Doob decomposition of V .

Hence, Proposition 3.3 can in principle be used to determine the Snell envelope nu-merically, namely by minimizing M(0) over all martingales dominating X . The resultingprocess coincides with the Snell envelope up to time τ . Cf. also Remark 9.7 in this context.

The following result helps to determine both the Snell envelope and an optimal stoppingtime.

Theorem 3.6 Let V denote the Snell envelope.

1. V is the smallest supermartingale dominating X .

2. V is obtained recursively by V (T ) = X(T ) and

V (t− 1) = maxX(t− 1), E(V (t)|Ft−1)

, t = T − 1, . . . , 0. (3.6)

3. The stopping times

τ t := infs ∈ t, . . . , T : V (s) = X(s)

and

τ t := T ∧ infs ∈ t, . . . , T − 1 : E(V (s+ 1)|Fs) < X(s)

(3.7)

are optimal in (3.2), i.e. they maximise E(X(τ)|Ft).

Proof.

2 and 3. Define V recursively as in statement 2 rather than as in Definition 3.2 andset τ = τ t or τ = τ t. We show that τ and V satisfy the conditions of Theorem3.4(2). It is obvious that V is a supermartingale with V ≥ X and V (τ) = X(τ). Fixs ∈ t+ 1, t+ 2, . . . , T. On the set s ≤ τ we have V (s− 1) = E(V (s)|Fs−1) bydefinition of τ . Hence V τ − V t is a martingale.

37

1. In view of Theorem 3.4(3) and statement 3 it remains to be shown that V ≤ W forany supermartingale W dominating X . To this end observe that

V (t) = ess supE(X(τ)|Ft) : τ stopping time in t, t+ 1, . . . , T

≤ ess sup

E(W (τ)|Ft) : τ stopping time in t, t+ 1, . . . , T

≤ W (t)

by Lemma 1.4.

In some sense, τ t is the earliest and τ t the latest optimal stopping time for (3.2). Oftenthe optimal stopping time is unique, in which case we have τ t = τ t. The solution to theoriginal stopping problem (3.1) is obtained for t = 0. In particular, Theorem 3.6(3) yieldsthat an optimizer of (3.1) exists.

Remark 3.7 1. In terms of the drift coefficient aV of V as in Lemma 1.20, (3.6) and(3.7) can be reformulated as

maxaV (t), X(t− 1)− V (t− 1)

= 0, t = 1, . . . , T

andτ(t) = T ∧ inf

s ∈ t, . . . T − 1 : aV (t+ 1) < X(t)− V (t)

,

respectively.

2. If the reward process X is nonnegative, one may also consider infinite time horizonT =∞, in which case we setX(∞) := 0. Proposition 3.3 and Theorems 3.4, 3.6(1,2)remain true in this case. However, it is not obvious how to obtain V from the “infiniterecursion” (3.6) any more. Moreover, an optimal stopping time may fail to exist.

As an example we consider the price of a perpetual put option in the so-called Cox-Ross-Rubinstein model.

Example 3.8 (Perpetual put) Suppose that S(t) is a geometric random walk such thatS(t)/S(t − 1) has only two possible values u > 1, d := 1/u < 1 which are assumedwith probabilities p resp. 1− p. In particular, the process S moves only on the grid S(0)uZ.Consider the reward process X(t) = e−rt(K − S(t))+, t = 0, 1, 2, . . . with some constantsr > 0, K > 0. In the context of Mathematical Finance, S(t) represents a stock price andX(t) the discounted payoff of a perpetual put option on the stock that is exercised at time t.The goal is to maximise the expected discounted payoff E(X(τ)) over all stopping times τ .

We make the natural ansatz that the Snell envelope is of the form

V (t) = e−rtv(S(t)) (3.8)

for some function v. If we guess that it is optimal to stop when S(t) falls below somethreshold s? ≤ K, we must have v(s) = (K − s)+ for s ≤ s?. As long as S(t) > s?, theprocess e−rtv(S(t)) should behave as a martingale, i.e.

0 = E(∆V (t)|Ft−1)

= e−rt(pv(S(t− 1)u) + (1− p)v(S(t− 1)d)− erv(S(t− 1))

), (3.9)

38 CHAPTER 3. OPTIMAL STOPPING

which only holds if v grows in the right way for s > s?. A power ansatz for v turns out tobe successful, i.e.

v(s) =

K − s for s ≤ s?,cs−a for s > s?

with some constants s?, a, c > 0. In order for (3.9) to hold, a needs be be chosen such thatpu−a + (1− p)ua = er, i.e.

u−a =er −

√e2r − 4p(1− p)

2p.

Subsequently, we hope that some sort of contact condition at the boundary leads to thesolution, which is often true for optimal stopping problems. More specifically, we choosethe largest c > 0 such that the linear function s 7→ K−s and the decreasing convex functions 7→ cs−a coincide precisely in one element s? in S(0)uZ, i.e. of the form s? = S(0)uk forsome integer k. Define the stopping time τ := inft ≥ 0 : S(t) ≤ s? and V as in (3.8). It isnow easy to verify that V ≥ X , V (τ) = X(τ), and V τ is a martingale. In view of Theorem3.4, it remains to show that V is a supermartingale. To this end, fix t ∈ 1, . . . , T. OnS(t− 1) > s? we have

E(V (t)|Ft−1) = E(e−rtcS(t)−a|Ft−1) = e−r(t−1)cS(t− 1)−a = V (t− 1).

Similarly, we have

E(V (t)|Ft−1) ≤ E(e−r(t)cS(t)−a|Ft−1) = e−r(t−1)cS(t− 1)−a = V (t− 1)

on S(t− 1) = s?. On S(t− 1) < s? we argue that

E(V (t)|Ft−1) = E(e−rt(K − S(t)|Ft−1)

= e−rtK

(1− S(t− 1)

s?

)+S(t− 1)

s?E

(e−rt

(K − S(t)

S(t− 1)s?)∣∣∣∣Ft−1

)≤ e−rtK

(1− S(t− 1)

s?

)+S(t− 1)

s?E

(e−rtc

(S(t)

S(t− 1)s?)−a∣∣∣∣∣Ft−1

)

= e−rtK

(1− S(t− 1)

s?

)+S(t− 1)

s?e−r(t−1)c(s?)−a

= e−rtK

(1− S(t− 1)

s?

)+S(t− 1)

s?e−r(t−1)(K − s?)

≤ e−r(t−1)(K − S(t− 1)) = V (t− 1),

which finishes the proof.If u is small, we can compute approximations of c, s?. Indeed, at s? the linear function

s 7→ K−s is almost tangent to s 7→ cs−a, i.e. their derivatives coincide. The two conditionscs?−a = K−s? and−acs?−a−1 ≈ −1 are solved by s? ≈ Ka/(1+a) and c ≈ K1+aaa/(1+a)1+a.

The Snell envelope can also be obtained by minimization over martingales rather thanmaximizing over stopping times. This fact is sometimes used for numerical solution ofoptimal stopping problems.

39

Proposition 3.9 The Snell envelope V of X satisfies

V (0) = min

E

(sup

t=0,...,T(X(t)−M(t))

): M martingale with M(0) = 0

and, more generally,

V (t) = min

E

(sup

s=t,...,T(X(s)−M(s))

∣∣∣∣Ft

): M martingale with M(t) = 0

for any t ∈ 0, . . . , T.

Proof. The first statement follows from the second one.“≤”: If τ is a stopping time with values in t, . . . , T, the optional sampling theorem

yields

E(X(τ)|Ft) ≤ E(X(τ)−M(τ)|Ft) ≤ E

(sup

s=t,...,T(X(s)−M(s))

∣∣∣∣Ft

)Since V (t) is the supremum of all such expressions, we have V (τ) ≤ min. . . .

“≥”: Since V is a supermartingale, the predictable part AV in its Doob decompositionV = V (0) +MV + AV is decreasing. The desired inequality follows from

E

(sup

s=t,...,T

(X(s)−MV (s) +MV (t)

)∣∣∣∣Ft

)= E

(sup

s=t,...,T

(X(s)− V (s) + V (0) + AV (s) +MV (t)

)∣∣∣∣Ft

)≤ E

(sup

s=t,...,T

(V (0) + AV (s) +MV (t)

)∣∣∣∣Ft

)= E(V (t)|Ft) = V (t).

Chapter 4

Markovian situation

Above we have derived results that help to prove that a candidate solution is optimal. How-ever, it is not obvious yet how to come up with a reasonable candidate. A standard approachin a Markovian setup is to assume that the value process is a function of the state variablesand to derive a recursive equation for this function — the so-called Bellman equation.

We consider the setup of Chapter 2 with a reward function as in Example 2.1. Supposethat the conditional jump distribution K(α) as in Definition 1.17 of the controlled processX(α) is of Markovian type in the sense thatK(α)(t, ·) depends on α only throughX(α)(t−1)and α(t), i.e.

K(α)(t, ·) = κ(α(t), t, X(α)(t− 1), ·) (4.1)

for some deterministic function κ. Moreover, assume that — up to some measurability orintegrability conditions — the set of admissible controls contains essentially all predictableprocesses with values in some set A ⊂ Rm. The initial value X(α) is supposed to coincidefor all controls α. Under these conditions, it is natural to assume that the value process is ofthe form

J(t, α) =t∑

s=1

f(s,X(α)(s− 1), α(s)) + v(t,X(α)(t)) (4.2)

for some so-called value function v : 0, 1, . . . , T × Rd → R of the control problem.Indeed, what else should the optimal expected future reward depend on?

In order for the supermartingale/martingale conditions from Theorem 2.3 to hold, weneed that

E(J(t, α)− J(t− 1, α)|Ft−1)

= f(t,X(α)(t− 1), α(t)) + E(v(t,X(α)(t))− v(t− 1, X(α)(t− 1))|Ft−1)

= f(t,X(α)(t− 1), α(t))

+

∫ (v(t,X(α)(t− 1) + y)− v(t,X(α)(t− 1))

)κ(α(t), t, X(α)(t− 1), dy)

+ v(t,X(α)(t− 1))− v(t− 1, X(α)(t− 1)) (4.3)= (f (α(t)) +G(α(t))v + ∆tv)(t,X(α)(t− 1)) (4.4)

is nonpositive for any control α and zero for some control α where we used the notation

(G(a)u)(t, x) :=

∫u(t, x+ y)κ(a, t, x, dy)− u(t, x), (4.5)

40

41

∆tu(t, x) := u(t, x)− u(t− 1, x), (4.6)

andf (a)(t, x) := f(t, x, a).

These considerations lead to the following result.

Theorem 4.1 As noted above we assume that there is some deterministic function κ suchthat

E(1B(∆X(α)(t))

∣∣Ft−1

)= κ(α(t), t, X(α)(t− 1), B), (4.7)

α ∈ A , t ∈ 1, . . . , T, B ⊂ Rd. In addition, let A ⊂ Rm be such that any admissiblecontrol is A-valued.

Suppose that function v : 0, 1, . . . , T × Rd → R satisfies

v(T, x) = g(x), (4.8)

the Bellman equation

supa∈A

(f (a) +G(a)v + ∆tv)(t, x) = 0, t = 1, 2, . . . , T, (4.9)

and

α?(t) = argmaxa∈A(f (a) +G(a)v + ∆tv)(t,X(α?)(t− 1)), t = 1, 2, . . . , T (4.10)

for some admissible control α?, where we once more used the notation (4.5). Then α? isoptimal and (4.2) is the value process with corresponding value function v.

Proof. Define (J(·, α))α∈A as in (4.2). The initial value J(0, α) coincides for all controlsα by assumption. (4.8) implies that J(T, α) = u(α). Equations (4.9) and (4.3) yield thatJ(·, α) is a supermartingale for any admissible control. Similarly, (4.9, 4.10, 4.3) imply themartingale property of J(·, α?). The assertion follows now from Theorem 2.3.

Note that the Bellman equation (4.9) allows to compute the value function v(t, ·) recur-sively starting from t = T , namely via v(T, x) = g(x) and

v(t− 1, x) = supa∈A

(f (a)(t, x) +

∫v(t, x+ y)κ(a, t, x, dy)

). (4.11)

Remark 4.2 In the situation of Theorem 4.1, the value function is the smallest function vsatisfying (4.8) and

(f (a) +G(a)v + ∆tv)(t, x) ≤ 0, t = 1, 2, . . . , T (4.12)

for any a ∈ A. Indeed, this follows recursively starting from t = T because (4.12) meansthat

v(t− 1, x) ≥ supa∈A

(f (a)(t, x) +

∫v(t, x+ y)κ(a, t, x, dy)

)and equality holds for the value function.

42 CHAPTER 4. MARKOVIAN SITUATION

Remark 4.3 (Semi-Markovian case) A careful analysis shows that we do not fully need theMarkovian structure (4.1) resp. (4.7) for the above approach to work. Suppose that κ in (4.1)resp. (4.7) depend explicitly on ω in an Ft−1-measurable way. Likewise we allow the valuefunction to be a function v : Ω×0, . . . , T×Rd → R, assumed to be Ft−1-measurable inits first argument ω. Then all of the above remains true, in particular Theorem 4.1, equation(4.11), and Remark 4.2. However, it may be less obvious how to obtain the value functionfrom the recursion (4.11) unless it depends on ω in a simple way.

As an illustration we consider variations of Examples 2.5 and 2.6 for power instead oflogarithmic utility functions.

Example 4.4 (Power utility of terminal wealth) We consider the same problem as in Exam-ple 2.5 but with power utility function u(x) = x1−p/(1− p) for some p ∈ (0,∞) \ 1, i.e.the investor’s goal is to maximise E(u(Vϕ(T ))) over all investment strategies ϕ. In orderto derive explicit solutions we assume that the stock price S(t) = S(0)E (X)(t) follows ageometric random walk.

The set of controls in Example 2.5 is not of the “myopic” form assumed in the beginningof this section. Therefore we consider again relative portfolios π(t), which represent thefraction of wealth invested in the stock, i.e. (2.2). By slight abuse of notation, we writeV (π)(t) for the wealth generated from the investment strategy π, which evolves as

V (π)(t) = v0

t∏s=1

(1 + π(s)∆X(s)

)= v0E (π • X)(t),

cf. (2.3). In order for wealth to stay nonnegative, π(t) needs to be A-valued for

A :=a ∈ R : 1 + ax ≥ 0 for any x in the support of ∆X(1)

,

i.e. we consider the set

A =π predictable : π(0) = 0 and π(t) ∈ A, t = 1, . . . , T

.

(4.9) reads assupa∈A

E(v(t, x(1 + a∆X(1))

))− v(t− 1, x) = 0. (4.13)

We guess that v factors in functions of t and x, respectively. Since the terminal condition(4.8) is v(T, x) = u(x), this leads to the ansatz v(t, x) = g(t)u(x) = g(t)x1−p/(1 − p) forsome function g with g(T ) = 1. Inserting into (4.13) yields

supa∈A

E((1 + a∆X(1))1−p) g(t) = g(t− 1),

which is solved by g(t) = %T−t for

% := E((1 + a?∆X(1))1−p)

anda? := argmaxa∈AE

((1 + a∆X(1))1−p)

Theorem 4.1 now yields that the constant deterministic strategy π?(t) = a? is optimal andthat the value function is indeed of product form v(t, x) = %T−tu(x).

Summing up, it is optimal to invest a fixed fraction of wealth in the stock. The optimalfraction depends on both the law of ∆X(1) and parameter p.

43

In the consumption case, one proceeds similarly.

Example 4.5 (Power utility of consumption) We consider now the counterpart of Example2.6, again with power instead of logarithmic utility, i.e. the aim is to maximise

E

(T∑t=1

e−δtu(ct) + e−δTVϕ,c(T )

)

over all predictable processes (ϕ, c) such that v0+ϕ • S(t)−∑t

s=1 c(s) ≥ 0 for t = 0, . . . , T .As in Example 4.4 the utility function is supposed to be of power type u(x) = x1−p/(1− p).The constant δ represents an impatience rate.

Also as above we need to consider relative portfolios and relative consumption rates, i.e.we consider π(t) and κ(t) as in (2.8, 2.7). Again by slight abuse of notation, we write V (π,κ)

for the corresponding wealth, which equals

Vϕ,c(t) = v0

t∏s=1

(1 + π(s)∆X(s))(1− κ(s)) = v0E (π • X)(t)E (−κ • I)(t)

cf. (2.9). Similarly as in Example 4.4 the set of admissible controls is defined as

A =

(π, κ) predictable : (π, κ)(0) = 0 and (π, κ)(t) ∈ A, t = 1, . . . , T

with

A :=

(a, b) ∈ R× (0, 1) : 1 + ax ≥ 0 for any x in the support of ∆X(1).

The Bellman equation (4.9) now reads as

sup(a,b)∈A

(e−δtu(xb) + E

(v(t, x(1 + a∆X(1))(1− b)

))− v(t− 1, x)

)= 0.

with terminal condition v(T, x) = e−δTu(x). The separation ansatz

v(t, x) = e−δtg(t)u(x) = e−δtg(t)x1−p/(1− p)

leads to

sup(a,b)∈A

(e−δb1−p + E

((1 + a∆X(1))1−p) (1− b)1−pe−δg(t)

)= g(t− 1).

Straightforward but tedious calculations yield that this is solved by

g(t) =

(ηT−t + eδ/p

ηT−t − 1

η − 1

)pwith

% := maxa∈A

E((1 + a∆X(1))1−p) ,

η := (%e−δ)1/p.

44 CHAPTER 4. MARKOVIAN SITUATION

The optimal controls are π?(t) = a? and κ?(t) = b? with

a? := argmaxa∈AE((1 + a∆X(1))1−p)

as in Example 4.4 and

b? :=(1 + (%g(t))1/p

)−1=

(1 +

ηT−t − 1

η − 1+ %1/pηT−t

)−1

.

Altogether, we observe that the fixed investment fraction from Example 4.4 is still op-timal in the consumption case. The optimal consumption fraction is deterministic and in-creasing over time.

Finally, we reformulate Theorem 4.1 for stopping problems.

Theorem 4.6 Suppose that X(t) = g(Y (t)) for g : Rd → R and some Rd-valued Markovprocess (Y (t))t=1,2,... with generator G in the sense of (1.18). If function v : 0, 1, . . . , T×Rd → R satisfies

v(T, y) = g(y)

and

maxg(y)− v(t− 1, y),∆tv(t, y) +Gv(t, y) = 0, t = 1, 2, . . . , T, (4.14)

then V (t) := v(t, Y (t)), t = 0, . . . , T is the Snell envelope of X . Here we use the notationGv(t, y) := G(v(t, ·))(y) and ∆tv(t, y) = v(t, y)− v(t− 1, y) similarly as in (4.6).

Proof. Since v(T, Y (T )) = g(Y (T )) and

v(t− 1, Y (t− 1)) = v(t− 1, Y (t− 1))

+ maxg(Y (t− 1))− v(t− 1, Y (t− 1)),

v(t, Y (t− 1))− v(t− 1, Y (t− 1)) +Gv(t, Y (t− 1))= maxg(Y (t− 1)), v(t, Y (t− 1)) +Gv(t, Y (t− 1))= maxX(t− 1), E(v(t, Y (t))|Ft−1),

the assertion follows from Theorem 3.6(2).

As in Theorem 4.1, equation (4.14) allows to compute v(t, ·) recursively starting fromt = T , namely via

v(t− 1, y) = max

g(y),

∫v(t, x)P (1, y, dx)

, t = T, . . . , 1, (4.15)

where P (·) denotes the transition function of Y .

Remark 4.7 The function v : 0, 1, . . . , T × Rd → R is Theorem 4.6 is the smallest onethat satisfies v(t, ·) ≥ g(·), t = 0, . . . , T and ∆tv+Gv ≤ 0. Indeed, this follows recursivelyfor t = T, . . . , 0 because these two properties imply

v(t− 1, y) = max

g(y),

∫v(t, x)P (1, y, dx)

,

with equality for the value function by (4.15).

Chapter 5