stephen thompson - poten & partners - m&a activity and outlook for the global o&g sector

TRANSCRIPT

© POTEN & PARTNERS 2008

CONFIDENTIAL

M&A activity and outlook

Prepared for: SEAAOC

Darwin, August 2015

Stephen Thompson

Manager, LNG & Gas, Asia Pacific

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 1

The world’s oldest and largest specialist LNG

consultancy

• Worldwide reach

• Support from strategy to execution

• ~80 LNG assignments per year

• 40+ full-time professionals, 5 senior advisors and over 700 years of energy experience

POTENCovers all major

functions

COMMERCIAL

SHIPPING

MARKET

TECHNICAL

MERLIN

Unique breadth and depth in LNG industry

MARKET COMMERCIAL

SHIPPINGTECHNICAL

Covers all

major functions

POTEN

MERLIN ADVISORS

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 2

Three basic strategies help drive recent big, M&As

• Strategy #1 - Refocus: Acquire or exit assets in order to refocus on core areas / core

business

• Strategy #2 - Reduce project capital cost: Reallocate some project assets to owners

with lower cost of capital

• Strategy #3 - Global portfolio rationalization: active buying and selling of assets to

optimize value

• Each of these strategies is evident in Australia—together they are restructuring the oil

and gas industry here

• Each strategy is partly subsumed within an overriding, short- or medium-term goal of

increasing cash flow

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 3

Strategy #1 - Refocus

• This strategy is exemplified by

Woodside’s acquisition of Apache’s LNG

assets in Australia and Canada for

US$3.8 billion in December 2014• Apache refocused on its US oil and gas business

• Woodside increased its focus on its core LNG

business in Western Australia, while getting

upside potential with the Kitimat venture in British

Columbia

• Straightforward value proposition to

investors• Lower overhead

• Simpler business

• Greater knowledge / expertise

• More control

• More commitment • Wheatstone, Pluto and Northwest Shelf

cluster for Woodside• WEL has a 1/6th interest in NWS and operates

• WEL has a 90% interest in Pluto and operates

• WEL has a 13% interest in Wheatstone and

operates the Julimar and Brunello fields that supply

20% of the venture’s feedgas

Australian LNG ventures

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 4

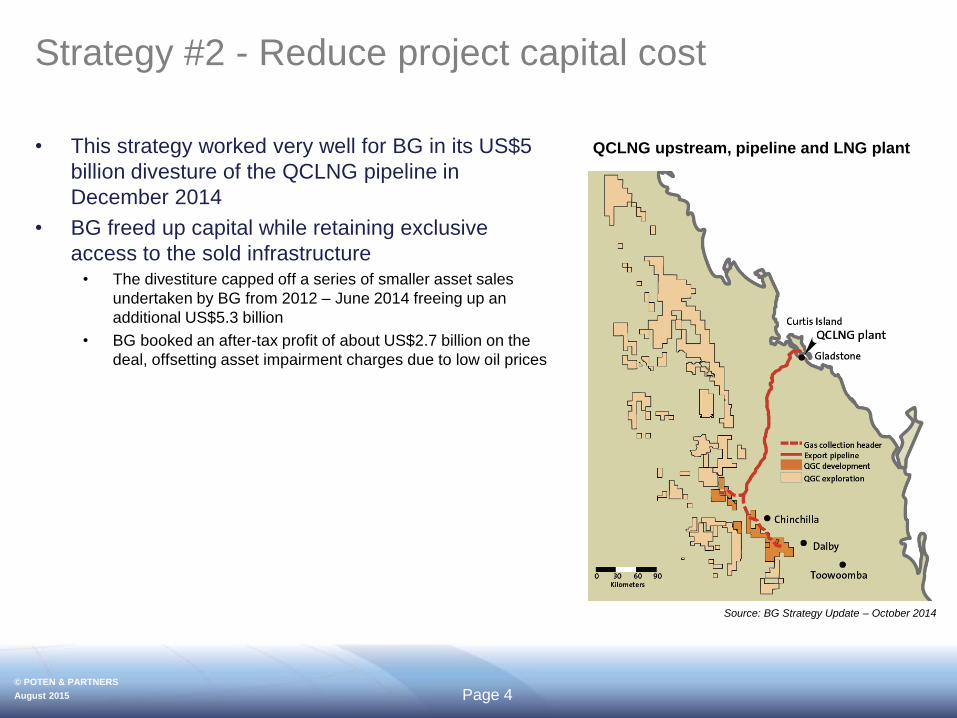

Strategy #2 - Reduce project capital cost

• This strategy worked very well for BG in its US$5

billion divesture of the QCLNG pipeline in

December 2014

• BG freed up capital while retaining exclusive

access to the sold infrastructure• The divestiture capped off a series of smaller asset sales

undertaken by BG from 2012 – June 2014 freeing up an

additional US$5.3 billion

• BG booked an after-tax profit of about US$2.7 billion on the

deal, offsetting asset impairment charges due to low oil prices

QCLNG upstream, pipeline and LNG plant

Source: BG Strategy Update – October 2014

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 5

QCLNG pipeline deal also good for acquirer

• BG’s counterparty, APA, buttressed its position as Australia’s leading pipeline company

while securing a large, low risk, long-term asset • APA’s share price appreciated by 15% on average in the months following announcement of the deal

• The deal turned on APA’s ability to access capital at a lower cost than BG, due to

APA’s recourse to higher leverage and its stable, low-risk infrastructure business• BG kept most of the risk associated with future pipeline throughput

The market liked it: APA shares got a 15% bump

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 6

Strategy #3 - Global portfolio rationalization

• In April 2015 Shell and BG announced agreement for Shell to acquire BG in for £47 billion

(US$82 billion)—27% of which attributable to Australia

• Shell will high-grade combined capital investments—LNG and deepwater are priorities• It also intends to sell assets totalling US$30 in 2016-18, effectively reducing net acquisition cost to US$52 billion

• Total Capex for the combined entity to be cut by around US$10 billion/year

Shell’s worldwide LNG footprint BG’s worldwide LNG footprint

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 7

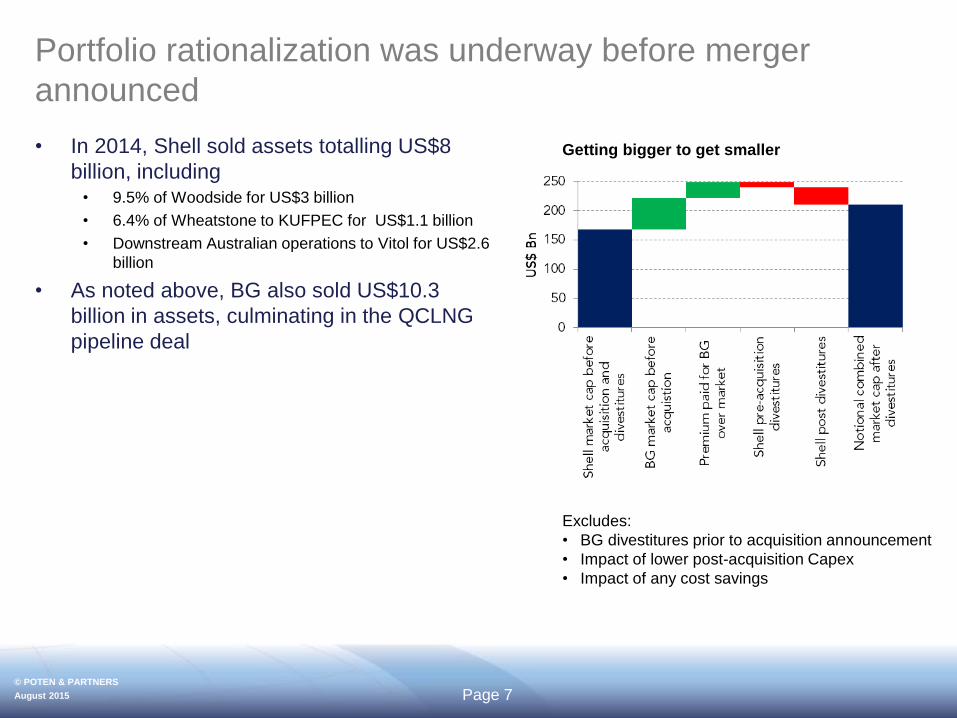

Portfolio rationalization was underway before merger

announced

• In 2014, Shell sold assets totalling US$8

billion, including• 9.5% of Woodside for US$3 billion

• 6.4% of Wheatstone to KUFPEC for US$1.1 billion

• Downstream Australian operations to Vitol for US$2.6

billion

• As noted above, BG also sold US$10.3

billion in assets, culminating in the QCLNG

pipeline deal

Getting bigger to get smaller

Excludes:

• BG divestitures prior to acquisition announcement

• Impact of lower post-acquisition Capex

• Impact of any cost savings

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 8

M&A strategies mix at edge with move toward non-

traditional equity pioneered by US

• US liquefaction ventures turn to non-traditional equity sources• Mandatory convertible bonds (Cove Point T1)

• Private equity (12 ventures + 2 in Canada securing funding from over 16 firms*)

• LPs/MLPs (Sabine, Cameron, Cove Point, Lake Charles)

• Infrastructure investors (Freeport) – IFM has invested US$1.3 in T2

• These equity investments are essentially ways for initial sponsors to divest a part of

their interest in the venture in order to secure the funds required for growth/project

execution

• Vanguard Natural Resources, a US MLP, made two separate acquisitions in Q2 2015

for a total of US$1.1 billion• It relies in part on unconventional outside financing including private equity to pursue its M&A-focused growth

strategy

• Other US players find less welcome attention from non-traditional investors• Activist investment manager JANA Partners amassed a US$1 billion stake in Apache then pressured it to

restructure its asset portfolio

* Includes Temasek Holding investment in Corpus Christi LNG

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 9

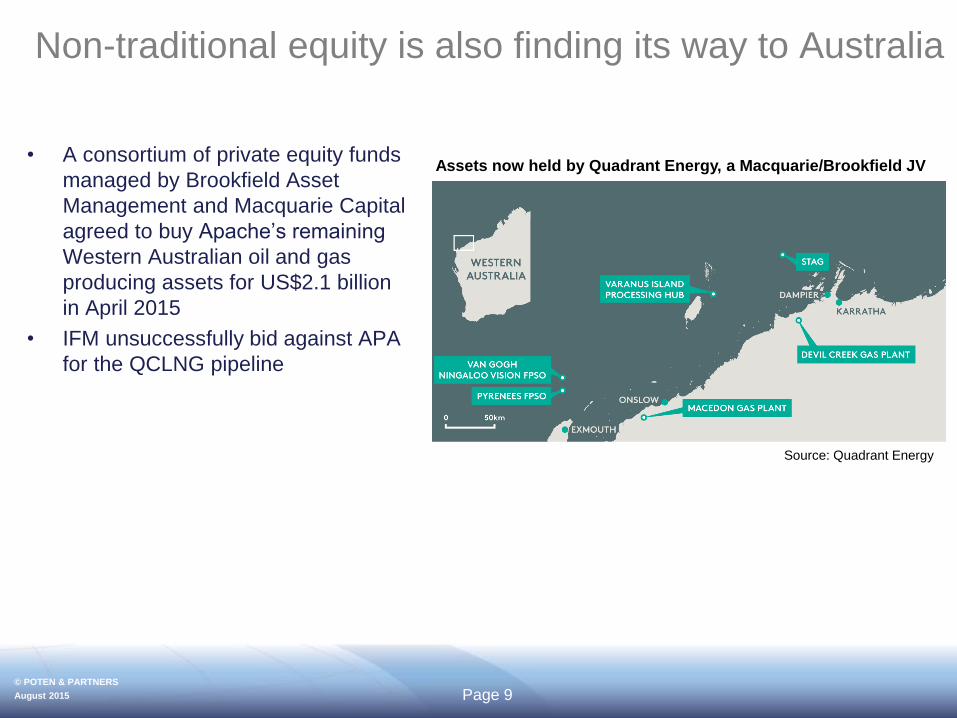

Non-traditional equity is also finding its way to Australia

• A consortium of private equity funds

managed by Brookfield Asset

Management and Macquarie Capital

agreed to buy Apache’s remaining

Western Australian oil and gas

producing assets for US$2.1 billion

in April 2015

• IFM unsuccessfully bid against APA

for the QCLNG pipeline

Assets now held by Quadrant Energy, a Macquarie/Brookfield JV

Source: Quadrant Energy

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 10

Short- to medium-term cash flow goals overshadow

M&A strategies

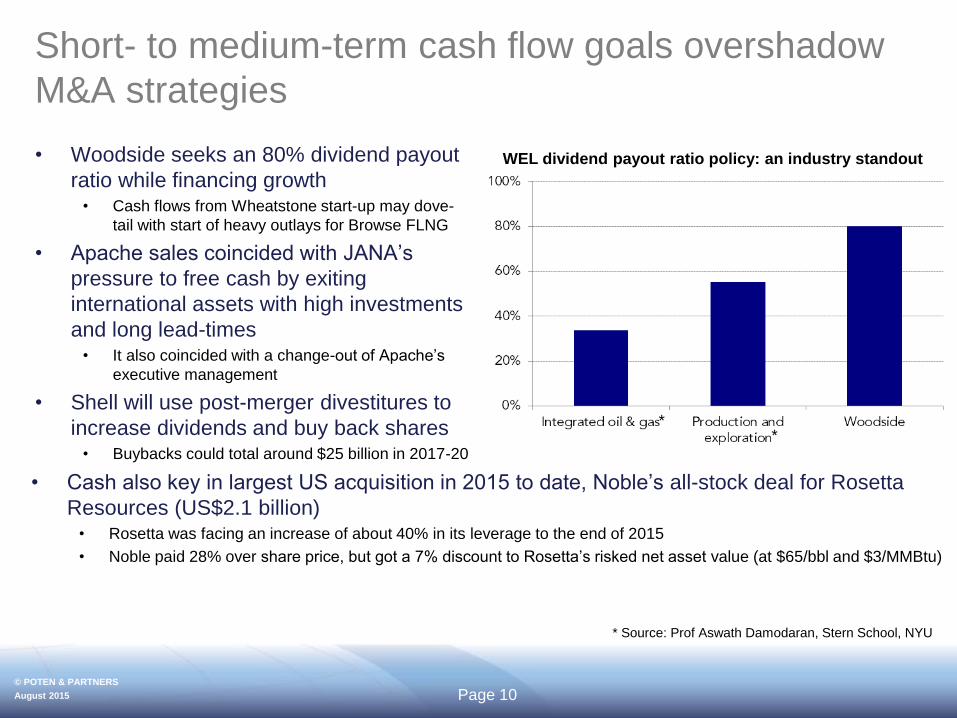

• Woodside seeks an 80% dividend payout

ratio while financing growth• Cash flows from Wheatstone start-up may dove-

tail with start of heavy outlays for Browse FLNG

• Apache sales coincided with JANA’s

pressure to free cash by exiting

international assets with high investments

and long lead-times• It also coincided with a change-out of Apache’s

executive management

• Shell will use post-merger divestitures to

increase dividends and buy back shares• Buybacks could total around $25 billion in 2017-20

WEL dividend payout ratio policy: an industry standout

• Cash also key in largest US acquisition in 2015 to date, Noble’s all-stock deal for Rosetta

Resources (US$2.1 billion)• Rosetta was facing an increase of about 40% in its leverage to the end of 2015

• Noble paid 28% over share price, but got a 7% discount to Rosetta’s risked net asset value (at $65/bbl and $3/MMBtu)

* Source: Prof Aswath Damodaran, Stern School, NYU

**

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 11

An economic framework for understanding M&A

• A corporation chooses how to mix cash

between dividend payouts and share

buybacks, on the one hand, and

reinvestment for future growth on the other• Its share bundles these two sources of value

• Its best potential combinations of these sources of

values are shown in corporate possibilities frontier

• A corporation has strong incentive to move

to a feasible combination of dividends and

growth that provides the highest possible

utility to investors• Utility is shown by the investor preference curve

• Laws of decreasing marginal returns and

satisfaction apply, giving curves their

respective and convex shapes• The best feasible combination for the corporation is

where the two curves touch

Investor preference

curve

Corporate

possibilities frontier

Div

ide

nd

s / s

ha

re b

uyb

acks

Growth potential

Share-price

maximization point

is where curves

touch and are

tangent

Firms exist to keep their investors happy…

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 12

Applying the framework to the current environment

• Firms are not offering the optimal mix of dividends and growth

• The combined corporate possibilities frontiers is greater than the sum of the parts

• M&As can happen for partly symbolic reasons• The event mobilizes the acquiring firm to take actions that it theoretically could have done anyway, but failed to do

• Executive management can “spin” the meaning of the merger or acquisition to the investor community, influencing

its responseD

ivid

en

ds / s

ha

re b

uyb

acks

Growth potential

• Investors perceive oil price crash as a

downshift in corporate possibilities

• This downshift pushes the corporation to a

lower investor preference curve, resulting in a

lower share price

• The point of tangency between curves also

shifts, changing mix of dividends and growth

to weigh dividends more strongly

• M&A in this context can occur for several

reasons• Firms are not performing on the corporate possibilities

frontier

Adverse shifts in business environment

change the meaning of investor happiness

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 13

More to come

• All three M&A strategies are viable

• Cash flow pressures continue to build

as oil prices languish

• Plenty of capital to be accessed• Not all from traditional sources

• M&A may well pick up pace

Oil price rebound was short-lived

Hot off the presses

Source: CNBC, Bloomberg

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

August 2015 Page 14

LNG & NATURAL GAS CONSULTING CONTACTS:

AMERICAS

NEW YORK

Jim Briggs

Tel: +1 212 230 2000

EUROPE, MIDDLE EAST, AFRICA

LONDON

Graham Hartnell

Tel: +44 207 493 7272

ASIA PACIFIC

PERTH

Stephen Thompson

Tel: +61 8 6468 7942