states internhflon4. development agency …pdf.usaid.gov/pdf_docs/pdkat852.pdf · meacr monitoring,...

TRANSCRIPT

fDK485 2-

UNITED STATES INTERNhflON4. DEVELOPMENT COOPERATION AGENCY AGENCY FOR INTERNATIONAL DEVELOPMENT

Washington,. D. C. 20523

JA! AICA

PROJIC PAPER

REVENUE BOARD ASSISTANCE

Amendment No. 2

AID/LAC/P-485 Project Number: 532-0095 CR P-303 P-142 Loan Number: 532-V-023

=MAISSIFIED

______

APPENTIX 3A, Attach.n,t 1

Chapter 3, Handbook 3 (TM 3:43)

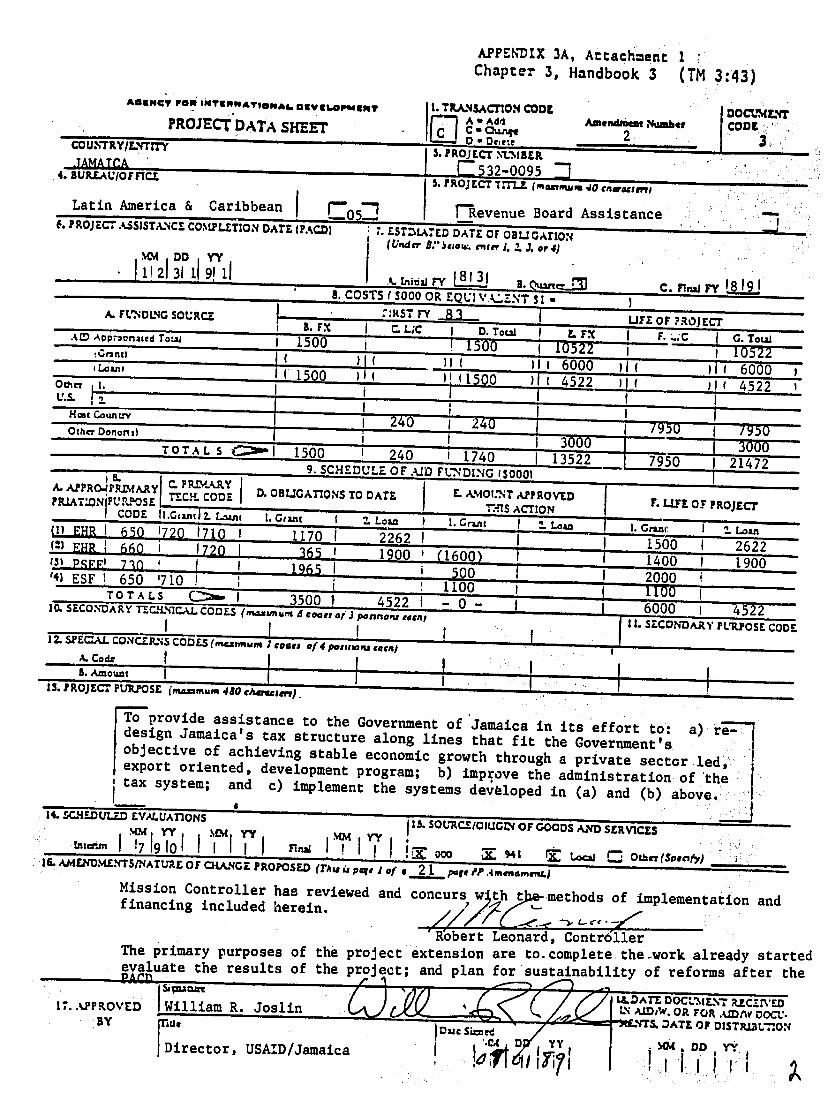

A@EWCY FOR IN"WA. I@A =2V.6+,P,. 1.TpRNSACrIO.IrA a Adel CODE AI~mtrIIwNuaber IMDOCIXcoot 'PROJECT DATA SHEETC U 'A /. ,f"O c-aC C -•Oe:ee 22I OO ,COUNTRY/Wr7TrY

3.FROJ ECT NUMBER" .TAMA TCA

j 532-00954. 3UPJE.AUIOFFIC.Z 5. PROJECT T.r=Z'man ,,W ,40 cnl-ags -

Latin America & Caribbean 05-1 I F-Revenue Board AssistanceF. PROJECT ASSISTA.NCE COMPLETION DATE IPACD) 7.rSTIA7D DATE OF OBLZ GATION

(Under 8:*b egow. enter 1..(' 1.or 4) 112131 11!11i I ,. 8 13 . C...j.n,- yr,,8. COSTS t3000 OR LQ'VA-T $I31

A. F'LNG SOURCE .I - -- Y &3 ._ __ QT-----_ UrO .ROIECrB. X C.LC.IC I .To I LFX I . GcAI1DAPPrcnatedTow~i 1 1500 i 1 _ - ___: ___ __________L 6000"iz102 tc,,o ( Q-- - IH I 6000 6_____-_-___"_,Oche5 15001 45221_ ( i 4522

11

LU.S. . HO Court At 1 240 1 4_-v_73Other Donons)

I 30r TOA : i10 1 240 1 1740 1132 TU 21472 9. SCHEDULE OF AuD FL.DING (50001

PCARYA. A "PPRO I D. OBLIGATIONS TO DATE E AMOI..T APPROVEDPRIAT:O:NJ'PUMOSE .TE. .CODE . - SACTION F__LIFE OF PROJECTL i . ant 1 -1.Gant2. Lo n . rin t 2.Loan G m 1 . Ln(1 650 '720 1710 1, 1170 Ii2 jjJ 660 1 1720 I 365

2262 I, .... 26221 .900- .(1600) 1 140(3) PFF' 710 1 I 191969 1 1 50092000

f4 l ESF ! 650 '7 TOTALS

10 I 3500 1

1100 11004522 1 - 0 _____n10.SECONDARY TECNiCAL CODES(aaamurn6 000 4522coast orJponnons fcnt ______.... _ II.SZCOUjUYPLRPOSECOOE

12. SP£MFA- CONCERNS CODES (maxnnum 7 coaes of4 posionj 96cA1A.Code 1 • " B.Amount l .

13. PROJECT PUR.POSE (m.actmum 480 cAwawg).-

To provide assistance to the Government of Jamaica in its effort to: a) redesign Jamaica's tax structure along lines that fit the Government'sobjective of achieving stable economic growth through a private sector led,export oriented, development program; b) improve the administration of thetax system; and c) implement the systems devbloped in (a) and (b) above. 'I

14.50hEDULED EVALUATIONS 1. SORCEIOIUGLN OF GOODS A, D SERVICES --

Inei 11'!7 1 y %1oo atI [-ber(Spcfyj~LOI'ILAMEINDM.ENSNIATUR. OF ___CHANGE PROPOSED (Thui pqe I of. 21 parfP.4menam)

Mission Controller has reviewed and concurs wth the-methods of implementation andfinancing included herein. 4.

'R'obert Leonard, Contr6llerThe primary purposes of the project extension are to.complete the-work already startedevaluate the results of the project; and plan for sustainability of reforms after the , " tLLDATE " +17. PPROVED ISWilliam R. Joslin DOCL.%sLV- REC-IVED

INA"W'ORFORAriWY [.D 00C1-' ucS. DATE OF DISTR13L

Director, USAID/Jamaica I " I ;04

Table of Contenbts

Project Data Sheet Action Memo to the Director Project AuthorizatLon Amendment List of Acronyms

I. Summary and Recommendations 1

A Summary Description of the Project:Extension iB. Recommendations 1

II Project Background and Description 1 A. Background 1 B. Project Description 2

1. The Project as Implemented to Date 2

2. Proposed ProjectExtension'Activities 4

(i) Computerization 5

(ii) Training, 9

1-iiProceduralrAssistance for Tax A'dministration :12

(iv) Monitoring,, Evaluation, Adjustm'ent. and'COhtinuing.Ref orm..13

III. Implementation and Financing. 14

A. Present Situation. 14B. Cost Estimates and Financial Pl:an, 14C. Implementation Schedule 19

IV. Monitoring, Evaluation Plans,Conditions Precedent

and Covenants 20,

V. Unfinanced Requirements, 20

iList of AcronVms

EEC European .Economic Community

EDP Electronic,Data.Processing

FACT Finance andAccOntingC..ollegeof Training

FSL Fiscal Services Limited

GCT General Consumption Tax

GOJ Government 'of"Jamaica,

'IRS Internal ):Revefnu Service

LOP Life of Project,

MEACR Monitoring, Evaluat ion, Adj.ustment,...:and ContinuinggReform'

PACD Project"Assist ance Comp:leti on 'Date

SAT SystemsAcceptanceTei

--

I. Summary and Recommendations

A. Summary Descrition of the Second Project Paoer Supplement.

The primary purposes of the project extension are to completethe work already started; evaluate the impact and results of theproject, and to plan for the sustainability of the project reforms after the PACD. The emphasis during the extension period will be on tax administration, and to a lesser extent, on tax policyissues. Project extension activities will focus on:

1. Implementation of the GCT effective January 1, 1990.

2. Completing the computerization efforts started earlier.

3. Institutional strengthening through training.

4. Overall project evaluation.

5. Policy analysis necessary for further tax reforms, eg." in payroll taxation.

By the time the project is completed on December 31, 1991,the GOJ should have a modern tax system that is fully consistentwith private sector led, export-oriented development and that canbe sustained with little outside technical assistance.

B. Recommendations

It is recommended that:

The Board of Revenue Assistance Project be extended',as, described in thisldocument i

-- A new PACD ofDecemberl3, 1991 be authorized.

,II. Project Background and Descriotion

A. Bkground

In 1983 USAID developed the Revenue Board Assistance Projectto provide technical assistance to help the Government of Jamaica (GOJ) reform its tax system to make it consistent with the achievement of a more nearly market directed economy, efficientutilization of resources and stable economic growth. Workingthrough the newly created Revenue Board, this technical assistance project has had two components -- tax policy and tax administration -- conducted in two overlapping phases -- design and implementation.

5X

-2-

With the legislative enactment of the personal income tax reformsand property tax reforms in 1986, and the corporate income taxes in1987, and the scheduled implementation of the GCT effective January1, 1990, the design of the new tax structure will be substantiallycomplete and carried out up to the point at which the new system isinstalled and ready to run. In addition, the GOJ by agreementwith the World Bank, is implementing a streamlined set of importduties and taxes.

In summary, the project to date has included tax policyreforms, implementation of the reforms, and basic training in theadministration of the new system. In this extension, the primaryobjective is to complete the work already started and to completethe project assistance by the end of 1991.

B. Project Description

This project, in conjunction with other on-going and plannedprojects, is expected to contribute significantly towards a largergoal of assisting Jamaica in reaching a path to sustainable stablegrowth of employment, production and income.

1. The Proiect as Implemented to Date

Initially, Syracuse University was the prime technicalassistance contractor under the project, and provided the requiredadvisors, analysts and staff.

The design of the project called for two major activities:

(a) I ii . Structural studies that would analyze thedata and issues and point the way to viable tax reform.

(b) Tax Administration. Basic administrative improvementsthat could be implemented prior to the full structural reform or as the reform proceeded, and training and theestablishment of a training capability.

Taxolic.y. On June 6, 1985, the GOJ issued a "Green Paper"that contained the GOJ's tentative proposals for comprehensive taxreform. The reform proposals were guided by four principles:

Neutrality. The tax structure should interfere aslittle as possible with 'the responsiveness of the economy to market forces.

'I0

-3-

Equity. The old tax system was not very equitable in practice because high and steeply graduated rate structures of the individual income tax encouragedevasion, avoidance and the creation of legal loopholes.

Buoyancy. Tax revenue should grow with real GDP growth,,but at a lower rate so that the share of GDPrepresented by public sector activities declines.

Simplicity. The tax system should be susceptible to efficient administration within the constraints ofadministrative capabilities, and should be easilyunderstood by taxpayers.

The analytical work of the Syracuse team and the review by ahigh level Tax Reform Committee, appointed by the Prime Minister,laid the basis for the following GOJ decisions:

Legislative enactment in February 1986 of the personalincome tax reforms, which introduced a flat rate tax of 33-1/3 percent and an exemption level of J$8,580(US$1,560 at US$1 = J$5.5).

Legislative enactment of new property tax reforms in February 1986.

Implementation of a reformed corporation income tax in 1987.

Plans for a new general consumption tax (GCT) to : replace myriad indirect taxes in October 1986..,

For various reasons, including a:change in governmen~ he ....GCT has not yet been implemented. The new government has embraced,GCT and is planning to implement it effective January 1, 1990.

Tax Administration. The GOJ organization for taxadministration was changed with the coming into operation of theRevenue Administration Act on September 1, 1985. The Act createdfive new departments under the aegis of the Board of Revenue:

-- Income Tax Department -- Inland Revenue -- Customs and Excise -- Stamp Duties -- Land Valuation

-4-

The new arrangements under the Revenue Administration Act areintended to:

a) Rationalize the functions of assessment and collectionthrough organizational adjustments;

b) Improve service to the public through simplificationof existing procedures, forms and records, andcomputerization of the revenue collection system;

c) Improve existing physical facilities;

d) Promote efficiency throughout the Revenue Serviceby.improving the management and control functions of the,Department;

e) Provide more meaningful career developmentopportunities for employees.

The project, to date, has made important contributions in theareas of administration. Initially, through the prime contractor,the Customs Administration Advisor concentrated on replacingobsolescent procedures, training, and assistance in theestablishment of a suitable structure for the new Customs andExcise Department. A full-time Training and Comprehensive AuditAdvisor has been assigned to the project. Assistance has beenprovided in developing a master training program for the RevenueBoard. A training center was established and is furnished withmodern training equipment. Training courses have includedaccounting, auditing techniques, customs and excise valuation, andvarious revenue laws.

In addition a full-time GCT advisor has been utilized toprovide assistance to the Revenue Board to prepare for theimplementation of the new tax.

This project included a construction component, whichincluded a USAID contribution of $1,000,000; however, this component was not funded by USIAD.

2. Proposed Project Extension Activities

While the accomplishments of the project to date are'notable, much remains to be done. If the project were to end now,it would be difficult for the GOJ to push forward with the fullimplementation of the tax reform and administration plans.

The project objectives will not have been accomplisheduntil a modern and efficient tax system is fully in place and untilthe various elements of the new tax structure have been harmonizedwith-general economic objectives.

--

-5-

In particular, the extension will provide support forthe implementation of the last major tax reform component, i.e.GCT, and will help to ensure the sustainability of the new taxstructure; by completing the computerization started earlier in the .project by strengthening and deepening the administration andtraining efforts; and by continuing analytical work vital tofurther policy initiatives.

The basic rationale for AID assistance for the projectextension lies in the observation that the most cleverly andefficiently designed tax system and carefully drafted tax statutesare only as effective as their administration. Significantefforts have been devoted to tax administration, but prior effortsneed to be completed to get the full benefit of the efforts alreadyexpended. The present interest of the Government of Jamaica incompleting the strengthening of administrative capabilities as partof a major tax reform effort reflects the understanding that arevitalization of tax policy must be accompanied by improvements inthe effectiveness and efficiency of tax administration.

(i) Computerization.

The prior administrative system was mostly a manualoperation which was incapable of generating information necessaryto monitor the efficiency of tax collections and assessments.Significant work is underway to modernize through extensivecomputerization, but this work is not yet complete. The Board ofRevenue has identified the completion of this modernization of thenew tax structure via computerization of the assessment andcollection functions as its first priority for the projectextension.

To strengthen tax administration and to complete thecomputerization efforts, this extension proposes the use of a fulltime EDP advisor (possibly from IRS) for 12 months and the trainingof 10 computer audit specialists.

The overall objectives of the revenue serviceautomation effort are as follows:

To improve the identification of tax payers and toreduce avoidance and evasion on the part of thehard-to-tax sectors. This can be done by creatinga Master List of taxpayers and assigning a uniquetaxpayer ID number.

To automate record keepinq, tax calculations and billing for all taxes.

cV

To increase the tax base through computer assisted assessment. This can be done for income tax, bydetecting, through third party information, peoplecurrently not paying or underpaying. Similar useof third party information can be made with respect to GCT, import taxes and company tax.Property valuation can also be improved throughcomputer assisted mass appraisal.

To improve the quality and quantity of information on the amounts assessed and collected as the basis for projections of cash flow in the consolidatedfunds. The availability of a computerized profileof taxpayers will allow the Revenue Board toevaluate relatively quickly and easily the effects of changing policies on revenue collection.

-- To develop an evolutionary system so as to respondto the need for changes which can be foreseen in the areas of tax policy and administration.

The Revenue Services Automation Plan. The Board of Revenuerequested financial assistance from the EEC in 1981 for the purpose of computerizing its tax system. The EEC has provided a grant of 3.26 million ECUs (about US$2.5 million) for computerhardware and technical assistance. The EEC then commissioned afunctional design and a system requirements specification study.The conclusions reached and recommendations made in the studiesform the basis for the Revenue Services Automation Plan.

In order to implement its automation plan, the Board ofRevenue created Fiscal Services Limited as its wholly ownedsubsidiary. For the purpose of planning and controlling, theRevenue Services Automation Plan has been organized forimplementation in four phases, namely:

Phase 1: computerization of the coll3ction system, Inland' Revenue Department;

Phase 2: computerization of the collection and assessmentl system, Customs and Excise Department;

Phase 3: computerization of the assessment system,o Income Tax-" Department;

Phase 4: computerization of the assessment system, Land

Valuation Department.

-7-

The Board divided its approach to automation into collection(Phase 1) and assessment activities (Phases 3 and 4). In addition,for administrative convenience, an additional category (Phase 2) is used involving all activities associated with customs and excise duties and the GCT. The February 1986 Preliminary Proposalsubmitted to USAID by the Revenue Board divides computerization of Revenue Services into these components.

Collection System. The Collection System constitutes Phase 1 of the automation plan. Included in this system are:

Discharge of all tax liabilities except those associated with Customs.

Functions associated with the Pay As You Earn (PAYE) system of income and other tax withholding for employees.

-- Functions associated with penalties.

-- Creation of maintenance of a taxpayer master file and summary level taxpayer accounts receivable file.

-- Calculation of property tax amounts, and handling of all adjustments thereto.

The collection system includes an electronic data processing(EDP) environment. With EEC assistance, a computer center has been built. Computer hardware has been acquired consisting of threeDigital Equipment Corporation (DEC) Vax 11/785 mainframe computersand associated peripherals. Software development as of July 1989 is estimated to be 75-90% complete.

Assessment System. The assessment system comprises Phases 3and 4 of the Revenue Services Automation Plan. Normally,assessment is associated with the creation of tax liabilities andincludes compliance functions such as tax audit. Under the plannedrevenue services automation, most of the taxes are assessed and collected at the same time. The two major exceptions are propertytax and income tax. In the case of property tax, the actual function of creating the liability has been assumed by the collection system (see above). Income tax is therefore the focus: of the assessment component of the proposed tax administration system. Functions included in the area of income tax assessment are:

-8

-- Recording and data entry of income tax returns.

Initial processing and automated classification of returns. Classification refers to the process of screening returns to identify items which exceed certain thresholds and therefore are flagged for manual examination.

Services for audit and research, including:

- Audit management: tracking of individual cases.

Statistical selection of returns for audit and additional examination.

Third party matchi~ng to assist in identifyingpossible tax liabilities. For example, this mayinclude matching against vehicle registrations,for example, or comparing levels of commercial activity with levels of tax payments.

- Modeling and other automated tools for research.

-- Processing of income tax refunds.

-- Correspondence management.

-- Objections and appeals management.

Software development in these areas, as of July'1989 is estimated to be 75 to 90% complete.

Customs and Excise System. The Customs and Excise Systemrepresenting Phase 2 of the Revenue Services Automation Plan, will facilitate the imposition and collection of all forms of importduties and domestic excise taxes on certain commodities such aspetroleum products. Software development in this area, as of July1989 is estimated to be 75-90% complete.

Proposed Proiect Extension Activities for Comuterization. As mentioned earlier, the focus of the project extension relative to computerization will focus on completing activities alreadybegun and in training computer audit specialists. The RevenueBoard estimates that software development to date is approximately

-9

75-90%. The Revenue Board has experienced some difficulty inmanaging these efforts, including acceptance of the softwarevendor, Datacentralen. To rectify this situation it is proposedthat a full-time EDP advisor (probably from IRS) be added to theproject for 1 year. This advisor would work with the ManagingDirector of FSL. The duties of the EDP advisor would include thecontrol of systems development and implementation including SAT.He/she will also work closely with the GCT advisor, and will have a,background in both tax administration and EDP.

(ii) -zjing

Considerable training has been performed under thisproject. A full-time Training Advisor has been assigned to theproject and it is proposed that he continue in this capacity untilDecember 31, 1990. To date over 3,000 persons have receivedtraining as presented in the following table.

REVENUE AGENT SCHOLARSHIP PROGRAM

Group I (11/86 - 11/87) 10 Group II (1/87 - 12/87) >1i Group III (11/87 - 11/88) 18Group IV (10/88 - 10/89) 21%. Group V (1/89 - 1/90 )

.79 GENERAL TRAINING

Supervisory Management & Executive Trainingl ,460Specialist & Technical Training. 112002Clerical & Support Services Training 76 Instructor Training

ELECTRONIC DATA PROCESSING (EDP) TRAINING

Software Development 102EDP Management 60System Development & Hardware Maintenance JA

-10-

It is proposed that an additional 275 persons willreceive training through December 31, 1990. The training componentof the project extension focuses on two basic areas: (1)meetingthe ongoing training needs in the operating departments, and (2)the continuation of the revenue agent scholarship program described below.

Overall planned training for the extension period is summarized as follows:

Training Reguired Number of Persons'

Specialized Tax Courses - local Z0O Overseas Participant Training 5 Computer Audit Specialists - local. 10 Revenue Agent Scholarship Program - local

TOTAL

(1) Ongoing Training Needs. The most immediate of theBoard of Revenue's ongoing needs is to enable the staff of assessors and collectors to administer the major taxes. There is a very important need to train sales tax inspectors to implement theGCT. In addition, there is a backlog of training to be done with respect to income tax assessment and collections.

(2) Development of the Revenue Agent. The goal ofBoard of Revenue's "Revenue Agent" plan is the recruitment,training, and retention of qualified people to implement the new tax structure, in concert with the advent of modern computercapabilities to do high-speed calculation and analysis of data.The development of the Revenue Agent Scholarship Program is viewed as a success in meeting this goal and will continue during the extension period.

The trained Revenue Agents specialize in one ofthe major tax areas. The revenue agent, however, is able toprovide a "one call does it all" service to taxpayer and caninvestigate the full realm of tax responsibility of each taxpayerwith whom he or she comes in contact. The trained Revenue Agentcan handle all delinquency, compliance and information checkspreviously assigned piecemeal to different personnel from the various tax departments.

It is estimated that 60 students will complete theRevenue Agent Scholarship Program during the extension period.,

USAID's project contribution to training. USAID has beenproviding funding to the training program. This project papersupplement proposes that USAID continue this funding for 24 months. with the bulk of these expenditures coming in the first year.

To date, the Revenue Board has utilized the services of the Finance and Accounting College of Training (FACT). It is proposedthat this arrangement continue during the extension period.

The following is the training budget for the project extension.-

ESTIMATED TRAINING BUDGET FOR PROJECT EXTENSION

Training Advisor 165,500

Specialized Tax Courses 50,00,0

Overseas Participant Training 50;000

EDP'User Training...... 5000

Sub Total 315,;500

Revenue Agent Program

Tuition Fees -Lecturers and Fieldwork Supervisors 106,000"

Textbooks, Manuals etc. 30,000,

Field Trips 2,500,

Living Expenses 127,580

Course "Administration 33,000

Facilities &",Off ice Operations. 2

SubTotal 325,000

Total 640,500

-12

(iii) Procedural Assistance for Tax Administration.

In addition to the EDP and Training Advisors who will work on the preceding two project components, the General Consumption Tax (GCT) Advisor currently assigned to the projectwill continue to assist in installing administrative proceduresthat are more efficient and that conform to the new tax structure,and to ensure that staff are adequately trained for their tasks. In addition short term IRS advisors will be called in as situations warrant to assist in tax administration.

The Consumption Tax Division will have completejurisdiction over registration, interpretation, taxpayer service and education, compliance, audit, assessment, and appeals of tax assessments. Close coordination will be necessary with the Customs Division for the collection of tax at importation, and with the Income Tax Department for the coordination of income tax audit and exchange of information. The centering of responsibility for the consumption tax in one division will provide for an effective administration of the tax. This will enable an orientation toward accounting rather than physical control -- except over a few selected commodities such as alcoholic beverages, tobacco productsand motor fuels.

The objective of this component will be to completethe design of the GCT administration:

-- Create a taxpayer master file, i.e., a data bank for all persons required to register as taxable persons under the GCT.

-- Provide comprehensive, accurate and timely technical information to taxpayers.

-- Develop return forms and payment of tax due by taxpayers.

-- Establish effective audit functions,

-- Develop a system for objections and appeals.

The full implementation of the GCT will require an additional 14, person months for the GCT Advisor currently assigned to the project' The task of this advisor to be funded by USAID will be:

-13

1) To maintain continubus surveillance over the master file, systems developed, to institute control over compliance, develop a taxpayer assistance and education program and to ascertain needs for modifications and upgrading of systems and training of staff.

2) To develop and implement an effective audit .function.

3) To provide continuing technical advice on thelo development and implementation of the audit service, compliance function, the taxpayer assistance and' education program and the upgrading of the technical. knowledge of staff.

4) To develop and implement the necessary administration, and control systems in respect to assessments, objection to assessments and technical support for the defense of appeals in the Revenue Court.

5) To develop and assist in the implementation of a computerized management information system.

6) To monitor on a continuing basis the implementation of. the GCT.

7) To provide support to the EDP specialists in the development of specifications, test data and to generally act as an expert advisor on the requirements of the system and its management.

USAID will provide 14 months of technical assistance of a GCT Advisor at a cost of approximately $163,000. Presently$16,500 is planned for short term IRS consultants related primarilyto taxpayer assistance.

(iv) Monitoring. Evaluation and Adiusting the New Systemand Continuing Reform

Although MEACR are considered important aspects of the project, the focus of the project extension is on other activities during the extension period due to the higher priority of other components and funding limitations. However, $100,000 of extension funds contributed by USAID is budgeted for technical assistance associated with policy analysis necessary for further reform in such areas as payroll taxation.

-14-

III. Imolementation and Financing

A. Present Situation

The administrative and management- responsibilities of theproject are divided between GOJ officials attached to the Board of Revenue and USAID.

The Revenue Board has primary responsibility for managing theimplementation of this project. The Chairman of the Revenue Board. serves as the GOJ's Project Director. He has the final approval onbehalf of the Government of Jamaica for all decisions to implementor refrain from implementing program recommendations.

All technical assistance personnel report directly to theChairman of the Revenue Board. The three long-term advisors workdirectly with Board of Revenue personnel in the performance of theteam's duties, and serve in an advisory or consultative capacity.The Chairman of the Board of Revenue is accountable to USAID forensuring that project inputs are applied in an orderly and timely manner.

B. Cost Estimates and Financial Plan

The total costs of the two-year extension is estimated to beUS$3,649,000. Of this amount, A.I.D. will contribute resources totalling US$1,100,000, while the equivalent of US$2,549,000 willbe contributed by the GOJ. Contingency and inflation factors havenot been considered since a majority of the costs will be incurred during the first year.

1. SuMarv Cost Estimate and Financial Plan

Table I presents a summary of the cost estimates and financial plan for the two-year extension. USAID will finance forty person-months of long and twelve person-monthsof short term U.S. technical assistance, in-country and U.S.short-term training and funds for an evaluation. The GOJcontribution includes construction costs, administrative costs including staffing, supplies, equipment and recurring, costs.

2. Projection of Expenditures by Fiscal Year

Table II shows the estimated expenditures by component byyear. It is projected that 72% of the goods and services. will be provided in U.S. fiscal year 1990 with the balance provided in U.S. fiscal year 1991.

-15-

M3Method'of Imlnlementation and Financin

Table III shows the basic methods of implementation and financing for the USAID funded activities of the Project.The methods of financing do not deviate from AID's preferredmethods as described in the Payment Verification Policies.

The two long term advisors currently under host countrypersonal services contracts will have their contracts extended with prior USAID approval. USAID is the payingagent for these contracts. The other technical assistance will be provided under a PASA with the Internal Revenue Service and Host Country Contracts. The in-country trainingwill be contracted for by the Board of Revenue with the Finance and Accounting College of Training (FACT) with USAID being the paying agent. The USAID's Controller's Office previously reviewed the accounting and reporting capabilitiesof FACT and found them adequate. A follow-up review will be conducted before the close of the ProjecV. FACT opened a special bank account under the current phase for the advance/reimbursement method of financing and this account will be maintained for the extension period.

TABLE I fSUMMARCOST ESTIMATES AND FINANCIAL PLAN, (IN"THOUSANDS)."

INPUTS FX LC TOTALV LC FX LC

1. Technical Assistance Administrative Costs .... 75 7-Training & Comprehensive -Audit Advisor 165 - 165

---

165-General Consumption Tax Advisor,163 ' 163 163Computerization Advisor 130 130

-

130 ' IRS Monitoring of the Implementation of the Policy Analysis (MEACR) - 100600 - 100 -Tax Systems .7I2 _

2. TrainingRevenue Agent Scholarship Prog. - 325 325 - 325Specialized Tax Course " 50 50 50EDP User Training - -

-

50Overseas

0. .-- - 50 25 475: .. 50'" 425

3. Evaluation/Audit - 50 50, - -50

4. Administrative SupportInt*rduction of GCT - 303 303- -'":

Recurrent Budget , 4 " " "'": . -- 849.. 849

5. Construction & Equipment,,

St. Andrew Collection Center . ... .. -

Totals 5:2.-4 2-5,54 9

-17-

TABLE I -'PROJEcTIONS OF EXPENDITURES BY FISCALYEAR

(IN THOUSANDS)

. 2FY90 FY 9 1TOTAL

AID GOJ AID, GOJ AID GOJ

1. Technical Assistance

Administrative Costs " 55 - 20 75 Training &.Comprehensive Audit Advisor

General Consumption Tax Advisor

120

120.

- 45

-43

-

-'

165

63

,

Computerization Advisor 90 - 40.- 130 -I.R.S. Monitoring of the Implementation of the

Policy Analysis (MEACR) 505 50... Tax Systems - -

2. Training

Revenue Agent ScholarshipProgram 250 - 75 -3 5 . -Specialized Tax Course 33 - 17 50 EDP User Training 38 . 12 -

-

50 -

-Overseas -2 15 25 JU550 30

3" 15 1,U 1475 30-U

3. Evaluation/Audit 5

4. Administrative Support Introduction of GCT '200 - 103 303 Recurrent Budget 1-

-

-546

5. Construction & Equipment

St. Andrew Collection Center ,- 1,625 1,625

Totals in, 2.305. a. 23407J1,100 2,579

TABLE III-

Inputs

Technical Assistance-Long Term - U.S.

Short.,Term - U.S Short Term - U.S.

TrainingIn-Country U.S.A.

Evaluation

S/T Tech. Assistance

-18-

METHODS OF IMPLEMENTATION AND FINANCING (IN THOUSANDS)

Method of Method of Implementation ina AmoUntQi

H/C Contract Direct Payment .328 PASA Direct Payment .130

PASA Direct Payment 17 H/C Contracts Direct Payment iO.

H/CG Contract, Advance/Reimbursement 4251 PIO/P's Transfer of Funds.' 50

,AID DiL'rect Direct Payment

Total

C. IMPLEMENTATION SCHEDULE

Activit

Loan/Grant ProAg Amendment' signed

Amend FACT Contract

TA - Training Advisor, contractsigned,

TA,- GCT Advisor, contract'.signed

GCT Legislation Enacted.

TA,- IRS PASA signed Implement GCT

Complete Revenue.AgentScholarship Program.

Departure of Long Term Advisors.

Complete Specialized.Training:

Complete. Software, Deveiopment

Date C om ieted

August 31, 1989

October 31, 1989

October'.31, 1989

October31, 1989.

September 30, 1989

J :"auary "1990 January 1,1990

December3..1i, 1990

December 31, 1990

December 31, 1991

Decembeki3.1 1,99,1

-20-

IV. Evaluation. Monitoring Plans. Conditions Precedent and

Evaluation. An evaluation is planned for July 1990 to verifythat project objectives have been met. Areas of evaluation include the achievement of project goals; sustainability of reforms without further USAID assistance, appropriateness of project inputs, and efficiency and effectiveness of multi-donor participation.

Monitoring Plans. Monitoring will be performed by a Mission Project Committee, whose members will have the following responsibilities:

(1) The Project Officer, currently the Senior Economic Advisor, will be responsible for the primaryadministrative monitoring. The Project Officer will maintain liaison with the Revenue Board, coordinate necessary Mission Project backstopping, and prepareand present quarterly progress reports to the AID mission.

(2) The USAID Controller will review all disbursement requests for conformity with A.I.D. regulations, and will ensure that adequate financial control methods are followed by the Revenue Board.

(3) The USAID Contracting Officer will review all Host Country contracts generated under the project for conformity with A.I.D. regulations.

(4) Quarterly progress reports, and audits, financial and other reports will be required of the Revenue Board.

No additional conditions precedent or covenants are anticipated under this Project Paper Supplement.

V. Unfinanced Reguirements

It should be noted that the original request for USAID financingfrom the Revenue Board totalled over $3 million. Because of the current availability of $1.1 million, selected items had to be eliminated from current plans, however, should additional financing,from either USAID or another donor be available at a later date,consideration should be given to the following components.

2

-21

1. Completion of outstanding' tax reform items $500,000

examination of finan iAl institutions

examination ofltax incentives,

- taxi'burden studies

redeve'lopment of computer model- for revenue projections and monitoring of revenue performance,-

Hardware for Income Tax, Business! 500,000Enterprise Number (BENO), Collection Systems and Public Education, Taxpayer Information and Assistance.

3. Software for Unique Taxpayer Number System 150,000 Taxpayer Information, Education and Assistance

4. Continuation of Training Programs for an 800,000 additional year.

5. Staff Development for Tax.ReformM nitorIngand Evaluation,-Unit: 100,000