state update: south australia€¦ · state update: south australia july 2016 contents 2 | key...

TRANSCRIPT

STATE UPDATE: SOUTH AUSTRALIA JULY 2016

CONTENTS 2 | Key points 3 | In Focus: Structural changes in SA economy reflected in the labour market 4 | Consumer & household sector 5 | Business sector 6 | Commercial property sector 7 | Residential property 8 | Demographics 9 | Labour market 10 | Economic structure and trade 11 | Fiscal outlook 12 | Semi government and credit outlook

CONTACTS Vyanne Lai Riki Polygenis Skye Masters Economist Head of Australian Head of Interest Rate Strategy +61 (0) 386340198 Economics +61 2 9295 1196 [email protected] +61 3 8697 9534 [email protected]

Important Notice This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please click here to view our disclaimer and terms of use.

-4

0

4

8

12

1992 1996 2000 2004 2008 2012 2016

SA Australia

CHART 1: STATE GSP GROWTH FORECASTS Annual growth (%)

CHART 2: STATE FINAL DEMAND Per cent (%)

Source: ABS and NAB Group Economics 2

KEY POINTS: Green shoots emerging for SA economy but fundamentals remain soft

More recently, there are some signs of green shoot emerging for the SA economy; the lower AUD is offering support to areas such as hospitality and education exports, while notable improvements in business conditions and confidence in the NAB Business Survey are a welcome sign that the economic situation is beginning to turn. Recent policy announcements at both the state and federal level, aimed at promoting jobs and economic growth, are also encouraging, although the likely size and timing of their impact is unlikely to fully offset major headwinds, such as the imminent end to car manufacturing activity. Household income growth continues to gain traction, which in turn is supporting retail spending and household consumption. That said, SA’s well-known economic challenges, such as the narrowing industrial base -- characterised more recently by the shutdown of Arrium’s steelworks in Wyalla -- and an industry mix that may not appeal enough to younger workers, have continued to result in a net outflow of interstate migration, weak labour market conditions and limited demand and price impetus for residential property. Following moderate growth in real GSP of 1.8% in 2015-16, we expect the SA economy to grow by another 1.8% in 16-17 and by 2.4% in 2017-18 . The unemployment rate is expected to gradually fall from 7.3% in 15-16 to 7.0% in 16-17 and 6.8% in 2017-18.

There is now more certainty that all of the 12 new submarines under the $50 bn Future Submarines project announced by Federal Government will be built at Osborne in Adelaide starting 2018. This project is expected to create around 2800 new jobs, with 1700 of them at the ASC plant on the Port River at Osborne. However, this will only provide partial offset to the expected 3,000 job losses due to the imminent closure of Holden’s car manufacturing plant at Elizabeth over the course of four years to 2017.With the construction of Royal Adelaide Hospital coming to an end, possibly by December this year, there could be a fall-off in construction activity in the near term, but this will be partly offset by a pick-up in housing construction, indicated by a rise in residential housing approvals.

After moving sideways for a number of years, residential property prices in Adelaide appear to have turned up more notably since the start of 2016, although at a rate that is much lower than the national average. However, the average regional house price has continued to contract over the year to date. We expect Adelaide house prices to grow moderately in 2016 by 3.5%, before easing to 1.7% in 2017.

Supported by surprisingly resilient wages growth, household consumption is a standout contributor to SA’s recent economic performance, with retail spending and household expenditure growth maintaining strong momentum. This is despite generally weak labour market conditions as SA continues to experience the highest unemployment rate across the states and territories.

Business conditions have gained some momentum of late, characterised by higher capacity utilisation and an upturn in the NAB Business Conditions index, although the business investment outlook remains weak and the office vacancy rate is elevated. Capital expenditure expectations for buildings and structures suggest a notable deterioration for 2016-17.

In terms of goods exports, the value of SA’s mineral shipments fell sharply last year, but a partial recovery of commodity prices this year is likely to see a lift in SA’s overall exports. Meanwhile, the lower AUD continues to deliver dividends to the state’s services sectors through higher international student enrolments and overall tourism expenditure.

0

2

4

6

8

10

12

NSW VIC QLD SA WA TAS NT ACT

2013-14 2014-15 2015-16 (f) 2016-17 (f) 2017-18 (f)

IN FOCUS: Structural changes in SA economy reflected in the labour market

Consequently, employment growth in SA has fallen below its civilian population growth, and has mostly lagged the national average since 2011 (Chart 5).

Despite the soft growth in labour force, tepid employment growth has resulted in a gradual rise in SA unemployment rate since 2012, to be the highest among all states (Chart 6). It has moderated somewhat in the last six months, but it is largely attributable to a shrinking labour force rather than a pick-up in employment growth.

Source: ABS, NAB Group Economics

The SA labour market has deteriorated notably relative to the national average since late 2012. A slowing and ageing civilian population and weaker participation rate (Chart 3) have led to subdued growth in SA’s labour force (Chart 4).

Part of this reflects the ongoing structural changes in the industry make-up of the state which is seeing an erosion of its manufacturing base, as evidenced by the recent struggle of Arrium steelworks in Wyalla, while the imminent closure of Holden’s Elizabeth plant next year is likely to see further job losses.

CHART 3: SA AND AUS LABOUR MARKET PARTICIPATION RATE Per cent of labour force

CHART 5: SA AND AUS EMPLOYMENT GROWTH Year-on-year percentage growth

58596061626364656667

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA Participation Rate AUS Participation Rate

%

3

4

5

6

7

8

9

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA UR AUS UR

%%

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA Employment Growth AUS Employment Growth%

-3.0-2.0-1.00.01.02.03.04.05.0

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA Labour Force Growth AUS Labour Force Growth

%

CHART 4: SA AND AUS LABOUR FORCE GROWTH Year-on-year percentage growth

CHART 6: SA AND AUS UNEMPLOYMENT RATE Per cent of labour force

3

CONSUMER AND HOUSEHOLD SECTOR: A pick-up in income helps to support retail and household spending

Probably reflecting the soft fundamentals in the labour market, SA consumershave become more conservative in their spending patterns. Based on our survey,consumers are now less inclined to incur more credit card debt and spend ondiscretionary items such as travel, home improvements etc., while continuing tofocus on paying down their debt and concentrating most spending on essentialitems such as medical expenses, transport and utilities (Chart 9).

Source: ABS, NAB Group Economics 4

Wages growth in SA has managed to maintain momentum, which is helping tosupport household consumption growth (Chart 7).

As a result, retail spending growth remains reasonably resilient. In turn thisappears to be offering some support to house price growth, which is showingsome tentative signs of a pick-up (Chart 8).

CHART 7: AVERAGE COMPENSATION OF EMPLOYEES AND HOUSEHOLD CONSUMPTION GROWTH Year-on-year percentage growth

CHART 9: NAB CONSUMER ANXIETY SURVEY - CONSUMER SPENDING PREFERENCES Changes in Consumer Spending Preferences (net balance)

CHART 8: RETAIL TURNOVER AND HOUSE PRICE GROWTH Year-on-year percentage growth

-5.0%-3.0%-1.0%1.0%3.0%5.0%7.0%9.0%

11.0%13.0%15.0%

2000 2002 2004 2006 2008 2010 2012 2014 2016

Nominal Household Consumption Total Compensation of Employees

-12.0%-8.0%-4.0%0.0%4.0%8.0%12.0%16.0%20.0%

-8.0%-4.0%0.0%4.0%8.0%

12.0%16.0%20.0%24.0%

2006 2008 2010 2012 2014 2016

Adelaide House PriceGrowth (y/y %) - RHSRetail Turnover Growth(y/y%) - LHS

-40-30-20-10

01020

Major HH items

Entertainment

Eating out

Charitable donations

Use of credit

Travel

Home improvementsSavings, super,

investmentsPersonal goods

Groceries

Children

Utilities

Transport

Medical expenses

Paying off debt

Q1'16 Q2'16

-30

-20

-10

0

10

20

30

40

-30

-20

-10

0

10

20

30

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Spread Total South Australia

BUSINESS SECTOR: SA business conditions and capacity utilisation have improved

Consistent with a recent pickup in business conditions, SA capex expectations for the next 12 months have picked up strongly, but business investment growth continues to be subdued. This is likely to be a reflection of the continuously shrinking manufacturing base and weakness in commodity prices (Chart 12), but steadily improving capex expectations suggest that appetite for business investment could improve. In terms of business conditions, the financial services, personal services and transport/utility sectors are the outperformers, while the mining sector is faring the worst (Chart 13).

5 Source: ABS, NAB Group Economics

According to the monthly NAB Business Survey, the capacity utilisation of businesses in SA has been improving of late, albeit falling slightly in Q2 (Chart 10). This trend is consistent with the steady improvements in SA business conditions in the past three months, with the index moving into positive territory (Chart 11).

CHART 10: NAB BUSINESS SURVEY – CAPACITY UTILISATION Per cent of total capacity (%)

CHART 11: SPREAD IN NAB BUSINESS CONDITIONS Net balance, 3-month-moving-average

CHART 12: NAB SURVEY CAPEX EXPECTATIONS & PRIVATE BUSINESS INVESTMENT GROWTH

CHART 13; BUSINESS CONDITIONS AND CONFIDENCE BY INDUSTRY Net balance

74

76

78

80

82

84

86

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA Total

%

-60

-40

-20

0

20

40

60

-30

-15

0

15

30

45

60

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA Capex Expectations (12-month) - LHS

SA Business Investment Growth (y/y%) -RHS

%

-40

-20

0

20

40 Net Balance (%). June quarter 2016

Conditions Confidence

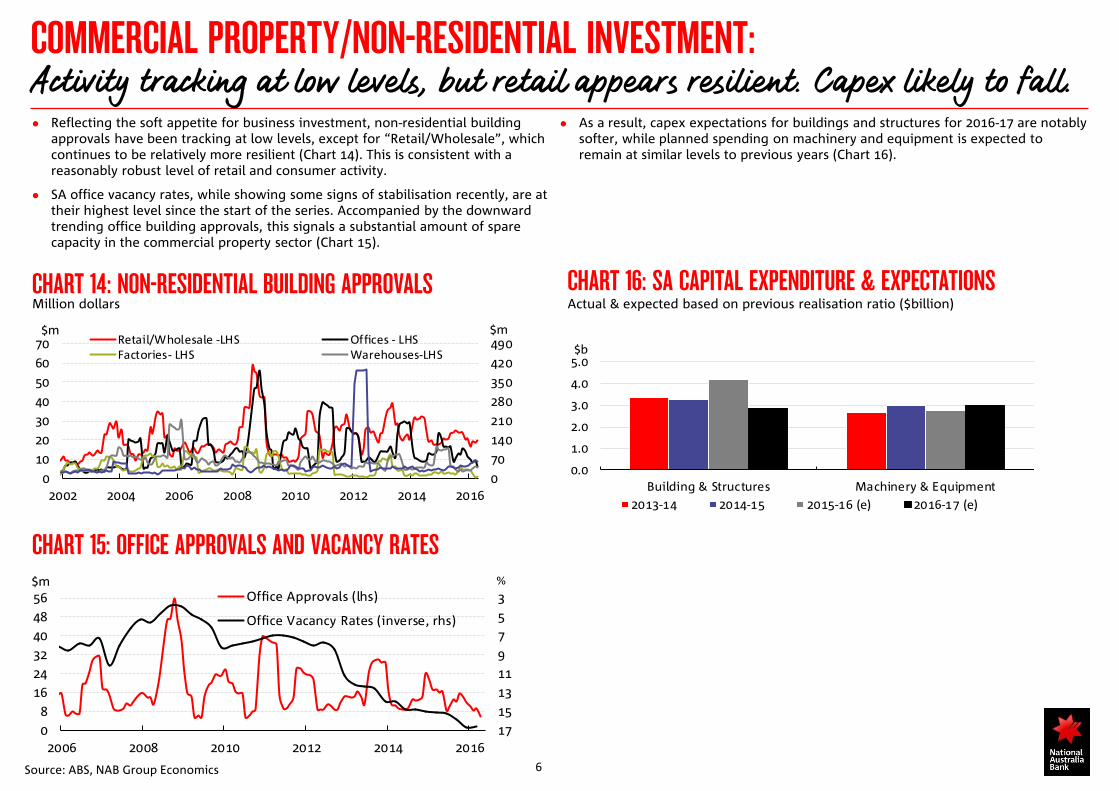

COMMERCIAL PROPERTY/NON-RESIDENTIAL INVESTMENT: Activity tracking at low levels, but retail appears resilient. Capex likely to fall.

As a result, capex expectations for buildings and structures for 2016-17 are notably softer, while planned spending on machinery and equipment is expected to remain at similar levels to previous years (Chart 16).

6 Source: ABS, NAB Group Economics

Reflecting the soft appetite for business investment, non-residential building approvals have been tracking at low levels, except for “Retail/Wholesale”, which continues to be relatively more resilient (Chart 14). This is consistent with a reasonably robust level of retail and consumer activity.

SA office vacancy rates, while showing some signs of stabilisation recently, are at their highest level since the start of the series. Accompanied by the downward trending office building approvals, this signals a substantial amount of spare capacity in the commercial property sector (Chart 15).

CHART 14: NON-RESIDENTIAL BUILDING APPROVALS Million dollars

CHART 15: OFFICE APPROVALS AND VACANCY RATES

CHART 16: SA CAPITAL EXPENDITURE & EXPECTATIONS Actual & expected based on previous realisation ratio ($billion)

0

70

140

210

280

350

420

490

0

10

20

30

40

50

60

70

2002 2004 2006 2008 2010 2012 2014 2016

Retail/Wholesale -LHS Offices - LHSFactories- LHS Warehouses-LHS

$m $m

3579111315170

8162432404856

2006 2008 2010 2012 2014 2016

Office Approvals (lhs)

Office Vacancy Rates (inverse, rhs)

%$m

0.0

1.0

2.0

3.0

4.0

5.0

Building & Structures Machinery & Equipment2013-14 2014-15 2015-16 (e) 2016-17 (e)

$b

-4.0-3.0-2.0-1.00.01.02.03.0

Q1'

13

Q2'

13

Q3'

13

Q4'

13

Q1'

14

Q2'

14

Q3'

14

Q4'

14

Q1'

15

Q2'

15

Q3'

15

Q4'

15

Q1'

16

Q2'

16

Nex

t Q

tr

Nex

t 12

m

Nex

t 2y

Australia SA/NT

ExpectationsEstimated price growth in relevant survey period

%

RESIDENTIAL PROPERTY: Subdued economic conditions continue to constrain SA housing market

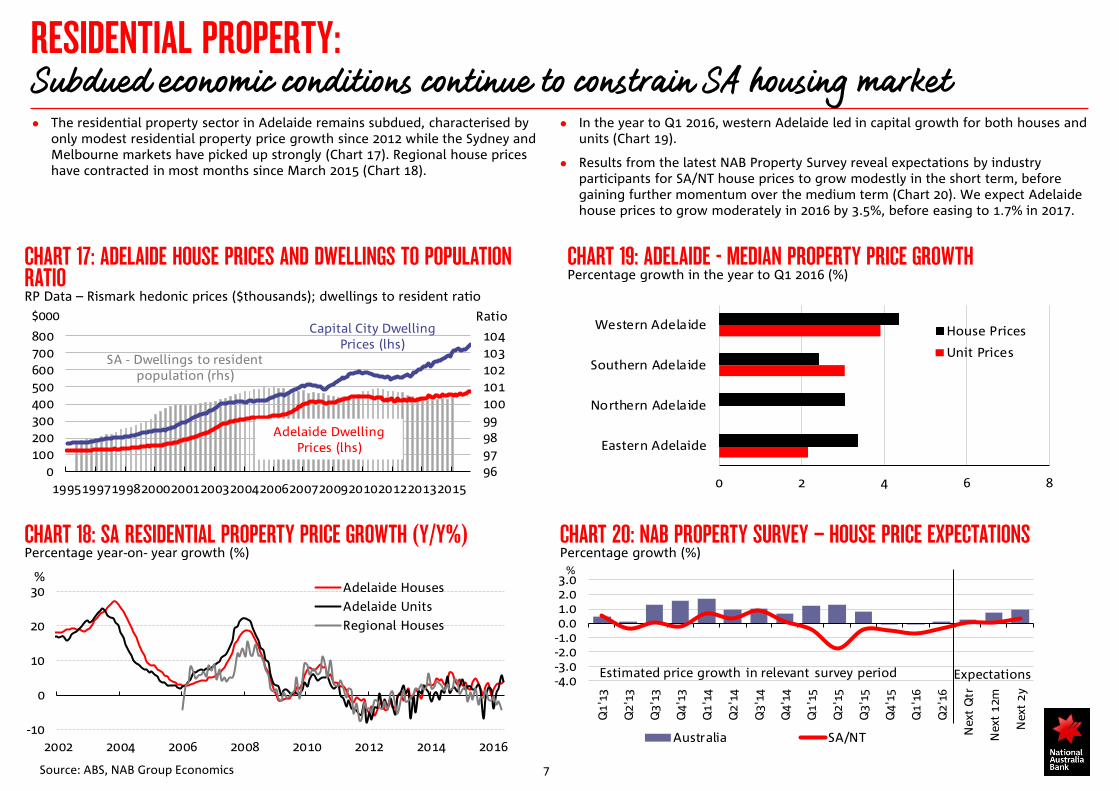

In the year to Q1 2016, western Adelaide led in capital growth for both houses and units (Chart 19).

Results from the latest NAB Property Survey reveal expectations by industry participants for SA/NT house prices to grow modestly in the short term, before gaining further momentum over the medium term (Chart 20). We expect Adelaide house prices to grow moderately in 2016 by 3.5%, before easing to 1.7% in 2017.

7 Source: ABS, NAB Group Economics

The residential property sector in Adelaide remains subdued, characterised by only modest residential property price growth since 2012 while the Sydney and Melbourne markets have picked up strongly (Chart 17). Regional house prices have contracted in most months since March 2015 (Chart 18).

CHART 17: ADELAIDE HOUSE PRICES AND DWELLINGS TO POPULATION RATIO RP Data – Rismark hedonic prices ($thousands); dwellings to resident ratio

CHART 18: SA RESIDENTIAL PROPERTY PRICE GROWTH (Y/Y%) Percentage year-on- year growth (%)

CHART 19: ADELAIDE - MEDIAN PROPERTY PRICE GROWTH Percentage growth in the year to Q1 2016 (%)

CHART 20: NAB PROPERTY SURVEY – HOUSE PRICE EXPECTATIONS Percentage growth (%)

-10

0

10

20

30

2002 2004 2006 2008 2010 2012 2014 2016

Adelaide HousesAdelaide UnitsRegional Houses

%

0 2 4 6 8

Eastern Adelaide

Northern Adelaide

Southern Adelaide

Western Adelaide House Prices

Unit Prices

96979899100101102103104

0100200300400500600700800

19951997199820002001200320042006200720092010201220132015

$000 Ratio

SA - Dwellings to resident population (rhs)

Adelaide Dwelling Prices (lhs)

Capital City Dwelling Prices (lhs)

-10

-5

0

5

10

15

20

25

2001 2003 2005 2007 2009 2011 2013 2015

'000s Natural increase Net overseas migrationNet interstate migration Total population growth

DEMOGRAPHICS: SA population growth continues to moderate as interstate migration accelerates

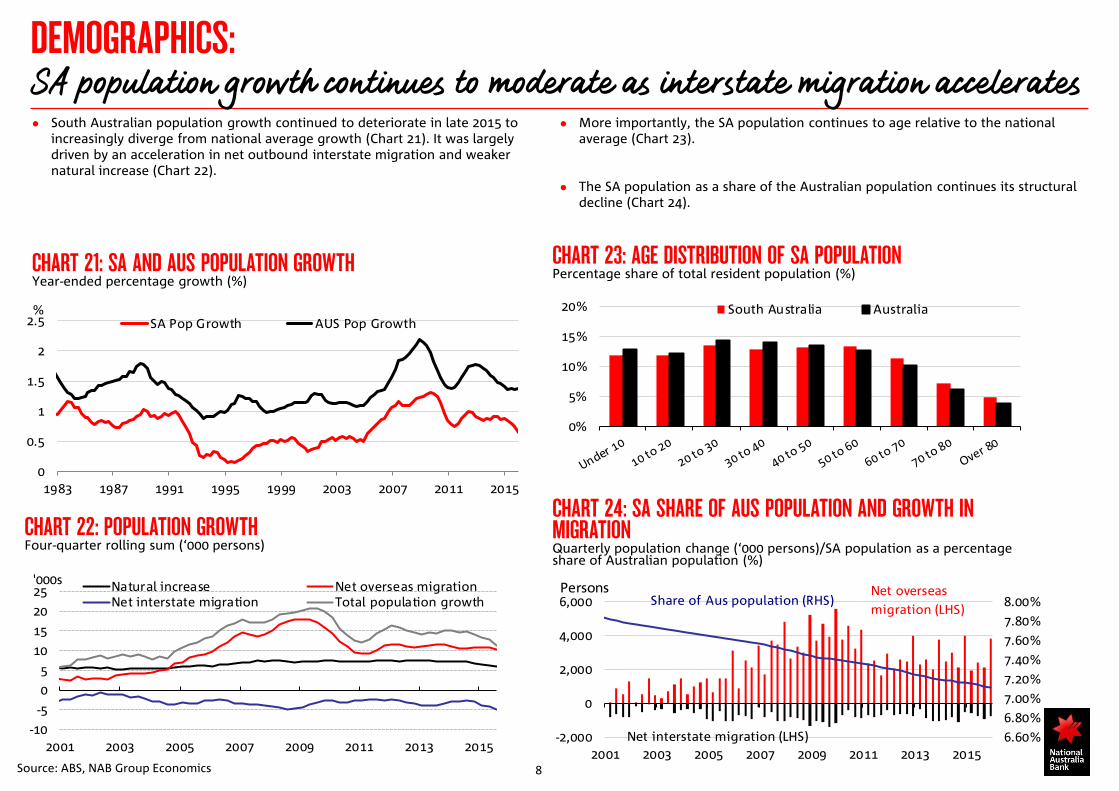

More importantly, the SA population continues to age relative to the national average (Chart 23).

The SA population as a share of the Australian population continues its structural decline (Chart 24).

8 Source: ABS, NAB Group Economics

South Australian population growth continued to deteriorate in late 2015 to increasingly diverge from national average growth (Chart 21). It was largely driven by an acceleration in net outbound interstate migration and weaker natural increase (Chart 22).

CHART 24: SA SHARE OF AUS POPULATION AND GROWTH IN MIGRATION Quarterly population change (‘000 persons)/SA population as a percentage share of Australian population (%)

CHART 22: POPULATION GROWTH Four-quarter rolling sum (‘000 persons)

CHART 21: SA AND AUS POPULATION GROWTH Year-ended percentage growth (%)

6.60%6.80%7.00%7.20%7.40%7.60%7.80%8.00%

-2,000

0

2,000

4,000

6,000

2001 2003 2005 2007 2009 2011 2013 2015

Net overseas migration (LHS)

Net interstate migration (LHS)

Share of Aus population (RHS)Persons

0%

5%

10%

15%

20% South Australia Australia

CHART 23: AGE DISTRIBUTION OF SA POPULATION Percentage share of total resident population (%)

0

0.5

1

1.5

2

2.5

1983 1987 1991 1995 1999 2003 2007 2011 2015

SA Pop Growth AUS Pop Growth%

LABOUR MARKET: SA unemployment rate eases, but structural job losses continue

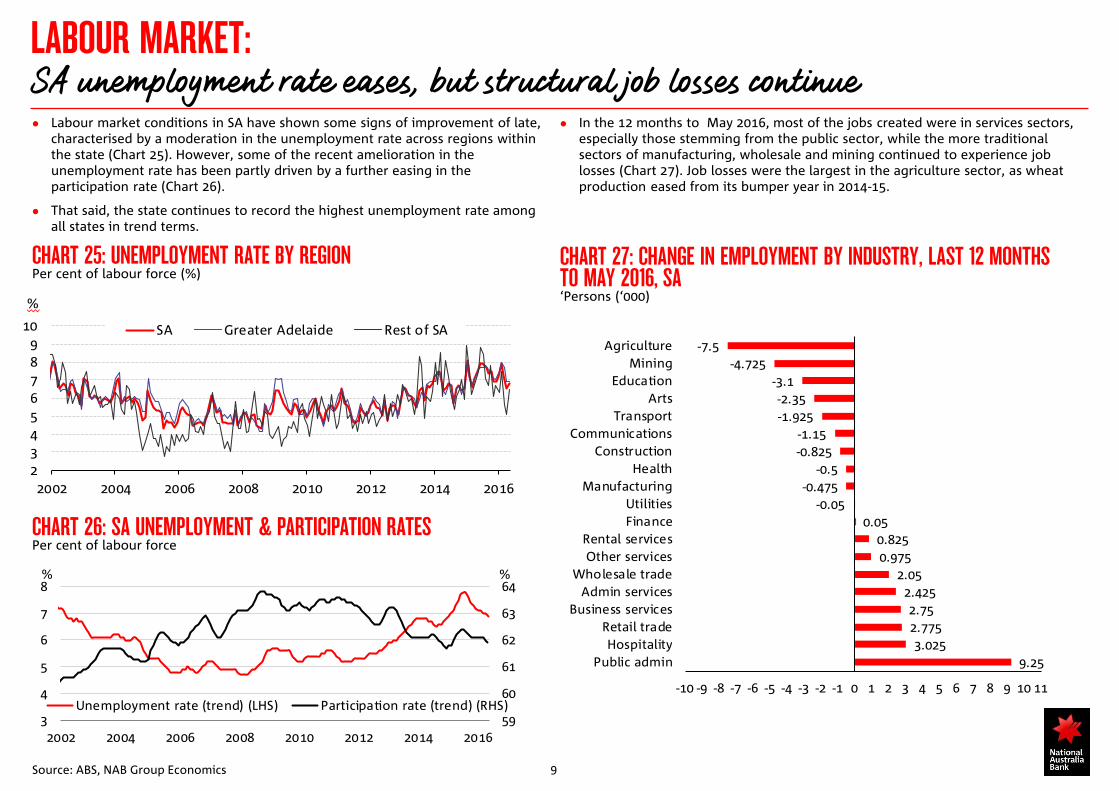

In the 12 months to May 2016, most of the jobs created were in services sectors, especially those stemming from the public sector, while the more traditional sectors of manufacturing, wholesale and mining continued to experience job losses (Chart 27). Job losses were the largest in the agriculture sector, as wheat production eased from its bumper year in 2014-15.

9 Source: ABS, NAB Group Economics

Labour market conditions in SA have shown some signs of improvement of late, characterised by a moderation in the unemployment rate across regions within the state (Chart 25). However, some of the recent amelioration in the unemployment rate has been partly driven by a further easing in the participation rate (Chart 26).

That said, the state continues to record the highest unemployment rate among all states in trend terms.

CHART 25: UNEMPLOYMENT RATE BY REGION Per cent of labour force (%)

CHART 27: CHANGE IN EMPLOYMENT BY INDUSTRY, LAST 12 MONTHS TO MAY 2016, SA ‘Persons (‘000)

CHART 26: SA UNEMPLOYMENT & PARTICIPATION RATES Per cent of labour force

23456789

10

2002 2004 2006 2008 2010 2012 2014 2016

SA Greater Adelaide Rest of SA

%

9.253.025

2.7752.75

2.4252.05

0.9750.825

0.05-0.05

-0.475-0.5

-0.825-1.15

-1.925-2.35

-3.1-4.725

-7.5

-10 -9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11

Public adminHospitality

Retail tradeBusiness services

Admin servicesWholesale trade

Other servicesRental services

FinanceUtilities

ManufacturingHealth

ConstructionCommunications

TransportArts

EducationMining

Agriculture

59

60

61

62

63

64

3

4

5

6

7

8

2002 2004 2006 2008 2010 2012 2014 2016

Unemployment rate (trend) (LHS) Participation rate (trend) (RHS)

% %

CHART 28 : COMPOSITION OF EMPLOYMENT & GVA IN 2014-15 Percentage share (%)

10 Source: ABS, NAB Economics

ECONOMIC STRUCTURE AND TRADE The health sector dominates in terms of output and employment

0% 2% 4% 6% 8% 10% 12% 14% 16%

HealthManufacturing

FinanceConstructionPublic admin

EducationTransport

AgricultureRetail trade

Business servicesWholesale trade

MiningUtilities

Admin servicesHospitality

Other servicesRental services

CommunicationsArts

GVA Employment

TABLES 29 & 30: TOP SA EXPORT DESTINATIONS AND IMPORT SOURCE COUNTRIES, 2014-15

Value of exports ($m)

1 China 2251

2 ASEAN 1970

3 US 1626

4 EU 1278

5 India 600

6 Japan 502

7 New Zealand 453

8 UK 406

9 Taiwan 295

10 Korea 264

11 HK 236

12 Singapore 154

13 Germany 122

Value of imports ($m)

1 China 1645

2 ASEAN 1632

3 EU 1407

4 US 765

5 Japan 629

6 Korea 463

7 Singapore 459

8 Germany 249

9 UK 203

10 New Zealand 190

11 Taiwan 115

12 HK 23

The top three sectors in SA by output share are health services, manufacturing and finance & insurance services. The former overtook manufacturing as the largest industry by gross value added in 2008-09 and the largest employer in 2006-07 (Chart 28).

By employment share, manufacturing (9%) is ranked third behind health & social services (15%) and retail trade (11%).

China and the ASEAN bloc are the main trading partners for SA (Chart 29 & 30).

SA’s top commodity exports in 2014-15 included wheat ($1.3bn), alcoholic beverages ($1.2bn) and copper ($1bn). Meanwhile, SA imports mainly refined petroleum ($1.1bn), passenger motor vehicles ($0.6bn) and vehicle parts and accessories (Charts 31 & 32).

Major exports, goods, 2014-15A$m

Wheat 1,300Alcoholic beverages 1,238Copper 951Copper ores & concentrates 927Meat (excl beef) 737

Major imports, goods, 2014-15A$m

Refined petroleum 1,115 Passenger motor vehicles 643 Vehicle parts & accessories 353 Goods vehicles 312 Alcoholic beverages 284

Million ($m)

TABLES 31 & 32: TOP SA MERCHANDISE EXPORTS AND IMPORTS

FISCAL OUTLOOK General government net debt forecast to be higher in most years

Relative to the Mid-Year Budget Review (MYBR), total taxation revenues have beenrevised down in all years, mainly due to lower-than-expected payroll tax,conveyance duty and gambling tax in the year to date. Meanwhile, GST grantshave been revised up for 2015-16 but revised down in all other years reflectingchanges to SA’s expected share of the GST pool, updated population estimatesand revised estimates of the national GST pool. GST is the single largest source ofrevenue for the state at 32% (Chart 34).

11

Compared to the Mid-Year Budget Review, the SA government has revised itsforecast for general government net debt higher for 2015-16 and all years in theforward estimates, except for 2016-17. This primarily reflects higher expectedcapital investment for the new Royal Adelaide Hospital across all years, with apartial offset from increased capital returns from the Motor Accident Commission(MAC), especially in 2016-17. Net debt is now expected to peak in 2017-18 at$6.6bn instead of $6.3bn at 2016–17.

CHART 33: SA NET OPERATING BALANCE CHART 34: SA COMPOSITION OF STATE REVENUEPercentage share (%)

22.533.544.555.566.57

2000

3000

4000

5000

6000

7000

2015-16 2016-17 2017-18 2018-19 2019-20

Net Debt Level (LHS) Net Debt as a Share of GSP (RHS) %$m

Taxation25%

GST32%

Other Grants

24%

Sales of Goods and

Services14%

Other5%

SEMI GOVERNMENT BONDS AND CREDIT RATINGS SA government credit rating metrics at risk of slight downgrade by S&P

SAFA funding program for FY17 is $5.5bn (vs $3.7bnbn in FY16). This comprises$0.1bn of new financing, $2bn of PN and ECP rollovers and $3.4bn of maturities.For liquidity reasons SAFA plans to refinance the Sep 17 bond line (2.4bnoutstanding) via issuing into existing 2025 and 2016 lines and potentially creating2022, 2024 and 2027 (Chart 38).

Source: SAFA and SA budget papers 12

On a total state level, net debt will rise to $13.8bn in FY 17 (from $10.9bn) whichis expected to be close to the peak for net debt over the forecast horizon. Therise in net debt in FY 17 largely reflects the financial obligations for the newRoyal Adelaide Hospital (Chart 35).

S&P is yet to confirm SA’s credit rating. Our estimates of the rating metrics showsome slippage from the MYBR but it is not material (Chart 37).

CHART 35: SA NON-FINANCIAL PUBLIC SECTOR NET DEBT CHART 37: S&P CREDIT METRIC: BUDGET PERFORMANCE METRICS

CHART 36: SA BORROWING PROGRAMME CHART 38: SAFA TERM BONDS OUTSTANDING AS AT END JUNE 2016

8

9

10

11

12

13

14

15

2015-16 2016-17 2017-18 2018-19 2019-20

$bnFY-17 BudgetFY16 MYBR

FY16

-1

0

1

2

3

4

5

6

7

FY 15 FY 16 e FY 17 (f) FY 18 (f) FY 19 (f) FY 20(f)

AUDbn

Refinancing

New financing

Borrowing programme

nb: forecasts for new financing estimated from budget

Pre funding/liquidty

0.0

0.5

1.0

1.5

2.0

2.5

3.0AUDbn

Issuance as at 30