state of the bangladesh economy - united...

TRANSCRIPT

State of the Bangladesh Economy Early Signals of FY2005

(First Reading)

A paper prepared under the programme Independent Review of Bangladesh’s Development (IRBD)

implemented by the Centre for Policy Dialogue (CPD)

January 15, 2005

B A N G L A D E S H CENTRE FOR POLICY DIALOGUE (CPD)

a c i v i l s o c i e t y t h i n k - t a n k House 40C, Road 11, Dhanmondi R/A, Dhaka-1209

Tel: 9141734, 9141703, 9145090; Fax: 8130951 E-mail: [email protected]; Website: www.cpd-bangladesh.org

CPD: IRBD FY05 (First Interim) ii

Credit

Dr. Debapriya Bhattacharya, Executive Director, Centre for Policy Dialogue (CPD) was in overall charge of preparing this report. Drafts on various sections were prepared by Professor Mustafizur Rahman, Research Director, CPD (External Sector and MFA Phase-out), Dr. Ananya Raihan, Research Fellow, CPD (Banking Sector and Exchange Rate), Dr. Uttam Kumar Deb, Research Fellow, CPD (Agriculture Situation; Food Security; and PRSP), Dr. Fahmida Khatun, Research Fellow, CPD (Assessment of Flood 2004), Dr. Khondaker Golam Moazzem, Research Fellow, CPD (Investment Scenario in the Private Sector), and Mr. M. Syeed Ahamed, Senior Research Associate, CPD (Macroeconomic Trends). Database development and analysis were carried out by Mr. Mabroor Mahmood, Senior Research Associate (Banking Sector), Mr. Noor Mohammad Wasi Uddin, Research Associate, CPD (Macroeconomic Trends), Mr. Wasel Bin Shadat, Research Associate, CPD (Flood Assessment), Mr. Kazi Mahmudur Rahman, Research Associate, CPD (Investment Scenario), Mr. Syed

Saifuddin Hossain, Research Associate, CPD (Flood Assessment), Mr. Md. Masum Billah, System Analyst, CPD (Agriculture Situation and Food Security), Mr. Asif Anwar, Programme Associate, CPD (Flood Assessment), Ms. Farhana Rahman, Programme Associate, CPD (Banking Sector and Exchange Rate), Mr. Narayan Chandra Das, Programme Associate, CPD (Agriculture Situation and Food Security), Mr. Shubhasish Barua, Programme Associate, CPD (Exchange Rate and Investment).

CPD: IRBD FY05 (First Interim) iii

Expert Group Meeting on

CPD-IRBD 2005 (Interim)

As part of the CPD-IRBD tradition, CPD organised an Expert Group Consultation Meetings on

January 12, 2005 at the CPD Dialogue Room. The First Interim Report on the State of the

Bangladesh Economy: Early Signals of FY2005 was shared at this in-house meeting with a

distinguished group of policymakers and professionals with direct exposure to macroeconomic

policy crafting in the country. Professor Rehman Sobhan, Chairman, CPD chaired the session.

CPD-IRBD Research Team acknowledges the participants for sharing their views and comments

on the draft report. However, CPD is solely responsible for the observations and analysis made in

this paper.

A list of the participants of the meeting is provided below in alphabetical order:

Dr Q K Ahmad President, Bangladesh Unnayan Parishad (BUP) Dr. Quazi Mesbahuddin Ahmed Member (GED), Planning Commission Professor Amirul Islam Chowdhury Former Vice Chancellor, Jahangirnagar University and Former Chairman, Sonali Bank Dr. Mirza Azizul Islam Chairman, Securities and Exchange Commission Mr. M. Hafizuddin Khan Former Finance Advisor to the Caretaker Government and

Chairman, Public Expenditure Review Commission Professor Wahiduddin Mahmud Former Finance Advisor to the Caretaker Government and Professor, Economics Department, University of Dhaka

Dr. A.K.M. Masihur Rahman Former Secretary, ERD, Ministry of Finance Mr. Mustafizur Rahman Former Chairman, Revenue Reform Commission and

Director, Far-East Finance and Investment Dr. Quazi Shahabuddin Director General, Bangladesh Institute of

Development Studies (BIDS)

Mr. M. Syeduzzaman Former Finance Minister and Chairman, Bank Asia

CPD: IRBD FY05 (First Interim) iv

Acronyms

ADB - Asian Development Bank

ADP - Annual Development Programme

BB - Bangladesh Bank

BBS - Bangladesh Bureau of Statistics

BOI - Board of Investment

BTTB - Bangladesh Telegraph and Telephone Board

CDBL - Central Depository Bangladesh Limited

CPI - Consumer Price Index

EPZ - Export Processing Zone

FCB - Foreign Commercial Bank

FDI - Foreign Direct Investment

FFW - Food for Work

Forex - Foreign Exchange

GDP - Gross Domestic Product

GNI - Gross National Income

GOB - Government of Bangladesh

GSP - Generalized System of Preferences

HYV - High Yielding Variety

ICMA - Institute of Cost and Management Accountants

IMF - International Monetary Fund

IPO - Initial Public Offering

IPRSP - Interim Poverty Reduction Strategy Paper

LC - Letter of Credit

MFA - Multi Fibre arrangement

MGD - Millennium Development Goal

MOFDM- Ministry of Food and Disaster Management

MTMF - Medium Term Macroeconomic Framework

NCB - Nationalized Commercial Bank

CPD: IRBD FY05 (First Interim) v

NER - Nominal Exchange Rate

NGO - Government of Bangladesh

NSD - National Savings Deposit

OMS - Open Market Sale

PCB - Private Commercial Bank

PRSP - Poverty Reduction Strategy Paper

REER - Real Effective Exchange Rate RTA - Regional Trading Agreement

SEC - Securities and Exchange Commission

SME - Small and Medium Enterprise

VAT - Value Added Tax

VGD - Vulnerable Group Development

VGF - Vulnerable Group Feeding

CPD: IRBD FY05 (First Interim) vi

Table of Content

I. INTRODUCTION 1

PART A II. GROWTH, SAVINGS AND INVESTMENT 3

2.1 Economic Growth Trend Decelerates? 3 2.2 Sources of Growth – Service Sector Dominated 5 2.3 Per-capita Income 6 2.4 Inadequate Savings-Investment to Accelerate Growth 7

III. STATE OF THE FISCAL SECTOR 12

3.1 Revenue Receipts 12 3.2 Public Expenditure 15

IV. STATE OF THE MONETARY SECTOR 19

4.1 Domestic Credit Expansion 19 4.2 Government Borrowing and Public Debt 21 4.3 Agricultural Credit 23 4.4 Industrial Credit 24 4.5 Price and Wage Inflation 26

V. STATE OF THE REAL SECTOR 32

5.1 Agricultural Production 32 5.2 Industrial Production 34 5.3 Foreign Investment 36 5.4 Capital Market 39

VI. STATE OF THE EXTERNAL SECTOR 43 6.1 Export Likely to Survive the Phasing out of MFA 43 6.2 Import Sees Robust Growth Especially in Investment Items 48 6.3 Opening and Settlement of Import LCs 50 6.4 Balance of Payments Regimented 53 6.5 Flow of Remittance Continuing Escalation 55 6.6 Forex Reserves Continues to Swell 57 6.7 Foreign Aid Failed to Supplement Growth Instruments 59

CPD: IRBD FY05 (First Interim) vii

PART B VII. ASSESSMENT OF FLOOD 2004 63

7.1 Background 63 7.2 Damage Assessment 64 7.3 Relief and Rehabilitation 66 7.4 CPD’s Recommendations and GOB Initiatives 67

VIII. MFA PHASE-OUT: EARLY INDICATIONS AND CHALLENGES AHEAD IN FY2005 73

8.1 So Far So Good! 73 8.2 Post-MFA Scenario Will be Different 75

8.3 Designing an Appropriate Strategy 77

IX. INVESTMENT SCENARIO IN THE PRIVATE SECTOR 80 9.1.1 Major Advances to a Limited Number of Large and

Medium Industries 80 9.1.2 Sluggish Trend of Investment in Capital Market 83

9.2 Slow Rise of Industrial Consumption of Energy 84 9.3 More Promises of FDIs 85 9.4 Investment in the Interim Period—Concentration in a Limited Number of Large and Medium Industries 86

X. NCBs REFORM: WHERE DOES IT STANDS 88 10.1 Reform Agenda 88 10.2 Reform Process 91 10.3 Consequences 95

XI. PRICES OF ESSENTIAL COMMODITIES, INCREASE IN DIESEL PRICE AND FOOD SECURITY 102 11.1 Price Surge of Essential Commodities 102 11.2 Trends in Import of Foodgrains 106 11.3 Monga in Northern Districts 108 11.4 Increase in Diesel Price 111 11.5 Implications for Food Security 112

XII. INFLUENCE OF EXCHANGE RATE MOVEMENTS ON EXPORT

PERFORMANCE OF BANGLADESH 113 12.1 Exchange Rate Behaviour: Is there Any Significant Change Since Floating Mechanism? 113 12.2 Export Performance of Bangladesh: Does Exchange Rate Matter? 116 XIII. PRSP AND IPRSP: A COMPARISON OF MEDIUM TERM

MACROECONOMIC FRAMEWORK 119 13.1 Targets for Economic Growth and Money Supply 119 13.2 Government Revenue and Public Expenditure 121 13.3 Balance of Payments 122 13.4 Conclusion 124

XIV. CONCLUDING BALANCE SHEET 124

CPD: IRBD FY05 (First Interim) viii

LIST OF TABLES

Table 1: Savings/Investment Scenario FY04-FY05

Table 2: Comparison of Inflation in India, Pakistan and Bangladesh

Table 3: Summary of CPD’s Damage Estimates

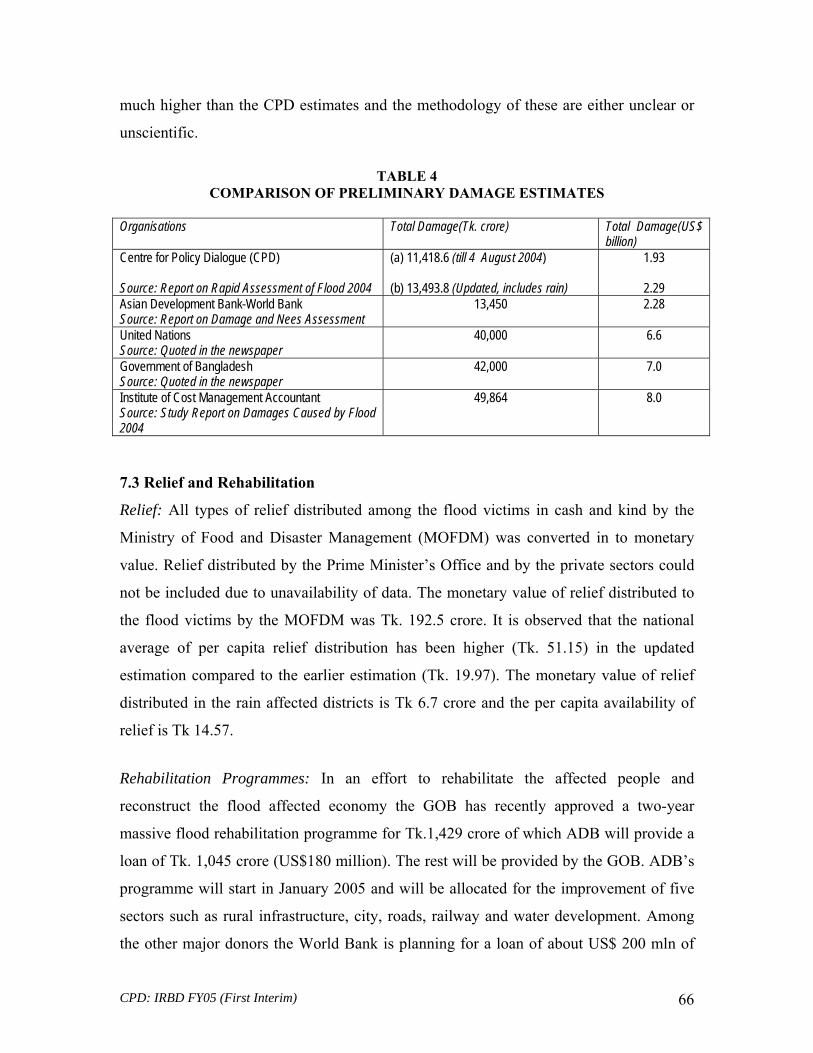

Table 4: Comparison of Preliminary Damage Estimates

Table 5: Comparison of CPD’s Recommendations and GOB Implementation

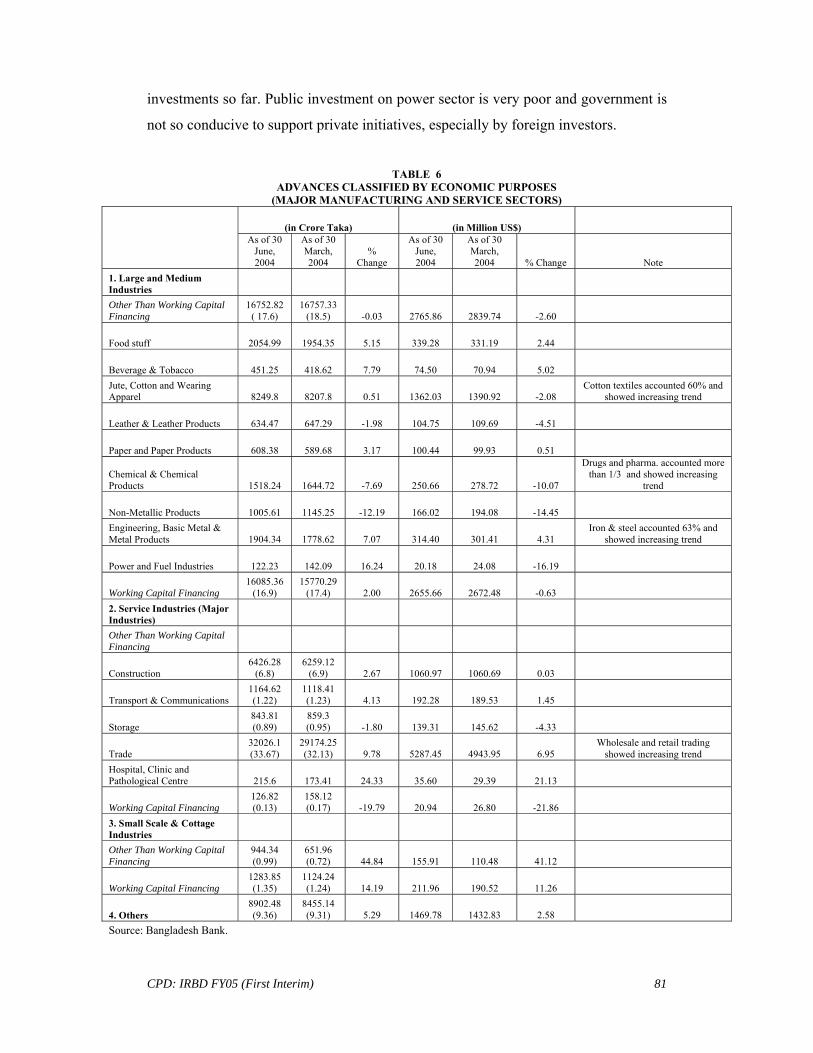

Table 6: Advances Classified by Economic Purposes (Major Manufacturing and Service Sectors)

Table 7: Capital Machinery and Industrial Raw Materials Imported for Manufacturing and Service Industries

Table 8: Initial Public Offering (IPO) for July-November, FY2004 and FY2005

Table 9: Industrial Consumption of GAS and Electricity

Table 10: Prospective FDIs in Bangladesh by Selected Countries

Table 11: State-Owned Bank Assets as a Percentage of Total Bank Assets

Table 12: Scenario of Manpower Restructuring, Data as of June, 2004

Table 13: Import of Rice (Aid/Commercial/Private) in Bangladesh, 2001/02-2004/05

Table 14: Targets for Economic Growth in IPRSP and PRSP

Table 15: Targets for Money Supply (Percent Change in Money and Credit) in IPRSP and PRSP

Table 16: Targets for Government Revenue and Public Expenditure as Percent of GDP in IPRSP and PRSP

Table 17: Targets for Balance of Payments in IPRSP and PRSP

Annex Table 1: State-Ownership vs. Banking Performance in Selected Countries

Annex Table 2: Comparatives Picture of Commercial Banks’ Performance

LIST OF FIGURES

Figure 1: Trend in GDP Growths

Figure 2: Periodic Linear Growth Rates of GDP

Figure 3: GDP Growth of Selected South Asian Countries

Figure 4: Incremental Growth of Sectors ofGDP: FY91-04

Figure 5: Savings as Percent of GDP during FY91-FY04

Figure 6: Investment as Percent of GDP during FY91-FY04

CPD: IRBD FY05 (First Interim) ix

Figure 7: Savings-Investment Gap as Percent of GDP

Figure 8: Revenue-GDP Ratio in Bangladesh

Figure 9: Revenue-GDp Ratio in Bangladesh (Linear and Average)

Figure 10: Revenue Earnings During FY91-FY05

Figure 11: VAT vs Income Tax During FY91-FY05

Figure 12: Taka Release and Expenditure of ADP During the 1st Quarter of FY02-FY05

Figure 13: Target ADP and Actual Implementation During FY02-FY05 (1st Quarter)

Figure 14: Performance of Major Ministries (in terms of ADP Allocation)

Figure 15: Domestic Credit Expansion During July-October FY01 to FY05

Figure 16: Growths in Domestic Credit During July-October FY01 to FY05

Figure 17: Private Sector Share in Domestic Credit During Jul-Oct FY01 to FY05

Figure 18: Growth of Net Government Borrowing During July-October FY05 (point-to-point)

Figure 19: Sale and Repayment of NSD Certificate

Figure 20: Growths in Agricultural Credit Expansion During July-October FY05

Figure 21: Term Loan for the FY04 and FY05

Figure 22: Working Capital for the FY04 and FY05

Figure 23: Inflation (moving Average)

Figure 24: Food Inflation (Point to Point)

Figure 25: Wage Inflation (Point to Point)

Figure 26: Comparison among India, Pakistan and Bangladesh

Figure 27: Inflation During the Flood Year 1998

Figure 28: Growths of Major Industries During July to October of FY04 and FY05

Figure 29: Quantum Index of Production during FY03-05 (1988-89=100)

Figure 30: Foreign Investment During FY00-FY04

Figure 31: Foreign Investment During July-September of FY04-05

Figure 32: FDI Flow: Survey and Banking Data

Figure 33: Sectoral Composition of Registered FDI in FY04

Figure 34: Entry of IPOs in the Capital Market (Monthly Statistics)

Figure 35: Structure of Exports during July-October FY04-05

CPD: IRBD FY05 (First Interim) x

Figure 36: Sectoral Growth of Exports during July-October FY05

Figure 37: Monthly Dynamics of Export Earnings During FY01-05 (Jul-Oct)

Figure 38: Decomposition of Export Growth for July-October FY05

Figure 39: Export and Import during FY91-FY04

Figure 40: Imports and Sectoral Growth during the First Quarter of FY01-05

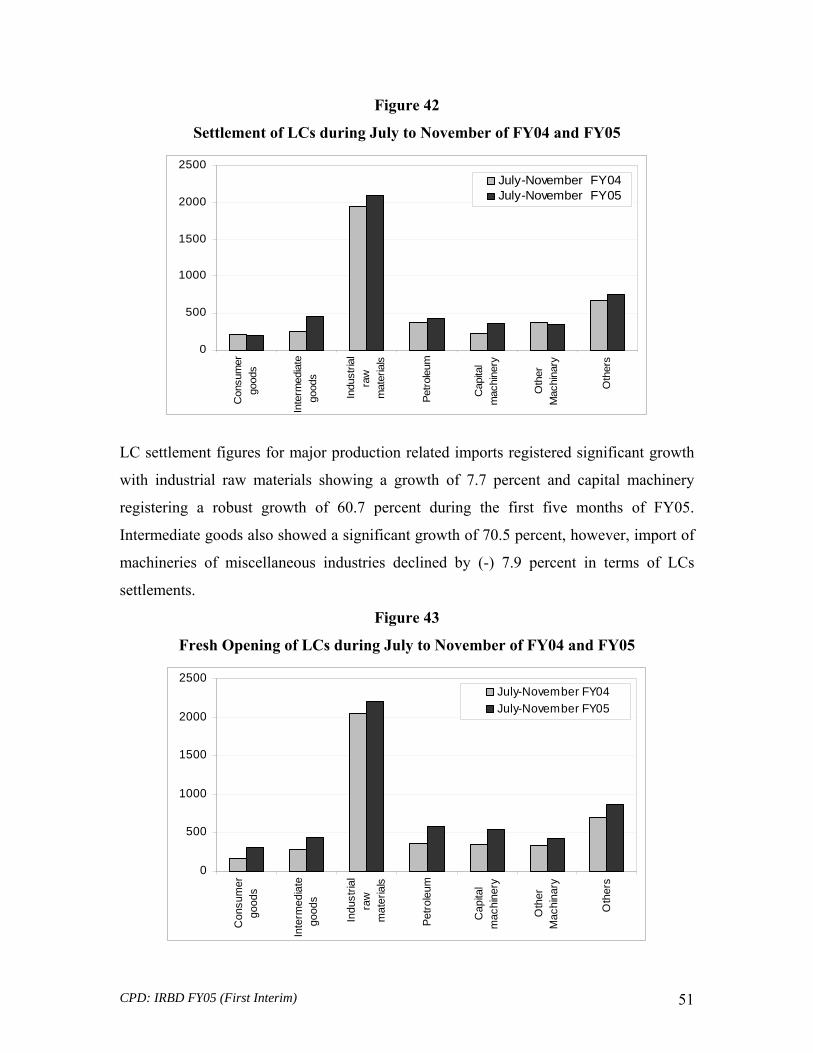

Figure 41: Sectoral Growth of Imports during the First Quarter of FY05 Figure 42: Settlement of LCs during July to November of FY04 and FY05

Figure 43: Fresh Opening of LCs during July to November of FY04 and FY05

Figure 44: Growth Rates of Opening and Settlement of LCs FY05 over FY04 (July to November)

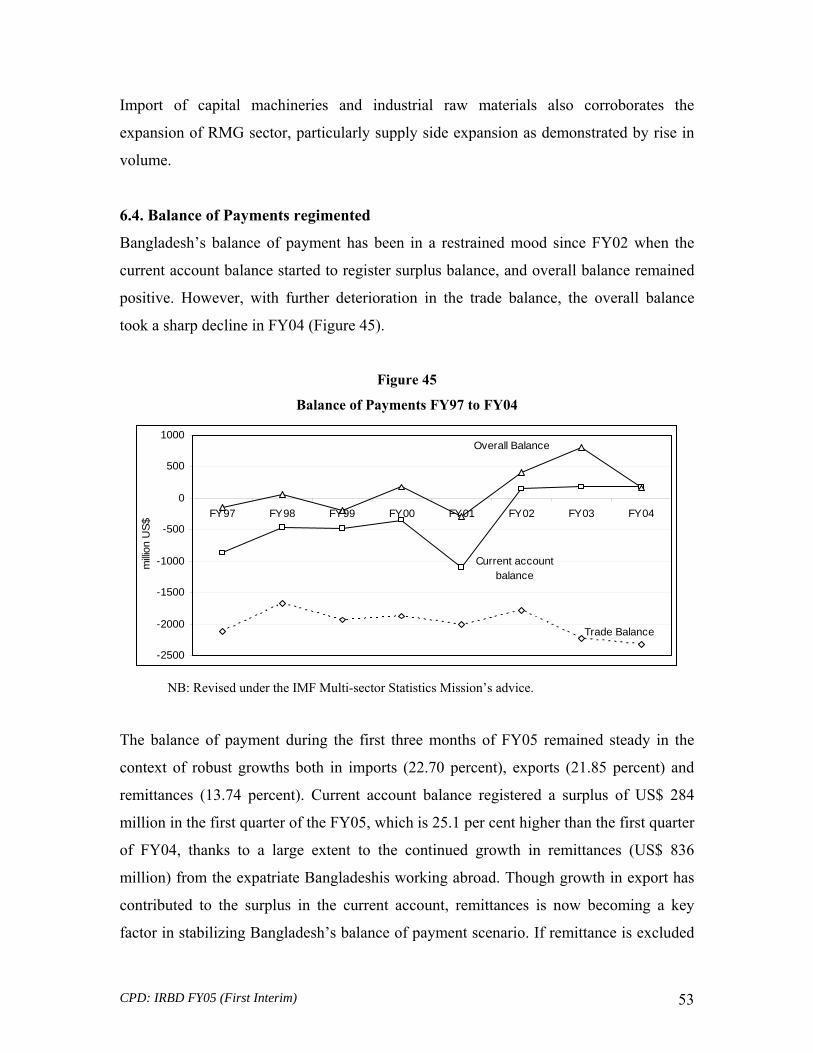

Figure 45: Balance of Payments FY97 to FY04

Figure 46: Balance of Payment Scenario During Jul-Sep in FY04-05

Figure 47: Flow of Remittances During Jul-Dec in FY01-FY05

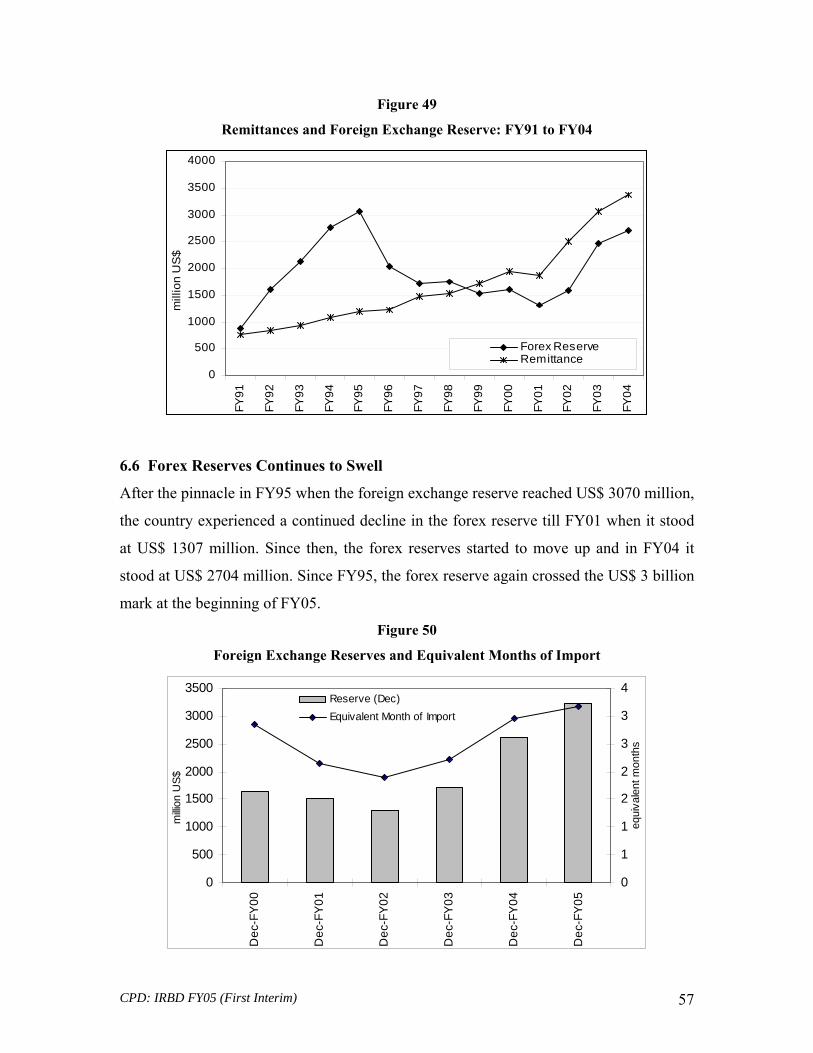

Figure 48: Monthly Trend in the Flow of Remittances During FY04-FY05 Figure 49: Remittances and Foreign Exchanges Reserve: FY91 to FY04

Figure 50: Foreign Exchange Reserves and Equivalent Months of Import

Figure 51: Decomposition of Sources of Import Financing

Figure 52: Flow of Foreign Aid in Bangladesh During FY90-04

Figure 53: Flow of Foreign Aid During July to October of FY04-05

Figure 54: Declining Foreign Aid in the Context of Stagnated Domestic Savings

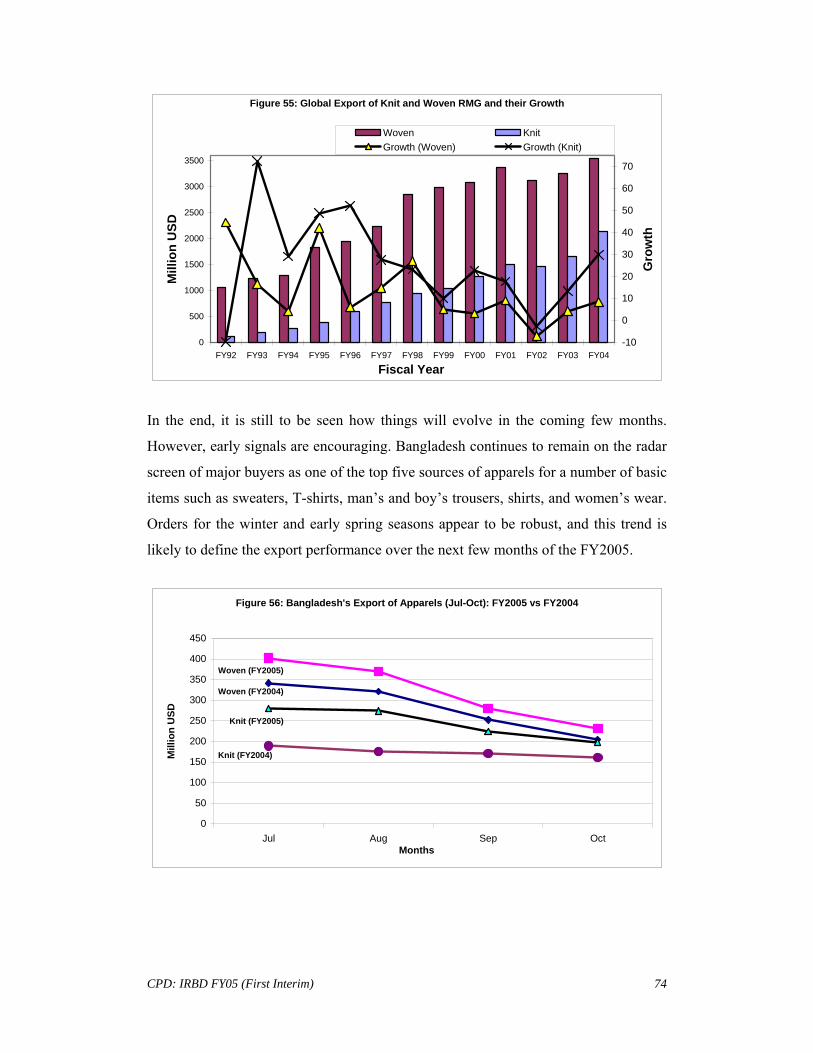

Figure 55: Global Export of Knit and Woven RMG and their Growth

Figure 56: Bangladesh’s Export of Apparels (Jul-Oct): FY05 vs FY04

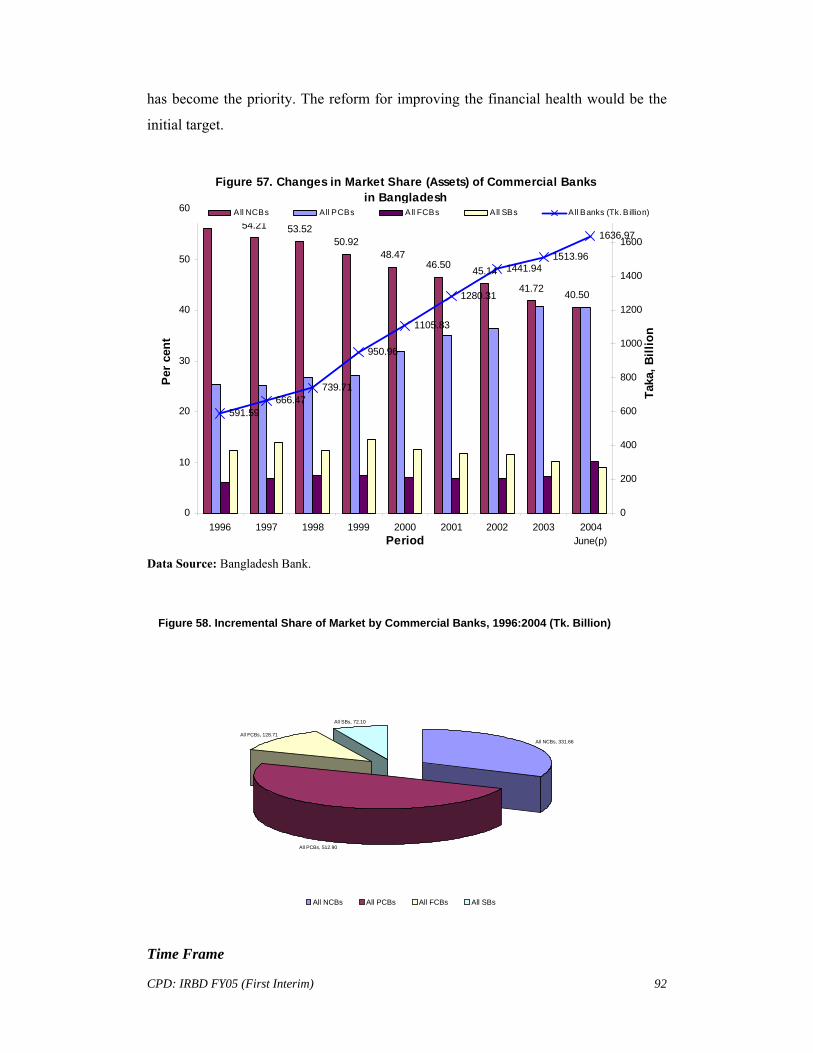

Figure 57: Changes in Market Share (Assets) of Commercial Banks in Bangladesh

Figure 58: Incremental Share of Market by Commercial Banks, 1996:2004

Figure 59: Comparative Geographical Distribution of Branches of Commercial Banks

Figure 60: Average Wholesale Price of Coarse Rice in Bangladesh: FY01-FY05

Figure 61: Comparison of Domestic Prices of Rice with Import Partly Price: FY00-FY05

Figure 62: Rice Prices and Quantity of Private Rice Imports in Bangladesh, 1999-2004 Figure 63: Distribution of Foodgrains through FFW and VGD: 1998/89-2004/05

Figure 64: Depreciation of Some Selected Currencies, Base Period June 2000

CPD: IRBD FY05 (First Interim) xi

Figure 65: Comparative Movement of Euro-USD Cross Rate in Bangladesh and Global Euro-USD Rates, Monthly Average

Figure 66: Movement of EURO-USD Global Exchange Rate and EURO-USD Cross Rate, November 2004 – January 10, 2005

Figure 67: Depreciation of Some Selected Currencies, Base Period June 2000 LIST OF BOXES Box 1: An Enquiry in Factors Influencing Inflation

Box 2: A Balance Sheet of Bangladesh Economy Box 3: Major Findings of the Thematic Issues

I. INTRODUCTION

The first reading of the Independent Review of Bangladesh’s Economy for 2004-05

(FY05) essentially covers the first six months (July-December 2004) of the fiscal year.

The review, drawing on official data, has been presented in two analytical components.

The first component (Part A) provides a macro-economic overview focussing on the

following four major areas.

(i) Growth, Saving and Investment (ii) Monetary Sector (iii) Real Economy (iv) External Sector

Recognising the relative stability prevailing in the macro-economic situation, the review

highlights some sources of its fragility. It raises the question whether the macro-

economic stability of Bangladesh has been rewarded with adequate growth payoff. The

review underscores the negative implications of the creeping rise in consumer price index

in the backdrop of perceptible credit expansion in both manufacturing and agricultural

sector. In the real economy, shortfall in foodgrain production remains the major concern,

while capital market has been attracting increased liquidity. The external sector balance is

experiencing consolidation, notwithstanding the total phase-out of the apparel quota.

The second component (Part B) of the review addresses a select set of issues which

would underpin the final outcomes of FY04. These issues are the following:

(i) Consequences of Flood 2004

(ii) Impact of MFA Phase-out

(iii) Trends in Industrial Investment

(iv) NCB Reforms

(v) Exchange Rate Movement

(vi) Price Rise of Essentials

(vii) Finalisation of PRSP

CPD: IRBD FY05 (First Interim) 1

CPD: IRBD FY05 (First Interim) 2

PART A

CPD: IRBD FY05 (First Interim) 3

II. GROWTH, SAVINGS AND INVESTMENT

2.1 Economic Growth Momentum Decelerates?

Following a decline of the GDP growth rate to 4.2 percent in FY02, the national economy

repositioned itself in a five percent plus growth trajectory during the subsequent two

years (FY03 and FY04). The economy posted a growth of 5.5 percent in FY04 in line

with the I-PRSP target; however such marginal improvement in economic growth rate

compares unfavourably with the record figure of 5.9 percent achieved in FY00.

The recently finalised national PRSP provides a set of growth targets which has revised

downward the figure for FY05 from 6.0 percent to 5.5 percent. PRSP has fixed the GDP

growth targets at 6.0 percent and 6.5 percent for FY06 and FY07 respectively.

Figure 1

Trend in GDP Growths

Source: Computed from Finance Division (2004c) and ERD (2003) Note: * PRSP Targets.

It is known that the Bangladesh economy has been experiencing five percent plus growth

rate during the past few years. However, when compared with the trend growth rates of

1990s, one can notice a deceleration of national growth rates. The GDP grew at faster

rate during the 1990s (4.6 percent linear growth) in comparison to 1980s (3.6 percent

linear growth). Within 1990s, the growth momentum was even higher during the second

half of the decade in comparison to the first half. The linear growth rate of GDP during

CPD: IRBD FY05 (First Interim) 4

the period of FY91-95 was 3.95 percent, while during the next five year (FY96-00) it

grew at even a faster rate of 4.79 percent. However, taking into account the PRSP target

growth of FY05 (5.5 percent), the economy during the FY01-05 is programmed at a

linear growth rate of 4.88 percent, indicating a stagnation in its second derivative.

Figure 2 Periodic Linear Growth Rates of GDP

0

1

2

3

4

5

6

FY81-85 FY86-90 FY91-95 FY96-00 FY01-05*

perc

ent

Note: * GDP growth for FY05 is based on PRSP Target.

Figure 3 GDP Growth Rate of Selected South Asian Countries

1.8

6.5

4.4

5.8

4.0

8.1

-1.4

7

5.3

4.4

5.5 5.56.4 6.5

6.5

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

FY01 FY02 FY03 FY04 FY05

GD

P gr

owth

(per

cent

)

Pakistan

Sri Lanka

Bangladesh

India

CPD: IRBD FY05 (First Interim) 5

At the same time, when compared with the major countries in the South Asia region, the

growth scenario looks moderate for Bangladesh. The GDP growth rates of India (8.1

percent), Pakistan (6.4 percent) and Sri Lanka (6.5 percent) have been higher in FY04

than that of Bangladesh (5.5 percent). The GDP growth target for FY05 also appears to

be restrained when compared with other South Asian countries as India, Pakistan and Sri

Lanka have targeted growth targets for FY05 at 6.5 percent, 6.5 percent and 7 percent

respectively. During the first quarter of FY05, India has already achieved a 7.4 percent

growth.

2.2 Sources of Growth – Service Sector Dominated

The contribution of the real economic sectors to incremental growth has declined to 32.97

percent in FY04 from 34.40 percent in FY03. The annual growth of the real economic

sector stagnated at 4.60 percent during the last two fiscal years (FY03-04). This is largely

because of decline in the incremental growth of agriculture sector, which went from

13.30 percent in FY03 to 11.00 percent in FY04. The incremental growth of the service

sector has increased to 51.02 percent in FY04 from 49.87 percent in FY03 (see figure 4).

Figure 4

Incremental Growth of Sectors of GDP: FY91-04

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

Agriculture Industry Service

Source: Computed from CPD (2004)

CPD: IRBD FY05 (First Interim) 6

The on-going structural transformation of the Bangladesh economy is characterised by

falling share of the agriculture sector with marginal increase of the manufacturing in the

backdrop of increasing contribution of the service sector. The share of service sector has

increased to 61.27 percent in FY04 from 60.95 percent in FY03. The real economic

sector accounted for 39.00 percent of the GDP in FY03, which has decreased to 38.70

percent in FY04. A decade back, the said proportion was 42.00 percent. This suggests

that in spite of improved growth, the evolution of the Bangladesh economy remains

biased against modern, industrial transformation, having concomitant implications for

sustained growth and equitable income distribution.

2.3 Per-capita Income

The per capita GDP and GNI scenario are gradually improving after a decline in FY02. In

FY03 the per capita GDP and GNI was recorded to be US$389 and US$411 respectively.

In FY04 the corresponding figures are US$421 and US$444 respectively. The annual

growth is of 8.23 percent for per capita GDP and 8.03 percent for per capita GNI in terms

of US dollars. Once we adjust these figures by the extent of devaluation of US Dollar, the

per capita GDP growth comes down to 5.3 percent.

It is well known that poverty trends are influenced by the changes in inequality. Income

inequality at the national level has increased from 25.9 percent in 1991-92 to 30.6 percent

in 2000. During the same period, urban inequality was rising at a higher pace- from 30.7

percent in 1991-92 to 36.8 percent in 2000, than rural inequality- from 24.3 percent in

1991-92 to 27.1 percent in 2000 (BBS, 2003).

Between 1995-96 and 2000, national income attributable to the poorest 10 percent of the

population declined further from the miniscule proportion of 2.24 percent to 1.84 percent.

Conversely, the control on the national income by the richest 10 percent of the population

increased from 34.68 percent to 40.72 percent (ibid). In other words, the income

differential between the poorest and the richest increased from 35.7 times to 53.4 times

during the second half of 1990s. The sources of rising inequality are linked with the

uneven spread of economic and social opportunities, unequal distribution of assets

CPD: IRBD FY05 (First Interim) 7

especially in respect of human capital and financial capital, growing disparity between

urban and rural areas as well as between developed and underdeveloped areas.

The IRBD2003 opined that the incremental growth does not automatically benefit the

poor in Bangladesh (Bhattacharya, 2004). In this context and also in connection with the

completion of the initial year of the I-PRSP, we have not been provided with any

assessment on the poverty situation. There is no evidence which suggests that this trend

has been reversed during the last couple of years. Absence of such an assessment also

fails us to benchmark our programmes regarding MDGs.

2.4 Inadequate Savings-Investment to Accelerate Growth

The deceleration of Bangladesh’s national growth can be substantiated by the stagnated

savings-investment scenario. Recent growth models1 predicts that higher savings and the

related increase in capital accumulation can result in a permanent increase in growth rates

as savings determine the national capacity to invest and thus to produce, which in turn

affect the economic growth potential. On the contrary, low saving rates have been cited

as one of the most serious constraints to sustainable economic growth.

In this context, Bangladesh’s savings-investment scenario is showing a rather stagnant

trend during last few years. Domestic savings has increased marginally to 18.27 percent

of the GDP in FY04 from 18.21 percent in FY03. The share of national savings to GDP

has also showed signs of stagnation in FY04 at 24.49 percent of GDP against 24.45

percent in FY03. Though the national savings rate projected in the I-PRSP document for

FY04 (23.3 percent) was achieved (thanks to our NRBs for their remittances), the

projected domestic savings rate for FY04 (19.0 percent) was not achieved (see table 1).

1 Notion supported by the empirical works of Romer (1986), Lucas (1988), Barro (1991), De Long and Summers (1991).

CPD: IRBD FY05 (First Interim) 8

TABLE 1

SAVINGS/INVESTMENT SCENARIO FY04-FY05

FY04 IPRSP Actual

Deviation from IPRSP

I-PRSP FY05

Gross Domestic Savings 19.20 18.27 - 0.93 20.00 Gross National Savings 24.30 24.49 + 0.19 25.20 Gross Investment 25.40 23.58 - 1.82 27.00

(24.20 in PRSP)

Private 18.70 17.47 - 1.23 19.90 Public 6.70 6.12 -0.58 7.10

Source: Computed from Finance Division (2004c) and ERD (2003)

On the other hand, during the last five years (FY00-FY04), the gross investment ratio has

increased by only 0.50 percent of the GDP. For example, the ratio was 23.02 percent in

FY00; whilst it crawled only up to 23.58 percent in FY04. Increasing investment

continues to remain one of the core challenges of Bangladesh’s macro-economy. In

FY04, the country recorded the lowest public investment ratio of the last 14 years, 6.12

percent. The sectors left behind by public investment were not adequately picked up by

private investment. Private investment as a share of GDP increased marginally from

17.21 percent in FY03 to 17.47 percent in FY04. In this context, the new PRSP has

stepped back from forecasting any savings target for the next fiscal year. The only target

available is for gross investment which is set at 24.20 percent of GDP. This is far below

the target of IPRSP which was set at 27.0 percent and does not hold the aim to overcome

the existing investment stagnation soon.

CPD: IRBD FY05 (First Interim) 9

0

5

10

15

20

25

30

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

*

FY06

*

as p

erce

nt o

f GDP

Gross National Savings

Gross Domestic Savings

0

5

10

15

20

25

30

35

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

*

FY06

*

FY07

*

as p

erce

nt o

f GDP

Public Investment

Private Investment

Gross Investment

Figure 5

Savings as percent of GDP during FY 91-FY04

Note: * Targets for FY05 and FY06 are based on I-PRSP

Figure 6 Investment as percent of GDP during FY 91-FY04

Note: * Gross Investment target for FY05-FY07 is based on PRSP.

The breakdown of investment target (private and public) for FY05-FY06 is based on I-PRSP.

CPD: IRBD FY05 (First Interim) 10

Paradoxically, Bangladesh continues to remain an under-invested country, while its

national savings rate (24.49 percent) supposes its gross investment rate (23.58 percent).

After the late 1990s, when the savings and investment were almost equal, Bangladesh

experienced a net resource gap during FY01 (-0.77 percent) and FY02 (-0.72 percent).

Then the idle resource (i.e., excess savings as regard to investment as a ratio of GDP)

started climbing up.

Figure 7 Savings-Investment Gap as percent of GDP

-1

-0.5

0

0.5

1

1.5

2

2.5

3

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

The idle resource stood at 1.0 percent in FY03 and then with a marginal decline stood at

0.9 percent in FY04 as both investment and savings increased (or rather remained idle)

by the same factor. We are failing to convert all our savings into investment as we

continue to borrow from foreign sources.

Bangladesh needs to pay special attention to encourage savings and to create

opportunities for investment. In the context of low bank and NSD interest rates,

government needs to encourage savings by increasing variety of savings products, e.g.

promotion of other form of savings such as life insurance, provident funds, mutual funds,

investment in the stock market etc.

CPD: IRBD FY05 (First Interim) 11

At the same time, opportunities to invest this savings also needed to be broadened.

Savings is not an unconditional panacea for growth. Coherent and consistent long-term

policy to encourage investment in a stable socio-political and economic environment is a

prerequisite for this growth and development. The absorptive capacity, which is in many

ways constrained by the institutional bottlenecks and lack of profitable investment

opportunities, is also important for a transitional economy like Bangladesh. Otherwise

this excess liquidity of savings will end up with obvious consumption or even flight of

capital!2

In this context it can be mentioned that Bangladesh has experienced a major shift in her

consumption pattern during the last four fiscal years. While in the private sector the

consumption as percent of GDP has decreased from 77.5 percent in FY01 to 76.3 percent

in FY04, the propensity to consume has increased in the public sector, from 4.5 percent in

FY01 to 5.4 percent in FY04 (as percent of GDP).

2 CPD-GCR survey reveals that overseas investment by the entrepreneur of this investment-starved country is increasingly becoming a reality, while NRBs are not investing in Bangladesh as much as we want them to.

CPD: IRBD FY05 (First Interim) 12

0

2

4

6

8

10

12

14

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

*

FY06

*

FY07

*

Tax-

GDP

Rat

io (p

erce

nt)

III. STATE OF THE FISCAL SECTOR 3.1 Revenue Receipts Inefficient and inadequate revenue mobilisation has been a major weakness for

Bangladesh’s fiscal sector. The historically low revenue-GDP ratio of Bangladesh

experienced a marginal upsurge during the FY00-FY04, when the revenue-GDP ratio

increased from 9.0 percent in FY00 to 10.8 percent in FY04. The periodic average of

revenue-GDP ratio increased from 8.45 percent in FY91-95 to 10.20 percent in FY01-04

percent. According to the PRSP target the revenue-GDP ratio will decline to 10.7 percent

in FY05. The sluggish trend in revenue collection during the first four months of FY05

substantiates this decline in revenue-GDP ratio.

Figure 8

Revenue-GDP Ratio in Bangladesh

The PRSP has set a very defensive set of targets for revenue-GDP ratio for FY06 (11.2

percent) and FY07 (11.7 percent), which is still low when compared with other South

Asian countries. This low tax-to-GDP ratio indicates the inefficiency of Bangladesh’s tax

system in financing public services and redistributing income3.

3 Assuming that increases in a country's tax-to-GDP ratio often indicate a greater provision of tax-financed services and/or a greater redistributive role of the tax system.

CPD: IRBD FY05 (First Interim) 13

0

2

4

6

8

10

12

FY91-95 FY96-00 FY01-04 FY05-07*

Reve

nue-

GDP

ratio

(per

cent

)

Revenue-GDP Ratio (linear)

Revenue-GDP Ratio (period average)

Figure 9 Revenue-GDP Ratio in Bangladesh (Linear and Average)

Note: * Figures for FY05-07 are based on PRSP target

Latest available figure shows a modest revenue growth by the National Board of Revenue

(NBR) as it registered a 9.52 percent growth during the first four months of FY05 over

the corresponding figure of the previous fiscal year. During this period (July-October)

tax as percent of GDP has increased slightly, from 2.24 percent in FY04 to 2.26 percent

in FY05. During the July-October period of FY05, total import related revenue has

increased by about 6.46 percent while total internal trade related revenue registered a

robust 12.06 percent growth. Though import related supplementary duty showed a

marginal negative growth (-0.17 percent), supplementary duty at the local level registered

a moderate 10.43 percent growth during the period under reporting. Among others, VAT

(local), VAT (import) and income tax increased by about 13.94 percent, 12.52 percent

and 16.72 percent respectively. The encouraging point to be noted that during this July-

October period, the share of direct tax (income tax) has increased from 14.24 percent in

FY04 to 15.17 percent in FY05. However this share of direct tax is still appallingly low

and there is an urgent need for a shift in the composition of revenues away from tax on

goods and services towards direct taxes on income and profit. It is to be noted that the

NBR component covers more then three quarter of the total revenue income and the

CPD: IRBD FY05 (First Interim) 14

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

*

Reve

nue

Earn

ings

(cro

re T

k)

0

5

10

15

20

25

Ann

ual G

row

th (p

erce

nt)

Non-Tax RevenueTax RevenueAnnual Growth

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

*

perc

ent o

f GDP

VAT as percent of GDPTrend Line

overall growth observed in the revenue is mainly the contribution of this NBR part, while

other parts (non-NBR tax and non-tax) of revenue sources remains stagnant.

Figure 10

Revenue Earnings During FY91-FY05

Note: * Target for FY05

Figure 11 VAT vs Income Tax During FY91-FY05

Note: * Target for FY05

CPD: IRBD FY05 (First Interim) 15

In the context of a declining trend in public investment and stagnated savings-investment

scenario at the national level, the major challenge remains for Bangladesh’s fiscal policy

is to strengthen the effort to mobilise domestic resources to generate a larger share of

resources for investment. Reformation of the tax management and providing right

incentives to stimulate domestic savings is essential to achieve this goal.

3.2 Public Expenditure

Annual Development Programme

The size of the Annual Development Programme (ADP) for FY05 has been fixed at Tk

22000 crores, which is 15.78 percent higher than that the revised ADP of FY04 and about

30.31 higher than the actual implemented ADP of FY04. While only 83 percent of the

original size of the ADP i.e. 89 percent of the revised size was implemented during the

FY04, questions were raised regarding rationale of fixing such an ambitious target.

However, CPD in its post-budget reflection pointed out that this so-called ambitious ADP

target needs to be seen from the perspective that Bangladesh remains an under invested

economy and as such a large ADP target is worth chasing for. Thus, implementation of a

fuller ADP became the major challenge, than targeting a bigger ADP. The second aspect,

which needs to be underscored in this respect, is that the issue of quality is no less

important than the question of size of the ADP.

The ADP for FY05 took some steps decrease the number of projects, which has been

slashed down from 1163 in FY04 to 869 in FY05 including about 150 new projects.

CPD: IRBD FY05 (First Interim) 16

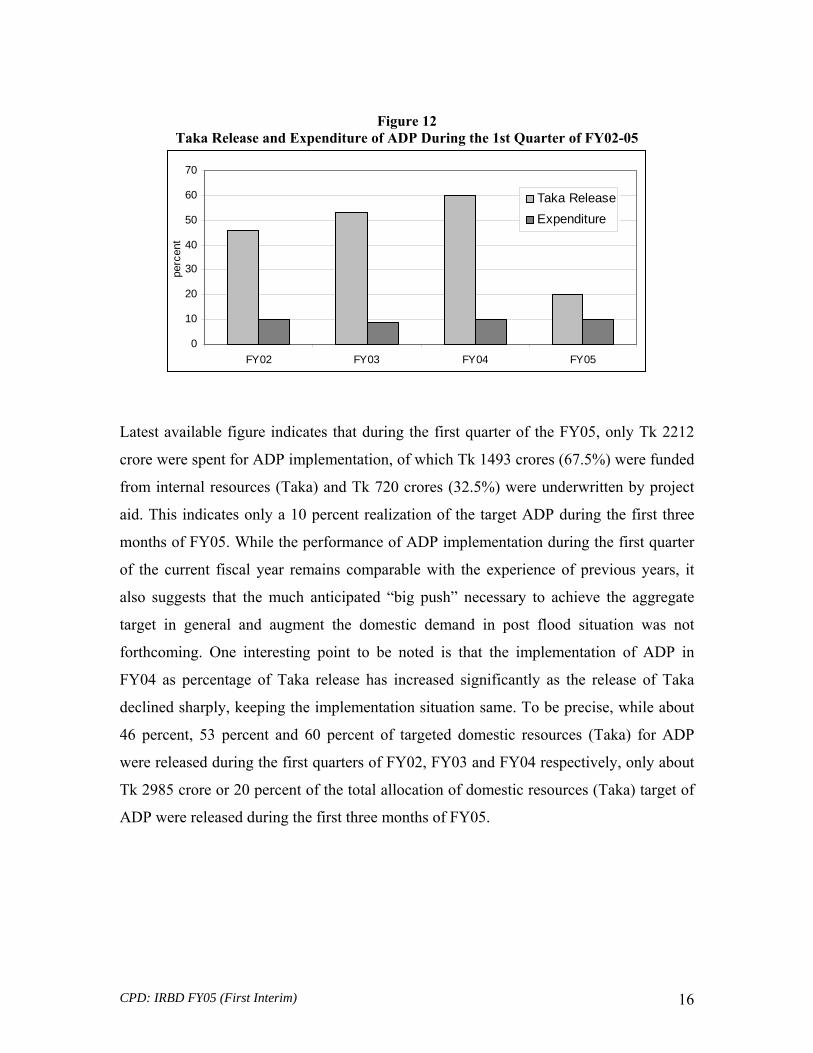

Figure 12

Taka Release and Expenditure of ADP During the 1st Quarter of FY02-05

0

10

20

30

40

50

60

70

FY02 FY03 FY04 FY05

perc

ent

Taka ReleaseExpenditure

Latest available figure indicates that during the first quarter of the FY05, only Tk 2212

crore were spent for ADP implementation, of which Tk 1493 crores (67.5%) were funded

from internal resources (Taka) and Tk 720 crores (32.5%) were underwritten by project

aid. This indicates only a 10 percent realization of the target ADP during the first three

months of FY05. While the performance of ADP implementation during the first quarter

of the current fiscal year remains comparable with the experience of previous years, it

also suggests that the much anticipated “big push” necessary to achieve the aggregate

target in general and augment the domestic demand in post flood situation was not

forthcoming. One interesting point to be noted is that the implementation of ADP in

FY04 as percentage of Taka release has increased significantly as the release of Taka

declined sharply, keeping the implementation situation same. To be precise, while about

46 percent, 53 percent and 60 percent of targeted domestic resources (Taka) for ADP

were released during the first quarters of FY02, FY03 and FY04 respectively, only about

Tk 2985 crore or 20 percent of the total allocation of domestic resources (Taka) target of

ADP were released during the first three months of FY05.

CPD: IRBD FY05 (First Interim) 17

0

2

4

6

8

10

12

14

16

18

20

Pow er Division Education LocalGovernment

Communication Health and FamilyWelfare

perc

ent

Figure 13

Target ADP and Actual Implementation During FY02-05 (1st Quarter)

0

5000

10000

15000

20000

25000

FY02 FY03 FY04 FY05

cror

e Tk Actual During 1st Quarter (P.A.)

Actual During 1st Quarter (Taka)Target ADP for the Full Fiscal

A closer look at the ADP implementation reveals that among the ministries/divisions

which received the highest allocation in the target ADP, the Ministry of Health and

Family Welfare implemented the least spending, only 2 percent of its allocation during

the first quarter of the FY05. Others performed moderately during this period: Power

Division 15 percent, M/O Education 15 percent, Local Government Division 18 percent

and M/O Communication 10 percent.

Figure 14 Performance of Major Ministries (in terms of ADP Allocation)

CPD: IRBD FY05 (First Interim) 18

It was perceived that the government will use the ADP resources for the post-flood

rehabilitation programme. CPD’s Rapid Flood Assessment 2004 pointed out that the

government could utilise Tk 1278.57 crore from its development budget which were kept

as sectoral and unallocated block allocation. CPD also mentioned that

ministries/divisions of some selected sectors,4 which can be closely involved in the post-

flood rehabilitation programme, have a block allocation of Tk 667.03 crores or 3.0% in

their ADP budget. Surprisingly many line ministries of this group showed very low ADP

realisation that involved Ministry of Industries (6 percent), Ministry of Agriculture (13

percent), Ministry of Fisheries and Livestock (9 percent) and Ministry of Water

Resources only (3 percent). More surprisingly, unallocated block allocation of Tk 295

crore and sector-wise block allocation of Tk 983.57 crore remained untouched during the

first three months of FY05. One needs to take a closer look at the financing of

government’s post-flood rehabilitation programme in the context of this low ADP

implementation and even lower foreign aid flow.

4 Sectors which CPD thought would be involved more directly in the post-flood rehabilitation programme are: Agriculture, Rural Development, Water Resources, Industry, Transport, Communication, Infrastructure & Water Supply and Health, Population & Family Planning.

CPD: IRBD FY05 (First Interim) 19

IV. STATE OF THE MONETARY SECTOR 4.1 Domestic Credit Expansion

The outstanding amount of domestic credit at the end of October 2004 stood at Tk

129183.00 crore of which Tk 99057 crores was in the private sector and rest percent in

the public sector. Total domestic credit during the first four months of the current fiscal

year registered a perceptible 15 percent growth over its matching figure for FY04.

Government’s expansionary approach following the Flood 2004 was reflected by this

upward trend in domestic credit expansion.

But it needs to be pointed out that though borrowing in the public sector increased on a

point to point basis by 3486.50 crores (i.e. by 13.09 percent) in October 2004 against the

decline of Tk.1005.30 crores (i.e. (-) 3.64 percent) during the comparable period of the

preceding year (2002); the high growth rate largely resulted from an increase of Tk.

1140.30 crores (i.e. 14.87 percent) in credit to the “Other Public Sector”. Net credit

expansion to government sector was 12.37 percent more than that of the matching figure

of the previous year.

Figure 15 Domestic Credit Expansion During Jul-Oct FY01 to FY05

0

20000

40000

60000

80000

100000

120000

140000

2001 2002 2003 2004

Tk in

Cro

re

Government Other Public Private Sector

CPD: IRBD FY05 (First Interim) 20

The 15 percent growth of private sector during the first four months of FY05 seems quite

low, when compared with the growth rate of 22 percent during the same period of

previous year. It may be noted that the correlation of credit growths between public and

private sector often appears to be negative5. When government borrows excessively from

the banking sector, it usually squeezes banks’ private sector lending capacity. As shown

in figure 16, growth of credit expansion in the private sector increased from 14.80 percent

in October 2002 to 22.23 percent in October 2003, while the growth of credit expansion

in the government sector declined from 0.40 percent to (-) 6.70 percent during the same

period. As the economy observed a high growth in the public sector (government 12.37

percent, and other public 14.87 percent) in October 2004, the growth in the private sector

declined to 15 percent.

Figure 16 Growths in Domestic Credit During Jul-Oct FY01 to FY05

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2001 2002 2003 2004

perc

ent

Government Other Public Private Total

However, excess liquidity in the banks provides enough room for government sector

borrowing to expand without crowding out the share of private sector. As seen during the

first four months of FY05, credit to private sector increased both in terms of absolute

volume and in terms of share corroborating the expansionary approach of the government

after the post-flood situation. 5 For example, on a point-to-point basis, growths during the first four months of FY01 to FY04 indicate a negative correlation of -0.4 percent.

CPD: IRBD FY05 (First Interim) 21

Figure 17

Private Sector Share in Domestic Credit During Jul-Oct FY01 to FY05

64.00

66.00

68.00

70.00

72.00

74.00

76.00

78.00

2001 2002 2003 2004

perc

ent

Share of private investment marginally increased from 76.29 percent during October

2003 to 76.68 percent during October 2004. This is quite high when compared to the

average share of 72 percent as was observed during the past five years.

4.2 Government Borrowing and Public Debt During the first four months of FY05, the government borrowing experienced a major

shift as regard to its source by way of moving away from non-bank sources to banking

sources. This process has been underpinned by a drastic fall in net the sale of National

Savings Deposits (NSD). Total public borrowing during the July-October period of FY05

stood at Tk 22150.77 crore registering a growth rate of about 7 percent over the

corresponding period of the previous fiscal year. Share of government borrowing from

the non-bank sources during this period decreased from 8.35 percent in FY04 to 3.77

percent in FY05. While net borrowing from the banking sector increased by about 12.37

percent, net borrowing of government from the non-bank sources decreased by (-) 51.72

percent during the period under report.

CPD: IRBD FY05 (First Interim) 22

-60.00

-50.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

Borrowing from Bank Borrowing from Non-Bank

Total GovernmentBorrowing

perc

ent

Figure 18 Growth of Net Government Borrowing During Jul-Oct FY05

(point-to-point)

Government borrowing through sale of NSD certificates during the first four months of

FY05 stood at Tk 3291.46 crore registering a (-) 6.50 percent negative growth, while the

repayment of principal increased by 37.15 percent, registering a (-) 51.72 percent

negative growth in the net sale. This decline in the sale of savings certificate is a response

to the government’s decision of lowering the interest rate of NSD certificates to reduce

the cost of borrowing and to encourage people to invest in the economy. The recent

upward movements in the capital market can be correlated with the declining trend of

NSD sale. Though the second aim of the government was somewhat achieved, the

lowering of interest rate however backfired with a sharp decline in NSD sale, putting the

government at a risk to face financing crisis to fulfil the budget deficit with borrowing. In

that case, the government will have to increase its borrowing from the banking sector,

which will then create a negative impact on the private sector investment by squeezing

the private sector’s share of borrowing from the bank.

CPD: IRBD FY05 (First Interim) 23

0

500

1000

1500

2000

2500

3000

3500

4000

Jul-Oct FY04 Jul-Oct FY05

Cror

e Tk

Sal

e

Net Sale

Repayment

Figure 19 Sale and Repayment of NSD Certificate

In the context of this dilemma, recently the government has taken some decisions to

increase the sale of NSD certificates with the same lowered interest rate. The government

has increased the limit of investment in NSD certificates, for single owner from Tk 20

lakh to Tk 25 lakh and in dual name, from Tk 40 lakh to Tk 50 lakh, which is equally

applicable for re-investment. Besides one can also reinvest his/her interest with the

principal. The commission of banks and post-offices has also been increased from Tk 20

to 5 percent for each transaction to encourage their selling effort.

4.3 Agricultural Credit

It was expected that the post-flood rehabilitation programme of the government will be

reflected by an increase in the agricultural credit. However agricultural credit expansion

during the first four months of FY05 shows a mixed picture with improved disbursement

rate which remains low in terms of target achievement.

Credit disbursement to the agricultural sector stood at Tk 1154.78 crore at the end of

October 2004 which is about 58 percent higher than the disbursement of the matching

period of the previous year. However this extraordinarily high growth rate can be

explained by its lower benchmark during the previous year. During the first four months

of FY04 only Tk 729.53 core were disbursed as against Tk 850.60 crore of recovery. This

out-flowed an amount of Tk 121 crore from the rural economy.

CPD: IRBD FY05 (First Interim) 24

-200.00

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

Disbursement Recovery Netf low

taka

in c

rore

Jul-Oct FY04 Jul-Oct FY05

Figure 20 Growths in Agricultural Credit Expansion During Jul-Oct FY05

In this context, a moderately high credit expansion during the agricultural sector could

take a breath following the devastating flood. However, notwithstanding the agricultural

credit growth of FY03, the post-flood disbursement of agricultural credit during the FY05

falls short of the target as only 20.85 percent of the total target (Tk 5537.9 crore) was

disbursed during the first four months of FY05. It may be recalled that CPD in its Flood

2004 report suggested for disbursement of Tk. 5000 crore as agricultural credit in FY05. 4.4 Industrial Credit

In the backdrop of the slowdown in growth of industrial term loans in the recent years

(since FY01), the disbursement record for FY04 was quite impressive – Tk. 6619.60

crores, i.e. 67.08 percent growth. After a recovery of Tk 4954.24 crores in FY04, the net

flow to the sector is Tk. 1304.97 crores which compares favourably with the outflow of

(-) Tk. 40.90 crores during the comparable period in FY03.

The expansionary trends in the disbursements of industrial term loan continued in the

first quarter of FY05 (61.5 per cent growth). But in the absence of the data on recovery of

the loans, it is hard to get a complete picture of the term loan situations.

CPD: IRBD FY05 (First Interim) 25

However, one interesting feature is that loan disbursement by NCBs declined by 60

percent, though the loan sanctioned was 257 per cent higher than the first quarter of the

FY04. Loan disbursement from PCB (domestic) shows a growth rate of 154 per cent,

which has also emerged decisively as the largest contributor (almost 65 per cent) to total

industrial loan disbursement. Figure 21

Term Loan for the FY04 and FY05

0.00

1000.00

2000.00

3000.00

4000.00

5000.00

6000.00

7000.00

FY04 (July-Sep.) FY05 (July-Sep.)

Cro

re T

k

NBFI

PCB(F)

PCB(D)

DFI

NCB

Figure 22

Working Capital for the FY04 and FY05

0.00

500.00

1000.00

1500.00

2000.00

2500.00

FY04 (July-Sep.) FY05 (July-Sep.)

Cro

re T

k

NBFI

PCB(F)

PCB(D)

DFI

NCB

CPD: IRBD FY05 (First Interim) 26

The disbursement of working capital grew at 46 per cent in FY05 (July-Sept). Similar to

the term loan, PCB (domestic) has the largest share (almost 65 per cent) in total

disbursement of working capital.

4.5 Price and Wage Inflation 4.5.1 Trend in Inflation

The rising trend in inflation is another concerning issue of the last few months. The

general inflation in October 2004 rose to 7.92 on point-to-point basis while inflation in

October 2003 was 6.16 per cent. Three major features of the recent rise in the price level

is: (i) inflation is higher in the rural areas, (ii) food inflation is higher in both rural and

urban areas; and (iii) non-food inflation showing a declining trend since October 2002.

The 12-month moving average inflation rate also shows an increasing trend, reaching as

high as 6.21 per cent in October 2004. The major factor behind this trend is the increase

in food price, which increased to 7.57 per cent (10.46 per cent on point to point basis).

However, the weakening of Taka against dollar and the rising import prices also added

fuel to the rising trend of inflation.

Figure 23

Inflation (Moving Average)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Jul-0

1

Sep-

01

Nov

-01

Jan-

02

Mar

-02

May

-02

Jul-0

2

Sep-

02

Nov

-02

Jan-

03

Mar

-03

May

-03

Jul-0

3

Sep-

03

Nov

-03

Jan-

04

Mar

-04

May

-04

Jul-0

4

Sep-

04

Per

cen

t

General Food Non Food

CPD: IRBD FY05 (First Interim) 27

4.5.2 Trend in Food Inflation

The recent flood may be the most influencing factor in the rise in the food price, although

the upturn started back in January, 2003. The food inflation in FY04 was 6.64 per cent

(on point to point basis), the food inflation then started accelerating and on October 2004,

it reached 10.46 per cent (on point to point basis), a record high since FY99.

Figure 24

Food Inflation (Point to Point)

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Jul-0

0

Oct

-00

Jan-

01

Apr-

01

Jul-0

1

Oct

-01

Jan-

02

Apr-

02

Jul-0

2

Oct

-02

Jan-

03

Apr-

03

Jul-0

3

Oct

-03

Jan-

04

Apr-

04

Jul-0

4

Oct

-04

Per

cen

t

National Rural Urban

4.5.3 Wage Inflation

The general wage index grew by 5.38 per cent in October 2004, on a point to point basis.

The general wage inflation in October 2002 and 2003 was 11.25 and 6.83 per cent,

respectively. The crucial point here was that CPI inflation is increasing on the one hand

while the wage index was falling on the other hand in FY04. However, wage inflation in

FY04 was 3.93 per cent and since then it started increasing. Agricultural wage index also

started increasing since July 2004, following a decreasing trend over the previous 12

months.

CPD: IRBD FY05 (First Interim) 28

Figure 25

Wage Inflation (Point to Point)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00Ja

n-02

Mar

-02

May

-02

Jul-0

2

Sep

-02

Nov

-02

Jan-

03

Mar

-03

May

-03

Jul-0

3

Sep

-03

Nov

-03

Jan-

04

Mar

-04

May

-04

Jul-0

4

Sep

-04

Per c

ent

General Manufacturing Construction Agriculture Fishery

4.5.4 Inflation Trend in South Asia

Inflation in India (on a point to point basis) in July 2004 was 6.16 per cent, which was

inclined by an increase of the oil price in the international market. WPI inflation reached

at 8.3 per cent in August 2004; and then gradually decreased to 7.1 per cent in October

2004. The CPI inflation in Pakistan was also quite high, but it shows a declining trend in

contrast to Bangladesh.

TABLE 2

COMPARISON OF INFLATION IN INDIA, PAKISTAN AND BANGLADESH

Bangladesh (CPI) India (WPI) Pakistan (CPI) Jul-04 5.6 6.2 9.3

Aug-04 5.5 8.3 9.2 Sep-04 7.4 7.8 9.0 Oct-04 7.9 7.1 8.7

CPD: IRBD FY05 (First Interim) 29

Figure 26

Comparison among India, Pakistan & Bangladesh

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jul-04 Aug-04 Sep-04 Oct-04

Bangladesh (CPI) India (WPI) Pakistan (CPI)

4.5.5 Experience with 1998 Flood: (Base FY1986=100)

The post flood trends of the 1998 show that inflation rose to as high as 12 per cent in

December 1998, then decreased gradually. Experts are predicting similar trends in

inflation after the recent flood. Moreover, the increase in the price of oil, diesel and

kerosene in December 2004 may increase the rate of inflation further.

CPD: IRBD FY05 (First Interim) 30

Figure 27

Inflation During the Flood Year 1998

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00Ju

l-96

Oct

-96

Jan-

97

Apr

-97

Jul-9

7

Oct

-97

Jan-

98

Apr

'98

July

'98

Oct

'98

Jan'

99

Apr

'99

July

'99

Oct

-99

Jan-

00

Apr

-00

Per

cen

t

Moving Average Point to Point

4.5.6 Projection on Food Inflation

Preliminary estimates suggest that production of Aman rice in FY05 will be 10 per cent

less than the last year. Per unit production cost of Boro rice will go up due to increased

cost of diesel and there is apprehension that Boro production will be adversely affected

due to increase in diesel price (see section 11.4 for details). International price of

foodgrains is on the rise and is expected to increase further in the coming months due to

low production prospect of rice in Thailand, Vietnam and India caused by abnormal

dryness (see section 11.1 for details).

Therefore, it is most likely that inflation in food prices may continue until the harvest of

Boro rice in April-May.

CPD: IRBD FY05 (First Interim) 31

Box 1 An Enquiry into Factors Influencing Inflation: Inflation, as measured by changes in CPI, increased sharply between FY98-99, but this trend was reversed in FY00. Inflation started climbing again on FY02 and in FY04 it reached 5.8 per cent, the highest since FY99. Data on some of the factors likely to have influenced the inflationary process in Bangladesh is reported below:

Factors Influencing Inflation

Inflation Rate (End of

Period)

Budget Deficit (as % of GDP)

Exchange Rate Depreciation (%)

Real GDP Growth (%)

Broad Money Growth

FY97 4.0 2.0 -4.4 5.4 10.8FY98 8.7 2.1 -5.7 5.2 10.2FY99 7.1 3.2 -4.5 4.9 12.8FY00 2.8 4.5 -4.9 5.9 18.6FY01 1.9 4.1 -10.5 5.3 16.6FY02 2.8 3.7 -1.6 4.4 13.1FY03 4.4 3.4 0.0 5.3 15.6FY04 5.8 3.4 na 5.5 13.8

The significant decline in the inflation rate since FY98 reflects the impacts of tight monetary policies and contractionary fiscal policies of the previous year, as the budget deficit as % of GDP was only 2.0 per cent in FY97. The government and the central bank pursued expansionary monetary and fiscal policies in the late 90s and early 2000s. As a result, the inflation started increasing but with lagged response. Moreover, a large depreciation of the exchange rate by 10.5 per cent in FY01 along with monetary and fiscal expansion contributed toward an upward trend in inflation, started in FY02. The budget deficit as per cent of GDP shows a declining trend since FY00, from 4.5 per cent in FY00 to 3.4 per cent in FY04. On the other hand, the growth rate of broad money supply averaged 15.5 per cent in the last 5 years. This indicates preference toward the monetary policies over the fiscal policies by the government. The correlation between inflation and budget deficit as % of GDP for the same period and one lagged period is -0.6 and -0.7, respectively. On the other hand, the correlation between inflation and budget deficit as % of GDP for 2 and 3 lagged periods is -0.2 and 0.1, respectively. However, the correlation between inflation and budget deficit as % of GDP for 4 and 5 lagged periods is 0.3 and 0.3, respectively. This implies that fiscal policies take at least 2 periods to affect inflation. The correlation between inflation and 3 and 4 period lagged money supply growth is 0.8 and 0.2, respectively. The correlation between inflation and the same, 1 and 2 period lagged money supply growth is negative, which contradicts the theory.

CPD: IRBD FY05 (First Interim) 32

V. STATE OF THE REAL SECTOR 5.1 Agricultural Production Crop

Foodgrain production in FY04 recorded the highest production in the history of

Bangladesh since independence. According to the final estimates of the BBS, actual

foodgrain production in FY04 was 27.44 million metric tons (Aus: 1.83 million metric

tons, Aman: 11.52 million metric tons, Boro: 12.84 million metric tons, and wheat: 1.25

million metric tons) which was 2.80 percent higher than that of FY03. In FY04, total rice

production increased by 3.98 percent (compared to FY03), while wheat production

decreased by 16.85%. It may be mentioned here that wheat production has been gradually

decreasing since 1999/00. Thus, it appears that increase in total foodgrain production in

recent years is mainly due to the increase in rice production.

The operational target for foodgrain production in FY05 has been set at 30.0 million

metric tons which is 9.32 percent higher than actual production in FY04. Initial estimates

show that harvested area under Aus rice has declined from 1.2 million ha in FY04 to 1.0

million ha in FY05, while production of Aus rice has declined from 1.83 million tons to

1.45 million tons. Decrease in Aus production was mainly due to the damage caused by

July-August flood in 46 districts and also because of decrease in area under Aus rice.

Achieved area under transplanted Aman rice (after damage by July-August flood in 46

districts and excessive rain and flash flood in September in 24 districts) is 4.88 million ha

which was 3.44% less than last year. On the other hand, achieved area under broadcast

Aman was 0.42 million ha (33.15% less than FY04). According to the Directorate of

Agricultural Extension (DAE), 35.0 percent of the transplanted Aman area was under

local variety and 65.0 percent area was under HYVs. Most importantly, rice plants had

limited time for tillering and vegetative growth which might have effected plant densities

and thereby, number of plants per hectare in many districts. Though we had floods and

excessive rains in 2004 in most of the areas of Bangladesh but one district (Nilphamari)

experienced drought. It is well known that yield potential of local varieties is much lower

than that of HYVs.

CPD: IRBD FY05 (First Interim) 33

Therefore, all these factors (decrease in Aman area, dominance of local varieties, lower

number of effective tillers per unit area in many districts and drought) would have a

negative effect on the production level. Harvesting of Aman rice is almost over.

However, the respective agencies would require some time to come up with the

production estimates of Aman. There is apprehension among experts that Aman

production in FY05 might be about 10 percent less than that of FY04. This implies that

the government must have to take extra efforts for increased production in Boro season

by ensuring delivery of seed, fertilizer and irrigation fuels.

This year farmers have taken extra effort to increase vegetable production by observing

high prices of vegetables during August-October. Increased effort of farmers had

increased production and supply of vegetables since November which helped to reduce

price. However, farmers’ success in increased vegetables production has been penalizing

them in a very harsh way. In many areas farmers are not able to sell their vegetables even

at their cost of marketing.

Livestock

Production of eggs in FY04 was 4.780 billions which was slightly higher than FY03

(4.777 billion). Total meat production increased from 0.83 million tons in FY03 to 0.91

million tons in FY04 (9.64 percent increase). Milk production has increased from 1.82

million tons in FY03 to 1.99 million tons in FY04 (9.34 percent increase). July-August

flood and excessive rain in September has severely affected the livestock sector. A total

of 293,301 poultry birds, 1649 cattles, and 4546 goats and sheep were killed by the flood.

After the natural disaster of this enormous scale it was a great concern of outbreak

diseases of poultry and cattle. No epidemic of diseases has so far been reported. Hence,

it is expected that this year’s production of different livestock products would be good.

CPD: IRBD FY05 (First Interim) 34

Fisheries

Total fisheries production has increased from 2004 thousand metric tons in FY03 to 2126

thousand tonnes in FY04 (6.09 percent increase). Contribution of inland open water

(capture), inland open water (culture) and marine fisheries was 36.41, 41.63 and 21.97

percent, respectively. Flood 2004 had devastating impact on fish farms. According to the

Ministry of Livestock and Fisheries, flood has damaged shrimp, fish and fingerlings in 43

districts of Bangladesh amounting Tk. 9907.4 million. The government has taken

initiatives to rehabilitate farmers with a total budget of Tk 206.86 million.

We may conclude by saying that production prospect of foodgrains in FY05 is bleak. It is

widely speculated that aman production would be around 10 percent less than that of last

year (FY04) while aus production was 0.38 million tonnes less (21% less) than last year’s

production. Therefore, extra efforts need to be taken for increased production of Boro

rice. Crop sector may have slow growth in this year, but livestock and fisheries sub-

sectors may register medium growth.

5.2 Industrial Production The country observed a moderate recovery in the industrial sector during the first four

months of the FY05 after the devastating flood that the economy experienced at the

beginning of the FY05. The weighted growth of major industries which accounts for

about 68.18 percent of the whole manufacturing sector experienced a moderate 3.87

percent growth during the July-October period of FY05 over the corresponding figure of

the previous fiscal year. Yarn, cloth and garments showed 18.44 percent, 26.75 percent

and 17.37 percent growth supporting the high growth performance in the export in this

sectors. Among others, sector which showed modest to high growth during this period

includes: fertilizer (13.97 percent), MS rod (5.93 percent), cement (12.27 percent) and

drugs and pharmaceuticals (10.19 percent). However, jute textile, paper and petroleum

products showed negative growths during this period registering (-) 8.12 percent, (-)19.53

percent and (-) 4.91 percent negative growth respectively.

CPD: IRBD FY05 (First Interim) 35

-30

-20

-10

0

10

20

30

40

50

Jute

Tex

tile

Gar

men

ts

Ferti

lizer

Cem

ent

Ciga

rette

s

Drug

s &

Phar

mac

eutic

als

Salt

Soap

&de

terg

entG

row

th (p

erce

nt)

FY04 (Jul-Oct)FY05 (Jul-Oct)

0

50

100

150

200

250

300

350

July

Aug Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

June

2002-032003-042004-05

Figure 28

Growths of Major Industries During July to October of FY04 and FY05

Figure 29

Quantum Index of Production during FY03-05 (1988-89=100)

The quantum index of production shows a robust 8.58 percent growth during the first

four months of the FY05 when compared with the 3.52 percent of growth during the

FY04 over the corresponding period f the previous fiscal year. This growth is even more

encouraging keeping in mind that the economy started with a flood during the FY05.

CPD: IRBD FY05 (First Interim) 36

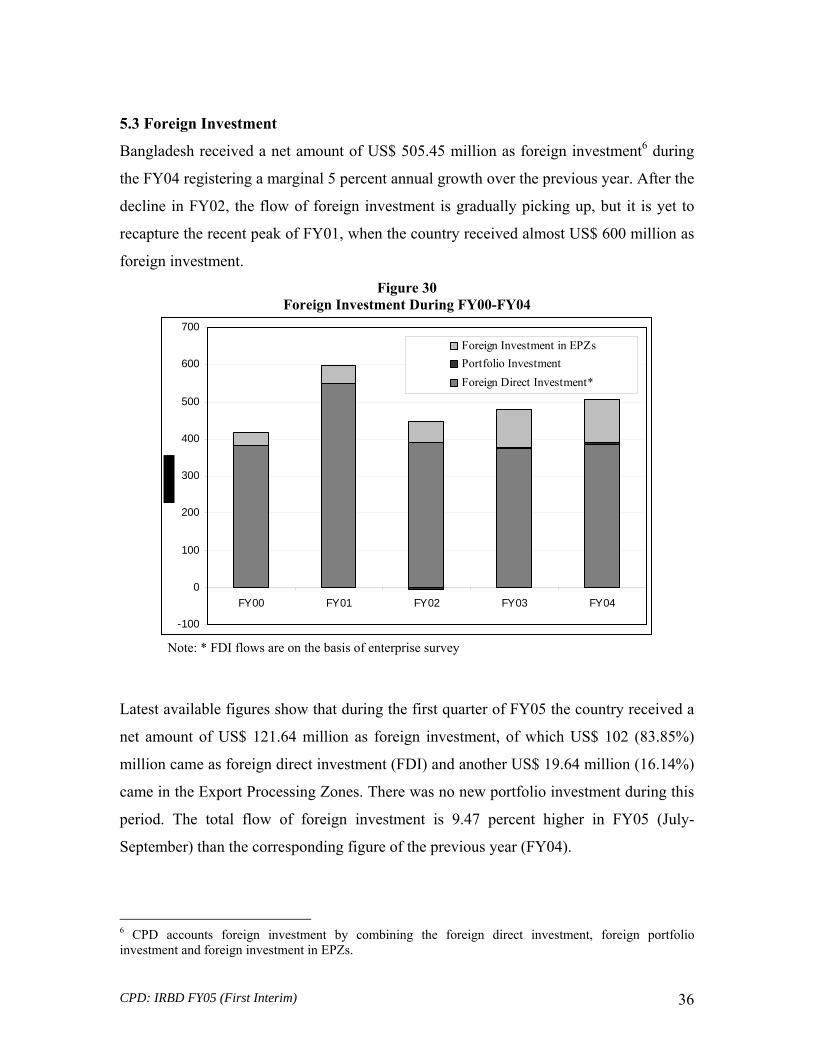

5.3 Foreign Investment

Bangladesh received a net amount of US$ 505.45 million as foreign investment6 during

the FY04 registering a marginal 5 percent annual growth over the previous year. After the

decline in FY02, the flow of foreign investment is gradually picking up, but it is yet to

recapture the recent peak of FY01, when the country received almost US$ 600 million as

foreign investment.

Figure 30 Foreign Investment During FY00-FY04

-100

0

100

200

300

400

500

600

700

FY00 FY01 FY02 FY03 FY04

Foreign Investment in EPZsPortfolio InvestmentForeign Direct Investment*

Note: * FDI flows are on the basis of enterprise survey

Latest available figures show that during the first quarter of FY05 the country received a

net amount of US$ 121.64 million as foreign investment, of which US$ 102 (83.85%)

million came as foreign direct investment (FDI) and another US$ 19.64 million (16.14%)

came in the Export Processing Zones. There was no new portfolio investment during this

period. The total flow of foreign investment is 9.47 percent higher in FY05 (July-

September) than the corresponding figure of the previous year (FY04).

6 CPD accounts foreign investment by combining the foreign direct investment, foreign portfolio investment and foreign investment in EPZs.

CPD: IRBD FY05 (First Interim) 37

Figure 31 Foreign Investment During July-September of FY04-05

0

20

40

60

80

100

120

140

FY04 (Jul-Sep) FY05 (Jul-Sep)

Foreign Investment inEPZs

Portfolio Investment

Foreign DirectInvestment*

Note: * FDI flows are on the basis of enterprise survey

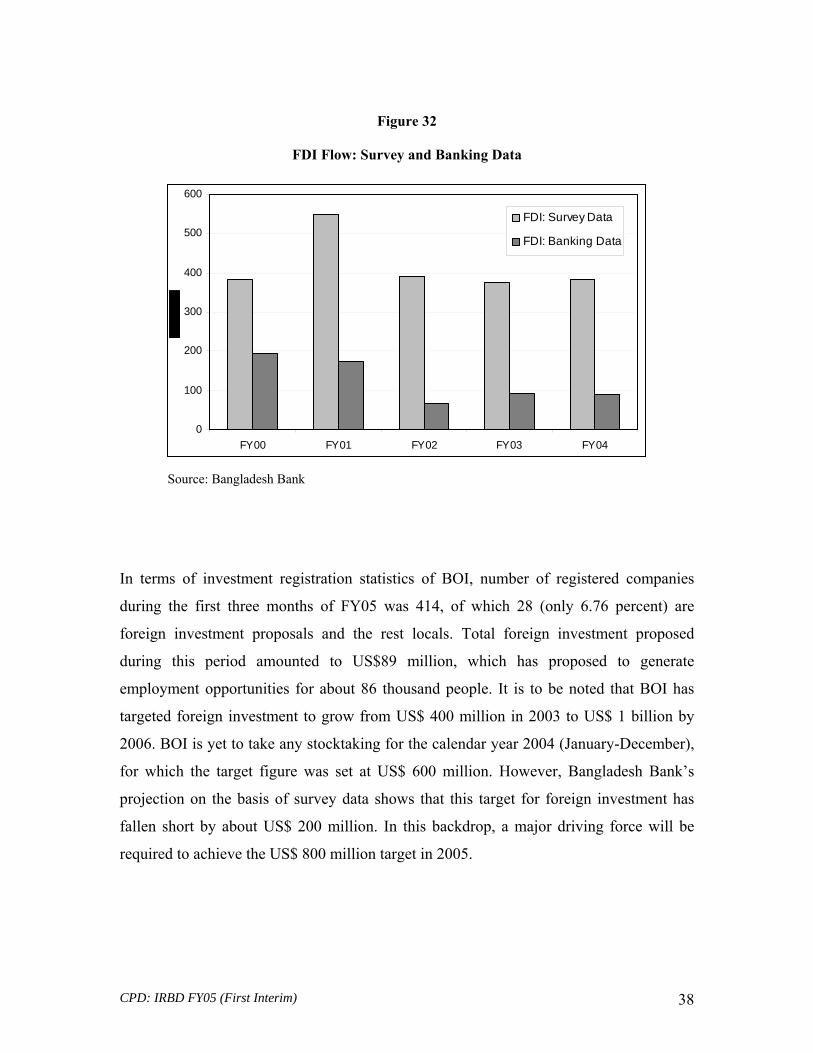

However, following detection of the huge discrepancy between the Bangladesh Bank and

BOI’s foreign investment data, recently the Bangladesh Bank, with the support of IMF,

has taken the initiative to incorporate survey data (instead of banking data) to account the

foreign investment flow. Since the banking data gives only a very partial coverage as

reinvested earnings are excluded altogether, intra-company loans are under-reported and

non-cash equity flow (e.g. equity contribution in the form of machinery and equipments)

are not identified from the trade returns and it remains substantially under-covered.

Following figure shows the difference between survey data and banking data during the

previous five years. Still there are remain some divergence between the FDI survey data

of Bangladesh Bank and BOI.

CPD: IRBD FY05 (First Interim) 38

Figure 32

FDI Flow: Survey and Banking Data

0

100

200

300

400

500

600

FY00 FY01 FY02 FY03 FY04

FDI: Survey Data

FDI: Banking Data

Source: Bangladesh Bank

In terms of investment registration statistics of BOI, number of registered companies

during the first three months of FY05 was 414, of which 28 (only 6.76 percent) are

foreign investment proposals and the rest locals. Total foreign investment proposed

during this period amounted to US$89 million, which has proposed to generate

employment opportunities for about 86 thousand people. It is to be noted that BOI has

targeted foreign investment to grow from US$ 400 million in 2003 to US$ 1 billion by

2006. BOI is yet to take any stocktaking for the calendar year 2004 (January-December),

for which the target figure was set at US$ 600 million. However, Bangladesh Bank’s

projection on the basis of survey data shows that this target for foreign investment has

fallen short by about US$ 200 million. In this backdrop, a major driving force will be

required to achieve the US$ 800 million target in 2005.

CPD: IRBD FY05 (First Interim) 39

Figure 33

Sectoral Composition of Registered FDI in FY04

Textile16%

Services62%

Chemical7%

Agro-based6%

Misc0%

Engineering1%

Food and allied3%

Leather and rubber

3%

Printing and publication

2%

Source: Board of Investment.

The sectoral decomposition of FDI flow of FY04 revels that the majority of the FDI in

Bangladesh comes to the services sector which accumulates about 62 percent of the total

FDI flow, which is followed by the textile (16 percent), chemical (7 percent) and agro-

based industries (6 percent) sector. However sectors like infrastructure, engineering and

leather remains under-invested.

5.4 Capital Market The dynamics of capital market in Bangladesh is such that it does not reflect the real

macroeconomic performance of the country. However certain aspects of investment

scenario can be observed from the movements in the capital market. Since the 1996

incident, the capital market experienced a deliberately slow but steady recovery that

continued throughout the FY04. Several new IPOs came into the market and a bullish

trend was observed from the mid-November of FY04, which gathered momentum in the

early part of December recording a 1015.97 general index for the first time after 1996.

CPD: IRBD FY05 (First Interim) 40

0

1

2

3

4

5

During the first half of FY05 a spectacular upsurge in all share price index was observed

both in Dhaka Stock Exchange (DSE) and Chittagong Stock Exchange (CSE). The

general index of DSE increased from 967.88 in December 2003 to 1971.31 in December

2004 registering a thousand-point increase in one year. This was however contributed

mostly by the category-A companies as DSE 20 index also registered a 930.46 point

increase during the same period (from 1228.20 in December 2003 to 2158.66 in

December 2004). CSE also followed the suit as the CSE general and CSE 30 index went

up to as high as 3597.70 and 3463.76 at the end of December 2004.

Figure 34 Entry of IPOs in the Capital Market (Monthly Statistics)

On the contrary, the issuance of IPO has gone down dramatically since no new IPO

entered into the market in between November 2003 and July 2004 (see figure 34). This is

a worrying concern as following the simple law of demand-supply theory; the rate of over

subscription has gone up.

There is a substantial amount of liquid money in the hands of common people and at the

household level, other than that of in the banking system of Bangladesh. In view of the

fact that the income potentials from sources like bank and NSD certificates have gone

down due to lowering of the interest rates, a number of small and medium investors are

now coming into the capital markets with their investible surplus. Following the boom

and burst of the Capital Balloon in 1996, several initiatives taken by the Securities and

CPD: IRBD FY05 (First Interim) 41

Exchange Commission7 (SEC) also contributed to this over subscription of IPOs.

However, very recently some new IPOs have entered into the market8 and several others

are on the pipeline9.

IPOs these days are mainly coming from the banking and financial sectors and not from

the real sector (after the Lafarge Surma Cement in November 2003). No IPOs from

telecommunication services was observed. A number of non-bank financial institutions

have applied and are coming to the market soon. In general, banking financial institutions

performed better in security market, out of 29 enlisted banking and non-banking financial

institutions, 21 are of ‘A’ category, whose price earning ratios are mostly near about 10.

It seems that private commercial banks have performed well under prudent laws and

regulations and better supervision of Bangladesh Bank, introducing new products with

traditional one, such as government treasury bills, prize bonds, shares of public limited

companies, treasury dealings both in local and foreign currency, automation tools such as

ATM, SWIFT, extended consumer credit scheme, merchant banking, credit card

operation and Islamic banking.

However IPOs from the real sectors also needed to be encouraged. Major reason for

profit making companies for not entering in the capital market can be the absence of

managerial expertise to expand their business further. Some also fears to loose their

family ownership from the company if they go to the share market. Besides it also induce

them to have more accountability and transparency in terms of profit making.

This scarcity of IPOs can also be linked with the ever increasing all share price index.

Since the buying of new IPOs is becoming increasingly expensive (for higher price) and

difficult (for lower IPO entry); investors are now trying to make profit from selling and

buying second-hand shares. Besides, the dividend and profit they are provided for these