state contract law and debt contracts · 1032 the journal of law & economics ies generally...

TRANSCRIPT

1031

[ Journal of Law and Economics, vol. 57 (November 2014)]

© 2014 by The University of Chicago. All rights reserved. 0022-2186/2014/5704-0040$10.00

State Contract Law and Debt Contracts

Colleen Honigsberg Columbia University

Sharon Katz Columbia University

Gil Sadka University of Texas at Dallas

Abstract

This paper examines the relationship between debt contracts and state contract

law. We first develop an index to evaluate whether each state’s law is favorable or

unfavorable to lenders. We then analyze how the contract terms, the frequency

of covenant violations, and the repercussions of covenant violations vary across

states. We find that cash collateral is most likely to be used when the contract

is governed by law that is favorable to debtors and that out-of-state borrowers

who use favorable law pay higher yield spreads. In addition, when the law is

favorable to lenders, there are significantly fewer covenant violations, and the

repercussions of covenant violations—measured as changes in the borrower’s

investment policy—are more severe. We also compare the characteristics of rel-

evant parties across states, and the results provide support for the theory that

there is a market for contracts similar to the market for incorporations.

1. Introduction

This paper examines the association between state contract law and debt con-tracts. A recent stream of papers in finance and economics study the role that debt contracts play in mitigating agency problems between equity and debt hold-ers (for example, Baird and Rasmussen 2006; Chava and Roberts 2008; Roberts and Sufi 2009; Nini, Smith, and Sufi 2009). This area of literature examines both the contract terms and the implications of covenant violations. While these stud-

We are grateful for helpful comments and suggestions from Sam Peltzman, an anonymous ref-eree, Thomas Bourveau, Alon Cohen, J. Anthony Cookson, Shahar Dillbary, Miguel Duro-Rivas, Fabrizio Ferri, Victor P. Goldberg, Shachar Hadar, Sharon Hannes, Trevor Harris, Robert Jackson, Jr., Alon Kalay, Urooj Khan, Mattia Landoni, Ningzhong Li, Suresh Nallareddy, Doron Nissim, Stephen Penman, Ariel Porat, Robert E. Scott, Ofer Setty, Elissa Swift, Frederick Tung, Omri Yadlin, and Yu-Ting Forester Wong. We are also grateful to workshop participants at the 2013 Conference on Empirical Legal Studies, the 2014 American Accounting Association annual meeting, the 2014 European Accounting Association Annual Congress, the 2014 Financial Accounting and Reporting Section Midyear Meeting, the 2014 Midwest Economics Association annual meeting, the 2014 Tem-ple University annual conference, the 2014 Trans-Atlantic Doctoral Conference, Columbia Business School, and Tel Aviv University. All errors are our own.

1032 The Journal of LAW & ECONOMICS

ies generally treat contract law as a uniform product across states and assume

that all contracts are enforced in a similar fashion, in practice lenders and bor-

rowers select the state law that will govern the contract. Because the legal rights of

both parties vary depending on the law chosen, the state contract law may be as-

sociated with enforcement. To examine this relationship, we first categorize each

state’s contract law by whether it is favorable or unfavorable to lenders, and then

we examine the characteristics of the contracts and the relevant parties across

states. Finally, we test whether the contract terms, frequency of covenant viola-

tions, and repercussions of covenant violations are related to the state contract

law.

We begin by classifying states according to whether they are favorable to lend-

ers (pro-lender) or favorable to debtors (pro-debtor). In our primary analysis, we

present two metrics to represent the state law. The first metric is the Pro-Debtor

Index, which captures six distinct features of state law that are related to contract

enforcement and that differ across states. The second metric is the perceived lit-

igation risk, which measures the rate of litigation using the reported number of

lawsuits (for a use of such methodology, see Li et al. 2012; Heninger 2001; Fran-

cis, Philbrick, and Schipper 1994). For robustness, we supplement our two pri-

mary rankings of state law with two additional metrics: an alternative classifi-

cation based on the frequency of litigation and a measure in which we rank the

states on the basis of the average number of lenders per loan. All of our different

rankings clearly identify New York as the most pro-lender state and California as

the most pro-debtor state.

Using these rankings of state contract law, we provide descriptive statistics on

the characteristics of contracts, borrowers, and lenders across states to better un-

derstand how borrowers and lenders self-select into different legal regimes. The

analysis suggests that there are significant differences in borrower-lender pairs

across states, most notably that they are more likely to use pro-lender law when

the borrower is highly leveraged and when the deal size is larger. Our findings

also suggest that borrowers and lenders with operations in fewer states are more

likely to use the law of the state in which they are primarily located but that par-

ties with significant multistate operations are more likely to use law from pro-

lender states. This suggests that the costs and benefits to using out-of-state law

vary depending on the geographic characteristics of the borrower and lender.

The observed self-selection is consistent with the legal argument that states

compete to provide law for commercial contracts and that New York has been

particularly successful in courting commercial contracts (Eisenberg and Miller

2010). In our data, we find that New York law is used most frequently and is

especially popular with multistate lenders. It is also noteworthy that the states

that have developed more pro-lender law are the ones in which the financial sec-

tor contributes a greater percentage of the state’s gross domestic product (GDP).

Given that state legislators can affect the state’s contract law, it is important to

acknowledge the role of the state in setting contract law.

We then examine how the contract terms, the frequency of covenant viola-

Debt Contracts 1033

tions, and the consequences of violations vary with the original choice of con-tract law. We first document that cash collateral, which is defined as cash and cash- equivalent assets that are pledged as security for a loan, is used most fre-quently when the contract is governed by pro-debtor law and that out-of-state borrowers who use pro-debtor law pay a premium. We next show that the fre-quency of financial covenant violations increases as the law becomes more favor-able to debtors. Financial covenants are accounting-based measures of perfor-mance with which the borrower must comply (for example, a financial covenant might require that the borrower’s debt be no more than a certain percentage of its assets). A borrower who violates a covenant must inform the lender; such vi-olations are considered technical default and provide lenders with contractual rights to make substantial changes to the loan agreement, including the right to demand immediate repayment. Prior literature has shown that creditors use the contractual rights granted by covenant violations to force the borrower to imple-ment a more conservative investment policy (Roberts and Sufi 2009; Nini, Smith, and Sufi 2012). To test whether there is an association between the legal regime and the repercussions of covenant violations, we test whether changes in firm in-vestment policy postviolation—measured as changes in net debt issuance, acqui-sitions, capital expenditures, and physical property postviolation (see, for exam-ple, Roberts and Sufi 2009; Nini, Smith, and Sufi 2012)—are uniform across legal regimes. Our analysis shows that when the contract is governed by pro-lender law, there are significantly fewer covenant violations but that the repercussions of those violations are significantly more severe.

Our findings should be interpreted with caution because parties to the contract are able to select their governing law and because state legislators can affect the governing law in each state. As a result, the associations reported in the paper are descriptions of an equilibrium sorting of borrowers and creditors. However, regardless of whether our results arise because of self-selection or because parties respond to differences in the law, they indicate that the contract law is an im-portant consideration in understanding the relationship between borrowers and lenders.

We contribute to the literature in several ways. First, as the first empirical paper to test differences in state contract law, we address the issue of how to measure contract law and provide a ranking of states based on the degree to which each state’s contract law is favorable or unfavorable to lenders. Second, we provide the first descriptive evidence that the variation in state contract law is associated with real differences in firm financing, investment policy, and contract terms. Third, our analysis provides initial evidence consistent with the legal theory that there is a market for contracts. We document that New York, the primary state for debt contracts and a state widely known for its efforts to attract commercial contracts, has increased its dominance since the mid-1990s. We note, however, that we can-not identify whether New York’s dominance has increased because of its more pro-lender laws.

The remainder of our paper proceeds as follows. Section 2 describes the rel-

evant legal framework and background literature. Section 3 describes our data.

1034 The Journal of LAW & ECONOMICS

Section 4 presents our main empirical findings. Section 5 presents our robustness tests. Section 6 concludes.

2. Legal Framework for Private Debt Contracts

2.1. Choice of Contract Law

Prior literature on U.S. law and debt contracts has studied the relationship be-tween the laws of the state in which the borrower is incorporated and the con-tract (Qi and Wald 2008; Mansi, Maxwell, and Wald 2009), but no prior work has considered the contract law itself.1 Although the state of incorporation and the state of contract can be the same, we find that this occurs less than 10 percent of the time. As a general rule, the internal affairs of a corporation, such as the rela-tionship between shareholders and management, are governed by the laws of the state in which the firm is incorporated. However, substantial commercial con-tracts such as debt contracts are considered to be part of the external affairs of a corporation and are governed by the state contract law chosen by the parties and noted in a choice-of-law clause in the contract. Therefore, it is the state contract law rather than the state corporate law that governs debt contracts.2 In this paper, we thus make the distinction between state corporate law and state contract law, and we study contract law specifically.3

Over the past few decades, there have been two significant developments in the legal framework surrounding choice-of-law clauses. First, courts have become more willing to enforce the parties’ choice of law. The general rule is that courts will enforce the parties’ choice of law only if that state has a nexus—or a rea-sonable relationship—to the contract. However, the required closeness for a rela-tionship to be deemed reasonable has been interpreted far more broadly over the past few decades (Eisenberg and Miller 2010).4 Second, many states have passed

1 Beginning with La Porta et al. (1998), the relation between law and debt contracting has also been studied in international settings. See, for example, Davydenko and Franks (2008), Cumming and Johan (2006), and Qian and Strahan (2007). Our U.S. setting controls for disadvantages that arise in international settings, such as different levels of economic development.

2 See, for example, Engel v. Ernst, 724 P.2d 215, 216 (Nev. 1986): “It is well settled that parties are permitted to select the law that will govern the validity and effect of their contract.” We focus here on the choice of law rather than the forum selection because of concerns regarding the enforceabil-ity of forum-selection clauses during our sample period. See, for example, Atlantic Marine Construc-tion Co. v. U.S. District Court for the Western District of Texas 571 U.S. ___ (2013), which resolves a circuit split in federal courts over how to enforce forum-selection clauses.

3 Although we focus on the contract law, we also estimate the models in Tables 7–10 controlling for the payout restrictions noted in Wald and Long (2007), Qi and Wald (2008), and Mansi, Max-well, and Wald (2009). All of our results remain consistent and significant at current levels. In ad-dition, because we expect private lenders who rely on corporate law to prohibit reincorporation without permission, we review all of our contracts to determine whether any of our lenders restrict reincorporation. We do not find any such clauses.

4 See, for example, Mechanic v. Princeton Ski Shop, Inc., 1992 U.S. Dist. LEXIS 19979 (S.D.N.Y. 1992), which finds that the parties’ decision to elect the law involved was a sufficient relationship. We caution that our description of enforcement of choice-of-law clauses is intended for commercial contracts between sophisticated parties. Courts can decline to enforce choice-of-law clauses when doing so would violate public policy, and courts face additional public policy considerations in other types of contractual disputes, such as labor disputes, so the outcome is less certain.

Debt Contracts 1035

statutes allowing their law to be used for commercial contracts exceeding a min-imum dollar value (usually $250,000) regardless of whether the contract has any connection to the state.5 Many states also have corresponding statutes allowing parties to litigate in their state courts providing that the contract exceeds a min-imum dollar value (usually $1 million) and that the parties have selected the law of that state.6 Consequently, parties to substantial commercial contracts can now feel confident that their choice of law will be enforced.

There are four important reasons why parties to debt contracts may prefer the law of one state over another. First, and possibly most important, the law regard-ing debt contracts is more developed in some states than in others, which thereby reduces uncertainty with regard to enforcement of the contract. Second, the law of a state may be appealing because of its court system and the procedural rules regarding litigation. As noted, parties who select the law of a particular state may be allowed to litigate there even if the contract otherwise bears no relationship to the state. New York in particular is known for developing a court system that is friendly to commercial parties—especially to lenders (Eisenberg and Miller 2010). Third, the parties may prefer the law of a state because its legislature is par-ticularly responsive.7 Finally, there are differences in the substantive law across states that will affect the lender’s ability to enforce the contract. Substantive law refers to the law that governs the rights and duties of each party, and it includes both common law created by judges and statutory law enacted by legislators. For lenders, the issues of substantive law that will be most important are the state laws relating to lender liability and to the enforceability of specific contract pro-visions.

Lender liability is not one particular claim but is instead a compilation of many different state and federal claims. When reviewing the cases of lender liability during our sample period, we found that the vast majority of claims were based on the state law that governs contracts and torts (civil acts that are recognized as wrong and for which a claim is available) rather than on federal law. In the typical claim, the borrower faced financial difficulty, and the lender responded by tak-ing an action for which he had a contractual right—such as seizing the collateral

5 See, for example, N.Y. Gen. Oblig. Law sec. 5-1401; Cal. Civ. Code sec. 1646.5 (West 2009); Fla. Stat. Ann. sec. 685.101 (West 2009); Del. Code Ann., tit. 6, sec. 2708 (2000); Ohio Rev. Code Ann. sec. 2307.39 (West 2009); and Tex. Bus. & Com. Code Ann. sec. 35.51 (Vernon 2009).

6 See, for example, N.Y. Gen. Oblig. Law sec. 5-1402; Cal. Civ Proc. sec. 410.40; Fla. Stat. Ann. secs. 685.101–.102 (West 2009); Del. Code. Ann., tit. 6 sec. 2708 (2000); Ohio Rev. Code Ann. sec. 2307.39 (West 2009); Tex. Bus. & Com. Code Ann. sec. 35.51 (Vernon 2009); Ill. Comp. Stat. Ann. 105/5-1 (West Supp. 1998). New York was the first state to enact the complementary statutes allow-ing for court access and ensuring that choice-of-law clauses will be enforced, and the state did so in 1984 after a recommendation from the New York Bar Association (NYBA). The NYBA’s recom-mendation was thought to be motivated by self-interest because it provides more work for attorneys licensed in New York.

7 For example, after the introduction of the euro, there was concern that contracts requiring pay-ment in currencies that had been replaced by the euro would become invalid. In response, financial institutions pressured states to enact legislation that would mitigate this potential issue. Some states responded more quickly than others, and New York and Illinois were the first to enact the necessary legislation in this instance (Freis 1998).

1036 The Journal of LAW & ECONOMICS

or demanding immediate repayment without prior notice—that the borrower argued was overly aggressive given the circumstances. The borrower’s business usually suffered extreme difficulty following the lender’s actions, and the bor-rower then sued the lender, claiming that the lender’s actions violated the duty of good faith that is implicit in every commercial contract. The court then decided whether the lender violated the duty of good faith by taking the action in ques-tion and, if so, to what extent the lender had damaged the borrower.8

Lenders will also be concerned with prior legal rulings on the enforceability of

specific contract provisions. Courts have the right to void contract clauses they

deem to be unconscionable or against public policy, and this has resulted in dif-

ferent states treating the same clause differently. For example, lenders may seek

to include a contractual waiver of the duty of good faith in order to avoid poten-

tial liability. While state courts generally decline to enforce these waivers, courts

applying Illinois law have enforced them (Silver 2013). For further detail on dif-

ferences in the substantive law across states, see the Appendix.

2.2. The Association between Contract Law and Debt Contracts

Our first research question relates to the market for contracts and asks whether

there are systematic differences in debt contracts across states. Legal literature has

documented that states actively compete for contracts and that the law of some

states is used more frequently in commercial contracts than others (Eisenberg

and Miller 2010). However, no prior study has examined the characteristics of

borrowers, lenders, and contract terms across states. If a market for contracts ex-

ists, we would expect the states that compete most stringently for debt contracts

not only to have a disproportionate number of contracts but also to have at-

tracted the most informed investors and the largest deals regardless of their geo-

graphic location. While we cannot identify whether more pro-lender laws attract

more deals, we should observe a positive association between pro-lender regimes

and the market share of contracts if such a market exists.

Our second research question asks whether the contract terms vary with the

law governing the contract. Because the state contract law governs the enforce-

ment of the contract and the parties to the contract select the state law, it is likely

that the terms of the contracts will also vary with the state contract law. Cash

collateral is thought to provide lenders with greater control rights in the event

of default (Baird and Rasmussen 2006), so we start by examining the correlation

between the state contract law and the use of cash collateral. We then examine

the relationship between state contract law and the yield spread, where the yield

8 The most well-known lender liability case is K.M.C. Co. v. Irving Trust Co., 757 F.2d 752 (6th Cir. 1985). In this case, the lender refused to provide additional funds that were available under the borrower’s line of credit because the lender believed that the borrower posed a credit risk. When the borrower ultimately went out of business and sued the lender for violating the duty of good faith, the jury awarded the borrower $7,500,000. The case was unusual in finding the lender liable for tak-ing an action that was expressly permitted by the contract terms, and it sparked a flurry of litigation against lenders that created uncertain precedent in many states.

Debt Contracts 1037

spread is defined as the total amount paid by the borrower in fees and interest

over the London Interbank Offered Rate.Our third research question asks whether the frequency of financial covenant

violations varies with the law governing the contract. Assuming that the fre-quency of violations is related to the tightness of the covenants, the association between the legal environment and covenant violations is not clear ex ante. On the one hand, lenders may compensate for pro-debtor law by demanding tighter covenants. On the other hand, lenders who are sufficiently comfortable with their borrowers to allow pro-debtor law may also allow loose covenants. In addition, if lenders are better able to enforce the contract under pro-lender law, there may be fewer covenant violations because the borrowers are more reluctant to violate.

Our final research question examines whether the repercussions of covenant

violations vary with the law governing the contract. We do not have a clear pre-

diction on the direction of the association. All else equal, lenders exert more in-

fluence on the borrower when they have more power. As explained above, lend-

ers will have more negotiating power when they are better able to enforce the

contract, and enforcement can vary because of procedural differences in state

courts or substantive differences in state law. The states that are favorable to lend-

ers have clear rules allowing lenders wide discretion when enforcing their con-

tract rights, whereas the states that are less favorable to lenders have conflicting

precedent that can be worrisome.

All else equal, laws that are more pro-lender should result in more severe re-

percussions postviolation. However, different types of borrowers and lenders

may select into different legal regimes, and their actions may vary correspond-

ingly. For example, borrowers who are willing to select pro-lender law may know

that they pose little risk to the lenders, in which case we would not expect to see

severe repercussions when these borrowers violate a covenant. On the other

hand, borrower- lender pairs that select into more pro-lender laws could do so be-

cause the lenders want the extra protection of knowing that they can enforce the

contract as written without liability, in which case we would expect more severe

repercussions when the borrowers violate a covenant. Hence, the relationship be-

tween state contract law and the role of lenders postviolation remains an open

empirical question.

3. Data

3.1. Data Set Overview

Our main data set is from Nini, Smith, and Sufi (2009), which the authors kindly provide online.9 This data set contains information for 3,720 private debt contracts (that is, bank loans) that the authors obtained from the Securities and Exchange Commission’s EDGAR database of registered public company filings

9 Amir Sufi, Data and Appendices (http://faculty.chicagobooth.edu/amir.sufi/data.html).

1038 The Journal of LAW & ECONOMICS

using a text-search program.10 The authors provide the number and type of cov-enants, an indicator variable noting whether the firm violated a covenant in the prior year, and the relevant information necessary to match their data set with existing commercial databases. The authors also provide the contracts.

We reviewed these contracts and examined the governing law for each one. Af-ter discarding 31 contracts for which no statement of governing law is available—most of which state that the contract is to be governed in accordance with the law noted in the prior agreement, which we do not have—we have 3,689 contracts. Similar to Eisenberg and Miller (2009), we find that New York law is favored for debt contracts (51 percent). The next three most heavily favored states are Illinois, Texas, and California (8 percent, 8 percent, and 7 percent, respectively).

In addition, although the merged data set contains an indicator variable noting whether the borrower violated a financial covenant in the prior year, it does not specify the covenant that was violated. Thus, we hand checked all the violations to determine whether the borrower violated a covenant associated with a prior ver-sion of a contract in our data set that was renegotiated or a covenant associated with a contract that is not in our data set. This step was necessary because compa-nies do not always use the same law for each contract, and we needed to associate the violation with the respective governing law. We found that only 94 of the initial 232 violations were associated with the contract in question.11 For the 94 violations, we reviewed the original contract whenever possible and found that the renegotiated contract was governed by different law than the original contract in only two instances.

In order to obtain data on financial performance, we then merged this data set with the Compustat North America Fundamentals Quarterly database main-tained by Standard & Poor’s (S&P). This database includes quarterly account-ing reports for all public companies and descriptive information such as the company’s state of incorporation. During this merge, we lost one observation. As described below, our proxies include only those 10 states with 1 percent or more of the total number of contracts, which results in a total of 3,322 observations (roughly 90 percent of the initial sample). We use this data set for our descriptive statistics and our analyses of the frequency of violations and the changes in firm activity postviolation.12

This data set contains far fewer contracts in 1996, but the rest of the years, from 1997 to 2005, are fairly consistent. The most striking time trend of our contracts is that New York’s predominance increased during our time period. While 46

percent of our contracts used New York law in 1996, 70 percent of our contracts

10 Securities and Exchange Commission regulations require registered public companies to dis-close material contracts as exhibits to registration statements and periodic reports (17 C.F.R. 229.601[b][10]). Substantial loan contracts are considered material and must be disclosed.

11 In a limited number of instances, we were unable to determine the covenant violated. These ob-servations were dropped from our sample.

12 Although the full sample includes 3,322 observations, there are fewer observations in most analyses because we omit the observations that are missing relevant information from either Com-pustat or the original Nini, Smith, and Sufi (2009) data set.

Debt Contracts 1039

used it in 2005. This increase in use is consistent with New York’s well-known attempts to court commercial contracts (Eisenberg and Miller 2009). Meanwhile, the percentage of contracts using law from all our other 10 states—with the ex-ception of North Carolina, which increased from 1.8 percent to 2.5 percent— decreased.

Finally, for our regressions on contract terms, we further merge this data set with the Dealscan database maintained by Thomson Reuters. This database con-tains detailed deal terms, such as the loan maturity and deal size, for private loans and other financing agreements. Many of the contracts offer multiple facilities, where each facility is a separate term loan or line of credit, so we treat each facil-ity as a unique observation. This approach is feasible because Dealscan reports the different loan characteristics for each facility. The descriptive statistics for the contract terms include all available information, but the regressions exclude those observations that are missing necessary contract control variables such as the deal size, yield spread, or lender. We also drop 271 observations that are miss-ing complete firm-specific information from Compustat and 124 observations missing the number of financial covenants from the initial Nini, Smith, and Sufi (2009) data set. The final data set includes a total of 4,157 facilities, of which 3,880 use law from our 10 states. We use this data set for our analysis of yield spreads and cash collateral. Throughout the paper, all continuous, nonlog variables are winsorized at the 1st and 99th percentiles.

3.2. Classification of Contract Law

The first metric we use to classify contract law is the Pro-Debtor Index, which is an index of six features of state law that relate to the lender’s ability to enforce the contract. Prior literature has used an index based on state law to rank corpo-rate law (see, for example, Bebchuk and Cohen 2003). The specific practices and standards, which are shown Table 1, are drawn from legal literature and reflect the state court system, the lender’s ability to enforce the contract as written, and the uncertainty relating to lender liability. Each state receives a ranking of 1–3 for each feature. While the practices and standards used here are by no means the only differences between the laws of each state, we focus on the features that are mentioned most frequently in the legal literature.

Our second ranking scheme is based on the perceived risk of litigation for each state. To classify the states into three legal regimes, we reviewed the Cappello (2009) lender liability treatise and catalogued the number of lawsuits brought against lenders under each state’s law during our sample period 1996–2005.13 Al-though there are multiple theories for why parties choose to litigate rather than

13 As part of this process, we removed those lawsuits that were brought under only federal law. Under federal law, claims can be brought against lenders under a number of statutes, such as the Comprehensive Environmental Response, Compensation, and Liability Act, the Racketeer Influ-enced and Corrupt Organizations Act, or the bankruptcy code. For example, if a bankruptcy court finds that a creditor has engaged in conduct that provides him with an unfair advantage or that injures other creditors, the doctrine of equitable subordination allows the court to subordinate that creditor’s claim to those of other creditors (11 U.S.C. sec. 510[c][2000]).

Tab

le 1

Fea

ture

s o

f S

tate

Law

Use

d t

o C

om

pu

te P

ro-D

ebto

r In

dex

Va

lues

CA

FL

GA

ILM

AN

YN

CO

HP

AT

X

Do

es t

he

stat

e al

low

fo

r th

e en

forc

emen

t o

f p

red

isp

ute

ju

ry t

rial

wai

vers

?3

13

11

13

11

1D

oes

th

e st

ate

hav

e sp

ecia

lize

d b

usi

nes

s co

urt

s?2

11

11

11

31

3D

oes

th

e st

ate

reco

gniz

e th

e to

rt o

f d

eep

enin

g in

solv

ency

?2

22

22

12

23

1T

o w

hat

ext

ent

do

es t

he

stat

e en

forc

e w

aive

rs o

f le

nd

er li

abil

ity?

22

12

11

12

13

Do

es t

he

stat

e h

ave

stat

ute

s al

low

ing

cho

ice

of

law

an

d f

oru

m f

or

com

mer

cial

co

ntr

acts

of

a m

inim

um

do

llar

val

ue?

11

31

31

31

31

To

wh

at e

xten

t is

a le

nd

er r

equ

ired

to

act

in

go

od

fai

th w

hen

tak

ing

dis

cret

ion

ary

acti

on

s?2

11

12

11

11

2

T

ota

l12

811

81

06

11

10

10

11

No

te.

Bec

ause

th

e st

ate

law

may

ch

ange

ove

r ti

me,

th

e ra

nk

ing

for

each

sta

te i

s d

eter

min

ed a

s o

f D

ecem

ber

31,

200

5. 1

= r

elat

ivel

y fa

vora

ble

to

len

der

s, 2

= u

nce

rtai

n a

nd

/or

mix

ed, 3

= u

nfa

vora

ble

to

len

der

s.

Debt Contracts 1041

settle, the predominant theory is that litigation is driven by uncertainty (Priest and Klein 1984).14 When both parties think they will prevail, they have less incen-tive to settle. As such, we expect that there will be more litigation against lenders in states with greater uncertainty.

We thus follow prior literature in estimating litigation risk using an ex post approach based on the number of lawsuits (for example, Li et al. 2012; Heninger 2001; Francis, Philbrick, and Schipper 1994), and we calculate perceived litiga-tion risk as the number of reported lawsuits per state divided by the number of contracts per state. Each state is then categorized as pro-lender, intermediate, or pro-debtor. The pro-lender states are the three states with the lowest frequency of litigation, the intermediate states are those four states in the middle of the distri-bution, and the pro-debtor states are the three states with the highest frequency of litigation.

Both classifications are limited to those states with 1 percent or more of the total number of contracts because of concerns that the inclusion of all U.S. states would bias the rankings. Many of the features in our Pro-Debtor Index are based on common law, so the law will be uncertain in the state if there is no prior prec-edent. As such, the inclusion of all U.S. states would introduce noise into our in-dex because many of the states that are rarely used for debt contracts have sparse relevant law and thus cannot be ranked with certainty. The inclusion of all U.S. states would bias our litigation risk measure as well. Since many states have fewer than five contracts, there would be small-denominator problems that would in-flate the litigation measure. Using only those states with 1 percent or more of the total number of contracts leaves us with 10 states that make up roughly 90 per-cent of the original sample.

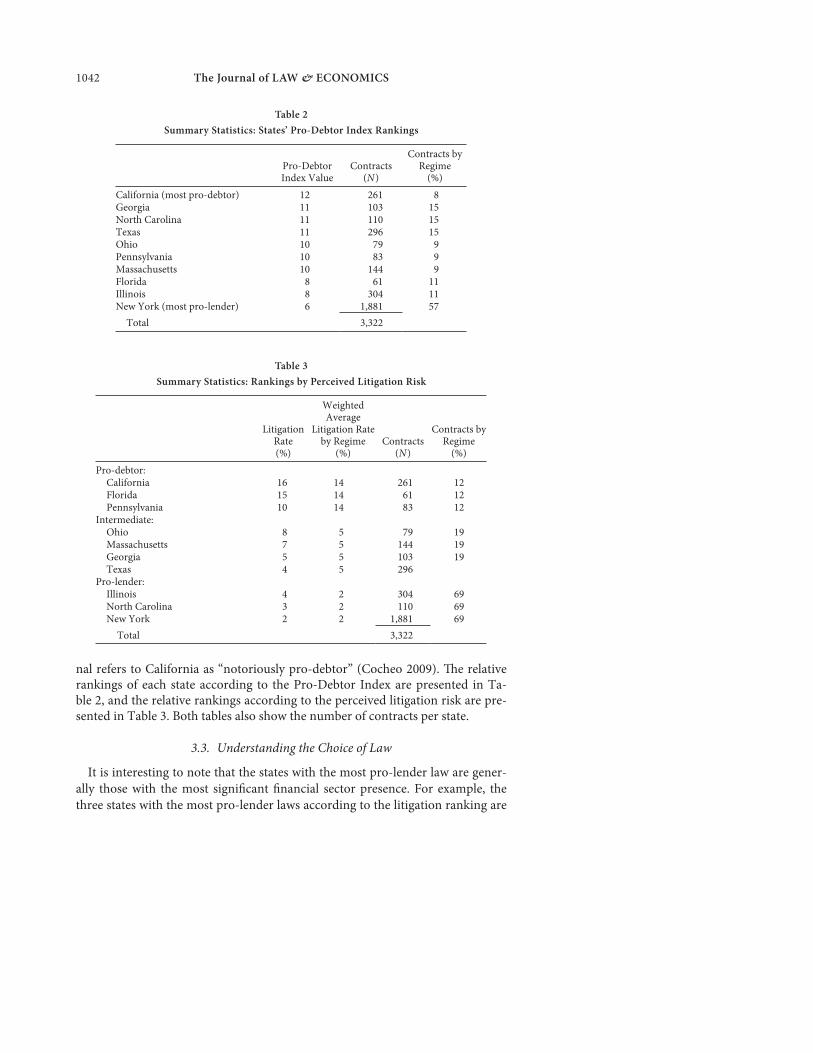

Under both classifications, California and New York are at the two extremes: California represents the most pro-debtor state and New York the most pro-lender. These rankings are consistent with the view of practitioners. For example, New York is known for being so favorable to lenders that one law firm advises lenders to select New York law as one of four suggested tactics to avoid lender li-ability.15 Conversely, an article posted by an American Bankers Association jour-

14 In general, common law in most states was traditionally pro-lender but became more pro-debtor following the wave of lender liability litigation in the late 1980s and early 1990s. However, the pro-debtor rulings of this era did not necessarily overrule the prior law but instead created seem-ingly contradictory precedent that created uncertainty, especially for lenders. For example, while all states allow a lender to demand repayment after the borrower violates a covenant, there are states with conflicting precedent as to what sort of notice, if any, the lender needs to provide to the bor-rower before demanding repayment. As such, a lender in these states is more likely to open itself to litigation because there is no clear rule for it to follow. We thus expect borrowers in these uncertain states to be more likely to sue the lenders because they have precedent on which they can rely, even if it seems to contradict other precedent in the same state, and we expect lenders to be less likely to settle the litigation out of court because they too have precedent on which they can rely.

15 “Some states are more liberal than others on lender liability. New York is a state that takes a stricter approach to enforcing the terms of the loan documents and the exercise of lender rights. Other states may be more lenient, particularly if the borrower is a ‘home town favorite’ while the lender comes from outside of the jurisdiction. What can lenders do to use more favorable law to increase their chances of defeating lender liability suits? . . . Choice of law provisions in loan docu-ments—or in loan modification documents—can be the answer” (Epstein 2010, p. 27).

1042 The Journal of LAW & ECONOMICS

nal refers to California as “notoriously pro-debtor” (Cocheo 2009). The relative rankings of each state according to the Pro-Debtor Index are presented in Ta-ble 2, and the relative rankings according to the perceived litigation risk are pre-sented in Table 3. Both tables also show the number of contracts per state.

3.3. Understanding the Choice of Law

It is interesting to note that the states with the most pro-lender law are gener-

ally those with the most significant financial sector presence. For example, the

three states with the most pro-lender laws according to the litigation ranking are

Table 2

Summary Statistics: States’ Pro-Debtor Index Rankings

Pro-Debtor Index Value

Contracts (N )

Contracts by Regime

(%)

California (most pro-debtor) 12 261 8Georgia 11 103 15North Carolina 11 110 15Texas 11 296 15Ohio 10 79 9Pennsylvania 10 83 9Massachusetts 10 144 9Florida 8 61 11Illinois 8 304 11New York (most pro-lender) 6 1,881 57

Total 3,322

Table 3

Summary Statistics: Rankings by Perceived Litigation Risk

Litigation Rate (%)

Weighted Average

Litigation Rate by Regime

(%)Contracts

(N )

Contracts by Regime

(%)

Pro-debtor: California 16 14 261 12 Florida 15 14 61 12 Pennsylvania 10 14 83 12Intermediate: Ohio 8 5 79 19 Massachusetts 7 5 144 19 Georgia 5 5 103 19 Texas 4 5 296Pro-lender: Illinois 4 2 304 69 North Carolina 3 2 110 69 New York 2 2 1,881 69

Total 3,322

Debt Contracts 1043

also the three of the four states in which the financial sector contributes most to

the state’s GDP.16 In contrast, the financial sector is not even a top-five industry

for any of the three states considered to be pro-debtor. Given that legislators can

make their law and/or courts more attractive to the financial sector by passing

statutes,17 it is important to consider that borrowers, lenders, and the states them-

selves self-select into legal regimes.

While states appear to self-select into regimes on the basis of their relationship

with the financial industry, lenders’ selection of law seems to be related to their

geographic presence. Specifically, it appears that local lenders use local law but

that multistate lenders use law from many states. For example, LaSalle Bank—a

smaller lender located in Chicago—uses Illinois law in 92 percent (46 out of 50) of

the loans for which it is the lead arranger, the primary lender responsible for the

structure and execution of the loan. In comparison, Bank of America, the most

frequent lead arranger in our sample, uses law from 24 different jurisdictions.

The choice of contract law for each lead arranger is shown in Table 4, but for con-

cision we present data only for those lead arrangers with 1 percent or more of the

full sample (by necessity this excludes some local lenders such as LaSalle Bank).

However, although there is variation in the choice of law, the most prolific mul-

tistate lead arrangers show a strong preference for New York law—the five most

common lead arrangers in our sample all use New York law more frequently than

the law of any other state. In total, they use New York law in over 70 percent of

their contracts; in comparison, arrangers in the full sample use New York law

in 51 percent of contracts.18 The five lead arrangers are Bank of America, Chase

Manhattan Bank, Citibank, JP Morgan Chase, and Wachovia Bank, and they use

New York law in 52 percent, 90 percent, 96 percent, 90 percent, and 52 percent of

their contracts, respectively.

16 State profiles created by Boston College (Center on Aging and Work at Boston College, State Contexts [http://www.bc.edu/research/agingandwork/projects/stateProfiles.html]) show that the four states in our sample in which the financial sector most contributes to the state’s gross domestic prod-uct are New York (14.6 percent), North Carolina (10.4 percent), Massachusetts (10 percent), and Illinois (9.2 percent). Although the profiles were published in 2008, the data on economic output by industry sector are based on 2005 data from the Bureau of Economic Analysis. The suggestion that states’ political pressures can affect contract outcomes is consistent with Cookson (2010).

17 As one such example, New York legislators made a procedural change that is specifically de-signed to expedite the litigation process for lenders suing borrowers. See N.Y. C.P.L.R. 3213 ( McKinney 2009): “When an action is based upon an instrument for the payment of money only or upon any judgment, the plaintiff may serve with the summons a notice of motion for summary judgment and the supporting papers in lieu of a complaint.” In addition, as noted, the financial sec-tor successfully lobbied several state legislatures to pass legislation following the introduction of the euro (Freis 1998). There are also many examples of legislators passing statutes to overrule the com-mon law. For example, attorneys’ fees are not recoverable under traditional American common law, but many states have enacted statutes allowing—or even requiring—the nonprevailing party to pay the attorneys’ fees for the other side and/or guiding the interpretation of contract clauses allowing for attorneys’ fees (see, for example, Cal. Civ. Code sec. 1717; Ariz. Rev. Stat. Ann. sec. 12-341.01 (2003); 735 ILCS 5/5-108). This type of legislative activity is so common that Saltzman (1985) notes that Illinois alone had 88 statutes related to attorneys’ fees.

18 This estimate differs from that of 57 percent in Table 2 because Table 2 is based on only the top 10 states.

Tab

le 4

Ch

oic

e o

f C

on

tra

ct L

aw b

y L

ead

Arr

ang

er

Pri

nci

pal

Pla

ce

of

Bu

sin

ess

Stat

e o

f In

corp

ora

tio

n

Lo

ans

Usi

ng

the

Co

ntr

act

Law

fro

m E

ach

Sta

te

Lea

d A

rran

ger

CA

FL

GA

ILM

AN

YN

CO

HP

AT

XO

ther

To

tal

Ban

k O

ne

Co

rp.

ILD

E4

424

65

81

21

10

13

7B

ank

of

Am

eric

aN

CD

E11

114

2698

12

49

73

92

92

74

96

5B

ank

of

New

Yo

rkN

YN

Y2

70

27

4B

ank

ers

Tru

st C

o.

NY

NY

11

64

16

7C

IBC

On

tari

oO

nta

rio

45

42

60

Ch

ase

Man

hat

tan

Ban

kN

YN

Y1

36

63

16

40

7C

itib

ank

NY

DE

11

24

24

91

12

59

Cre

dit

Su

isse

Fir

st B

ost

on

NY

DE

98

41

02

Fir

st U

nio

n N

atio

nal

Ban

kN

CN

C9

51

19

23

61

22

86

Fle

et N

atio

nal

Ban

kM

AM

A2

60

54

22

17

13

7G

ener

al E

lect

ric

Cap

ital

Co

rp.

CT

DE

44

75

42

89

JP M

org

anN

YD

E5

10

81

11

11

26

JP M

org

an C

has

eN

YD

E1

151

38

33

11

37

42

4L

ehm

an C

om

mer

cial

Pap

er, I

nc.

NY

NY

16

46

5M

org

an G

uar

anty

Tru

stN

YN

Y6

91

37

3N

atio

nsB

ank

NC

NC

317

101

45

20

22

42

11

43

PN

C B

ank

PA

PA

36

18

39

31

87

8Su

nT

rust

Ban

kG

AG

A6

263

56

47

7W

ach

ovi

a B

ank

NC

NC

15

394

11

11

32

24

87

21

4W

ells

Far

go B

ank

CA

SD28

22

81

12

14

85

No

te.

Lea

d a

rran

gers

wit

h 1

% o

r m

ore

of

the

tota

l sa

mp

le w

ith

ava

ilab

le d

ata

are

incl

ud

ed.

Bec

ause

nat

ion

al b

ank

s h

ave

no

sta

te o

f in

corp

ora

tio

n,

the

stat

e d

esig

nat

ed i

n a

n

atio

nal

ban

k’s

org

aniz

atio

n c

erti

fica

te i

s li

sted

. Th

e ar

ran

ger’

s lo

cati

on

is

det

erm

ined

as

of

its

fin

al d

ay o

f ex

iste

nce

or

Dec

emb

er 3

1, 2

005.

CIB

C =

Can

adia

n I

mp

eria

l B

ank

of

Co

mm

erce

.

Debt Contracts 1045

Given that the majority of borrower-lender pairs in our sample select New York law, we look at the pairs that select California law to understand what fac-tors influenced those pairs to pick law at the opposite end of the spectrum. We find that geography plays the most important role—66 percent of the borrowers consider California to be their primary place of business, and roughly 85 percent of the borrowers are based on the West Coast. In comparison, the contract law is the same as the borrower’s primary place of business in roughly 35 percent of the contracts for the full sample. Many of the lead arrangers have a geographic connection as well—38 percent of them consider California to be their primary place of business, and 39 percent are located on the West Coast. For the full sam-ple, the contract law is the same as the lead arranger’s primary place of business in roughly 32 percent of the contracts. We then reviewed the contracts for the borrower-lender pairs that did not have an obvious geographic connection to the West Coast, and we found that in many instances one or more lenders had an of-fice in California and/or the contract was signed in California.

3.4. Descriptive Statistics

Given that the selection of contract law is an active decision, we examine whether there are significant differences in contract and borrower characteristics across regimes. For brevity and to better show trends across legal regimes, we present our descriptive statistics on contracts and borrowers using only the clas-sification based on perceived litigation risk because this classification contains fewer groupings.

Table 5 provides descriptive statistics for contract characteristics across legal regimes and shows that many of the characteristics increase or decrease mono-tonically. For example, as we move from pro-debtor to pro-lender law, the num-ber of lenders, the loan maturity, and the deal size consistently increase across each regime. However, while loans using pro-lender law have fewer covenants and are less likely to be secured, these differences are not monotonic.19 Overall, Table 5 shows that the larger deals with more players select into pro-lender law. The self-selection observed here is consistent with the legal argument that there is a market for contracts and that states such as New York have succeeded in at-tracting the biggest deals.

Table 6 shows average borrower characteristics across legal regimes. As we move from pro-debtor to pro-lender law, we find that borrowers’ debt-to-asset

ratios, capital expenditures, and acquisitions increase, while their current ratios (a liquidity measure defined as current assets divided by current liabilities) de-crease. However, not all borrower characteristics increase or decrease monotoni-cally. For example, while the borrowers using pro-lender law are larger, the mean asset value is smallest for borrowers using intermediate law.

19 A limited number of borrowers in our data set have multiple contracts and use law from more than one state. We examine the contract characteristics of this limited data set in an untabulated analysis. While the results are qualitatively similar, statistical significance remains only for deal size and maturity.

1046

Tab

le 5

Un

ivar

iate

Tes

ts C

om

par

ing

Co

ntr

act

Ch

ara

cter

isti

cs a

cro

ss L

ega

l R

egim

es

Reg

ime

1: P

ro-L

end

erR

egim

e 2:

In

term

edia

teR

egim

e 3:

Pro

-Deb

tor

Fu

ll S

amp

leR

egim

e 1

— R

egim

e 3

NM

ean

Med

ian

NM

ean

Med

ian

NM

ean

Med

ian

NM

ean

Med

ian

t-V

alu

ez-

Val

ue

Dea

l Siz

e ($

mil

lio

ns)

2,97

434

818

567

813

470

442

132

50

4,0

94

28

91

50

9.4

4**

15

.36

**Y

ield

Sp

read

2,94

918

216

367

418

617

543

518

81

55

4,0

58

18

41

75

–.9

2-1

.11

Nu

mb

er o

f L

end

ers

2,09

211

.91

958

25.

794

379

5.17

33

,05

39

.90

71

1.4

5**

14

.44

**M

atu

rity

(m

on

ths)

2,94

648

.38

6066

641

.22

3643

139

.48

36

4,0

43

46

.25

48

7.6

0**

7.8

9**

Nu

mb

er o

f C

ove

nan

ts2,

869

2.62

367

02.

863

419

2.80

33

,95

82

.68

32

.77

**–

3.3

7**

Secu

riti

zed

2,55

9.6

71

555

.76

136

1.6

91

3,4

75

.69

1–

.46

–.4

6C

ash

Co

llat

eral

2,97

4.0

260

678

.029

044

2.0

290

4,0

94

.02

70

–.3

9–

.39

Co

ven

ant

Vio

lati

on

2,26

2.0

240

621

.034

040

5.0

350

3,2

88

.02

70

–1

.27

–1

.27

So

urc

e.

Val

ues

fo

r D

eal S

ize,

Yie

ld S

pre

ad, N

um

ber

of

Len

der

s, M

atu

rity

, Sec

uri

tize

d, a

nd

Cas

h C

oll

ater

al a

re f

rom

Dea

lsca

n; N

um

ber

of

Co

ven

ants

is f

rom

Am

ir S

ufi

, Dat

a an

d

Ap

pen

dic

es (

htt

p:/

/fac

ult

y.ch

icag

ob

oo

th.e

du

/am

ir.s

ufi

/dat

a.h

tml)

.N

ote

. Y

ield

Sp

read

is

bas

is p

oin

ts o

ver

the

Lo

nd

on

In

terb

ank

Off

ered

Rat

e. C

ove

nan

t V

iola

tio

n r

efer

s to

wh

eth

er t

he

bo

rro

wer

vio

late

d a

co

ven

ant

asso

ciat

ed w

ith

a c

on

trac

t in

th

e d

ata

set

du

rin

g th

e p

rio

r ye

ar.

The

stat

isti

cal

sign

ifica

nce

rep

rese

nti

ng

the

diff

eren

ce b

etw

een

th

e m

ean

an

d m

edia

n v

alu

es o

f re

gim

es 1

an

d 3

is

sho

wn

in

th

e fi

nal

tw

o

colu

mn

s.**

p <

.01.

1047

Tab

le 6

Un

ivar

iate

Tes

ts C

om

par

ing

Bo

rro

wer

Ch

ara

cter

isti

cs a

cro

ss L

ega

l R

egim

es

Reg

ime

1: P

ro-L

end

erR

egim

e 2:

In

term

edia

teR

egim

e 3:

Pro

-Deb

tor

Fu

ll S

amp

leR

egim

e 1

— R

egim

e 3

NM

ean

Med

ian

NM

ean

Med

ian

NM

ean

Med

ian

NM

ean

Med

ian

t-V

alu

ez-

Val

ue

To

tal A

sset

s ($

mil

lio

ns)

2,32

41,

709

1,16

963

670

133

841

379

63

14

3,3

73

1,4

07

76

61

2.3

5**

13

.70

**P

rop

erty

, Pla

nt,

an

d

Eq

uip

men

t ($

mil

lio

ns)

2,3

1644

432

363

623

310

941

220

06

63

,36

43

74

21

11

2.7

4**

13

.88

**C

apit

al E

xpen

dit

ure

s ($

mil

lio

ns)

2,2

6412

.03

4.92

609

7.82

3.59

405

7.43

3.0

63

,27

81

0.6

84

.22

4.9

9**

3.1

6**

Cu

rren

t R

atio

2,2

771.

911.

4962

62.

041.

6840

22.

211

.82

3,3

05

1.9

71

.49

–1

.50

–6

.12

**M

ark

et-t

o-B

oo

k2,

026

2.32

1.89

577

2.10

1.67

368

2.55

1.8

52

,97

12

.30

1.8

4–

.68

–.7

7L

ever

age

2,28

2.2

93.2

5862

1.2

55.2

3539

8.2

12.1

98

3,3

01

.27

6.2

58

7.7

2**

8.7

6**

Acq

uis

itio

ns/

Ass

ets t−

12,

156

.138

.004

959

8.1

13.0

006

389

.078

03

,14

3.1

26

.00

43

.32

**3

.34

**

Net

Wo

rth

/Ass

ets

2,2

87.6

13.4

7362

7.5

27.5

0140

8.5

57.5

30

3,3

22

.59

0.4

87

1.7

3+–

2.9

2**

Op

erat

ing

Cas

h F

low

/A

vera

ge A

sset

s2,

223

.035

.034

603

.039

.034

399

.033

.02

83

,22

5.0

36

.03

4.5

65

1.3

63

Inte

rest

Exp

ense

/ A

vera

ge A

sset

s2,

101

.006

.006

547

.005

.004

323

.005

.00

42

,97

1.0

06

.00

62

.42

*4

.12

**

No

te.

All

var

iab

les

are

fro

m C

om

pu

stat

an

d r

eflec

t th

e m

ost

rec

ent

fin

anci

al d

ata

that

wer

e p

ub

licl

y av

aila

ble

at

the

tim

e o

f th

e co

ntr

act.

Val

ues

are

rat

ios

un

less

in

dic

ated

o

ther

wis

e. Th

e st

atis

tica

l sig

nifi

can

ce r

epre

sen

tin

g th

e d

iffer

ence

bet

wee

n t

he

mea

n a

nd

med

ian

val

ues

of

regi

mes

1 a

nd

3 i

s sh

ow

n i

n t

he

fin

al t

wo

co

lum

ns.

+ p

< .1

0.

* p

< .0

5.

** p

< .0

1.

1048 The Journal of LAW & ECONOMICS

Given the previously noted importance of geography in selecting contract law,

we conducted additional untabulated analysis on borrowers who use the law of a

state other than their primary place of business. First, we estimated the descrip-

tive statistics in Tables 5 and 6 using only out-of-state borrowers and found that

the trends generally remain consistent or become stronger. Most noteworthy, the

mean yield spread across regimes, which is monotonic but not significant in our

initial analysis, becomes significant at 5 percent (t = –2.51). This suggests that any

differences in yield spreads are largely due to those borrowers who use out-of-

state law. Second, we compared the frequency of out-of-state borrowers by re-

gime. We found that the percentage of out-of-state borrowers increases mono-

tonically from an average of 33 percent in the states considered pro-debtor to

85 percent in the states considered pro-lender. In addition, the three states con-

sidered pro-lender according to our proxy based on litigation risk are also the

three with the highest percentage of out-of-state borrowers—87 percent, 76 per-

cent, and 80 percent of the borrowers in New York, Illinois, and North Carolina

are from out of state, respectively. Prior literature on corporate law measures the

competitiveness of each state’s law by that state’s ability to attract out-of-state

firms (for example, Barzuza and Smith 2013), so our analysis suggests that the

pro-lender states have more attractive law.

Overall, the data show that borrower-lender pairs have a general preference for

pro-lender law but that geography plays a large role in the selection of contract

law. The role of geography is particularly relevant for local lenders and borrow-

ers, which suggests that there are costs to using out-of-state law that are more

substantial for smaller parties with more limited geographic reach. For example,

a local borrower or lender may incur costs to become familiar with out-of-state

law and to find attorneys licensed to write such contracts. Borrowers and lenders

with greater geographic reach would presumably already be familiar with out-of-

state law and would have relationships with out-of-state attorneys. In addition,

some of the benefits of out-of-state law will be less attractive to local parties. Most

notably, a local borrower or lender would benefit less from access to the courts of

another state because it would incur additional travel expenses to litigate in that

state. While it could still benefit from the out-of-state law by having its local court

apply this law, there is a greater risk that the local court will be unfamiliar with

the foreign law and misinterpret it. In contrast, parties with greater geographic

reach would be less hampered by geography and would be able to enjoy the bene-

fits of out-of-state law at a lower cost.

4. Method and Empirical Results

4.1. Contract Terms

Because the state contract law governs the enforcement of the contract and the

parties to the contract select the state law, it is likely that the terms of the contract

will also vary with the state contract law. We examine two contract terms: the use

of cash collateral and the yield spread.

Debt Contracts 1049

We begin by examining the correlation between the state contract law and the use of cash collateral, and we find that contracts in states that are more pro-debtor are more likely to use cash collateral. We follow Ivashina (2009) and use borrower-, contract-, and lender-specific controls for both the use of cash collat-eral and the yield-spread regressions. The borrower-specific controls are whether the borrower’s short-term, subordinated, or long-term debt is rated by S&P, the natural logarithms of sales and assets in the quarter prior to loan origination, and the borrower’s leverage ratio and return on assets. The contract-specific con-trols are the natural logarithm of the dollar amount, the number of loans or lines of credit associated with the contract, whether the loan is secured, the number of financial covenants, whether the base rate is the prime rate, and whether the loan spread will be adjusted to reflect the borrower’s subsequent financial perfor-mance. The lender-specific controls include controls for both the lead arranger and the reputation of the whole group, or syndicate, of lenders. The controls for the lead arranger are whether the lead arranger has arranged other loans for the borrower in the previous 3 years, the lead arranger’s market share, the share of the loan retained by the lead arranger, and the lead arranger’s lending limit, which is defined as the 75th percentile of the dollar value of loans issued by the lead ar-ranger over the past 3 years. The reputation of the syndicate is measured by the frequency with which the lead arranger works with members of the syndicate and by whether the lead arranger and members of the syndicate have switched roles in the past 3 years.20 Finally, all models control for the probability of loss in the borrower’s two-digit Standard Industrial Classification (SIC) industry (as deter-

20 The control for whether the loan is secured is not included in the probit regressions that esti-mate the use of cash collateral. In addition, the variables for whether the loan is secured and for the percentage of the loan retained by the lead arranger are sparsely populated. Rather than include only the populated variables, which would decrease our sample from over 3,000 observations to fewer than 1,000 observations, we add a dummy variable that indicates whether the variable is available and interact the availability with the original variable. Finally, we note that the sources for our con-trol variables may differ slightly from those in Ivashina (2009).

Table 7

Cash Collateral and Legal Regime

Pro-Debtor Index Litigation Risk

Legal Regime .329**(.097)

.833*(.349)

Note. Values are the results from estimating the following probit model: Cash Collateral = α + β

1Legal Regime + Controls + Fixed

Effects. The dependent variable is a dummy variable set equal to one if the borrower employs cash collateral and zero otherwise. Higher values of the Legal Regime variables reflect more pro-debtor law. All models include borrower-, contract-, and lender-specific controls and fixed effects for the loan purpose, bank, industry, borrower’s long-term issuer credit rating, and fiscal quarter-year. All models also control for the probability of loss in the borrower’s industry. Standard errors, in parentheses, are clustered by firm and year. N = 510. * p < .05. ** p < .01.

1050 The Journal of LAW & ECONOMICS

mined by S&P) and include fixed effects for the quarter-year, bank, loan purpose, and the borrower’s industry (based on the borrower’s four-digit SIC code) and long-term issuer credit rating. The standard errors are clustered by firm and year.

Our results, presented in Table 7, confirm the suggestion in our univariate sta-tistics that cash collateral is used most frequently when contracts are governed by pro-debtor law.21 Although the differences across regimes are not statistically significant in Table 5, we note that the difference in significance for the probit regressions appears to be driven by the inclusion of quarter-year and industry fixed effects and that the results are only marginally affected by the inclusion of all other control variables. To ease interpretation and help assess the economic magnitude of the reported coefficients, we compute the marginal probability ef-fects of our variables of interest and provide the results here. The calculations indicate that a 1-unit increase in the Pro-Debtor Index, which ranges from 6 to 12, increases the probability that cash collateral will be used by 4.32 percent. For the litigation ranking, which ranges from 1 to 3, a 1-unit increase in the legal re-gime increases the probability that cash collateral will be used by 11.10 percent. It is interesting to note that cash collateral, which represents stronger protection for lenders, is used more frequently when the contract law is favorable to debtors.

Next we examine the association between the state contract law and the yield spread on the loan. We initially analyzed this relationship for the full sample and did not find a significant association. However, given the importance of geogra-phy in the selection of contract law, we expect that the association between con-tract law and yield spread may be stronger for those out-of-state borrowers who select the law of another state. For example, California law may not be priced for a local borrower-lender pair, but it may be priced for an out-of-state borrower who negotiates to use pro-debtor law. Indeed, untabulated univariate statistics using only out-of-state borrowers support this argument by showing that the yield spread increases monotonically as the law becomes more pro-debtor and that the difference between yield spreads for contracts using pro-lender and pro-debtor law is significant at 5 percent. As such, we conduct the analysis using out-of-state borrowers. The findings indicate that out-of-state borrowers are subject to higher yield spreads and that this result is driven by those out-of-state borrow-ers who use pro-debtor law.

Table 8 presents our findings. As shown in column 1, the coefficient on Out-of-State Borrower suggests that out-of-state borrowers pay an average of 7.26 ba-sis points more than in-state borrowers (t = 2.20).22 In comparison, untabulated univariate statistics show that out-of-state borrowers pay an average of 7.32 basis

21 Our probit regressions do not converge with the inclusion of both fiscal and calendar quarter- year fixed effects, so they are presented with fiscal quarter-year effects only. We also note that our finding that cash collateral is more likely to be used in pro-debtor regimes becomes stronger after article 9 of the Revised Uniform Commercial Code went into effect.

22 In an untabulated analysis, we follow Ivashina (2009) and included only the largest facility in terms of deal size for each package. This affects only Tables 7 and 8 because the other tables do not include Dealscan data. All of our results in Table 8 and for the Pro-Debtor Index in Table 7 remain consistent, but the statistical significance of the findings for litigation risk in Table 7 decreases in magnitude, and the z-statistic is reduced to 1.54 (p > .15).

Debt Contracts 1051

points more than in-state borrowers (significant at 10 percent). We also estimate the regression in column 1 of Table 8 using only fixed effects, and the resulting coefficient, 7.95, remains fairly consistent (significant at 10 percent). Overall, the magnitude of the reported coefficient for the full sample is fairly consistent, and increasing the number of controls, particularly contract controls such as deal size and collateral, generally increases the statistical significance.

We next test whether all out-of-state borrowers pay higher yield spreads or whether this finding is driven by borrowers who select into a particular regime. To do this, we run additional regressions on subsets of legal regimes so that we can compare the magnitude and significance of the coefficients for those borrow-ers who opt into pro-debtor or pro-lender regimes with the coefficient for the full sample. In columns 2 and 4, we analyze only those borrowers who opt into inter-mediate and/or pro-lender law. For these subsets, Out-of-State Borrower is no longer statistically significant. In columns 3 and 5, we analyze only those borrow-ers who opt into intermediate and/or pro-debtor law. For these subsets, Out-of-State Borrower increases in both statistical significance and economic magnitude. The out-of-state borrowers who opt into intermediate and/or pro-debtor law pay an additional 14.42–19.92 basis points (significant at 1 percent). To summarize, analysis of the subsets suggests that the higher yield spreads for out-of-state bor-rowers are driven by those who opt into favorable law.23 This finding is consistent

23 Because clustered standard errors may be too small—particularly when the number of clusters is small (Cheah 2009)—we estimate maximum likelihood multilevel models. Our findings in Table 8 remain consistent, and our findings in Table 10 are very similar (although the statistical signif-icance is reduced in some estimations). Although we also estimate multilevel models for Tables 7 and 9, these estimations do not converge. Prior literature notes that issues with convergence are a disadvantage associated with multilevel models (for example, Primo, Jacobsmeier, and Milyo 2007; Dedrick et al. 2009).

Table 8

All-in-Drawn Yield Spread and Legal Regime

Pro-Debtor Index Litigation Risk

FullSample

(1)

ExcludesPro-Debtor

(2)

ExcludesPro-Lender

(3)

ExcludesPro-Debtor

(4)

ExcludesPro-Lender

(5)

Out-of-State Borrower 7.26*(3.30)

4.71(3.13)

14.42**(4.22)

1.40(3.59)

19.92**(7.54)

N 3,880 3,625 1,528 3,478 1,058R2 .75 .76 .80 .77 .81

Note. Results are from estimating Yield Spread = α + β1Out-of-State Borrower + Controls + Fixed Effects.

The dependent variable is the all-in-drawn yield spread over London Interbank Offered Rate: it is defined in basis points and includes all fees and interest assuming that the borrower has drawn the full dollar value available under the loan. Out-of-State Borrower is a dummy variable set equal to one if the borrower uses law from a state other than its principal place of business and zero otherwise. Higher values reflect more pro-debtor law. All models include borrower-, contract-, and lender-specific controls and fixed effects for the loan purpose, bank, industry, borrower’s long-term issuer credit rating, and fiscal and calendar quarter-year. All models also control for the probability of loss in the borrower’s industry. Standard errors, in parentheses, are clustered by firm and year. * p < .05. ** p < .01.

1052 The Journal of LAW & ECONOMICS

with out-of-state borrowers who opt into pro-debtor law paying for the privilege of that law.24

4.2. Frequency of Violations

We next examine the frequency of covenant violations across legal regimes

and find that the frequency is highest when contracts are governed by pro-debtor

law. In our first model, we follow Nini, Smith, and Sufi (2012) and control for

the measures of operating performance that are most likely to be used in cove-

nants. These variables were presented in Table 4 and include the following: op-

erating cash flow scaled by lagged assets, interest expense scaled by lagged assets,

the leverage ratio (total debt divided by assets), the current ratio, the net worth

ratio (shareholders’ equity divided by assets), and the market-to-book ratio. Al-

though the market-to-book ratio is not as frequently used in financial covenants,

we follow Nini, Smith, and Sufi (2012) and control for it because it predicts many

future outcomes such as earnings and bankruptcy. We also include the 4- quarter

lag of each control variable and higher-order covenant controls (the second and

third power of each covenant control variable) and drop all observations for

which any of the current or lagged control variables are not available in the Com-

pustat Fundamentals Quarterly database. In our second model, we also control

for the number of covenants and the interaction between the legal regime and

the number of covenants. Both specifications are probit models in which the de-

pendent variable is a dummy that indicates whether a covenant associated with

that particular contract was violated in the prior year.25 Our models include fiscal

quarter-year and industry fixed effects, as measured by four-digit SIC codes, and

the standard errors are clustered by firm and year.

Our results, presented in Table 9, show that the frequency of covenant violations

differs significantly across regions; borrowers violate the least when contracts are

governed by pro-lender law. Before controlling for the number of covenants, the

coefficients on the violation dummies are .320 (z = 9.56) and .888 (z = 6.06) for

states ranked by the Pro-Debtor Index and perceived litgation risk, respectively.

We compute the marginal probability effects of these coefficients, and the results

are economically meaningful. Our calculations suggest that a 1-unit change in the

Pro-Debtor Index, which ranges from 6 to 12, increases the probability of violation

by 3.30 percent, and a 1-unit change in the litigation ranking, which ranges from 1

to 3, increases the probability of violation by 9.27 percent. After controlling for the

number of covenants, the coefficients increase to .439 (z = 2.49) and 1.652 (z = 2.57)

for the Pro-Debtor Index and perceived litgation risk, respectively. The marginal

24 In untabulated analyses, we test whether the nonlinearity found in Table 8 affects any of our other results. In particular, we partition the full-sample results in Tables 7, 9, and 10 both by sub-samples of legal regimes and by in-state and out-of-state borrowers. We do not find that the nonlin-earity found in Table 8 applies to any of the other analyses.

25 We are grateful to Mitchell A. Petersen for his cluster2.ado program (http://www.kellogg .northwestern.edu/faculty/petersen/htm/papers/se/cluster2.ado).

Debt Contracts 1053

effects of the legal regime also increase. A 1-unit change in the Pro-Debtor Index

increases the probability of violation by 4.25 percent, and a 1-unit change in the

litigation ranking increases the probability of violation by 16.4 percent. Although