stanford law school - university of colorado boulder

TRANSCRIPT

Stanford Law School

John M. Olin Program in Law and Economics

Working Paper 225

November 2001

INSTITUTIONAL SHAREHOLDERS’ SPLIT PERSONALITY ON CORPORATE GOVERNANCE: ACTIVE IN PROXIES, PASSIVE IN

IPOS (Forthcoming, Directorship Newsletter)

Michael Klausner

This paper can be downloaded without charge from the Social Science Research Network Electronic Paper Collection:

http://papers.ssrn.com/abstract=292083

and asks the question: Why do institutional investors passively accept takeover defenses among

the companies in which they invest through private equity funds? The article concludes with

some potential explanations but ultimately invites the institutions to provide the answer.

Institutional shareholder activism in voting proxies

The Investor Responsibility Research Center (IRRC) collects yearly data on the results of

proxy contests for a sample of approximately 2,000 firms. Table 1 reports IRRC data on

shareholder proposals (a) to repeal classified boards, and (b) either to redeem poison pills or to

require the adoption of a pill to be ratified by shareholders. When a firm has both a poison pill

and a classified board, it can ward off a hostile acquirer for up to two years. As Table 1 shows,

there has been substantial shareholder opposition to takeover defenses since the 1980s.

Moreover, the figures on the average votes in favor of these proposals reflect a large increase in

shareholder support between 1987 and the present. In 1987, the average vote in favor of

proposals opposing poison pills was 29.4 percent, and the vote in favor of proposals to declassify

boards was 16.4 percent. By the year 2000, both sets of votes averaged more than 50 percent.

2

Table 1 Poison Pill Shareholder

Proposals Classified Board Shareholder

Proposals

Year No. of proposals Average vote Year

No. of proposals Average vote

1987 32 29.4% 1987 22 16.4%1988 19 38.7% 1988 38 20.3%1989 20 41.5% 1989 50 21.8%1990 41 42.1% 1990 47 25.8%1991 40 44.8% 1991 42 28.3%1992 23 43.1% 1992 35 23.1%1993 18 44.3% 1993 34 31.9%1994 12 53.7% 1994 42 35.7%1995 10 45.2% 1995 65 39.1%1996 14 53.4% 1996 63 42.2%1997 18 54.9% 1997 42 43.8%1998 13 57.4% 1998 49 47.3%1999 27 61.9% 1999 63 47.3%

2000 24 57.8% 2000 54 52.7%

Source: Investor Responsibility Research Center

Shareholder opposition to takeover defenses appears as well in the IRRC data on

management attempts to adopt classified boards. The adoption of a classified board requires a

charter amendment, which requires a shareholder vote. Table 2 presents data on how many

companies in the IRRC sample proposed charter amendments to their shareholders. In 1986, the

management of 88 companies sought amendments. Between 1986 and 2000, the IRRC sample

doubled in size while the number of sample companies attempting to adopt a classified board

declined by about 90 percent. This decline reflects management realization that there is no point

3

in even asking shareholders to support a classified board. Indeed, of the ten sample firms that

attempted to classify their boards in 2000, management of six of them already held over 35

percent of their companies’ shares, and of the remaining four attempts, only one succeeded.

Table 2

Source: Investor Responsibility Research Center

Management Proposals on Classified Boards

Year # of proposals1986 88 1987 40 1988 26 1989 27 1990 26 1991 12 1992 5 1993 4 1994 5 1995 7 1996 8 1997 13 1998 13 1999 21 2000 10

Other IRRC data confirms that institutional shareholders have led and continue to lead

the charge against takeover defenses. Their opposition appears explicitly in their internal

guidelines for proxy voting. In addition, the Institutional Shareholder Services’ Proxy Voting

Manual, which both advises subscribing institutions on how to vote their proxies and reflects

commonly held positions among institutional shareholders, advises as follows:

• Vote against staggered board proposals by management.

• Vote for shareholder proposals asking that a company submit its poison pill to

shareholder ratification.

4

In short, institutional shareholders strongly oppose corporate governance structures that allow

management to thwart a takeover bid.

Economists have studied the effects of anti-takeover charter provisions, and for the most

part their research supports institutional shareholders’ concerns. These studies show that (a)

share prices tend to drop when a firm adopts an anti-takeover charter amendment; (b) firms that

have adopted such an amendment receive fewer takeover bids than other firms—and the bids

they do receive do not provide higher premiums than do the bids made for other firms; and (c)

following the adoption of one of these provisions, management compensation tends to rise more

than compensation at comparable firms without takeover protection in their charters. A

potentially important caveat, however, is that these studies are based on data from no later than

1990.

In addition to fighting anti-takeover charter provisions, institutional shareholders have

also affirmatively advocated the adoption of charter provisions establishing governance

structures that they believe benefit shareholders. Examples include provisions mandating

independent boards, certain independent board committees (e.g., nominating and compensation

committees), separation in the positions of CEO and chairman and confidential voting. Although

shareholder proposals seeking such charter provisions command substantial votes in their favor,

they do not receive as many votes as those seeking to make firms more takeover-friendly, nor are

they as numerous as shareholder proposals to dismantle takeover defenses.

Institutional shareholder passivity as firms go public

The activist posture of institutional shareholders changes dramatically when one looks at

their involvement in private companies whose shares they indirectly own through private equity

funds. Institutional investors, including those that are the most active on corporate governance

5

issues, are major investors in private equity funds. Private equity fund managers are actively

engaged in the management of their portfolio companies and in the many decisions surrounding

the initial public offering of a portfolio company. One would expect, therefore, that institutions

are well positioned to influence the governance structures of those companies. When one

examines the charters of companies that private equity firms take public, however, one finds

numerous companies with staggered boards and one does not find any restriction on the use of

poison pills. In addition, many of these companies prohibit shareholders from voting by written

consent or calling a special meeting. The impact of these restrictions is to force shareholders to

wait for a company’s next annual meeting before attempting to replace its board of directors and

thereby allow a takeover attempt to succeed. Finally, there is a complete absence in these

charters of provisions that provide for a non-CEO chairman, an independent board, or any of the

other governance arrangements that institutional shareholders seek through proxy battles.

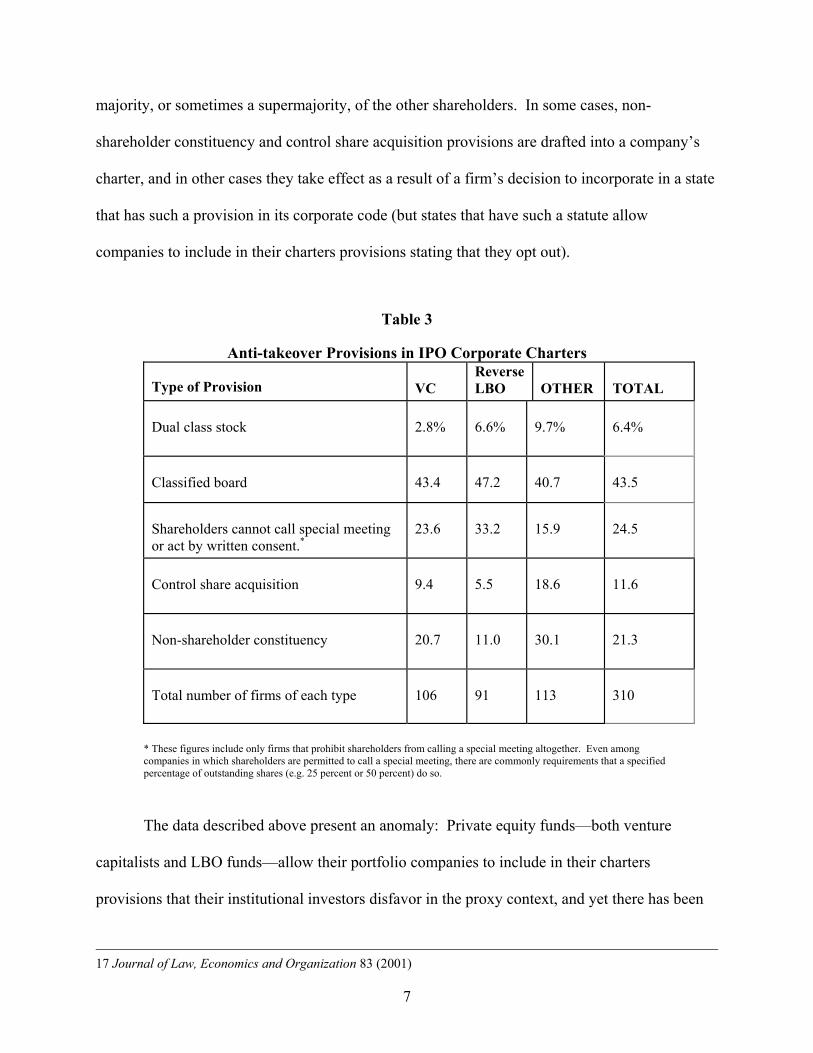

Professor Robert Daines of New York University Law School and I have recently

published a study of anti-takeover provisions in corporate charters as of the time companies go

public.1 Our study is based on a random sample of 310 firms that went public between January

1994 and June 1997. Table 3 presents some of our basic findings. In addition to the charter

provisions described above, Table 3 presents data on the adoption of two other defenses that can

be significant as well. A non-shareholder constituency provisions allows the board to consider

the interests of parties other than shareholders (e.g., employees, customers) in managing the

company generally and in responding to a takeover bid in particular. A control share acquisition

provision suspends the voting rights of a shareholder that acquires a block of shares above a

specified threshold. That shareholder’s voting rights are reinstated only upon the approval of a

6

1 Robert Daines & Michael Klausner, “Do IPO Charters Maximize Firm Value? Antitakeover Protection in IPOs,”

majority, or sometimes a supermajority, of the other shareholders. In some cases, non-

shareholder constituency and control share acquisition provisions are drafted into a company’s

charter, and in other cases they take effect as a result of a firm’s decision to incorporate in a state

that has such a provision in its corporate code (but states that have such a statute allow

companies to include in their charters provisions stating that they opt out).

Table 3

Anti-takeover Provisions in IPO Corporate Charters Type of Provision

VC

ReverseLBO

OTHER

TOTAL

Dual class stock

2.8%

6.6%

9.7%

6.4%

Classified board

43.4

47.2

40.7

43.5

Shareholders cannot call special meeting or act by written consent.*

23.6

33.2

15.9

24.5

Control share acquisition

9.4

5.5

18.6

11.6

Non-shareholder constituency

20.7

11.0

30.1

21.3

Total number of firms of each type

106

91

113

310

* These figures include only firms that prohibit shareholders from calling a special meeting altogether. Even among companies in which shareholders are permitted to call a special meeting, there are commonly requirements that a specified percentage of outstanding shares (e.g. 25 percent or 50 percent) do so.

The data described above present an anomaly: Private equity funds—both venture

capitalists and LBO funds—allow their portfolio companies to include in their charters

provisions that their institutional investors disfavor in the proxy context, and yet there has been

7

17 Journal of Law, Economics and Organization 83 (2001)

no objection to date on the part of those investors. I base this statement on discussions I have

had with many institutional investors and private equity fund managers and an off-the-record

meeting of institutional shareholders and venture capitalists. At that meeting participants

uniformly reported that they were unaware of the issue. Since that meeting, at which I

distributed a draft of this article, some institutions have raised the issue with private equity fund

managers.

One potential explanation for our findings is that when management of a public company

attempts to adopt a takeover defense, it tends to do so for purposes of entrenching itself, but that

when a firm backed with private equity investment adopts the same defenses there may be reason

to expect the defense to be used to benefit shareholders. Two such benefits are well recognized

by academics as well as by business and legal practitioners (Directorship, February 1998). First,

takeover defenses may be used to gain leverage over a hostile bidder in order to obtain a higher

bid. Second, if the price of a firm’s shares does not reflect the firm’s true long-term value,

takeover defenses may be needed to allow management to manage the firm efficiently for the

long run. Daines and I investigated these potential explanations statistically and found that

neither explains the data. To the contrary, we found that firms with defenses tended to be firms

that needed bargaining power least, because they were in industries with relatively numerous

potential bidders, and their shares were least likely to be mispriced because they tended to be

relatively low tech, with relatively small R&D expenditures.

We are thus left with a puzzle. Why do institutional investors passively accept takeover

defenses among the companies in which they invest through private equity funds?

8

Possible explanations

Two fairly mundane potential explanations come initially to mind for institutional

investors’ split personalities. First, institutional investors may be unaware of the fact that

takeover defenses are present in the charters of portfolio companies going public. Second, the

staffs of institutional investors are divided along functional lines, with some specialized in

placing investments in private equity funds and others specialized in proxy battles. Perhaps the

investment specialists have no interest in exerting influence over private equity fund managers

with respect to governance provisions in the charters of their portfolio companies. (One proxy

battler with an institutional investor reflected this divided turf when she said “Firms better adopt

these provisions at the IPO stage because we sure won’t let them do it later!”) These

explanations are plausible, if somewhat unsatisfying. How could institutions be unaware of

takeover defenses in IPO charters for so long? And why would top managers of institutions

support proxy battles but allow their private equity specialists to ignore the terms of those

battles? Furthermore, leaving aside the silence of the institutions, why do private equity funds

themselves accept these charter provisions?

Another potential explanation is that even if takeover defenses are detrimental to

shareholder interests, the public equity markets may not price these provisions when a company

adopts them at the IPO stage. Consequently, one might expect shareholders of companies going

public to be indifferent to the presence of takeover defenses. This explanation is problematic for

a number of reasons. For one, why would the securities market ignore an aspect of a company

that reduces its value? Second, studies have generally found that the market does price takeover

defenses when a firm adopts them by charter amendment or when a state adopts them by

legislation, so why wouldn’t the market price them at the IPO stage? Third, even if one would

9

expect IPO pricing to be less than perfect and to ignore the presence of takeover defenses in an

issuer’s charter, private equity funds must hold their shares in an issuer for at least six months

following an IPO, at which point they typically distribute the shares to their investors.

Therefore, if mispricing renders institutions indifferent to an issuer’s takeover defenses, it

must be the case that the mispricing occurs not only in the IPO market but also in the secondary

market. But, again, why would the market react to a charter amendment that adds a takeover

defense to a firm’s charter but not to a defense that is there from the start? Finally, even if

institutions intend quickly to sell the shares of firms they initially own through private equity

funds, and even if the market does not price takeover defenses for six months following the IPO,

these institutions may acquire those shares some time in the future, at which point their proxy

department will presumably go to work trying to dismantle the defenses. Surely, the institutions

would have preferred to have the work done for them at the outset.

A fourth potential explanation is that takeover defenses may be harmless and that the

institutional proxy battlers are misguided in their concerns—or at least that they were during the

mid- to late-1990s, the period covered by Daines’ and my sample. No academic study has tested

this hypothesis, and since charter amendments were rare during that period, it would be difficult

to do so.

A final potential explanation for Daines’ and my findings is that perhaps private equity

firms insist on allowing management to adopt takeover defenses at the time of the IPO in order

to develop a reputation for being friendly to successful managers. The funds may have an

implicit understanding with the managers of their portfolio companies that they will adopt a

hands-off approach once a company is successful enough to go public. Two colleagues at

Stanford Law School, Bernie Black and Ron Gilson, have elaborated this possibility, which is

consistent with their view that venture capitalists have an implicit contract with entrepreneurs to

10

return control to them (by having them go public) if they succeed. Even if takeover defenses

reduce share value, private equity funds would be acting rationally in making this implicit deal if

doing so attracts investment opportunities in the future. If this is what is going on, the losers are

the funds’ institutional investors—even if the funds themselves succeed in this tactic.

Institutional investors can spread their investment among many private equity funds and

therefore have little stake in competition among funds for attractive companies in which to

invest. To the extent inter-fund competition leads funds to offer portfolio companies value-

reducing takeover defenses, this competition results in a divergence in the interests of fund

managers and fund investors.

This explanation may well account for the behavior of private equity fund managers. It

does not explain, however, why institutional investors that assume such activist postures in the

proxy battle context have passively stood by as fund managers have engaged in intramural

competition apparently at their expense. Are they aware of their apparently contradictory

behavior? Is shareholder activism the province of their professional proxy battlers alone? Does

the apparent indifference of colleagues responsible for private equity investment indicate a lack

of commitment, or perhaps doubt, among the institutions’ senior management to the proxy

batters’ governance goals?

____

11