standardized measurement approach for operational risk...

TRANSCRIPT

Standardized Measurement Approach for Operational RiskConsultative proposals

Caio Ferreira

Monetary and Capital Markets DepartmentInternational Monetary Fund

October 20, 2016

2016 Seminar for Senior Bank Supervisors from Emerging Economies

2

Outline

Current approaches

Operational Risk Proxy

Use of Internal loss data

Capital Charge

3

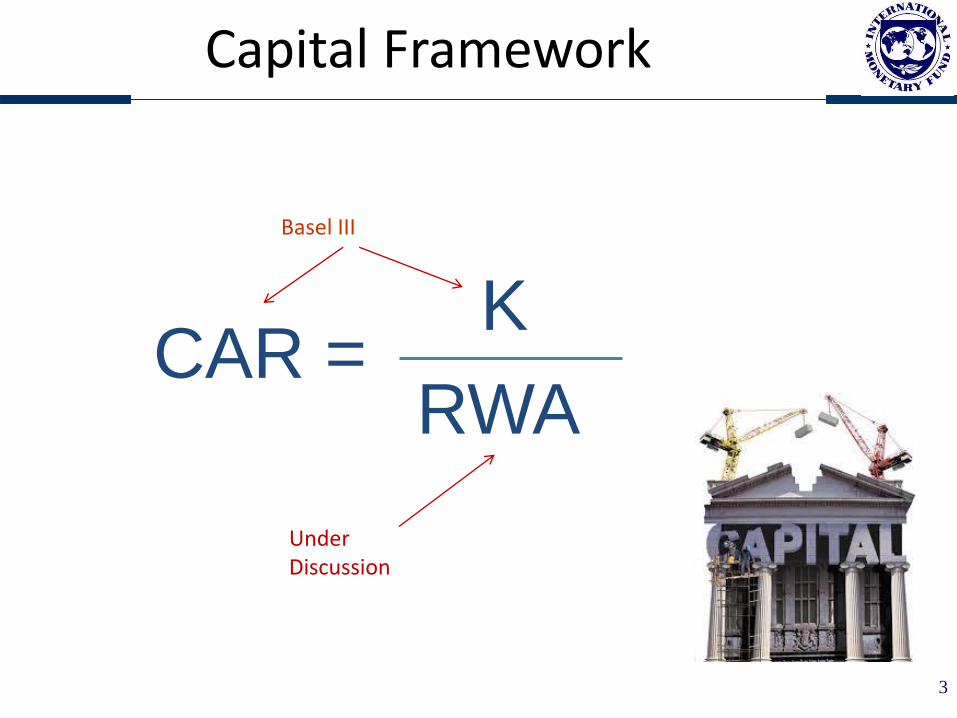

Capital Framework

K

RWACAR =

Basel III

Under Discussion

4

Changing Landscape

Pillar 1

Charges

Credit risk

Market risk

Operational risk

FIRB

AIRB

Internal Models

Standardized

Cred. Standardized

IMM Market Standardized

BIA

TSA / ASAAMA

5

Op. Risk Current Approaches

BIA

K= GI x 0,15

TSA

AMA

6

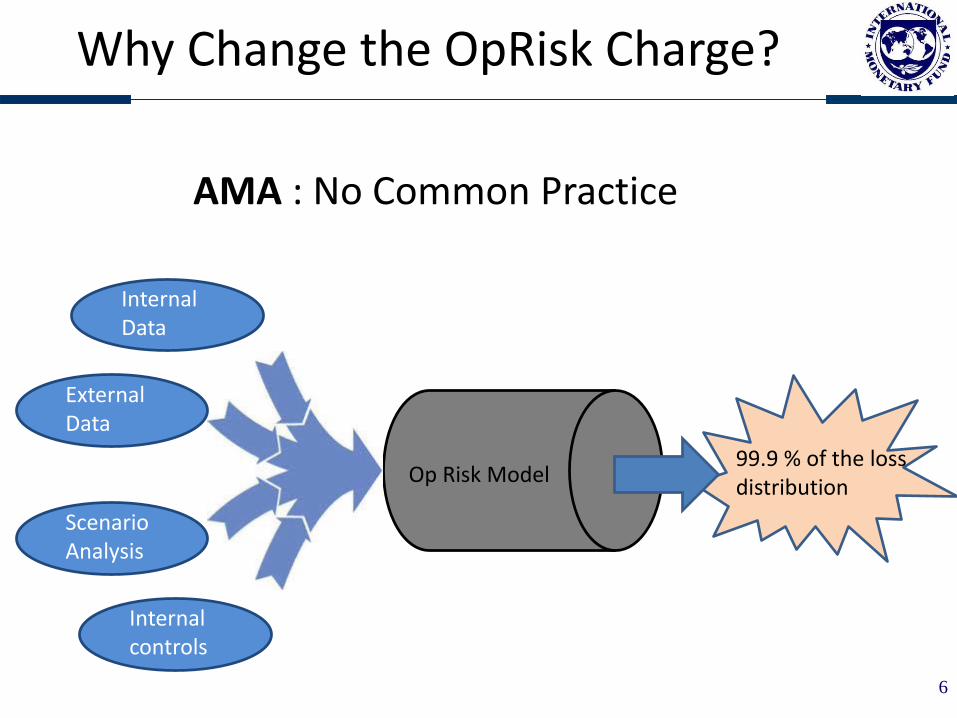

Why Change the OpRisk Charge?

Op Risk Model

Internal Data

99.9 % of the loss distribution

External Data

Scenario Analysis

Internal controls

AMA : No Common Practice

7

Why Change the OpRisk Charge?

Standardized• Not risk sensitive• Counterintuitive results• Bad proxy (gross income)

8

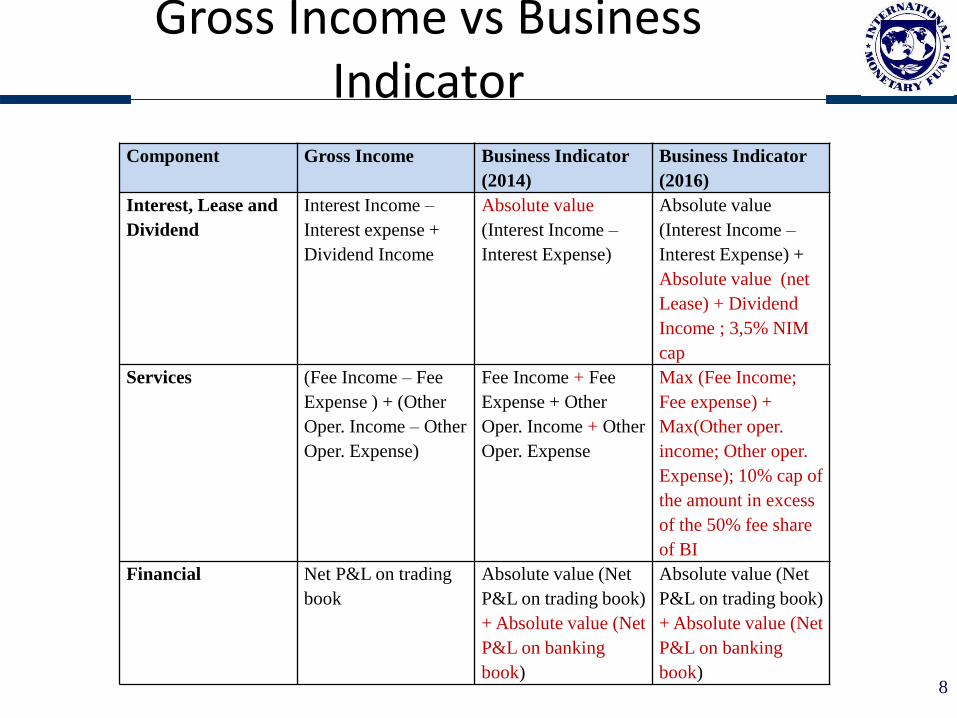

Gross Income vs Business Indicator

Component Gross Income Business Indicator

(2014)

Business Indicator

(2016)

Interest, Lease and

Dividend

Interest Income –

Interest expense +

Dividend Income

Absolute value

(Interest Income –

Interest Expense)

Absolute value

(Interest Income –

Interest Expense) +

Absolute value (net

Lease) + Dividend

Income ; 3,5% NIM

cap

Services (Fee Income – Fee

Expense ) + (Other

Oper. Income – Other

Oper. Expense)

Fee Income + Fee

Expense + Other

Oper. Income + Other

Oper. Expense

Max (Fee Income;

Fee expense) +

Max(Other oper.

income; Other oper.

Expense); 10% cap of

the amount in excess

of the 50% fee share

of BI

Financial Net P&L on trading

book

Absolute value (Net

P&L on trading book)

+ Absolute value (Net

P&L on banking

book)

Absolute value (Net

P&L on trading book)

+ Absolute value (Net

P&L on banking

book)

9

Gross Income vs Business Indicator

Problems:• Impact on certain business models (e.g.

originate to distribute);- Solution: Max (Fee income; Fee Expenses)

• Overcapitalization of banks with high NIM;- Solution: NIM cap set to 3.5%

• Inconsistency in the “dividend income”;- Solution: include dividend income

10

Gross Income vs Business Indicator

Problems:• Overcapitalization of banks with high fee

revenues;- Solution: adjust the BI for banks with high share of

fees. Account for only 10% of the fees above threshold

• Leasing- Include explicitly leasing income and leasing expense

11

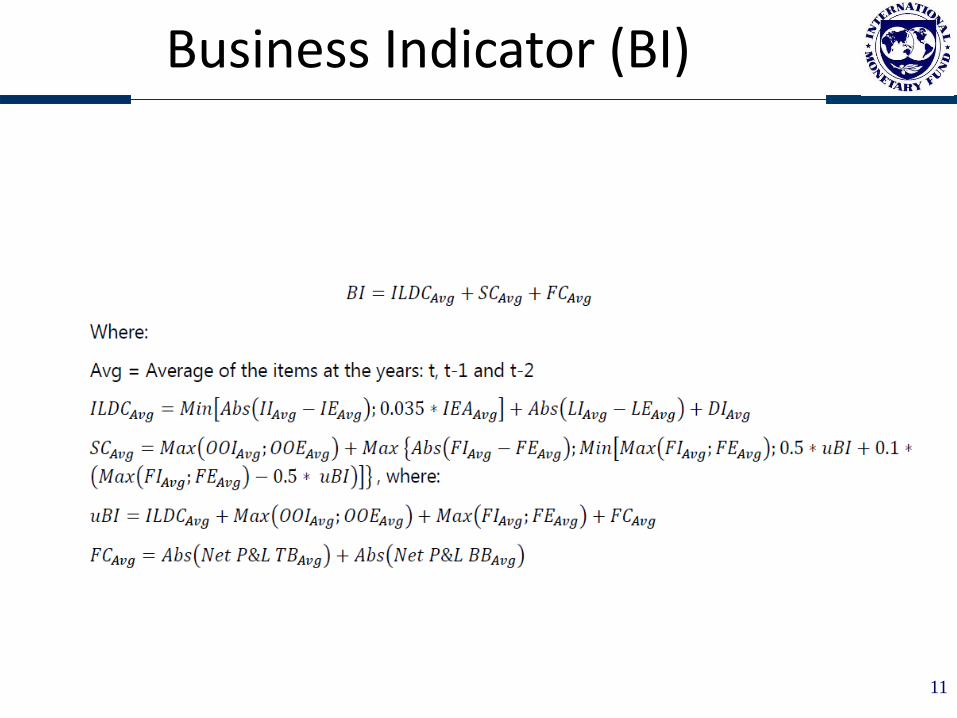

Business Indicator (BI)

12

BI Component

Operational Risk is non linear on BI

13

Loss Multiplier

Attempt to increase risk sensitivity

Loss Component= 7* Average Total Annual Loss+

7* Average Total Annual loss events above € 10 million+5* Average Total Annual Loss events above € 100 million

Average bank: Loss Component = BI

14

Loss Multiplier

0

0.5

1

1.5

2

2.5

3

0 2 4 6 8 10 12

Loss Multiplier

Loss / BI

15

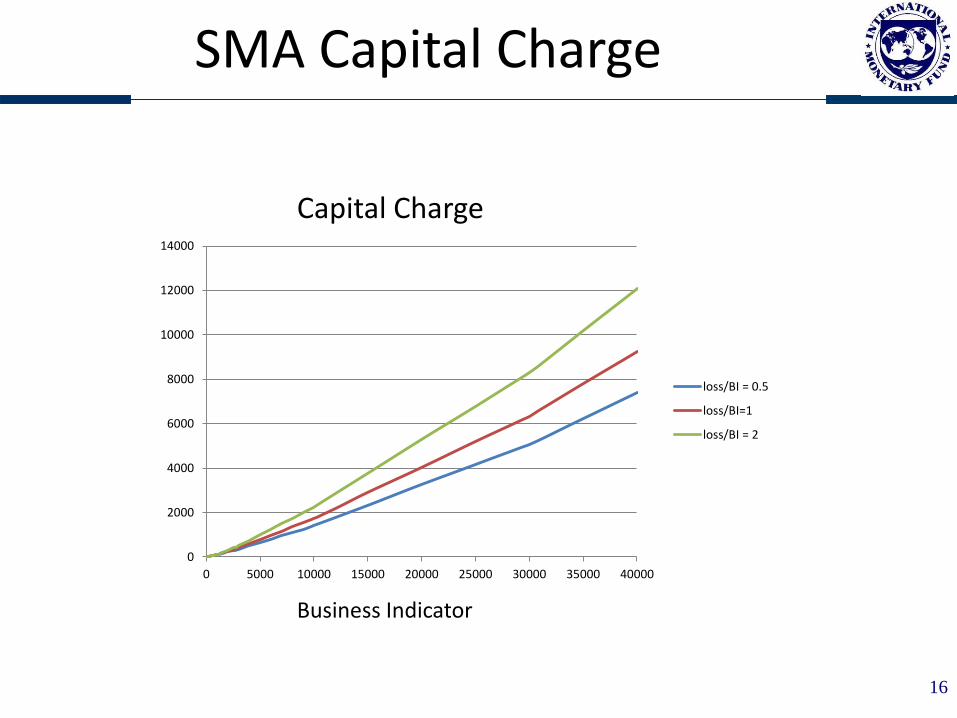

SMA Capital Charge

BI Component ; if bucket 1

SMA Capital =

110 Mln +(BI component – 110 Mln) * lossmultip ;

if bucket 2 – 5.

16

SMA Capital Charge

0

2000

4000

6000

8000

10000

12000

14000

0 5000 10000 15000 20000 25000 30000 35000 40000

loss/BI = 0.5

loss/BI=1

loss/BI = 2

Capital Charge

Business Indicator

17

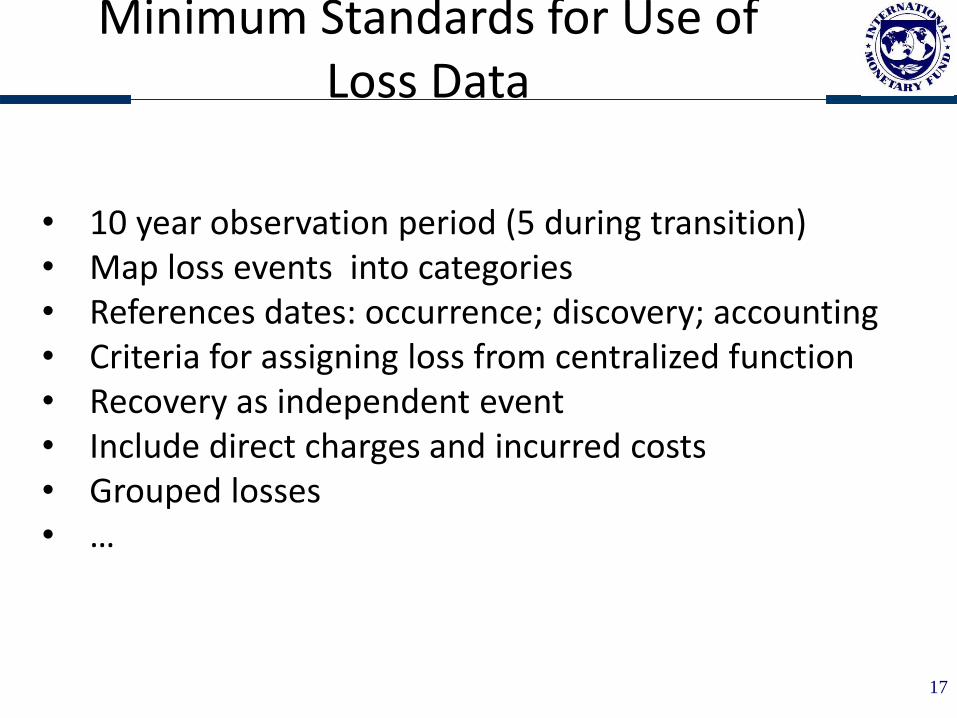

Minimum Standards for Use of Loss Data

• 10 year observation period (5 during transition)• Map loss events into categories• References dates: occurrence; discovery; accounting• Criteria for assigning loss from centralized function• Recovery as independent event• Include direct charges and incurred costs• Grouped losses• …

18

Impact

On going calibration• Goal: no overall material increase• Banks on lower buckets likely to have reduction

19

Question for Discussion

• Should the new OpRisk Capital Charge be a priority for EM?

Thank you

2016 Seminar for Senior Bank Supervisors from Emerging Economies