st. edward’s university gift acceptance policies and

TRANSCRIPT

St. Edward’s University Gift Acceptance Policies

and Procedures

Revised: May 2012 Approved by Board of Trustees May 10, 2012

2

TABLE OF CONTENTS INTRODUCTION………………………………………………………………………………… 4 PURPOSE AND RESPONSIBILITY ………………………………………………………….. 4 GENERAL POLICIES …………………………………………………………………………... 5 ACCEPTANCE POLICIES AND PROCEDURES BY TYPE OF GIFT ASSET …………... 8

OUTRIGHT ……………………………………………………………………………………... 9 I. Cash and Cash Equivalents II. Third-Party/Assignment of Interest

III. Matching Gifts IV. Marketable Securities V. Closely Held Securities

VI. Mutual Funds VII. Life Insurance

VIII. Retirement Plan /IRA Distributions IX. Real Property and Mineral Interests X. Tangible and Intangible Personal Property

XI. Gifts-in-Kind SPLIT-INTEREST GIFTS ……………………………………………………………………….. 35

I. Charitable Gift Annuities II. Charitable Remainder Trusts

III. Charitable Lead Trusts IV. Pooled Income Fund

DEFERRED ……………………………………………………………………………………. 46 I. Bequest Expectancies II. Life Insurance Beneficiary Designations

III. Retirement Plans/IRA Beneficiary Designations IV. Retained Life Estate Agreements V. Payable-On-Death/Transfer-On-Death Forms

PLEDGES ……………………………………………………………………………………… 58 Pledge Receivables Statements of Intent Annual Fund Pledges Pledge Write-off Policy

GIFTS WITH ASSOCIATED BENEFITS …………………………………………………….. 62 ENDOWMENTS ………………………………………………………………………………… 66 RESTRICTIONS ON GIFTS …………………………………………………………………… 68 GIFT ACKNOWLEDGEMENT AND STEWARDSHIP ………………………………………. 69 NAMING POLICY ………………………………………………………………………………. 71 GIFT REFUNDING POLICY …………………………………………………………………... 75 AMENDMENTS TO POLICY ………………………………………………………………….. 76 APPENDIX ………………………………………………………………………………………. 77

Other Guidelines and Policies Donor Bill of Rights Club, Organization, Department or Team Fundraising Policy and Guidelines Commemorative Plaque and Naming Policy

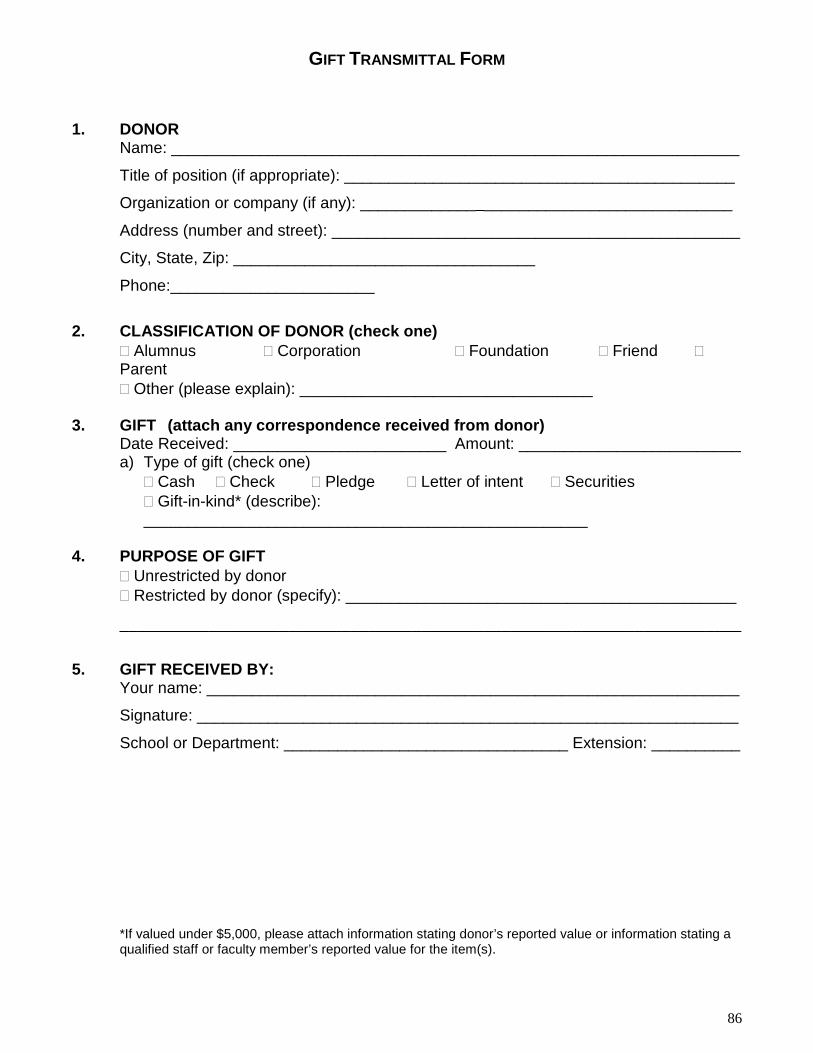

Environmental Assessment Gift Transmittal Forms Gift Transmittal Form

Currency Acceptance Form Donor Letter of Transfer

3

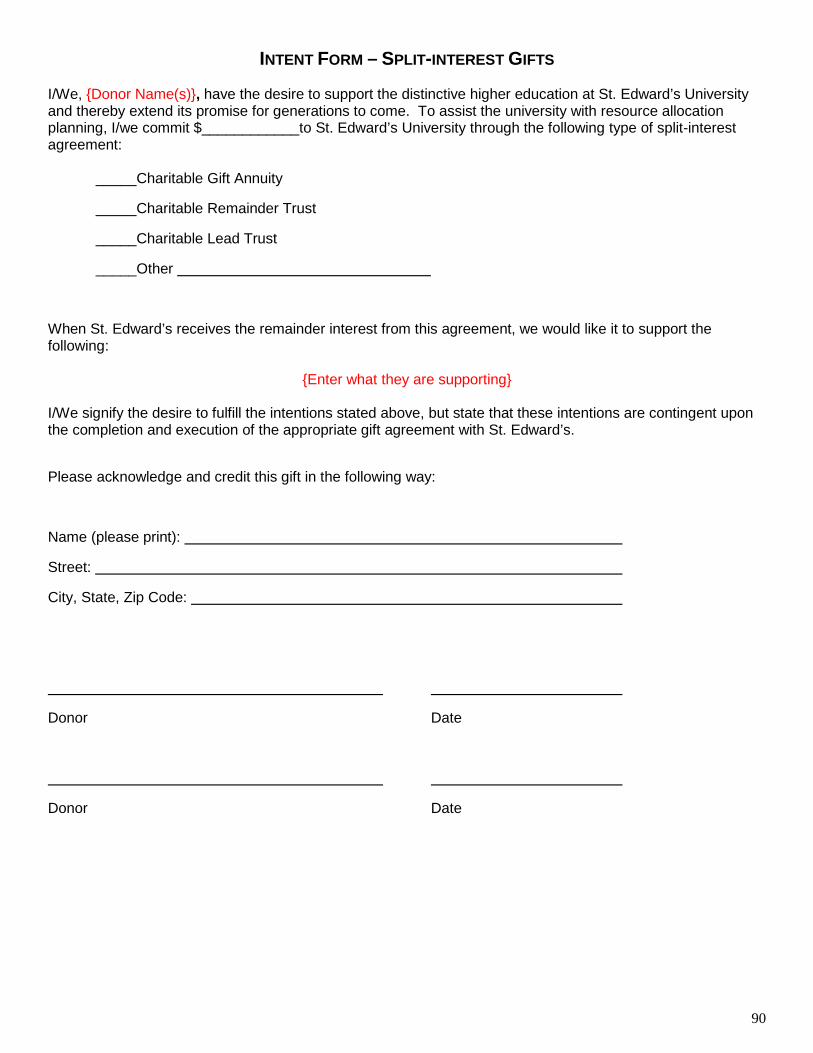

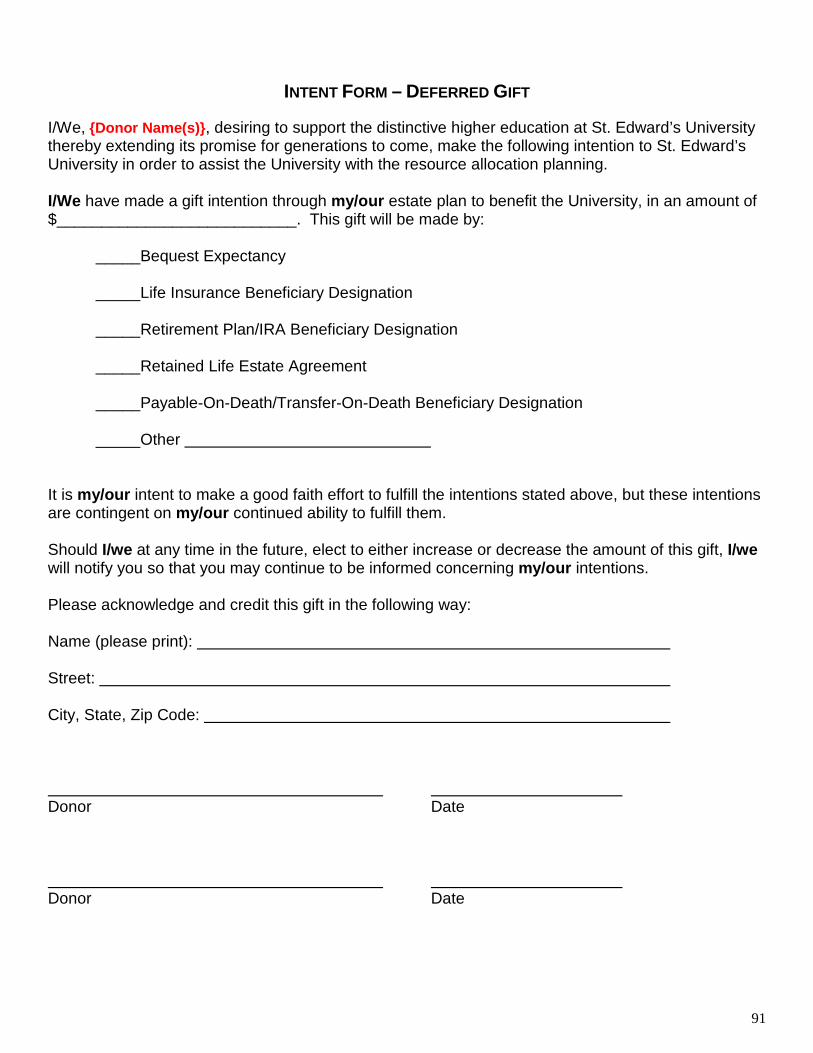

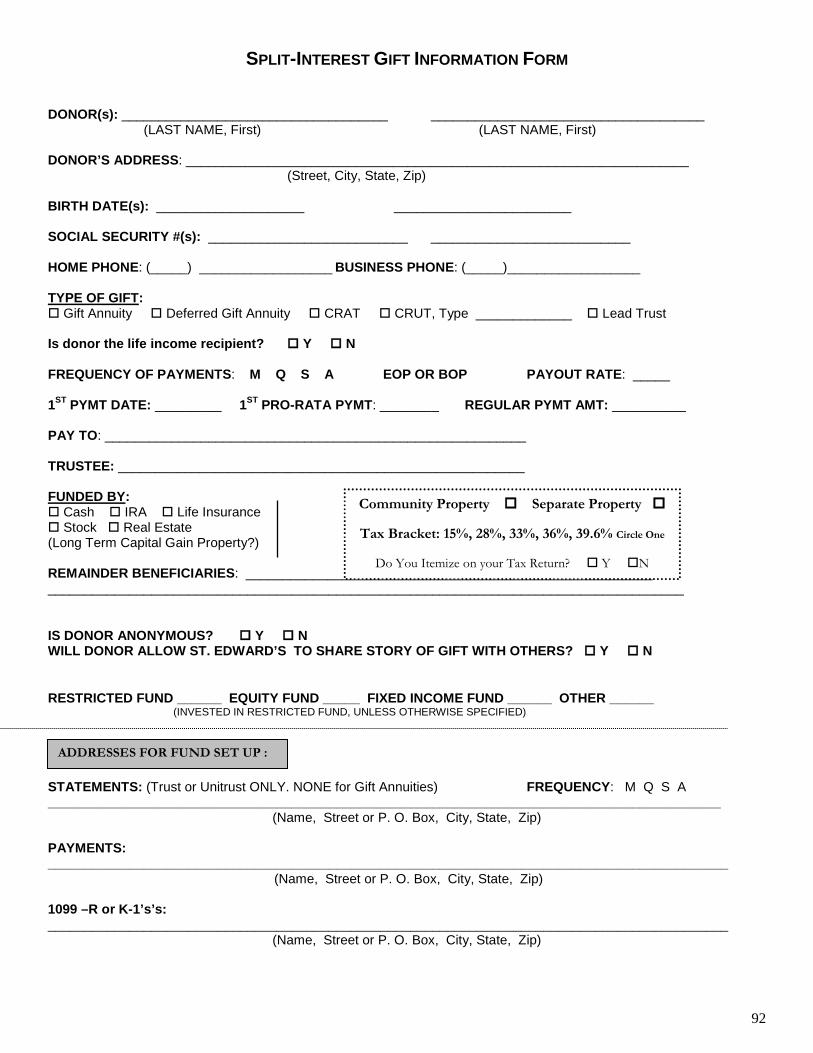

Gift Intent Forms Intent Form – Outright Gifts

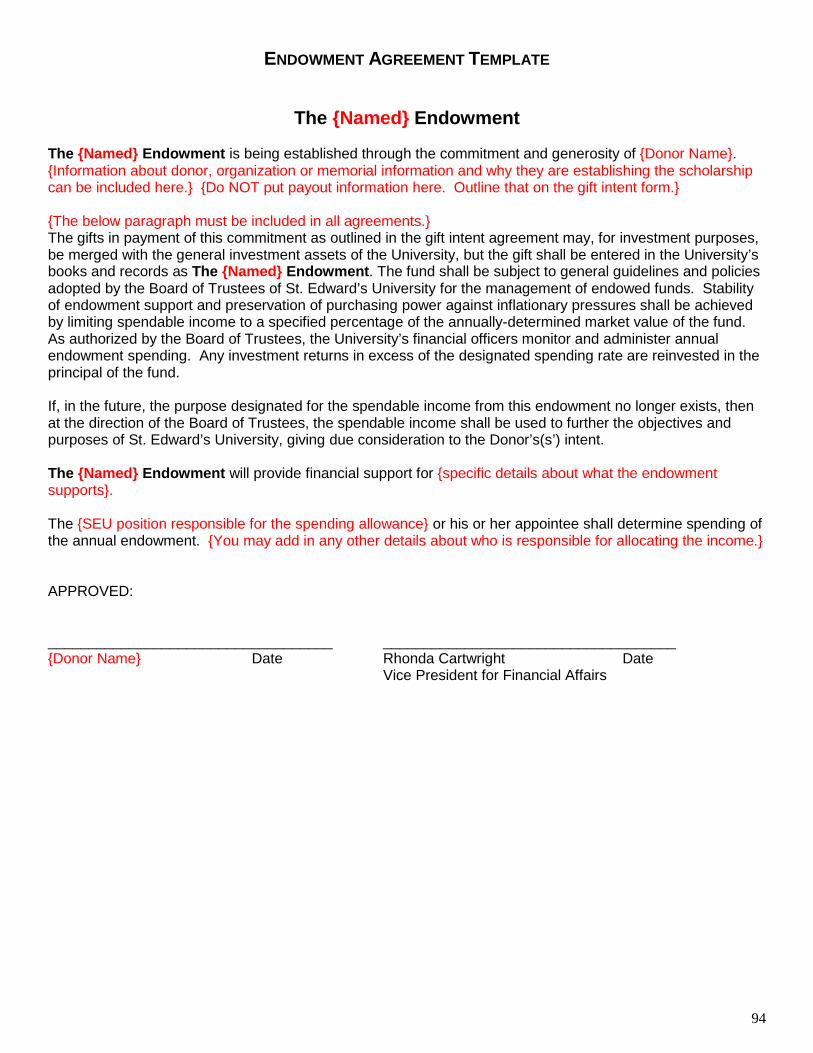

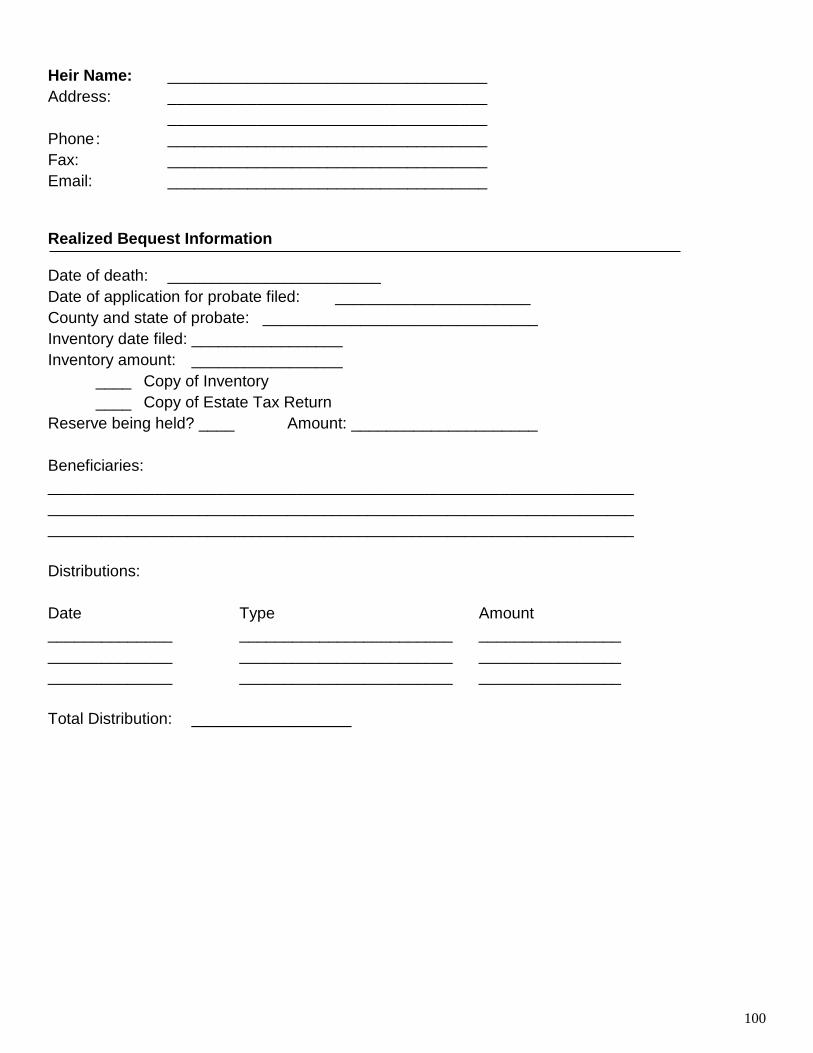

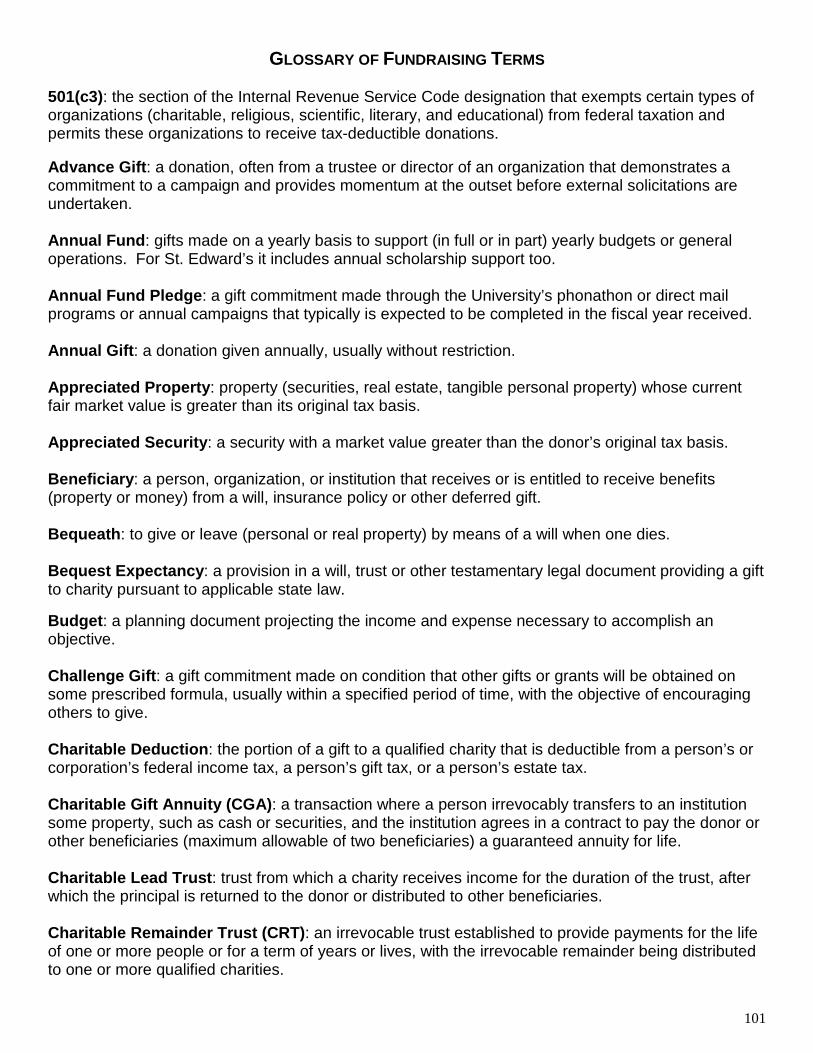

Intent Form – Split-interest Gifts Intent Form – Deferred Gifts Gift Information Forms Split-interest Gift Information Form Mary Doyle Heritage Society Bequest Checklist Agreement Forms Endowment Agreement Template Endowed Scholarship Agreement Template Annual Scholarship Agreement Template Life Estate Agreement Office of University Advancement Best Practices Glossary of Terms

4

INTRODUCTION

St. Edward’s University (hereinafter referred to as “St. Edward’s” or the “University”) is a diverse, nationally recognized liberal arts institution overlooking downtown Austin, Texas. Founded in 1885 by the Congregation of Holy Cross, the university emphasizes critical thinking, social justice and ethical practice. Combining a Holy Cross, Catholic heritage with a clear vision for the future, St. Edward’s is dedicated to preparing students for the opportunities and challenges of a 21st century world. PURPOSE AND RESPONSIBILITY The purpose of the Gift Acceptance Policies and Procedures is to support the mission of St. Edward’s and to give University staff guidelines approved by the Board of Trustees concerning the acceptance of charitable gifts to the University. These policies will facilitate giving by allowing University staff to respond quickly in the affirmative, when appropriate, and to seek broader approval before acceptance, when necessary. It will also guide and encourage University staff to decline gifts which are not appropriate and cannot be used for the greatest good of St. Edward’s. The Board of Trustees for St. Edward’s is responsible for reviewing these policies on an ongoing basis and periodically monitoring staff adherence to the policies. Staff bears responsibility for maintaining the policies on a day-to-day basis.

5

GENERAL POLICIES St. Edward’s will not accept a gift, whether outright or life-income in character, if the gift would be inconsistent with the goals and objectives of the University. The designated entity for acceptance of charitable gifts is the Office of University Advancement. All gifts solicited or unsolicited of money, gifts-in-kind, and/or property of any description to the University shall be immediately reported to, and when appropriate, receipted by the Office of University Advancement. Gifts received by any University personnel should be delivered immediately (the same day), if possible, to the Office of University Advancement. A guiding principle in soliciting and accepting gifts to the University is that the donor is to be treated fairly and with respect. Seeking to further the philanthropic cause of St. Edward’s shall not outweigh a proper concern for the best interest of the donor. All information concerning donors and prospective donors, including names, names of beneficiaries, amount of gift, size of estate, etc., shall be kept in strict confidence by St. Edward’s and its representatives. A donor, or, in the case of a testamentary gift or other acceptable circumstances, an executor, beneficiary, or close family member, may grant permission to the University to publicly announce any gift or feature of a gift to the University. Counting and Reporting University Advancement Office “Counting” and “reporting” are terms used by advancement offices to track all of the gifts, pledges, and deferred gifts received during a specified period towards a specific fundraising goal. The intent of counting and reporting is to reflect the total impact of fundraising efforts by representing all gifts, pledges and deferred gifts at their face value. St. Edward’s Office of University Advancement counts all gifts received at face value in its fundraising reports. Financial Affairs Office St. Edward’s follows Generally Accepted Accounting Principles (GAAP). St. Edward’s accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117, which require the classification of gifts into three categories,

I. gifts that are permanently restricted by the donor; II. gifts that are temporarily restricted by the donor; and,

III. gifts with no donor-imposed restrictions.

Fundraising amounts represented in St. Edward’s financial statements follow FASB guidelines, which discount the face value of gifts and pledges for determining the present value of future receipts and establish an allowance for uncollectable pledges. This is not a measure of fundraising effort, but a measure of the future value of a gift. Physical Acceptance of Funds When a St. Edward’s staff member receives a check, cash, or other currency, it is the responsibility of that staff member to transmit the funds to the Office of University Advancement along with any accompanying donor correspondence within twenty-four hours. If a St. Edward’s staff member receives funds while traveling on University business, he or she shall transmit the funds to University Advancement within twenty four hours after his or her return. A Gift Transmittal Form (see Appendix) or reply form from an approved University solicitation must be attached.

6

The use of campus or interoffice mail to transmit funds to University Advancement is discouraged. Acceptable means of transmission include hand-delivery and courier delivery. Gifts of cash must be delivered in person to the Office of University Advancement. At the time of delivery a University Advancement staff member will verify the cash amount with the deliverer. A completed Cash Acceptance Form (see Appendix) will be signed by the University Advancement staff member and the deliverer as verification of the amount delivered and accepted for deposit by University Advancement.

No St. Edward’s staff member may take physical possession of any non-cash item prior to receiving approval from the Vice Presidents for University Advancement and Financial Affairs where such is required. If Vice President approval is not required for a non-cash item, the staff member shall follow the acceptance procedures as outlined in these policies (Section X: Tangible and Intangible Personal Property).

Legal Counsel

St. Edward’s shall seek the advice of legal counsel in matters relating to acceptance of gifts where appropriate.

Conflicts of Interest

All prospective donors shall be strongly urged to seek the assistance of personal legal and financial advisors in matters relating to their gifts and the resulting tax and/or estate planning consequences.

At no time should any St. Edward’s staff member or volunteer involved in the solicitation of a gift serve as professional legal, tax, or financial advisor to a donor or prospect in matters relating to a gift. St. Edward’s staff may sometimes provide gift-planning information that addresses the needs of the donor and assists the donor’s professional advisors. That information may include sample documents and financial projections for specific gift options. To protect the University from potential claims that a gift was incompetently presented and/or solicited with undue influence and because the University representatives do not represent the donor, the donor will be encouraged, in writing, to finalize any documents and review all projections with his or her own advisors to ensure that the donor is receiving proper income tax, gift and/or estate planning advice. In all cases, University representatives will emphasize that they are employees of the university, and that they do not represent the donor.

Only attorneys-at-law, serving as outside counsel on behalf of St. Edward’s, shall be authorized to offer legal opinions on matters related to gift solicitation, acceptance, and disposition. Qualifying Gifts

To qualify as a gift to St. Edward’s, the following conditions must be met:

• The transfer of cash or other assets must be unconditional; • The transfer must be in furtherance of St. Edward’s charitable mission; and, • The transfer must be non-reciprocal, which means there must be no implicit or

explicit statement of exchange, purchase of services, or provision of exclusive information to the donor in exchange for his or her gift.

7

If a donor receives benefits in return for his or her gift to St. Edward’s, the amount of the benefit he or she receives is deducted from the gift in any receipting, reporting, and gift crediting in accordance with IRS regulations. St. Edward’s will not serve as an administrator of donor advised funds, but can accept gifts from donor advised funds administered by another non-profit. Beyond the restriction to a specific fund or project as determined at the time of gift, the donor will not have the power to direct how funds are invested or directed.

8

ACCEPTANCE POLICIES AND PROCEDURES BY TYPE OF GIFT ASSET

9

OUTRIGHT GIFTS I. Cash and Cash Equivalents Definition Cash and cash equivalents include all U.S. or foreign currency, checks drawn on U.S. or foreign banks, credit/debit card payments (Visa, MasterCard, American Express and Discover), wire transfers, money orders and payroll deductions. Examples • John Donor wishes to make a gift to The St. Edward’s Fund. He sends a check to

University Advancement. • Jane Donor hands a $50 bill to a development officer at an alumni event. • Joe Donor calls University Advancement and makes a $100 gift via credit card. • Jane Staff signs up for payroll deduction during the Faculty and Staff Campaign drive. Acceptance Policy a. Cash and cash equivalent gifts can be delivered to University Advancement in person, by

USPS mail, through electronic funds transfer, through direct deposit (payroll deduction), through the lockbox or through the internet via St. Edward’s online giving site. The use of campus or interoffice mail to transmit cash and cash equivalent gifts to University Advancement is not permitted. Acceptable means of transmission include hand-delivery and courier delivery. Gifts of currency must be delivered in person to University Advancement. At the time of delivery a University Advancement staff member will verify the currency amount with the deliverer. A completed Currency Acceptance Form will be signed by the University Advancement staff member and the deliverer as verification of the amount delivered and accepted for deposit by University Advancement.

b. In general, a gift that is mailed or delivered by an overnight delivery service recognized by the Internal Revenue Service is deemed made when posted and surrendered for delivery in the regular course of business. In determining the date of the gift, particular attention should be given to the envelope transmitting any gift that is mailed or sent by such an overnight delivery service, because the postmark on the envelope will generally establish the date for computing the value of the gift.

c. A gift that is transferred electronically is deemed made when it is credited to the University’s account. St. Edward’s is not required nor obligated to establish the appropriate date used to determine the date the gift was made for the donor’s purposes.

Processing Procedure a. Checks and money orders should be payable to St. Edward’s University. b. All cash and cash equivalent gifts will be deposited in the University’s bank via the

University’s business office. c. The gift will be batched and entered into the University Advancement database within two

business days of receipt of the gift.

10

Gift Acceptance Considerations • Who is the legal donor? • Is the check made payable to St. Edward’s? • What is the date on check? What is the postmark date? Stewardship Gifts will be processed and receipted within two business days of receipt of the gift. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Cash and cash equivalent gifts processed will be recorded and reported at face value for

both public reporting purposes and CASE. • St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all

gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Director of Advancement Services 512-448-8430 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

11

II. Third Party/Assignment of Gift Income Definition A person may assign to an institution income that the person would have received from a third party as payment for services (e.g., payment for serving on a corporate board, honoraria for speaking engagements, etc.). In such circumstances, credit for the gift will be given to the person making the assignment. This assumes that the organization making the payment will report the payment for services as income to the individual (usually on IRS Form 1099), and the individual would then take a corresponding tax deduction. The individual may choose to decline the payment and request the third party contribute the payment to the institution. In this case, the gift is from the third party and the third party does not report the payment as income to the individual.

Examples • Joe Donor serves on a committee for XYZ Corporation. He is paid for this and requests the

check be made out to St. Edward’s University. XYZ makes the check payable to St. Edward’s and sends it with a letter stating that the check is a charitable contribution from Joe Donor. Joe receives credit for the gift.

• Jane Donor serves on the board of ABC Foundation. She is paid for her services. She declines being paid, but requests the foundation contribute the payment to St. Edward’s. ABC receives credit for the gift and soft credit is given to Jane.

Acceptance Policy a. If a check has already been issued in the donor’s name, he or she must endorse it to St.

Edward’s University in order to be accepted. b. Alternatively, the donor may request that the income be remitted directly to St. Edward’s

and any check drafted be written in St. Edward’s name. If the check is payable directly to St. Edward’s by the third party, a letter must accompany the check identifying the payment as a charitable contribution from the individual. If the University receives the check directly from the third party organization with this letter, credit for the gift will be given to the person who performed the services, not the third-party organization.

c. A person has the option to waive all rights to the payment and suggest that, in lieu of payment, the organization contribute to the University. In this case, the organization is making the gift and will receive the credit. A soft credit will be given to the individual making the recommendation. If the circumstances of the gift are not clear, the University will contact the check issuer to ascertain legal ownership of the gift.

Processing Procedure a. All checks will be deposited in the University’s bank via the University’s business office.

The gift will be batched and entered into the University Advancement database within two business days of receipt of the gift.

Gift Acceptance Considerations • Who is the legal donor? • Did the donor assigning the income to St. Edward’s actually receive income credit for his or

her gift?

Stewardship Gifts will be processed and receipted within two business days of receipt of the gift. See the Gift Acknowledgement and Stewardship section for details.

12

Campaign and Annual Counting Guidelines • Third party/assignment of interests gifts processed will be recorded and reported at face

value for both public reporting purposes and CASE. • St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all

gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Director of Advancement Services 512-448-8430 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

III. Employer-Sponsored Matching Gifts Definition A matching gift may be received from a company or a company funded foundation, matching a gift given to St. Edward’s by an employee, retired employee, or a director of the company, foundation, or other organization. Examples • Jim Donor works for XYZ, Inc. XYZ, Inc. matches employee contributions to qualified

charities on a 2:1 basis. Jim gives a $50 gift to St. Edward’s and submits a matching claim form. XYZ, Inc. processes the claim and gives St. Edward’s $100.

• Jill Donor signs a legally enforceable pledge agreement to pay St. Edward’s $3,000 for five years. In year one, she submits a check to St. Edward’s for $2,000 and includes a matching form from her husband’s company, ABC Co. St. Edward’s processes the match and receives $1,000 from ABC Co. However, that amount is not credited against Jill’s pledge.

Acceptance Policy The University will accept matching gifts from all qualified matching gift entities. Processing Procedure a. In most cases, a donor wishing to maximize his or her contribution to St. Edward’s with a

match from his or her employer may obtain a matching gift claim form from the corporate employment or benefit office. Many companies are now employing online processes for employees to submit claims.

b. The donor should complete the portion of the form with the corporation's employee information, and then submit the form with her or his gift to St. Edward’s or go online to submit the claim after they give the gift to St. Edward’s.

c. The gift and data specialist will complete the matching gift claim form and submit it to the company or foundation according to the instructions on the claim form. If claims are submitted online, the gift specialist will verify the gift when the request is made from the company.

d. Matching gifts must be credited to the same account(s) as the original gift unless restricted by the matching company. These gifts will be matched to The St. Edward’s Fund for the general use of the University or to the fund specified by the matching gift company.

e. The donor’s giving record is soft credited for the value of the matching gift when received. When the gift being matched is a stock gift, the value that will be matched is the internally

13

calculated value as described in Section IV on marketable securities, and not the net proceeds from the sale.

f. Potential matching gifts cannot be entered as a part of a pledge the donor makes for future support since those are not funds the donor has control of or is irrevocably entitled to receive.

g. All matching gifts will be deposited in the University’s bank via the University’s business office.

h. The gift will be batched and entered into the University Advancement database within two business days of receipt of the gift.

Gift Acceptance Considerations • Is the match being claimed for a gift from a donor advised fund? If so the matching gift

company should be notified of the source of the gift to ensure St. Edward’s matching eligibility.

Stewardship Gifts will be processed within two business days of receipt of the gift. Receipts will be sent to those companies that require it. For matching gifts of $1,000 or more, the donor will be notified that the match was received. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Matching gifts received from companies and foundations are counted at the face value of

the gift. Potential matching gifts, or claims, are not counted and should never be considered as a way to fulfill an individual’s pledge to St. Edward’s.

• St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Director of Advancement Services 512-448-8430 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

14

IV. Marketable Securities Definition Marketable securities are stocks, bonds and other financial instruments that are regularly listed for sale on public exchanges. Unlike closely held securities, shares or units that are “marketable” have readily ascertainable values and are freely transferable to other owners, including charities. Examples • Jane Donor transfers electronically to St. Edward’s 350 shares of XYZ, Inc. stock, which

trades on the New York Stock Exchange. • Joe Donor holds 500 shares of ABC Co. in certificate form. ABC Co. trades on the NYSE.

He submits the stock certificate and stock power form in separate envelopes along with a letter of instruction to a representative of the University, who forwards the stock to the University’s bank for processing and deposit.

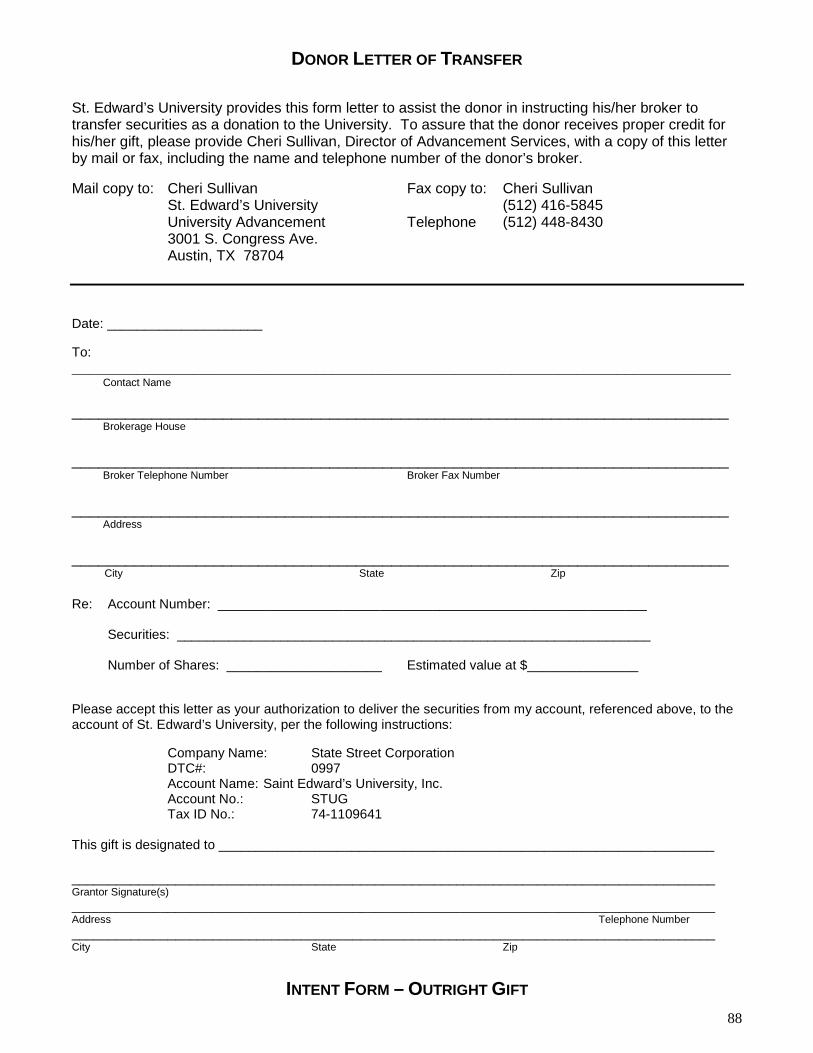

Acceptance Policy a. Upon learning of a proposed gift of marketable securities, a University Advancement staff

member will make every practical effort to contact the prospective donor and request the completion of the Donor Letter of Transfer. The staff member accepting a gift of marketable securities must notify the Director of Advancement Services.

b. Marketable securities gifted by electronic transfer from a donor’s brokerage firm to the University’s brokerage firm should be preceded by the Donor Letter of Transfer providing instructions.

c. Marketable securities not handled by a broker should be delivered by hand or sent only by certified or registered mail, or by an overnight delivery service recognized by the Internal Revenue Service. A stock power form (available from the Director of Advancement Services) signed by the donor naming the University as transferee should also be sent along with a notarized Donor Letter of Transfer. If a blank stock power is used, it should be sent in a separate envelope, using certified or registered mail, or hand delivery. In general, when a stock certificate is mailed, it should be left blank and sent in one envelope. A separate envelope should be sent which includes the signed stock power with signature guaranteed and the notarized letter of instruction. Both envelopes should be delivered as noted above.

d. In general, a gift that is mailed or delivered by an overnight delivery service recognized by the Internal Revenue Service is deemed made when posted and surrendered for delivery in the regular course of business. In determining the date of the gift, particular attention should be given to the envelope transmitting any gift of marketable securities that is mailed or sent by such an overnight delivery service, because the postmark on the envelope will generally establish the date for computing the value of the gift. When two envelopes are used, the date on the postmark of the later envelope will control. A gift that is transferred electronically is deemed made when it is credited to the University’s account. St. Edward’s is not required nor obligated to establish the appropriate date used to determine the fair market value of the gift for the donor’s purposes.

Processing Procedure a. To determine the fair market value of the gift of stock for University purposes, the University

will use the average of the high and the low value of the stock as listed on the applicable stock exchange using Yahoo Finance or any other comparable reporting website for the appropriate date of receipt of the stock. If that date should fall on a day the exchange is closed, the average will be computed between the high and low values of the stock as

15

listed on the applicable stock exchange using Yahoo Finance or any other comparable reporting website for both the preceding business day and the following business day from the date of receipt of the gift. The average of such two averages will be the appropriate value for University purposes. In all events the responsibility for determining the value of a gift of marketable securities for purposes of the donor’s income tax charitable deduction shall be exclusively the responsibility of the donor.

b. Upon receipt of a gift, the Director of Advancement Services (DAS) will verify the receipt of the asset to the University. Once receipt has been verified, the DAS will prepare a memo with details of the transfer, including the gift value, to the Vice President for University Advancement, the Vice President for Financial Affairs, the Controller, the Gift and Data Specialist and the donor’s manager.

c. In general, gifts of marketable securities will be sold as soon as practical unless: i. The Vice President for Financial Affairs for the University decides that the stock

should be held as a part of the organization’s portfolio; ii. The number of shares involved is sufficient to have a depressing impact on the price

of the stock, in which event the sale may be extended over a period of time necessary to avoid such an impact; or

iii. The terms of the gift declare otherwise or the stock is subject to contractual or regulatory restrictions on sale, such as the resale restrictions of Rule 144 under the Securities Act of 1933 and revised in 2008.

d. Securities that have certain resale restrictions generally should be held until the restrictions on sale expire and then sold under the guidelines above.

e. Gifts of bonds that require a holding period generally should be accepted and cashed when the holding period has expired.

f. The gift will be batched and entered into the University Advancement database within two business days of receipt of the gift.

Gift Acceptance Considerations Unless otherwise approved by the Vice President for Financial Affairs for the University, gifts of marketable securities that should not be accepted include:

• Securities that may create a liability to the University; • Securities that by their nature may not be assigned (excepting securities with transitory

restrictions on assignment, such as stock subject to the resale restrictions of Rule 144 under the Securities Act of 1933 and revised in 2008); and

• Securities that, on investigation, have no apparent value. Stewardship Gifts of marketable securities will be processed and receipted within two business days of receipt of the gift. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Gifts of marketable securities processed will be recorded and reported at the fair market

value of the gift of stock as determined by the University following the procedures outlined above.

• St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413

16

Director of Advancement Services 512-448-8430 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

17

V. Closely Held Securities Definition Closely held securities are an asset category that includes the total value of stock in closely held corporations. Closely held corporations are those whose ownership is concentrated among a relatively small numbers of owners, and whose stock is not traded publicly. These corporations include all S corporations and some C corporations. An S corporation, for United States federal income tax purposes, is a corporation that makes a valid election to be taxed under Subchapter S of Chapter 1 of the Internal Revenue Code. In general, S corporations do not pay any federal income taxes. Instead, the corporation's income or losses are divided among and passed through to its shareholders. The shareholders must then report the income or loss on their own individual income tax returns. A C corporation, for United States federal income tax purposes, is a corporation that is taxed under 26 U.S.C. § 11 and Subchapter C (26 U.S.C. § 301 et seq.) of Chapter 1 of the Internal Revenue Code. Most major companies (and many smaller companies) are treated as C corporations for federal income tax purposes. Examples John Donor is the President of a small, privately held company. He gives fifty shares of his company’s stock to St. Edward’s. Acceptance Policy a. Closely held securities may be accepted only with the approval of the Vice President for

Financial Affairs for the University and only when an investigation reveals no significant potential liability for St. Edward’s in receiving the gift, and only if any lack of liquidity is anticipated to present no major difficulties for the University.

b. The closely held security must have a minimum value of $1,000.00. c. Interest in closely-held entities that transfer control of the entity to the University may be

accepted only when the potential benefits from the gift outweigh potential liabilities – where the company involved is not engaged in activities inconsistent with the mission, goals and objectives of the University and where the demands on staff time regarding the management of the company are acceptable.

Processing Procedure a. Gifts of closely held securities that exceed $10,000 in value should be reported at the fair

market value placed on them by a qualified independent appraiser as required by the Internal Revenue Service (IRS) for valuing gifts of stock that are not publicly traded. In the U.S., the institution by obtain the appraiser’s valuation figure from “Noncash Charitable Contributions,” IRS Form 8283, which the donor must usually provide for the recipient organization’s signature. A signature by the recipient organization does not signify an approval of the indicated amount. This confirmation of receipt will only be applied by the recipient organization after the donor and the independent appraiser sign the document. 1

b. Gifts of closely held securities less than $10,000 may be valued at the per-share cash purchase price of the most recent transaction. Normally, this transaction is the redemption of the stock by the corporation. If no redemption has occurred during the reporting period,

1 CASE Reporting Standard & Management Guidelines for Educational Fundraising, 4th Edition

18

an independent certified public accountant (CPA) who maintains the books for that corporation is qualified to value its stock. 2

c. The gift will be batched and entered into the University Advancement database within two business days of receipt of the gift.

Gift Acceptance Considerations • Unless waived by the Vice President for Financial Affairs for the University, if the proposed

gift is one of stock in a closely-held corporation that currently owns or formerly owned real property, or other property (such as mortgage notes) secured by an interest in real property, St. Edward’s shall comply with its Environmental Assessment Policy Number G-15.

• Is the Fair Market Value (FMV) at an amount that will yield benefit to the university or establish a fund once all of the incurred costs are applied?

• Can the stock be liquidated immediately? • Are there any conditions which prohibit disposal of the stock? • Is the gift credit the donor will receive consistent with his or her intentions? Stewardship Gifts of closely held securities will be processed and receipted within two business days of receipt of the gift. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Gifts of closely held securities processed will be recorded and reported at the appraised or

per-share cash purchase price as determined by the University following the procedures outlined above.

• St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413 Director of Advancement Services 512-448-8430 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

2 CASE Reporting Standard & Management Guidelines for Educational Fundraising, 4th Edition

19

VI. Mutual Funds Definition A mutual fund is an open-ended fund operated by an investment company which raises money from shareholders and invests in a group of assets, in accordance with a stated set of objectives. There are many different types of mutual funds. Examples Jane Donor has $40,000 in securities she wants to donate to St. Edward’s. Of that amount, more than half is held in mutual funds and the rest is held in individual company shares. Acceptance Policy • Mutual funds may be held in certificate form but they are more likely held in electronic form

by a brokerage firm, financial institution, or the mutual fund company itself. Since the transfers of mutual funds vary widely from firm to firm, gifts of mutual funds are dealt with on a case-by-case basis and may not be able to be transferred to or accepted by the University.

• Due to the administrative costs associated with the transfer of mutual funds, mutual funds valued at less than $1,000 will not be accepted by the University.

Processing Procedure If the mutual fund is accepted by the University, the basic process is as follows:

a. The development officer shall notify the Director of Advancement Services (DAS). b. The DAS will work with the appropriate Finance offices and personnel to determine

whether the mutual fund shares can be transferred and how they are to be transferred. c. Note that depending on how the shares are held, the transfer can take anywhere from a

week to more than three months to complete. Development staff should be mindful of this potential for delay, especially if a donor is attempting to make a year-end gift.

d. The DAS will value the mutual fund shared at the public redemption value, which is the net asset value of the fund on the date of the gift. Net asset value is determined by valuing all securities in the fund at day’s end, reducing that value by expenses, and dividing that figure by the number of shares outstanding. This price is published in a variety of publications and on numerous websites daily.

e. The gift will be batched and entered into the University Advancement database within two business days of receipt of the gift.

Gift Acceptance Considerations • Can the mutual funds be liquidated easily? • Are there any conditions which prohibit disposal of the mutual funds? Stewardship Mutual funds will be processed within two business from the completion of the transfer into the University’s control. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Gifts of mutual fund shares are counted at the public redemption value, which is the net

asset value of the fund on the date of the gift. Net asset value is determined by valuing all securities in the fund at day’s end, reducing that value by expenses, and dividing that figure by the number of shares outstanding. This price is published in a variety of publications and on numerous websites daily.

20

• St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413 Director of Advancement Services 512-448-8430 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

21

VII. Life Insurance Definition Life insurance is a policy that will pay a specified sum to beneficiaries upon the death of the insured. Donors may make an outright gift of a policy to St. Edward’s by irrevocably transferring all incidents of ownership in a policy to St. Edward’s. Examples • John Donor, age 60, bought a whole life policy on his life when his children were very

young. Now that his children are grown and the policy is fully paid up, he donates it to St. Edward’s which surrenders it and receives cash.

• Jane Donor owns a universal life policy on her life that currently has a cash surrender value of $57,000. She transfers it to St. Edward’s which cashes it out and uses the funds for a purpose the donor has specified.

Acceptance Policy a. St. Edward’s University will accept two types of life insurance gifts:

i. gift of a paid-up insurance policy; ii. gift of a new or existing insurance policy, for which the donor intends to continue

making payments so that the policy does not lapse. b. In either case, the donor must name the University as both the owner and the beneficiary of

the insurance policy with the understanding that St. Edward’s will cash in the policy as soon as practicable, at the discretion of St. Edward’s. If the donor only specifies St. Edward’s as the beneficiary of a policy, but retains ownership, the donor has made a revocable deferred gift, which is addressed later in these policies in the Life Insurance Beneficiary Designations section.

c. The FMV of the policy must be at least $5,000. d. St. Edward’s University will make payments on a policy if the donor makes annual gifts at

least equivalent to the amount of the premium. The University is under no obligation, but may continue to pay the premiums if the donor does not make an equivalent annual gift.

e. St. Edward’s will not: i. Accept ownership of term policies as they have no current cash value and seldom

remain in force until the death of the insured. ii. Accept group life insurance as it is owned by the employer. Donors may opt to name

St. Edward’s as beneficiary of either a term or group life policy, but that would qualify as a revocable deferred gift as opposed to a current outright gift.

iii. Participate in any pooled insurance program including Investor-Owned Life Insurance or Stranger-Owned Life Insurance programs.

iv. Endorse any particular insurance product, company, program, agent, agency, or company, nor will it provide donor lists to any of them.

Processing Procedure a. When a gift of life insurance that meets the above criteria is proposed, the gift officer should

notify the Director of Planned Giving who will assess the policy, consulting with external and internal experts as necessary. The Director of Planned Giving will obtain all relevant data on the insured, secure an in-force illustration on the policy, and then submit the proposal to the Vice President for Financial Affairs for approval.

b. If approved, the Director of Planned Giving will coordinate the transfer of ownership with the donor and insurance company and provide documentation to Advancement Services for processing.

22

c. Advancement services will provide all necessary information to the Office of Financial Affairs and the Business Office for their records and systems.

d. A life insurance gift is a noncash gift and should be reported by the donor on IRS Form 8283 if the donor claims a charitable deduction of $500 or more. Moreover, if the policy’s value is $5,000 or more, in order to obtain the benefit of a charitable deduction, the Internal Revenue Service will require the donor to (1) complete IRS Form 8283, (2) obtain a “qualified appraisal” of the property from a qualified appraiser, (3) attach a fully completed appraisal summary to the tax return in which the deduction is first claimed, and (4) maintain records of certain information listed in Treas. Reg. § 1.170A-13(b)(2)(ii). These obligations rest upon the donor and do not affect acceptance of the donated property by the University. Upon presentation and acceptance of the gift, however, the University will sign the Donee Acknowledgment for such gift contained in Form 8283, if requested to do so by the donor. If St. Edward’s University sells, exchanges or otherwise disposes of any property for which it has signed a Donee Acknowledgment within two years of the date the University received the gift, the University shall file Form 8282, Donee Information, with the Internal Revenue Service, with a copy to the donor, disclosing that fact and such other information as the Internal Revenue Service may require.

e. A life insurance policy with cash value is a current asset of the donor, which upon transfer, becomes an asset of St. Edward’s. As with all of St. Edward’s assets, life insurance policies are periodically reviewed and monitored in light of the asset’s performance and the goals of both the donor and the unit for which the policy is designated.

f. The gift will be batched and entered into the University Advancement database within two business days of receipt of the gift.

Stewardship Gifts of life insurance will be processed and receipted within two business days of transfer of ownership to the University. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines a. Irrevocable gifts of fully paid-up life insurance policies where St. Edward’s has been named

both owner and beneficiary of the policy are counted as outrights gifts at the cash surrender value as identified in writing by the insurance provider.

b. Irrevocable gifts of new or partially paid-up life insurance policies where St. Edward’s has been named both owner and beneficiary of the policy are counted as outrights gifts at the cash surrender value as identified in writing by the insurance provider. In addition, the premium payments made by the donor to the institution, which in turn pays the premium to the insurer, will be counted as outright gifts at the full value of the premiums paid. If no gift is received to pay the premium and the University chooses to pay it, this is an expenditure and will not be counted as gift. In addition, if there are any increases in the cash surrender value, it will not be reported as a gift.

c. Realized death benefits of a previously recorded policy will not be counted as gift income. If the realized benefits are more than the reported cash surrender value, this is considered a gain on the disposition of the institution’s assets and will not be recorded as gift income.

d. Realized death benefits on a policy that was not previously recorded will be recorded at the insurance company’s settlement amount.

e. Realized death benefits on a policy for which the University was only named beneficiary and counted in gift reports previously as a deferred gift will be counted at the insurance company’s settlement amount less any amounts previously counted. The cash settlement will be applied to the deferred gift and the remaining balance will count as an outright gift.

23

f. St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Gift Acceptance Considerations • Is the policy paid up? • Will the donor continue to make annual gifts to the University to cover the premium

payments? Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413 Director of Advancement Services 512-448-8430 Director of Planned Giving 512-233-1401 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

24

VIII. Retirement Plan/IRA Distributions

Definition Retirement plan and IRA distributions are the payments made from a retirement plan or IRA to the account owner, or, in the case of the account owner's death, the beneficiary. Acceptance Policy A beneficiary may transfer funds from a retirement plan by following the steps outlined below.

a. Take a distribution from the plan b. Pay income tax on that distribution c. Make an outright cash or cash equivalent gift to St. Edward’s d. Take a charitable deduction for the outright gift. The charitable deduction may not be

available to all donors. Processing Procedure See Processing Procedures under Cash and Cash Equivalents section. Gift Acceptance Considerations An outright gift of a retirement plan or IRA distribution during life is not a tax efficient option under current law. However, recent legislation has allowed for charitable IRA rollover incentives which have made it more beneficial to use IRA funds to make a charitable contribution. The University attempts to remain current on such benefits and will inform donors accordingly. Stewardship Gifts will be processed and receipted within two business days of receipt of the gift. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Retirement plan and IRA distribution gifts are treated as outright gifts and counted at the

face value of the gift. • St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all

gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Director of Advancement Services 512-448-8430 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

25

IX. Real Property and Mineral Interests Definition Real property (also called real estate or realty) is land, its natural resources, and any permanent buildings on it. Mineral rights is the ownership of all rights to gas, oil or other minerals as they naturally occur in place, at or below the surface of a tract of land. Examples • Jane Donor owns 100 undeveloped acres in the mountains that she would like to give to St.

Edward’s. • John Donor would like to donate his house in Atlanta to St. Edward’s. • Jane Donor proposes funding a charitable remainder trust with her vacation home. (Any

proposed gift of real property to fund a planned gift will be subject to the Gift Acceptance Policies governing both Real Property and the proposed type of planned gift vehicle, such as a bequest, life estate or charitable remainder trust.)

Acceptance Policy a. Upon notification of a potential gift of real property, St. Edward’s will:

i. Make every practical effort to meet personally with the prospective donor; ii. Request an inspection of the property by the Vice President for Financial Affairs or the

Director of Physical Plant; iii. Comply with Environmental Assessment Procedures (Appendix Section I).

b. The donor will have a survey done of any gifts of real property. Unless otherwise approved by the Vice President for Financial Affairs for the University, St. Edward’s will not pay for such survey.

c. The donor will have a building inspection done of any improvements on commercial property given to St. Edward’s. Unless otherwise approved by the Vice President for Financial Affairs for the University, St. Edward’s will not pay for such building inspection.

d. The donor will have gifts of real property appraised by a qualified appraiser to establish a fair market value for the donor’s purposes. Unless otherwise approved by the Vice President for Financial Affairs for the University, St. Edward’s will not pay for such an appraisal.

i. The appraisal must be prepared not earlier than 60 days prior to the date that the contribution is made, and must be prepared not later than the due date of the return on which the deduction is claimed or the date that an amended return is filed if the amended return is the first return on which the deduction is claimed.

ii. The appraisal must be prepared, signed, and dated by a qualified appraiser as defined below.

iii. The appraisal must include the following information: 1. A description of the property in sufficient detail for a person who is not generally

familiar with the type of property to ascertain that the property that was appraised is the property that was (or will be) contributed;

2. In the case of tangible property, the physical condition of the property; 3. The date (or expected date) of contribution to the donee; 4. The terms of any agreement or understanding entered into (or expected to be

entered into) by or on behalf of the donor, which relates to the use, sale or other disposition of the property contributed. This includes restrictions on the donee’s right to use or dispose of the donated property, all provisions which confer on anyone, other than the donee charity, the right to income from the donated property or the right to possession of the property, including voting rights to securities, a right of purchase, or a right to designate the person to

26

receive income, possession or right to purchase, or a provision which earmarks the donated property for a particular use. As an added precaution, all agreements between the donor and the donee charity relating to the gift should be attached to the appraisal and incorporated into it by reference;

5. The name, address, and taxpayer identification number of the qualified appraiser and, if the qualified appraiser is a partner in a partnership, an employee of any person (whether an individual, corporation, or partnership), or an independent contractor engaged by a person other than the donor, the name, address and taxpayer identification number of the partnership or the person who employs or engages the qualified appraiser;

6. The qualifications of the appraiser; 7. A statement that the appraisal was prepared for income tax purposes; 8. The date or dates on which the property was valued; 9. The appraised fair market value of the property on the date (or expected date)

of contribution; 10. The method of valuation used to determine the fair market value, such as the

income approach, the market data approach, or the replacement-cost-less-depreciation approach;

11. The specific basis for the valuation, if any, such as any specific comparable sales transactions;

12. A description of the fee arrangement between the donor and the appraiser. iv. The appraiser must sign the Appraisal Summary when the donor presents it. In this

regard, no part of the fee arrangement for a qualified appraisal can be based, in effect, on a percentage (or set of percentages) of the appraised value of the property.

v. To be a “qualified appraiser,” the appraiser must sign and complete Internal Revenue Service Form 8283, Section B, denoted “Appraisal Summary.” The Appraisal Summary includes declarations by the appraiser that:

a. The individual holds himself or herself out to the public as an appraiser. b. Because of the appraiser’s qualifications as described in the appraisal, the

appraiser is qualified to make appraisals of the type of property being value. c. The appraiser understands that a false or fraudulent overstatement of the

value of the property described in the qualified appraisal or appraisal summary may subject the appraiser to a civil penalty under Section 6701 for aiding and abetting an understatement of tax liability, and consequently the appraiser may have appraisals disregarded pursuant to 31 U.S.C. Section 330(c).

d. The appraiser is not: i. The donor or the taxpayer who claims or reports the deduction under

Section 170 for the contribution of the property being appraised; ii. A party to the transaction in which the donor acquired the property

being appraised (i.e. the person who sold, exchanged or gave the property to the donor, or any person who acted as an agent for the transferor or for the donor with respect to such sale, exchange or gift), unless the property is donated within two months of the date of acquisition and its appraised value does not exceed its acquisition price;

iii. The donee of the property; iv. Any person employed by any of the foregoing persons or related to any

of the foregoing persons under Section 267(b) (e.g., if the donor acquired a painting from an art dealer, neither the art dealer nor persons employed by the dealer can be qualified appraisers with respect to that painting);

27

v. Any person whose relationship with any of the persons listed in (1) through (4) above would cause a reasonable person to question the independence of such appraiser. For example, an appraiser who is regularly used by any person described in (1) through (3) above and who does not perform a substantial number of appraisals for other persons has a relationship with such person that is similar to that of an employee and cannot be a qualified appraiser with respect to the property contributed.

e. Unless otherwise approved by the Vice President for Financial Affairs, the minimum FMV of the property must be at least $200,000.

f. In general, it is the policy of St. Edward’s not to accept contributions of property subject to any form of indebtedness or other liability in order to prevent the University from becoming responsible for the payment thereof. Circumstances may arise where the Vice President for Financial Affairs for the University believes that the acceptance of a gift encumbered by some form of liability would be in the University’s best interest and that any financial risk would be within acceptable limits. In such event, the Vice President for Financial Affairs shall determine whether to accept the gift and will prepare a response for the donor as soon as possible and preferably within 10 working days. In evaluating whether to accept such gift, consideration shall be given to the fair market value of the gift, the amount of the potential liability, the ability to sell the property, the costs associated with selling the property, and all other matters deemed relevant.

g. In general, St. Edward’s will not accept a gift involving real property that makes the University a principal in a real estate partnership, undivided interests in real estate, joint venture, or business activity in which the University participates fully in the risks of the operation and has more than limited liability for the conduct of the business (e.g., as a general partner, principal in a joint venture, or as an owner of a working interest).

h. If appropriate, St. Edward’s may accept gifts of real property for programmatic purposes. Gifts of real property that are programmatically advantageous must be accompanied by endowed funds, a revenue generating mechanism, or some other explicit financial plan to support the maintenance of the gift and the fulfillment of the programmatic purpose. Specific criteria will be used over time to evaluate the success of the proposed program and whether or not the program should be continued, and to enable judgment as to whether the property should be retained, used for another purpose, sold or transferred to another owner.

i. Gifts of mineral interests may be received absent extenuating circumstances such as extended liabilities or other considerations making receipt of the gift inadvisable. In this regard, prior to the acceptance of mineral interests, all offered gifts are to be first examined by a qualified consultant for such extenuating circumstances that would argue against receipt of the gift. The expense of the examination must be borne by the donor unless the Vice President for Financial Affairs for St. Edward’s and the Fiduciary Committee of the Board of Trustees approves an exception. Working mineral interests, which entail special problems regarding taxation, should be considered in advance of receipt of the gift, with a view towards establishing a plan that will minimize any adverse effect on the tax status of St. Edward’s.

j. If St. Edward’s receives a gift of a personal residence or farm with a life estate retained, see the section under Retained Life Estate for additional information.

Processing Procedure a. Preferably before acceptance, but in all events no later than upon acceptance of a gift of

real property, St. Edward’s will endeavor to advise the donor in writing of the value placed

28

on the gift by the University for its purposes, including the price the University will seek in any sale of the property.

b. Upon acceptance of a gift, St. Edward’s will provide a letter of acknowledgment and appreciation to the donor meeting Internal Revenue Service substantiation requirements.

c. In general, when a donor contributes property (other than publicly traded securities) for which a charitable deduction in excess of $5,000 is claimed, in order to obtain the benefit of a charitable deduction, the Internal Revenue Service will require the donor to (1) complete IRS Form 8283, (2) obtain a “qualified appraisal” of the property from a qualified appraiser, (3) attach a fully completed appraisal summary to the tax return in which the deduction is first claimed, and (4) maintain records of certain information listed in Treas. Reg. § 1.170A-13(b)(2)(ii). These obligations rest upon the donor and do not affect acceptance of the donated property by St. Edward’s. Upon presentation and acceptance of the gift, however, the University will sign the Donee Acknowledgment for such gift contained in Form 8283, if requested to do so by the donor.

d. If St. Edward’s sells, exchanges or otherwise disposes of any property for which it has signed a Donee Acknowledgment within two years after the date it received the gift, the University shall file Form 8282, Donee Information, with the Internal Revenue Service, with a copy to the donor, disclosing that fact and such other information as the Internal Revenue Service may require.

e. With respect to real property that neither St. Edward’s nor one of its supported organizations desires to use or which, for any other reason, the University decides to dispose of, St. Edward’s, in its sole discretion, will list such property for sale, and, with full disclosure to the donor if it is within two years after the date the gift is received, will attempt to realize a sale which will result in a purchase price of no less than the appraised value of the property, although it is not bound to do so.

f. The gift will be batched and entered into the University Advancement database within two business days of completed transfer of ownership.

g. All copy of all of the related documentation will be sent to the Business Office. Gift Acceptance Considerations • Who will pay for the Phase 1 Inspection? • Is the property subject to mortgage or debt? • St. Edward’s will not accept gifts of an interest in a timeshare property or program. • Are there any unrelated business income tax issues? • Is there any reasonable possibility that the property could be contaminated by hazardous

waste? • Has the property been utilized in a manner that would embarrass St. Edward’s? Stewardship Gifts of real property and mineral rights will be processed and receipted within two business days of transfer of ownership to the University. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Gifts of real property are counted at the values placed on them by a qualified independent

appraiser as required by the IRS for valuing non-cash charitable contributions. • St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all

gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

29

Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413 Director of Advancement Services 512-448-8430 Director of Planned Giving 512-233-1401 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

30

X. Tangible and Intangible Personal Property Definition Tangible personal property is an asset that can be touched, handled, or moved by an individual, as opposed to intangible assets. Tangible personal property includes automobiles, art, furniture, jewelry, coin or stamp collections, boats, and similar assets. Intangible or intellectual property refers to assets produced through creativity and innovation such as inventions, patents and copyrights of literary or artistic works.

Examples Tangible property:

• Joan Donor owns an automobile she wishes to donate to St. Edward’s. • John Donor owns an 18th century painting he wishes to donate to St. Edward’s. • Jillian and Jorge Donor own a collection of rare books they would like to donate to the

St. Edward’s library system. Intangible or intellectual property:

• John Donor, a professor, gives to St. Edward’s the copyright to his popular book. • Jane Donor, a scientist, donates to St. Edward’s her patented process for making a

vaccine. • Joan Donor, a cartoonist, gives to St. Edward’s all trademark and licensing rights

associated with one of her popular characters. • Royalties. Institutions that receive gifts for royalties from property they do not own

(such as patents) – or from property that could not be values and thus was not counted at the time of the gift – should count and report the income they receive resulting from that ownership each time a payment is received. However, do not enter a pledge in anticipation of such payments. Royalties from vendor affinity agreements, such as alumni credit card programs are not countable.

Acceptance Policy a. Gifts of both tangible and intangible personal property will be subject to advance approval

by the Vice President for Financial Affairs and the Vice President for University Advancement of the University.

b. While exceptions may be considered, St. Edward’s requires that gifts such as art, furniture, computers, boats, automobiles, medical equipment, and other forms of tangible personal property, must satisfy each of the following before acceptance: i. The item to be received can be used by the University and the University can sell or

otherwise dispose of the property; ii. For property that cannot be used by the University but can be sold, the FMV must be at

least $5,000 and verified by a qualified appraisal; iii. The item to be received is not encumbered by high transportation costs, storage costs,

or unusual maintenance; and iv. The item to be received must not be encumbered by debt.

Processing Procedure a. Upon learning of a proposed gift of tangible or intangible personal property to St. Edward’s,

a University staff member will make every practical effort to meet personally with the prospective donor and obtain advance approval of acceptance from the Vice President for Financial Affairs and the Vice President for University Advancement of the University.

31

b. In general, when a donor contributes property (other than publicly traded securities) for which a charitable deduction in excess of $5,000 is claimed, in order to obtain the benefit of a charitable deduction, the Internal Revenue Service will require the donor to (1) complete IRS Form 8283, (2) obtain a qualified appraisal of the property from a qualified appraiser, (3) attach a fully completed appraisal summary to the tax return in which the deduction is first claimed, and (4) maintain records of certain information listed in Treas. Reg. § 1.170A-13(b)(2)(ii). These obligations rest upon the donor and do not affect acceptance of the donated property by the University. Upon presentation and acceptance of the gift, however, St. Edward’s will sign the Donee Acknowledgment for such gift contained in Form 8283, if requested to do so by the donor.

c. If St. Edward’s sells, exchanges or otherwise disposes of any property for which it has signed a Donee Acknowledgment within two years of the date the gift was received, the University shall file Form 8282, Donee Information, with the Internal Revenue Service, with a copy to the donor, disclosing that the property was disposed of and such other information as the Internal Revenue Service may require. St. Edward’s reserves the right to liquidate, upon transfer or any time thereafter, any tangible or intangible property obtained through charitable donation, unless otherwise specified in a legally binding agreement between St. Edward’s and the donor(s). Any such restrictions may impact its marketability and therefore the value of the gift.

d. Donors are responsible for establishing the value of tangible and intangible personal property donated to charity for reporting to the IRS. St. Edward’s will count gifts of tangible and intangible personal property that qualify as a charitable deduction for a donor at fair market value regardless of the value the donor may be able to take as a charitable deduction.

e. For property valued at $5,000 or more given to the University, St. Edward’s requires that a current independent appraisal be provided. Any gift received by the University accompanied by a written independent appraisal acceptable to the Vice President for Financial Affairs for the University shall be credited at the appraised value.

f. For gifts or property valued at less than $5,000, the University will use the value provided in any one of the following ways:

i. The value placed on the gift by a qualified appraiser. While not necessary for IRS purposes, the donor my nonetheless obtain such an appraisal;

ii. The value declared by the donor. The donor should provide a copy of either the paid bill of sale or the invoice and copy of the check or personal credit card statement showing payment. Sales tax will not be included in the gift’s value.

iii. The value determined by a qualified expert on the faculty or staff of the University, but not an individual whose fundraising totals are directly affected by the gift.

iv. The value established by a purchaser’s winning auction bid at a charity auction run by the University, if no fair market value for the item was available before the auction.

v. In the absence of a provided value, the gift will be carried on the books of the University in the manner deemed most appropriate by the Vice President for Financial Affairs of the University.

g. In general, a gift that is mailed or delivered by an overnight delivery service recognized by the Internal Revenue Service is deemed made when posted and surrendered for delivery in the regular course of business. In determining the date of the gift, particular attention should be given to the package or envelope transmitting any gift that is mailed or sent by such an overnight delivery service because the postmark on the package or envelope will generally establish the date for determining when the gift was made. Otherwise, either the date the property’s ownership is completely assigned to the University via a deed of gift, or when an employee of the University takes possession of the property will be the date of the gift for University purposes. St. Edward’s is not required nor obligated to establish the appropriate date used to determine the date the gift was made for the donor’s purposes.

32

h. The gift will be batched and entered into the University Advancement database within two business days of transfer of ownership of the property. If value is in question, a $1 will be assigned until appropriate value has been sustained.

Gift Acceptance Considerations • Does transfer of the gift require a title transfer? • Does the gift appraise in excess of $5,000? • Does the gift require additional expenditures to maintain the asset after receipt? • Is there potential for unrelated business taxable income, the carrying costs, and the

potential for revenue from the gift? • Are there any legal, ethical, and public relations issues which might arise from acceptance

of such a gift? • Will receiving and enjoying the value or benefit of the intellectual property subject St.

Edward’s to any risk of a legal claim? It may be necessary to obtain paperwork and assurances from the donor verifying his or her rights and the absence of any infringement issues.

• Some intellectual property rights cannot be transferred or can be transferred only under certain conditions.

Stewardship Gifts of tangible or intangible personal property will be processed and receipted within two business days of transfer of ownership to the University. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • Gifts of tangible and intangible personal property which qualify for a charitable deduction

are counted at their full fair market value as determined by the processes outlined above. • Gifts of software and hardware that qualify as a charitable donation under the laws of the

appropriate tax authority and that have an established retail value are counted at the educational discount value if such exists or the fair market value.

• St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413 Director of Advancement Services 512-448-8430 Director of Planned Giving 512-233-1401 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

33

XI. Gifts-in-Kind Definition Gifts-in-kind are generally defined as non-cash donations of material or long-lived assets, other than real and tangible or intangible property (see Sections IX and X). Gifts-in-kind might include such items as equipment, software, printed materials, food or other items used for hosting dinners, etc. Gifts-in-kind usually (although no always) come from companies, corporations, or vendors in contrast to individuals, who typically give personal property. Examples • Deep discounts or bargain sales. Company ABC offers to sell their product to St. Edward’s

at a “deep discount” or “bargain sale,” that is not a discount that applies to purchases made by the University or other higher education institutions on a regular basis and is not uniquely identified as a special reduction to be considered as a donation.

• Royalties. Institutions that receive gifts for royalties from property they do not own (such as patents) – or from property that could not be values and thus was not counted at the time of the gift – should count and report the income they receive resulting from that ownership each time a payment is received. However, do not enter a pledge in anticipation of such payments. Royalties from vendor affinity agreements, such as alumni credit card programs are not countable.

• Software and hardware. Irrevocable gifts of software or hardware with an established retail value count at the educational discount value (if one exists) or the fair market value, as long as the agreement qualifies as a charitable donation under IRS regulations.3

Acceptance Policy a. The acceptance of gifts-in-kind to be recorded as assets of the University will be subject to

advance approval by the Vice President for Financial Affairs and the Vice President for University Advancement of the University. Gifts-in-kind valued at less than $5,000 that are not tangible property to reside on University property will not be recorded as an asset or posted to the general ledger and will not require the approval of the Vice President for Financial Affairs and the Vice President for University Advancement. Examples include a book, a gift certificate for the donor’s product, vendor discounts, etc.

Processing Procedure a. Upon acceptance of the gift, the donor must submit the Gift-in-Kind information form and

attach the documentation used to determine the value (bill of sale indicating the retail or educational discount price less the discounted amount, royalty check or information establishing the retail value or fair market value).

b. University Advancement will record the gift at the educational discount value and/or the value the institution would have paid had it purchased the item outright from the vendor. In the case of deep discounts or bargain sales, the gift the discounted amount will be recorded as the gift.

c. Gifts-in-kind to be recorded as University assets will be sent for processing to the general ledger. The corresponding documentation will be sent to the Business Office.

d. Gifts-in-kind not recorded as University assets will be entered in the University Advancement database but not transferred to the general ledger.

Gift Acceptance Considerations

3 When entering into agreements with companies to accept “mega gifts” of software and hardware and be a test site for the company, the University needs to ascertain whether it is a gift, partial interest, or an exchange transaction according to the IRS and CASE standards.

34

• Is this a gift-in-kind or gift tangible or intangible personal property? • Does the gift assist the University in accomplishing its goals, mission or programs? Stewardship Gifts-in-kind will be processed and receipted within two business days of being notified of the University’s possession of them. See the Gift Acknowledgement and Stewardship section for details. Campaign and Annual Counting Guidelines • University Advancement will count the gift at the educational discount value and/or the

value the institution would have paid had it purchased the item outright from the vendor. In the case of deep discounts or bargain sales, the discounted amount will be recorded as the gift.

• A person’s or organization’s time or service is not considered a charitable contribution and is not countable, regardless of whether the assistance is as a volunteer or a professional specialized service (accounting, legal work, consulting.)

• St. Edward’s follows Generally Accepted Accounting Principles (GAAP) and accounts for all gifts in its financial statements in accordance with Financial Standards Accounting Board (FASB) Rules 116 and 117.

Contacts Office of University Advancement 512-464-8826 Office of Financial Affairs 512-448-8413 Director of Advancement Services 512-448-8430 Director of Planned Giving 512-233-1401 Controller 512-448-8773 Gift and Data Specialist 512-448-8776 Accounts Receivable/Business Office 512-448-8785

35

SPLIT-INTEREST GIFTS I. Charitable Gift Annuities Definition A standard charitable gift annuity (CGA) is transaction where a person irrevocably transfers to an institution some property, such as cash or securities, and the institution agrees in a contract to pay the donor or other beneficiaries (maximum allowable of two beneficiaries) a guaranteed annuity for life. A deferred payment charitable gift annuity is almost identical in construct to the standard charitable gift annuity. The significant difference is that the contract stipulates some date in the future when payments to the donor or other beneficiaries will begin. Examples • Joan Donor is a 67 year old woman, recently widowed. She donates $100,000 in cash in

exchange for a one-life CGA. St. Edward’s agrees to pay her the current rate offered by the ACGA for her age, which is 6.2%. Each year, St. Edward’s will pay her $1,240. When she dies, the payments will terminate and the residuum of her gift will fund the school or program she designated.

• Jill and Jesse Donor are 74 and 82, respectively. They donate $280,000 in stock that is traded on the NYSE. In exchange for their donation, St. Edward’s agrees to a two-life gift annuity with the rate of 6.6%. They receive annual payments of $18,480. Jill dies, and Jesse continues to receive the full amount of the annuity. Jesse dies and the remaining funds will fund the school or program they designated.

Acceptance Policy a. In working with prospective gift annuity donors, care will be taken to assure that the person

entering into the annuity fully understands that the annuity gift is irrevocable and understands the nature of the fixed payment which will be payable to them. All prospective donors will be urged to seek advice of their own legal and/or tax counsel. The relevant University staff member will communicate clearly to the prospective donor that he or she represents St. Edward’s.

b. A University staff member will make every practical effort to meet personally with prospective gift annuity donors.

c. All gift annuities entered into with the University must predominantly benefit the University and in every instance must benefit exclusively charitable, religious or educational causes.