ssrn-id1631346

TRANSCRIPT

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 1

Asif Ahmed

BBA Student

Department of Accounting & Information Systems

Faculty of Business Studies

University of Dhaka, Bangladesh.

E-mail: [email protected]

Website: http://ssrn.com/author=1447219

June 30, 2010

“Ethics in Auditing; And Ethical Studies in

Different Accounting Bodies”

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 2

Abstracts

One of the most important activities of the professional public accountant around

the world is auditing to set the accountability and reliability of the provided

accounting information. In this regard ethics is one of the most important things

for an accountant. The base of ethics is come from the professional training and

professional education. The basic objective of this paper is to discuss the various

ethical dilemmas, threats, safeguard and steps of avoiding ethical threats in

selecting auditing engagement. The second part of the paper comprises of a

comparative study on the ethical studies provided by various public accounting

bodies around the world.

Methodology:

The report is mainly divided into two parts – the explanation of concepts of ethics

and studies of degrees of ethical studies in various public accountants’ bodies

around the world. To fulfill the requirement of preparing the first part of the

report data are collected mainly form the following sources –

1. Different books, study materials and journals on ethics and auditing.

2. IFAC Code of Conduct for professional accountant.

3. Websites of the various professional bodies around the world.

And for the information of the second part of the report are mainly collected form

the syllabus of various public accounting bodies. For measuring the degrees of

studies and for make it more comparable courses or section that are indicated

under ethical studies of the Institute of Chartered Accountants of England and

Wales (ICAEW) syllabus are considered under ethical studies.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 3

Introduction:

Accounting is a very valuable knowledge and important component for a market

economy. No economic activity would be possible without accountancy. It

provides information on financial position and profitability of operations. It is the

foundation of countries’ fiscal, monetary & financial systems and plays a key role

in ‘governance’ towards establishing accountability and transparency in the

economies. But high profile corporate collapses and fraud, with which accountants

have been associated as auditors, executives and directors have prompted

searching questions to be asked as to the integrity of the professional accountants

involved. The core issue in the context of the accountancy profession is the

statutory audit monopoly privilege enjoyed by public accounting practitioners and

the accountability that is demanded by that privilege. This monopoly is defended

by the profession on the grounds of the professions superior qualities of

independence, integrity, and of serving the public interest. The relationship of

these characteristics to ethical behavior is central too much of the criticisms

leveled at the profession over the past 30 years. The accountancy profession has

claimed to be both moral and ethical throughout the 20th century, but this

assertion has been questioned by the regulators / legislators / investors /

stakeholders.

Objective:

Based on the above mentioned criticism of public accountant, the objectives of

preparing this paper is to –

1. Discuss the basic concepts of ethics.

2. Discuss the necessity of ethics in accounting and auditing profession.

3. Types and sources of ethical threats of professional accountant, especially

public accountant (CPA) and chartered accountant (CA).

4. Discuss the process of avoiding ethical threats in auditing.

5. Measure the degree of ethical study of various professional accounting

bodies, like – AICPA, ICAEW, ICAB, ACCA etc, around the world.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 4

What is Ethics?

Ethics can be defined as the branches of philosophy concerns value regarding

human behavior pertaining to the rightness and wrongness of actions and to the

goodness and badness of the intent and consequences of such actions (Smith &

Lee, 2009). Ethics can be defined broadly as a set of moral principles or values.

Each of us has such a set of values, although we may or may not have considered

them explicitly. Philosophers, religious organizations and other groups have

defined in various ways ideal sets of moral principles or values. Examples of

prescribed sets of moral principles or values at the implementation level include

laws and regulations, religious doctrine, codes of business ethics for professional

and industry groups, and codes of conduct within individual organizations (Kabir,

2009). In other words, ethics is the set of moral standards for judging whether

something is right or wrong (Gitman & McDaniel, 2002).

Need of Ethics for Professional Accountants:

Now the question is why ethics is so much important in accounting and auditing

profession? There are several reasons for that. These are –

1. Professional accountants have a responsibility to consider the public

interest and maintain the reputation of the accounting profession. Personal

interest must not prevail over these duties (ICAEW, 2009 and 2010).

2. Accountants deal with a range of issues on behalf of clients. They often

have access to confidential and sensitive information. Auditors claim to

give an independent view (ICAEW, 2009 and 2010).

3. The professional sees himself or herself as responsible to the customer; the

mission is to solve the problem of the customer, to create the value that the

customer requires. If that value is not created, if problem is not solved, the

professional has not done his or her job. It is only by producing the result

that customer requires- by performing the entire process that yields that

result-that the professional discharges his or her responsibility (Kabir,

2009).

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 5

4. Technically, the professional accountants should carry out professional

services in accordance with the relevant technical and professional

standards. The professional accountants have a duty to carry out with care

and skill, the instructions of the client or employer in so far as they are

compatible with the requirements of integrity, objectivity and, in the case

of professional accountants in public practice, independence (Kabir, 2009).

To meet the need of compliance with the ethics a professional accountant should

conform to the technical and professional standards promulgated by:

a. International Federation of Accountants (IFAC) on International

Standards of Auditing (ISA);

b. International Accounting Standards Committee (IASC);

c. In line with the instructions of professional accounting body of the

country; and

d. Incompliance with requirements of corporate laws and relevant

regulatory bodies and legislation.

Fundamental Principles of Ethics:

International Federation of Accountants (IFAC) code of ethics for professional

accountants has prescribed five (5) fundamental principles. These are as follows –

Integrity: A professional accountant should be straight forward and honest in all

professional and business relationship.

Objectivity: A professional accountant should not allow bias, conflictive interest

or undue influence of others to override professional or business judgment.

Professional Competence and Due Care: A professional accountant has a

continuing duty to maintain professional knowledge and skill at the level required

to ensure that a client or employer receives competent professional service based

on current developments in practice, legislation and techniques. A professional

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 6

accountant should act diligently and in accordance with applicable technical and

professional standards when providing professional services.

Confidentiality: A professional accountant should respect the confidentiality of

information acquired as a result of professional and business relationships and

should not disclose any such information to third parties without proper and

specific authority unless there is a legal or professional right or duty to disclose.

Confidential information acquired as a result of professional and business

relationships should not be used for the personal advantage of the professional

accountant or third party.

Professional Behavior: A professional accountant should comply with relevant

laws and regulations and should avoid any action that discredits the profession.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 7

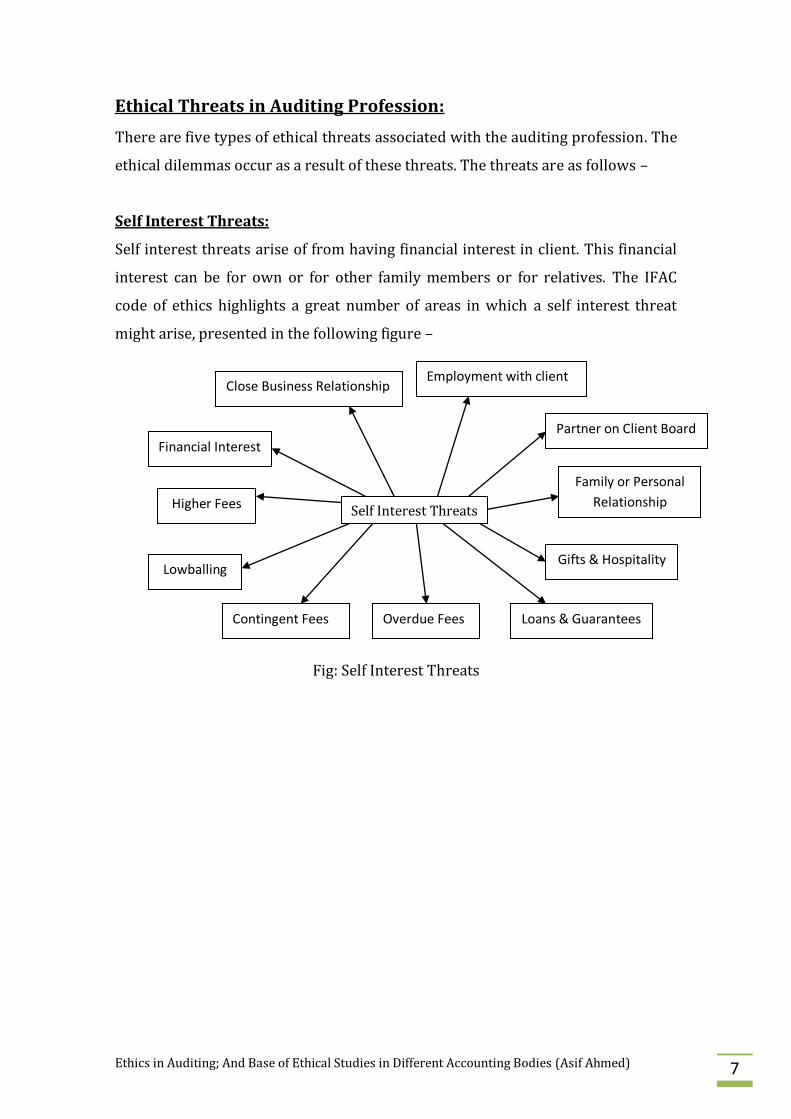

Ethical Threats in Auditing Profession:

There are five types of ethical threats associated with the auditing profession. The

ethical dilemmas occur as a result of these threats. The threats are as follows –

Self Interest Threats:

Self interest threats arise of from having financial interest in client. This financial

interest can be for own or for other family members or for relatives. The IFAC

code of ethics highlights a great number of areas in which a self interest threat

might arise, presented in the following figure –

Fig: Self Interest Threats

Self Interest Threats

Family or Personal

Relationship

Financial Interest Partner on Client Board

Close Business Relationship Employment with client

Loans & Guarantees

Lowballing

Higher Fees

Contingent Fees

Gifts & Hospitality

Overdue Fees

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 8

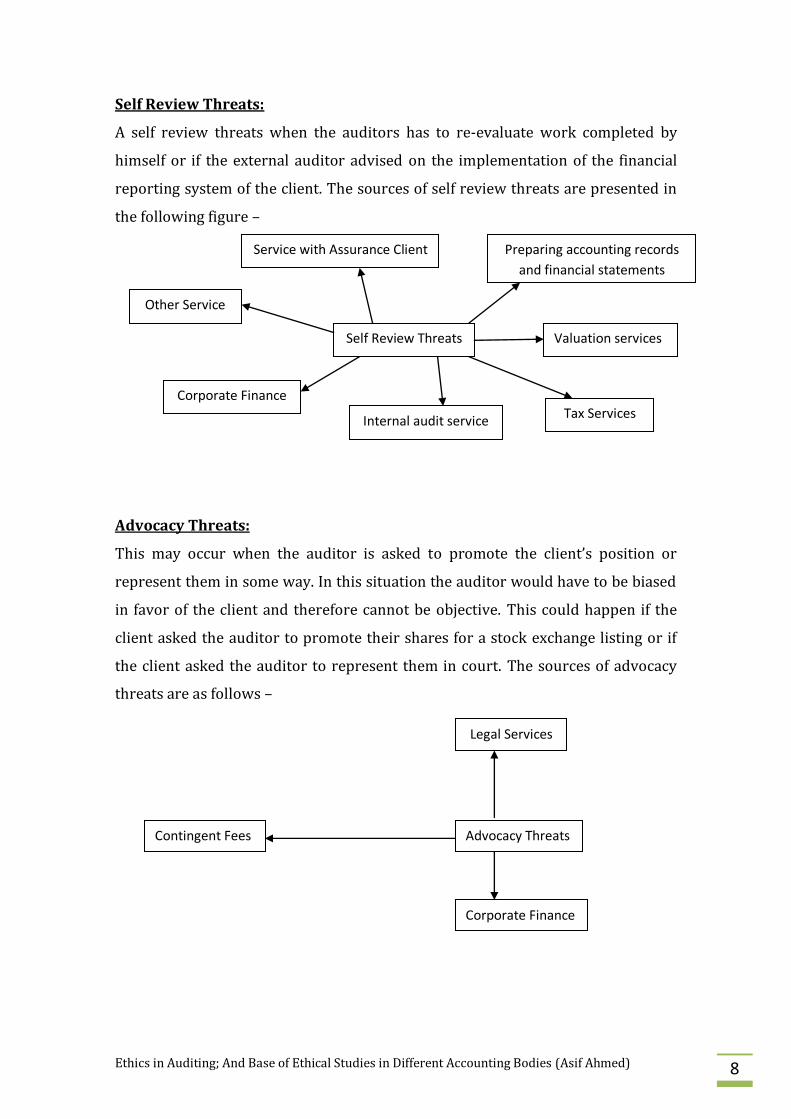

Self Review Threats:

A self review threats when the auditors has to re-evaluate work completed by

himself or if the external auditor advised on the implementation of the financial

reporting system of the client. The sources of self review threats are presented in

the following figure –

Advocacy Threats:

This may occur when the auditor is asked to promote the client’s position or

represent them in some way. In this situation the auditor would have to be biased

in favor of the client and therefore cannot be objective. This could happen if the

client asked the auditor to promote their shares for a stock exchange listing or if

the client asked the auditor to represent them in court. The sources of advocacy

threats are as follows –

Service with Assurance Client

Other Service

Self Review Threats Valuation services

Tax Services Internal audit service

Corporate Finance

Preparing accounting records

and financial statements

Advocacy Threats

Corporate Finance

Legal Services

Contingent Fees

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 9

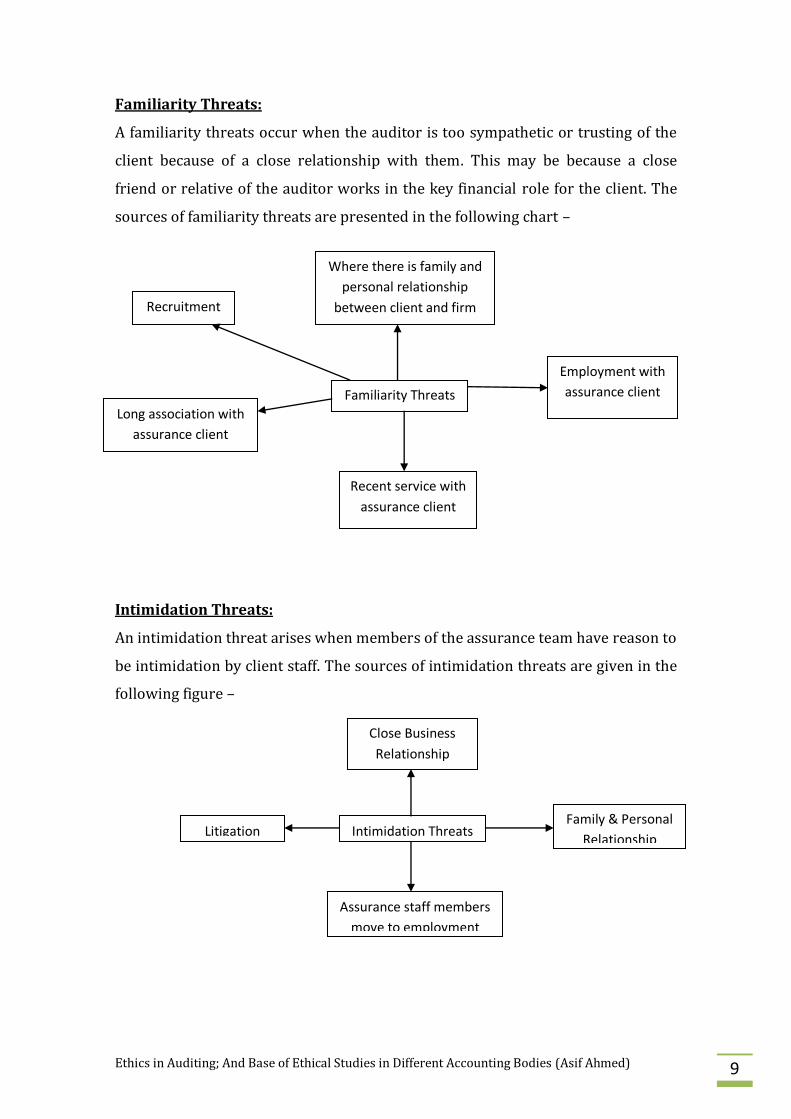

Familiarity Threats:

A familiarity threats occur when the auditor is too sympathetic or trusting of the

client because of a close relationship with them. This may be because a close

friend or relative of the auditor works in the key financial role for the client. The

sources of familiarity threats are presented in the following chart –

Intimidation Threats:

An intimidation threat arises when members of the assurance team have reason to

be intimidation by client staff. The sources of intimidation threats are given in the

following figure –

Familiarity Threats

Long association with

assurance client

Recent service with

assurance client

Employment with

assurance client

Where there is family and

personal relationship

between client and firm Recruitment

Intimidation Threats

Assurance staff members

move to employment

with client

Close Business

Relationship

Family & Personal

Relationship Litigation

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 10

Management Threat:

A management threat is indentified in the Accounting Practicing Board (APB)

ethical standards rather than in the IFAC code. A management threat arises when

the audit firm undertakes work involving making judgment and taking decision

that is the responsibility of management. There is a significant cross-over with

self-review threats here, and, as we have already seen, assurance provider are

forbidden to take decision behalf of management, therefore this risk should be

removed by avoiding situations or not accepting engagements where the client is

asking the assurance firm to take management decisions (ICAEW, 2009 and 2010).

Safeguard of the Threats:

The IFAC code of ethics also prescribed some safeguard against these threats. The

safeguards are discussed by dividing into two parts, as –

1. Safeguard created by the profession, legislation or regulation.

2. Safeguards within the working environment.

The safeguards that are created by the profession, legislation and regulation are as

follows –

a. Educational training and experience requirements for entry into the

profession.

b. Continuing professional development requirements.

c. Corporate governance regulations.

d. Professional standards.

e. Professional or regulatory and disciplinary procedures.

f. External review by a legally empowered third party of the reports, returns,

communication or information produced by a professional accountant.

The safeguards that are created by the working environment –

a. Involving an additional professional accountant to review the work done or

otherwise advice as necessary.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 11

b. Consulting an independent third parity, such as a committee of

independent directors, a professional regulatory body or another

professional accountant.

c. Rotating senior professionals.

d. Discussing ethical issues with those in charge of client governance.

e. Disclosing to those charged with governance the nature of services

provided and extend of fees charged.

f. Involving another firm to perform or reperform part of engagement.

To avoid the ethical threats the IFAC Code prohibits the following non-audit

services for audit clients:

1. Bookkeeping Services;

2. Valuation services;

3. Management decision making functions;

4. Broker-dealer or investment advisor services; and

5. Litigation support.

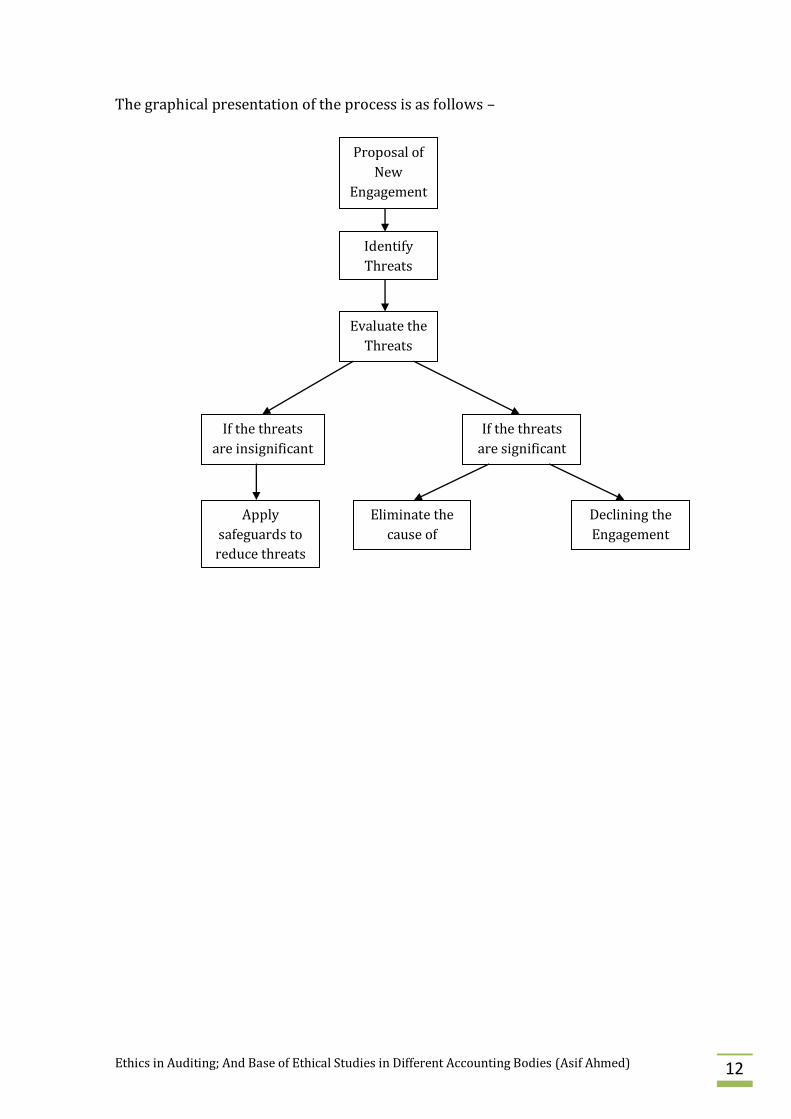

Steps in Accepting Auditing Engagement to Avoid Threats:

The steps that are prescribed by the IFAC code of ethics are as follows –

Step – 1: indentify threats of independence.

Step – 2: evaluate whether the threats are insignificant.

Step – 3: if the threats are insignificant, identified and apply safeguards to

eliminate risk or reduce it to an acceptable level.

It also recognizes that there may be occasion where no safeguard is available. In

such situation, it is only appropriate to –

1. Eliminating the interest or activities causing the threats.

2. Decline the engagement or discontinue.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 12

The graphical presentation of the process is as follows –

Proposal of

New

Engagement

Eliminate the

cause of

threats

Apply

safeguards to

reduce threats

Identify

Threats

If the threats

are significant

Evaluate the

Threats

If the threats

are insignificant

Declining the

Engagement

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 13

Base of Ethical Studies in Various Public Accounting Bodies:

In order to be a public accountant a person need acquire expertise in –

1. Practical Auditing Experiences under experienced qualified accountant.

2. Educational qualification runs through specific professional bodies.

As the educational qualification laid the foundation of the ethical standard,

following part of the paper discuss the base of ethical studies under some prime

accounting bodies around the world, especially ICAEW (England), AICPA (USA),

ACCA, NZICA etc. the analysis of the ethical studies are given below.

ICAEW:

Institute of Chartered Accountants of England and Wales (ICAEW) is one of the

most prestigious public accounting bodies in the world provide public accounting

degree designated as ACA (Associate Chartered Accountant). There are some

other accounting organizations in various countries around the world under

Memorandum of Association (MOU) and direct learning with ICAEW provide more

or less same studies. The professional bodies associated with the ICAEW are as

follows –

1. The Institute of Chartered Accountants of Bangladesh (ICAB).

2. The Canadian Institute of Certified Public Accountants (CICPA).

3. Direct Program through Chartered Accountants Student Society (CASS)

Cyprus.

4. The Institute of Chartered Accountants of India (ICAI).

5. Direct Program in Greece through PriceWaterHouse Coopers (PWC) of

Greece.

6. The Institute of Chartered Accountants of Pakistan (ICAP)

7. Direct Learning Program in Gulf.

8. Direct Learning Program in Malaysia through tuition of Sunway University

College.

9. Direct Full Learning Program in Mauritius.

10. Direct Full Learning Program in Romania.

11. Direct Learning Program in Russia through tuition of Moscow by Emile

Woolf International (EWI).

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 14

12. Direct Full Program or through the Institute of Certified Public Accountants

of Singapore (ICPAS).

Besides of these countries the study syllabus of Ireland and Scotland are also vary

similar to the ICAEW.

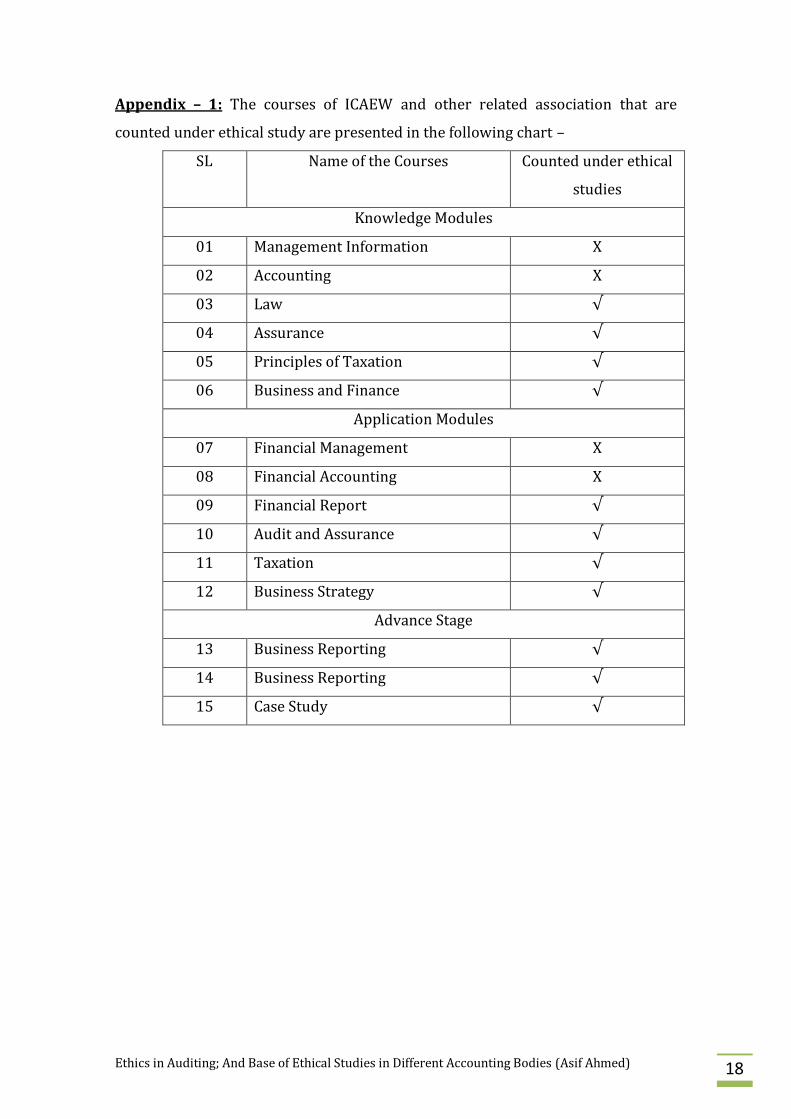

There are 15 courses offer by the ICAEW in three stages – Professional Knowledge

Modules, Professional Application Modules and Professional Advantage Stage. Out

of the 15 courses 11 courses (appendix – 1, page - 18) are marked by ICAEW as

base of the ethical studies. That means almost 73.33% of the studies under ICAEW

and its’ related associations are concentrated on ethics.

AICPA:

The American Institute of Certified Public Accountants (AICPA) the professional

body of public accountant in USA provides CPA degree. The studies for the CPA are

different depending on the requirements of different states of USA. Despite of the

examination determined by the each state candidates for the CPA are required to

seat for the “uniform CPA examination” at the last stage. The examination consists

of four sections - Auditing and Attestation, Business Environment and Concepts,

Financial Auditing and Reporting and Regulation. And all of these four sections,

that mean 100%, are related to ethical studies.

NZICA:

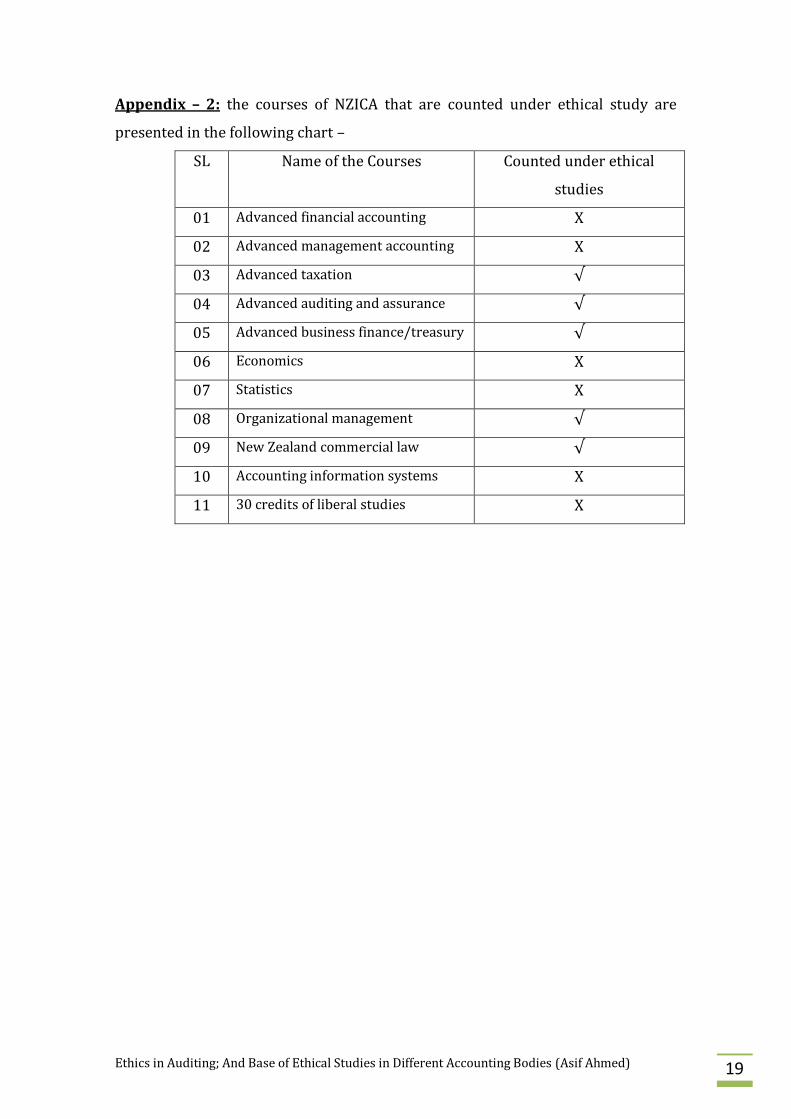

New Zealand Institute of Chartered Accountants (NZICA) is the public accounting

authority of New Zealand provides ACA degree. In the professional level studies of

NZICA there are 11 courses. Out of these 11 courses 5 courses are related to the

ethical studies (appendix – 2, page - 19). That means 45.45% of the studies are

related to ethics.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 15

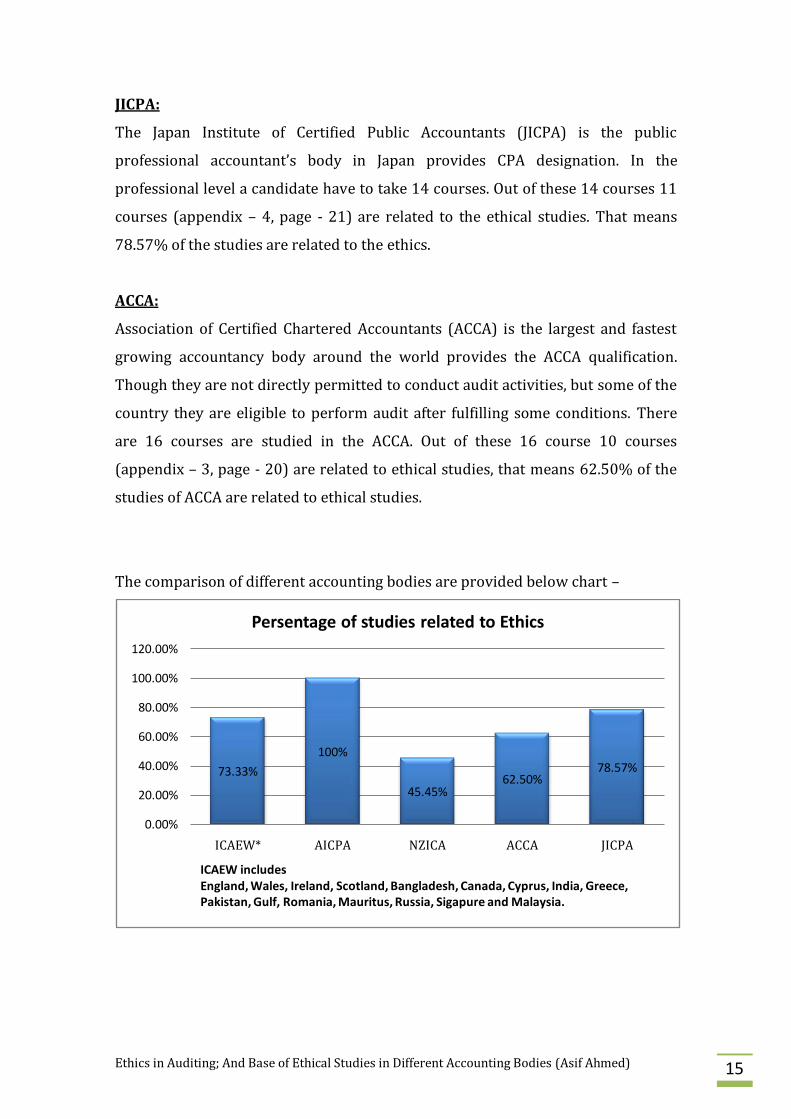

JICPA:

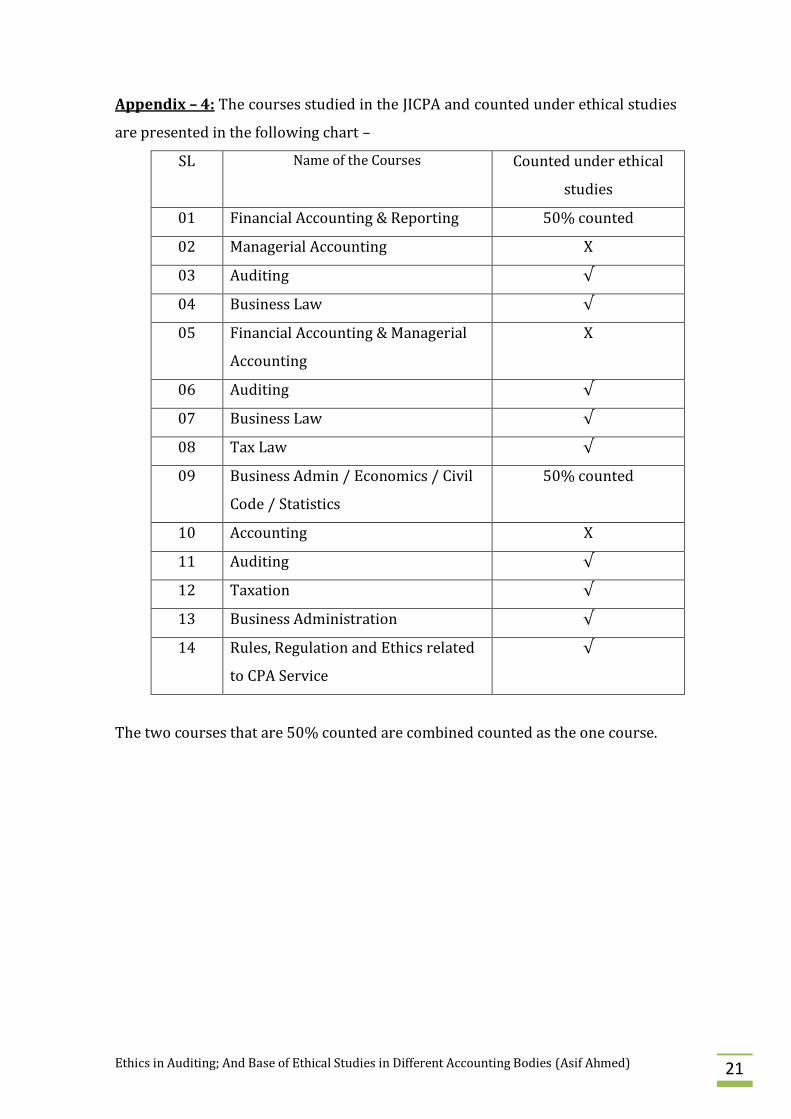

The Japan Institute of Certified Public Accountants (JICPA) is the public

professional accountant’s body in Japan provides CPA designation. In the

professional level a candidate have to take 14 courses. Out of these 14 courses 11

courses (appendix – 4, page - 21) are related to the ethical studies. That means

78.57% of the studies are related to the ethics.

ACCA:

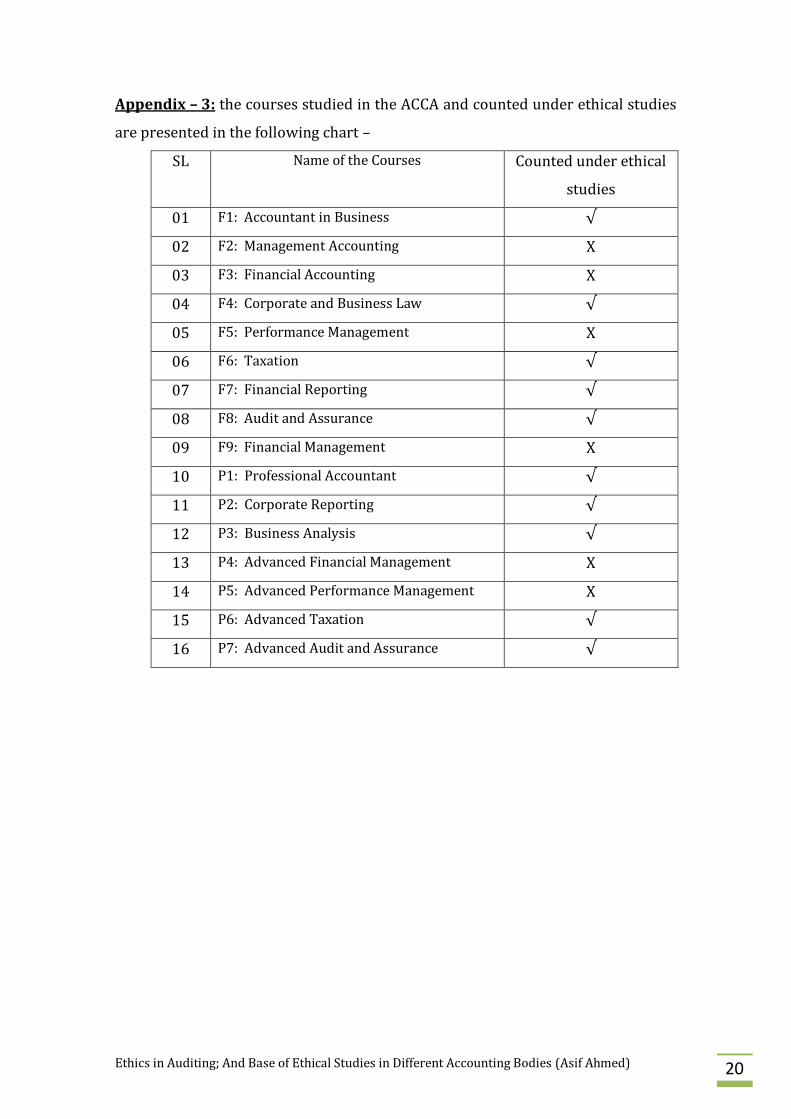

Association of Certified Chartered Accountants (ACCA) is the largest and fastest

growing accountancy body around the world provides the ACCA qualification.

Though they are not directly permitted to conduct audit activities, but some of the

country they are eligible to perform audit after fulfilling some conditions. There

are 16 courses are studied in the ACCA. Out of these 16 course 10 courses

(appendix – 3, page - 20) are related to ethical studies, that means 62.50% of the

studies of ACCA are related to ethical studies.

The comparison of different accounting bodies are provided below chart –

73.33%

100%

45.45%62.50%

78.57%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

ICAEW* AICPA NZICA ACCA JICPA

ICAEW includes England, Wales, Ireland, Scotland, Bangladesh, Canada, Cyprus, India, Greece, Pakistan, Gulf, Romania, Mauritus, Russia, Sigapure and Malaysia.

Persentage of studies related to Ethics

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 16

Conclusion:

Form the studied made in this paper it is clears that all the accounting bodies are

maintain high level of ethical studies for the candidates. Most of the courses

offered by the bodies are related to ethics. Auditors, therefore, should observe the

code of ethics and maintain their independence while certifying and expressing

opinion on the financial statements. Accounting profession has important public

responsibilities. So as the professional accounting bodies are provided adequate

ethical studies to the professional accountants, is the duty of the auditors to

implement these studies to their practical field to ensure accountability and

reliability.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 17

References:

1. Aspects of Accounting code of ethics in Canada, Egypt, and Japan by L.

Murphy Smith (Texas A & M University), Kuo Hao Howard Lee (Texas A &

M University), November/December, 2009.

2. Ethics and Independence in Accountancy Profession by Mohammed Humayun

Kabir FCA (ICAB, Bangladesh), Continuing Professional Development (CPD)

Seminar paper, 2009.

3. “The Future of Business” by Lawrence J. Gitman (San Diego State

University) and Carl McDaniel (University of Texas, Arlington), Chapter 4

(page 98 – 135), Interactive Edition, South-Western College Publishing

USA, 2002.

4. Assurance Study Manual, ACA Professional Stage Knowledge Level, The

Institute of Chartered Accountants of England and Wales (ICAEW), for

exams in 2009 and 2010.

5. Code of Ethics for Professional Accountants by Nasir Uddin Ahmed, FCA

(Bangladesh), December, 2008.

6. International Federation of Accountants (IFAC) Code of Ethics for Accountants.

7. Syllabus for ACA, ICAEW.

8. Syllabus for uniform CPA examination, AICPA.

9. Syllabus of the ACCA, ACCA Global.

10. Syllabus of the CA, NZICA.

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 18

Appendix – 1: The courses of ICAEW and other related association that are

counted under ethical study are presented in the following chart –

SL Name of the Courses Counted under ethical

studies

Knowledge Modules

01 Management Information X

02 Accounting X

03 Law √

04 Assurance √

05 Principles of Taxation √

06 Business and Finance √

Application Modules

07 Financial Management X

08 Financial Accounting X

09 Financial Report √

10 Audit and Assurance √

11 Taxation √

12 Business Strategy √

Advance Stage

13 Business Reporting √

14 Business Reporting √

15 Case Study √

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 19

Appendix – 2: the courses of NZICA that are counted under ethical study are

presented in the following chart –

SL Name of the Courses Counted under ethical

studies

01 Advanced financial accounting X

02 Advanced management accounting X

03 Advanced taxation √

04 Advanced auditing and assurance √

05 Advanced business finance/treasury √

06 Economics X

07 Statistics X

08 Organizational management √

09 New Zealand commercial law √

10 Accounting information systems X

11 30 credits of liberal studies X

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 20

Appendix – 3: the courses studied in the ACCA and counted under ethical studies

are presented in the following chart –

SL Name of the Courses Counted under ethical

studies

01 F1: Accountant in Business √

02 F2: Management Accounting X

03 F3: Financial Accounting X

04 F4: Corporate and Business Law √

05 F5: Performance Management X

06 F6: Taxation √

07 F7: Financial Reporting √

08 F8: Audit and Assurance √

09 F9: Financial Management X

10 P1: Professional Accountant √

11 P2: Corporate Reporting √

12 P3: Business Analysis √

13 P4: Advanced Financial Management X

14 P5: Advanced Performance Management X

15 P6: Advanced Taxation √

16 P7: Advanced Audit and Assurance √

Ethics in Auditing; And Base of Ethical Studies in Different Accounting Bodies (Asif Ahmed) 21

Appendix – 4: The courses studied in the JICPA and counted under ethical studies

are presented in the following chart –

SL Name of the Courses Counted under ethical

studies

01 Financial Accounting & Reporting 50% counted

02 Managerial Accounting X

03 Auditing √

04 Business Law √

05 Financial Accounting & Managerial

Accounting

X

06 Auditing √

07 Business Law √

08 Tax Law √

09 Business Admin / Economics / Civil

Code / Statistics

50% counted

10 Accounting X

11 Auditing √

12 Taxation √

13 Business Administration √

14 Rules, Regulation and Ethics related

to CPA Service

√

The two courses that are 50% counted are combined counted as the one course.