sri lanka : banking sector - john keells stock brokers [ jksb

TRANSCRIPT

1

Equities Sector Update

Sri Lanka : Banking Sector

A J

KSB

Res

earc

h P

ubli

cati

on

John Keells Stock Brokers (Pvt) LtdCompany No. PV 89130, Glennie Street,Colombo 2,Sri Lanka.

Tel: 9411 2421 101-9 (Gen.),9411 2326 003,9411 2439 047/8

Fax: 9411 2326 863,9411 2342 068

Yolan [email protected]

October 2007

LOW BANKING PENETRATION

Sri Lanka’s financial services sector is dominated by licensed commercialbanks (LCB) with a 48% share of assets while banking penetration in thecountry remains significantly low in comparison to regional nations despitea relatively high per capita GDP. The LCB segment is dominated by statebanks Peoples Bank and Bank of Ceylon accounting for 42% of LCBassets, while the four largest local private banks account for a share of39%. Operational inefficiencies in state and local banks have forced highercost to income ratios, while high effective tax rates and a low variance inrisk free rates on gov. securities and the AWPLR have lead to wide interestspreads contributing to the lower level of banking penetration in the country.

ASSET GROWTH AND ASSET QUALITYCredit to the private sector has grown by a CAGR of 21.1% since 2001,while average net advances in LCB’s have grown at a CAGR of 18.26% inthe same period, led by growth in consumer finance, leasing and pawningsub segments. Asset quality has also improved considerably over the last 5years with gross non performing assets declining from 15.3% in 2001 to5.54% in 2006 with provision cover also improving consistently over thesame period. Deposits have grown by a CAGR of 17% in the last fiveyears. High interest rates currently prevalent are expected to continue inthe short term, and decline modestly by approximately 100-150 basis pointsby year end 2008. Earnings however could be significantly affected byprovisions on rising non performing assets, should interest rates rise furtheror remain at current levels for over a 12mth – 18mth period.

NET INTEREST MARGINSNet interest margins have remained stable despite improvements in cost toincome ratios and a declining gross NPA ratio. In addition the re-pricing ofassets ahead of deposits in a rising interest rate environment has resultedin higher margins over a period of time. Central Bank statistics indicate arise in ROA from 0.62% in 2001 to 1.32% in 2006 among LCB’s.

REGULATORY ENVIRONMENTA Central Bank directive issued in January this year has restricted ownershipin banks to 15% of their voting rights. Capital requirements have alsoincreased with new risk weightings assigned to assets effectively increasingtotal capital adequacy requirements from 10% to 11%, while the adoptionof the Basel II framework from January 2008 would make regulatorycapital more sensitive to the risk exposure of the bank. This along withincreased provisioning requirements, a high effective tax rate and guidelineson distribution of profits has made the task of generating returns to attractfresh capital that is necessary to fuel growth, a much harder challenge.

EARNINGSWe expect earnings growth of 33% and 25% in FY07 and FY08 respectively,among the six listed banks covered in this report, stemming from healthynet interest margins, sound loan growth, and a steady decline in cost toincome ratios. The sector trades at a price/earnings multiple of 8.47xcarrying a 12.6% discount to the market.

Indexed ASPI / BFI

-

100

200

300

400

500

600

700

02-J

an-0

102

-May

-01

02-S

ep-0

102

-Jan

-02

02-M

ay-0

202

-Sep

-02

02-J

an-0

302

-May

-03

02-S

ep-0

302

-Jan

-04

02-M

ay-0

402

-Sep

-04

02-J

an-0

502

-May

-05

02-S

ep-0

502

-Jan

-06

02-M

ay-0

602

-Sep

-06

02-J

an-0

702

-May

-07

ASPI BFI

2007E PRICE P/E EPS GTH DVD YLD ROE ROAA

COMB 135 8.7 41% 4.4% 18% 1.55%

HNB 103 9.0 19% 4.9% 17% 1.21%

SAMP 120 5.3 46% 2.1% 18% 1.31%

NDB 162 9.3 40% 3.1% 12% 1.98%

DFCC 129 8.9 19% 3.9% 11% 2.32%

NTB 35 9.2 47% 2.9% 16% 0.92%

Source : JKSB Estimates

2

FINANCIAL SECTOR

The Financial Sector in Sri Lanka is dominated by Licensed CommercialBanks (LCB’s) which account for 48% of the assets of the country’sfinancial services sector. The country has 23 LCB’s of which 11 arelocal banks while 12 are foreign. The LCB segment is dominated bythe two large public banks, Bank of Ceylon and Peoples Bank whichtogether hold a 42% market share of LCB assets. The two state banksalong with the 4 largest local banks account for as much as 81% ofLCB assets.

Given the dominance of LCB’s in the financial sector, other alternativesources of finance to private enterprises are significantly smaller. Nearlytwo thirds of assets under licensed specialized banks arise from theNational Savings Bank which by design invests much of its funds intogovernment securities. In addition the nation’s provident funds whichaccount for 18% of the financial sector assets invests only a marginalportion of their funds outside of government securities. Thuscompetition to LCB’s from alternative sources of funds amount toapproximately 25% of the nation’s financial services sector assets.

The financial sector remains significantly under developed with regardto diversification and management of risk, with derivative instrumentsan active corporate debt market and securitization that feature stronglyin more developed financial sectors being largely absent in Sri Lanka atpresent. The sector has however advanced significantly in the provisionof services relating to provision of credit, mobilisation of savings forinvestment and the facilitation of trade and payments.

Low Banking Penetration in Sri Lanka

Sri Lanka exhibits a relatively low banking penetration, measured by aratio of Broad Money to GDP in comparison to regional standardsand neighbours India and Pakistan despite a relatively higher per capitaGDP. Sri Lanka also ranks lower to most regional nations apart fornations such as Thailand and India, in terms of the degree ofsophistication of the financial intermediary sector denoted by thecurrency to M1 ratio, which is representative of the currency incirculation against demand deposits. The higher the ratio the lower thedeemed level of sophistication in the country’s financial system. M2(M1 + Time and Savings Deposits) to GDP ratio, often used as ameasure of the depth of the financial sector or level of financialintermediation in the county, ranks Sri Lanka below most major regionalcountries. Some of the more developed nations increasingly exhibitsome level of disintermediation with funds being diverted away fromdeposits to debt instruments and equities. Given the significantly lowbanking penetration despite a relatively high per capita GDP and lowprivate sector credit to GDP, we surmise that Sri Lanka’s economy isunder banked.

Financial System in Sri Lanka (Assets)

Central Bank13%

Licensed Commercial Banks48%Licensed

Specialised Banks10%

Specialised Financial institutions (Primary dealers, S. leasing Companies, Co-orperative Rural Banks)4%

Non Bank Deposits Taking Financial Institutions4%

Providents Funds (EPF, ETF and Others)18%

Insurance Companys3%

Source : Central Bank Publications

Source : Central Bank Publications & Bank Annual Reports

LCB's Advances by Sector - 2002 - 2006

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Com

mer

cial

Fina

ncia

l

Agr

icul

tura

l

Indu

stria

l

Tour

ism

Hou

sing

Con

sum

ptio

n

Serv

ices

Oth

er

%

2002 2003 2004 2005 2006

Source : Central Bank Publications

Market Share - 2006 (Assets)

SAMP, 6%

NDB, 4%

SEYB, 8%

NTB, 3%

HNB, 12%

COMB, 13%Others, 12%

Peoples Bank, 20%

Bank of Ceylon, 22%

Australia 13% 14% 87% 70% 687% 497% 36,553 China 22% 24% 162% 139% 755% 568% 2,001 Hong Kong 43% 47% 281% 236% 650% 501% 27,466 India 54% 61% 70% 63% 130% 104% 797 Indonesia 43% 44% 41% 47% 95% 106% 1,640 Malaysia 24% 27% 128% 133% 526% 493% 5,718 Pakistan 32% 44% 47% 44% 146% 100% 830 Philippines 41% 47% 55% 58% 135% 125% 1,345 Singapore 29% 34% 125% 114% 427% 331% 29,917 South Korea 27% 31% 70% 76% 257% 241% 18,392 Thailand 71% 76% 104% 113% 147% 150% 3,136 SRI LANKA 52.0% 54.0% 35.45% 32.26% 68% 60% 1,355 Data Source : International Financial Statistics - IMF 2007

Currency/M1 2006

Currency/M1 2002

M2/GDP 2006

M2/GDP 2002

Overall Financial Penetration 2006

(Currency/M1)/M2/GDP

Overall Financial Penetration 2002

(Currency/M1)/M2/GDP

Per Capita GDP 2006 (Nominal)

3

ADVANCES AND DEPOSITS

Asset Mix

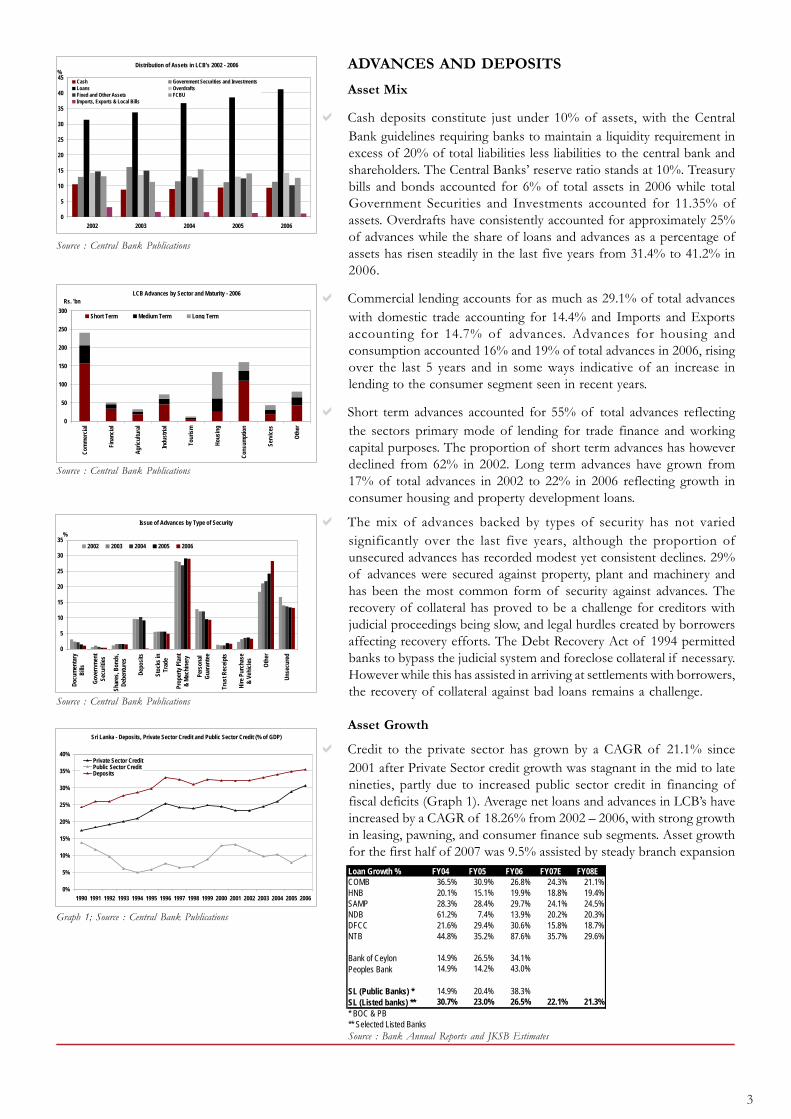

Cash deposits constitute just under 10% of assets, with the CentralBank guidelines requiring banks to maintain a liquidity requirement inexcess of 20% of total liabilities less liabilities to the central bank andshareholders. The Central Banks’ reserve ratio stands at 10%. Treasurybills and bonds accounted for 6% of total assets in 2006 while totalGovernment Securities and Investments accounted for 11.35% ofassets. Overdrafts have consistently accounted for approximately 25%of advances while the share of loans and advances as a percentage ofassets has risen steadily in the last five years from 31.4% to 41.2% in2006.

Commercial lending accounts for as much as 29.1% of total advanceswith domestic trade accounting for 14.4% and Imports and Exportsaccounting for 14.7% of advances. Advances for housing andconsumption accounted 16% and 19% of total advances in 2006, risingover the last 5 years and in some ways indicative of an increase inlending to the consumer segment seen in recent years.

Short term advances accounted for 55% of total advances reflectingthe sectors primary mode of lending for trade finance and workingcapital purposes. The proportion of short term advances has howeverdeclined from 62% in 2002. Long term advances have grown from17% of total advances in 2002 to 22% in 2006 reflecting growth inconsumer housing and property development loans.

The mix of advances backed by types of security has not variedsignificantly over the last five years, although the proportion ofunsecured advances has recorded modest yet consistent declines. 29%of advances were secured against property, plant and machinery andhas been the most common form of security against advances. Therecovery of collateral has proved to be a challenge for creditors withjudicial proceedings being slow, and legal hurdles created by borrowersaffecting recovery efforts. The Debt Recovery Act of 1994 permittedbanks to bypass the judicial system and foreclose collateral if necessary.However while this has assisted in arriving at settlements with borrowers,the recovery of collateral against bad loans remains a challenge.

Asset Growth

Credit to the private sector has grown by a CAGR of 21.1% since2001 after Private Sector credit growth was stagnant in the mid to latenineties, partly due to increased public sector credit in financing offiscal deficits (Graph 1). Average net loans and advances in LCB’s haveincreased by a CAGR of 18.26% from 2002 – 2006, with strong growthin leasing, pawning, and consumer finance sub segments. Asset growthfor the first half of 2007 was 9.5% assisted by steady branch expansion

Distribution of Assets in LCB's 2002 - 2006

0

5

10

15

20

25

30

35

40

45

2002 2003 2004 2005 2006

%

Cash Government Securities and InvestmentsLoans OverdraftsFixed and Other Assets FCBUImports, Exports & Local Bills

LCB Advances by Sector and Maturity - 2006

0

50

100

150

200

250

300

Com

mer

cial

Fina

ncia

l

Agr

icul

tura

l

Indu

stria

l

Tour

ism

Hou

sing

Con

sum

ptio

n

Serv

ices

Oth

erRs. 'bn

Short Term Medium Term Long Term

Issue of Advances by Type of Security

0

5

10

15

20

25

30

35

Doc

umen

tary

Bill

s

Gov

ernm

ent

Secu

ritie

s

Shar

es, B

onds

,D

eben

ture

s

Dep

osits

Stoc

ks in

Trad

e

Prop

erty

Pla

nt&

Mac

hine

ry

Pers

onal

Gua

rant

ee

Trus

t Rec

eipt

s

Hire

Pur

chas

e&

Veh

icle

s

Oth

er

Uns

ecur

ed

%

2002 2003 2004 2005 2006

Loan Growth % FY04 FY05 FY06 FY07E FY08ECOMB 36.5% 30.9% 26.8% 24.3% 21.1%HNB 20.1% 15.1% 19.9% 18.8% 19.4%SAMP 28.3% 28.4% 29.7% 24.1% 24.5%NDB 61.2% 7.4% 13.9% 20.2% 20.3%DFCC 21.6% 29.4% 30.6% 15.8% 18.7%NTB 44.8% 35.2% 87.6% 35.7% 29.6%

Bank of Ceylon 14.9% 26.5% 34.1%Peoples Bank 14.9% 14.2% 43.0%

SL (Public Banks) * 14.9% 20.4% 38.3%SL (Listed banks) ** 30.7% 23.0% 26.5% 22.1% 21.3%* BOC & PB** Selected Listed BanksSource : Bank Annual Reports and JKSB Estimates

Source : Central Bank Publications

Source : Central Bank Publications

Source : Central Bank Publications

Sri Lanka - Deposits, Private Sector Credit and Public Sector Credit (% of GDP)

0%

5%

10%

15%

20%

25%

30%

35%

40%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Private Sector CreditPublic Sector CreditDeposits

Graph 1; Source : Central Bank Publications

4

Leases outstanding among listed banks have significantly outpaced loangrowth, growing at a CAGR of 29.8% from 2002 to 2006. Leasesaccounted for just 9% of the loan book of listed banks, and is expectedto continue to be a key driver of growth in the lending portfolio ofbanks.

The number of credit cards issued has also grown significantly in thelast 5 years with total cards issued growing at a CAGR of 25.99%while total outstanding credit from credit cards has grown at a CAGRof 32.73% in the same period. Further non interest income in banksare being boosted by increased use of value added services (Table 3)as well as fees and commission income from trade finance activitiesand the steady depreciation of the SLR leading to substantial earningsfrom foreign exchange income via FCBUs. Non interest income nowaccounts for approximately a third of operating income.

Loan growth has been particularly strong over the last three years andwe expect growth in advances to slow down to an average of 22.1%this year and 21.3% for FY08. A tightening of monetary expansion bythe central bank to restrict growth in private sector credit in a bid tocurtail rising inflation has led to a sharp rise in interest rates this year.Thus plans for aggressive loan book growth have been somewhatrestricted given the general slow down in economic activity, with banksexercising greater prudence in expanding its loan book in a high interestrate environment. Interest rates are not expected to decline in the shortterm this year, but we expect interest rates to decline modestly byapproximately 100 to 150 basis points by year end 2008.

Deposits and Liabilities

Time and savings deposits account for 61.5% of total capital andliabilities in banks, with 76% of time and savings deposits arising fromthe commercial banking sector while the National Savings Bank accountsfor 17% of time and savings deposits. Non residents, primarilyrepresenting Sri Lankans employed abroad accounted for 23.3% oftime and savings deposits in 2006, down from 26.3% in 2004. Residentsin the country account for 76.1% of time and saving deposits whileaccounting for 78.6% of demand deposits. The GOSL accounted for19.4% of demand deposits in 2006.

Total deposits in LCB’s recorded a growth of 18.9% in 2006, whilegrowing at a CAGR of 17% from 2002 – 2006, despite treasury billrates continuing to earn a better yield than yields on bank fixed andsavings deposits. We estimate deposit growth of the above selectedlisted banks to record an average of 19% this year and 20% in FY08.

YOY % Growth in Assets and Liabilities of LCBs'

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999 2000 2001 2002 2003 2004 2005 2006*

AssetsNet Loans and AdvancesDepositsBorrowings

Source : Central Bank Publications

Table 3; Source : Central Bank Publications

2003 2004 2005 2006*

Internet Banking Transactions '000 188 439 874 1,162 * Annualised

Source : Bank Annual Reports and JKSB Estimates

Deposit Growth 2005 2006 2007E 2008ECOMB 29% 24% 22% 23%HNB 8% 15% 11% 13%SAMP 27% 27% 21% 22%NDB 26% 52% 20% 23%DFCC 38% 134% 35% 30%NTB 37% 44% 20% 22%SL (Listed banks) ** 21% 26% 19% 20%** Selected Listed Banks

Distribution of Capital and Liabilities in LCB's - 2002 - 2006

-

10

20

30

40

50

60

70

DemandDeposits

Time andSavingsDeposits

Domestic Inter-Bank

Borrowing

ForeignBorrowing

Other Liabilities Capital &Reserves

%

2002 2003 20042005 2006

YOY Deposit and Bank Borrowings Growth / AWDR % T Bill

-40%

-20%

0%

20%

40%

60%

80%

100%

1999 2000 2001 2002 2003 2004 2005 2006

0

2

4

6

8

10

12

14

16

18

20%

DepositsBorrowingsAWDR1yr T Bill

Source : Central Bank Publications

Source : Central Bank Publications

YOY Credit and Deposit Growth

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Private Sector Credit Public Sector CreditDeposits

Source : Central Bank Publications

5

Asset Quality

Non performing advances in commercial banks have declinedsignificantly over the last five years from a gross NPA ratio of 15.30%in 2001 to 5.54% in 2006, despite strong growth in advances.

Improved resources in terms of expertise and information systemswith regard to risk assessment and credit monitoring coupled with moreeffective internal systems and loan approval procedures has contributedsignificantly to the improvement in asset quality over the last 5 years,as depicted with a decline in the NPA Ratio. The decline in the NPAratio was also assisted by the decline in interest rates witnessed between2001 and 2003. Further banks have also exercised greater prudence inprovisioning for bad loans with provision cover also improvingappreciably since 2001 (Graph 2). Public sector banks as well as listedbanks recorded consistent in improvement in asset quality as well as anincrease in their loan loss reserves (Table 4 & 5).

The high interest rates this year have resulted in a sharp rise in nonperforming loans in the first half of FY07. NPL’s increased by 9.12%last year among the 6 selected listed banks listed in Table 6, while 1Hresults for FY07 indicate a 14.87% increase in NPL’s in the first sixmonths for the same group of listed banks. NPLs ratios have howeverremained healthy given continued strong loan growth, while bankrecovery efforts should mitigate the adverse growth in NPL’s in thesecond half of this year. However 1H growth in NPL’s indicate thatthe consistent improvement seen in asset quality over the past fewyears may reverse should the present high interest rate environmentpersist over the next 12mths. Most banks exhibiting improved provisioncover will be cushioned by the rise in NPL’s, but earnings may beadversely affected if rates remain high over a 12 - 18 mth period.

NPL & Provision Cover / AWPLR

-

2

4

6

8

10

12

14

16

18

20

1998 1999 2000 2001 2002 2003 2004 2005 2006

%

-

10

20

30

40

50

60

70

80%

Gross Non-performing Advances RatioNet Non-performing Advances RatioProvision Coverage Ratio (RHS)AWPLR (RHS)

YOY Assets and NPA Growth

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1999 2000 2001 2002 2003 2004 2005 2006*

Net Loans and AdvancesGross Non-performing Advances Net Non-performing AdvancesProvision for Bad and Doubtful Advances

Graph 2; Source : Central Bank Publications

Source : Central Bank Publications

NPL Coverage FY04 FY05 FY06 FY07E FY08ECOMB 50.0% 53.9% 60.4% 59.6% 62.2%HNB 48.8% 63.5% 65.6% 62.5% 62.4%SAMP 64.4% 82.4% 82.3% 88.3% 92.3%NDB 86.5% 125.6% 188.2% 156.8% 123.2%DFCC 32.0% 47.0% 37.5% 39.6% 43.6%NTB 48.6% 56.4% 58.3% 60.0% 62.0%

Bank of Ceylon 70.3% 82.2% 72.2%Peoples Bank 87.4% 87.2% 92.3%

SL (Public Banks) * 79.8% 85.1% 82.9%SL (Listed banks) ** 53.5% 67.7% 69.0% 67.2% 67.7%* BOC & PB** Selected Listed Banks

Table 5; Source : Bank Annual Reports and JKSB Estimates

Table 4; Source : Bank Annual Reports and JKSB Estimates

NPL Ratio FY04 FY05 FY06 FY07E FY08ECOMB 4.53% 3.43% 2.79% 2.97% 3.11%HNB 10.30% 8.21% 7.46% 6.93% 6.38%SAMP 8.64% 6.19% 5.52% 5.16% 4.85%NDB 7.08% 4.32% 2.22% 1.98% 1.90%DFCC 8.89% 4.95% 4.90% 5.00% 5.00%NTB 6.44% 6.12% 5.37% 5.26% 5.32%

Bank of Ceylon 11.68% 7.61% 6.49%Peoples Bank 14.53% 11.78% 7.65%

SL (Public Banks) * 13.11% 9.59% 7.06%SL (Listed banks) ** 7.69% 5.57% 4.80% 4.62% 4.47%* BOC & PB** Selected Listed Banks

YOY Change in NPL's FY04 FY05 FY06 FY07E FY08ECOMB -4.44% -0.89% 3.14% 32.19% 27.03%HNB -15.80% -8.21% 8.87% 10.43% 9.88%SAMP -2.90% -7.98% 15.71% 15.87% 17.07%NDB -9.97% -34.55% -41.46% 7.36% 15.20%DFCC -5.18% -27.86% 29.04% 18.24% 18.65%NTB 52.18% 28.41% 64.68% 32.84% 31.06%SL (Listed banks) ** -9.01% -11.01% 9.12% 17.51% 17.33%

Table 6; Source : Bank Annual Reports and JKSB Estimates

6

INTEREST SPREADS AND OPERATING COSTS

Sri Lanka has consistently exhibited high interest spreads and is oftenseen as a fundamental reason for the nation’s relatively low credit tothe private sector as a % of GDP and a consequently low level ofbanking penetration. Net interest margins among banks in Sri Lankaare some of the highest in the region, comparing favourably only toPakistan and Indonesia in 2006.

Cost / Income Ratio

The two large state banks Bank of Ceylon and Peoples Bank whichaccount for 42% of commercial banking assets have consistentlyreported high cost to income ratios due to operational inefficiencies.The large market shares held by the two state banks therefore permitthe local private banks to enjoy even higher margins than the statebanks despite themselves ranking lower than banks in most regionalnations. Sri Lanka also exhibits a fairly volatile interest rate environment,and when rates change assets are predictably re-priced ahead of depositsthus contributing to higher net interest margins over a period of time.

Cost / Income ratios of local banks excluding VAT compare morefavorably to regional countries with banks such as COMB and the twopredominantly development banks NDB and DFCC also exhibit asound cost to income ratio (excl. VAT). Cost to Income ratios excludingVAT in banks such as COMB compares well even with the bankingsector in more developed nations indicating that curtailing of operatingcosts among banks in Sri Lanka is possible if a banks’ operating modelis managed effectively

Cost / Income FY04 FY05 FY06COMB 56.5% 54.6% 50.4%HNB 70.8% 63.3% 67.7%SAMP 74% 71% 64%NDB 63.5% 63.3% 56.0%DFCC 43.4% 44.2% 45.1%NTB 79.7% 76.8% 71.5%

Bank of Ceylon 67.8% 80.3% 79.1%Peoples Bank 73.1% 71.6% 72.8%

SL (Public Banks) * 70.4% 75.7% 75.8%SL (Listed banks) ** 63.7% 60.8% 59.2%SL 67.2% 67.9% 67.4%* BOC & PB** Selected Listed Banks

Source : Bank Annual Reports and JKSB Estimates

Interest Rates

0

2

4

6

8

10

12

14

16

18

20

22

24

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

%

AWPLRAWDRT Bill RateSPREAD

Source : Central Bank Publications

FY06Australia 2.3China 2.6Hong Kong 1.9India 3.1Indonesia 6.3Malaysia 2.4Pakistan 5.6Philippines 3.9Singapore 2.1South Korea 3.1Taiwan 2.0Thailand 3.4SL (Public Banks) * 4.0SL (Listed banks) ** 4.3* BOC & PB** Selected Listed Banks

NIM FY06Australia 47.34China 44.89Hong Kong 34.83India 57.29Indonesia 53.14Malaysia 42.75Pakistan 32.25Philippines 60.55Singapore 42.87South Korea 44.19Taiwan 45.24Thailand 55.19SL (Public Banks) * 75.8SL (Listed banks) ** 59.2* BOC & PB** Selected Listed Banks

Cost / income

Source : Bank Annual Reports; Deutsche Bank Global Markets Reserach, Asia Pac (ExJapan) Bank, Sept. 17th 2007

Cost / income (Excl. VAT) FY04 FY05 FY06 FY07E FY08ECOMB 50.5% 47.4% 41.9% 40.5% 40.2%HNB 66.7% 61.4% 59.9% 60.4% 59.0%SAMP 68.1% 65.0% 55.3% 54.8% 54.4%NDB 58.4% 58.0% 44.2% 47.1% 47.6%DFCC 36.3% 36.0% 34.9% 36.0% 37.1%NTB 76.4% 72.5% 71.5% 69.8% 67.1%

Bank of Ceylon 62.2% 74.0% 69.9%Peoples Bank 65.8% 64.8% 63.8%

SL (Public Banks) * 63.9% 69.2% 66.7%SL (Listed banks) ** 58.4% 55.6% 50.9% 51.0% 50.4%* BOC & PB** Selected Listed Banks

Source : Bank Annual Reports and JKSB Estimates

7

Implications of high Cost/Income ratio

Local banks have steadily improved the cost / income ratios over thepast few years. However despite these improvements, lower NPL’sand consequently lower provision expense, have not resulted in anarrowing of spreads but rather an increase in returns for the bankwith net interest margins remaining stagnant. (Table 7). The retentionof higher margins has helped banks to generate sufficient earnings tofund future growth or attract investors to infuse new capital to fundgrowth. However wider spreads act as a constraint to increase bankingpenetration to under banked segments such as the SME and consumersegments.

The VAT on financial services of 20% charged to banks significantlycontributes to a higher cost structure. Regulations including new riskweightings and the adoption of Basel II regulations from January 2008and the requirement to build up general provisions to 1% of performingloans have made growing retained earnings and raising of fresh capitala challenge for the banks. Most local private banks which are listedhave successfully raised Tier 1 Capital through rights issues in the recentpast. However increasing constraints on earnings brought about byincreased provisioning requirements and the high effective tax ratescoupled with guidelines on distribution of profits, makes the task ofgenerating sufficient returns to attract investors to persist in infusingfresh capital, much harder.

Risk free government securities have also closely tracked the averageprime lending rate which has also been a key contributor in facilitatingbanks to maintain high rates and high spreads. The end result howeverof wide spreads is the stifling of growth of private sector credit,particularly to SME’s while acting as a constraint to deepen the level ofbanking penetration in the country.

Further as mentioned earlier in this report, with the commercial bankingsector being the dominant segment in the nations financial sector,alternatives sources of funds for private enterprises are smaller. Therebyprivate enterprises have to endure higher funding costs while bankscontinue to grow lending portfolios at a steady pace while retaininghigh margins. In this context while taxes on the sector are unlikely to belowered in the short and medium term, it becomes increasingly necessaryfor state banks to lower their operating cost structure and take the leadin facilitating the narrowing of spreads in the sector, with competitivepressures inevitably forcing the smaller local private banks to follow.This is essential for growth in credit to the private sector and a greaterlevel of banking penetration in the SME and consumer segments.

Personnel Cost/Av. Assets FY04 FY05 FY06 FY07E FY08ECOMB 1.4% 1.3% 1.3% 1.2% 1.2%HNB 1.5% 1.5% 1.5% 1.6% 1.8%SAMP 1.4% 1.4% 1.3% 1.3% 1.4%NDB 1.7% 1.8% 1.3% 1.4% 1.5%DFCC 1.1% 1.1% 1.0% 1.0% 1.0%NTB 1.3% 1.6% 1.7% 1.5% 1.5%SL (Listed banks) ** 1.4% 1.4% 1.4% 1.4% 1.4%

Source : Bank Annual Reports and JKSB Estimates

Licensed Comemrcial Banks : NIM, NPL, Cost/Income & ROE

(15)(10)(5)

-5

101520253035404550556065707580

1998 1999 2000 2001 2002 2003 2004 2005 2006

%

Interest Margin(h)Gross Non-performing Advances RatioReturn on Equity (ROE)Cost to Income Ratio

Table 7; Source : Central Bank Publications

AWPLR and 3mth T Bill Rate

5

7

9

11

13

15

17

19

21

23

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

%

AWPLR3mth T Bill Rate

Source : Central Bank Publications

8

CHANGES IN THE REGULATORY ENVIRONMENT

Ownership

The maximum ownership of the issued capital carrying voting rightsof banks has been limited to 15% following a directive issued by theCentral Bank in January 2007. This limit will apply to the acquisition orholding of shares by all categories of shareholders individually or in agroup, whether acquired directly or indirectly through a nominee orthrough parties acting in concert. In the case of Licensed CommercialBanks acquisition of voting rights in excess of 10% requires priorapproval of the Monetary Board with the consent of the Minister ofFinance. Shareholders carrying voting rights in excess of 15% havebeen requested to dispose / reduce their respective shareholding to15% during a period not exceeding 5 years from April 2007, as specifiedby the Monetary Board on a case by case basis. While specific dateshave not been disclosed shareholders of certain banks have been issuedwith a shorter period of time in which to reduce their holding to themaximum limit of 15%. DFCC Bank reported to the CSE that theMonetary Board had requested the Bank to reduce its’ stake in COMBfrom its’ present 28.99% to 15% by October 2008. It is understoodthat DFCC Bank will be requesting an extension, given that the stakein COMB was acquired from Standard Chartered Bank at the requestof the Central Bank.

Capital Adequacy

Tier 1 and Total Capital Adequacy Ratios have been maintained at 5%and 10% of risk weighted assets, respectively. However new riskweightings assigned to different classes of assets have effectivelyincreased the total capital requirement to approximately 11% of riskweighted assets.

Provisioning Requirements

The Central Bank has required all banks to make a mandatory generalprovision of 0.1% per quarter for 10 consecutive quarters totaling a1% general provision on all performing loans and overdue NPL’s inarrears for 3 to 6 month commencing from December 2007. Mostbanks, particularly the larger banks have proactively begun providingfor the short fall in this requirement well ahead of the stipulated timeframe given by the Central Bank.

Mandatory Code of Corporate Governance in Licensed Banks

The Central bank released an exposure draft of the above for publiccomment, with the intention of articulating a corporate governancecode intended to make the Board of Directors of banks responsibleand accountable for management affairs of banks inclusive of riskmanagement. The draft has also prescribed principle based rules onresponsibilities of directors, chairman and CEO and criteria for fitnessand propriety of directors, management of related party transactionsand conflicts of interest and functions of board appointed committeesto supervise the executive management.

Requirements on maximum amount of accommodation grantedby Banks

The central bank issued revisions to prudential requirements on singleborrower limits of licensed banks in order to mitigate the banks’ credit

9

concentration risk arising from advances and other facilities granted tolarge clients. While the maximum limits remain the same as specifiedunder the Banking Act, the accommodations that are subject to fallwithin limits of the maximum amount specified now includes any loan,overdraft or advance inclusive of finance lease, hire purchase, andreverse agreements against debt securities, investments in debenturesand other debt instruments and any commitment to grant any loan oroverdraft or advance or other facility, including a commitment to accepta contingent liability. These are subject to certain types of securitiesthat are excluded from the computation of accommodations for thepurpose of calculating the maximum limits. These for example interalia include advances granted against cash, gold government securitiesetc.

Implementation of Basel II

Banks have been geared toward compliance with Basel II from 2008onwards under the guidance of the Central Bank’s Bank SupervisionDepartment. The new capital accord to be adopted seeks to effectivelycombine a risk sensitive capital requirement with risk mitigationpractices, by seeking a balance between internal risk systems andsupervisory prudence. The accord is reinforced via a minimum capitalrequirement, a supervisory review process and market discipline. TheBasel II framework permits a preferential risk weighting of 75% forclaims against the regulatory retail portfolio however the Basel IIframework also introduces a capital charge for operational risk. Mostbank have geared themselves with the process and disclosurerequirements of the Basel II framework. With regard to the minimumcapital requirement, it is clear that while banks have been given flexibilityin terms of selecting a measurement option, regulatory capital hasbeen made more sensitive to the risk exposure of the bank.

10

SECTOR COMPARISON

The Banking Finance and Insurance index has grown in line with the ASPIsince the CSE’s resurgence in late 2001 and the sustained appreciationwitnessed through the years of the cease fire agreement. The ASPI hasgrown at a CAGR of 29.2% while the BFI has marginally underperformedthe ASPI, growing at a CAGR of 28.2% in the same period.

SAMP appears the most undervalued of the six banks covered in thisreport. Attractive valuations with a P/E multiple of 5.3x FY07 earnings,with impressive earnings growth and sound fundamentals in terms ofasset quality, good provision cover and a healthy ROE. However thebank does have a higher cost to income ratio as well as a lower equity toassets ratio in comparison to some of its established peers such as COMB.

COMB has consistently demonstrated superior fundamentals with regardto earnings and asset growth, a low cost to income ratio and a healthy NPLratio. The banks’ growth prospects in Sri Lanka and in Bangladesh arereflected in its higher valuations particularly after its improved capitalposition following a rights issue earlier this year. HNB has commanded ahigher valuation in the market this year stemming from its substantialimprovement in asset quality over the last 3 years which has contributedto improved profitability from lower provision expense.

Aggressive growth over the last 3 years has seen NTB also commanding apremium to the sector reflecting its prospects of strong earnings growth inthe short to medium term. We believe the bank will be successful in infusingfresh capital within the next 12 months which it requires in order to maintainits current growth momentum.

NDB and DFCC are banks in transition from core operators in the projectfinance segment, to increasing exposure in commercial banking. NDB andDFCC have a superior capital position in comparison to the othercommercial banks in the market which would provide a strong base for itsgrowing retail and corporate lending portfolios. NDB offers a diversifiedportfolio of financial services providing significant opportunities of crossselling of services within the group. Much of DFCC’s growth would liewith its commercial banking subsidiary DFCC Vardhana, which mayculminate in a merger over the next few years. In addition DFCC’s associatestake in COMB which has been a significant contributor to earnings in thepast is likely to be pruned down over the next few years due to new central

bank guidelines on ownership.

Tabled overleaf are key indicators of a selected pool of listed banks coveredin this report

Indexed Selected Listed Banks (Adjusted for Bonus and Rights)

50

100

150

200

250

300

350

02/0

1/20

03

02/0

4/20

03

02/0

7/20

03

02/1

0/20

03

02/0

1/20

04

02/0

4/20

04

02/0

7/20

04

02/1

0/20

04

02/0

1/20

05

02/0

4/20

05

02/0

7/20

05

02/1

0/20

05

02/0

1/20

06

02/0

4/20

06

02/0

7/20

06

02/1

0/20

06

02/0

1/20

07

02/0

4/20

07

02/0

7/20

07

COMB HNB SAMP NTB

NDB DFCC

11

Sour

ce :

Ban

k A

nnua

l R

epor

ts an

d JK

SB E

stim

ates

Valu

atio

nsFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EC

OM

B2.

4

2.

1

2.

1

1.

6

1.

3

22

.515

.812

.48.

76.

821

%42

%28

%41

%29

%4.

4%4.

4%4.

4%4.

4%4.

4%H

NB

2.7

2.2

1.9

1.5

1.2

32.0

13.6

10.8

9.0

7.2

-50%

134%

26%

19%

26%

3.4%

3.9%

4.9%

4.9%

4.9%

SAM

P1.

9

1.

4

1.

2

1.

0

0.

8

12

.09.

77.

75.

34.

2-7

%25

%25

%46

%25

%1.

7%1.

7%2.

1%2.

1%2.

1%N

DB

1.6

1.5

1.4

1.1

1.0

18.9

12.8

13.1

9.3

7.8

-37%

47%

-2%

40%

20%

3.6%

3.7%

2.5%

3.1%

3.1%

DFC

C1.

7

1.

4

1.

3

1.

0

0.

9

12

.49.

910

.68.

97.

7-1

%25

%-6

%19

%15

%4.

3%4.

7%3.

9%3.

9%3.

9%N

TB3.

3

3.

0

1.

5

1.

5

1.

2

96

.835

.313

.69.

26.

7-8

2%17

4%15

9%47

%39

%1.

4%1.

4%2.

9%2.

9%2.

9%SL

(Lis

ted

bank

s) **

2.1

1.8

1.6

1.3

1.1

20.0

13.2

11.2

8.5

6.8

-19%

51%

18%

33%

25%

2.6%

2.8%

2.6%

2.8%

2.8%

PBV

PER

EPS

GR

OW

THD

VD Y

LD

Prof

itabi

lity

FY04

FY05

FY06

FY07

EFY

08E

FY04

FY05

FY06

FY07

EFY

08E

FY04

FY05

FY06

FY07

EFY

08E

FY04

FY05

FY06

FY07

EFY

08E

CO

MB

11%

13%

17%

18%

19%

12%

14%

17%

21%

21%

1.17

%1.

32%

1.34

%1.

55%

1.64

%3.

7%3.

6%3.

7%3.

8%3.

9%H

NB

8%16

%17

%17

%17

%9%

18%

19%

19%

19%

0.50

%1.

05%

1.17

%1.

21%

1.35

%3.

6%4.

4%4.

8%5.

1%5.

2%SA

MP

16%

14%

15%

18%

19%

17%

17%

17%

20%

21%

1.11

%1.

14%

1.12

%1.

31%

1.37

%4.

5%4.

6%4.

5%5.

1%4.

8%N

DB

8%12

%10

%12

%12

%9%

12%

10%

13%

13%

1.37

%1.

68%

1.56

%1.

98%

1.98

%4.

4%4.

7%4.

9%5.

0%5.

0%D

FCC

13%

14%

13%

11%

11%

14%

16%

13%

13%

12%

3.28

%3.

32%

2.43

%2.

32%

2.24

%5.

5%5.

2%4.

7%4.

6%4.

5%N

TB3%

9%11

%16

%18

%3%

9%15

%16

%20

%0.

22%

0.53

%0.

89%

0.92

%1.

07%

2.9%

4.1%

3.9%

3.9%

4.0%

SL (L

iste

d ba

nks)

**11

%14

%14

%15

%16

%11

%15

%15

%17

%17

%1.

11%

1.41

%1.

37%

1.50

%1.

58%

4.0%

4.3%

4.3%

4.5%

4.5%

RO

AE

RO

AA

NIM

RO

E

Effic

ienc

yN

on In

t. In

c./O

p In

c.FY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EC

OM

B36

%33

%36

%36

%37

%57

%55

%50

%51

%50

%3.

3%3.

0%2.

9%2.

9%3.

0%51

%47

%42

%41

%40

%H

NB

36%

35%

31%

33%

34%

71%

63%

68%

68%

67%

3.8%

3.8%

4.4%

4.7%

5.0%

67%

61%

60%

60%

59%

SAM

P38

%32

%37

%37

%37

%74

%71

%64

%64

%64

%5.

0%4.

7%4.

5%4.

7%5.

0%68

%65

%55

%55

%54

%N

DB

39%

43%

54%

24%

24%

63%

63%

56%

56%

57%

4.6%

4.9%

3.4%

3.7%

3.7%

58%

58%

44%

47%

47%

DFC

C39

%33

%29

%29

%29

%43

%44

%45

%46

%48

%3.

4%3.

1%2.

9%2.

8%2.

8%36

%36

%35

%36

%37

%N

TB47

%40

%35

%39

%40

%80

%77

%71

%70

%67

%4.

4%5.

2%5.

2%4.

5%4.

6%76

%73

%66

%64

%62

%SL

(Lis

ted

bank

s) **

37%

35%

36%

33%

34%

64%

61%

59%

60%

59%

3.9%

3.8%

3.7%

3.8%

4.0%

58%

56%

51%

51%

50%

Fee

Inco

me

/ Ope

ratin

g In

com

eC

ost /

Inco

me

Cos

t / In

com

e (E

xcl.

VAT)

Cos

t / A

vera

ge A

sset

s

Bal

ance

She

etFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EC

OM

B37

%31

%27

%24

%21

%26

%27

%24

%22

%22

%77

%78

%76

%76

%77

%9.

9%8.

9%7.

1%7.

7%7.

8%H

NB

20%

15%

20%

19%

19%

15%

8%18

%13

%14

%77

%78

%76

%76

%75

%5.

5%6.

4%6.

2%6.

7%7.

3%SA

MP

28%

28%

30%

24%

25%

15%

25%

30%

19%

19%

77%

79%

76%

77%

79%

6.1%

6.9%

6.1%

6.2%

6.4%

ND

B61

%7%

14%

20%

20%

34%

10%

0%21

%19

%31

%28

%39

%48

%48

%14

.2%

13.6

%16

.3%

15.2

%14

.6%

DFC

C22

%29

%31

%16

%19

%21

%25

%31

%21

%18

%19

%20

%34

%39

%43

%22

.4%

20.6

%17

.0%

19.5

%18

.6%

NTB

45%

35%

88%

36%

30%

16%

17%

87%

18%

20%

51%

60%

46%

47%

48%

6.2%

5.8%

6.0%

5.3%

5.4%

SL (L

iste

d ba

nks)

**30

.7%

23.0

%26

.5%

22.1

%21

.3%

20.5

%18

.0%

24.1

%18

.4%

18.6

%67

.8%

67.7

%67

.1%

68.8

%69

.4%

9.4%

9.3%

8.5%

8.9%

9.0%

Loan

Gro

wth

%A

sset

Gro

wth

%D

epos

its /

Liab

ilitie

s %

Equi

ty /

Ass

ets

%

Ass

et Q

ualit

yFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EFY

04FY

05FY

06FY

07E

FY08

EC

OM

B4.

5%3.

4%2.

8%3.

0%3.

1%50

%54

%60

%60

%62

%-4

.4%

-0.9

%3.

1%32

.2%

27.0

%H

NB

10.3

%8.

2%7.

5%6.

9%6.

4%49

%63

%66

%63

%62

%-1

5.8%

-8.2

%8.

9%10

.4%

9.9%

SAM

P8.

6%6.

2%5.

5%5.

2%4.

8%64

%82

%82

%88

%92

%-2

.9%

-8.0

%15

.7%

15.9

%17

.1%

ND

B7.

1%4.

3%2.

2%2.

0%1.

9%86

%12

6%18

8%15

7%12

3%-1

0.0%

-34.

5%-4

1.5%

7.4%

15.2

%D

FCC

8.9%

5.0%

4.9%

5.0%

5.0%

32%

47%

37%

40%

44%

-5.2

%-2

7.9%

29.0

%18

.2%

18.7

%N

TB6.

4%6.

1%5.

4%5.

3%5.

3%49

%56

%58

%60

%62

%52

.2%

28.4

%64

.7%

32.8

%31

.1%

SL (L

iste

d ba

nks)

**7.

7%5.

6%4.

8%4.

6%4.

5%53

%68

%69

%67

%68

%-9

.0%

-11.

0%9.

1%17

.5%

17.3

%

NPL

ratio

N

PL C

over

age

% C

hang

e N

PL's

12

REGIONAL COMPARATIVES

Source : Deutsche Bank Global Markets Reserach, Asia Pac (Ex Japan) Bank, Sept. 17th 2007; Bank Annual Reports and JKSB Estimates

ValuationsFY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E

Australia 3.0 2.5 2.3 17.3 15.0 13.5 13.9 14.0 9.9 4.0 4.5 5.0China 4.3 3.6 3.2 35.0 24.0 18.5 10.5 32.4 27.3 1.1 1.9 2.4Hong Kong 2.7 2.5 2.4 16.9 14.9 14.8 7.9 2.8 -0.7 3.9 4.2 4.4India 3.8 3.3 2.3 25.7 22.3 17.9 -10.4 6.9 16.1 0.9 1.0 1.1Indonesia 3.1 2.7 2.4 19.7 16.0 12.6 19.3 19.5 26.8 1.9 2.3 2.9Malaysia 2.9 2.6 2.5 19.4 17.1 14.1 22.3 9.0 17.6 3.2 3.7 4.9Pakistan 3.4 2.8 2.4 13.6 11.6 10.6 38.2 16.0 9.1 1.9 2.3 2.7Philippines 2.4 2.0 1.9 20.4 15.4 13.3 13.2 9.5 16.0 2.4 3.0 3.2Singapore 1.9 1.6 1.5 13.4 13.2 12.0 79.2 2.3 10.2 3.2 3.9 3.8South Korea 1.6 1.4 1.3 9.8 7.7 8.1 26.5 25.7 -5.0 1.2 3.4 3.4Taiwan 1.7 1.6 1.5 69.1 16.0 13.8 -73.1 326.3 16.4 2.7 4.1 4.6Thailand 1.8 1.6 1.4 19.2 17.5 10.4 -40.7 -7.0 49.9 2.3 2.1 2.7SRI LANKACOMB 2.1 1.6 1.3 12.4 8.7 6.8 27.7 41.5 29.1 4.4 4.4 4.4HNB 1.9 1.5 1.2 10.8 9.0 7.2 26.5 19.2 26.4 4.9 4.9 4.9SAMP 1.2 1.0 0.8 7.7 5.3 4.2 25.5 45.6 25.0 2.1 2.1 2.1NDB 1.4 1.1 1.0 13.1 9.3 7.8 -2.1 40.2 19.9 2.5 3.1 3.1DFCC 1.3 1.0 0.9 10.6 8.9 7.7 -6.1 19.3 15.4 3.9 3.9 3.9NTB 1.5 1.5 1.2 13.6 9.2 6.7 159.2 47.4 38.7 2.9 2.9 2.9SL (Listed banks) ** 1.6 1.3 1.1 11.2 8.5 6.8 17.8 32.5 25.1 2.6 2.8 2.8

DVD YLDPBV PER EPS GTH

ProfitabilityFY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E

Australia 16.7 17.9 17.5 16.7 17.9 17.5 1.0 1.0 1.0 2.3 2.1 2.1China 14.6 16.5 18.4 14.6 16.5 18.4 0.7 0.9 1.1 2.6 2.8 2.8Hong Kong 17.1 17.4 16.4 17.1 17.4 16.4 1.5 1.5 1.4 1.9 2.0 1.9India 16.9 16.0 15.0 16.9 16.0 15.0 1.0 1.0 1.0 3.1 3.2 3.2Indonesia 17.0 17.9 20.0 17.0 17.9 20.0 1.6 1.9 2.2 6.3 6.5 7.0Malaysia 15.4 16.1 18.3 15.4 16.1 18.3 1.1 1.1 1.2 2.4 2.4 2.3Pakistan 28.2 26.7 24.1 28.2 26.7 24.1 2.8 2.9 2.8 5.6 5.7 5.5Philippines 12.8 14.3 14.6 12.8 14.3 14.6 1.2 1.3 1.4 3.9 4.0 4.0Singapore 15.2 13.4 12.8 15.2 13.4 12.8 1.4 1.2 1.2 2.1 2.2 2.2South Korea 17.7 19.2 16.2 17.7 19.2 16.2 1.1 1.2 1.1 3.1 3.1 3.0Taiwan 2.5 10.2 11.2 2.5 10.2 11.2 0.2 0.8 0.8 2.0 1.8 1.8Thailand 9.7 9.6 14.4 9.7 9.6 14.4 0.8 0.9 1.4 3.4 3.3 3.5SRI LANKA 0.0 0.0 0.0COMB 17.0 18.3 19.1 17.0 20.8 21.1 1.3 1.5 1.6 3.7 3.8 3.9HNB 17.3 17.1 17.5 18.6 18.7 19.3 1.2 1.2 1.3 4.8 5.1 5.2SAMP 15.4 18.5 18.7 16.6 20.3 20.7 1.1 1.3 1.4 4.5 5.1 4.8NDB 9.6 11.9 12.4 10.5 12.6 13.3 1.6 2.0 2.0 4.9 5.0 5.0DFCC 12.6 10.8 11.1 13.1 12.6 11.8 2.4 2.3 2.2 4.7 4.6 4.5NTB 11.3 16.1 18.2 15.0 16.3 20.0 0.9 0.9 1.1 3.9 3.9 4.0SL (Listed banks) ** 14.5 15.3 16.0 15.3 17.0 17.4 1.4 1.5 1.6 4.3 4.5 4.5

NIMROE ROAE ROAA

Capital & EfficiencyFY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E

Australia 21.2 21.1 21.4 47.3 45.6 43.4 1.63 1.58 1.49 47.3 45.6 43.4China 8.6 10.7 11.5 44.9 41.3 41.1 1.24 1.29 1.29 44.9 41.3 41.1Hong Kong 18.8 20.9 20.6 34.8 34.7 34.6 0.92 0.92 0.9 34.8 34.7 34.6India 20.0 21.4 22.4 57.3 55.0 53.1 2.3 2.21 2.12 57.3 55.0 53.1Indonesia 11.1 11.5 11.6 53.1 51.1 48.0 3.65 3.61 3.73 53.1 51.1 48.0Malaysia 15.5 17.0 17.5 42.8 43.1 42.7 1.66 1.61 1.6 42.8 43.1 42.7Pakistan 12.9 13.3 14.7 32.3 31.7 31.6 2.35 2.35 2.29 32.3 31.7 31.6Philippines 11.8 15.1 14.6 60.6 62.0 60.3 3.38 3.61 3.29 60.6 62.0 60.3Singapore 21.7 21.6 20.9 42.9 40.9 40.4 1.21 1.22 1.18 42.9 40.9 40.4South Korea 20.9 22.9 18.7 44.2 42.8 44.9 1.63 1.62 1.56 44.2 42.8 44.9Taiwan 17.4 23.4 24.1 45.2 45.8 43.4 1.03 1.03 0.98 45.2 45.8 43.4Thailand 19.2 20.7 21.5 55.2 55.5 52.1 2.5 2.5 2.47 55.2 55.5 52.1SRI LANKACOMB 35.9 35.5 36.7 50.4 50.5 50.2 2.9 2.9 3.0 41.9 40.5 40.2HNB 31.5 32.7 34.2 67.7 68.4 67.0 4.4 4.7 5.0 59.9 60.4 59.0SAMP 36.6 36.8 37.0 64.5 64.0 63.6 4.5 4.7 5.0 55.3 54.8 54.4NDB 53.7 23.6 23.7 56.0 56.4 56.8 3.4 3.7 3.7 44.2 46.9 47.3DFCC 29.5 29.1 28.8 45.1 46.5 47.6 2.9 2.8 2.8 34.9 36.0 37.1NTB 35.3 38.6 39.6 71.5 69.8 67.1 5.2 4.5 4.6 66.5 64.3 61.6SL (Listed banks) ** 35.7 33.4 34.3 59.2 59.6 59.0 3.7 3.8 4.0 50.5 50.6 50.0

Cost / incomeFee Inc / Op Income Cost / income Cost / Average Assets

Cost / Income Excl. VAT

13

Source : Deutsche Bank Global Markets Reserach, Asia Pac (Ex Japan) Bank, Sept. 17th 2007; Bank Annual Reports and JKSB Estimates

Balance SheetFY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E

Australia 13.0 14.0 11.9 15.1 15.7 12.2 10.3 12.7 12.7 54.6 52.8 52.4China 14.5 14.5 13.2 17.4 15.8 12.4 14.9 17.3 14.7 88.7 85.5 83.7Hong Kong 9.7 13.3 10.6 16.7 13.4 9.2 13.6 14.1 11.3 85.4 83.6 83.6India 34.6 30.8 25.6 20.9 23.3 22.2 28.7 29.9 28.2 80.6 80.6 81.5Indonesia 13.7 23.7 18.3 13.0 5.0 7.6 15.9 17.7 18.4 87.0 87.3 87.6Malaysia 16.9 9.4 10.3 23.8 9.3 8.2 17.5 15.9 9.8 87.0 87.6 87.9Pakistan 15.5 14.4 15.7 14.5 13.4 13.1 23.2 19.6 19.6 53.6 83.8 84.1Philippines 10.9 30.4 17.2 18.0 26.1 7.1 17.4 25.1 19.2 84.0 85.0 85.4Singapore 9.9 17.7 15.0 11.3 17.3 12.2 12.8 17.6 17.3 77.4 71.6 70.3South Korea 18.1 14.3 8.3 15.6 15.2 7.3 13.7 16.1 11.2 63.3 59.1 59.8Taiwan 2.3 6.3 7.6 3.9 4.8 6.6 10.6 7.0 10.1 52.6 53.1 53.2Thailand 4.0 8.7 11.2 7.3 4.5 7.1 3.8 4.8 8.5 88.8 88.1 88.7SRI LANKACOMB 26.8 24.5 21.1 24.4 21.8 21.8 32.7 22.7 21.8 75.7 76.1 76.8HNB 19.9 18.8 19.4 18.3 12.9 13.9 29.5 18.9 19.0 76.2 75.6 75.2SAMP 29.7 24.1 24.5 30.1 19.2 19.4 44.6 21.2 24.3 75.8 77.2 78.7NDB 13.9 20.2 20.3 0.4 21.1 19.2 13.5 24.4 17.8 38.5 47.6 47.5DFCC 30.6 15.8 18.7 30.6 20.8 18.3 76.8 19.4 18.3 34.2 39.5 42.8NTB 87.6 35.7 29.6 87.4 17.6 19.9 83.1 18.7 19.9 46.2 46.7 47.6SL (Listed banks) ** 26.5 22.1 21.3 24.1 18.4 18.6 38.4 21.1 20.6 67.1 68.8 69.4

Loan Growth % Asset Growth % RWA Growth % Deposits / Liabilities %

Balance SheetFY06 FY07E FY08E FY04 FY05 FY08E

Australia 134.0 136.6 137.2 69.0 68.0 67.8China 61.6 63.3 65.1 51.4 50.8 51.2Hong Kong 56.3 57.3 57.6 43.7 43.7 44.2India 75.2 79.4 81.8 56.5 60.0 61.6Indonesia 58.4 69.2 76.4 45.6 53.6 59.0Malaysia 73.3 72.8 73.8 59.2 59.2 60.4Pakistan 78.2 79.5 81.7 58.3 58.8 60.2Philippines 51.5 52.4 57.1 38.9 40.3 44.0Singapore 69.4 75.5 78.7 48.4 48.6 49.8South Korea 122.1 219.5 129.5 72.1 71.5 72.2Taiwan 81.9 82.0 82.3 40.1 40.5 40.7Thailand 86.6 91.8 95.1 70.3 73.2 76.0SRI LANKACOMB 95.5 97.6 96.4 67.1 68.6 68.2HNB 86.4 92.1 97.7 61.7 64.9 68.1SAMP 90.6 92.9 94.8 64.3 66.9 69.8NDB 198.4 199.6 195.9 64.6 64.2 64.7DFCC 254.2 218.0 199.0 71.6 68.7 68.9NTB 117.7 133.2 141.3 51.1 58.9 63.6SL (Listed banks) ** 104.9 107.9 109.3 64.3 66.3 67.9

Loan /Deposits % Loan /Assets %

Asset QualityFY06 FY07E FY08E FY06 FY07E FY08E FY06 FY07E FY08E

Australia 0.5 0.5 0.6 135.8 123.1 118.0 6.0 22.2 21.5China 3.3 2.8 2.4 84.2 98.1 106.6 -5.7 -3.5 -0.9Hong Kong 0.7 0.6 0.5 62.8 71.9 79.0 -27.7 -9.4 0.6India 3.0 2.4 2.2 60.5 54.9 51.7 -17.8 4.3 15.9Indonesia 7.8 6.1 5.3 85.8 106.9 123.1 -16.9 -3.4 3.3Malaysia 6.8 5.9 5.4 59.9 66.9 65.3 0.8 -5.2 0.2Pakistan 7.5 6.8 6.3 89.2 91.2 91.5 3.4 3.8 7.0Philippines 7.2 6.8 5.9 73.9 80.8 81.6 -14.7 22.7 1.9Singapore 2.9 2.5 2.7 93.3 86.0 75.8 -20.3 3.1 22.2South Korea 1.0 0.9 1.0 156.1 159.9 136.4 -24.7 7.9 18.9Taiwan 1.7 1.8 1.8 87.8 66.5 65.5 6.1 13.0 6.7Thailand 8.4 6.5 5.6 65.3 78.5 80.0 -8.1 -15.7 -4.1SRI LANKACOMB 2.8 3.0 3.1 60.4 59.6 62.2 3.1 32.2 27.0HNB 7.5 6.9 6.4 65.6 62.5 62.4 8.9 10.4 9.9SAMP 5.5 5.2 4.8 82.3 88.3 92.3 15.7 15.9 17.1NDB 2.2 2.0 1.9 188.2 156.8 123.2 -41.5 7.4 15.2DFCC 4.9 5.0 5.0 37.5 39.6 43.6 29.0 18.2 18.7NTB 5.4 5.3 5.3 58.3 60.0 62.0 64.7 32.8 31.1SL (Listed banks) ** 4.8 4.6 4.5 69.0 67.2 67.7 9.1 17.5 17.3

NPL ratio NPL Coverage % Change NPL's

This document is published by John Keells Stockbrokers (Pvt.) Limited for the exclusive use of their clients. All information has been compiled from availabledocumentation and JKSB’s own research material. Whilst all reasonable care has been taken to ensure the accuracy of the contents of this issue, neither JKSB norits employees can accept responsibility for any decisions made by investors based on information contained herein.

14

Rs. 135.00 BUY

Sri Lanka Equities Corporate Update

Commercial Bank of Ceylon PLC (COMB)

A J

KSB

Res

earc

h P

ubli

cati

on

COMB PRICE - VOLUME GRAPH

40

60

80

100

120

140

160

180

01-A

pr-

03

20-

Ju

n-0

329

-Au

g-0

31

3-N

ov-

03

29-

Jan

-04

20-A

pr-

04

13-

Ju

l-0

427

-Sep

-04

17-

De

c-0

415

-Mar

-05

07-

Ju

n-0

524

-Au

g-0

50

7-N

ov-

05

24-

Jan

-06

27-A

pr-

06

17-

Ju

l-0

623

-Oc

t-0

60

8-Ja

n-0

723

-Mar

-07

25-

Ju

n-0

704

-Sep

-07

Price

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000Volume

VolumePrice

Commercial Bank became the largest local private bank in the country lastyear, with a market share of 13% of LCB assets. The bank has traditionallygrown from being a predominantly corporate lender, to now establishing itself as a national bank with approximately 48% of its lending portfolioassets arising from the growing SME and consumer segments. In additionCOMB has also successfully established a presence in Bangladesh with 9branches, and is expected to be a key driver of growth for the bank in themedium to long term. The operations in Bangladesh accounted for 7.4%of group assets and 14.16% of group PAT excluding exceptional items.

COMB is expected to record slower yet healthy loan growth of 24.3% inFY07 and 21.1% in FY08 given the high interest rate environment, whiledeposit growth is expected at 23% in FY07 and FY08. The high marginSME and consumer segments continue to be key driver of loan growth,with leasing and pawning businesses also performing well. Net interestmargins have widened this year on account of the rising interest rateswhich have customarily resulted in advances being re-priced ahead ofdeposits. In addition the bank continues to benefit from a surplus of retaildeposits over its retail lending which it mobilizes to its corporate lendingportfolio.

The steady depreciation of the SLR this year is expected to augment foreignexchange income while regular trade finance activities is expected to boostfee and commission based income which accounts for 50% of non interestincome. We expect non interest income to grow by 24% in FY07.

The bank is expected to register modest declines in its cost to income ratioover the next two years which at present ranks as the best amongst localbanks. The bank continues to benefit from the rationalisation of internalprocesses, as well as expenses being curtailed by the increased adoption oftechnology in the provision of the bank’s services.

Absolute NPL’s increased by 3.1% last year and has increased at a greaterpace in 1H07, although healthy loan growth has meant that the NPL Ratioremained steady. We prudently expect the gross NPL ratio to expandmarginally to 2.97% in FY07 and 3.11% in FY08 given the likelihood oflower recoveries and a rise in NPLs due to the present macro environment.Provision cover is however expected to be maintained at 60% in FY07increasing to 62.2% in accordance with guidelines issued by the centralbank.

A successfully concluded rights issue raising Rs. 5.74bn for the bank, hasboosted the Tier 1 and Total CAR to 10.51% and 14.08% in the 1H FY07from 7.62% and 11.58% recorded at year end FY06. The scrip issuestemmed the decline in capital adequacy witnessed in the bank with COMBs’

2004 7,397 1,727 1,495 6.01 21.04 22.48 2.38 4.4% 6.00 2005 8,769 2,360 2,128 8.55 42.32 15.79 2.11 4.4% 6.00 2006 11,473 2,951 2,718 10.92 27.73 12.37 2.10 4.4% 6.00

2007E 14,376 3,961 3,845 15.44 41.47 8.74 1.60 4.4% 6.00 2008E 18,133 4,970 4,965 19.94 29.13 6.77 1.29 4.4% 6.00

DPS Rs.

EPS Growth

PER (x) Rs.

Dividend Yield %

P/BVFinancial

Year (Dec)Net Income

(Rs.mn)NPAT

(Rs.mn)EPS (Rs.)

PAT, MI & Pref Divid

COMBReuters CodeBloomberg CodeShare Price LKRIssued Share Capital (Shares)*Voting*Non Voting12 mth High/Low (Rs.) - VotingAverage Daily Volume (Voting Shares)Market Capitalisation (Voting) Rs. mnPrice Performance (%) - VotingASPI 1.30 (8.70) 6.63COMB - (5.26) 28.13* Adjusted for bonus and rights issues

31,430

COMB.SL135.00

COMB.CM

160.70 / 104.6986,292

232,817,073 16,120,797

John Keells Stock Brokers (Pvt) LtdCompany No. PV 89130, Glennie Street,Colombo 2,Sri Lanka.

Tel: 9411 2421 101-9 (Gen.),9411 2326 003,9411 2439 047/8

Fax: 9411 2326 863,9411 2342 068

Yolan [email protected]

October 2007

15

COMB 2004 2005 2006 2007E 2008EPrice / Book Value 2.4 2.1 2.1 1.6 1.3 EPS 6.0 8.5 10.9 15.4 19.9 PER 22.5 15.8 12.4 8.7 6.8 EPS Growth 21.0% 42.3% 27.7% 41.5% 29.1%DVD YLD 4.4% 4.4% 4.4% 4.4% 4.4%ROE 10.6% 13.3% 17.0% 18.3% 19.1%ROAE 11.5% 14.2% 17.0% 20.8% 21.1%ROAA 1.2% 1.3% 1.3% 1.5% 1.6%NIM 3.7% 3.6% 3.7% 3.8% 3.9%Fee Income / Operating Income 36% 33% 36% 36% 37%Cost / Income 56.5% 54.6% 50.4% 50.5% 50.2%Cost / Income (Excl VAT) 50.5% 47.4% 41.9% 40.5% 40.2%Cost / Average Assets 3.28% 2.97% 2.86% 2.92% 3.01%Tier 1 10.78% 9.68% 7.62%Loan Growth 36.5% 30.9% 26.8% 24.5% 21.1%Asset Growth 25.7% 27.0% 24.4% 21.8% 21.8%RWA Growth 37% 29% 33% 23% 22%Loan/ Deposits 91.9% 93.1% 95.5% 97.6% 96.4%Loan / Assets 63.9% 65.9% 67.1% 68.6% 68.2%Deposits / Liabilities 77.2% 77.6% 75.7% 76.1% 76.8%Equity / Assets 9.9% 8.9% 7.1% 7.7% 7.8%NPL Ratio 4.53% 3.43% 2.79% 2.96% 3.11%NPL Coverage 50.0% 53.9% 60.4% 59.6% 62.2%% Change in NPLS -4.4% -0.9% 3.1% 32.2% 27.0%Personnel Cost / Average Assets 1.4% 1.3% 1.3% 1.2% 1.2%

capital position failing to keep pace with its

aggressive loan book growth over the last 5 years.

COMB’s has consistently exhibited strongfundamentals over the years and is very likely tobe successful in navigating what is at present achallenging environment. Earnings growth forecastsof 41.4% and 29.13% for FY07 and FY08excluding exception items correspond to a PERof 8.7x at 6.8x at a market price of Rs. 135/-.The counter currently trades at a 9.8% discountto the market. Given the continued consolidationof its market position in Sri Lanka and its strongmedium to long term prospects in the region, it isour view that COMB ought to be trading at asignificant premium to the market. We recommendBUY.

This document is published by John Keells Stockbrokers (Pvt.) Limited for the exclusive use of their clients. All information has been compiled from availabledocumentation and JKSB’s own research material. Whilst all reasonable care has been taken to ensure the accuracy of the contents of this issue, neither JKSB norits employees can accept responsibility for any decisions made by investors based on information contained herein.

Income Statement 2002 2003 2004 2005 2006 2007E 2008EFor the Year Ended 31st December Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mnIncome 8,900 9,749 12,437 16,226 23,418 30,412 41,682

Net Interest Income 3,021 3,751 4,738 5,837 7,357 9,271 11,483 Foreign exchange profit 464 397 874 587 1,439 1,700 2,050 Fee and commisison income 824 1,051 1,377 1,760 2,011 2,525 3,450 Other Income 232 671 409 586 665 880 1,150 Net Income 4,465 5,870 7,397 8,769 11,473 14,376 18,133 Less Operating ExpensesPersonnel Costs 1,121 1,398 1,820 2,144 2,566 3,070 3,650 Premises and Equipment expenses 684 833 1,019 1,146 1,384 1,610 1,850 Provision for staff retirement benefits 196 311 326 236 - - - Loan losses and Provisions 413 623 699 415 655 909 1,214 Other Overhead expenses 375 708 1,015 1,258 1,829 2,580 3,600 Total Expenses (2,790) (3,874) (4,879) (5,199) (6,435) (8,169) (10,314) Profit from Operations 1,675 1,996 2,518 3,570 5,038 6,207 7,819 Add: Share of PBT of Assoc. 28 43 76 100 62 183 197 Profit before Tax 1,704 2,039 2,594 3,670 5,101 6,389 8,016 Less: Provision for Taxation 391 572 867 1,311 2,150 2,428 3,046 Profit after taxation 1,313 1,467 1,727 2,360 2,951 3,961 4,970 Less: Minority Interest 2 2 2 2 3 4 5 Net profit for the year 1,311 1,465 1,725 2,358 2,948 3,957 4,965 Cum. Red. Pref. Shares 13% 117.78 117.78 117.78 117.78 117.78 Cum. Red. Pref. Shares 11.25% 112.50 112.50 112.50 112.50 112.50 NPAT, MI & Pref. Dividend 1,193 1,235 1,495 2,128 2,718 3,845 4,965

117.78 230.28

Balance Sheet 2002 2003 2004 2005 2006 2007E 2008EAs at 31st December Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mnASSETSCash and short-term funds 1,837 9,002 12,136 18,657 13,731 23,817 23,709 Balances with Central Banks 3,244 5,233 6,320 9,045 12,574 17,550 20,851 Government Treasury Bills and Bonds 16,778 20,748 6,647 19,160 12,222 14,666 17,599 Commercial paper 1,080 547 560 408 423 620 885 Sec. purchased under re-sale agreements 1,449 3,971 2,087 808 4,593 5,600 6,752 Dealing Securities 200 - 110 182 145 298 360 Investment securities 705 2,606 2,940 3,691 1,795 3,941 4,798 Treasury Bonds Maturing after one year 148 - 14,379 1,714 20,025 9,287 18,777 Bills of Exchange 2,552 2,495 2,799 2,790 3,288 3,740 4,255 Loans and Advances 47,350 60,585 82,605 108,917 137,720 170,773 205,781 Lease rec. within one year 698 1,277 2,004 2,676 3,007 4,233 5,570 Lease rec. from one to five years 1,197 2,050 3,243 4,295 6,415 8,468 11,177

77,238 108,513 135,828 172,345 215,938 262,992 320,515

Investment in Assoc. 141 171 243 283 41 63 76 Interest and Fees receivables 295 390 1,143 1,199 1,639 1,956 2,365 Other Assets 1,958 1,872 1,445 2,944 3,006 3,644 4,356 Property, Plant and Equipment 1,753 1,877 3,134 3,365 3,438 4,200 5,100 TOTAL ASSETS 81,385 112,823 141,792 180,135 224,061 272,854 332,412 Financed By : - - - - - - - Deposits form customers 54,480 75,097 98,622 127,491 157,532 191,745 235,328 Dividends Payable 121 190 232 230 113 113 113 Borrowings 4,200 5,406 9,090 13,453 18,944 24,248 31,038 Sec. sold under repurchase agreements 9,922 12,951 12,261 11,386 14,317 15,892 17,640 Other Liabilties 3,912 4,596 3,491 6,070 8,402 8,654 8,914 Tax Payable 64 231 484 773 1,420 2,150 2,428 Deferred Taxation 253 259 251 239 625 1,062 1,487 Debentures 500 2,244 3,244 4,553 6,680 7,950 9,460

73,453 100,973 127,676 164,168 208,033 251,814 306,407 Minority Interest 13 13 12 13 11 12 12 SHAREHOLDERS FUNDSShare Capital 1,324 2,603 2,603 3,327 2,428 3,489 2,489 Statutory Reserve Fund 1,009 1,009 1,010 1,422 1,429 1,422 1,422 Reserves 5,586 8,224 10,491 11,205 12,159 16,116 22,081 Shareholders Funds 7,919 11,836 14,105 15,954 16,016 21,027 25,992

81,385 112,822 141,792 180,135 224,061 272,854 332,412

16

Rs. 103.00 BUY

Sri Lanka Equities Corporate Update

Hatton National Bank PLC (HNB)

A J

KSB

Res

earc

h P

ubli

cati

on

HNB PRICE - VOLUME GRAPH

0

20

40

60

80

100

120

02-J

an-0

325

-Feb

-03

24-A

pr-0

318

-Jun

-03

05-A

ug-0

324

-Sep

-03

13-N

ov-0

309

-Jan

-04

09-M

ar-0

406

-May

-04

25-J

un-0

413

-Aug

-04

04-O

ct-0

425

-Nov

-04

19-J

an-0

517

-Mar

-05

13-M

ay-0

507

-Jul

-05

31-A

ug-0

520

-Oct

-05

14-D

ec-0

509

-Feb

-06

03-A

pr-0

601

-Jun

-06

31-J

ul-0

613

-Oct

-06

06-D

ec-0

629

-Jan

-07

22-M

ar-0

724

-May

-07

19-J

ul-0

713

-Sep

-07

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000VolumePrice

HNB is the second largest private local bank in the country with the largestdomestic branch network amongst private banks with 152 banking centresacross the island. The banks subsidiaries include Insurance and Stock brokingfirms while also functioning as a Primary Dealer for Government Securities.Contributions from these entities are relatively small. HNB has witnessedhealthy earnings growth over the last two years largely due to improvedasset quality resulting in lower provision expense coupled with healthy loangrowth.

The banks corporate lending portfolio accounts for approximately 65%of its loan book, although much of the recent growth in its loan book hasarisen from high margin consumer loans relating to leases, pawning andhousing loans. This together with the prevailing high interest rates has meantthat the bank has enjoyed healthy net interest margins while recordingsound loan growth. We expect loan growth of 18.8% and 19.4% in FY07and FY08 respectively.

Steep gains from foreign exchange income along with steady growth infees and commission income should see non interest income grow by 26.8%and 27.5% in FY07 and FY08 respectively. Non interest income hasconsistently contributed a third of total income in recent years and isexpected to increase marginally in the next two years.

HNBs’ cost to income ratio continues to remain high although the cost toincome ratio excluding VAT has declined marginally over last year. Arestructuring of the bank’s pension scheme as well as the roll out of a coreIT network in the next 12mths is expected to have a favourable impact onoperating expenses in the medium term.

The management of credit risk in the bank has been significantlystrengthened by the implementation of an integrated system across itsnetwork of banking centres over the last few years. In addition greaterexpertise brought into credit risk management has resulted in improvedassessment and monitoring and is reflected in significant improvements inthe quality of its lending portfolio. The Banks NPL ratio has improvedsignificantly from 10.3% in FY04 to 6.9% in FY07E, while provision coverhas also improved from 48.8% in FY04 to 62.5% in FY07E. Creditconcentration is however a concern with 5 of the largest clients representingover a tenth of the banks loan book.

Deposits accounted for 76.2% of liabilities in FY06, being the primarysource of funding. Deposits are expected to grow by 11.5% and 12.5% inFY07 and FY08 respectively. The banks cost of funds has increased withan increase in borrowings to fund loan growth as well as a shift in thebanks’ deposit mix, with more demand and savings deposits being shiftedto high yield time deposits.

2004 8,141 756 3.21 (49.63) 32.11 2.71 3% 3.50 2005 10,228 1,770 7.52 134.33 13.70 2.15 4% 4.00 2006 12,425 2,239 9.51 26.47 10.83 1.87 5% 5.00

2007E 15,181 2,670 11.33 19.23 9.09 1.55 5% 5.00 2008E 18,506 3,373 14.32 26.36 7.19 1.25 5% 5.00

EPS Growth %

PER (x) Rs.

Dividend Yield %

Financial Year (Dec)

Net Income (Rs.mn)

PAT (Rs.mn)

EPS (Rs.)

P/BV DPS Rs.

HNBReuters CodeBloomberg CodeShare Price LKR

*Voting*Non Voting12 mth High/Low (Rs.) - VotingAverage Daily Volume (Shares)- VotingMarket Capitalisation (Voting) Rs. mn 19,501

Price Performance (%)1 mth 6 mth 12 mth

ASPI 1.37 (8.70) 6.63HNB 1.98 2.74 74.58* Adjusted for bonus and rights issues

107.50 / 58.0038,497

Issued Share Capital (Shares)189,329,400

46,200,000

HNB.CMHNB.SL103.00

John Keells Stock Brokers (Pvt) LtdCompany No. PV 89130, Glennie Street,Colombo 2,Sri Lanka.

Tel: 9411 2421 101-9 (Gen.),9411 2326 003,9411 2439 047/8

Fax: 9411 2326 863,9411 2342 068

Yolan [email protected]

October 2007

17

HNB 2004 2005 2006 2007E 2008EPrice / Book Value 2.7 2.2 1.9 1.5 1.2 EPS 3.2 7.5 9.5 11.3 14.3 PER 32.0 13.6 10.8 9.0 7.2 EPS Growth -49.6% 134.3% 26.5% 19.2% 26.4%DVD YLD 3.4% 3.9% 4.9% 4.9% 4.9%ROE 8.5% 15.8% 17.3% 17.1% 17.5%ROAE 9.4% 17.6% 18.6% 18.7% 19.3%ROAA 0.5% 1.1% 1.2% 1.2% 1.3%NIM 3.6% 4.4% 4.8% 5.1% 5.2%Fee Income / Operating Income 36% 35% 31% 33% 34%Cost / Income 70.8% 63.3% 67.7% 68.4% 67.0%Cost / Income (Excl VAT) 66.7% 61.4% 59.9% 60.4% 59.0%Cost / Average Assets 3.81% 3.85% 4.40% 4.71% 4.96%Tier 1 9.83% 10.87% 10.23%Loan Growth 20.1% 15.1% 19.9% 18.8% 19.4%Asset Growth 14.8% 8.2% 18.3% 12.9% 13.9%RWA Growth - 11% 30% 19% 19%Loan/ Deposits 78.3% 83.2% 86.4% 92.1% 97.7%Loan / Assets 57.3% 60.9% 61.7% 64.9% 68.1%Deposist / Liabilities 77.5% 78.3% 76.2% 75.6% 75.2%Equity / Assets 5.5% 6.4% 6.2% 6.7% 7.3%NPL Ratio 10.3% 8.2% 7.5% 6.9% 6.4%NPL Coverage 48.8% 63.5% 65.6% 62.5% 62.4%% Change in NPLS -16% -8% 9% 10% 10%Personnel Cost / Average Assets 1.5% 1.5% 1.5% 1.6% 1.8%

Income Statement 2004 2005 2006E 2007E 2008EFor the Year Ended 31st December Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn

Income 14,503 18,298 23,233 28,760 33,726 Net Interest Income 5,218 6,671 8,513 10,222 12,184 Foreign exchange profit 663 646 793 1,125 1,524 Fee and commisison income 1,574 1,639 1,861 2,264 2,823 Other Income 686 1,272 1,258 1,570 1,975 Net Income 8,141 10,228 12,425 15,181 18,506 Less Operating Expenses 2,923 3,557 3,912 Personnel Costs 2,285 2,535 2,895 3,525 4,415 Premises and Equipment expenses 1,409 1,665 1,752 2,145 2,595 Provision for staff retirement benefits 1,941 1,843 3,344 4,100 4,950 Loan losses and Provisions 235 328 401 400 375 Other Overhead expenses 1,566 1,759 932 1,123 1,462 Total Expenses (7,332) (8,237) (9,344) (11,512) (13,866) Profit from Operations 809 1,991 3,082 3,669 4,640 Add: Share of PBT of Assoc. 23 17 14 17 17 Profit before Tax 832 2,008 3,095 3,686 4,657 Less: Provision for Taxation (15) 214 820 1,014 1,281 Profit after taxation 847 1,795 2,276 2,672 3,377 Less: Minority Interest 92 24 37 3 3 Net profit for the year 756 1,770 2,239 2,670 3,373

Balance Sheet 2004 2005 2006E 2007E 2008EAs at 31st December Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mn Rs. 'mnASSETSCash and short-term funds 20,113 21,194 23,344 26,054 26,405 Balances with Central Banks 9,120 8,566 12,017 8,566 8,566 Government Treasury Bills and Bonds 5,650 2,001 2,452 7,845 8,630 Commercial paper 682 434 291 434 434 Sec. purchased under re-sale agreements 5,650 3,881 4,393 4,613 4,982 Dealing Securities 417 320 975 1,411 1,811

Investment securities 18,761 18,817 22,660 17,525 18,121 Bills of Exchange 2,077 2,027 1,911 1,949 1,988 Loans and Advances 83,701 95,676 114,277 135,418 161,148 Lease receivable within one year 2,564 3,112 3,796 4,745 5,931 Lease receiveable from one to five years 4,274 5,752 7,756 9,696 12,119 Investment in Assoc. 169 171 165 165 165 Other Assets 5,527 5,145 5,112 6,142 6,918 Property, Plant and Equipment 7,959 7,892 7,571 9,194 8,998 TOTAL ASSETS 161,761 174,987 206,979 233,756 266,217 Financed By :Deposits form customers 118,342 128,131 147,788 164,754 185,425 Dividends Payable 108 50 - - - Borrowings 15,303 16,044 24,924 30,407 36,489 Non Life Ins. reserves & Long Term Ins. Funds 344 568 827 869 912 Other Liabilties 12,457 12,509 12,168 13,263 14,457 Tax Payable (158) 37 774 1,006 1,308 Deferred Taxation 353 316 318 327 339 Debentures 5,983 5,977 7,083 7,367 7,809

152,733 163,632 193,883 217,993 246,738 Minority Interest 125 149 180 149 149 SHAREHOLDERS FUNDSOrdinary Shares - Voting 770 947 947 1,893 1,893 Ordinary Shares - Non Voting 231 231 231 462 462 Share Capital 1,001 1,178 1,178 2,355 2,355 Statutory Reserve Fund 570 625 670 625 625 Reserves 7,332 9,404 11,068 12,634 16,350 Shareholders Funds 8,903 11,206 12,916 15,614 19,330

161,761 174,987 206,979 233,756 266,217

The banks’ Tier 1 and Total CAR stood at 8.90%and 10.42% respectively as at the 1H of FY07.Rs. 2bn raised via a debenture issue in 3Q of FY07should help boost Tier 2 capital to approximately12% by the end of the 3Q.

The bank has witnessed sound growth along withimproved asset quality and provision cover as wellas enhanced profitability. Earnings growth of19.23% and 26.36% in FY07 and FY08respectively correspond to a P/E multiple of 9.09xand 7.19x. Given the banks’ strong fundamentalswe believe the counter presents further upside inthe medium to long term. We recommend BUY

This document is published by John Keells Stockbrokers (Pvt.) Limited for the exclusive use of their clients. All information has been compiled from availabledocumentation and JKSB’s own research material. Whilst all reasonable care has been taken to ensure the accuracy of the contents of this issue, neither JKSB norits employees can accept responsibility for any decisions made by investors based on information contained herein.

18

Rs. 120.00 BUY

Sri Lanka Equities Corporate Update

Sampath Bank PLC (SAMP)

A J

KSB

Res

earc

h P

ubli

cati

on

SAMP PRICE - VOLUME GRAPH

-

10

20

30

40

50

60

70

80

90

100

110

120

130

140

02-

Jan

-03

27-M

ar-0

32

3-J

un

-03

02-S

ep-0

31

9-N

ov

-03

13-

Feb

-04

20-

Ma

y-0

412

-Au

g-0

40

5-N

ov

-04

03-

Feb

-05

29-A

pr-

052

6-J

ul-

05

14-O

ct-

050

5-J

an-0

630

-Mar

-06

26-

Ju

n-0

610

-Oc

t-06

27-

Dec

-06

21-M

ar-0

72

5-J

un

-07

07-S

ep-0

7

Rs.

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000Volume

Volume

Price

SAMPReuters CodeBloomberg CodeShare Price LKR

Voting12 mth High/Low (Rs.)Market Capitalisation (Rs.mn)Average Daily Volume (Shares)Market Capitalisation (Voting) Rs. mn 8,267 Price Performance (%)