spring 2012 practice questions. security analysis (spring 2012)asif ali qureshi, cfa question # 1...

TRANSCRIPT

Spring 2012

Practice Questions

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

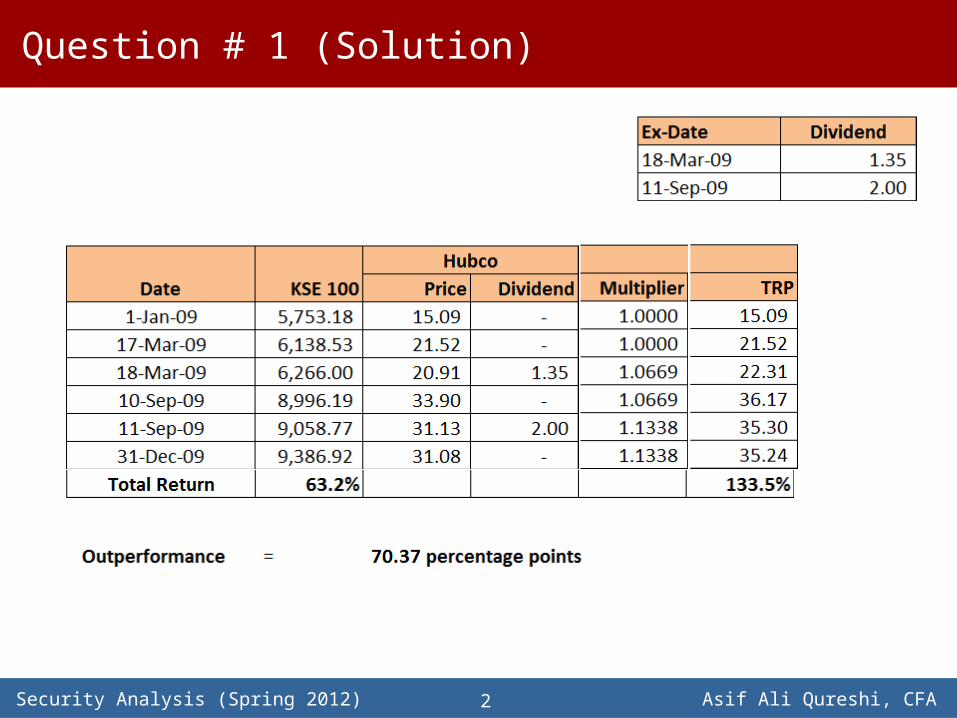

Question # 1 (Solution)

2

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

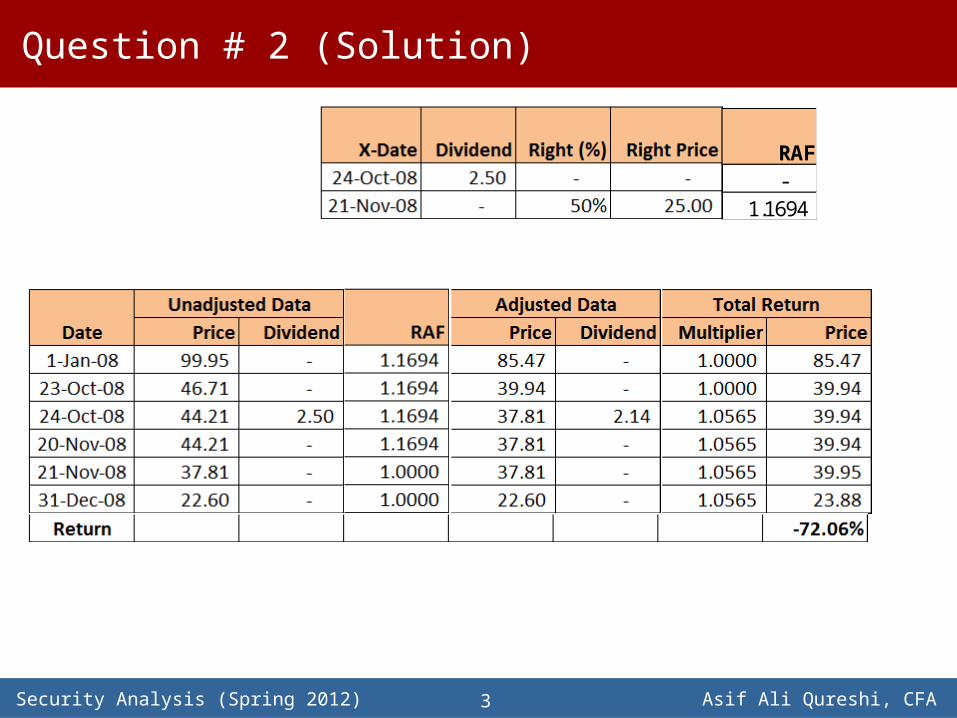

Question # 2 (Solution)

3

RAF-

1.1694

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

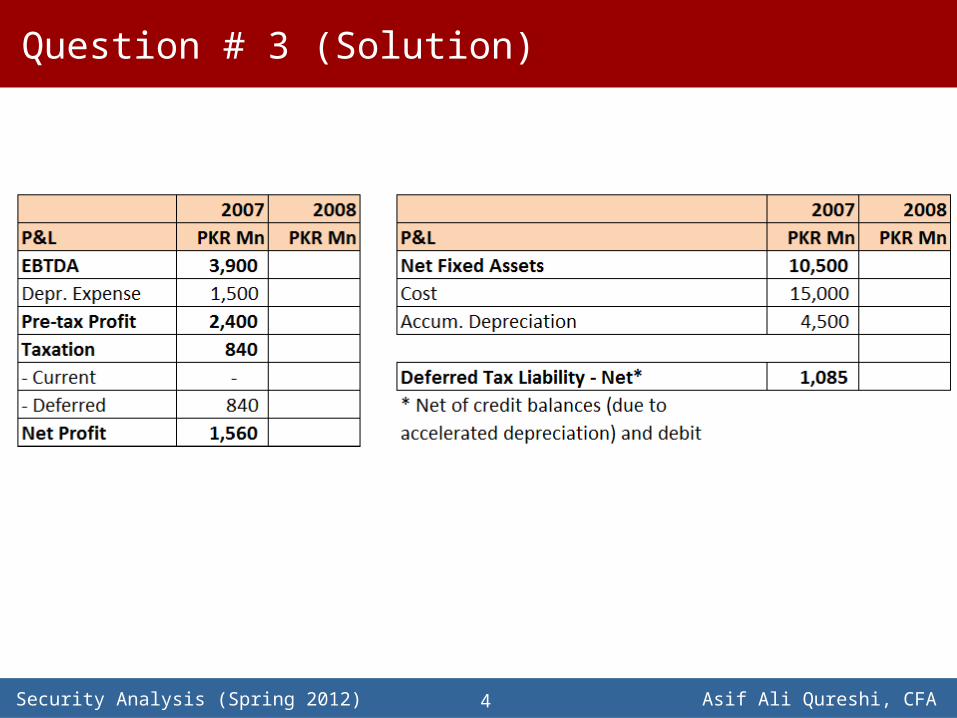

Question # 3 (Solution)

4

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

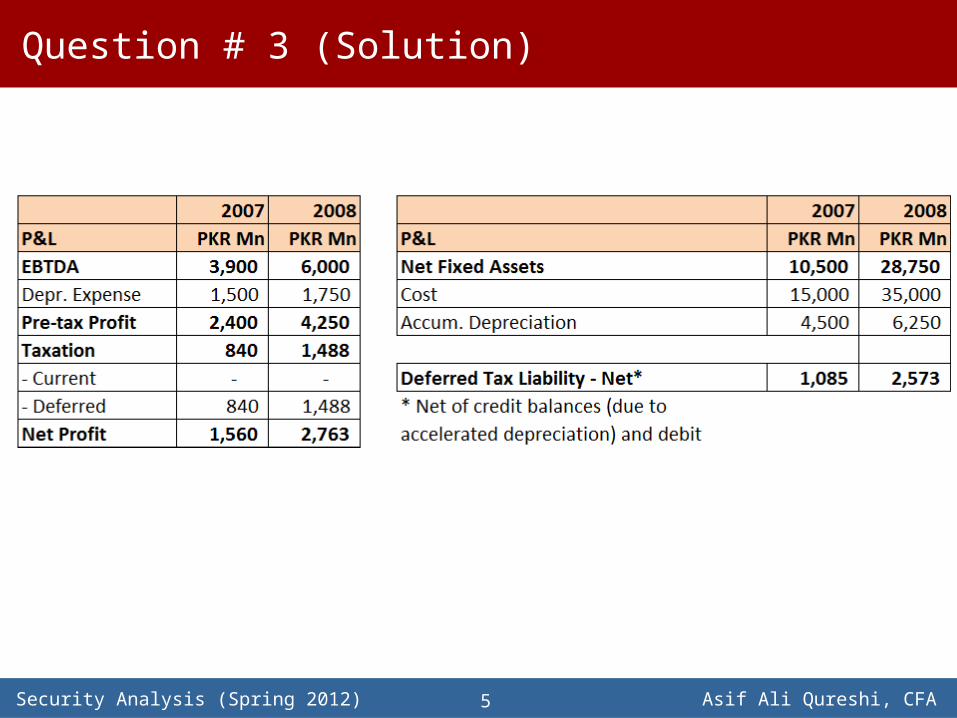

Question # 3 (Solution)

5

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

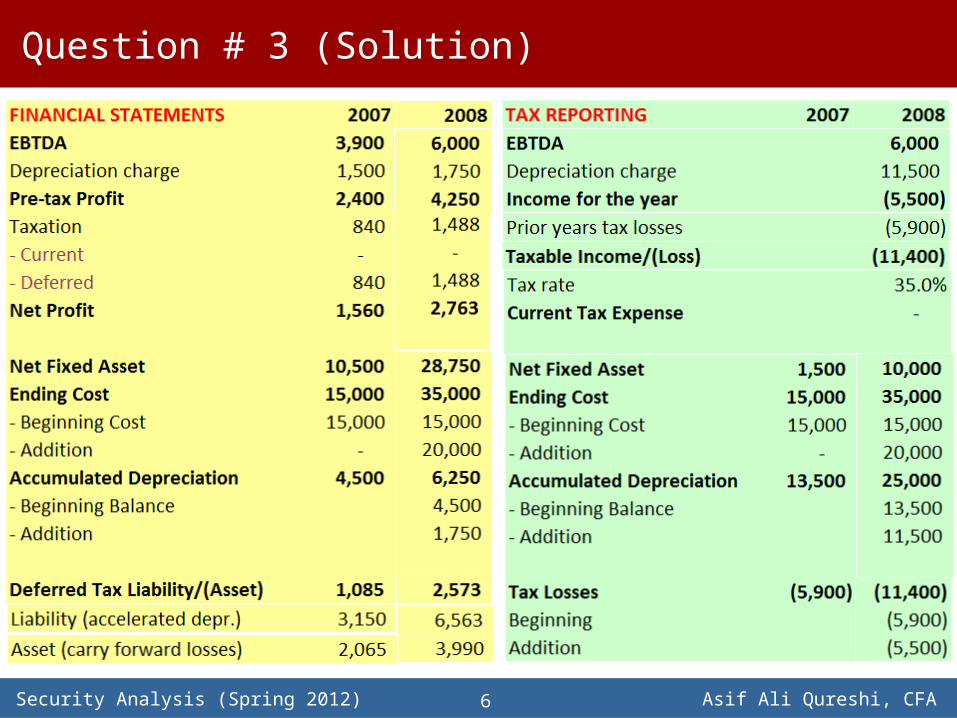

Question # 3 (Solution)

6

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

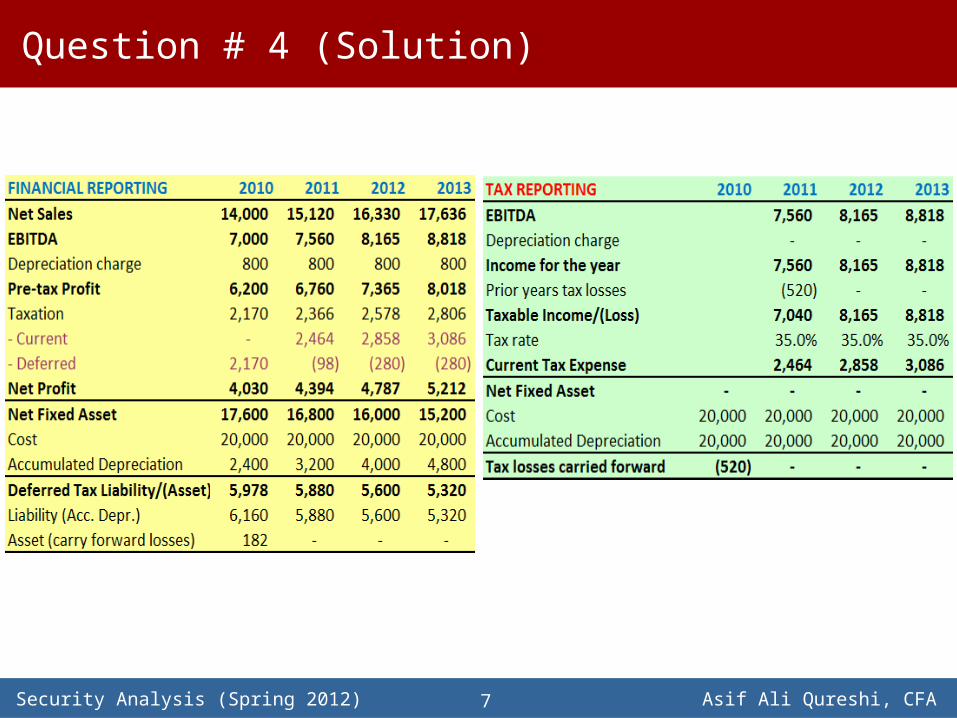

Question # 4 (Solution)

7

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

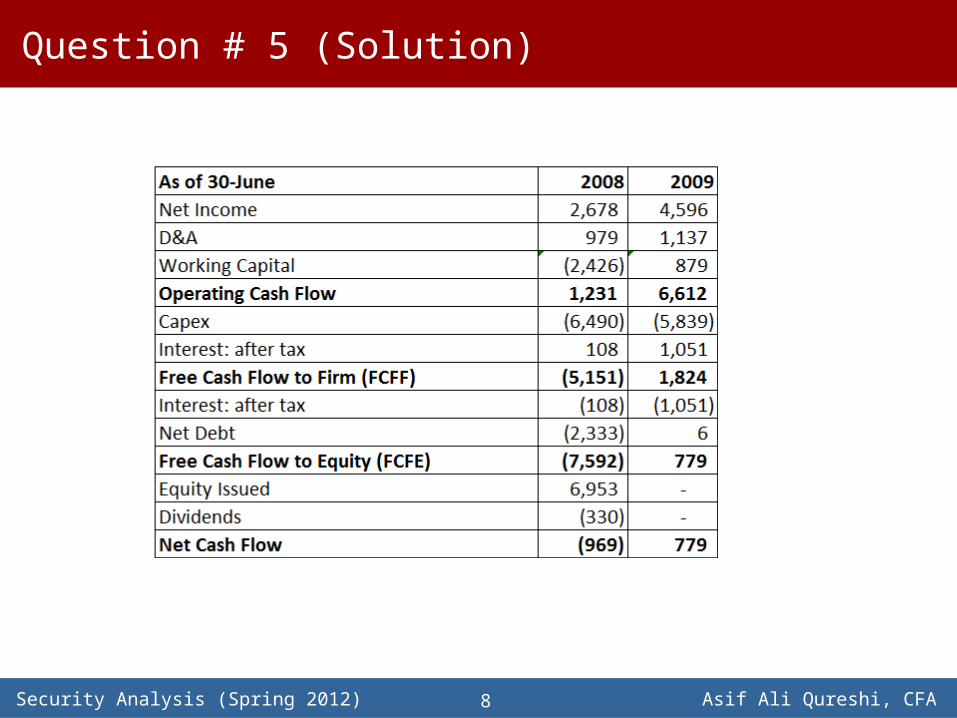

Question # 5 (Solution)

8

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

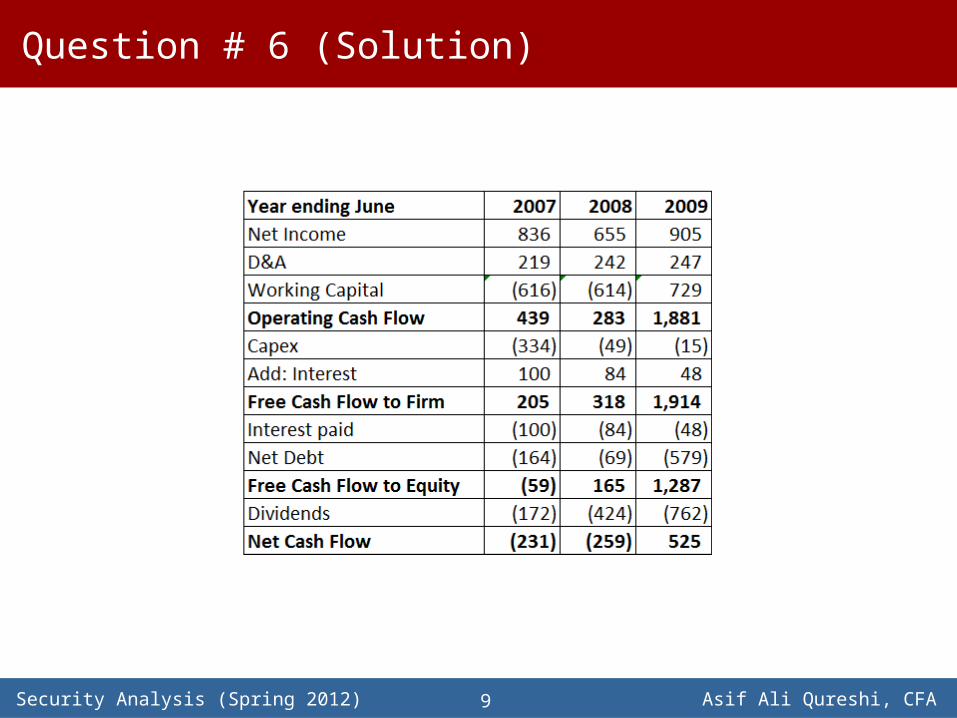

Question # 6 (Solution)

9

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

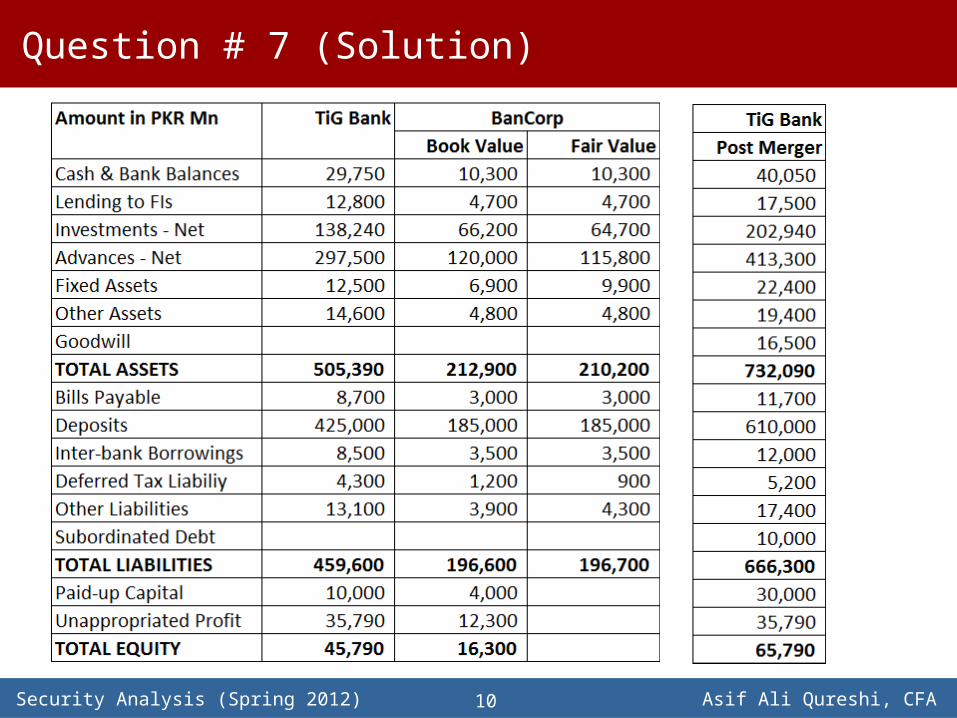

Question # 7 (Solution)

10

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

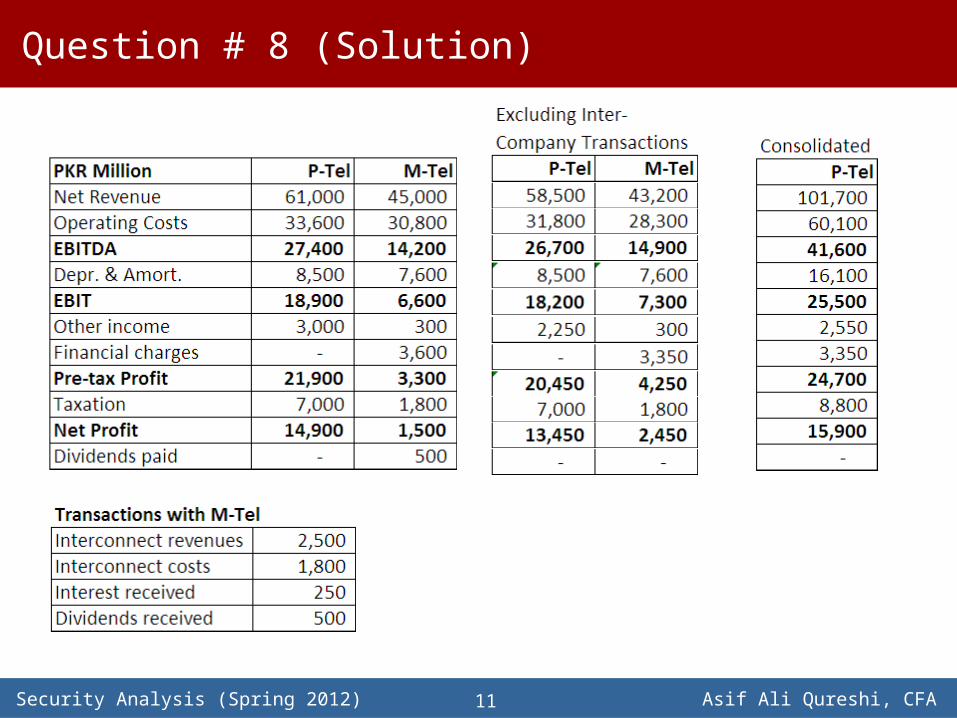

Question # 8 (Solution)

11

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

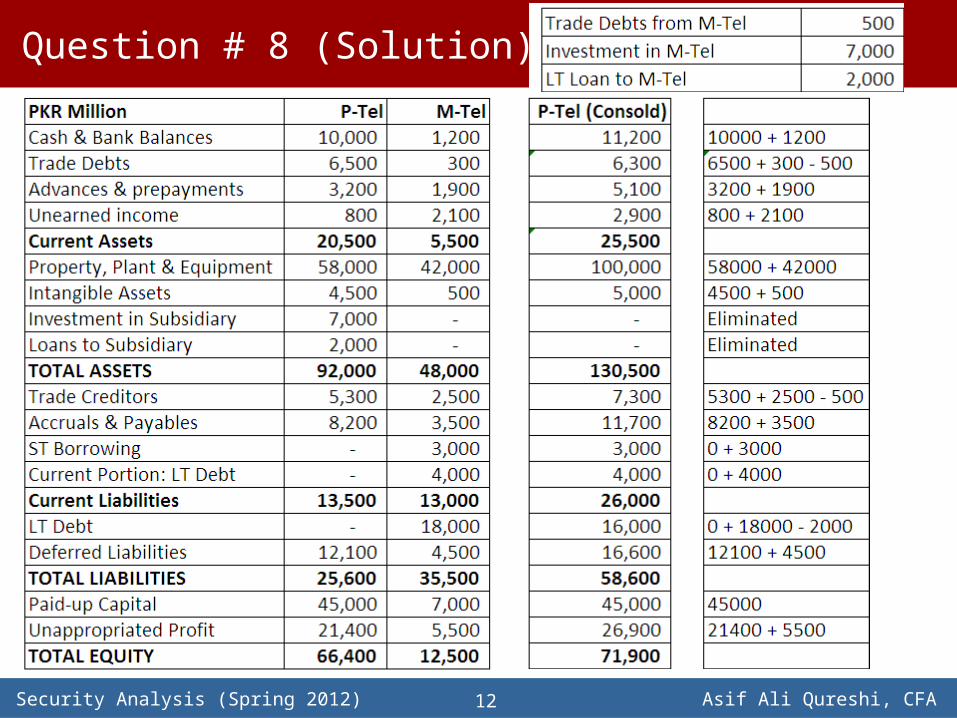

Question # 8 (Solution)

12

Spring 2012

Estimating Earning per Share (EPS)

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA14

Earnings per Share (EPS)

EPS measures the portion of a company's profit allocated to each outstanding share of common stock.

IAS-33 (Earnings Per Share) prescribes the principles for the determination and presentation of earnings per share (EPS).

Complex capital structures need to be appropriately accounted for.

When a company has any securities that are potentially convertible into common

stock (ordinary shares), it is said to have a complex capital structure.

Such securities can potentially “dilute” the ordinary shareholders’ portion in the

company’s earnings.

Examples of these kind of securities are convertible bonds, convertible preferred

stock, employee stock options and warrants.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA15

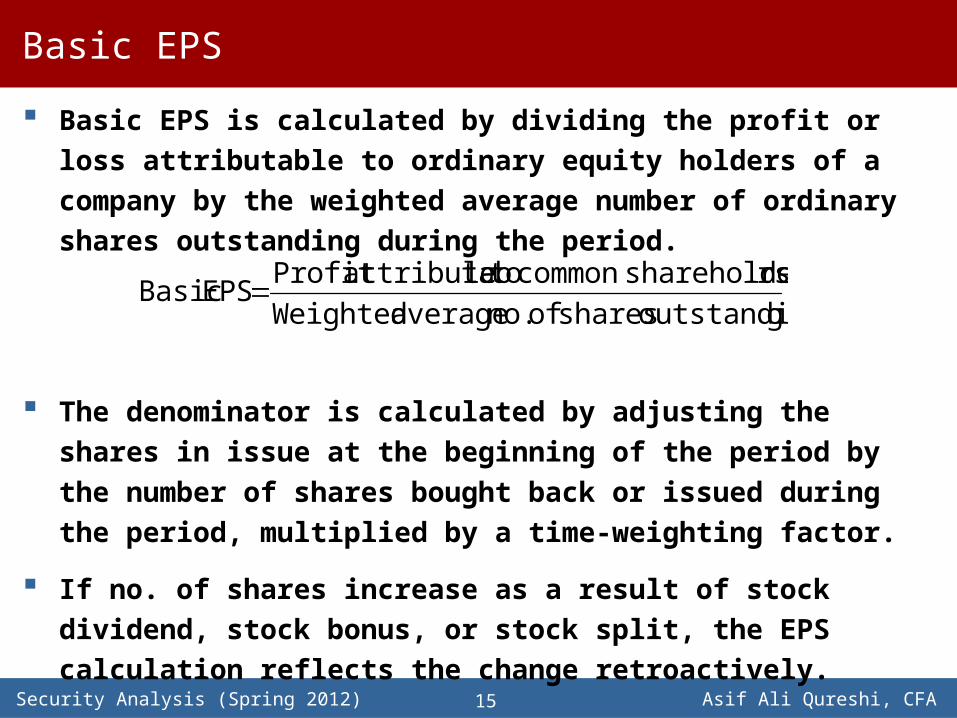

Basic EPS

Basic EPS is calculated by dividing the profit or loss attributable to ordinary equity holders of a company by the weighted average number of ordinary shares outstanding during the period.

The denominator is calculated by adjusting the shares in issue at the beginning of the period by the number of shares bought back or issued during the period, multiplied by a time-weighting factor.

If no. of shares increase as a result of stock dividend, stock bonus, or stock split, the EPS calculation reflects the change retroactively.

goutstandin sharesof no. average Weightedrsshareholde common to leattributab Profit

EPS Basic

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA16

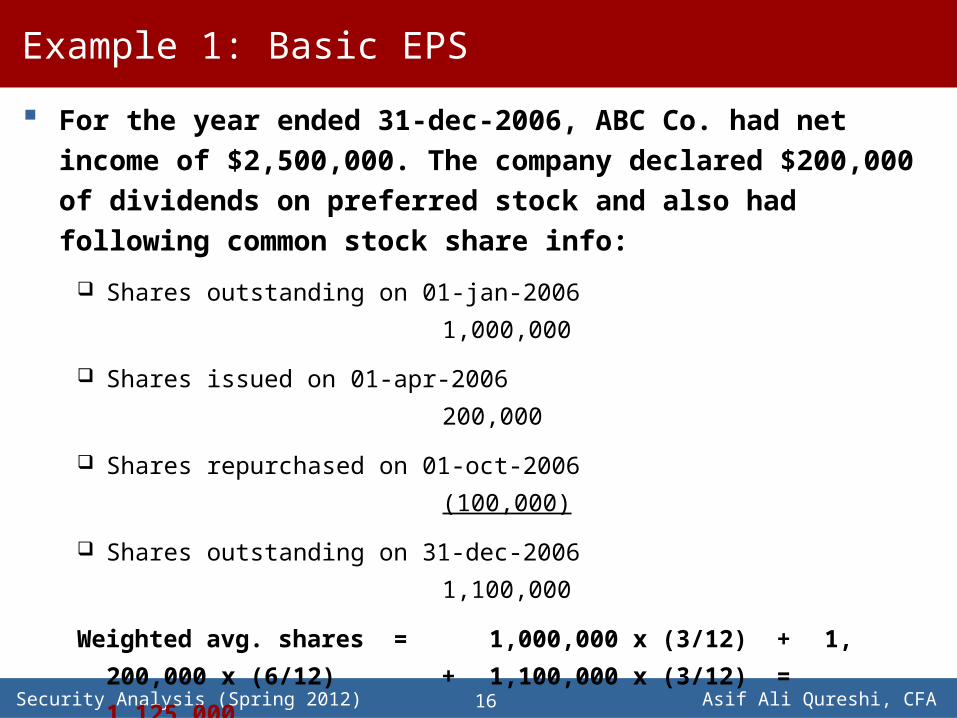

Example 1: Basic EPS

For the year ended 31-dec-2006, ABC Co. had net income of $2,500,000. The company declared $200,000 of dividends on preferred stock and also had following common stock share info:

Shares outstanding on 01-jan-2006 1,000,000

Shares issued on 01-apr-2006 200,000

Shares repurchased on 01-oct-2006 (100,000)

Shares outstanding on 31-dec-2006 1,100,000

Weighted avg. shares = 1,000,000 x (3/12) + 1, 200,000 x

(6/12) + 1,100,000 x (3/12) = 1,125,000

Basic EPS = ($2,500,000 – $200,000) / 1,125,000 = $2.04

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

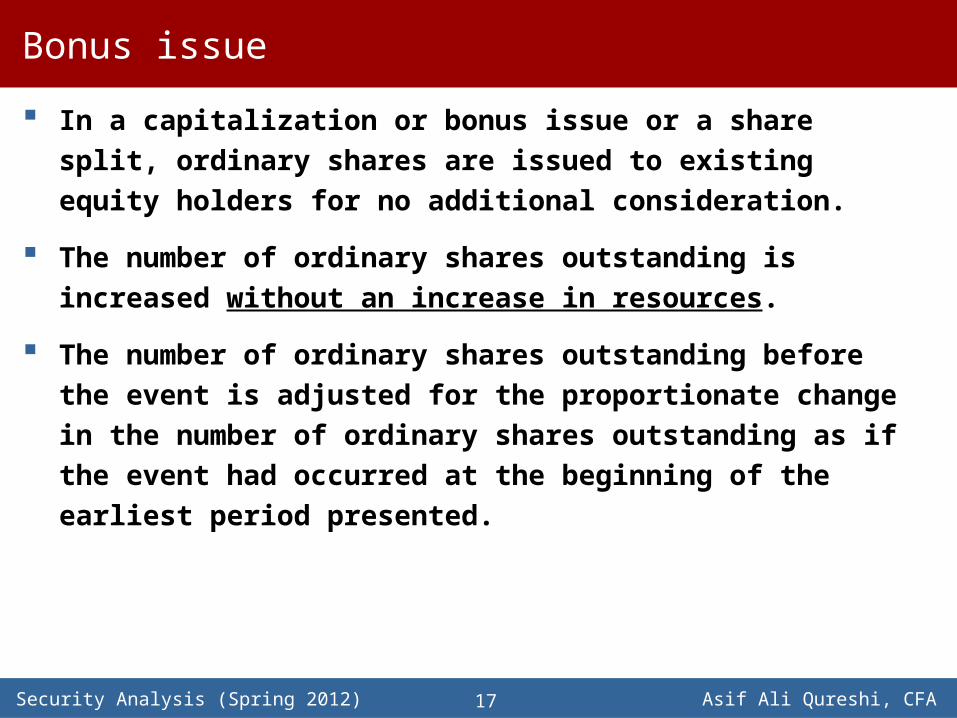

Bonus issue

In a capitalization or bonus issue or a share split, ordinary shares are issued to existing equity holders for no additional consideration.

The number of ordinary shares outstanding is increased without an increase in resources.

The number of ordinary shares outstanding before the event is adjusted for the proportionate change in the number of ordinary shares outstanding as if the event had occurred at the beginning of the earliest period presented.

17

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

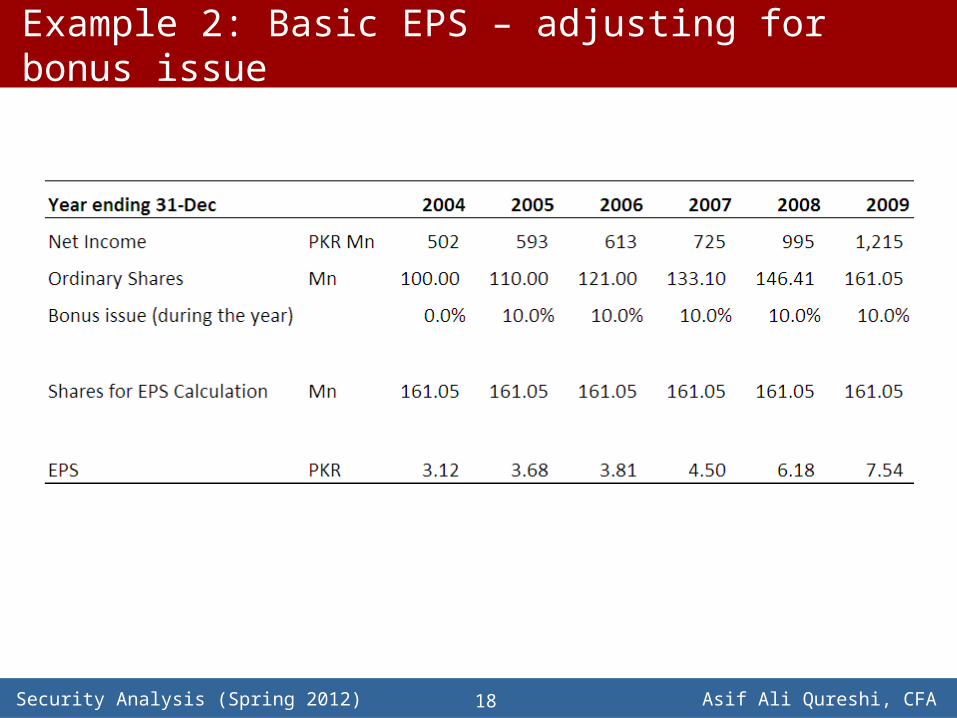

Example 2: Basic EPS – adjusting for bonus issue

18

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

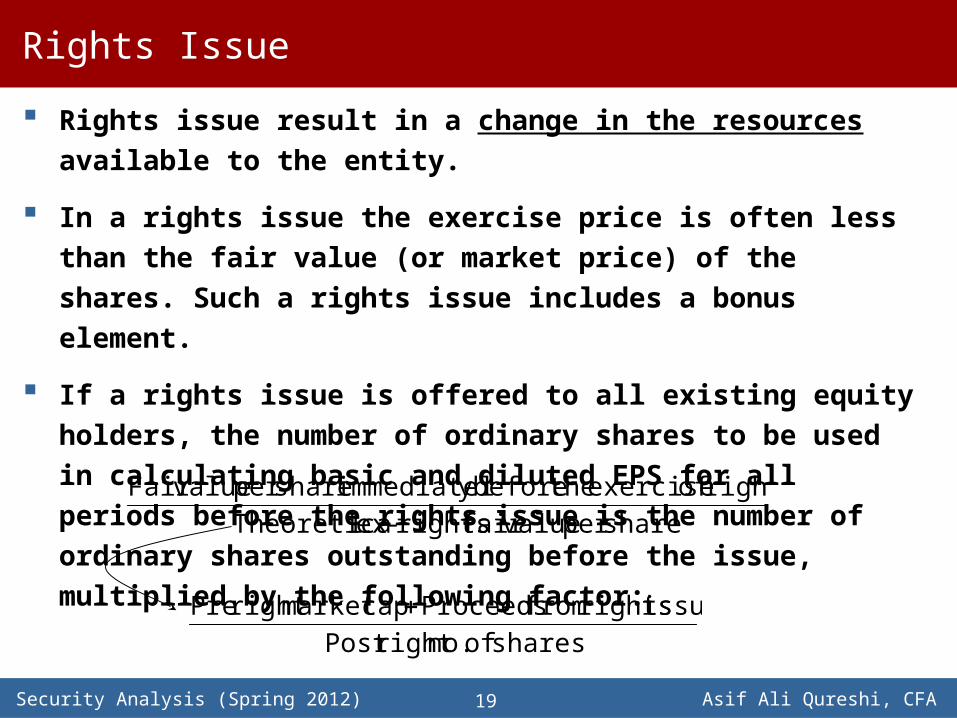

Rights Issue

Rights issue result in a change in the resources available to the entity.

In a rights issue the exercise price is often less than the fair value (or market price) of the shares. Such a rights issue includes a bonus element.

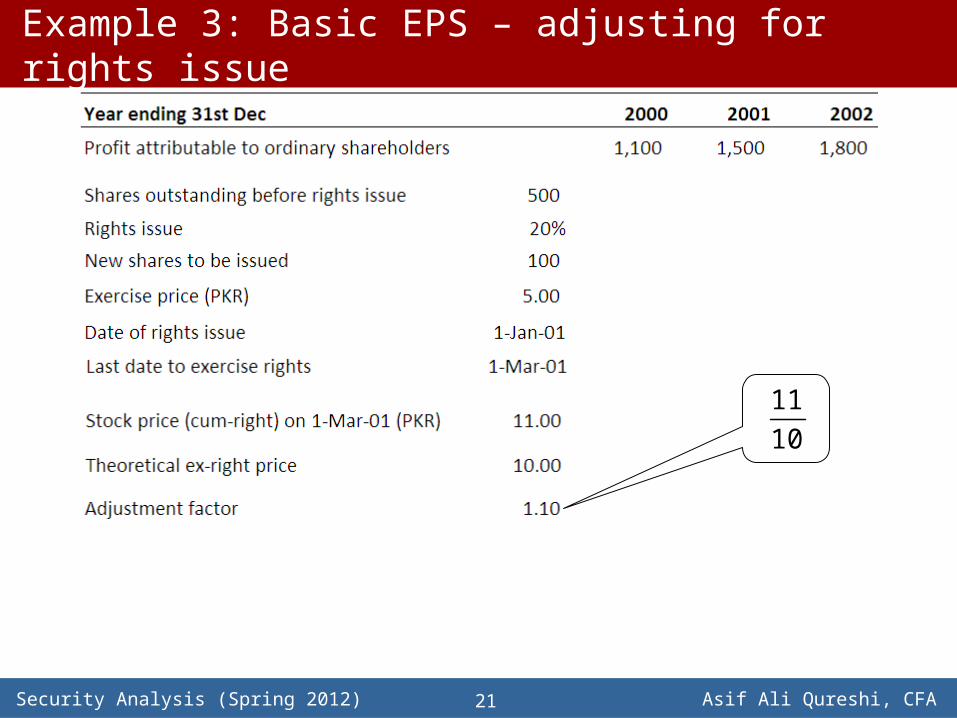

If a rights issue is offered to all existing equity holders, the number of ordinary shares to be used in calculating basic and diluted EPS for all periods before the rights issue is the number of ordinary shares outstanding before the issue, multiplied by the following factor:

19

share per value fair rights-ex lTheoreticarightsof exercise the before yimmediatel share per value Fair

sharesof no. right Postissue rights from Proceeds cap market right Pre

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

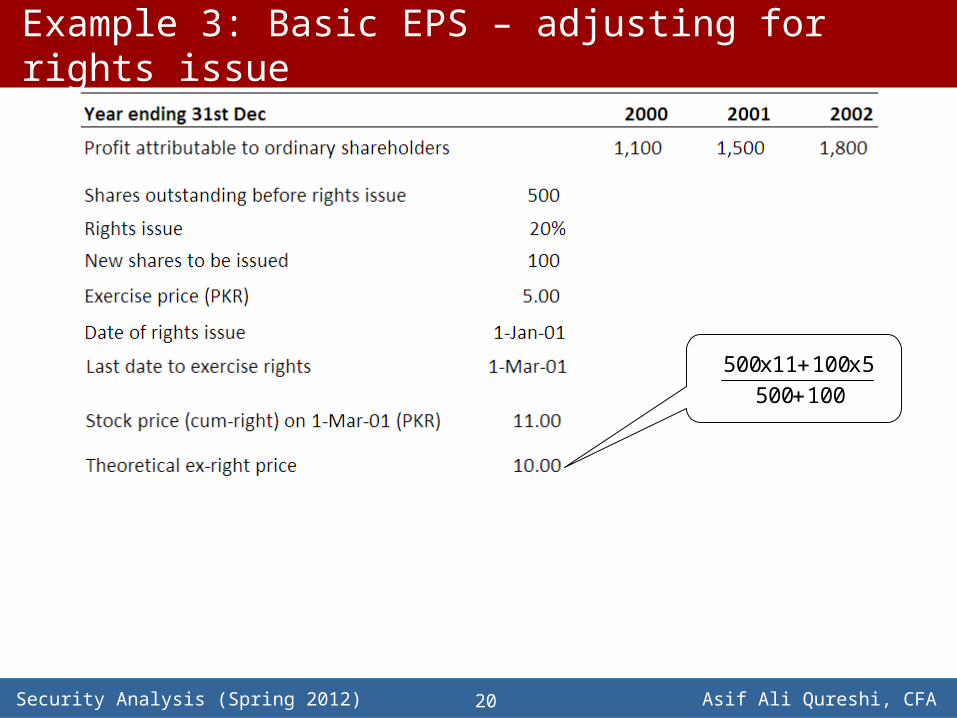

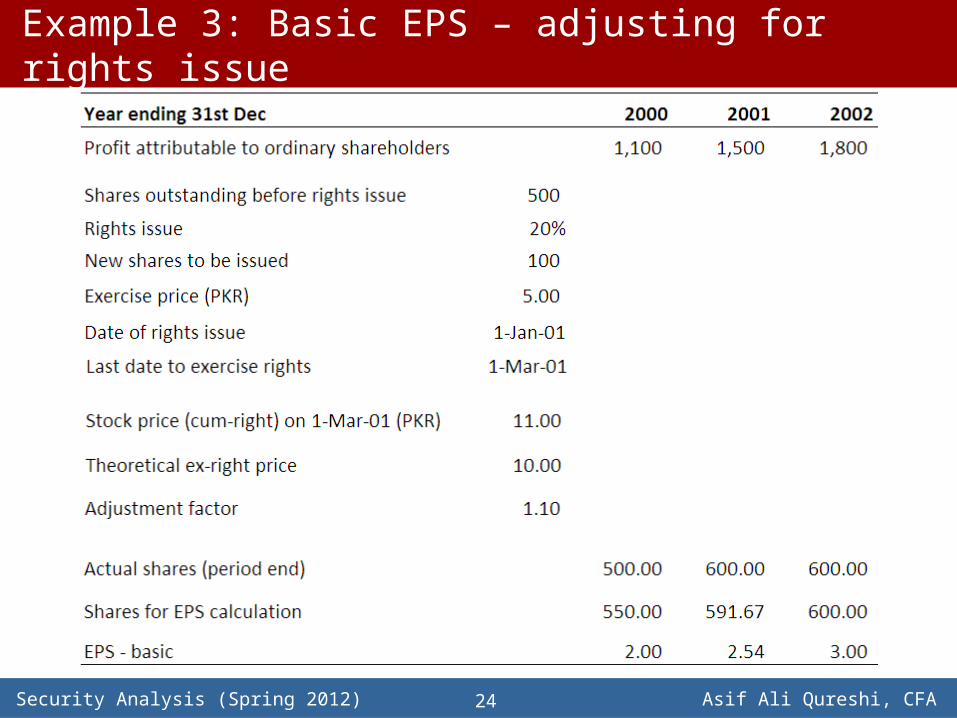

Example 3: Basic EPS – adjusting for rights issue

20

100 5005 x 100 11 x 500

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

Example 3: Basic EPS – adjusting for rights issue

21

1011

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

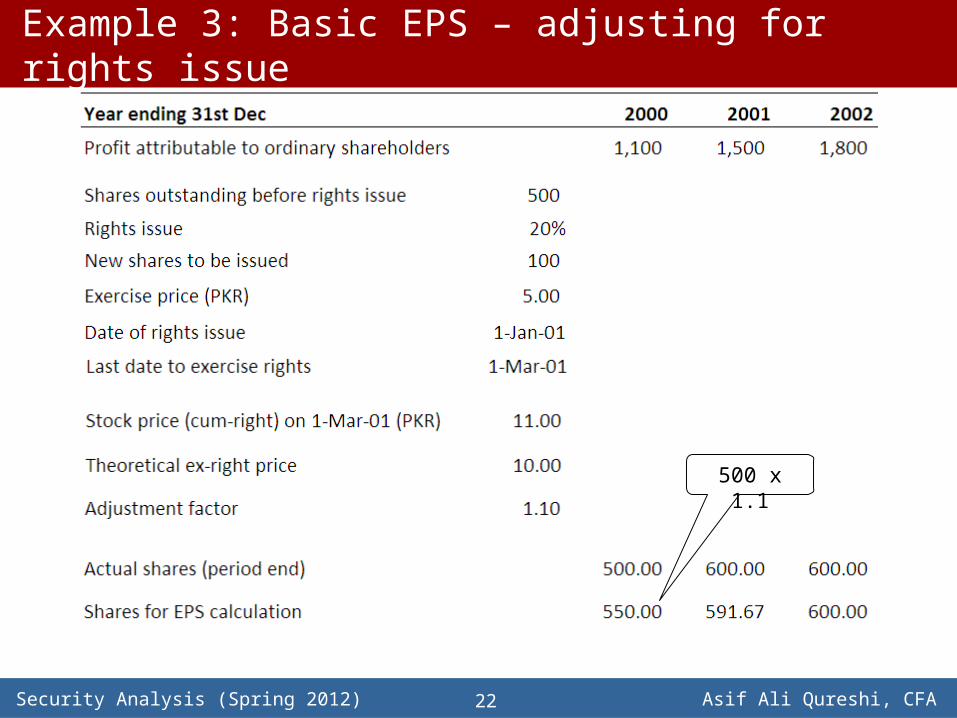

Example 3: Basic EPS – adjusting for rights issue

22

500 x 1.1

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

Example 3: Basic EPS – adjusting for rights issue

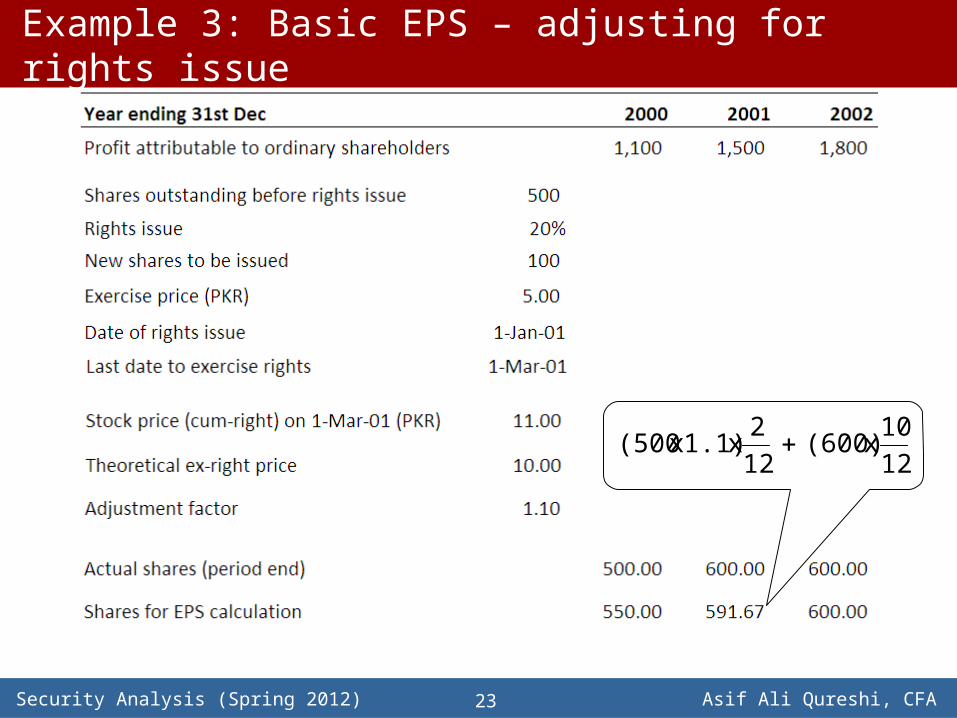

23

1210 x (600)

122

x 1.1) x (500

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA

Example 3: Basic EPS – adjusting for rights issue

24

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA25

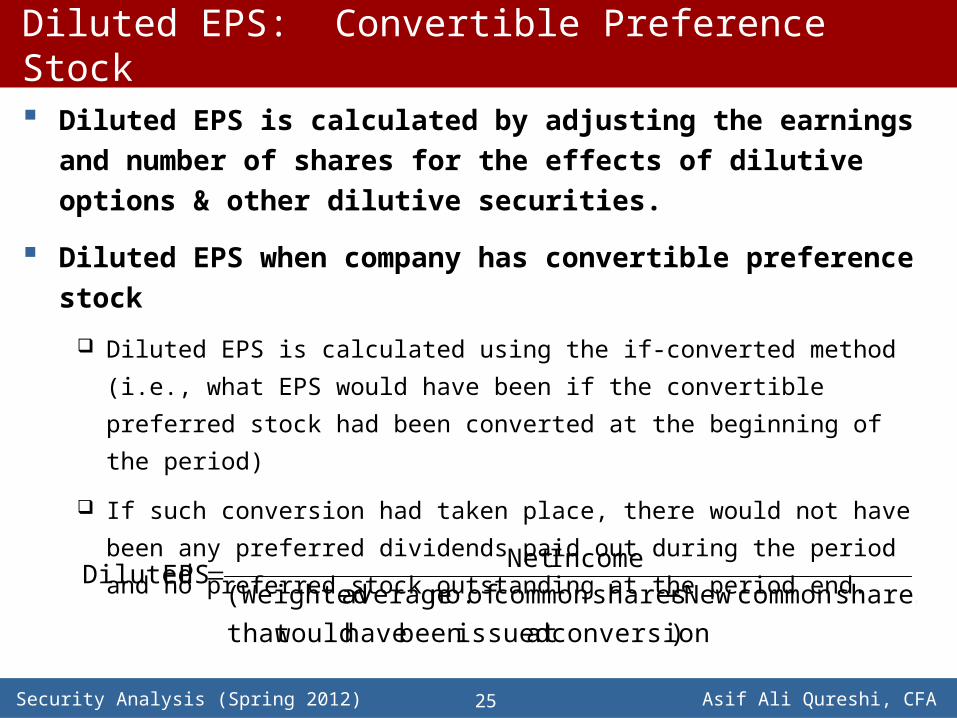

Diluted EPS: Convertible Preference Stock

Diluted EPS is calculated by adjusting the earnings and number of shares for the effects of dilutive options & other dilutive securities.

Diluted EPS when company has convertible preference stock

Diluted EPS is calculated using the if-converted method (i.e., what EPS would have

been if the convertible preferred stock had been converted at the beginning of the

period)

If such conversion had taken place, there would not have been any preferred

dividends paid out during the period and no preferred stock outstanding at the

period end.

)conversion at issued been have would that shares common New shares commonof no. average (Weighted

Income Net EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA26

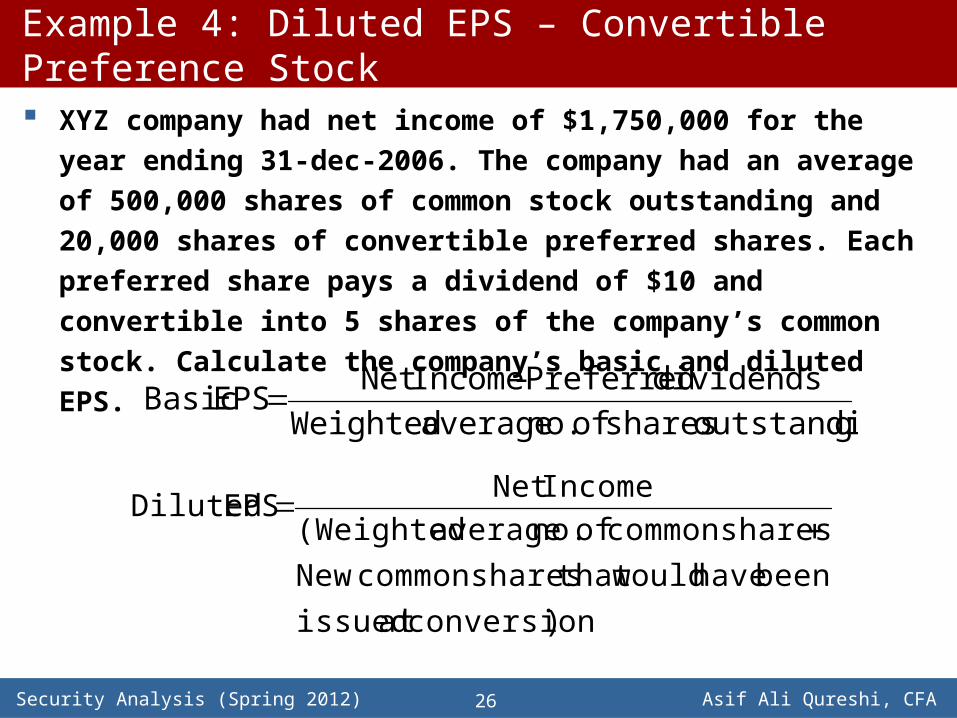

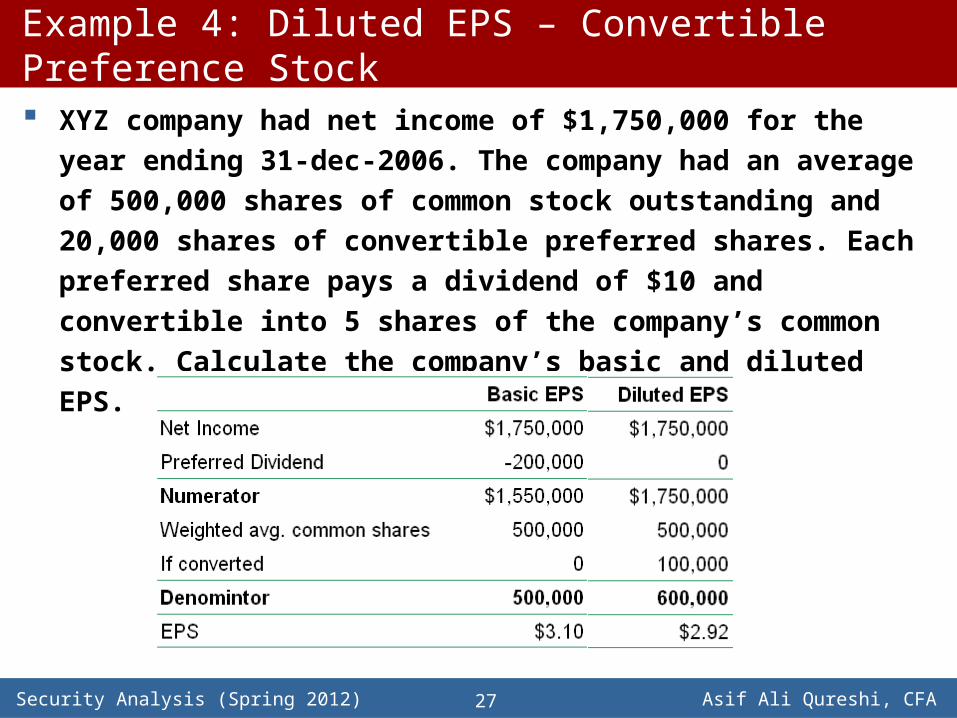

Example 4: Diluted EPS – Convertible Preference Stock XYZ company had net income of $1,750,000 for the year ending 31-dec-

2006. The company had an average of 500,000 shares of common stock outstanding and 20,000 shares of convertible preferred shares. Each preferred share pays a dividend of $10 and convertible into 5 shares of the company’s common stock. Calculate the company’s basic and diluted EPS.

goutstandin sharesof no. average Weighteddividends Preferred - Income Net

EPS Basic

)conversion at issued been have would that shares common New shares commonof no. average (Weighted

Income Net EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA27

Example 4: Diluted EPS – Convertible Preference Stock XYZ company had net income of $1,750,000 for the year ending 31-dec-

2006. The company had an average of 500,000 shares of common stock outstanding and 20,000 shares of convertible preferred shares. Each preferred share pays a dividend of $10 and convertible into 5 shares of the company’s common stock. Calculate the company’s basic and diluted EPS.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA28

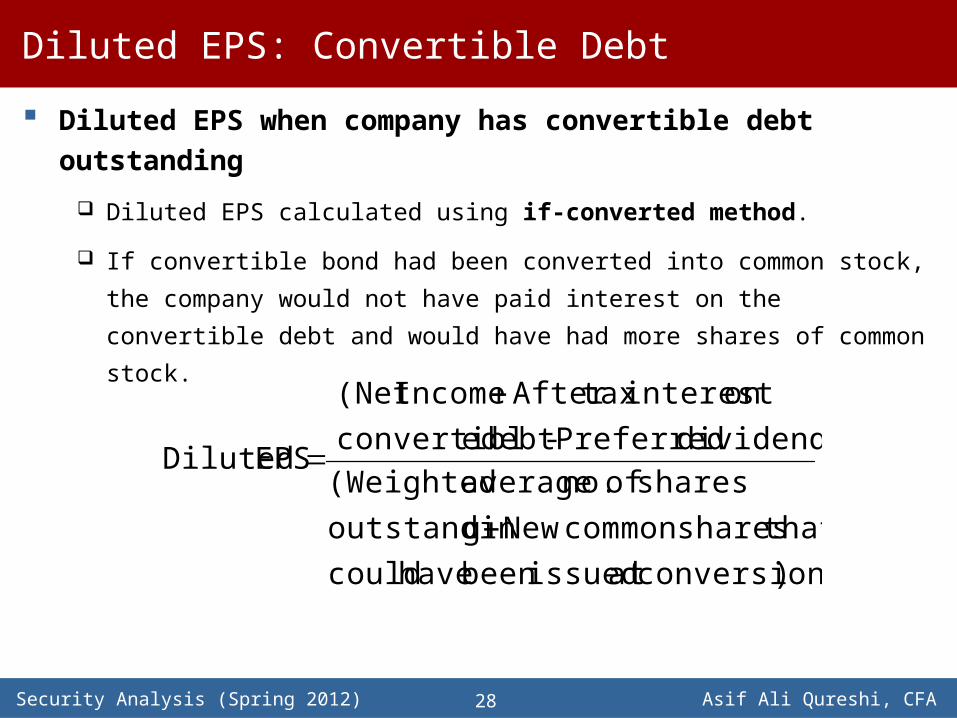

Diluted EPS: Convertible Debt

Diluted EPS when company has convertible debt outstanding

Diluted EPS calculated using if-converted method.

If convertible bond had been converted into common stock, the company would not

have paid interest on the convertible debt and would have had more shares of

common stock.

)conversion at issued been have couldthat shares common New goutstandin

sharesof no. average (Weighteddividends) Preferred - debt econvertibl

on interest tax After Income (Net

EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA29

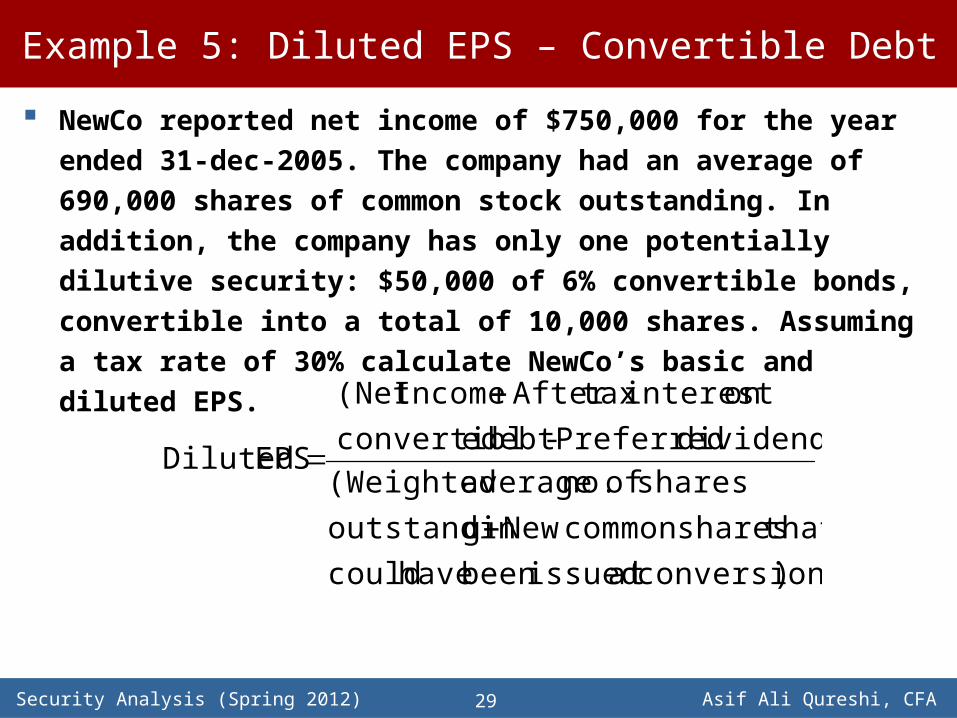

Example 5: Diluted EPS – Convertible Debt

NewCo reported net income of $750,000 for the year ended 31-dec-2005. The company had an average of 690,000 shares of common stock outstanding. In addition, the company has only one potentially dilutive security: $50,000 of 6% convertible bonds, convertible into a total of 10,000 shares. Assuming a tax rate of 30% calculate NewCo’s basic and diluted EPS.

)conversion at issued been have couldthat shares common New goutstandin

sharesof no. average (Weighteddividends) Preferred - debt econvertibl

on interest tax After Income (Net

EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA30

Example 5: Diluted EPS – Convertible Debt

NewCo reported net income of $750,000 for the year ended 31-dec-2005. The company had an average of 690,000 shares of common stock outstanding. In addition, the company has only one potentially dilutive security: $50,000 of 6% convertible bonds, convertible into a total of 10,000 shares. Assuming a tax rate of 30% calculate NewCo’s basic and diluted EPS.

$50,000 x 6% x (1 – 30%)

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA31

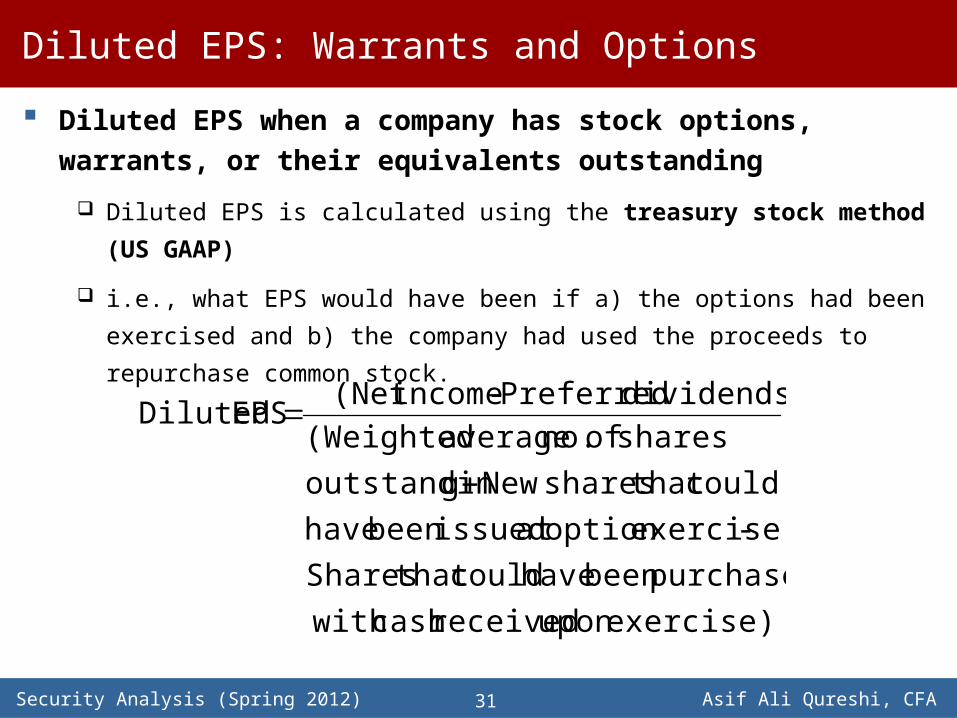

Diluted EPS: Warrants and Options

Diluted EPS when a company has stock options, warrants, or their equivalents outstanding

Diluted EPS is calculated using the treasury stock method (US GAAP)

i.e., what EPS would have been if a) the options had been exercised and b) the

company had used the proceeds to repurchase common stock.

exercise) upon received cash with purchased been have could that Shares

- exercise option at issued been have could that shares New goutstandin

sharesof no. average (Weighteddividends) Preferred - income (Net

EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA32

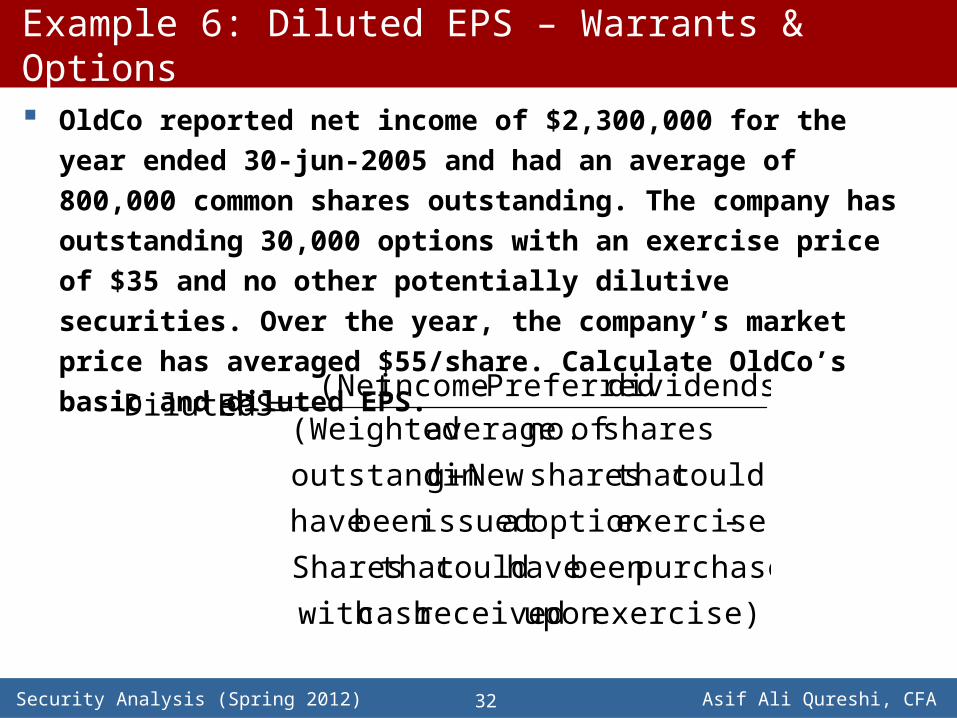

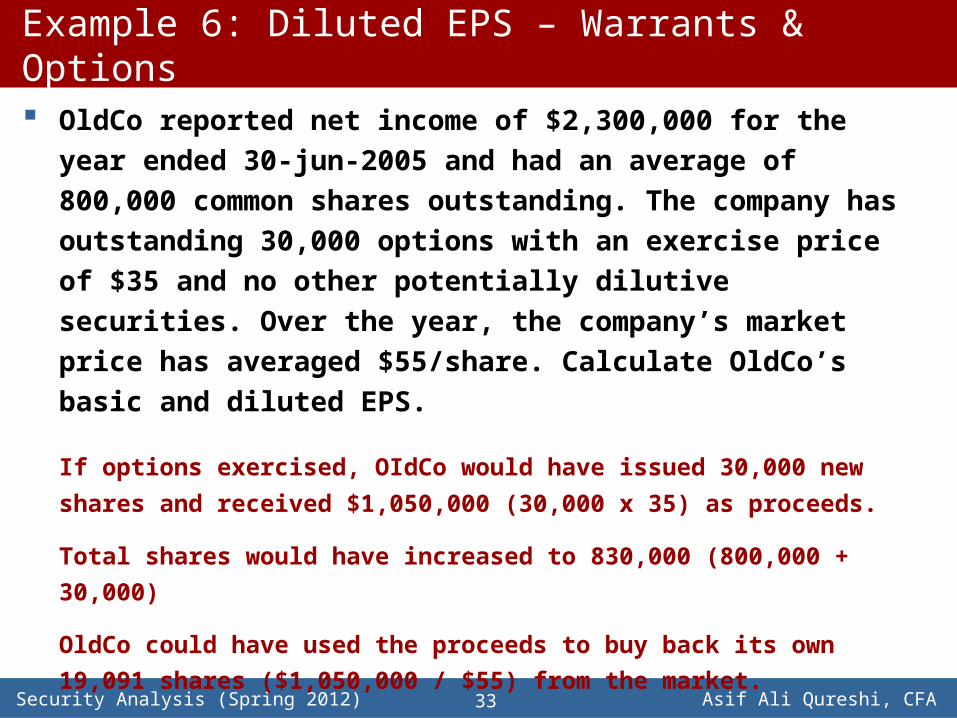

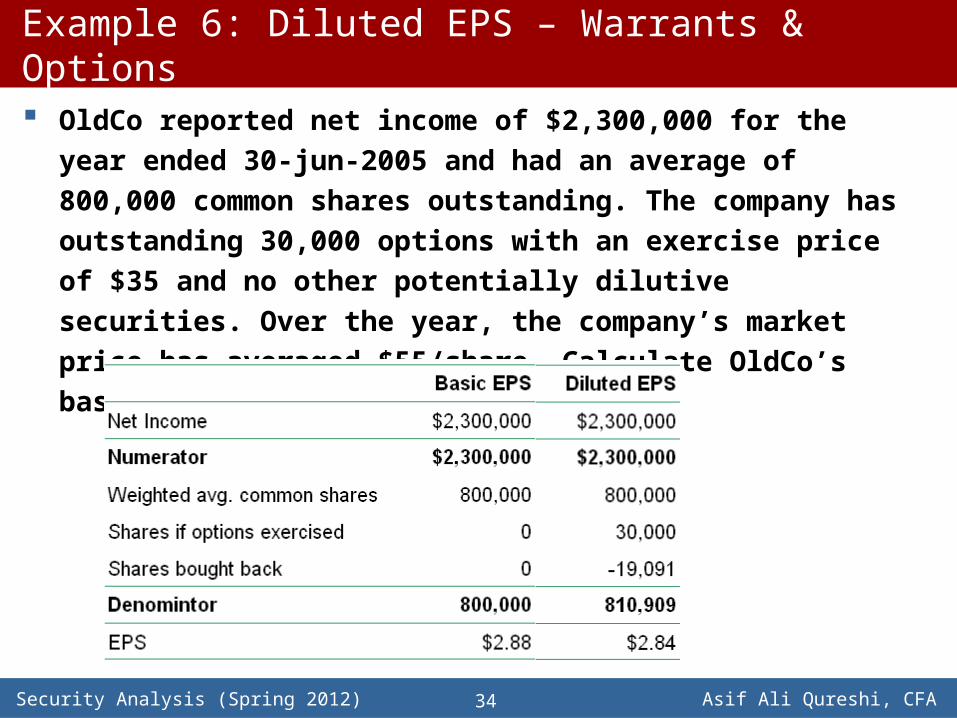

Example 6: Diluted EPS – Warrants & Options

OldCo reported net income of $2,300,000 for the year ended 30-jun-2005 and had an average of 800,000 common shares outstanding. The company has outstanding 30,000 options with an exercise price of $35 and no other potentially dilutive securities. Over the year, the company’s market price has averaged $55/share. Calculate OldCo’s basic and diluted EPS.

exercise) upon received cash with purchased been have could that Shares

- exercise option at issued been have could that shares New goutstandin

sharesof no. average (Weighteddividends) Preferred - income (Net

EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA33

Example 6: Diluted EPS – Warrants & Options

OldCo reported net income of $2,300,000 for the year ended 30-jun-2005 and had an average of 800,000 common shares outstanding. The company has outstanding 30,000 options with an exercise price of $35 and no other potentially dilutive securities. Over the year, the company’s market price has averaged $55/share. Calculate OldCo’s basic and diluted EPS.

If options exercised, OIdCo would have issued 30,000 new shares and received $1,050,000 (30,000 x 35) as proceeds.

Total shares would have increased to 830,000 (800,000 + 30,000)

OldCo could have used the proceeds to buy back its own 19,091 shares ($1,050,000 / $55) from the market.

Total shares would resultantly reduce to 810,909 (830,000 – 19,091).

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA34

Example 6: Diluted EPS – Warrants & Options

OldCo reported net income of $2,300,000 for the year ended 30-jun-2005 and had an average of 800,000 common shares outstanding. The company has outstanding 30,000 options with an exercise price of $35 and no other potentially dilutive securities. Over the year, the company’s market price has averaged $55/share. Calculate OldCo’s basic and diluted EPS.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA35

Anti-dilutive Securities

It is possible that some potentially convertible securities could be antidilutive i.e., their inclusion in the computation would result in an EPS higher than the company’s basic EPS.

Under accounting standards, antidilutive securities are not included in the calculation of diluted EPS.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA36

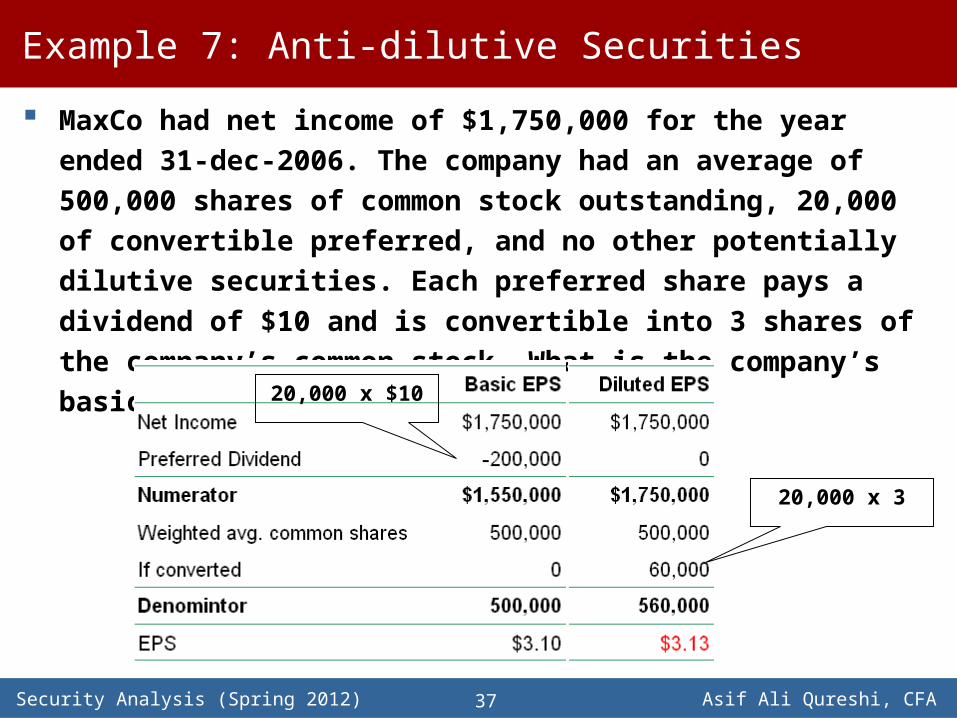

Example 7: Anti-dilutive Securities

MaxCo had net income of $1,750,000 for the year ended 31-dec-2006. The company had an average of 500,000 shares of common stock outstanding, 20,000 of convertible preferred, and no other potentially dilutive securities. Each preferred share pays a dividend of $10 and is convertible into 3 shares of the company’s common stock. What is the company’s basic and diluted EPS?

)conversion at issued been have would that shares common New shares commonof no. average (Weighted

Income Net EPS Diluted

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA37

Example 7: Anti-dilutive Securities

MaxCo had net income of $1,750,000 for the year ended 31-dec-2006. The company had an average of 500,000 shares of common stock outstanding, 20,000 of convertible preferred, and no other potentially dilutive securities. Each preferred share pays a dividend of $10 and is convertible into 3 shares of the company’s common stock. What is the company’s basic and diluted EPS?

20,000 x 3

20,000 x $10

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA38

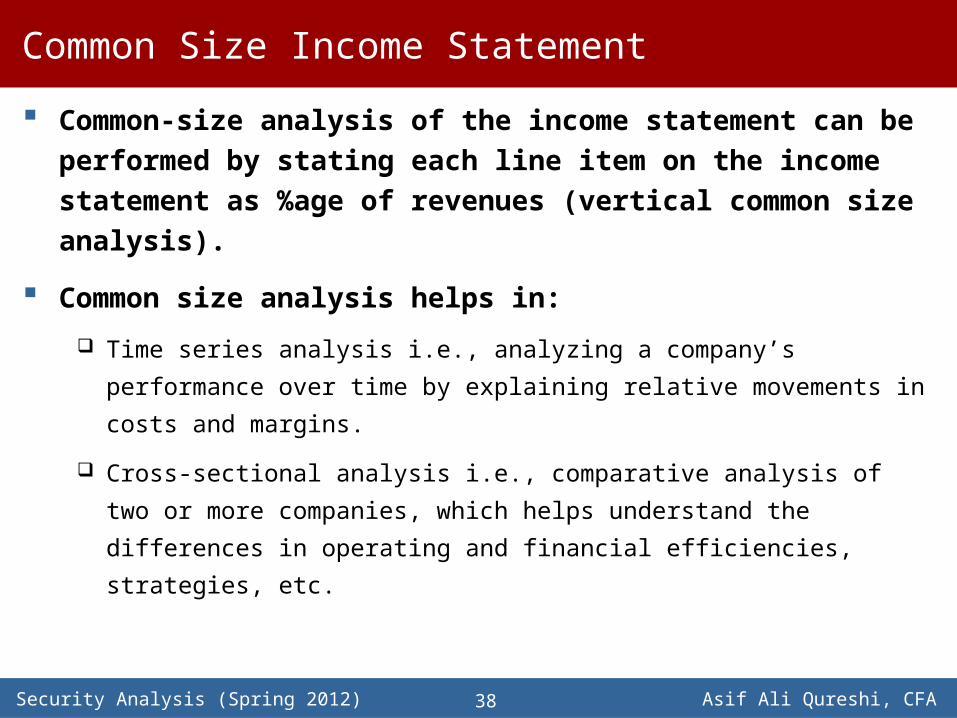

Common Size Income Statement

Common-size analysis of the income statement can be performed by stating each line item on the income statement as %age of revenues (vertical common size analysis).

Common size analysis helps in:

Time series analysis i.e., analyzing a company’s performance over time by explaining

relative movements in costs and margins.

Cross-sectional analysis i.e., comparative analysis of two or more companies, which

helps understand the differences in operating and financial efficiencies, strategies,

etc.

Spring 2012

Financial Analysis Techniques

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA40

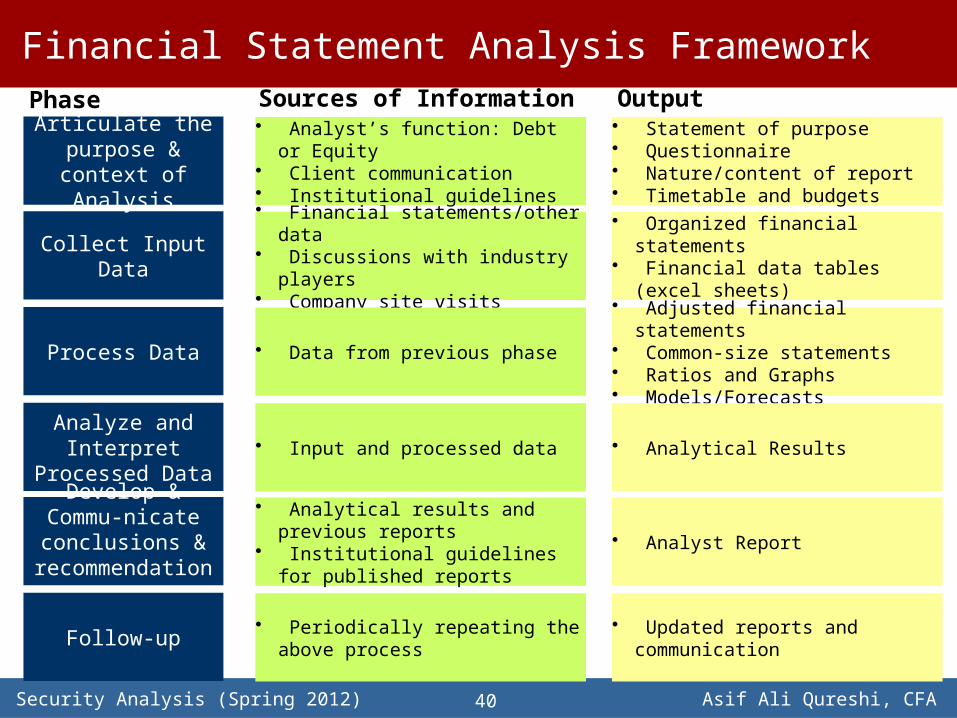

Financial Statement Analysis Framework

• Financial statements/other data• Discussions with industry players• Company site visits

• Data from previous phase

• Input and processed data

• Analytical results and previous reports• Institutional guidelines for published

reports

• Periodically repeating the above process

• Organized financial statements• Financial data tables (excel sheets)

• Adjusted financial statements• Common-size statements• Ratios and Graphs• Models/Forecasts

• Analytical Results

• Analyst Report

• Updated reports and communication

Collect Input Data

Process Data

Analyze and Interpret Processed Data

Develop & Commu-nicate conclusions &

recommendations

Follow-up

Articulate the purpose & context of

Analysis

Phase• Analyst’s function: Debt or Equity• Client communication• Institutional guidelines

Sources of Information• Statement of purpose• Questionnaire• Nature/content of report• Timetable and budgets

Output

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA41

Analysis Tools and Techniques

Financial Ratios

Common Size Analysis

Graphical Analysis

Regression Analysis

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA42

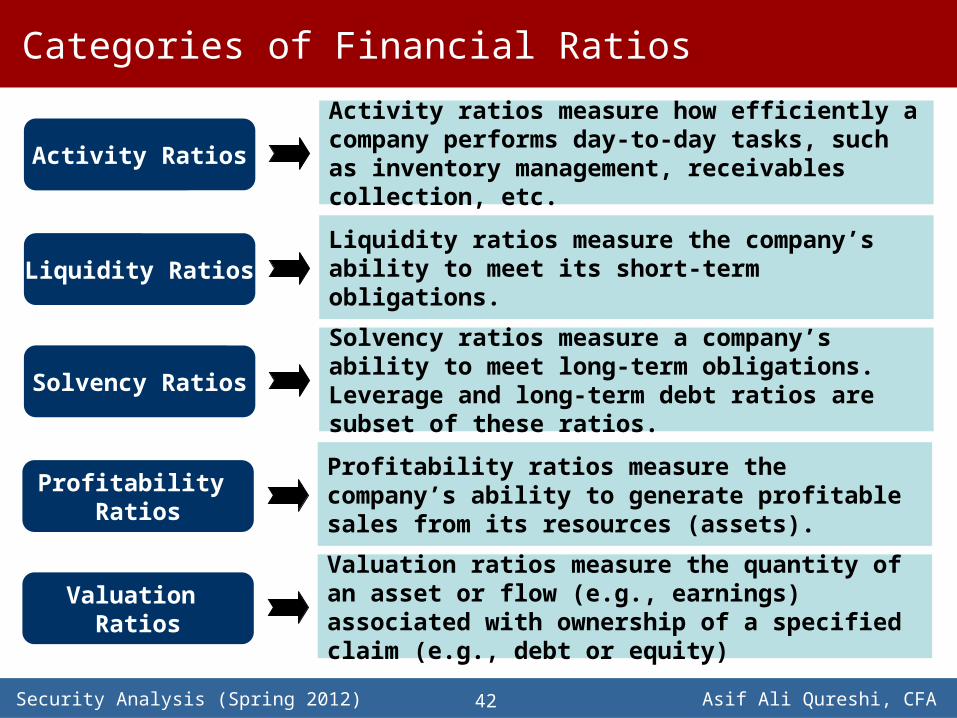

Categories of Financial Ratios

Activity RatiosActivity ratios measure how efficiently a company performs day-to-day tasks, such as inventory management, receivables collection, etc.

Liquidity RatiosLiquidity ratios measure the company’s ability to meet its short-term obligations.

Solvency RatiosSolvency ratios measure a company’s ability to meet long-term obligations. Leverage and long-term debt ratios are subset of these ratios.

Profitability Ratios

Profitability ratios measure the company’s ability to generate profitable sales from its resources (assets).

Valuation Ratios

Valuation ratios measure the quantity of an asset or flow (e.g., earnings) associated with ownership of a specified claim (e.g., debt or equity)

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA43

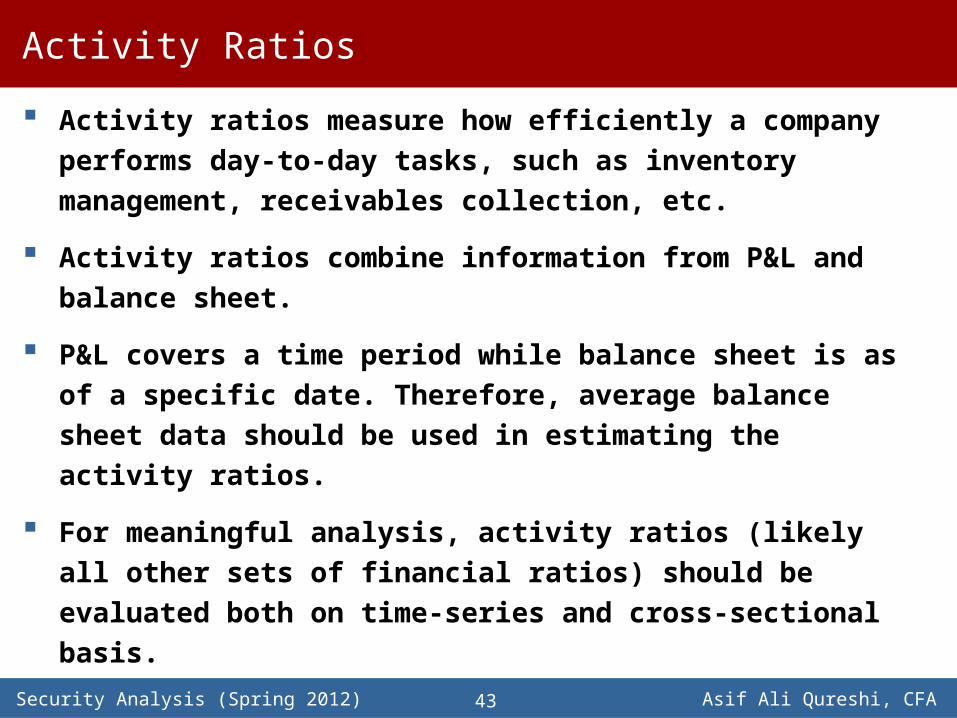

Activity Ratios

Activity ratios measure how efficiently a company performs day-to-day tasks, such as inventory management, receivables collection, etc.

Activity ratios combine information from P&L and balance sheet.

P&L covers a time period while balance sheet is as of a specific date. Therefore, average balance sheet data should be used in estimating the activity ratios.

For meaningful analysis, activity ratios (likely all other sets of financial ratios) should be evaluated both on time-series and cross-sectional basis.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA44

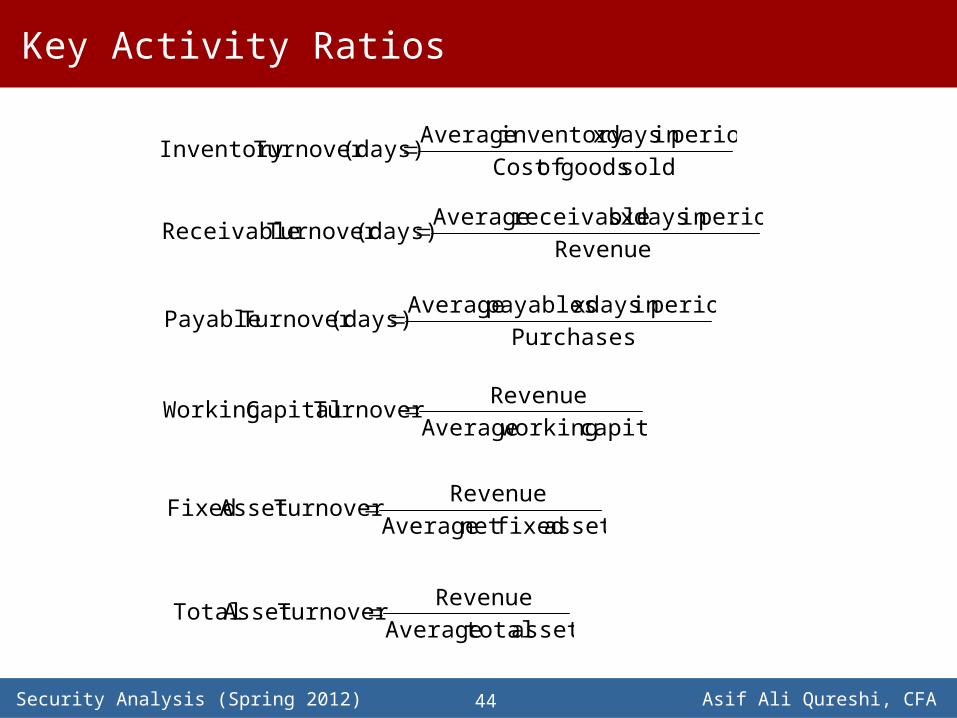

Key Activity Ratios

sold goodsof Costperiod in days x inventory Average

(days) Turnover Inventory

Revenueperiod in days x sreceivable Average

(days) Turnover Receivable

Purchasesperiod in days x payables Average

(days) Turnover Payable

capital working AverageRevenue

Turnover Capital Working

assets fixed net AverageRevenue

Turnover Asset Fixed

assets total AverageRevenue

Turnover Asset Total

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA45

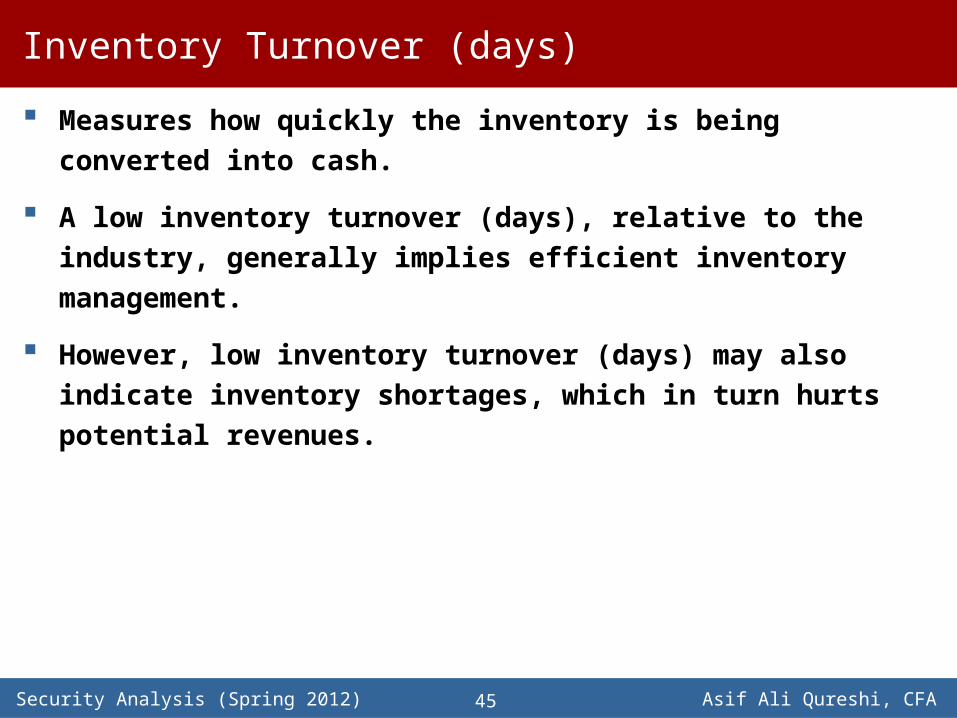

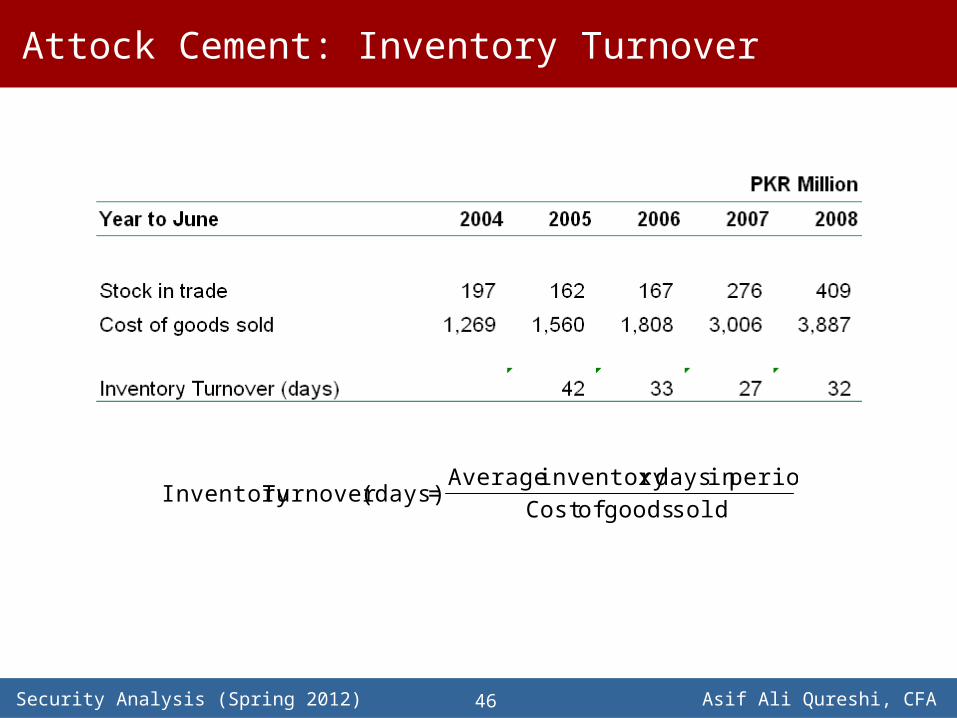

Inventory Turnover (days)

Measures how quickly the inventory is being converted into cash.

A low inventory turnover (days), relative to the industry, generally implies efficient inventory management.

However, low inventory turnover (days) may also indicate inventory shortages, which in turn hurts potential revenues.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA46

Attock Cement: Inventory Turnover

sold goods of Cost

period in daysx inventory Average = (days) TurnoverInventory

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA47

Receivables Turnover (days)

Measures how quickly the company is converting its receivables into cash.

A low receivable turnover (days), relative to the industry, generally indicates efficient receivables collection and low (client) credit risks.

However, the same may also indicate that the company is potentially loosing sales due to over-stringent credit policies.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA48

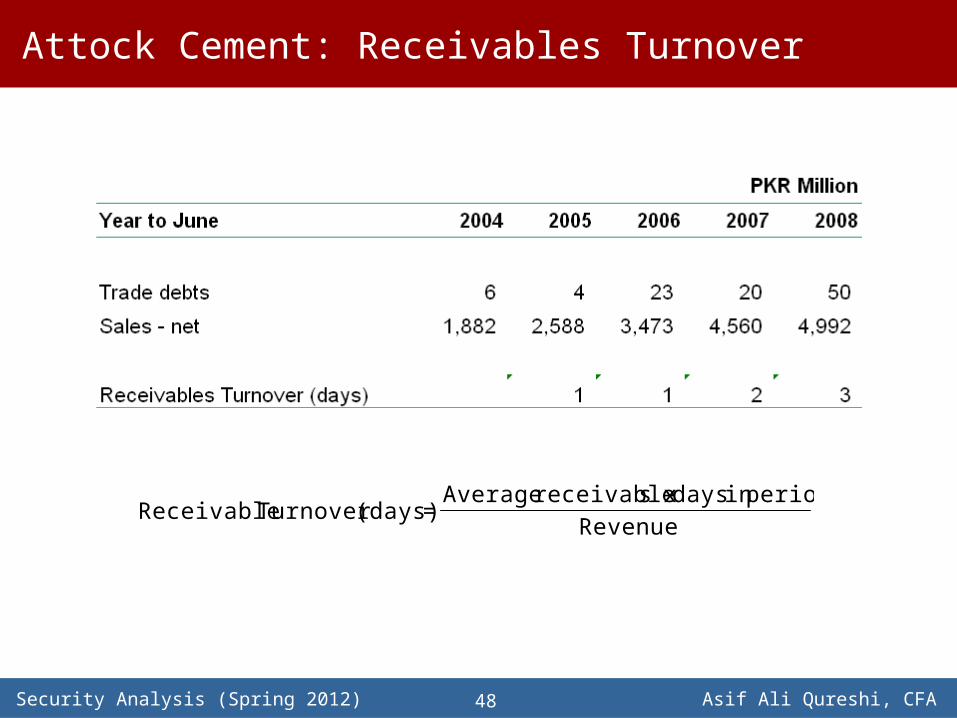

Attock Cement: Receivables Turnover

Revenue

period in days x sreceivable Average = (days) Turnover Receivable

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA49

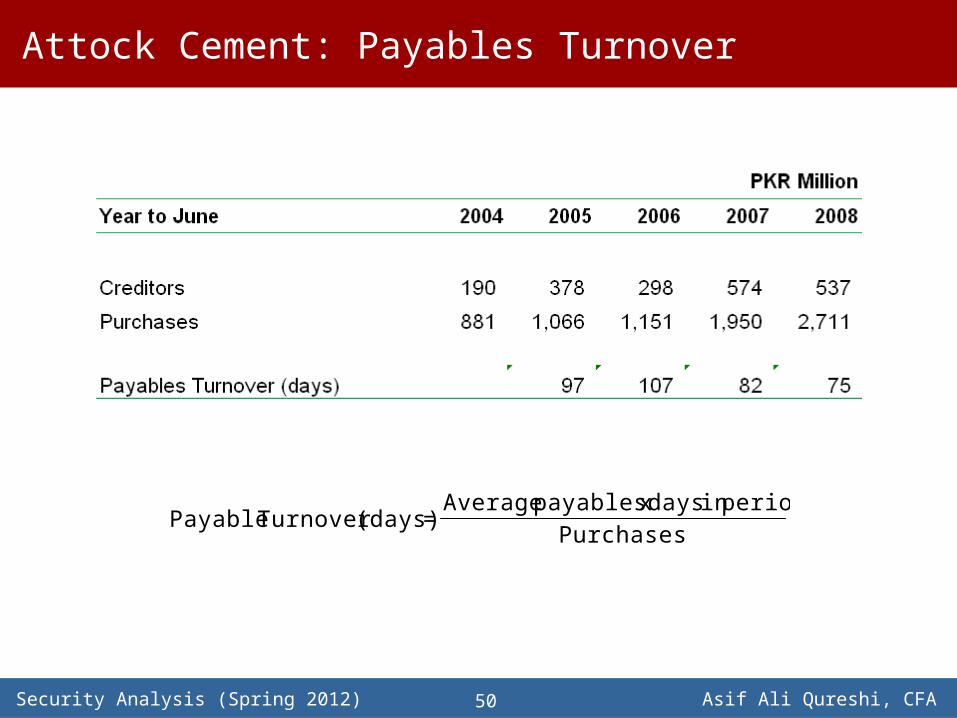

Payables Turnover (days)

Measures average suppliers payment cycle of a company.

A high payable turnovers (days), relative to the industry, indicates that the company has more favorable credit terms from its suppliers.

However, for a given period, the same may also indicate that the company is facing problems in meeting its payments towards its suppliers.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA50

Attock Cement: Payables Turnover

Purchases

period in days x payables Average = (days) Turnover Payable

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA51

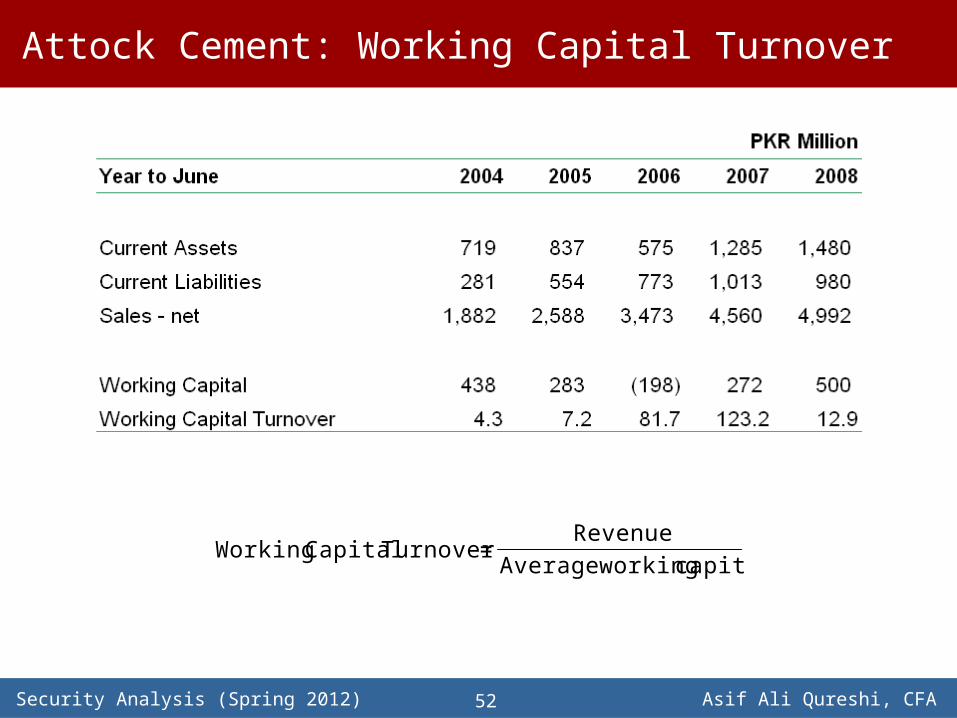

Working Capital Turnover

Measures how efficiently the company generates revenue with its working capital.

A high working capital, relative to industry, would indicate higher efficiency.

For some companies, working capital can be near zero or negative, which renders this ratio incapable of being interpreted. Asset turnover ratios are more useful in such situations.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA52

Attock Cement: Working Capital Turnover

capital workingAverage

Revenue = Turnover Capital Working

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA53

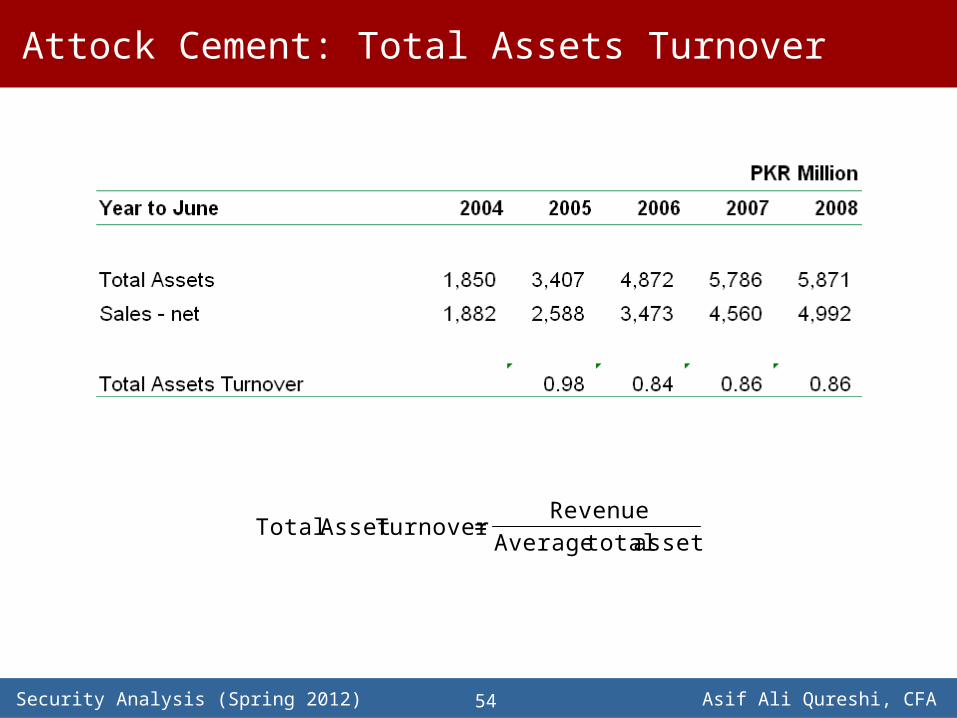

Assets turnover

Measures the company’s overall ability to generate revenues with a given level of assets.

A higher ratio, relative to the industry, generally shows greater efficiency.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA54

Attock Cement: Total Assets Turnover

assets total Average

Revenue = Turnover AssetTotal

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA55

Liquidity Ratios

Liquidity ratios measure the company’s ability to meet its short-term obligations.

In day-to-day operations, liquidity management is typically achieved through efficient use of assets. In the medium term, liquidity is also addressed by managing the structure of liabilities.

Contingent liabilities, such as letters of credit or financial guarantees, can also be relevant when assessing liquidity.

The level of liquidity needed varies markedly from one industry to another. Liquidity ratios of sectors such as Utilities and Telecoms, are generally lower than those for manufacturing industries.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA56

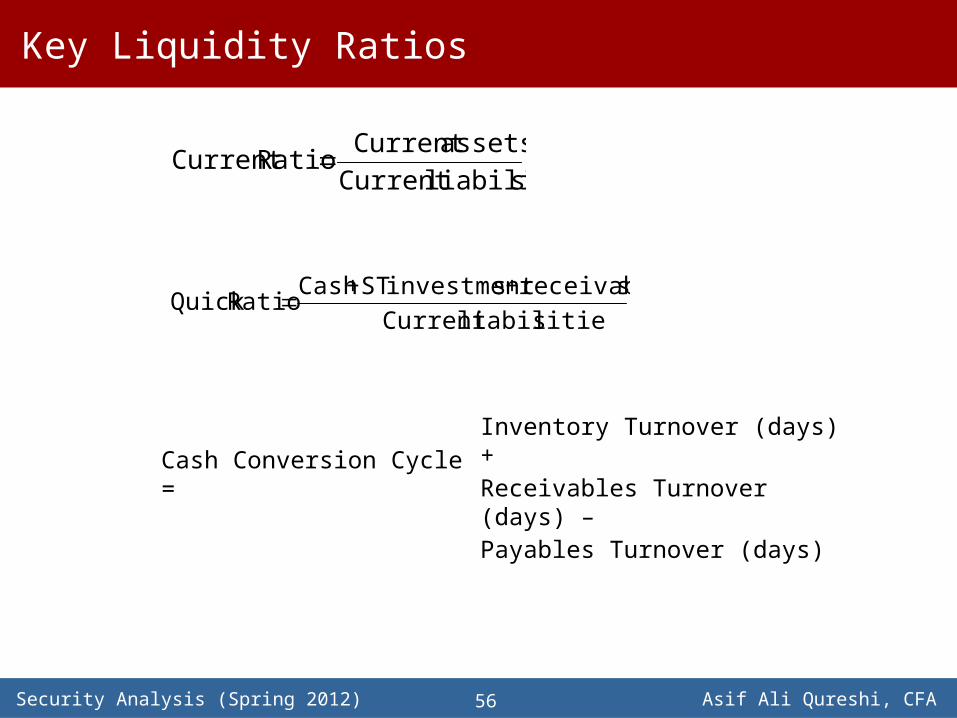

Key Liquidity Ratios

sliabilitie Currentassets Current

Ratio Current

sliabilitie Currentsreceivable + sinvestment ST + Cash

Ratio Quick

Cash Conversion Cycle = Inventory Turnover (days) + Receivables Turnover (days) – Payables Turnover (days)

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA57

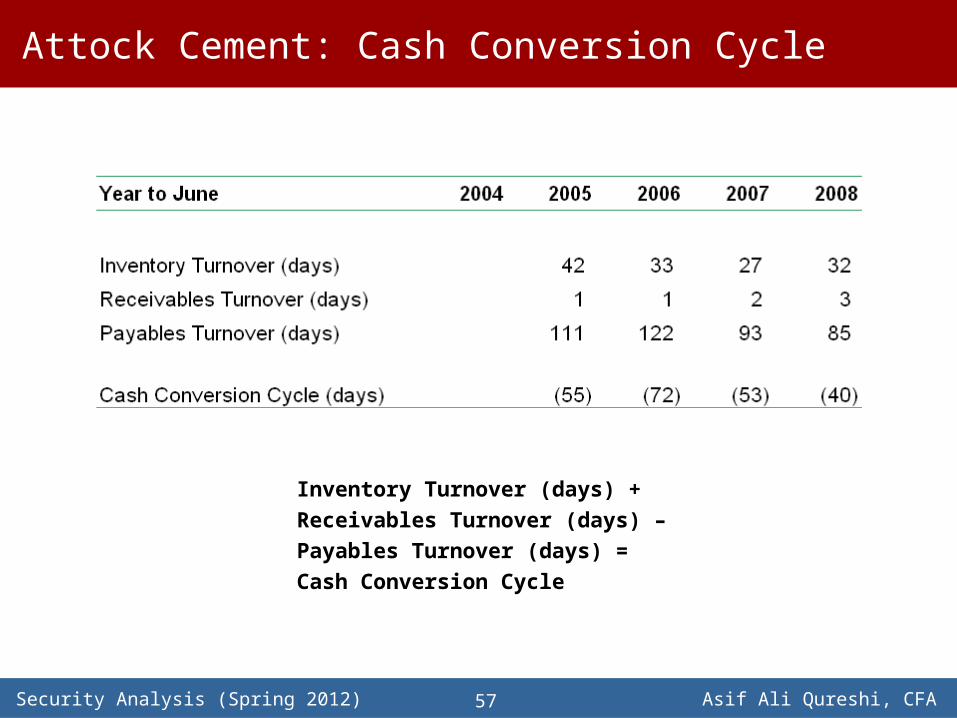

Attock Cement: Cash Conversion Cycle

Inventory Turnover (days) + Receivables Turnover (days) – Payables Turnover (days) = Cash Conversion Cycle

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA58

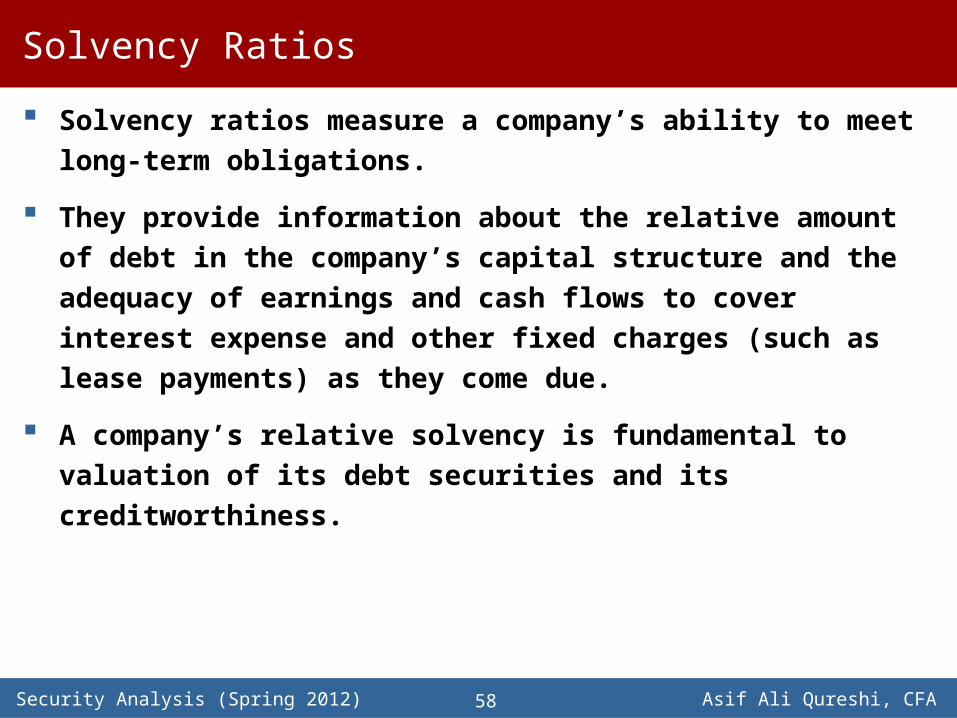

Solvency Ratios

Solvency ratios measure a company’s ability to meet long-term obligations.

They provide information about the relative amount of debt in the company’s capital structure and the adequacy of earnings and cash flows to cover interest expense and other fixed charges (such as lease payments) as they come due.

A company’s relative solvency is fundamental to valuation of its debt securities and its creditworthiness.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA59

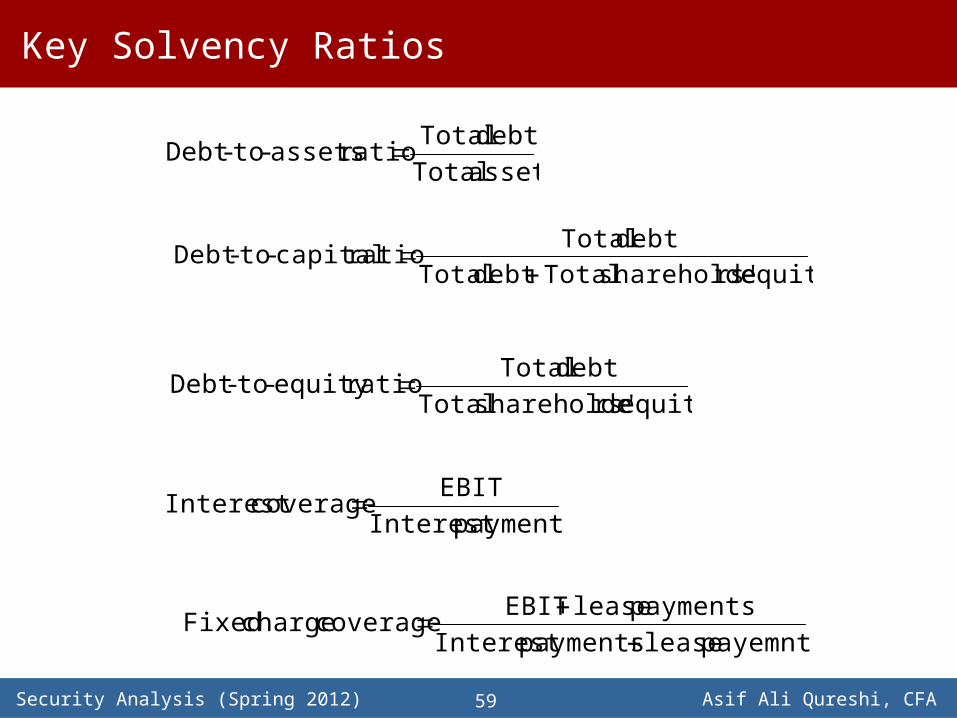

Key Solvency Ratios

assets Totaldebt Total

ratio assets-to-Debt

equity rs'shareholde Total debt Totaldebt Total

ratio capital-to-Debt

equity rs'shareholde Totaldebt Total

ratio equity-to-Debt

payments InterestEBIT

coverage Interest

payemnts lease payments Interestpayments lease EBIT

coverage charge Fixed

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA60

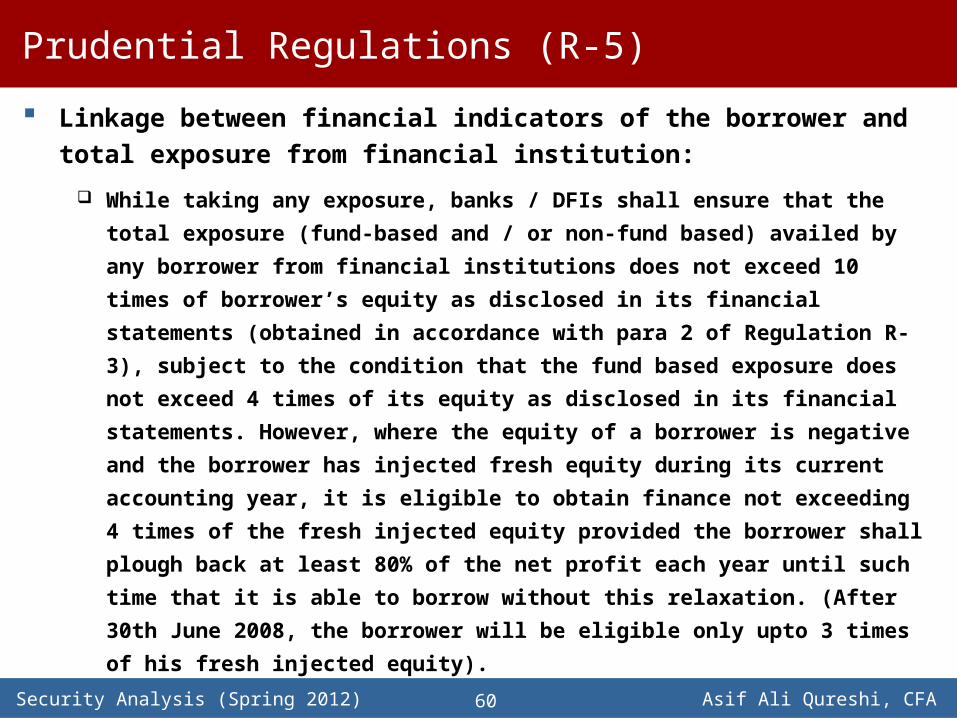

Prudential Regulations (R-5)

Linkage between financial indicators of the borrower and total exposure from financial institution:

While taking any exposure, banks / DFIs shall ensure that the total exposure (fund-based

and / or non-fund based) availed by any borrower from financial institutions does not exceed

10 times of borrower’s equity as disclosed in its financial statements (obtained in accordance

with para 2 of Regulation R-3), subject to the condition that the fund based exposure does

not exceed 4 times of its equity as disclosed in its financial statements. However, where the

equity of a borrower is negative and the borrower has injected fresh equity during its current

accounting year, it is eligible to obtain finance not exceeding 4 times of the fresh injected

equity provided the borrower shall plough back at least 80% of the net profit each year until

such time that it is able to borrow without this relaxation. (After 30th June 2008, the

borrower will be eligible only upto 3 times of his fresh injected equity).

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA61

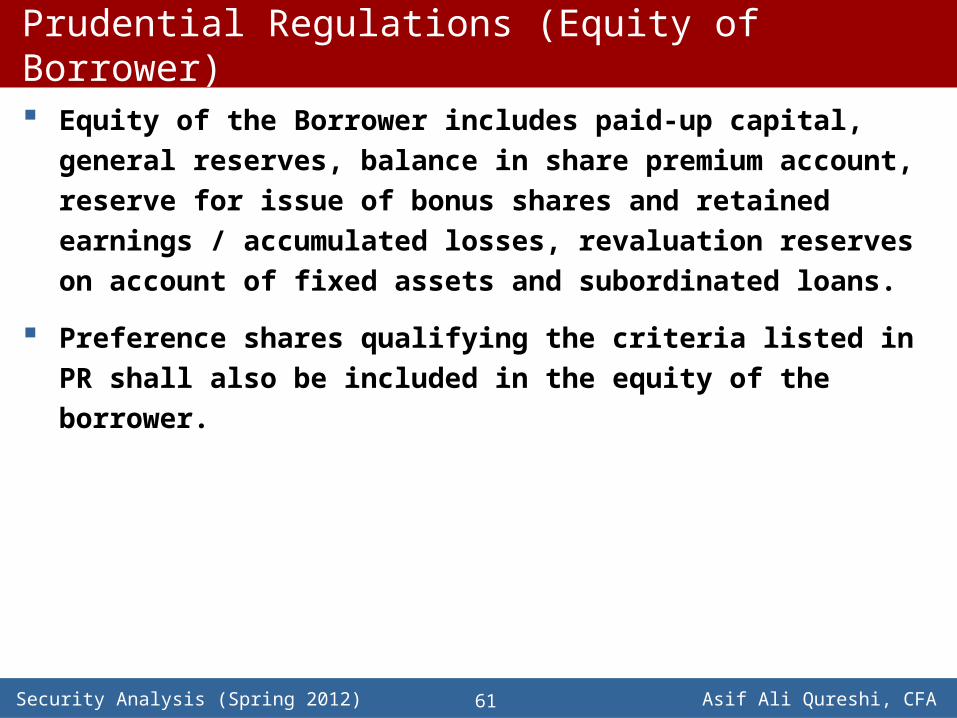

Prudential Regulations (Equity of Borrower)

Equity of the Borrower includes paid-up capital, general reserves, balance in share premium account, reserve for issue of bonus shares and retained earnings / accumulated losses, revaluation reserves on account of fixed assets and subordinated loans.

Preference shares qualifying the criteria listed in PR shall also be included in the equity of the borrower.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA62

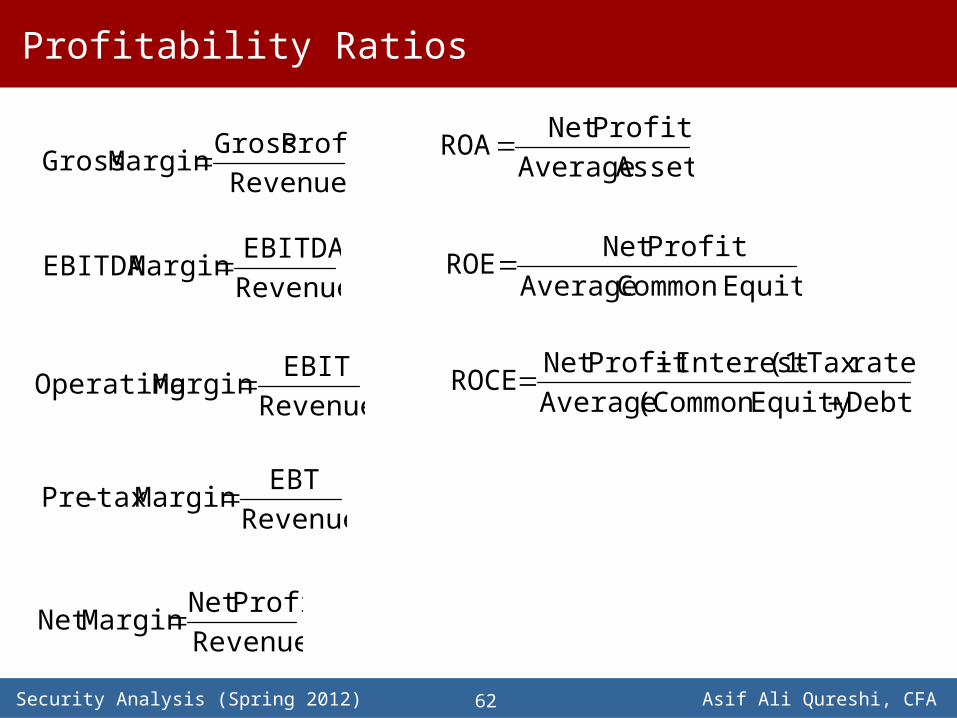

Profitability Ratios

RevenueProfit Gross

Margin Gross

RevenueEBIT

Margin Operating

RevenueEBT

Margin tax-Pre

RevenueProfit Net

Margin Net

RevenueEBITDA

Margin EBITDA

Assets AverageProfit Net

ROA

Equity Common AverageProfit Net

ROE

Debt) Equity (Common Averagerate) Tax - (1 Interest Profit Net

ROCE

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA63

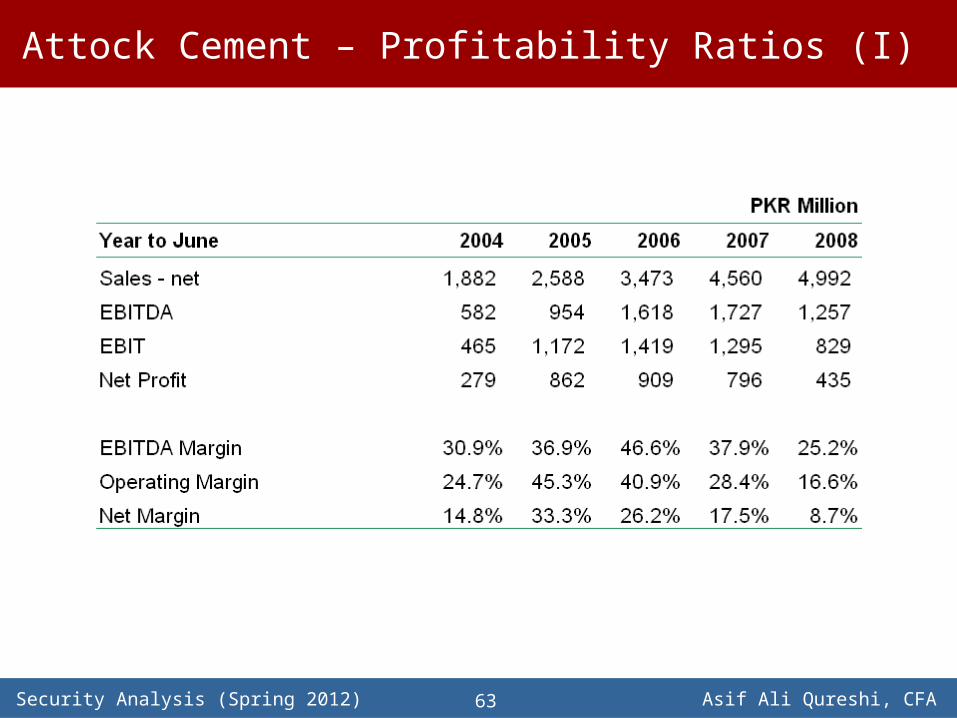

Attock Cement – Profitability Ratios (I)

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA64

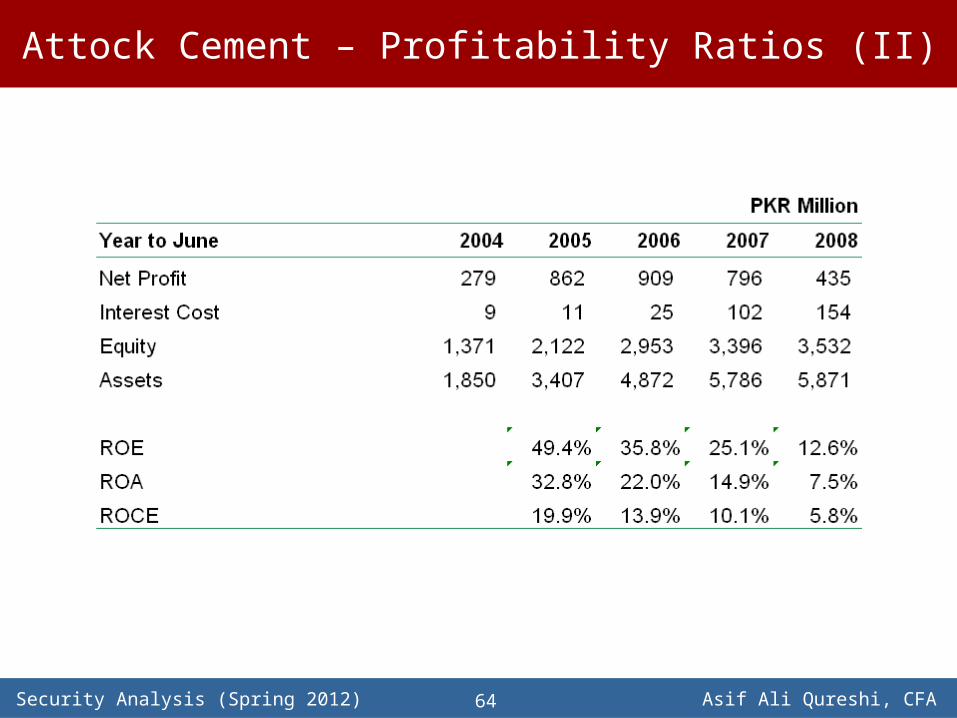

Attock Cement – Profitability Ratios (II)

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA65

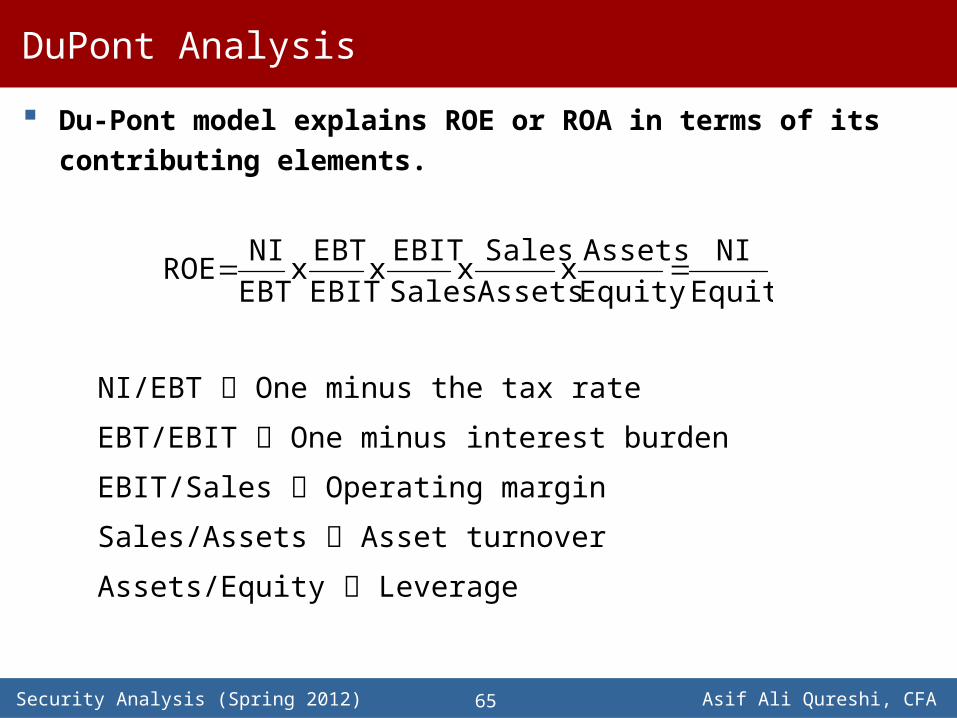

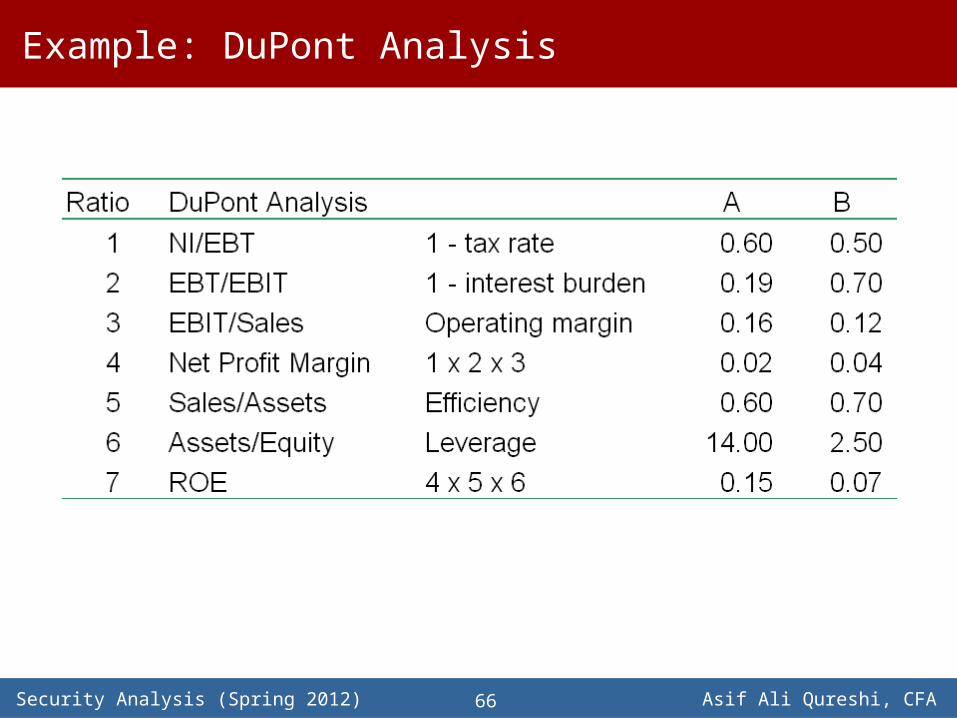

DuPont Analysis

Du-Pont model explains ROE or ROA in terms of its contributing elements.

EquityNI

Equity

Assets x

AssetsSales

x SalesEBIT

x EBITEBT

x EBTNI

ROE

NI/EBT One minus the tax rate

EBT/EBIT One minus interest burden

EBIT/Sales Operating margin

Sales/Assets Asset turnover

Assets/Equity Leverage

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA66

Example: DuPont Analysis

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA67

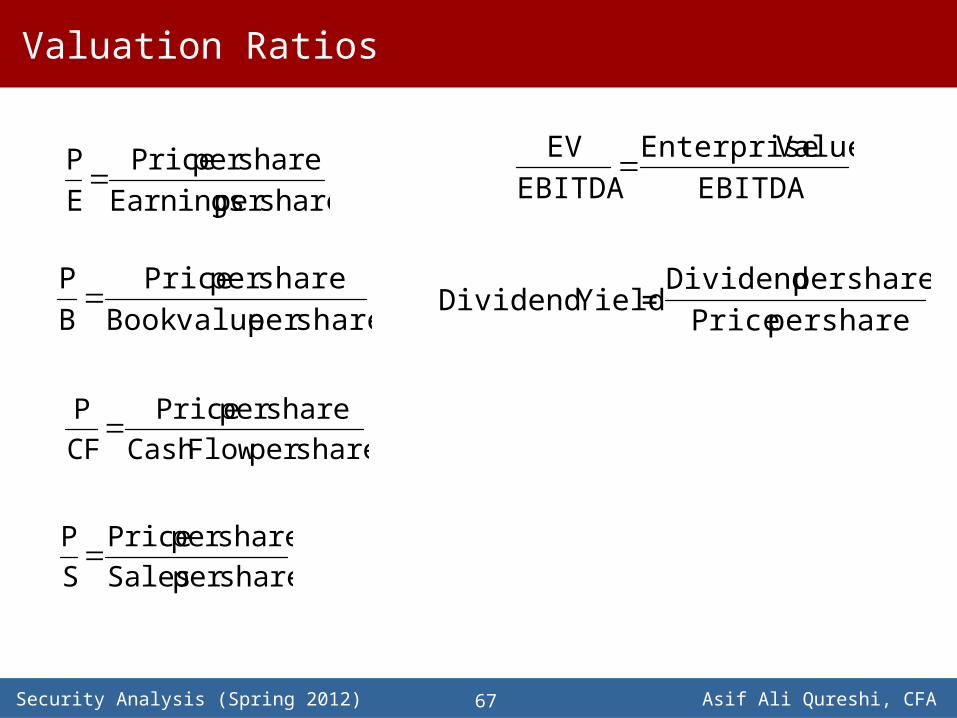

Valuation Ratios

share per Earningsshare per Price

EP

share per Flow Cashshare per Price

CFP

share per Salesshare per Price

SP

share per value Bookshare per Price

BP

EBITDAValue Enterprise

EBITDA

EV

share per Price

share per Dividend = YieldDividend

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA68

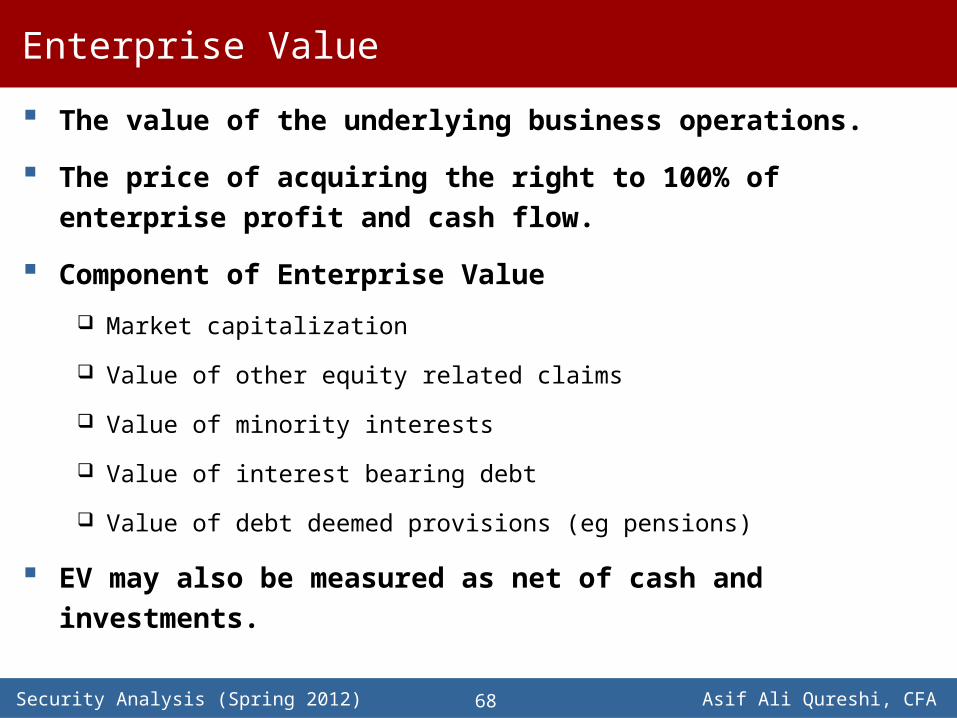

Enterprise Value

The value of the underlying business operations.

The price of acquiring the right to 100% of enterprise profit and cash flow.

Component of Enterprise Value

Market capitalization

Value of other equity related claims

Value of minority interests

Value of interest bearing debt

Value of debt deemed provisions (eg pensions)

EV may also be measured as net of cash and investments.

Security Analysis (Spring 2012) Asif Ali Qureshi, CFA69

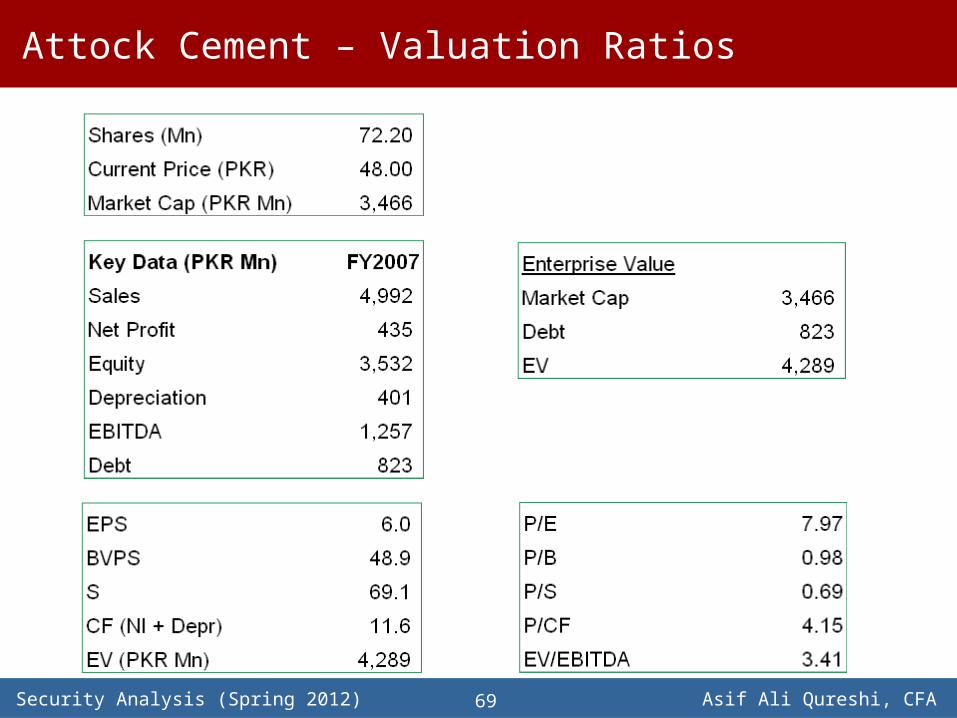

Attock Cement – Valuation Ratios