spread trading - singapore management university: … · 6 of 63 february 6, 2017 qf206 week 6...

TRANSCRIPT

1 of 63 February 6, 2017

QF206 Week 6

Spread Trading

Bread & Butter of Prop Traders

© Christopher Ting

2 of 63 February 6, 2017

QF206 Week 6

© Christopher Ting

Ex-SIMEX Locals

© Christopher Ting

Source: AFACT

Association of Financial and Commodity Traders

3 of 63 February 6, 2017

QF206 Week 6

Revenge of the Geeks

© Christopher Ting

During the open-outcry era, locals who were less “vocal” couldn’t match the big-time order-fillers.

But when the floor gave way to screen-based trading, locals who adapted to the new landscape of computer and automated trading survived and thrived.

4 of 63 February 6, 2017

QF206 Week 6

© Christopher Ting

Trading Arcade

© Christopher Ting

5 of 63 February 6, 2017

QF206 Week 6

Calendar Spread

© Christopher Ting

This is the simplest form of trading strategy and very easy to implement.

Roll

When the current near month futures contract is about to expire and to be replaced by the far month contract, i.e., the far month is going to become near month.

CTA (Commodity Trading Advisor) and other investors need to roll over their futures positions.

6 of 63 February 6, 2017

QF206 Week 6

Calendar Spread Conventions

Quoted as

Calendar Spread = Back Month Futures Price

– Front Month Futures Price

CTAs who have long positions in the front month and want to roll over will buy the calendar spread.

By buying the calendar spread, CTAs simultaneously close their front month futures and buy the back month futures

CTAs who have short positions in the front month and want to roll over will sell the calendar spread.

© Christopher Ting

7 of 63 February 6, 2017

QF206 Week 6

What’s the Fair Price of a Calendar Spread?

© Christopher Ting

The fair price of a calendar spread is simply the difference of the fair prices of front month and back month contracts:

Fair Calendar Spread = Back Month Fair Price – Front Month Fair Price

8 of 63 February 6, 2017

QF206 Week 6

Market Neutral

© Christopher Ting

Calendar spread is inherently a long-short strategy.

Suppose the fair calendar spread is -1

Suppose the back month is traded at 330 index points and front month at 331 index points.

The market price of the spread is -1 index point

The market calendar spread is traded at the same value as the fair calendar spread,

If market rallies, the back month moves up by x points, the front month should also move up by x points.

The spread is still the same

330 + x – (331 + x) = 330 – 331 + x – x = -1

9 of 63 February 6, 2017

QF206 Week 6

© Christopher Ting

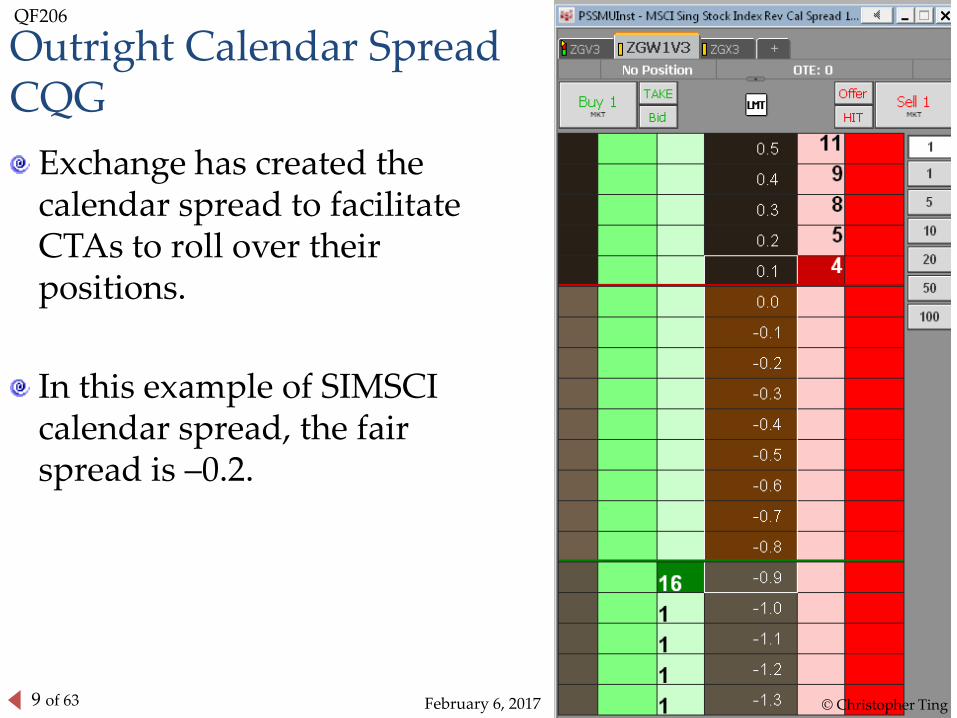

Outright Calendar SpreadCQG

© Christopher Ting

Exchange has created the calendar spread to facilitate CTAs to roll over their positions.

In this example of SIMSCI calendar spread, the fair spread is –0.2.

© Christopher Ting

10 of 63 February 6, 2017

QF206 Week 6

© Christopher Ting

CQG’s Auto-Spreader

Outright and synthetic calendar spreads

Set the auto-spread buying and selling according to the outright spread

© Christopher Ting

11 of 63 February 6, 2017

QF206 Week 6

© Christopher Ting

In this example of SIMSCI calendar spread, the fair spread is –0.8.

Why is the market outright spread different from the fair spread?

© Christopher Ting

Outright Calendar SpreadTT

12 of 63 February 6, 2017

QF206 Week 6

Calendar Spread

© Christopher Ting

Outright Spread Synthetic Spread Quoting Leg Hedging Leg

Jan 12, 2016

13 of 63 February 6, 2017

QF206 Week 6

Buying Calendar Spread with AutoSpreader

© Christopher Ting

Quoting leg as bait Hedging leg

Jan 12, 2016

14 of 63 February 6, 2017

QF206 Week 6

Selling Calendar Spread with AutoSpreader

© Christopher Ting

Quoting leg as bait Hedging leg

Jan 12, 2016

4

15 of 63 February 6, 2017

QF206 Week 6

Buying and Selling Synthetically

© Christopher Ting

Quoting leg as bait Hedging leg

Jan 12, 2016

16 of 63 February 6, 2017

QF206 Week 6

Calendar Spread is Market Neutral

© Christopher Ting

Jan 16 and Feb 16 prices have come down a lot, but the calendar spread does not change much. Jan 26, 2016

17 of 63 February 6, 2017

QF206 Week 6

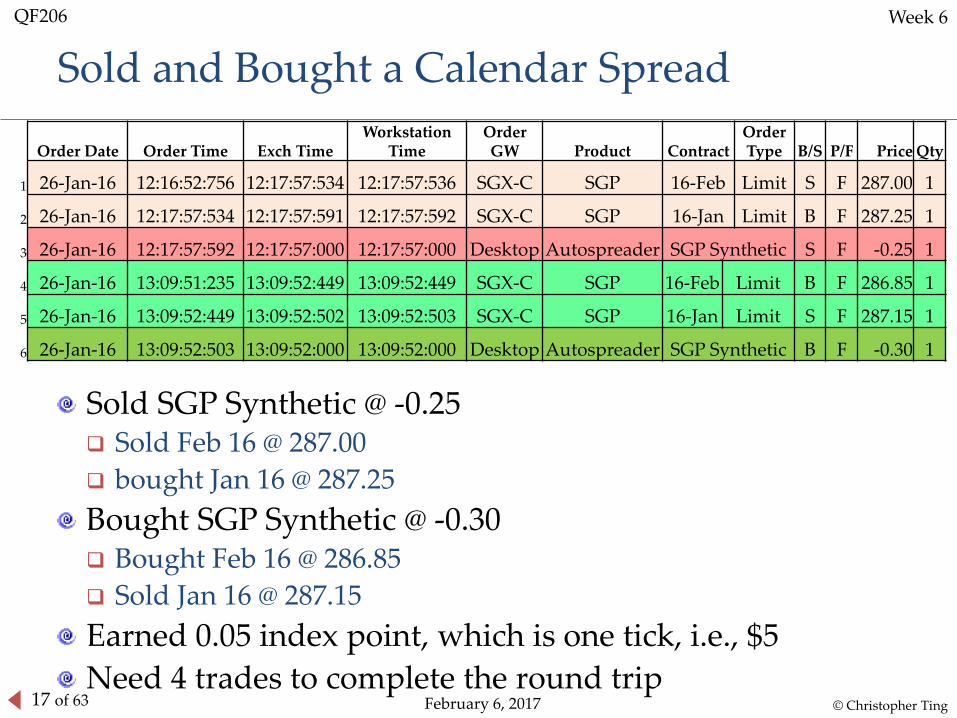

Sold and Bought a Calendar Spread

© Christopher Ting

Sold SGP Synthetic @ -0.25 Sold Feb 16 @ 287.00

bought Jan 16 @ 287.25

Bought SGP Synthetic @ -0.30 Bought Feb 16 @ 286.85

Sold Jan 16 @ 287.15

Earned 0.05 index point, which is one tick, i.e., $5

Need 4 trades to complete the round trip

Order Date Order Time Exch TimeWorkstation

TimeOrder GW Product Contract

Order Type B/S P/F Price Qty

1 26-Jan-16 12:16:52:756 12:17:57:534 12:17:57:536 SGX-C SGP 16-Feb Limit S F 287.00 1

2 26-Jan-16 12:17:57:534 12:17:57:591 12:17:57:592 SGX-C SGP 16-Jan Limit B F 287.25 1

3 26-Jan-16 12:17:57:592 12:17:57:000 12:17:57:000 Desktop Autospreader SGP Synthetic S F -0.25 1

4 26-Jan-16 13:09:51:235 13:09:52:449 13:09:52:449 SGX-C SGP 16-Feb Limit B F 286.85 1

5 26-Jan-16 13:09:52:449 13:09:52:502 13:09:52:503 SGX-C SGP 16-Jan Limit S F 287.15 1

6 26-Jan-16 13:09:52:503 13:09:52:000 13:09:52:000 Desktop Autospreader SGP Synthetic B F -0.30 1

18 of 63 February 6, 2017

QF206 Week 6

Outright versus Synthetic

© Christopher Ting

Whether using outright or synthetic, each position involves two trades.

You can use the outright to close the calendar position opened by synthetic.

Short a calendar spread synthetically Sold SGP Feb16 @ 292.90

Bought SGP Jan16 @ 292.95

Long a calendar spread outright at T+1 session Sold SGP Jan16 @ 291.00

Bought SGP Feb16 @ 290.85

19 of 63 February 6, 2017

QF206 Week 6

P&L of a Round-Trip Calendar Spread

© Christopher Ting

SGP Jan16 lost 39 ticks

291.00 – 292.95 = —1.95 index points

SGP Feb16 gained 41 ticks.

292.90 – 290.85 = 2.05 index points

The net gain is 0.10 index points, which is S$10.

Is the net position 1 contract oustanding?

20 of 63 February 6, 2017

QF206 Week 6

Quiz: What Happened?

© Christopher Ting

Quoting leg as bait Jan 26, 2016

21 of 63 February 6, 2017

QF206 Week 6

Quoting and Hedging on Both Legs to Buy!

© Christopher Ting

Jan 26, 2016

22 of 63 February 6, 2017

QF206 Week 6

Quoting and Hedging on Both Legs to Sell!

© Christopher Ting

Jan 26, 2016

23 of 63 February 6, 2017

QF206 Week 6

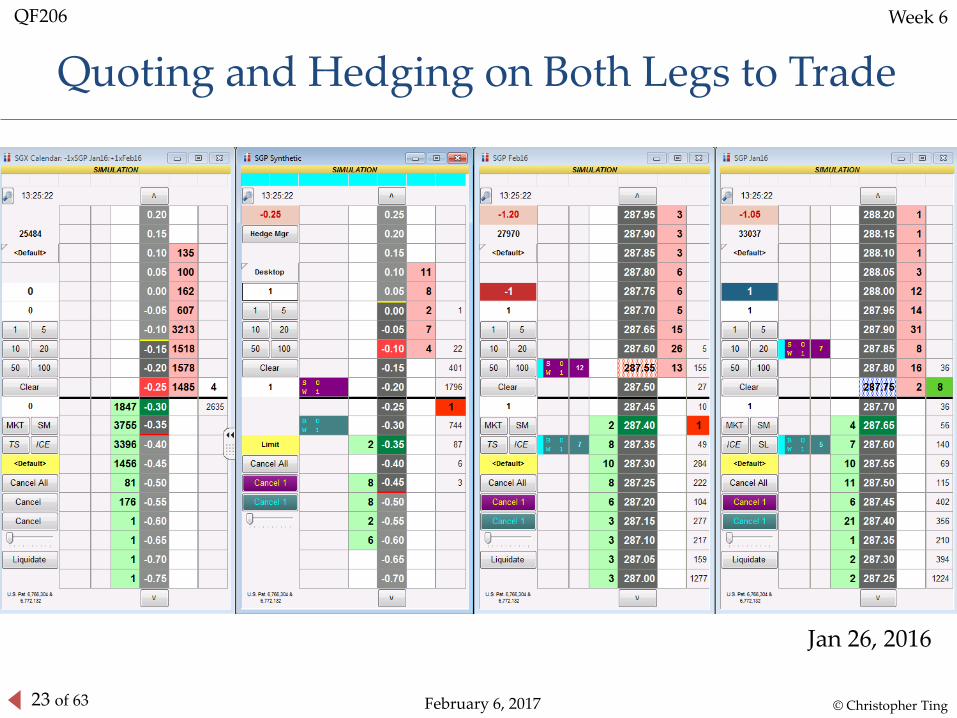

Quoting and Hedging on Both Legs to Trade

© Christopher Ting

Jan 26, 2016

24 of 63 February 6, 2017

QF206 Week 6

Quiz: What Happened?

© Christopher Ting

25 of 63 February 6, 2017

QF206 Week 6

Using the Outright Calendar Spread to Square Off Your Position

© Christopher Ting

26 of 63 February 6, 2017

QF206 Week 6

Mis-Hedges

© Christopher Ting

27 of 63 February 6, 2017

QF206 Week 6

Wait or Don’t Wait?

© Christopher Ting

28 of 63 February 6, 2017

QF206 Week 6

What are the risks of calendar spread?

© Christopher Ting

Mis-hedge!

When a synthetic spread order is legged, a mis-hedge occurs and the spreader becomes a direction speculator at the wrong starting line.

Basis risk: the spread price can change

Position size needs to be large, hence greater exposure.

29 of 63 February 6, 2017

QF206 Week 6

Summary of Spread Trading

© Christopher Ting

Quoting orders as “baits”

Limit orders placed on the less liquid leg

Hedge orders

When the quoting orders are hit, hedge orders are triggered and enter the more liquid futures market

If the quoting orders are sell (buy), hedge orders are buy (sell).

Hedge orders are limit orders.

How do you do spread trading, buy and sell contracts on different markets simultaneously?

Answer: HFT!

30 of 63 February 6, 2017

QF206 Week 6

Not one-to-one Spread Trading

For Advanced Prop Traders

© Christopher Ting

31 of 63 February 6, 2017

QF206 Week 6

Nikkei 225 Index Futures

© Christopher Ting

Big Nikkei at Osaka tick size: 10 points, multiplier ¥1,000

Mini Nikkei at Osaka tick size: 5 points, multiplier ¥100

Regular Nikkei at SGX tick size: 5 points, multiplier ¥500

Regular Nikkei NIY at CME tick size: 5 points, multiplier ¥500

Regular Nikkei NKD at CME tick size: 5 points, multiplier $5

Mutualoffset

32 of 63 February 6, 2017

QF206 Week 6

Calendar Spread for Nikkei Futures

© Christopher Ting

All share the same underlying Nikkei 225 index

5 contracts of mini versus 1 contract of regular

1 Big Nikkei versus 2 SGX’s regular NK

1 CME regular NIY versus 1 SGX’s regular NK

What about 1 CME regular NKD versus 1 SGX’s regular NK or CME’s NIY?

33 of 63 February 6, 2017

QF206 Week 6

Synthetic Cross-Market Spreads

© Christopher Ting

Nikkei futures versus Topix futures

Taiex futures versus MSCI Taiwan futures

Dax futures versus STOXX 50 futures

What is the ratio of one futures versus the other?

Concept

Notional value = index points × price multiplier

Example

SGX’s Nikkei 225 futures

14,600 × ¥500 = ¥7,300,000

Eurex’s DAX futures

9,300 × €25 = €232,500

34 of 63 February 6, 2017

QF206 Week 6

Cross-Market Spread Ratio

© Christopher Ting

Dax futures versus STOXX 50 futures as an example.

The multiplier of STOXX 50 futures is €10.

The underlying indexes are different but highly correlated!

Synthetic spread trading strategy can be constructed.

The key lies in: What’s the ratio R of Dax to STOXX 50?

Run the regression:

Dt = a + b St + et

Here, Dt is the notional amount of Dax futures and St is the notional amount of STOXX 50 futures.

The coefficient estimate b is the required ratio R.

35 of 63 February 6, 2017

QF206 Week 6

Specific Numbers

© Christopher Ting

Using the nearest to maturity active contracts of these two futures from June 23, 1998 to February 7, 2014, based on daily last prices, the linear regression result is

Dt = 24.7 + 3.7 St

So the ratio is 1 Dax futures contract to 3.7 STOXX 50 futures contracts.

In practice, we use 2 Dax futures contract to 7 STOXX 50 contracts as the ratio.

36 of 63 February 6, 2017

QF206 Week 6

Price Differential

© Christopher Ting

In calendar spread, we use only the price differential:

LegA.Price - LegB.Price

This differential is called the implied price, which was the calendar spread.

More generally,

LegA.Price * User-Defined Multiplier A

– Leg B Price * User-Defined Multiplier B

The user-defined multiplier takes into account the contract unit (price multiplier).

37 of 63 February 6, 2017

QF206 Week 6

Example

© Christopher Ting

In the earlier example of Dax versus STOXX 50,

Dt = 3.7 St + a constant

So the price differential dt is

dt =Dt —3.7 × St

Leg A’s price is the Dax futures price Dt

Leg A’s multiplier is 1

Leg B’s price is the STOXX 50 price St

Leg B’s multiplier is 3.7

If the change in price differential is much bigger than 24.7, sell the spread, which is 2 Dax futures contracts to 7 STOXX 50 contracts.

38 of 63 February 6, 2017

QF206 Week 6

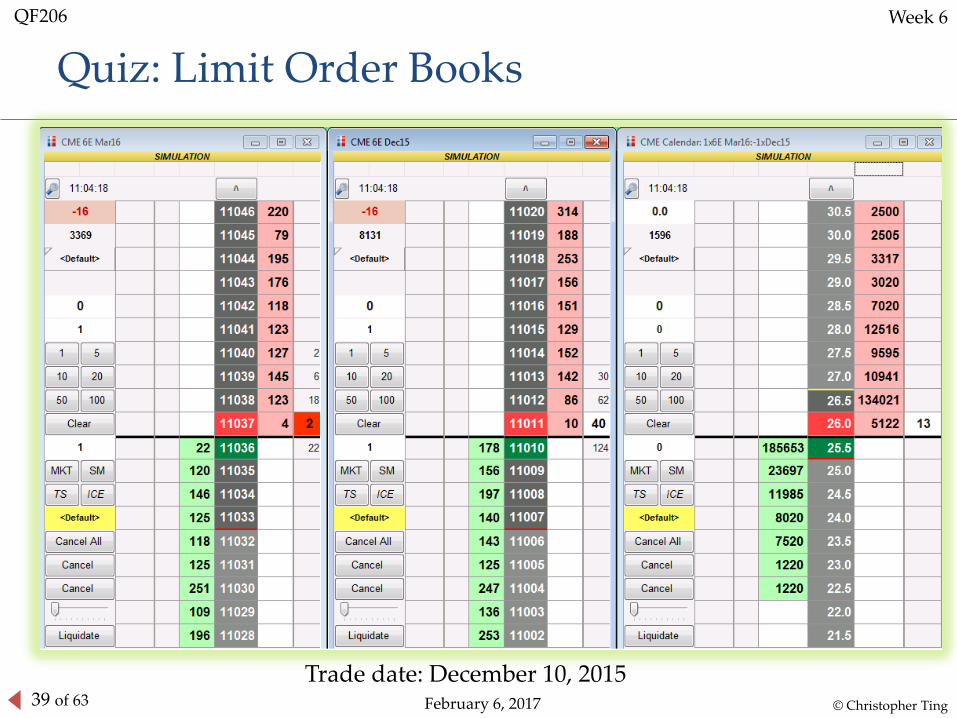

Summary by Quiz Questions

© Christopher Ting

The limit-order books of EUR/USD futures 6E in the next slide are a snapshot on December 10, 2015.

Considering the liquidity, which leg or futures product should you put out as bait?

Suppose you have constructed a synthetic calendar spread.

what should be the buying price of the calendar spread?

What should be the selling price of the calendar spread?

39 of 63 February 6, 2017

QF206 Week 6

Quiz: Limit Order Books

© Christopher Ting

Trade date: December 10, 2015

40 of 63 February 6, 2017

QF206 Week 6

A Tale of Two Futures:$ versus ¥ Nikkei 225 Index Futures

Quanto Spread

© Christopher Ting

41 of 63 February 6, 2017

QF206 Week 6

Learning Objectives

Define quanto

Understand inter-market spread trading strategy

Analyze the P&L of a short quanto position

© Christopher Ting

42 of 63 February 6, 2017

QF206 Week 6

Quanto

Quantos are derivatives where the payoff is defined using variables measured in one currency but paid in another currency.

Example:

Futures contract providing a payoff of NT – F dollars(USD) rather than yens (JPY) to the buyer of NKD.

Here, NT is the Nikkei 225 index value at maturity T and F is the futures price that the buyer has entered.

© Christopher Ting

43 of 63 February 6, 2017

QF206 Week 6

Nikkei 225 Futures in USD and JPY

Contract Multiplier USD 5 for NKD; JPY 500 for NIY

Minimum Price Change (Tick) 5 index points

Final Settlement: Cash-settled to Special Opening Quotation of the Nikkei 225 Index on 2nd Friday of the contract expiry month

Last Trading Day 3:15 p.m. Central Time on the day preceding final settlement – usually the Thursday prior to 2nd Friday of the contract expiry month

Contract Months: Quarterlies for NKD; Quarterlies and Serials for NIY

© Christopher Ting

44 of 63 February 6, 2017

QF206 Week 6

Trading Hours

At 3:30 p.m. Singapore Time, T+1 session for Nikkei index futures opens

Simex: (multiplier ¥500, tick size 5 index points)

Osaka:

Big (multiplier ¥1,000, tick size 10 index points)

Mini (multiplier ¥100, tick size 5 index points)

Before 2011

At 4 p.m. Singapore Time, NKD futures market opens

At 7 p.m. Singapore Time, NIY futures market opens

Now

NKD and NIY trade almost around the clock

© Christopher Ting

45 of 63 February 6, 2017

QF206 Week 6

CME’s NKD, NIY, and SGX’s NK

© Christopher Ting

NKD Mar16

Bid Size Price Ask Size

18970 13

18965 7

18960 15

18955 7

18950 16

18945 12

18940 22

18935 10

18930 10

18925 2

35 -35 70

1 18920

7 18915

11 18910

7 18905

9 18900

9 18895

15 18890

7 18885

15 18880

6 18875

NIY Mar16

Bid Size Price Ask Size

18935 9

18930 17

18925 10

18920 19

18915 10

18910 11

18905 14

18900 10

18895 9

18890 8

80 26 54

5 18880

11 18875

14 18870

26 18865

24 18860

19 18855

19 18850

28 18845

17 18840

11 18835

NK Mar16

Bid Size Price Ask Size

18935.00 15

18930.00 14

18925.00 8

18920.00 12

18915.00 12

18910.00 35

18905.00 16

18900.00 16

18895.00 28

18890.00 11

102 -5 107

10 18880.00

32 18875.00

12 18870.00

29 18865.00

19 18860.00

16 18855.00

13 18850.00

23 18845.00

10 18840.00

7 18835.00

46 of 63 February 6, 2017

QF206 Week 6

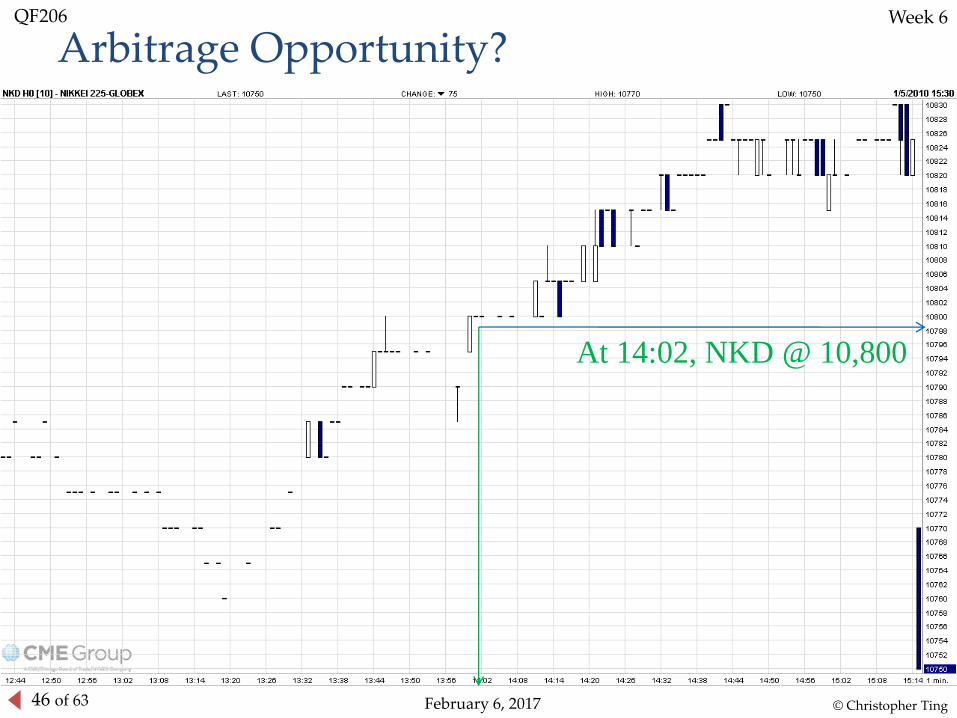

Arbitrage Opportunity?

At 14:02, NKD @ 10,800

© Christopher Ting

47 of 63 February 6, 2017

QF206 Week 6

Arbitrage Opportunity?

At 14:02, NIY @ 10,735

© Christopher Ting

48 of 63 February 6, 2017

QF206 Week 6

Motivating Questions

© Christopher Ting

Why was the market price of NKD 65 points higher than that of NIY on Jan 5?

Risk-free arbitrage opportunity? Short NKD and long NIY?

The exchange rate on Jan 5, 2010 at 14:00 Central Time Cash Market: ¥91.71 per $1

Futures Market: front quarter JPY/USD futures (6J) price was 109,040, which was equivalent to ¥91.71 per dollar.

49 of 63 February 6, 2017

QF206 Week 6

Follow-up Question

What should the futures price of NKD be relative to the futures price of NIY?

What should be the spread between these two futures prices?

© Christopher Ting

50 of 63 February 6, 2017

QF206 Week 6

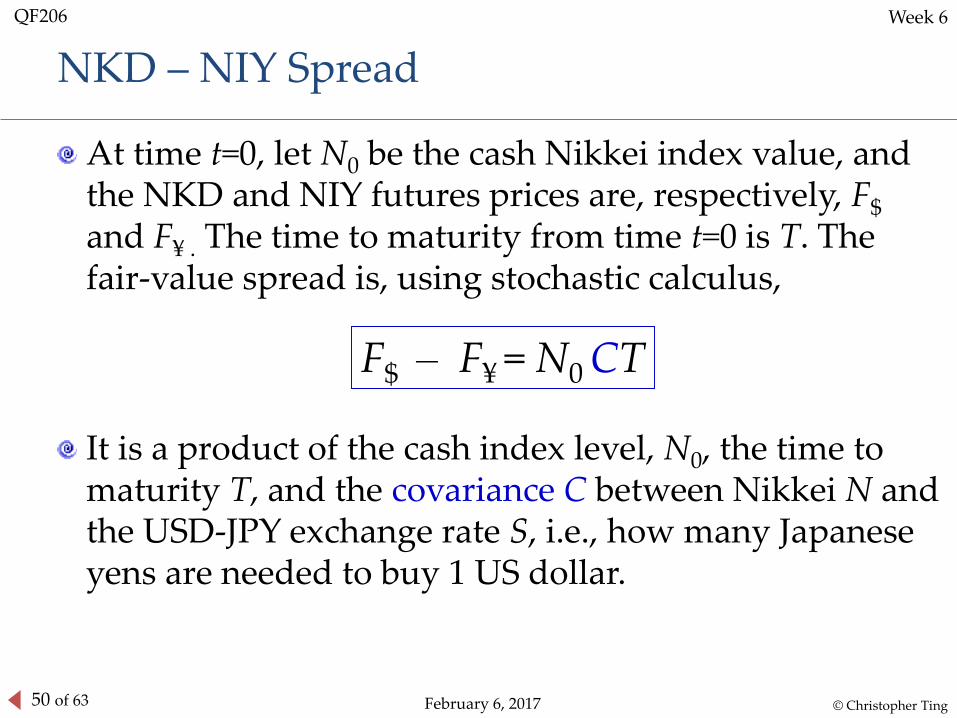

NKD – NIY Spread

At time t=0, let N0 be the cash Nikkei index value, and the NKD and NIY futures prices are, respectively, F$

and F¥ . The time to maturity from time t=0 is T. The fair-value spread is, using stochastic calculus,

It is a product of the cash index level, N0, the time to maturity T, and the covariance C between Nikkei N and the USD-JPY exchange rate S, i.e., how many Japanese yens are needed to buy 1 US dollar.

F$ – F¥ = N0 CT

© Christopher Ting

51 of 63 February 6, 2017

QF206 Week 6

Behavior of the NKD – NIY Spread

© Christopher Ting

When cash market N goes up, dollar tends to strengthen (i.e., S increases), and vice versa.

In other words, when dollar strengthens (i.e., Sincreases), cash market N tends to go up. Why?

Dollar strengthening means Yen depreciating, which will be helpful to export-oriented companies in Nikkei 225 index N, so N tends to go up.

Thus the covariance between the (percentage) change in N and the (percentage) change in S is positive.

52 of 63 February 6, 2017

QF206 Week 6

Illustration

© Christopher Ting

Suppose the covariance is 0.0225, the index level is at 10,680 and the time to maturity is 3 months.

The spread is about 60 index points:

10,680 0.0225 3/12 = 60.1

53 of 63 February 6, 2017

QF206 Week 6

Money-Making Opportunity?

© Christopher Ting

At maturity, T = 0, the NKD – NIY spread is zero. This is the linear time decay effect.

Since the NKD – NIY spread is positive, one can take a short position in this spread (i.e. sell NKD and buy NIY), and hold this spread position until maturity to benefit from the time decay.

Is it a good money-making opportunity?

54 of 63 February 6, 2017

QF206 Week 6

Quanto Spread’s Time Decay (2010 Dec)

© Christopher Ting

55 of 63 February 6, 2017

QF206 Week 6

Profit and Loss

At time t=0, sell short one NKD contract at a price of F$, and buy R number of NIY contracts at a price of F¥.

At maturity T, ST is the spot yen per dollar exchange rate

Let NT be the settlement price of the futures contract, which is based on the special opening quotation (SOQ) of cash Nikkei 225 index value. The position’s payoff at maturity T is, in dollars

5 (F$ – NT) + R 500 (NT – F¥) / ST

© Christopher Ting

56 of 63 February 6, 2017

QF206 Week 6

Profit and Loss (cont’d)

Suppose the (hedge) ratio R is chosen to be

Then the P&L is

which is

100= 0S

R

5 (F$ –NT) + 5 S0 (NT – F¥) / ST

)(515 $0 FFFN

S

ST

T

¥¥

CTNFNS

ST

T

00 515L&P

¥

© Christopher Ting

57 of 63 February 6, 2017

QF206 Week 6

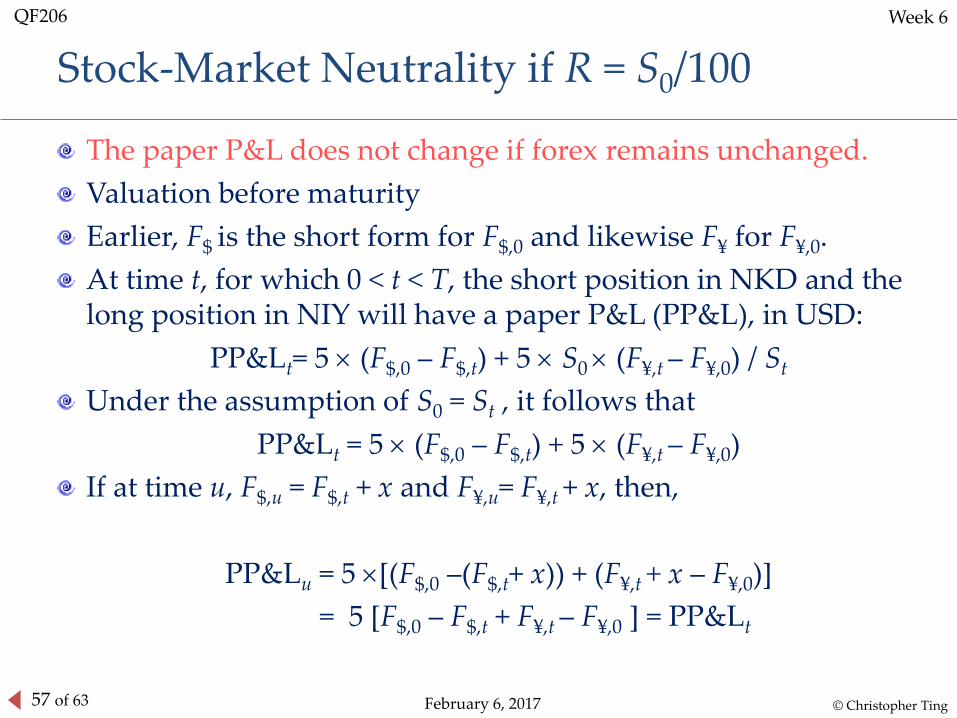

Stock-Market Neutrality if R = S0/100

© Christopher Ting

The paper P&L does not change if forex remains unchanged.

Valuation before maturity

Earlier, F$ is the short form for F$,0 and likewise F¥ for F¥,0.

At time t, for which 0 < t < T, the short position in NKD and the long position in NIY will have a paper P&L (PP&L), in USD:

PP&Lt= 5 (F$,0 – F$,t) + 5 S0 (F¥,t – F¥,0) / St

Under the assumption of S0 = St , it follows that

PP&Lt = 5 (F$,0 – F$,t) + 5 (F¥,t – F¥,0)

If at time u, F$,u = F$,t + x and F¥,u= F¥,t + x, then,

PP&Lu = 5 [(F$,0 –(F$,t+ x)) + (F¥,t + x – F¥,0)]

= 5 [F$,0 – F$,t + F¥,t – F¥,0 ] = PP&Lt

58 of 63 February 6, 2017

QF206 Week 6

What is Covariance?

© Christopher Ting

A measure of how two assets move together.

Recall that when cash market N goes up (down), dollar tends to strengthen (weaken) and S increases (decreases). So we expect C to be positive.

How should C be estimated?

At 3 PM Tokyo time, observe both the cash market index N and the USD-JPY exchange rate S. Do it for many days.

Calculate two time series of daily returns, called r1t and r2t.

Calculate the average values of r1t and r2t, called a1 and a2.

From M pairs of returns, r1t and r2t , the covariance is computed as

221

111

1arar

MC t

M

tt

59 of 63 February 6, 2017

QF206 Week 6

P&L Example: Normal Market

© Christopher Ting

Same parameters as in the illustration, the spread is 60 points. Thus, gain from time decay is $5 60 = $300.

Suppose S0 = 90 yens per dollar.

So the ratio R is short 10 NKD contracts and long 9 NIY contracts.

Suppose ST is 87 yens per dollar, i.e., dollar weakens, and the settlement is 800 points lower, i.e., NT – F¥ = –800 at maturity.

Then 5 (90 – 87)/87 = 15/87, and the P&L per NKD contract is

–$800 15/87 + $300 = $162.07.

60 of 63 February 6, 2017

QF206 Week 6

P&L Example: Market Crashes

© Christopher Ting

Suppose the market crashes, and ST becomes 85 yens per dollar, i.e., dollar weakens substantially, and the settlement is 2,000 points lower, i.e., NT – F¥ = –2,000.

Then 5 (90 – 85)/85 = 25/85, and the P&L at maturity is, for every NKD contract,

–$2,000 25/85 + $300 = –$288.24.

61 of 63 February 6, 2017

QF206 Week 6

P&L Example: Market Rally

© Christopher Ting

Suppose the market rallies, and ST becomes 95 yens per dollar, i.e., dollar strengthens, and the settlement is 2,000 points higher, i.e., NT – F¥ = 2,000.

Then 5 (90 – 95)/95 = –25/95, and the P&L at maturity per NKD contract is

$2,000 (–25/95) + $300 = –$226.32

62 of 63 February 6, 2017

QF206 Week 6

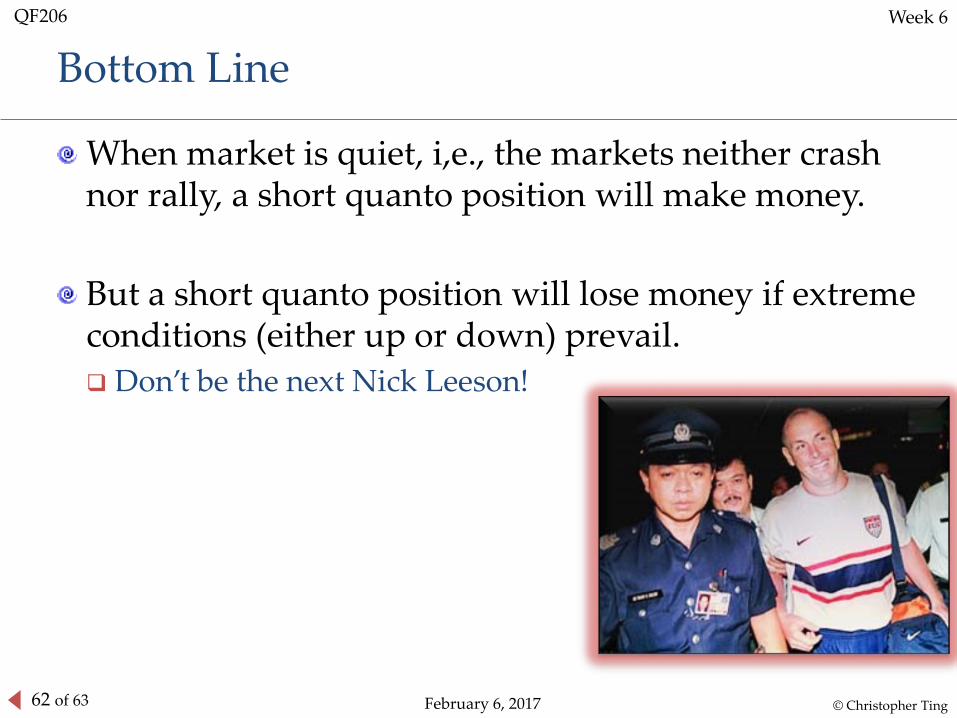

Bottom Line

© Christopher Ting

When market is quiet, i,e., the markets neither crash nor rally, a short quanto position will make money.

But a short quanto position will lose money if extreme conditions (either up or down) prevail.

Don’t be the next Nick Leeson!

63 of 63 February 6, 2017

QF206 Week 6

Remarks and Summary

© Christopher Ting

Quanto spread is a volatility trading strategy.

If big moves are expected, then long the quanto spread.

Otherwise, sell the quanto spread

You can also do the intra-day quanto spread. But make sure you have closed your position before the end of the trading session.

In Singapore, it is better to use NK as the fungible substitute of NIY because the latency is lower.