specialty strength: chemicals & pharmaceuticalsbreport.myiris.com/sfspl/vivlabs_20101112.pdf ·...

TRANSCRIPT

High Entry Barriers to become a preferred supplier Customer qualification norms are complicated, stringent, and costly making the registration a time consuming process. It takes around 3-5 years for a company to make inroads to become a preferred supplier for major global companies. Business is normally not done on “price” but on relationships, product portfolio, service levels and quality standards. However, quality of the product takes the topmost level in the pyramid for clients since they invest a lot of time and money to get in a new supplier as any compromise on the quality front could tarnish the brand value of the product and the company as well.

Strong clientele base Vivimed is an approved supplier to global personal care giants like L’Oreal, Unilever, P&G, and Johnson & Johnson etc., wherein the contracts are generally long-term in nature. In the specialty pharmaceuticals division, it supplies to major pharmaceutical companies like Merck, Lupin, Novartis, Cipla, and AstraZeneca etc.

Continuous capacity expansion in existing plants and setting up of an SEZ Capacity expansion is a continuous and an ongoing process for Vivimed. Vivimed has been undertaking Brownfield expansion by building new blocks at its Bonthapally plant catering to specialty chemical segments of Skincare, Hair & Oral care and also at its Jeedimetla (Pharma) plant. Vivimed is also setting up a pharmaceutical manufacturing plant in Choutuppal, Hyderabad (AP) and has received an in-principle approval for setting up an SEZ, on 250 acres of land for its specialty chemicals business.

Alliance with ISP Vivimed has entered into a manufacturing alliance with US-based International Specialty Products (ISP) in Jun’10 for sunscreens, with full support from ISP's global sales, marketing and technical service teams. We believe this alliance would generate revenue of around Rs. 421 mn in FY12E.

Focus more on Branded formulations Vivimed has forayed into formulation exports to Russia / CIS countries, where we believe the Company will witness a CAGR growth of 16.5% in sales for the period of FY09-FY12E.

OUTLOOK & VALUATION Vivimed backed by its strong product profile has delivered excellent numbers in the past. Its revenue has grown at a CAGR of 37% from FY07-10, while the EBITDA and PAT have grown at a CAGR of 32% and 34%, respectively. Vivimed has embarked on a Rs. 1.58 bn expansion plan to be executed over the next three years, which we believe will be a significant growth driver. Keeping in mind the Company’s strong track record, established customer base, increasing product profile and increasing demand for its products backed by volume expansion, we expect its revenue and PAT to grow at a CAGR of 27.7% and 35.8% over FY09-12E. It is currently trading at a P/E of 6.8x its FY12E diluted EPS of Rs. 50 and we recommend a “BUY” with a target price of Rs. 450 (9x FY12E EPS).

Vivimed Labs Limited

Please refer to important disclosures at the end of the report For private Circulation Only.

November 12, 2010 BUY HIGH RISK PRICE Rs.338 TARGET Rs. 450

Specialty Chemicals &

Pharmaceuticals

SHARE HOLDING (%)

Promoters 52.2

FII 6.4

FI / MF 0.2

Body Corporates 5.8

Public & Others 32.6

STOCK DATA

Reuters Code Bloomberg Code

VVMD.BO VILA IN

BSE Code NSE Symbol

532660 VIVIMEDLAB

Market Capitalization*

Rs. 3876.8 mn US$ 86.2 mn

Shares Outstanding*

114.7 mn

52 Weeks (H/L) Rs. 351/114

Avg. Daily Volume (6m)

85,474 Shares

Price Performance (%)

1M 3M 6M

7 54 114

200 Days EMA: Rs.218

*On fully diluted equity shares

Please refer to important disclosures at the end of the report For private Circulation Only.

Sushil Financial Services Private Limited Member : BSEL, SEBI Regn.No. INB/F010982338 | NSEIL, SEBI Regn.No.INB/F230607435. Office : 12, Homji Street, Fort, Mumbai 400 001. Phone: +91 22 40936000 Fax: +91 22 22665758 Email : [email protected]

KEY FINANCIALS

Y/E Mar.

Revenue (Rs mn)

RPAT (Rs mn)

AEPS (Rs)

AEPS (% Ch.)

P/E (x)

ROCE (%)

ROE (%)

P/BV (x)

FY09 2761.2 193.5 20.6 21.3 16.4 11.4 20.7 3.1

FY10 3434.9 310.1 31.1 51.2 10.9 12.9 25.1 2.3

FY11E 4116.1 391.4 39.3 26.2 8.6 14.2 23.7 1.8

FY12E 5598.0 572.1 50.0 27.1 6.8 15.7 26.0 1.5

ANALYST Suneel Rao | +91 22 4093 5068 [email protected]

SALES: Devang Shah | +91 22 4093 6060/61

Nishit Shah | +91 22 4093 5074 [email protected]

Initiating Coverage

STRENGTH: High Entry Barriers, Early mover advantage, Growing end user industry, Strong

Clientele, Consistent Past Performance WEAKNESS: Difficult to make inroads to acquire

new customers. OPPORTUNITIES: Foray into branded formulations space in the

Russia/CIS region; Capacity Expansion in Specialty chemicals & Pharmaceuticals. THREAT: Exchange rate volatility, Dilution risk.

November 12, 2010

2

Vivimed Labs Ltd.

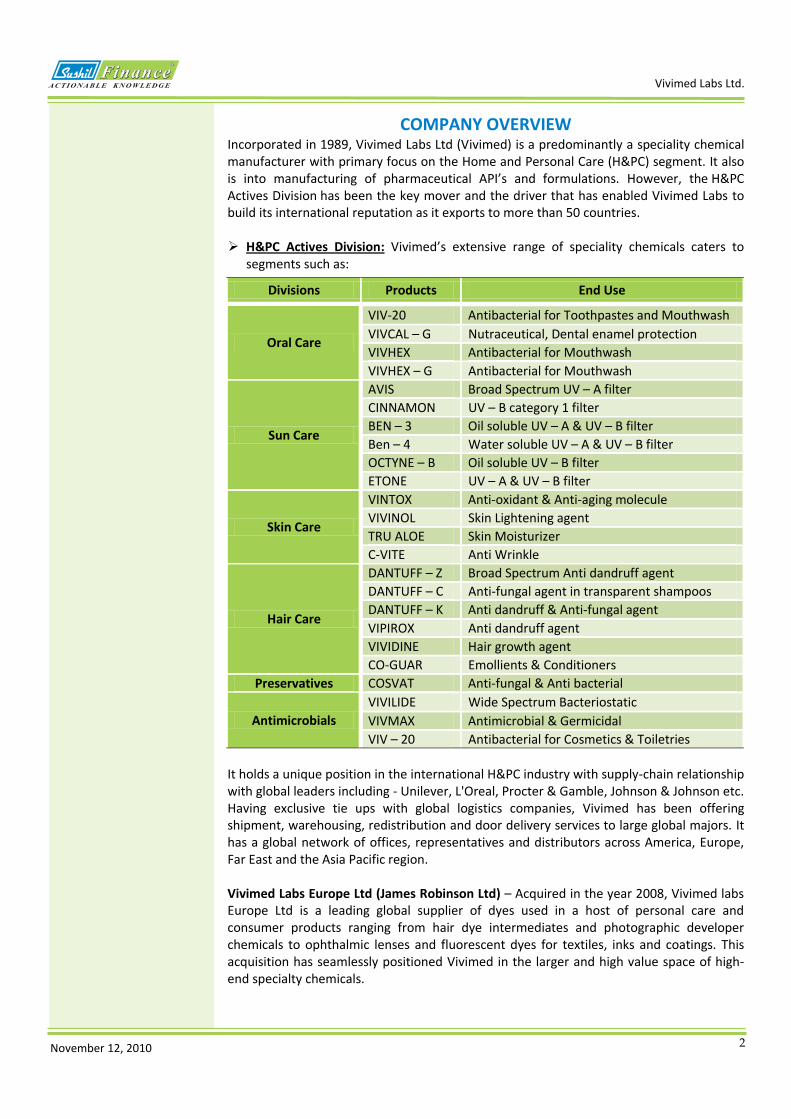

COMPANY OVERVIEW Incorporated in 1989, Vivimed Labs Ltd (Vivimed) is a predominantly a speciality chemical manufacturer with primary focus on the Home and Personal Care (H&PC) segment. It also is into manufacturing of pharmaceutical API’s and formulations. However, the H&PC Actives Division has been the key mover and the driver that has enabled Vivimed Labs to build its international reputation as it exports to more than 50 countries. H&PC Actives Division: Vivimed’s extensive range of speciality chemicals caters to

segments such as:

Divisions Products End Use

Oral Care

VIV-20 Antibacterial for Toothpastes and Mouthwash

VIVCAL – G Nutraceutical, Dental enamel protection

VIVHEX Antibacterial for Mouthwash

VIVHEX – G Antibacterial for Mouthwash

Sun Care

AVIS Broad Spectrum UV – A filter

CINNAMON UV – B category 1 filter

BEN – 3 Oil soluble UV – A & UV – B filter

Ben – 4 Water soluble UV – A & UV – B filter

OCTYNE – B Oil soluble UV – B filter

ETONE UV – A & UV – B filter

Skin Care

VINTOX Anti-oxidant & Anti-aging molecule

VIVINOL Skin Lightening agent

TRU ALOE Skin Moisturizer

C-VITE Anti Wrinkle

Hair Care

DANTUFF – Z Broad Spectrum Anti dandruff agent

DANTUFF – C Anti-fungal agent in transparent shampoos

DANTUFF – K Anti dandruff & Anti-fungal agent

VIPIROX Anti dandruff agent

VIVIDINE Hair growth agent

CO-GUAR Emollients & Conditioners

Preservatives COSVAT Anti-fungal & Anti bacterial

Antimicrobials

VIVILIDE Wide Spectrum Bacteriostatic

VIVMAX Antimicrobial & Germicidal

VIV – 20 Antibacterial for Cosmetics & Toiletries

It holds a unique position in the international H&PC industry with supply-chain relationship with global leaders including - Unilever, L'Oreal, Procter & Gamble, Johnson & Johnson etc. Having exclusive tie ups with global logistics companies, Vivimed has been offering shipment, warehousing, redistribution and door delivery services to large global majors. It has a global network of offices, representatives and distributors across America, Europe, Far East and the Asia Pacific region. Vivimed Labs Europe Ltd (James Robinson Ltd) – Acquired in the year 2008, Vivimed labs Europe Ltd is a leading global supplier of dyes used in a host of personal care and consumer products ranging from hair dye intermediates and photographic developer chemicals to ophthalmic lenses and fluorescent dyes for textiles, inks and coatings. This acquisition has seamlessly positioned Vivimed in the larger and high value space of high-end specialty chemicals.

November 12, 2010

3

Vivimed Labs Ltd.

Vivimed Labs USA, Inc. (Harmet International Ltd) – acquired in the year 2009 as a US hub to increase its global footprint and cut down the time to market for global customers Harmet International has become a strategic and relevant entity.

Revenue Growth

Source: Annual Report Specialty Pharma Division: This specialty division has its inherent strengths in drug delivery and drug discovery with focus on providing cures in the oncology space, arthritis, syndrome X, macular degeneration, psoriasis and stress. Moreover, Vivimed is an active player in CRAMS (Contract Research and Manufacturing Services) segment providing vendor partnerships ranging from molecular research to collaborative manufacturing. Vivimed has shown a steady growth in its revenues across segments over the past four years.

Revenue Growth

Source: Annual Report

992

1275

2076

2615

0

500

1000

1500

2000

2500

3000

FY07 FY08 FY09 FY10

H&PC Actives Division

348

535

686

820

0

100

200

300

400

500

600

700

800

900

FY07 FY08 FY09 FY10

Speciality Pharmaceuticals

November 12, 2010

4

Vivimed Labs Ltd.

812

464

518

17

1329

481

516

1560

655

31

1170

1591

658

1957

775

45

1433

2001

0 300 600 900 1200 1500 1800 2100

Domestic

Export

Domestic

Export

Domestic

ExportSp

ecia

lty

Chem

ical

sSp

ecia

lty

Phar

mac

eutic

als

Tota

l

Rs. in Mn

Segmental Breakup

FY10 FY09 FY08

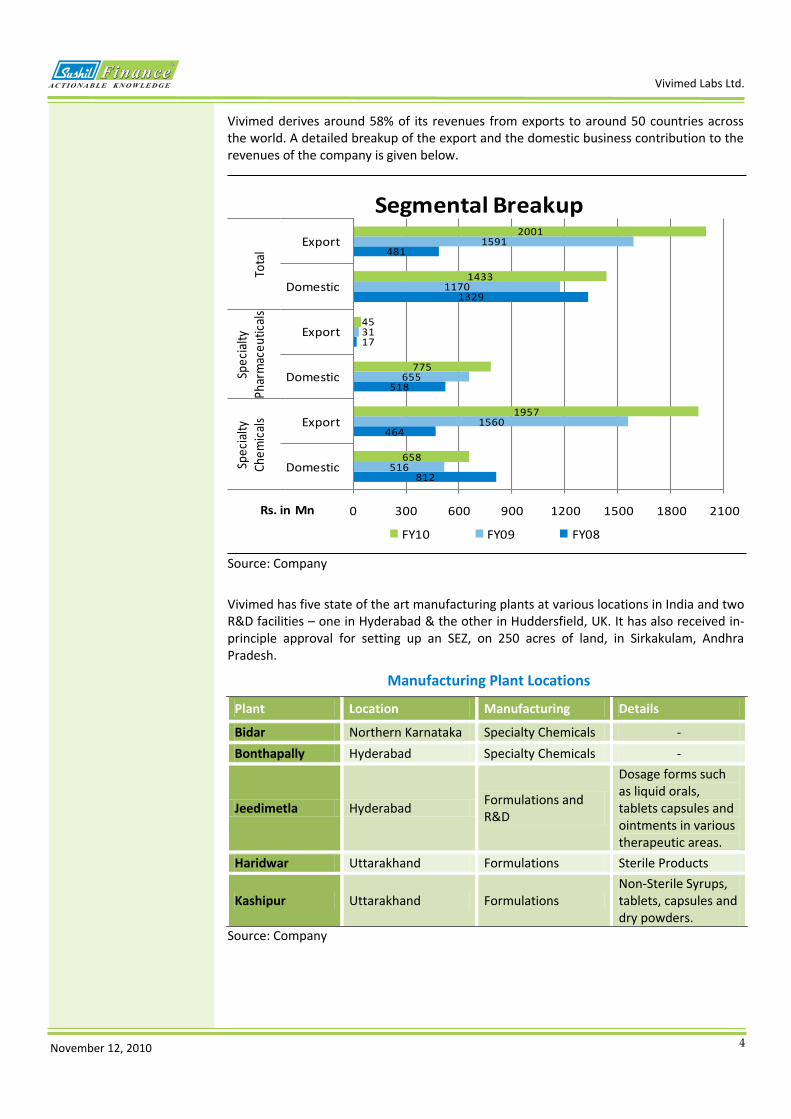

Vivimed derives around 58% of its revenues from exports to around 50 countries across the world. A detailed breakup of the export and the domestic business contribution to the revenues of the company is given below.

Source: Company

Vivimed has five state of the art manufacturing plants at various locations in India and two R&D facilities – one in Hyderabad & the other in Huddersfield, UK. It has also received in-principle approval for setting up an SEZ, on 250 acres of land, in Sirkakulam, Andhra Pradesh.

Manufacturing Plant Locations

Plant Location Manufacturing Details

Bidar Northern Karnataka Specialty Chemicals -

Bonthapally Hyderabad Specialty Chemicals -

Jeedimetla Hyderabad Formulations and R&D

Dosage forms such as liquid orals, tablets capsules and ointments in various therapeutic areas.

Haridwar Uttarakhand Formulations Sterile Products

Kashipur Uttarakhand Formulations Non-Sterile Syrups, tablets, capsules and dry powders.

Source: Company

November 12, 2010

5

Vivimed Labs Ltd.

Preferred Supplier

Service Levels

Quality of the products

Relationship

INVESTMENT ARGUMENTS

High Entry Barriers to become a preferred supplier Specialty chemicals forms an important part of the personal care product even though on volume basis its presence in the product is approximately in the range of 0.1% to 0.5%. Since it forms a very small part of the manufacturing costs of the personal care products, and hence companies like Unilever, L’Oreal, etc, focus more on the quality of these ingredients. Business is not done on “price” but on relationships, product portfolio, service levels and quality standards. Any compromise on the quality front could tarnish the billion dollar image of the product and the company as well. As a result, stringent quality norms need to be followed by the suppliers of these specialty chemical ingredients. If the company is happy with the quality, it rarely changes the supplier. Vivimed enjoys the benefits of early mover advantage as it has been in this line of business since a long time and it is already an approved supplier for global giants as well as domestic companies like L’Oreal, Unilever, P&G, Marico etc. for certain personal care ingredients and therefore it faces limited competition.

The entry barriers in the line of the speciality business that Vivimed caters to is substantial which makes it difficult for new companies to make inroads and takes as much as 3-5 years to become a preferred supplier to global giants in the personal care segment in the US and European markets. Also due to brand sensitivity, vendor qualification is of paramount importance and usually involves elaborate procedures for introducing new suppliers. In case of a new product approval process, it takes around 12 months for the existing supplier to get an approval after which yearly supplies of the product commences with the maximum order to one supplier being close to 60% of the requirement which maintains healthy competition and also reduces over dependency on one supplier incase of unexpected conditions affecting the timely completion of orders in hand or quality problems if any.

New Product Development Process

• Time taken to develop a product - Upto 12 Months.

New Product Approval

•Time Frame

•Existing Supplier - 12 Months

• New Supplier - 36-60 months

Supply Agreements

• 1st Year - 10-20% of Supply.

• 2nd Year - 25-30% of Supply.

• 3rd Year - 50-60% of Supply.

November 12, 2010

6

Vivimed Labs Ltd.

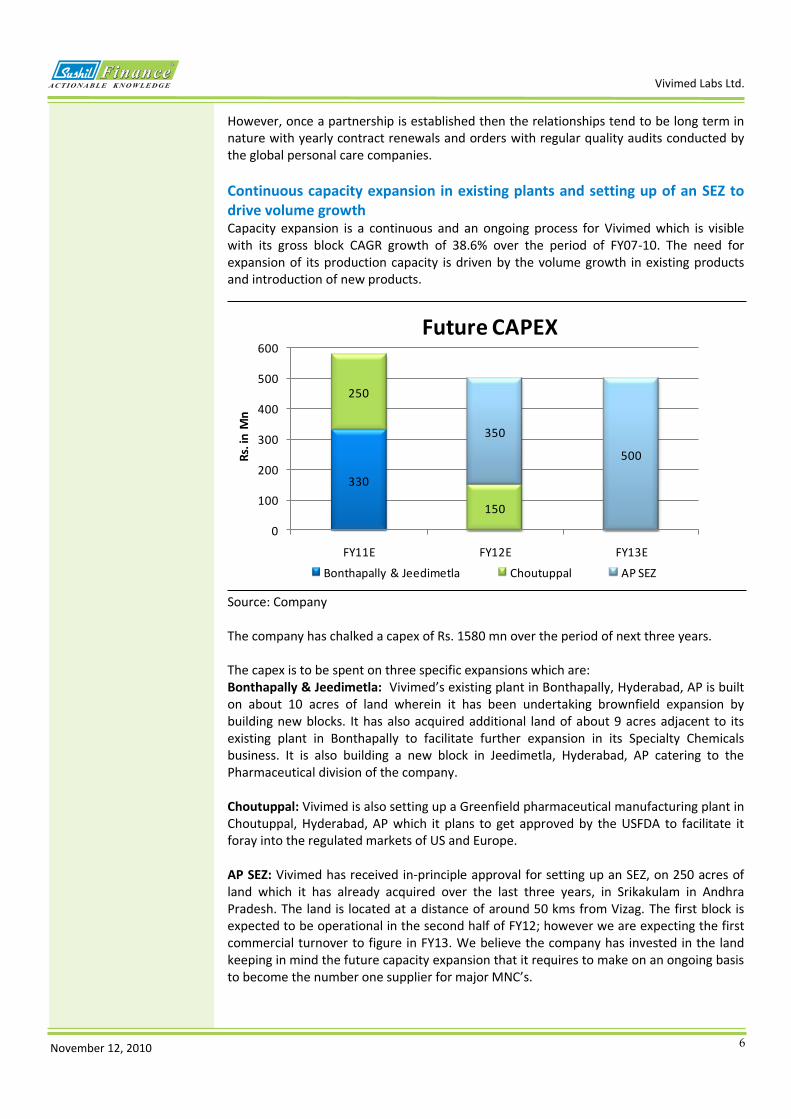

However, once a partnership is established then the relationships tend to be long term in nature with yearly contract renewals and orders with regular quality audits conducted by the global personal care companies.

Continuous capacity expansion in existing plants and setting up of an SEZ to drive volume growth Capacity expansion is a continuous and an ongoing process for Vivimed which is visible with its gross block CAGR growth of 38.6% over the period of FY07-10. The need for expansion of its production capacity is driven by the volume growth in existing products and introduction of new products.

Source: Company The company has chalked a capex of Rs. 1580 mn over the period of next three years. The capex is to be spent on three specific expansions which are: Bonthapally & Jeedimetla: Vivimed’s existing plant in Bonthapally, Hyderabad, AP is built on about 10 acres of land wherein it has been undertaking brownfield expansion by building new blocks. It has also acquired additional land of about 9 acres adjacent to its existing plant in Bonthapally to facilitate further expansion in its Specialty Chemicals business. It is also building a new block in Jeedimetla, Hyderabad, AP catering to the Pharmaceutical division of the company. Choutuppal: Vivimed is also setting up a Greenfield pharmaceutical manufacturing plant in Choutuppal, Hyderabad, AP which it plans to get approved by the USFDA to facilitate it foray into the regulated markets of US and Europe. AP SEZ: Vivimed has received in-principle approval for setting up an SEZ, on 250 acres of land which it has already acquired over the last three years, in Srikakulam in Andhra Pradesh. The land is located at a distance of around 50 kms from Vizag. The first block is expected to be operational in the second half of FY12; however we are expecting the first commercial turnover to figure in FY13. We believe the company has invested in the land keeping in mind the future capacity expansion that it requires to make on an ongoing basis to become the number one supplier for major MNC’s.

330

250

150

350

500

0

100

200

300

400

500

600

FY11E FY12E FY13E

Rs.

in M

n

Future CAPEX

Bonthapally & Jeedimetla Choutuppal AP SEZ

November 12, 2010

7

Vivimed Labs Ltd.

Source: Company We believe the anti-microbial and the sunscreen facility will be operational in the last quarter of FY11 whereas the remaining capacity expansions in anti-dandruff, catonic guar & skin whitener will become operational in FY12. With the above mentioned capacity expansion in the segments of skincare, oral care and hair care we believe the company would be in a position to garner additional revenue of Rs. 240 mn & Rs. 1070 mn in FY11E and FY12E respectively.

Long term nature of contracts The contracts that Vivimed has entered into with global giants are generally long-term in nature. This is because, once the customers are convinced with the quality and the delivery commitment then the customer prefer not to change the supplier since it has to invest a lot of time and money to get in a new supplier.

It gives an opportunity to players like Vivimed to partner in the growth of these personal care companies, both from the perspective of volume growth of a product and geographical expansion as well as becoming a supplier for new products introduced by the personal care company.

Alliance with ISP Vivimed enters into alliances with companies that are already preferred suppliers to big personal care companies or have a wide distribution network in order to increase geographical presence and also take cost-based advantages. Vivimed entered into a manufacturing alliance with International Specialty Products Inc. (ISP) USA, in Jun’10, for sunscreens, which will eventually see it emerging as a major global provider of sunscreen ingredients. ISP is a leading global supplier of specialty chemicals and performance enhancing products and produces more than 500 specialty chemicals, which it markets and sells worldwide. The two companies will use this alliance for joint marketing of some products. From November 2010, ISP will add a number of UVA and UVB absorbers that are already manufactured by Vivimed, to its portfolio of sun protection ingredients. We have factored in revenues of Rs. 421 mn from this alliance to accrue in FY12E.

Strong focus on R&D and continuous development of new products A key requisite to remain competitive in the field of specialty chemicals is to continuously come up with new products at regular intervals. Vivimed has two R&D facilities, in

1500

350

200

500

30

0

200

400

600

800

1000

1200

1400

1600

Sun Screen Anti Dandruff Anti Microbial Haircare Skin Whitener

Capacity Additions (MT)

November 12, 2010

8

Vivimed Labs Ltd.

Hyderabad and Huddersfield (UK), and also partners with its customers to continuously develop new ingredients wherein it gets the added incentive of 100% supply if the product gets approved. Since the company is investing in R&D activity in a significant way, it is in a position to cater to the client’s continuous need for innovation. R&D expenditure for Vivimed could be in the range of 1-2% of sales going forward.

The company is planning to launch new products like C-Vite and Catonic guar in H2FY11. We believe C-Vite, which is a specialty chemical for the sunscreen segment, will clock revenues of around Rs. 140 mn in FY12E. Cationic Guar is an ingredient which has been approved by an existing customer of Vivimed for their global shampoo brand. We believe the company can clock revenues of around Rs. 140 mn from this launch in FY12E. The company is also developing a proprietary product for skin lightening which is undergoing trial-runs with a global major in India. Global supplies for this product are expected to start in FY12E with contribution towards revenue expected to be around Rs. 150 mn.

In order to make the most of the increasing demand for natural ingredients the company has undertaken investment in R&D to discover alternate natural ingredients for some of its applications in its R&D facility in Hyderabad. However we have not factored any revenue contribution from the same since it is at a very nascent stage.

Strong clientele Vivimed enjoys an early mover advantage on the back of which it boasts a strong clientele base. Even though US and Europe have been the biggest markets for personal care products; the developing nations are also catching up on the back of changing lifestyle, higher disposable income, higher outdoor activity, etc. It is expected to capitalize on the opportunities available in the personal care ingredients space as it is an approved supplier to global personal care giants like L’Oreal, Unilever, P&G, etc.

Research & Development

• Partner with Customer/ Joint Research

• Independent Research

New Molecule Development Process

•Product Innovation

•Synthesis

•Saturation Studies

•Formulation

Supply Agreements

• Joint Research - 100% Supply Agreement

• Independent Research - Agreement is subject to a no of factors.

November 12, 2010

9

Vivimed Labs Ltd.

Source: Company, Sushil Finance

274 328 361 397

411

492566

668

0

200

400

600

800

1000

1200

FY09 FY10 FY11E FY12E

Increasing contribution from Branded Formulations

CRAMS Branded Formulations

In terms of leading brands in which ingredients manufactured by Vivimed are used are Clinic All clear, Head & Shoulders, Colgate, Revlon Color Silk, Fair & Lovely, Pepsodent, Palmolive Naturals Shampoo etc. The Speciality Pharmaceuticals segment of the company is also witnessing steady growth. It supplies to major pharmaceutical companies like Merck, Lupin, Novartis, Cipla etc.

Focus more on Branded formulations:

Vivimed has seen a steady growth in the Pharma segment and has strengthened its position among marquee MNCs like Novartis, Merck Ltd, AstraZeneca etc as a consistent and quality conscious manufacturer of branded formulations.

The pharmaceutical formulations business is segmented in two growth driving areas going ahead namely:-

Establish own brand sales in Eastern European Markets

Contract Manufacturing

The Company has forayed into formulation exports to Russia / CIS countries and we are optimistic of witnessing a CAGR growth of 16.5% in the export sales for the period of FY09-FY12E. Vivimed has been actively registering more products for future exports. The division has now appointed a full fledged sales team for the African Continent and has already initiated registrations in eight African countries. We have factored in revenue of Rs. 566 mn and Rs. 668 mn in FY11E and FY12E from its branded

formulations business. We believe the sales mix would see a marginal change with greater contribution from the company’s branded formulations business going forward. Also with the setting up the USFDA approved pharmaceutical plant in Hyderabad, we believe the company would be in a position to foray into the regulated markets of US and Europe. However, we have not factored in any revenue increment coming from these markets.

November 12, 2010

10

Vivimed Labs Ltd.

Source: Annual Report, Sushil Finance

FY08 FY09 FY10 FY11E FY12E

0.0

5.0

10.0

15.0

20.0

25.0

30.0Improving ROE & ROCE

ROCE (%) ROE (%)

13401810

2761

3435

4116

5598

0

1000

2000

3000

4000

5000

6000

FY07 FY08 FY09 FY10 FY11E FY12E

Net Sales (Rs. In Mn)

260313

450

631

770

1075

0

200

400

600

800

1000

1200

FY07 FY08 FY09 FY10 FY11E FY12E

EBIDTA (Rs. In Mn)

136159

194

310

391

572

0

100

200

300

400

500

600

700

FY07 FY08 FY09 FY10 FY11E FY12E

RPAT (Rs. In Mn)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY07 FY08 FY09 FY10 FY11E FY12E

0

500

1000

1500

2000

2500

3000

3500

Debt to Equity

Debt D:E Ratio

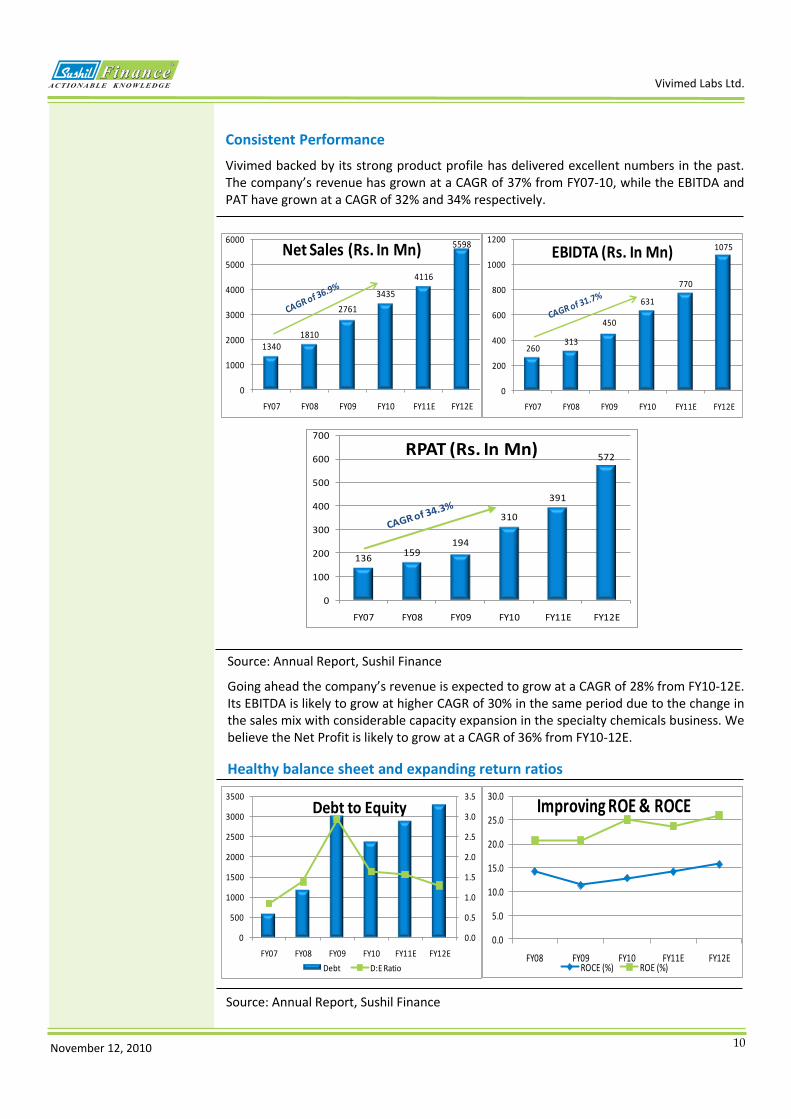

Consistent Performance

Vivimed backed by its strong product profile has delivered excellent numbers in the past. The company’s revenue has grown at a CAGR of 37% from FY07-10, while the EBITDA and PAT have grown at a CAGR of 32% and 34% respectively.

Source: Annual Report, Sushil Finance

Going ahead the company’s revenue is expected to grow at a CAGR of 28% from FY10-12E. Its EBITDA is likely to grow at higher CAGR of 30% in the same period due to the change in the sales mix with considerable capacity expansion in the specialty chemicals business. We believe the Net Profit is likely to grow at a CAGR of 36% from FY10-12E.

Healthy balance sheet and expanding return ratios

November 12, 2010

11

Vivimed Labs Ltd.

The D: E ratio of the company has fallen from 2.9x in FY09 to almost 1.6x in FY10 which is further likely to decline to 1.3x by FY12E, thus strengthening the balance sheet. Also the Company has healthy return ratios with ROE & ROCE pegged at 26% and 16% respectively for FY12E.

INDUSTRY OVERVIEW

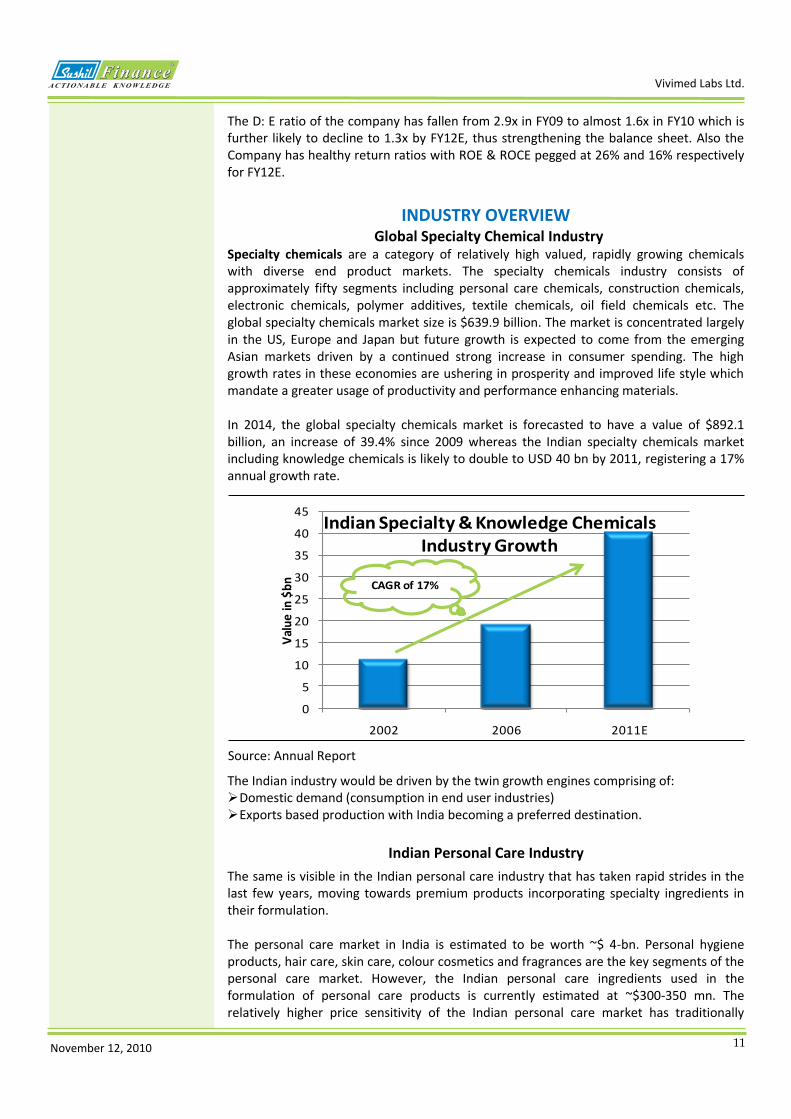

Global Specialty Chemical Industry Specialty chemicals are a category of relatively high valued, rapidly growing chemicals with diverse end product markets. The specialty chemicals industry consists of approximately fifty segments including personal care chemicals, construction chemicals, electronic chemicals, polymer additives, textile chemicals, oil field chemicals etc. The global specialty chemicals market size is $639.9 billion. The market is concentrated largely in the US, Europe and Japan but future growth is expected to come from the emerging Asian markets driven by a continued strong increase in consumer spending. The high growth rates in these economies are ushering in prosperity and improved life style which mandate a greater usage of productivity and performance enhancing materials. In 2014, the global specialty chemicals market is forecasted to have a value of $892.1 billion, an increase of 39.4% since 2009 whereas the Indian specialty chemicals market including knowledge chemicals is likely to double to USD 40 bn by 2011, registering a 17% annual growth rate.

Source: Annual Report

The Indian industry would be driven by the twin growth engines comprising of: Domestic demand (consumption in end user industries) Exports based production with India becoming a preferred destination.

Indian Personal Care Industry

The same is visible in the Indian personal care industry that has taken rapid strides in the last few years, moving towards premium products incorporating specialty ingredients in their formulation. The personal care market in India is estimated to be worth ~$ 4-bn. Personal hygiene products, hair care, skin care, colour cosmetics and fragrances are the key segments of the personal care market. However, the Indian personal care ingredients used in the formulation of personal care products is currently estimated at ~$300-350 mn. The relatively higher price sensitivity of the Indian personal care market has traditionally

0

5

10

15

20

25

30

35

40

45

2002 2006 2011E

Val

ue

in $

bn

Indian Specialty & Knowledge Chemicals Industry Growth

CAGR of 17%

November 12, 2010

12

Vivimed Labs Ltd.

Expanding demand for

personal care

Burgeoning

middle class

Growing beauty

consciousness

Increasing disposable

income levels

A growing population

of women in the 25-44 age group

Increasing urbanization

limited the role of high value personal care ingredients. This has also contributed to lower R&D spends and fewer innovations by the Indian personal care product formulation companies, few of which are backward integrated in the personal care ingredients space. However, the recent market developments and changed competitive landscape with the advent of large corporations willing to take investment decisions for a longer time horizon have contributed to changing the scenario. Also favorable demographic factors and increasing beauty consciousness indicate high future demand for personal care products and specifically for active ingredients. Indian personal care industry typically uses specialty chemicals, such as surfactants, fragrance compounds, polymer compounds and UV filters as active ingredients. Growing demand is leading to development of high-end specialty active ingredients, with a stronger emphasis on organic (natural) ingredients. Driven by increasing consumer preference for products with better functional benefits, the personal care ingredients market is expected to surpass the growth of the personal care products market. However, it will be important for companies in the personal care ingredients space to develop R&D capabilities to further customize products and also to introduce new products on a regular basis to be the eventual winners.

November 12, 2010

13

Vivimed Labs Ltd.

RISK & CONCERNS

Foreign Exchange Risk Vivimed derives close to 58% of its revenues from global markets. Thus any adverse movement in USD-INR could affect the margins of the company going forward. Although it does have a partial natural hedge against such adverse movement as it imports raw materials and also majority of its debt is foreign currency term loans. Dilution Risk In order to keep a check on the debt levels, the company might think of diluting equity further to fund its future expansion plans. However we have not factored in any further equity dilution other than the warrant conversion expected in FY12 which would increase its equity capital to Rs. 114.7 mn.

OUTLOOK & VALUATION Vivimed Labs is involved in the manufacture of specialty chemicals (contributing nearly 75% of its revenues) and pharmaceutical formulations. The mantra at Vivimed now is to focus more on specialty chemicals with a target to see around 75% of its revenues coming from this segment. It is also making an effort towards moving out of low margin products and focusing on the relatively higher margin products which would better the margins going ahead. It has embarked on a Rs. 1580 mn expansion plan to be executed over the next three years. Going forward, we expect the growth in the Specialty Chemicals business to come from continuous volume expansion, supplying ingredients to the already existing customers in new geographies in addition to supplying ingredients for new products and new customers whereas in the Pharma business we believe the growth would be driven by increasing focus on branded formulation exports to Russia / CIS and other eastern European countries. Keeping in mind the company’s strong track record, established customer base, increasing product profile and increasing demand for its products backed by volume expansion, we expect its revenue and PAT to grow at a CAGR of 27.7% and 35.8% over FY09-12E. It is currently trading at a P/E of 6.8x its FY12E diluted EPS of Rs. 50 and we recommend a “BUY” with a target price of Rs. 450 (9x FY12E EPS).

November 12, 2010

14

Vivimed Labs Ltd.

PROFIT & LOSS STATEMENT (Rs.mn)

Y/E March FY09 FY10 FY11E FY12E

Net Sales 2761.2 3434.9 4116.1 5598.0

Raw material 1872.6 2282.2 2778.4 3778.7

Manufacturing 236.4 258.9 296.4 403.1

Staff Cost 167.7 220.7 226.4 279.9

Total Expenditure 2311.2 2804.1 3346.4 4523.2

PBIDT 450.1 630.8 769.7 1074.8

Interest 172.7 212.3 230.5 263.0

Depreciation 71.5 87.3 108.8 136.4

Other Income 25.3 65.3 70.0 56.0

PBT incl OI 231.1 396.5 500.3 731.4

Tax 37.6 86.3 109.0 159.3

RPAT 193.5 310.1 391.4 572.1

Minority Interest 0.0 0.0 0.0 0.0

RPAT after MI 193.5 310.1 391.4 572.1

BALANCE SHEET STATEMENT (Rs.mn)

As on 31st March FY09 FY10 FY11E FY12E

Share Capital 94.0 99.7 99.7 114.7

Warrant Application Money

23.4 49.6 79.6 0.0

Reserves & Surplus 908.1 1299.4 1673.3 2437.9

Net Worth 1025.5 1448.6 1852.5 2552.5

Secured Loans 2237.7 2345.5 2874.2 3280.2

Unsecured Loans 767.0 7.4 7.4 7.4

Total Loan funds 3004.7 2352.9 2881.6 3287.6

Deferred Tax 130.3 161.9 161.9 161.9

Capital Employed 4161 3963 4896 6002

Net Block 1480.3 1607.4 2078.6 2442.2

Cap. WIP 268.8 11.4 11.4 11.4

Investments 804.8 939.8 939.8 939.8

Sundry Debtors 707.5 938.6 1014.9 1380.3

Cash & Bank Bal 169.8 56.2 219.6 390.0

Loans & Advances 264.1 152.3 248.1 337.4

Inventory 691.3 793.5 875.4 1190.5

Curr Liab & Prov 313.5 593.8 549.8 747.7

Net Current Assets 1519.1 1346.7 1808.2 2550.6

Total Assets 4161 3963 4896 6002

FINANCIAL RATIO STATEMENT

Y/E March FY09 FY10 FY11E FY12E

Growth (%)

Net Sales 52.5 24.4 19.8 36.0

EBITDA 43.7 40.2 22.0 39.6

Adjusted Net Profit 21.3 60.2 26.2 46.2

Profitability (%)

EBIDTA Margin (%) 16.3 18.4 18.7 19.2

Net Profit Margin (%) 7.0 9.0 9.5 10.2

ROCE (%) 11.4 12.9 14.2 15.7

ROE (%) 20.7 25.1 23.7 26.0

Per Share Data (Rs.)

EPS (Rs.) 20.6 31.1 39.3 50.0

CEPS (Rs.) 29.2 42.9 54.0 66.6

BVPS (Rs) 109.1 145.4 185.9 222.6

Valuation

PER (x) 16.4 10.9 8.6 6.8

PEG (x) 0.8 0.2 0.3 0.3

P/BV (x) 3.1 2.3 1.8 1.5

EV/EBITDA (x) 13.4 9.0 7.8 6.3

EV/Net Sales (x) 2.2 1.6 1.5 1.2

Turnover

Debtor Days 84.0 87.5 90.0 90.0

Creditor Days 43.5 50.5 50.0 50.0

Gearing Ratio

D/E 2.9 1.6 1.6 1.3

Source: Company, Sushil Finance Research Estimates

CASH FLOW STATEMENT (Rs.mn)

Y/E March FY09 FY10 FY11E FY12E

Profit before tax & Extraordinary Items

231.1 396.5 500.3 731.4

Depreciation & Amortization

71.5 87.3 108.8 136.4

Chg. in Working Capital -476.5 58.9 -298.1 -572.0

Cash Flow from Operating

-168.2 551.3 202.1 136.6

(Incr)/ Decr in Gross PP&E

-616.1 -214.5 -580.0 -500.0

(Incr)/Decr In Intangibles

-804.8 -135.0 0.0 0.0

Cash Flow from Investing

-1610.7 -71.3 -580.0 -500.0

(Decr)/Incr in Debt 1837.5 -651.8 528.8 406.0

(Decr)/Incr in Share Capital

0.0 5.6 0.0 15.0

Dividend -16.5 -17.5 -17.5 -17.5

Cash Flow from Financing

1793.3 -593.6 541.3 533.9

Cash at the End of the Year

169.8 56.2 219.6 390.0

November 12, 2010

15

Vivimed Labs Ltd.

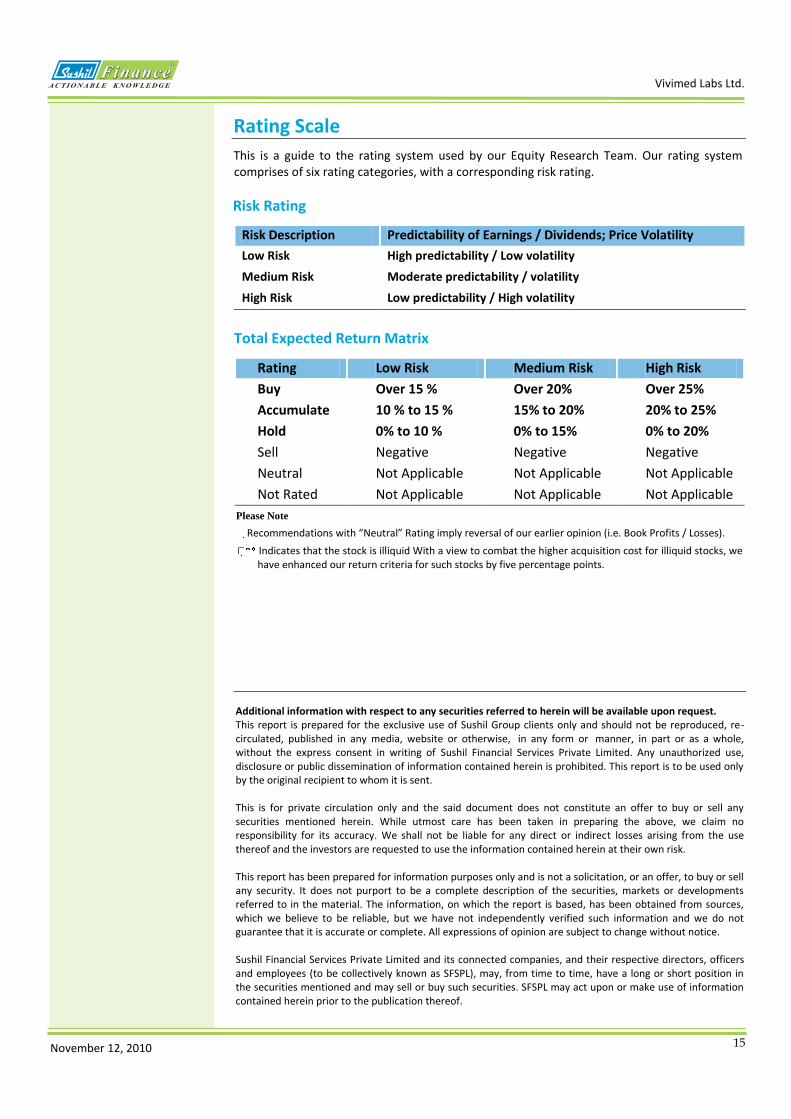

Rating Scale

This is a guide to the rating system used by our Equity Research Team. Our rating system comprises of six rating categories, with a corresponding risk rating.

Risk Rating

Risk Description Predictability of Earnings / Dividends; Price Volatility

Low Risk High predictability / Low volatility

Medium Risk Moderate predictability / volatility

High Risk Low predictability / High volatility

Total Expected Return Matrix

Rating Low Risk Medium Risk High Risk

Buy Over 15 % Over 20% Over 25%

Accumulate 10 % to 15 % 15% to 20% 20% to 25%

Hold 0% to 10 % 0% to 15% 0% to 20%

Sell Negative

Returns

Negative

Returns

Negative

Returns Neutral Not Applicable Not Applicable Not Applicable

Not Rated Not Applicable Not Applicable Not Applicable

Please Note

Recommendations with “Neutral” Rating imply reversal of our earlier opinion (i.e. Book Profits / Losses).

Indicates that the stock is illiquid With a view to combat the higher acquisition cost for illiquid stocks, we have enhanced our return criteria for such stocks by five percentage points.

Additional information with respect to any securities referred to herein will be available upon request. This report is prepared for the exclusive use of Sushil Group clients only and should not be reproduced, re-circulated, published in any media, website or otherwise, in any form or manner, in part or as a whole, without the express consent in writing of Sushil Financial Services Private Limited. Any unauthorized use, disclosure or public dissemination of information contained herein is prohibited. This report is to be used only by the original recipient to whom it is sent. This is for private circulation only and the said document does not constitute an offer to buy or sell any securities mentioned herein. While utmost care has been taken in preparing the above, we claim no responsibility for its accuracy. We shall not be liable for any direct or indirect losses arising from the use thereof and the investors are requested to use the information contained herein at their own risk. This report has been prepared for information purposes only and is not a solicitation, or an offer, to buy or sell any security. It does not purport to be a complete description of the securities, markets or developments referred to in the material. The information, on which the report is based, has been obtained from sources, which we believe to be reliable, but we have not independently verified such information and we do not guarantee that it is accurate or complete. All expressions of opinion are subject to change without notice. Sushil Financial Services Private Limited and its connected companies, and their respective directors, officers and employees (to be collectively known as SFSPL), may, from time to time, have a long or short position in the securities mentioned and may sell or buy such securities. SFSPL may act upon or make use of information contained herein prior to the publication thereof.