spain reduces its tax haven “blacklist” reduces its tax haven “blacklist” summary the...

TRANSCRIPT

Spain reduces its tax haven “blacklist”Summary

The Spanish Government is putting significant efforts into expanding its tax treaty and tax information exchange agreement network, particularly with countries and territories included on the Spanish tax haven “blacklist.” By way of example, a tax treaty with Singapore will enter into effect on 1 January 2013.

States that enter into a tax treaty or tax information exchange agreement are excluded from the Spanish tax haven “blacklist” and, consequently, from the restrictive provisions in Spanish tax legislation that apply to tax havens.

Below is a review of recent developments on this matter and an update of the situation relating to the Spanish tax haven “blacklist.”

Detailed analysis

Spanish domestic legislation provides a number of anti-avoidance rules for transactions with entities that reside in tax havens, ranging from disallowing Spanish participation exemption benefits for dividends or income from tax haven resident subsidiaries, to the need to evidence the effectiveness of services rendered by tax haven residents. Countries and territories that qualify as Spanish tax havens are those included on the tax haven “blacklist,” which was approved by article 1 of Royal Decree 1080/1991, of 5 July 1991. It is, however, provided that countries and territories are automatically excluded from the “blacklist” when they sign a tax exchange of Information agreement or a tax Treaty containing an exchange of information clause with Spain. The exclusion is effective on the date the agreement or treaty enters into force.

Thirteen out of the forty-eight countries and territories included on the initial list have concluded a tax treaty or an exchange of information agreement with Spain and are consequently no longer deemed as tax havens for Spanish tax purposes (see chart on the next page).

19 January 2012

International Tax Alert

Get the world to go!

You can access corporate income tax rates of over 65 countries for multiple years using your mobile device:

• Type into your web browser: www.ey.mobi/ITS/rates

2 International Tax Alert

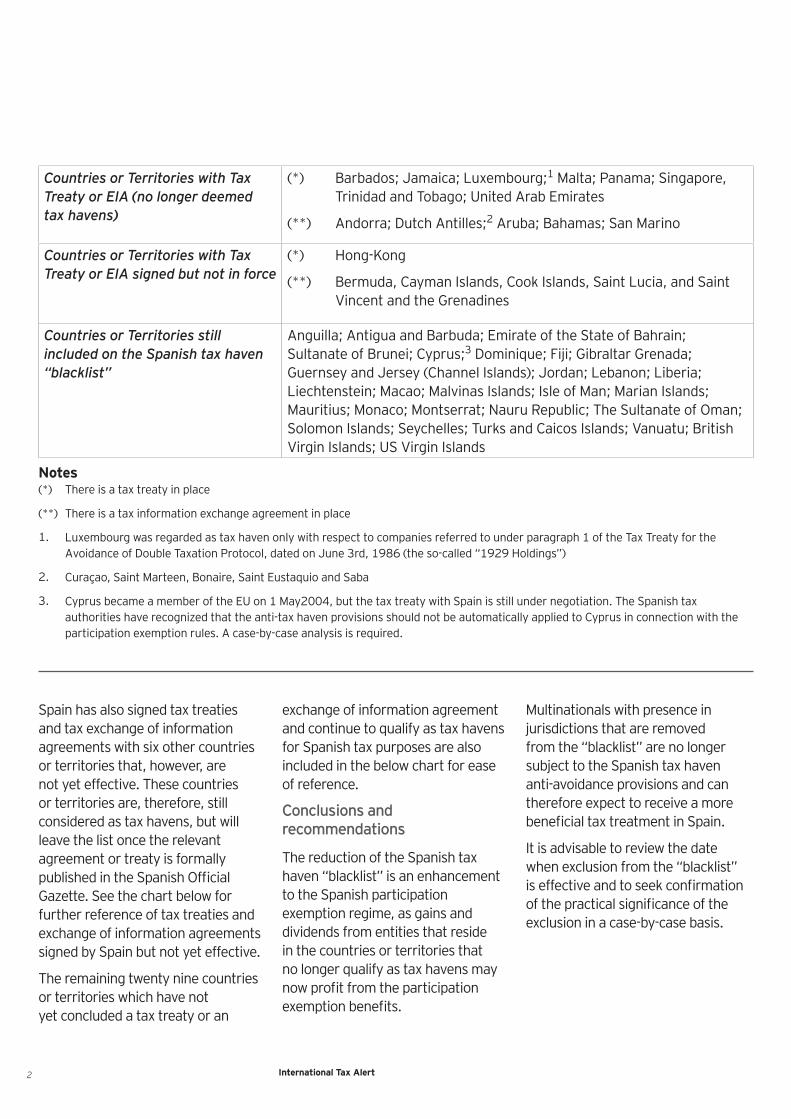

Countries or Territories with Tax Treaty or EIA (no longer deemed tax havens)

(*) Barbados; Jamaica; Luxembourg;1 Malta; Panama; Singapore, Trinidad and Tobago; United Arab Emirates

(**) Andorra; Dutch Antilles;2 Aruba; Bahamas; San Marino

Countries or Territories with Tax Treaty or EIA signed but not in force

(*) Hong-Kong

(**) Bermuda, Cayman Islands, Cook Islands, Saint Lucia, and Saint Vincent and the Grenadines

Countries or Territories still included on the Spanish tax haven “blacklist”

Anguilla; Antigua and Barbuda; Emirate of the State of Bahrain; Sultanate of Brunei; Cyprus;3 Dominique; Fiji; Gibraltar Grenada; Guernsey and Jersey (Channel Islands); Jordan; Lebanon; Liberia; Liechtenstein; Macao; Malvinas Islands; Isle of Man; Marian Islands; Mauritius; Monaco; Montserrat; Nauru Republic; The Sultanate of Oman; Solomon Islands; Seychelles; Turks and Caicos Islands; Vanuatu; British Virgin Islands; US Virgin Islands

Notes(*) There is a tax treaty in place

(**) There is a tax information exchange agreement in place

1. Luxembourg was regarded as tax haven only with respect to companies referred to under paragraph 1 of the Tax Treaty for the Avoidance of Double Taxation Protocol, dated on June 3rd, 1986 (the so-called “1929 Holdings”)

2. Curaçao, Saint Marteen, Bonaire, Saint Eustaquio and Saba

3. Cyprus became a member of the EU on 1 May2004, but the tax treaty with Spain is still under negotiation. The Spanish tax authorities have recognized that the anti-tax haven provisions should not be automatically applied to Cyprus in connection with the participation exemption rules. A case-by-case analysis is required.

Spain has also signed tax treaties and tax exchange of information agreements with six other countries or territories that, however, are not yet effective. These countries or territories are, therefore, still considered as tax havens, but will leave the list once the relevant agreement or treaty is formally published in the Spanish Official Gazette. See the chart below for further reference of tax treaties and exchange of information agreements signed by Spain but not yet effective.

The remaining twenty nine countries or territories which have not yet concluded a tax treaty or an

exchange of information agreement and continue to qualify as tax havens for Spanish tax purposes are also included in the below chart for ease of reference.

Conclusions and recommendations

The reduction of the Spanish tax haven “blacklist” is an enhancement to the Spanish participation exemption regime, as gains and dividends from entities that reside in the countries or territories that no longer qualify as tax havens may now profit from the participation exemption benefits.

Multinationals with presence in jurisdictions that are removed from the “blacklist” are no longer subject to the Spanish tax haven anti-avoidance provisions and can therefore expect to receive a more beneficial tax treatment in Spain.

It is advisable to review the date when exclusion from the “blacklist” is effective and to seek confirmation of the practical significance of the exclusion in a case-by-case basis.

3International Tax Alert

For additional information with respect to this Alert, please contact the following:

Ernst & Young Abogados, International Tax Services, Madrid• Laura Ezquerra +34 91 572 7570 [email protected]• Federico Linares +34 91 572 7482 [email protected]

Ernst & Young LLP, Spanish Tax Desk, New York• Inigo Alonso Salcedo +1 212 773 8692 [email protected]

4 International Tax Alert

www.ey.com

© 2012 EYGM Limited. All Rights Reserved.

EYG no. CM2675

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 152,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com. Ernst & Young Abogados is a member firm serving clients in Spain.

International Tax ServicesAbout Ernst & Young’s International Tax services practices

Our dedicated international tax professionals assist our clients with their cross-border tax structuring, planning, reporting and risk management. We work with you to build proactive and truly integrated global tax strategies that address the tax risks of today’s businesses and achieve sustainable growth. It’s how Ernst & Young makes a difference.

Ernst & Young

Assurance | Tax | Transactions | Advisory

Ernst & Young International Tax Services• Global ITS, Jim Tobin

• Americas, Jeffrey Michalak

• Asia Pacific, Alice Chan

• Europe, Middle East, India and Africa, Alex Postma

• Japan, Kai Hielscher

• Argentina Carlos Casanovas Buenos Aires• Australia Daryn Moore Sydney• Austria Roland Rief Vienna• Belgium Herwig Joosten Brussels• Brazil Gil Mendes Sao Paulo• Canada George Guedikian Toronto• Central America Rafael Sayagues San José• Chile Osiel Gonzalez Santiago• China Becky Lai Beijing• Colombia Ximena Zuluaga Bogota• Czech Republic Libor Frýzek Prague• Denmark Niels Josephsen Soborg• Finland Katri Nygård Helsinki • France Claire Acard Paris• Germany Stefan Koehler Frankfurt• Hong Kong Christian Pellone Hong Kong• Hungary Botond Rencz Budapest

Balazs Szolgyemy Budapest• India Hitesh Sharma Mumbai• Ireland Joe Bollard Dublin• Israel Sharon Shulman Tel Aviv• Italy Marco Magenta Milan• Japan Kai Hielscher Tokyo• Korea Kyung-Tae Ko Seoul• Luxembourg Frank Muntendam Luxembourg• Malaysia Hock Khoon Lee Kuala Lumpur• Mexico Koen van ‘t Hek Mexico City• Middle East Tobias Lintvelt Abu Dhabi • Middle East Michelle Kotze Dubai• Netherlands Johan van den Bos Amsterdam• Norway Oyvind Hovland Oslo• Peru Roberto Cores Lima• Philippines Ma Fides Balili Makati City• Poland Andrzej Broda Warsaw• Portugal Antonio Neves Lisbon• Russia Vladimir Zheltonogov Moscow• Singapore Andy Baik Singapore• South Africa Justin Liebenberg Johannesburg• Spain Federico Linares Madrid• Sweden Erik Hultman Stockholm• Switzerland Daniel Gentsch Zurich• Taiwan Alice Chung Taipei• Thailand Anthony Loh Bangkok• Turkey Feridun Gungor Istanbul• United Kingdom Matthew Mealey London

Anna Anthony London• United States Jeffrey Michalak Detroit• Venezuela Jose Velazquez Caracas• Vietnam Vu Huong Hanoi

Ernst & Young Member Firm Contacts