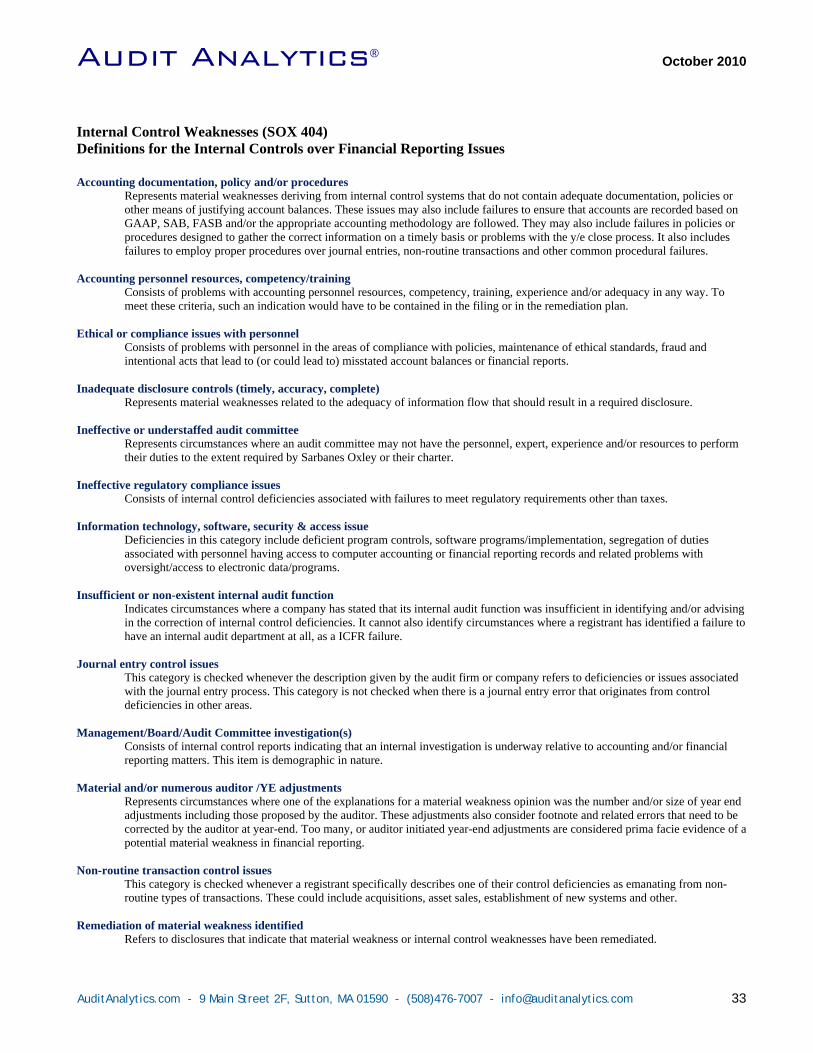

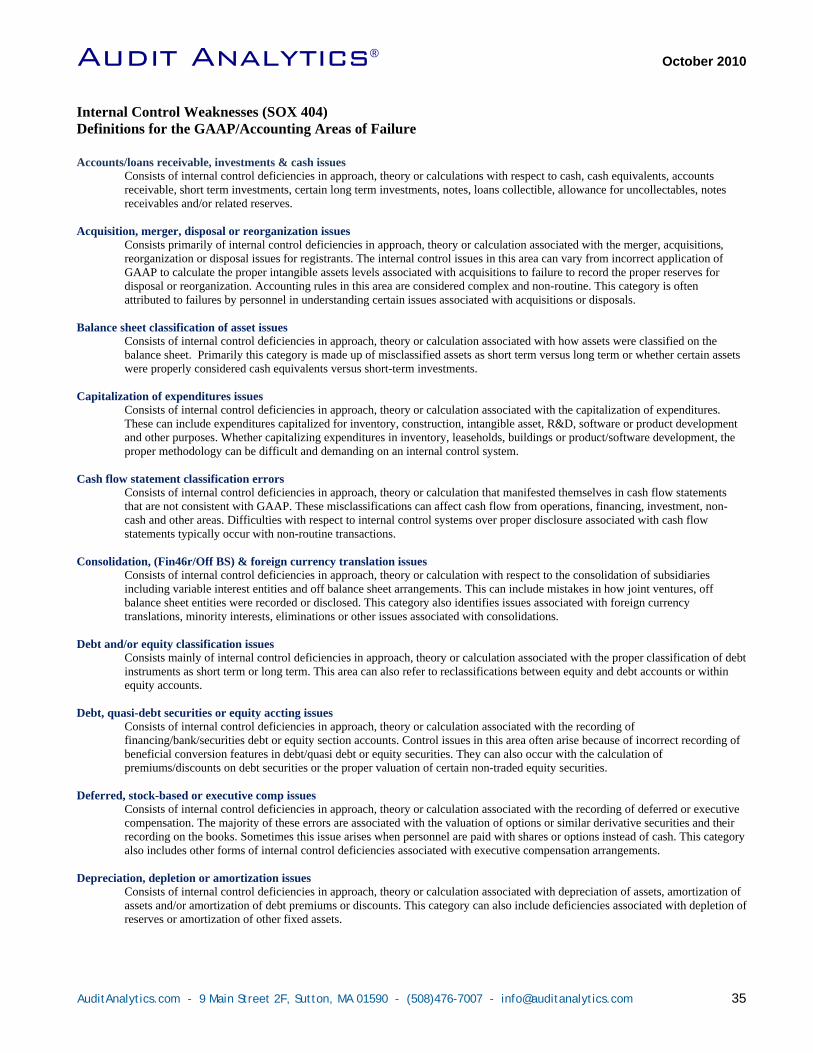

sox 404 dashboard - audit analyticsdisclosures made pursuant to the securities laws, and for other...

TRANSCRIPT

SOX 404 Dashboard Year 6 Update

October 2010

Don Whalen, Esq. Research [email protected] x222

Mark Cheffers, CPA, ABV, [email protected] x223

Maggie Thrun, Research [email protected] 508.476.7007 x236

Audit Analytics® October 2010

AuditAnalytics.com ● 9 Main Street 2F, Sutton, MA 01590 ● (508) 476-7007 ● [email protected]

Table of Contents

Page

A. Summary 1 B. Introduction 2 C. SOX 404 Requirement History: The Staggered and Two-Tiered Implementation of SOX 404 2 D. Executive Summary – Year 6 Section SOX 404 Update 3 E. SOX 404 Year 5 Tables 7 F. SOX 404 Year 6 Tables (Partial Year Data) 20 G. Definitions for the Internal Control Issues 33 H. Definitions for the GAAP/Accounting Areas of Failure 35 I. Definitions for Exemption Reasons 37 J. Overview: Audit Analytics 38

Audit Analytics® October 2010

SOX 404 Dashboard; Year 6 Update Summary

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508)476-7007 - [email protected] 1

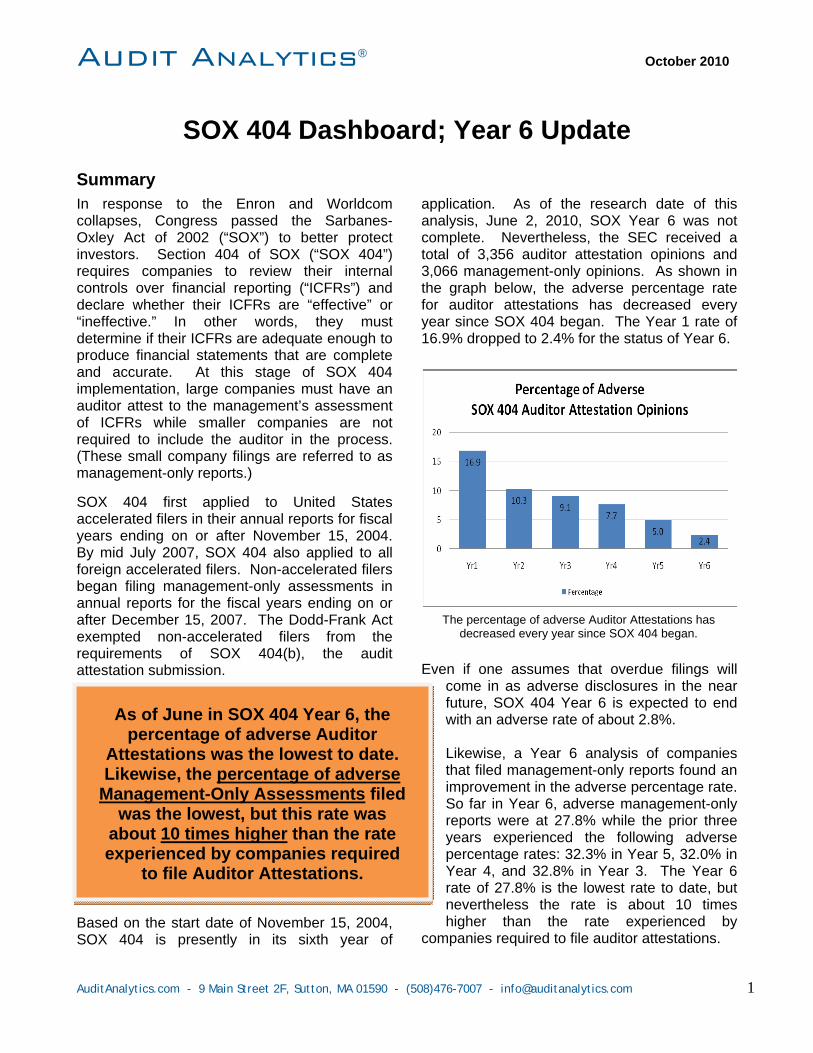

In response to the Enron and Worldcom collapses, Congress passed the Sarbanes-Oxley Act of 2002 (“SOX”) to better protect investors. Section 404 of SOX (“SOX 404”) requires companies to review their internal controls over financial reporting (“ICFRs”) and declare whether their ICFRs are “effective” or “ineffective.” In other words, they must determine if their ICFRs are adequate enough to produce financial statements that are complete and accurate. At this stage of SOX 404 implementation, large companies must have an auditor attest to the management’s assessment of ICFRs while smaller companies are not required to include the auditor in the process. (These small company filings are referred to as management-only reports.) SOX 404 first applied to United States accelerated filers in their annual reports for fiscal years ending on or after November 15, 2004. By mid July 2007, SOX 404 also applied to all foreign accelerated filers. Non-accelerated filers began filing management-only assessments in annual reports for the fiscal years ending on or after December 15, 2007. The Dodd-Frank Act exempted non-accelerated filers from the requirements of SOX 404(b), the audit attestation submission.

Based on the start date of November 15, 2004, SOX 404 is presently in its sixth year of

application. As of the research date of this analysis, June 2, 2010, SOX Year 6 was not complete. Nevertheless, the SEC received a total of 3,356 auditor attestation opinions and 3,066 management-only opinions. As shown in the graph below, the adverse percentage rate for auditor attestations has decreased every year since SOX 404 began. The Year 1 rate of 16.9% dropped to 2.4% for the status of Year 6.

Even if one assumes that overdue filings will come in as adverse disclosures in the near future, SOX 404 Year 6 is expected to end with an adverse rate of about 2.8%. Likewise, a Year 6 analysis of companies that filed management-only reports found an improvement in the adverse percentage rate. So far in Year 6, adverse management-only reports were at 27.8% while the prior three years experienced the following adverse percentage rates: 32.3% in Year 5, 32.0% in Year 4, and 32.8% in Year 3. The Year 6 rate of 27.8% is the lowest rate to date, but nevertheless the rate is about 10 times higher than the rate experienced by

companies required to file auditor attestations.

The percentage of adverse Auditor Attestations has decreased every year since SOX 404 began.

As of June in SOX 404 Year 6, the percentage of adverse Auditor

Attestations was the lowest to date. Likewise, the percentage of adverse

Management-Only Assessments filed was the lowest, but this rate was

about 10 times higher than the rate experienced by companies required

to file Auditor Attestations.

Audit Analytics® October 2010

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508)476-7007 - [email protected] 2

Introduction

Both the Enron and Worldcom collapse culminated from a practice of disguising the true operating performance of the companies. In response these meltdowns, Congress passed the Sarbanes-Oxley Act of 2002 (“SOX”). In its title, the declared purpose of SOX is to “protect investors by improving the accuracy and reliability of corporate disclosures made pursuant to the securities laws, and for other purposes.” One section of SOX, Section 404 (“SOX 404”), furthers this goal by instructing the SEC to prescribe rules imposing a duty on officers and management to implement, review, and certify the effectiveness of a company’s internal controls for financial reporting (ICFRs).1 In addition, the registered public accountant is to attest to and report on the management’s assessment. In short, SOX 404(a) requires management to assess a company’s ICFRs while SOX 404(b) requires a registered public accountant to attest to the management’s report. SOX 404 Requirements History: The Staggered and Two-Tiered Implementation of SOX 404.

SOX 404, presently in its sixth year of application,2 began to apply to different categories of companies at different times. Moreover, as summarized in the table below, the two subsections of SOX 404, subsection 404(a) and 404(b), did not necessarily come into effect at the same time. United States accelerated filers3 were first required to provide SOX 404 certifications in annual reports for fiscal years ending on or after November 15, 2004. At that time both provisions were required: the management assessment (subsection 404(a)) and the auditor attestation (subsection 404(b)). During SOX 404’s third year of application, its provisions began to apply a new category of public registrant: accelerated foreign filers. For year 3, a large accelerated foreign filer was required to adhere to both provisions in its annual report for the fiscal year ending on or after July 15, 2006. However, an accelerated foreign filer that was not a large accelerated foreign filer was given a gradual two-tier requirement. That category of foreign filer was only required to provide a management opinion for July 15, 2006 and did not need to give an auditor attestation until the following year. In similar fashion, the SEC initially intended to apply a two-step approach to non-accelerated filers. Non-accelerated filers were required to provide a management opinion (but not an auditor attestation) in their annual reports for the fiscal years ending on or after December 15, 2007. Before subsection 404(b) became effective, however, the Dodd-Frank Act exempted the non-accelerated filers from the auditor attestation requirement.4 Therefore, except for asset backed securities and registered investment companies,5 all SEC registrants are required to provide at least a management report and accompanying certification6 in their annual reports unless the annual report is their very first (unless the registrant is a “newly public company”7).

1 In general, Section 404 requires that each annual report contain an “internal control report” that (1) acknowledges the management’s responsibility to maintain adequate internal controls, (2) identifies the “framework” used to evaluate the effectiveness of the internal controls over financial reporting, and (3) provides an assessment of the effectiveness of these internal controls as of the end of the fiscal year. 2 In this analysis, Year 6 (still ongoing) is defined as November 15, 2009 to November 14, 2010, inclusive. This 12-month period is consistent with the initial SEC requirement that United States accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. 3 An accelerated filer is a company whose public Float (as opposed to Market Capitalization) exceeds $75 million as of the last day of their second quarter. Once a registrant becomes an accelerated filer, it will not lose this status unless its float drops below $50 million. A large accelerated filer is a company whose public Float exceeds $700 million. See Rule 12b-2 of the Securities Exchange Act of 1934. 4 See Section 989G of the Dodd-Frank Wall Street Reform and Consumer Protection Act. 5 Registered investment companies are expressly exempt from Section 404 by Section 405 of SOX. 6 The SEC provides a form entitled “CERTIFICATIONS” to be attached to the annual report that contains the necessary language for a 404 certification. A separate copy of this form must be signed by both the CEO and CFO without any change in the language and attached as Exhibit 31. 7 Pursuant to the SEC instructions to Item 308 under regulation S-K, a registrant need not comply with SOX 404 “until it either had been required to file an annual report . . . for the prior fiscal year or had filed an annual report with the Commission for the prior fiscal year.” See also, SEC Release No. 33-8731 (Aug. 9, 2006).

Audit Analytics® October 2010

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508)476-7007 - [email protected] 3

Executive Summary – Year 6 Section 404 Update

For SOX 404 Year 6, as of June 2, 2010, the SEC had received a total of 3,356 auditor attestation opinions and 3,066 management-only opinions (6,422 total).8 The adverse auditor attestation disclosures filed represented 2.4% of the attestation filings. This figure is expected to increase to about 2.8%, assuming that overdue filings disclose adverse conditions. The 2.8% figure could further increase as some companies ascertain, mostly through financial restatements, that they erred in the original clean assessment. Nevertheless, this adverse figure of 2.8% is the lowest disclosed to date, down from 5.0% in year 5; 7.7% in year 4; 9.1% in year 3; 10.3% in Year 2 and 16.9% in Year 1. The management-only assessments also showed improvement. The adverse disclosures in the management-only assessments represented 27.8% of those filed. This is the first time the figure is below 30%, with the prior three years experiencing the following adverse percentage rates: 32.3% in year 5; 32.0% in year 4 and 32.8% in year 3.

1. As of June 2, 2010, the overall rate of adverse Year 6 auditor attestations has continued to declined.

In SOX 404 Year 1, when U.S. accelerated filers first provided auditor attestations (in their annual reports for fiscal years ending on or after November 15, 2004), the adverse disclosure rate came in at 16.9%. Thereafter, each year experienced a decline in the percentage of adverse auditor attestations. The Year 1 rate of 16.9% dropped to 10.3% in Year 2, to 9.1% in Year 3, to 7.7% in Year 4, to 5.0% in Year 5, and to 2.4% in Year 6. (See graph on right.) Even if one assumes that overdue filings will come in as adverse disclosures in the near future, Year 6 is expected to end with an adverse rate of about 2.8%. (See table on page 21: SOX 404 Auditor Attestations: Year 6 Update with Year 1, Year 2, Year 3, Year 4, and Year 5 Adverse Opinion Comparison.) This incremental drop from year to year suggests that the ICFRs of companies improve over time when auditors are involved in the evaluation process. The improvement over this time has been dramatic. 2. When management-only assessments are added to the population of SOX 404 filings, the adverse

percentage rate for Year 6 increases to 14.6%.

In Year 6, the SEC has received 3,066 annual reports with management-only assessments. Of those disclosures, 853 provided an adverse assessment regarding ICFRs, an adverse opinion rate of 27.8%. The high percentage indicates that non-accelerated filers fail to maintain ICFRs that are as reliable as accelerated filers. The high adverse percentage rate is due, in large part, to the fact that many non-accelerated filers are comprised of many small companies, including many 10KSB (small business) filers, with fewer employees and other resources. When this population is added to the 3,356 auditor attestation opinions, the adverse percentage of the total population of 6,422 disclosures becomes 14.6%. (See table on page 22: SOX 404 Disclosures including Management Only Reports: Year 6 Update with Year 1, Year 2, Year 3, Year 4, and Year 5 Adverse Opinion Comparison.) Although the adverse opinion rate for management-only assessments is high, the 27.8% figure is lower the three prior years. As shown in the table above, the prior three years experienced an adverse percentage rate of about 32%. (See also, table on page 22.)

8 The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing (to exclude duplicate material weakness filings by non-tickered subsidiaries).

Audit Analytics® October 2010

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508)476-7007 - [email protected] 4

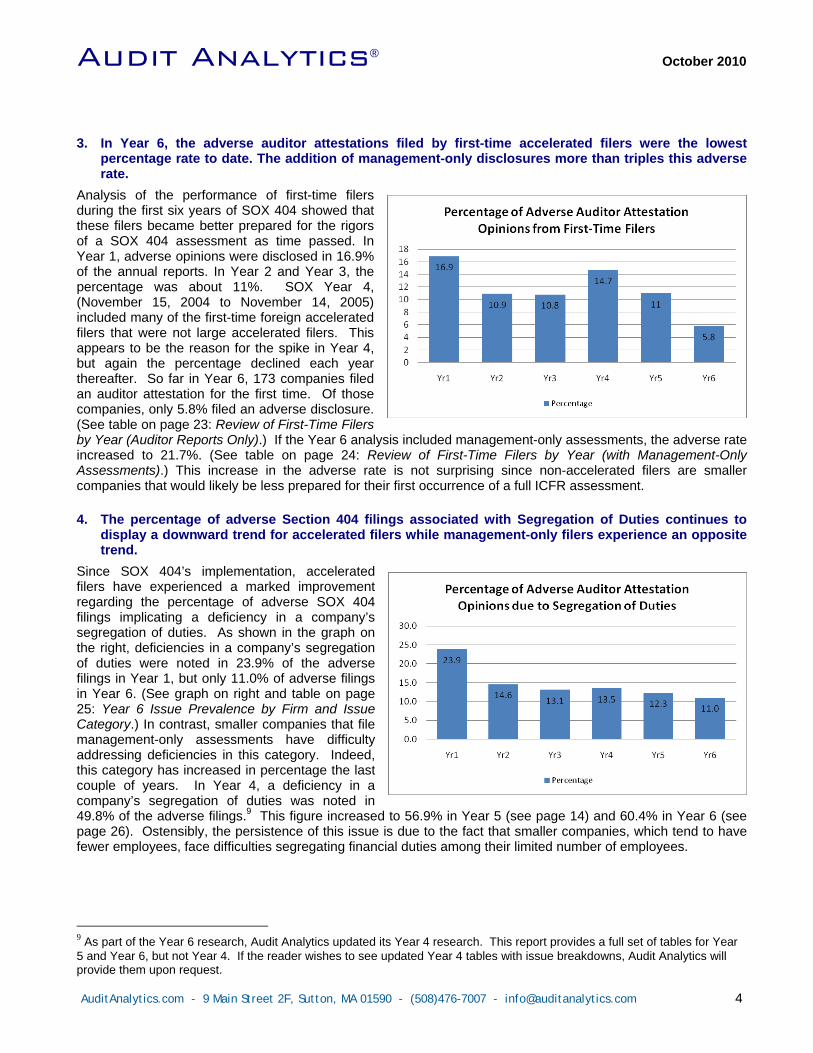

3. In Year 6, the adverse auditor attestations filed by first-time accelerated filers were the lowest

percentage rate to date. The addition of management-only disclosures more than triples this adverse rate.

Analysis of the performance of first-time filers during the first six years of SOX 404 showed that these filers became better prepared for the rigors of a SOX 404 assessment as time passed. In Year 1, adverse opinions were disclosed in 16.9% of the annual reports. In Year 2 and Year 3, the percentage was about 11%. SOX Year 4, (November 15, 2004 to November 14, 2005) included many of the first-time foreign accelerated filers that were not large accelerated filers. This appears to be the reason for the spike in Year 4, but again the percentage declined each year thereafter. So far in Year 6, 173 companies filed an auditor attestation for the first time. Of those companies, only 5.8% filed an adverse disclosure. (See table on page 23: Review of First-Time Filers by Year (Auditor Reports Only).) If the Year 6 analysis included management-only assessments, the adverse rate increased to 21.7%. (See table on page 24: Review of First-Time Filers by Year (with Management-Only Assessments).) This increase in the adverse rate is not surprising since non-accelerated filers are smaller companies that would likely be less prepared for their first occurrence of a full ICFR assessment. 4. The percentage of adverse Section 404 filings associated with Segregation of Duties continues to

display a downward trend for accelerated filers while management-only filers experience an opposite trend.

Since SOX 404’s implementation, accelerated filers have experienced a marked improvement regarding the percentage of adverse SOX 404 filings implicating a deficiency in a company’s segregation of duties. As shown in the graph on the right, deficiencies in a company’s segregation of duties were noted in 23.9% of the adverse filings in Year 1, but only 11.0% of adverse filings in Year 6. (See graph on right and table on page 25: Year 6 Issue Prevalence by Firm and Issue Category.) In contrast, smaller companies that file management-only assessments have difficulty addressing deficiencies in this category. Indeed, this category has increased in percentage the last couple of years. In Year 4, a deficiency in a company’s segregation of duties was noted in 49.8% of the adverse filings.9 This figure increased to 56.9% in Year 5 (see page 14) and 60.4% in Year 6 (see page 26). Ostensibly, the persistence of this issue is due to the fact that smaller companies, which tend to have fewer employees, face difficulties segregating financial duties among their limited number of employees. 9 As part of the Year 6 research, Audit Analytics updated its Year 4 research. This report provides a full set of tables for Year 5 and Year 6, but not Year 4. If the reader wishes to see updated Year 4 tables with issue breakdowns, Audit Analytics will provide them upon request.

Audit Analytics® October 2010

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508)476-7007 - [email protected] 5

5. The percentage of adverse auditor attestations implicating Depreciation/Amortization has steadily decreased since SOX Year 1.

In Year 1 of SOX 404, accelerated filers disclosed a deficiency in their accounting of Depreciation and/or Amortization in 12.5% of their adverse filings. (See graph on right.) This percentage dropped dramatically the next year to 6.7% and continued to decline each year thereafter. So far in Year 6, 2.4% of adverse SOX 404 filings implicated Depreciation and/or Amortization issues. The high percentage in Year 1 is likely due to the letter dated February 7, 2005 from SEC chief accountant Donald Nicolaise to the AICPA.10 The SEC letter provided lease accounting clarification on (1) the amortization of lessor improvements, (2) rent holidays, and (3) landlord construction incentives. This clarification appears to have caused a high percentage of adverse 404 disclosures. Since Year 1, companies have steadily improved their accounting procedures in this area. 6. During SOX Year 5, the top-three accounting issues identified by the clients of each of the Big-4

accounting firms fall within seven taxonomy categories.

The last SOX 404 report published by Audit Analytics provided an update for SOX Year 4 disclosures.11 As a result, Audit Analytics attached a Year 5 set of tables to the appendix of this report in addition to the Year 6 tables. The table on page 17 of this report lists 22 accounting issues that can be disclosed in an adverse SOX 404 assessment. (See table on page 17: SOX 404 Disclosures: Year 5 Issue Update; GAAP Financial Issues in Adverse Disclosures.) A review of the clients of the Big-4 accounting firms found that the total number of adverse disclosures filed by clients of Ernst & Young, PricewaterhouseCoopers, KPMG, and Deloitte & Touche totaled 40, 23, 30 and 31, respectively. All these adverse disclosures identified over 20 taxonomy issues, but a review of each client grouping by auditor revealed that the top-three issues of each group all fell within a list of only seven taxonomy issues.12 The table below groups the SOX Year 5, Big-4 clients by their auditor and provides the percentage of occurrence for the top-three issues for each group. If there was a tie in the third-place ranking, all issues with the third-place percentage are shown. As shown below, all four client groupings have the same two taxonomy issues in their top-three list: (1) Revenue Recognition Issues and (2) Tax Expense/Benefit/Deferral/ Other (FAS 109) Issues.

Percentage of Occurrence of the Top-Three Accounting Issues in SOX 404 Year 5 As Identified by Companies Filing Auditor Attestations from Big-4 Audit Firms

(Companies Grouped by Auditor) 10 A group of restatements caused the AICPA to request a clarification from the SEC and the letter followed. 11 See Audit Analytics, 404 Dashboard, Year 4 Update, December 2008. 12 The top-three issue does not include the broad category, Unspecified/Unidentified/Inapplicable FASB/GAAP Issues.

Audit Analytics® October 2010

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508)476-7007 - [email protected] 6

7. During SOX Year 6, the top-three accounting issues identified by the clients of each of the Big-4

accounting firms fall within eight taxonomy categories.

Similar to the Year 5 analysis above, Audit Analytics reviewed SOX 404 Year 6 to identify the top-three issues. The total number of adverse disclosures filed by clients of Ernst & Young, PricewaterhouseCoopers, KPMG, and Deloitte & Touche totaled 12, 17, 10 and 16, respectively. (See table on page 30: SOX 404 Disclosures: Year 6 Issue Update; GAAP Financial Issues in Adverse Disclosures.) All these adverse disclosures identified 18 taxonomy issues, but the top-three issues of each client group all fell within a list of only eight taxonomy issues. The table below groups the SOX Year 6, Big-4 clients by their auditor and provides the percentage of occurrence for the top-three issues for each group. If there was a tie in the third-place ranking, all issues with the third-place percentage are shown. Unlike Year 5, no single issue appeared as a top-three category for all four client groupings. While one issue disappeared from the top-three list (Deferred, Stock-Based or Executive Compensation Issues), two new categories emerged: (1) Debt, Quasi-Debt, Warrants & Equity ( BCF) Security Issues and (2) Foreign, Related Party, Affiliated and/or Subsidiary Entity Issues) Issues.

Percentage of Occurrence of the Top-Three Accounting Issues in SOX 404 Year 6 As Identified by Companies Filing Auditor Attestations from Big-4 Audit Firms

(Companies Grouped by Auditor) 8. During SOX Year 5 and Year 6, the top-two internal control issues identified by the clients of each of

the Big-4 accounting firms were the same for both years.

The tables on page 14 and page 27 list sixteen internal control issues and quantify how often these issues were disclosed in adverse SOX 404 filings. A review of Year 5 and Year 6 that focused on Big-4 client groupings found that the same two issues ranked in the top of the list for both years: (1) Accounting Personnel Resources, Competency/Training and (2) Material and/or Numerous Auditor /YE Adjustments. Although the percentage of adverse auditor attestations has decreased every year since SOX Year 1, the adverse attestations that were filed commonly disclosed personnel resources and/or competency as an issue of concern. As shown in the graph on the right, in recent years larger companies that filed adverse SOX 404 disclosures more often than not had personnel issues as at least one of their internal control weaknesses. (See table on page 25: Year 6 Issue Prevalence by Firm and Issue Category.)

Audit Analytics® October 2010

AuditAnalytics.com ● 9 Main Street, Sutton 2F, MA 01590 ● (508) 476-7007 ● [email protected] Page 7

SOX 404 Year 5 Tables

Audit Analytics®October 2010

SOX 404Year 4

SOX 404Year 3

SOX 404Year 2

SOX 404Year 1

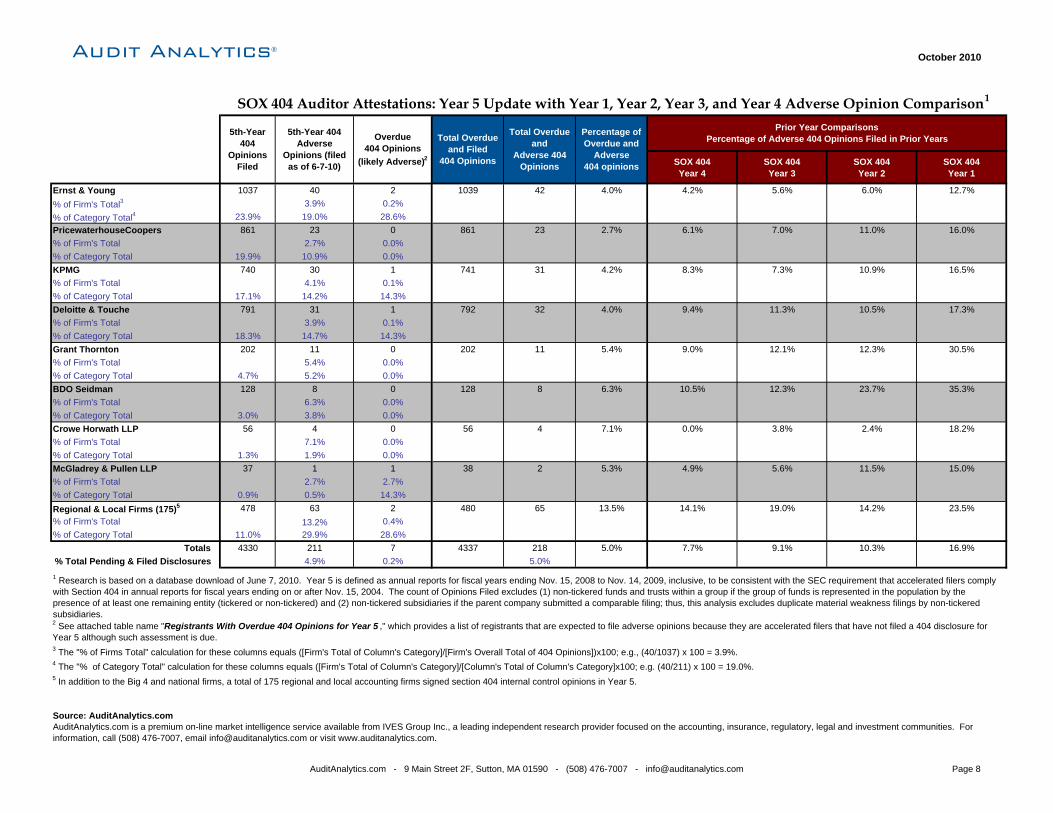

Ernst & Young 1037 40 2 1039 42 4.0% 4.2% 5.6% 6.0% 12.7%% of Firm's Total3 3.9% 0.2%% of Category Total4 23.9% 19.0% 28.6%PricewaterhouseCoopers 861 23 0 861 23 2.7% 6.1% 7.0% 11.0% 16.0%% of Firm's Total 2.7% 0.0%% of Category Total 19.9% 10.9% 0.0%KPMG 740 30 1 741 31 4.2% 8.3% 7.3% 10.9% 16.5%% of Firm's Total 4.1% 0.1%% of Category Total 17.1% 14.2% 14.3%Deloitte & Touche 791 31 1 792 32 4.0% 9.4% 11.3% 10.5% 17.3%% of Firm's Total 3.9% 0.1%% of Category Total 18.3% 14.7% 14.3%Grant Thornton 202 11 0 202 11 5.4% 9.0% 12.1% 12.3% 30.5%% of Firm's Total 5.4% 0.0%% of Category Total 4.7% 5.2% 0.0%BDO Seidman 128 8 0 128 8 6.3% 10.5% 12.3% 23.7% 35.3%% of Firm's Total 6.3% 0.0%% of Category Total 3.0% 3.8% 0.0%Crowe Horwath LLP 56 4 0 56 4 7.1% 0.0% 3.8% 2.4% 18.2%% of Firm's Total 7.1% 0.0%% of Category Total 1.3% 1.9% 0.0%McGladrey & Pullen LLP 37 1 1 38 2 5.3% 4.9% 5.6% 11.5% 15.0%% of Firm's Total 2.7% 2.7%% of Category Total 0.9% 0.5% 14.3%Regional & Local Firms (175)5 478 63 2 480 65 13.5% 14.1% 19.0% 14.2% 23.5%% of Firm's Total 13.2% 0.4%% of Category Total 11.0% 29.9% 28.6%

Totals 4330 211 7 4337 218 5.0% 7.7% 9.1% 10.3% 16.9%% Total Pending & Filed Disclosures 4.9% 0.2% 5.0%

Source: AuditAnalytics.com

Percentage ofOverdue and

Adverse404 opinions

Prior Year ComparisonsPercentage of Adverse 404 Opinions Filed in Prior Years

SOX 404 Auditor Attestations: Year 5 Update with Year 1, Year 2, Year 3, and Year 4 Adverse Opinion Comparison1

4 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column's Total of Column's Category]x100; e.g. (40/211) x 100 = 19.0%.

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 See attached table name "Registrants With Overdue 404 Opinions for Year 5 ," which provides a list of registrants that are expected to file adverse opinions because they are accelerated filers that have not filed a 404 disclosure for Year 5 although such assessment is due. 3 The "% of Firms Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions])x100; e.g., (40/1037) x 100 = 3.9%.

5 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.

5th-Year404

OpinionsFiled

5th-Year 404 Adverse

Opinions (filed as of 6-7-10)

Overdue404 Opinions

(likely Adverse)2

Total Overdueand Filed

404 Opinions

Total Overdueand

Adverse 404Opinions

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508) 476-7007 - [email protected] Page 8

Audit Analytics®October 2010

SOX 404Year 4

SOX 404Year 3

SOX 404Year 2

SOX 404Year 1

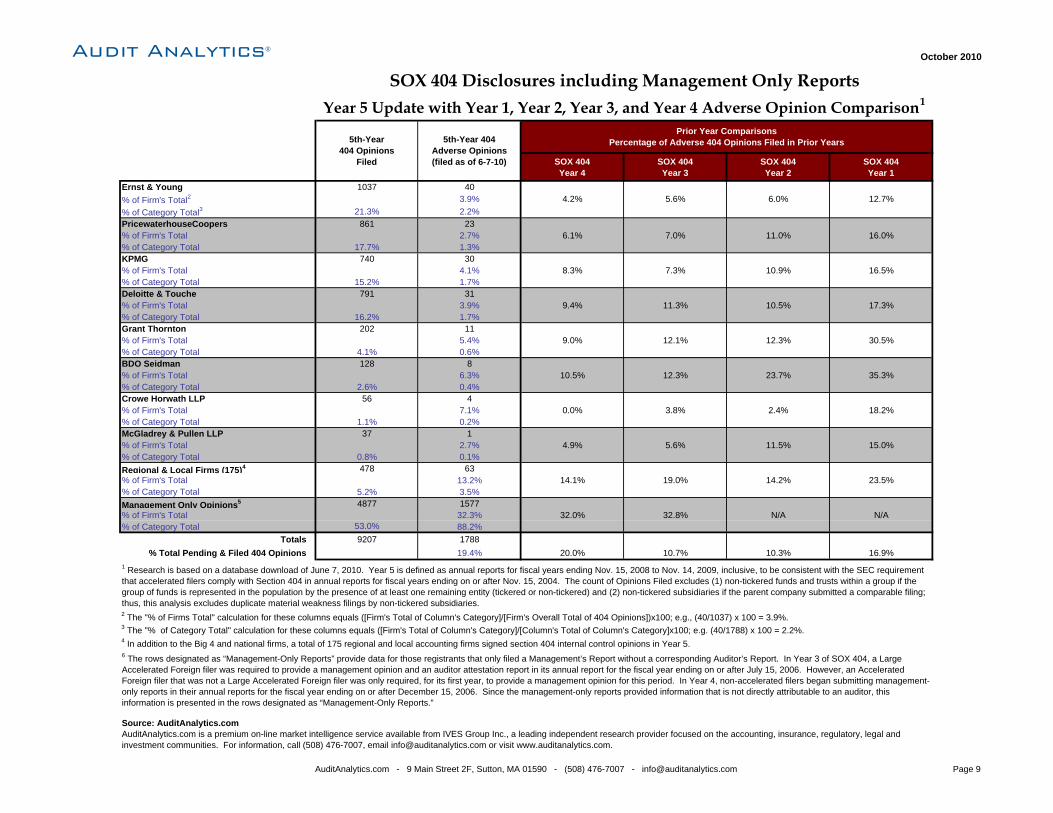

Ernst & Young 1037 40% of Firm's Total2 3.9% 4.2% 5.6% 6.0% 12.7%% of Category Total3 21.3% 2.2%PricewaterhouseCoopers 861 23% of Firm's Total 2.7% 6.1% 7.0% 11.0% 16.0%% of Category Total 17.7% 1.3%KPMG 740 30% of Firm's Total 4.1% 8.3% 7.3% 10.9% 16.5%% of Category Total 15.2% 1.7%Deloitte & Touche 791 31% of Firm's Total 3.9% 9.4% 11.3% 10.5% 17.3%% of Category Total 16.2% 1.7%Grant Thornton 202 11% of Firm's Total 5.4% 9.0% 12.1% 12.3% 30.5%% of Category Total 4.1% 0.6%BDO Seidman 128 8% of Firm's Total 6.3% 10.5% 12.3% 23.7% 35.3%% of Category Total 2.6% 0.4%Crowe Horwath LLP 56 4% of Firm's Total 7.1% 0.0% 3.8% 2.4% 18.2%% of Category Total 1.1% 0.2%McGladrey & Pullen LLP 37 1% of Firm's Total 2.7% 4.9% 5.6% 11.5% 15.0%% of Category Total 0.8% 0.1%Regional & Local Firms (175)4 478 63% of Firm's Total 13.2% 14.1% 19.0% 14.2% 23.5%% of Category Total 5.2% 3.5%Management Only Opinions5 4877 1577% of Firm's Total 32.3% 32.0% 32.8% N/A N/A% of Category Total 53.0% 88.2%

Totals 9207 1788% Total Pending & Filed 404 Opinions 19.4% 20.0% 10.7% 10.3% 16.9%

Source: AuditAnalytics.com

SOX 404 Disclosures including Management Only ReportsYear 5 Update with Year 1, Year 2, Year 3, and Year 4 Adverse Opinion Comparison1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries.2 The "% of Firms Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions])x100; e.g., (40/1037) x 100 = 3.9%.3 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column's Total of Column's Category]x100; e.g. (40/1788) x 100 = 2.2%.

5th-Year404 Opinions

Filed

5th-Year 404Adverse Opinions(filed as of 6-7-10)

Prior Year ComparisonsPercentage of Adverse 404 Opinions Filed in Prior Years

4 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.6 The rows designated as “Management-Only Reports” provide data for those registrants that only filed a Management’s Report without a corresponding Auditor’s Report. In Year 3 of SOX 404, a Large Accelerated Foreign filer was required to provide a management opinion and an auditor attestation report in its annual report for the fiscal year ending on or after July 15, 2006. However, an Accelerated Foreign filer that was not a Large Accelerated Foreign filer was only required, for its first year, to provide a management opinion for this period. In Year 4, non-accelerated filers began submitting management-only reports in their annual reports for the fiscal year ending on or after December 15, 2006. Since the management-only reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as “Management-Only Reports.”

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508) 476-7007 - [email protected] Page 9

Audit Analytics® October 2010

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

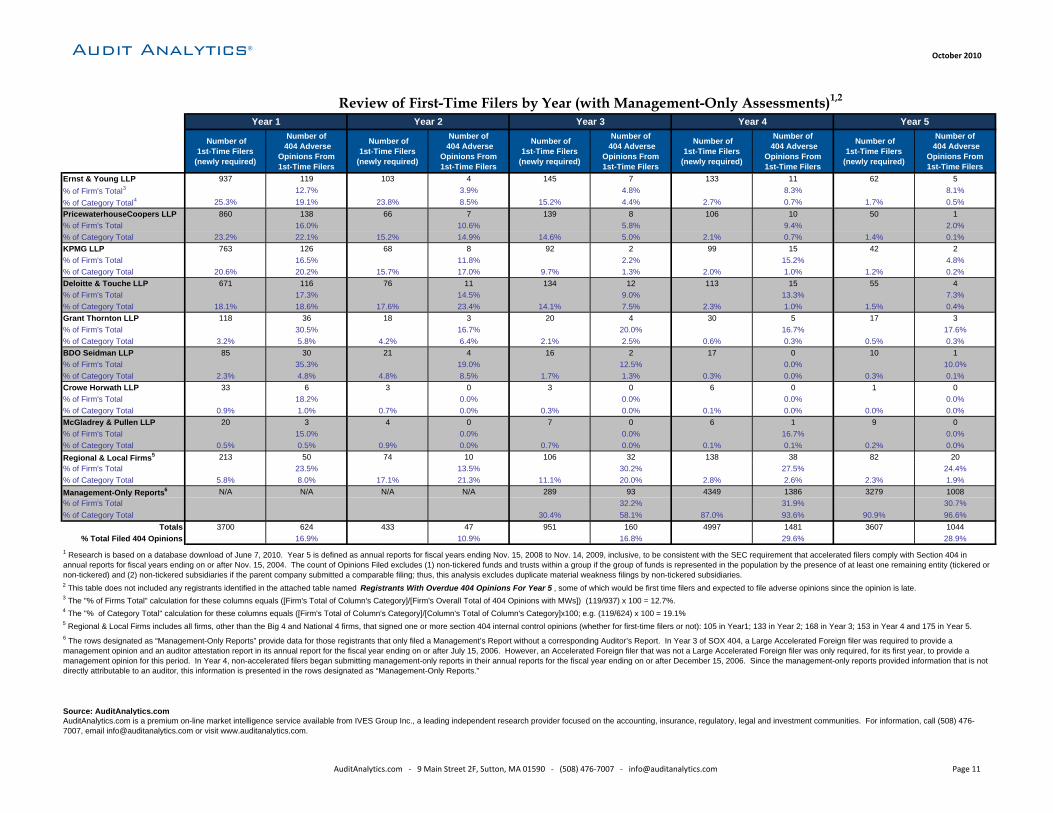

Ernst & Young LLP 937 119 103 4 149 7 133 11 62 5% of Firm's Total4 12.7% 3.9% 4.7% 8.3% 8.1%% of Category Total5 25.3% 19.1% 23.8% 8.5% 21.1% 9.2% 20.5% 11.6% 18.9% 13.9%PricewaterhouseCoopers LLP 860 138 66 7 150 10 106 10 50 1% of Firm's Total 16.0% 10.6% 6.7% 9.4% 2.0%% of Category Total 23.2% 22.1% 15.2% 14.9% 21.2% 13.2% 16.4% 10.5% 15.2% 2.8%KPMG LLP 763 126 68 8 102 3 99 15 42 2% of Firm's Total 16.5% 11.8% 2.9% 15.2% 4.8%% of Category Total 20.6% 20.2% 15.7% 17.0% 14.4% 3.9% 15.3% 15.8% 12.8% 5.6%Deloitte & Touche LLP 671 116 76 11 134 12 113 15 55 4% of Firm's Total 17.3% 14.5% 9.0% 13.3% 7.3%% of Category Total 18.1% 18.6% 17.6% 23.4% 19.0% 15.8% 17.4% 15.8% 16.8% 11.1%Grant Thornton LLP 118 36 18 3 23 4 30 5 17 3% of Firm's Total 30.5% 16.7% 17.4% 16.7% 17.6%% of Category Total 3.2% 5.8% 4.2% 6.4% 3.3% 5.3% 4.6% 5.3% 5.2% 8.3%BDO Seidman LLP 85 30 21 4 18 4 17 0 10 1% of Firm's Total 35.3% 19.0% 22.2% 0.0% 10.0%% of Category Total 2.3% 4.8% 4.8% 8.5% 2.5% 5.3% 2.6% 0.0% 3.0% 2.8%Crowe Horwath LLP 33 6 3 0 3 0 6 0 1 0% of Firm's Total 18.2% 0.0% 0.0% 0.0% 0.0%% of Category Total 0.9% 1.0% 0.7% 0.0% 0.4% 0.0% 0.9% 0.0% 0.3% 0.0%McGladrey & Pullen LLP 20 3 4 0 8 0 6 1 9 0% of Firm's Total 15.0% 0.0% 0.0% 16.7% 0.0%% of Category Total 0.5% 0.5% 0.9% 0.0% 1.1% 0.0% 0.9% 1.1% 2.7% 0.0%Regional & Local Firms6 213 50 74 10 119 36 138 38 82 20% of Firm's Total 23.5% 13.5% 30.3% 27.5% 24.4%% of Category Total 5.8% 8.0% 17.1% 21.3% 16.9% 47.4% 21.3% 40.0% 25.0% 55.6%

Totals 3700 624 433 47 706 76 648 95 328 36 % Total Filed 404 Opinions 16.9% 10.9% 10.8% 14.7% 11.0%

Source: AuditAnalytics.com AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries.

3 This table does not include any registrants identified in the attached table named Registrants With Overdue 404 Opinions For Year 5 , some of which would be first time filers and expected to file adverse opinions since the opinion is late.4 The "% of Firms Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) (119/937) x 100 = 12.7%.

6 Regional & Local Firms includes all firms, other than the Big 4 and National 4 firms, that signed one or more section 404 internal control opinions (whether for first-time filers or not): 105 in Year1; 133 in Year 2; 168 in Year 3; 153 in Year 4 and 175 in Year 5.

2 The table above does not list the data regarding Management-Only opinions. To view this data incoporated into the table, see table on next page: Review of First-Time Filers by Year (with Management-Only Assessments) .

Year 1 Year 2 Year 5

Review of First-Time Filers by Year (Auditor Reports Only)1, 2, 3

5 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column's Total of Column's Category]) x 100; e.g. (119/624) x 100 = 19.1%

Year 3 Year 4

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508) 476-7007 - [email protected] Page 10

Audit Analytics®October 2010

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Number of1st-Time Filers

(newly required)

Number of 404 Adverse

Opinions From1st-Time Filers

Ernst & Young LLP 937 119 103 4 145 7 133 11 62 5% of Firm's Total3 12.7% 3.9% 4.8% 8.3% 8.1%% of Category Total4 25.3% 19.1% 23.8% 8.5% 15.2% 4.4% 2.7% 0.7% 1.7% 0.5%PricewaterhouseCoopers LLP 860 138 66 7 139 8 106 10 50 1% of Firm's Total 16.0% 10.6% 5.8% 9.4% 2.0%% of Category Total 23.2% 22.1% 15.2% 14.9% 14.6% 5.0% 2.1% 0.7% 1.4% 0.1%KPMG LLP 763 126 68 8 92 2 99 15 42 2% of Firm's Total 16.5% 11.8% 2.2% 15.2% 4.8%% of Category Total 20.6% 20.2% 15.7% 17.0% 9.7% 1.3% 2.0% 1.0% 1.2% 0.2%Deloitte & Touche LLP 671 116 76 11 134 12 113 15 55 4% of Firm's Total 17.3% 14.5% 9.0% 13.3% 7.3%% of Category Total 18.1% 18.6% 17.6% 23.4% 14.1% 7.5% 2.3% 1.0% 1.5% 0.4%Grant Thornton LLP 118 36 18 3 20 4 30 5 17 3% of Firm's Total 30.5% 16.7% 20.0% 16.7% 17.6%% of Category Total 3.2% 5.8% 4.2% 6.4% 2.1% 2.5% 0.6% 0.3% 0.5% 0.3%BDO Seidman LLP 85 30 21 4 16 2 17 0 10 1% of Firm's Total 35.3% 19.0% 12.5% 0.0% 10.0%% of Category Total 2.3% 4.8% 4.8% 8.5% 1.7% 1.3% 0.3% 0.0% 0.3% 0.1%Crowe Horwath LLP 33 6 3 0 3 0 6 0 1 0% of Firm's Total 18.2% 0.0% 0.0% 0.0% 0.0%% of Category Total 0.9% 1.0% 0.7% 0.0% 0.3% 0.0% 0.1% 0.0% 0.0% 0.0%McGladrey & Pullen LLP 20 3 4 0 7 0 6 1 9 0% of Firm's Total 15.0% 0.0% 0.0% 16.7% 0.0%% of Category Total 0.5% 0.5% 0.9% 0.0% 0.7% 0.0% 0.1% 0.1% 0.2% 0.0%Regional & Local Firms5 213 50 74 10 106 32 138 38 82 20% of Firm's Total 23.5% 13.5% 30.2% 27.5% 24.4%% of Category Total 5.8% 8.0% 17.1% 21.3% 11.1% 20.0% 2.8% 2.6% 2.3% 1.9%Management-Only Reports6 N/A N/A N/A N/A 289 93 4349 1386 3279 1008% of Firm's Total 32.2% 31.9% 30.7%% of Category Total 30.4% 58.1% 87.0% 93.6% 90.9% 96.6%

Totals 3700 624 433 47 951 160 4997 1481 3607 1044 % Total Filed 404 Opinions 16.9% 10.9% 16.8% 29.6% 28.9%

Source: AuditAnalytics.com

Year 1 Year 2 Year 5

Review of First-Time Filers by Year (with Management-Only Assessments)1,2

4 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column's Total of Column's Category]x100; e.g. (119/624) x 100 = 19.1%

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 This table does not included any registrants identified in the attached table named Registrants With Overdue 404 Opinions For Year 5 , some of which would be first time filers and expected to file adverse opinions since the opinion is late.3 The "% of Firms Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) (119/937) x 100 = 12.7%.

5 Regional & Local Firms includes all firms, other than the Big 4 and National 4 firms, that signed one or more section 404 internal control opinions (whether for first-time filers or not): 105 in Year1; 133 in Year 2; 168 in Year 3; 153 in Year 4 and 175 in Year 5.

Year 3

6 The rows designated as “Management-Only Reports” provide data for those registrants that only filed a Management’s Report without a corresponding Auditor’s Report. In Year 3 of SOX 404, a Large Accelerated Foreign filer was required to provide a management opinion and an auditor attestation report in its annual report for the fiscal year ending on or after July 15, 2006. However, an Accelerated Foreign filer that was not a Large Accelerated Foreign filer was only required, for its first year, to provide a management opinion for this period. In Year 4, non-accelerated filers began submitting management-only reports in their annual reports for the fiscal year ending on or after December 15, 2006. Since the management-only reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as “Management-Only Reports.”

Year 4

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 11

Audit Analytics® October 2010

Fifth Year 404 Opinions Filed

Fifth Year 404 Opinions with Material Weaknesses

Personnel Issues

Segregation of Duties

Restatements of Financials

Material YE Adjustments

Internal Audit Issues

IT Processing, Access Issues

Ernst & Young 1037 40 24 4 16 26 2 8% of Firm's Total2 3.9% 60.0% 10.0% 40.0% 65.0% 5.0% 20.0%% of Category Total3 23.9% 19.0% 19.4% 15.4% 30.8% 18.8% 16.7% 13.8%PricewaterhouseCoopers 861 23 14 0 9 12 1 5% of Firm's Total 2.7% 60.9% 0.0% 39.1% 52.2% 4.3% 21.7%% of Category Total 19.9% 10.9% 11.3% 0.0% 17.3% 8.7% 8.3% 8.6%KPMG 740 30 22 2 7 23 1 8% of Firm's Total 4.1% 73.3% 6.7% 23.3% 76.7% 3.3% 26.7%% of Category Total 17.1% 14.2% 17.7% 7.7% 13.5% 16.7% 8.3% 13.8%Deloitte & Touche 791 31 15 3 10 18 1 11% of Firm's Total 3.9% 48.4% 9.7% 32.3% 58.1% 3.2% 35.5%% of Category Total 18.3% 14.7% 12.1% 11.5% 19.2% 13.0% 8.3% 19.0%Grant Thornton 202 11 5 1 2 6 0 5% of Firm's Total 5.4% 45.5% 9.1% 18.2% 54.5% 0% 45.5%% of Category Total 4.7% 5.2% 4.0% 3.8% 3.8% 4.3% 0% 8.6%BDO Seidman 128 8 5 3 1 7 1 4% of Firm's Total 6.3% 62.5% 37.5% 12.5% 87.5% 12.5% 50.0%% of Category Total 3.0% 3.8% 4.0% 11.5% 1.9% 5.1% 8.3% 6.9%Crowe 56 4 0 0 0 3 0 0% of Firm's Total 7.1% 0.0% 0.0% 0.0% 75.0% 0.0% 0.0%% of Category Total 1.3% 1.9% 0.0% 0.0% 0.0% 2.2% 0.0% 0.0%McGladrey & Pullen LLP 37 1 1 0 0 1 0 0% of Firm's Total 2.7% 100.0% 0.0% 0.0% 100.0% 0.0% 0.0%% of Category Total 0.9% 0.5% 0.8% 0.0% 0.0% 0.7% 0.0% 0.0%Regional & Local Firms (175 firms) 478 63 38 13 7 42 6 17% of Firm's Total 13.2% 60.3% 20.6% 11.1% 66.7% 9.5% 27.0%% of Category Total 11.0% 29.9% 30.6% 50.0% 13.5% 30.4% 50.0% 29.3%Totals 4330 211 124 26 52 138 12 58% Total of 404 Opinions 4.9% 58.8% 12.3% 24.6% 65.4% 5.7% 27.5%

Year 4 Comparison 4496 347 226 47 77 233 12 907.7% 65.1% 13.5% 22.2% 67.1% 3.5% 25.9%

Year 3 Comparison 4216 382 179 50 126 260 14 749.1% 46.9% 13.1% 33.0% 68.1% 3.7% 19.4%

Year 2 Comparison 3791 390 207 57 177 250 4 7910.3% 53.1% 14.6% 45.4% 64.1% 1.0% 20.3%

Year 1 Comparison 3700 624 304 149 324 335 17 13516.9% 48.7% 23.9% 51.9% 53.7% 2.7% 21.6%

Source: AuditAnalytics.com AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc. a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

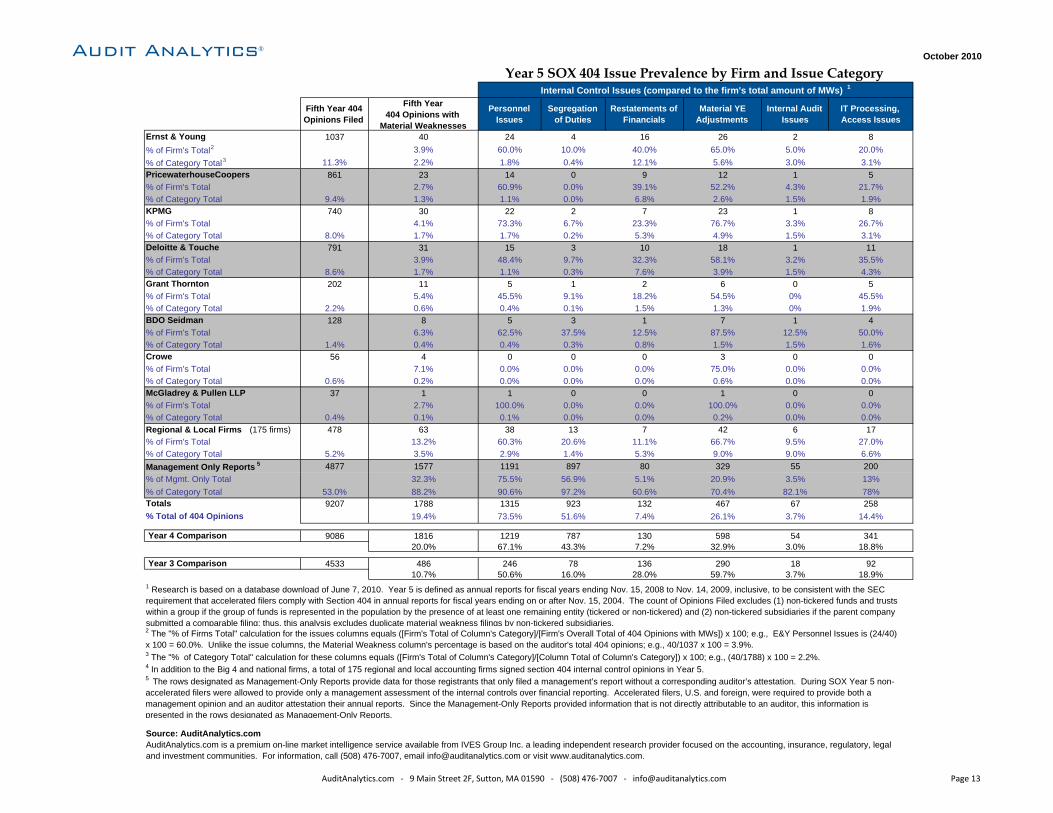

Year 5 SOX 404 Issue Prevalence by Firm and Issue CategoryInternal Control Issues (compared to the firm's total amount of MWs) 1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 The "% of Firms Total" calculation for the issues columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) x 100; e.g., E&Y Personnel Issues is (24/40) x 100 = 60.0%. Unlike the issue columns, the Material Weakness column's percentage is based on the auditor's total 404 opinions; e.g., 40/1037 x 100 = 3.9%.3 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column Total of Column's Category]) x 100; e.g., (40/211) x 100 = 19.0%.4 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 12

Audit Analytics®October 2010

Fifth Year 404 Opinions Filed

Fifth Year 404 Opinions with

Material Weaknesses

Personnel Issues

Segregation of Duties

Restatements of Financials

Material YE Adjustments

Internal Audit Issues

IT Processing, Access Issues

Ernst & Young 1037 40 24 4 16 26 2 8% of Firm's Total2 3.9% 60.0% 10.0% 40.0% 65.0% 5.0% 20.0%% of Category Total3 11.3% 2.2% 1.8% 0.4% 12.1% 5.6% 3.0% 3.1%PricewaterhouseCoopers 861 23 14 0 9 12 1 5% of Firm's Total 2.7% 60.9% 0.0% 39.1% 52.2% 4.3% 21.7%% of Category Total 9.4% 1.3% 1.1% 0.0% 6.8% 2.6% 1.5% 1.9%KPMG 740 30 22 2 7 23 1 8% of Firm's Total 4.1% 73.3% 6.7% 23.3% 76.7% 3.3% 26.7%% of Category Total 8.0% 1.7% 1.7% 0.2% 5.3% 4.9% 1.5% 3.1%Deloitte & Touche 791 31 15 3 10 18 1 11% of Firm's Total 3.9% 48.4% 9.7% 32.3% 58.1% 3.2% 35.5%% of Category Total 8.6% 1.7% 1.1% 0.3% 7.6% 3.9% 1.5% 4.3%Grant Thornton 202 11 5 1 2 6 0 5% of Firm's Total 5.4% 45.5% 9.1% 18.2% 54.5% 0% 45.5%% of Category Total 2.2% 0.6% 0.4% 0.1% 1.5% 1.3% 0% 1.9%BDO Seidman 128 8 5 3 1 7 1 4% of Firm's Total 6.3% 62.5% 37.5% 12.5% 87.5% 12.5% 50.0%% of Category Total 1.4% 0.4% 0.4% 0.3% 0.8% 1.5% 1.5% 1.6%Crowe 56 4 0 0 0 3 0 0% of Firm's Total 7.1% 0.0% 0.0% 0.0% 75.0% 0.0% 0.0%% of Category Total 0.6% 0.2% 0.0% 0.0% 0.0% 0.6% 0.0% 0.0%McGladrey & Pullen LLP 37 1 1 0 0 1 0 0% of Firm's Total 2.7% 100.0% 0.0% 0.0% 100.0% 0.0% 0.0%% of Category Total 0.4% 0.1% 0.1% 0.0% 0.0% 0.2% 0.0% 0.0%Regional & Local Firms (175 firms) 478 63 38 13 7 42 6 17% of Firm's Total 13.2% 60.3% 20.6% 11.1% 66.7% 9.5% 27.0%% of Category Total 5.2% 3.5% 2.9% 1.4% 5.3% 9.0% 9.0% 6.6%Management Only Reports 5 4877 1577 1191 897 80 329 55 200% of Mgmt. Only Total 32.3% 75.5% 56.9% 5.1% 20.9% 3.5% 13%% of Category Total 53.0% 88.2% 90.6% 97.2% 60.6% 70.4% 82.1% 78%Totals 9207 1788 1315 923 132 467 67 258% Total of 404 Opinions 19.4% 73.5% 51.6% 7.4% 26.1% 3.7% 14.4%

Year 4 Comparison 9086 1816 1219 787 130 598 54 34120.0% 67.1% 43.3% 7.2% 32.9% 3.0% 18.8%

Year 3 Comparison 4533 486 246 78 136 290 18 9210.7% 50.6% 16.0% 28.0% 59.7% 3.7% 18.9%

Source: AuditAnalytics.com

5 The rows designated as Management-Only Reports provide data for those registrants that only filed a management’s report without a corresponding auditor’s attestation. During SOX Year 5 non-accelerated filers were allowed to provide only a management assessment of the internal controls over financial reporting. Accelerated filers, U.S. and foreign, were required to provide both a management opinion and an auditor attestation their annual reports. Since the Management-Only Reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as Management-Only Reports.

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc. a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

Year 5 SOX 404 Issue Prevalence by Firm and Issue CategoryInternal Control Issues (compared to the firm's total amount of MWs) 1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 The "% of Firms Total" calculation for the issues columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) x 100; e.g., E&Y Personnel Issues is (24/40) x 100 = 60.0%. Unlike the issue columns, the Material Weakness column's percentage is based on the auditor's total 404 opinions; e.g., 40/1037 x 100 = 3.9%.3 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column Total of Column's Category]) x 100; e.g., (40/1788) x 100 = 2.2%.4 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 13

Audit Analytics®October 2010

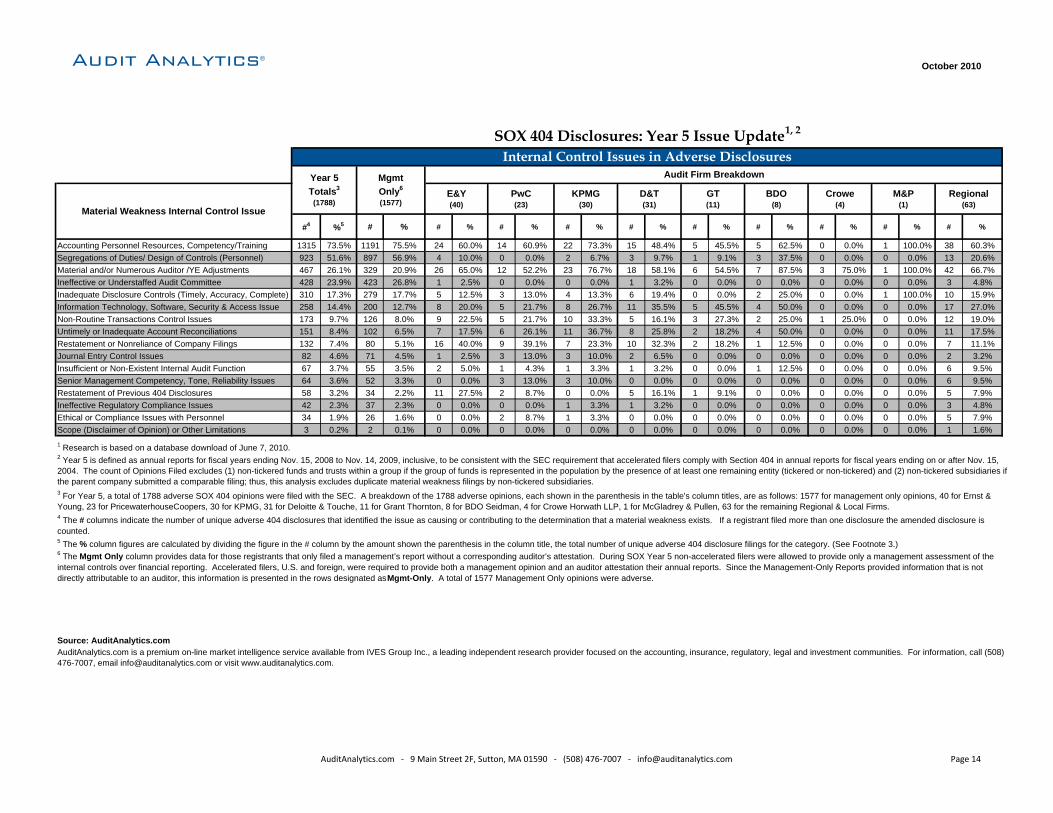

#4 %5 # % # % # % # % # % # % # % # % # % # %

Accounting Personnel Resources, Competency/Training 1315 73.5% 1191 75.5% 24 60.0% 14 60.9% 22 73.3% 15 48.4% 5 45.5% 5 62.5% 0 0.0% 1 100.0% 38 60.3%Segregations of Duties/ Design of Controls (Personnel) 923 51.6% 897 56.9% 4 10.0% 0 0.0% 2 6.7% 3 9.7% 1 9.1% 3 37.5% 0 0.0% 0 0.0% 13 20.6%Material and/or Numerous Auditor /YE Adjustments 467 26.1% 329 20.9% 26 65.0% 12 52.2% 23 76.7% 18 58.1% 6 54.5% 7 87.5% 3 75.0% 1 100.0% 42 66.7%Ineffective or Understaffed Audit Committee 428 23.9% 423 26.8% 1 2.5% 0 0.0% 0 0.0% 1 3.2% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 3 4.8%Inadequate Disclosure Controls (Timely, Accuracy, Complete) 310 17.3% 279 17.7% 5 12.5% 3 13.0% 4 13.3% 6 19.4% 0 0.0% 2 25.0% 0 0.0% 1 100.0% 10 15.9%Information Technology, Software, Security & Access Issue 258 14.4% 200 12.7% 8 20.0% 5 21.7% 8 26.7% 11 35.5% 5 45.5% 4 50.0% 0 0.0% 0 0.0% 17 27.0%Non-Routine Transactions Control Issues 173 9.7% 126 8.0% 9 22.5% 5 21.7% 10 33.3% 5 16.1% 3 27.3% 2 25.0% 1 25.0% 0 0.0% 12 19.0%Untimely or Inadequate Account Reconciliations 151 8.4% 102 6.5% 7 17.5% 6 26.1% 11 36.7% 8 25.8% 2 18.2% 4 50.0% 0 0.0% 0 0.0% 11 17.5%Restatement or Nonreliance of Company Filings 132 7.4% 80 5.1% 16 40.0% 9 39.1% 7 23.3% 10 32.3% 2 18.2% 1 12.5% 0 0.0% 0 0.0% 7 11.1%Journal Entry Control Issues 82 4.6% 71 4.5% 1 2.5% 3 13.0% 3 10.0% 2 6.5% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 2 3.2%Insufficient or Non-Existent Internal Audit Function 67 3.7% 55 3.5% 2 5.0% 1 4.3% 1 3.3% 1 3.2% 0 0.0% 1 12.5% 0 0.0% 0 0.0% 6 9.5%Senior Management Competency, Tone, Reliability Issues 64 3.6% 52 3.3% 0 0.0% 3 13.0% 3 10.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 6 9.5%Restatement of Previous 404 Disclosures 58 3.2% 34 2.2% 11 27.5% 2 8.7% 0 0.0% 5 16.1% 1 9.1% 0 0.0% 0 0.0% 0 0.0% 5 7.9%Ineffective Regulatory Compliance Issues 42 2.3% 37 2.3% 0 0.0% 0 0.0% 1 3.3% 1 3.2% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 3 4.8%Ethical or Compliance Issues with Personnel 34 1.9% 26 1.6% 0 0.0% 2 8.7% 1 3.3% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 5 7.9%Scope (Disclaimer of Opinion) or Other Limitations 3 0.2% 2 0.1% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 1 1.6%

Source: AuditAnalytics.com

SOX 404 Disclosures: Year 5 Issue Update1, 2

Internal Control Issues in Adverse DisclosuresYear 5Totals3

(1788)

MgmtOnly6

(1577)

Audit Firm Breakdown

Material Weakness Internal Control Issue

E&Y(40)

PwC(23)

KPMG(30)

D&T(31)

GT(11)

BDO(8)

Crowe(4)

M&P(1)

Regional(63)

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

1 Research is based on a database download of June 7, 2010.2 Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 3 For Year 5, a total of 1788 adverse SOX 404 opinions were filed with the SEC. A breakdown of the 1788 adverse opinions, each shown in the parenthesis in the table's column titles, are as follows: 1577 for management only opinions, 40 for Ernst & Young, 23 for PricewaterhouseCoopers, 30 for KPMG, 31 for Deloitte & Touche, 11 for Grant Thornton, 8 for BDO Seidman, 4 for Crowe Horwath LLP, 1 for McGladrey & Pullen, 63 for the remaining Regional & Local Firms.4 The # columns indicate the number of unique adverse 404 disclosures that identified the issue as causing or contributing to the determination that a material weakness exists. If a registrant filed more than one disclosure the amended disclosure is counted.5 The % column figures are calculated by dividing the figure in the # column by the amount shown the parenthesis in the column title, the total number of unique adverse 404 disclosure filings for the category. (See Footnote 3.) 6 The Mgmt Only column provides data for those registrants that only filed a management’s report without a corresponding auditor’s attestation. During SOX Year 5 non-accelerated filers were allowed to provide only a management assessment of the internal controls over financial reporting. Accelerated filers, U.S. and foreign, were required to provide both a management opinion and an auditor attestation their annual reports. Since the Management-Only Reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as Mgmt-Only. A total of 1577 Management Only opinions were adverse.

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 14

Audit Analytics®October 2010

Fifth-Year404

OpinionsFiled

Fifth Year 404Opinions with

Material Weaknesses

Cash FlowStatement

(FAS 95) Error

Debt, Warrants& Equity (BCF)Security Issues

Depreciation /Amortization

Inventory /Vendor Cost

of Sales

Leases orContingencies

Fixed /Intangible

Assets

Revenue Recognition

Tax AccrualsDeferrals etc.

ConsolidationFin (46) Issues

Ernst & Young 1037 40 2 3 0 4 3 6 12 15 4% of Firm's Total2 3.9% 5.0% 7.5% 0.0% 10.0% 7.5% 15.0% 30.0% 37.5% 10.0%% of Category Total3 23.9% 19.0% 100.0% 25.0% 0.0% 10.5% 37.5% 20.0% 24.0% 28.8% 36.4%PricewaterhouseCoopers 861 23 0 0 2 4 1 6 6 7 1% of Firm's Total 2.7% 0.0% 0.0% 8.7% 17.4% 4.3% 26.1% 26.1% 30.4% 4.3%% of Category Total 19.9% 10.9% 0.0% 0.0% 25.0% 10.5% 12.5% 20.0% 12.0% 13.5% 9.1%KPMG 740 30 0 1 1 7 2 3 10 11 1% of Firm's Total 4.1% 0.0% 3.3% 3.3% 23.3% 6.7% 10.0% 33.3% 36.7% 3.3%% of Category Total 17.1% 14.2% 0.0% 8.3% 12.5% 18.4% 25.0% 10.0% 20.0% 21.2% 9.1%Deloitte & Touche 791 31 0 2 1 5 1 3 5 8 3% of Firm's Total 3.9% 0.0% 6.5% 3.2% 16.1% 3.2% 9.7% 16.1% 25.8% 9.7%% of Category Total 18.3% 14.7% 0.0% 16.7% 12.5% 13.2% 12.5% 10.0% 10.0% 15.4% 27.3%Grant Thornton 202 11 0 0 0 1 0 1 1 2 0% of Firm's Total 5.4% 0.0% 0.0% 0.0% 9.1% 0.0% 9.1% 9% 18% 0.0%% of Category Total 4.7% 5.2% 0.0% 0.0% 0.0% 2.6% 0.0% 3.3% 2% 4% 0.0%BDO Seidman 128 8 0 1 0 4 0 1 2 2 0% of Firm's Total 6.3% 0.0% 12.5% 0.0% 50.0% 0.0% 12.5% 25.0% 25.0% 0.0%% of Category Total 3.0% 3.8% 0.0% 8.3% 0.0% 10.5% 0.0% 3.3% 4.0% 3.8% 0.0%Crowe 56 4 0 1 0 0 0 0 0 1 0% of Firm's Total 7.1% 0.0% 25.0% 0.0% 0.0% 0.0% 0.0% 0.0% 25.0% 0.0%% of Category Total 1.3% 1.9% 0.0% 8.3% 0.0% 0.0% 0.0% 0.0% 0.0% 1.9% 0.0%McGladrey & Pullen LLP 37 1 0 0 0 0 0 1 0 0 0% of Firm's Total 2.7% 0.0% 0.0% 0.0% 0.0% 0.0% 100.0% 0.0% 0.0% 0.0%% of Category Total 0.9% 0.5% 0.0% 0.0% 0.0% 0.0% 0.0% 3.3% 0.0% 0.0% 0.0%Regional & Local Firms (175 firms) 478 63 0 4 4 13 1 9 14 6 2% of Firm's Total 13.2% 0.0% 6.3% 6.3% 20.6% 1.6% 14.3% 22.2% 9.5% 3.2%% of Category Total 11.0% 29.9% 0.0% 33.3% 50.0% 34.2% 12.5% 30.0% 28.0% 11.5% 18.2%Totals 4330 211 2 12 8 38 8 30 50 52 11% Total of 404 Opinions 4.9% 0.9% 5.7% 3.8% 18.0% 3.8% 14.2% 23.7% 24.6% 5.2%

Year 4 Comparison 4496 347 11 15 17 77 31 58 90 104 337.7% 3.2% 4.3% 4.9% 22.2% 8.9% 16.7% 25.9% 30.0% 9.5%

Year 3 Comparison 4216 382 16 22 25 72 30 79 106 124 319.1% 4.2% 5.8% 6.5% 18.8% 7.9% 20.7% 27.7% 32.5% 8.1%

Year 2 Comparison 3791 390 28 19 26 102 45 70 119 133 3710.3% 7.2% 4.9% 6.7% 26.2% 11.5% 17.9% 30.5% 34.1% 9.5%

Year 1 Comparison 3700 624 44 45 78 172 106 120 198 198 5816.9% 7.1% 7.2% 12.5% 27.6% 17.0% 19.2% 31.7% 31.7% 9.3%

Source: AuditAnalytics.com AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc. a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

Year 5 SOX 404 Issue Prevalence by Firm and Issue CategoryGAAP / Accounting Areas of Failure (compared to the firm's total amount of MWs) 1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 The "% of Firms Total" calculation for the issues columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) x 100; e.g., E&Y Cash Flow is (2/40) x 100 = 5.0%. Unlike the issue columns, the Material Weakness column's percentage is based on the auditor's total 404 opinions; e.g., 40/1037 x 100 = 3.9%.3 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column Total of Column's Category]) x 100; e.g., (2/2) x 100 = 100%.4 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 15

Audit Analytics®October 2010

Fifth Year404

OpinionsFiled

Fifth Year 404Opinions with

Material Weaknesses

Cash FlowStatement

(FAS 95) Error

Debt, Warrants& Equity (BCF)Security Issues

Depreciation /Amortization

Inventory /Vendor Cost

of Sales

Leases orContingencies

Fixed /Intangible

Assets

Revenue Recognition

Tax AccrualsDeferrals etc.

ConsolidationFin (46) Issues

Ernst & Young 1037 40 2 3 0 4 3 6 12 15 4% of Firm's Total2 3.9% 5.0% 7.5% 0.0% 10.0% 7.5% 15.0% 30.0% 37.5% 10.0%% of Category Total3 11.3% 2.2% 25.0% 2.7% 0.0% 4.3% 18.8% 7.7% 9.4% 13.2% 12.5%PricewaterhouseCoopers 861 23 0 0 2 4 1 6 6 7 1% of Firm's Total 2.7% 0.0% 0.0% 8.7% 17.4% 4.3% 26.1% 26.1% 30.4% 4.3%% of Category Total 9.4% 1.3% 0.0% 0.0% 11.1% 4.3% 6.3% 7.7% 4.7% 6.1% 3.1%KPMG 740 30 0 1 1 7 2 3 10 11 1% of Firm's Total 4.1% 0.0% 3.3% 3.3% 23.3% 6.7% 10.0% 33.3% 36.7% 3.3%% of Category Total 8.0% 1.7% 0.0% 0.9% 5.6% 7.5% 12.5% 3.8% 7.9% 9.6% 3.1%Deloitte & Touche 791 31 0 2 1 5 1 3 5 8 3% of Firm's Total 3.9% 0.0% 6.5% 3.2% 16.1% 3.2% 9.7% 16.1% 25.8% 9.7%% of Category Total 8.6% 1.7% 0.0% 1.8% 5.6% 5.4% 6.3% 3.8% 3.9% 7.0% 9.4%Grant Thornton 202 11 0 0 0 1 0 1 1 2 0% of Firm's Total 5.4% 0.0% 0.0% 0.0% 9.1% 0.0% 9.1% 9% 18% 0.0%% of Category Total 2.2% 0.6% 0.0% 0.0% 0.0% 1.1% 0.0% 1.3% 1% 2% 0.0%BDO Seidman 128 8 0 1 0 4 0 1 2 2 0% of Firm's Total 6.3% 0.0% 12.5% 0.0% 50.0% 0.0% 12.5% 25.0% 25.0% 0.0%% of Category Total 1.4% 0.4% 0.0% 0.9% 0.0% 4.3% 0.0% 1.3% 1.6% 1.8% 0.0%Crowe 56 4 0 1 0 0 0 0 0 1 0% of Firm's Total 7.1% 0.0% 25.0% 0.0% 0.0% 0.0% 0.0% 0.0% 25.0% 0.0%% of Category Total 0.6% 0.2% 0.0% 0.9% 0.0% 0.0% 0.0% 0.0% 0.0% 0.9% 0.0%McGladrey & Pullen LLP 37 1 0 0 0 0 0 1 0 0 0% of Firm's Total 2.7% 0.0% 0.0% 0.0% 0.0% 0.0% 100.0% 0.0% 0.0% 0.0%% of Category Total 0.4% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 1.3% 0.0% 0.0% 0.0%Regional & Local Firms (175 firms) 478 63 0 4 4 13 1 9 14 6 2% of Firm's Total 13.2% 0.0% 6.3% 6.3% 20.6% 1.6% 14.3% 22.2% 9.5% 3.2%% of Category Total 5.2% 3.5% 0.0% 3.6% 22.2% 14.0% 6.3% 11.5% 11.0% 5.3% 6.3%Management-Only Reports 5 4877 1577 6 99 10 55 8 48 77 62 21% of Mgmt. Only Total 32.3% 0.4% 6.3% 0.6% 3.5% 0.5% 3.0% 4.9% 4% 1%% of Category Total 53.0% 88.2% 75.0% 89.2% 55.6% 59.1% 50.0% 61.5% 60.6% 54% 66%Totals 9207 1788 8 111 18 93 16 78 127 114 32% Total of 404 Opinions 19.4% 0.4% 6.2% 1.0% 5.2% 0.9% 4.4% 7.1% 6.4% 1.8%

Year 4 Comparison 9086 1816 19 93 34 172 49 116 193 179 5920.0% 1.0% 5.1% 1.9% 9.5% 2.7% 6.4% 10.6% 9.9% 3.2%

Year 3 Comparison 4533 486 16 29 28 83 33 85 117 132 4010.7% 3.3% 6.0% 5.8% 17.1% 6.8% 17.5% 24.1% 27.2% 8.2%

Source: AuditAnalytics.com

5 The rows designated as Management-Only Reports provide data for those registrants that only filed a management’s report without a corresponding auditor’s attestation. During SOX Year 5 non-accelerated filers were allowed to provide only a management assessment of the internal controls over financial reporting. Accelerated filers, U.S. and foreign, were required to provide both a management opinion and an auditor attestation their annual reports. Since the Management-Only Reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as Management-Only Reports.

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc. a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

Year 5 SOX 404 Issue Prevalence by Firm and Issue CategoryGAAP / Accounting Areas of Failure (compared to the firm's total amount of MWs) 1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 The "% of Firms Total" calculation for the issues columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) x 100; e.g., E&Y Cash Flow is (2/40) x 100 = 5.0%. Unlike the issue columns, the Material Weakness column's percentage is based on the auditor's total 404 opinions; e.g., 40/1037 x 100 = 3.9%.3 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column Total of Column's Category]) x 100; e.g., (2/8) x 100 = 25.0%4 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 16

Audit Analytics®October 2010

#4 %5 # % # % # % # % # % # % # % # % # % # %

Unspecified/Unidentified/Inapplicable FASB/GAAP Issues 1095 61.2% 1056 67.0% 4 10.0% 2 8.7% 5 16.7% 7 22.6% 5 45.5% 1 12.5% 0 0.0% 0 0.0% 15 23.8%Accounts/Loans Receivable, Investments & Cash Issues 167 9.3% 118 7.5% 9 22.5% 6 26.1% 7 23.3% 4 12.9% 3 27.3% 2 25.0% 3 75.0% 1 100.0% 14 22.2%Revenue Recognition Issues 127 7.1% 77 4.9% 12 30.0% 6 26.1% 10 33.3% 5 16.1% 1 9.1% 2 25.0% 0 0.0% 0 0.0% 14 22.2%Foreign, Related Party, Affiliated and/or Subsidiary Entity Issues 117 6.5% 84 5.3% 4 10.0% 1 4.3% 9 30.0% 4 12.9% 3 27.3% 1 12.5% 1 25.0% 0 0.0% 10 15.9%Tax Expense/Benefit/Deferral/Other (FAS 109) Issues 114 6.4% 62 3.9% 15 37.5% 7 30.4% 11 36.7% 8 25.8% 2 18.2% 2 25.0% 1 25.0% 0 0.0% 6 9.5%Debt,Quasi-Debt, Warrants & Equity ( BCF) Security Issues 111 6.2% 99 6.3% 3 7.5% 0 0.0% 1 3.3% 2 6.5% 0 0.0% 1 12.5% 1 25.0% 0 0.0% 4 6.3%Liabilities, Payables, Reserves and Accrual Estimate Failures 104 5.8% 72 4.6% 3 7.5% 7 30.4% 5 16.7% 5 16.1% 2 18.2% 0 0.0% 1 25.0% 0 0.0% 9 14.3%Inventory, Vendor and Cost of Sales Issues 93 5.2% 55 3.5% 4 10.0% 4 17.4% 7 23.3% 5 16.1% 1 9.1% 4 50.0% 0 0.0% 0 0.0% 13 20.6%PPE, Intangible or Fixed Asset (Value/Diminution) Issues 78 4.4% 48 3.0% 6 15.0% 6 26.1% 3 10.0% 3 9.7% 1 9.1% 1 12.5% 0 0.0% 1 100.0% 9 14.3%Expense Recording (Payroll, SG&A) Issues 75 4.2% 54 3.4% 3 7.5% 3 13.0% 5 16.7% 0 0.0% 1 9.1% 1 12.5% 0 0.0% 0 0.0% 8 12.7%Deferred, Stock-Based or Executive Compensation Issues 61 3.4% 42 2.7% 2 5.0% 4 17.4% 3 10.0% 6 19.4% 0 0.0% 1 12.5% 0 0.0% 0 0.0% 3 4.8%Acquisition, Merger, Disposal or Reorganization Issues 52 2.9% 33 2.1% 6 15.0% 5 21.7% 2 6.7% 1 3.2% 1 9.1% 1 12.5% 0 0.0% 0 0.0% 3 4.8%Consolidation, (Fin46r/Off BS) & Foreign Currency Translation 32 1.8% 21 1.3% 4 10.0% 1 4.3% 1 3.3% 3 9.7% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 2 3.2%Intercompany/Investment with Subsidiary/Affiliate Entity Issues 26 1.5% 14 0.9% 2 5.0% 3 13.0% 2 6.7% 2 6.5% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 3 4.8%Financial Derivatives/Hedging (FAS 133) Accounting Issues 24 1.3% 15 1.0% 2 5.0% 1 4.3% 1 3.3% 2 6.5% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 3 4.8%Depreciation, Depletion or Amortization Issues 18 1.0% 10 0.6% 0 0.0% 2 8.7% 1 3.3% 1 3.2% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 4 6.3%Lease, FAS 5, Legal, Contingency & Commitments Issues 16 0.9% 8 0.5% 3 7.5% 1 4.3% 2 6.7% 1 3.2% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 1 1.6%Capitalization of Expenditures Issues 14 0.8% 8 0.5% 1 2.5% 1 4.3% 0 0.0% 1 3.2% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 3 4.8%Income Statement Classification, Margin and EPS Issues 11 0.6% 6 0.4% 1 2.5% 1 4.3% 0 0.0% 2 6.5% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 1 1.6%Cash Flow Statement (FAS 95) Classification Errors 8 0.4% 6 0.4% 2 5.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0%Gain or Loss Recognition Issues 5 0.3% 5 0.3% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0%Debt and/or Equity Classification Issues 4 0.2% 3 0.2% 0 0.0% 0 0.0% 1 3.3% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0%

Source: AuditAnalytics.com

4 The # columns indicate the number of unique adverse 404 disclosures that identified the issue as causing or contributing to the determination that a material weakness exists. If a registrants filed more than one disclosure the amended disclosure is counted.5 The % column figures are calculated by dividing the figure in the # column by the amount shown the parenthesis in the column title, the total number of unique adverse 404 disclosure filings for the category. (See Footnote 3.)

KPMG(30)

D&T(31)

Audit Firm Breakdown

Material Weakness GAAP Financial Issue

E&Y(40)

PwC(23)

6 The Mgmt Only column provides data for those registrants that only filed a management’s report without a corresponding auditor’s attestation. During SOX Year 5 non-accelerated filers were allowed to provide only a management assessment of the internal controls over financial reporting. Accelerated filers, U.S. and foreign, were required to provide both a management opinion and an auditor attestation their annual reports. Since the Management-Only Reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as Mgmt-Only. A total of 1577 Management Only opinions were adverse.

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

Regional(63)

1 Research is based on a database download of June 7, 2010. 2 Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 3 For Year 5, a total of 1788 adverse SOX 404 opinions were filed with the SEC. A breakdown of the 1788 adverse opinions, each shown in the parenthesis in the table's column titles, are as follows: 1577 for management only opinions, 40 for Ernst & Young, 23 for PricewaterhouseCoopers, 30 for KPMG, 31 for Deloitte & Touche, 11 for Grant Thornton, 8 for BDO Seidman, 4 for Crowe Horwath LLP, 1 for McGladrey & Pullen, 63 for the remaining Regional & Local Firms.

GT(11)

BDO(8)

Crowe(4)

M&P(1)

SOX 404 Disclosures: Year 5 Issue Update1, 2

GAAP Financial Issues in Adverse DisclosuresYear 5Totals3

(1788)

MgmtOnly6

(1577)

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 17

Audit Analytics®October 2010

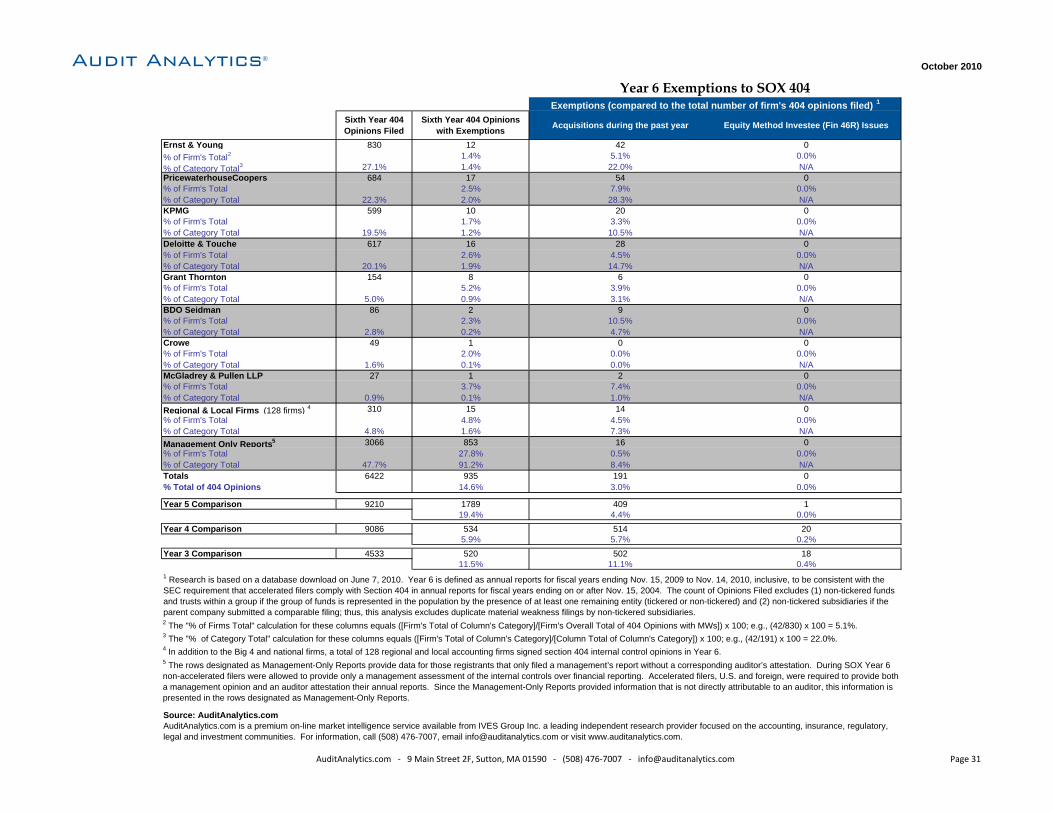

Fifth Year 404 Opinions Filed3

Fifth Year 404 Opinionswith Exemptions Acquisitions during the past year Equity Method Investee (Fin 46R) Issues

Ernst & Young 1037 40 92 1% of Firm's Total2 3.9% 8.9% 0.1%% of Category Total3 11.3% 2.2% 22.5% 100.0%PricewaterhouseCoopers 861 23 82 0% of Firm's Total 2.7% 9.5% 0.0%% of Category Total 9.4% 1.3% 20.1% 0.0%KPMG 740 30 49 0% of Firm's Total 4.1% 6.6% 0.0%% of Category Total 8.0% 1.7% 12.0% 0.0%Deloitte & Touche 791 31 82 0% of Firm's Total 3.9% 10.4% 0.0%% of Category Total 8.6% 1.7% 20.1% 0.0%Grant Thornton 202 11 15 0% of Firm's Total 5.4% 7.4% 0%% of Category Total 2.2% 0.6% 3.7% 0%BDO Seidman 128 8 17 0% of Firm's Total 6.3% 13.3% 0%% of Category Total 1.4% 0.4% 4.2% 0%Crowe 56 4 1 0% of Firm's Total 7.1% 1.8% 0%% of Category Total 0.6% 0.2% 0.2% 0%McGladrey & Pullen LLP 37 1 4 0% of Firm's Total 2.7% 10.8% 0%% of Category Total 0.4% 0.1% 1% 0%Regional & Local Firms (175 firms) 4 5 478 63 30 0% of Firm's Total 13.2% 6.3% 0%% of Category Total 5.2% 3.5% 7.4% 0%Management Only Reports 4877 1577 36 0% of Firm's Total 32.3% 0.7% 0%% of Category Total 53.0% 88.2% 8.8% 0%Totals 9207 1788 408 1% Total of 404 Opinions 19.4% 4.4% 0.0%

Year 4 Comparison 9086 534 514 205.9% 5.7% 0.2%

Year 3 Comparison 4533 520 502 1811.5% 11.1% 0.4%

Source: AuditAnalytics.com

5 The rows designated as Management-Only Reports provide data for those registrants that only filed a management’s report without a corresponding auditor’s attestation. During SOX Year 5 non-accelerated filers were allowed to provide only a management assessment of the internal controls over financial reporting. Accelerated filers, U.S. and foreign, were required to provide both a management opinion and an auditor attestation their annual reports. Since the Management-Only Reports provided information that is not directly attributable to an auditor, this information is presented in the rows designated as Management-Only Reports.

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc. a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

Year 5 Exemptions to SOX 404Exemptions (compared to the total number of firm's 404 opinions filed) 1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries. 2 The "% of Firms Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Firm's Overall Total of 404 Opinions with MWs]) x 100; e.g., (92/1037) x 100 = 8.9%.3 The "% of Category Total" calculation for these columns equals ([Firm's Total of Column's Category]/[Column Total of Column's Category]) x 100; e.g., (92/408) x 100 = 22.5%.4 In addition to the Big 4 and national firms, a total of 175 regional and local accounting firms signed section 404 internal control opinions in Year 5.

AuditAnalytics.com ‐ 9 Main Street 2F, Sutton, MA 01590 ‐ (508) 476‐7007 ‐ [email protected] Page 18

Audit Analytics® October 2010

Company CIK Code Ticker Auditor Name Accelerated FilerFiscal

YE2 Status Summary

Wilson Bank Holding Co. 885275 WBHC Maggart & Associates PC Accelerated Filer 12/31 Claimed to file auditor attestation, unable to locate in any SEC filing

Fairpoint Communications Inc. 1062613 Ernst & Young LLP Accelerated Filer 12/31 Accelerated filer, no auditor attestation filed

Heckmann Corp. 1403853 HEK GHP Horwath PC Accelerated Filer 12/31 Accelerated filer, no auditor attestation filed

Medifast Inc. 910329 MED McGladrey & Pullen LLP Accelerated Filer 12/31 Accelerated filer, no auditor attestation filed

YM Biosciences Inc. 1178347 YMI KPMG LLP Accelerated Filer 6/30 Accelerated filer, no auditor attestation filed

Mesa Air Group Inc. 810332 Deloitte & Touche LLP Accelerated Filer 9/30 Subsequent NT-10K filed 12/30/09; Disclosure Due: FYE = 9/30/09 + 75 days = 12/14/09

Volt Information Sciences, Inc. 103872 VOL Ernst & Young LLP Accelerated Filer 11/1 Filed 10-K on 2/2/09 for FYE 11/1/08 (SOX Yr 4), then filed NT-10K on 1/15/10

Company CIK Code Ticker Auditor Name Accelerated FilerFiscal

YE2 Status Summary

American Bancorp Of New Jersey Inc. 1330039 Crowe Horwath LLP Accelerated Filer 9/30 Subsequent Termination filed on 2/8/2010; Disclosure Due: FYE = 9/30/09 + 75 days = 12/14/09

Asyst Technologies Inc. 909326 PricewaterhouseCoopers LLP Accelerated Filer 3/31 Subsequent Termination filed on 3/12/2010; Disclosure Due: FYE = 3/31/09 + 75 days = 6/14/09

Avanex Corp. 1056794 Deloitte & Touche LLP Accelerated Filer 6/30 Subsequent Termination filed on 10/14/2009; Disclosure Due: FYE = 6/30/09 + 75 days = 9/13/09

Brink's Home Security Holdings, Inc. 1436040 KPMG LLP Large Accelerated Filer 12/31 Subsequent Termination filed on 5/25/2010; Disclosure Due: FYE = 12/31/08 + 60 days = 3/1/09

Charlotte Russe Holding, Inc. 1092006 Ernst & Young LLP Accelerated Filer 9/26 Subsequent Termination filed on 12/9/2009; Disclosure Due: FYE = 9/26/09 + 75 days = 12/10/09

Fleetwood Enterprises Inc./DE/ 314132 Ernst & Young LLP Accelerated Filer 4/30 Subsequent Termination filed 8/23/10; Disclosure Due: FYE = 4/27/08 + 75 days = 7/11/08

GDF Suez 1243443 Ernst & Young LLP Large Accelerated Filer 12/31 Subsequent Termination filed on 7/30/2009; Disclosure Due: FYE = 12/31/08 + 60 days = 3/1/09

Media & Entertainment Holdings, Inc. 1337749 Marcum & Kliegman LLP Accelerated Filer 3/31 Subsequent Termination filed on 6/19/2009; Disclosure Due: FYE = 3/31/09 + 75 days = 6/14/09

Source: AuditAnalytics.com

Registrants with Overdue SOX 404 Auditor Attestations for Year 5 (and thus Expected to File an Adverse 404 in the Future)1

1 Research is based on a database download of June 7, 2010. Year 5 is defined as annual reports for fiscal years ending Nov. 15, 2008 to Nov. 14, 2009, inclusive, to be consistent with the SEC requirement that accelerated filers comply with Section 404 in annual reports for fiscal years ending on or after Nov. 15, 2004. The count of Opinions Filed excludes (1) non-tickered funds and trusts within a group if the group of funds is represented in the population by the presence of at least one remaining entity (tickered or non-tickered) and (2) non-tickered subsidiaries if the parent company submitted a comparable filing; thus, this analysis excludes duplicate material weakness filings by non-tickered subsidiaries.2 Large accelerated filers have 60 days to file an annual report, accelerated filers have 75 days, and foreign filers have 6 months.

AuditAnalytics.com is a premium on-line market intelligence service available from IVES Group Inc., a leading independent research provider focused on the accounting, insurance, regulatory, legal and investment communities. For information, call (508) 476-7007, email [email protected] or visit www.auditanalytics.com.

3 Geeknet, Inc. (CIK 1096199) and Charlotte Russe Holding, Inc. (CIK 1092006) did not file a SOX 404 disclosure for Year 5, but were not required to do so because the companies changed their fiscal year end(s) for Aug. 31 to Dec. 31.

Registrants that Failed to File a SOX 404 Auditor Attestations for Year 5 but Subsequently Filed a Termination

1 The following companies filed a termination (Form 15) with the SEC before the their annual reports were due: Endo Pharmaceuticals Solutions Inc. (CIK 854222), hi/fn, inc. (CIK 1065246), Tailwind Financial Inc. (CIK 1368879), Stoneleigh Partners Acquisition Corp. (CIK 1345715), Accenture Ltd. (CIK 1134538), Zila, Inc (CIK 827156), Particle Drilling Technologies, Inc. (CIK 759153), FCStone Group, Inc. (CIK 1297846).

AuditAnalytics.com - 9 Main Street 2F, Sutton, MA 01590 - (508) 476-7007 - [email protected] Page 19

Audit Analytics® October 2010

AuditAnalytics.com ● 9 Main Street, Sutton 2F, MA 01590 ● (508) 476-7007 ● [email protected] Page 20

SOX 404 Year 6 Tables (Partial Year Data)

Audit Analytics®October 2010

SOX 404Year 5

SOX 404Year 4

SOX 404Year 3

SOX 404Year 2

SOX 404Year 1