sovereign debt structure for crisis prevention - world bank internet

TRANSCRIPT

O C C A S I O N A L PA P E R

Sovereign Debt Structure forCrisis Prevention

Eduardo Borensztein, Marcos Chamon, Olivier Jeanne,Paolo Mauro, and Jeromin Zettelmeyer

237

INTERNATIONAL MONETARY FUND

Washington DC

2004

237

Sovereign Debt Structure forCrisis Prevention

237

Sovereign D

ebt Structure fo

r Crisis P

revention

2004

O C C A S I O N A L PA P E R 237

Sovereign Debt Structure for Crisis Prevention

Eduardo Borensztein, Marcos Chamon, Olivier Jeanne,Paolo Mauro, and Jeromin Zettelmeyer

INTERNATIONAL MONETARY FUND

Washington DC

2004

© 2004 International Monetary Fund

Production: IMF Multimedia Services DivisionFigures: Jorge Salazar

Typesetting: Alicia Etchebarne-Bourdin

Cataloging-in-Publication Data

Price: US$25.00(US$22.00 to full-time faculty members and

students at universities and colleges)

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431, U.S.A.Tel.: (202) 623-7430 Telefax: (202) 623-7201

E-mail: [email protected]: http://www.imf.org

recycled paper

Sovereign debt structure for crisis prevention/Eduardo Borensztein . . . [et al.]—Washington, D.C.: International Monetary Fund, 2004.

p. cm.—(Occasional paper); 237

Includes bibliographical references.ISBN 1-58906-377-5

1. Debts, public. 2. Financial instruments. I. Borensztein, Eduardo. II. Occa-sional paper (International Monetary Fund); no. 237.

HJ8011.S68 2004

Preface vii

I Overview 1

Two Views on the Status Quo 1Debt Structures with Existing Instruments: Emerging Market

Countries Versus Advanced Economies 3Ideas for Sovereigns from the Corporate Context: Explicit Seniority 3Expanding the Set of Instruments: Real Indexation 4Toward Better Sovereign Debt Structures: A Road Map 5

II Facts on Existing Public Debt Structures 7

Public Debt in Emerging Market Countries Versus Advanced Economies 7

Sovereign Versus Corporate Liability Structures 11

III Rendering Debt Structures Less Crisis Prone with ExistingInstruments 14

Problems with the Status Quo 14Determinants of Government Debt Structure 15Policy Implications 19

IV Explicit Seniority in Privately Held Sovereign Debt 23

Economic Role of Seniority 23Approaches and Obstacles in Implementing Explicit Seniority 25Conclusions 28

V Expanding the Set of Instruments: Indexation to Real Variables 29

Benefits of Indexation to Real Variables 29Real Variables Beyond the Control of the Country’s Authorities 31Real Variables Partially Within the Control of the Country’s

Authorities 38Obstacles for Variables Partly Within the Control of the Government 42Steps to Foster Acceptance 43Real Indexation: Which Variables for Which Countries? 44

VI Past and Future of Innovation in Sovereign Borrowing 46

Financial Innovation in Sovereign Borrowing: A Haphazard Process 46Road Maps for Future Innovation 48

VII Conclusions 49

Contents

iii

CONTENTS

Appendix Investors’ Attitudes Toward Growth-Linked and Other Innovative Financial Instruments for Sovereign Borrowers: Results of a Survey 51

References 56

Boxes

1. Debt Structure and Hedging 172. Creating Domestic Markets for Long-Term Domestic-Currency

Bonds: Country Experiences 203. Developing International Markets for Bonds in Emerging

Market Currencies 214. Enforcing Contractual Seniority 265. Effect on Borrowing Costs of a Switch to First-in-Time

Seniority 276. Proposals for Indexation to Real Variables 307. Benefits of GDP Indexation for Emerging Markets and

Advanced Economies 418. Previous Examples of Indexation to Real Variables 43

Text Tables

1. External Sovereign Debt: Currency Composition, 1980–2003 102. Structure of Domestically Issued Government Bonds at

End-2001 103. Structure of Total (Domestic and External) Central Government

Debt, 2001 124. Percentage Share of the Top Three Exports in Total Exports,

1990–99 325. Top Five Natural Disasters by Percent of GDP Lost 346. Small Countries: Types of Disasters, 1975–2002 367. Output Growth and Trading Partners’ Growth, 1970–2002 388. Introduction of Inflation-Indexed Securities by Sovereigns 47

Text Figures

1. Advanced Economies and Emerging Market Countries: Public Debt Stocks and Debt Composition 7

2. Structure of External Public Debt in Emerging Market Countries 83. Emerging Market Countries: Fixed- Versus Floating-Rate

Sovereign Bond Issues 84. Structure of Internationally Issued Debt: Maturity Composition 95. Emerging Market Countries: Structure of Public Debt 116. All Developing Countries: Public Sector Bonds and Loans

Issued in International Markets 137. Recent Crises: Impact of Exchange Rate Depreciation on Public

Debt-to-GDP Ratio 158. Share of Long-Term Local-Currency Bonds in Total Government

Domestic Bonds and Inflation History 169. Share of Long-Term Local-Currency Bonds and Financial

Liberalization 1810. Institutional Quality and Domestically Issued Long-Term

Local-Currency Debt 1911. Interest Savings over the Economic Cycle 40

iv

Contents

Appendix Tables

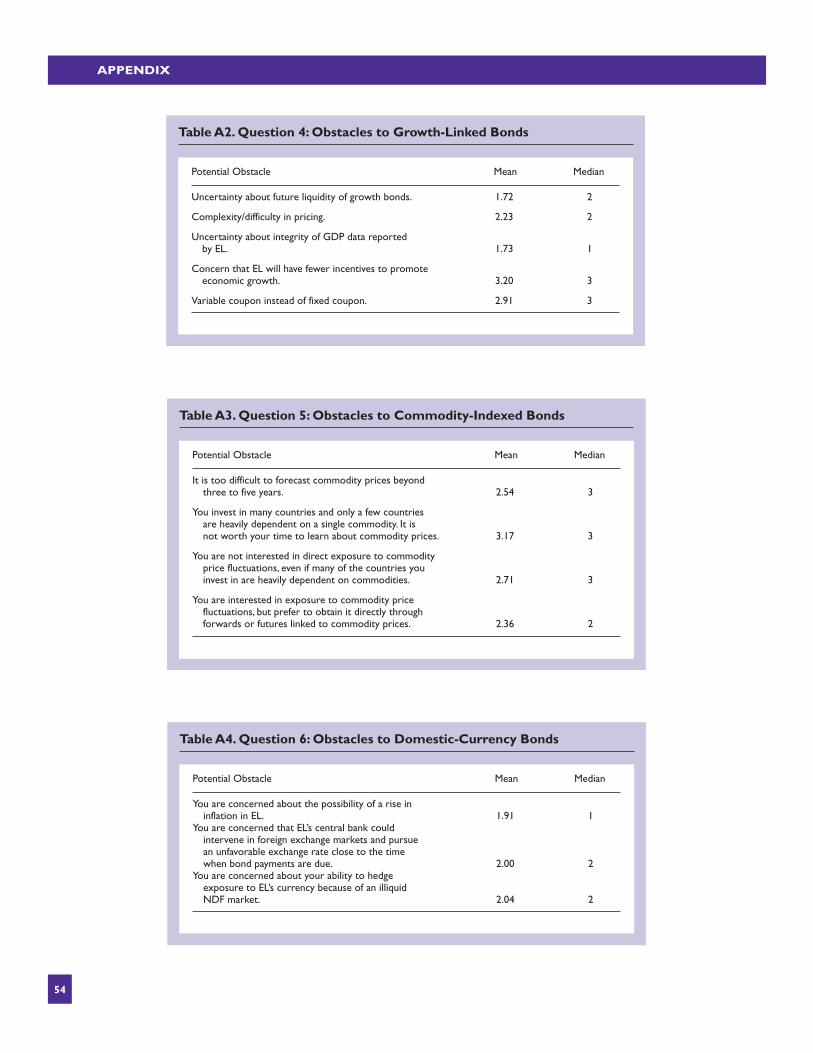

A1. Question 3: Obstacles to Growth-Linked Bonds 53A2. Question 4: Obstacles to Growth-Linked Bonds 54A3. Question 5: Obstacles to Commodity-Indexed Bonds 54A4. Question 6: Obstacles to Domestic-Currency Bonds 54

Appendix Figures

A1. Question 1: Premium over Plain Vanilla Bonds 52A2. Question 2: Premium over Plain Vanilla Bonds 53

v

The following symbols have been used throughout this paper:

. . . to indicate that data are not available;

— to indicate that the figure is zero or less than half the final digit shown, or that the itemdoes not exist;

– between years or months (e.g., 2001–02 or January–June) to indicate the years ormonths covered, including the beginning and ending years or months;

/ between years (e.g., 2001/02) to indicate a fiscal (financial) year.

“n.a.” means not applicable.

“Billion” means a thousand million.

Minor discrepancies between constituent figures and totals are due to rounding.

The term “country,” as used in this paper, does not in all cases refer to a territorial entity thatis a state as understood by international law and practice; the term also covers some territorialentities that are not states, but for which statistical data are maintained and provided interna-tionally on a separate and independent basis.

This Occasional Paper is intended to stimulate debate on the issue of sovereigndebt structures for crisis prevention. It was prepared under the general guidance ofRaghuram Rajan. The authors include Eduardo Borensztein, Marcos Chamon, OlivierJeanne, Paolo Mauro, and Jeromin Zettelmeyer. Work on the paper was led by PaoloMauro. The authors are grateful to Jonathan Ostry, Anna Gelpern, Sean Hagan,Simon Johnson, Thomas Laryea, and several other colleagues for helpful comments;to Priyanka Malhotra and Martin Minnoni for excellent research assistance; and toUsha David for editorial assistance. Special thanks to Leslie Payton-Jacobs of EMTAfor helpful suggestions and cooperation in circulating the survey, and to Kellett Han-nah for web services. Archana Kumar of the External Relations Department editedthe paper and coordinated its production.

The opinions expressed are solely those of the authors and do not necessarily re-flect the views of the International Monetary Fund or its Executive Directors.

Preface

vii

The way countries structure their public borrow-ing has long been considered an important de-

terminant of economic performance. This topic hasrecently received renewed attention as a result of notonly steep increases in public debt levels in emerg-ing market countries—and a number of highly visi-ble and damaging crises—but also pronouncedchanges in the composition of those debts.1 There isincreasing recognition that debt structure has impor-tant implications for both the frequency of crises andthe disruption they cause when they strike.2 Indeed,the official sector is beginning to give renewedprominence to the possible need for innovations inthe design of countries’ financial liabilities.3

The debate on government debt in the context ofpossible reforms of the international financial archi-tecture has thus far focused on crisis resolution.4This Occasional Paper seeks to broaden the debateby asking how government debt could be structuredto pursue other objectives, including crisis preven-tion, international risk-sharing, and facilitating theadjustment of fiscal variables to changes in domesticeconomic conditions. To that end, this paper consid-ers recently developed analytical approaches to im-proving the structure of sovereign debt using exist-ing debt instruments. It then reviews a number ofproposals—including the introduction of explicit se-niority and GDP-linked instruments—in the sover-eign context and discusses their pros and cons, andthe related practical challenges.

While recognizing that there is no easy substitutefor sound macroeconomic policies—fiscal policiesin particular—and that no amount of financial engi-neering could eliminate crises, this paper askswhether greater use of relatively underutilized fi-nancial instruments could help reduce the frequencyof damaging crises. After identifying commonsources of vulnerability, the paper takes a first passat identifying instruments and structures that couldhelp achieve a more resilient debt structure, and setsforth some preliminary considerations about theirfeasibility.

Two Views on the Status Quo

Developing a strategy for addressing possible in-efficiencies in existing debt structures requires anunderstanding of what may cause them. On this sub-ject, there are two views in the policy and academicdebate. The first, which underlies most proposals forreforming the “international financial architecture,”assumes that today’s array of instruments is inher-ited from historical accident and has persisted owingto inertia: the existing structures can be changed,though not without substantial effort, through re-forms involving coordination among market partici-pants. The second view argues that the status quo isan adaptation to deeper problems, such as difficul-ties in enforcing contracts in the international set-ting, lack of policy credibility, and weaknesses indomestic institutions. The outcome may well be in-efficient, but it cannot be improved without address-ing the underlying problems.

History and Inertia

The “architecture” analogy is one of a housewhose current form results from the way it wasbuilt in the past, in response to incentives or needsthat may have had little to do with those of its pre-sent inhabitants. Under this view, making a case forreform merely requires showing that the architec-ture gives rise to costly and inefficient outcomes.Of course, structures that are considered part of the

I Overview

1

Note: The authors of this section are Paolo Mauro and JerominZettelmeyer.

1International Monetary Fund and World Bank (2001 and2003); IMF, World Economic Outlook (September 2003, Chapter3); Reinhart, Rogoff, and Savastano (2003); Guidotti and Kumar(1991).

2International Monetary Fund (2003a); and Allen and others(2002).

3The Declaration of Nuevo León (Special Summit of the Ameri-cas, Monterrey, Mexico, January 2004) supports “the efforts of bor-rowing countries to work with the private sector to explore new ap-proaches to reduce the burden of debt service during periods ofeconomic downturns” (available via the Internet: www.summit-americas.org/SpecialSummit/declaration_monterrey-eng.htm).

4International Monetary Fund (2003b).

I OVERVIEW

architecture do not generally change by them-selves: this requires a reform effort. But the goodnews is that through such an effort, most structurescan be torn down and rebuilt, or at least renovatedand cleaned.

Changes to the status quo could however be diffi-cult to achieve for many reasons, especially a needfor coordination among market participants. For in-dividual market participants, it is hard to go againstmarket practice in drafting contracts. Moreover, re-forms often require mustering support from nationalparliaments, international bodies, or market partici-pants. A number of potential obstacles thus stand inthe way of contractual or financial innovation (Allenand Gale, 1994):

• Coordination problems and the need to ensure“critical mass” for new instruments. The appealof an innovation often depends on its simultane-ous adoption by many contracting parties. Forexample, learning to price new financial instru-ments may require excessive resources from theviewpoint of an individual investor, but may beworth the effort collectively for the potential in-vestor class. More generally, individual borrow-ers considering whether to issue a new financialinstrument will not take into account the benefitsfor other borrowers and investors that would re-sult from establishing a new asset class. And inthe absence of a concerted effort to guarantee aminimum critical mass, investors may be con-cerned about the possibility of limited liquidityfor the new instruments and thus demand a “nov-elty premium.”

• The highly competitive structure of financialmarkets. A private financial institution wouldhave to incur costs to develop a new type of fi-nancial instrument. However, it may be unable tomaintain a monopoly over the provision of thisinstrument for a long time: patents are still rarely(though increasingly) used for financial instru-ments, and imitation is relatively easy. Thus, theprivate incentive to develop the instrument in thefirst place may be low, even if its social benefitmay be high.

• The need for standards. To create a liquid sec-ondary market where investors can easily diver-sify their portfolio, it is important to have in-struments with the same features for allcountries or all firms issuing them. Moreover,for financial instruments where payments aredue when certain conditions are met, it is cru-cial to have verifiable standards for whetherthose conditions are met. For example, the mar-ket for credit default swaps remained small foryears but took off as soon as the standards for a

“credit event” were properly defined and be-came broadly accepted.5

• Signaling. Individual countries may be reluctantto issue new financial instruments or existing in-struments with new contractual features if theyfear that such innovations may be misperceivedas signs of weakness or lack of commitment togood policies.

Deeper Problems

An alternative view is that prevailing contracts andmarket practices result from the responses of credi-tors and sovereign debtors to deeper problems, in-cluding difficulties in enforcing contracts involvingsovereign borrowers, and the possibility of moralhazard (behavior that does not maximize the likeli-hood of repayment) on the part of debtors. Costlydebt crises may look inefficient ex post but are, inthis view, the only way to discourage defaults (Doo-ley, 2000; Dooley and Verma, 2001). Existing debtinstruments are seen as optimal because they implythat crises will occasionally occur to constrain or dis-cipline borrowing governments. Similarly, “risky”and seemingly inefficient debt structures heavilyweighted toward foreign-currency-denominated debtand short-term debt are rationalized as necessaryevils to reduce moral hazard on the part of policy-makers, or minimize debt dilution (Chamon, 2002;Jeanne, 2000, 2004; Tirole, 2002; and Sections II andIII).6 Thus, crisis-prone debt structures can be asymptom rather than the root cause of countries’ in-ability to commit to good policies; such inability mayin turn result from weak domestic institutions.

Under this view, attempts to reform the interna-tional financial architecture by changing outcomesbut without addressing underlying distortions couldwell be counterproductive. For example, restrictionsor taxes on short-term debt might seek to induce amove from short-term to long-term flows. However,their impact might be undone by international in-vestors’ shift toward other forms of debt that aresimilarly difficult to dilute, such as foreign-currencydebt. Alternatively, if the impact of the restrictionscannot be undone, they might end up reducing oreliminating capital flows altogether. As in OscarWilde’s Canterville Ghost, for the stain to ceasefrom reappearing on the carpet the next morning, itis not enough to apply the latest carpet cleaner. Theghost itself must be laid to rest.

2

5Credit default swaps are instruments giving the holder theright to sell a bond at its face value in the event of default by theissuer.

6The disciplining role of short-term and other risky forms ofdebt has also been emphasized in the corporate context(Calomiris and Kahn, 1991; Diamond, 1991).

Ideas for Sovereigns from the Corporate Context

Both interpretations of the status quo have somemerit, and this paper draws upon them in the subse-quent sections. The focus on underlying causes ofinefficiencies in existing debt structures leads to adiscussion of associated policy and institutional fail-ures, and remedies for them. Beyond this, though,and recognizing that crises are exceedingly costly,7this paper provides a preliminary analysis of the casefor innovations that could directly improve sover-eign debt structures, but may have been impeded inthe past primarily by inertia.

Debt Structures with ExistingInstruments: Emerging MarketCountries Versus Advanced Economies

In analyzing existing debt structures, two sets ofcomparisons provide insights into how debt struc-tures might be improved (Section II). First, a com-parison between debt structures in emerging marketcountries and advanced economies highlights char-acteristics that make advanced economies less crisisprone. Second, a comparison between sovereignsand corporates highlights the roles of equity and se-niority in corporate liability structures, with poten-tial applications in the sovereign context.

Compared with advanced economies, emergingmarket and developing countries find it relativelydifficult to issue long-term debt in their own curren-cies. Greater reliance on short-term and foreign-currency debt is associated with a higher frequencyof debt crises (Section III). Short-term debt (or debt indexed to short-term domestic interest rates) is associated with vulnerability to sudden changes inmarket sentiment: worsening perceptions of thecountry’s creditworthiness can quickly feed intohigher interest costs, often leading to vicious circles.Similarly, with relatively large shares of foreign-currency debt, depreciations can abruptly render acountry insolvent.

Only a handful of the largest economies issue debtdenominated in their own currency on internationalmarkets, perhaps reflecting in part their economicsize and the use of their currencies as a vehicle for in-ternational trade. Bonds issued internationally areotherwise relatively homogeneous, usually taking the

form of fixed-rate bonds with relatively long maturi-ties. By contrast, the composition of debt issued do-mestically varies considerably across countries. Fewemerging markets issue large amounts of long-termlocal-currency debt, even in their domestic markets.But a number of them have increasingly made use ofdomestically issued alternatives to foreign-currencydebt, including short-term debt, inflation-indexeddebt, and floating-interest-rate debt.

Emerging market countries’ difficulties in issuinglong-term local-currency bonds on the domesticmarket seem to result from deeper problems, such aslack of monetary and fiscal policy credibility, and re-lated worries about the possibility of inflation or out-right default. While the requisite credibility may takea long time to build, several emerging market coun-tries have recently begun issuing local-currencybonds with maturities of a few years, and have reliedon inflation-indexed bonds for longer maturities.Compared with floating-rate and foreign-currencydebt, CPI indexation is less likely to lead to debtcrises, because it tends to not amplify the effects ofadverse shocks. Moreover, the development of do-mestic private pension funds often creates a naturalbase of investors seeking the protection againstchanges in purchasing power that CPI indexationprovides.

Regarding debt issued internationally, some inter-national financial institutions (IFIs) have often beenamong the first parties to issue bonds denominated inthe currencies of emerging markets (usually in com-bination with exchange rate swaps with emergingmarket residents that issue in one of the world’s maincurrencies). Opportunities to raise funds at more fa-vorable rates have been, and should continue to be,the primary motivation for the IFIs’ involvement inthese operations: the IFIs have been able to tap newinvestor bases interested in holding assets denomi-nated in emerging market currencies but bearing nodefault risk. This said, contributions to the develop-ment of new financial markets that can later betapped by developing countries are a welcome by-product of such funding decisions by the IFIs.

Ideas for Sovereigns from theCorporate Context: Explicit Seniority

Partly as a result of contract enforcement issues,sovereign liability structures both in emerging mar-ket countries and in advanced economies are not asrich as those of corporations. A notable difference isa lack of an explicit seniority structure, which at thecorporate level exists either by statute or throughbond covenants. As a result, sovereign creditors tendto be more exposed to “debt dilution” than do their

3

7It is difficult to estimate the extent to which the costs to thedomestic economy result from default itself rather than other as-pects—such as bank runs or sudden drops in the exchange rate—with which defaults are typically associated. Nevertheless, de-faults are associated with widespread bankruptcies, sizable joblosses, and declines in domestic demand. In addition, the negativedomestic implications of a forced debt restructuring are perceivedto be so traumatic that policymakers will delay this option untilall other possibilities have been exhausted (IMF, 2002a).

I OVERVIEW

corporate counterparts (Section IV). Debt dilutionoccurs when new debt reduces the claim that exist-ing creditors can hope to recover in the event of a de-fault. Long recognized as a problem in corporatedebt, dilution seems to have recently become a sig-nificant problem in emerging sovereign debt mar-kets. For example, by issuing large numbers of newbonds to a wide base of creditors in the 1990s, Ar-gentina drastically reduced the value of the initialbondholders’ claims.

Debt dilution has undesirable consequences forboth debt structures and the amounts and terms atwhich sovereigns borrow. Its adverse effects on debtstructure stem from investors’ efforts to hold debtforms that are harder to dilute—such as short-termdebt or debt that is costly to restructure. Such instru-ments in turn make the debtor more vulnerable tocrises and render the impact of crises more severe.Dilution also increases the likelihood that highly in-debted countries will overborrow. Countries near de-fault may be able to place new debt with investorswithout facing prohibitive interest rates, as the newcreditors effectively obtain a share of the existingcreditors’ debt recovery value. At low debt levels, theopposite problem may occur, as the possibility of di-lution tends to raise interest rates unnecessarily.

In principle, debt dilution could be ruled out by anexplicit, “first-in-time” seniority structure giving pri-ority to earlier debt issues, because in the event ofbankruptcy the original creditors would be repaidfirst. First-in-time seniority would tend to reduce bor-rowing costs at low debt levels, but make borrowingmore expensive at high debt levels. In fact, if the prob-ability of a debt crisis were substantial, markets wouldexpect a new debt issue to be junior to most outstand-ing debt in the event of a crisis, and thus demand ahigher interest rate compared to the present system.The effect on borrowing costs would reward prudentborrowing behavior and discourage overborrowing.Explicit seniority could also improve debt structuresby reducing incentives to issue “crisis-prone” debtforms that are hard to dilute.

Explicit seniority would also entail risks, however.In particular, an unavoidable consequence of limit-ing dilution and making new borrowing harder athigh levels of debt is that this may prevent somecountries from accessing debt markets in situationsof illiquidity, in turn increasing the likelihood of liq-uidity crises. Another potential drawback is that se-niority could complicate debt pricing and, as a re-sult, make debt more expensive (at least untilmarkets became familiar with the new system). Un-certainty would be increased by the possibility thatsovereigns find ways to circumvent seniority whentheir borrowing levels are elevated, for example, byobtaining direct bank loans under different jurisdic-tions or providing collateral for subsequent loans.

Finally, explicit seniority could have consequencesfor sovereign debt restructurings, an issue that is notanalyzed in this paper.

Explicit seniority in sovereign debt could be im-plemented in a number of ways, including statutes atthe international level; national statutes in debtorcountries and issuing jurisdictions; debt contracts; orsome combination of the three. This paper exploresideas for a contractual implementation of explicit se-niority in general terms and describes some of theobstacles. The two main difficulties that arise in acontractual framework are how to ensure that thesovereign continues to apply the first-in-time senior-ity structure to all subsequent borrowing and how toenforce the priority structure in the event of restruc-turing. This paper suggests an approach to deal withthose issues, although this area clearly requires fur-ther work.

While this paper concludes that explicit seniority isa novel approach to improving debt structures that isworthy of further research, it is only a first pass at theissue, and further research is needed before arrivingat a definite conclusion. In fact, while seniority couldbe beneficial for countries with moderate debt levels,it may make market access more difficult for coun-tries with elevated levels of debt: although desirablein many circumstances to prevent overborrowing,this could present new policy challenges. Moreover,an overall judgment would depend on the effects ofseniority on crisis resolution, which is not taken uphere. Further analysis would also be needed on howto overcome potential legal and practical obstacles tointroducing contract-based seniority. Nevertheless,given the potential benefits of explicit seniority forcrisis prevention—and other enhancements to bondcontracts that would also mitigate debt dilution—thispaper calls for further analysis and discussion of theissue.

Expanding the Set of Instruments:Real Indexation

Another key difference between sovereigns andcorporates is that sovereigns lack equity, or equity-like instruments, whereby investors would share insovereigns’ fortunes and misfortunes. Although equitycould never be fully reproduced in the sovereign con-text, the risk-sharing benefits of equity might be mim-icked through currently underutilized financial instru-ments with payment terms indexed to real variablessuch as gross domestic product (GDP) (Section V).

Real indexation involves higher payments wheneconomic performance is relatively strong, and lowerpayments when economic performance is relativelyweak. For example, countries could issue bonds providing for lower payments when GDP growth is

4

Toward Better Sovereign Debt Structures: A Road Map

weak or in the event of a natural disaster. Real index-ation would thus tend to stabilize the debt-to-GDPratio, providing two main benefits: first, it would re-duce the likelihood of debt crises and, second, itwould reduce the need for procyclical fiscal policies.

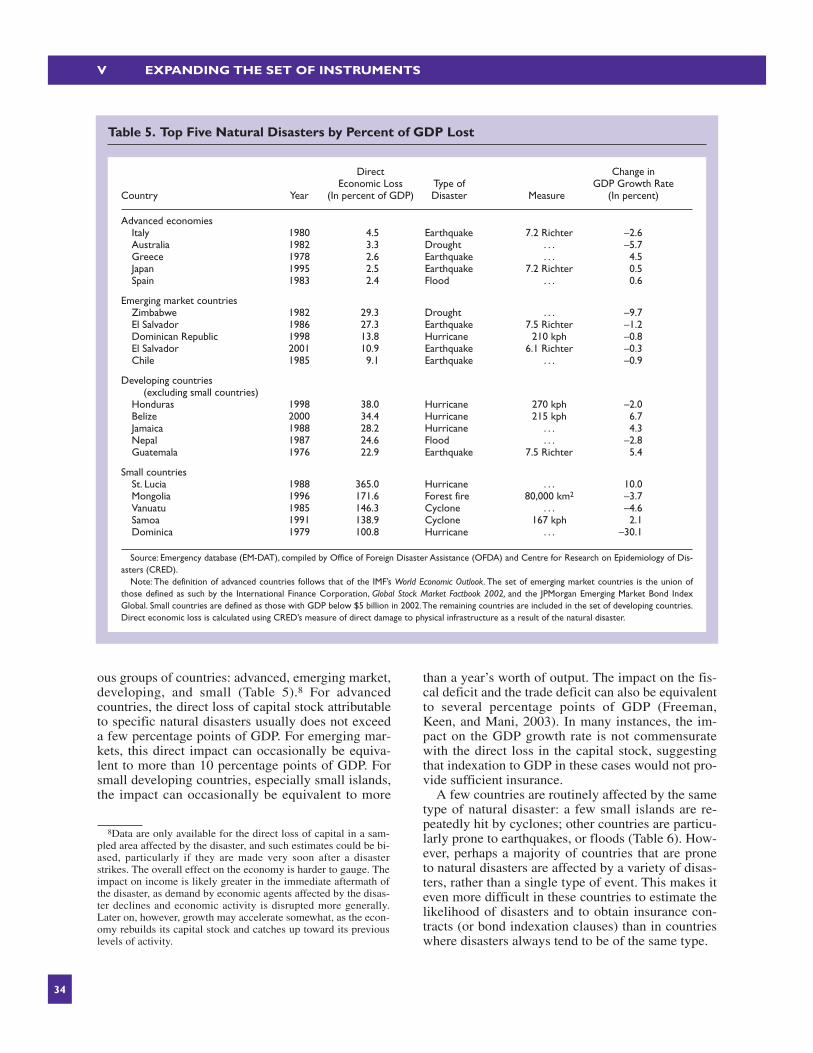

Indexation to variables largely outside the controlof the authorities, such as commodity prices, naturaldisasters, or output of trading partner countries,might provide considerable insurance benefits,though only to limited groups of countries. Indexa-tion to variables partly within the control of the au-thorities, such as GDP or exports, could provide sub-stantial insurance benefits to a broad spectrum ofcountries, though its introduction would presentgreater challenges.

The cost of such insurance for borrowing coun-tries is likely to depend on the extent to which anumber of obstacles can be overcome. In addition tothe need for large-scale issuance to ensure marketliquidity, the main obstacles seem to relate to theneed for investors to be able to hedge the risk in-volved in holding such instruments; the potential foropportunistic mismeasurement by country authori-ties of variables partly within their control; and pos-sible difficulties in pricing complex instruments.

The requisite large scale for launching new typesof bonds could be attained in the context of a debtrestructuring or through international coordination.Should a number of emerging markets issue GDP-indexed bonds, international investors holding aportfolio of such bonds would find GDP risk to bewell diversified, because the correlation of growthrates across emerging markets is typically very low.Reforms that would help overcome obstacles relatedto potential mismeasurement include strengtheningthe independence of national statistical agencies.

Toward Better Sovereign DebtStructures: A Road Map

Improved debt structures should not be viewed asa substitute for sound policies. Sound policies notonly reduce the likelihood of debt crises directly butare also a prerequisite for better debt structures andpossible financial innovations that would in turnmake countries less prone to crises. Nevertheless,this paper argues that improved debt structuresmight play a role in ameliorating economic perfor-mance and making crises both less likely and lessdamaging.

Historically, financial innovation seems to havetaken place in a somewhat haphazard manner, andhas often been prompted by intervention on the partof policymakers (Section VI). Innovations in theareas described above are unlikely to be an excep-tion to this historical norm, especially because the

incentives for individual market participants to inno-vate are likely to be lower than for the group as awhole.

A potential road map for implementing the policysteps analyzed in this paper is likely to require ef-forts by a number of different actors, includingcountry authorities, international investors, the inter-national community, and researchers.

Sound macroeconomic policies are by far themost important prerequisite for more desirable debtstructures. Indeed, excessive reliance on “risky”types of debt is primarily a symptom, rather than acause, of a perception of risk on the part of investors.Sound policies and credibility are also a precondi-tion for issuing new forms of debt, such as instru-ments involving elements of real indexation, and forminimizing potentially adverse effects on localbanking systems that may be large holders of gov-ernment debt.

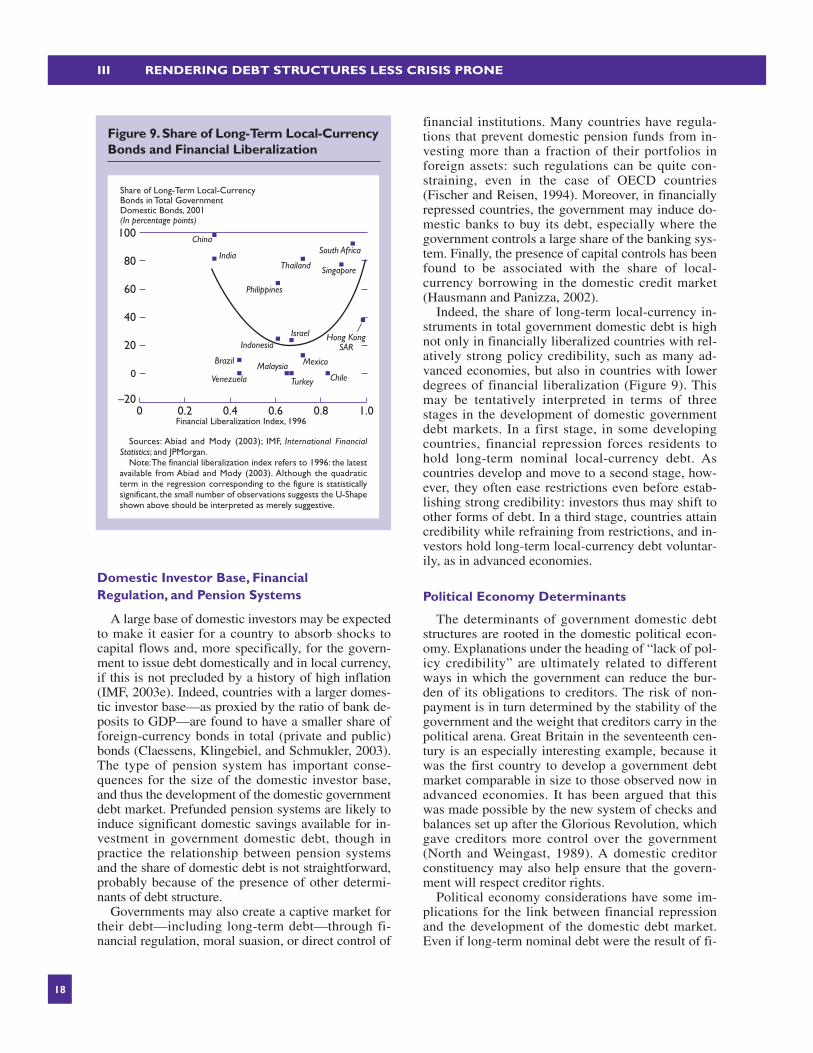

Beyond better policies, country authorities couldseek to create or deepen the market for local-currency-denominated debt by issuing, for example,local-currency-denominated bonds with shorter ma-turities, and inflation-indexed bonds for longer ma-turities. In doing so, they should be alert to opportu-nities provided by private pension systems thatcreate a natural demand for local-currency and infla-tion-indexed debt, and in some cases GDP-indexeddebt. In these endeavors, the authorities need to bemindful of sequencing: in countries where long-termlocal-currency-denominated debt is widely held as aresult of restrictions on capital flows or on the rangeof assets that banks and institutional investors canhold, it would be crucial to establish greater credibil-ity before lifting such restrictions.

There are advantages of using instruments withreturns indexed to real variables closely related to is-suing countries’ economic performance. For thosesmall countries that are especially vulnerable to nat-ural disasters, disaster insurance would seem to bedesirable if available at a reasonable cost. Greateruse of hedging against commodity price fluctuationswould also seem desirable for countries relying on asmall set of commodities in their export and revenuestructure. Larger, more diversified countries (bothadvanced and emerging) will be better hedgedagainst macroeconomic fluctuations if they issuebonds indexed to a key macroeconomic aggregate,such as GDP.

Financial market participants’ willingness to en-gage in a dialogue with the official sector, and sharetheir views, expertise, and concerns regarding poten-tial innovations is an indispensable ingredient forprogress in improving debt structures. Market partici-pants can only be expected to explore innovations thatmake good business sense for them. However, twosets of considerations suggest that market participants

5

I OVERVIEW

may collectively have an incentive to participate insuch a dialogue. First, the initial costs associated withinnovation (including learning costs) are lower whenshared by market participants as a group than if in-curred individually. Second, innovations—includingsome in which the official sector played a major role,such as the creation of Brady bonds—have occasion-ally helped expand the scope of financial markets,thereby generating business opportunities.

The IFIs should continue to track short-term debtand foreign-currency debt as indicators of vulnera-bility. They should also encourage countries to bor-row in local currency and with longer maturities,while recognizing that crisis-prone debt structurestypically result from underlying problems that them-selves need to be addressed. To the extent that highshares of short-term or foreign-currency debt reflectpolitical economy pressures (perhaps motivated bythe electoral calendar) on debt managers to attainshort-run interest cost “savings” at the expense ofundue increases in the risk of crises, conditionalitywith respect to debt structure could be considered,on a case-by-case basis. However, its desirabilitywould have to be weighed against the costs thatmight result, for example, from reducing capitalmarket access for countries where short-term andforeign-currency instruments are the only ways ofpreserving it—possibly in the context of an incipientliquidity crisis.

While the IFIs’ primary goal in deciding upon thecurrency composition of their own debt issuancemust remain the minimization of borrowing costs,market development may continue to be a welcomeby-product. The first bond issues in a currency unfa-miliar to international markets require substantial

additional preparatory work: the IFIs are wellplaced to work with the authorities toward that end,though the costs in terms of staff resources shouldnot be neglected.

If relatively underutilized instruments such as inflation- or GDP-indexed bonds are deemed desir-able, their emergence could be aided in a number ofways: international dialogue among potentially in-terested parties; strengthened independence of coun-tries’ statistical agencies; and technical assistance toimprove the quality and transparency of national in-come statistics.

A number of potential steps analyzed in thispaper—such as the creation of an international debtregistry to help monitor seniority features of sover-eign debt held by private agents—would take some-what longer to implement. The desirability and prac-tical feasibility of such innovations in theinstitutional framework could be further explored.

Additional research would seem especially desir-able in the following areas:

• the determinants and consequences of domesticdebt structures (including the collection of dataon domestic debt for a large number of coun-tries);

• empirical evidence on debt dilution and the theo-retical case for and against seniority in the sover-eign context;

• surveys of investors’ and borrowers’ attitudes to-ward financial innovation and obstacles relatedto it; and

• the development of pricing models for currentlyunderutilized financial instruments.

6

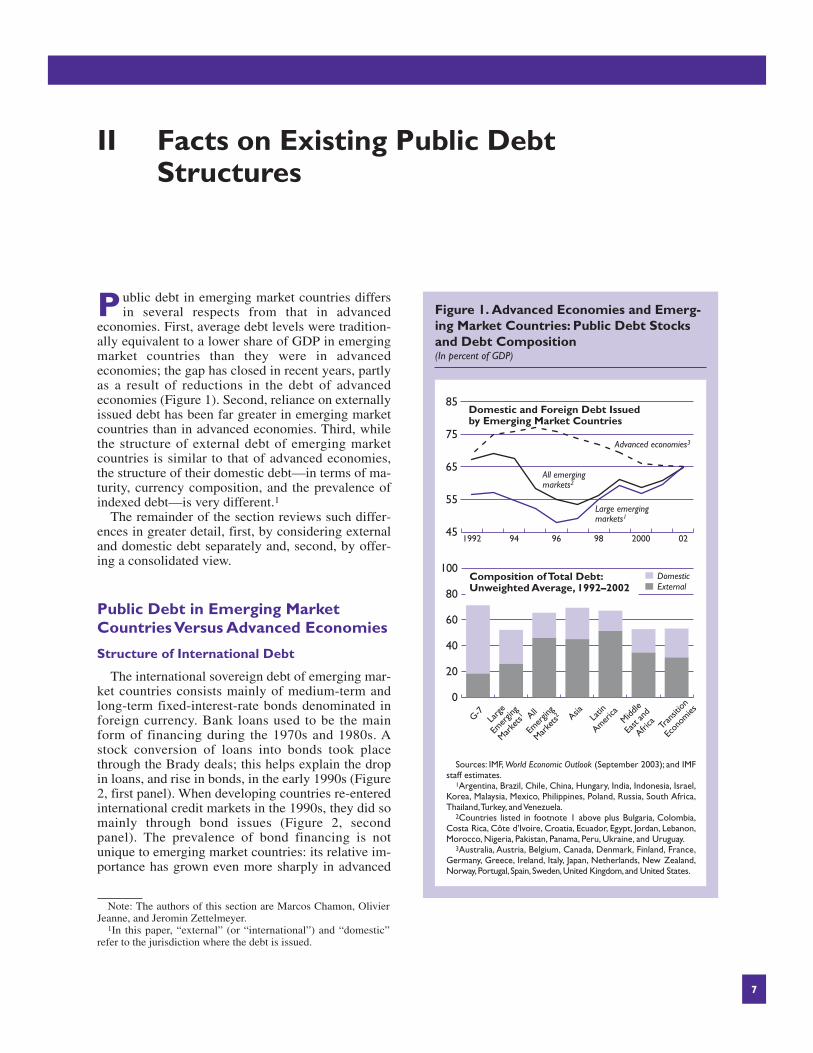

Public debt in emerging market countries differsin several respects from that in advanced

economies. First, average debt levels were tradition-ally equivalent to a lower share of GDP in emergingmarket countries than they were in advancedeconomies; the gap has closed in recent years, partlyas a result of reductions in the debt of advancedeconomies (Figure 1). Second, reliance on externallyissued debt has been far greater in emerging marketcountries than in advanced economies. Third, whilethe structure of external debt of emerging marketcountries is similar to that of advanced economies,the structure of their domestic debt—in terms of ma-turity, currency composition, and the prevalence ofindexed debt—is very different.1

The remainder of the section reviews such differ-ences in greater detail, first, by considering externaland domestic debt separately and, second, by offer-ing a consolidated view.

Public Debt in Emerging MarketCountries Versus Advanced Economies

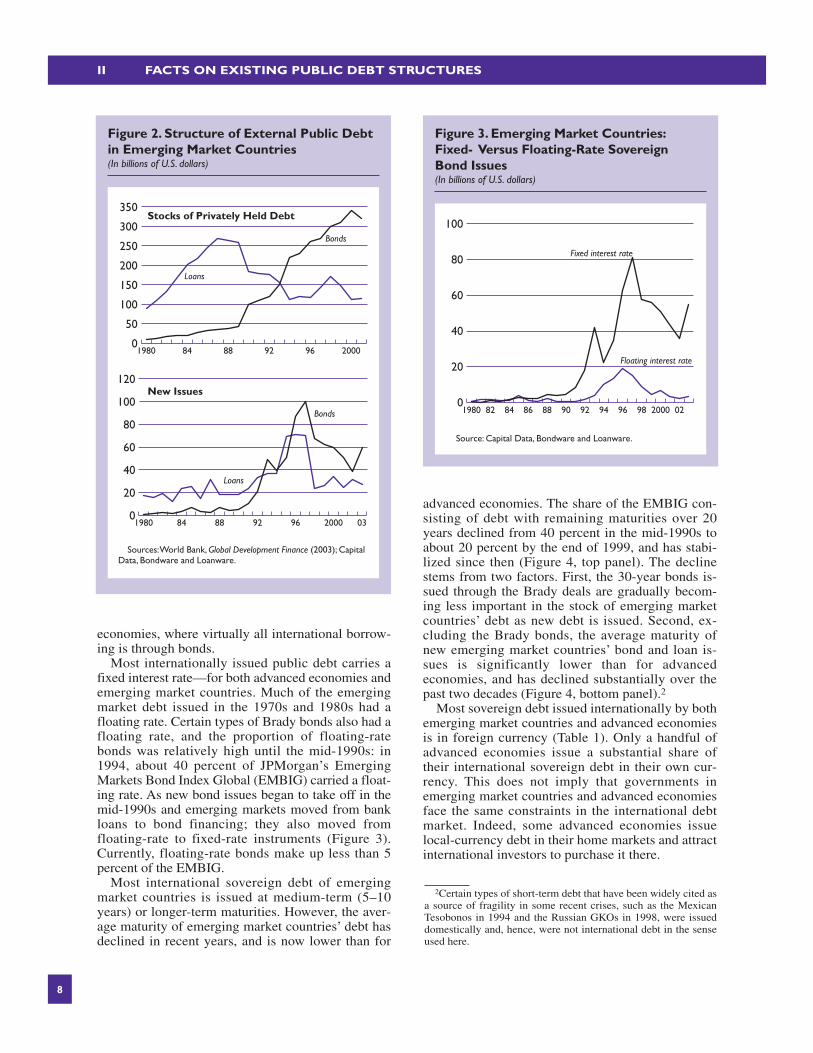

Structure of International Debt

The international sovereign debt of emerging mar-ket countries consists mainly of medium-term andlong-term fixed-interest-rate bonds denominated inforeign currency. Bank loans used to be the mainform of financing during the 1970s and 1980s. Astock conversion of loans into bonds took placethrough the Brady deals; this helps explain the dropin loans, and rise in bonds, in the early 1990s (Figure2, first panel). When developing countries re-enteredinternational credit markets in the 1990s, they did somainly through bond issues (Figure 2, secondpanel). The prevalence of bond financing is notunique to emerging market countries: its relative im-portance has grown even more sharply in advanced

II Facts on Existing Public Debt Structures

7

Note: The authors of this section are Marcos Chamon, OlivierJeanne, and Jeromin Zettelmeyer.

1In this paper, “external” (or “international”) and “domestic”refer to the jurisdiction where the debt is issued.

45

55

65

75

85

Advanced economies3

All emerging markets2

Large emerging markets1

0220009896941992

Domestic and Foreign Debt Issued by Emerging Market Countries

Composition of Total Debt:Unweighted Average, 1992–2002

0

20

40

60

80

100DomesticExternal

Tran

sition

Econ

omies

Middle

East

and

Africa

Latin

AmericaAsiaAll

Emer

ging

Marke

ts2

Larg

e

Emer

ging

Marke

ts1G-7

Figure 1. Advanced Economies and Emerg-ing Market Countries: Public Debt Stocksand Debt Composition(In percent of GDP)

Sources: IMF, World Economic Outlook (September 2003); and IMFstaff estimates.

1Argentina, Brazil, Chile, China, Hungary, India, Indonesia, Israel,Korea, Malaysia, Mexico, Philippines, Poland, Russia, South Africa,Thailand,Turkey, and Venezuela.

2Countries listed in footnote 1 above plus Bulgaria, Colombia,Costa Rica, Côte d’Ivoire, Croatia, Ecuador, Egypt, Jordan, Lebanon,Morocco, Nigeria, Pakistan, Panama, Peru, Ukraine, and Uruguay.

3Australia, Austria, Belgium, Canada, Denmark, Finland, France,Germany, Greece, Ireland, Italy, Japan, Netherlands, New Zealand,Norway,Portugal, Spain, Sweden,United Kingdom,and United States.

II FACTS ON EXISTING PUBLIC DEBT STRUCTURES

economies, where virtually all international borrow-ing is through bonds.

Most internationally issued public debt carries afixed interest rate—for both advanced economies andemerging market countries. Much of the emergingmarket debt issued in the 1970s and 1980s had afloating rate. Certain types of Brady bonds also had afloating rate, and the proportion of floating-ratebonds was relatively high until the mid-1990s: in1994, about 40 percent of JPMorgan’s EmergingMarkets Bond Index Global (EMBIG) carried a float-ing rate. As new bond issues began to take off in themid-1990s and emerging markets moved from bankloans to bond financing; they also moved from floating-rate to fixed-rate instruments (Figure 3).Currently, floating-rate bonds make up less than 5percent of the EMBIG.

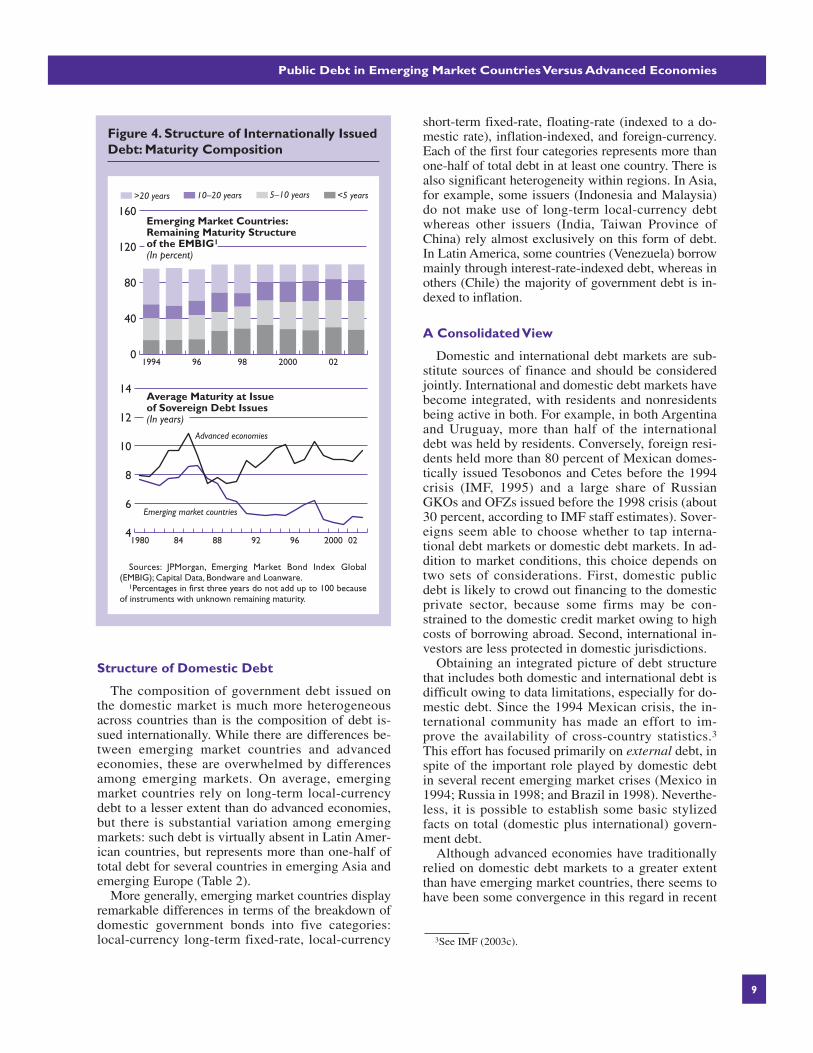

Most international sovereign debt of emergingmarket countries is issued at medium-term (5–10years) or longer-term maturities. However, the aver-age maturity of emerging market countries’ debt hasdeclined in recent years, and is now lower than for

advanced economies. The share of the EMBIG con-sisting of debt with remaining maturities over 20years declined from 40 percent in the mid-1990s toabout 20 percent by the end of 1999, and has stabi-lized since then (Figure 4, top panel). The declinestems from two factors. First, the 30-year bonds is-sued through the Brady deals are gradually becom-ing less important in the stock of emerging marketcountries’ debt as new debt is issued. Second, ex-cluding the Brady bonds, the average maturity ofnew emerging market countries’ bond and loan is-sues is significantly lower than for advancedeconomies, and has declined substantially over thepast two decades (Figure 4, bottom panel).2

Most sovereign debt issued internationally by bothemerging market countries and advanced economiesis in foreign currency (Table 1). Only a handful ofadvanced economies issue a substantial share oftheir international sovereign debt in their own cur-rency. This does not imply that governments inemerging market countries and advanced economiesface the same constraints in the international debtmarket. Indeed, some advanced economies issuelocal-currency debt in their home markets and attractinternational investors to purchase it there.

8

2Certain types of short-term debt that have been widely cited asa source of fragility in some recent crises, such as the MexicanTesobonos in 1994 and the Russian GKOs in 1998, were issueddomestically and, hence, were not international debt in the senseused here.

Stocks of Privately Held Debt

New Issues

0

50

100

150

200

250

300

350

Loans

Bonds

2000969288841980

0

20

40

60

80

100

120

Loans

Bonds

032000969288841980

Figure 2. Structure of External Public Debtin Emerging Market Countries(In billions of U.S. dollars)

Sources:World Bank, Global Development Finance (2003); CapitalData, Bondware and Loanware.

0

20

40

60

80

100

Floating interest rate

Fixed interest rate

0220009896949290888684821980

Figure 3. Emerging Market Countries:Fixed- Versus Floating-Rate Sovereign Bond Issues(In billions of U.S. dollars)

Source: Capital Data, Bondware and Loanware.

Public Debt in Emerging Market Countries Versus Advanced Economies

Structure of Domestic Debt

The composition of government debt issued onthe domestic market is much more heterogeneousacross countries than is the composition of debt is-sued internationally. While there are differences be-tween emerging market countries and advancedeconomies, these are overwhelmed by differencesamong emerging markets. On average, emergingmarket countries rely on long-term local-currencydebt to a lesser extent than do advanced economies,but there is substantial variation among emergingmarkets: such debt is virtually absent in Latin Amer-ican countries, but represents more than one-half oftotal debt for several countries in emerging Asia andemerging Europe (Table 2).

More generally, emerging market countries displayremarkable differences in terms of the breakdown ofdomestic government bonds into five categories:local-currency long-term fixed-rate, local-currency

short-term fixed-rate, floating-rate (indexed to a do-mestic rate), inflation-indexed, and foreign-currency.Each of the first four categories represents more thanone-half of total debt in at least one country. There isalso significant heterogeneity within regions. In Asia,for example, some issuers (Indonesia and Malaysia)do not make use of long-term local-currency debtwhereas other issuers (India, Taiwan Province ofChina) rely almost exclusively on this form of debt.In Latin America, some countries (Venezuela) borrowmainly through interest-rate-indexed debt, whereas inothers (Chile) the majority of government debt is in-dexed to inflation.

A Consolidated View

Domestic and international debt markets are sub-stitute sources of finance and should be consideredjointly. International and domestic debt markets havebecome integrated, with residents and nonresidentsbeing active in both. For example, in both Argentinaand Uruguay, more than half of the internationaldebt was held by residents. Conversely, foreign resi-dents held more than 80 percent of Mexican domes-tically issued Tesobonos and Cetes before the 1994crisis (IMF, 1995) and a large share of RussianGKOs and OFZs issued before the 1998 crisis (about30 percent, according to IMF staff estimates). Sover-eigns seem able to choose whether to tap interna-tional debt markets or domestic debt markets. In ad-dition to market conditions, this choice depends ontwo sets of considerations. First, domestic publicdebt is likely to crowd out financing to the domesticprivate sector, because some firms may be con-strained to the domestic credit market owing to highcosts of borrowing abroad. Second, international in-vestors are less protected in domestic jurisdictions.

Obtaining an integrated picture of debt structurethat includes both domestic and international debt isdifficult owing to data limitations, especially for do-mestic debt. Since the 1994 Mexican crisis, the in-ternational community has made an effort to im-prove the availability of cross-country statistics.3This effort has focused primarily on external debt, inspite of the important role played by domestic debtin several recent emerging market crises (Mexico in1994; Russia in 1998; and Brazil in 1998). Neverthe-less, it is possible to establish some basic stylizedfacts on total (domestic plus international) govern-ment debt.

Although advanced economies have traditionallyrelied on domestic debt markets to a greater extentthan have emerging market countries, there seems tohave been some convergence in this regard in recent

9

3See IMF (2003c).

0

40

80

120

160>20 years 10–20 years 5–10 years <5 years

02200098961994

Emerging Market Countries:Remaining Maturity Structure of the EMBIG1

(In percent)

Average Maturity at Issue of Sovereign Debt Issues(In years)

4

6

8

10

12

14

Emerging market countries

Advanced economies

022000969288841980

Figure 4. Structure of Internationally IssuedDebt: Maturity Composition

Sources: JPMorgan, Emerging Market Bond Index Global(EMBIG); Capital Data, Bondware and Loanware.

1Percentages in first three years do not add up to 100 becauseof instruments with unknown remaining maturity.

II FACTS ON EXISTING PUBLIC DEBT STRUCTURES

10

Table 1. External Sovereign Debt: Currency Composition, 1980–20031

(Unweighted average, in percent)

Emerging Market AdvancedCountries2 Economies3

Domestic currency4 0.3 7.5

Foreign currency 99.7 92.5U.S. dollar 54.8 42.4Euro 14.6 6.5Japanese yen 14.0 14.5Deutsche mark5 11.7 11.1European Currency Unit (ECU)5 . . . 8.0Others6 4.6 10.0

Source: IMF, Bonds, Equities and Loans database.1All bond and loan issues, 1980–2003.2Argentina, Brazil, Chile, China, Hungary, India, Indonesia, Israel, Korea, Malaysia, Mexico, Philippines, Poland, Rus-

sia, South Africa,Thailand,Turkey, and Venezuela.3Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Japan, Nether-

lands, New Zealand, Norway, Portugal, Spain, Sweden, United Kingdom, and United States.4Includes euro issues (but not European currency unit issues) for European Monetary Union member countries.5Prior to the introduction of the euro.6Includes Italian lira, British pound, French franc, and Swiss franc.

Table 2. Structure of Domestically Issued Government Bonds at End-2001(In percent of total)

DomesticDomestic-Currency-Denominated Bonds

Foreign-____________________________________________

Government Indexed to Currency-_____________________Bonds/GDP Not indexed Domestic Denominated______________________(In percent) Long term1 Short term1 interest rate Inflation Bonds

Emerging market countries 28.2 41.5 18.6 26.4 7.2 6.3

Latin America 24.0 5.6 13.7 50.8 16.6 13.4Brazil 52.1 9.5 0.0 53.0 7.0 30.5Chile2 . . . 0.0 21.0 0.0 55.8 23.2Mexico 11.0 12.8 23.6 60.1 3.5 0.0Venezuela 9.0 0.0 10.0 90.0 0.0 0.0

Asia 26.6 52.4 16.5 22.2 7.8 1.1India 27.0 81.6 18.4 0.0 0.0 0.0Indonesia 34.0 24.6 0.0 30.9 38.9 5.6Malaysia 36.3 0.0 19.8 80.2 0.0 0.0Thailand 13.8 91.5 8.5 0.0 0.0 0.0Philippines 22.0 64.2 35.8 0.0 0.0 0.0

Europe and others 32.4 56.5 23.6 13.6 0.4 5.9Czech Republic . . . 41.1 58.9 0.0 0.0 0.0Hungary 27.0 56.0 23.0 21.0 0.0 0.0Poland 16.0 62.6 26.5 10.9 0.0 0.0Slovak Republic 29.0 86.8 13.2 0.0 0.0 0.0South Africa 35.0 92.4 5.2 0.0 2.4 0.0Turkey 55.0 0.0 14.5 49.9 0.0 35.6

Sources: IMF staff estimates; and JPMorgan, Guide to Local Markets (2002).1Short term is defined as an initial maturity of less than one year, and long term is defined as an initial maturity of more than one year.2For Chile, the shares refer to bonds issued by the central bank.The amount of bonds issued domestically by the central government is negligible.

Sovereign Versus Corporate Liability Structures

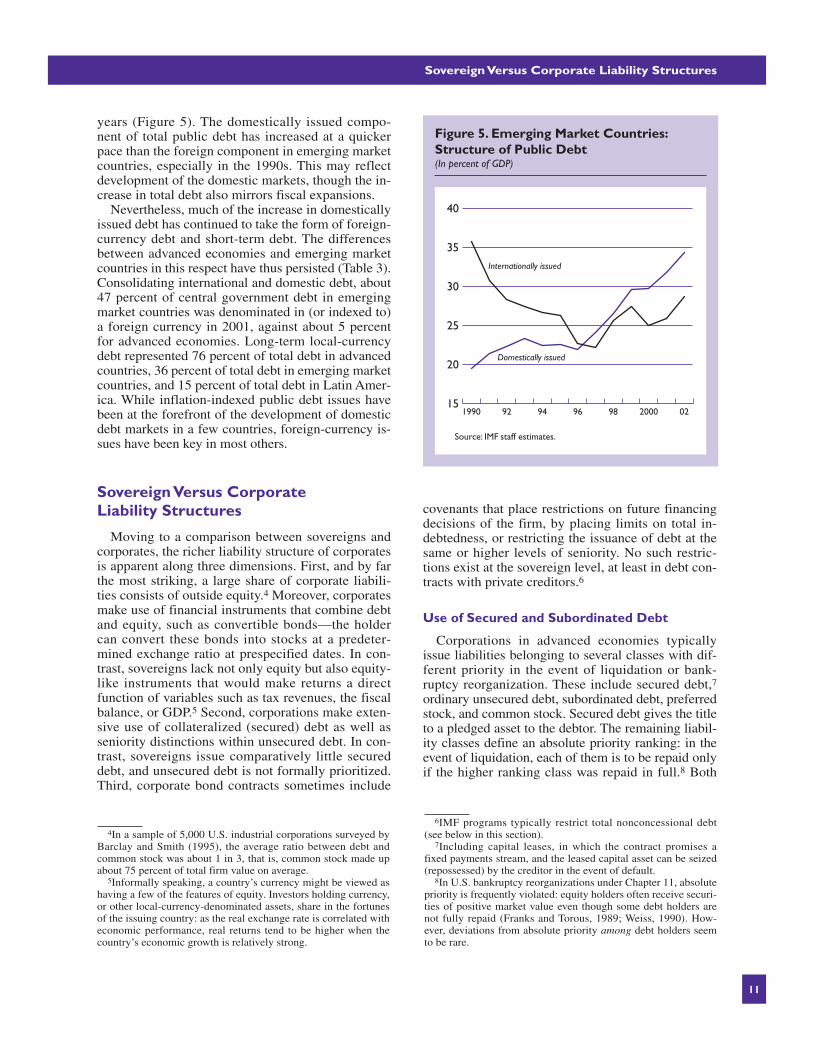

years (Figure 5). The domestically issued compo-nent of total public debt has increased at a quickerpace than the foreign component in emerging marketcountries, especially in the 1990s. This may reflectdevelopment of the domestic markets, though the in-crease in total debt also mirrors fiscal expansions.

Nevertheless, much of the increase in domesticallyissued debt has continued to take the form of foreign-currency debt and short-term debt. The differencesbetween advanced economies and emerging marketcountries in this respect have thus persisted (Table 3).Consolidating international and domestic debt, about47 percent of central government debt in emergingmarket countries was denominated in (or indexed to)a foreign currency in 2001, against about 5 percentfor advanced economies. Long-term local-currencydebt represented 76 percent of total debt in advancedcountries, 36 percent of total debt in emerging marketcountries, and 15 percent of total debt in Latin Amer-ica. While inflation-indexed public debt issues havebeen at the forefront of the development of domesticdebt markets in a few countries, foreign-currency is-sues have been key in most others.

Sovereign Versus Corporate Liability Structures

Moving to a comparison between sovereigns andcorporates, the richer liability structure of corporatesis apparent along three dimensions. First, and by farthe most striking, a large share of corporate liabili-ties consists of outside equity.4 Moreover, corporatesmake use of financial instruments that combine debtand equity, such as convertible bonds—the holdercan convert these bonds into stocks at a predeter-mined exchange ratio at prespecified dates. In con-trast, sovereigns lack not only equity but also equity-like instruments that would make returns a directfunction of variables such as tax revenues, the fiscalbalance, or GDP.5 Second, corporations make exten-sive use of collateralized (secured) debt as well asseniority distinctions within unsecured debt. In con-trast, sovereigns issue comparatively little secureddebt, and unsecured debt is not formally prioritized.Third, corporate bond contracts sometimes include

covenants that place restrictions on future financingdecisions of the firm, by placing limits on total in-debtedness, or restricting the issuance of debt at thesame or higher levels of seniority. No such restric-tions exist at the sovereign level, at least in debt con-tracts with private creditors.6

Use of Secured and Subordinated Debt

Corporations in advanced economies typicallyissue liabilities belonging to several classes with dif-ferent priority in the event of liquidation or bank-ruptcy reorganization. These include secured debt,7ordinary unsecured debt, subordinated debt, preferredstock, and common stock. Secured debt gives the titleto a pledged asset to the debtor. The remaining liabil-ity classes define an absolute priority ranking: in theevent of liquidation, each of them is to be repaid onlyif the higher ranking class was repaid in full.8 Both

11

6IMF programs typically restrict total nonconcessional debt(see below in this section).

7Including capital leases, in which the contract promises afixed payments stream, and the leased capital asset can be seized(repossessed) by the creditor in the event of default.

8In U.S. bankruptcy reorganizations under Chapter 11, absolutepriority is frequently violated: equity holders often receive securi-ties of positive market value even though some debt holders arenot fully repaid (Franks and Torous, 1989; Weiss, 1990). How-ever, deviations from absolute priority among debt holders seemto be rare.

4In a sample of 5,000 U.S. industrial corporations surveyed byBarclay and Smith (1995), the average ratio between debt andcommon stock was about 1 in 3, that is, common stock made upabout 75 percent of total firm value on average.

5Informally speaking, a country’s currency might be viewed ashaving a few of the features of equity. Investors holding currency,or other local-currency-denominated assets, share in the fortunesof the issuing country: as the real exchange rate is correlated witheconomic performance, real returns tend to be higher when thecountry’s economic growth is relatively strong.

15

20

25

30

35

40

Domestically issued

Internationally issued

022000989694921990

Figure 5. Emerging Market Countries:Structure of Public Debt(In percent of GDP)

Source: IMF staff estimates.

II FACTS ON EXISTING PUBLIC DEBT STRUCTURES

12

Table 3. Structure of Total (Domestic and External) Central GovernmentDebt, 2001(In percent of total)

Long-Term Total Debt as a Foreign-Currency Domestic- Share of GDP

Debt1 Currency Debt1 (In percent)

Emerging market countries 47.1 35.7 48.8

Latin America 67.9 15.2 37.0Argentina 96.8 . . . 53.7Brazil 43.82 3.33, 4 66.22, 5

Chile 92.7 0.0 15.6Mexico 35.6 57.56 22.6Venezuela 70.6 0.0 27.0

Asia 29.3 53.7 56.5China 17.7 82.3 24.0India 14.5 69.97 65.17

Indonesia 46.0 51.06 90.9Malaysia 16.7 0.0 69.2Philippines 47.4 17.68 64.9Thailand 33.6 78.8 24.8

Others 47.6 17.4 51.3Poland 34.8 34.8 39.3Russia 90.3 . . . 50.0South Africa 14.4 61.23, 4, 8 46.8Hungary 30.1 44.09 52.1Turkey 68.2 0.0 68.5

Advanced economies6 5.6 75.9 51.8Australia 0.53 85.53 10.1Belgium 1.3 80.4 101.2Canada 6.03 41.53 40.3Denmark 12.1 69.0 52.5Finland 16.3 66.7 45.4France 0.0 92.0 49.4Germany 0.0 97.0 35.3Italy 3.2 86.8 102.6Japan 0.0 74.8 121.6Netherlands 0.0 81.0 43.1New Zealand 18.53 48.23 31.2Norway 3.73 60.53 18.4Portugal 8.6 87.4 58.9Spain 4.13 83.83 47.2Sweden 20.1 55.9 51.6United Kingdom 1.4 60.5 38.6United States 0.0 58.8 33.1

Sources: IMF staff; OECD, Central Government Debt Yearbook 1992–2001; and websites of the country authorities.1In percent of total central government debt for emerging market countries and total central government mar-

ketable debt for advanced economies.2Includes debt held by the Central Bank.3Based on residual maturity.4Only marketable domestic-currency bonds.5Consolidated government debt.6Includes debt indexed to inflation and domestic interest rates.7Includes debt owed to National Small Savings Funds.8Includes debt with maturities of three years or more.9Data for 2002.

Sovereign Versus Corporate Liability Structures

secured and subordinated debt make up significantportions of the corporate debt stock.9

In contrast, sovereign liabilities generally fall intojust two classes—secured debt and unsecured debt.Within the unsecured debt class, there is no distinc-tion between ordinary debt and subordinated debt.Secured sovereign claims are generally collateralizedby future receipts, such as oil revenue or other exportreceivables (Chalk, 2002; and IMF, 2003d). To serveas collateral, future receipts need to be removed fromthe direct control of the sovereign, that is, the transac-tions associated with future receipts need to occurunder foreign jurisdiction. For this reason, collateral-ized future receipts typically involve export revenuesaccruing to the government (usually through a publicenterprise), rather than domestic tax revenues.

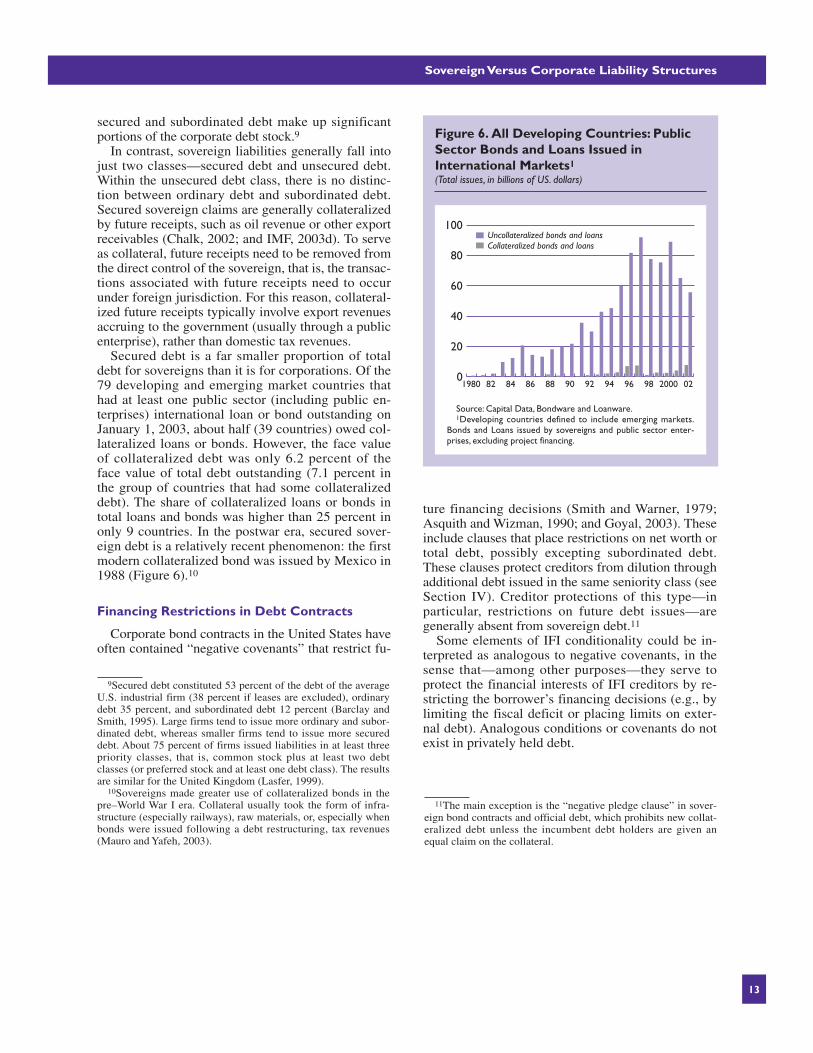

Secured debt is a far smaller proportion of totaldebt for sovereigns than it is for corporations. Of the79 developing and emerging market countries thathad at least one public sector (including public en-terprises) international loan or bond outstanding onJanuary 1, 2003, about half (39 countries) owed col-lateralized loans or bonds. However, the face valueof collateralized debt was only 6.2 percent of theface value of total debt outstanding (7.1 percent inthe group of countries that had some collateralizeddebt). The share of collateralized loans or bonds intotal loans and bonds was higher than 25 percent inonly 9 countries. In the postwar era, secured sover-eign debt is a relatively recent phenomenon: the firstmodern collateralized bond was issued by Mexico in1988 (Figure 6).10

Financing Restrictions in Debt Contracts

Corporate bond contracts in the United States haveoften contained “negative covenants” that restrict fu-

ture financing decisions (Smith and Warner, 1979;Asquith and Wizman, 1990; and Goyal, 2003). Theseinclude clauses that place restrictions on net worth ortotal debt, possibly excepting subordinated debt.These clauses protect creditors from dilution throughadditional debt issued in the same seniority class (seeSection IV). Creditor protections of this type—inparticular, restrictions on future debt issues—aregenerally absent from sovereign debt.11

Some elements of IFI conditionality could be in-terpreted as analogous to negative covenants, in thesense that—among other purposes—they serve toprotect the financial interests of IFI creditors by re-stricting the borrower’s financing decisions (e.g., bylimiting the fiscal deficit or placing limits on exter-nal debt). Analogous conditions or covenants do notexist in privately held debt.

13

9Secured debt constituted 53 percent of the debt of the averageU.S. industrial firm (38 percent if leases are excluded), ordinarydebt 35 percent, and subordinated debt 12 percent (Barclay andSmith, 1995). Large firms tend to issue more ordinary and subor-dinated debt, whereas smaller firms tend to issue more secureddebt. About 75 percent of firms issued liabilities in at least threepriority classes, that is, common stock plus at least two debtclasses (or preferred stock and at least one debt class). The resultsare similar for the United Kingdom (Lasfer, 1999).

10Sovereigns made greater use of collateralized bonds in thepre–World War I era. Collateral usually took the form of infra-structure (especially railways), raw materials, or, especially whenbonds were issued following a debt restructuring, tax revenues(Mauro and Yafeh, 2003).

11The main exception is the “negative pledge clause” in sover-eign bond contracts and official debt, which prohibits new collat-eralized debt unless the incumbent debt holders are given anequal claim on the collateral.

0

20

40

60

80

100Uncollateralized bonds and loansCollateralized bonds and loans

0220009896949290888684821980

Figure 6. All Developing Countries: PublicSector Bonds and Loans Issued inInternational Markets1

(Total issues, in billions of US. dollars)

Source: Capital Data, Bondware and Loanware.1Developing countries defined to include emerging markets.

Bonds and Loans issued by sovereigns and public sector enter-prises, excluding project financing.

Existing debt structures in emerging market coun-tries seem to rely excessively on risky forms of

debt—such as short-term and foreign-currencydebt—which may amplify the economic cycle, in-crease the likelihood of crises, and make crises moredifficult to manage. Increases in risky forms of debtmay be the result of worsening debt sustainability,but they also reinforce the rise in vulnerability.

Problems with the Status Quo

Short-Term Debt

Empirical studies have found short-term debt to bea leading indicator of vulnerability to internationalfinancial crises (Bussière and Mulder, 1999; and Ro-drik and Velasco, 1999). Theoretical models haveput forward two types of mechanisms to explain thisempirical association.

First, short-term debt may make governmentsmore vulnerable to debt rollover crises. Indeed, thisseems to have been an important factor in triggeringthe recent crises in Mexico (1994) and Russia(1998). In the extreme case of a pure liquidity crisis,investors stop lending to the government simply be-cause they expect others to do the same. If the aver-age maturity of the debt is low, the government isthen at the mercy of self-fulfilling creditor panicsthat can be triggered by shifts in market sentiment(Sachs, 1984; Alesina, Prati, and Tabellini, 1990;Cole and Kehoe, 2000; and Chamon, 2003). In theless extreme but probably more realistic case wherethe crisis mixes elements of illiquidity and insol-vency, the government would be vulnerable to apiece of bad news, whose real impact would be am-plified by creditors’ unwillingness to roll over theirclaims (Jeanne, 2004; in the corporate context, seeDiamond, 1991).

Second, short-term debt can give rise to viciouscircles stemming from the two-way interaction be-

tween debt levels and interest rates. If the debt has ashort maturity or bears a floating interest rate,changes not only in the international interest ratesbut also in the country’s own creditworthiness willaffect the interest bill relatively quickly. A sovereignwith a high level of short-term debt may thus find it-self trapped in a bad equilibrium in which high inter-est payments lead to a high probability of default,which in turn increases the default risk premium andthe interest rate (Calvo, 1988).

More generally, the relatively short average matu-rity of debt in emerging markets may also amplifythe economic cycle. In emerging market countries,economic downturns are typically associated withincreases in interest rates because of increases in thedefault and devaluation risk premiums, thus reduc-ing the scope for countercyclical fiscal policies.1

Foreign-Currency Debt

The vulnerabilities created by significant levels ofdebt denominated in (or indexed to) a foreign cur-rency have also been evident in several recent crises,an aspect emphasized, for both private and publicdebt, in the balance sheet approach to crises (Allenand others, 2002). In fact, the depreciation of the localcurrency has often led to a sharp increase in govern-ment debt as a share of domestic GDP or fiscal re-ceipts (Figure 7). The contribution of this revaluationwas especially large in Argentina and Uruguay—twocountries where the fraction of debt denominated inforeign currency and the depreciation of the local cur-rency were substantial. By contrast, it was small inKorea, where the government had little foreign-currency debt, and in Turkey, where the real deprecia-tion of the currency was moderate.

Not only does foreign-currency debt make crisesmore severe but it also reduces the scope for domes-tic policies to alleviate the impact of crises. The

III Rendering Debt Structures Less Crisis Prone with Existing Instruments

14

1GDP growth is negatively correlated with the spread on foreign-currency bonds issued internationally by emerging mar-ket countries (Eichengreen and Mody, 1998). This effect is likelyaugmented, for domestic currency borrowing, by the expected de-preciation premium.

Note: The authors of this section are Marcos Chamon andOlivier Jeanne.

Determinants of Government Debt Structure

revaluation of government debt amplifies the initialfiscal problem and reduces the ability of the govern-ment to implement policies that might mitigate thedisruption in the private sector (Jeanne andZettelmeyer, 2002). In addition, monetary policycannot be used to inflate foreign-currency debt away.The government is faced with the well-known andmuch-debated dilemma of choosing between raisingthe interest rate and letting the currency depreciate,with both options having adverse effects on domes-tic balance sheets.

Such amplification mechanisms resulting fromhigh shares of foreign-currency debt create the poten-tial for vicious circles and can thus make countriesmore vulnerable to crises in the first place. Imbal-ances in domestic balance sheets would lead investorsto attack the local currency; with the resulting depre-ciation, balance sheets would in turn deteriorate evenfurther (Krugman, 1999; Aghion, Bacchetta, andBanerjee, 2001; and Jeanne and Zettelmeyer, 2002).

Determinants of Government Debt Structure

Why do governments in emerging market coun-tries and their lenders settle on debt that seems to beunduly crisis prone, even though they are the firstones to suffer the costs in a crisis? Lack of credibilityof monetary and fiscal policies seems to be an impor-tant factor. Other factors may also be at work, includ-ing the nature of the domestic investor base and char-acteristics of domestic financial regulation (in thecase of domestic debt), as well as the country’s eco-nomic size (in the case of international debt).

Credibility of Monetary and Fiscal Policies

Governments in many emerging market countriescannot borrow on the same terms as advancedeconomies because of lack of credibility of mone-tary and fiscal policies. Unsustainable policies leadcreditors to anticipate that the government will ex-propriate them in one way or another—directlythrough a default or indirectly through inflation ifdebt is denominated in local currency. Thus, not onlydo governments face higher and more volatile inter-est rates, and—from time to time—loss of marketaccess, but they are also under pressure to issue debtinstruments that are more prone to crises.

Lack of credibility plays an especially importantrole in the period leading up to crises, as govern-ments tend to shift the composition of their debt to-ward shorter maturities and foreign-currency de-nomination. Notable examples include Mexico’sshift to Tesobonos in 1994 and Brazil’s switch to-

ward short-term, foreign-currency, and floating-ratedebt in 1998.2 These examples are consistent withthe view that short-term debt is a symptom, ratherthan a cause, of an impending crisis.3 With a loom-ing crisis, investors would usually prefer to holdshort-term debt for two reasons:

• Dilution. First, investors holding short-term debtmay expect the government to repay them beforethe default actually takes place (Rogoff, 1999).Thus issuing short-term debt dilutes the out-standing long-term debt.4

15

2In the period leading up to Mexico’s 1994 crisis, both thestock of Tesobonos and the interest rate differential between thepeso-denominated Cetes and the dollar-linked Tesobonos rosesharply (IMF, 1995, pp. 53–69, Figures I–6 and I–7).

3Indeed, systematic panel regressions show that, while highershares of short-term debt are associated with greater likelihood ofdebt crises, that association is no longer significant when takinginto account that greater use of short-term debt is itself influencedby other factors, including low credibility (Detragiache andSpilimbergo, 2001).

4Anticipating dilution, investors could be reluctant to lend on along-term basis or be willing to do so only at high interest rates(Bolton and Jeanne, 2004). In fact, the government could useshort-term debt to postpone the necessary adjustment at the ex-pense of long-term creditors. However, such dilution might turnout to be desirable, even for long-term creditors, if it bought timeto permit the necessary adjustment and avoided a default.

0

20

40

60

80

100

120Contribution of exchange rate depreciationIncrease in the public debt-to-GDP ratio

Argen

tina

2000

–02Uru

guay

2000

–02Tu

rkey

2000

–02

Braz

il

2000

–02

Russia

1997

–99

Indon

esia

1996

–98

Korea

1996

–98Tha

iland

1997

–98

Figure 7. Recent Crises: Impact ofExchange Rate Depreciation on PublicDebt-to-GDP Ratio1

(In percentage points of GDP)

Sources: IMF, Country Reports and International Financial Statistics.1The contribution of exchange rate depreciation is measured as

the increase in the precrisis debt-to-GDP ratio that results fromsetting the precrisis real exchange rate to its postcrisis level.

III RENDERING DEBT STRUCTURES LESS CRISIS PRONE

• Discipline. Second, investors may expect that ifthe government deviated from desirable policies,it would soon face higher interest rates or a roll-over crisis (Diamond, 1993; Diamond and Rajan,2001; and Jeanne, 2004). Short-term debt may bethe best option when the need for discipline out-weighs the expected costs—to both the borrowerand its lenders—resulting from the possibility ofa rollover crisis.

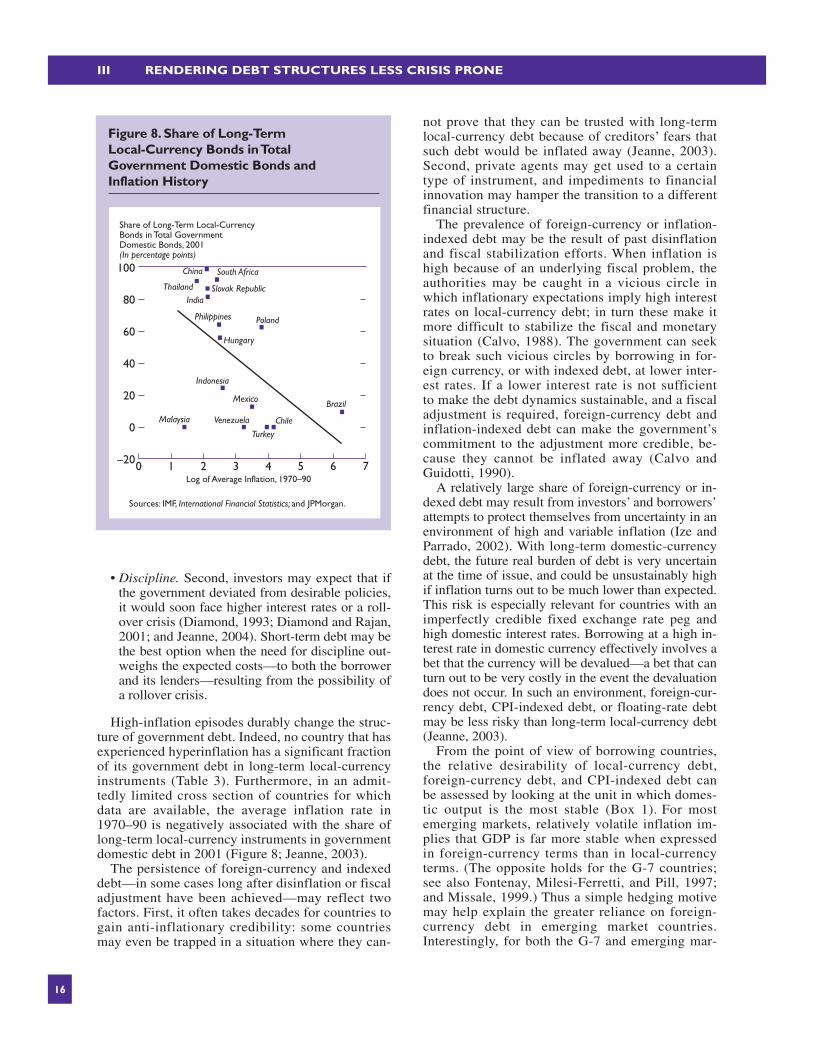

High-inflation episodes durably change the struc-ture of government debt. Indeed, no country that hasexperienced hyperinflation has a significant fractionof its government debt in long-term local-currencyinstruments (Table 3). Furthermore, in an admit-tedly limited cross section of countries for whichdata are available, the average inflation rate in1970–90 is negatively associated with the share oflong-term local-currency instruments in governmentdomestic debt in 2001 (Figure 8; Jeanne, 2003).

The persistence of foreign-currency and indexeddebt—in some cases long after disinflation or fiscaladjustment have been achieved—may reflect twofactors. First, it often takes decades for countries togain anti-inflationary credibility: some countriesmay even be trapped in a situation where they can-

not prove that they can be trusted with long-termlocal-currency debt because of creditors’ fears thatsuch debt would be inflated away (Jeanne, 2003).Second, private agents may get used to a certaintype of instrument, and impediments to financialinnovation may hamper the transition to a differentfinancial structure.

The prevalence of foreign-currency or inflation-indexed debt may be the result of past disinflationand fiscal stabilization efforts. When inflation ishigh because of an underlying fiscal problem, theauthorities may be caught in a vicious circle inwhich inflationary expectations imply high interestrates on local-currency debt; in turn these make itmore difficult to stabilize the fiscal and monetarysituation (Calvo, 1988). The government can seekto break such vicious circles by borrowing in for-eign currency, or with indexed debt, at lower inter-est rates. If a lower interest rate is not sufficient to make the debt dynamics sustainable, and a fiscaladjustment is required, foreign-currency debt andinflation-indexed debt can make the government’scommitment to the adjustment more credible, be-cause they cannot be inflated away (Calvo andGuidotti, 1990).

A relatively large share of foreign-currency or in-dexed debt may result from investors’ and borrowers’attempts to protect themselves from uncertainty in anenvironment of high and variable inflation (Ize andParrado, 2002). With long-term domestic-currencydebt, the future real burden of debt is very uncertainat the time of issue, and could be unsustainably highif inflation turns out to be much lower than expected.This risk is especially relevant for countries with animperfectly credible fixed exchange rate peg andhigh domestic interest rates. Borrowing at a high in-terest rate in domestic currency effectively involves abet that the currency will be devalued—a bet that canturn out to be very costly in the event the devaluationdoes not occur. In such an environment, foreign-cur-rency debt, CPI-indexed debt, or floating-rate debtmay be less risky than long-term local-currency debt(Jeanne, 2003).

From the point of view of borrowing countries,the relative desirability of local-currency debt,foreign-currency debt, and CPI-indexed debt canbe assessed by looking at the unit in which domes-tic output is the most stable (Box 1). For mostemerging markets, relatively volatile inflation im-plies that GDP is far more stable when expressed in foreign-currency terms than in local-currencyterms. (The opposite holds for the G-7 countries;see also Fontenay, Milesi-Ferretti, and Pill, 1997;and Missale, 1999.) Thus a simple hedging motivemay help explain the greater reliance on foreign-currency debt in emerging market countries. Interestingly, for both the G-7 and emerging mar-

16

Share of Long-Term Local-Currency Bonds in Total Government Domestic Bonds, 2001 (In percentage points)

Log of Average Inflation, 1970–900 1 2 3 4 5 6 7–20

0

20

40

60

80

100 China

Thailand

South Africa

Slovak RepublicIndia

Philippines

Hungary

Poland

Brazil

Indonesia

Mexico

Chile

Turkey

VenezuelaMalaysia

Figure 8. Share of Long-Term Local-Currency Bonds in Total Government Domestic Bonds and Inflation History

Sources: IMF, International Financial Statistics; and JPMorgan.

ket countries, the volatility of GDP is smallestwhen GDP is expressed in terms of CPI-indexedunits, suggesting that CPI-indexed bonds may provide substantial advantages to both groups ofcountries.

Finally, governments may borrow in foreign cur-rency to reduce nominal interest payments (whichare high in local-currency terms owing to the infla-tion premium) and thus the headline fiscal deficit(Blejer and Cheasty, 1991). Typical measures of

the public deficit take into account the flow of in-terest payments but not the changes in the realvalue of the principal due to currency depreciationor inflation.5

17

Determinants of Government Debt Structure

Box 1. Debt Structure and Hedging

In assessing the relative merits of local-currencydebt, foreign-currency debt, and inflation-indexed debt,a key criterion is which type of debt results in the low-est probability of the debt-to-GDP ratio exceeding agiven threshold. This is equivalent to asking whetherthe volatility of output is lowest when output is ex-pressed in terms of local currency, dollars, or the con-sumer price index. In fact, debt commits the borrowerto repay a fixed quantity in terms of some unit—thelocal currency, a foreign currency, or, for inflation-indexed debt, a price index. For example, a 10-yeardollar-denominated zero coupon bond issued in 2004commits the government to repay a certain quantity D$

of dollars in 2014. Assuming that this is the only debtissued by the government, the debt-to-GDP ratio in2014 is given by D$/Y$, where Y$ is the country’s GDP in 2014 expressed in terms of dollars. Viewed from2004, the principal debt repayment due is known (with no uncertainty): the likelihood that the debt-to-

GDP ratio will exceed a given threshold is therefore en-tirely determined by the volatility of Y$. More gener-ally, debt denominated in unit A is preferable to debtdenominated in unit B if output is less variable whenexpressed in unit A than in unit B. Thus one way of as-sessing the relative desirability of local-currency debt,dollar debt, and CPI-indexed debt is simply to comparethe volatility of output expressed in terms of local cur-rency, dollars, and the consumer price index. In the ex-ercise conducted below, volatility is defined more pre-cisely as the standard deviation of those changes in the10-year growth rate of output (in each of the threeunits, considered in turn) that cannot be predicted on the basis of past output growth. For advancedeconomies, or G-7 countries, the volatility of output islower when denominated in local currency than it iswhen denominated in foreign currency, but for emerg-ing market countries, this is reversed, owing to theirhigher and more volatile inflation.

5Several countries where inflation is an important considera-tion report an “operational” fiscal balance that includes the effectof inflation on the debt principal.

0

50

100

150

200

250

Dollar Indexed

Inflation Indexed

Local Currency

Emerging Market Countries

0

5

10

15

20

25

Dollar Indexed

Inflation Indexed

Local Currency

Advanced Economies

SD of Cumulative GDP Growth

SD of Cumulative GDP Growth

Standard Deviation of Cumulative 10-Year Unexpected Growth(In percentage points)

Source: IMF, International Financial Statistics.Note:The sample of emerging markets consists of 11 countries. (None experienced annual inflation rates higher than 100 percent in any year

during 1955–2000).The result that GDP is more stable when expressed in foreign-currency terms rather than in local-currency terms becomeseven more striking when countries that experienced inflation rates above 100 percent are included in the sample. The sample of advancedeconomies consists of 21 countries. Unexpected output growth is the difference between actual growth and the growth predicted by an autore-gressive (AR (1)) process.The sample period is 1965–2000. For a given year, growth is predicted for the subsequent 10 years based on data forthe previous 20 years.

Domestic Investor Base, Financial Regulation, and Pension Systems