southern acids (m) berhad shareholders’ briefing audited fy10 results 28 october 2010 delivering...

TRANSCRIPT

SOUTHERN ACIDS (M) BERHAD

Shareholders’ BriefingAudited FY10 Results

28 October 2010

DELIVERING QUALITY SINCE 1981

Contents

2

1. Group Financial Highlights

5. Share Price Performance

4. Dividend Record

2. Review of Major Operations

3. 5-Year Financial Performance

3

GroupFinancial

Highlights

4

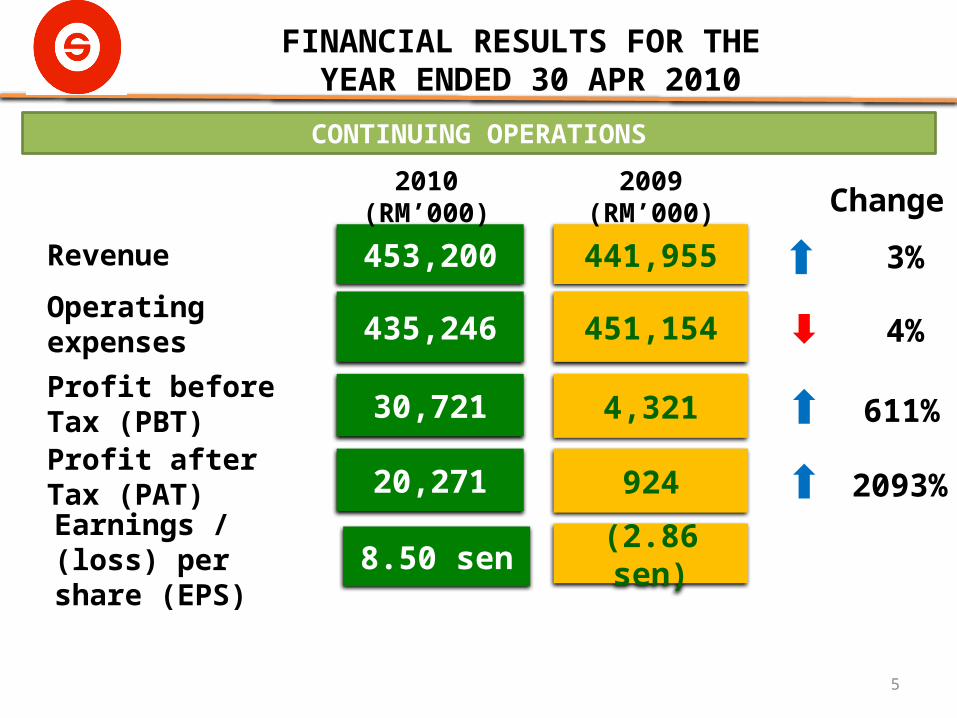

FINANCIAL RESULTS FOR THE YEAR ENDED 30 APR 2010

Oleochemical

Palm Oil Plantation

Healthcare

Warehousing & Port Cargo Handling

Investment & management

Continuing Operations

5

FINANCIAL RESULTS FOR THE YEAR ENDED 30 APR 2010

453,200 441,955

2010 (RM’000) 2009 (RM’000) Change

3%

4%

611%

435,246

30,721

451,154

4,321Profit before Tax (PBT)

Operating expenses

Revenue

CONTINUING OPERATIONS

8.50 sen (2.86 sen)Earnings / (loss) per share (EPS)

20,271Profit after Tax (PAT) 924 2093%

6

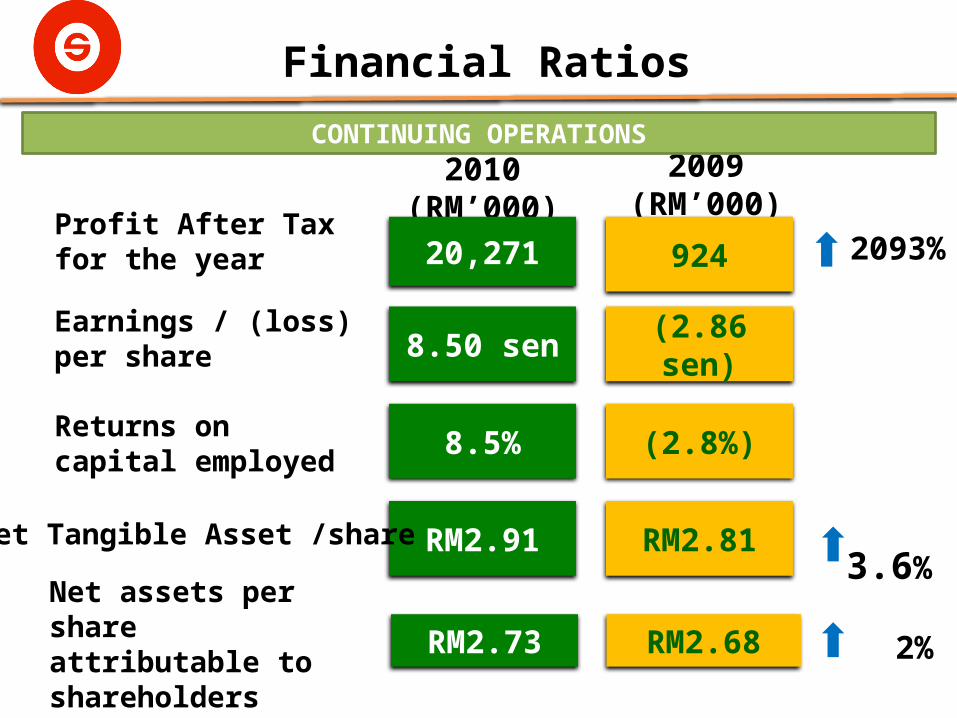

Financial Ratios

2009 (RM’000)

Returns on capital employed

8.5% (2.8%)

RM2.91 RM2.81

Net assets per share attributable to shareholders

(2.86 sen)8.50 senEarnings / (loss) per share

2010 (RM’000)

CONTINUING OPERATIONS

92420,271Profit After Tax for the year 2093%

3.6%

RM2.73 RM2.68

Net Tangible Asset /share

2%

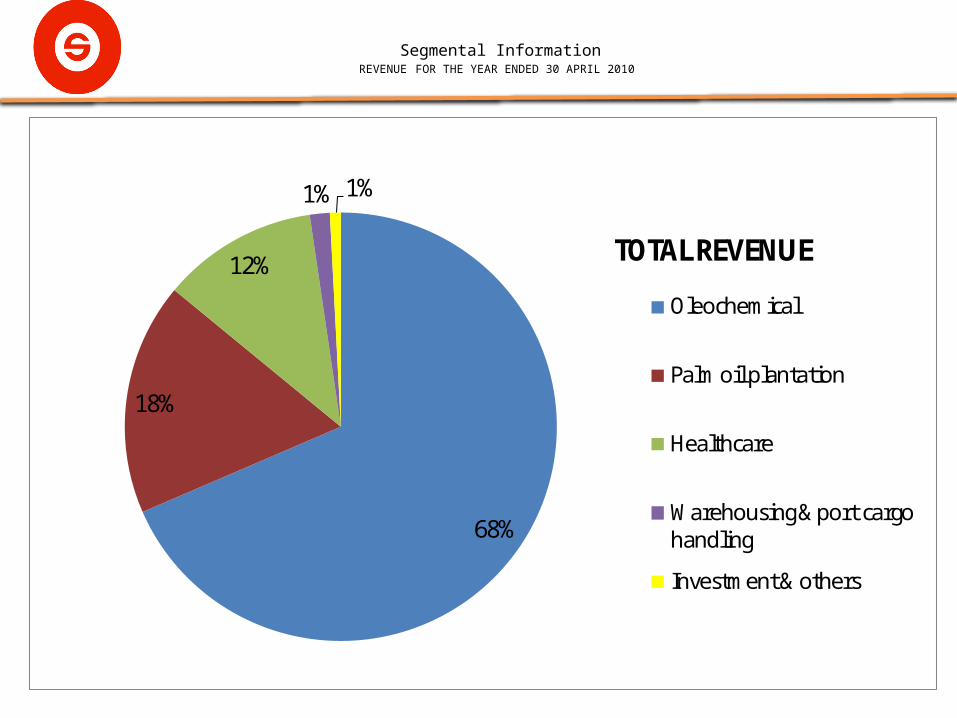

Segmental InformationREVENUE FOR THE YEAR ENDED 30 APRIL 2010

68%

18%

12%

1% 1%

TOTAL REVENUE

Oleochemical

Palm oil plantation

Healthcare

Warehousing & port cargo handling

Investment & others

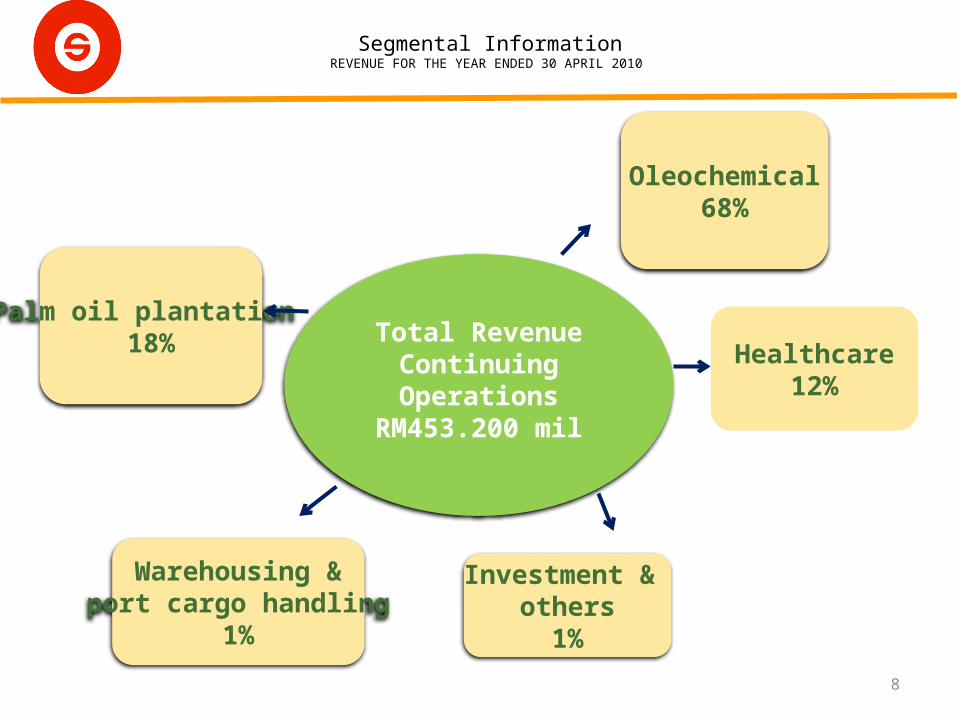

Segmental InformationREVENUE FOR THE YEAR ENDED 30 APRIL 2010

8

Oleochemical68%

Palm oil plantation 18%

Investment & others

1%

Warehousing &port cargo handling

1%

Healthcare12%

Total RevenueContinuingOperations

RM453.200 mil

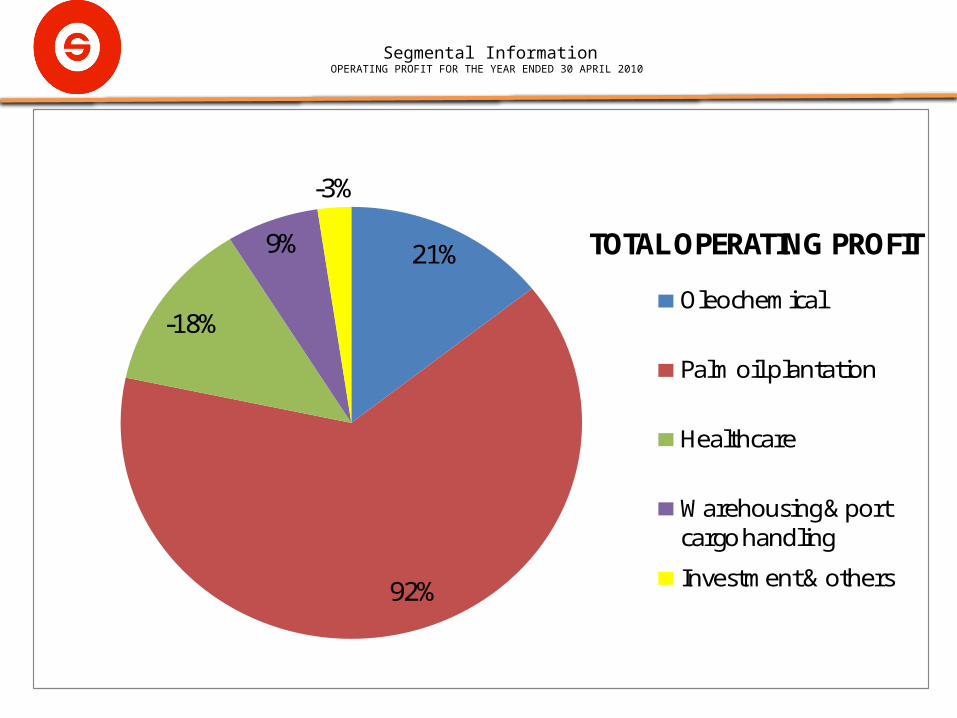

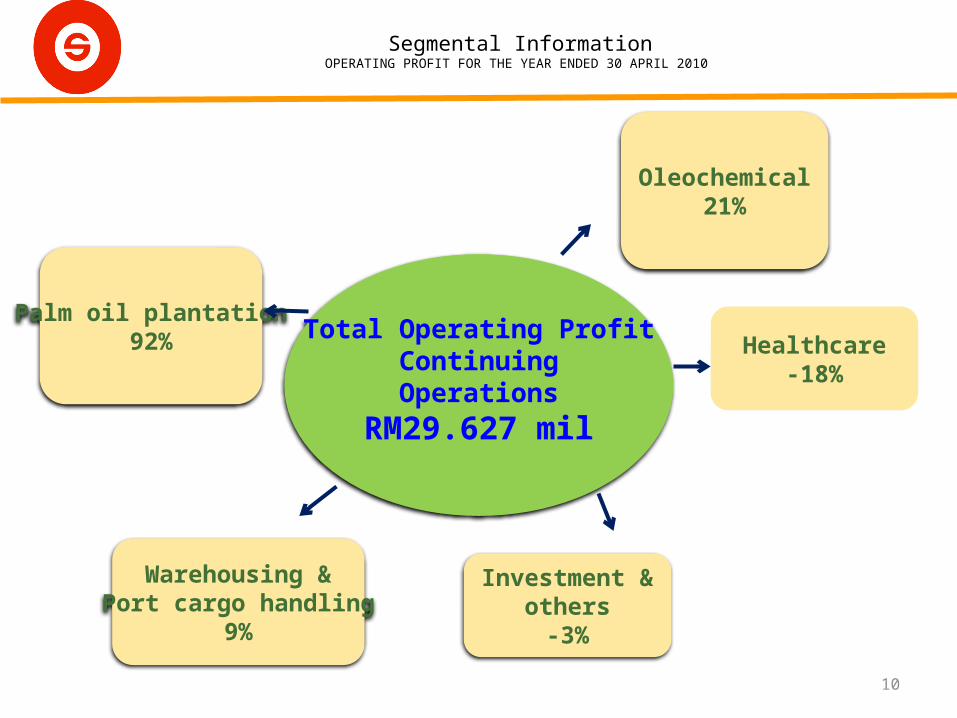

Segmental InformationOPERATING PROFIT FOR THE YEAR ENDED 30 APRIL 2010

21%

92%

-18%

9%

-3%

TOTAL OPERATING PROFIT

Oleochemical

Palm oil plantation

Healthcare

Warehousing & port cargo handling

Investment & others

Segmental InformationOPERATING PROFIT FOR THE YEAR ENDED 30 APRIL 2010

10

Oleochemical21%

Palm oil plantation92%

Investment &others

-3%

Warehousing &Port cargo handling

9%

Healthcare-18%

Total Operating ProfitContinuingOperations

RM29.627 mil

11

ReviewOf Major

Operations

(50,000)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

316,

446

(13,

153)

310,

387

6,08

9

FYE 2009

FYE 2010

Review of Major Operations

12

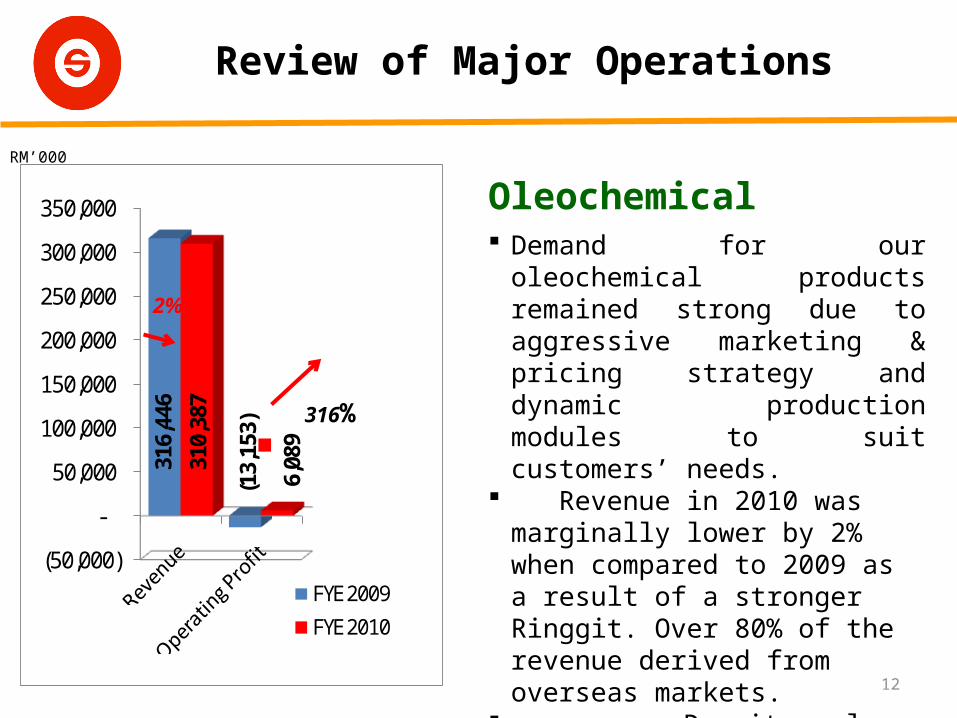

Oleochemical Demand for our oleochemical products

remained strong due to aggressive marketing & pricing strategy and dynamic production modules to suit customers’ needs.

Revenue in 2010 was marginally lower by 2% when compared to 2009 as a result of a stronger Ringgit. Over 80% of the revenue derived from overseas markets.

Despite a lower revenue, the oleochemical division staged a turnaround from a loss of RM13.153 mil to a profit of RM6.089 mil mainly due to lower forex loss.

RM’000

2%

316%

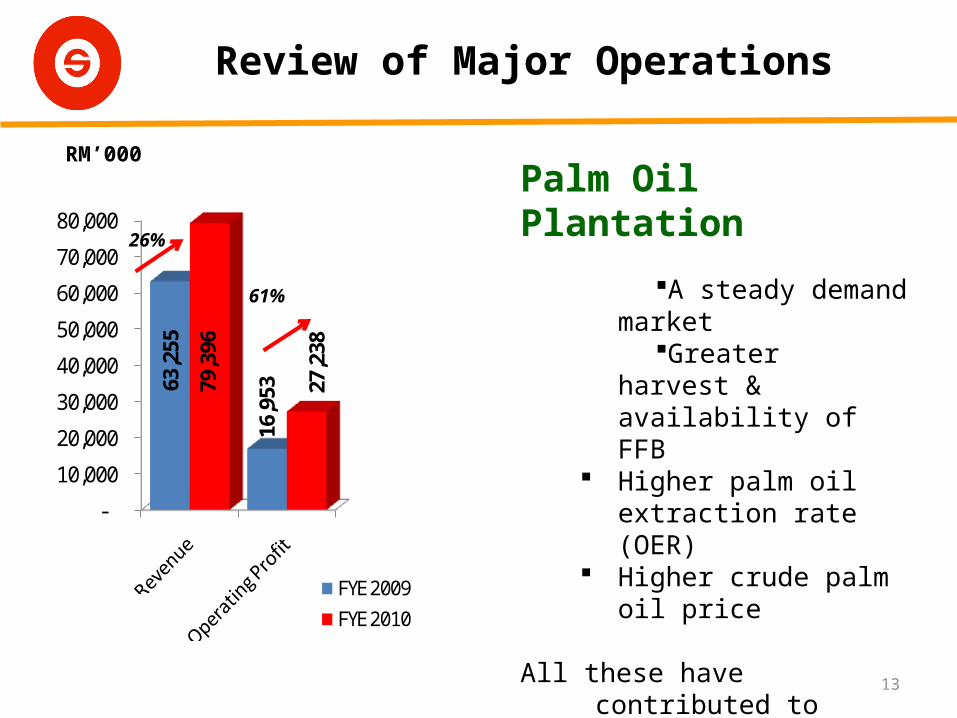

Review of Major Operations

13

Palm Oil Plantation

A steady demand marketGreater harvest &

availability of FFB Higher palm oil extraction rate

(OER) Higher crude palm oil price

All these have contributed to increase in both revenue and profitability of our palm oil division.

RM’000

79%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

63,2

55

16,9

53

79,3

96

27,2

38

FYE 2009

FYE 2010

26%

61%

Review of Major Operations

14

(10,000)

-

10,000

20,000

30,000

40,000

50,000

60,000

50,9

08

(2,9

88)

52,9

76

(5,4

53)

FYE 2009

FYE 2010

Private Healthcare

Our Sri Kota Medical Specialist Centre continued to operate in a highly competitive environment with many new competitors blooming in the surrounding areas.

• Despite the stiff competitions, revenue increased by 4% from RM50.908 mil to RM52.976 mil.

• Higher patient registration contributed to 4.1% increase in revenue.

• Increased loss due to non-recurrent expenses brought to account in FY2010.

• Aggressive marketing and pursuing MSQH Accreditation to tap into Health Tourism market.

4%

(82%)

RM’000

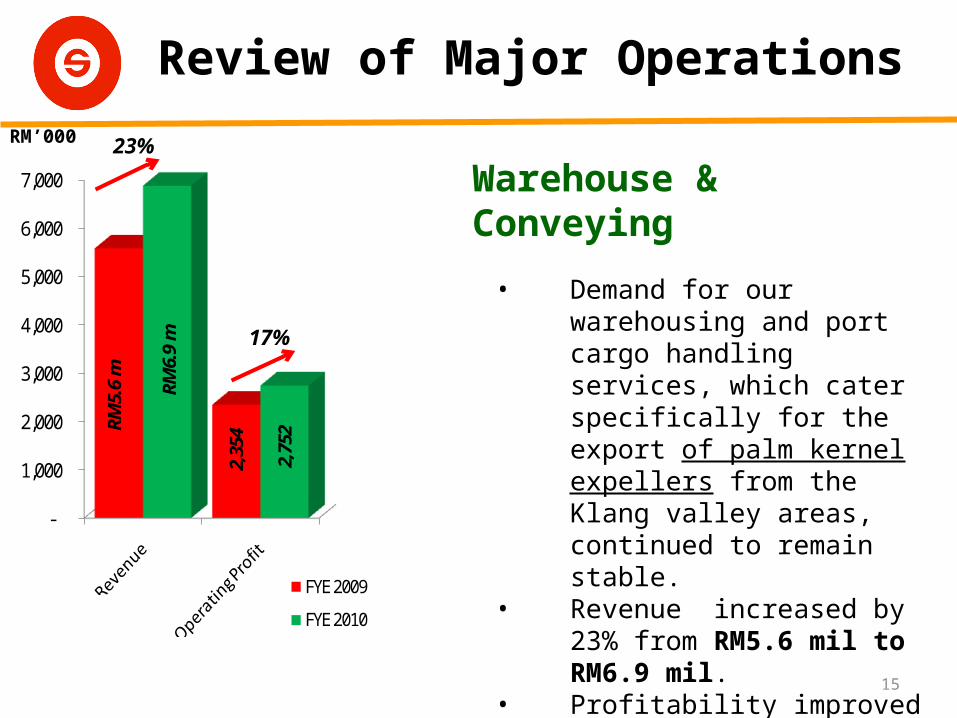

Review of Major Operations

15

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

RM5.

6 m

2,35

4

RM6.

9 m

2,75

2

FYE 2009

FYE 2010

Warehouse & Conveying

• Demand for our warehousing and port cargo handling services, which cater specifically for the export of palm kernel expellers from the Klang valley areas, continued to remain stable.

• Revenue increased by 23% from RM5.6 mil to RM6.9 mil.

• Profitability improved 17% from RM2.354 mil to RM2.752 mil.

• Improved result was due to higher revenue from warehouse rental

RM’000

17%

23%

16

5-YearFinancial

Performance

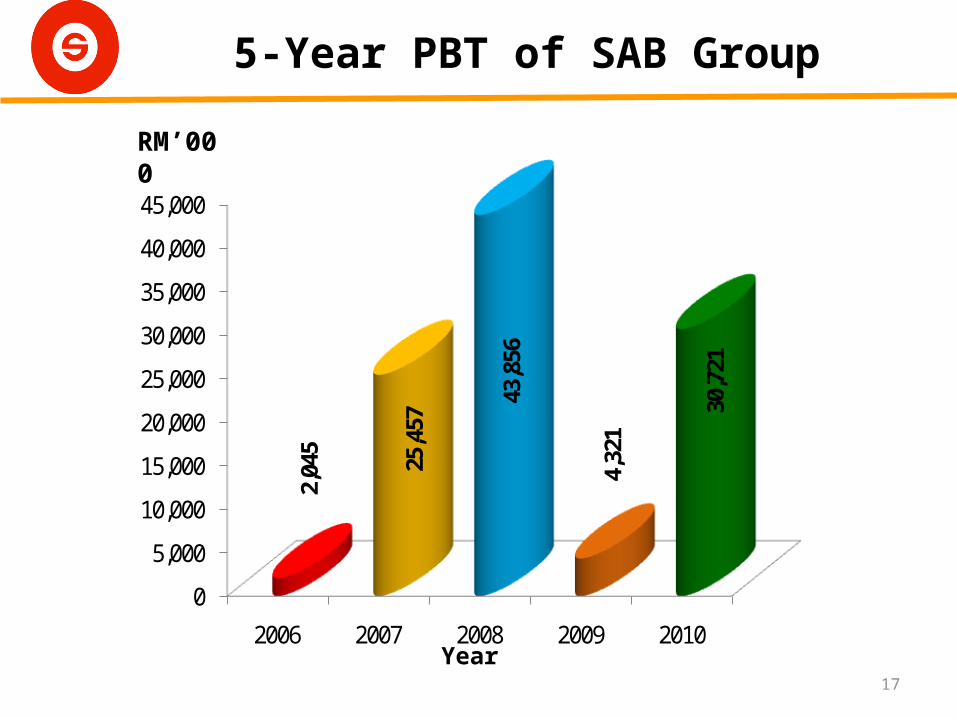

5-Year PBT of SAB Group

17

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2006 2007 2008 2009 2010

2,04

5

25,4

57 43

,856

4,32

1

30,7

21

RM’000

Year

18

DividendRecord

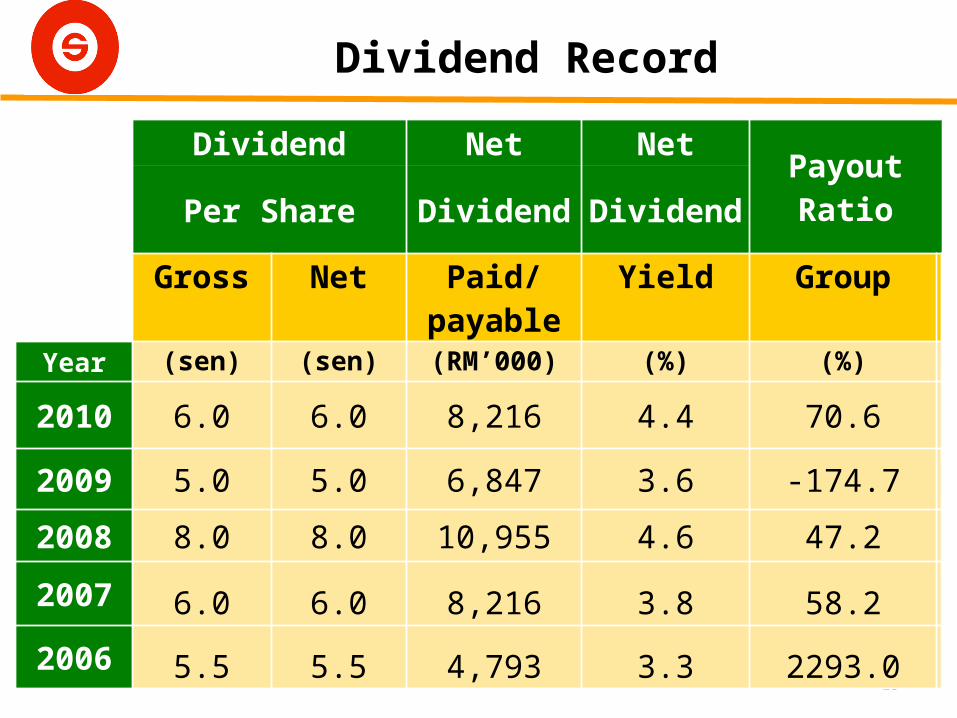

Dividend Record

19

Dividend Net NetPayout Ratio

Per Share Dividend Dividend

Gross Net Paid/payable Yield Group

Year (sen) (sen) (RM’000) (%) (%)

2010 6.0 6.0 8,216 4.4 70.6

2009 5.0 5.0 6,847 3.6 -174.7

2008 8.0 8.0 10,955 4.6 47.2

2007 6.0 6.0 8,216 3.8 58.2

2006 5.5 5.5 4,793 3.3 2293.0

20

Share PricePerformance

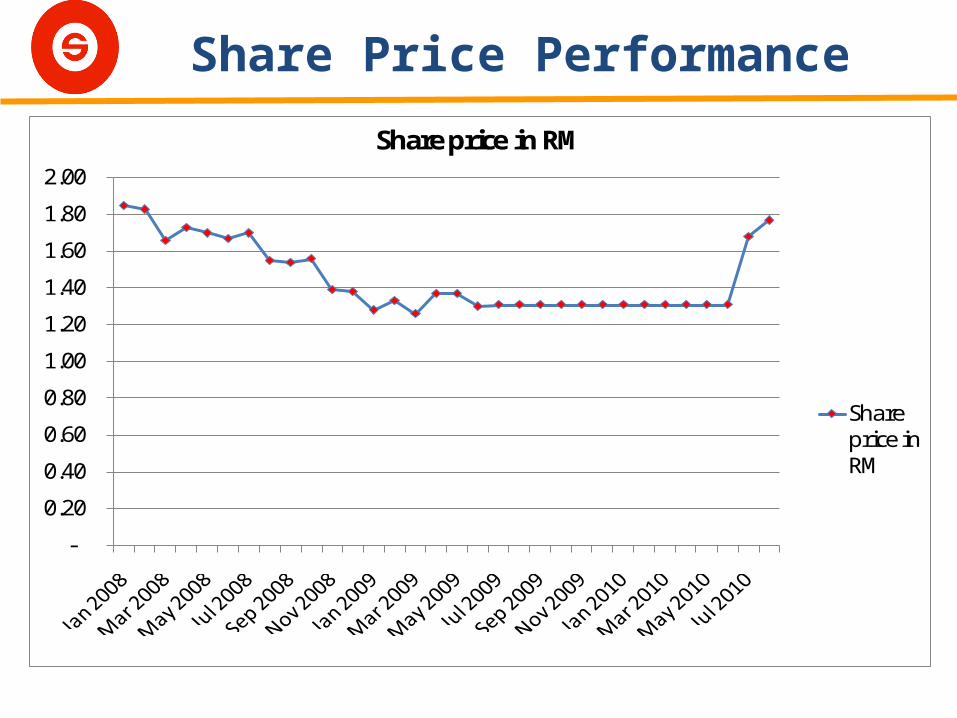

Share Price Performance

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Share price in RM

Share price in RM

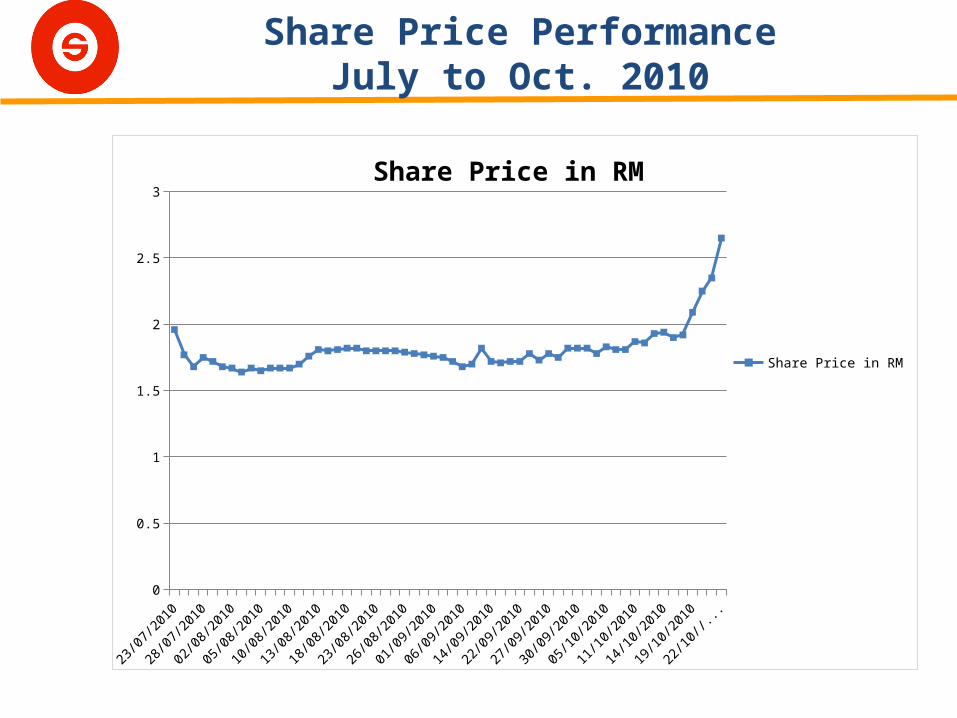

Share Price PerformanceJuly to Oct. 2010

23/07/2

010

27/07/2

010

29/07/2

010

02/08/2

010

04/08/2

010

06/08/2

010

10/08/2

010

12/08/2

010

16/08/2

010

18/08/2

010

20/08/2

010

24/08/2

010

26/08/2

010

30/08/2

010

02/09/2

010

06/09/2

010

08/09/2

010

15/09/2

010

22/09/2

010

24/09/2

010

28/09/2

010

30/09/2

010

04/10/2

010

07/10/2

010

11/10/2

010

13/10/2

010

15/10/2

010

19/10/2

010

21/10/2

0100

0.5

1

1.5

2

2.5

3

Share Price in RM

Share Price in RM