south african mining development association · south african mining development association ......

TRANSCRIPT

South African Mining Development Association

Submission to the Portfolio Committee on

Trade and Industry26 August 2014

1

PCTI/20140826/CoB/SAMDA/32

South African Mining Development Association

• The South African Mining Development Association was started in 2000 as the Junior Mining Initiative by South African junior and black economic empowerment (BEE) mining investors.

• While the founders' initial impetus was to present a united response to government on the Minerals Bill, the need for a strong, permanent lobby, representative of the interests of junior mining companies on several fronts, soon became apparent.

• The need for and support of such a body was confirmed subsequently by research conducted by the Minerals and Energy Policy Centre (MEPC).

• In the research conducted by the MECP on the junior Mining sector the following definition of junior mining companies was concluded. e.g

– Junior Miners are companies with an Asset base of R50 million to R7 billion.– Above R7 billion are the majors.– Below R50 million are Small Scale miners.– Below the small scale miners are the Artisanal miners.

2

South African Mining Development Association

3

Vision

SAMDA's vision is to be the vehicle for the development of a vibrant and sustainable junior mining sector which contributes towards the growth and prosperity of the mining industry.

Mission• to create an enabling environment for raising finance;• developing technical and other skills;• practicing responsible environmental management and sustainable development; and• the maintenance of standards of good practice in the junior mining sector

To Lobby;• government;• organised labour; and• other stakeholders and institutions• to promote mutual understanding• to encourage local and international investment• to conduct research to understand the sectors needs• to promote beneficiation• to build African and global alliances• and to facilitate the transformation of the mining industry by promoting emerging junior mining operations and

those who are historically disadvantaged.

4

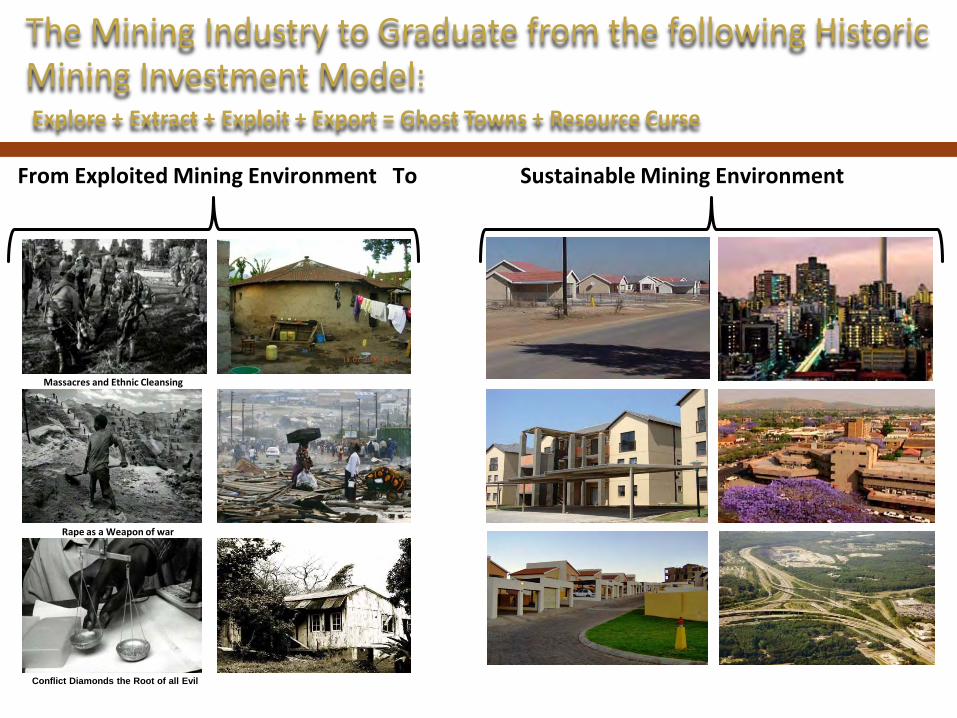

Historically, Investments in Mining had an exploitation culture in Africa – The Resource curse:

Monopolistic industry in

South Africa pre 1994

Militant labour force fighting exploitative

labour practices

Ghost towns

No black ownership

No royalty payments to

rural communities

Neo-colonialism

Eg: Case Study South Africa

The Mining Industry to Graduate from the following Historic Mining Investment Model:Explore + Extract + Exploit + Export = Ghost Towns + Resource Curse

From Exploited Mining Environment To Sustainable Mining Environment

Massacres and Ethnic Cleansing

Rape as a Weapon of war

Conflict Diamonds the Root of all Evil

WHAT IS BENEFICIATION?Broad-Based Socio-Economic Empowerment Charter For The

South African Mining And Minerals Industry

• “Beneficiation” means the transformation of a mineral (or a combination of minerals) to a higher value product, which can either be consumed locally or exported. The term “beneficiation” is often used interchangeably with mineral “value-addition” or “downstream beneficiation”

• Beneficiation seeks to translate comparative advantage in mineral resources endowment into competitive advantage as fulcrum to enhance industrialization in line with State developmental priorities. In this regard, mining companies must facilitate local beneficiation of mineral commodities by adhering to the provision of Section 26 of the MPRDA and the mineral beneficiation strategy:

– Mining companies may offset the value of the level of beneficiation achieved by the company against a portion of its HDSA ownership requirements not exceeding 11 percent.

7

Mineral Beneficiation Section 26 of the MPRDA

Section 26(1) The Minister may initiate or prescribe incentives to promote the beneficiation of minerals in the Republic.

(2) If the Minister, acting on advice of the Board and after consultation with the Minister of Trade and Industry, finds that a particular mineral can be beneficiated economically in the Republic, the Minister may promote such beneficiation subject to such terms and conditions as the Minister may determine.

(3) Any person who intends to beneficiate any mineral mined in the Republic outside the Republic may only do so after written notice and in consultation with the Minister.

8

Section 100 (2)(a) of the MPRDA

Section 100• (2) (a) To ensure the attainment of Government’s objectives of

redressing historical, social and economic inequalities as stated in the Constitution, the Minister must within six months from the date on which this Act takes effect develop a broad-based socio-economic empowerment Charter that will set the framework, targets and time-table for effecting the entry of historically disadvantaged South Africans into the mining industry, and allow such South Africans to benefit from the exploitation of mining and mineral resources.

9

ELEMENTS OF THE CHARTER - A TOOL TO REALIZE THE NATIONAL DEVELOPMENT PLAN VISION FOR 2030

The Elements of the Mining Charter are some of the Mining Economy’s National Development Plan tools in eliminating poverty and reducing inequality by 2030.

IN SECTION 100 (2)a OF THE MINERALS AND PETROLEUM RESOURCES DEVELOPMENT ACT, THE MINING CHARTER WAS CREATED as a historic charter for the transformation of the mining sector that would introduce elements of sustainable growth of the mining industry, with the intention to ensure transformation of the mining industry.

Below are the elements of the Mining Charter:

• Ownership - 26% equity participation by May 2014

• Procurement and Enterprise Development

• Beneficiation

• Employment Equity - 40% black managers by May 2014

• Human Resources Development – Skills Development Spend by May 2014 should be 5% of payroll

10

ELEMENTS OF THE CHARTER - A TOOL TO REALIZE THE NATIONAL DEVELOPMENT PLAN VISION FOR 2030

• Mine Community Development through Integrated Development Plans and Social and Labour Plan

• Housing and Living Conditions Requirements:- To attain the occupancy rate of one person per room by 2014;- To upgrade or convert hostels into family units by 2014;- To promote home ownership.

• Sustainable Development through:- Environmental Management Plan- Rehabilitation - Waste Removal and Storage- Improve Health and Safety Performance

11

Ownership - 26% equity participation by May 2014

• The Charter requires a minimum effective participation of 26% by HDSA by the 1st of May 2014

• The current Ownership Structure is a neo-colonialist ownership model that perpetuates ownership of the country’s resources and mines by foreign investor monopoly.

• 26% Broad Based Black Economic Empowerment Ownership through Unencumbered Net Value in the mining industry by 2014 has not been reached by the majority of the mining companies.

• Many of The Broad Based Black Economic Empowerment investors that have not yet realized 26% unencumbered net value by the 1 May 2014 as prescribed by the Mining Charter through section 100 (2) a of the MPRDA are the following:

– Employee Ownership Schemes (ESOPs)– Community Trusts – Broad Based Business Trusts– BEE Technical Producers– Women In Mining – Youth In Mining– People living with Disabilities

• Ownership is still unrealised in the majority of Broad Based Black Economic Empowerment transactions. 12

Ownership - 26% equity participation by May 2014

• According to the research of the JSE Top 49 Mining Companies conducted by SAMDA In 2014

• The market capitalisation of the Top 49 JSE-Resources companies is R2,574 trillion (100% of the resources sector’s value on the JSE main board).

• The charter requires a minimum effective participation of 26% by HDSA in each of the 49 listed companies

• If all the Top 49 Listed Mining Companies had 26% HDSA ownership of R2,574 trillion the value would have been R669 billion HDSA participation in 2014.

• The majority of black producers do not own mines because the shareholding has not been paid up due to Transfer Pricing

13

The Majority Of The JSE Top 49 Mining Companies Has A Charter Non-Compliant Ownership Profile (2013/2014)

Number Name Market Cap (Rm) HDSA Interest %

Gross HDSA Value (Rm) Yes / No Value (Rm)

Net Value as % of Market Cap

1 African Ra inbow Minera ls Ltd. 47 310 55.00% 26 021 Yes 26 021 1.01%2 Assore Ltd. 55 642 26.10% 14 523 Yes 14 523 0.56%3 Impala Platinum Holdings Ltd. 72 983 14.60% 10 656 Yes 10 656 0.41%4 Royal Bafokeng Platinum Ltd. 10 380 57.13% 5 930 Yes 5 930 0.23%5 Atlatsa Resources Corporation 2 601 55.00% 1 431 Yes 1 431 0.06%6 Pan African Resources PLC 4 880 26.00% 1 269 Yes 1 269 0.05%7 Harmony Gold Mining Company Ltd. 14 191 14.74% 2 092 Yes 2 092 0.08%8 Merafe Resources Ltd. 2 469 29.00% 716 Yes 716 0.03%9 Gold Fields Ltd. 30 243 2.30% 696 Yes 696 0.03%

10 Sibanye Gold Ltd. 11 644 2.30% 268 Yes 268 0.01%11 Wescoal Holdings Ltd. 422 34.40% 145 Yes 145 0.01%12 Vi l lage Main Reef Ltd. 406 23.00% 93 Yes 93 0.00%13 Firestone Energy Ltd. 248 25.70% 64 Yes 64 0.00%14 Infrasors Holdings Ltd. 204 28.40% 58 Yes 58 0.00%15 Witwatersrand Consol idated Gold Resources Ltd. 366 9.86% 36 Yes 36 0.00%16 Exxaro Resources Ltd. 53 667 34.40% 18 461 No 0 0.00%17 Northam Platinum Ltd. 16 559 26.60% 4 405 No 0 0.00%18 Palabora Mining Company Ltd. 5 544 26.00% 1 441 No 0 0.00%19 AngloGold Ashanti Ltd. 65 534 1.90% 1 245 No 0 0.00%20 Anglo American Platinum Ltd. 119 391 1.00% 1 194 No 0 0.00%21 Aquarius Platinum Ltd. 3 428 15.20% 521 No 0 0.00%22 Petmin Ltd. 1 137 24.00% 273 No 0 0.00%23 Coal of Africa Ltd. 1 153 10.58% 122 No 0 0.00%24 Trans Hex Group Ltd. 444 20.40% 91 No 0 0.00%25 Wes izwe Platinum Ltd. 1 270 6.00% 76 No 0 0.00%26 Sentula Mining Ltd. 194 17.00% 33 No 0 0.00%27 Bui ldmax Ltd. 453 6.75% 31 No 0 0.00%28 Glencore Xstrata plc 783 691 0.00% 0 No 0 0.00%29 BHP Bi l l i ton Plc 700 947 0.00% 0 No 0 0.00%30 Anglo American plc 364 817 0.00% 0 No 0 0.00%31 Kumba Iron Ore Ltd. 144 501 0.00% 0 No 0 0.00%32 Lonmin plc 32 084 0.00% 0 No 0 0.00%33 ArcelorMitta l South Africa Ltd. 17 005 0.00% 0 No 0 0.00%34 DRDGOLD Ltd. 1 684 0.00% 0 No 0 0.00%35 Evraz Highveld Steel and Vanadium Ltd. 1 676 0.00% 0 No 0 0.00%36 Resource Generation Ltd. 1 279 0.00% 0 No 0 0.00%37 Eastern Platinum Ltd. 826 0.00% 0 No 0 0.00%38 Keaton Energy Holdings Ltd. 540 0.00% 0 No 0 0.00%39 Tawana Resources NL 429 0.00% 0 No 0 0.00%40 Gol iath Gold Mining Ltd. 317 0.00% 0 No 0 0.00%41 South African Coal Mining Holdings Ltd. 267 0.00% 0 No 0 0.00%42 The Waterberg Coal Company Ltd. 225 0.00% 0 No 0 0.00%43 Rockwel l Diamonds Inc. 193 0.00% 0 No 0 0.00%44 Ferrum Crescent Ltd. 167 0.00% 0 No 0 0.00%45 Randgold & Exploration Co Ltd. 154 0.00% 0 No 0 0.00%46 Forbes & Manhattan Coal Corp 126 0.00% 0 No 0 0.00%47 Miranda Minera l Holdings Ltd. 114 0.00% 0 No 0 0.00%48 Bauba Platinum Ltd. 102 0.00% 0 No 0 0.00%49 Sable Platinum Ltd. 100 0.00% 0 No 0 0.00%

Tota l 2 574 007 3.57% 91 888 63 995 2.49%

Net Value

14

STRATEGIC MINERALS

15

Commodity Needs of the Country and the Value Chain

Coal Energy supply risk - Fuel , Gas, gasoline and diesel

GoldMoney and Gold Coins, Jewellery, restorative dentistry, Food & Drink eg. Gold Leaf, Good Reflector ofelectromagnetic radiation eg. Infrared and visible light, High-end CDs, Electronics eg. Computers, communicationsystems, spacecraft, jet aircraft engines, etc.

Iron Ore Steel - Infrastructure and job creation prerogative,

Manganese Steel - Infrastructure and job creation prerogative

Diamonds Job creation potential-jewellery beneficiation

PGM SA’s international dominance; job creation– Jewellery, Energy supply eg. Fuel Cells, Catalytic converter for cars,medical instruments, ships, pipelines, and steel piers

Chrome SA’s international dominance - jet engines and gas turbines, Dye and yellow pigment

Vanadium SA’s international dominance, jet aircraft engines,

Titanium High technology industries - stainless steel, white permanent pigment used in paints, paper, toothpaste, andplastics, aircraft, armor plating, naval ships, spacecraft, and missiles as well as Jewelry

Nickel Niche steel products - stainless steel, magnets, coins, rechargeable batteries, electric guitar strings, microphonecapsules, and special alloys

Uranium Clean Energy – Power Plants and military use in ammunition and weapons

SAMDA proposes that the State include the following commodities to be Additional Strategic Minerals:

Phosphate food security and fertilizer supply

Limestone Required for cement manufacture and construction projects

Shale Gas Energy supply risk and Job Creation through industrialization

Oil (Petroleum) Energy supply risk and Job Creation through industrialization

16

LOCATION OF STRATEGIC MINERALS IDENTIFIED BY THE DMR

17

LOCATION OF ADDITIONAL STRATEGIC MINERALS PROPOSED BY SAMDA

18

BENEFICIATION AS A GOVERNMENT LED STRATEGY

The ten commodities have been clustered according to their value chains. The government has identified five value chains that will be the preliminary focus of the Beneficiation Strategy. There are instances where some of the commodities share value chains, such as Gold and Platinum. The five value chains are:

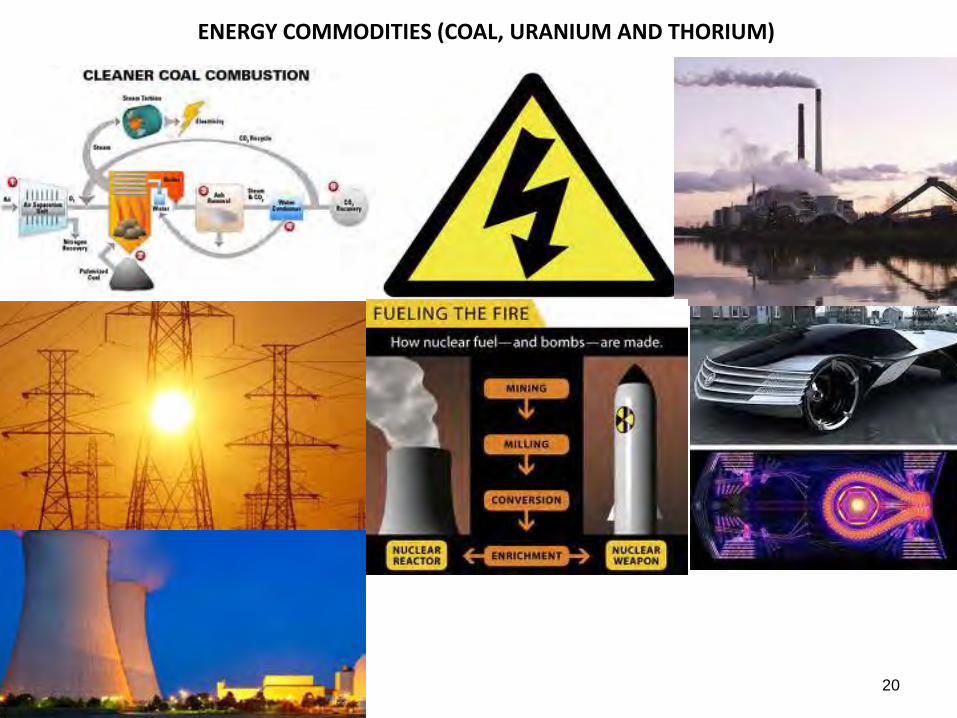

• Energy commodities(coal, uranium and thorium)

• Iron and steel (iron-ore, manganese, chrome, vanadium and nickel)

• Pigment and titanium metal production (titanium)

• Autocatalytic converters and diesel particulate filters(platinum)

• Jewellery fabrication (diamonds, gold and platinum)

Each value chain requires specific interventions in order to maximise the value extraction of the associated mineral. Each value chain has its own unique beneficiation strategy, in which the technicalities can be further unpacked.

19

STEEL VALUE CHAIN (IRON ORE, MANGANESE, NICKEL, VANADIUM & CHROME

20

ENERGY COMMODITIES (COAL, URANIUM AND THORIUM)

JOB CREATION & ECONOMIC GROWTH THROUGH BENEFICIATION OF GOLD, DIAMONDS AND PLATINUM

21

Phosphate

Limestone

FOOD SECURITY THROUGH ROBUST AGRICULTURE

INFRASTRUCTURE DEVELOPMENT

STRATEGIC MINERALS SUGGESTED BY SAMDA - BENEFICIATION ENGINE FOR ECONOMIC GROWTH IN THE PARADIGM SHIFT

22

GEOLOGICAL OVERVIEW OF SOUTH AFRICA

2310/28/2014 12

GEOLOGICAL OVERVIEW OF SOUTH AFRICA

2413

GEOLOGICAL OVERVIEW OF SOUTH AFRICA

2514

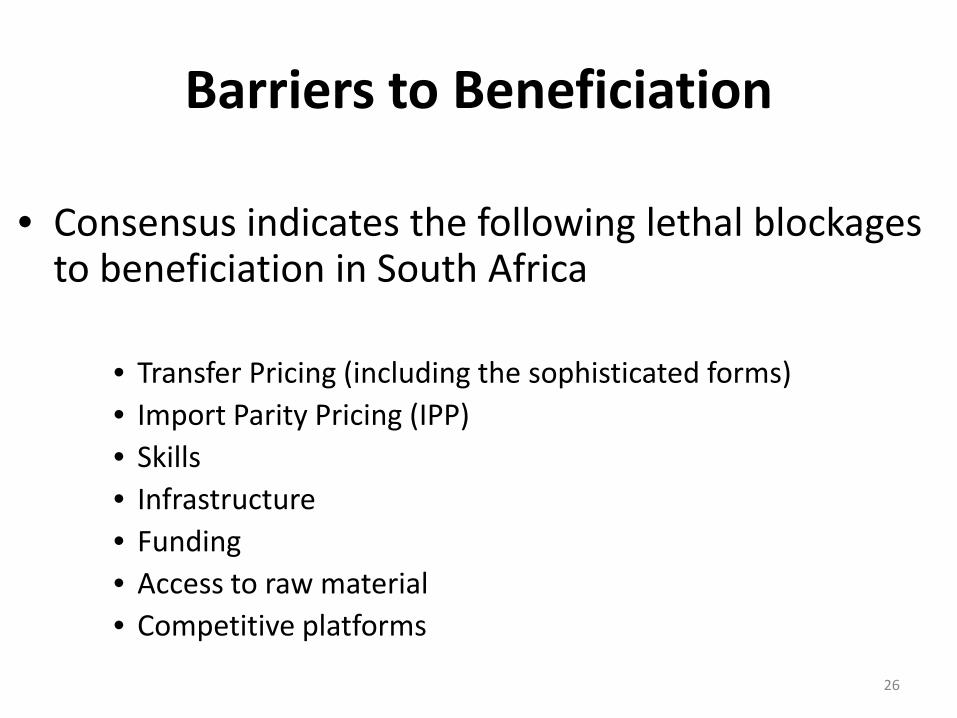

Barriers to Beneficiation

• Consensus indicates the following lethal blockages to beneficiation in South Africa

• Transfer Pricing (including the sophisticated forms)• Import Parity Pricing (IPP)• Skills• Infrastructure• Funding• Access to raw material• Competitive platforms

26

WHAT IS TRANSFER PRICING?

27

• The term ‘transfer pricing’ is used to describe arrangements involving the transfer of goods or services, at an artificial price, (usually lower) in order to transfer income from one business to an associated business in a different tax jurisdiction which is often lower

• Some producer companies sell the companies commodities to its marketing divisions at lower than market related prices.

• This results in the exportation of profits to the tax haven off shore accounts and the declaration of low profits and the payment of low tax in the country where the commodity is being produced and exported from. In this case a loss to South Africa

• As Transfer Pricing regulating are tightened in South Africa, more sophisticated forms are developed, such as abuse of Advanced Pricing Agreeemnts

WHAT IS IMPORT PARITY PRICING?

• The term ‘import parity pricing’ is used to describe arrangements where local companies are permitted to sell products at excessive prices. These are usually then at international prices.

• Cost of manufacture, and transport are at the core of IPP

• IPP becomes even more painful for local industries when they are reliant on a company that has market dominance because their options to buy elsewhere is very limited

• Ongoing IPP reflects that local demand is high(and local supply is low requiring ongoing importing)

28

Dealing with Barriers to Beneficiation

29

Transfer Pricing • Limit perpetual forward selling if it is an abuse of advanced pricing agreements

• Monitor the various types of Transfer Pricing, such as abuse of Advanced Payment Agreements; Monitor the Marketing relationships where these do not add value but add costs; Look at manipulation of pricing based on fictitious or irregular inter-company loans (thin capitalization)

• Enforce transfer pricing conventions

Import Parity Pricing

• Eliminate IPP tariffs

• Pursue aggressively the developmental pricing agenda through mechanisms in the amended MPRDA;

• Set local levels of beneficiation in the hands of producers;

Dealing with Barriers to Beneficiation

30

Skills • Commodity producers must invest in local skills development at a larger rate than is current

• Stop the Stripping of R&D capacity locally by allowing offshoring of head offices must be stopped.

Infrastructure • Government investment in energy infrastructure is critical but Eskom cannot be held hostage to the coal export trade.

• Eskom’s requirements must first be satisfied before exporting is permitted.

Funding • Development funders must increase investment in the manufacturing sector. Forexample IDC and PIC must increase exposure to manufacturing sector

• Procurement driven beneficiation/manufacturing programmes

Access to RawMaterial

• Forward selling and threats of expropriation of commodity claims has ensured that foreign buyers continue to bleed unprocessed commodities out of South Africa.

• We need to ensure that the Department enforce the requirements that local needs are first addressed BEFORE export of unprocessed material is allowed.

Competitive Platforms

• IDZs and SEZs allow South Africa to compete globally and incubate manufacturing SMMEs.

• Prioritise the giving the majority of incentives to South African companies before giving an incentive to a competing foreign-owned company.

Procurement The Leading Force Behind Enterprise Development

• Develop BEE mining support industries

Source: SAMPPF - 2006

Approximately $600 million

to HDSA500 Buyers

4

Total annual procurement

budget – estimated at

$6 billion

3

33 mining houses;15 venues;

6 provincial governments

1

41 000suppliers

(2500 Narrow Based HDSAs

500 BBBEE)

2

31

Procurement an Engine for Economic Growth

• Develop BEE mining support industries

Source: DECTI - 2008

Approximately $950 million

to HDSA600 Buyers

4

Total annual procurement

budget – estimated at

$8.5 billion

3

66 mining houses;15 venues;

6 provincial governments

1

65 000suppliers

(4500 Narrow Based HDSAs

12000 BBEE)

2

32

Example: Northern Cape Mines

Top 2000 suppliers to mines: 2010

33

34

Procurement and Enterprise Development

• PROCUREMENT AND ENTERPRISE DEVELOPMENT OF THE CHARTER BY 2014, CONTRIBUTES TOWARDS THE ACHIEVEMENT OF THE NDP WITH THE AIM OF CREATING SUSTAINABLE BUSINESSES THROUGH THE MINING ECONOMY BY 2030.

• The following diagrams demonstrate how the mining industry is able to develop BEE mining support industries through Preferential Procurement from 2006, 2008 to 2013.

• Note that this research does not include all the mining companies in South Africa.

• This research demonstrates that a mining industry that is procurement driven does generate economic growth and job creation and by so doing contributes towards the aspirations of the NDP.

• It is unfortunate that many of the mining companies procure goods manufactured off shore, eg. China,etc or bigger cities in South Africa instead of promoting goods manufactured in South Africa or in mining towns to contribute towards Local Economic Development .

35

INTERGRATED RESOURCES DEVELOPMENT MODELS

• A Integrated Mining Development Partnership with Local, Provincial and National Government, as well as Producers, Labour,Rural Communities, Business and various other stake holders.

• Objective is to create a sustainable mining economy in the rural areas where mining production takes place in a model that willsustain and develop the mining areas , rather than creating Ghost Towns.

• The example of an integrated resource development model has been implemented in the Eastern Limb of the Bushveld IgneousComplex since 2002. This section provides an updated progress report, highlights some of the challenges faced by thestakeholders operating within the socio-economic development domain in the region, and demonstrates that this modelrepresents a viable option for government in the future.

• The integrated resource management development model is dynamic and adjusts to changes resulting from government policydecisions taken at national, provincial and local levels. A three-tier approach has been adopted to ensure integrateddevelopment planning and implementation to occur between national and provincial government, mining producers, ruralcommunities, labour and other stakeholders, eg

– Liaison by mining houses collaboratively with national government

– Liaison by mining houses collaboratively with provincial government

– Liaison by mining houses collaboratively with relevant district & local municipalities.

– Liaison by mining houses collaboratively with rural communities

– Liaison by mining houses collaboratively with organised labour

– Liaison by mining houses collaboratively with organised business

– Liaison by mining houses collaboratively with other stakeholders, eg SMMEs, Co-operatives, etc.

36

37

The Integrated Solution Model

38

Municipalities in Context

39SLP – Social Labour Plan

LED – Local Economic Development

The Mining Industry in Context

40

Mining Companies involved in Rural UpliftmentPartnership Models through Producers Forums:

• Akanani Mining (Pty) Limited

• Anglo Operations Limited• Anglo Platinum• ARM Platinum (Pty) Limited• ASA Metals (Pyt) Limited• Assmang Limited (Dwarsrivier Mine)

• Barplats Mines Limited (Rhodium Reefs)• Boynton Investments (Pty) Limited• Chromex Mining (Pty) Limited

• Corridor Mining Resource (Pty) Limited• Eastern Platinum Limited

• Impala Platinum Limited• Lebowa Platinum• Marula Platinum

• Modikwa Platinum Mine Joint Venture• MTC Minerals• Northam Platinum Limited• Pan Palladium South Africa (Pty) Limited• Plateau Resources (Pty) Limited• Platreef Resource (Pty) Limited• Rustenburg Platinum Mines (Pty) Limited

(Eastern Limb Development)• Samancor Chrome Limited• Sishen Iron Ore Company (Pty) Limited• Two Rivers Platinum (Pty) Limited• Umnotho weSizwe Investment Holdings Limited• Veremo Holdings Limited• Westen Platinum Limited (On behalf of Messina

Platinum Mines Limited)• Xstrata South Africa (Pty) Limited

41

Public Private Partnership Funds Invested in creating a Sustainable Rural Economy:

Sekhukhune District

• The Sekhukhune District cuts across the north-eastern part of the Bushveld Complex.

• Population 1.1 million• Mining’s contribution to GGP in Sekhukhune is

estimated at between 15 – 20%• It is estimated that mining grew at an annual rate

of 5.4% from 1996 – 2001• 17 Operating Mines• 23 Mining Projects

42

43

Mining Projects In Sekhukhune (Limpopo)

Expansion in progress or production building up

Number Mine Name Company Mineral1 Lebowa Platinum Anglo Platinum PGM

2Modikwa A.R.M & Anglo Platinum

PGM3 Mototolo Anglo Platinum PGM4 Everest South Aquarius PGM

5Two Rivers African Rainbow Minerals

PGM6 Marula UG2 Implats PGM7 Steelpoortdrift 94 Chrome

Bankable feasibility study completed8 Blue Ridge Ridge PGM

Bankable feasibility study planned or underway

9 Sheba’s Ridge Ridge PGM10 Smokey Hills Platinum Australia PGM11 Twickenham Anglo Platinum PGM12 Mareesburg Eastern Plats PGM13 Marula Merensky Implats PGM

Pre-feasibility study in progress or completed

14 Kennedy’s Vale Eastern Plats PGM15 Der Brochen Anglo Platinum PGM16 Booysensdal Anglo Platinum PGM

Advanced exploration17 Ga-Phasha Anglo Platinum PGM18 Loskop Boynton PGM

Early exploration19 Grootboom Boynton PGM20 Tjate Jubilee PGM21 Kliprivier Nkwe PGM22 Tinderbox Placer Dome PGM23 Berg Platfields PGM

44

45

BENEFICIATION INCENTIVES – SPECIAL ECONOMIC ZONES

Special Economic Zone (SEZ) programme

•A geographical region that has economic and other laws that are more free-market-oriented than a country's typical or national laws. "Nationwide" laws may be suspended inside a special economic zone.

•In 2013, the Minister of Finance, Pravin Gordhan announced, what is an unprecedented move to bolster support for government’s Special Economic Zone (SEZ) programme.

•Investors in such zones are expected to qualify for a 15% corporate tax rate, and in addition, a further tax deduction for companies employing workers earning less than R60,000 per year.

•Mining companies have the opportunity to establish beneficiation plants at any of the Special Economic Zones, for example in Mpumalanga, the Eastern Bushveld, the Western Bushveld and Northern Cape.

46

BENEFICIATION INCENTIVES

Section 12 I Tax Allowance Incentive (12I TAI) (SARS)

The Section 12 I Tax Incentive is designed to support Greenfield investments (i.e. new industrial projects that utilise only new and unused manufacturing assets), as well as Brownfield investments (i.e. expansions or upgrades of existing industrial projects). The new incentive offers support for both capital investment and training.

The incentive offers:

•R900 million in the case of any Greenfield project with a preferred status;•R550 million in the case of any other Greenfield project;•R550 million in the case of any Brownfield project with a preferred status;•R350 million in the case of any other Brownfield project;•An additional training allowance of R36 000 per employee may be deducted from taxable income; and•A maximum total additional training allowance per project, amounting to R20 million, in the case of a qualifying project, and R30 million in the case of a preferred project

Benefits of Special Economic Zones

• Beneficiation and procurement could benefit from the various incentives provided by government for investors that develops businesses in Special Economic Zones.

• Mining companies must facilitate local beneficiation of mineral resources of mineral commodities by adhering to the provision of section 26 of the MPRDA and the mineral beneficiation strategy.(Mining Charter, Pg 2)

• It is unfortunate that a majority of the companies import finished (manufactured) goods from off shore instead of manufacturing goods locally .

• By complying to the Mining Charter through Beneficiating minerals, small and medium enterprises and manufacturing industries will be promoted and thus stimulating job creation and economic development.

47

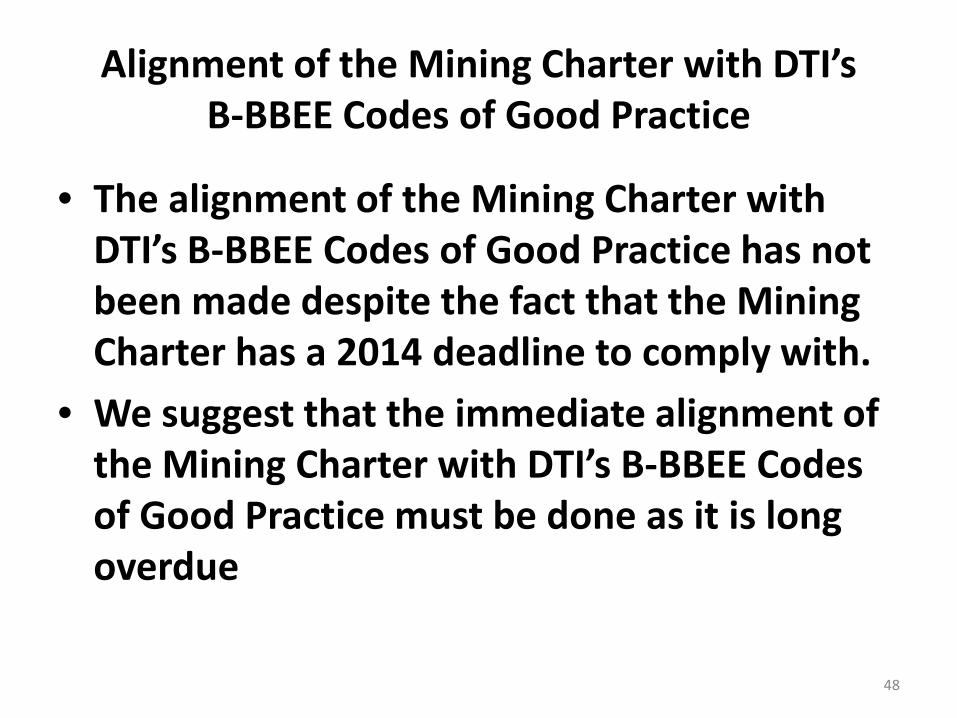

Alignment of the Mining Charter with DTI’s B-BBEE Codes of Good Practice

• The alignment of the Mining Charter with DTI’s B-BBEE Codes of Good Practice has not been made despite the fact that the Mining Charter has a 2014 deadline to comply with.

• We suggest that the immediate alignment of the Mining Charter with DTI’s B-BBEE Codes of Good Practice must be done as it is long overdue

48

Thank You

49