south africa: the economics of nuclear energy russia · south africa’s planned nuclear energy...

TRANSCRIPT

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk

Russia

Overview

Over the past year, political momentum has been building in South Africa behind the plan to

build a modern fleet of nuclear power plants (NPPs) with aggregate capacity of nearly 10GW. At

the same time, the plan remains the subject of lively debate, much of which is focused on the

affordability for South Africa of the substantial cost of as much as US$50 billion. Against this

background, this report considers some of the economic implications were this nuclear energy

initiative to go ahead. First, we estimate the cost of nuclear generated electricity. We then model

the extent of the resulting reduction in CO2 emissions. A further modelling exercise is focused

on the impact on economic growth in South Africa economy from varying degrees of

localization of the investment involved in building nuclear power capacity on the scale

envisaged.

Main findings

Applying the IEA’s method and formula for the “levelised cost of electricity” (LCOE) –

that is, the average lifetime cost of generating electricity using different fuels over the life

of the corresponding technologies – the resulting estimate of the nuclear LCOE compares

favourably with the current cost of coal-fired generation (US$86.88/MWh in our base

case vs the IEA’s estimate for coal of US$99.79/MWh at the same cost of capital).

South Africa’s planned nuclear energy development would reduce carbon emissions

compared to the business-as-usual baseline by 21 per cent. A monetary value may be put

on this reduction based on carbon tax rates. That value would be around US5 billion

assuming a modest tax rate of US$5/tonne that may seem suitable for a developing

country, rising to about US$22 billion if South Africa were to introduce a carbon tax

close to conservative forecasts of future European levels – around €20/tonne. These

values apply to our modelling period out to 2040 but would be higher in practice since

the NPPs’ useful life would continue for another three decades.

The localization of a portion of the investment in the envisaged NPP new builds would

produce a positive shock for South African industry and economic growth. At the highest

plausible localization level of 45 per cent, the multiplier effect of this industrial

investment on GDP would be 3.4x, and the monetary value of the incremental value

added in current US dollars would be over US$77 billion (about one quarter of the

country’s current GDP).

South Africa: The economics of nuclear energy

March 2016

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 2

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

Policy background

In GDP terms, South Africa is the second largest economy in Africa – but it has the highest

energy consumption on the continent, accounting for about 30 per cent of total primary energy

consumption in Africa. Its economy is heavily reliant on the energy-intensive coal mining

industry, as coal accounts for about 72 per cent of the country's total primary energy

consumption – and over 90 per cent of electricity generation. This heavy dependence on coal has

led the country to become Africa’s leading emitter of carbon dioxide (CO2, the single most

important “greenhouse gas”), accounting for 40 per cent of the entire continent’s emissions and

making South Africa the 13th largest emitter in the world, according to the latest (2012) EIA

estimates.

Following the 2009 climate change Summit in Copenhagen at which President Zuma pledged

ambitious reductions in CO2 emissions on condition that South Africa was supported in this goal

by international financial and technology transfers, the Department of Energy released a draft

Integrated Electricity Resource Plan (IERP) for 2010-2030. The IERP forecasts electricity

demand and outlines how this demand might be met in a way that would also lead to secure

energy supplies and reduced CO2 emissions. The IERP calls for 52GW of new electricity

generation capacity by 2030, assuming 3.4GW of demand-side savings owing to the expected

reduced energy intensity of GDP.

This was the first official policy statement which signaled a growing role for nuclear power as

part of the country’s low carbon strategy. The plan foresaw that South Africa’s generation mix

by 2030 should break down as follows: 48 per cent coal; 13.4 per cent nuclear; 6.5 per cent

hydro, 14.5 per cent other renewables, and 11 per cent open cycle gas turbines to meet peak-load

demand. An updated version of this plan published in 2011 increased the projected share of

nuclear to 22 per cent based on the construction of 9.6 GW of new nuclear capacity by 2030.

This nuclear power strategy has moved into a higher gear since 2014. In its annual report to

parliament submitted in October 2015, the Department of Energy reported the completion of

“vendor parades” with five countries: China, France, Russia, South Korea and the US. Following

the completion of the preliminary formality of signing inter-governmental agreements on nuclear

energy with all five of these countries, the Department called in December 2015 for initial

nuclear construction and financing proposals from these potential bidders.

This momentum appeared to be underpinned by a clear reaffirmation of the nuclear energy

strategy by Zuma in his annual State of the Nation Address in February 2015:

“Our plan is to introduce 9,600MW of nuclear energy in the next decade. We will test the market

to ascertain the true cost of building modern nuclear plants. Let me emphasize that we will only

procure nuclear on a scale and pace that our country can afford”.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 3

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

In the ensuing parliamentary debate on the Address, the Energy Minister Tina Joemat-Pettersson

emphasized the importance of water conservation as a factor underlying the plan to build a fleet

of modern nuclear power plants (NPPs). She noted that Koeberg (South Africa’s one existing

NPP, commissioned in 1984) recycles 22 billion litres of seawater, while Medupi (a coal-fired

power station) uses 17 billion litres of freshwater “that we don’t have enough of.” Her

conclusion was clear: “We simply have to go the nuclear route.”

This clear political momentum behind the nuclear power option co-exists with continuing

debates about the economic rationale for South Africa taking on an investment commitment

likely to be as high as US$50 billion (a concern to which Zuma nodded in his February Address).

Against this background, we take a closer look at the economic case for developing nuclear

energy in South Africa on the scale now envisaged by the authorities.

The following three main sections of this report estimate the cost of nuclear generated electricity,

the extent and benefits of the resulting reduction in CO2 emissions, and the impact on South

Africa’s economy from varying degrees of localization of the investment involved. In each case,

we present our assumptions, method and the results that come out of our models.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 4

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

Levelised cost of electricity

We start by assessing the likely cost of the electricity that would be generated by the ten new

reactors necessary to meet the goal of installing nearly 10GW of nuclear-powered generation

capacity. For this purpose, we use the well-established method developed under the auspices of

the IEA that is designed to estimate the levelised cost of electricity (LCOE). The term

“levelised” captures a key feature of this approach in permitting comparison of the unit costs of

different generation technologies (involving both low-carbon sources and fossil fuels) over their

economic life.

Method & assumptions

To calculate the levelised average lifetime cost of generating electricity from nuclear power in

South Africa, we use the formula used in the IEA publication Projected Costs of Generating

Electricity 2015. This formula breaks down the costs into initial investment, operations and

maintenance, cost of fuel, carbon costs (zero in the case of nuclear) and the cost of capital (or

discount rate).

We posit a staggered timeframe for the construction of each of the ten planned reactors during

the overall period 2018-40. The LCOE is calculated for each reactor then a blended final figure

is arrived at based on the average NPP lifetime.

Detailed Assumptions

Operational parameters

The total cost of building new NPPs with an aggregate capacity of 9.6GW will be US$50

billion.

Building each reactor will take 10 years and construction of the first seven reactors will

be underway by 2020 with 30 per cent of the construction cost of each reactor disbursed

in the first five years from the start of construction.

Once connected to the grid, each plant will operate at 90 per cent of its capacity.

The lifetime of each plant will be 40 years.

Financial parameters

The financial assumptions below use OECD benchmarks for a conservative base case, and a

better case where operational and fuel costs are reduced to a mid-point between the OECD

average and Chinese levels. As for the cost of capital, the better case assumption – while

undercutting the rate implied by the present yields on South African sovereign debt – would stem

from generous vendor finance that may be expected given the competitive pressures in the global

nuclear industry.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 5

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

Operational and management costs (O&M)

o Base case: US$14.5/MWh

o Better case: US$10.7/MWh

Fuel costs

o Base case: US$10.8/MWh

o Better case: US$9.8/MWh

Cost of capital

o Base case: 10 per cent

o Better case: 7 per cent

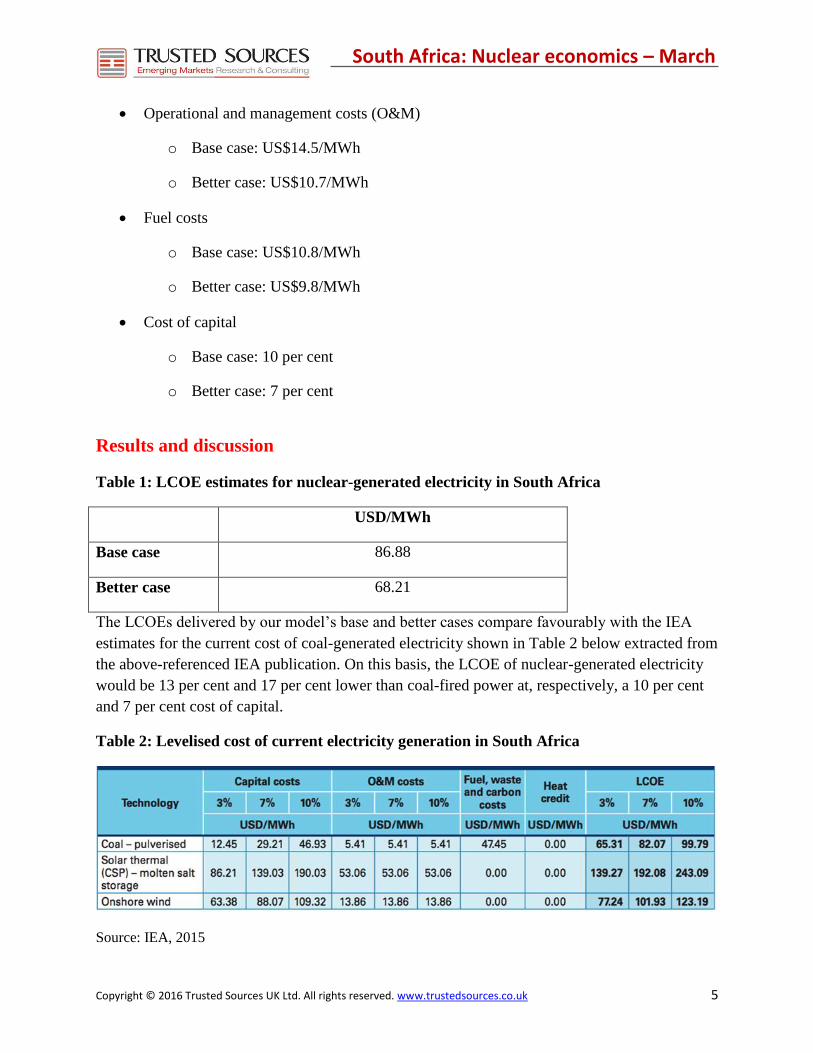

Results and discussion

Table 1: LCOE estimates for nuclear-generated electricity in South Africa

USD/MWh

Base case 86.88

Better case 68.21

The LCOEs delivered by our model’s base and better cases compare favourably with the IEA

estimates for the current cost of coal-generated electricity shown in Table 2 below extracted from

the above-referenced IEA publication. On this basis, the LCOE of nuclear-generated electricity

would be 13 per cent and 17 per cent lower than coal-fired power at, respectively, a 10 per cent

and 7 per cent cost of capital.

Table 2: Levelised cost of current electricity generation in South Africa

Source: IEA, 2015

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 6

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

The comparison with the cost of coal-generated power would have been even more favourable

based on longer-term average coal prices, as the current cost of the fuel is well below that

average as a result of sharp price falls during the present decade. In the future, the underlying

coal price is likely to continue its decline with demand for this most polluting of fuels falling

away as countries strive to reduce emissions. On the other hand, the actual price of coal will, on

the contrary, be increased in countries that introduce meaningful carbon taxation.

Either way, the prospect for coal is one of price volatility: and in this area, nuclear-generated

power has the advantage of offering steady supply at stable prices (assuming only that regulation

of end-user electricity prices maintains a level playing field as between fuels and technologies).

Since South Africa’s nuclear power plans would, if implemented, result in nuclear taking a 20

per cent share of the generation market, it is reasonable to expect that volatility in the overall cost

– and, subject to regulatory decisions, price – of electricity would be reduced by the same 20 per

cent. Reduced volatility in costs and output might be advantageous for the industrial sector, as it

means fewer interruptions in the production process due to electricity shortages. More stable

electricity – in terms both of cost (price) and output – should support existing industrial

capabilities of the country, as well as stimulating further investment in energy intensive

industries.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 7

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

Low carbon effect

In this section we present the results of modelling the extent of reduction in carbon emissions

that would result from the implementation of South Africa’s announced intention to develop

large scale nuclear energy capacity.

Step-by-step assumptions

The first step in this analysis is to estimate the outlook for electricity consumption. Our starting

assumption here is that per capita consumption will remain steady at the level of a little over

4,600kWh as predicted by a MA (moving average, or ARIMA 001) model. (We rejected the

alternative modelling approach of extrapolating from an historic trend since the increases in

consumption seen in the 1970-80s were driven by the rapid development of electricity supplies at

that time.)

Chart 1: Electric power consumption

This projection shown in Chart 1 above of constant average per capita consumption assumes a

mutually offsetting effect of two drivers: first, on the positive side, increases in per capita

incomes and consumption will include electricity consumption; second, on the negative side, the

adoption of energy efficient technology will reduce the energy intensity of GDP.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 8

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

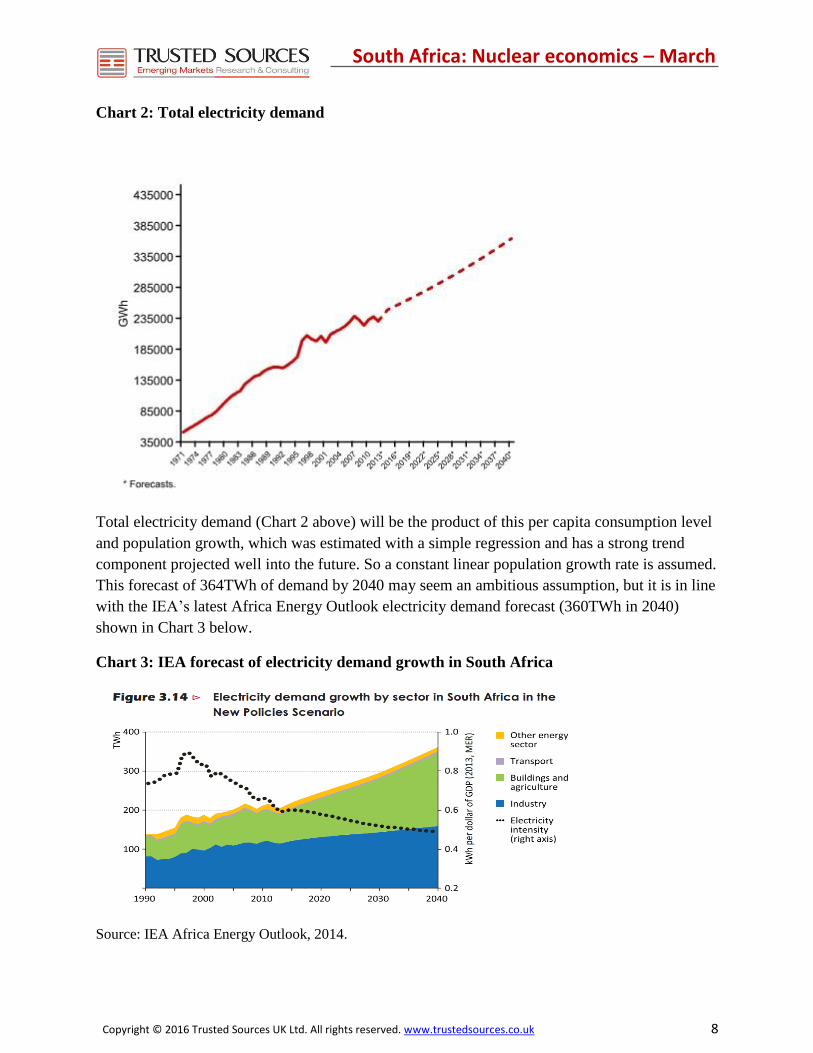

Chart 2: Total electricity demand

Total electricity demand (Chart 2 above) will be the product of this per capita consumption level

and population growth, which was estimated with a simple regression and has a strong trend

component projected well into the future. So a constant linear population growth rate is assumed.

This forecast of 364TWh of demand by 2040 may seem an ambitious assumption, but it is in line

with the IEA’s latest Africa Energy Outlook electricity demand forecast (360TWh in 2040)

shown in Chart 3 below.

Chart 3: IEA forecast of electricity demand growth in South Africa

Source: IEA Africa Energy Outlook, 2014.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 9

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

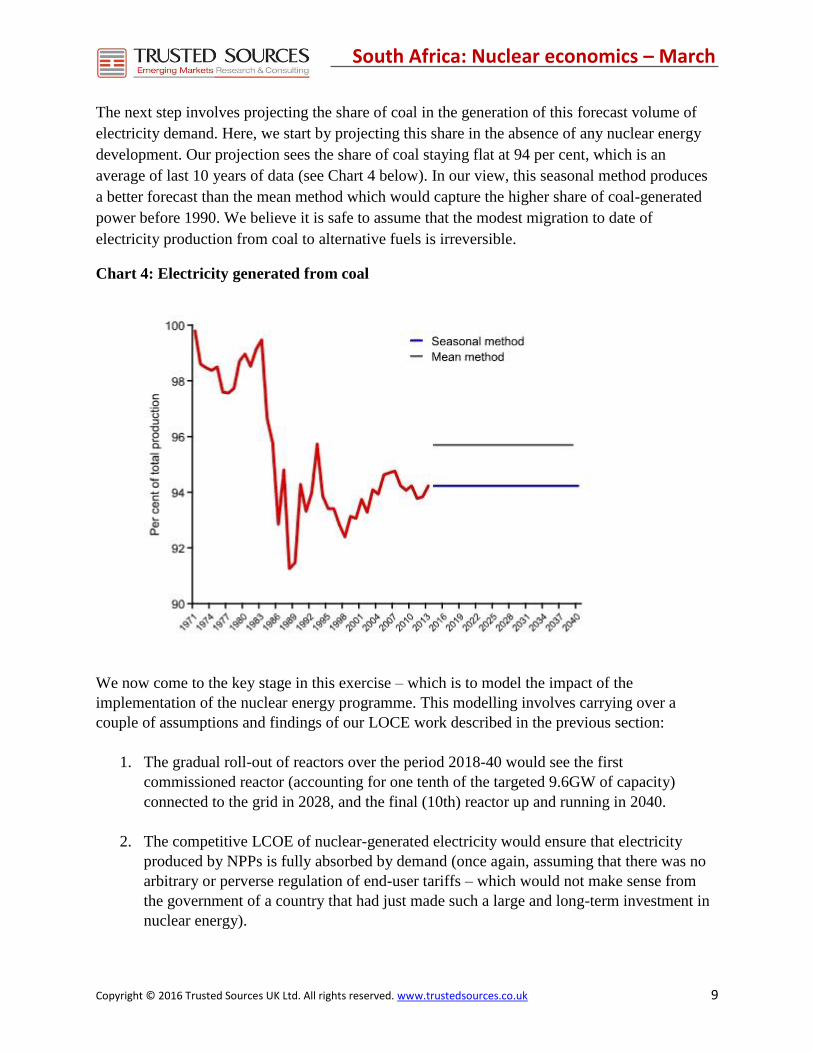

The next step involves projecting the share of coal in the generation of this forecast volume of

electricity demand. Here, we start by projecting this share in the absence of any nuclear energy

development. Our projection sees the share of coal staying flat at 94 per cent, which is an

average of last 10 years of data (see Chart 4 below). In our view, this seasonal method produces

a better forecast than the mean method which would capture the higher share of coal-generated

power before 1990. We believe it is safe to assume that the modest migration to date of

electricity production from coal to alternative fuels is irreversible.

Chart 4: Electricity generated from coal

We now come to the key stage in this exercise – which is to model the impact of the

implementation of the nuclear energy programme. This modelling involves carrying over a

couple of assumptions and findings of our LOCE work described in the previous section:

1. The gradual roll-out of reactors over the period 2018-40 would see the first

commissioned reactor (accounting for one tenth of the targeted 9.6GW of capacity)

connected to the grid in 2028, and the final (10th) reactor up and running in 2040.

2. The competitive LCOE of nuclear-generated electricity would ensure that electricity

produced by NPPs is fully absorbed by demand (once again, assuming that there was no

arbitrary or perverse regulation of end-user tariffs – which would not make sense from

the government of a country that had just made such a large and long-term investment in

nuclear energy).

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 10

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

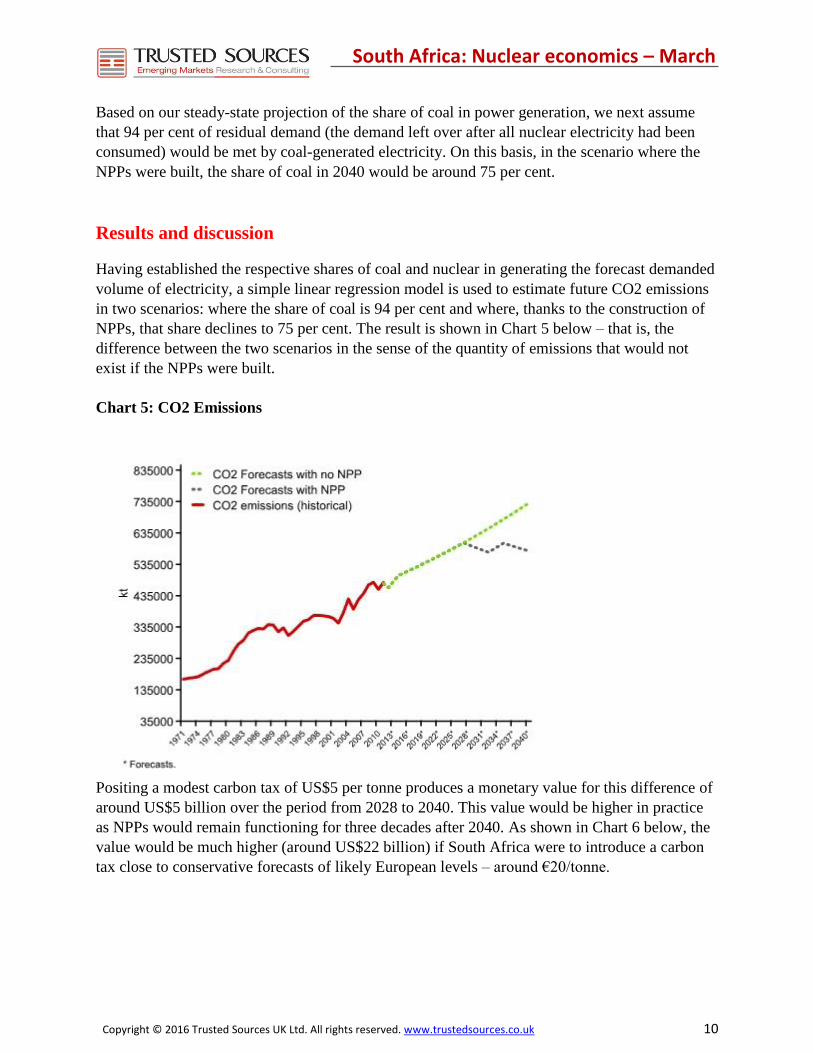

Based on our steady-state projection of the share of coal in power generation, we next assume

that 94 per cent of residual demand (the demand left over after all nuclear electricity had been

consumed) would be met by coal-generated electricity. On this basis, in the scenario where the

NPPs were built, the share of coal in 2040 would be around 75 per cent.

Results and discussion

Having established the respective shares of coal and nuclear in generating the forecast demanded

volume of electricity, a simple linear regression model is used to estimate future CO2 emissions

in two scenarios: where the share of coal is 94 per cent and where, thanks to the construction of

NPPs, that share declines to 75 per cent. The result is shown in Chart 5 below – that is, the

difference between the two scenarios in the sense of the quantity of emissions that would not

exist if the NPPs were built.

Chart 5: CO2 Emissions

Positing a modest carbon tax of US$5 per tonne produces a monetary value for this difference of

around US$5 billion over the period from 2028 to 2040. This value would be higher in practice

as NPPs would remain functioning for three decades after 2040. As shown in Chart 6 below, the

value would be much higher (around US$22 billion) if South Africa were to introduce a carbon

tax close to conservative forecasts of likely European levels – around €20/tonne.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 11

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

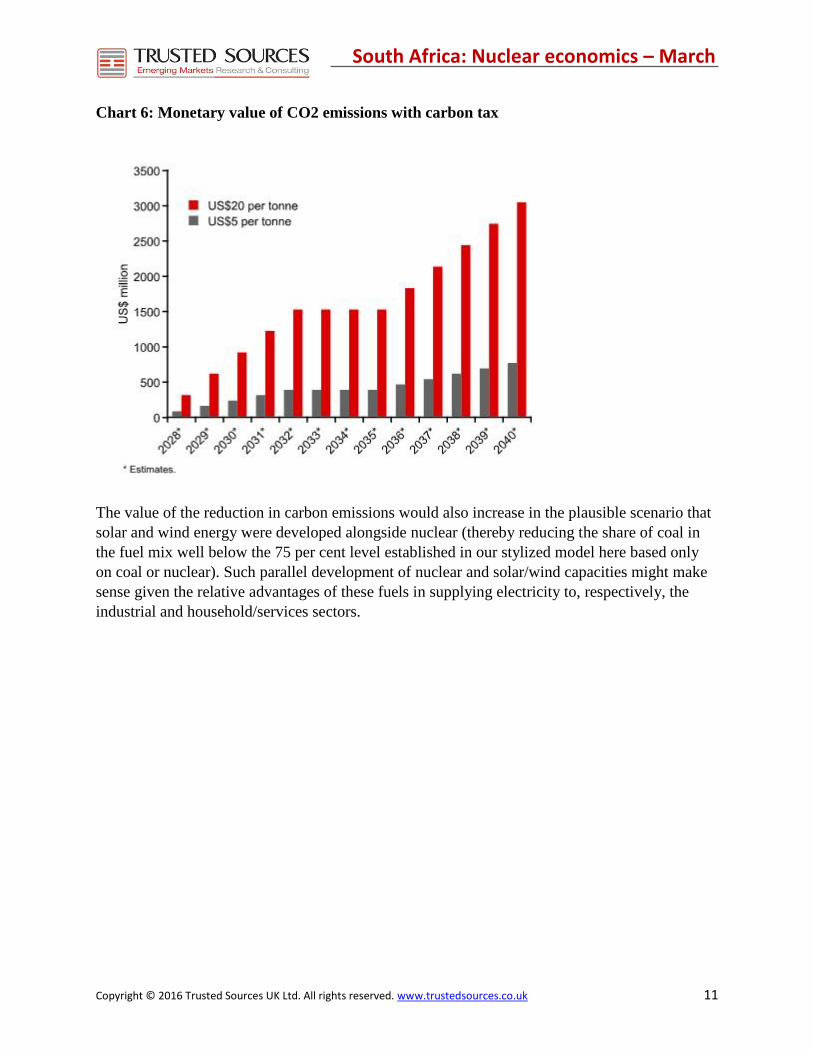

Chart 6: Monetary value of CO2 emissions with carbon tax

The value of the reduction in carbon emissions would also increase in the plausible scenario that

solar and wind energy were developed alongside nuclear (thereby reducing the share of coal in

the fuel mix well below the 75 per cent level established in our stylized model here based only

on coal or nuclear). Such parallel development of nuclear and solar/wind capacities might make

sense given the relative advantages of these fuels in supplying electricity to, respectively, the

industrial and household/services sectors.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 12

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

Localization scenarios

A major attraction for countries developing nuclear energy for the first time or, as would be

South Africa’s case, expanding materially on a small existing base of capacity and scientific and

technical skills established at the Koeberg NPP, is the positive shock to industry and the skills

base that can come from the localization of a part of the investment in nuclear new builds. The

extent of potential localization varies according to the choice of main vendor and technology.

We have modelled the impact on overall economic growth of two levels of localization relative

to a scenario of “no localization” (that is, no nuclear energy development). The base level is 15

per cent localization, and the high case is 45 per cent, based on indications of maximum possible

localization levels indicated by some potential vendors including the French and the Russians.

Assumptions and method

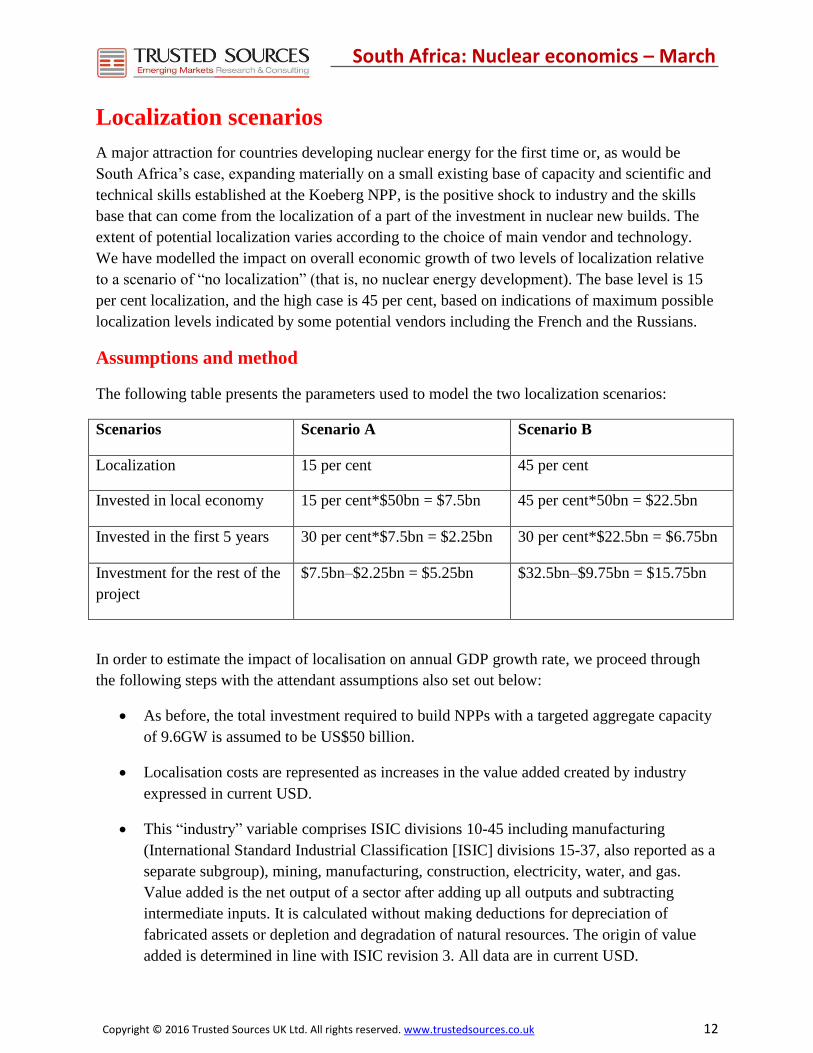

The following table presents the parameters used to model the two localization scenarios:

Scenarios Scenario A Scenario B

Localization 15 per cent 45 per cent

Invested in local economy 15 per cent*$50bn = $7.5bn 45 per cent*50bn = $22.5bn

Invested in the first 5 years 30 per cent*$7.5bn = $2.25bn 30 per cent*$22.5bn = $6.75bn

Investment for the rest of the

project

$7.5bn–$2.25bn = $5.25bn $32.5bn–$9.75bn = $15.75bn

In order to estimate the impact of localisation on annual GDP growth rate, we proceed through

the following steps with the attendant assumptions also set out below:

As before, the total investment required to build NPPs with a targeted aggregate capacity

of 9.6GW is assumed to be US$50 billion.

Localisation costs are represented as increases in the value added created by industry

expressed in current USD.

This “industry” variable comprises ISIC divisions 10-45 including manufacturing

(International Standard Industrial Classification [ISIC] divisions 15-37, also reported as a

separate subgroup), mining, manufacturing, construction, electricity, water, and gas.

Value added is the net output of a sector after adding up all outputs and subtracting

intermediate inputs. It is calculated without making deductions for depreciation of

fabricated assets or depletion and degradation of natural resources. The origin of value

added is determined in line with ISIC revision 3. All data are in current USD.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 13

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

This “industry” variable is then forecast using ARIMA (extending an increasing trend).

A new variable is added: “industry + localization boost”, which combines the base

forecast for industry value added with one or another level of localization.

This produces three industry forecasts (no localization, 15 per cent and 45 per cent

localizations).

The next step is to use this “industry” variable to forecast GDP growth and compare the

results in the no localization, 15 per cent localization and 45 per cent localization

scenarios.

Results and discussion

The differences between those forecasts are shown in Chart 7 below.

Chart 7: Effect of localization on GDP

As can be seen in this chart, there is a clear reaction of GDP to localized investment and its effect

of increasing industrial activity. Under the highest level of localization (Scenario B) the model

indicates that the average annual GDP growth rate would be 0.007 per cent higher than in the no

localization scenario, while the equivalent figure in the 15 per cent localization scenario

(Scenario A) would be 0.002 per cent. While these gains are clearly marginal, they are not

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 14

South Africa: Nuclear economics – March

2016 20162016Outlook

Report

negligible given that the largest incremental input is only 45 per cent of US$50 billion spread out

over 22 years, where every year GDP is over US$300 billion.

Another perspective on the scale of this contribution can be gained by aggregating the monetary

value in current USD of the incremental GDP attributable to the 45 per cent localization of

investment in NPP development. That number is USD77.3 billion (compared to US$26 billion in

the 15 per cent localization scenario) – or around one quarter of South Africa’s current annual

GDP. This compares with the USD22.5 billion of “localized” investment in domestic industry:

there is thus a substantial multiplier effect that, according to our model, would be around 3.4x.

It is worth noting an additional benefit of localization that cannot be directly quantified. Industry

experts would expect around a third of the localized investment to be directed towards the

production of specialized equipment for use in the future NPPs (while the rest would create more

generic manufacturing capacity for construction materials and so on). That specialized part of

localization may provide future opportunities to export NPP components (similar to the way that

some German vehicle makes now assembled in South Africa are exported to Asia). This point

underlines the potential returns to scale – that is, prospects of this indirect benefit for the real

economy would rise in the line with the extent, and efficiency, of localization.

.

Copyright © 2016 Trusted Sources UK Ltd. All rights reserved. www.trustedsources.co.uk 15

South Africa: Nuclear economics – March

2016 2016 Outlook

5

Quarterly Report

Trusted Sources Disclosure Statement

The analysis and information presented in this report (Report) by Trusted Sources UK Limited (TS) may include summary profiles of key companies in the relevant sector and the information is offered for subscriber interest only. This Report is not to be used or considered as a recommendation to buy, hold or sell any securities or other financial instruments and does not constitute an investment recommendation or investment advice. The information contained in this Report has been compiled by TS from various public and industry sources that we believe to be reliable; no representation or warranty, expressed or implied is made by TS, its affiliates or any other person as to the accuracy or completeness of the information. TS is not responsible for any errors in or omissions to such information, or for any consequences that may result from the use of such information. Such information is provided with the expectation that it will be read as part of a wider investment analysis and this Report should not be relied upon on a stand-alone basis. Past performance should not be taken as an indication or guarantee of future performance; we make no representation or warranty regarding future performance. The opinions expressed in this Report reflect the judgment of TS as of the date hereof and are subject to change without notice. This Report is not an offer to sell or a solicitation of an offer to buy any securities. The offer and sale of securities are regulated generally in various jurisdictions, particularly the manner in which securities may be offered and sold to residents of a particular country or jurisdiction. Securities referenced in this Report may not be eligible for sale in some jurisdictions. To the fullest extent provided by law, neither TS nor any of its affiliates, nor any other person accepts any liability whatsoever for any direct or consequential loss, including without limitation, lost profits arising from any use of this Report or the information contained herein. No director, officer or employee of TS is on the board of directors of any company referenced herein and no one at any such referenced company is on the board of directors of TS. TS does not invest in any securities although it is possible that one or more of TS's directors, officers, employees or consultants may at times be invested in the securities of a referenced company. TS is not authorised or regulated in the United Kingdom by the Financial Services Authority or by any other regulator in any jurisdiction for the provision of investment advice. Specific professional financial and investment advice should be sought from your stockbroker, bank manager, solicitor, accountant or other independent professional adviser authorised pursuant to the Financial Services and Markets Act 2000 if you are resident in the United Kingdom or, if not, another appropriately qualified independent financial adviser who specialises in advising on the acquisition of shares and other securities before any investment is undertaken. This Report, including the text and graphics, is subject to copyright protection under English law and, through international treaties, other countries. No part of the contents or materials available in this Report may be reproduced, licensed, sold, hired, published, transmitted, modified, adapted, publicly displayed, broadcast or otherwise made available in any way without TS's prior written permission. All rights reserved.

Trusted Sources UK Limited

Europe +44 (0) 20 7183 5280 The Americas +1 (646) 496 9856 Asia +852 2973 6093 [email protected] www.trustedsources.co.uk

Contact us

Please read this important disclosure statement which includes our disclaimer and copyright status