smart infrastructure business and policy dialogue 2014:global best practice infrastructure - who...

DESCRIPTION

A presentation conducted by Mr Ross Love, Senior Partner, Boston Consulting Group, Australia and New Zealand. Presented on Wednesday the 13th of August, 2014. Ross Love is a Senior Partner of The Boston Consulting Group (BCG) in Australia and New Zealand, and until July 2014 the Managing Partner of BCG’s Australian and New Zealand Offices,and a member of the firm’s Asia Pacific Management Team. He has over 20 years experience consulting to senior executives and boards in the transport, consumer, industrial goods and public sectors. He has been the global leader of BCG’s Travel and Tourism Practice and is a member of the leadership team for BCG’s Consumer Practice and Business Transformation Practice. He consults on issues of strategy (including acquisitions), operations (including pricing), supply chain effectiveness and workforce productivity, and organisation (including design and change management). Ross is a Director of Jawun – Indigenous Corporate Partnerships, and a Special Advisor to the Wunan Foundation, an Indigenous development organisation in the East Kimberley. He has recently supported the Australian B20 leadership team, and in particular the Infrastructure and Investment Taskforce chaired by David Thodey. Before joining BCG in 1993, Ross was the Chief of Staff to the Premier of Western Australia. This followed four at Harvard University and consulting in California, and three years as an economic policy adviser to the Government of Western Australia. Ross has a Bachelor of Arts with first class honours in Politics from the University of Western Australia, a Masters of Public Administration from Harvard University and has completed further business studies at the London Business School. He was a Harkness Fellow for Australia in 1986. Ross is a Past President of the Harvard Club of Australia.TRANSCRIPT

Monday, 30th September 2013: Business & policy Dialogue

Tuesday 1 October to Thursday, 3rd October: Academic and Policy Dialogue

www.isngi.org

ENDORSING PARTNERS

The following are confirmed contributors to the business and policy dialogue in Sydney:

• Rick Sawers (National Australia Bank)

• Nick Greiner (Chairman (Infrastructure NSW)

smart.uow.edu.au

Global Best Practice Infrastructure – Who Does it Best and What Can Australia Learn?

Presented by: Mr Ross Love, Senior Partner, Boston Consulting Group, Australia and New Zealand

Leading practices in infrastructure Presentation to SMART Infrastructure Business and Policy Dialogue

August 2014

SMART BPD Presentation - Ross Love BCG.pptx 2

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Introduction

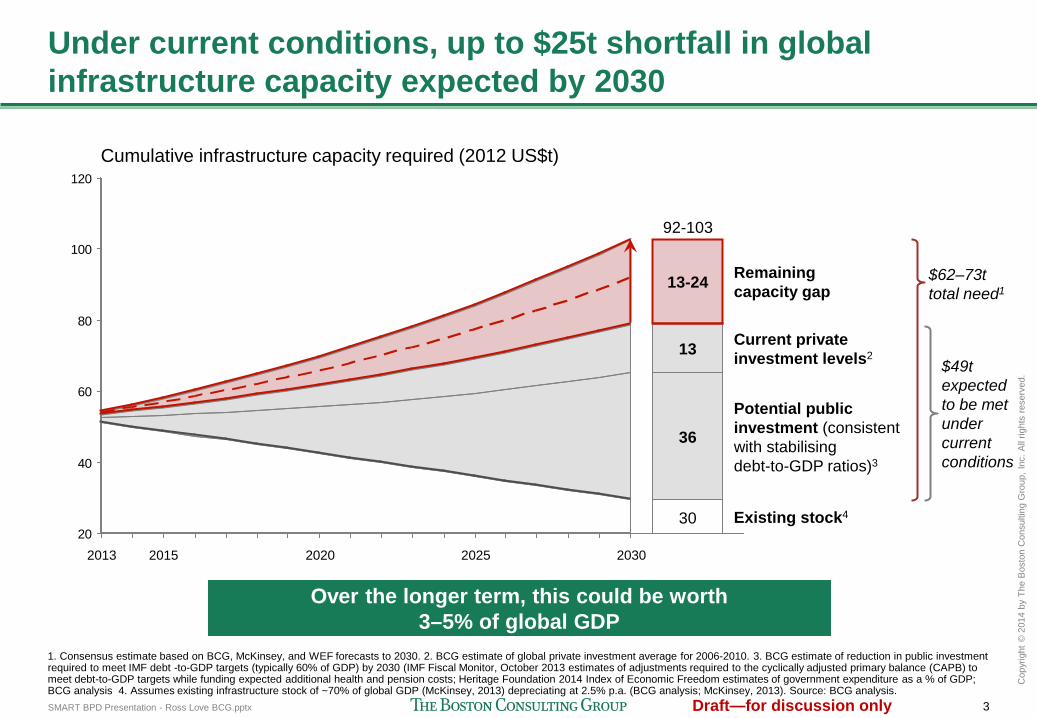

There is a pressing need to address the growing global infrastructure gap • Under current conditions, up to $25t shortfall in global infrastructure capacity expected by 2030 • Over the long-term, this could be worth 3–5% of global GDP

Closing this gap requires improvements across the infrastructure life-cycle

• Credible infrastructure pipelines that prioritise the right investments • Rigorous preparation and procurement to set them up for success • Ongoing optimisation of operations and maintenance to maximise their value over time • A supportive, predictable and transparent enabling environment

Australia has a strong foundation to build on, but there is clear room for improvement, e.g.

• Ensure IA reforms translate into real improvements in project selection • Make more systemic use of user charging and alternative revenue sources • Promote greater innovation in project delivery and execution • Improve data capture and availability, and enable super funds to take greater responsibility for

long-term capital formation

SMART BPD Presentation - Ross Love BCG.pptx 3

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Under current conditions, up to $25t shortfall in global infrastructure capacity expected by 2030

20

40

60

80

100

120

2025 2020 2015 2013 2030

Cumulative infrastructure capacity required (2012 US$t)

92-103

13

Existing stock4

Potential public investment (consistent with stabilising debt-to-GDP ratios)3

13-24

30

36

Remaining capacity gap

Current private investment levels2 $49t

expected to be met under current conditions

$62–73t total need1

1. Consensus estimate based on BCG, McKinsey, and WEF forecasts to 2030. 2. BCG estimate of global private investment average for 2006-2010. 3. BCG estimate of reduction in public investment required to meet IMF debt -to-GDP targets (typically 60% of GDP) by 2030 (IMF Fiscal Monitor, October 2013 estimates of adjustments required to the cyclically adjusted primary balance (CAPB) to meet debt-to-GDP targets while funding expected additional health and pension costs; Heritage Foundation 2014 Index of Economic Freedom estimates of government expenditure as a % of GDP; BCG analysis 4. Assumes existing infrastructure stock of ~70% of global GDP (McKinsey, 2013) depreciating at 2.5% p.a. (BCG analysis; McKinsey, 2013). Source: BCG analysis.

Over the longer term, this could be worth 3–5% of global GDP

SMART BPD Presentation - Ross Love BCG.pptx 4

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Closing this gap will require improvements across the infrastructure lifecycle ...

20

40

60

80

100

120

2030 2025 2020 2015 2013

Cumulative infrastructure capacity required (2012 US$t)

Increased availability of financing

Enhanced enabling environment

Improved project execution

Rigorous preparation and procurement

Improved project selection and prioritisation

~15%

10-15%

~30%

~30-35%

~10%

Maximum lever potential

Note: Based on estimates: of the benefits of improved project selection and prioritisation (BCG; McKinsey); the 'privatisable' share of current government non-financial assets (Infrastructure Australia; The Economist; OECD; BCG analysis); increased revenue potential of user charges, land value capture, and ancillary revenue (African Infrastructure Country Diagnostic; IEA; WEF; BCG analysis); cost efficiencies in construction and O&M (WEF; BCG; McKinsey); the impact of improving all countries' regulatory environment to current best practice (World Bank; BCG analysis); and the impact of increasing depth of national financial markets towards world best practice (World Bank; BCG analysis). Source: BCG analysis.

SMART BPD Presentation - Ross Love BCG.pptx 5

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Origination Preparation and procurement Execution

Source: BCG; World Economic Forum

... but this is primarily about getting 'the basics' right

Project cycle

Needs-based, long-term infrastructure vision

Bankable feasibility studies that rigorously forecast demand, revenue and cost

Optimised asset value and utilisation

Integrated, evidence-based selection and prioritisation

Clear allocation of risks to parties best able to manage them

Lifecycle-focus in maintenance and investment to increase lifetime value

Rigorous 'value for money' analysis to determine delivery model

Rigorous, standardised project preparation processes

Lean organisation and processes to minimise construction and operating costs

Transparent, competitive, and efficient procurement processes

Enabling environment

Stable, transparent and effective legal & regulatory framework

High quality, widely accessible data and benchmarks

Efficient regulatory and approvals processes

High capability workforce

Adequate access to long-term finance

SMART BPD Presentation - Ross Love BCG.pptx 6

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Origination Preparation and procurement Execution

Source: BCG; World Economic Forum

... but this is primarily about getting 'the basics' right

Project cycle

Needs-based, long-term infrastructure vision

Bankable feasibility studies that rigorously forecast demand, revenue and cost

Optimised asset value and utilisation

Integrated, evidence-based selection and prioritisation

Clear allocation of risks to parties best able to manage them

Lifecycle-focus in maintenance and investment to increase lifetime value

Rigorous 'value for money' analysis to determine delivery model

Rigorous, standardised project preparation processes

Lean organisation and processes to minimise construction and operating costs

Transparent, competitive, and efficient procurement processes

Enabling environment

Stable, transparent and effective legal & regulatory framework

High quality, widely accessible data and benchmarks

Efficient regulatory and approvals processes

High capability workforce

Adequate access to long-term finance

SMART BPD Presentation - Ross Love BCG.pptx 7

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Origination Preparation and procurement Execution

Source: BCG; World Economic Forum

... but this is primarily about getting 'the basics' right

Project cycle

Needs-based, long-term infrastructure vision

Bankable feasibility studies that rigorously forecast demand, revenue and cost

Optimised asset value and utilisation

Integrated, evidence-based selection and prioritisation

Clear allocation of risks to parties best able to manage them

Lifecycle-focus in maintenance and investment to increase lifetime value

Rigorous 'value for money' analysis to determine delivery model

Rigorous, standardised project preparation processes

Lean organisation and processes to minimise construction and operating costs

Transparent, competitive, and efficient procurement processes

Enabling environment

Stable, transparent and effective legal & regulatory framework

High quality, widely accessible data and benchmarks

Efficient regulatory and approvals processes

High capability workforce

Adequate access to long-term finance

SMART BPD Presentation - Ross Love BCG.pptx 8

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Origination Preparation and procurement Execution

Source: BCG; World Economic Forum

... but this is primarily about getting 'the basics' right

Project cycle

Needs-based, long-term infrastructure vision

Bankable feasibility studies that rigorously forecast demand, revenue and cost

Optimised asset value and utilisation

Integrated, evidence-based selection and prioritisation

Clear allocation of risks to parties best able to manage them

Lifecycle-focus in maintenance and investment to increase lifetime value

Rigorous 'value for money' analysis to determine delivery model

Rigorous, standardised project preparation processes

Lean organisation and processes to minimise construction and operating costs

Transparent, competitive, and efficient procurement processes

Enabling environment

Stable, transparent and effective legal & regulatory framework

High quality, widely accessible data and benchmarks

Efficient regulatory and approvals processes

High capability workforce

Adequate access to long-term finance

SMART BPD Presentation - Ross Love BCG.pptx 9

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Origination Preparation and procurement Execution

Source: BCG; World Economic Forum

... but this is primarily about getting 'the basics' right

Project cycle

Needs-based, long-term infrastructure vision

Bankable feasibility studies that rigorously forecast demand, revenue and cost

Optimised asset value and utilisation

Integrated, evidence-based selection and prioritisation

Clear allocation of risks to parties best able to manage them

Lifecycle-focus in maintenance and investment to increase lifetime value

Rigorous 'value for money' analysis to determine delivery model

Rigorous, standardised project preparation processes

Lean organisation and processes to minimise construction and operating costs

Transparent, competitive, and efficient procurement processes

Enabling environment

Stable, transparent and effective legal & regulatory framework

High quality, widely accessible data and benchmarks

Efficient regulatory and approvals processes

High capability workforce

Adequate access to long-term finance

Selected examples

SMART BPD Presentation - Ross Love BCG.pptx 10

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Institutional set-up is critical to establishing a credible infrastructure pipeline that prioritises the right investments

Needs-based long-term

infrastructure vision

Integrated, evidence-based selection

and prioritisation

Rigorous 'value for money' analysis

Preparation and procurement

Early and effective public involvement E.g. France's National Commission for Public Debate (CNDP) is charged with organising public consultation as early as possible in the project lifecycle

Formal requirement for independent, expert review (incl. ex-post evaluation) and advice E.g. South Korea's PIMAC is required to verify CBA and value-for-money analyses before a project can proceed

Transparency of assessments and decision-making E.g. Infrastructure Ontario ensures value-for-money methodology and assessments are publicly disclosed

Clearly defined stage gates E.g. UK Major Projects Authority is responsible for formal stage gate reviews, including explicit option to halt projects based on updated information

Project selection clearly separated from choice of delivery model

Unfettered choice to review projects, incl. unsolicited proposals

Source: BCG.

SMART BPD Presentation - Ross Love BCG.pptx 11

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Sustainable revenue models leverage a broad range of funding sources: not just taxes or user charges

Source: BCG; World Economic Forum.

50% of RDE PPPs rely on user fees vs. few in developed countries

Potential can range from 010% of revenue utilities

to 50% in airports

Metro lines have recovered 50-85% of

required funding

India limits viability gap funding to 20% of total

project cost

User charges

Ensure public buy-in • Clearly link to quality

improvements (e.g. Stockholm congestion charge)

Optimise pricing

• Minimise 'pain' of payment (e.g. e-tolling)

• Diversify service levels to balance cost and revenue (e.g. Manila Water's 'Water for the Poor')

Ancillary revenue

Address user needs holistically

• Satisfy advanced needs in core business (e.g. energy-saving solutions)

• Pursue adjacent services (e.g. sell warehousing at ports)

• Consider unrelated revenue sources (e.g. cabling under roads)

Partner effectively to up the odds of success

Land value capture

Choose an appropriate level of risk

• Tradable development rights (e.g. CEPACs in Brazil)

• Joint-develop land with concessionaire (e.g. MTR in HK)

• Buy and re-sell land before announcement (e.g. Copenhagen metro)

Act quickly to exploit window of opportunity

Government payments

Use to bridge 'viability-gap' where necessary

• Based on rigorous analysis, not by default

Ensure risk allocation incentivises outcomes

• Availability payments reflect service-levels (e.g. UK A1 payments inversely proportional to congestion levels)

• Shadow tolling (e.g. Belras road in Portugal)

Key

suc

cess

fact

ors

Pote

ntia

l

SMART BPD Presentation - Ross Love BCG.pptx 12

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Operations control

Maintenance

User self-regulation

Time-based charging

3

2

1

Data-driven technology can drive significant improvements in asset utilisation and maintenance

Impact Leading practice

Ope

rato

rs

Use

rs

Incr

easi

ng in

terv

entio

n w

ith u

ser b

ehav

iour

Provide users with data they

need to change behavior

Impose usage limitations only

when/where necessary

Use social mitigation

measures to ensure public

buy-in

Monitor data to predict

deterioration in asset condition

Example

• SF Smart Parking program uses a smart phone app to broadcast the location of available parking spaces in real-time (including their demand-adjusted parking prices)

• Average time searching for parking has decreased 43%; target occupancy met 31% more often

• NYC system, Midtown in Motion monitors real-time microwave sensors, cameras and e-tolling readers to identify choke points, adjust signals and clear traffic

• Travel speeds improved by 10%

• Proportion of potholes closed within 2 days increased from 48 to 92%

• Boston's pothole-finding app, Street Bump crowdsources asset condition data to locate patches of road that need or will need repair

• Washington State Route 167 dynamically prices HOT (High Occupancy Toll) lanes based on real-time traffic levels updated every 5 minutes

• Vehicle numbers reduced by 5%; collisions down 2% and speeds have increased by 20%

4

Source: BCG; World Economic Forum; San Francisco Municipal Transportation Agency; City of Boston Public Works Department.

SMART BPD Presentation - Ross Love BCG.pptx 13

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Dramatic efficiency improvements in approvals possible without compromising the integrity of the process

Source: BCG; European Commission (2011) Permitting procedures for energy infrastructure projects in the EU: evaluation and legal recommendations; Canada MPMO (Major Projects Management Office; OECD (2010) Better regulation in Europe: France; Memorandum of Understanding (2009) Transmission Siting on Federal Lands.

Standardised approval pathways

with a single point of

accountability

Early and effective public

participation

Clear allocation of responsibility

between agencies

Rationalised regulatory objectives

• Legislation enforces strict timeframes for overall approvals

• Responsible agency can take decision in lieu of local authorities if input not provided

Netherlands

• 9 Federal agencies signed an MoU

to speed up approval of transmission lines, reduce duplication and ensure seamless processes

United States Canada

• Created single point of entry for resource projects

• Reduced number of agencies involved from 40 to 3

• Legislation requires public involvement as early as possible in the approval process to improve buy-in and identify areas of tension

France

Clear time limits for overall approvals

SMART BPD Presentation - Ross Love BCG.pptx 14

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Origination Preparation and procurement Execution

Source: BCG; World Economic Forum

Australia has a strong foundation to build from, but there is clear room for improvement

Project cycle

Needs-based, long-term infrastructure vision

Bankable feasibility studies that rigorously forecast demand, revenue and cost

Optimised asset value and utilisation

Integrated, evidence-based selection and prioritisation

Clear allocation of risks to parties best able to manage them

Lifecycle-focus in maintenance and investment to increase lifetime value

Rigorous 'value for money' analysis to determine delivery model

Rigorous, standardised project preparation processes

Lean organisation and processes to minimise construction and operating costs

Transparent, competitive, and efficient procurement processes

Enabling environment

Stable, transparent and effective legal & regulatory framework

High quality, widely accessible data and benchmarks

Efficient regulatory and approvals processes

High capability workforce

Adequate access to long-term finance

Ensure Infrastructure Australia reforms translate into real improvements in

practice

Make more systemic use of user charging

and alternative revenue sources

Promote greater innovation in execution

Improve data capture and availability Enable super funds to take greater responsibility for long-term capital formation

SMART BPD Presentation - Ross Love BCG.pptx 15

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Direct user charges are a small proportion of Australian road-related revenue

50

100

0

11%

25%

9%

50%

75%

91%

France Switzerland

8%

81%

44%

41%

Australia

41%

Germany UK

19%

2%

98%

US

5%

75%

Norway

% of annual road-related revenue

25%

Note: Direct usage charges comprise tolls; indirect usage charges include fuel and motor vehicle taxes; one-off fees include vehicle registration and licensing fees; unrelated income includes e.g. investment income; for Australia, Fringe Benefits Tax was treated as a one-off fee; for the US, motor-vehicle and other taxes and fees were split among one-off fees and indirect usage charges. Source: Australian Department of Infrastructure and Transport 2011; Comité des Constructeurs Français d'Automobiles 2009; Eidgenössische Finanzverwaltung 2009; Bundesministerium der Finanzen 2009; HM Revenue and Customs 2009; Bråthen & Odeck, 'Funding of Road Construction in Norway' 2006; US Federal Highway Administration 2011.

Unrelated income One-off fees Indirect usage charges Direct user charges

Backup

SMART BPD Presentation - Ross Love BCG.pptx 16

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Australian construction firms and infrastructure operators amongst the least innovative sectors of the economy

31 31 3028

25 25 22 2219 18

14 12 11 11 11 11 10

2024

30

19 1814

17 15 1620 18

15

25

1216 16

10

0

10

20

30

40

Agric

ultu

re

Elec

trici

ty, G

as &

W

ater

ser

vice

s

% of Australian businesses introducing innovation, 2012-13

Tran

spor

t &

War

ehou

sing

Con

stru

ctio

n

Rea

l Est

ate

serv

ices

Adm

inis

trativ

e se

rvic

es

Fina

ncia

ll se

rvic

es

Hos

pita

lity

Hea

lth c

are

Rec

reat

ion

serv

ices

Oth

er s

ervi

ces

Prof

essi

onal

se

rvic

es

Med

ia &

Te

leco

Who

lesa

le

Man

ufac

turin

g

Ret

ail

Min

ing

Operational processes Goods or services

Source: ABS, Summary of IT Use and Innovation in Australian Business, 2012-13

Operational processes (Average=18%)

Goods or services (Average=19%)

Backup

SMART BPD Presentation - Ross Love BCG.pptx 17

Draft—for discussion only

Cop

yrig

ht ©

201

4 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Australian super funds have relatively high allocations to infrastructure, particularly in unlisted equity

0

5

10

15

20

25

Ende

sa

Au

stra

lianS

uper

Sust

aina

bilit

y Fu

nd

O

MER

S

GEP

F

C

alPE

RS

Prev

i

AFP

Prov

ida

PFZW

ABP

Ø 0.9 Ø 3.3

CG

D P

ensõ

es

AP

3

Ba

nco

BPI

AFP

Hor

izon

te P

eru

OYA

K

Pe

nsio

n Fu

nd

FA

PES

FUN

CEF

Can

ada

PPI B

oard

PFA

Pens

ion

Imm

arin

en

Afor

e X

XI B

anor

te

Fond

itel

PMT

Pension fund infrastructure investments (% of total assets)

Men

ora-

Miv

tach

im

N

Z Su

per F

und

Que

bec

Pens

ion

Plan

AP4

USS

BT P

ensi

on S

chem

e

OTP

P

Fu

ture

Fun

d

Suns

uper

33 selected funds

69 surveyed funds

Debt Unlisted Equity

Listed Equity

Note: Average infrastructure investments shown include debt and unlisted equity as a % of total assets under management for the 69 funds reflects the average of all funds in the OECD Annual Survey of Large Pension Funds (0.9%). The higher 3.3% figure reflects the weighted average of the 33 funds with any infrastructure allocation. Source: OECD, Annual Survey of Large Pension Funds and Public Pension Reserve Funds, October 2013, BCG analysis.

Backup

Thank you

bcg.com | bcgperspectives.com