slovenia tax guide 2013 - pkf pkf tax guide 2013.pdf · slovenia tax guide 2013. ... the slovenian...

TRANSCRIPT

SloveniaTax Guide

2013

PKF Worldwide Tax Guide 2013 I

Fore

wor

d

foreword

A country’s tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed?

Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. This handy reference guide provides clients and professional practitioners with comprehensive tax and business information for over 90 countries throughout the world.

As you will appreciate, the production of the WWTG is a huge team effort and I would like to thank all tax experts within PFK member firms who gave up their time to contribute the vital information on their country’s taxes that forms the heart of this publication.

I hope that the combination of the WWTG and assistance from your local PKF member firm will provide you with the advice you need to make the right decisions for your international business.

Richard SackinChairman, PKF International Tax CommitteeEisner Amper LLP [email protected]

PKF Worldwide Tax Guide 2013II

Disclaimer

important disclaimer

This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication.This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication.

The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.

PKF International is a network of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms.

PKF Worldwide Tax Guide 2013 III

Pref

ace

preface

The PKF Worldwide Tax Guide 2013 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world’s most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 1 January 2013, while also noting imminent changes where necessary.

On a country-by-country basis, each summary addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country’s personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments.

While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice.

In addition to the printed version of the WWTG, individual country taxation guides are available in PDF format which can be downloaded from the PKF website at www.pkf.com

PKF INTERNATIONAL LIMITEDMAY 2013

©PKF INTERNATIONAL LIMITEDALL RIGHTS RESERVEDUSE APPROVED WITH ATTRIBUTION

PKF Worldwide Tax Guide 2013IV

Introduction

about pKf international limited

PKF International Limited (PKFI) administers the PKF network of legally independent member firms. There are around 300 member firms and correspondents in 440 locations in around 125 countries providing accounting and business advisory services. PKFI member firms employ around 2,270 partners and more than 22,000 staff.PKFI is the 11th largest global accountancy network and its member firms have $2.68 billion aggregate fee income (year end June 2012). The network is a member of the Forum of Firms, an organisation dedicated to consistent and high quality standards of financial reporting and auditing practices worldwide.

Services provided by member firms include:

Assurance & AdvisoryInsolvency – Corporate & PersonalFinancial Planning/Wealth managementTaxationCorporate FinanceForensic AccountingManagement ConsultancyHotel ConsultancyIT Consultancy

PKF member firms are organised into five geographical regions covering Africa; Latin America; Asia Pacific; Europe, the Middle East & India (EMEI); and North America & the Caribbean. Each region elects representatives to the board of PKF International Limited which administers the network. While the member firms remain separate and independent, international tax, corporate finance, professional standards, audit, hotel consultancy and business development committees work together to improve quality standards, develop initiatives and share knowledge and best practice cross the network.

Please visit www.pkf.com for more information.

PKF Worldwide Tax Guide 2013 V

Stru

ctur

e

structure of country descriptions

a. taXes payable

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES

b. determination of taXable income

CAPITAL ALLOWANCES DEPRECIATION STOCK/INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

c. foreiGn taX relief

d. corporate Groups

e. related party transactions

f. witHHoldinG taX

G. eXcHanGe control

H. personal taX

i. treaty and non-treaty witHHoldinG taX rates

PKF Worldwide Tax Guide 2013VI

Time Zones

AAlgeria . . . . . . . . . . . . . . . . . . . .1 pmAngola . . . . . . . . . . . . . . . . . . . .1 pmArgentina . . . . . . . . . . . . . . . . . .9 amAustralia - Melbourne . . . . . . . . . . . . .10 pm Sydney . . . . . . . . . . . . . . .10 pm Adelaide . . . . . . . . . . . . 9.30 pm Perth . . . . . . . . . . . . . . . . . .8 pmAustria . . . . . . . . . . . . . . . . . . . .1 pm

BBahamas . . . . . . . . . . . . . . . . . . .7 amBahrain . . . . . . . . . . . . . . . . . . . .3 pmBelgium . . . . . . . . . . . . . . . . . . . .1 pmBelize . . . . . . . . . . . . . . . . . . . . .6 amBermuda . . . . . . . . . . . . . . . . . . .8 amBrazil. . . . . . . . . . . . . . . . . . . . . .7 amBritish Virgin Islands . . . . . . . . . . .8 am

CCanada - Toronto . . . . . . . . . . . . . . . .7 am Winnipeg . . . . . . . . . . . . . . .6 am Calgary . . . . . . . . . . . . . . . .5 am Vancouver . . . . . . . . . . . . . .4 amCayman Islands . . . . . . . . . . . . . .7 amChile . . . . . . . . . . . . . . . . . . . . . .8 amChina - Beijing . . . . . . . . . . . . . .10 pmColombia . . . . . . . . . . . . . . . . . . .7 amCyprus . . . . . . . . . . . . . . . . . . . .2 pmCzech Republic . . . . . . . . . . . . . .1 pm

DDenmark . . . . . . . . . . . . . . . . . . .1 pmDominican Republic . . . . . . . . . . .7 am

EEcuador . . . . . . . . . . . . . . . . . . . .7 amEgypt . . . . . . . . . . . . . . . . . . . . .2 pmEl Salvador . . . . . . . . . . . . . . . . .6 amEstonia . . . . . . . . . . . . . . . . . . . .2 pm

FFiji . . . . . . . . . . . . . . . . .12 midnightFinland . . . . . . . . . . . . . . . . . . . .2 pmFrance. . . . . . . . . . . . . . . . . . . . .1 pm

GGambia (The) . . . . . . . . . . . . . 12 noonGermany . . . . . . . . . . . . . . . . . . .1 pmGhana . . . . . . . . . . . . . . . . . . 12 noonGreece . . . . . . . . . . . . . . . . . . . .2 pmGrenada . . . . . . . . . . . . . . . . . . .8 amGuatemala . . . . . . . . . . . . . . . . . .6 am

Guernsey . . . . . . . . . . . . . . . . 12 noonGuyana . . . . . . . . . . . . . . . . . . . .7 am

HHong Kong . . . . . . . . . . . . . . . . .8 pmHungary . . . . . . . . . . . . . . . . . . .1 pm

IIndia . . . . . . . . . . . . . . . . . . . 5.30 pmIndonesia. . . . . . . . . . . . . . . . . . .7 pmIreland . . . . . . . . . . . . . . . . . . 12 noonIsle of Man . . . . . . . . . . . . . . 12 noonIsrael . . . . . . . . . . . . . . . . . . . . . .2 pmItaly . . . . . . . . . . . . . . . . . . . . . .1 pm

JJamaica . . . . . . . . . . . . . . . . . . .7 amJapan . . . . . . . . . . . . . . . . . . . . .9 pmJordan . . . . . . . . . . . . . . . . . . . .2 pm

KKenya . . . . . . . . . . . . . . . . . . . . .3 pm

LLatvia . . . . . . . . . . . . . . . . . . . . .2 pmLebanon . . . . . . . . . . . . . . . . . . .2 pmLuxembourg . . . . . . . . . . . . . . . .1 pm

MMalaysia . . . . . . . . . . . . . . . . . . .8 pmMalta . . . . . . . . . . . . . . . . . . . . .1 pmMexico . . . . . . . . . . . . . . . . . . . .6 amMorocco . . . . . . . . . . . . . . . . 12 noon

NNamibia. . . . . . . . . . . . . . . . . . . .2 pmNetherlands (The) . . . . . . . . . . . . .1 pmNew Zealand . . . . . . . . . . .12 midnightNigeria . . . . . . . . . . . . . . . . . . . .1 pmNorway . . . . . . . . . . . . . . . . . . . .1 pm

OOman . . . . . . . . . . . . . . . . . . . . .4 pm

PPanama. . . . . . . . . . . . . . . . . . . .7 amPapua New Guinea. . . . . . . . . . .10 pmPeru . . . . . . . . . . . . . . . . . . . . . .7 amPhilippines . . . . . . . . . . . . . . . . . .8 pmPoland. . . . . . . . . . . . . . . . . . . . .1 pmPortugal . . . . . . . . . . . . . . . . . . .1 pmQQatar. . . . . . . . . . . . . . . . . . . . . .8 am

RRomania . . . . . . . . . . . . . . . . . . .2 pm

international time Zones

AT 12 NOON, GREENwICH MEAN TIME, THE STANDARD TIME ELSEwHERE IS:

PKF Worldwide Tax Guide 2013 VII

Tim

e Zo

nes

Russia - Moscow . . . . . . . . . . . . . . .3 pm St Petersburg . . . . . . . . . . . .3 pm

SSingapore . . . . . . . . . . . . . . . . . .7 pmSlovak Republic . . . . . . . . . . . . . .1 pmSlovenia . . . . . . . . . . . . . . . . . . .1 pmSouth Africa . . . . . . . . . . . . . . . . .2 pmSpain . . . . . . . . . . . . . . . . . . . . .1 pmSweden . . . . . . . . . . . . . . . . . . . .1 pmSwitzerland . . . . . . . . . . . . . . . . .1 pm

TTaiwan . . . . . . . . . . . . . . . . . . . .8 pmThailand . . . . . . . . . . . . . . . . . . .8 pmTunisia . . . . . . . . . . . . . . . . . 12 noonTurkey . . . . . . . . . . . . . . . . . . . . .2 pmTurks and Caicos Islands . . . . . . .7 am

UUganda . . . . . . . . . . . . . . . . . . . .3 pmUkraine . . . . . . . . . . . . . . . . . . . .2 pmUnited Arab Emirates . . . . . . . . . .4 pmUnited Kingdom . . . . . . .(GMT) 12 noonUnited States of America - New York City . . . . . . . . . . . .7 am Washington, D.C. . . . . . . . . .7 am Chicago . . . . . . . . . . . . . . . .6 am Houston . . . . . . . . . . . . . . . .6 am Denver . . . . . . . . . . . . . . . .5 am Los Angeles . . . . . . . . . . . . .4 am San Francisco . . . . . . . . . . .4 amUruguay . . . . . . . . . . . . . . . . . . .9 am

VVenezuela . . . . . . . . . . . . . . . . . .8 am

ZZimbabwe . . . . . . . . . . . . . . . . . .2 pm

PKF Worldwide Tax Guide 2013 1

slovenia

Currency: Euro Dial Code To: 386 Dial Code Out: 00 (EUR)

Member Firm:City: Name: Contact Information:Ljubljana Primoz Pecnik 1 230 85 10 (Managing Director, Partner) [email protected]

Tomaz Lajnscek [email protected] (Verified Tax Expert)

a. taXes payable

FEDERAL TAxES AND LEVIESCOMPANy TAxA company is resident in Slovenia if it has its legal seat or place of effective management in Slovenia. Resident companies are taxed on their worldwide income. Non-resident companies are taxed on their Slovenian source income. Corporate income tax is levied on the taxable profits of private companies at a rate of 18 % for year 2012 with a special rate of 0% for investment funds, pension funds, insurance undertakings for pension plans (under certain conditions) and venture capital companies which were set up under the Venture Capital Companies Act and which prepare a separate tax statement for that part of their activity.

The Corporate income tax rate will be reduced to 17% in 2013, 16% in 2014 and 15% for 2015 onwards.

BRANCH PROFIT TAxNon-resident companies are subject to corporate income tax in Slovenia on business activities carried on through a permanent establishment in Slovenia.

SALES TAx/VALUE ADDED TAx (VAT)GENERALAll companies pay VAT except those carrying out certain defined activities, small businesses and farmers with a turnover and income below defined thresholds, and those dealing with products intended for export and international transport.

VAT is payable on all supplies of goods and services effected by a taxable person acting as such for consideration within the territory of Slovenia, on intra-Community acquisition, including intra-Community acquisition of new means of transport, and on importation of goods. It is also imposed on the transfer of ownership of buildings or parts thereof if the transfer is made before first occupancy or within a period of two years after first occupancy.

Slovenia adopted a value added tax system in July 1999. In May 2004, when Slovenia became a member of the European Union, all provisions concerning intra-Community trade were enacted. The Slovenian VAT Act was changed with effect from 1 January 2010. The purpose of those changes was to follow the development of European VAT regulations.

TAxABLE PERSONSA taxable person is any person who independently carries out in any location any economic activity, whatever the purpose or result of that activity. Taxable persons established abroad who perform taxable economic activity in Slovenia must also register with the Tax Administration.

A taxable person must apply for registration if the value of his supplies within the period of the last 12 months exceeds the threshold of EUR 25,000. There is a separate threshold for registration in the VAT system for agricultural activities exceeding EUR 7,500 in accordance with the cadastral income of agricultural and forestry land.

Small businesses (including farmers) may apply for voluntary registration which is valid for at least a five-year period.

RATESThere are two VAT rates applicable in Slovenia:(1) The standard rate of 20% applies to all supplies of goods and services not

specified as being subject to the reduced rate or to exemptions.

Slovenia

PKF Worldwide Tax Guide 20132

(2) The reduced rate of 8.5% applies to goods and services specifically defined by the VAT Act. These include food, medicines, the supply of medical appliances for the personal use of disabled persons, supply of water, supply of books and other printed materials, tickets to cultural and sports events and the construction, renovation and supply of residential property unless it is built or supplied as part of social policy.

ExERCISING OF VAT DEDUCTION FOR UNPAID INVOICES Except in certain circumstances, a person registered for VAT purposes in Slovenia who fails to pay a supplier’s invoice on time and has already claimed a deduction for VAT purposes, will have this clawed back to the extent that the invoice remains unpaid. Any such person who has not claimed a VAT deduction by the due date, will not be entitled to claim a deduction in current or subsequent tax periods.

The tax refund must take place within 21 days of the day the taxpayer filed a tax balance to the tax authorities.

THE PLACE OF SUPPLy OF SERVICESThere are different rules depending on the place of the provision and type of service. From 1 January 2010, business-to-business (B2B) supplies of services are taxed where the buyer is situated, rather than where the seller is located. For business-to-consumer (B2C) supplies of services, the place of taxation is where the seller is established.

However, in certain circumstances, the place of supply is the place of consumption. These exceptions include services such as:intermediary services; services connected with immovable property; transport services; cultural, artistic, sporting, scientific, educational, entertainment or similar services, ancillary transport services, valuations of movable tangible property or work on such property; restaurant and catering services; the hiring of means of transport, and electronic services supplied to consumers.

For services provided in the fields of culture, art, sports, science, education, entertainment, fairs, exhibitions to businesses, the place of consumption is the headquarters of the purchaser.

FOREIGN TAxABLE PERSONS VAT REFUNDForeign taxable persons are entitled to a refund of VAT paid in the Republic of Slovenia on supplies of goods and services and upon importation of goods if the conditions defined by law are fulfilled. The claim for a refund of VAT must be filed electronically in the claimant’s own territory.

To obtain a refund of VAT in Slovenia, the taxable person, if established in another Member State, must address an electronic refund application to Slovenia and submit it to the Member State in which he is established via the electronic portal set up by that Member State.

Minimum refund limits are as follows: • EUR400ortheequivalentinnationalcurrencyiftherefundperiodisbetween

three months and less than a calendar year • EUR50ortheequivalentinnationalcurrencyiftherefundperiodisofa

calendar year or the remainder of a calendar year.

VAT refunds due to taxable persons established outside the EU are only granted according to the conditions of reciprocity. Refund applications must be submitted by 30 June of the calendar year following the refund period to the competent tax authority.

SPECIAL SCHEMESSPECIAL SCHEME FOR SMALL TAxABLE PERSONSSmall enterprises whose turnover does not exceed EUR 25,000 are exempt from charging VAT and have consequently no right to recover input VAT.

SPECIAL SCHEME FOR FARMERSFarmers are exempt from charging VAT if their farming income does not exceed EUR 7,500. They are not able to recover VAT incurred on their purchases but they are allowed to charge VAT at a flat rate at 8% on supplies to taxable persons and retain it.

SPECIAL CASH ACCOUNTING SCHEMESmall businesses with a taxable turnover of up to EUR 400,000 per year, exclusive of VAT, may opt for the cash accounting scheme under which a taxable person may account for VAT on the basis of cash paid and received. Certain transactions are excluded from the scheme eg exports, imports, intra-Community supplies, intra-Community acquisitions, etc).

Slovenia

PKF Worldwide Tax Guide 2013 3

FINANCIAL SERVICES TAxThe Financial Services Tax Act was published in the Official Journal of the Republic of Slovenia, No. 94/12 on 10 December 2012. It entered into force on the fifteenth day following its publication in the Official Journal.

The new Financial Services Tax Act introduces a liability to pay tax VAT exempt financial services such as: a) grant and negotiation of credits or loans in the form of money and the management of

credits or loans in the form of money by the person granting them b) negotiation of or any dealings in credit guarantees or any other security for money and

the management of credit guarantees by the person who is granting the credit c) transactions, including negotiation, involving deposit and current accounts, payments,

transfers, debts, cheques and other payment instruments d) transactions, including negotiation, involving currency, bank notes and coins used as

legal tender; e) services provided by insurance brokers and insurance agents.

Transactions in shares, interests in companies or associations, debentures and other securities and management of investment funds are not subject to the financial services tax, even though these services are exempt from VAT.

Any person performing financial services in the territory of the Republic of Slovenia is subject to the financial services tax. A financial services tax return must be filed by anyone subject to the tax. It is a transaction tax and is charged at the moment when the financial service is performed. A financial service is considered to have been performed when a fee (commission) has been paid for this service.

The tax rate is 6.5% of the tax base.

FRINGE BENEFITS TAxIn principle, all fringe benefits given by employers or other persons to their employees or family members of employees in connection with employment, such as the private use of company cars, rental benefits, zero-interest loans, discounts on products and services, gifts and share options, are taxed.

LOCAL TAxESThere are no special regional or local taxes in Slovenia.

OTHER TAxESOther taxes not covered above are:• personalincometax• derivativeinstrumentsgainstax• contractualworktax• contributionstosocialsecurityinsurance• taxesonlotterywinnings• taxongambling• inheritanceandgifttax• propertytax• taxonvessels• circulationtax• taxoninsuranceservices• immovablepropertytransfertax• customsdutiesandexciseduties.

b. determination of taXable income

DEPRECIATIONDepreciation costs are allowed in Slovenia. Rates applicable to the main types of assets are:

Building projects, including investment property 3%

Parts of building projects, including parts of investment property 6%

Equipment, vehicles and machinery 20%

Parts of equipment and equipment for research 33.3%

Computers and computer equipment 50%

Long-term plantations 10%

Breeding and working herds 20%

Other investments 10%

Slovenia

PKF Worldwide Tax Guide 20134

STOCK/INVENTORy AND RECEIVABLESIf the cost of stock/inventories exceeds the net realisable value, the effect of write-offs is tax deductible.

The write-off of a receivable is recognised as an expense when recorded in the business accounts. However, the amount written off must not exceed the lower of the following two amounts: the arithmetical average of the actual write-off of the last three years or the amount representing 1% of taxable revenues in the tax period.

CAPITAL GAINS AND LOSSESCapital gains from regular income are subject to tax. Capital gains are included within the profits chargeable to corporation tax for an accounting period. Capital losses can be set against income of an accounting period when they are realised.

50% of capital gains derived on the disposal of shares are exempt where:• thesharesrepresentatleastan8%participationincapitalorvotingrightsof

the company• theshareshavebeenheldforatleastsixmonths• thecompanyhasatleastoneemployee• theparticipationisnotinacompanyinalowtaxjurisdiction(wherethenominal

tax rate is less than 12.5%).

DIVIDENDSCompanies paying dividends withhold tax at a rate of 15% on each dividend distributed to residents and non-residents of Slovenia. If international treaties on the avoidance of double taxation stipulate a tax rate lower than 15%, the tax rate from the treaty applies. No withholding tax applies where a resident taxpayer notifies the payer of its tax number or if a non-resident taxpayer with activities in a business unit in Slovenia notifies the payer of its tax number. No tax is withheld from payments of dividends and similar income distributed to companies resident in the EU with at least 10% equity stake which has been held for at least 24 months prior to the dividend payment..

There is no withholding tax on dividends paid to a non-resident who is a resident of the EU or EEA (excluding the Principality of Liechtenstein) if the recipient of the dividend is not able to set off the applicable Slovenian withholding tax in his/her country of residence. Similar applies to payments of dividends and interest paid from Slovenia to EU and EEA (excluding the Principality of Liechtenstein) investment and pension funds.

Companies are, in most cases, exempt from tax on dividends if the payer is:• liabletopaytaxbytheCorporateIncomeTaxAct;or• ataxpayingresidentinanEUMemberStateunderthatState’sdomestictaxlaw,

is not deemed to be resident outside the EU under a tax treaty concluded with a non-member state; or

• liabletopaytheequivalentofSloveniancorporateincometaxandisresidentinacountry in which the rate of tax on corporate profits is at least 12.5%.

INTEREST DEDUCTIONSInterest paid on borrowed money is treated as a regular financial expense and can be set against income arising in the same accounting period. Thin capitalisation rules apply to loan finance received from shareholders who have at least a 25% participation in the company unless the taxpayer can demonstrate that the loan finance would have been provided on the same terms by a non-related entity. These rules prescribe a maximum debt to equity ratio of 6:1 in 2008 to 2010, 5:1 in 2011, and 4:1 from 2012.

LOSSESLosses are calculated as the surplus of expenses over revenues defined by the Corporate Income Tax Act. Losses may be offset against taxable profits in the following years. Losses may be carried forward undefined but the carry back of losses is not permitted.

The tax base may be decreased by the amount of loss from previous tax periods up to a maximum of half the tax base (before1 January 2013, 100% of the tax base) and may be carried forward indefinitely (unless more than 50% ownership of the capital has changed in the meantime).

FOREIGN SOURCE INCOMESlovenia has no special rules that apply to foreign source income. All legal persons carrying out commercial activities and having their head offices in Slovenia or having their place of effective management in Slovenia (partnerships and other corporate forms, investment funds, banks, insurance companies, co-operative enterprises, public enterprises and other legal persons) are subject to corporate income tax. Non-residents (legal persons who do not have their headquarters in Slovenia or their place of effective management in Slovenia) are subject to corporate income tax to the extent that their income has its source in Slovenia.

Slovenia

PKF Worldwide Tax Guide 2013 5

INCENTIVESA 100% deduction is available for research and development (R&D) investment activities and the purchase of R&D services not exceeding the amount of the taxable base. There is also a 40% deduction for amounts invested in equipment and intangibles, again only up to the amount of the taxable base. There are also further general tax incentives under certain conditions for entities that provide work for employees, trainees or disabled persons, as well as relief for donations and voluntary supplementary pension insurance.

A tax relief of 45% of eligible salary payments (subject to a maximum of the employer’s tax base) is granted to a taxpayer who employs a person under the age of 26 or a person above the age of 55 who has been registered as unemployed with the Employment Service of the Republic of Slovenia for at least six months and has not been employed with this taxpayer or his/her associated enterprise for the last 24 months.

There are further general tax incentives available to entities that provide work for apprentices or disabled persons. A taxpayer who employs disabled persons under the Act regulating the vocational rehabilitation and employment of disabled persons may claim a tax deduction equal to 50% of the salaries of such persons but not exceeding the amount of the taxable base.

A taxpayer who employs disabled persons with a 100 % physical or hearing disability may claim a reduction in the taxable base in the amount of 70% of the salaries of such persons but not exceeding the amount of the taxable base. A taxpayer who employs disabled persons above the prescribed quota, their disability not being the consequence of a workplace injury or occupational disease at the same employer, may claim a reduction in the taxable base in the amount of 70% of the salaries of such persons but not exceeding the amount of the taxable base.

If a taxpayer under a teaching agreement employs an apprentice or student to perform practical work in professional education, the taxpayer may claim a reduction in the taxable base in the amount of the salary paid but not exceeding 20% of the average monthly salary in Slovenia for each month of performing practical work and for each individual person who takes part in such professional education.

A taxpayer may claim a reduction in the taxable base for amounts paid in cash and in kind for humanitarian, disabled, charitable, scientific, educational, medical, sports, cultural, ecological and religious purposes. A reduction may also be claimed for payments made to residents of Slovenia or residents of Member States of the EU or EEA (excluding the Principality of Liechtenstein) who are established under special regulations for the performance of such activities and up to an amount equivalent to 0.3% of the taxpayer’s taxable revenue in the current tax period.

A taxpayer may also claim a reduction in the taxable base for amounts paid in cash and in kind to political parties up to an amount equivalent to three times the average monthly salary per employee of the taxpayer in the current tax period. The cumulative amount of relief granted may not exceed the amount of the taxable base. An additional reduction of 0.2% of the taxpayer’s taxable revenue is granted for amounts paid in cash and in kind for cultural purposes and voluntary societies incorporated for protection from natural and other disasters who work in the public interest and are residents of Slovenia or residents of Member States of the EU or EEA (excluding the Principality of Liechtenstein) and are established under special regulations for the performance of such activities.

Relief is available for voluntary supplementary pension insurance up to 24% of the compulsory contributions for pension and disability insurance for an insured employee but no more than EUR 2,683.26 annually per employee may apply under certain conditions.

Additional tax incentives for eligible costs for initial investments and employment costs are given to companies which operate in an economic zone (for details see in the section on economic zones).

c. foreiGn taX relief

Relief for double taxation is provided by means of credit for overseas tax suffered on overseas income. The credit is the lower of the foreign tax paid and the Slovenian tax on the income concerned.

d. corporate Groups

Groups cannot be taxed as a single entity in Slovenia.

Slovenia

PKF Worldwide Tax Guide 20136

e. related party transactions

Transactions of Slovenian resident companies with non-resident companies must be carried out on an arm’s length basis or adjustments are required for tax purposes. The rules also apply to transactions between Slovenian resident companies with which they are related where one is in a tax-advantageous position (e.g. through losses brought forward from an earlier period). Companies are related by virtue of a 25% participation of one in the other or a common 25% participation by a third company.

f. witHHoldinG taX

A company paying dividends withholds tax at a rate of 15% on each distributed dividend to residents and non-residents of Slovenia but this may be reduced under the terms of a relevant double taxation treaty. No withholding tax is payable on dividends distributed to persons where a common system of taxation applies (broadly where the payee has at least 10% equity in the payor, with shares having been held for at least 24 months prior to the payment) or where the recipient is resident in another EU or EEA member state (provided that the withholding tax cannot be credited in the recipient’s residence state).

There is no withholding tax on dividends paid to a non-resident who is a resident of the EU or EEA (excluding the Principality of Liechtenstein) if the recipient of the dividend is not able to set off the applicable Slovenian withholding tax in his/her country of residence. A similar principle applies to payments of dividends and interest paid from Slovenia to EU and EEA (excluding the Principality of Liechtenstein) investment and pension funds.

Withholding tax is charged in respect of payments to resident and non-resident persons by a resident of the Republic of Slovenia. This applies to dividends and similar incomes, except for dividends and similar incomes distributed through a business unit of non-residents located in the Republic of Slovenia including:• interest(withsomeexceptionssuchasinterestonloanstakenoutbythe

Republic of Slovenia or any interest paid by a bank to a non-resident, except inter-bank interest)

• paymentsforusingorfortherighttousecopyrights,patents,licences,trademarks and other owners’ rights and other similar incomes

• paymentsforrealestateleases• paymentsfortheservicesofcontractorsandathletesifthesepaymentsbelong

to another person (for example a society where they perform the service)• paymentsforservicestonon-EUresidentcompaniessufferingtaxatarateless

than 12.5%.

Withholding tax is not required on payments to:• theRepublicofSlovenia,aself-governinglocalunitinSloveniaortheBankof

Slovenia• ataxablepersonwhohasinformedtheincomepayeroftheirtaxnumber• anon-residenttaxablepersonwhoisobligedtopaytheincometaxwhichthey

generate through activities in a business unit or via a business unit in the Republic of Slovenia and who has informed the income payer of their tax number.

The domestic tax rate is 15% in all cases. Double tax treaties may apply which reduce the rate applicable.

G. eXcHanGe controls

There are no exchange controls in Slovenia.

H. personal taX

PERSONAL INCOME TAxPersonal income tax is levied on six categories of income:• incomefromemployment• businessincome• incomefrombasicagricultureandforestry• incomefromrentsandroyalties• incomefromcapital• otherincomeaccruingtopersonsliabletotaxintheRepublicofSlovenia.

Residents are liable to income tax on their worldwide income (i.e. income derived in Slovenia as well as abroad). Non-residents are liable to income tax on income derived in Slovenia.

Slovenia

PKF Worldwide Tax Guide 2013 7

An individual, regardless of his nationality, is a resident in Slovenia for personal income tax purposes if he has a formal residential tie with Slovenia (i.e. has permanent residence in Slovenia, is a Slovenian public employee employed abroad or was a Slovenian resident but is currently employed in an EU institution). A person who is present for more than 183 days in a taxable year in Slovenia is deemed to be resident there in that tax year.

Each individual is treated as a separate taxpayer. There is no taxation of spouses or a family as a whole. The tax year is the calendar year.

Tax on income from capital (on interest, dividends and capital gains) is paid according to a flat income tax rate. Any such tax payment is treated as a final tax for residents and non-residents alike. Tax rates are the following:• interest:25%(20%before1January2013)• dividends:25%(20%before1January2013)• capitalgains:25%(20%before1January2013)foraholdingperiodofuptofive

years, 15% for a holding period from five to 10 years, 10% for a holding period from 10 to 15 years, 5% for a holding period from 15 to 20 years, and 0% for a holding period greater than 20 years.

Income tax on other categories of income (income from employment, business income, income from basic agriculture and forestry, rental income, royalties and other income hereinafter referred to as active income) is paid during the tax year in the form of advance tax payments. The rate for advance tax payment is prescribed by the Personal Income Tax Act. Any such advance tax payment of a non-resident is treated as a final tax while, in the case of a resident, it is treated as a prepayment of tax. The tax schedule for the year 2011 is as follows:

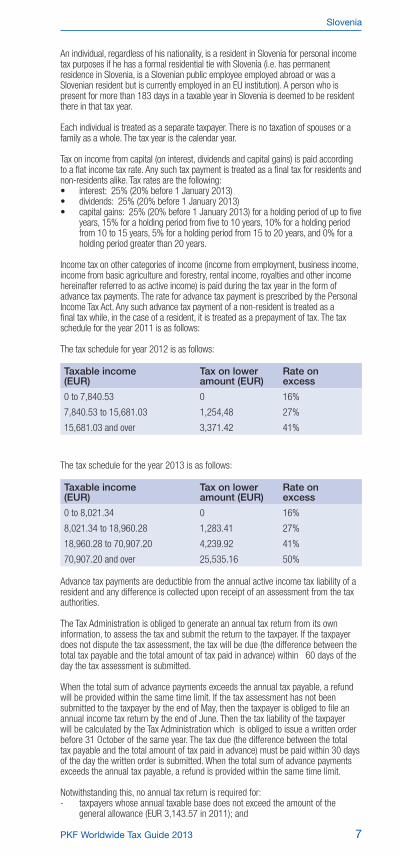

The tax schedule for year 2012 is as follows:

Taxable income (EUR)

Tax on lower amount (EUR)

Rate on excess

0 to 7,840.53 0 16%

7,840.53 to 15,681.03 1,254,48 27%

15,681.03 and over 3,371.42 41%

The tax schedule for the year 2013 is as follows:

Taxable income (EUR)

Tax on lower amount (EUR)

Rate on excess

0 to 8,021.34 0 16%

8,021.34 to 18,960.28 1,283.41 27%

18,960.28 to 70,907.20 4,239.92 41%

70,907.20 and over 25,535.16 50%

Advance tax payments are deductible from the annual active income tax liability of a resident and any difference is collected upon receipt of an assessment from the tax authorities.

The Tax Administration is obliged to generate an annual tax return from its own information, to assess the tax and submit the return to the taxpayer. If the taxpayer does not dispute the tax assessment, the tax will be due (the difference between the total tax payable and the total amount of tax paid in advance) within 60 days of the day the tax assessment is submitted.

When the total sum of advance payments exceeds the annual tax payable, a refund will be provided within the same time limit. If the tax assessment has not been submitted to the taxpayer by the end of May, then the taxpayer is obliged to file an annual income tax return by the end of June. Then the tax liability of the taxpayer will be calculated by the Tax Administration which is obliged to issue a written order before 31 October of the same year. The tax due (the difference between the total tax payable and the total amount of tax paid in advance) must be paid within 30 days of the day the written order is submitted. When the total sum of advance payments exceeds the annual tax payable, a refund is provided within the same time limit.

Notwithstanding this, no annual tax return is required for: - taxpayers whose annual taxable base does not exceed the amount of the

general allowance (EUR 3,143.57 in 2011); and

Slovenia

PKF Worldwide Tax Guide 20138

- taxpayers whose only income is a pension and who have not paid an advance tax during the taxable year and have not claimed an allowance for dependent family members, and whose additional income does not exceed EUR 80.

These taxpayers may opt, whether to file a tax return or not.

Taxpayers who are liable to tax on business income are obliged to submit their income tax declarations on business income to the local Tax Administration office by 31 March of the following year.

All taxpayers (except for basic agricultural and forestry activity) must keep records of their income.

They are obliged to keep records for at least five years from the year to which they relate.

To avoid double taxation of income, Slovenia has concluded a considerable number of double taxation conventions.

ExEMPTIONSThere are a number of exemptions within each category of income which are defined by the Personal Income Tax Act.

ALLOwANCES AND DEDUCTIONSAllowances for 2013

General allowance: - EUR 6,519.82 for residents with active income up to EUR 10,866.37 - EUR 4,418.64 for residents with active income between EUR 10,866.37 and

EUR 12,570.89 - EUR 3,302.70 for residents with active income more than EUR 12,570.89.

Personal allowances: - Disabled person’s allowance: EUR 17,658.84 if the resident is a disabled

person - Seniority allowance: EUR 1,421.35 for a resident older than 65 years of age - Independent artists, journalists and sportsmen: a special deduction of 15% of

their revenues (up to EUR 25,000.00 of revenues) - Student allowance: EUR 2,477.03 for income earned by pupils or students for

temporary work done on the basis of a referral issued by a special organisation dealing with job-matching services for pupils and students.

Family allowances: granted to residents who are supporting their family members, as follows: - EUR 2,436.92 for the first dependent child; for each subsequent dependent

child this amount is increased - EUR 8,830.00 for a dependent child who requires special care - EUR 2,436.92 for any other dependent family member.

Special deduction for voluntary additional pension insurance payments: - premiums paid by a resident to the provider of a pension plan based in Slovenia

or in an EU Member State according to a pension plan that is approved and entered into a special register but limited to a sum equal to 24% of the compulsory contribution for compulsory pension and disability insurance for the taxpayer, or 5.844% of the taxpayer’s pension, and no more than EUR 2,819.62 annually.

Pensioners and working disabled persons are entitled to a tax credit in the amount of 13.5% of the pension/compensation received from compulsory pension and disability insurance.

Self-employed persons may claim additional allowances: - for investment - for investment in research and development - for employing disabled persons - for donations.

DIRECT TAxES ON PROPERTyINHERITANCE AND GIFT TAxInheritance and gift tax applies to transfers of property. The tax is paid by individuals or legal persons of private law receiving property in the form of inheritance or gifts.

Taxpayers are divided into four categories according to their relationship with the

Slovenia

PKF Worldwide Tax Guide 2013 9

deceased or donor as follows:• ClassI:alldirectdescendantsandspouses• ClassII:parents,siblingsandtheirdescendants• ClassIII:grandparents• ClassIV:others.

The tax base of inherited or given property is the value after deduction of debts and other liabilities.

For real estate, this value is set at 80% of gross appraisal value. For movable property except money this value is set as market value.

Exemptions to the inheritance and gift tax include: • individualsclassifiedunderClassI• taxpayerswhoinheritahouseorapartmentandwhoownonlyonehouseor

apartment themselves and have lived in the same house as the decedent• farmerswhoinheritagriculturallandoranentirefarm• andlegalpersonsofprivatelaw,establishedforreligious,humanitarian,

educational, cultural, charitable and certain other activities.

Movable property up to a value of EUR 5,000 is also exempt from taxation.

The tax is levied progressively depending on the value of the property and the category under which the relation to the deceased or donor is classified. Inheritance and gift tax rates are as follows:

Tax rate ranges

Class II 5% to 14%

Class III 8% to 17%

Class IV 12% to 39%

Taxpayers must declare their liability to the local tax authority within 15 days of receiving a gift. The assessment of inheritance tax is made according to the inheritance decision sent by the court to the tax authority. The tax is payable within 30 days of the assessment being issued.

PROPERTy TAxCHARGE FOR THE USE OF BUILDING LANDA charge is levied on vacant land (but on which building is planned) and land on which buildings have already been constructed, held by legal persons and individuals. The charge is set by local communities. For vacant land, this is based on the area of thebuilding planned to be built. For ‘occupied’ land it is based on the useful area of the residential house or business premises thereon.

Exemptions are available for land and buildings used by the Army, churches, embassies and international organisations, for temporary or new buildings or apartments for five years, partial or full exemption for people with low incomes, building land planned for public infrastructure (health, social security, schools, culture, science, sport and public administration, etc.) and developed building land under public infrastructure.

The tax authority assesses the charge by 31 March for the present year. Tax is paid in instalments for the year in advance.

REAL PROPERTy TAx Real property tax is levied on premises such as buildings and parts of buildings, including apartments, garages and secondary homes. The taxpayer is the individual who is the actual or beneficial owner of the premises.

The taxable base for premises is the value ascertained according to special criteria issued by the government and local communities.

The tax rate for premises depends of the type of property and its value. The tax rate for dwellings varies from 0.10% to 1% of the value. The tax rates on premises used for rest and recreation are in the range of 0.20% to 1.50%. The tax rate for business premises varies from 0.15% to 1.25%. For business premises that are not used for attendant activities or are not rented, the tax rate is increased by 50%.

Exemptions to the real property tax include: - buildings of less than 160 square metres- buildings used for agricultural purposes

Slovenia

PKF Worldwide Tax Guide 201310

- business premises used by the owner or user for business activity - cultural or historical monuments.

In addition, there is a temporary exemption for 10 years to taxpayers who own a newly constructed building or repaired or renovated buildings, if the value of these buildings has increased by more than 50% as a result of renovation .

Wheremore than three family members live in the owner’s house, the tax decreases by 10% for the fourth and every additional family member.

The tax is assessed by the tax authorities by 31 March for the present year. Tax is paid in instalments for the year in advance. Tax is payable within 45 days of the assessment being issued.

i. treaty and non-treaty witHHoldinG taX rates

List of double taxation conventions currently in force at 1 January 2013

Dividends (%)

Interest (%)

Royalties (%)

Non-Treaty Countries: 15 15 15

Albania 10/5 7 7

Austria 15/5 5 5

Azerbaijan 8 8 5/10

Belarus 5 5 5

Belgium 15/5 10 5

Bosnia-Herzegovina 10/5 7 5

Bulgaria 10/5 5 5/10

Canada 15/5 10 10

China 5 10 10

Croatia 5 5 5

Cyprus 5 5 5

Czech Republic 15/5 5 10

Denmark 15/5 5 5

Estonia 15/5 10 10

Finland 15/5 5 5

France 15/0 5 5

Germany 15/5 5 5

Greece 10 10 10

Hungary 15/5 5 5

Iceland 15/5 5 5

India 15/5 10 10

Ireland 15/5 5 5

Israel 5/10/15 5 5

Italy 5/15 10 5

Korea, Republic of 15/5 5 5

Latvia 15/5 10 10

Lithuania 15/5 10 10

Luxembourg 15/5 5 5

Macedonia 15/5 10 10

Malta 15/5 5 5

Moldova 10/5 5 5

Montenegro 10/5 10 5/10

The Netherlands 15/5 5 5

Norway 15/0 5 5

Slovenia

PKF Worldwide Tax Guide 2013 11

Dividends (%)

Interest (%)

Royalties (%)

Poland 15/5 10 10

Portugal 15/5 10 5

Qatar 5 5 5

Romania 5 5 5

Russia 10 10 10

Singapore 5 5 5

Serbia 10/5 10 5/10

Slovak Republic 15/5 10 10

Spain 15/5 5 5

Sweden 15/5 0 0

Switzerland 15/5 5 5

Thailand 10 10/15 10/15

Turkey 10 10 10

Ukraine 5/15 5 5/10

United Kingdom 15/0 5 5

United States 15/5 5 5

New conventions have been ratified with Armenia, Kuwait and Egypt but are not yet effective.

Slovenia

www.pkf.com