sipho nkosi chief executive officer exxaro resources limited merrill lynch global metals and mining...

TRANSCRIPT

Sipho Nkosi

Chief Executive Officer

Exxaro Resources Limited

Merrill Lynch Global Metals and Mining ConferenceMiami, USA11 - 13 May 2010

1

2

Content• Who is Exxaro?

• Exxaro’s strategy

• RSA environment

- What is happening in RSA since recession?

- What challenges does RSA economy face?

- What challenges does RSA mining industry face?

• Exxaro response

• Country response

• Conclusion

3Introduction to Exxaro

COALthe fourth largest coal producer in South Africa. Largest supplier to Eskom MINERAL SANDSone of the world's top three producers of zircon and chlorinatable TiO2 slag

BASE METALS AND INDUSTRIAL MINERALSthe only zinc producer in South Africa

IRON ORE20% holding in Sishen Iron Ore Company

Our commodities At a glance…

One of South Africa’s diversified resources company

One of the top 40 companies on the JSE

Approximately 11 000 employees

Head office in Pretoria, South Africa

Market capitalisation ~R45bn

Revenue: R15,0bn*

Net operating profit: R1,74bn*

Dividend: 200cps* * for year-ended 31 December 2009

4Powering possibility through our strategyExxaro wants to:

• Be a South African diversified resources company with global assets

• Be a long-term sustainable business

• Produce 75Mtpa coal and 750kt reductants by 2015

• Diversify into sought-after commodities (iron ore and energy)

• Operate successfully in any environment

• Create strategic alliances with key local and international partners

• Bring to fruition its exciting pipeline of growth projects

5Project pipeline and opportunities

Ownership Scope Estimated capex

Status Estimated start-up

Sands Kwinana expansion (Australia 100%)(Approval Feb 2008)

40ktpa AUD117m Construction 2Q10

Coal Medupi(Approval May 2006) 14,6Mtpa R9bn Detail

engineering 2Q12

Sands Dry mine replacement (Australia 100%) 100-200ktpa TBD Pre-feasibility 2011

Coal Belfast 3-5Mtpa TBD Pre-feasibility 2011

Energy Co-generation 20MW TBD Feasibility 2012

Coal Char phase 2 140ktpa TBD Feasibility 2013

Energy Wind energy 100MW TBD Pre-feasibility 2013

Coal Moranbah South (Australia 50%) 4,5Mtpa TBD Concept 2014

Energy Solar plant 20MW TBD Pre-feasibility 2014

Coal Market coke 750ktpa TBD Pre-feasibility 2014

Coal Thabametsi 17Mtpa TBD Pre-feasibility 2015

6What happened in RSA since recession?

• SA economy exited recession during 3Q09 with 3,2% real GDP growth

recorded in 4Q09

• CPI inflation under control and mostly within target range

• Reserve Bank cut rates to 6,5% from 7,0%

• Strong currency weighed heavily on corporate earnings

however

• Foreigners continue to be strong buyers of SA equity (US$8,9bn)

• Resources led the rally on JSE on continuing signs of a global recovery

and strong demand for some commodities

• RSA Government continues to invest aggressively into infrastructure

(electricity, rail, roads, SWC stadiums etc)

7What challenges face SA economy?

• Despite significant progress made in getting the economy back on to a higher

growth path (3,3% 1994 to 2009), the country faces major unemployment and

poverty challenges

• SA’s labour participation rate at 42% is low vs peers, its unemployment rate is

high (>20%), its levels of income inequality are very high (Gini coefficient 0,59)

and too many people are caught in the poverty trap

• Government has now placed the creation of meaningful employment as a

central pillar of economic policy

• All parties recognise that higher levels of sustainable, balanced and labour

absorbing economic growth is key to reducing unemployment and poverty.

8Too much of the economy’s recent growth has been driven by credit fuelled non-tradable demand side, and tradable export sectors have languished…..

9To ensure more balanced and higher levels of growth the country needs its tradable export sectors to grow at a faster pace

• This is where mining fits in

• Mining has a very large foreign exchange earning, GDP multiplier and

employment creation foot print

• But questions need to be asked and answered as to what role mining can play in

the future:

- Does South Africa have the environment to support a growing mining industry?

- What role can mining play in the economy?

- What are the factors affecting the competitiveness (and growth) of the mining sector and can we fix them?

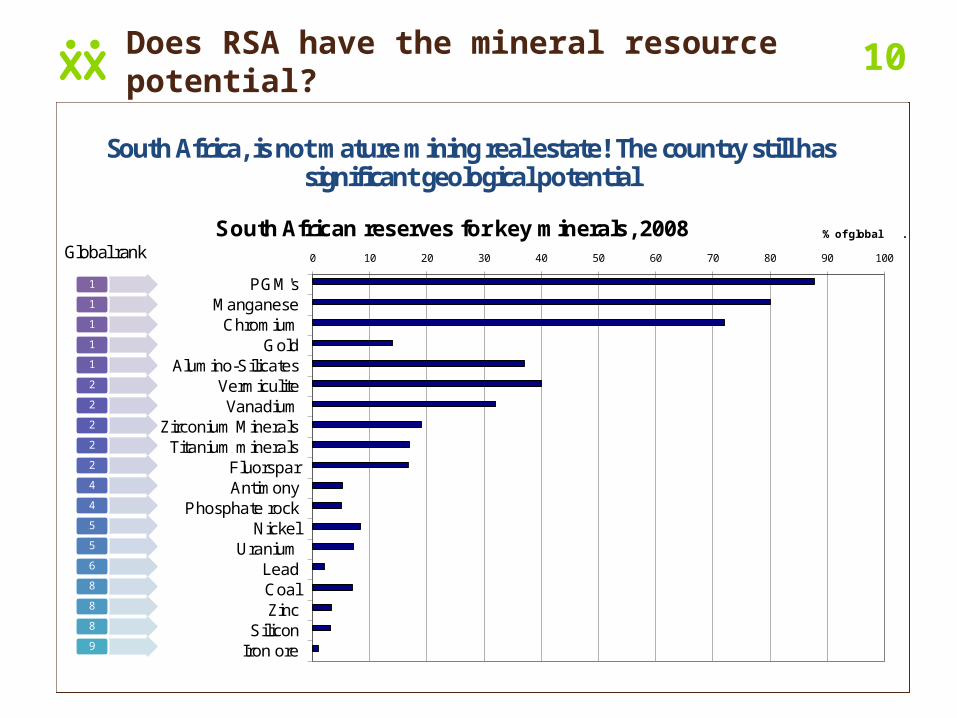

10Does RSA have the mineral resource potential?

0 10 20 30 40 50 60 70 80 90 100

PGM'sManganese

ChromiumGold

Alumino-SilicatesVermiculiteVanadium

Zirconium MineralsTitanium minerals

FluorsparAntimony

Phosphate rockNickel

UraniumLeadCoalZinc

SiliconIron ore

% of global .South African reserves for key minerals, 2008

1

1

1

1

1

2

2

2

2

2

4

4

5

5

6

8

8

8

9

South Africa, is not mature mining real estate! The country still has significant geological potential

Global rank

11What role can mining play in the economy?

Mining industry the essential core of SA economy

• Creates 1 million jobs (500 000 direct and 500 000 indirect)

• Accounts for about 18% of GDP (8% direct, 10% indirect and induced)

• Critical earner of foreign exchange >50%

• Accounts for 18% of investment (9% direct)

• Attracts significant foreign savings (>30% of value of JSE)

• 18,5% of corporate tax receipts (2007 - R22 billion, 2008 - R33 billion)

• 50% of volume of Transnet’s rail and ports

• 93% of electricity generation via coal power plants

• 15% of electricity demand

• About 37% of country’s liquid fuels via coal (R30 billion worth)

12What challenges does SA mining industry face?

• Mine closures for safety related issues (some valid, some not)

• Binding infrastructure constraints (electricity, rail)

• Red tape constraints (e.g. water licenses)

• Policy uncertainty

• Human capital constraints

• Stagnant productivity and rapidly escalating costs

• Volatility in rand-dollar exchange rate, and then

• The global crisis hit!

but …

Mining production declined in period 2006 to 2008, despite significant increase in

investment in that period. Challenges included:

The lack of growth in the mining sector is also due to a combination of drivers

eroding the sector’s competitiveness

13Can we fix the problems?

Exxaro’s response to challenges and opportunities includes:

1. Safety ~ CEO safety summit and continuous awareness campaigns

2. Infrastructure

• Electricity ~ Co-generation and facilitating various renewable energy discussions

• Rail ~ Close co-operation with rail and port authorities

3. Red tape and policy uncertainties ~ Chamber of Mines and various

stakeholder forums where industry issues are discussed

4. Human capital constraints ~ Extensive bursary and learning programmes

5. Escalating costs ~ CI and BI culture

6. Rand/dollar exchange rate ~ Uncontrollable, hence position on cost curve NB

14Can the country fix these problems?• SA ranked reasonably well in ease of doing business

• Infrastructure – at a general level SA’s infrastructure is ranked as reasonable, but specific constraints have emerged (rail and electricity)

• Social license to operate (safety, health, environment, etc) important component of the industry’s long-term license to operate

• Sustainable mining into the 21st century a case for change, whereby the industry stakeholders need to work together in helping to improve on the social license to operate, including the continued improvement in technology to ensure a sustainable sector into the future

• Macro-economic stability – the issue of the volatility in the rand exchange rate has been raised (especially its impact on L/T planning)

• Political stability – SA is a stable constitutional democracy. Parties agree that transformation is a key component of promoting stability and long-term license to operate

Specific initiatives taken to address the above include…

15Stakeholder response to challenges

• Formation of MIGDETT competitiveness task team to jointly look at macro-economic issues that could have a material impact on the competitiveness of the mining industry

• General agreement by all role players that objectives of MPRDA of promoting a sustainable, safe, environmentally responsible, growing and transformed industry are NB and globally aligned

• Role of Chamber of Mines to ensure:– Issue of lack of clarity in the laws, and view that certain administrative

discretionary powers create uncertainty is raised

– The issue of time periods for processing and granting rights raised

– The issue of understanding the high refusal and rejection rates raised

• The promotion of exploration and small scale mining

• Developing trust amongst players

16

• The country and Exxaro face numerous challenges and opportunities to unlock significant underlying potential. Do we believe we can do it?

• Exxaro can ~ It has the strategy and ability

• The country can ~ Willingness by all stakeholders to improve competitiveness and unlock potential

• Exxaro has a strong and rosy future

Conclusion

THANK YOU

www.exxaro.com