singapore competitiveness: a nation in transition files/20061128_singapore... · bangladesh...

TRANSCRIPT

Launch of the Asia Competitiveness Institute

Singapore Competitiveness:A Nation in Transition

This presentation draws on ideas from Professor Porter’s books and articles, in particular, “Building the Microeconomic Foundations of Prosperity,”in The Global Competitiveness Report 2006-07 (World Economic Forum, 2006); “Clusters and the New Competitive Agenda for Companies and Governments,” in On Competition (Harvard Business School Press, 1998); Clusters of Innovation Initiative (www.compete.org), a joint effort of the Council on Competitiveness, Monitor Group, and ongoing research. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means—electronic, mechanical, photocopying, recording, or otherwise—without the permission of the author

Additional information may be found at the website of the Institute for Strategy and Competitiveness, www.isc.hbs.edu

Prof. Michael E. PorterHarvard Business School

Singapore28 November 2006

2GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Trends in the Global Economy

• Globalization of markets

• Globalization of value chains

• Globalization of knowledge

• Innovation and skill an increasing share of value added

• Services an increasing share of value added

• Competitiveness depends on productivity

• The bar for competitiveness is rising

• Competitiveness in the global economy is a positive-sum game

3GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Singapore Competitiveness in Transition

• Singapore is one of the most impressive success stories of economic growth in the 20th century

• The country has successfully weathered a series of external shocksfrom the Asian crisis (1997-98) to the bursting of the IT bubble (2001) to SARS (2003)

• It is now on a challenging path to move from an economy based on efficiency to one based on differentiation and innovation

• The track record so far is encouraging, but much work lies ahead

• An enduring strength of Singapore is its willingness to questionwhether the current sources of its economic success are sustainable

4GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

0% 1% 2% 3% 4% 5% 6%

Prosperity PerformanceSelected Countries

Norway

Denmark

Poland

Germany

Real PPP-adjusted GDP per Capita, 2005

Growth of Real GDP per Capita (PPP-adjusted), CAGR, 2000-2005Source: EIU (2006), authors’ calculations

U.S.

S Korea

HungarySlovakia

Czech Rep.

JapanNL

Switzerland

Italy

Mexico

Spain

Turkey

Greece

IrelandBelgium,Austria

France

New Zealand

U.K., Sweden,Australia, Finland

China (8.8%, $6,290)

India

Iceland

Canada

Singapore

VietnamLaos

Thailand

Hong Kong

IndonesiaSri LankaPhilippines

Malaysia

Myanmar

5GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Innovation and Competitiveness

ProductivityProductivity

Innovative CapacityInnovative CapacityInnovative Capacity

Competitiveness

• Innovation is more than just scientific discovery

• There are no low-tech industries, only low-tech firms

ProsperityProsperityProsperity

6GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. PorterSource: Groningen Growth and Development Centre and The Conference Board, 2006.

Labor Productivity Level and GrowthSelected Countries

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

-1% 0% 1% 2% 3% 4% 5%

GDP per Employee, US-$, 2005

Growth of Real GDP Employee, CAGR, 2000 - 2005

France

UK

U.S.

BelgiumNetherlands

FinlandGermany

Italy

SpainCanada

Norway

Sweden

Australia,Denmark

Switzerland

Austria

GreeceIceland

Ireland

Japan

Portugal

New Zealand

Czech Rep.

Turkey

Slovakia Poland

South Korea

Mexico

Myanmar

Philippines

Sri Lanka IndiaVietnam

Singapore

Hungary

Hong Kong

Bangladesh

Thailand

Indonesia

Malaysia

Taiwan

7GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

International Patenting OutputSelected Countries

Source: USPTO, 2005

Annual U.S. patents per 1 million population, 2005

Compound annual growth rate of US-registered patents, 2000 – 2005

0

50

100

150

200

250

300

-8% -3% 2% 7%

U.S.

Japan

Taiwan

Switzerland

Denmark

Canada

FranceU.K.

Australia

Sweden

Finland

Italy

Netherlands

Germany

NorwayAustria

Israel

South Korea Singapore

8GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Microeconomic FoundationsMicroeconomic Foundations

Determinants of Competitiveness

The Quality of the Microeconomic

BusinessEnvironment

The Quality of the Microeconomic

BusinessEnvironment

The Sophisticationof Company

Operations andStrategy

The SophisticationThe Sophisticationof Companyof Company

Operations andOperations andStrategyStrategy

Macroeconomic, Political, Legal, and Social ContextMacroeconomic, Political, Legal, and Social ContextMacroeconomic, Political, Legal, and Social Context

• A sound macroeconomic, political, legal, and social context creates the potential for competitiveness, but is not sufficient

• Only firms can create wealth, not government

9GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

Availability of high quality, specialized inputs available to firms

– Human resources– Capital resources– Physical infrastructure– Administrative infrastructure

(e.g. registration, permits)– Information infrastructure (e.g.

economic data, corporate disclosure)

– Scientific and technological infrastructure

– Natural resources

Access to capable, locally based suppliersand firms in related fieldsPresence of clusters instead of isolated industries

A local context and rules that encourage productivity

– e.g., incentives for capital investments, intellectual property protection

Incentive systems based on meritOpen and vigorous local competition, especially among locally based rivals More sophisticated and

demanding local customer(s)Local customer needs that anticipate those elsewhereUnusual local demand in specialized segments that can be served nationally and globally

Determinants of CompetitivenessEnhancing the Business Environment

• Successful economic development is a process of successive economic upgrading, in which the business environment evolves to support and encourage increasingly sophisticated ways of competing

10GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Traditional Strengths of the Singaporean Business Environment

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

World-class infrastructureEfficient government services and regulationsWell-trained and flexible workforceSolid financial market

Focus on selected clusters (electronics, chemicals, logistics, financial services) to overcome small economy-disadvantages

High openness to global competitionAggressive attraction of foreign companiesAttractive tax regimeProfessional management and governance of government-linked companies

11GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Equipment Suppliers

(e.g. Oil Field Chemicals,

Drilling Rigs, Drill Tools)

Specialized Institutions (e.g. Academic Institutions, Training Centers, Industry Associations)

SpecializedTechnology

Services

(e.g. Drilling Consultants,

Reservoir Services, Laboratory Analysis)

Subcontractors

(e.g. Surveying,Mud Logging,Maintenance

Services)

BusinessServices

(e.g. MIS Services,Technology Licenses,

Risk Management)

OilTrans-

portation

OilTrading

OilRefining

Oil Retail

Marketing

OilWholesaleMarketing

OilDistribution

GasGathering

GasProcessing

GasTrading

GasTransmis-

sion

GasDistribution

GasMarketing

Oil & Natural GasExploration & Development

Oil & Natural Gas Completion &

Production

Upstream Downstream

Oilfield Services/Engineering & Contracting Firms

Cluster DevelopmentOil and Gas, Houston

12GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

SingaporeExport Portfolio by Cluster, 1997-2005

Change in Singapore’s world export market share, 1997 – 2005Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Sing

apor

e’s

wor

ld e

xpor

t mar

ket s

hare

, 200

5

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

-2.00% -1.50% -1.00% -0.50% 0.00% 0.50% 1.00% 1.50% 2.00%

Change In Singapore’s Overall World Export Share: -0.07%

Singapore’s Average World Export Share: 2.34%

Exports of US$10 Billion =

Information Technology

Oil and Gas Products

Business Services

Communications Equipment

Entertainment and Reproduction Equipment

Hospitality and Tourism

Power and Power Generation Equipment

Tobacco(1.9%, -3.6%)

Publishing and Printing

Chemical Products

Motor Driven ProductsHeavy Machinery

Aerospace Engines

13GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

SingaporeExport Portfolio by Cluster, 1997-2005 (continued)

Change in Singapore’s world export market share, 1997 – 2005Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Sing

apor

e’s

wor

ld e

xpor

t mar

ket s

hare

, 200

5

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

-0.50% -0.40% -0.30% -0.20% -0.10% 0.00% 0.10% 0.20% 0.30% 0.40% 0.50%

Change In Singapore’s Overall World Export Share: -0.07%

Singapore’s Average World Export Share: 2.34%

Exports of US$10 Billion =

Oil and Gas ProductsBusiness Services

Analytical InstrumentsTransportation and Logistics

Production Technology

Plastics

Metal Mining and Manufacturing

Lighting and Electrical Equipment

Biopharmaceuticals

Financial Services

Jewelry, Precious Metals and Collectibles

Automotive

Medical Devices

Processed Food

Agricultural Products

Aerospace Vehicles and Defense

Apparel

Textiles

Marine Equipment

Sporting, Recreational and Children's Goods

Forest Products

Fishing and Fishing Products

Building Fixtures and Equipment

Communications Services

Construction ServicesLeather and Related Products

FurniturePrefabricated Enclosures and Structures

Footwear

Construction Materials

14GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Foreign Investment Stocks and FlowsSelected Countries

Stock of FDI as a % of GDP, Average 2001-2004

FDI Inflows as a % of Gross Fixed Capital Formation, Average 2001-2004

Source: UNCTAD (2005)

0%

20%

40%

60%

80%

100%

120%

140%

160%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

U.S.

Finland

Germany

Italy, Turkey

Denmark

Norway

SwedenSwitzerland

IcelandJapan

Portugal

New Zealand, NetherlandsIreland

Greece,Korea

Hungary

Slovenia

Czech. Rep.

Spain Slovakia

Singapore

Vietnam

Thailand

India

China

15GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

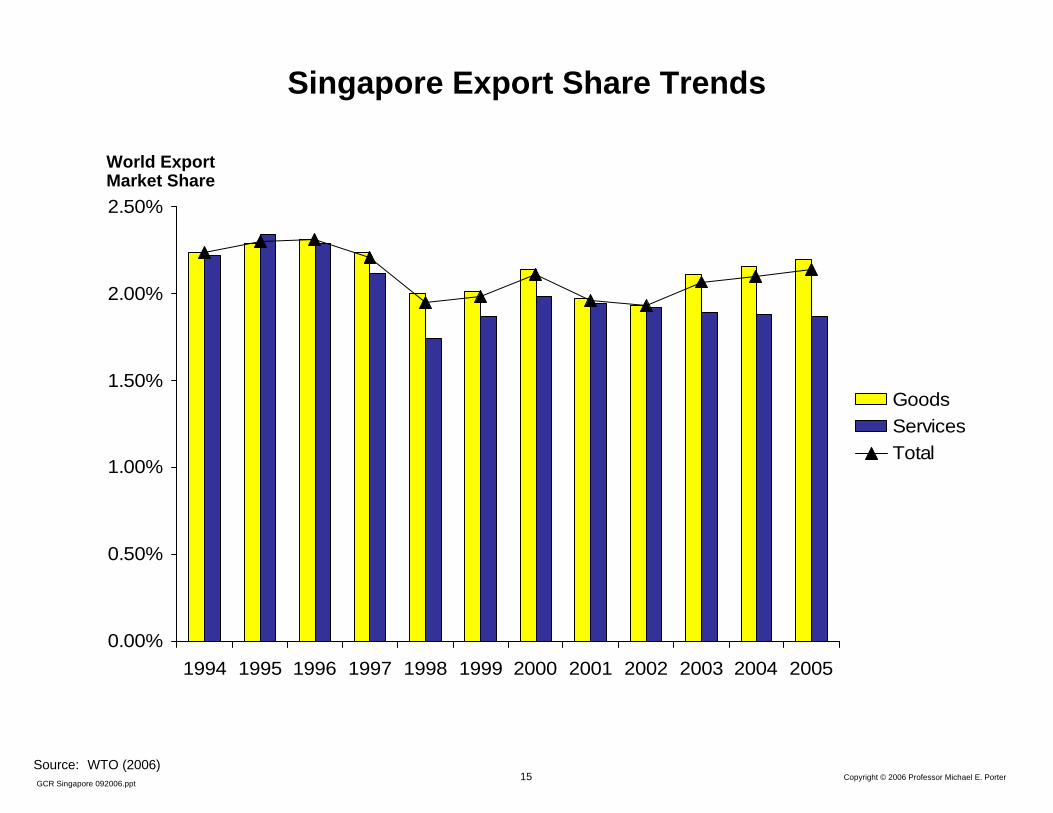

Singapore Export Share Trends

Source: WTO (2006)

World Export Market Share

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

GoodsServicesTotal

16GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

The Process of Economic DevelopmentShifting Roles and Responsibilities

Old ModelOld Model

• Government drives economic development through policy decisions and incentives

• Government drives economic development through policy decisions and incentives

New ModelNew Model

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Competitiveness must become a bottom-up process in which many individuals, companies, and institutions take responsibility

• Every community and cluster can take steps to enhance competitiveness

17GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Institutions for CollaborationSelected Massachusetts Organizations, Life Sciences

Economic Development InitiativesEconomic Development Initiatives

Massachusetts Technology CollaborativeMass Biomedical InitiativesMass DevelopmentMassachusetts Alliance for Economic Development

Massachusetts Technology CollaborativeMass Biomedical InitiativesMass DevelopmentMassachusetts Alliance for Economic Development

Life Sciences Industry AssociationsLife Sciences Industry Associations

Massachusetts Biotechnology CouncilMassachusetts Medical Device Industry CouncilMassachusetts Hospital Association

Massachusetts Biotechnology CouncilMassachusetts Medical Device Industry CouncilMassachusetts Hospital Association

General Industry AssociationsGeneral Industry Associations

Associated Industries of MassachusettsGreater Boston Chamber of CommerceHigh Tech Council of Massachusetts

Associated Industries of MassachusettsGreater Boston Chamber of CommerceHigh Tech Council of Massachusetts

University InitiativesUniversity Initiatives

Harvard Biomedical CommunityMIT Enterprise ForumBiotech Club at Harvard Medical SchoolTechnology Transfer offices

Harvard Biomedical CommunityMIT Enterprise ForumBiotech Club at Harvard Medical SchoolTechnology Transfer offices

Informal networksInformal networks

Company alumni groupsVenture capital communityUniversity alumni groups

Company alumni groupsVenture capital communityUniversity alumni groups

Joint Research InitiativesJoint Research Initiatives

New England Healthcare InstituteWhitehead Institute For Biomedical ResearchCenter for Integration of Medicine and Innovative Technology (CIMIT)

New England Healthcare InstituteWhitehead Institute For Biomedical ResearchCenter for Integration of Medicine and Innovative Technology (CIMIT)

18GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Singapore in Transition: Focus of Current Economic Policies

Innovation Entrepreneurship

Efficiency Social policyDefend Singapore’s core competitive advantages

• Tax reductions

Create new competitive advantages for Singapore

• Investments in universities

• R&D fund for companies / clusters

• Reform of school system

• Focus on more ‘creativeenvironment’

Address existing competitive disadvantages of Singapore

• Support internationalization of Singaporean companies

• Liberalization of domestic markets, e.g. telecom

• FTAs with US, ASEAN, etc.

Defend Singapore’ssocial fabric

• ‘Progress Package’ of spending for low-income citizens

19GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Singapore Biotech Cluster Evolution Over Time

20051995

1995BioprocessingTechnology Centre

1998Centre for Drug EvaluationJohns Hopkins Singapore

2000Genomics Institute of SingaporeBiomedical Research CouncilBioethics Advisory CommitteeTuas Biomedical Park

2001Bioinformatics InstituteNovartis Institute of Tropical DiseasesBiomedical Sciences Manpower Advisory CommitteeGroundbreaking of Biopolis

2003BioPolis opens for businessCenter for Natural Product Research privatized to form MerLionPharmaNational University of Singapore and Duke University agree to open a Graduate Medical School

2002Singapore Tissue NetworkInstitute of Bioengineering and NanotechnologyCancer Syndicate

2005Launch of new biotech courses in Ngee Ann PolytechnicNovartis breaks ground on US$115 million production facility in Tuas Biomedical ParkAlbany Molecular Research established Research Center

2004A*Star and JDRF provide grants to support 7 stem cell research projectsPfizer opens US$220 million manufacturing plant

20022000

Source: Research by HBS student teams in 2005 – Li-Mei Chee, Kola Luu, Gopal Raman, Hwee Yee Yong

20GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Value PropositionValue Proposition

National Economic Strategy

Developing Unique StrengthsDeveloping Unique Strengths Achieving and Maintaining Parity with Peers

Achieving and Maintaining Parity with Peers

• What elements of the business environment are essential to the national value proposition?

• What existing and emerging clusters must be mobilized?

• What macro/political/legal/social improvements are necessary to maintain parity with peer countries or regions?

• What areas of the general business environment must improve to maintain parity with peer countries or regions?

• What is the unique competitive position of the nation?

– What roles in the world and regional economies?– What unique value as a business location?– For what range or types of businesses and

functions can the nation be competitive?

21GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Asia Competitiveness Institute

• Barriers to competitiveness improvement:

– The lack of objective, relevant microeconomic data to analyze competitiveness and track the impact of competitiveness efforts

– The lack of an independent research organization separate from the government

– The individuals with advanced training in the concepts and practice of competitiveness

• The Asia Competitiveness Institute (ACI) will have an important impact on all three dimensions

• As the node in an emerging network of professionals and institutions throughout the ASEAN region, ACI will also become a central facilitator of more effective regional co-operation on competitiveness

22GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Asia Competitiveness InstituteAction Priorities 2006-2007

Organizational launch Initial research projects

• Strategic plan for ACI• Official ACI launch• Recruitment of 2 Senior Research

Fellows and 2 Research Fellows or equivalent

• HBS case study on Singaporean competitiveness

• Singapore Competitiveness Report• Assembly of Singapore competitiveness

data and development of competitiveness research database

• Projects on Indonesia and Vietnam

Network building Education and training

• Stakeholders• Related Institutes, universities and

government bodies• Regional media

• Microeconomic of Competitiveness course as an elective in LKY SPP

• 5-day executive program• Explore customized programs for ASEAN

governments

23GCR Singapore 092006.ppt

Copyright © 2006 Professor Michael E. Porter

Asia Competitiveness InstituteConditions for Success

• Independence

• Permanence

• Inclusiveness

• Clear intellectual framework

• World class research

• Strong leadership