silverdäle - indian corporate ,indian company … meet/131500_20110214.pdfmetal master & rubber...

TRANSCRIPT

PRIVATE AND CONFIDENTIAL for discussions purposes only

Global presence in Gold Jewellery

January 2011

1

RAJESH EXPORTS LIMITED

Silverdäle

Disclaimer

2

This document contains selected information regarding “Rajesh Exports Limited (REL)” (“the Company”), its subsidiaries, and/or associatecompanies. It does not purport to be comprehensive or to contain all of the information that a prospective investor may desire in investigating theCompany or the securities; hence each prospective investor should conduct its own independent due diligence in connection with any transactioninvolving the securities and seek the advice of its own professional advisors. The information contained in this document has not beenindependently verified. Neither the Company nor any of its affiliates, advisers, officers, representatives or agents make or will make anyrepresentation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and any and all legalliability or responsibility is expressly disclaimed based on or relating to: (i) information contained in, or errors in or omissions from this document, or(ii) the recipient’s use of this presentation, or (iii) any other written or oral communications transmitted to the recipient or its affiliates, advisers,officers, representatives or agents in the course of its evaluation of the Company or its securities. Accordingly, no information contained in thisdocument or any written or oral communication transmitted or made available to a recipient of this document: (i) is, or shall be relied upon, as apromise or representation, whether as to the past or future performance; or (ii) will form the basis of any contract.

This presentation includes statements which may constitute forward-looking statements. Although the Company believes that the expectationscontained in such forward–looking statements are conservative and reasonable, they involve many subjective assumptions and are subject to risksand uncertainties which could cause actual results to differ materially. Such statements are not guarantees of future performance. Accordingly, theCompany and its respective affiliates, advisers, officers, representatives or agents give no (and will not give any) assurances, and norepresentation or warranties can be or will be made, as to the accuracy or attainability of such projections, estimates or other forward-lookingstatements.

The estimates statements given in the presentation are not guarantees of future performance; and may or may not be achieved. Please conductindependent due diligence before taking any decision based on these estimates.

No part of this document may be distributed, reproduced, taken or transmitted into the United States, Canada or Japan.

This document is neither an offering memorandum nor an offer or an invitation for the sale or purchase of any securities of the Company or arecommendation in relation to the foregoing. It is not intended to form, and should not be treated as, the basis of any investment decision.

Contents

3

Company Overview12 Jewellery Market

Growth Strategy3

4 Recent Developments

6 Recap

5 The Offering

4

34

32

28

19

16

4

Company Overview

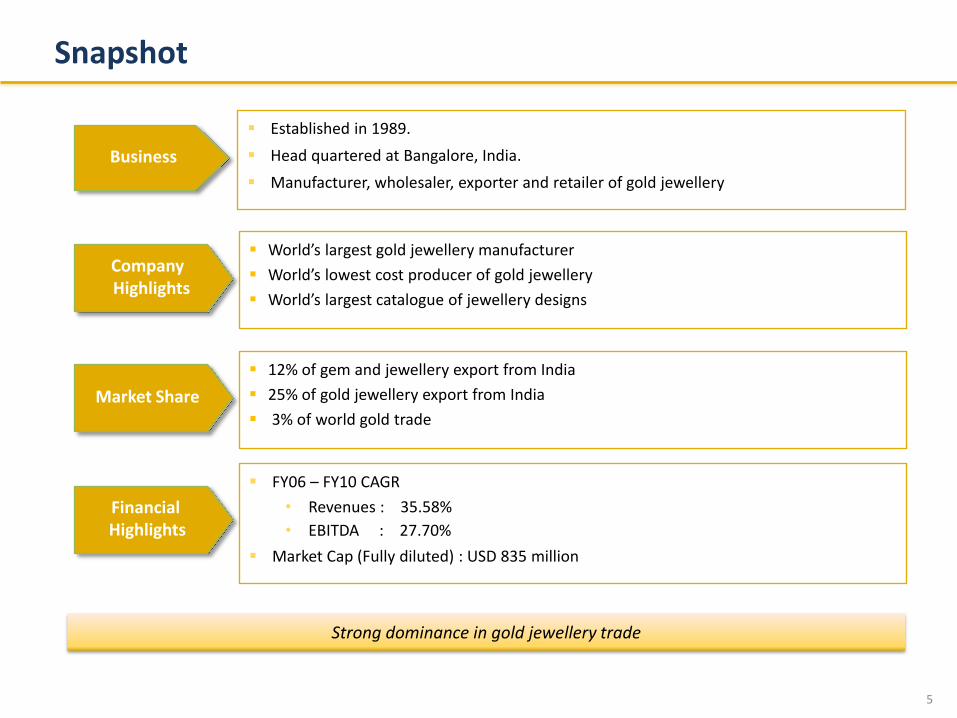

Snapshot

Established in 1989.

Head quartered at Bangalore, India.

Manufacturer, wholesaler, exporter and retailer of gold jewellery

FY06 – FY10 CAGR

• Revenues : 35.58%

• EBITDA : 27.70%

Market Cap (Fully diluted) : USD 835 million

World’s largest gold jewellery manufacturer

World’s lowest cost producer of gold jewellery

World’s largest catalogue of jewellery designs

CompanyHighlights

Business

5

Market Share

12% of gem and jewellery export from India

25% of gold jewellery export from India

3% of world gold trade

Financial Highlights

Strong dominance in gold jewellery trade

Saga of Rapid Growth

6

1989 : Year of Establishment

1996 : India’s largest jewellery manufacturer (6 tpa)

1995: IPO of 2m shares @ 400% to face value of INR 10

2006 : Revenues exceed USD 1 billion

2003 : World’s largest jewellery manufacturing facility (250 tpa)

1994 : India’s first R&D facility

2009 : Revenues exceed USD 4 billion

2010 : Launch of Retail Gold revolution under the brand name SHUBH

Promoters engaged in gold jewellery retailing

1960 to

1989

Expansion of Retail Gold Revolution pan India and Globally

2011 to

2016

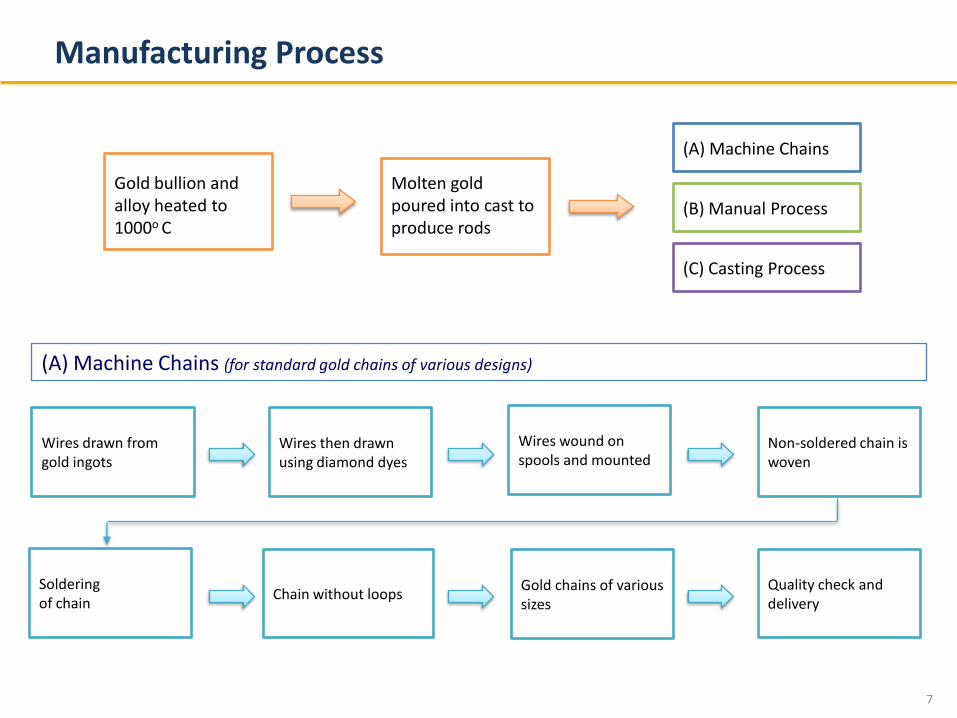

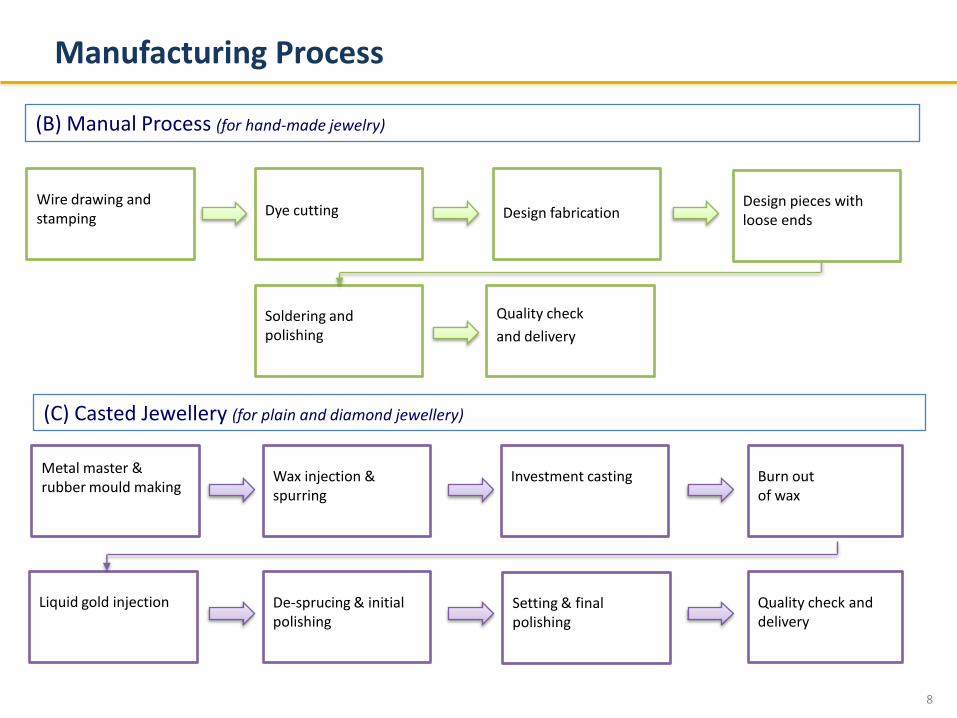

Manufacturing Process

7

Gold bullion and alloy heated to 1000o C

Molten gold poured into cast to produce rods

(A) Machine Chains

(B) Manual Process

(C) Casting Process

Wires drawn from gold ingots

Wires then drawn using diamond dyes

Wires wound on spools and mounted

Non-soldered chain is woven

Soldering of chain

Chain without loopsGold chains of various sizes

Quality check and delivery

(A) Machine Chains (for standard gold chains of various designs)

Manufacturing Process

8

Metal master & rubber mould making

Wax injection & spurring

Investment casting Burn out of wax

Liquid gold injection De-sprucing & initial polishing

Setting & final polishing

Quality check and delivery

(C) Casted Jewellery (for plain and diamond jewellery)

(B) Manual Process (for hand-made jewelry)

Wire drawing and stamping

Dye cutting Design fabricationDesign pieces with loose ends

Soldering and polishing

Quality check

and delivery

Technology

9

REL extensively utilizes latest technology at various production stages -

Alloying - REL has developed proprietary alloys and utilizes the latest alloying technology for creating goldalloys.

Melting - Gold alloy and other precious metals are melted using induction technology.

Wire Drawing - Specialized wire drawing machines and diamond dyes are used for wire drawing and forproduction of various other raw materials.

Master Making - Most advanced prototyping equipments are used for creating masters of jewellerypieces.

Casting - REL has developed technology to cast the minutest and fine filigree designs.

Chain Making - High precision robotic machinery are used for producing the finest chains.

Engraving - Laser technology is extensively used for making engraving dyes and for marking the jewellery.

Soldering - REL has created process for solder free handmade jewellery using advanced laser solderingtechnology. Laser technology is also extensively used in soldering various parts of jewellery.

First time in the world REL has developed 100% solder free Indian jewellery

Consistent Growth

10

In USD million

0

1000

2000

3000

4000

5000

2008 2009 2010

Total Income

84.82

53.77

67.65

0

20

40

60

80

100

2008 2009 2010

EBITDA

0

10

20

30

40

50

60

2008 2009 2010

Profit before Tax

0

10

20

30

40

50

2008 2009 2010

Profit after Tax

Brief Financials

11

Particulars 2009-10 2008-09 2007-08

Total Income 4117.65 2,746.91 1926.00

Total Expenditure 4050.00 2,693.13 1841.17

EBITDA 67.65 53.77 84.82

Interest 21.19 31.44 32.86

Depreciation 0.39 0.37 0.36

Profit before Tax 46.04 21.88 51.57

Taxation 3.06 2.48 5.68

Profit after Tax 42.97 19.41 45.90

Earnings per Share in INR 7.28

Face Value Rs. 1/- per share

3.40

Face Value Rs. 1/- per share

8.24

Face Value Rs. 2/- per hare

Particulars 30th September 2010 30th June2010

Total income 1,119.91 951.88

Total Expenditure 1,092.93 934.39

EBITDA 26.98 17.49

Interest 9.67 6.86

Depreciation 0.92 0.10

Profit after Tax 16.39 10.53

Summarized profit statement (in USD million)

I and II Quarter 2010-11 performance (in USD million)

Awards and Achievements

12

Karnataka State Government Best Exporter Award for past 13 years (from 1997 to 2010)

“Overall Excellence in the category of Gold Exports” Award by the “Gem & Jewellery Export Promotion

Council” for 16 consecutive years (from 1994 to 2010)

Ranked as the ‘Second Fastest Growing Company’ in the Large Scale Sector in 2009

Accorded as the “Jeweller of the Year” Award by Jewellers Association, Bangalore in 2009

Awarded Gold Trophy for exports by Federation of Imports & Exports in 2008

Ranked as the most investor friendly company in India in 2007 by Business India

Ranked No. 1 in the Gems & Jewellery sector in India by Dun & Bradstreet in 2007

The only “Premier Trading House” in Jewellery Sector in India

Accorded ‘Nominated Agency‘ status to import gold for domestic consumption.

In News

13

In News

14

Rajesh Exports ranked as the ‘Second Fastest Growing Company’ in the Large Scale Sector in 2009

Management Team

15

Rajesh MehtaExecutive Chairman

• Experience of over 20 years in the jewellery industry• Pioneer in organising jewellery trade in India• Director, Handloom & Handicrafts Exports Promotion Corp President,

Jewellery Exporters Association of Karnataka

Prashant MehtaManaging Director

• Experience of over 22 years in jewellery manufacturing• Expert on global best practices in jewellery manufacturing and

technology.

Vijyendra RaoCEO (Export)

• Experience of over 20 years in exports• Expert in overall management of export business• Specialist in marketing and finance aspects of export business.

Mayank MallickCEO (Retail Branding)

• Experience of over 12 years in brand building & jewellery retailing• Expert in establishing new jewellery stores, creating awareness and

branding of the jewellery store.• In charge of establishing 500 retail stores pan India

Prasanna KumarCEO (Retail)

• Experience of over 20 years in retailing • Expert in day-to-day management of retail business specializing in

logistics of the retail stores and relationship building with the associates

16

Jewellery Market

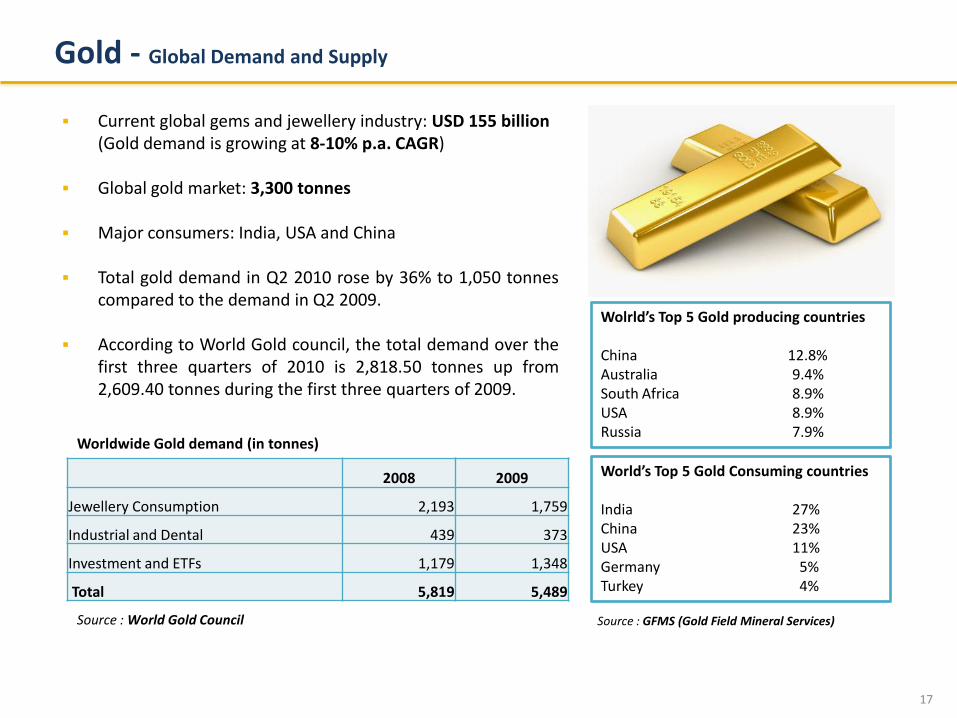

Gold - Global Demand and Supply

17

Current global gems and jewellery industry: USD 155 billion(Gold demand is growing at 8-10% p.a. CAGR)

Global gold market: 3,300 tonnes

Major consumers: India, USA and China

Total gold demand in Q2 2010 rose by 36% to 1,050 tonnescompared to the demand in Q2 2009.

According to World Gold council, the total demand over thefirst three quarters of 2010 is 2,818.50 tonnes up from2,609.40 tonnes during the first three quarters of 2009.

Wolrld’s Top 5 Gold producing countries

China 12.8%Australia 9.4%South Africa 8.9%USA 8.9%Russia 7.9%

2008 2009

Jewellery Consumption 2,193 1,759

Industrial and Dental 439 373

Investment and ETFs 1,179 1,348

Total 5,819 5,489

Worldwide Gold demand (in tonnes)

World’s Top 5 Gold Consuming countries

India 27%China 23%USA 11%Germany 5%Turkey 4%

Source : GFMS (Gold Field Mineral Services)Source : World Gold Council

Gold – Indian Scenario

18

India is the world's largest buyer of gold and world’s largest Jewellerymarket with an -

Average consumption of 850 tonnes p.aValued at USD 37 billionGrowing at 10% p.a

India uses 90% of its total gold consumption for Gold Jewellery making.

Indian gold demand is firmly embedded in cultural and religioustraditions (Stridhan)

GoldFirst Half 2009 First Half 2010 % Growth

Tonnes INR (Billion) Tonnes INR (Billion) Volume Value

Jewellery 163 326 272.5 545 67% 70%

Investment 25.4 51 92.5 185 264% 332%

Total 188.4 377 365 730 94% 97%

Source : India Infoline News Service, 25 Aug’2010

India Gold demand growth figures H1 2009 VS H1 2010

Over centuries and millennia, gold has become an inseparable part of the Indiansociety and fused into the psyche of an Indian.

Indians see Gold as a symbol of purity, prosperity, investment and good fortune.

19

Growth Strategy

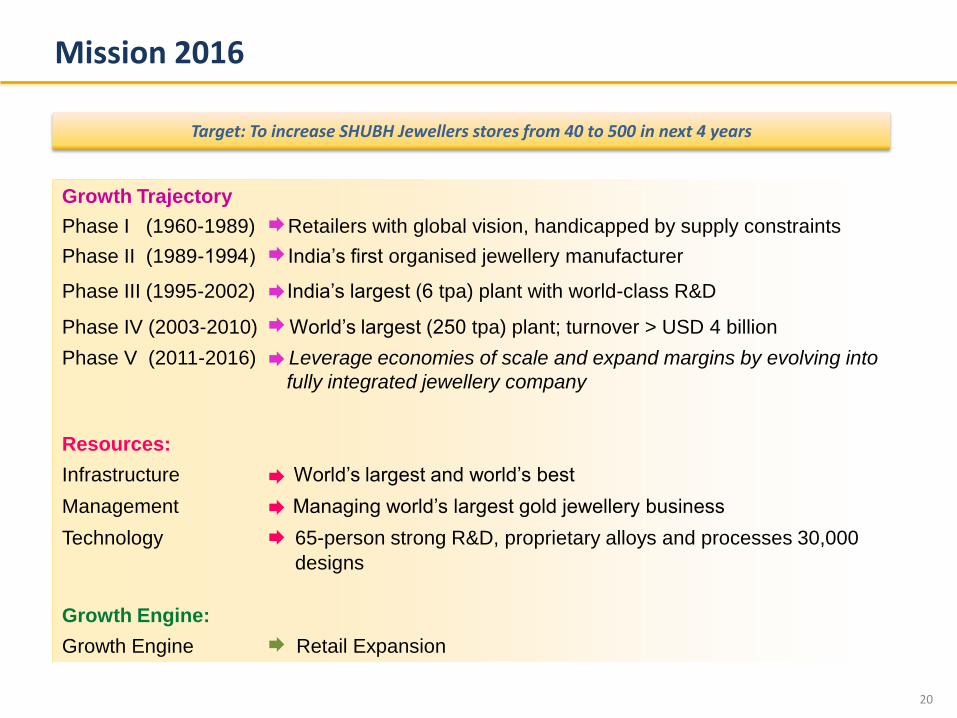

Mission 2016

20

Growth Trajectory

Phase I (1960-1989) Retailers with global vision, handicapped by supply constraints

Phase II (1989-1994) India’s first organised jewellery manufacturer

Phase III (1995-2002) India’s largest (6 tpa) plant with world-class R&D

Phase IV (2003-2010) World’s largest (250 tpa) plant; turnover > USD 4 billion

Phase V (2011-2016) Leverage economies of scale and expand margins by evolving into

fully integrated jewellery company

Resources:

Infrastructure World’s largest and world’s best

Management Managing world’s largest gold jewellery business

Technology 65-person strong R&D, proprietary alloys and processes 30,000

designs

Growth Engine:

Growth Engine Retail Expansion

Target: To increase SHUBH Jewellers stores from 40 to 500 in next 4 years

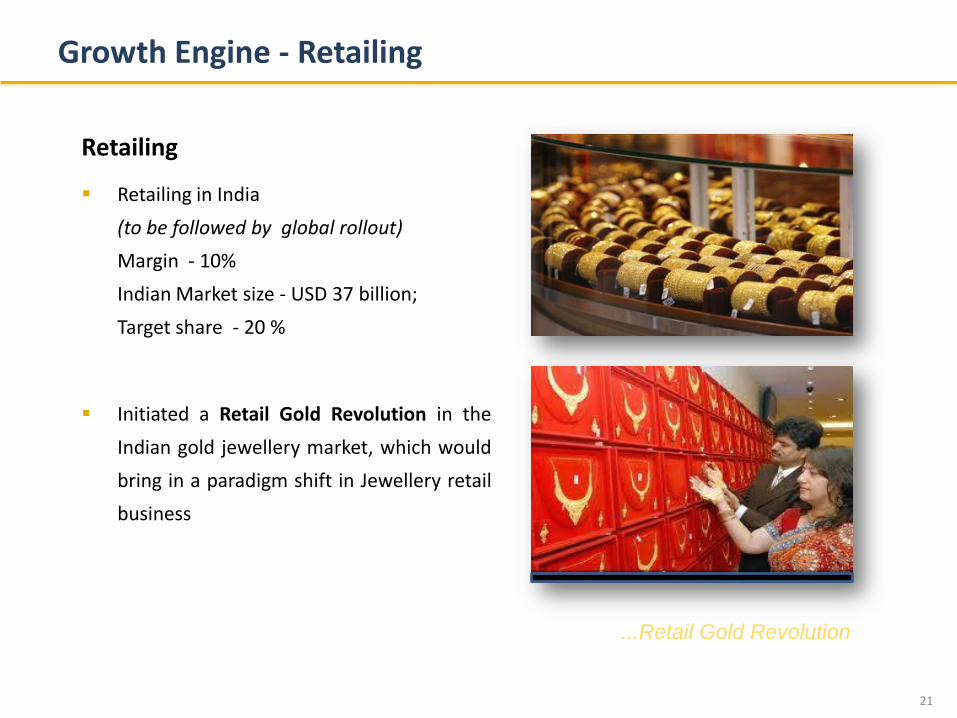

Growth Engine - Retailing

21

Retailing

Retailing in India

(to be followed by global rollout)

Margin - 10%

Indian Market size - USD 37 billion;

Target share - 20 %

Initiated a Retail Gold Revolution in the

Indian gold jewellery market, which would

bring in a paradigm shift in Jewellery retail

business

...Retail Gold Revolution

Jewellery Retail – Indian Scenario

22

96% is in unorganized sector (globally 70% isunorganized)

Very highly fragmented (no pan-India stores)

Over 400,000 small retailers and 850,000 goldsmiths

Branded gold jewellery is a very recent phenomenon

Branded jewellery accounts for only 4% of totaljewellery market, but growing at 30-40% pa and isslated to constitute 10% of total jewellery market by2009

Value for money, Quality, consistency and variety ofdesigns hold the key to retailing success

The organized market has shown an annual growth rate of 40% since 2005

Retail Venture USP

23

Punch Mantra (the five doctrines)

22K GuaranteeBacked by life-time buyback guarantee

Largest RangeBacked by proprietary library of 30,000 active designs

TechnologyProprietary technology to ensure standardization, consistency, color, Tarnish free etc.

Competitive PricingPowered by economies of scale, lowest manufacturing costs, lowest finance cost, technology resulting in lower use of gold for same design. Introduced the revolutionary “Real Rate Per Gram”

ServicePan-India network of retail showrooms providing life-time free repair service at any store

Service

Pricing

Technology

Guarantee

Range

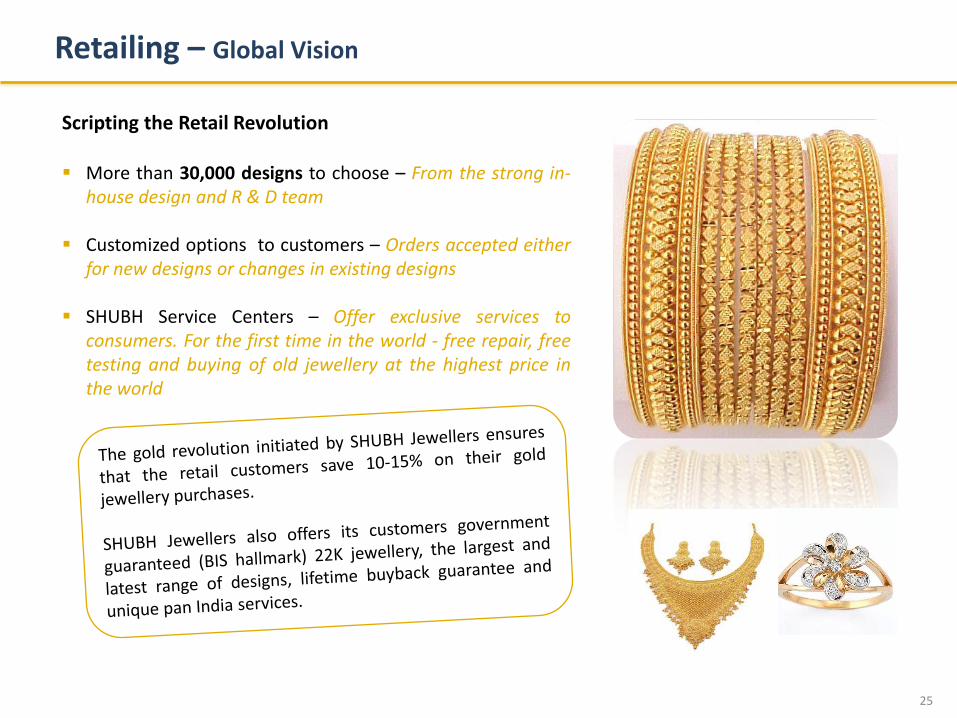

Retailing – Global Vision

24

Scripting the Retail Gold Revolution

Retail customers have been offered REAL RATE PERGRAM - An unheard concept in the industry

No miscellaneous charges such as makingcharges, stone charges, wastage etc – Customerscharged only on Gold

Achievable because of the advantage of Integratedfacilities – The USP of Rajesh Exports Limited

The price advantage – No middlemen in the wholeprocess from importing raw gold from the mines to endcustomer

Currently with 28 stores under the Gold revolution–Target of 500 stores pan India by 2015

Unique concept of Franchise model – A Win Winsituation for the Franchisor and Franchisee

An awareness campaign of Rajesh Exports Limited to educate customers on the concept of REAL RATE PER GRAM.

Retailing – Global Vision

25

Scripting the Retail Revolution

More than 30,000 designs to choose – From the strong in-house design and R & D team

Customized options to customers – Orders accepted eitherfor new designs or changes in existing designs

SHUBH Service Centers – Offer exclusive services toconsumers. For the first time in the world - free repair, freetesting and buying of old jewellery at the highest price inthe world

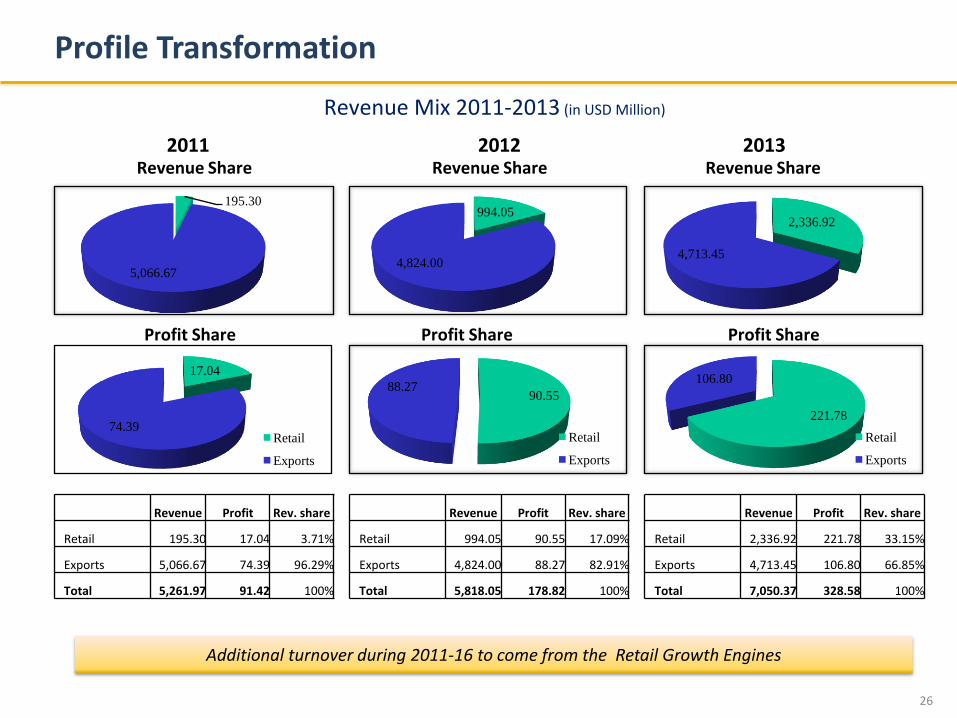

Profile Transformation

26

17.04

74.39Retail

Exports

Revenue Profit Rev. share

Retail 195.30 17.04 3.71%

Exports 5,066.67 74.39 96.29%

Total 5,261.97 91.42 100%

Revenue Profit Rev. share

Retail 994.05 90.55 17.09%

Exports 4,824.00 88.27 82.91%

Total 5,818.05 178.82 100%

Revenue Profit Rev. share

Retail 2,336.92 221.78 33.15%

Exports 4,713.45 106.80 66.85%

Total 7,050.37 328.58 100%

2011 20132012

Profit Share Profit Share Profit Share

90.5588.27

Retail

Exports

221.78

106.80

Retail

Exports

Revenue ShareRevenue ShareRevenue Share

195.30

5,066.67

994.05

4,824.00

2,336.92

4,713.45

Revenue Mix 2011-2013 (in USD Million)

Additional turnover during 2011-16 to come from the Retail Growth Engines

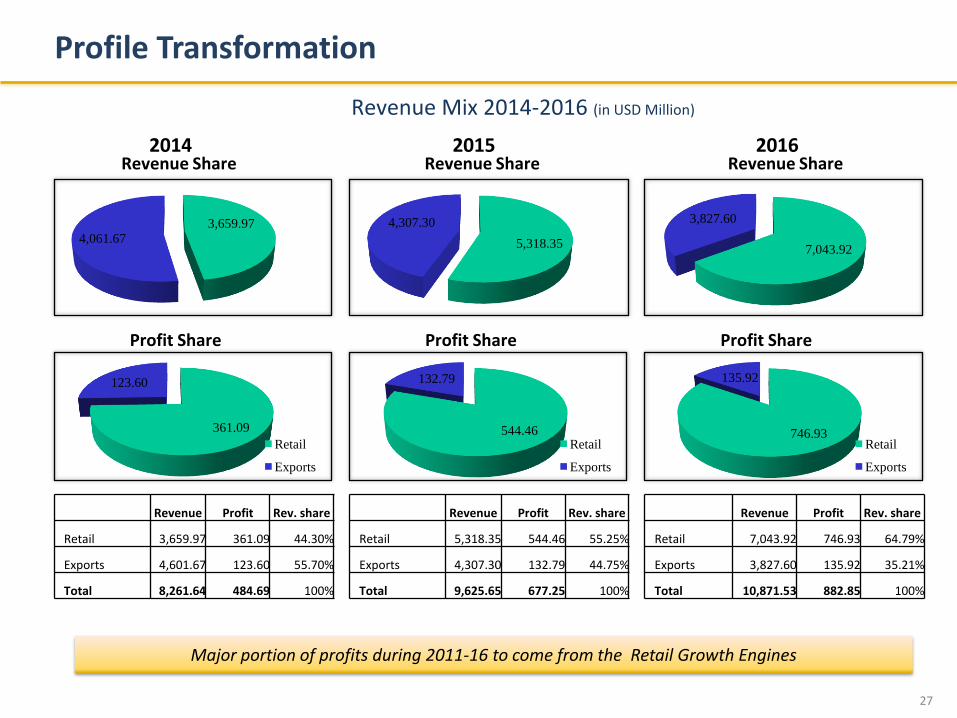

Profile Transformation

27

Revenue Profit Rev. share

Retail 3,659.97 361.09 44.30%

Exports 4,601.67 123.60 55.70%

Total 8,261.64 484.69 100%

Revenue Profit Rev. share

Retail 5,318.35 544.46 55.25%

Exports 4,307.30 132.79 44.75%

Total 9,625.65 677.25 100%

Revenue Profit Rev. share

Retail 7,043.92 746.93 64.79%

Exports 3,827.60 135.92 35.21%

Total 10,871.53 882.85 100%

2014 2015 2016Revenue Share Revenue ShareRevenue Share

361.09

123.60

Retail

Exports

544.46

132.79

Retail

Exports

746.93

135.92

Retail

Exports

Profit ShareProfit ShareProfit Share

3,659.974,061.67 5,318.35

4,307.30

7,043.92

3,827.60

Revenue Mix 2014-2016 (in USD Million)

Major portion of profits during 2011-16 to come from the Retail Growth Engines

28

Recent Developments

Corporate Structure

29

SHUBH INFRASHUBH RETAIL

PARENT COMPANY

SUBSIDIARIES

STORE BRANDS9 BRANDS OF DIAMOND

JEWELLERYSHUBH LAABH

RAJESH EXPORTS LIMITEDManufacturers, Exporters and Wholesalers

Manufacture of Gold and Diamond Jewellery, Bulk Exports, Wholesale, White Label Branded Exports and

Diamond Jewellery Exports.

SHUBH Retail

30

For sharper focus:

All retailing ventures to be put under 100% subsidiary:

SHUBH Retail

Team (ex-Oyzterbay, ex-Titan)

Pioneers in creating branded retail jewellery in India

with over 50 man-years of experience

Team that created ‘super brands’ – Titan, Tanishq, Oyzterbay – are now

part of the team at Rajesh Exports

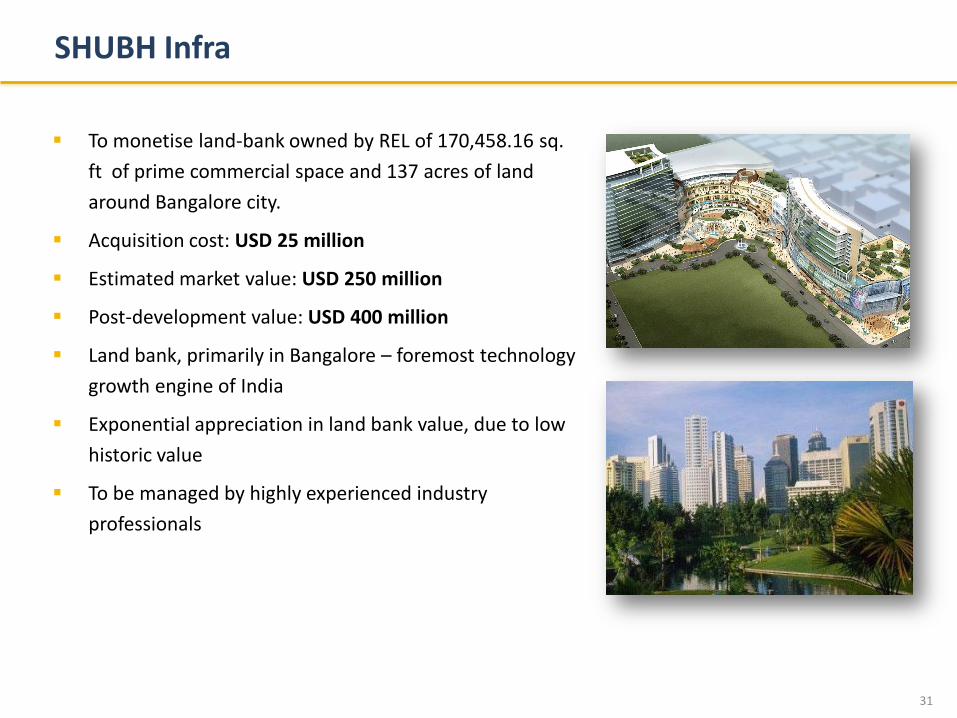

SHUBH Infra

31

To monetise land-bank owned by REL of 170,458.16 sq.

ft of prime commercial space and 137 acres of land

around Bangalore city.

Acquisition cost: USD 25 million

Estimated market value: USD 250 million

Post-development value: USD 400 million

Land bank, primarily in Bangalore – foremost technology

growth engine of India

Exponential appreciation in land bank value, due to low

historic value

To be managed by highly experienced industry

professionals

32

Recap

33

Lowest cost manufacturer of gold jewellery

Most advanced technology.

Stable existing volume business.

USP: 22K Guarantee, Range, Technology, Pricing,

Service

SHUBH Retail – Laabh, Shubh, and Oyzterbay

Retail

Gold Processing

SHUBH Infra to monetize land bankInfra

Zero gold price risk, price-hedging, technologyOperational Excellence

Quick Recap....

Retailers achieving economies of scale in manufacturing onto margin expansiontrajectory to emerge as fully integrated company

Market Snapshot

34

122% increase in PAT from FY 2009 to FY 2010. Capitalized onthe downturn by climbing up the value chain into high valueadded products and lowering the cost structure by backwardintegration.

Particulars 2009-10 2008-09 2007-08 2006-07

Revenue 4,117.65 2,746.91 1,926.00 1,531.87

EBITDA 67.65 53.77 84.82 47.62

EBITDA % 1.6% 2.0% 4.4% 3.1%

PAT 42.97 19.41 45.90 22.51

Cash Bank 1,478.60 1,230.53 1,111.56 1,280.89

Particulars % of Holding

Promoters 52.42

FII 11.37

DII 4.01

Public 32.20

Total 100.00

Brief Financials (USD in Million)

Shareholding Pattern (Sept’10)

Particulars Value

CMP in INR as on 10 Jan’ 11 132.55

Mcap ( INR million) 37,570.00

Mcap ( USD million) 835

EPS (INR) 6.80

P/E 19.50

NSE Code RAJESHEXPO

Reuters Code REXP.BO

Bloomberg Code RJEX@IN

Index Comparison (BSE)

35

Thank You

For further information, please contact:

Somitra Agrawal

Managing Director

Silverdale Services (Hong Kong) Limited.

Suite 802 - A, 8/F Pacific House

20 - 20B Queen's Road Central,

Central, Hong Kong

Tel HK : (852) 28680444

Fax HK : (852) 28680447

Tel IND : (91 ) 22 66301626 / 27

Email: [email protected]

Rajesh MehtaExecutive Chairman(Registered Office)No. 4, Batavia Chambers, Kumara Krupa Road, Kumara Park (East),Bangalore – 560001, INDIA.Tel: + 91 (80) 2226 6735Fax: +91 (80) 2228 5218Email: [email protected]