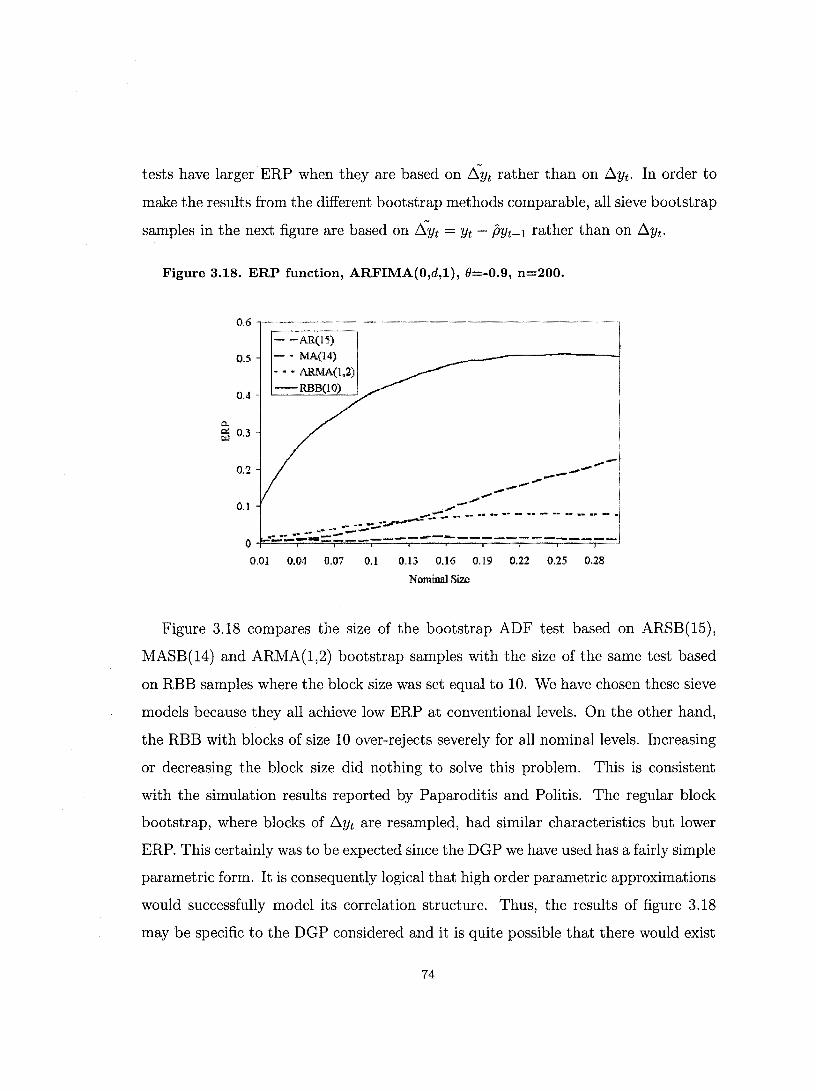

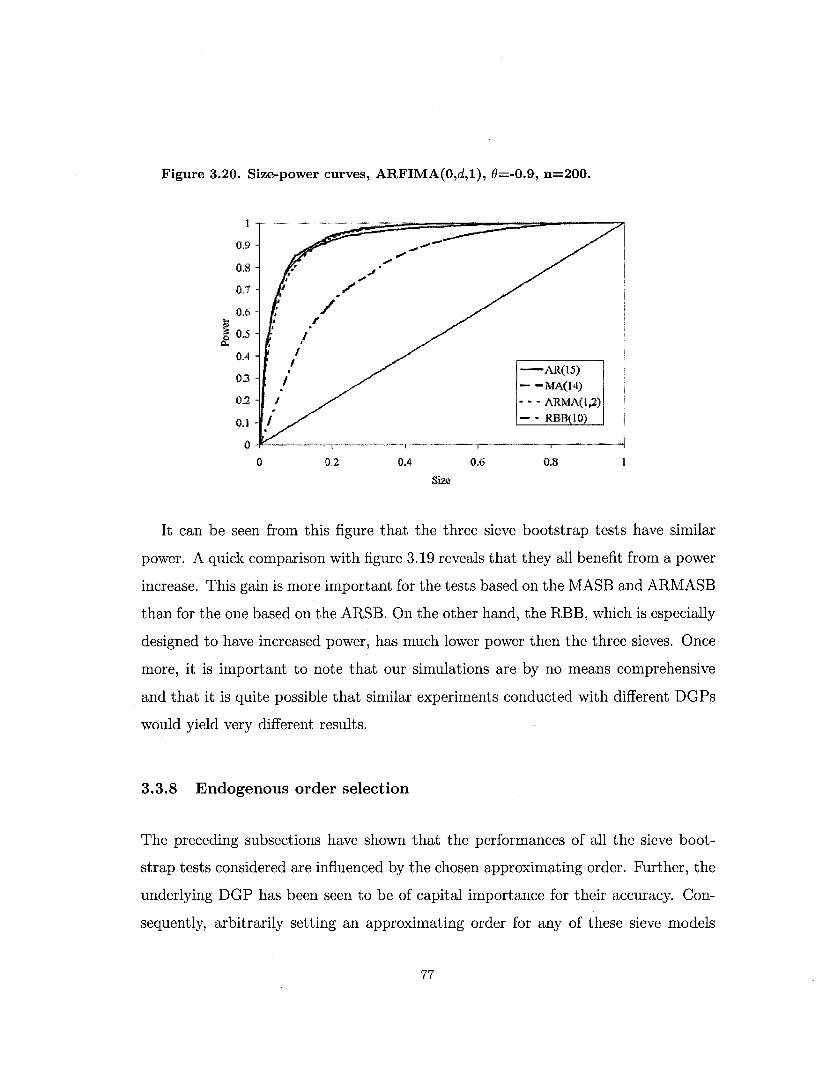

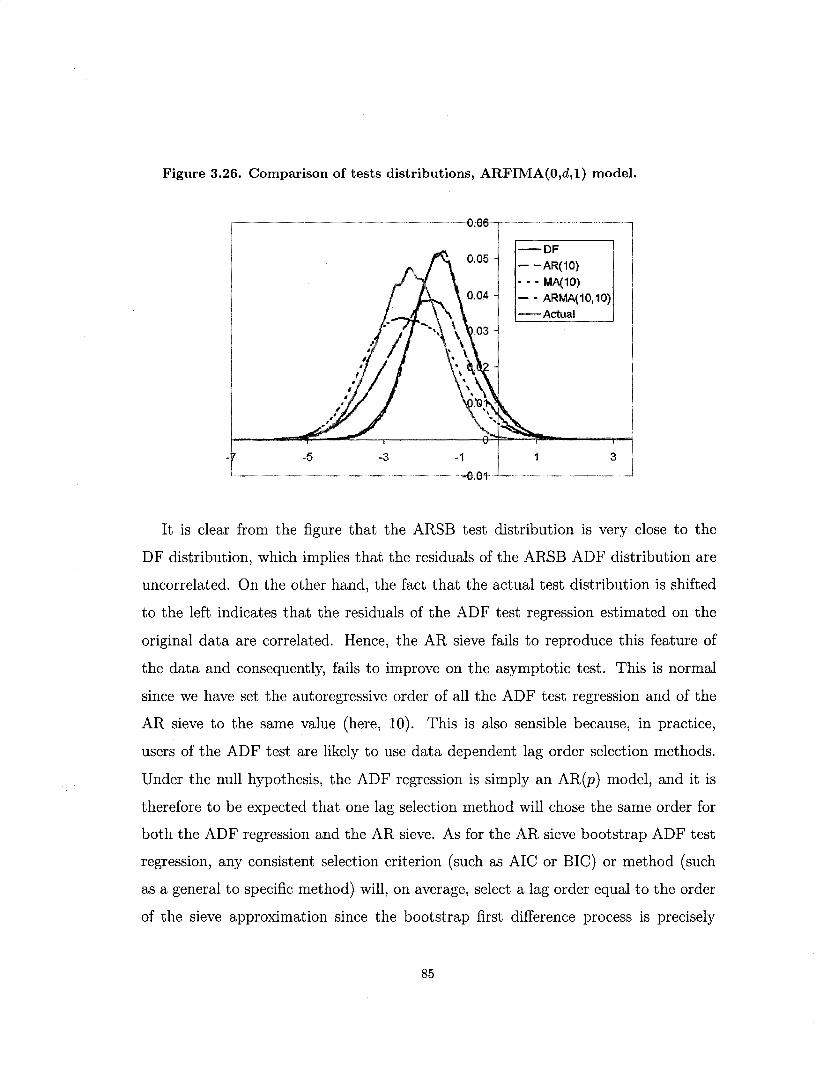

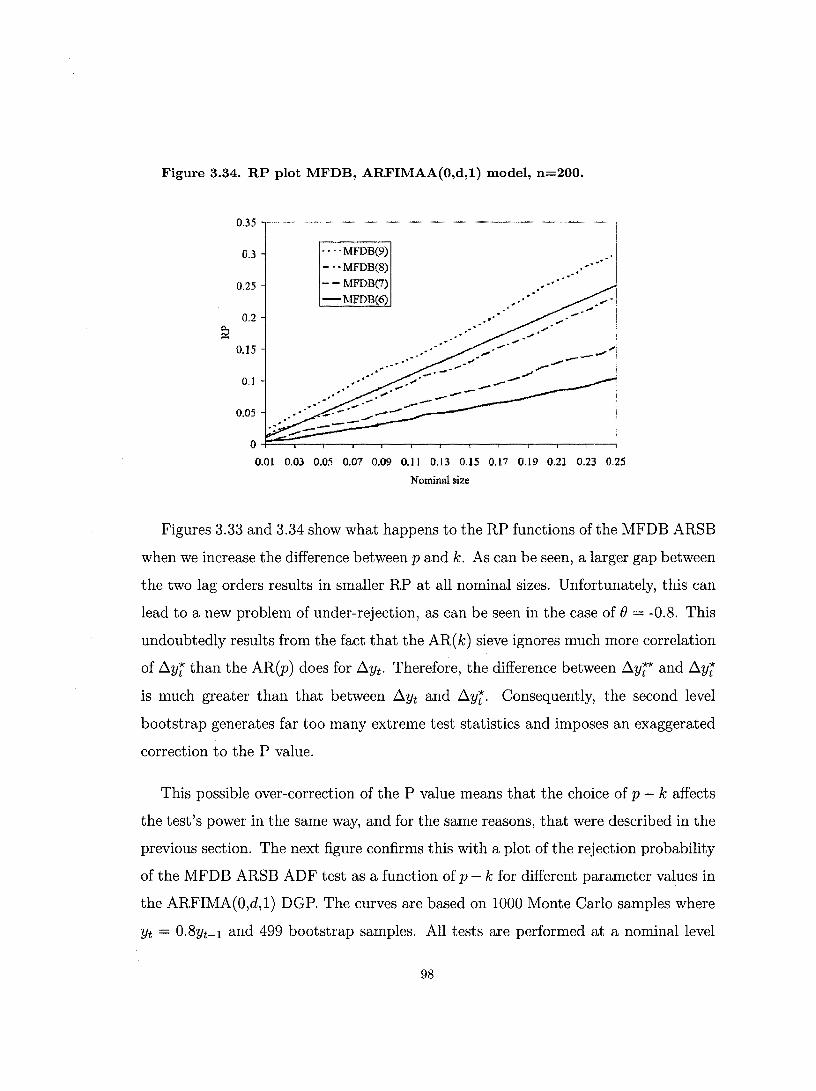

sieve bootstrap unit root tests - mcgill...

TRANSCRIPT

Sieve Bootstrap Unit Root Tests

Patrick Richard Department of Economies

McGill University

Montréal

A thesis submitted to McGill University

in partial fulfillment of the requirements of the degree of Doctor of Philosophy

June 2007

@Patrick Riehard, 2007

1+1 Libraryand Archives Canada

Bibliothèque et Archives Canada

Published Heritage Branch

Direction du Patrimoine de l'édition

395 Wellington Street Ottawa ON K1A ON4 Canada

395, rue Wellington Ottawa ON K1A ON4 Canada

NOTICE: The author has granted a nonexclusive license allowing Library and Archives Canada to reproduce, publish, archive, preserve, conserve, communicate to the public by telecommunication or on the Internet, loan, distribute and sell theses worldwide, for commercial or noncommercial purposes, in microform, paper, electranic and/or any other formats.

The author retains copyright ownership and moral rights in this thesis. Neither the thesis nor substantial extracts from it may be printed or otherwise reproduced without the author's permission.

ln compliance with the Canadian Privacy Act some supporting forms may have been removed from this thesis.

While these forms may be included in the document page count, their removal does not represent any loss of content fram the thesis.

• •• Canada

AVIS:

Your file Votre référence ISBN: 978-0-494-38635-4 Our file Notre référence ISBN: 978-0-494-38635-4

L'auteur a accordé une licence non exclusive permettant à la Bibliothèque et Archives Canada de reproduire, publier, archiver, sauvegarder, conserver, transmettre au public par télécommunication ou par l'Internet, prêter, distribuer et vendre des thèses partout dans le monde, à des fins commerciales ou autres, sur support microforme, papier, électronique eUou autres formats.

L'auteur conserve la propriété du droit d'auteur et des droits moraux qui protège cette thèse. Ni la thèse ni des extraits substantiels de celle-ci ne doivent être imprimés ou autrement reproduits sans son autorisation.

Conformément à la loi canadienne sur la protection de la vie privée, quelques formulaires secondaires ont été enlevés de cette thèse.

Bien que ces formulaires aient inclus dans la pagination, il n'y aura aucun contenu manquant.

2

Abstmct

We consider the use of a sieve bootstrap based on moving average (MA) and au

toregressive moving average (ARMA) approximations to test the unit root hypothesis

when the true Data Generating Pro cess (DGP) is a generallinear process. We provide

invariance principles for these bootstrap DGPs and we prove that the resulting ADF

tests are asymptotically valid. Our simulations indicate that these tests sometimes

outperform those based on the usual autoregressive (AR) sieve bootstrap. We study

the reasons for the failure of the AR sieve bootstrap tests and propose sorne solutions,

including a modified version of the fast double bootstrap.

We also argue that using biased estimators to build bootstrap DGPs may result in

less accurate inference. Sorne simulations confirm this in the case of ADF tests. We

show that one can use the GLS transformation matrix to obtain equations that can be

used to estimate bias in general ARMA(p,q) models. We compare the resulting bias

reduced estimator to a widely used bootstrap based bias corrected estimator. Our

simulations indicate that the former has better finite sample properties then the latter

in the case of MA models. Finally, our simulations show that using bias corrected or

bias reduced estimators to build bootstrap DGP sometimes provides accuracy gains.

3

Résumé

Nous étudions l'application du bootstrap aux tests de racine unitaire lorsque

le processus générateur de données (PDG) est infiniment corrélé. Nous proposons

l'utilisation du bootstrap de type sieve basé sur des modèles approximatifs des types

moyenne mobile et autorégressifs-moyenne mobile. Nous prouvons l'existence de

théorèmes de la limite centrale fonctionnels s'appliquant à ces PGD bootstraps. Nous

démontrons également que les tests de racine unitaire ADF basés sur ces PGD boot

straps sont asymptotiquement valides. Nos simulations indiquent que ces tests sont

parfois plus précis que ceux utilisant le bootstrap sieve autorégressif. L'examen des

causes de ce phénomène nous amène à proposer quelques solutions, incluant une forme

modifiée du bootstrap double rapide.

Nous remarquons aussi que la construction de PGD bootstraps à l'aide d'estimateurs

biaisés affecte négativement la précision des tests. Nous démontrons qu'il est possible

d'utiliser la matrice de transformation des moindres carrés généralisés pour obtenir des

équations permettant d'estimer le biais d'un estimateur des paramètres d'un modèle

ARMA(p,q). Nos simulations indiquent que cette méthode de correction de biais

est plus précise qu'une méthode populaire basée sur le bootstrap dans le cas des

modèles de moyenne mobile. Finalement, nous simulations indiquent que l'utilisation

d'estimateurs corrigés pour le biais dans la construction des PGD bootstraps résulte

parfois en des tests plus précis

4

Aknowledgement

1 am particularly indebted to my thesis supervisor, professor Russell Davidson, for

numerous helpful, as weIl as enjoyable, discussions. 1 also thank professors John Gal

braith and Victoria Zinde-Walsh for their help at different stages of the preparation

of this thesis. The comments of professors Nikolai Gospodinov, Jennifer Hunt, James

MacKinnon, Mary MacKinnon Alex Maynard, Daniel Parent and David Stephens as

weIl as those of M. Christ os Ntantamis and seminar participants at the 2006 Canadian

economics association meeting and second annual CIREQ Ph.D. student conference

were also greatly appreciated.

5

Table of Contents

Chapter 1. General Introduction ....................................... 8

1.1. Introduction ......................................................................... 8

1.2. Unit Root Tests ................................................................... 10

1.3. The Bootstrap ..................................................................... 11

1.4. Bootstrap Unit Root Tests .................................................. 20

1.4. ARMA Sieve Bootstrap ....................................................... 21

1.6. Bootstrap and Bias Correction ............................................ 22

1.7. Conclusion ........................................................................... 22

Chapter 2. Invariance Principle and Validity of Sieve Bootstrap ADF Tests .................................................................................. 23

2.1. Introduction ......................................................................... 23

2.2. General Bootstrap Invariance Principle ............................... 24

2.3. Invariance Principle for MA Sieve Bootstrap ....................... 27

2.4. Invariance Principle for ARMA Sieve Bootstrap .................. 32

2.5. Asymptotic Validity of MASB and ARMASB ADF tests .... 35

2.6. Conclusion ............................................................................ 41

Chapter 3. Simulations ...................................................... 42

3.1. Introduction ......................................................................... 42

3.2. Methodological Issues .......................................................... 45

3.3. Simulations .......................................................................... 49

3.4. Correlation of the Error Terms ............................................ 83

3.5. A Modified Fast Double Bootstrap ...................................... 92

3.6. Conclusion ............................................................................ 99

6

Chapter 4. Bias Correction and Bias Reduction ................ 101

4.1. Introduction .......................................................................... 101

4.2. Bootstrap Bias Correction Methods ..................................... 103

4.3. The GLS Bias Reduction ..................................................... 106

4.4. Simulations ........................................................................... 117

4.5. Unit Root Tests in the Finite Correlation Case ................... 131

4.6. Infinite autocorrelation ......................................................... 138

4.7. Conclusion ............................................................................ 146

Chapter 5. Conclusion ........................................................ 148

References ........................................................................... 151

Appendix: Mathematical Proofs ......................................... 159

7

Chapter 1

General Introduction

1.1 Introduction

This thesis considers the application of bootstrap methods to Augmented Dickey

Fuller (ADF) unit root tests. It is a very well documented fact that ADF tests based

on the asymptotic Dickey Fuller distribution suffer from severe error in rejection

probability (ERP) under the null hypothesis when the underlying pro cess is a general

linear pro cess. While the bootstrap has proved to be a very effective method to reduce

ERP, its application in such cases is not at aIl straightforward because it is impossible

to generate bootstrap samples having the same autocorrelation characteristics as the

original data. Among aIl possible methods that have been devised to circumvent this

difficulty is one called the sieve bootstrap, where one approximates the true, infinite

order, pro cess using a finite or der model. It has been shown that allowing the or der

of the approximating model to increase to infinity at an appropriate rate function

of the sample size in sures the consistency of the inference based on this. Although

several time series models are available as potential sieves, only autoregressive (AR)

ones have been considered in the literature thus far.

8

We propose the use of a sieve bootstrap based on moving average (MA) and autore

gressive moving average (ARMA) approximations. We derive invariance principles

that can be applied to the partial sum pro cesses built from bootstrap samples thus

generated, and show that ADF tests based on these methods are asymptotically valid.

We argue that one reason for the bad performances of bootsttrap AR sieve ADF tests

is that the AR sieve bootstrap method fails to reproduce the dependence structure

present in the residuals of the original ADF test regression and provide compelling

evidence to that effect. Using this finding, we introduce a simple modification that

greatly improves finite sample performances of these tests. We also propose a mod

ified version of the fast double bootstrap, which sometimes provides an additional

accuracy gain.

Further, we argue that bootstrap tests may be inaccurate when they are based

on biased estimators of the true DGP. Simulation evidence to that effect is provided

in the case of unit root models driven MA and AR first differences. In an effort to

solve this problem, we introduce a novel bias correction method based on an exact

analytical form of the GLS transformation matrix. This method is shown to belong

to the family of analytical indirect inference methods for MA and ARMA models.

We use simulations to compare it to a weIl known and widely used bootstrap bias

correction technique. Our simulations show that using bias corrected bootstrap DGPs

to conduct ADF tests often allows for a rejection probability doser to the nominal

level.

This thesis is organized as follows. The rest of the present chapter provides a

short introduction to unit root testing and problems related to it. It also discusses

the principles of bootstrap inference and describes methods that are weIl suited for the

analysis of data generated by generallinear pro cess and their applications to unit root

tests. In chapter 2, we derive invariance princip les for partial sum pro cesses built from

MA and ARMA sieve bootstrap samples. These results are then used to prove that

ADF tests based on these sieve bootstraps are asymptotically valid. The finite sample

9

properties of these tests are explored through simulation experiments in chapter 3.

Simulations are also used to identify the causes of the relative performances of different

sieve bootstrap methods and to propose some solutions. Chapter 4 discusses bias

correction for the parameters of ARMA(p,q) models and introduces the GLS based

bias correction method. Simulations are used to investigate the relative performances

of several bias correction procedures and the utility of using them to build bootstrap

DGPs. Chapter 5 concludes.

1. 2 Unit Root tests

Consider a vector y of time series observations generated by an unknown DGP. The

simplest possible manner of testing whether these observations result from a unit root

process is to test the null hypothesis Ho : (3=0 in the simple regression of ~Yt on Yt-l:

~Yt = (3Yt-l + Ut· (1.1 )

Evidently, the null hypothesis corresponds to the case where Yt is a unit root process,

that is, Yt = Yt-l + Ut. Most unit root tests are based on such a null hypothe

sis. However, several tests with stationarity as a null exist. These include the tests

of Kwiatkowski, Phillips, Schmidt and Shin (1992) and Saikkonen and Luukkonen

(1993). We will not discuss these tests here. The simple test described above was

originally proposed by Dickey and Fuller (1979) and is consequently known as the

Dickey-Fuller (DF) test. It is sometimes desirable to add a deterministic part to re

gression (1.1). This usually takes the form of a constant term, a deterministic time

trend or a quadratic time trend. For the sake of simplicity, and because it can be

do ne without any loss of generality, we will ignore these possibilities in most of what

follows.

Because our goal is to test for the stationarity of Yt, the null hypothesis Ho is

tested against the one-sided alternative Hl : (3 <O. Consequently, the DF test can

10

be carried out at nominal level ct by computing a simple t-statistic and comparing

it to the le ft tail ct level critical value of the proper distribution. Under the nulI, Yt

is non-stationary and we say that regression (1.1) is unbalanced. It follows that the

t-statistic does not have the standard normal distribution asymptotically when Ho

is true. In order to avoid any confusion, it is usual to calI this statistic T instead of

t, and we henceforth follow this practice. If the UtS are uncorrelated, then Phillips

(1987) has shown that the distribution of T under the null converges to a functional

of Weiner processes: l (W(I)2 - 1)

T =} -::2:.....:..-:.....:..-:.....:..-_-:-=

(J W(r)2dr)1/2 (1.2)

where W is the standard Wiener process. This distribution is commonly referred to

as the Dickey-Fuller (DF) distribution and, although analytical expressions exist (see

Abadir, 1995), its critical values are generally obtained via simulations (see MacKin

non, 1996). As most standard asymptotic results, (1.2) does not require any specifie

assumptions about the distribution of the error terms. It does however require that

they be serially uncorrelated. If this is not the case, then the asymptotic distribution

of T under Ho is function of the dependence structure. In fact, as shown in Phillips

(1987), the limiting distribution of the DF test is

where

and 1 n

(j~ = lim - LE (Ut)2 n-+oo n t=l

where n is the sample size, (j2 is called the variance of the sum of errors and (j~ is simply

the variance of the errors of regression (1.1). Obviously, (j2 = (j~ when the errors in

(1.1) are independent and T therefore follows the DF distribution asymptoticalIy.

11

When the UtS are dependent, (/2 =1= (/~ and the limiting distribution of 7" is not the DF

one.

The Augmented Dickey-Fuller test procedure, proposed by Dickey and Fuller

(1979) and Said and Dickey (1984), was introdueed as a potential solution to the

problems related to the correlation of the errors. It simply consists in replacing re

gression model (1.1) by the more general specification:

k

~Yt = 8Yt-l + L ,e~Yt-e + Ut, e=l

(1.3)

where one can add a constant and a deterministic trend, as required by the data at

hand. The idea of this new test regression is to include as many lags into equation

(1.3) as is neeessary for the errors to be independent. If this is done properly, then

the test statistic 7" of the hypothesis Ho : 8 = 0 against the alternative Hl : 8 < 0

asymptotically follows the distribution DF given in (1.2). In particular, suppose

that ~Yt is a stationary AR(p) process. Then, the test 7" based on equation (1.3)

asymptotically follows the DF distribution for aIl k 2:: p. Notiee however that the

power of the ADF test will be maximized only if k = p sinee any unneeessary lag only

contributes to increase the variance of the estimated parameters.

When ~Yt is an invertible ARMA(p,q) proeess, regression (1.3) does not aIlow,

in finite samples, to obtain errors that are completely uncorrelated. This follows

from the weIl known fact that any invertible MA(q) can be written as an AR(oo)

process. Nevertheless, Said and Dickey (1984) show that the unit root test based

on 7" is asymptotically valid for a finite lag length if k = o(n1/ 3 ). The problem with

such a rule is that it gives no indication on how many lags is enough for a given

finite sample size and a given DGP. Sinee the correlation structure of the errors of

equation (1.3) depends on the parameters of the ARMA(p,q) DGP of /).Yt, it would

seem sensible that a good finite sam pIe rule should be sensitive to different values of

the parameters in the MA part of the proeess. On the other hand, sinee the inclusion

of one too many parameter in the regression leads to a loss of power and that this

12

loss of power is function of the sample size, it is necessary that a good selection rule

be also sensitive to sample size.

Ng and Perron (1995, 2001) address this question. Ng and Perron (1995) find

that both the Aikaike and Baysian information criterion (AIC and BIC) choose low

lag orders, thus resulting in high error in rejection probability (ERP) under the null.

They also consider a general to specifie selection method, such as the one studied in

Hall (1994), and find that it yields a higher average lag order than AIC and BIC and,

consequently, lower ERP and power. Finally, Ng and Perron (2001) introduce a novel

way to select k which decreases ERP but decreases power. Ng and Perron (1995)

also suggest that one could try to construct a test regression based on an ARMA(p,q)

process rather than trying to approximate an infinite process with a finite AR model.

Very little attention has been devoted to this approach, which first appeared in the

econometric literature in Said and Dickey (1985). This is undoubtedly due to the fact

that ARMA processes are harder to estimate than AR ones.

Galbraith and Zinde-Walsh (1999) develop this ide a by proposing to estimate equa

tion (1.3) by feasible generalized least squares (FGLS) to take explicit account of the

MA part ofthe DGP of tlYt. Vnder the hypothesis that Yt is an ARIMA(O,l,q), they

fit an MA(q) model to tlYt and use its covariance matrix to obtain FGLS estimates

of the parameters of the usual ADF regression. This last regression is estimated with

a given number of lags k which are used to capture any remaining correlation due

to estimation error of the MA part. Tests based on this FGLS-ADF method have

the correct asymptotic RP for a fixed lag order k instead of k = o(nl/3 ). This cornes

from the fact that the remaining correlation disappears asymptotically because of the

consistency of the MA estimator used in the first step of FGLS estimation. Their sim

ulations suggest that this method results in lower small sample ERP. Their method

can easily be extended to ARFIMA(p,l,q) models.

Instead of trying to parametrically model the dependence structure of the errors

of the DF regression, Phillips (1987) and Phillips and Perron (1988) propose a non-

13

parametric correction of the statistic T computed from regression (1.1). The resulting

statistics, called the Phillips and Perron (PP) test statistic is:

where 8~ and 8 2 are consistent estimators of (]"~ and (]"2 respectively and T is the

ordinary DF statistic. Zt can be shown to follow distribution (1.2) asymptotically.

Evidently, the finite sample accuracy of the PP test is a function of how precisely

(]"2 and (]"~ are estimated. As usual, a consistent and unbiased estimator of (]"~ is

given by (n - 1)-1 L~l û;, where {Ût}f=l is the series of residuals from regression

(1.1). There are several consistent estimators available for (]"2. For example, Perron

and Ng (1996) use kernel estimation based on the sample autocovariance and an

autoregressive spectral density estimator. Unfortunately, a problem similar to that

of selecting a lag or der for the ADF regression is inevitable because any consistent

estimator of (]"2 requires that we set sorne lag truncation or window width.

Several simulation studies have established that PP tests do not perform as weIl

as ADF tests in finite samples, see for example, Schwert (1989) and Perron and Ng

(1996). Therefore, we do not study their properties in this thesis. It is nevertheless

worth noting that a modified form of the PP test introduced by Perron and Ng (1996)

have much better finite sample characteristics than the original version.

Unit root testing has been one of the most active fields in econometrics in the last

three decades. There is consequently a huge literature on this topic. We have only

provided an extremely restricted introduction to it. For example, we have completely

ignored the very important problem of power against nearly integrated or fraction

ally integrated alternatives. Sorne interesting surveys are Maddala and Kim (1998),

Hayashi (2000) and Bierens (2001).

14

1.3 The Bootstrap

Let y be a vector of random variables generated by a DGP, which we denote by 1-",

belonging to a given model M. Let 7(Y) be a statistic computed using the vector y.

For short, we will suppress the dependence on y and denote it by 7. Since 7 depends

on y, its probability distribution depends on that of y and therefore, on the DGP 1-".

Suppose that 7 is used to test a given null hypothesis represented by a set of DGPs

which we will denote by Mo. If the probability distribution of 7 is the same for all

DGPs in Mo, then we say that it is a pivotaI statistic, or that it is a pivot. Similarly,

if its asymptotic distribution is the same for all DGPs in Mo, we say that it is an

asymptotically pivotaI statistic, or that it is an asymptotic pivot. Most commonly

used statistics in econometrics are asymptotic pivots.

Consider a given sample of n observations of y and denote by f the statistics

which is computed using it, so that f is a realisation of 7. Further, assume that f

is asymptotically pivotaI and that its asymptotic cumulative density function (CDF)

under the null hypothesis is F 00 (x). If 7 is a test statistic with which we want to

perform inference, then standard asymptotic theory procedure consists in looking at

the position of f, the numerical value of the statistic computed with the data at hand,

with respect to F 00 (x) and to make a judgment on how probable it is that f is indeed

the result of a drawing from Foo(x). If that probability is lower than a predetermined

nominal level, we reject the null hypothesis.

One problem that arises with test statistics that are only asymptotic pivots is that

their finite sample CDF under the null, which we will denote by F(x), may be very

different from Foo(x) and inference based on this latter may be quite misleading. The

reason for this is that being non-pivotaI implies that f's distribution is function of 1-",

the DGP that actually generated the observations, and is different for different DGPs

in Mo. The ide a of the bootstrap is to approximate F(x) by resampling from an

estimate of 1-" respecting the null, say il E Mo, which we obtain using sorne consistent

15

estimation method.

In the simple case of linear regression models with i.i.d. errors, this is easily

accomplished by estimating a regression model on which we impose the restrictions

corresponding to the null hypothesis. Under standard regularity conditions, this

yields consistent parameter estimation as weIl as a vector of residuals whose limit as

the sample size increases is the vector of error terms. In other words, the residuals

are consistent estimators of the error terms. It therefore follows that the empirical

density function (EDF) of the residuals is a consistent estimator of the CDF of the

error terms. Rence, bootstrap samples of the dependent variable with characteristics

belonging to the null hypothesis can be created by drawing from p, the DGP built

from the estimated linear model and the residuals' EDF. For each such sample, a

bootstrap test statistic, Tj, can be computed. The EDF of these bootstrap statistics

can be shown to be a consistent estimator of the actual test distribution under very

weak conditions. It can also be shown that tests conducted using the bootstrap

benefit from asymptotic refinements over their asymptotic counter-parts. This means

that their finite sample error decreases faster as a function of the sample size. Rence,

bootstrap tests can be expected to be more accurate than asymptotic tests in finite

samples. This is also true for confidence intervals.

The existence of these refinements depends on the ability of the bootstrap DG P

to correctly replicate the features of the true DGP. This means that resampling the

residuals as if they were i.i.d. may not always be appropriate. For example, if

the original errors are heteroskedastic, it is important that the bootstrap errors also

be heteroskedastic. This apparently simple requirement necessitates the utilization

of more elaborate bootstrap schemes such as the wild bootstrap of Davidson and

Flachaire (2001).

Similarly, whenever the errors of the original model are serially correlated, it is

necessary that the bootstrap error terms be correlated in a similar fashion. A partic

ularly challenging situation occurs when the errors are generated by a generallinear

16

process. lndeed, sinee it is impossible to correctly model such a dependence using a

finite number of observations, the bootstrap DGP will invariably be different from

the true DGP. It is nevertheless possible to obtain sorne asymptotic refinements by

using more sophisticated bootstrap methods that are specifically designed to handle

such cases. The next two subsections introduee the two most popular such methods.

1.3.1 The block bootstrap

The block bootstrap is a non-parametric resampling method whereby one builds boot

strap samples by putting together blocks of observations drawn at random, with

replacement, instead of single observations. By doing this, one makes sure that what

ever correlation structure exists in the original sample is preserved perfectly intact

within each block. This has the obvious advantage of not requiring any parametric

estimation (nor any knowledge) of the true process. On the other hand, bootstrap

samples built in such a way have a discontinuous correlation structure between each

blocks (the join point problem) as weIl as more variable moments than what would

be obtained with an iid bootstrap.

The former problem cornes from the fact that the last observation of any given

block is not properly correlated with the first observation of the following block. Thus

bootstrap samples fail to exactly replicate the original data's correlation structure.

However, this problem goes away as the sample size in creas es and the block size is

allowed to go to infinity. Nevertheless, it can be shown that the block bootstrap

provides sm aller asymptotic refinements than the iid bootstrap would if we could

correctly model the correlation.

Andrews (2004) proposes a method called the block-block bootstrap which is de

signed to provide asymptotic refinements that tend to what one obtains with the

iid bootstrap. In short, it consists of calculating the test statistic over the original

sample from which sorne observations have been deleted and replaeed by zeros. This

17

effectively introduces in the original sample the same kind of discontinuities that

are inevitable in the bootstrap sample. Paparoditis and Politis (2001, 2002) also

introduced a method to reduce the join point problem, which they call the tapered

bootstrap. This consists of putting less weight on the observations located at the end

of each blocks. They show that this method has better asymptotic refinements than

the simple block bootstrap.

The latter problem with the block bootstrap, the variability of the moments, cornes

from the fact that there are always fewer blocks than observations. This means that

the bootstrap samples are created by drawing from a smaller number of elements.

Thus, the bootstrap sample moments are computed over fewer elements and are

therefore more variable. Hall and Horowitz (1996), in the very general context of

hypothesis testing in GMM estimation with dependent data, suggest rescaling the

test statistics by a factor function of the true variance of the bootstrap data, which

is function of the block length. They show that this allows for a gain in asymptotic

refinements. More recently, Inoue and Shintani (2006) proposed using a similar cor

rection in the G MM criterion function weighting matrix, thus eliminating the need

to correct any subsequent test statistics. Further treatment of this problem may be

found in Hirukawa (2006).

A critical issue for any application of the block bootstrap is the choice of the block

length. Evidently, the larger this is, the smaller is the number of blocks that can be

formed and that must be drawn to construct the bootstrap samples. Consequently,

the join point problem de creas es with the size of the blocks but the variability of the

moments problem increases. Paparoditis and Politis (2003) provide a discussion of

this problem and propose sorne sample based selection methods. The idea is to find

a block size that minimises a criteria such as the accuracy of the estimation of the

distribution function or the accuracy in achieving the nominal coverage of a confidence

interval. The difficulty lies in the fact that the optimal block size depends on unknown

characteristics of the data. Sorne papers propose to estimate these features (Politis

18

and White, 2000 among others) while others suggest avoiding this by the use of non

parametric cross-validation techniques, see Hall, Horowitz and Jing (1995). We shall

not go into further details here.

1.3.2 The sieve bootstrap

One way to avoid the problems associated with the block bootstrap is to use a fi

nite or der parametric approximation of the true dependence structure to generate

bootstrap samples. This method, called the sieve bootstrap was first proposed by

Bühlmann (1997) and further developed by Bühlmann (1998), Choi and Hall (2000)

and Park (2002) among others. Prior to Bühlmann (1997), Kreiss (1992) had consid

ered the possibility of using finite or der AR models to construct bootstrap samples

for AR( (0) models. The sieve bootstrap is based on the fact that any linear and in

vertible time series process can be written in an AR( (0) form. It consists of fitting a

finite order AR(p) model to the data and drawing bootstrap errors from the residuals

as if they were iid. It can be shown that, if we let p go to infinity at a proper rate as

the sample size increases, tests based on the resulting sieve bootstrap samples benefit

from some asymptotic refinements. 80 far, no effort has been made to develop sieve

bootstrap methods based on other models than AR(p) ones.

While it provides us with bootstrap samples with a continuous correlation structure

and does not imply higher variability of the moments, the sieve bootstrap always fails

to replicate the true correlation structure of the data. This may be a particularly bad

problem in small samples where p must be relatively small. In such cases, bootstrap

inferences based on sieves may be just as bad as asymptotic ones. Of course, a similar

critique applies to the block bootstrap. On the other hand, the sieve bootstrap is

incapable of capturing higher moments seriaI dependence, such as GARCH processes,

unless it is specifically modeled. Thus, in this respect, the block bootstrap is superior.

19

1.4 Bootstrap unit root tests

Because standard unit root tests such as the ADF test often have poor finite sample

properties, it is natural to try to use bootstrap methods to obtain more accurate

inferences. Unfortunately, since the ADF regression is unbalanced under the null

hypothesis, none of the theoretical results alluded to above on the asymptotic re

finements provided by the bootstrap ho Ids in this case. In fact, the only theoretical

proof of the existence of bootstrap refinements for ADF tests was devised by Park

(2003). It must be noted however that his results only apply to cases where the first

difference pro cess under the null is a stationary AR(p) with p finite and known. This

is unfortunate because this assumption excludes aIl infinite AR cases, which are the

ones in which the most severe problems are encountered. Nevertheless, several simu

lation studies indicate that block and sieve bootstrap unit root tests often outperform

asymptotic tests in these cases.

Although there is no theoretical proof that they may provide refinements over

asymptotic tests, unit root tests based on sieve and block bootstrap distributions have

some desirable properties. In particular, Park (2002) develops an invariance principle

for partial sum pro cesses built from sieve bootstrap data and uses this results to

show that sieve bootstrap DF tests yield asymptotically valid inference. Further,

Chang and Park (2003) use these results to show that sieve bootstrap ADF tests

are also asymptotically valid under weak regularity conditions. On the other hand,

Paparoditis and Politis (2003) introduce a residual based block bootstrap (RBB)

procedure for unit root testing. This method, which will be described in more details

in chapter 3, is designed to increase the power of the unit root test and to be valid

for a wide variety of models. The authors derive a functional central limit theorem

and show that RBB ADF tests are asymptotically valid. Only a few other papers

consider these issues. Among them is Psaradakis (2001), who studies the properties

of a sieve bootstrap similar to that of Chang and Park (2003), and Swensen (2003),

who studies the properties of unit root tests based on the stationary block bootstrap

20

of Politis and Romano (1994). Both Psaradakis (2001) and Swensen (2003) provide

proofs of the asymptotic validity of the bootstrap tests they consider. The finite

sample performances of ADF tests based on these different methods are investigated

in a detailed Monte Carlo study by Palm, Smeekes and Urbain (2006). According to

them, sieve bootstrap ADF tests have slightly better accuracy than block bootstrap

tests.

1.5 ARMA sieve bootstrap

Although sieve bootstrap tests based on autoregressive approximations often provide

sorne accuracy gains over asymptotic tests, there are circumstances where they per

form very badly. In particular, whenever the true DGP is an ARIMA(p,l,q) with a

large negative MA root, the autoregressive sieve bootstrap (ARSB) ADF test over

rejects almost as much as the asymptotic one. This is, of course, due to the fact

that such MA roots coincide with very strong AR( 00) forms which are difficult to

approximate with a finite order autoregression. Thus, sieve models that explicitly

take MA parts into account may solve this problem at least partially.

It is somewhat surprising that absolutely no effort has been made for the develop

ment of sieve bootstrap methods based on MA and ARMA models. This most likely

depends on the fact that estimating such models requires more effort than is needed

to estimate an AR. However, the apparition of new estimation techniques such as the

analytical indirect inference methods of Galbraith and Zinde-Walsh (1994, 1997), has

changed this. These methods, which de duce parameter estimates for an MA(q) or an

ARMA(p,q) model from a simple AR(k), are simpler and faster to implement than

maximum likelihood. Thus, their development makes moving average sieve boot

strap (MASB) and autoregressive moving average sieve bootstrap (ARMASB) more

practical. We will formally introduce such sieves in the next chapter.

21

1.6 Bootstrap and bias correction

Another reason why the bootstrap may fail to provide accurate inference is estima

tion bias. Indeed, as we mentioned ab ove , one condition for it to work well is that

the bootstrap samples should be able to mimic the original sample's features. This

requires that the parameters of the bootstrap DGP have values close to those of the

original DGP. Rence, bootstrap inference based on biased estimators is likely to be

inaccurate. There exist several bias correction techniques which may be used to ob

tain more precise estimates of the null DGP. In chapter 4, we review sorne of those

that can be applied to time series models and introduce a new bias reduction tech

nique based on the GLS transformation matrix. We then use bias corrected and bias

reduced estimators to build bootstrap samples and carry out unit root tests.

1. 7 Conclusion

ln this chapter, we have introduced the widely used ADF test for the unit root

hypothesis and have pointed out its problems under the null hypothesis when the

data is generated by a general linear process. We have also introduced the basics of

bootstrap testing and described specialized forms of the bootstrap that can be used

in these situations. The asymptotic and finite sam pIe properties of those methods

have been studied by several authors and we have reported their main conclusions.

Among these methods is the sieve bootstrap, which uses finite order AR models to

approximate generallinear processes. We propose to use finite or der MA and ARMA

models instead of AR ones to conduct sieve bootstrap inference.

Bootstrapping unit root tests sometimes yields disappointing results. We argue

that this may be due to the fact that bootstrap DGPs are sometimes based on biased

estimators. We therefore propose to use bias correction and bias reduction methods

to obtain more accurate finite sample inferences.

22

Chapter 2

Invariance Principle and Validity

of Sieve Bootstrap ADF Tests

2.1 Introduction

In this chapter, we der ive the invariance principles necessary to justify the use of MA

sieve bootstrap (MASB) and ARMA sieve bootstrap (ARMASB) samples to carry out

bootstrap unit root hypothesis tests. These results are often referred to as functional

central limit theorems because they extend standard asymptotic distribution theory,

which is applicable to simple random variables, to more complex mathematical objects

such as random functions. For a very accessible introduction to these topics, see

Davidson (2006). We also show that ADF tests based on MASB and ARMASB

samples are asymptotically valid.

Establishing invariance princip le results for sieve bootstrap procedures is a rela

tively new strand in the literature and, at the time of writing this, and to the author's

knowledge, only two attempts have been made. First, Bickel and Bühlmann (1999)

derive a bootstrap functional central limit theorem under a bracketing condition for

23

the AR sieve bootstrap (ARSB). Second, Park (2002) derives an invariance principle

for the ARSB. This latter approach is more interesting for our present purpose be

cause Park (2002) establishes the convergence of the bootstrap partial sum pro cess to

the standard Brownian motion, and most of the unit-root-tests asymptotic theory is

based on such processes. Further, as we will see below, his assumptions are standard

ones in time series econometrics.

We then use these results to show that the ADF bootstrap test based on the MASB

and ARMASB is asymptotically valid. A bootstrap test is said to be asymptotically

valid, or consistent, if it can be shown that its large sample distribution under the

null is the test's asymptotic distribution. Consequently, we will seek to prove that

MASB and ARMASB ADF tests statistics follow the DF distribution asymptotically

under the null.

The present chapter is organised as follows. The next section discusses bootstrap

invariance principles for partial sum pro cesses built from sets of i.i.d. random vari

ables. It is very similar to section 2 in Park (2002) and the results presented there

form the basis of the theory presented here. Section 3 introduces the MASB and

establishes an invariance principle for it. Section 4 introduces the ARMASB and, by

extending the results of section 3 and Park (2002), establishes an invariance princi

pIe. The asymptotic validity of the sieve bootstrap ADF tests is proved in section 5.

Section 6 concludes.

2.2 General bootstrap invariance princip le

Let {êt}r=l be a sequence of iid random variables with finite second moment a 2 .

Consider a sample of size n and define the partial sum process:

1 [nt)

Wn(t)= r,;:;Lêk av n k=l

24

where [y 1 denotes the largest integer smaller or equal to y and t is an index such

that ~ ::s t < *, where j = 1,2, ... n is another index that allows us to divide the

[0,1] interval into n + 1 parts. Thus, Wn(t) is a step function that converges to a

random walk as n -+ 00. AIso, as n -+ 00, Wn(t) becomes infinitely dense on the

[0,1] interval. By the classical Donsker's theorem, we know that

where W is the standard Brownian motion. The Skorohod representation theorem

tells us that there exists a probability space (0, F, P), where 0 is the space containing

aIl possible outcomes, F is a a-field and P a probability measure, that supports W

and a pro cess W~ such that W~ has the same distribution as W n and

W' a.s. W n -+ .

Indeed, as demonstrated by Sakhanenko (1980), W~ can be chosen so that

(2.1)

(2.2)

for any <5 > 0 and r > 2 such that Ejctjr < 00 and where Kr is a constant that

depends on r only. The result (2.2) is often referred to as the strong approximation.

Because the invariance principle we seek to establish is a distributional result, we do

not need to distinguish W n from W~. Consequently, because of equations (2.1) and

(2.2), we say that W n ~ W, which is stronger than the convergence in distribution

implied by Donsker's theorem.

Now, suppose that we can obtain an estimate of {Ct}~=l' which we will denote as

{€t}~=l' from which we can draw bootstrap samples of size n, denoted as {C;}~=l' If

we suppose that n -+ 00, then we can build a bootstrap probability space (0*, F*, P*)

which is conditional on the realization of the set of residuals {€t}~l from which the

bootstrap random variables are drawn. What this means is that each bootstrap draw

ing {C;}r=l can be seen as a realization of a random variable defined on (0*, F*, P*).

In aIl that follows, the expectation with respect to this space (that is, with re

spect to the probability measure P*) will be denoted by E*. For example, if the

25

bootstrap samples are drawn from {(Et - En)} f=l' then E* é; = 0 and E* é;2 = â; =

(lin) L:~1 (Et - En)2. Of course, whenever the EtS are residuals from a linear regres

sion model with a constant, En = 0 so that E*é;2 = â; = (lin) L:~=1 iF. Also, ~, ~ and a~* will be used to denote convergence in distribution, in probability and almost

sure convergence of the functionals of the bootstrap samples defined on (0*, F*, P*).

Further, following Park (2002), for any sequence of bootstrapped statistics {X~} we

say that X~ ~ X a.s. if the condition al distribution of { X~} weakly converges to

that of X a.s. on all sets of {Et}~l' In other words, if the bootstrap convergence in

distribution (~) of functionals of bootstrap samples on (0*, F*, P*) happens almost

surely for all realizations of {tt}~l' then we write ~ a.s.

Let {éa~l be a realization from a bootstrap probability space. Define

1 [nt]

W~(t) = A r,;; L ék' (Jnyn k=l

Once again, by Skorohod's theorem, there exists a probability space on which a

Brownian motion W* is supported and on which there also exists a pro cess W~'

which has the same distribution as W~ and such that

(2.3)

for 8, r and Kr defined as before. Because W~' and W~ are distributionally equivalent,

we will not distinguish them in all that follows. Equation (2.3) allows us to state the

following theorem, which is also theorem 2.2 in Park (2002)

Theorem (Park 2002, theorem 2.2, p. 473) If E*lé;lr < 00 a.s. and

(2.4)

d* for some r > 2, then W~ ----t W a.s. as n ----t 00.

This result comes from the fact that, if condition (2.4) holds, then equation (2.3)

implies convergence in probability over the bootstrap probability space which, as

26

usual, implies convergence in distribution that is, W~ ~ W* a.s. Since the distribu

tion ofW* is independent of the set ofresiduals {€d~u we can equivalently say W~ ~

W a.s. Hence, whenever condition (2.4) is met, the invariance principle follows. In

other words, Skorohod implies that there exists a pro cess W~' distributionaIly equiv

aIent to W~ and Sakhanenko implies that it can be chosen so as to satisfy equation

(2.3). Of course, this theorem is only valid for bootstrap samples drawn from sets

of i.i.d. random variables. Nevertheless, Park (2002) uses it to prove an invariance

princip le for the AR sieve bootstrap. In the next two sections, we do essentiaIly the

same thing for the MA and ARMA sieve bootstraps.

2.3 Invariance principle for MA sieve bootstrap

Let us consider a general linear process:

(2.5)

where 00

7r(z) = L 7rkZk k=O

and the CtS are i.i.d. randorn variables. Moreover, let 7r(z) and Ct satisfy the foIlowing

assurnptions:

Assurnption 2.1.

(a) The Ct are i.i.d. randorn variables such that E(ct)=O and E(lctn< 00 for sorne

r > 4.

(b) 7r(z) =1= 0 for aIl Izl ::; 1 and ~k::O Iklsl7rkl < 00 for sorne s ;::: 1.

These are usual assurnptions in stationary tirne series analysis. Notice that (a)

along with the coefficient surnrnability condition in sures that the pro cess is weakly

stationary. On the other hand, the assurnption that 7r(z) =1= 0 for aIl Izl ::; 1 is

27

neccssary for the process to have an AR( 00) form. See Chang and Park (2003) for a

discussion of these assumptions.

The MASB consists of approximating equation (2.5) by a finite or der MA(q) model:

Ut = 7flêq,t-l + 7f2êq,t-2 + ... + 7fqê q,t-q + êq,t (2.6)

where q is a function of the sample size. We believe that the analytical indirect

inference estimator for MA models introduced by Galbraith and Zinde-Walsh (1994),

henceforth GZW (1994), is the most appropriate one for this task. There are several

reasons for this. The first is computation speed. Consider that in practice, one

often uses information criteria such as the AIC and BIC to choose the order of the

MA sieve model. These criteria make use of the value of the loglikelihood at the

estimated parameters, which implies that, if we want q to be within a certain range,

say ql ::; q ::; q2, then we must estimate q2 - ql models. With maximum likelihood,

this requires us to maximize the log likelihood q2 - ql times. With GZW (1994)'s

method, we need only estimate one model, namely an AR(f) , from which we can

deduce an at once the parameters of an the q2 - ql MA( q) models. We then only need

to evaluate the loglikelihood function at these parameter values and choose the best

model accordingly. This is obviously much faster then maximum likelihood.

Second, the simulations of GZW (1994) indicate that their estimator is more ro

bust to changes in q. For example, suppose that the true model is MA(oo) and that

we consider approximating it by either a MA(q) or a MA(q + 1) model. If we use

the GZW (1994) method, for fixed J, going from a MA(q) to a MA(q + 1) specifi

cation does not alter the values of the first q coefficients. On the other hand, these

q estimates are likely to change very much if the two models are estimated by max

imum likelihood, because this latter method strongly depends on the specification.

Therefore, bootstrap samples generated from parameters estimated using the GZW

estimator are likely to be more robust to the choice of q than samples generated using

maximum likelihood estimates.

28

Another reason to prefer GZW (1994)'s estimator is that, according to their sim

ulations, it tends to yield fewer non-invertible roots, which are not at aIl desirable

here. FinaIly, it allows us to determine, through simulations, which sieve bootstrap

method yields more precise inference for a given quantity of information (that is, for

a given lag length).

Approximating an infinite order linear pro cess by a finite dimension model is an

old topic in econometrics. Most of the time, finite f -order autoregressions are used,

with f increasing as a function of the sample size. The classical reference on the

subject is Berk (1974) who proposes to increase f so that P /n --+ 0 as n --+ 00 (that

is, f = o( n 1/3)). This assumption is quite restrictive because it do es not allow f to

increase at the logarithmic rate, which is what happens if we use AIC or BIC. Here,

we make the following assumption about q and f:

Assumption 2.2.

Let q and f be, respectively, the orders of the approximating MA sieve model and

of the AR model used to estimate it via analytical indirect inference. Then, we

assume that q --+ 00 and f --+ 00 as n --+ 00 and q = a ((n/log (n))1/2) and f =

a ((n/log (n) )1/2) with f > q.

The reason for this choice is closely related to lemma 3.1 in Park (2002) and the

reader is referred to the discussion following it. Here, we limit ourselves to pointing

out that this rate is consistent with both AIC and BIC, which are commonly used

in practice. The restriction that f > q is necessary for the computation of the GZW

(1994) estimator.

The bootstrap samples are generated from the DGP:

(2.7)

where the 7rq ,i, i = 1,2, ... q are estimates of the true parameters 1fi, i = 1,2, ... and the

ct are drawn from the EDF of (tt-tn ), that is, from the EDF of the centered residuals

29

of the MA(q) sicvc. We will now cstablish an invariance princip le for the partial sum

pro cess of u; by considering its Beveridge-Nelson decomposition and showing that it

converges almost surely to the same limit as the corresponding partial sum pro cess

built with the original Ut. First, consider the decomposition of Ut:

where

and

00

Ut = L 7rkCt-k k=O

00

7rk = L 7ri· i=k+1

N ow, consider the partial sum process

1 [nt] 1 [nt] 00 [( 00 ) 1 = ;;:; L 7r(1)ct + ;;:; L L L 7ri (Ct-k-l - Ct-k)

V n k=l V n k=l k=O i=k+l

hence,

V n ( t) = (a7r (1) ) W n (t) + Jn (uo - U[nt]).

Under assumption 2.1, Phillips and Solo (1992) show that

Therefore, applying the continuous mapping theorem, we have

On the other hand, from equation (2.7), we see that u; can be decomposed as

where q

7T(1) = 1 + L 7Tq ,k

k=l

30

It therefore follows that we can write:

V*(t) 1 ~ * (A A (l))W* 1 (-* -*) n = r;;; L..J Ut = O'n7rn n + r;;; ua - u[nt] yn k=l yn

d* In or der to establish the invariance principle, we must show that V~ ---t V =

(O'7f(l))Wa.s. To do this, we need 3 lemmas. The first one shows that Ô"n and 7rn (l) d*

converge almost surely to 0' and 7f(1). The second demonstrates that W~(t) ---t W

a.s. Finally, the last one shows that

Pr*{ max In-1/ 2u*1 > c5} ~ 0

l::;t::;n t

for all c5 > 0, which is equivalent to saying that

max In- 1/

2ukl ~ o. a.s. l::;k::;n

(2.8)

and is therefore the bootstrap equivalent of the result of Philips and Solo (1992).

These 31emmas are closely related to the results of Park (2002) and their counterparts

in this paper are identified for reference.

Lemma 2.1 (Park 2002, lemma 3.1, p. 476)

Let assumptions 2.1 and 2.2 hold. Then,

for large n

Ô"~ = 0'2 + 0(1) a.s.

7rn (l) = 7f(1) + 0(1) a.s.

Proof: see the appendix.

31

(2.9)

(2.10)

(2.11)

Lemma 2.2 (Park 2002, lem ma 3.2, p. 477).

L t t · 2 1 d 2 2 h Id Th E*I *Ir and n1- rj2 E*lc*t Ir ~. 0 e assump IOns . an . o. en, Et < 00 a.s. ç,

Proof: see the appendix.

d* Lemma 2.2 proves that W~(t) --t Wa.s. because it shows that condition (2.4) holds

almost surely.

Lemma 2.3 (Park 2002, theorem 3.3, p. 478).

Let assumptions 2.1 and 2.2 hold. Then, equation (2.8) holds.

Proof: see the appendix.

With these 3 lemmas, the MA sieve bootstrap invariance principle is established.

It is formalized in the next theorem.

Theorem 2.1.

Let assumptions 2.1 and 2.2 hoid. Then by Iemmas 2.1, 2.2 and 2.3,

d* V~ --t V = (O"7r(l))W a.s.

2.4 Invariance principle for ARMA sieve bootstrap

We now establish an invariance principle for the ARMASB. It turns out to be a simple

matter of combining the results of the previous section to those of Park (2002). The

ARMASB procedure consists of approximating the above generallinear process (2.5)

by a finite or der ARMA(p,q) model:

(2.12)

32

where.e = p+q denotes the total number of parameters and is, of course, a function of

the sample size. As before, and for similar reasons, we propose that the parameters be

estimated using an analytical indirect inference method suit able for ARMA models.

Such a method has been proposed by Galbraith and Zinde-Walsh (1997). Rence, in

addition to p and q, we must also specify the or der of the approximating autoregression

from which the ARMA parameter estimates are deduced. As before, we let f denote

this order. Then, we make the following assumptions:

Assumption 2.3

Both.e and f go to infinity at the rate 0 ((njlog(n))1/2) and f > .e.

Notice that we do not require that both p and q go to infinity simultaneously. Rather,

we require that their sum does. Thus, the results that follow ho Id even if p or q is

held fixed while the sam pIe size increases, as long as the sum increases at the proper

rate. As before, the restriction that f > .e is required for the GZW (1997) estimator

to be consistent. The bootstrap samples are generated from the DGP:

(2.13)

where the âe,k and 1re,k can be combined using analytical indirect inference equations

to form consistent estimates of the true parameters of either the infinite order AR

or MA representation of u; and the c; are drawn from the EDF of (Êt - gn)~=l' that

is, from the empirical distribution of the centered residuals of the fitted ARMA(p,q).

N ext, we need to build a partial sum pro cess V~ of u;. The easiest way to do this

is to consider either the AR( (0) or the MA( (0) form of the ARMA(p,q) model and

build V~ based on this representation. Let us consider the MA( (0) form of u;, which

we define as

(2.14)

33

where êe 1 = ire 1 + tic 1, êe 2 = êe l tie 1 - tic 2 - ire 2 and so forth. Then, , , , , " , ,

V*(t) 1 ~ * (A (}A (1))W* 1 (-* -*) n =. r;;; L.J Ut = (}n n n + r;;; U o - u[nt] yn k=1 yn

(2.15)

where

and 00

Bk = L êi .

i=k+l

and where Ô"n is the estimated variance of the residuals of the ARMA(p,q) sieve. Then,

we need to show that V~(t) ~V a.s. This, as before, can be done through proving 3

results, which are simple corollaries of lemmas 2.1, 2.2 and 2.3 of the present chapter

and lemmas 3.1 and 3.2 as well as theorem 3.3 of Park (2002). Recall that 7rk denotes

the k th parameter of the true MA( 00) form of the process Ut.

Corollary 2.1.

Under assumptions 2.1 and 2.3,

for large n. Also,

Proof: see appendix.

Corollary 2.2.

max lêCk - 7rkl = 0 (1) a.s. l::ç;kg ,

Ô"~ = (}2 + 0(1) a.s.

ên (1) = 7r(1) + 0(1) a.s.

(2.16)

(2.17)

(2.18)

Under assumptions 2.1 and 2.3, the ARMA sieve bootstrap errors' partial sum

process converges in distribution to the standard Wiener pro cess almost surely over

all bootstrap samples as n goes to infinity:

d* W~ -+ Wa.s.

34

Proof: see appendix.

Corollary 2.3

Under assumptions 2.1 and 2.3,

for an 6 > 0 and u; generated from the ARMA(p,q) sieve bootstrap DGP.

Proof: see appendix.

These three results are sufficient to prove the invariance princip le of the ARMA

sieve bootstrap partial sum pro cess. This is formalized in the next theorem.

Theorem 2.2 Let assumptions 2.1, 2.2 and 2.3 hold. Then by corollaries 2.1, 2.2

and 2.3,

d* V~ -t V = (0"7r(l))W a.s.

2.5 Asymptotic Validity of MASB and ARMASB ADF tests

Consider a time series Yt with the following DGP:

Yt = exYt-l + Ut (2.19)

where Ut is the general linear pro cess described in equation (2.5). We want to test

the unit foot hypothesis against the stationarity alternative (that is, Ho : ex = 1

against Hl : ex < 1). This test is frequently conducted as a t-test in the so called

ADF regression, first proposed by Said and Dickey (1984):

p

Yt = exYt-l + L exkL:lYt-k + ep,t k=l

35

(2.20)

where p is chosen as a function of the sample size. A large literature has been

devoted to selecting p, see for example, Ng and Perron (1995, 2001). As noted in

the introduction, deterministic parts such as a constant and a time trend are usually

added to the regressors of (2.20). Chang and Park (CP) (2003) have shown that the

test based on this regression asymptotically follows the DF distribution when Ho is

true under very weak conditions, including assumptions 2.1 and 2.2. Let yt denote

the bootstrap pro cess generated by the following DGP: t

* ""' * Yt = L..J uk k=l

and the ut = !lyt are generated as in (2.7). The bootstrap ADF regression equivalent

to regression (2.20) is p

yt = ayt-l + L ak!lyt_k + et· (2.21) k=l

Let us suppose for a moment that !lyt has been generated by an AR(p) sieve

bootstrap DGP: p

!lyt = L âp,k!lyt_k + ct k=l

Then, letting a = 1 in (2.21), we see that the true parameters of this equation are

the âp,kS and that its the errors are identical to the errors driving the bootstrap DGP.

This is a convenient fact which CP (2003) use to prove the consistency of the ARSB

ADF test based on this regression. If however the yt are generated by the MA(q)

or ARMA(p,q) sieves described ab ove , then the errors of regression (2.21) are not

identical to the bootstrap errors under the null because the AR(p) approximation

captures only a part of the correlation structure present in the MA(q) or ARMA(p,q)

process. It is nevertheless possible to show that they will be equivalent asymptotically,

that is, that c; = et + 0(1) a.s. This is done in lemma Al, which can be found in the

appendix.

Let X;,t = (!lyt-l' !lyt-2' ... , !lyt_p) and define:

(t X;,tX;,t T) -1 (t X;,t C;) t=l t=l

n ( n ) * * * * *T An = LYt-lCt - LYt-lXp,t t=l t=l

36

B~ = t Y:-1 2 - (t Y:-1 X;,t T) (t X;,tX;,t T) -1 (t X;,tY:-1) t=l t=l t=l t=l

Notice that A~ is defined as a function of é;, not et. Then, it is easy to see that the

t-statistic computed from regression (2.21) can be written as:

* â~ - 1 () Tn = (A) + 0 1 a.s.

s a~

for large n and where â~ - 1 = A~B~-l and s(â~)2 = â;B~-l.

The equality is asymptotic and almost surely holds because the residuals of the ADF

regression are asymptotically equal to the bootstrap errors, as shown in lemma Al.

This also justifies the use of the estimated variance â;. Note that in small samples,

it may be preferable to use the estimated variance of the residuals from the ADF

regression, which is indeed what we do in the simulations. We must now address the

issue of how fast p is to increase. For the ADF regression, Said and Dickey (1984)

require that p = o(nk ) for sorne 0 < k ::; 1/3. But, as argued by CP (2003), these

rates do not allow the logarithmic rate. Hence, we state new assumptions about the

rate at which q, g and p (the ADF regression order) increase:

Assumption 2.2.'

q = cqnk, g = ccnk p = cpnk where cq, Cc and cp are constants and l/rs < k < 1/2.

Assumptions 2.2 and 2.3 can be fitted into this assumption for appropriate values

of k. AIso, notice that assumption 2.2' imposes a lower bound on the growth rate of

p, g and q. This is necessary to obtain almost sure convergence. See CP (2003) for

a weaker assumption that allows for convergence in probability. Several preliminary

and quite technical results are necessary to prove that the bootstrap test based on the

statistic T~ is consistent. To avoid rendering the present exposition more laborious

than it needs to be, we relegate them to the appendix (lemmas A2 to A5). For now,

let it be sufficient to say that they extend to the MA and ARMA sieve bootstrap

samples sorne results established by CP (2003) for the AR sieve bootstrap. In turn,

sorne of CP (2003)'s lemmas are adaptations of identical results in Berk (1974) and

37

An, Chen and Hannan (1982).

2.5.1 Consistency of MASB ADF test

In or der to prove that the MA sieve bootstrap ADF test is consistent, we now prove

two results on the elements of A~ and B~. These results are stated in terms of

bootstrap stochastic orders, denoted by 0; and 0;, which are defined as follows.

Consider a sequence of non-constant numbers {en}. Then, we say that X~ = 0; (cn)

a.s. or in p if Pr* {IX~/ Cn 1 > E} -+ 0 a.s. or in p for any E > O. Similarly, we say that

X~ = O(cn ) if for every E > 0, there exists a constant M > 0 such that for alllarge n,

Pr*{IX~/cnl > M} < E a.s or in p. It follows that if E*IX~I -+ 0 a.s., then X~ = 0;(1)

a.s. and that if E*IX~I = 0(1) a.s., then X~ = 0;(1) a.s. See CP (2003), p. 7 for a

slightly more elaborated discussion.

Lemma 2.4. Under assumptions 2.1 and 2.2', we have

h * ~t * W ere w t =L..k=l ck'

Proof: see appendix.

1 ~ * 2 A ( )2 1 ~ * 2 *() 2" ~ Yt-1 = 7rn 1 2" ~ wt- 1 + op 1 a.s. n t=l n t=l

Lemma 2.5. Under assumptions 2.1 and 2.2' we have

(

n )-1 ~ L:x;,tX;,tT = 0;(1) a.s. t=l

II~ X;,tY;-lll = 0;(np1/2) a.s.

38

(2.22)

(2.23)

(2.24)

(2.25)

(2.26)

Proof: see appendix.

We can place an upper bound on the absolute value of the second term of A~.

This is:

But by lemma 3.5, the right hand side is O;(n-1 )O;(npl/2)O;(n1/ 2pl/2) which gives

O;(n1/2p). Now, using the results of lemma 3.4, we have that:

-lA* A (1) 1 ~ * * *(1) n n = 7rn - ~ Wt-lCt + op a.s. n t=l

We can further say that

-2B* A (1)2 1 ~ * 2 *(1) n n = 7rn 2" ~ w t - 1 + op a.s. n t=l

because n-2 times the second part of B~ is O;(n-1). Therefore, the T~ statistic can

be seen to be: 1 ",n * *

7,* = ri L.".t=l W t - 1Ct + *(1) as

n 1/2 Op ..

()' (~2 l:~=l wt_1 2)

recalling that W;=l:t=l cZ, it is then easy to use the results of chapter 2 along with

the continuous mapping theorem to deduce that:

1 n d* 101 - L W;_l c; -+ WtdWt a.s. n t=l 0

1 ~ * 2 d* 101 2 2" ~ W t- 1 -+ Wtdt a.s. n t=l 0

under assumptions 1 and 2'. We can therefore state the following theorem.

Theorem 2.3. Under assumptions 1 and 2', we have

d* 7,* -+ n fol WtdWt

(J~ W;dtf/2

39

a.s.

which establishes the asymptotic validity of the MASB ADF test.

2.5.2 Consistency of ARMASB ADF tests

It is now very easy to prove the asymptotic validity of ADF tests based on the AR

MASB distribution. It indeed suffices to show that results similar to those presented

in the last subsection hold for the ARMASB DG P. In or der to do this, we make use of

the MA(oo) form of the ARMASB DGP (see equation 2.14 above) and its Beveridge

Nelson decomposition. Then, we can state the following corollaries of lemmas 2.4 and

2.5.

Corollary 2.4. Vnder assumptions 2.1 and 2.2', we have

1 ~ * * ()A ( ) 1 ~ * * *(1) - LJ Yt-1 é t = n 1 - LJ W t _ 1é t + op a.s. n t=l n t=l

1 ~ * 2 ()A ( )2 1 ~ * 2 *() 2 LJYt-1 = n 1 2 LJ wt- 1 + op 1 a.s. n t=l n t=l

Proof: see appendix.

Corollary 2.5. Vnder assumptions 2.1 and 2.2' we have

Proof: see appendix.

(

n )-1 ~ L X;,tX;,t T = 0; (1) a.s. t=l

II~X;,tY;-lll = 0;(np1/2) a.s.

II~ X;,té;11 = 0;(n1/2p1/2) a.s.

40

(2.27)

(2.28)

(2.29)

(2.30)

(2.31)

Theorem 2.4 evidently follows.

Theorem 2.4. Under assumptions 2.1 and 2.2', we have

This establishes the asymptotic validity of the MASB ADF test.

2.6 Conclusion

Invariance principles are a necessary tool for the derivation of the asymptotic prop

erties of unit root tests. In this chapter, we have established such a result for partial

sum pro cesses built from data generated by either an MA or an ARMA sieve boot

strap DGP. Then, we have established the asymptotic validity of ADF tests based

on MASB and ARMASB distributions. This justifies the use of these methods in

practical applications. However, it does not imply that doing so increases the test's

accuracy. At the time of writing this, no formaI proof of the existence of potential

asymptotic refinements resulting from utilizing sieve bootstrap methods with 1(1)

variables has been devised. Nevertheless, simulation results presented in the next

chapter indicate that such refinements may exist.

41

Chapter 3

Simulations

3.1 Introduction

We now present a set of simulations designed to illustrate the extent to which the

proposed MASB and ARMASB schemes improve upon the usual ARSB. For this

purpose, 1(1) data series were generated from the model described by equation (2.19)

with errors generated by a general linear model of the class described in equation

(2.5) with NID(O,l) innovations. Several DGPs were used for this purpose and each

one is described below.

Recently, Chang and Park (2003) (CP 2003 hereafter) have shown, through Monte

Carlo experiments, that the ARSB allows one to reduce the ADF test's error in re

jection probability (ERP), which is defined as the difference between the probability

of rejecting a true null hypothesis and the nominal level, but not to eliminate it

altogether. Such results are generally interpreted as evidence of the presence of as

ymptotic refinements in the sense of Beran (1987), even though no theoretical pro of

exists to date. Their simulations however show that the AR sieve bootstrap loses

42

sorne of its accuracy as the dependence of the error process increases. This is, of

course, not a surprise because the longer it takes for the dependence to decrease, the

larger is the difference between the correlation structure of the estimated AR(p) sieve

and that of the true AR( 00) process, and therefore, the greater the difference between

the true and the bootstrap DGPs. As we will see shortly, the same fate befalls both

the MA and ARMA sieve bootstrap.

Most of the existing literature on the rejection probability of unit root tests uses,

as an illustration of how bad things can get, the case where the unit root process's first

difference is stationary and invertible with a moving average root near the unit circle.

The simplest such model is the MA(l) with a parameter close to -1. This typically

results in a large ERP of the asymptotic ADF test because of the near cancellation

of the MA root with the autoregressive unit root. Classical references on this are

Schwert (1989) and Agiakoglou and Newbold (1992). Evidently, this setup is not

adequate in the present case because an MA(l) bootstrap DGP would be a correctly

specified model of the original data's correlation structure, so that the resulting test

would not be a sieve bootstrap test any longer. Further, to base a simulation study

on only one DGP creates the risk of obtaining results that are proper to this DGP

alone. Hence, our simulations use several DGPs which will be introduced later.

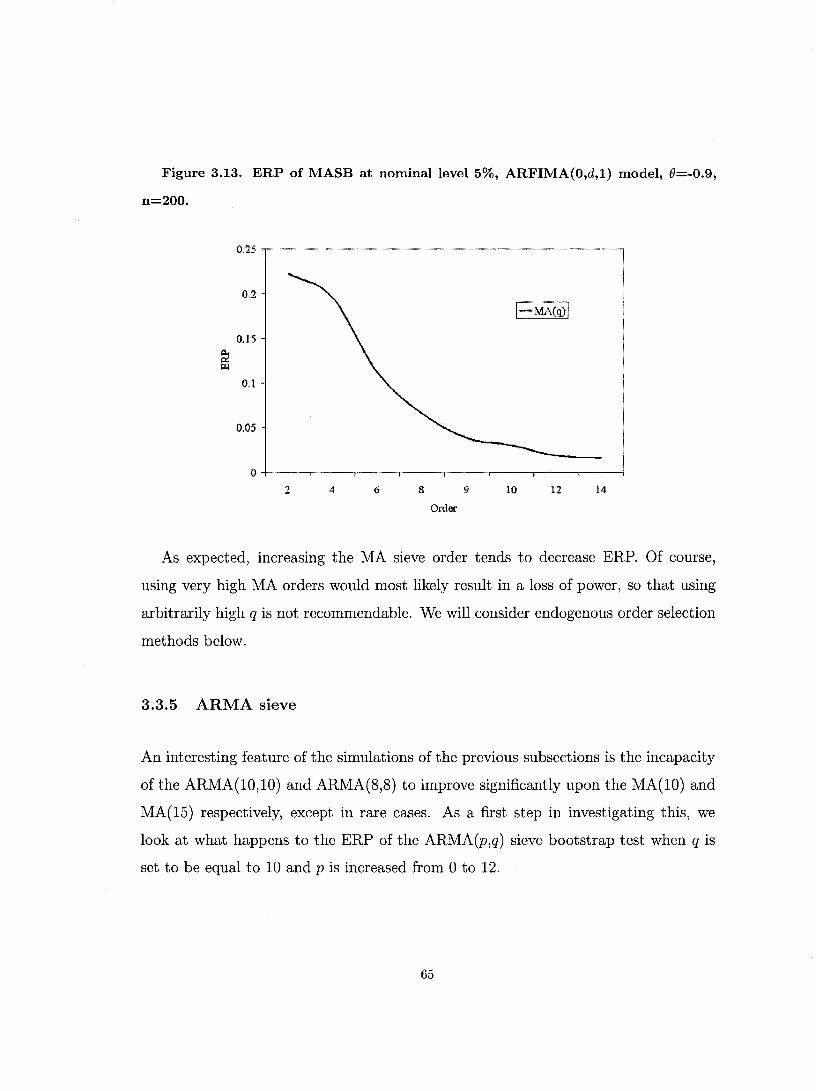

An interesting feature of the simulations presented below is the fact that the ADF

tests based on MA(q) and ARMA(p,q) sieves often widely outperform tests based

on ordinary AR(p), but never the reverse. In other words, bootstrap samples based

on MA(q) or ARMA(p,q) approximations sometimes bring substantial accuracy gains

over the AR(p) sieve in terms of ERP under the null, while every time the AR(p)

sieve performs better than the other two, the difference is not large. We argue that

this is so because the residuals of the ADF regression based on the ARSB samples

are roughly uncorrelated, as long as the order of the AR(p) sieve is the same as the

order of the ADF regression, which is commonly the case, while the residuals of the

43

ADF regression estimated on the MASB and ARMASB samples are correlated, and

their correlation structure is similar to that of the original test regression's residuals.

Simulation evidence seems to support this point of view.

These observations lead us to propose two modifications to the ARSB ADF test.

Firstly, we propose to use fewer lags in the ARSB ADF regression than in the ARSB

model itself. This effectively creates correlated residuals in the test regression and

therefore shifts the test statistics's distribution to the left. Secondly, we propose the

use of a modified version of the fast double bootstrap. Simulations indicate that both

these ideas yield improvements over the usual ARSB ADF test.

We also observe that situations in which the MASB and ARMASB tests greatly

outperform the asymptotic and ARSB tests are those when the underlying DGP

contains a strong, negative moving average root, which results into near cancellation

of the autoregressive unit root. It therefore appears natural that the MASB and

ARMASB would bear important ameliorations over the ARSB and asymptotic tests

because the first two explicitly model this MA root while neither of the latter does.

The rest of this chapter is organized as follows. Section 2 describes the met ho dol

ogy used to carry out the different bootstrap ADF tests. Section 3 discusses simulation

results for several DGPs and studies the characteristics of the different sieve models

utilized. Section 4 offers an explanation for the poor performances of the ARSB and

proposes a simple modification designed to increase its accuracy under the null. Along

the same line, section 5 introduces a modified fast double bootstrap and studies it

through simulations. Section 6 concludes.

44

3.2 Methodological issues

In order to obtain consistent test statistics, one must make sure that the parameters

used in the construction of the bootstrap DG P are consistent estimates under the

null. This is easily achieved in the present case by estimating the appropriate time

series model (ie: AR, MA or ARMA) of the first difference of Yt using any consistent

method. lndeed, whenever a = 1, (2.19) simply becomes

Yt - Yt-l = Ut,

which is our null hypothesis. Lemma 2.1 and corollary 2.1 discuss consistency of

the parameters of the MA and ARMA sieve while consistency of the parameters of

the AR sieve is shown by Berk (1974) and Park (2002). Bootstrap ADF tests are

conducted as follows:

1. Estimate the ADF test regression on the original data and compute the ADF test

statistic. In aIl that follows, we have used the ADF regression containing a constant

and no deterministic time trend. Thus, the statistic we compute is the one commonly

called Tc.

2. Estimate the sieve bootstrap model. This is do ne by fitting either an AR(p),

an MA(q) or an ARMA(p,q) to t::..Yt. Notice that this implicitly imposes the null

hypothesis. In order to draw bootstrap samples, we need to create the residuals

series. For the AR sieve, this is: p

Êt = .6..Yt - L (Xp,kt::..Yt-k k=l

For the MA and ARMA sieves, this is:

where lÎIt is the tth row of the triangular GLS transformation matrix for MA(q) or

ARMA(p,q) pro cesses evaluated at the parameter estimates (see the discussion below

45

and chapter 4).

3. Draw bootstrap errors (Er) from the EDF of the recentered residuals (Êt-~ 2:~=1 Êt ).

As is well known, OLS residuals under-estimate the error terms so that it may be

desirable to rescale the recentered residuals by a factor of ((n~f.») 1/2, where f is the

number of parameters.

4. Generate bootstrap samples of Yt. This first requires that we generate the bootstrap

first difference process. For the AR sieve bootstrap: p

~Y: = L âp,k~Y:_k + Et, k=l

for the MA sieve bootstrap:

for the ARMA sieve bootstrap: q p

~Y: = L 7rq,kEt_k + L âp,k~Y:-k + Et. k=l k=l

This requires some sort of initialisation for the ~Y; series. We postpone this discussion

for now. Then, we generate bootstrap samples of Yt: y; = 2:~=1 ~Y;

5. Compute the bootstrap T~i ADF test based on the bootstrap ADF regression:

p

y: = ao + aY:_1 + L ak~Y:_k + et k=l

where p is the same as above.

6. Repeat steps 2 to 4 B times to obtain a set of B ADF statistics T~i' i = 1,2, ... B.

The p-value of the test is defined as:

P* = ~ tJ(T~i < Tc) i=l

where Tc is the original ADF test statistic and JO is the indicator function which is

equal to 1 every time the bootstrap statistic is smaller than Tc and 0 otherwise. The

46

null hypothcsis is rcjected at the 5 percent level whenever P* is smaller than 0.05.

Repeating this B times aIlows us to obtain a number of test statistics, aIl computed

under the nuIl hypothesis, which can therefore be used to estimate the finite sample

distribution of the test and conduct inferences. Of course, the larger Bis, the more

precise this estimate is. Further, for a test conducted at nominallevel Œ, B should be

chosen so that (B+1)Πis an integer, see Dufour and Kiviet (1998) or Davidson and

MacKinnon (2004), chapter 4.

In aIl the simulations reported here, the AR sieve and the ADF regressions are

computed using OLS. Further, aIl MA and ARMA models were estimated by the an

alytical indirect inference methods of GZW (1994 and 1997). The bootstrap samples

are generated recursively, which requires sorne starting values for D..y;. There are

sever al ways to do this. The important thing is for the bootstrap sam pIe values not

to be infiuenced by whatever starting values we assume. In what follows, we have set

the first p or q, whichever is larger, values of D..y; equal to the first p or q values of

D..Yt and generated samples of n + 100 + p (or q) observations. Then, we have thrown

away the first 100 + p (or q) values and used the last n to compute the bootstrap

tests. This effectively removes the effect of the initial values and insures that D..Yt is

a stationary time series.