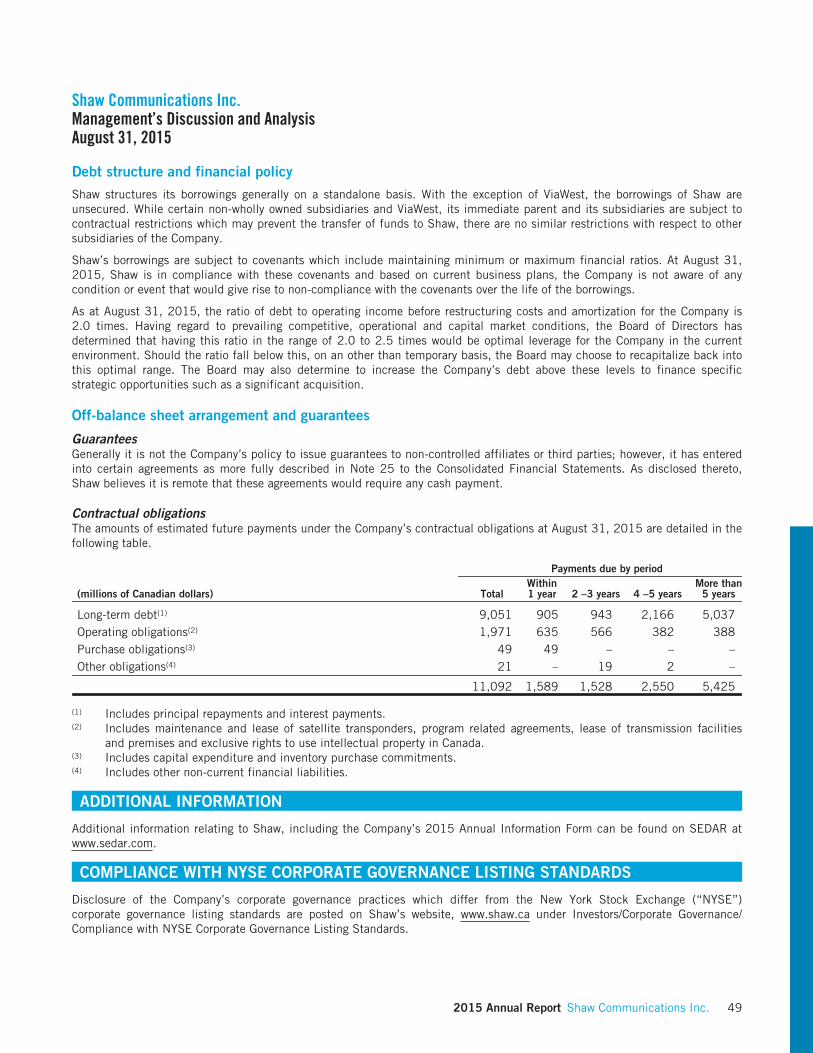

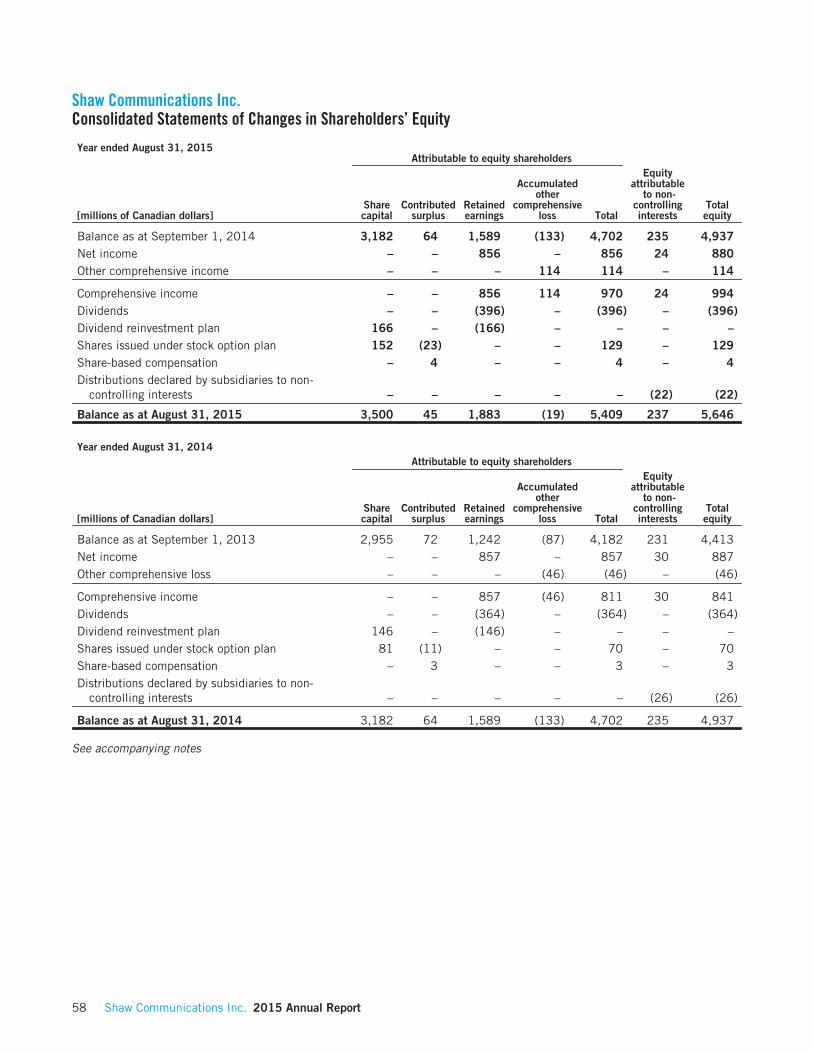

shw annual report 2015 v2 - shaw communications - bundles · pdf fileuncertainties”. the...

TRANSCRIPT

2015 Annual Report

1 Report to Shareholders

3 Management’s Discussion and Analysis

51 Management’s Responsibility for Financial Statements and Report on Internal Control over Financial Reporting

53 Independant Auditors’ Reports

55 Consolidated Financial Statements

106 Shareholders’ Information

107 Corporate Information

The Annual General Meeting of Shareholders will be held on January 14, 2016 at 11:00 am(Mountain Time) at Shaw Court, 630 – 3rd Avenue SW, Calgary, Alberta.

Shaw Communications Inc.Report to ShareholdersAugust 31, 2015

Dear Fellow Shareholders,

We are pleased to report solid fiscal 2015 results, a reflection of our commitment to customer service, focus on operationalexcellence and sound financial management for our shareholders.

Transformation in the Canadian communications sector continued through fiscal 2015 and we embrace the challenges andopportunities presented by evolving consumer preferences, regulatory change, technological advances and adjustments in theCanadian economy. We are genuinely excited about the possibilities for our customers and our business for many years to come.

From Shaw’s earliest days, we understood that delivering excellent products and customer service is fundamental to our growthand success. We are proud of the progress we have made to drive excellence in the ways we organize, plan and execute ourstrategy to achieve our corporate and operational goals. Guiding our operations and all of our decisions is our commitment todelivering exceptional experiences to our customers and viewers.

Operations

In 2015, our Consumer division took a major step forward by reorganizing our customer care operations into seven nationalcentres of expertise – in Victoria, Nanaimo, Vancouver, Kelowna, Winnipeg, Mississauga and Montreal. This realignment adoptsglobal best practices and enables us to specialize our knowledge, expertise, training, management and other processes to betterserve our customers.

Our shomi joint venture with Rogers Communications to provide subscription based streaming video on demand was madeavailable to all Canadians in 2015. Our work to provide more entertainment choices for customers continues in 2016 as wework closely with partners at Comcast to be the first to bring their market leading cloud-based X1 platform to Canadian viewers.X1 offers a seamless viewing experience across multiple screens and devices – both in and out of the home. We are planning toroll out X1 to our customers through 2016.

We are constantly investing in our network. As people embrace the power of new technology – whether through personaldevices, smart home features or new gadgets and tools still on the horizon – the demands on our hybrid fibre-coax networkincrease. We are committed to enhancing our broadband performance in 2016 through the technology provided by the DOCSIS3.1 protocol – known as Gigasphere. We know that we are now just scratching the surface of what our network is capable of andwe have a plan that will continue to deliver the speed and capacity that our customers want today and into the future. Ourpromise is simple: our customers will always be ready and always be connected so they never miss a thing.

Shaw Go WiFi is a valued extension of our network that now has nearly 75,000 access points across western Canada and morethan two million devices registered. We are committed to further extending the reach of our network so our customers canconnect outside the home.

We also made changes in 2015 to improve the performance of our Media division and transform it from a traditionalbroadcaster to a broader media company. In the shifting global media landscape, success is defined by the ability to engage inand monetize content across all platforms. Our Media team is exploring a number of next generation advertising solutions toensure that our offering evolves with the expectations of our advertising clients.

Growth

Our plans for growth are robust, yet disciplined. They are designed to ensure that we are making prudent moves andinvestments to ensure we retain our leadership in the marketplace and create value for our shareholders.

Business Infrastructure Services continues to capitalize on opportunities in its sector. ViaWest extended its reach with therecent opening of new facilities in Oregon and Calgary, and its recently announced move into the eastern U.S. with theacquisition of INetU and its facility in Pennsylvania.

We continue to address significant opportunities that we see in Business Network Services by strengthening our position as avalued advisor to small and medium sized businesses, and promoting our value proposition to “Grow your business with ShawBusiness.” Notably, in 2015 we worked with a number of global vendor partners to launch our “Smart” suite of flexible andeasy to use managed business communications solutions.

2015 Annual Report Shaw Communications Inc. 1

Shaw Communications Inc.Report to ShareholdersAugust 31, 2015

People

We are proud to support organizations that promote the communities where we work and live. In fiscal 2015, Shaw contributedapproximately $60 million in cash and in-kind contributions to charitable and community organizations that work to make ourneighbourhoods and cities better. Approximately 80% of this amount went to our multiple partnerships that benefit kids andyouth-focused charities under the Shaw Kids Investment Program (SKIP).

Every day, our more than 14,000 employees come to work and serve our customers, viewers and our communities the very bestway they can. They deliver time and time again, and we thank them for contributing to the success of our Company. We wouldalso like to commend our management team for their commitment to our customers and their ongoing leadership and thank themembers of our Board of Directors for their valued guidance, wisdom and insight.

Finally, we acknowledge the steady hand, sage counsel and unwavering support of Louis A. Desrochers, who passed awaypeacefully September 28, 2015. Louis was appointed Honourary Corporate Secretary for life in 1998, following decades ofproviding Shaw with excellent advice, including navigating our first licence application to the CRTC in 1970. We are lucky tohave worked so closely with him and to have gained so much from his friendship.

[Signed] [Signed]

JR ShawExecutive Chair

Bradley S. ShawChief Executive Officer

2 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

November 23, 2015

Forward

Tabular dollar amounts are in millions of Canadian dollars, except per share amounts or unless otherwise indicated. ThisManagement’s Discussion and Analysis should be read in conjunction with the Consolidated Financial Statements. The terms“we,” “us,” “our,” “Shaw” and “the Company” refer to Shaw Communications Inc. and, as applicable, Shaw CommunicationsInc. and its direct and indirect subsidiaries as a group.

Caution Concerning Forward Looking Statements

Statements included in this Management’s Discussion and Analysis that are not historic constitute “forward-lookingstatements” within the meaning of applicable securities laws. Such statements include, but are not limited to, statementsabout future capital expenditures, acquisitions and dispositions, financial guidance for future performance, business strategiesand measures to implement strategies, competitive strengths, expansion and growth of Shaw’s business and operations andother goals and plans. They can generally be identified by words such as “anticipate”, “believe”, “expect”, “plan”, “intend”,“target”, “goal” and similar expressions (although not all forward-looking statements contain such words). All of the forward-looking statements made in this report are qualified by these cautionary statements.

Forward-looking statements are based on assumptions and analyses made by Shaw in light of its experience and its perceptionof historical trends, current conditions and expected future developments as well as other factors it believes are appropriate inthe circumstances as of the current date. These assumptions include, but are not limited to, general economic conditions,interest, income tax and exchange rates, technology deployment, content and equipment costs, industry structure, conditionsand stability, government regulation and the integration of recent acquisitions. Many of these assumptions are confidential.

You should not place undue reliance on any forward-looking statements. Many factors, including those not within Shaw’scontrol, may cause Shaw’s actual results to be materially different from the views expressed or implied by such forward-lookingstatements, including, but not limited to, general economic, market and business conditions; changes in the competitiveenvironment in the markets in which Shaw operates and from the development of new markets for emerging technologies;industry trends and other changing conditions in the entertainment, information and communications industries; Shaw’s abilityto execute its strategic plans; opportunities that may be presented to and pursued by Shaw; changes in laws, regulations anddecisions by regulators that affect Shaw or the markets in which it operates; Shaw’s status as a holding company with separateoperating subsidiaries; and other factors described in this report under the heading “Known events, trends, risks anduncertainties”. The foregoing is not an exhaustive list of all possible factors. Should one or more of these risks materialize, orshould assumptions underlying the forward-looking statements prove incorrect, actual results may vary materially from thosedescribed herein.

The Company provides certain financial guidance for future performance as the Company believes that certain investors,analysts and others utilize this and other forward-looking information in order to assess the Company’s expected operational andfinancial performance and as an indicator of its ability to service debt and return cash to shareholders. The Company’s financialguidance may not be appropriate for this or other purposes.

Any forward-looking statement speaks only as of the date on which it was originally made and, except as required by law, Shawexpressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statement toreflect any change in related assumptions, events, conditions or circumstances.

2015 Annual Report Shaw Communications Inc. 3

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

ABOUT OUR BUSINESS

At Shaw, we are focused to deliver leading network and content experiences for our highly valued customers and viewers.

Š our Consumer team connects consumers in their homes and on the go with broadband Internet, Shaw Go WiFi, video andphone

Š our Business Network Services team enables businesses to focus on their core strategies with a full suite of connectivityand managed services

Š our Business Infrastructure Services team provides hybrid IT solutions, including colocation, managed services, cloudcomputing and security and compliance for North American enterprises

Š our Media team delivers engaging programming to Canadians through dynamic conventional and specialty televisionchannels along with online and over-the-top video platforms

In the following sections we provide select financial highlights and review our strategy, our four divisions, our network and ourpresence in the communities in which we operate.

Shaw is traded on the Toronto Stock Exchange (SJR.B) and the New York Stock Exchange (SJR) and is included in the S&P/TSX60 Index.

Select Financial and Operational Highlights

Through an evolving operating and competitive landscape our consolidated business has delivered stable and profitable resultsin 2015.

Year ended August 31,

(millions of Canadian dollars except per share amounts) 2015 2014Change

%

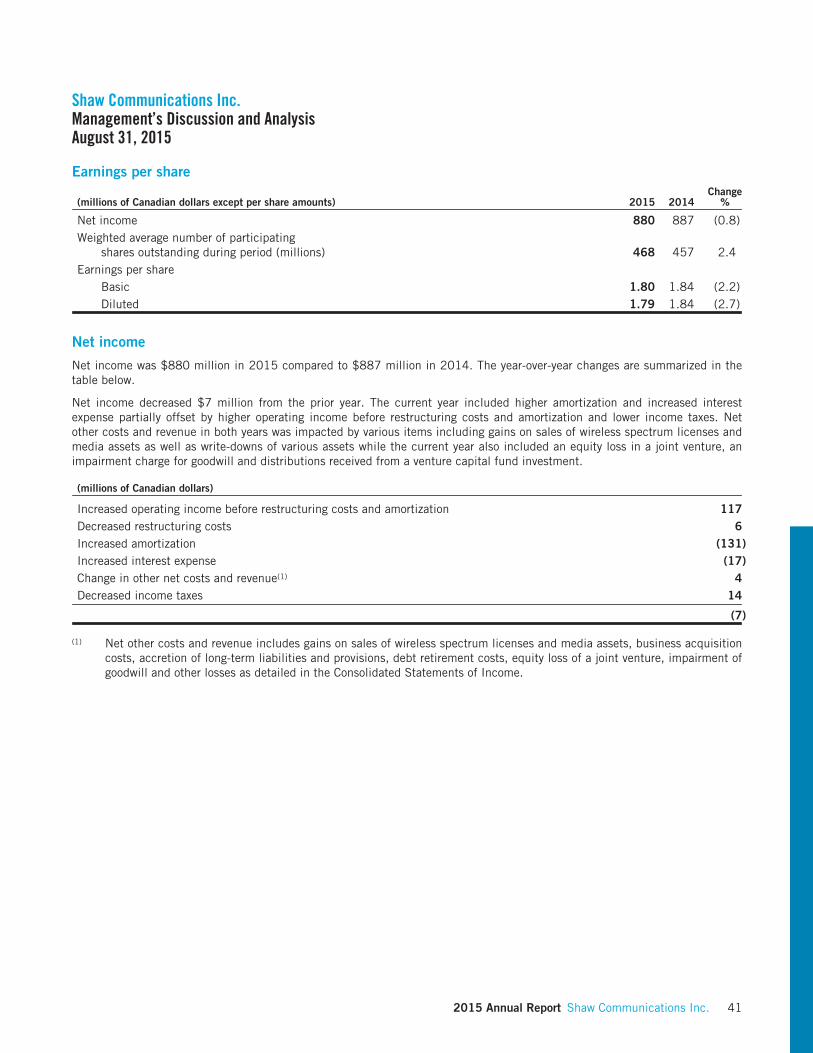

Operations:Revenue 5,488 5,241 4.7Operating income before restructuring costs and amortization(1) 2,379 2,262 5.2Operating margin(1) 43.3% 43.2% 0.1ptsNet income 880 887 (0.8)

Per share data:Earnings per share

Basic 1.80 1.84 (2.2)Diluted 1.79 1.84 (2.7)

Weighted average participating shares outstanding during period (millions) 468 457Funds flow from operations(2) 1,637 1,524 7.4Free cash flow(1) 653 698 (6.4)

(1) Refer to Key performance drivers.(2) Funds flow from operations is before changes in non-cash working capital balances related to operations as presented in

the Consolidated Statements of Cash Flows.

4 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

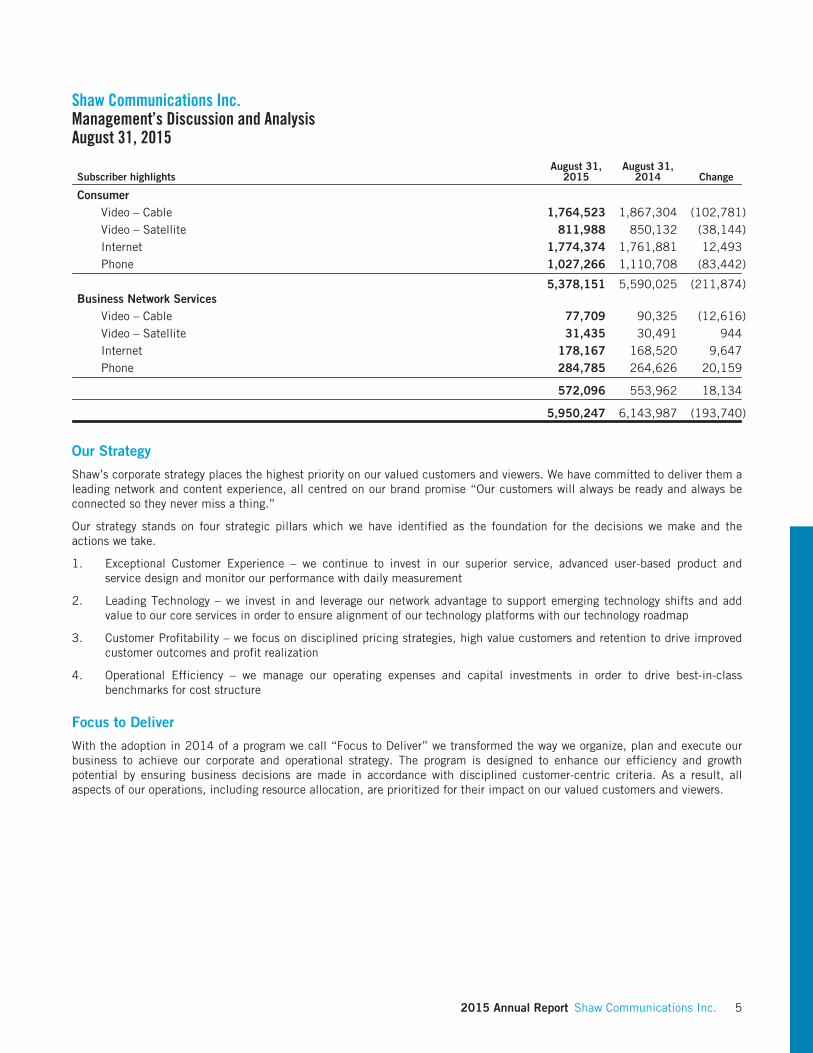

Subscriber highlightsAugust 31,

2015August 31,

2014 Change

ConsumerVideo – Cable 1,764,523 1,867,304 (102,781)Video – Satellite 811,988 850,132 (38,144)Internet 1,774,374 1,761,881 12,493Phone 1,027,266 1,110,708 (83,442)

5,378,151 5,590,025 (211,874)Business Network Services

Video – Cable 77,709 90,325 (12,616)Video – Satellite 31,435 30,491 944Internet 178,167 168,520 9,647Phone 284,785 264,626 20,159

572,096 553,962 18,134

5,950,247 6,143,987 (193,740)

Our Strategy

Shaw’s corporate strategy places the highest priority on our valued customers and viewers. We have committed to deliver them aleading network and content experience, all centred on our brand promise “Our customers will always be ready and always beconnected so they never miss a thing.”

Our strategy stands on four strategic pillars which we have identified as the foundation for the decisions we make and theactions we take.

1. Exceptional Customer Experience – we continue to invest in our superior service, advanced user-based product andservice design and monitor our performance with daily measurement

2. Leading Technology – we invest in and leverage our network advantage to support emerging technology shifts and addvalue to our core services in order to ensure alignment of our technology platforms with our technology roadmap

3. Customer Profitability – we focus on disciplined pricing strategies, high value customers and retention to drive improvedcustomer outcomes and profit realization

4. Operational Efficiency – we manage our operating expenses and capital investments in order to drive best-in-classbenchmarks for cost structure

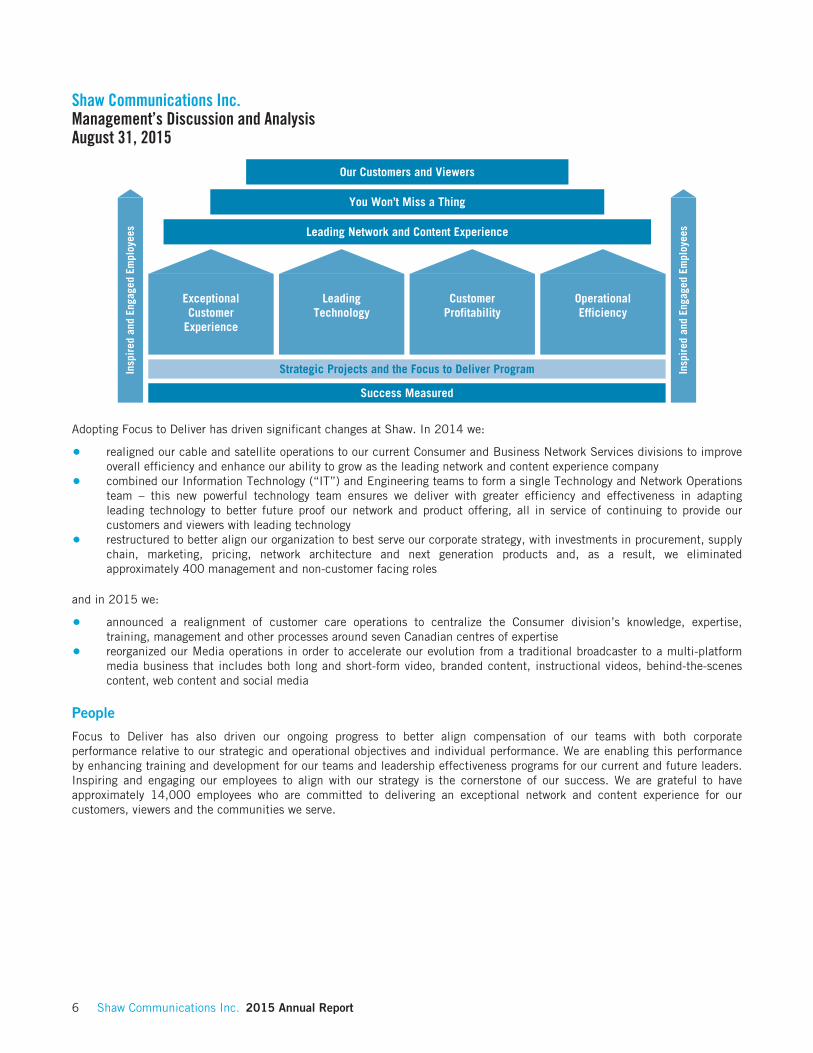

Focus to Deliver

With the adoption in 2014 of a program we call “Focus to Deliver” we transformed the way we organize, plan and execute ourbusiness to achieve our corporate and operational strategy. The program is designed to enhance our efficiency and growthpotential by ensuring business decisions are made in accordance with disciplined customer-centric criteria. As a result, allaspects of our operations, including resource allocation, are prioritized for their impact on our valued customers and viewers.

2015 Annual Report Shaw Communications Inc. 5

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Success Measured

Strategic Projects and the Focus to Deliver Program

ExceptionalCustomer

Experience

OperationalEfficiency

LeadingTechnology

CustomerProfitability

Leading Network and Content Experience

You Won’t Miss a Thing

Our Customers and Viewers

Insp

ired

and

Eng

aged

Em

ploy

ees

Insp

ired

and

Eng

aged

Em

ploy

ees

Adopting Focus to Deliver has driven significant changes at Shaw. In 2014 we:

Š realigned our cable and satellite operations to our current Consumer and Business Network Services divisions to improveoverall efficiency and enhance our ability to grow as the leading network and content experience company

Š combined our Information Technology (“IT”) and Engineering teams to form a single Technology and Network Operationsteam – this new powerful technology team ensures we deliver with greater efficiency and effectiveness in adaptingleading technology to better future proof our network and product offering, all in service of continuing to provide ourcustomers and viewers with leading technology

Š restructured to better align our organization to best serve our corporate strategy, with investments in procurement, supplychain, marketing, pricing, network architecture and next generation products and, as a result, we eliminatedapproximately 400 management and non-customer facing roles

and in 2015 we:

Š announced a realignment of customer care operations to centralize the Consumer division’s knowledge, expertise,training, management and other processes around seven Canadian centres of expertise

Š reorganized our Media operations in order to accelerate our evolution from a traditional broadcaster to a multi-platformmedia business that includes both long and short-form video, branded content, instructional videos, behind-the-scenescontent, web content and social media

People

Focus to Deliver has also driven our ongoing progress to better align compensation of our teams with both corporateperformance relative to our strategic and operational objectives and individual performance. We are enabling this performanceby enhancing training and development for our teams and leadership effectiveness programs for our current and future leaders.Inspiring and engaging our employees to align with our strategy is the cornerstone of our success. We are grateful to haveapproximately 14,000 employees who are committed to delivering an exceptional network and content experience for ourcustomers, viewers and the communities we serve.

6 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Global Technology Leaders

In order to efficiently secure and deliver leading technology for our customers – both for today and tomorrow – we recognize thatwe must join global scale initiatives. This ensures that the technology we adopt and invest in is, and continues to be, a standardfor the communications industry globally. This approach serves all of our strategic pillars.

This new approach allows us to leverage our current assets where we have strength and expertise, while also ensuring ourcapital investments are aligned with industry leaders to support the development, maintenance and advancement of newtechnology where it is impractical for us to do so on a standalone basis. This ensures that there is sufficient capital, resourcesand commitment to continue advances in innovation, performance and reliability of our services and products. In addition, thisstrategic approach to our business gives us the opportunity to better manage costs by participating in purchasing opportunitieson a global scale.

We are pleased to have collaborated this year with global leaders on two significant service offerings:

Š our planned rollout of the TV Everywhere X1 video platform developed by Comcast (see discussion under “Consumer”)Š our “Smart” suite of business services that includes SmartWiFi in collaboration with Cisco’s Meraki and SmartVoice with

Broadsoft (see discussion under “Business Network Services”)

Consumer

2015 2014

(millions of Canadian dollars) $share of

consolidated $share of

consolidated

Revenue 3,752 67%(1) 3,768 70%(1)

Operating income before restructuring costs and amortization(2) 1,686 71% 1,669 74%

(1) Before intersegment eliminations.(2) Refer to Key performance drivers.

Canadians trust Shaw to connect them to excellent network and content experiences. Our Consumer division was formed in2014 by bringing together all of our operations that serve residential customers. These customers are served on two platforms.

Š Network-Connected – we provide broadband Internet, Shaw Go WiFi, video and phone to customers that are connected toour local and regional hybrid fibre-coax network

Š Satellite – we provide video by satellite to customers across Canada

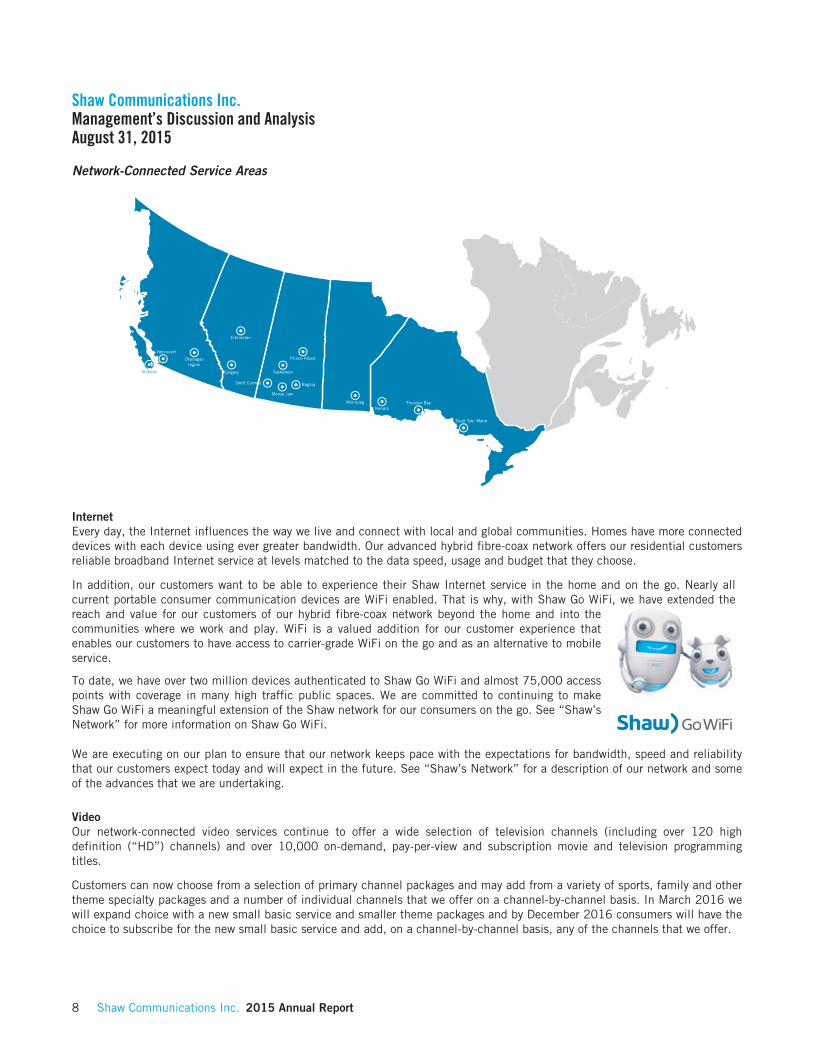

Network-Connected ServicesAs one of the largest providers of residential communications in Canada, Consumer connects families in British Columbia,Alberta, Saskatchewan, Manitoba and Northern Ontario on our hybrid fibre–coax network with broadband Internet, Shaw GoWiFi, video and home phone services to meet their needs at home and on the go.

As our customer needs evolve, we continue to be more flexible with our service offerings. Our customer-centric strategy isdesigned to deliver high-quality customer service, simplicity, value and choice for our customers.

2015 Annual Report Shaw Communications Inc. 7

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Network-Connected Service Areas

Calgary

Edmonton

Victoria

Okanaganregion

Saskatoon

Regina

Moose Jaw

Swift Current

Prince Albert

Winnipeg Thunder Bay

Sault Ste. Marie

Kenora

Vancouver

InternetEvery day, the Internet influences the way we live and connect with local and global communities. Homes have more connecteddevices with each device using ever greater bandwidth. Our advanced hybrid fibre-coax network offers our residential customersreliable broadband Internet service at levels matched to the data speed, usage and budget that they choose.

In addition, our customers want to be able to experience their Shaw Internet service in the home and on the go. Nearly allcurrent portable consumer communication devices are WiFi enabled. That is why, with Shaw Go WiFi, we have extended thereach and value for our customers of our hybrid fibre-coax network beyond the home and into thecommunities where we work and play. WiFi is a valued addition for our customer experience thatenables our customers to have access to carrier-grade WiFi on the go and as an alternative to mobileservice.

To date, we have over two million devices authenticated to Shaw Go WiFi and almost 75,000 accesspoints with coverage in many high traffic public spaces. We are committed to continuing to makeShaw Go WiFi a meaningful extension of the Shaw network for our consumers on the go. See “Shaw’sNetwork” for more information on Shaw Go WiFi.

We are executing on our plan to ensure that our network keeps pace with the expectations for bandwidth, speed and reliabilitythat our customers expect today and will expect in the future. See “Shaw’s Network” for a description of our network and someof the advances that we are undertaking.

VideoOur network-connected video services continue to offer a wide selection of television channels (including over 120 highdefinition (“HD”) channels) and over 10,000 on-demand, pay-per-view and subscription movie and television programmingtitles.

Customers can now choose from a selection of primary channel packages and may add from a variety of sports, family and othertheme specialty packages and a number of individual channels that we offer on a channel-by-channel basis. In March 2016 wewill expand choice with a new small basic service and smaller theme packages and by December 2016 consumers will have thechoice to subscribe for the new small basic service and add, on a channel-by-channel basis, any of the channels that we offer.

8 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Our network-connected customers access our television offerings through an interactive, on-screen program guide whichincludes access to on-demand movies and television programming and pay-per-view content, including scheduled sporting,concerts and other special events. With an enabled video terminal, customers can record and store programs for later viewingand pause and rewind live and recorded programs.

X1 for Network-Connected ConsumersWe recognize that, in order to ensure that we can deliver best in class customer experiences, we need to join with global scaleinitiatives and work with recognized industry leaders. In June 2015 we announced that we have partnered with Comcast tomake its market-leading cloud-based X1 video platform available to our customers. The X1 platform offers a seamless viewingexperience across multiple screens and devices both in and out of the home.

As a result of our collaboration with Comcast and Cisco, as integrator, we have aligned on the X1 technology roadmap and willbe the first in Canada to capitalize on this cloud technology.

We are in the late stages of our successful technical trial of this cloud-based platform and we are progressing on our plan to rollout this new technology through 2016.

In October 2015 we began deployment of the whole home video terminal used by Comcast in place of our current gateway andHD PVR terminals. This terminal operates on our current video platform and is future compatible for the rollout of the X1 in-home experience for network-connected customers.

PhoneShaw’s phone service offers a full-featured residential digital telephone service available in our network-connected homes as acomplement to our broadband Internet and video services.

SatelliteThrough Shaw Direct, our Consumer team connects families across Canada with video andaudio programming by satellite. Shaw Direct customers have access to over 550 digital videochannels (including over 220 HD channels) and over 10,000 on-demand, pay-per-view andsubscription movie and television programming titles.

Similar to our network-connected video service, satellite subscribers can now choose from a selection of primary channelpackages and may add from a variety of sports, family and other theme specialty packages and a number of individual channelsthat we offer on a channel-by-channel basis. In March 2016 we will expand choice with a new small basic service and smallertheme packages and by December 2016 consumers will have the choice to subscribe for the new small basic service and add,on a channel-by-channel basis, any of channels that we offer.

Shaw Direct is one of two satellite video services that are currently available across Canada. While Shaw Direct has manysubscribers in urban centres, market penetration for satellite video is stronger in areas having no or limited (generally fewer than80 channels) cable television coverage. The service is marketed through Shaw Direct and a nation-wide distribution network ofthird party retailers.

Shaw’s commitment to leading technology for Shaw Direct is evidenced on several fronts. With the 2013 launch of Anik G1,Shaw Direct added a third satellite to its platform. This third satellite increased Shaw Direct’s capacity by approximately 30%,enabling us to enhance our offerings, improve service quality and provide in-orbit back-up capacity. In addition, Shaw Directcontinues to transition to advanced modulation and encoding technology, including MPEG-4, for its programming which allowsus to increase channel capacity.

2015 Annual Report Shaw Communications Inc. 9

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Shaw Direct Satellite TranspondersSatellite Transponders Nature of Interest

Anik G1 16 xKu-band Leased

Anik F2 16Ku-band Owned6 Ku-band Leased2 Ku-band (partial) Leased

Anik F1R 28 Ku-band Leased1 C-band Leased

Intelsat Galaxy 16 1 Ku-band (partial) Leased

Video – over-the-top at home and on the goIn addition to television viewing, we know that our customers want to experience our video programming online and on mobiledevices at home and on the go. That is why we have expanded our over-the-top offering so that our network-connected andsatellite customers can stream live television and a selection of on-demand programming directly to a mobile device through aselection of entertainment, children and sports focused applications, including those within our Media division.

SeasonalityWhile financial results for Consumer are generally not subject to significant seasonal fluctuations, subscriber activity mayfluctuate from one quarter to another. Subscriber activity may also be affected by competition and Shaw’s promotional activity.Further, satellite subscriber activity is modestly higher around the summer time when more subscribers have second homes inuse. Shaw’s network-connected and satellite Consumer business does not depend on any single customer or concentration ofcustomers.

Business Network Services

2015 2014

(millions of Canadian dollars) $share of

consolidated $share of

consolidated

Revenue 520 9%(1) 484 9%(1)

Operating income before restructuring costs and amortization(2) 256 11% 240 11%

(1) Before intersegment eliminations.(2) Refer to Key performance drivers.

Our Business Network Services division was formed in 2014 by bringing together all of our operations that serve business andpublic sector customers – whether connected by our network and/or our satellite services. This reorganization allowed us tobetter focus on the needs of our business customers and offer a more integrated and consistent customer experience.

Shaw BusinessShaw Business connects customers of all sizes to our network or by satellite with a range ofcommunications services – from home offices and regional businesses to large scaleenterprises. While we provide business grade network access to smaller clients on our localand regional hybrid fibre-coax network, our larger enterprise customers are generallyconnected by fibre to the premise. This is particularly true in Calgary where, with our 2013 acquisition of ENMAX EnvisionInc., we significantly increased our fibre footprint and profile in the competitive Calgary marketplace.

The range of services offered by Shaw Business includes:

Š Fibre Internet – scalable, symmetrical fibre Internet solutions from 10 Mbps to more than 10GbpsŠ Data Connectivity – secure private connectivity for multiple locations

10 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Š Voice Solutions – from services that connect customer premise equipment to the phone network and single voice linesolutions to robust fully managed hosted unified communications functionality

Š Broadcast Video – high-quality video streaming across North America in real time

Business customers are looking for a communications partner that takes care of their communication infrastructure – a partnerthat will relieve them of the chore and complexity of managing communications so that they can focus on growing theirbusinesses. That is why we collaborated with global scale technology leaders to launch our “Smart” suite of easy to use andflexible managed business communications solutions:

Š SmartVoice is a unified communications solution that integrates instant messaging, presence, email, video conferencingand a mobile application – it is built on Broadsoft’s BroadWorks platform

Š SmartWiFi is a fully-managed internet solution designed to offer seamless secure wireless connectivity for employees andguests in the office and on the go with Shaw Go WiFi – it is deployed over Cisco’s Meraki platform

In order to continue to meet our customer needs in the future, we are executing our plan to ensure that our network keeps pacewith the expectations for bandwidth, speed and reliability that our customers expect today and will expect in the future. See“Shaw’s Network” for a description of our network and the advances that we are undertaking.

Shaw Business is also leading the rollout to customers in western Canada of hybrid IT services available from our recentlyopened Calgary1 data centre. These services complement the current Shaw Business offering and leverage ViaWest’s 16 yearsof experience as a hybrid IT solutions provider. See discussion under “Business Infrastructure Services.”

Wholesale Network ServicesUsing our national and regional fibre network, we provide services to internet service providers (“ISPs”), other communicationscompanies, broadcasters, governments and other businesses and organizations that require end-to-end Internet and dataconnectivity in Canada and the United States. We also engage in public and private peering arrangements with high speedconnections to major North American, European and Asian networks and other tier-one backbone carriers.

Broadcast ServicesShaw Broadcast Services uses our substantial fibre backbone network to manage one ofNorth America’s largest full-service commercial signal distribution networks, delivering moretelevision and radio signals by satellite to cable operators and other multi-channel systemoperators in Canada and the U.S. than any other single-source satellite supplier. Thisbusiness is referred to as a “satellite relay distribution undertaking” or “SRDU”. ShawBroadcast Services currently provides SRDU and advanced signal transport services to approximately 350 distributionundertakings and redistributes approximately 500 television signals and over 100 audio signals in both English and French tomulti-channel system operators.

TrackingShaw Tracking provides asset tracking and communication services primarily in Canada toapproximately 600 customers in the transportation industry that have an aggregate ofapproximately 45,000 vehicles. By satellite, cellular, WiFi and Bluetooth, Shaw Trackingprovides immediate real-time visibility to a customer’s fleet and freight. Specifically, Shaw Tracking’s services integrate with acarrier’s fleet management system and capture location, performance, productivity and other measures pertaining to acustomer’s assets.

2015 Annual Report Shaw Communications Inc. 11

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Business Infrastructure Services

2015(1)

(millions of Canadian dollars) $share of

consolidated

Revenue 246 4%(2)

Operating income before restructuring costs and amortization(3) 95 4%

(1) Fiscal 2014 numbers are not applicable prior to acquisition in September 2014.(2) Before intersegment eliminations.(3) Refer to Key performance drivers.

Our Business Infrastructure Services business unit was formed with the acquisition of Denver,Colorado based ViaWest in September 2014 for US$1.2 billion. We acquired ViaWest as a growthplatform in the attractive North American data centre sector and to support the expansion of ourbusiness offerings in western Canada.

ViaWest is a leading hybrid IT solutions provider, including colocation, managed services, cloud computing, and security andcompliance services. It enables businesses to leverage both their existing IT infrastructure and emerging cloud resources todeliver the right balance of cost, scalability and security.

ViaWest has grown from five data centres in two markets in 2004 to 28 data centres (with over 680,000 square feet of usableraised floor space) in eight key western U.S. markets, including Denver, Dallas, Austin, Salt Lake City, Las Vegas, Minneapolis,Phoenix and our recently opened facility in Portland.

ViaWest has the capacity to support further U.S. growth with 75% utilization in its current facilities and substantial expansioncapacity at its Denver, Las Vegas, Minneapolis and Portland properties.

Business Infrastructure Services continues to execute on its plans for continued growth. In thefall of 2015 we expanded operations into Canada with the opening of the new Calgary datacentre under our Canadian brand “Shaw Data Centre & Cloud Solutions, Powered by ViaWest”,

where customers will benefit from ViaWest’s leading expertise and 16-year track record. ViaWest will also extend its reach intothe eastern U.S. with the acquisition of INetU and its facility in Pennsylvania that was announced in November 2015.

Business Infrastructure Services - Cities where Facilities are Located

12 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

We also offer expanded security offerings through our recent acquisition of AppliedTrust to offer leading security, compliance,development operations (“DevOps”) and infrastructure consulting services that address pressing security and compliance needsof our customers.

Over 1,600 businesses trust their infrastructure and mission critical data to our Business Infrastructure Services team becauseof the dedicated personnel who provide local, personalized, flexible and tailored solutions to meet the unique business needs ofour customers. With our team-based account management approach and 100% uptime commitment, we offer tailored solutionsdesigned for maximum reliability and flexibility.

Media2015 2014

(millions of Canadian dollars) $share of

consolidated $share of

consolidated

Revenue 1,080 19%(1) 1,096 20%(1)

Operating income before restructuring costs and amortization(2) 342 14% 353 16%

(1) Before intersegment eliminations.(2) Refer to Key performance drivers.

Our Media team provides Canadians with engaging programming content through one of Canada’s largest conventional televisionnetworks, Global Television, 19 specialty networks and digital properties.

Shaw acquired its Media operations from Canwest Global Communications Corp. through a series oftransactions that concluded in October 2010.

Media derives revenues from two principal sources: advertising revenue and revenue from consumers subscribing to ourspecialty channels. For both, it is critical that we offer Canadians entertaining content that engages them. Our content isavailable to Canadians through a variety of dynamic channels, whether conventional or specialty television, online websites orover-the-top platforms. Catering to consumer demand for quality and choice, we strive to offer the best content available toCanadians when and where they choose to consume it.

Conventional TelevisionGlobal Television, reaches virtually all English-speaking Canadians through 12 over-the-air conventional televisionstations. Global Television offers a programming mix of entertainment and news programs aimed primarily atviewers aged 18 to 49. Global Television’s line-up includes hit programs such as Bones, TheBlacklist, the NCIS franchise, Hawaii Five-O, SuperGirl, Limitless, Rookie Blue, Elementary, The Late Show with StephenColbert and three reality series, Survivor, Big Brother and Big Brother Canada.

NewsThe Global News team produces the news and current affairs content for Global Television. Global News hassuccessful local news programs in every major market, including the only major daily supper hour nationalnews show originating from Vancouver, and is the dominant local news organization in western Canada. GlobalNational, the network’s early-evening newscast garners almost a million viewers every weekday.

GlobalNews.ca is Global’s online platform that enables Canadians to access Global News coveragewherever and whenever they want, through the web, mobile devices, email alerts, RSS feeds and socialmedia. It features user friendly technology, which automatically scales content to fit any screen size or resolution to create aseamless experience on all browsers and platforms, including tablets and smart phones. New native content advertisingopportunities have been incorporated into the site giving advertisers exciting new ways to engage with the Global Newsaudience.

2015 Annual Report Shaw Communications Inc. 13

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Specialty ChannelsShaw Media operates 19 of Canada’s most popularspecialty channels, including HGTV Canada, FoodNetwork Canada, Showcase, HISTORY, Slice andNational Geographic.

All of our specialty channels are wholly-owned by Shaw with the exception of channels for which we have partnered with globalleaders: Food Network Canada, HGTV Canada, DIY Canada (each of the foregoing with Scripps Networks), National GeographicCanada, National Geographic Canada Wild and BBCCanada. Our equity interests in these channels rangesbetween 50% and 71%, with voting control of 80% ormore.

Over-the-topTo meet the changing needs of our conventional and specialty viewing audiences, Media rolled out Global Go and HISTORY Goapps in 2014. These apps allow viewers to watch live TV, full episodes of select shows, clips and video exclusives on popularmobile devices, including WiFi enabled devices.

In November 2014, in partnership with Rogers Communications we launched shomi on a test basisto Shaw and Rogers customers. In August 2015, the service was made available to all Canadians.With a current library of approximately 1,200 films and 15,000 individual episodes in categories

curated by experts, shomi offers its subscribers some of the best entertainment available – whenever and wherever they want.shomi may be accessed over-the-top through the service’s website and the shomi app and on television through the on-demandlibraries of participating television providers.

AdvertisingOur Media team is exploring a number of next generation advertising solutions that combine the intelligence of data with thepower of television to maintain and grow our advertising business.

We are part of an industry working group that is looking at the development of a common video terminal based measurementsystem. We are also exploring new ways for advertisers to focus on optimal advertising placement on our programming byidentifying generic audience profiles and aggregate lifestyle demographics that can be used to identify relevant “audiences”.This allows advertisers to make decisions based on identified demographics to purchase “audiences” rather than shows andtime slots. All data collection, analysis and use is designed for compliance with applicable privacy protection laws.

The Media team is also continuing to create opportunities for branded content and product integrations within our shows andbrands. As one of the leading lifestyle content providers in Canada, we have a strong slate of context-relevant, originalproductions into which advertisers can integrate their products. This type of integration yields positive results for theadvertisers, generating a positive impact on brand perception, likelihood to purchase and consumer trust in the product.

Through these next generation advertising solutions Shaw is working to ensure that our advertising opportunities evolve with theexpectations of our advertising clients to position our Media team as the most innovative media partner for advertisers in ourspace.

We are also building revenues from our increasingly popular digital platforms along with further syndication opportunitiesaround our strong content.

Through these initiatives and advances in the way we create content, produce and deliver news and develop business, we havemoved Media beyond the traditional broadcast model to become a driven media company.

SeasonalityThe Media financial results are subject to fluctuations throughout the year due to, among other things, seasonal advertising andviewing patterns. In general, advertising revenues are higher during the fall, the first quarter, and lower during the summermonths, the fourth quarter, whereas expenses are incurred more evenly throughout the year. The specialty services depend on asmall number of broadcast distribution undertakings (“BDUs”) for distribution of their services.

14 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Shaw’s Network

At Shaw we are proud of our advanced hybrid fibre-coax network that is comprised of:

Š North American fibre backboneŠ regional fibre optic and co-axial distribution networksŠ local Shaw Go Wifi connectivity

BackboneThe backbone of Shaw’s network includes multiple fibre capacity on two diverse cross-North America routes. The southern routeprincipally consists of approximately 6,400 route kilometres of fibre located on routes between Seattle and New York City (viaVancouver, Calgary, Winnipeg, Toronto Buffalo, and Chicago). The northern route consists of approximately 4,000 routekilometres of fibre between Edmonton and Toronto (via Saskatoon, Winnipeg and Thunder Bay). These routes, along with anumber of secured capacity routes, provide redundancy for the network. Shaw also uses a marine route consisting ofapproximately 330 route kilometres from Seattle to Vancouver (via Victoria), and has secured additional capacity on routesbetween a number of cities, including Vancouver and Calgary, Vancouver and San Jose, Toronto and New York City, Seattle andVancouver and Edmonton and Toronto.

LONDON

AMSTERDAM

ASIA

ASIA

SASKATOONVANCOUVERCALGARY

VICTORIA

SAN JOSEPALO ALTO

BUFFALO

MONTREALOTTAWA

WASHINGTONASHBURN

WINNIPEG

TORONTO

CHICAGO

ED

MO

NTO

N

SEATTLE

KA

MLO

OP

S

REGINA

NEW YORK

Regional Distribution NetworkWe connect our backbone network to residential and business customers through our extensive regional fibre optic and co-axialcable distribution networks.

2015 Annual Report Shaw Communications Inc. 15

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

In 2013 we substantially completed a major upgrade of our co-axial access network to remove analog tier television services.This upgrade liberated bandwidth to significantly increase the capacity of our hybrid fibre-coax network and enabled theexpansion of our broadband Internet and other offerings. Digital video terminals were deployed into customer homes thatallowed them to receive digital television services in place of former analog services. We referred to this reclamation initiative asthe Digital Network Upgrade (“DNU”).

In 2014 and 2015, we removed the remaining analog basic services in the Vancouver area, our largest market, in an initiativereferred to as “DNU II”. As a result, customers in this region only receive digital video services. A similar process to removeremaining analog basic services in our other major markets will begin in 2016.

Shaw continues to optimize the capacity and efficiency of our network and reduce congestion by deploying fibre optic cabledeeper into our access networks and closer to our customers. We are also increasing the number of optical serving areas or“nodes” in the network. This is a continual process that we apply year-over-year to increase fibre optic usage in our network andreduce the distance signals travel over coaxial cable to each consumer.

In addition to the initiatives above, our network roadmap in 2016 includes the roll out of the latest version of the Data overCable Service Interface Specification or “DOCSIS 3.1” which will provide significant added capacity in our hybrid fibre-coaxnetwork and lay the groundwork for further speed increases for our broadband customers. DOCSIS 3.1 represents the latestdevelopment in a set of technologies that increase the capability of a hybrid fibrecoax network to transmit data both to and fromcustomer premises.

With the various DNU initiatives, the deployment of fibre closer to our customers, by continuing to increase the number ofnodes in our hybrid fibre-coax network and by implementing DOCSIS 3.1 technologies we will continue to significantly improvethe performance and capacity of our network for years to come.

Shaw Go WiFiIn 2011 we began deploying WiFi access points to create Canada’s most extensive managed carrier-grade WiFi network, Shaw Go WiFi, as a wireless extension of our access network into thecommunity. Shaw Go WiFi extends a customer’s broadband experience beyond the home as avaluable extension of our customer network experience as an alternative to relying on mobileservice.

We continue to expand our Shaw Go WiFi build-out. To date, we have over 73,000 Shaw Go WiFiaccess points installed and operating throughout the network and over two million unique activedevices using Shaw Go WiFi. In addition, we have entered into agreements with 90 municipalitiesto extend Shaw Go WiFi service into public areas within those cities.

Community Investment

Shaw has a proud and lengthy track record of supporting causes and charities that focus on the health and strength of Canadiancommunities. For decades, we have been recognized as a philanthropic leader in our communities, providing support tohundreds of small and large organizations.

In fiscal 2015, Shaw contributed approximately $60 million in cash and in-kind support to charitable and communityorganizations working to make our neighbourhoods and cities better. We also took steps in 2015 to focus our governance,discipline and awareness of our community contributions, reflecting the increased value our stakeholders place on communityinvestment activities when making decisions about doing business with organizations.

16 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Notably, we implemented a strategy in 2015 to focus the majority of our community investment activities on organizations thatsupport the needs of children, youth and millennials. Specifically, investments and causes that positively affect thisdemographic’s health and wellbeing, education and their access to technology and the Internet. This approach has resonatedwell with customers, employees, and government and community stakeholders, generating positivefeedback from local and federal government officials, a significant increase in applications forcharitable funding, and significantly higher media coverage of our initiatives. At the end of 2015,80% of Shaw’s community investments supported organizations focused on needs of children andyouth.

In 2015, Shaw also brought greater public and stakeholder awareness of our community investmentactivities under the umbrella of the Shaw Kids Investment Program, known as “SKIP”. SKIP is apublic platform used to describe our partnerships that benefit kids and youth-focused charities, andis an important vehicle by which we drive brand reputation.

Shaw’s partnerships with local and national charities are also used to complement local andregional marketing and sponsorship activities. Combining community investments withtraditional business activities speaks to our overall brand values of being a caring andcustomer centric organization. The most prominent example of this combination is Shaw’spartnership with local Calgary business leaders and the PGA TOUR in staging the ShawCharity Classic, a premier tournament on the Champions Tour that benefits 89 Albertacharities and has generated more than $8 million in charitable contributions in its three-yearhistory. The event has become a fixture on the Calgary tourism calendar, and has beenrecognized as one of the top tournaments on the Champions Tour. Importantly, the event alsostrengthens Shaw’s business and community relationships.

Additional Information Concerning the Business

Environmental MattersShaw’s operations are subject to environmental regulations, including those related to electronic waste, printed paper andpackaging. A number of provinces have enacted regulations providing for the diversion of certain types of electronic and otherwaste through product stewardship programs (“PSP”). Under a PSP, companies who supply designated products in or into aprovince are required to participate in or develop an approved program for the collection and recycling of designated materialsand, in some cases, pay a per-item fee. Such regulations have not had, and are not expected to have, a material effect on theCompany’s earnings or competitive position.

Foreign OperationsIn September 2014, the Company acquired ViaWest, a U.S.-based provider of hybrid IT solutions with 28 data centres in theU.S. ViaWest comprises substantially all of the assets and operations of the Business Infrastructure Services division.

Shaw Business U.S. Inc., a wholly-owned subsidiary of the Company, has entered into an indefeasible right of use (“IRU”) withrespect to a portion of a United States fibre network and owns certain other fibre and facilities in the United States. ShawBusiness U.S. Inc. commenced revenue-generating operations in the United States in 2002. Its revenues for the year endedAugust 31, 2015 were not material.

Government Regulations and Regulatory Developments

Substantially all of the Company’s Canadian business activities are subject to regulations and policies established under variouslegislation (Broadcasting Act (Canada) (“Broadcasting Act”), Telecommunications Act (Canada) (“Telecommunications Act”),Radiocommunication Act (Canada) (“Radiocommunication Act”) and Copyright Act (Canada) (“Copyright Act”)). Broadcastingand telecommunications are generally administered by the Canadian Radio-television and Telecommunications Commission(“CRTC”) under the supervision of the Department of Canadian Heritage (“Canadian Heritage”) and the Department of Industry(“Industry Canada”).

2015 Annual Report Shaw Communications Inc. 17

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Pursuant to the Broadcasting Act, the CRTC is mandated to supervise and regulate all aspects of the broadcasting system in aflexible manner. The Broadcasting Act requires BDUs to give priority to the carriage of Canadian services and to provideefficient delivery of programming services. The Broadcasting Act also sets out requirements for television broadcasters withrespect to Canadian content. Shaw’s businesses are dependent upon licenses (or operate pursuant to an exemption order)granted and issued by the CRTC and Industry Canada.

Under the Telecommunications Act, the CRTC is responsible for ensuring that Canadians in all regions of Canada have access toreliable and affordable telecommunication services of high-quality. The CRTC has the authority to forbear from regulatingcertain services or classes of services provided by a carrier if the CRTC finds that there is sufficient competition for that serviceto protect the interests of users. All of Shaw’s telecommunication retail services have been forborne from regulation and are notsubject to price regulation. However, regulations do impact certain terms and conditions under which these services areprovided.

The technical operating aspects of the Company’s businesses are also regulated by technical requirements and performancestandards established by Industry Canada, primarily under the Telecommunications Act and the Radiocommunication Act.

Pursuant to the Copyright Act, the Copyright Board of Canada oversees the collective administration of copyright royalties inCanada, including the review and approval of copyright tariff royalties payable to copyright collectives by BDUs, televisionbroadcasters and online content services.

The sections below include a more detailed discussion of various regulatory matters and recent developments specific to Shaw’sbusinesses.

Licensing and ownershipFor each of its cable, direct to home satellite (“DTH”) and SRDU undertakings, the Company holds a separate broadcastinglicense or is exempt from licensing. In November 2010, the majority of cable undertakings owned and operated by theCompany were renewed by the CRTC for a five-year period ending August 31, 2015. On February 16, 2015, the CRTC issuedan administrative renewal of the licenses for Shaw’s undertakings serving British Columbia, Alberta, Saskatchewan, Manitobaand Ontario for a period of one year, to August 31, 2016. The licenses of the Company’s DTH and SRDU undertakings wererenewed in 2013 by the CRTC for a seven year period ending August 31, 2019. Shaw has never failed to obtain a licenserenewal for its cable, DTH or SRDU undertakings.

The Company also holds a separate license for each of its conventional over the air (“OTA”) television stations and eachspecialty service. These CRTC broadcasting licenses must be renewed from time to time and cannot be transferred withoutregulatory approval. The majority of the Company’s licenses for its OTA television stations and specialty services are current toAugust 31, 2016 and are expected to be administratively renewed to August 31, 2017. Under these licenses, the Company issubject to an expenditure-based regulatory regime, whereby the Company must expend a certain percentage of its prior yearrevenues from its conventional OTA and specialty services on Canadian content, and also on specific categories of Canadianprograms defined as “programs of national interest”. These obligations are imposed on an individual license basis, but withcertain restrictions, may be shared among various conventional OTA and specialty licenses.

The potential for new or increased fees through regulationIn July 2012, the CRTC determined to phase out completely, as of September 2014, the Local Programming ImprovementFund to support local television stations operating in non-metropolitan markets with contributions from licensed BDUs.

CRTC Regulations require licensed cable BDUs to obtain the consent of an OTA broadcaster to deliver its signal in a distantmarket. The Regulations provide that DTH undertakings may distribute a local over-the-air television signal without consentwithin the province of origin, but must obtain permission to deliver the over-the-air television signal beyond the province oforigin unless the DTH distribution undertaking is required to carry the signal on its basic service. Broadcasters may assert aright to limit distribution of distant signals or to seek remuneration for the distribution of their signals in distant markets on thebasis of these Regulations.

The Copyright Board is considering a proposed tariff for the retransmission of programming in distant television stations for theyears 2014 through 2018. The tariff proposed by the retransmission rights collectives would, if approved, represent asignificant increase in the per subscriber rates payable for the retransmission of programming in distant signals. The Companyhas objected to the tariff on behalf of its cable and DTH satellite divisions and is participating in the current hearing.

18 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Let’s Talk TV regulatory frameworkIn October 2013, the CRTC initiated a “conversation with Canadians about the future of television”, commonly referred to as“Let’s Talk TV”, which led to a major review of the regulatory and policy framework for the Canadian television broadcastingsystem and a series of policy decisions in 2015. The new policy framework will require licensed BDUs to offer a $25 entry-levelservice offering (basic service) by March 2016. BDUs will be allowed to offer a larger “first-tier offering”. By March 2016, alldiscretionary services (not offered on the basic service) must be offered either on a standalone basis or in packages of up to tenprogramming services. On or after December 1, 2016, these services must be offered both on a standalone basis and inpackages of up to ten programming services. These changes will significantly impact BDUs’ customer management systems andmay create market uncertainty for both BDUs and programming services. Additional uncertainty may result from the eliminationof genre protection and changes to access rules. The CRTC has made new regulations, which will come into force onDecember 1, 2015, governing simultaneous substitution. These new regulations may result in rebates (BDU errors) or loss ofprivileges (broadcaster errors). The CRTC has also introduced new codes governing the relationship between BDUs and theircustomers, the “Television Service Provider Code of Conduct”, and the relationship between distributors and programmers, the“Wholesale Code”. The CRTC has, as well, prohibited 30-day cancellation policies for voice, Internet and broadcastingdistribution services. A proceeding on local and community television may result in changes to the policies and funding regimesgoverning community channels and local television stations.

Access rightsFor its network Shaw requires access to support structures, such as poles, strand and conduits of telecommunication carriersand electric utilities, in order to deploy cable facilities. Under the Telecommunications Act the CRTC has jurisdiction oversupport structures of telecommunication carriers, including rates for third party use. The CRTC’s jurisdiction does not extend toelectrical utility support structures, which are regulated by provincial utility authorities. For its network Shaw also requiresaccess to construct facilities in roadways and other public places. Under the Telecommunications Act, Shaw may do so with theconsent of the municipality.

New media and InternetThe CRTC has issued a digital media exemption order requiring that Internet-based and mobile point-to-point broadcastingservices not offer television programming on an exclusive or preferential basis in a manner that depends on subscription to aspecific mobile or retail Internet service and not confer an undue preference or disadvantage.

The CRTC has decided to not impose a levy on the revenue of exempt digital media undertakings to support Canadian newmedia content and instead issued an exemption order for VOD services offered both by licensed BDUs and direct to consumerover the Internet, such as shomi. These services benefit from virtually the same flexibility as services operating under the digitalmedia exemption order (including the ability to offer exclusive programming) and are subject to similar restrictions on offering aservice on an exclusive or preferential basis or conferring an undue preference or disadvantage.

Third Party Internet AccessShaw is mandated by the CRTC to allow independent ISPs to provide Internet services at premises served by Shaw’s network(“Third Party Internet Access” or “TPIA”). In 2014-2015, the CRTC completed a review of the wholesale wirelinetelecommunications policy framework, including TPIA, and extended mandated wholesale access services to include fibre-to-the-premise facilities, which will coincide with a shift to a new disaggregated wholesale Internet access service to be phased inover the next three years. The new disaggregated model will increase the number of interconnection points within the networksof wholesale providers, such as Shaw. Depending on how the model is implemented, Shaw may need to adjust its networkdesign and configuration.

Within the coming year, the CRTC also plans to review the competitor quality of service indicators and the rate rebate plan forcompetitors to ensure alignment with the new wholesale services framework. As part of this review, the CRTC may extendquality of service obligations to providers of wholesale Internet services.

CRTC basic services proceedingIn April 2015, the CRTC initiated a comprehensive review of basic telecommunications services to determine what services(e.g. telephone and broadband) are required by all Canadians to fully participate in the digital economy, whether there shouldbe changes to the subsidy regime and national contribution mechanism to fund expansion or adoption of broadband services in

2015 Annual Report Shaw Communications Inc. 19

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Canada, and what the respective roles of the private sector, the CRTC and government should be in providingtelecommunications services. Currently, the national contribution fund overseen by the CRTC provides subsidies for local phoneservices in high cost serving areas and video relay service. Canadian telecommunications service providers, including Shaw, arerequired to contribute to the fund.

Other legislationCanada’s anti-spam legislation (together with the related regulations “CASL”) sets out a comprehensive regulatory regimeregarding online commerce, including requirements to obtain consent prior to sending commercial electronic messages andinstalling computer programs. CASL is administered primarily by the CRTC, and non-compliance may result in fines of up to$10 million. To ensure compliance with CASL, Shaw reviewed and updated its current practices with respect to marketing andother communications with customers and its practices regarding computer program installations.

On March 10, 2015, Bill C-13, An Act to amend the Criminal Code, the Canada Evidence Act, the Competition Act and theMutual Legal Assistance in Criminal Matters Act (“Bill C-13”) came into force. Bill C-13 expands the lawful access powers ofthe Government and introduces new requirements for telecommunications providers to preserve and produce subscriberinformation. Almost all of the newly proposed measures under Bill C-13 are subject to judicial oversight and do not require theprovision of information without a warrant or discharge of a burden of proof.

On June 18, 2015, Bill S-4, An Act to amend the Personal Information Protection and Electronic Documents Act and to make aconsequential amendment to another Act” (“Bill S-4”) received Royal Assent. Bill S-4 will introduce a mandatory record-keeping and notification system applicable with respect to breaches of privacy respecting the personal information held byShaw, and penalties for failure to comply with these new requirements. In addition, Bill S-4 modifies the standard for obtainingconsent for the collection, use and retention of personal information, creating a higher burden for organizations.

Digital transition and repurposing of spectrumIn July 2009, the CRTC identified the major markets where it expected conventional television broadcasters to convert theirfull-power OTA analog transmitters to digital transmitters by August 31, 2011. The conversion from analog to digital freed upspectrum for government auction to mobile providers. The Company completed the digital transition in all mandatory markets asof August 31, 2011. Since then, the Company has been converting transmitters in non-mandatory markets with a view tocompletion in 2016, a condition of the CRTC’s approval of the Canwest Global acquisition. On December 18, 2014, IndustryCanada launched a consultation to consider repurposing some of the 600 MHz spectrum band currently used by our Mediadivision and other broadcasters for OTA transmission. At the same time, Industry Canada introduced a moratorium onapplications to modify existing television broadcasting certificates and on any new licensing in the spectrum band pending theconsultations and related processes. Shaw has, accordingly, requested from the CRTC an extension of the time line to completethe full slate of analog to digital conversions.

On August 14, 2015, Industry Canada confirmed its intent to proceed with repurposing some of the 600 MHz spectrum bandfor commercial mobile use and to jointly establish a new allotment plan in collaboration with the United States.Accommodating this change will require our Media division to install new equipment or reconfigure existing equipment ataffected sites and may have an impact on signal quality and coverage. Industry Canada has not yet decided whetherbroadcasters will be reimbursed for their costs of facilitating this transition, stating that this decision is the first step in a multi-year repurposing process and that consideration of compensation to broadcasters was not a part of this phase.

Limits on non-Canadian ownership and control for broadcasting undertakingsNon-Canadians are permitted to own and control, directly or indirectly, up to 33.3% of the voting shares and 33.3% of thevotes of a holding company that has a subsidiary operating company licensed under the Broadcasting Act. In addition, up to20% of the voting shares and 20% of the votes of a licensee may be owned and controlled, directly or indirectly, by non-Canadians. As well, the chief executive officer (CEO) and not less than 80% of the board of directors of the licensee must beresident Canadians. There are no restrictions on the number of non-voting shares that may be held by non-Canadians at eitherthe holding company or licensee level. Neither the holding company nor the licensee may be controlled in fact by non-Canadians, the determination of which is a question of fact within the jurisdiction of the CRTC.

20 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

The same restrictions apply to certain Canadian carriers pursuant to the Telecommunications Act, the Radiocommunication Actand associated regulations, except that there is no requirement that the CEO be a resident Canadian. In June 2012, theTelecommunications Act was amended to remove Canadian ownership requirements for wireline and wirelesstelecommunications carriers with annual revenues from the provision of telecommunications services in Canada that representless than 10% of the total annual revenues. This may lead to greater levels of competition in the Canadian telecommunicationsmarket.

The Company’s Articles contain measures to ensure the Company continues to comply with applicable Canadian ownershiprequirements and its ability to obtain, amend or renew a license to carry on any business. Shaw must file a compliance reportannually with the CRTC confirming that it is eligible to operate in Canada as a telecommunications common carrier.

KEY PERFORMANCE DRIVERS

Shaw measures the success of its strategies using a number of key performance drivers which are outlined below, including adiscussion as to their relevance, definitions, calculation methods and underlying assumptions.

Financial Measures

RevenueRevenue is a measurement determined in accordance with International Financial Reporting Standards (“IFRS”). It representsthe inflow of cash, receivables or other consideration arising from the sale of products and services. Revenue is net of itemssuch as trade or volume discounts, agency commissions and certain excise and sales taxes. It is the base on which free cashflow, a key performance driver, is determined; therefore, it measures the potential to deliver free cash flow as well as indicatinggrowth in a competitive market place.

The Company’s continuous disclosure documents may provide discussion and analysis of non-IFRS financial measures. Thesefinancial measures do not have standard definitions prescribed by IFRS and therefore may not be comparable to similarmeasures disclosed by other companies. The Company’s continuous disclosure requirements may also provide discussion andanalysis of additional GAAP measures. Additional GAAP measures include line items, headings and sub-totals in financialstatements. The Company utilizes these measures in making operating decisions and assessing its performance. Certaininvestors, analysts and others utilize these measures in assessing the Company’s operational and financial performance and asan indicator of its ability to service debt and return cash to shareholders. These non-IFRS measures and additional GAAPmeasures have not been presented as an alternative to net income or any other measure of performance or liquidity prescribedby IFRS. The following contains a description of the Company’s use of non-IFRS financial measures and additional GAAPmeasures and provides a reconciliation to the nearest IFRS measure or provides a reference to such reconciliation.

Operating income before restructuring costs and amortizationOperating income before restructuring costs and amortization is calculated as revenue less operating, general and administrativeexpenses. It is intended to indicate the Company’s ability to service and/or incur debt, and therefore it is calculated before one-time items like restructuring costs, amortization (a non-cash expense) and interest. Operating income before restructuring costsand amortization is also one of the measures used by the investing community to value the business.

2015 Annual Report Shaw Communications Inc. 21

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Relative increases period-over-period in operating income before restructuring costs and amortization and in operating marginare indicative of the Company’s success in delivering valued products and services, and engaging programming content to itscustomers in a cost-effective manner.

Year ended August 31,(millions of Canadian dollars) 2015 2014

Operating income 1,432 1,439Add back (deduct):

Restructuring costs 52 58Amortization:

Deferred equipment revenue (78) (69)Deferred equipment costs 164 142Property, plant and equipment, intangibles and other 809 692

Operating income before restructuring costs and amortization 2,379 2,262

Operating marginOperating margin is calculated by dividing operating income before restructuring costs and amortization by revenue.

Free cash flowFree cash flow is calculated as operating income before restructuring costs and amortization, less interest, cash taxes paid orpayable, capital expenditures (on an accrual basis and net of proceeds on capital dispositions and adjusted to exclude amountsfunded through the accelerated capital fund) and equipment costs (net), adjusted to exclude share-based compensationexpense, less cash amounts associated with funding the new and assumed CRTC benefit obligations related to the acquisitionof Shaw Media as well as excluding non-controlling interest amounts that are consolidated in the operating income beforerestructuring costs and amortization, capital expenditure and cash tax amounts. Free cash flow also includes changes inreceivable related balances with respect to customer equipment financing transactions as a cash item, and is adjusted forrecurring cash funding of pension amounts net of pension expense. Dividends paid on the Company’s Cumulative RedeemableRate Reset Preferred Shares are also deducted.

Free cash flow has not been reported on a segmented basis. Certain components of free cash flow including operating incomebefore restructuring costs and amortization, CRTC benefit obligation funding, and non-controlling interest amounts continue tobe reported on a segmented basis. Capital expenditures (on an accrual basis net of proceeds on capital dispositions) andequipment costs (net) are reported on a combined basis for Consumer and Business Network Services due to the commoninfrastructure while Business Infrastructure Services and Media are separately reported. Other items, including interest andcash taxes, are not generally directly attributable to a segment, and are reported on a consolidated basis.

22 Shaw Communications Inc. 2015 Annual Report

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

The Company uses free cash flow as a measure of the Company’s ability to repay debt and return cash to shareholders.Consolidated free cash flow is calculated as follows:

Year ended August 31,(millions of Canadian dollars) 2015 2014(3)

RevenueConsumer 3,752 3,768Business Network Services 520 484Business Infrastructure Services 246 –Media 1,080 1,096

5,598 5,348Intersegment eliminations (110) (107)

5,488 5,241

Operating income before restructuring costs and amortization(1)

Consumer 1,686 1,669Business Network Services 256 240Business Infrastructure Services 95 –Media 342 353

2,379 2,262

Capital expenditures and equipment costs (net):(2)

Consumer and Business Network Services 954 1,077Business Infrastructure Services 152 –Media 16 18

1,122 1,095Accelerated Capital Fund Investment(1) (150) (240)

Total 972 855

Free cash flow before the following 1,407 1,407Less

Interest (281) (264)Cash taxes (375) (359)

Other adjustments:Non-cash share-based compensation 4 3CRTC benefit obligation funding (31) (58)Non-controlling interests (26) (31)Pension adjustment (45) (5)Customer equipment financing 13 18Preferred share dividends (13) (13)

Free cash flow 653 698

Operating margin(1)

Consumer 44.9% 44.3%Business Network Services 49.2% 49.6%Business Infrastructure Services 38.6% n/aMedia 31.7% 32.2%

(1) Refer to Key performance drivers.(2) Per Note 24 to the audited Consolidated Financial Statements.(3) Restated to reflect the change in segment reporting whereby residential and enterprise services that were

included in the Cable and Satellite segments are now realigned into new Consumer and Business NetworkServices segments.

2015 Annual Report Shaw Communications Inc. 23

Shaw Communications Inc.Management’s Discussion and AnalysisAugust 31, 2015

Accelerated capital fundDuring 2013, the Company established a notional fund, the accelerated capital fund, of up to $500 million with proceedsreceived, and to be received, from several strategic transactions. The accelerated capital initiatives were funded through thisfund and not cash generated from operations. Key investments included the Calgary data centres, further digitization of thenetwork and additional bandwidth upgrades, development of IP delivery of video, expansion of the Shaw Go WiFi network, andadditional innovative product offerings related to Shaw Go and other applications to provide an enhanced customer experience.Approximately $110 million was invested in fiscal 2013, $240 million was invested in fiscal 2014 and $150 million investedin fiscal 2015.

Statistical MeasuresSubscriber counts (or Revenue Generating Units (“RGUs”)), including penetration and bundled customersThe Company measures the count of its customers in its Consumer and Business Network Services divisions. Cable videosubscribers include residential customers, multiple dwelling units (“MDUs”) and commercial customers. A residentialsubscriber who receives at a minimum, basic cable service, is counted as one subscriber. In the case of MDUs, such asapartment buildings, each tenant with a minimum of basic cable service is counted as one subscriber, regardless of whetherinvoiced individually or having services included in his or her rent. Each building site of a commercial customer (e.g., hospitals,hotels or retail franchises) that is receiving at a minimum, basic cable service, is counted as one subscriber. Satellite videosubscribers are counted in the same manner as cable video customers except that they also include seasonal customers whohave indicated their intention to reconnect within 180 days of disconnection. Internet customers include all modems on billingand Phone lines includes all phone lines on billing. All subscriber counts exclude complimentary accounts but includepromotional accounts.