should the financial sector be regulated by government? dr. j. d. han

TRANSCRIPT

Should the Financial Sector be Regulated by Government?

Dr. J. D. Han

Should Government Regulate the Financial Sector?

Pros

“ It should for the reasons …..”

Cons

“It should NOT for the reasons ……” Empirical/Historical Evidence

Alternatives to Government Regulation

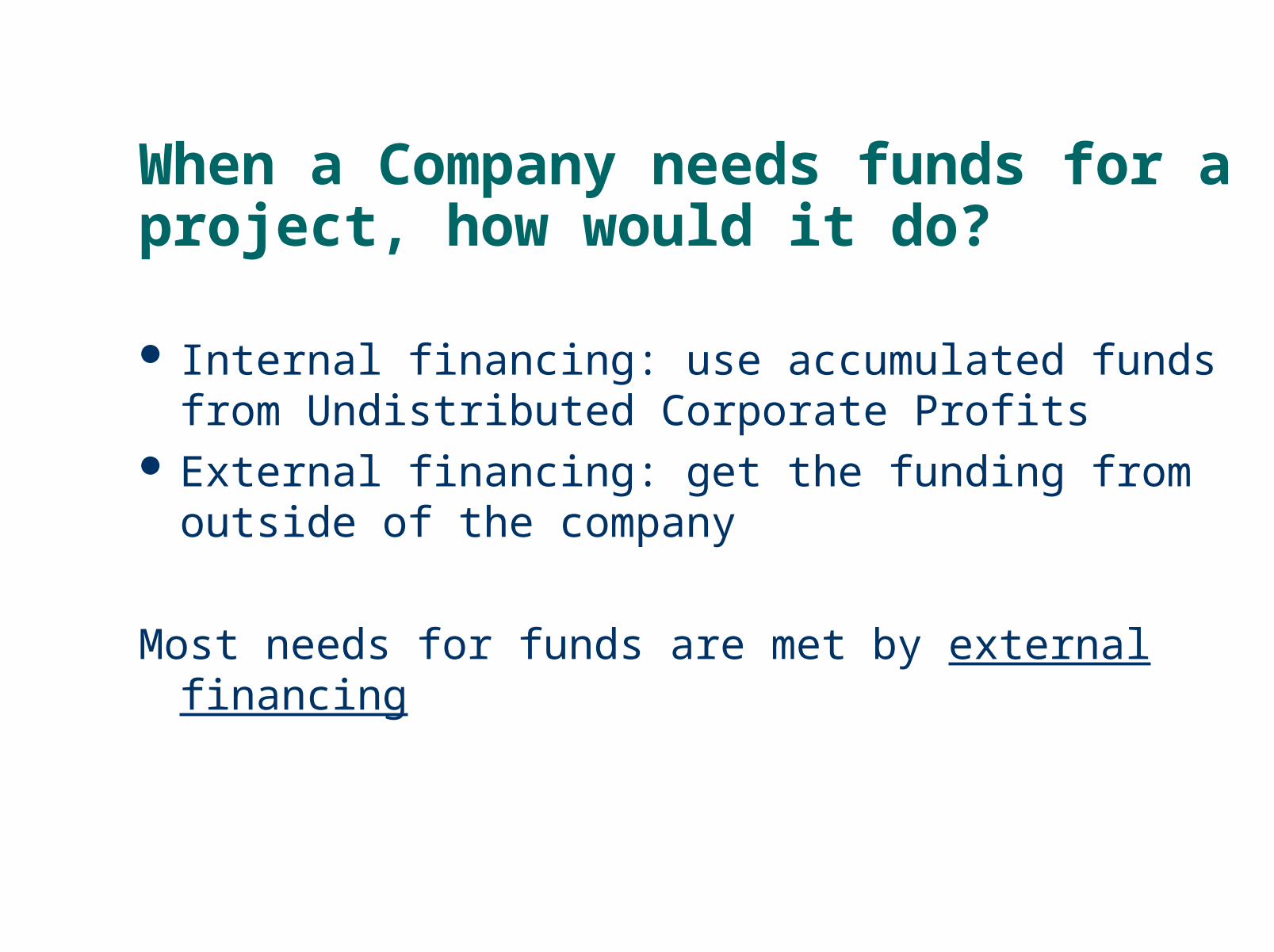

When a Company needs funds for a project, how would it do?

Internal financing: use accumulated funds from Undistributed Corporate Profits

External financing: get the funding from outside of the company

Most needs for funds are met by external financing

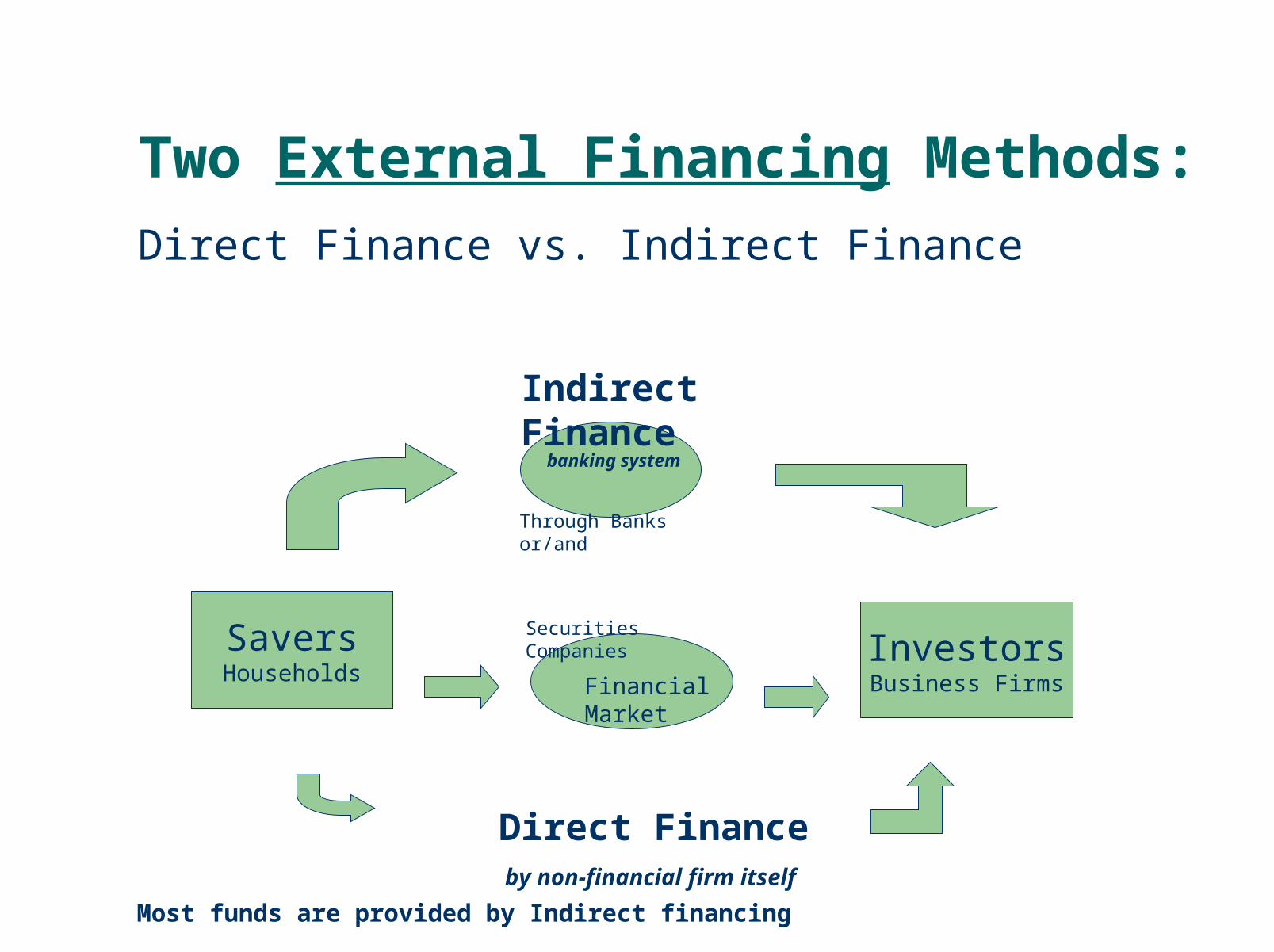

Two External Financing Methods:

Direct Finance vs. Indirect Finance

SaversHouseholds

InvestorsBusiness Firms

Indirect Finance

Direct Finance by non-financial firm itself

Financial Market

banking system

Through Banks or/and

Securities Companies

Most funds are provided by Indirect financing

Financial Intermediaries consists of

Depository Institutions (banks, trust co., credit unions),

Investment Intermediaries (securities co., finance co.),

And Contractual Savings Institutions (insurance co, pension funds).

Financial Intermediaries channel surplus funds from Savers to Investors

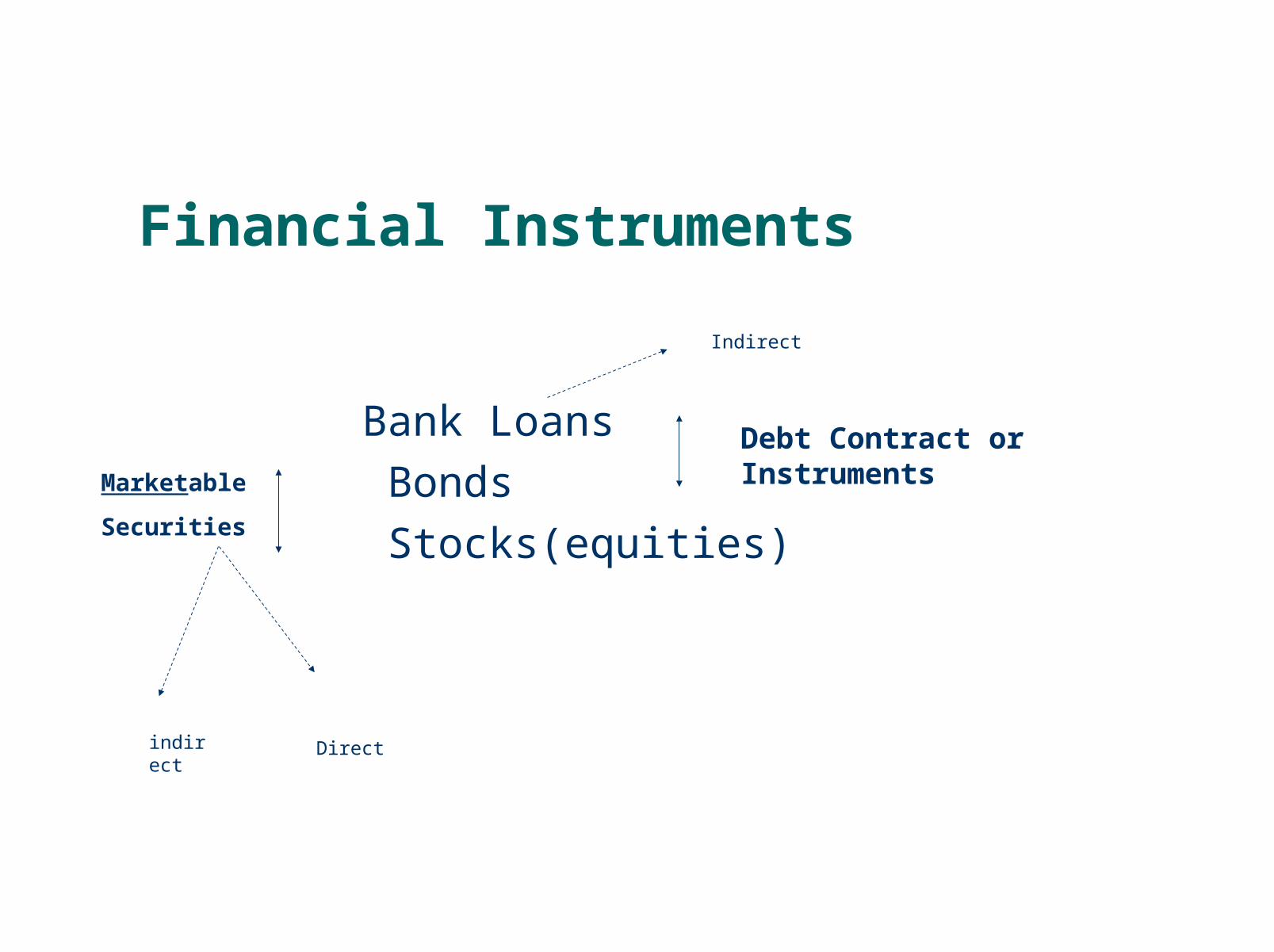

Financial Instruments

Bank Loans

Bonds

Stocks(equities)

Debt Contract or InstrumentsMarketable

Securities

Directindirect

Indirect

Pros

The financial sector is full of dangers, hazards and risks.

And we do not have enough information about them.

Thus government should regulate the financial sector and enforce information disclosure.

Note that

The biggest problem is ‘Information Asymmetry’

between the bona-fide investors and the financial sector players involved in direct and indirect financing (those using the funds, issuers/dealers of marketable securities, and other intermediaries)

The government regulations come in many forms and include (Financial) Information Disclosure Requirements on the financial sector players.

They take the following example:

Those arguing for government regulation use the following logics:

(1) Financial sector has a lot of hazards, risks and dangers;

(2) The general public as investors do not have enough information about them.

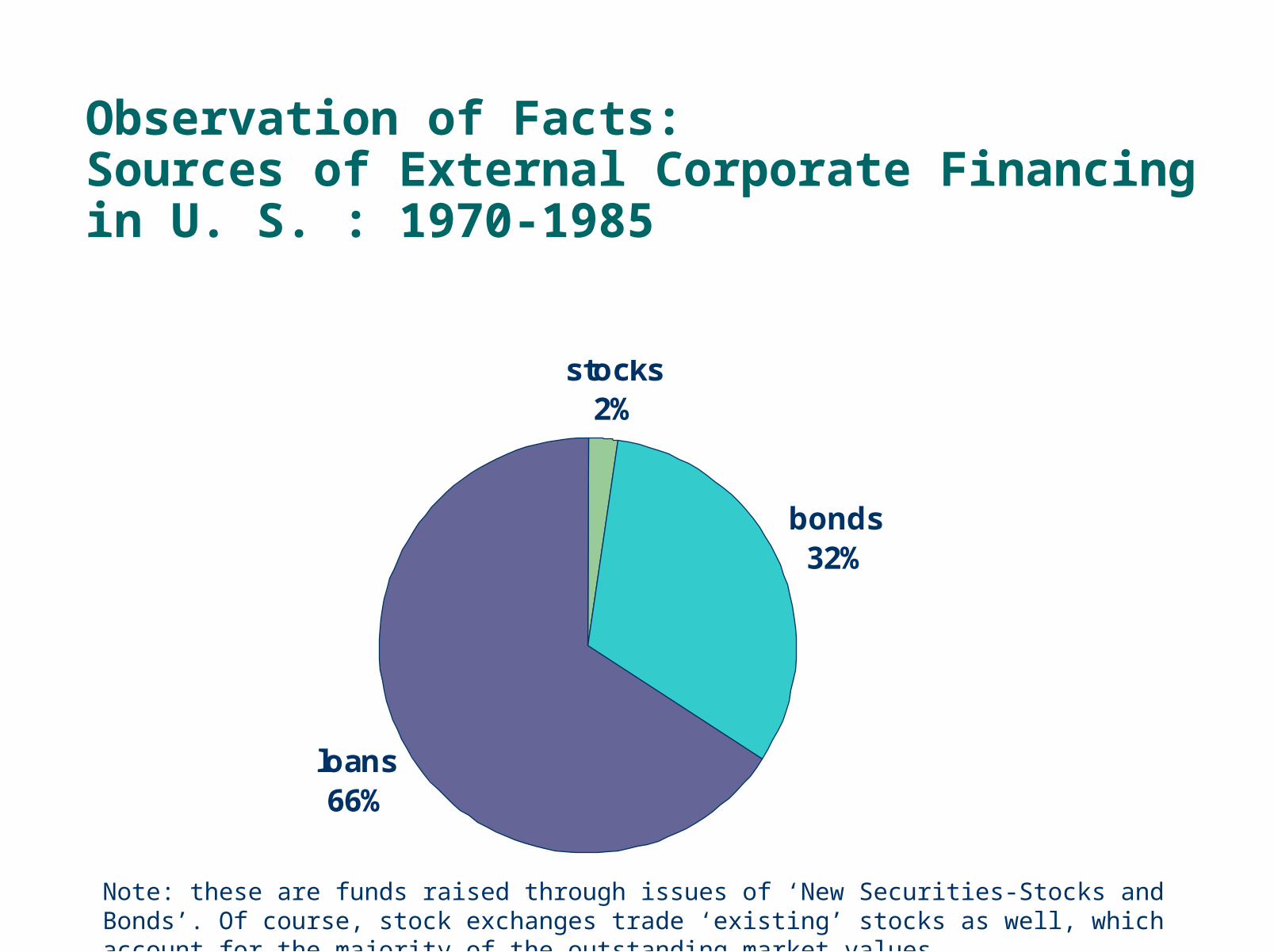

Observation of Facts:Sources of External Corporate Financingin U. S. : 1970-1985

stocks2%

bonds32%

loans66%

Note: these are funds raised through issues of ‘New Securities-Stocks and Bonds’. Of course, stock exchanges trade ‘existing’ stocks as well, which account for the majority of the outstanding market values.

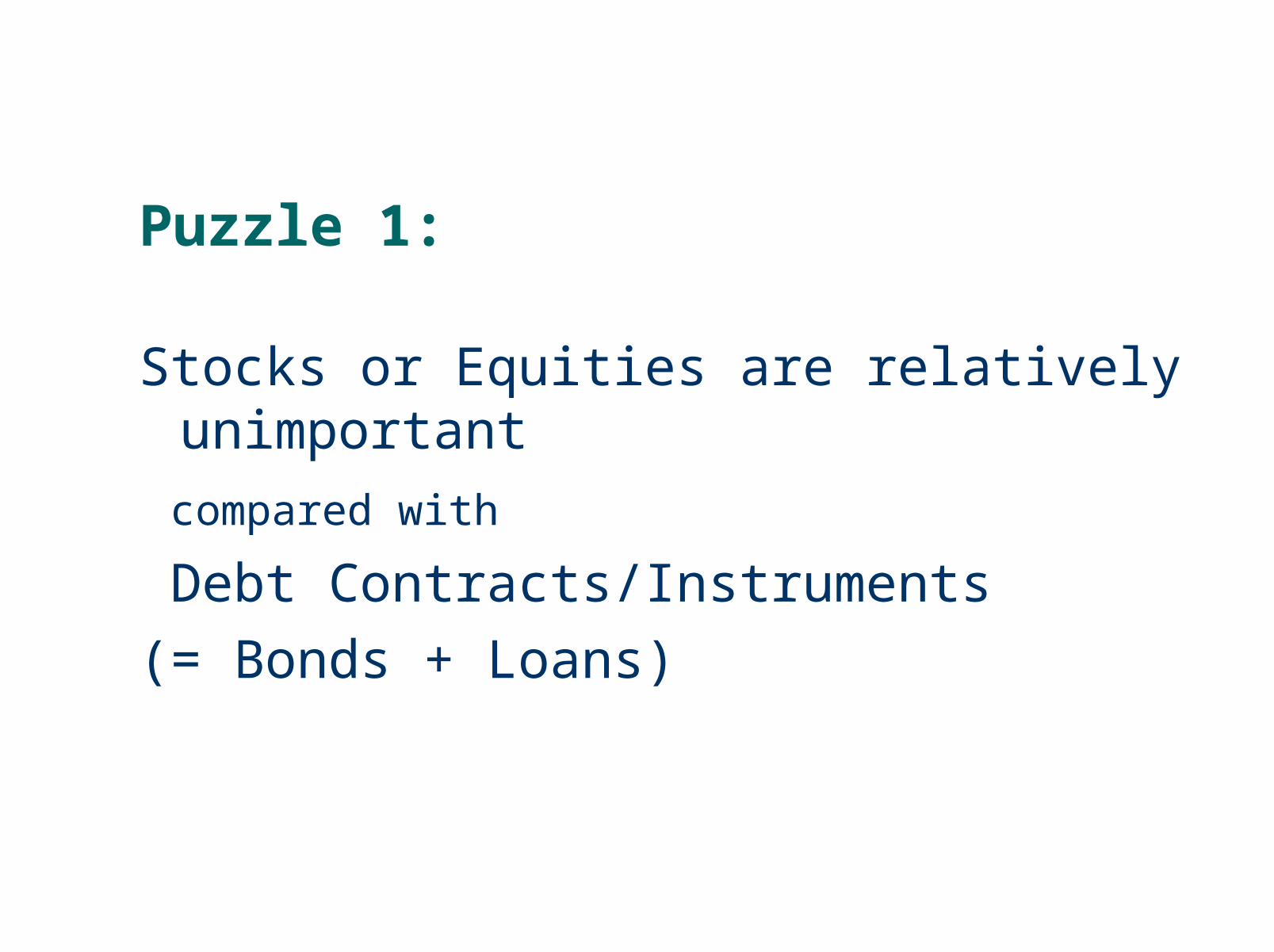

Puzzle 1:

Stocks or Equities are relatively unimportant

compared with

Debt Contracts/Instruments

(= Bonds + Loans)

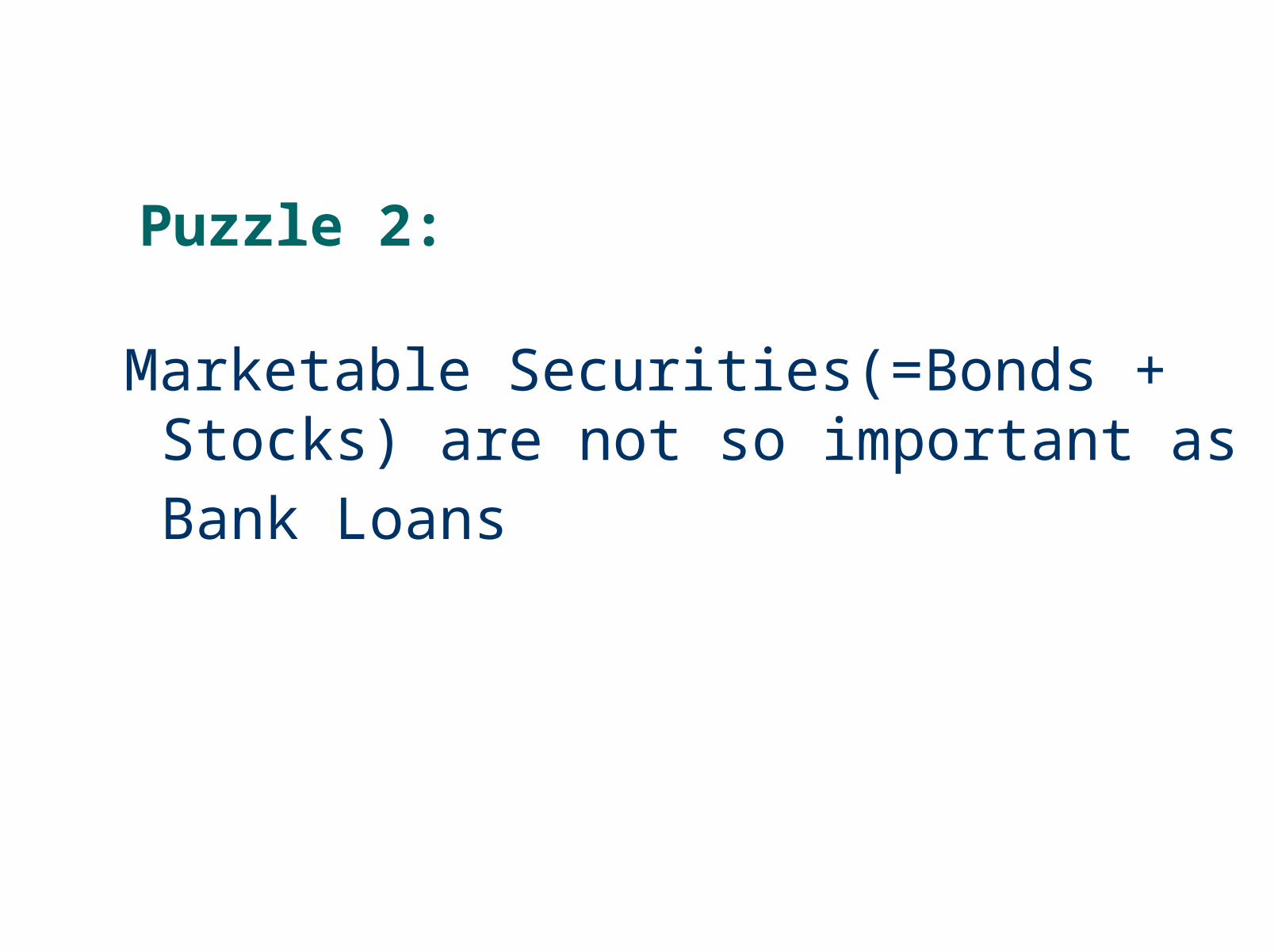

Puzzle 2:

Marketable Securities(=Bonds + Stocks) are not so important as Bank Loans

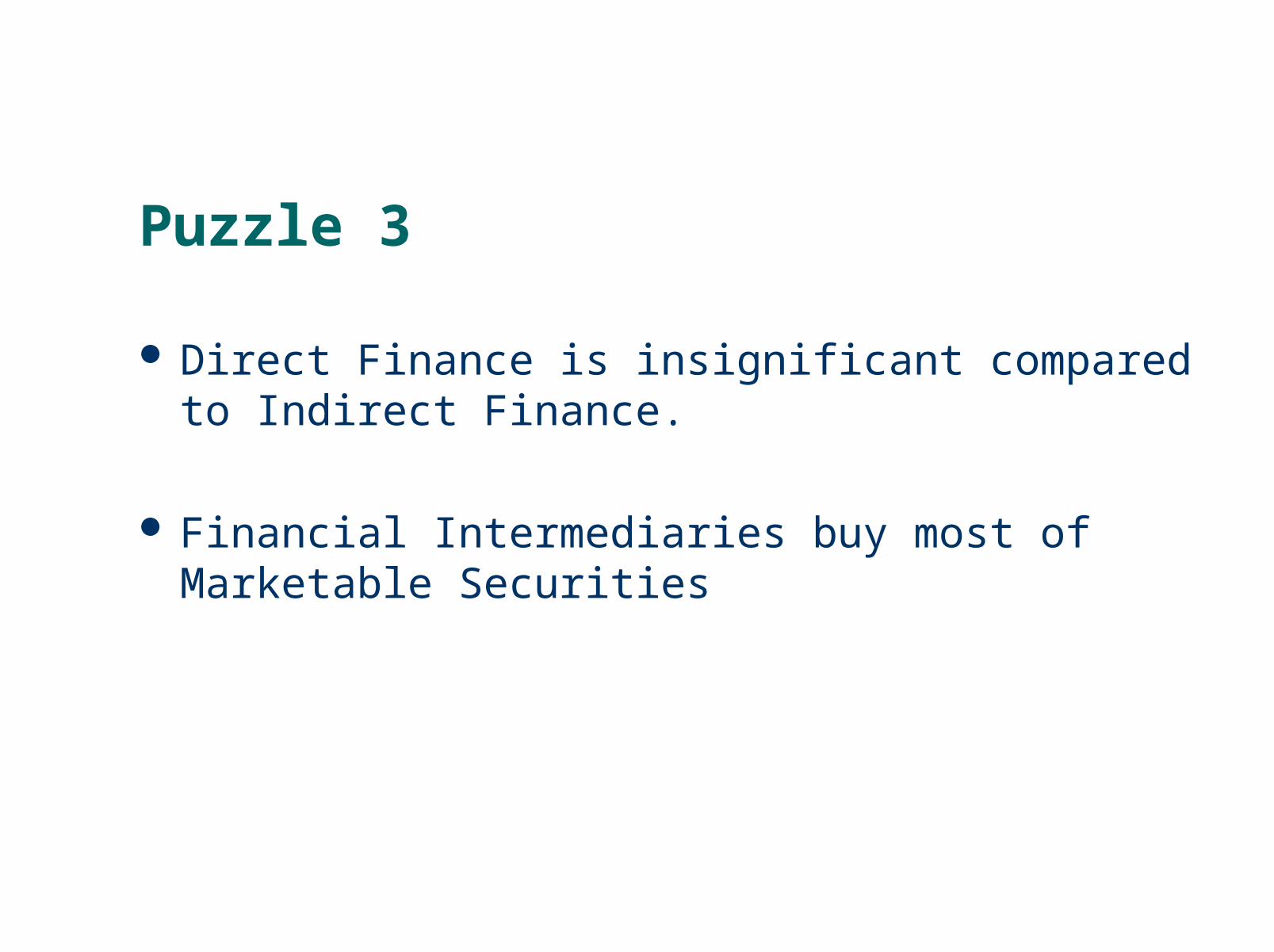

Puzzle 3

Direct Finance is insignificant compared to Indirect Finance.

Financial Intermediaries buy most of Marketable Securities

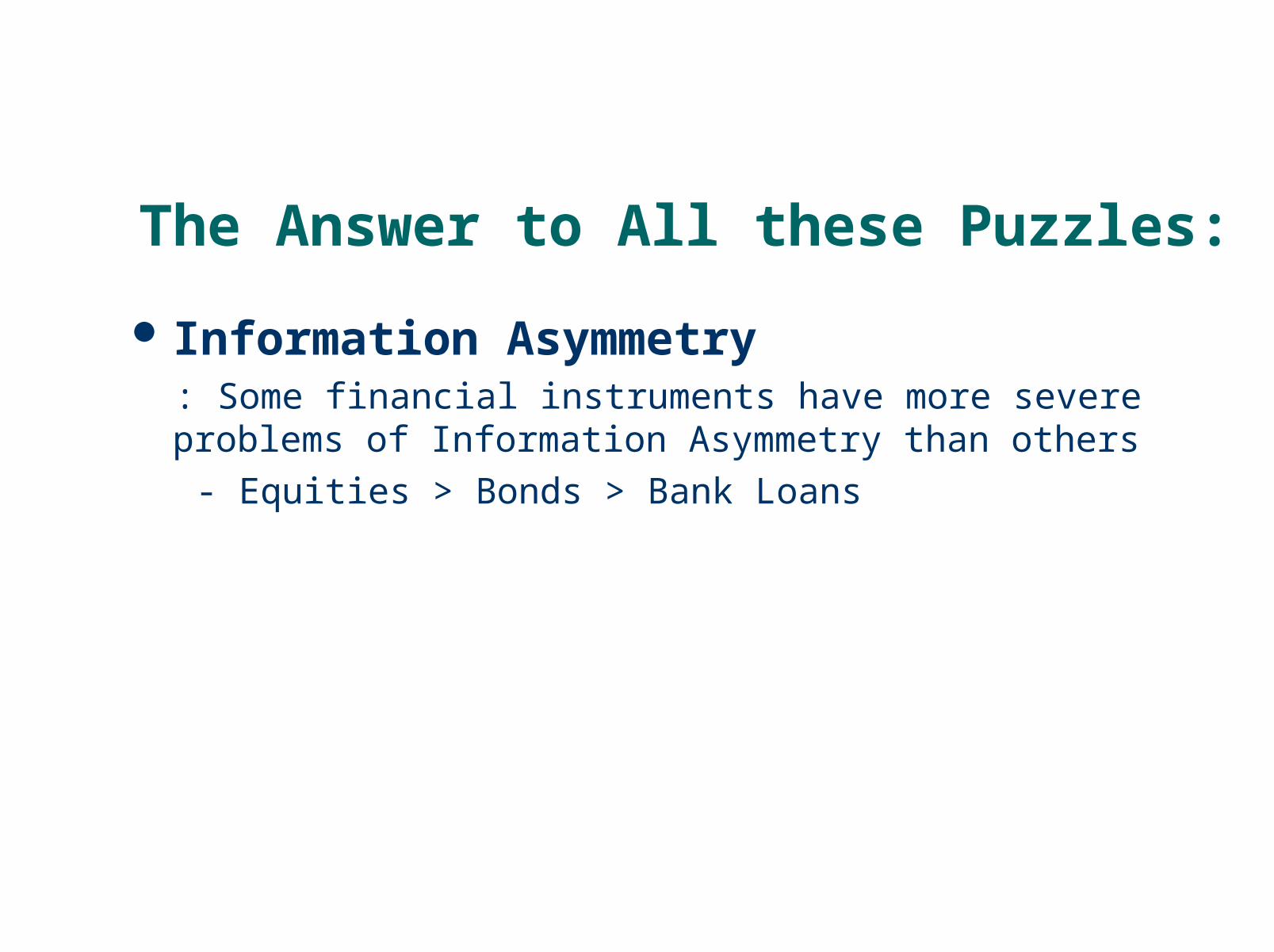

The Answer to All these Puzzles:

Information Asymmetry : Some financial instruments have more severe problems of

Information Asymmetry than others

- Equities > Bonds > Bank Loans

Other minor answers:

Transactions Costs

: Financial Institutions or Intermediaries lower Transactions Cost

Capital Structure (Comparative Cost of Funding)

: - interest payment is tax-deductible

- real cost of borrowing is the (actual) real interest rate (=nominal interest rate – inflation rate)

Issues of Management Control and a Possible Hostile Take Over

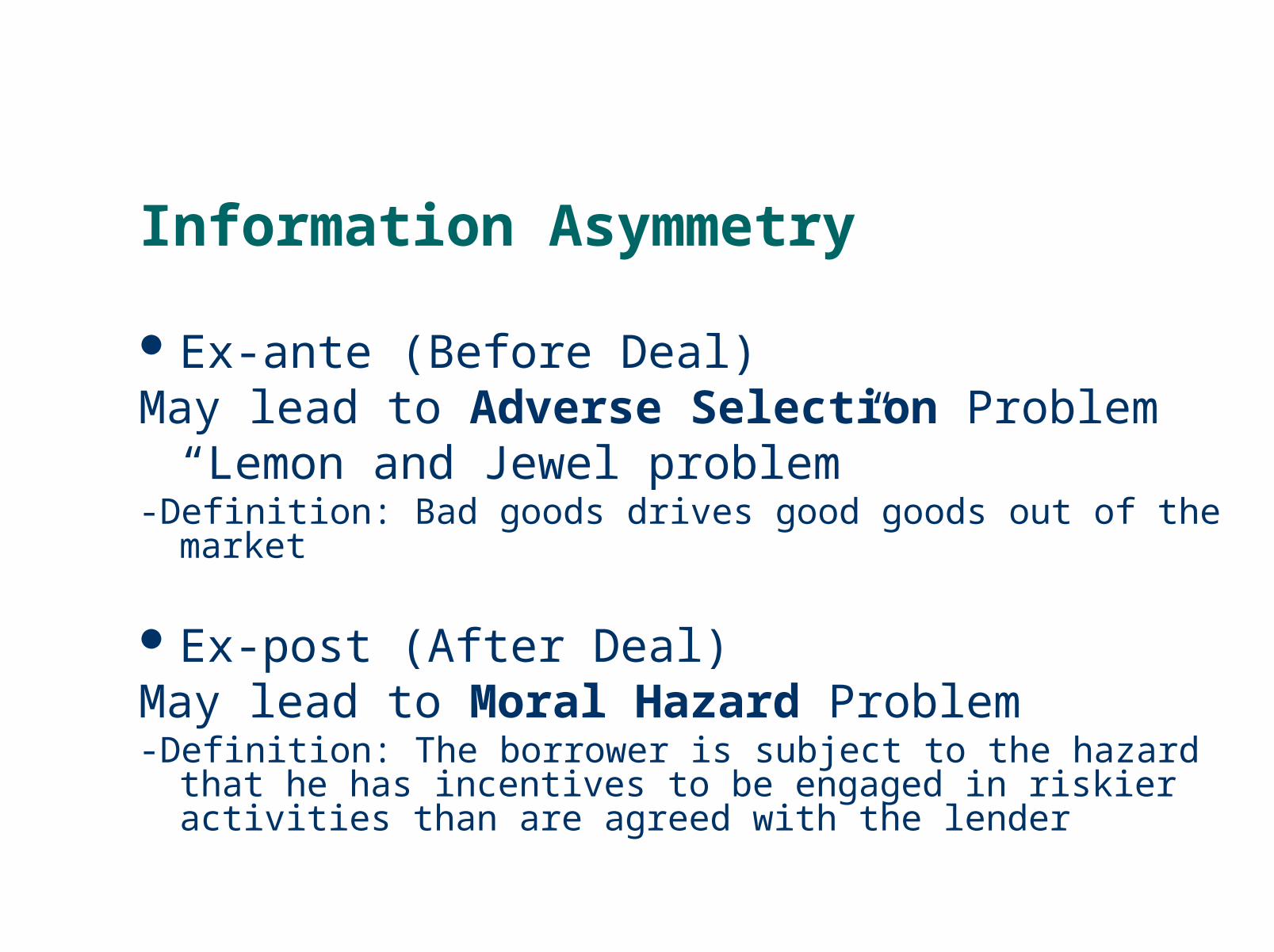

Information Asymmetry

Ex-ante (Before Deal)May lead to Adverse Selection Problem

“Lemon and Jewel problem” -Definition: Bad goods drives good goods out of the market

Ex-post (After Deal)May lead to Moral Hazard Problem-Definition: The borrower is subject to the hazard that he has

incentives to be engaged in riskier activities than are agreed with the lender

Marketable Securities(Direct Finance) versus Bank Loans (Indirect Finance)

Information Asymmetry causes a severe Adverse Selection Problem or “Lemon & Jewel” Problem in the case of all marketable securities

bank loans are less subject to information asymmetry(cause) or adverse selection(consequence). Why? The key lies in that enough information is generated about the demander of the fund in the case of bank loans while, due to information free rider problem, it is not the case for marketable securities.

As bank loans are less risky than marketable securities- Thus, the financial investor prefers bank loans to marketable securities.

Closer Look reveals

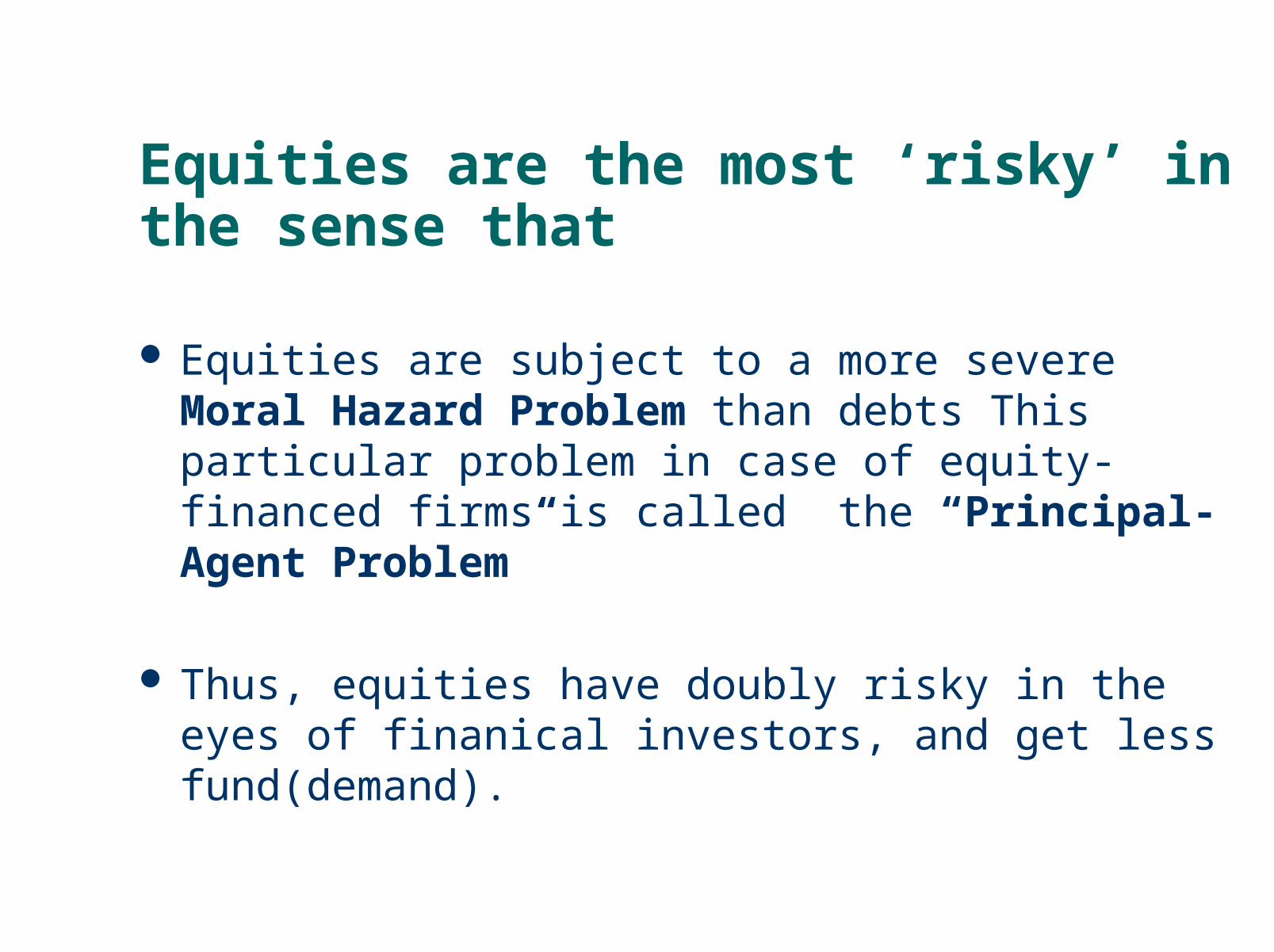

Equities are the most ‘risky’ in the sense that

Equities are subject to a more severe Moral Hazard Problem than debts This particular problem in case of equity-financed firms is called the “Principal-Agent Problem”

Thus, equities have doubly risky in the eyes of finanical investors, and get less fund(demand).

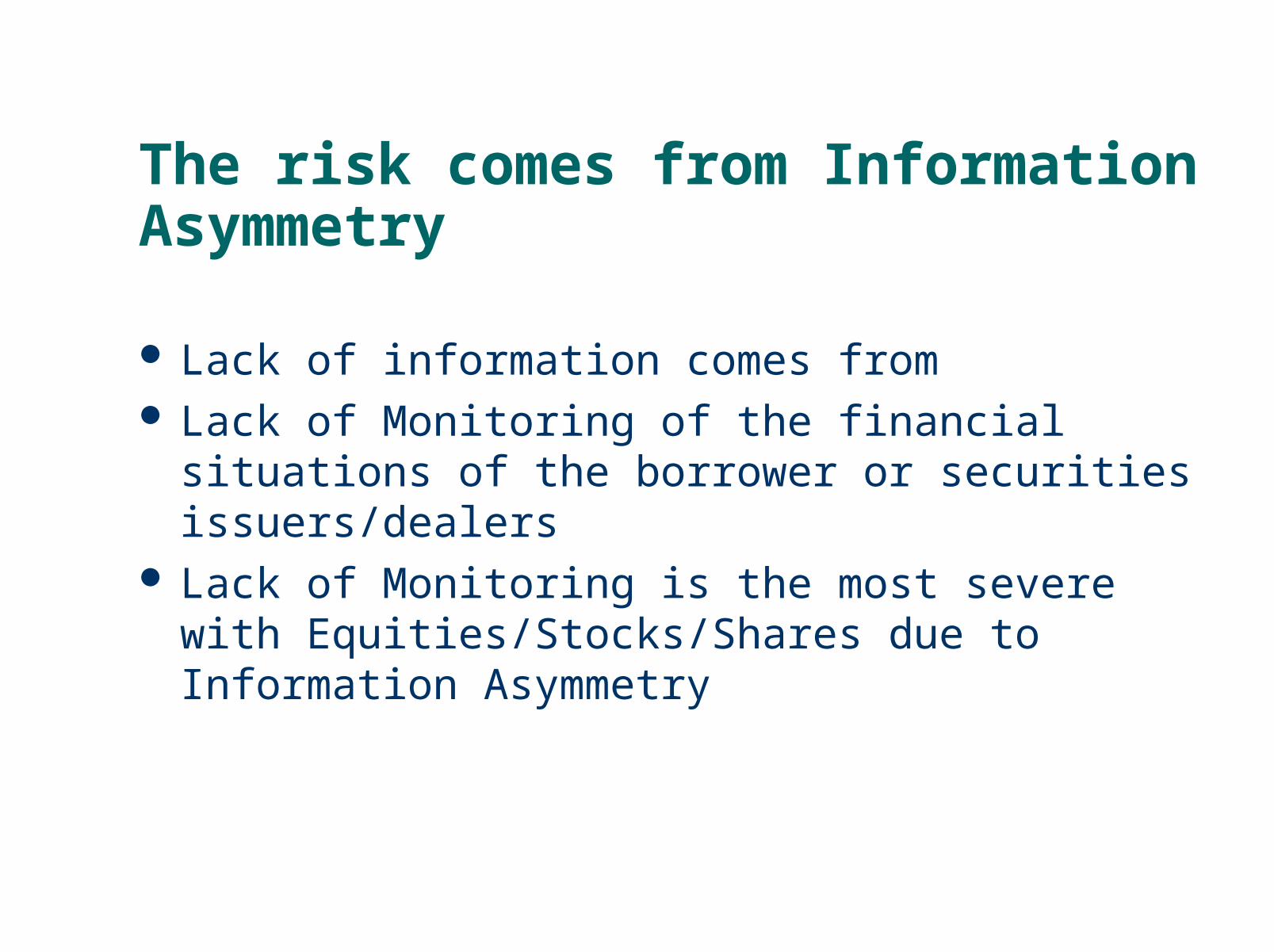

The risk comes from Information Asymmetry

Lack of information comes from Lack of Monitoring of the financial situations of the

borrower or securities issuers/dealers Lack of Monitoring is the most severe with

Equities/Stocks/Shares due to Information Asymmetry

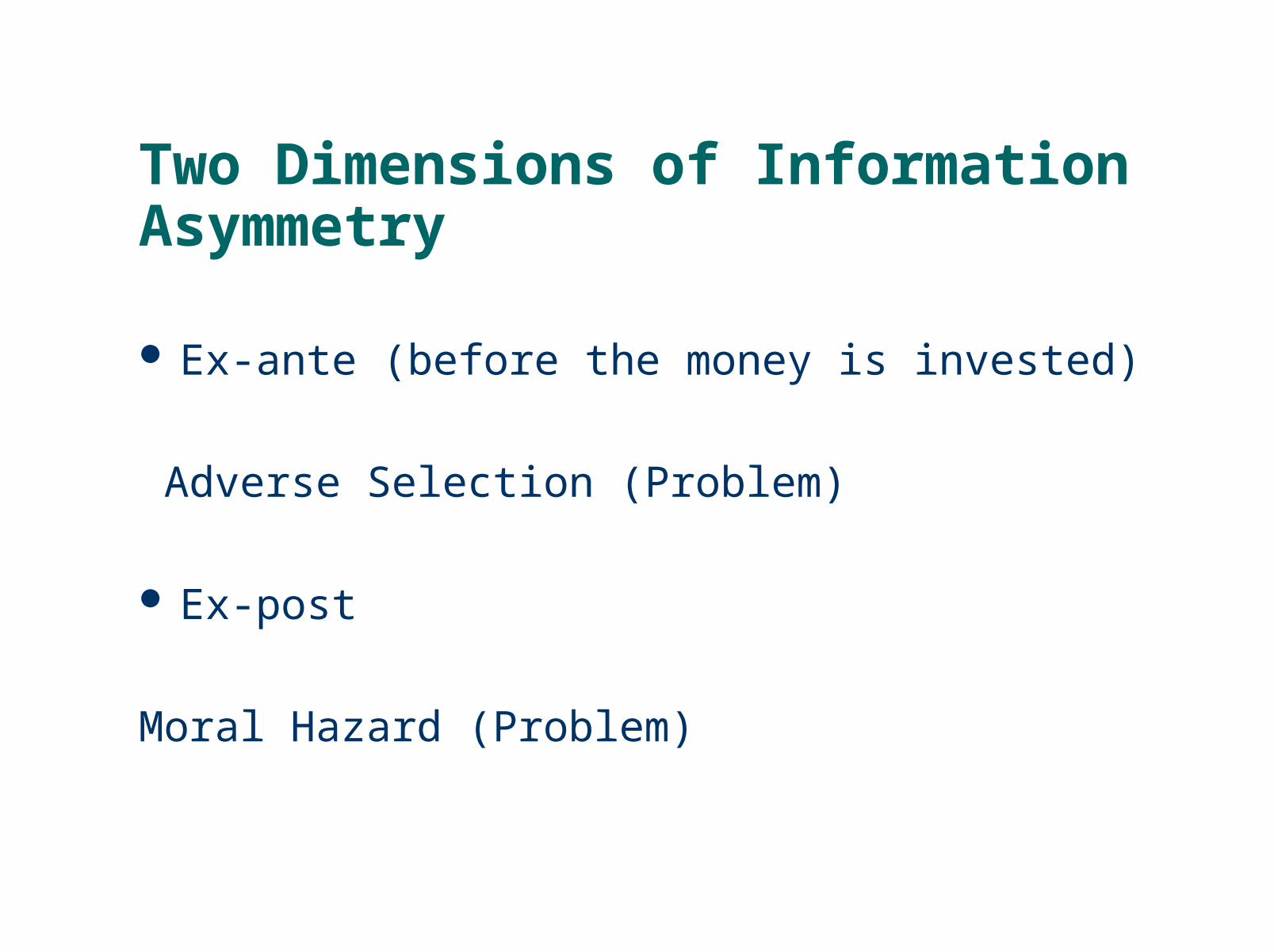

Two Dimensions of Information Asymmetry

Ex-ante (before the money is invested)

Adverse Selection (Problem)

Ex-post

Moral Hazard (Problem)

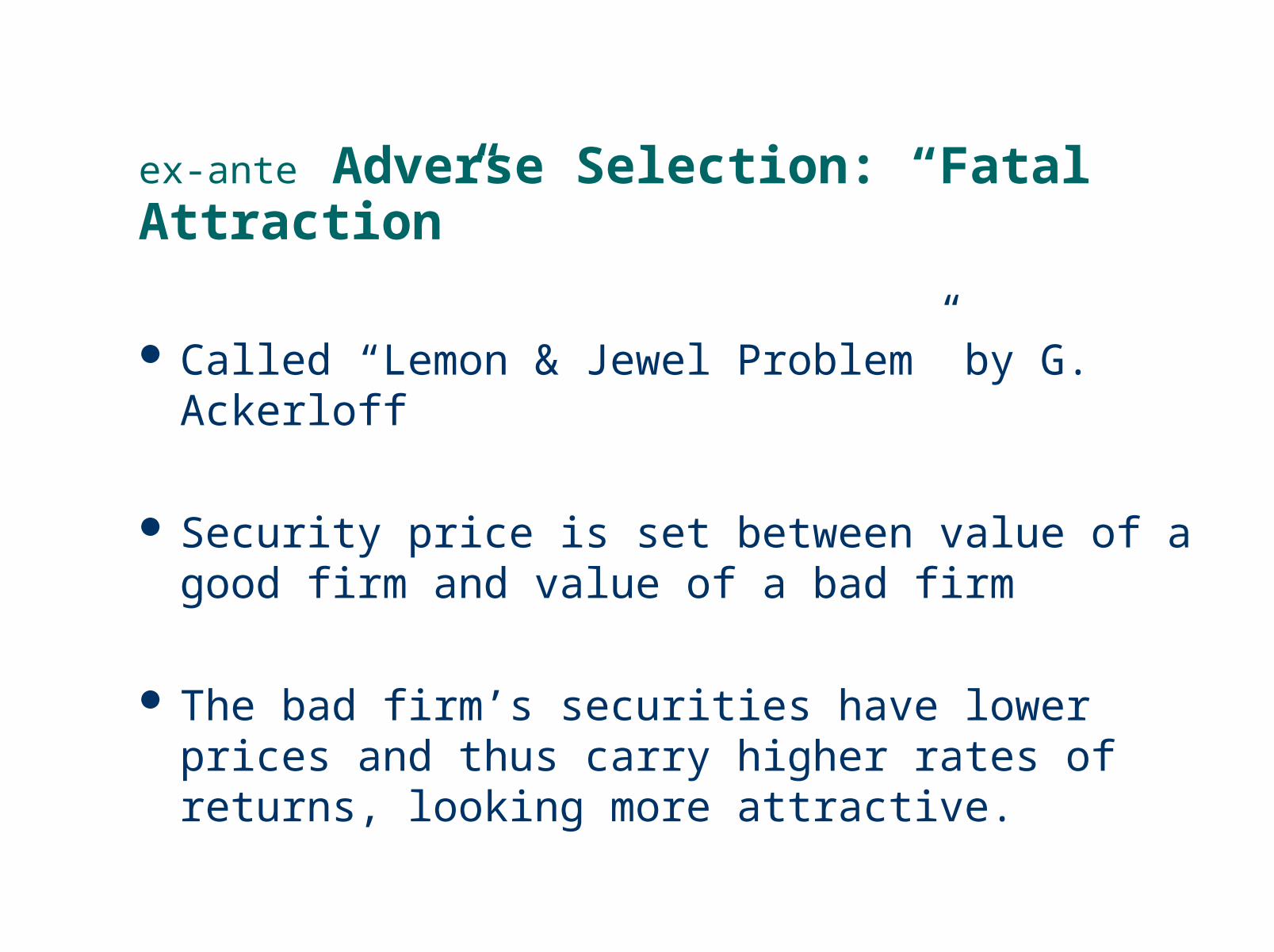

ex-ante Adverse Selection: “Fatal Attraction”

Called “Lemon & Jewel Problem” by G. Ackerloff

Security price is set between value of a good firm and value of a bad firm

The bad firm’s securities have lower prices and thus carry higher rates of returns, looking more attractive.

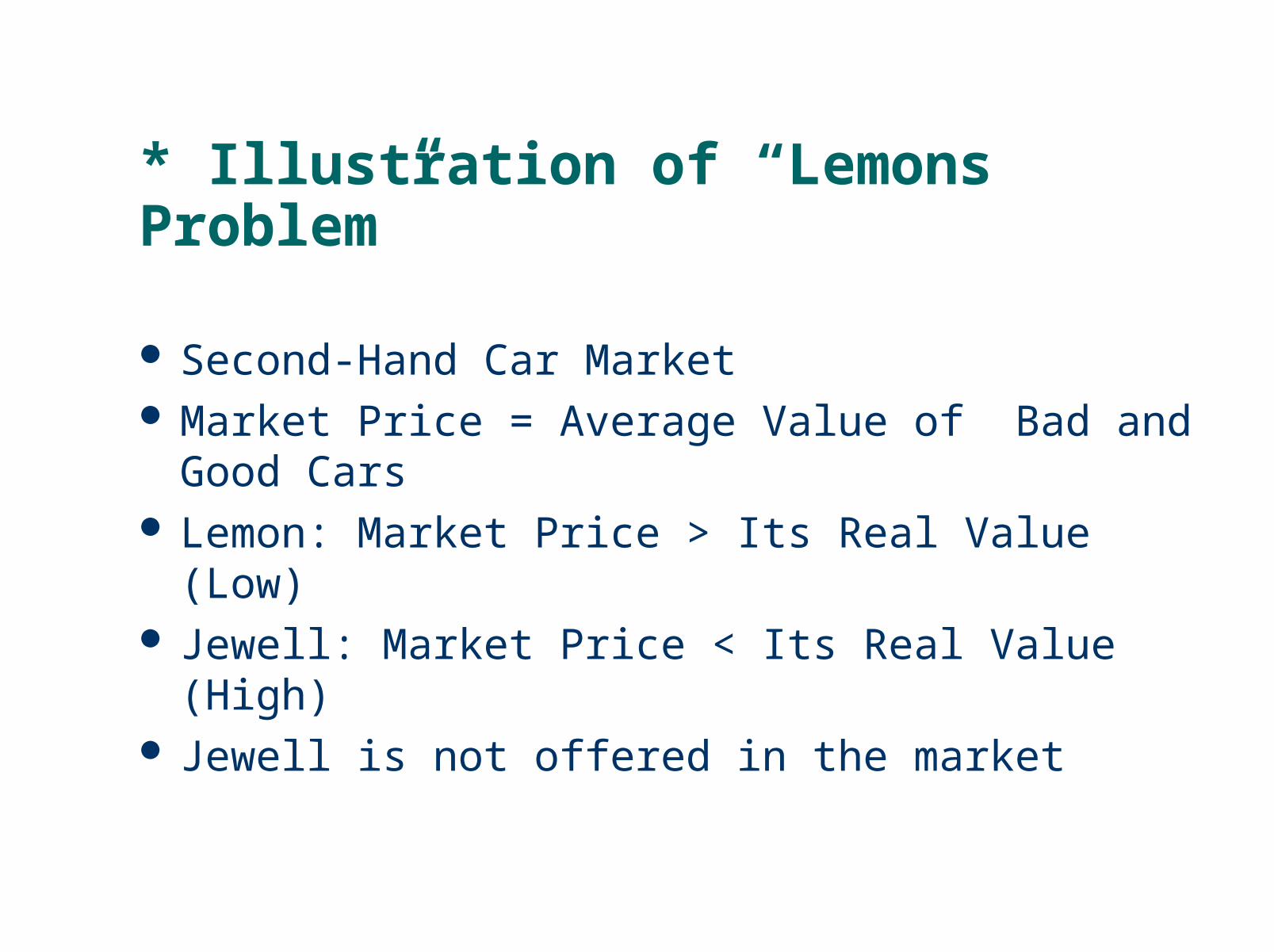

* Illustration of “Lemons Problem”

Second-Hand Car Market Market Price = Average Value of Bad and Good Cars Lemon: Market Price > Its Real Value (Low) Jewell: Market Price < Its Real Value (High) Jewell is not offered in the market

ex-post Moral Hazard Problem

Once the money is invested, the fund borrower or the securities issuers get engaged in more risky activities than are warranted. Here the hazard is endogenously increased by the user of the fund.

* Solutions to Adverse Selection

Custom-Made Private Information Financial intermediaries are specialized in collecting and processing

information-> explains why bank loans dominates: in case of bank loans, almost

complete information is generated. The remaining information asymmetry of the borrow is small. Of course, still there remains information asymmetry between banks and their depositors.

Private Provision of Information: Demand and supply of information leads to formation of

Information Market, where Information is generate and sold. : It is ultimately incomplete due to “Free Rider Problem” in the

Financial Market Public Provision of Information particularly is warranted and required for Securities Market-> explains why financial industry is heavily regulated

* Solutions to Moral Hazard Problem

Production of Information: “Monitoring” - The most severe problem exists, and “costly state verification’ and free-rider problem

will lead to insufficient monitoring in the stock market

- The same is true, if to a lesser extent, in the bond market

- The least severe problem, but collateral is inevitable in the bank loan market

Government Regulation to increase Information:

- “Disclosure Requirement”

Directly Participating in Management- Venture Capital Firm

- Japanese and German Banks

(Recap) Why should the financial industry be regulated by government?

Because information asymmetry is an intrinsic problem of the industry: adverse selection and moral hazards

-> First level of ‘Market Failure’ Unlike other sectors, due to free rider problem, information

asymmetry is not to be rectified by Private Provision of Information

-> Second level of ‘Market Failure’ = failure of Information Market

Ultimately, Public Provision of Information is required,which calls for Government Regulation

Cons: Government should not regulate the financial industry:

This revisionist view has been gaining an increasing popluarity in relation to finanical liberalization.

(Revisionist) The financial sector need not be regulated by government.

Information Asymmetry itself does not warrant Government Regulation

The key lies in Efficiency of Information

If enough information is generated and transmitted in the unregulated or free-market financial sector so as to ensure that the investor with due diligence or prudence may be protected from frauds in a reasonable way to a certain acceptable degree, then government intervention is not necessary.

What does the Empirical Evidence tell us?

Theoretically, it is possible, and empirically, there is a historical evidence

from the 18th century Scottish Free Banking System experiences(Banks) ;

from the 17th century Stock Market in Amsterdam(Securities Market);

from the 20th century Financial Crises in the U.S.

1) Free Banking: Free Entry and Self Regulated Note Issues

Historical Instances of Self-Regulated, or Free-Market Financial Industry

Scotland: 1720-1840 U. S. A.: 1836/7-1863 Canada: prior to Bank of Canada 1935 Sweden: 19C Hong Kong: Contemporary

Were They Stable?

Conventional Wisdom

-> Yes, Scotland, Canada, Sweden and HK

-> “No”, U. S. A.

We would like to challenge the second part of Conventional Wisdom

Scottish Free Banking:

Period: 1720-1840 How did it work?:-Banks could print out paper monies, or notes as long as

they do not default on redemption request of the notes for species

-No government charter needed; Self regulated, competitive (free market driven) supply of

money and banking practices

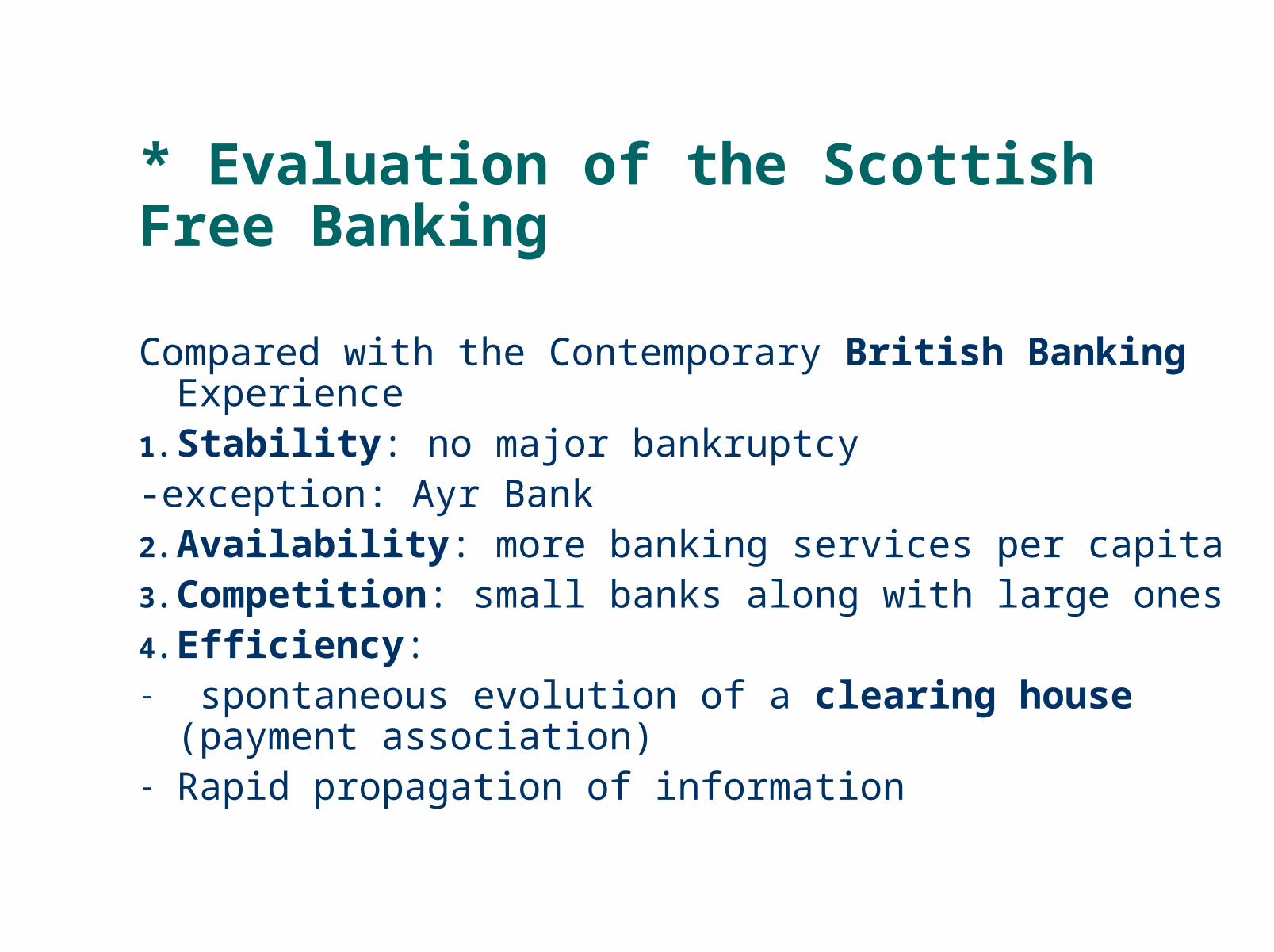

* Evaluation of the Scottish Free Banking

Compared with the Contemporary British Banking Experience

1. Stability: no major bankruptcy -exception: Ayr Bank2. Availability: more banking services per capita3. Competition: small banks along with large ones4. Efficiency: - spontaneous evolution of a clearing house (payment

association) - Rapid propagation of information

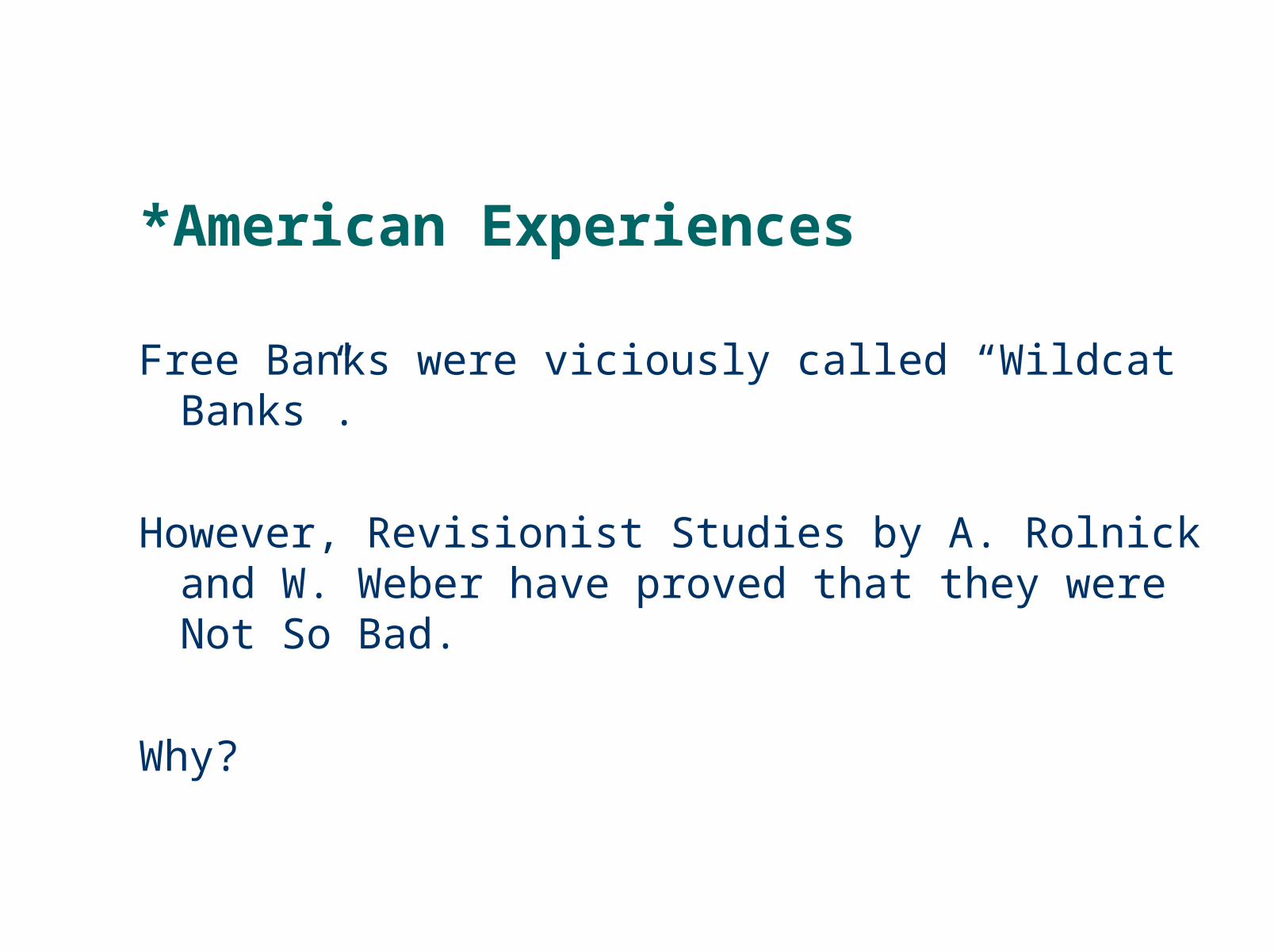

*American Experiences

Free Banks were viciously called “Wildcat Banks”.

However, Revisionist Studies by A. Rolnick and W. Weber have proved that they were Not So Bad.

Why?

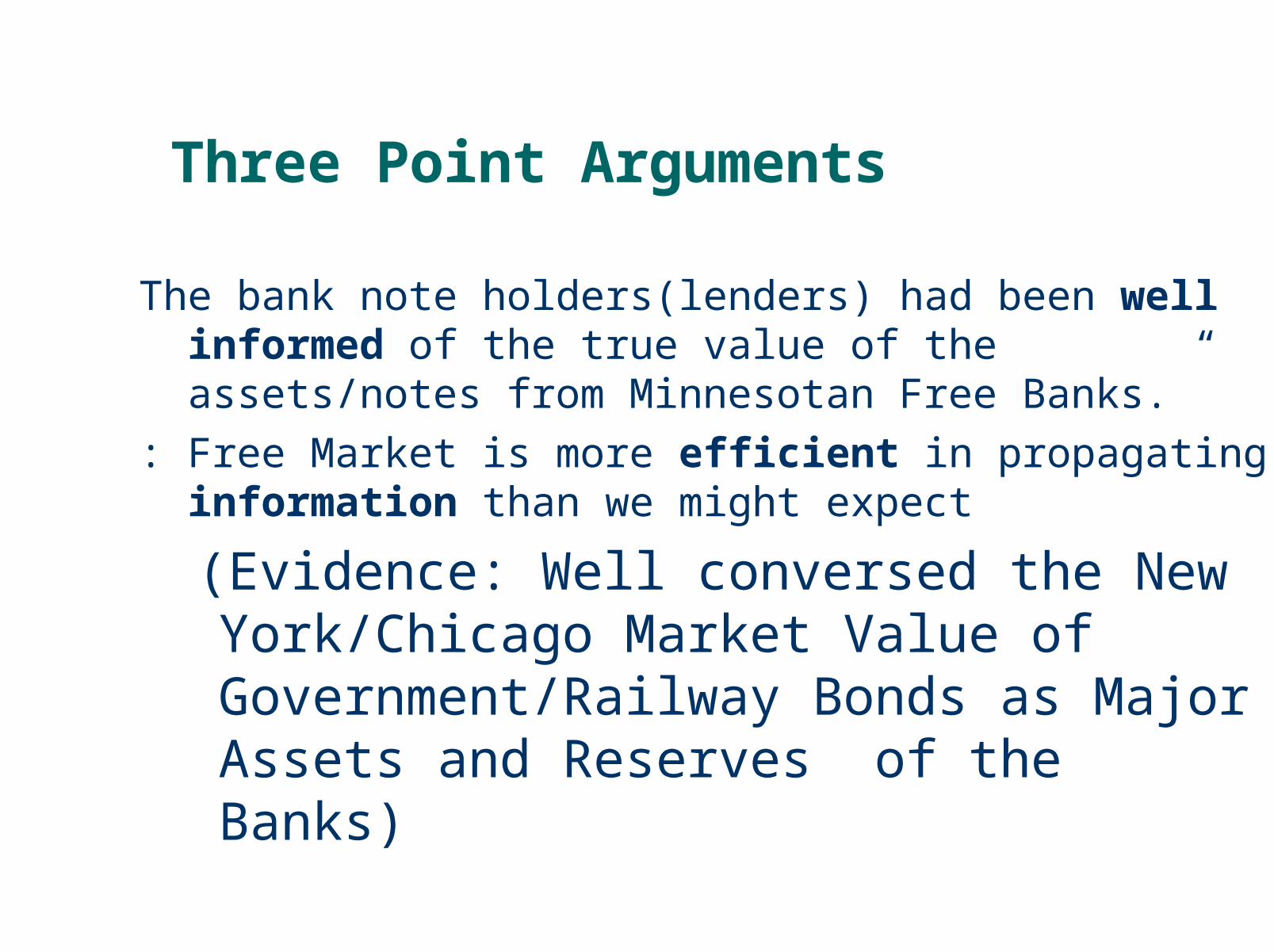

Three Point Arguments

The bank note holders(lenders) had been well informed of the true value of the assets/notes from Minnesotan Free Banks.”

: Free Market is more efficient in propagating information than we might expect

(Evidence: Well conversed the New York/Chicago Market Value of Government/Railway Bonds as Major Assets and Reserves of the Banks)

Lessons to be Learned from Free Banking Experiences

Self-Regulated,

Regulation-Free,

Banking/Financial Industry may be Viable

and even be superior.

2) Securities Market without Regulation

From studies on the Amsterdam Bourse of the 17th century, Edward Stringham of UC San Jose, concludes:

“…In the 1600s, the first century when equities were traded, there occurred a number of financial innovations, which were out of the bound set by the government.

They included short-selling, securitization and others.

Contrary to the idea that the government is needed for financial innovation and contractual performance, the case of the Amsterdam Bourse provides evidence that securities markets can function successfully with little assistance from the state…..”

3) Financial Crises in the 20th Century

1980s Crisis involving Savings & Loans Companies

2000 Crisis involving Subprime Mortgage and Mortgage Backed Securities

Who caused the financial crisis?

It is the Regulator that set out the ‘wrong’ rules and regulations , and sent out ‘wrong’ signals to the general public and the financial market.

Read the article by Jeffrey Friedman, Editor, Critical Review.

Full version or

Summary version

Then, what are the alternatives?

We all know that Information Asymmetry is an intrinsic problem to the financial industry.

How can we help the Market Economy solve its own problems?

What are the market-endogenous, as opposed to exogenous government intervention, solutions to Information Asymmetry?

1) Information Revolution will raise information efficiency to its maximum

Information Revolution may resolve Information Free Rider Problem

Then there occurs a Perfect Market of Information which will (almost) resolve Information Asymmetry

Insider-trading may be legalized –M. Friedman-, which will enhance information efficiency

2) Mergers and Acquisitions will lead to More Information Disclosures

M & A targets Firms with severe problems of Principal and Agent (a Moral Hazard), and tries to correct them.

M & A process reveals Moral Hazard problems of the target firm.

M & A uses Leveraged Buy Out (LBO) with bonds, and replaces equities with bonds which carry more management monitoring through restrictive covenant.

3) New Forms of Financing rises for Close Management Monitoring Private Equity is complex and elusive.

-What it does? One major function is Mezzanine Financing (preferred stocks, and subordinated bonds) combines Equities and Bonds with best of both worlds – Lenders can constantly and closely monitor management.

-related (confusingly) with Venture Capital (relatively new), Merchant Banking (as old as in 16th century)

Japanese Banking, European Banking, and U.S. Financial Trusts(J.P. Morgan) before Glass-Steagall Act of 1933 by B. De Long

- Gramm-Leach-Bliley Act of 1999 allows Financial Holding Company to become lenders(no meddling with management) as well as share-holders( who can do management monitoring), and boosts Private Equity(Merchant Banking)

- Performances in terms of Returns and Safety(Risk) are superior.

- The only problem is “social equity issue” or “protection of small investors” who go alongside with giants – However, it would not be bad at all because U.S. has unique legal system to protect them: “Lender’s Liability and Equitable Surbordination”

We should facilitate Information Revolution, and allows for active M & As and new forms of innovative financing formats.

In reality, the government often tries to suppress them.

Obama-Biden’s basic tone of objection to these pro-market evolutions may be wrong.

References

Read Neil Reynolds’s inspiring article on the Dutch Securities market of the 16th Century, entitled, “Self-regulation: The Dutch had it right,” The Globe and Mail, Aug.12, 2006.

Edward Stringham, “The extralegal development of securities trading

in seventeenth-century Amsterdam”, The Quarterly Review of Economics and Finance, 43 (2003) 321–344

J. Bradford De Long, Harvard University, “Did J. P. MORGAN’S MEN Add Value?: An Economist’s Perspective on Financial Capitalism, 1995.

A.J.R. Rolnick and W. Weber, "New Evidence on the Free Banking Era," American Economic Review, 1983, Vol. 73, No. 5:1080-1091

A.J.R. Rolnick and W. Weber, "Explaining the Demand for Free Bank Notes," Journal of Monetary Economics, 1988, Vol. 21: 47-71.