short: genworth mi canada - sohnconference.org · investment summary [email protected] 4 if...

TRANSCRIPT

Short:

Genworth MI CanadaTIM BERGIN

t i m @ o n b eyo n d i nve st i n g .co m

@ o n b eyon d i nvest

Genworth MI Canada Ticker: MIC Exchange: TSE

Financial Snapshot

Share price (as of 4/19/2018) $38.59

Shares outstanding (mil) 90.96

Market capitalization ($CAD bil) 3.51

Book value (incl. AOCI) 43.13

Price to book ratio 0.90

2017 ROE 13%

Dividend per share $1.88

Dividend yield 4.87%

52 week range $44.49 - $30.38

Cost to borrow 2.50%

Price target: Substantially lower…

Idea Premise

The Canadian housing bubble has burst

The balance sheet is risky

Revenues are booked aggressively

• Prices are down 10% nationally and 14% in Toronto from the peak last spring

• Sales volumes are down 20% year-over-year

• New “B-20” regulations have reduced affordability by 20%

• Over 80% of premiums are recorded as revenue in the first 5 years

• As house prices stop rising, more losses will occur and revenue recognition should extend

• Lower premium volumes and slower revenue recognition will mean much weaker earnings in the future

• The company has $218bil of outstanding mortgages insured

• $97bil for which ‘actual LTV’ is greater than 90%

• The company has loss reserves of only $119mil, and $3.9bil of equity

Investment Summary

If the bubble has burst…

the housing market crashes, and balance sheet risks could wipe out their equity.

If there is a (mythical) “soft-landing”…

future earnings will be materially weaker (I estimate down 66%).

The stock trades at 0.9x book (average price of 0.95x book since 2009). ROE was 13% in 2017 (10% if you normalize the loss ratio) and they have averaged ROE’s of 11% since 2013.

OR

The short is asymmetric

Downside: 20 to 30% Upside: 60 to 100%

Canadian Mortgages

Mortgages come with a short fixed interest rate period, typically 5 years, and mortgage is amortized over 25 to 30 years.

Once fixed interest rate period is over, borrower needs to reapply – rate does not simply roll-over.

Mortgages are recourse, however, if homeowner files for personal bankruptcy a mortgage shortfall becomes a general unsecured claim and is fully dischargeable!

Mortgage interest is not tax deductible.

Primary residence incurs no capital gains when sold.

of Canadian mortgages are up for renewal this year!50%

Borrower recourse not as valuable as people think

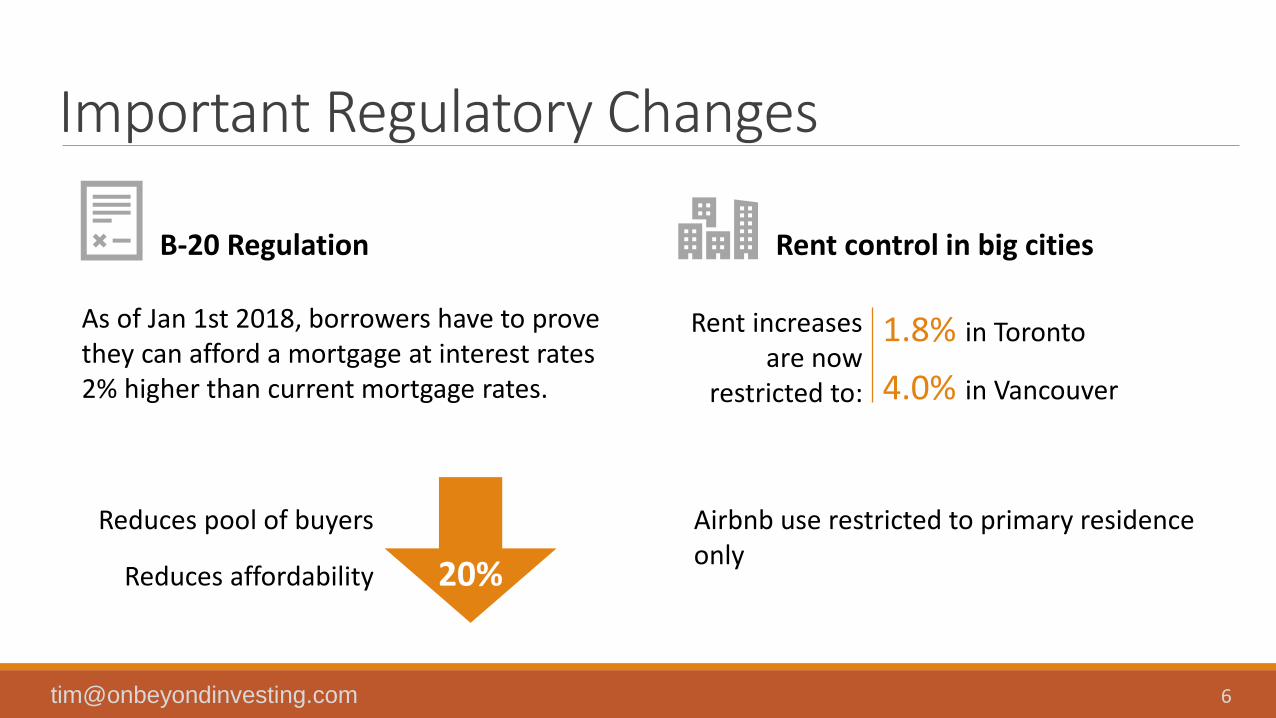

Important Regulatory Changes

B-20 Regulation Rent control in big cities

20%

Reduces pool of buyers

Reduces affordability

1.8% in Toronto

4.0% in Vancouver

Rent increases are now

restricted to:

Airbnb use restricted to primary residence only

As of Jan 1st 2018, borrowers have to prove they can afford a mortgage at interest rates 2% higher than current mortgage rates.

Canadian Mortgage Insurance

Market Share

MIC CMHC Canada Guaranty

• Required for any borrower that puts down less than 20% (i.e., >80% LTV)

• Insurer is liable for 100% of losses on default

• There are 3 insurance providers in Canada. The biggest player is CMHC - a Canadian Crown Corporation. Genworth MI Canada is the only publicly traded insurer (~ 32% market share).

If CMHC itself defaults, government covers 100% of banks’ losses

If MIC itself defaults, government covers 90% of banks’ losses

MIC likely insures a weaker pool of borrowers as banks hold 3.5% RWA vs 0% for CMHC-insured mortgages.

Canadian Mortgage Insurance continuedInsurers don’t individualize price; a standard one-timeupfront premium is charged. Price considers LTV only.

Is this a good way to underwrite risk?

Factors not considered in rates

dwelling type, credit score of borrower, location, house price, market conditions, etc.

Insurance Premium Rates

LTV New Rate(Mar 2017)

Prior rate

Up to 90% 3.15% 2.40%

Up to 95% 4.00% 3.60%

90 to 95% ‘non-traditional’

4.50% 3.85%

Portfolio Insurance 0.81% 0.36%

Loan: $300k

Mortgage: $300k + 4% x 300k+ interest

Insurance

4% x 300k

Example: $300k loan with 5% down. Premium is 4%. Bank pays $12k upfront to insurer and $12k is added to borrowers loan and also to the insured amount.

Underwriting at MIC

Genworth Canada has only 271 employees

Most underwriting decisions are made quickly;◦ 85% of applications are processed in 4 hrs!

◦ 95% within 24 hrs

Industry expert estimates that 85% of incoming applications are ultimately insured.

There are no loss reserves on insurance until a borrower is 90 days delinquent, at which point losses are estimated and a reserve is established

With their process, the banks’ perverse incentives, adverse selection issues, how exposed

are they to fraud?

Summary of Canadian Mortgage Insurance

Premiums are based on LTVs only

~ 85% of applications are approved

No initial reserves are required

Banks have no ‘skin-in-the-game’ andcapture the benefits

No wonder almost 50% of Canadian mortgages are insured.

Poor process!

Incentive misalignment!

THE CANADIAN HOUSING BUBBLE

(Scary) Canadian Housing Market Statistics

Statistic(at peak)

Debt to disposable income 171% 114%

Consumer debt to GDP 127% 94%

Price to income ratio 6.25x 3.8x

HELOC debt to GDP 12% 4.5%

12

Median home price

$500kMedian family income

$80.9kIn

2018:

% In

crease in p

rice

Year

House prices in Canada are 157% higher now than in 2003

Canadian HELOC Debt is a Problem

Common uses:

▪ giving down payments to children

▪ buying investment units

▪ investing in syndicated or private mortgages paying 8 to 10%

Annualized growth in HELOC debt

since 2000: 13.9% $235bil in total.

According to the Bank of Canada, 40% of HELOC borrowers do not make regular payments that

cover both interest and principal.

HELOC debt is floating rate, and borrower only required to pay interest

HELOCs have no amortized repayment, but are demand loans. If banks change amortization period to 5 years, monthly payments would increase by 550%

Genworth’s Exposure to Condo MarketCondos are the only market in Canada where prices haven’t dropped.

80% of new home sales in Toronto were condos and almost 50% of condo buyers were investors.

20% of condo owners in Toronto and 17% in Vancouver spend more than 50% of take home pay on shelter costs.

Condos are trading at sub 2% cap rates. They produce negative cashflow after financing costs. New

rent control rules mean that these units will stay that way for the foreseeable future.

Genworth has significant exposure to this market.

Volume of business in

condos:

30% in Toronto 40% in Vancouver11% nationally

Higher Interest Rates are Affecting Borrowers

“Nearly half of those polled (46 per cent) believe they’re now $200 or less away from financial insolvency after covering bills and debt at the end of the month. This was one of the few areas in which Albertans, at 41 per cent, came in lower than the national average.

Similarly, 47 per cent of respondents don’t believe they’ll be able to cover all their living and family expenses over the next year without plunging further into debt.”

Imagine what would happen if the Bank of Canada raises rates twice in 2018, as projected…

THE BALANCE SHEET IS RISKY

17

Balance Sheet Overview: Sufficient equity?

Key Elements for Calculating Losses:

1 LTV

2 Default rate

3 House price decline

18

$CAD billion

Total insurance written 495

Total insurance outstanding 218

Transactional insurance 118

Portfolio insurance 100

Equity 3.9

Loss reserves 0.1

Examining the LTV of Transactional Portfolio

Borrowers missed mortgage payments: 5% of property value

Lawyers fees to foreclose and sell property: 5% of property value

Repair costs, taxes etc.: 5% of property value

Upon default, in addition to losses on mortgage, MIC has to pay:

MIC estimates in its Annual Information form that these costs add up to 15%.

‘Actual’LTV:

In my analysis I add 15% to reported LTVs to adjust for these costs

Newly originated mortgages are underwritten at an average LTV of 92 or 93%, which implies ‘actual’ underwritten LTV is actually 107 to 108%!

These costs help explain why severity ratios have averaged around 30% for the last 10 years, despite a raging bull market in housing.

What Could Default Rates Look Like?

Historicaldefault rates of 1%

Today… house prices in Canada are 60% higher on a price-to-income basis than

any other time in its history. Debt has never been higher. Canadians

are significantly more levered than Americans were at the peak on every metric.

ComparableDefault

rateComments

Fannie/Freddie 7% Only 17% with LTV >80% vs 100% for MIC

US Mortgage Insurers 17 to 21% Direct comp to MIC

OR

What is more likely?

What Could Default Rates Look Like? continuedSimilarities between Ireland and Canada:

▪ On a price to income ratio, Canada is within 3% of the peak overvaluation in Ireland.

▪ Oligopoly banking sectors

▪ Economy that was dominated by real estate and related services (now 20% of Canadian GDP)

Analysis range:

5 to 15%1% default rate assumption

will prove to be too low.

Ireland conclusion: House prices dropped 51%, and non-performing loans (proxy for defaults) peaked at 37% of ALL loans!

Debt fueled housing bubbles result in crashes and massive increases in defaults.

Year

Overvalu

ation

relative to in

com

e

Long-run income

average*=100

House Price Declines

B-20 should reduce prices by 20%

40% decline would bring price-to-income ratio in line with US peak and in line with declines other countries have experienced.

Bank of Canada overnight rate is 1.25%. There isn’t much room to cut rates.

Notable House price declines since 1990

Years DeclineJapan 1992-2006 -46

Switzerland 1990-1999 -44

UK 1990-1996 -57

Spain 1992-1998 -45

Finland 1990-1993 -71

Italy 1993-1998 -40

France 1991-1997 -30

Sweden 1991-1993 -35

Ireland 2007-2012 -54

Spain 2008-2013 -36

Greece 2007-2017 -43

United States 2006-2011 -25

Average -44

Analysis range:

20 to 40%Sources: ECB Working Paper No 1071

The Economist house-price indices

Analysis of Potential Losses

Conservative: Ignores mortgages being underwritten now, and portfolio insurance business.

Best case scenario, wipes out excess regulatory capital of $400mil.

Default rates anywhere near US peers would wipe out equity.

See Annex A for sample calculation

Losses for varying default rates and housing price decreases (CAD$mil)

Housing price decrease (%)

Default rate (%)

5 10 15

203040

531976

1,485

1,0621,9522,970

1,5932,9284,455

Total equity plus loss reserves: 4,080

REVENUES ARE BOOKED AGGRESSIVELY

Income Statement Risks

80% or more of premiums are recognized as revenue within first 5 years.

Only $2.1bil of unearned premiums on $495bil of insurance unwritten.

Revenues are dependent on constant stream of new premiums.

In 2017, transactional premiums were down 14% year-over-year (applications were down 20%!).

Portfolio insurance premiums were down 51% year-over-year. Higher premium rates may mean this change is structural.

Normalization scenario: volumes down 30% from 2016, house prices down 20%, revenue recognition period of 10 years for new premiums and unearned reserves.

WHAT IF I AM

WRONGand Canadian default rates remain low?

The income statement has a lot of risk.

Current vs Future Earnings

Normalized premiums and extended revenue recognition would hurt the income statement even without defaults.

If revenue recognition extended only 1 year, in normalized scenario, net income would be down $190mil from 2017 levels.

Losses on claims in 2017 were 17pts below the 10 year average. Normal loss levels would add $115mil to expenses!

$CAD million

2017 Full YearNormalized

Scenario

Revenues 675 249

Operating expenses 134 134

Investment income 198 198

Interest cost 23 23

Losses on claims 69 69

Net income (26% tax rate)

479 164

See Annex B for sample calculations

Other Genworth MI Canada Risks

• Genworth Financial owns 57%, pledged 41% in recently issued term loan.

• Investment portfolio is highly correlated. They have $6.5bil of investments; $0.8bil is in bonds of Canadian financials and $500mil is in preferred shares ($309mil of which is in Canadian financials)

• Bad capital allocation. Raising dividend and buying back stock Lighting needed capital on fire.

• Homeownership Assistance Program: ~ 56% of potential delinquencies had some type of intervention; payment changes, payment deferrals, etc. These interventions are not reported as delinquencies. As a result, the market will be surprised by actual delinquency rates when they start to rise. There is a YouTube video describing the program (here).

Bull Case and Other Risks to Being Short

Bull case:

Genworth Canada insures first time homebuyers at price points well below average prices.

They cannot insure properties > $1mil, avoiding some of the excesses in Toronto and Vancouver.

While LTV’s are high, they claim their borrowers aren’t risky. Overall insurance volumes may decline, however they will increase market share (is that a good thing?), and higher premium rates should help stabilize revenues.

Bull case combined with ROE’s of 13% (unsustainable in my opinion), market could price stock at 1.3x book from current 0.9x book (although it historically trades at 0.95x book).

Risks to short position:

Government intervention. Could roll back regulatory changes or BOC could cut rates. Delaying inevitable.

Negative carry. Dividend yield of 4.6%, cost to borrow of 2.5%

Borrow rate cost. Borrow rates for HCG and EQB spiked dramatically (to 100%) last year when HCG ran into issues.

Conclusion

MIC is extremely vulnerable to the bursting of theCanadian housing bubble.

Two paths for housing market: Price target: $2

Crash: Balance sheet risks likely wipe out the equity.

Soft-landing: MIC’s earnings could drop 66%

Given the risks to the balance sheet and the income statement, and a

stock valuation that doesn’t account for these risks, I think this is a

compelling and asymmetric short.

Price target: Substantially lower…

Price target: $18

THANKS

My wife, Bev Bradley

Cam Sterrett

Ben Rabidoux

GLG

The Sohn Conference Foundation

… and everyone who helped me shape this idea

Annex A: ‘Actual’ LTV calculations

Source: Genworth MI Canada Annual Information Form 2017

Outstanding Mortgages Effective

LTV'Actual

LTV'Loss

($CAD bil)($CAD bil)

Portfolio Only 100 39% 54%

Transactional by Book Year

2009 and prior 15 37% 52% 0

2010 6 53% 68% 0.072

2011 7 57% 72% 0.126

2012 8 62% 77% 0.204

2013 10 65% 80% 0.3

2014 15 71% 86% 0.585

2015 20 75% 90% 0.9

2016 19 81% 96% 1.026

2017 18 91% 106% 1.242

Total: 218 4.455

Total since 2011 97

Wgt Average 'Actual LTV’ 90%

Example:Default rate (D): 15%House price decrease (H): 40%

Loss = (Actual LTV - (1 - H)) ×outstanding mortgages × D

Annex B: Normalized scenario calculation

A - 2016 Premiums ($bil) $20,000 Inv Yield 0.032

B - Volume Reduction 30% Inv Portfolio 6200

C - Home Price Reduction 20% Yearly Revenues 198.4

D - Average Insurance Rate 3.50%

New Unearned Premiums: A*(1-B)*(1-C)*D $392

Current Unearned Premium $2,100

Total Unearned Premiums (T) $2,492

Yearly Revs - 10yr recognition (T ÷ 10) $249

Yearly Revs - 6yr recognition (T ÷ 6) $415