shop the world

TRANSCRIPT

Shop the World!Consumer attitudes towards global distance selling

Shop the World 1

Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176 Mexico . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 192 Netherlands . . . . . . . . . . . . . . . . . . . . . . . . . 208 Poland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 224 Russia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240

South Korea . . . . . . . . . . . . . . . . . . . . . . . . . 256 Spain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272 Switzerland . . . . . . . . . . . . . . . . . . . . . . . . . 288 Turkey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 304 USA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 320

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . 336

Methodology: Study design and sample size . . . . 336 Questionnaire . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 337

Legal notice . . . . . . . . . . . . . . . . . . . . . . . . . 338

Editorial . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Shop the World! - in five minutes . . . . . . . . . 3

Shop the World! - in half an hour . . . . . . . . . 4

Media use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 Distance selling - Market overview . . . . . . . . . . 5 Distance selling - Use . . . . . . . . . . . . . . . . . . . . . . 6 Search for product information . . . . . . . . . . . . . 8 Supplier selection . . . . . . . . . . . . . . . . . . . . . . . . . 9 Placing orders . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Payment methods . . . . . . . . . . . . . . . . . . . . . . . 11 Delivery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Cross-boarder shopping . . . . . . . . . . . . . . . . . . . 14

Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Austria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Brazil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 China . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80 France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96 Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112 Great Britain . . . . . . . . . . . . . . . . . . . . . . . . . 128 India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144 Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

Table of Contents

Table of Contents

Shop the World 2

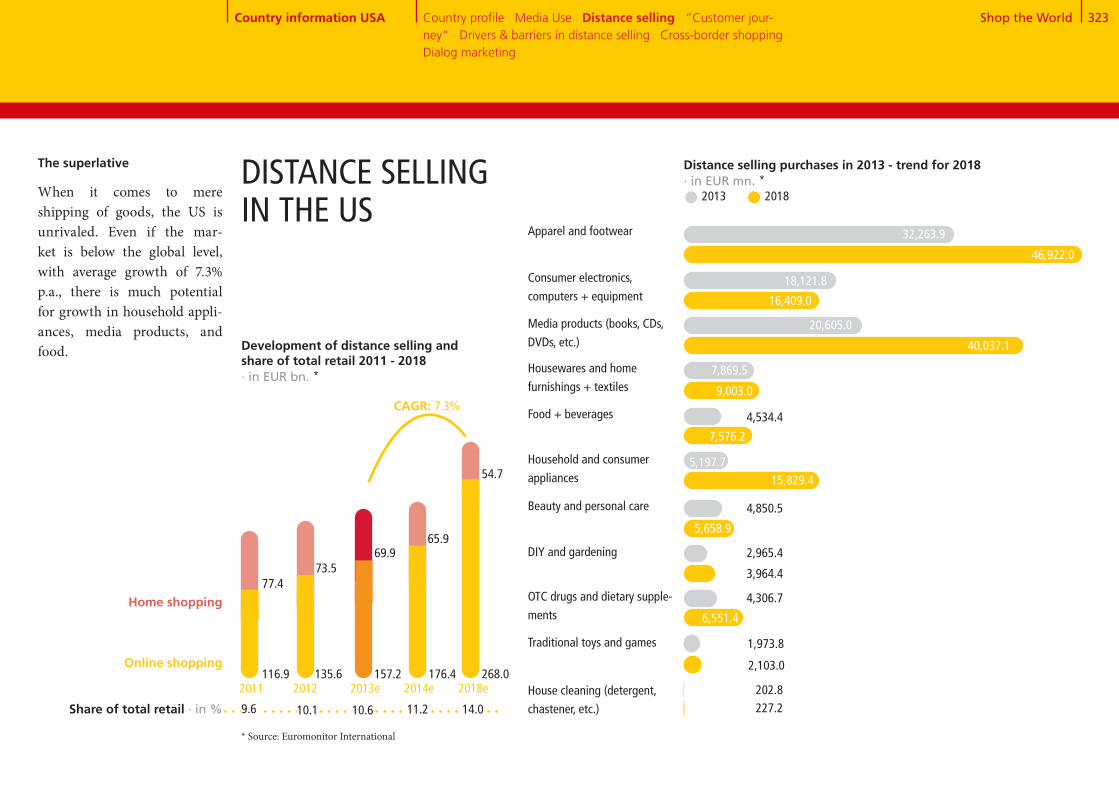

lobal distance selling account-ed for sales of €616 billion in

2013 and is expected to see annual growth of 10 .7% in the next five years . This trend now influences almost all sectors of the economy . An increasing focus is being placed on the eCommerce customers who decide whether, when and under what conditions they order goods online .

Businesses thus have to understand the var-ious steps in the customer’s journey through the online purchasing process . And they must also be aware of the economic and cultural dif-ferences that drive cross-border eCommerce .

In this Shop the World! consumer study, more than 11,000 people in 20 countries were asked about their attitudes, behavior and pref-erences in respect of different media, product selection criteria, payment methods, and de-

livery and return options . They were also asked about their rea-sons for ordering goods from abroad, and the obstacles they face in doing so .

The same data was collected for each country to allow the first ever comparative study of dis-

tance selling practices in 20 different countries around the world . The survey is supplemented by a set of country profiles containing current distance selling sales figures and forecasts, as well as demographic, economic and media-related data .

I trust you will find the study valuable in your work, and wish you an interesting and infor-mative read .

Dear Reader,

G

Yours

Thomas KippCEO DHL eCommerce

Editorial

Shop the World 3

• When it comes to internet use, the Nether-lands lead the field (93%) . China (42%), Mexico (38%) and India (13%) bring up the rear . South Korea is the market leader in terms of smartphone share (73%) .

• The global advertising industry is set to see revenue of €413 billion in 2014 . After the US and China, the biggest growth in glob-al advertising expenditure will be seen in emerging economies like Indonesia, Ar-gentina and Brazil . While TV remains the dominant medium in the global media mix, future growth will primarily occur through spends on mobile advertising .

• According to Euromonitor International, global distance selling sales amounted to €616 billion in 2013 .

• The three biggest distance selling markets are the US, China and Japan .

• The global distance selling market is ex-pected to see annual growth of 10 .7% between now and 2018 .

• The largest growth is expected in China (24 .5%), Mexico (16 .5%) and Australia (16 .4%) .

• The top products offered via distance sell-ing are fashion, consumer electronics, me-dia products and food . There are, however, marked country-specific differences .

• Some 84% of the online population are distance selling customers . Emerging economies see lower user numbers, but enjoy considerably higher growth fore-casts .

• Annual per capita orders average

13 in global comparison, with country-specific order numbers ranging from 6 in Mexico to 29 in Great Britain .

• As the only one of the emerging economies

covered by the study, China has extremely high user rates, order numbers and signifi-cant growth potential .

• Customers mainly search for products on-line (93%), largely via search engines and suppliers’ websites .

• Their main reasons for choosing a supplier are affordable prices and free delivery .

• Orders are primarily placed online using a PC, followed by those placed with mobile devices . China, South Korea, and Austra-lia have the highest shares in mCommerce (some 15% of orders overall) .

• Credit cards are the most frequent pay-ment method used . Preferences differ from region to region, however . These include for example the use of Alipay in China, and cash on delivery in India .

• The key ordering criteria are speedy, free delivery . Acceptable delivery times range from between 3 .8 days in Turkey to 12 .4 days in Russia .

• The highest return rates are seen in Ger-

many, Austria, Switzerland and the Nether-lands (between 9% and 13%) .

• Some 45% of internet users have ordered goods from abroad . Figures in emerging economies are significantly lower than those for industrialised countries .

• The main exporting countries are the US, Great Britain, Germany and China .

• The main reasons for ordering goods from abroad are that they are not available do-mestically and are lower-priced . In emerg-ing economies, better quality and protec-tion against counterfeit goods and product piracy are key drivers in the purchasing decision .

Shop the World! - in five minutes

Shop the World! - in five minutes

Media use Distance selling – market overview Customer Journey Cross-border shopping

Shop the World 4

Global advertising expenditure · in Eur bn. *

2011 2012 2013 2014 2015

436.

8

413.

1

391.

7

377.

3

363.

9

2016

462.

9

Mobile internet

TV

Desktop internet

Out of home

Radio

Movies

General magazines

Newspapers

24.6

24.2

19.4

4.1

2.1

0.6

-1.2

-2.7

Contributors to global growth in adspend by medium 2013-2016 · in Eur bn. *

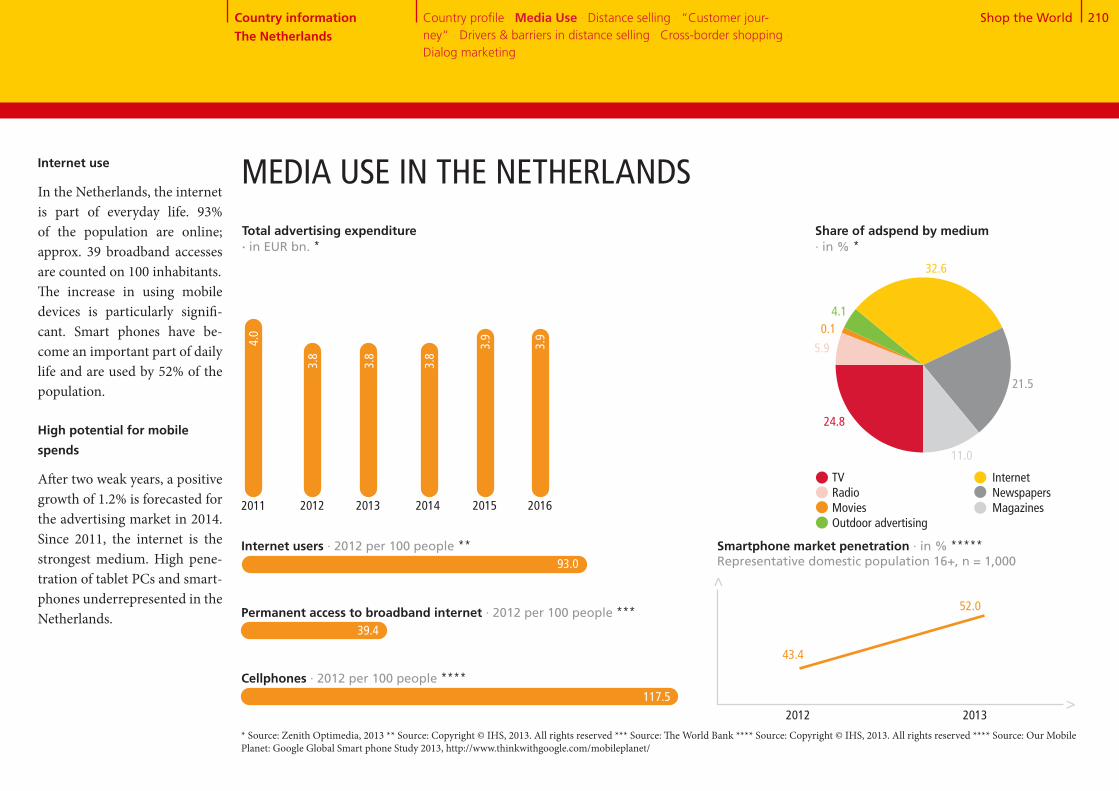

Internet use

As more and more people use the internet huge country-specific differences emerge . The Nether-lands lead the field with 93%, followed by Great Britain (87%) and Canada (86 .8%) . India, Chi-na and Mexico bring up the rear . While Mexico and China have online populations of 38% and 42% respectively, only 12 .6% of India's consumers use the inter-net .

With growing use of smart- phones, mobile access to online content is on the rise . Com- pared with 2012, state subsidisa-tion and billion-strong invest-ment in Brazil, Poland and Tur-key have led to a two-fold rise in use of internet-compatible smart-phones . In Russia and Mexico, smartphone use has risen from 20% to 37% . But South Korea, where 73% of the population own a smartphone, is the un-contested leader .

Advertising

The global advertising indus-try is set to see revenue of €413 billion in 2014 . Growth of 5 .8% and 6 .1% is forecast for 2015 and 2016 respectively . While TV re-mains the dominant medium in the global media mix, future growth will largely be seen in ex-penditure on mobile advertise-ment . The three biggest advertis-ing markets are the US (€130 .5 billion), Japan (€41 .4 billion) and China (€31 .9 billion), although Japan is expected to relinquish its No . 2 spot to China in 2016 . Apart from the US and China, the biggest growth in global ad-vertising expenditure will be seen in the emerging economies such as Indonesia, Argentina and Brazil .

* Source: Zenith Optimedia 2013

Internet desktopMobile internetNewspapers Magazines

40+7+1+7+18+3+17+7Global media mix · 2013 in % *

TV Radio Movies Outdoor advertising

18.0

17.0

8.0

7.01.07.0

40.0

3.0

India

USA

China

Indonesia

Argentina

Brazil

UK

Japan

South Korea

Russia

18.8

5.2

12.8

5.1

2.7

2.5

3.0

2.5

2.2

1.9

Top ten contributors to ad spend growth 2013 - 2016 · in Eur bn. *

Shop the World! - in half an hour

Shop the World! - in half an hourMedia use

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 5

Industrialised countries (Europe)

Industrialised countries (Americas & APAC)

Emerging economies

GL

US

CN

JP

UK

DE

KR

FR

RU

BR

IT

ES

CA

AU

NL

CH

MX

PL

AT

TR

IN

Distance selling sales by country in 2013 · in EUR bn. *

616.4

227.1

78.4

57.4

45.3

34.9

26.1

25.7

14.4

8.6

6.4

6.3

6.1

5.2

4.5

4.2

4.1

4.1

3.2

2.9

2.4

CN

MX

AU

BR

ES

IT

TR

PL

RU

IN

FR

CA

GL

DE

US

NL

KR

JP

AT

CH

UK

Distance selling market growth by country CAGR 2013 - 2018 · in % *

24.4

16.5

16.4

13.6

13.0

12.7

12.4

12.2

11.9

11.6

11.3

10.8

10.7

8.7

7.3

5.7

5.3

4.8

4.8

4.2

4.0

* Source: Euromonitor International

Market data and trends

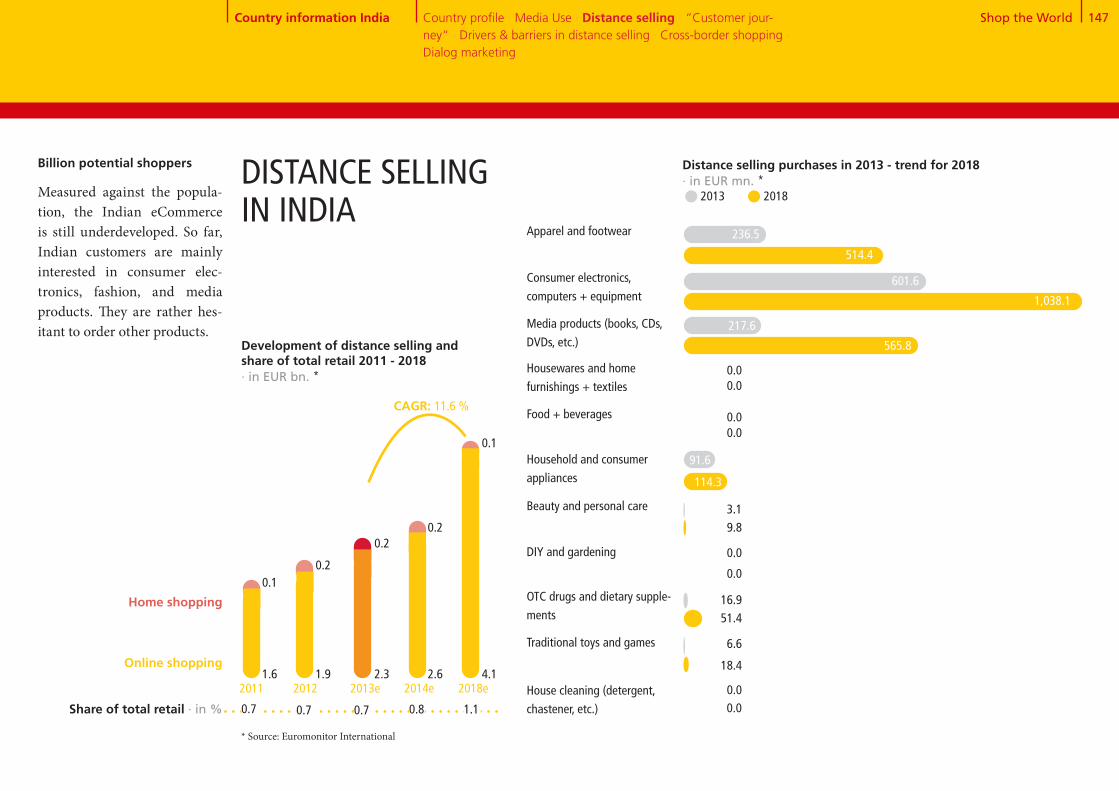

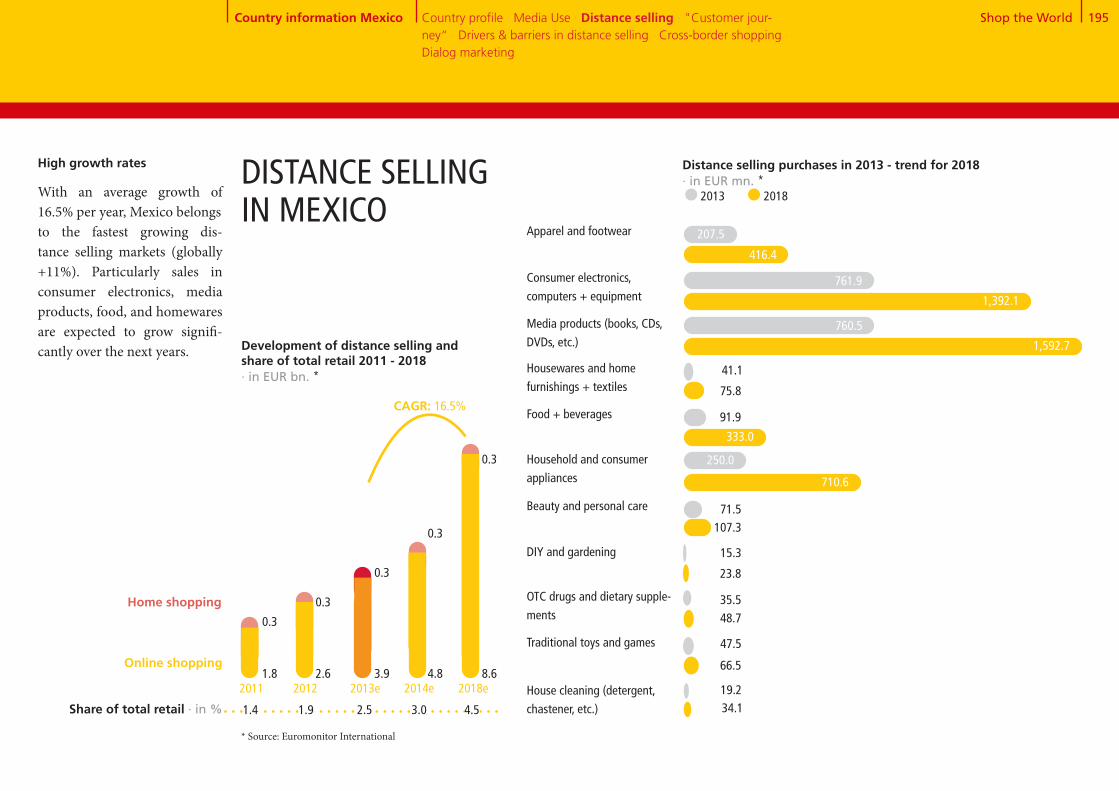

Distance selling sales rose again in 2013 . This boom is expected to continue: Euromonitor Inter-national forecasts annual growth of 10 .7% (CAGR) for the peri-od up to 2018 . While growth in most established distance selling markets in Europe and the US is below the global average, in the emerging economies investment in infrastructure and an increas- ing middle class are generating growth which in most cases ex-ceeds the global average by far .With estimated annual growth of 24 .4% for the period up to 2018, China leads the field – closely followed by Mexico with 16 .5% . Surprisingly, Australia is also among the leaders, with an

Shop the World! - in half an hour

Distance Selling – Market Overviewannual growth of 16 .4% . In Eu-rope above-average growth is ex-pected in Italy, Poland and Spain .

Around 46% of global distance selling revenue in 2013 was attributed to clothing, consum-er electronics, media products and food . However, country-by-country differences are evident: While clothing dominates in China and Germany (30 .4% and 27 .2%), clothing doesn’t play a role in Brazil . Here the highest demand is for consumer elec-tronics (38 .5%) . In Turkey, on the other hand, food sales domi-nate the market (24 .5%) and in Canada the demand for media products (28 .6%) .

Development of distance selling and share of total retail 2011 - 2018 · n Eur bn. *

CAGR: 10.7%

Home shopping

Online shopping 333.3 406.7 483.1

142.6138.2

133.3

558.7 912.2

127.2

110.5

2011 2012 2013e 2014e 2018eShare of total retail

· in % 5.0 5.5 5.9 6.4 8.4

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 6

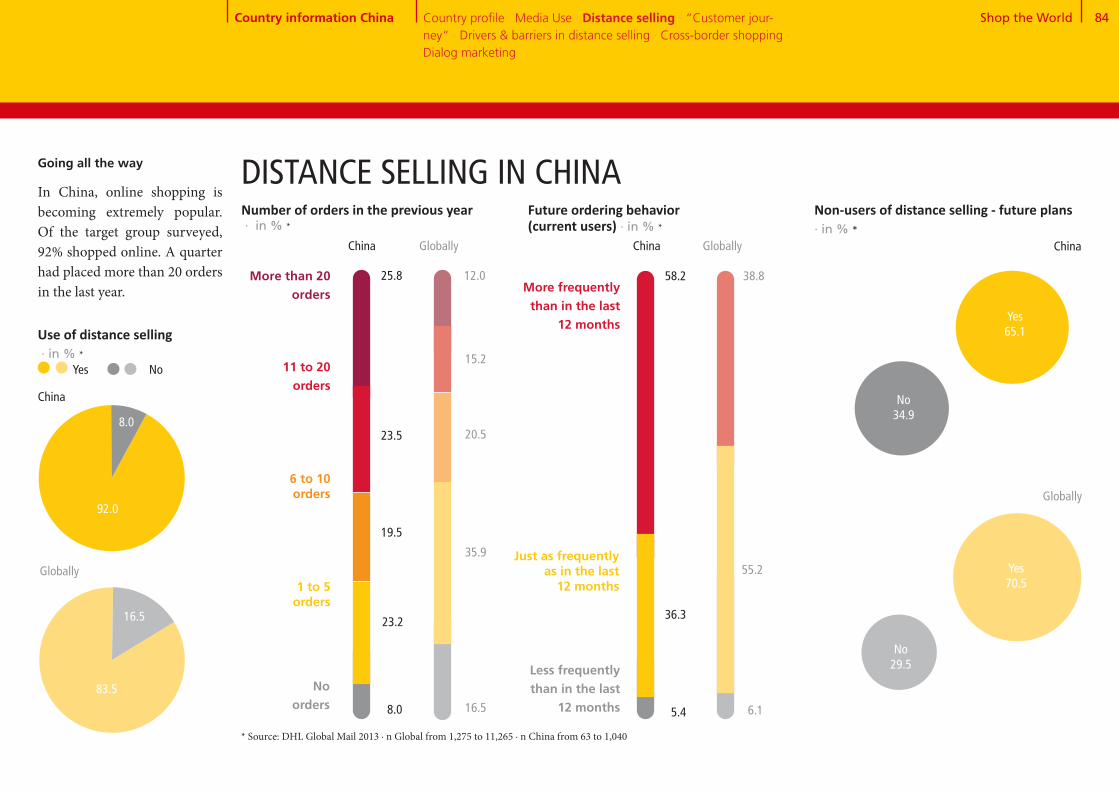

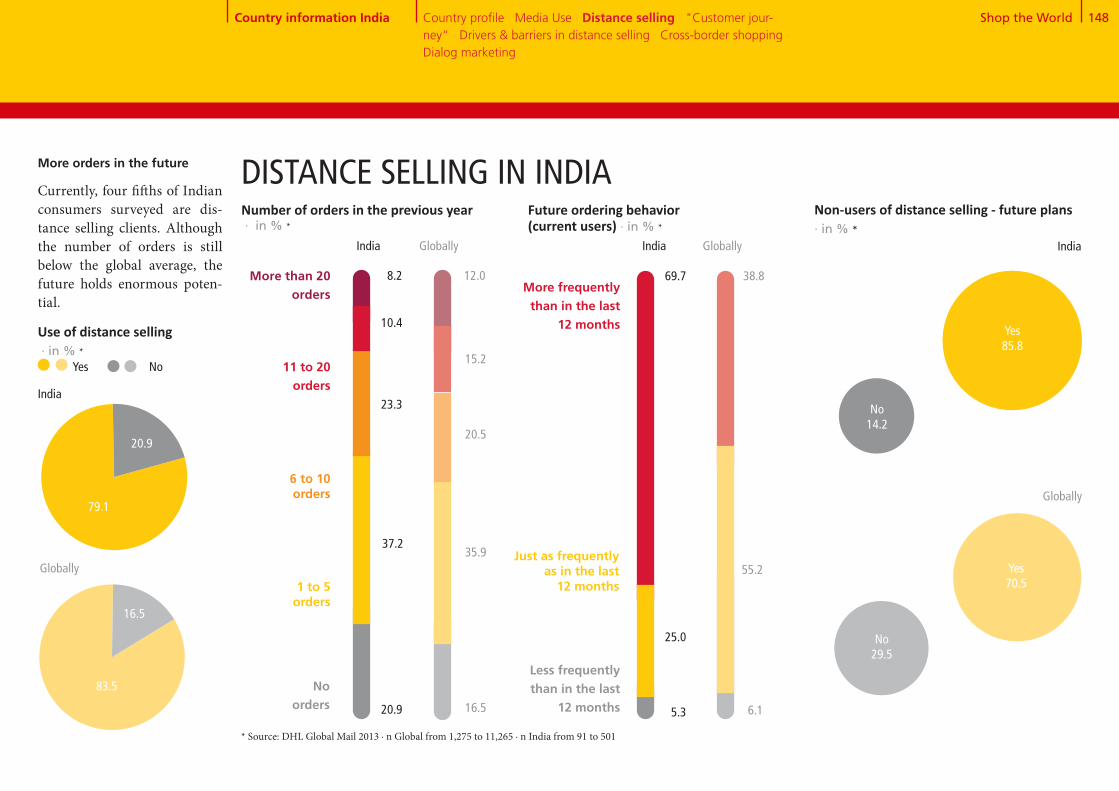

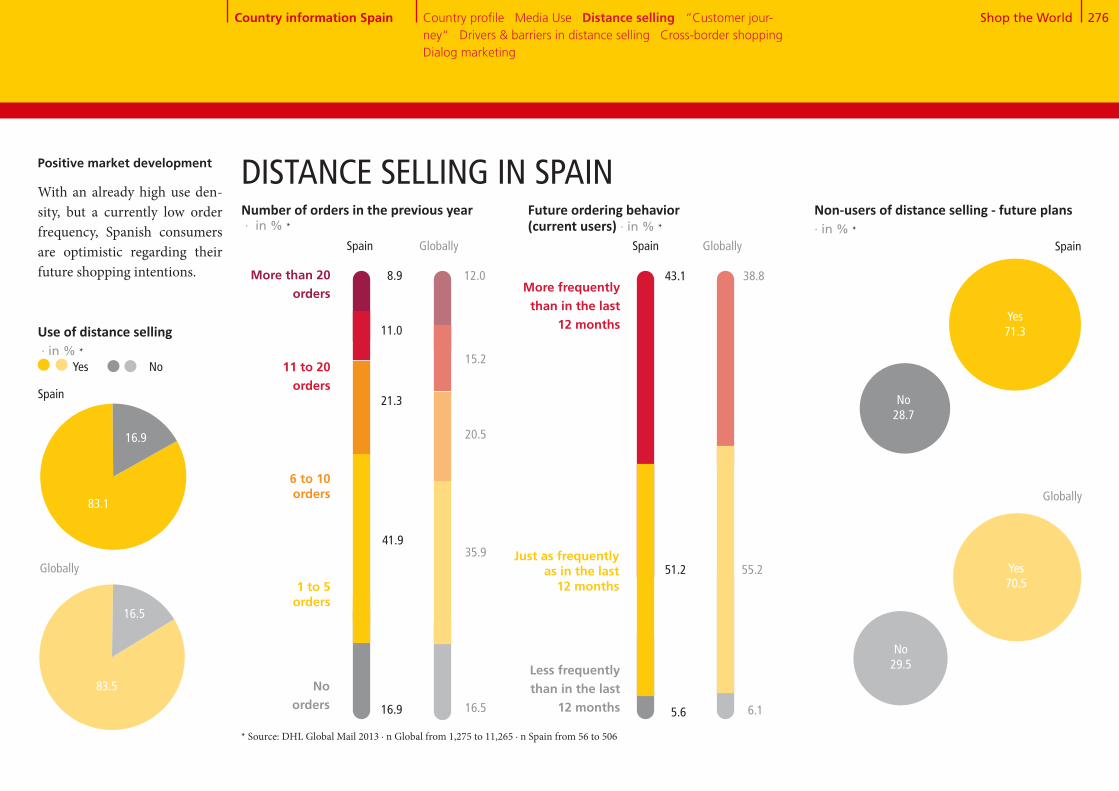

In the 20 countries covered by the study, on average 84% of the online population are order- ing goods via distance selling . Great Britain and Germany lead the field – both have dis-tance selling histories going back more than 100 years . The emerging economies bring up the rear, although the ‘lowest’ user rates there still amount to 73% .

In country-to-country com-parison, there are huge differ- ences in market size: Great Britain is the biggest distance selling market in the world on a per-capita basis, with annual sales of €45 .3 billion in 2013 and a number of orders per capita of 28 .7 per year . At the opposite end of the scale and typical of the emerging econ-omies, Mexico has significantly less experience in distance sell-ing, accruing just €4 .1 billion in sales in 2013 and a number of orders per capita amounting to 5 .8 per year .

Use of distance selling · in % *

Shop the World! - in half an hour

UK DE CN AT KR PL US CH JP FR GL IT ES NL AU IN BR RU TR CA MX

94 94 92 90 88 86 86 86 86 85 84 83 83 81 81 79 78 78

73 73 73

70

58 58

52 50 50 49

44 43

39 37 36

33 30 29 28 26 25 24 22

20

IN CN BR TR MX RU IT PL ES GL CA AU UK KR US NL FR DE AT CH JP

Planning higher number of orders in future (current users)

· in % **

Distance Selling – Use

Industrialised countries (Europe)Industrialised countries (Americas & APAC)Emerging economies

* Source: DHL Global Mail 2013 ∙ n (total) = 11,265; n (countries) = 500-1,040 ** n (total) = 9,161; n (countries) = 344-941, selec-tion by those planning a larger order volume, basis: Current distance selling users

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 7Shop the World! - in half an hour

UK 28.7

DE 18.2

CN 23.1

AT 15.6

KR 16.5

PL 12.7

US 13.6

CH 12.6

JP 13.1

FR 12.0

IT 10.1

ES 10.1

NL 7.9

AU 14.3

IN 8.5

BR 7.0

RU 6.8

TR 8.1

MX 5.8

CA 9.7

GL 12.7

< 8 orders

< 10 orders

< 15 orders

15 orders or more

Average number of orders per capita per year · Mean *

In Mexico, and also in Turkey, Brazil and India, distance sell-ing sales lie below €10 billion . About one-fifth of respondents made their purchases offline in stores . Annual number of or-ders per capita are in the sin-gle digit range . Nonetheless, these countries harbour growth potential: Over half of current distance selling customers plan to use this shopping channel more in future, and around 80% of those who visit stores say they intend to use distance selling in the future .

Less typical among the emerg-ing economies is China, where distance selling sales amount-ed to €78 .4 billion in 2013 . Of these, 95% were generated through eCommerce . Despite the country’s greater affinity to distance selling (92%) – the average number of orders per capita amount to 23 .1 per year – almost 60% of respondents say they intend to order more .

* Source: DHL Global Mail 2013 ∙ n (total) = 11,265; n (countries) = 500-1,040, Basis: all (including non-users with 0 orders)

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 8

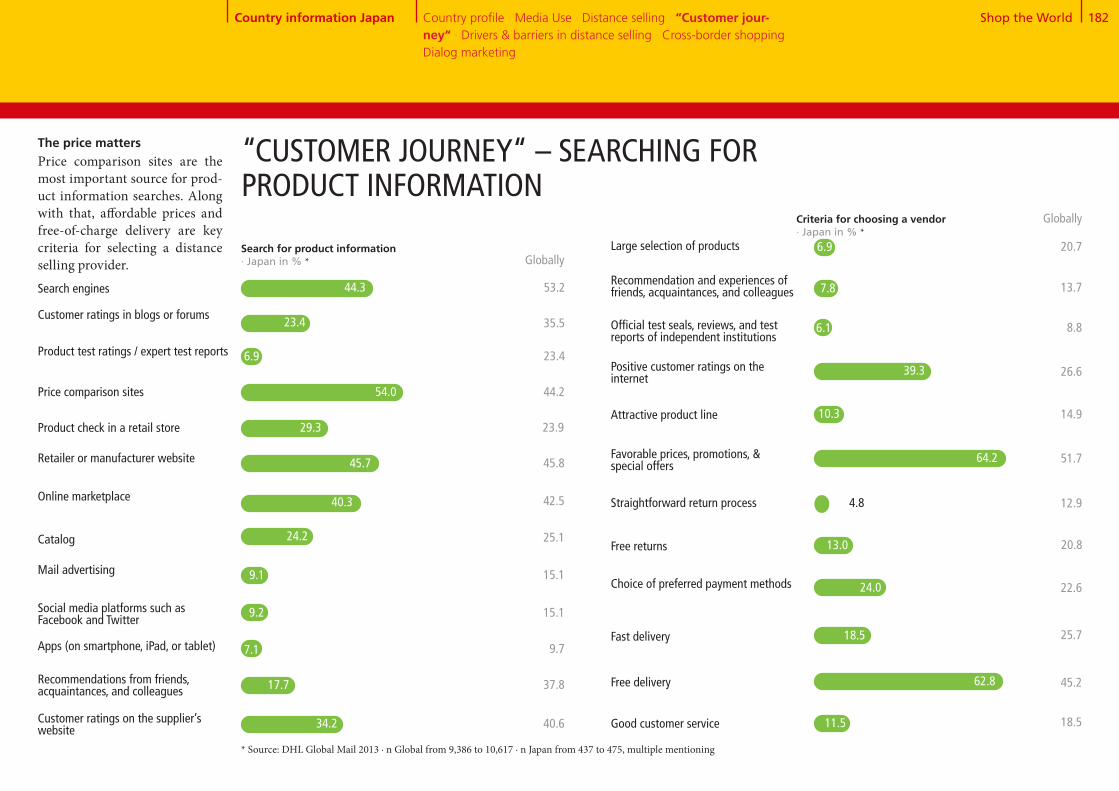

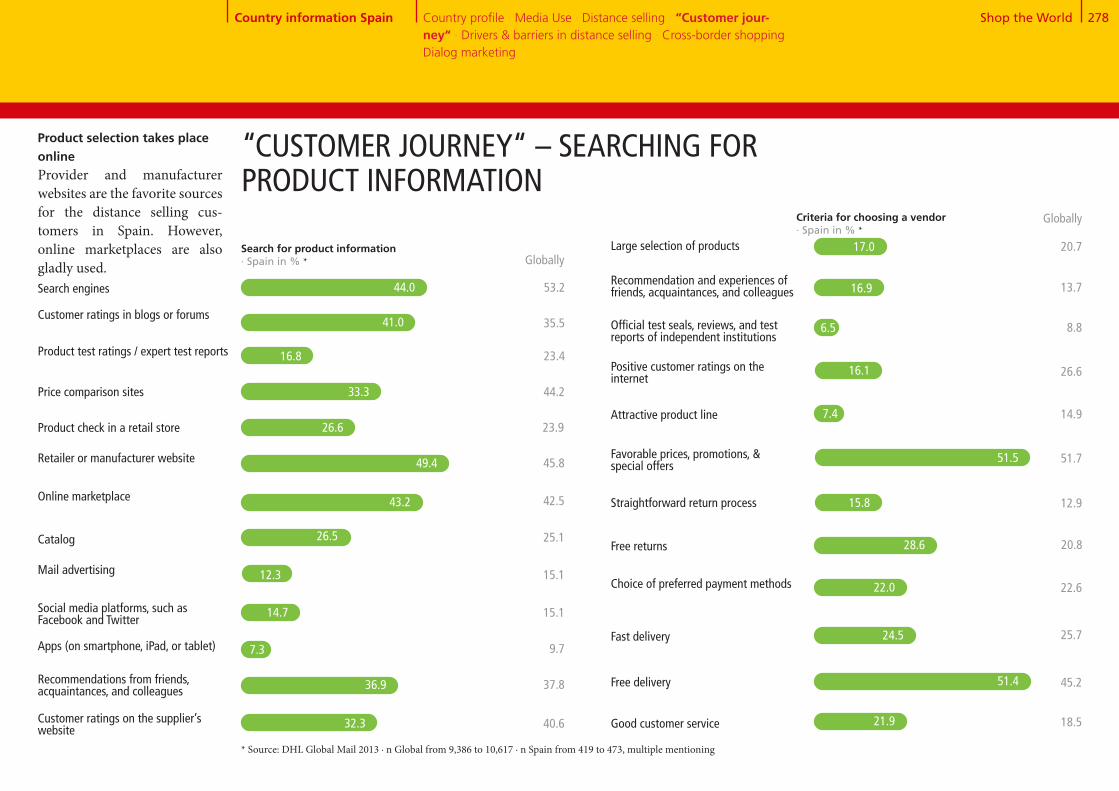

Searching for product information

Across all countries covered by the study, some 93% of respon-dents go online to search for product information . Search en-gines are the No . 1 choice (53%), followed by retailers’ websites (46%), price comparison sites (44%) and online marketplaces (43%) . Some 70% of distance selling customers also use offline sources, mostly in their immedi-ate environment . 38% rely on ex-perience gained by and tips from friends, acquaintances and col- leagues, while about a quarter use catalogs and product visibil-ity in retail stores .

Country-specific differences are evident in the way users search for information . People in Brazil tend to rely on personal recom-mendations (48%), social media platforms (26%) and customer reviews (53%) . In Japan, the trend goes more towards per-sonal dialog (18%), while social media plays only a subordinate role .

Online (net)

Search engines

Retailer or manufacturer website

Price comparison sites

Online marketplace

Customer ratings on the supplier’s website

Customer ratings in blogs and forums

Social media platforms, such as Facebook, Twitter

Apps (on smartphone, iPad or tablet)

Offline (net)

Recommendations from friends, acquaintances, and colleagues

Catalog

Product check in a retail store

Product test ratings / expert test reports

Mail advertising

93

53

46

44

43

41

36

15

10

70

38

25

24

23

15

Search for product information · in % *

Flags show national variations from the global average of at least +10% points.

Shop the World! - in half an hour

* Source: DHL Global Mail 2013 ∙ n = 9,386; Basis: Distance selling users

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 9

Price is the key criterion in choosing a supplier . This is es-pecially the case in Japan (64%) and South Korea (66%) . By way of contrast, people in India place significantly less importance on affordable prices (35%) . The second most important criteri-on is free delivery . This is a key purchasing factor for 45% of people worldwide, and is the most important supplier selec-tion driver in Japan and the US .

Of less importance when choos-ing a supplier are the criteria in-volved in the subsequent phases of the purchasing process . In global comparison, one in four people expect speedy delivery (26%) . This includes delivery time, which is of great impor-tance to customers in Brazil (38%) . Supplier preference can also be driven by customers’ pay-ment option preferences (23%) and free returns (21%), the latter being of particular importance to shoppers in Germany (35%) and Austria (35%), where distance selling and especially free returns have long been the norm .

Favorable prices, promotions, & special offers

Free delivery

Positive customer ratings on the internet

Fast delivery

Choice of preferred payment methods

Free returns

Large selection of products

Good customer service

Attractive product line

Recommendations and experiences of friends, acquaintances, and colleagues

Straightforward return process

Official test seals, reviews, and test reports of independent institutions

52

45

27

26

23

21

21

19

14

15

13

9

Criteria for choosing a vendor · in % *

Flags show national variations from the global average of at least +10% points.

Shop the World! - in half an hour

Supplier selection

* Source: DHL Global Mail 2013 ∙ n = 10,617, Basis: Current and future distance selling users

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 10

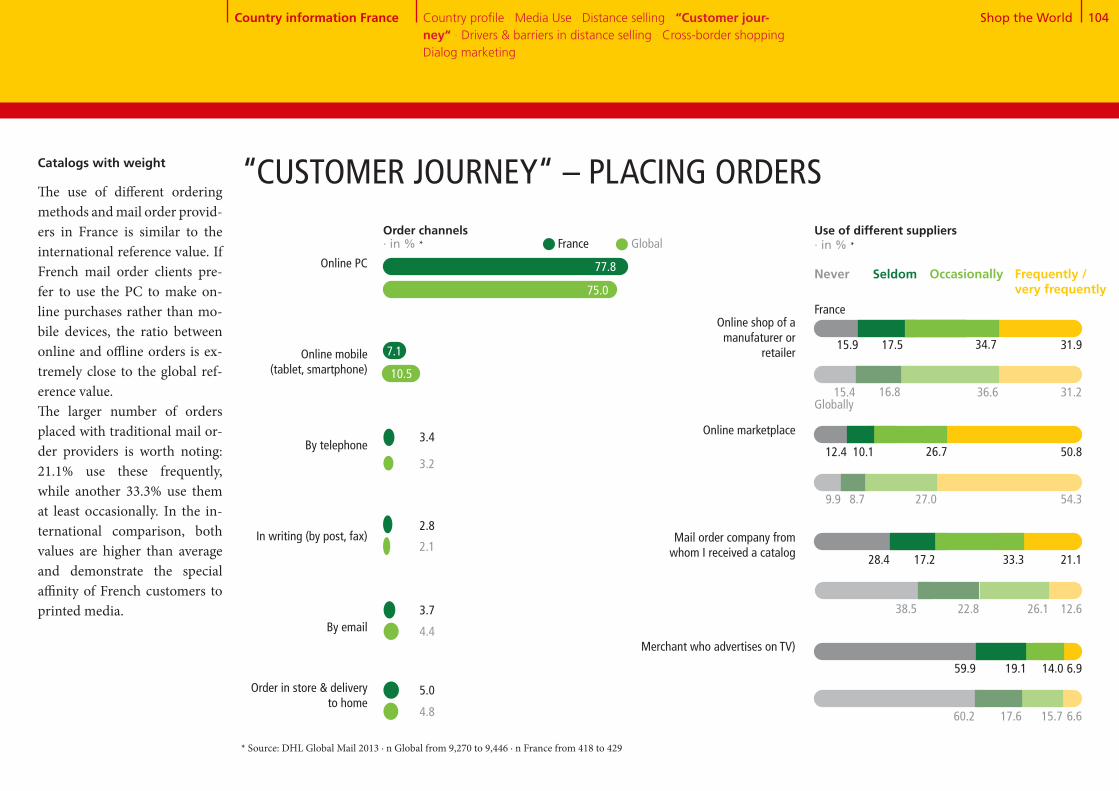

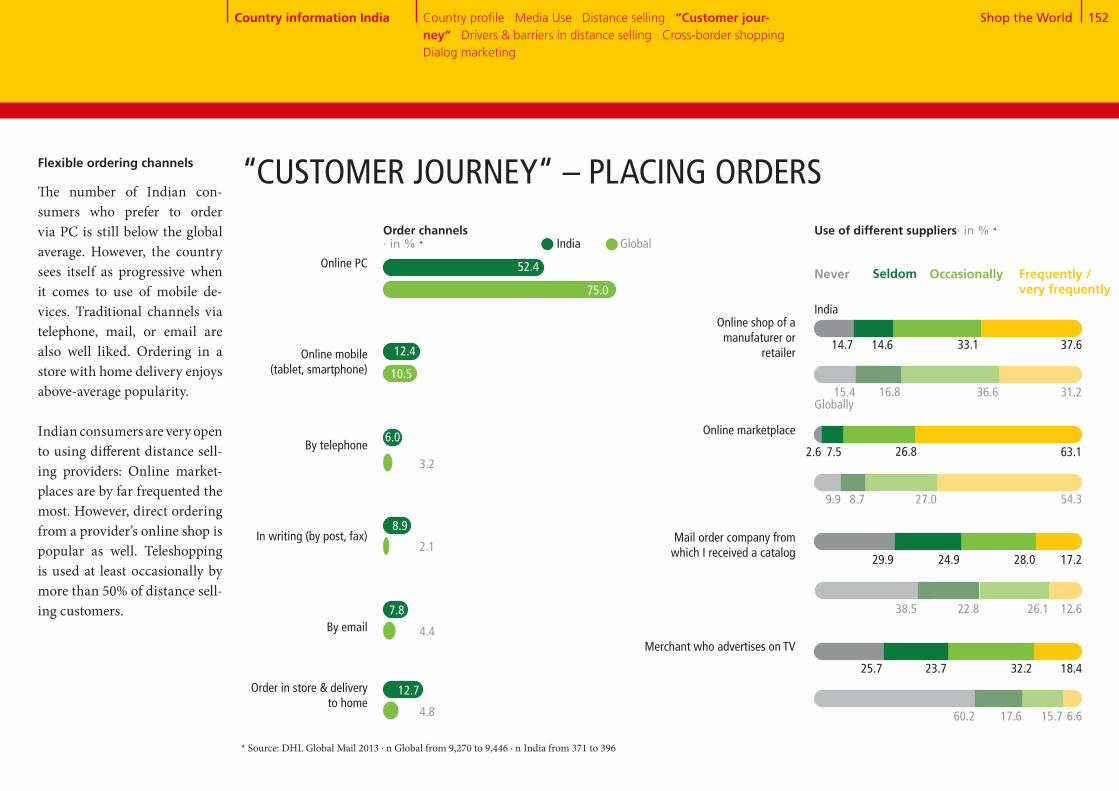

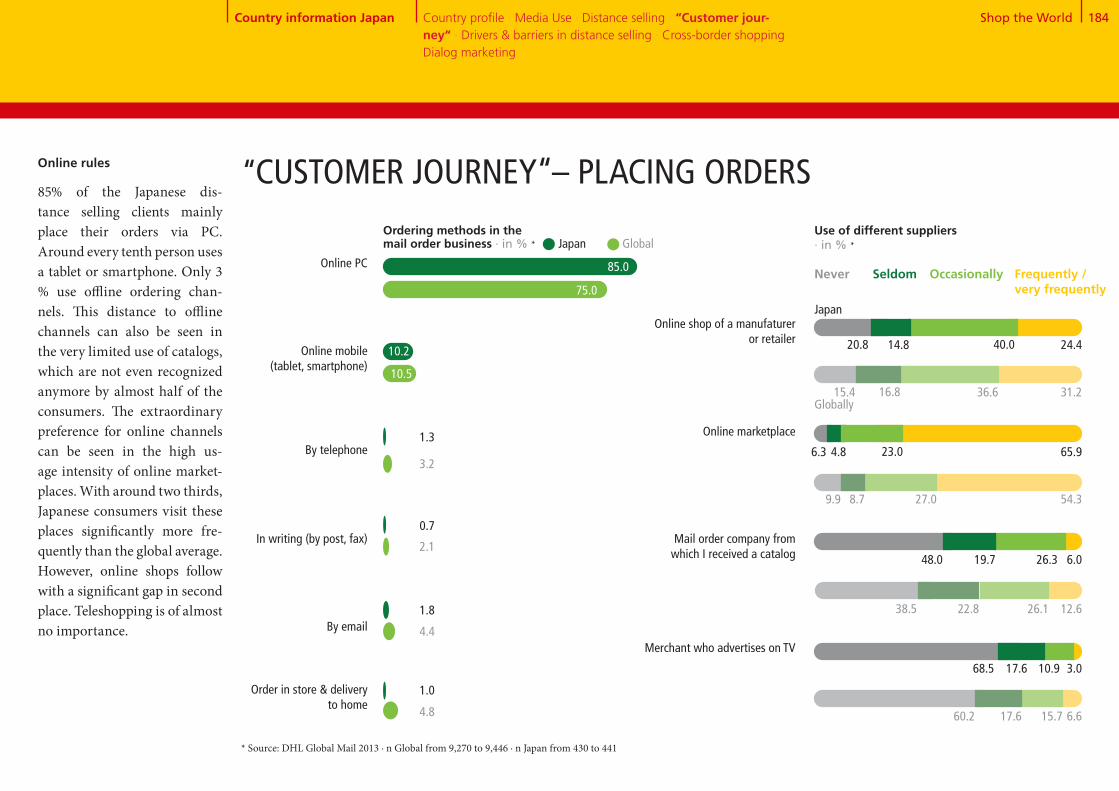

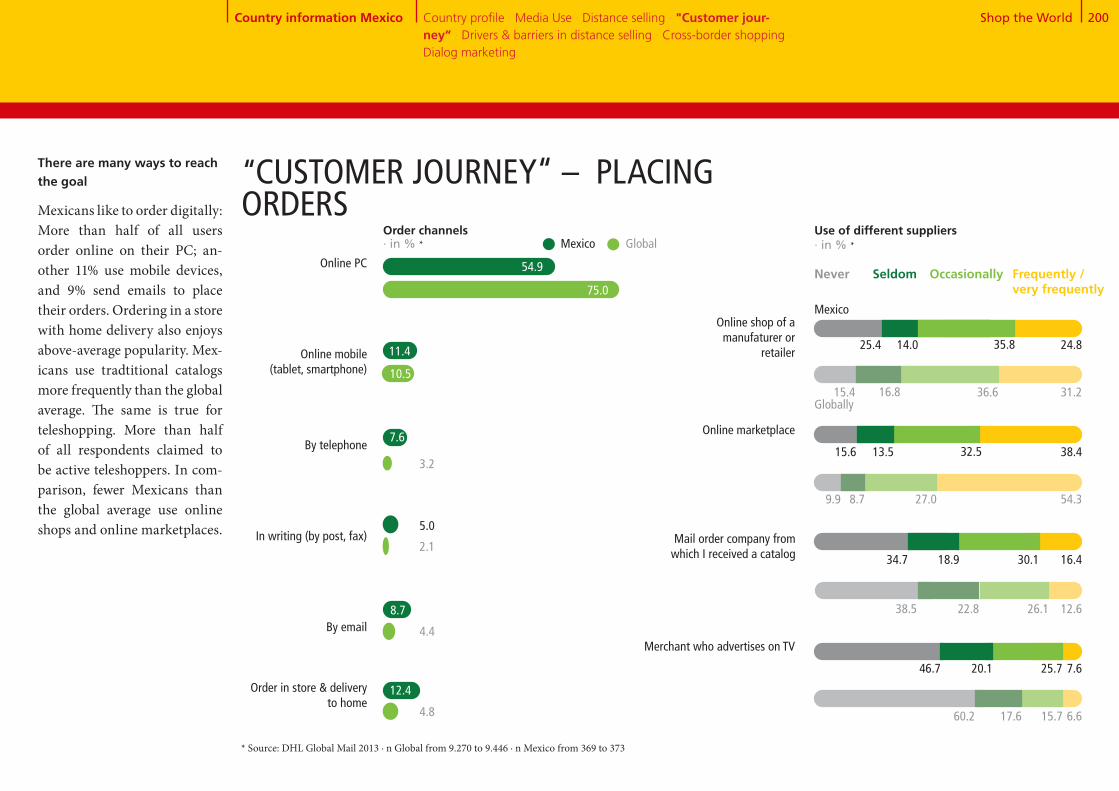

Some 84% of the online popula-tion across the 20 countries cov-ered by the study are distance selling customers who place on average 15 .2 orders per year . A large number of these orders are placed online (75% using a PC and 11% via mobile devices) . Use of mCommerce is disproportion- ately high in Australia, where 16% of orders are placed in this way, and also in China and South Korea (each at 15%) .

Although online orders tend to dominate, offline orders should not be neglected . Around one fifth of people who shop online also order goods in stores and have them delivered to their homes . Some 17% occasionally place orders by telephone, while 9% sometimes send a written order by post . However, the em-phasis here is on ‘occasionally’ and ‘sometimes’ rather than ‘reg-ularly’ . Thus, the three offline channels only account for 10% of orders . Of these, 5% are orders placed in stores, 3% by telephone and 2% by post . This applies both

to industrialised countries and most emerging economies .

There are three big exceptions, however: In Turkey (57%), Mexico (55%) and India (52%) the share of online orders made using a PC is significantly below the global average of 75% . Instead of PCs, distance selling custom-ers in these countries tend to order goods in stores (12%), by telephone (7%) and especially in India by post (9%) .

Shop the World! - in half an hour

Placing orders

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Share of distance selling order channels · in % *

* Source: DHL Global Mail 2013 - selected countries

JP US UK CN GL AU KR TR MX IN

1221

10

85

133

4

10

79

134

5

10

78

133

5

15

77

2

3

4

5

11

75

2

3

4

3

16

73

2

6

2

4

15

71

3

6

12

11

11

57

5

8

9

12

11

55

9

6

8

13

12

52

By post, faxBy telephoneBy email

Order in store & delivery to homeOnline mobileOnline PC

Shop the World 11

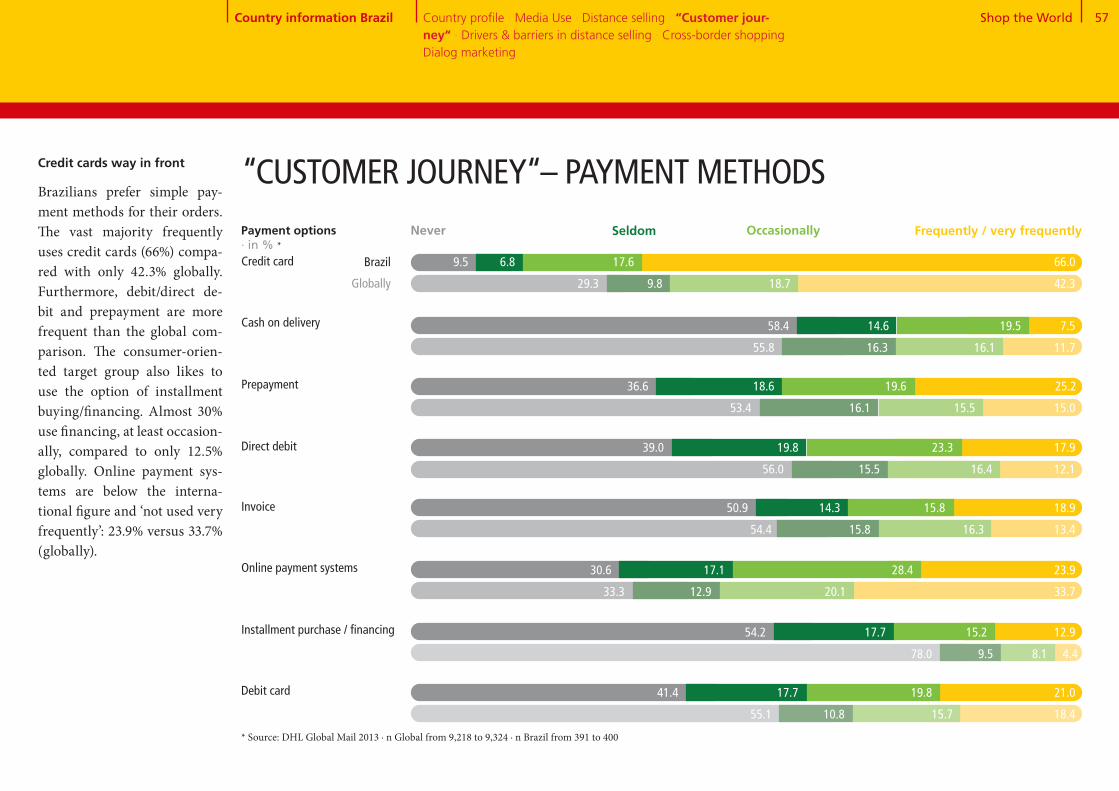

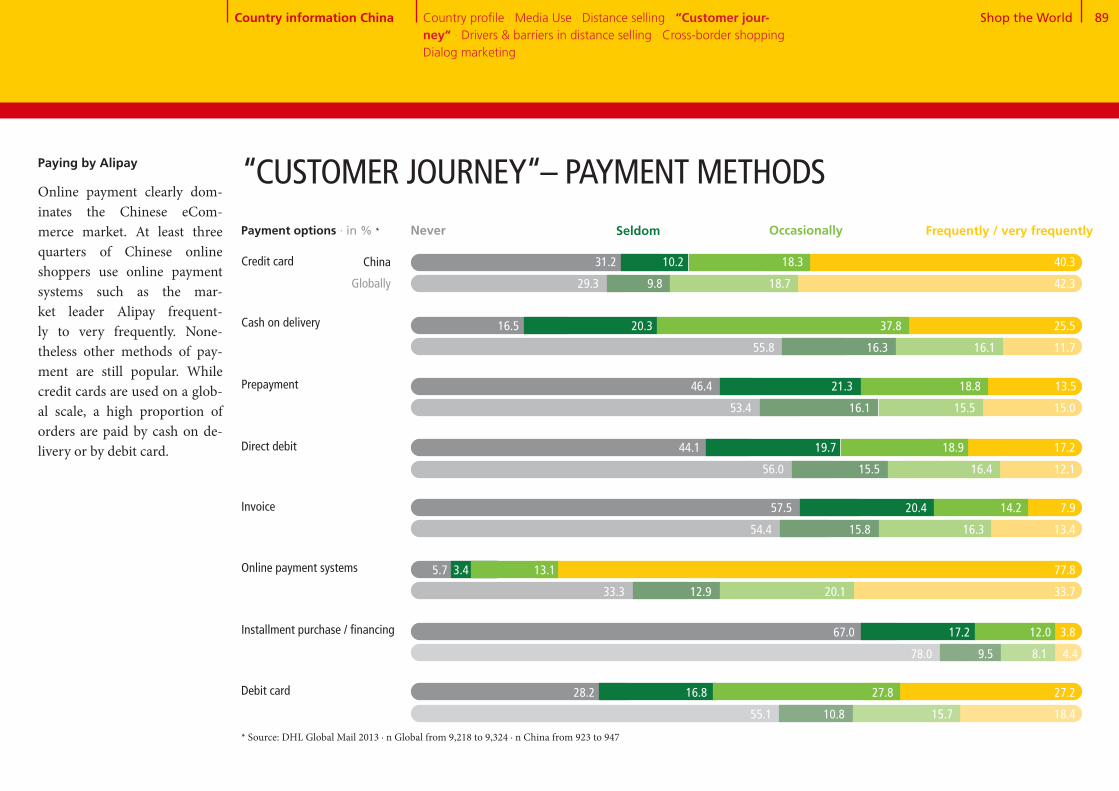

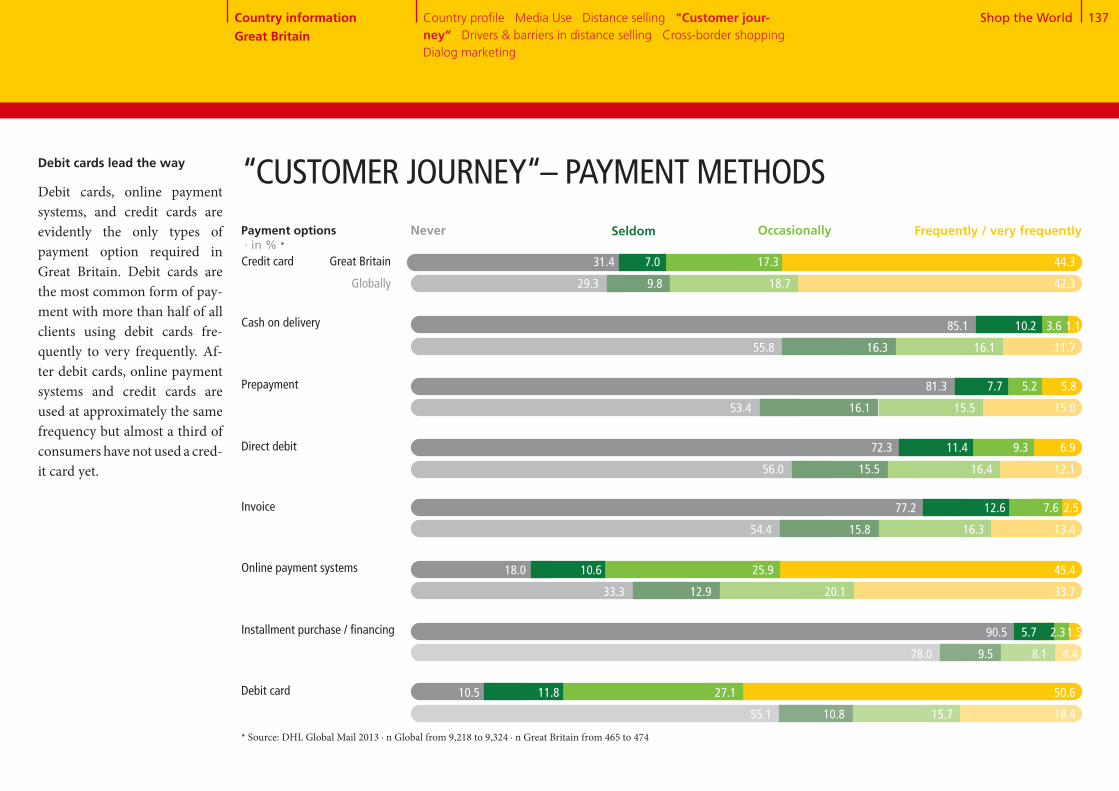

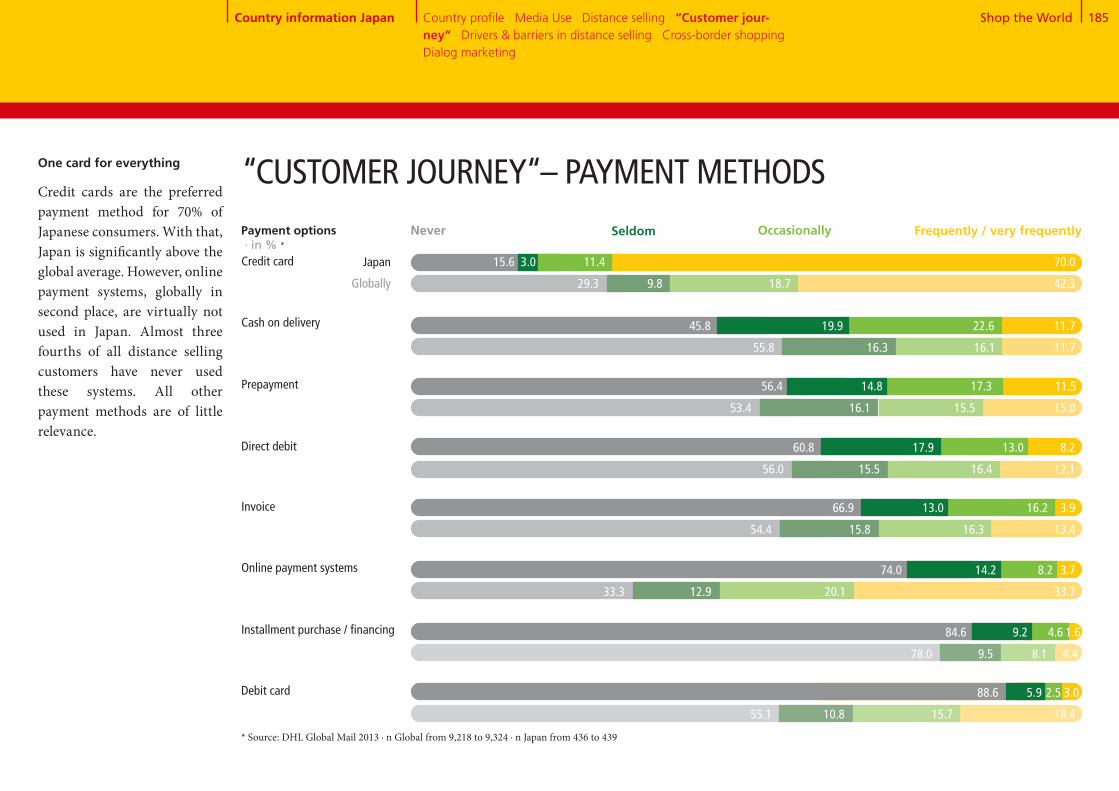

Credit cards are the most fre-quently used method of payment around the world . In global com-parison, some 61% of respon-dents said they used this method (very) frequently or occasionally . In Turkey, Japan, the US, South Korea, Brazil and Canada this figure rises to over 80% . The Netherlands, Poland and Russia tend to view credit card payment with scepticism – regular credit card use in these countries drops to just below 25% .

Online payment systems like PayPal and Alipay are the second most-frequent payment method used . More than half of distance selling customers around the world say they use them (very) frequently or occasionally . As with credit card payments, use of online payment systems varies from country to count-ry . In China, Aliplay – a wallet solution which supports all national debit cards and inter- national credit cards – is the do-minant choice . Almost all Chi-nese distance selling customers (91%) use it to pay for their or-ders . In Japan, by contrast, online payment systems are of little re- levance: Nine out of ten custom-

ers (88%) say they never use them or only use them on occa-sion .

Debit cards, prepayment, in-voice payment, direct debit and cash on delivery see similar use rates of between 28% and 34% . But there are some countries in which these payment methods are the preferred choice . Peo-ple in Great Britain (78%) prefer debit cards, while the Swiss (76%) and Germans (69%) like to receive an invoice before they pay . Cash on delivery, by con-trast, enjoys wide acceptance in India (75%) . Payment by install-ments is by far the least preferred method (12%), and is mostly used in South Korea (49%) .

Never Seldom Frequently / very frequentlyOccasionally

29 10 19 42Credit card

Online payment systems

Debit card

Prepayment

Invoice

Direct debit

Cash on delivery

Installment purchase / financing

33 13 20 34

55 11 16 18

53 16 16 15

54 16 16 13

56 16 16 12

78 9 8 4

56 1616 12

Frequently / very frequently

Payment in distance selling · in % *

Flags show national variations from the global average of at least +10% points.

Shop the World! - in half an hour

Payment methods

* Source: DHL Global Mail 2013 ∙ n = 9,218-9,324, Basis: Current distance selling users

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 12

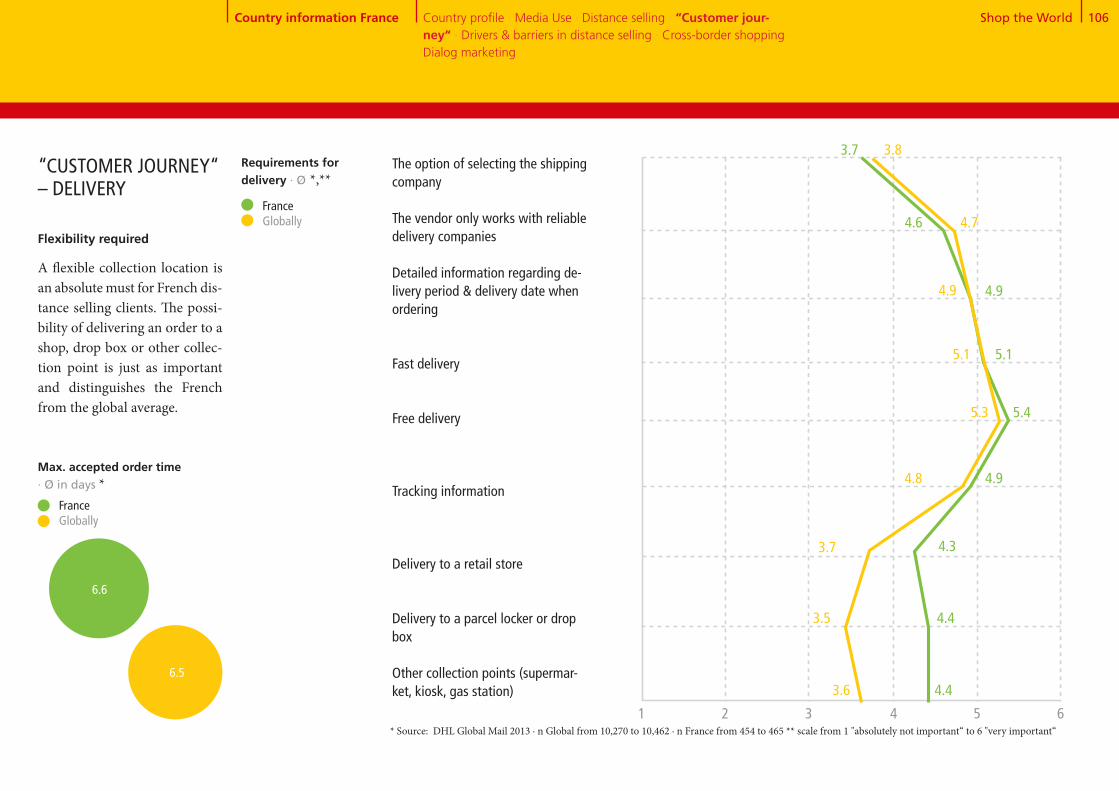

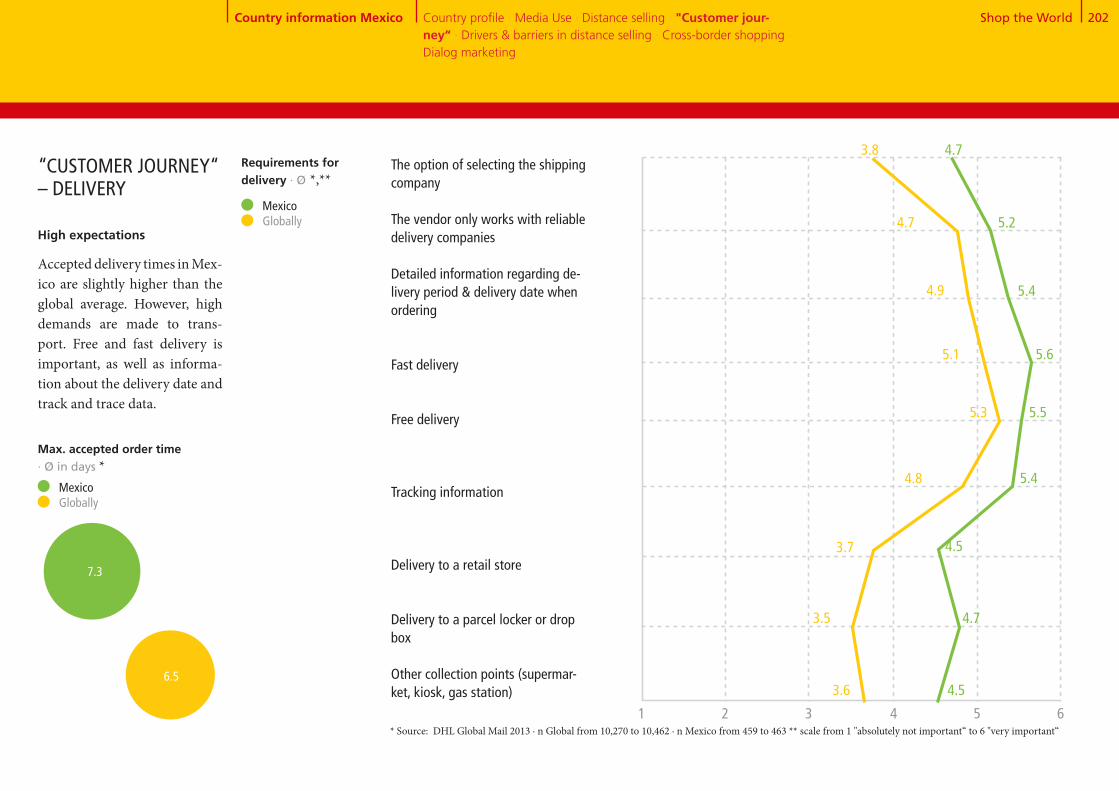

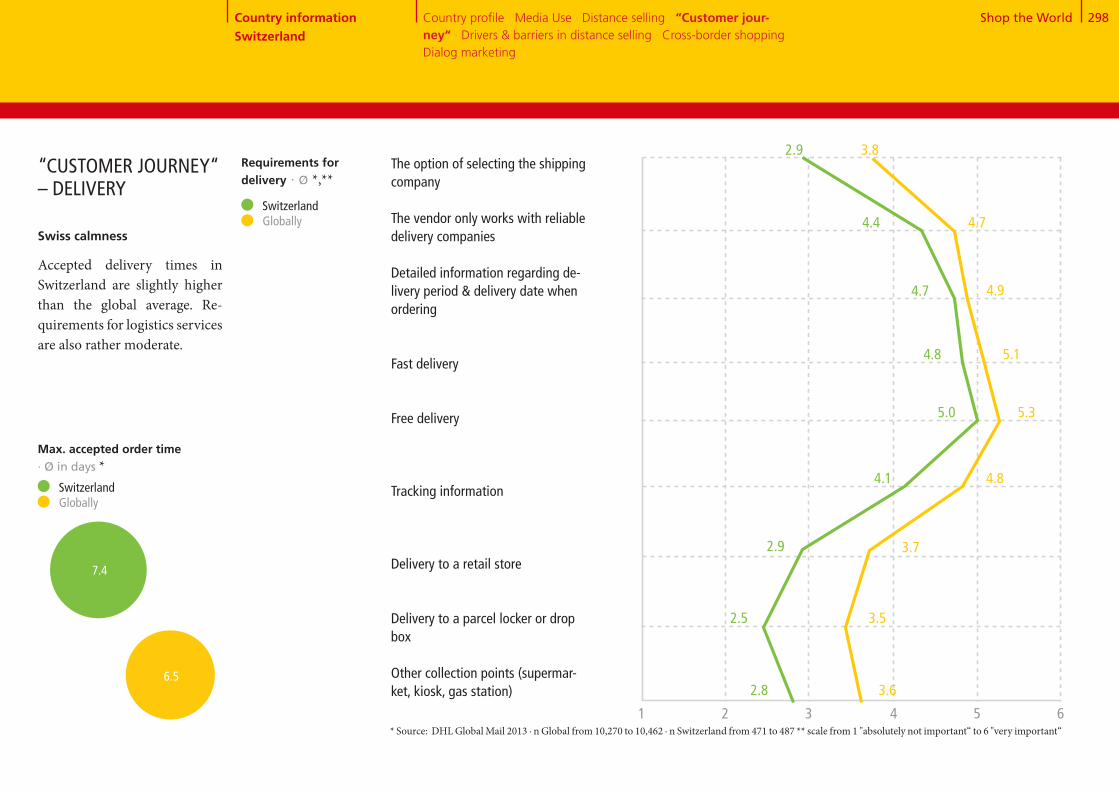

The maximum acceptable delivery time differs from country to country . Tol-erance ranges from 3 .8 days in Turkey to 12 .4 days in Russia, whereby the country’s size and the associated distances goods must travel are not necessarily the decid-ing factors . India is nine times the size of Germany, yet in both countries custom-ers expect delivery within 5 days . Signif-icantly more important, however, is pop-ulation density: In Russia, the country with the longest waiting times, there are only 9 inhabitants per square kilometer, while in Turkey there are 100 and over 500 in South Korea . As a result, Turkish and South Korean customers expect to receive their deliveries within 3 .8 and 3 .9 days respectively .

In all countries covered by the study, free and speedy deliveries are the key crite-ria when choosing a supplier . On a scale from 1 (not important) to 6 (very impor-tant), free delivery receives a 5 .3 rating, while speedy delivery gets a 5 .1 . Third place goes to ‘detailed information on de-livery times and delivery date at the time of order’ (4 .9) .

Preferences in respect of order tracking and supplier trustworthiness also differ from country to country: In emerging economies, some 30% of distance sell-ing customers fear that products might not arrive . As a result, the importance of track and trace options, and supplier trustworthiness is higher than in indus-trialised countries .

RU BR CA AU CH MX ES AT FR GL IT US JP CN UK IN DE NL PL KR TR

Max . accepted order time · in days *

Free delivery

Fast delivery

Detailed information regarding delivery period & delivery date when ordering

Tracking information

The vendor only works with reliable delivery companies

The option of selecting the shipping company

Delivery to a retail store

Other collection points (supermarket, kiosk, gas station)

Delivery to a parcel locker or drop box 1 2 3 4 5 6

Not important at all Very important

Globally

Requirements for delivery · Mean **

12.4

9.3

8.9

8.7

7.4

7.3

7.1

6.8

6.6 6.5

6.5

6.3 6.3

5.5

5.2

5.0 5.0

4.9

4.3

3.9

3.8

Shop the World! - in half an hour

Delivery

* Source: DHL Global Mail 2013 ∙ Mean, n (total) = 10,347; n (countries) = 424-989, Basis: Current and future distance selling users ** n = 10,270-10,462, Basis: Current and future distance selling users

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 13

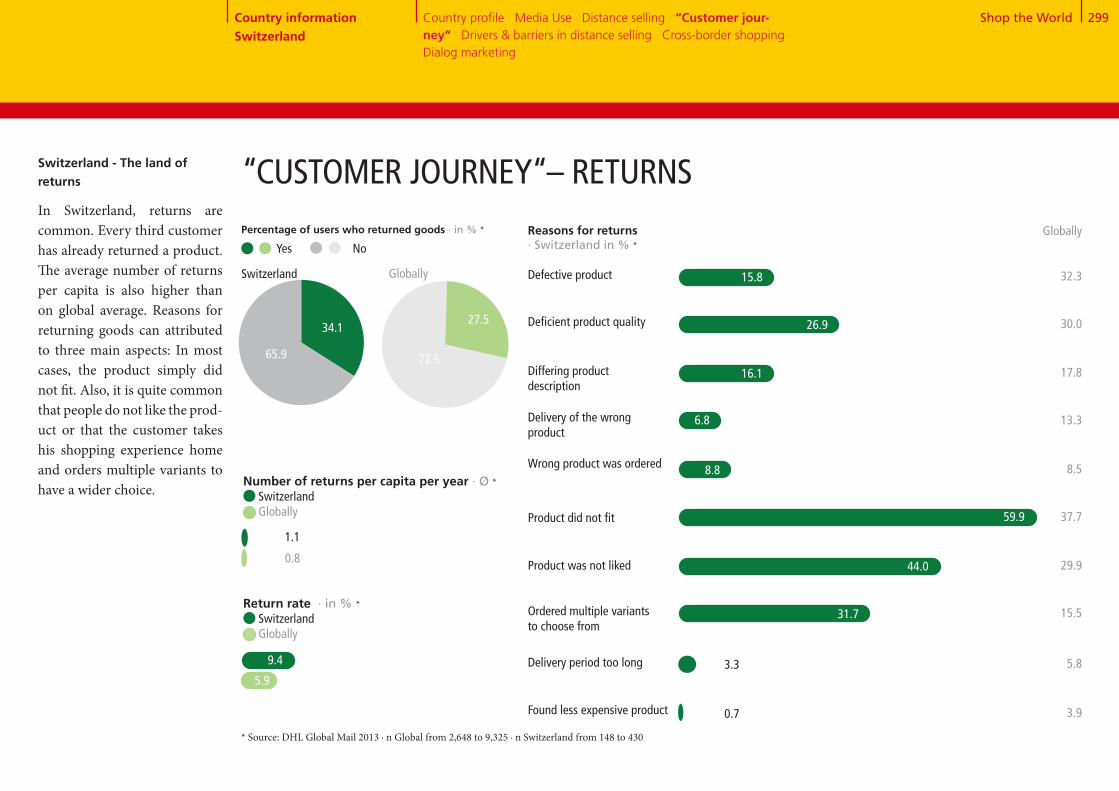

On average 13% of orders are returned in Germany and Aus- tria . In almost all other coun-tries, the return rate is below 10%; in Japan and Italy it is even as low as 2% . The global list of reasons for order returns is long, ranging from the top four – ‘does not fit’ (38%), ‘defect’ (32%), ‘poor quality’ (30%) and ‘does not meet expectations’ (30%) – to ‘excessive delivery time’ (6%) and ‘product cheaper elsewhere’ (4%) . However, the reasons for a return differ from region to re- gion . While fit and failure to meet expectations are the key rea- sons both in German-speaking countries and in Great Britain and Canada, poor quality do-minates in emerging economies and South Korea .The different return rates and reasons can in part be attributed to cultural preferences, shopping basket composition and coun-try-specific laws and legislation . Orders of clothing in multiple sizes and customer-friendly leg-

islation, certainly in German-speaking countries, result in high return rates, while the drivers in China are product piracy and poor quality standards .

Shop the World! - in half an hour

UK 6%

DE 13%

CN 5%

AT 13%

KR 5%

PL 3%

US 7%

CH 9%

JP 2%

FR 6%

IT 2%

ES 5%

NL 9%

AU 3%

IN 7%

BR 3%

RU 3%

TR 5%MX 3%

CA 4%

GL 6%

< 3% Returns

< 5% Returns

< 7% Returns

< 7% & more returns

Return rate · Mean in % *

Returns

* Source: DHL Global Mail 2013 ∙ n (total) = 9,325; n (countries) = 368-954, Basis: Current distance selling users

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 14

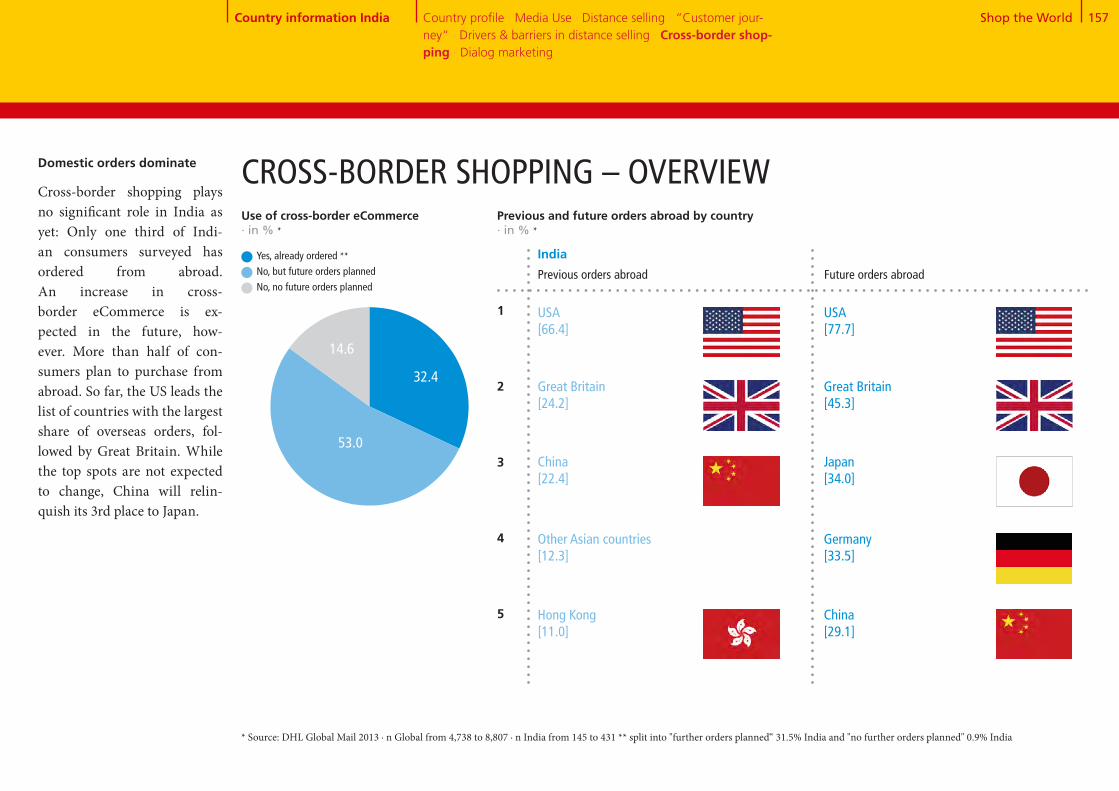

Cross-border shopping – Overview

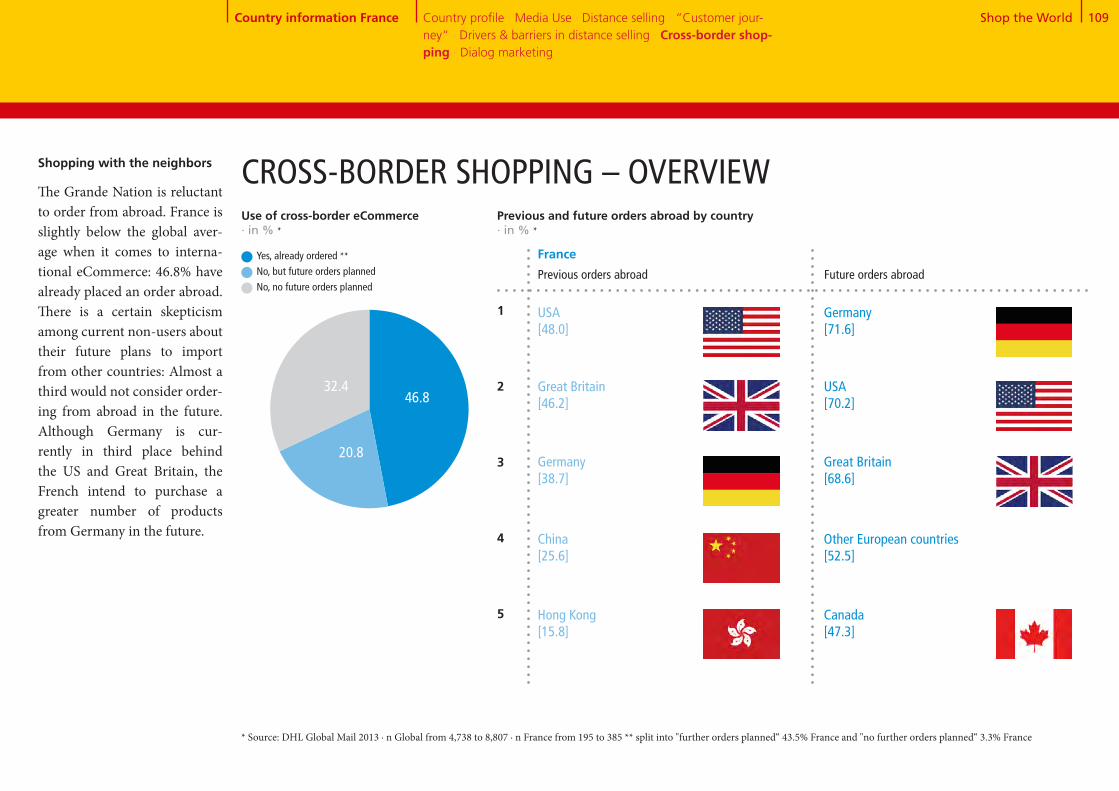

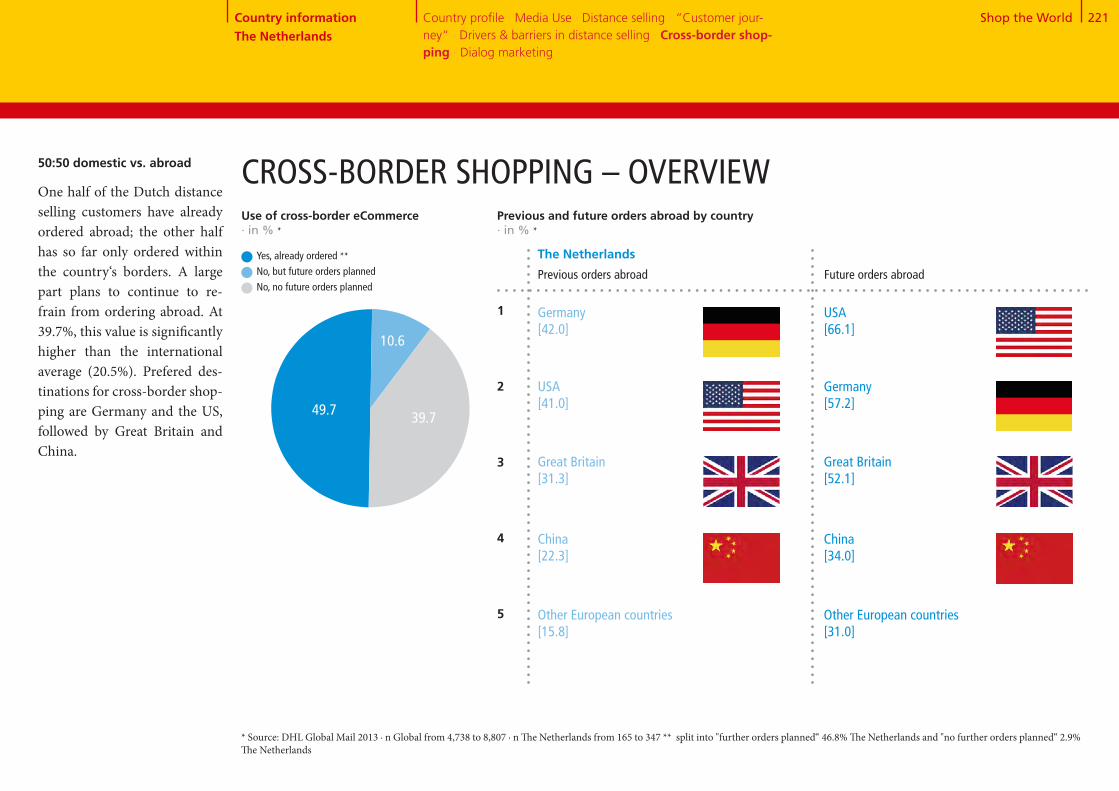

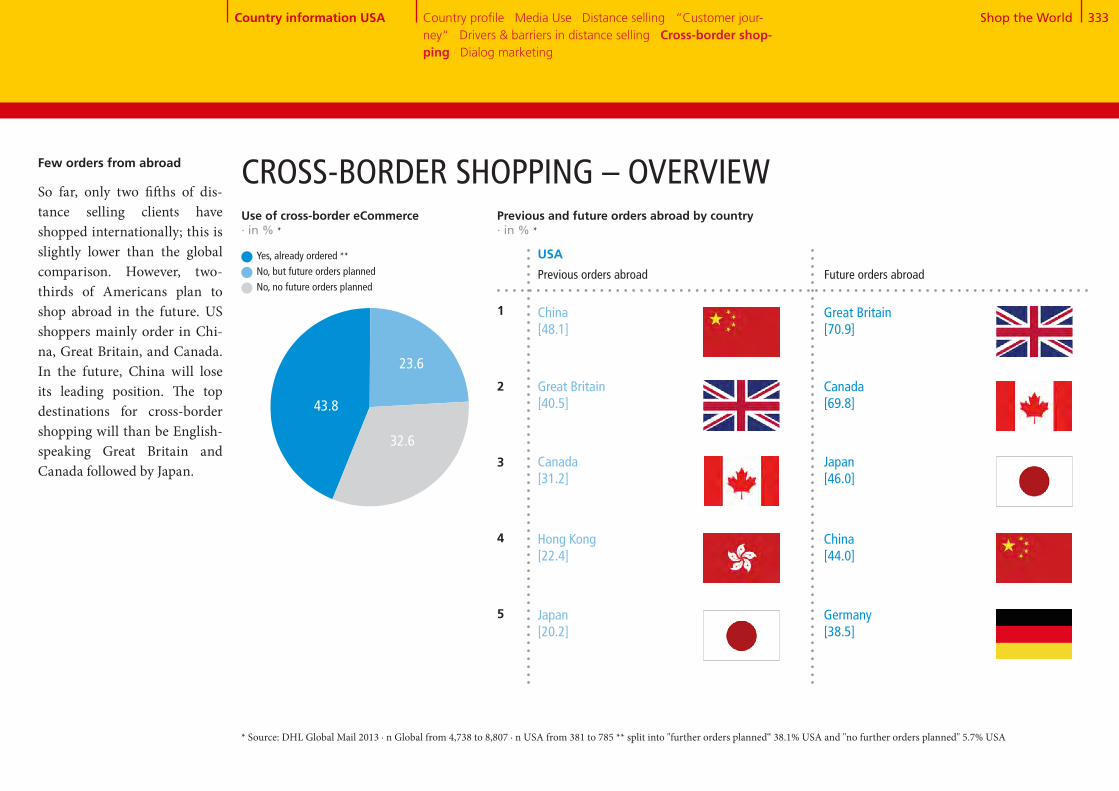

Shopping without limits is a way of life for many distance selling custom- ers . While some 45% have ordered goods from abroad, significant differ- ences are evident between industria-lised countries (53%) and emerging economies (31%) . While in parti-cular Europe has a well-established cross-border shopping tradition, it is the smaller or geographically iso-lated countries like Austria (79%), Australia (74%) and Switzerland (73%) that lead the field . Most of the goods ordered originate in the US . This applies to orders placed in emerging economies, industrialised countries in the Asia-Pacific re- gion, and Canada . Exceptions in-

clude Russia, where distance selling customers mostly order from China – as do those in the US . Customers in Europe tend to order from coun-tries in the region .

Cross-border shopping trends

While 45% of distance selling cus-tomers have ordered goods from abroad, 75% plan to do so in future . The share of cross-border orders will rise significantly among customers in emerging economies: India, Po-land and Mexico expect to see an in-crease from 30% to over 80%, while Brazil anticipates a rise from 41% to 84% . China promises a huge increa-se, from a low 20% to 78% . Some in-dustrialised countries err on the side

79

74

73

60

57

54

54

49

45

43

43

41

41

40

34

32

30

30

30

20

18

Use of cross-border eCommerce · in % **

123

GL AT CH DE ES FR IT NL UK AU CA JP KR US BR CN IN MX PL RU TR

(52) (91) (62) (47) (49) (48) (53) (42) (71) (77) (82) (69) (84) (48) (72) (66) (66) (87) (32) (66) (49)ASIA

(OTHER)

(31) (28) (42) (45) (45) (46) (53) (41) (37) (58) (41) (22) (19) (41) (55) (35) (24) (15) (32) (49) (40)

(29) (23) (37) (33) (42) (39) (36) (31) (31) (45) (29) (18) (8) (31) (18) (30) (22) (9) (24) (26) (18)

Top 3 countries for placing orders abroad · in % *

Example: In Austria, 91% of all respondents with experience of placing orders abroad had already ordered something in Germany.

Hong Kong

Shop the World! - in half an hour

Cross-border shoppingof caution when it comes to cross-border shopping: In Japan and the Netherlands, over 40% of respon-dents cannot see themselves placing an order with a supplier in another country . In South Korea and the US it is one third .

Despite the many obstacles, custom-ers seem satisfied with their cross-border orders . In global compari-son, only 3% of respondents who have ordered from abroad said they would not do so again . This number is particularly high in the US and in Switzerland (6% respectively) .

* Source: DHL Global Mail 2013 ∙ n (total) = 4,738; n (countries) = 91-393, Basis: Current users of distance selling ** n (total) = 11,030; n (countries) = 480-1,029, Basis: All *** n (total) = 8,932; n (countries) = 331-806, Basis: All

AT

AU

CH

UK

IT

ES

CA

DE

GL

NL

RU

FR

BR

US

MX

JP

KR

PL

IN

CN

TR

89

89

88

87

85

85

84

83

83

82

78

77

77

76

72

70

65

63

62

58

54

Future use of cross-border eCommerce · in % ***

AT

RU

IT

AU

ES

IN

BR

PL

CH

MX

CN

GL

UK

CA

DE

TR

FR

KR

US

NL

JP

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

Shop the World 15

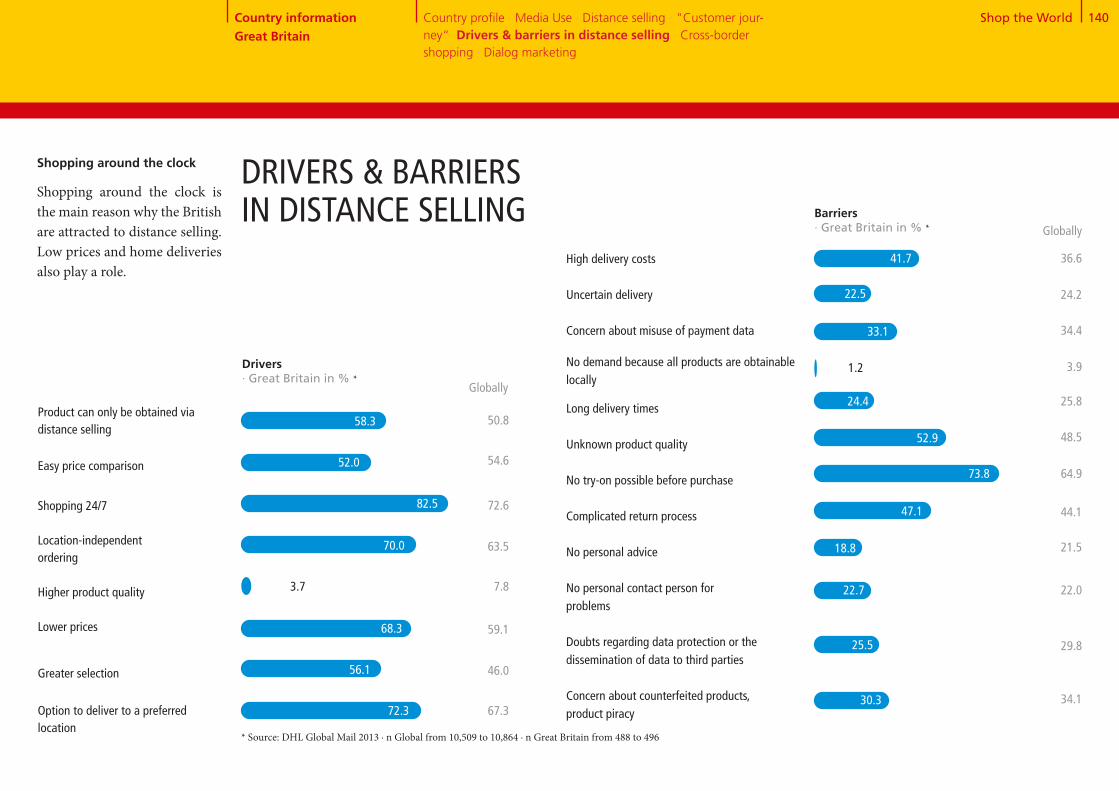

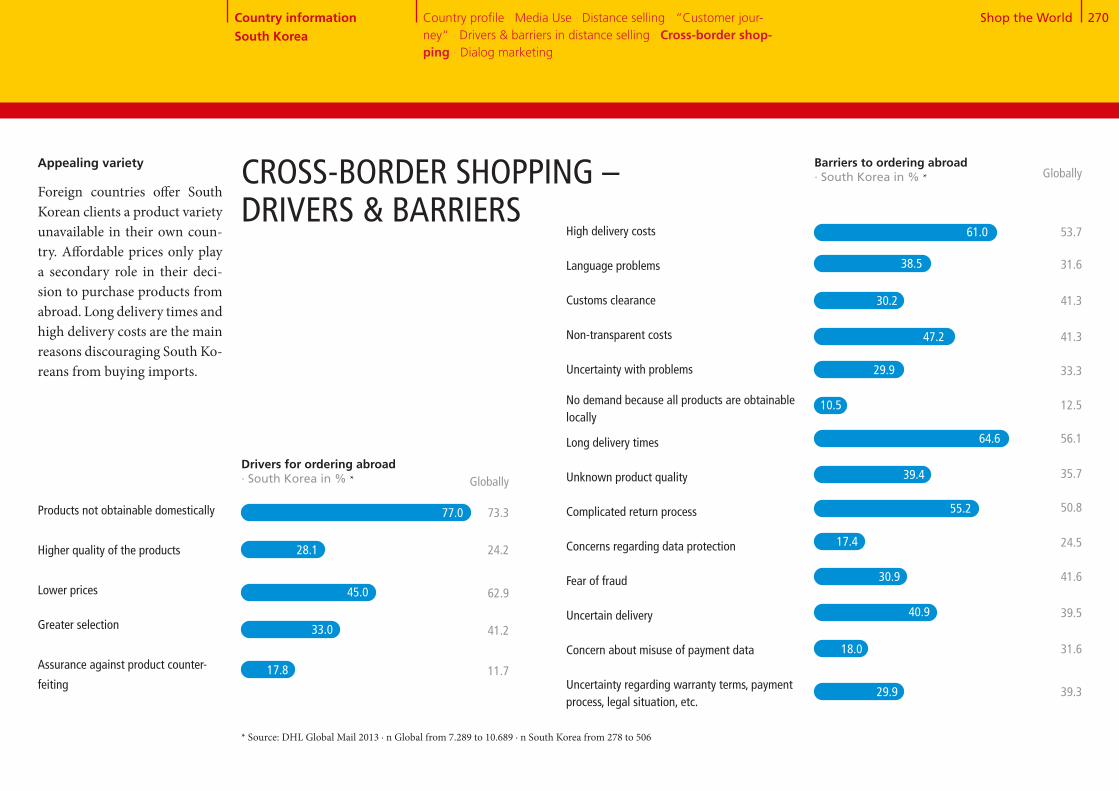

Drivers in cross-border shopping

The main reasons for shopping abroad are that products are not available domestically (73%) and that prices are lower elsewhere (63%) . In emerging economies, better quality and protection against counterfeit goods and product piracy are key factors . These were cited particularly fre-quently by customers in China, India and Russia . Obstacles to cross-border shopping

In global comparison, 20% of all internet users say they would not order from abroad in future . Among them are also experi-enced distance selling customers who think the obstacles and pro-blems of ordering abroad are just too big . The biggest obstacles are seen in the delivery process: Long delivery times (56%), high delivery charges (54%) and com-plex return management (51%) . These were cited to equal extent by respondents in all countries

covered by the study . Cultural differences between the coun-tries occur in the context of other barriers: Concern about counter-feit products is one of the main obstacles in Japan (56%), while in Switzerland only 31% share this concern . Language barriers tend to stop people in Turkey (49%), China (44%) and France (42%) from ordering goods from abroad .

Products not obtain-able domestically

Lower prices

Greater selection

Higher quality of the products

Assurance against product counterfeiting

74

74

72

57

69

62

49

35

41

49

8

15

24

4

6

Emerging economies

Industrialized countries (Europe)

Industrialized countries (Americas & APAC)

Drivers for ordering abroad · in % *

Shop the World! - in half an hour

* Source: DHL Global Mail 2013 ∙ n = 7,289, Basis: Current or future use of cross-border distance selling ** n = 10,689

Long delivery times

High delivery costs

Complicated return process

Fear of fraud

Customs clearance

Non-transparent costs

Uncertain delivery

Uncertainty regarding warranty terms, payment process, legal situation, etc.

Unknown product quality

Uncertainty with problems

Concern about misuse of payment data

Language problems

Concerns about data protection

No demand because all products are obtainable locally

56

54

51

42

41

41

39

39

33

36

32

32

Flags show national variations from the global average of at least +10% points.

24

13

Barriers to ordering abroad · in % **

Media Use · Distance selling-market overview · Distance selling use ·

Searching for product information · Supplier selection · Placing orders ·

Payment methods · Delivery · Returns · Cross-border shopping

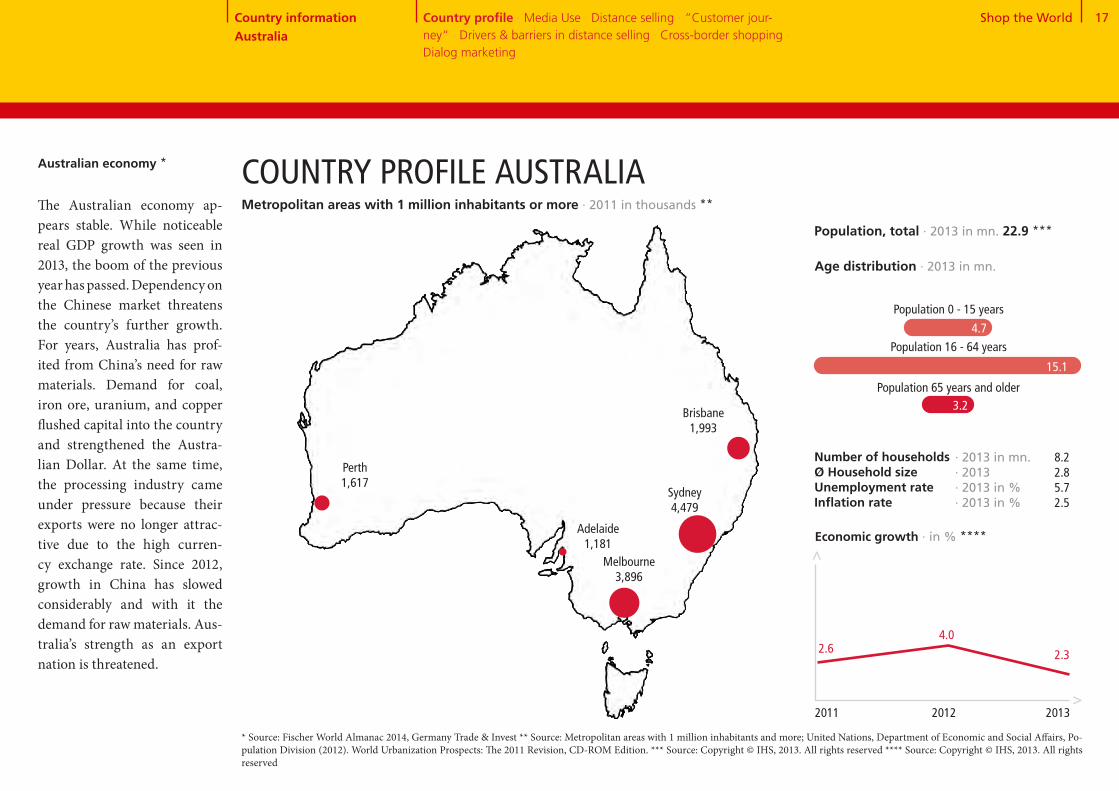

Country InformationAustralia

Beccy and Tom Australian distance selling clients are mobile, urban dwellers, price conscious, demanding… and 8 out of 10 shop abroad.

Shop the World 17

4.7

Population 0 - 15 years

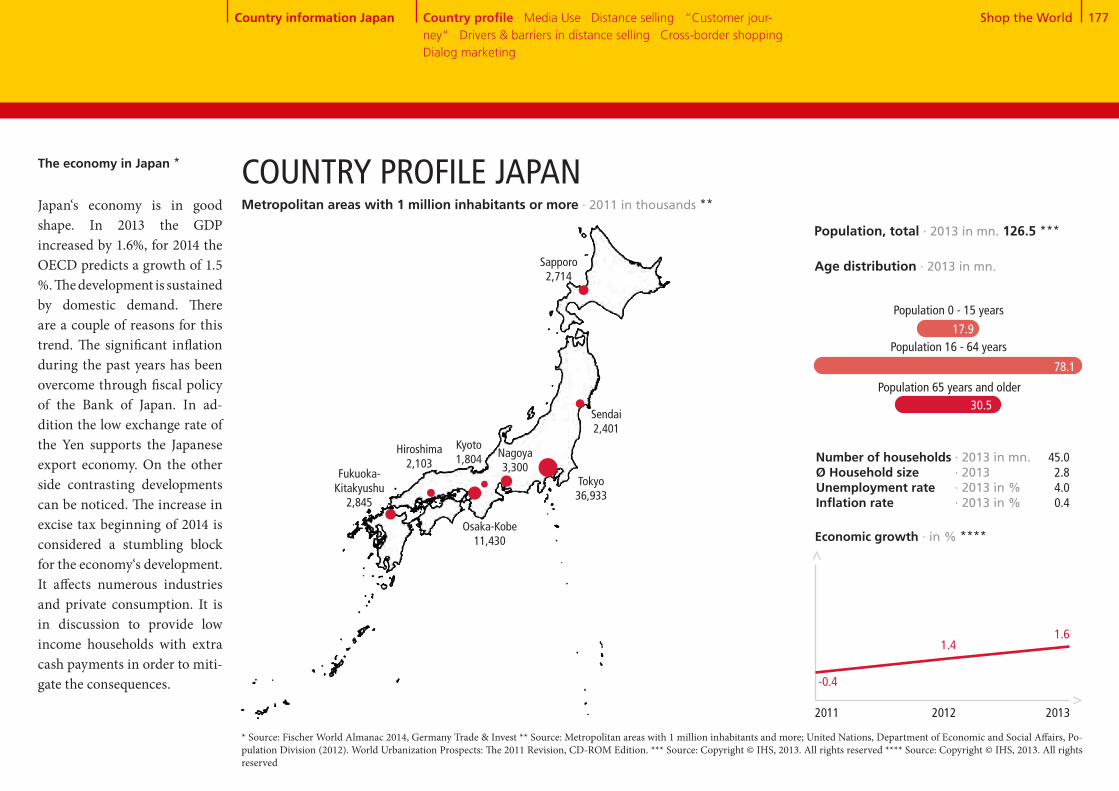

Australian economy * COUNTRY PROFILE AUSTRALIA

Melbourne 3,896

* Source: Fischer World Almanac 2014, Germany Trade & Invest ** Source: Metropolitan areas with 1 million inhabitants and more; United Nations, Department of Economic and Social Affairs, Po-pulation Division (2012). World Urbanization Prospects: The 2011 Revision, CD-ROM Edition. *** Source: Copyright © IHS, 2013. All rights reserved **** Source: Copyright © IHS, 2013. All rights reserved

Number of households Ø Household sizeUnemployment rateInflation rate

4.0

Economic growth · in % ****

>

>

2.32.6

2011 2012 2013

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

· 2013 in mn.· 2013· 2013 in %· 2013 in %

8.22.85.72.5

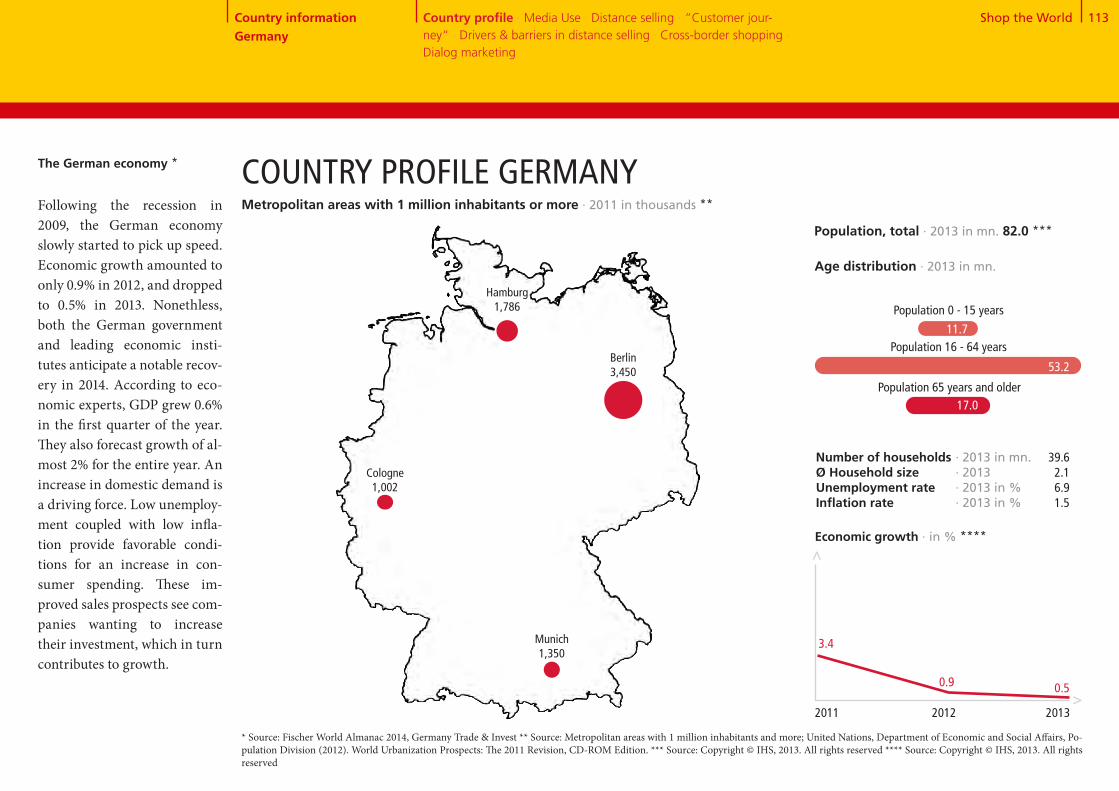

The Australian economy ap- pears stable. While noticeable real GDP growth was seen in 2013, the boom of the previous year has passed. Dependency on the Chinese market threatens the country’s further growth. For years, Australia has prof-ited from China’s need for raw materials. Demand for coal, iron ore, uranium, and copper flushed capital into the country and strengthened the Austra- lian Dollar. At the same time, the processing industry came under pressure because their exports were no longer attrac-tive due to the high curren-cy exchange rate. Since 2012, growth in China has slowed considerably and with it the demand for raw materials. Aus-tralia’s strength as an export nation is threatened.

15.1

3.2Brisbane 1,993

Perth 1,617

Adelaide 1,181

Sydney 4,479

Age distribution · 2013 in mn.

Population 65 years and older

Population, total · 2013 in mn. 22.9 ***

Population 16 - 64 years

Metropolitan areas with 1 million inhabitants or more · 2011 in thousands **

Shop the World 18

32+8+1+4+32+19+4MEDIA USE IN AUSTRALIA

25.1

106.2

Smartphone market penetration · in % *****Representative domestic population 16+, n = 1,000

52.2

Internet users · 2012 per 100 people **

Permanent access to broadband internet · 2012 per 100 people ***

Cellphones · 2012 per 100 people ****

2012 2013

64.6

Share of adspend by medium · in % *

TV Radio Movies Outdoor advertising

Total advertising expenditure · in EUR bn. *

Internet Newspapers Magazines

>>

2011 2012 2013 2014 2015

10.8

82.3

10.5

10.2

10.0

10.0

2016

11.2

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

32.5

18.5

4.3

4.10.8

8.2

31.6

* Source: Zenith Optimedia, 2013 ** Source: Copyright © IHS, 2013. All rights reserved *** Source: The World Bank **** Source: Copyright © IHS, 2013. All rights reserved **** Source: Our Mobile Planet: Google Global Smart phone Study 2013, http://www.thinkwithgoogle.com/mobileplanet/

Internet use

In Australia, the internet is part of everyday life. More than 80% of Australians are now online. The most widespread internet use is seen on the country’s heavily populated east coast. But even in the outback, which is somewhat behind in terms of development, surfing the web is by no means uncommon. Internet the most powerful medium

2013 saw the internet take the highest share of Australia’s media mix for the first time. High growth is expected primarily in internet and TV expenditure. Although spending in the big advertis- ing sectors of retail, automo-tive and FMCG is stunted by low consumer confidence, a stable annual increase of 2-3% in total expenditure is antici- pated by 2016.

Shop the World 19

Anything but laid back

With a CAGR of +16.5%, the Australian distance selling busi- ness is growing significantly faster than its global counter-part (+10.7%). This also applies to food, media products, and consumer electronics, which are already being ordered with above-average frequency.

DISTANCE SELLING IN AUSTRALIA

1,995.6

Distance selling purchases in 2013 - trend for 2018 · in EUR mn. * 2013 2018

Apparel and footwear

168.3

139.4

1,270.0

286.4

501.4

308.0

143.7128.1

106.4

119.7

91.3

47.9

Consumer electronics,

computers + equipment

Media products (books, CDs,

DVDs, etc.)

Housewares and home furni-

shings + textiles

Food + beverages

Household and consumer

appliances

Beauty and personal care

DIY and gardening

OTC drugs and dietary supple-

ments

Traditional toys and games

House cleaning (detergent,

chastener, etc.)

Development of distance selling and share of total retail 2011 - 2018 · in EUR bn. *

CAGR: 16.5%

Home shopping

Online shopping3.7 4.3 4.9

0.30.3

0.3

5.8 10.9

0.3

0.2

2011 2012 2013e 2014e 2018e

Share of total retail · in % 2.3 2.6 2.9 3.4

* Source: Euromonitor International

25.7

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

658.4

151.7

131.5

1,534.3

836.5

1,069.9

1,615.1

858.9

5.7

Shop the World 20

81+1984

+16

Distance selling on the up

Distance selling is a given in Australia. With over 80% of the population already placing orders online, this figure is set to rise.

Use of distance selling · in % *

80.8

19.2

Australia

Globally

83.5

16.5

Number of orders in the previous year · in % *

1 to 5 orders

6 to 10 orders

11 to 20 orders

More than 20 orders

No orders

25.5

28.9

14.3

19.2

12.0

20.5

35.9

15.2

16.5

12.0

Future ordering behavior (current users) · in % *

More frequently than in the last

12 months

Just as frequently as in the last

12 months

Less frequently than in the last

12 months

57.2

36.2

55.2

38.8

6.5 6.1

Non-users of distance selling - future plans · in % *

Yes59.4

Australia

Globally

Yes70.5

No40.6

No29.5

Yes No

Australia Globally Australia Globally

DISTANCE SELLING IN AUSTRALIA

* Source: DHL Global Mail 2013 ∙ n Global from 1,275 to 11,265 ∙ n Australia from 71 to 522

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

Shop the World 21

On trend, but different

Australia’s distance selling busi- ness is similar to the global average, but there are some differences in the ‘heavy users’ group. Highly active heavy internet users in Australia are broadly scattered across all age groups, with a slight majority among 30-49-year olds. They are ur-ban dwellers (68.3%) and tend to access the internet using mobile devices (60.2%). While the global average shows more women using distance selling, in Australia men have a slight edge. Another difference is seen in the number of older dis- tance selling clients in the heavy users group (27.1%). This compares with the global average of 21.2%.

DISTANCE SELLING IN AUSTRALIA

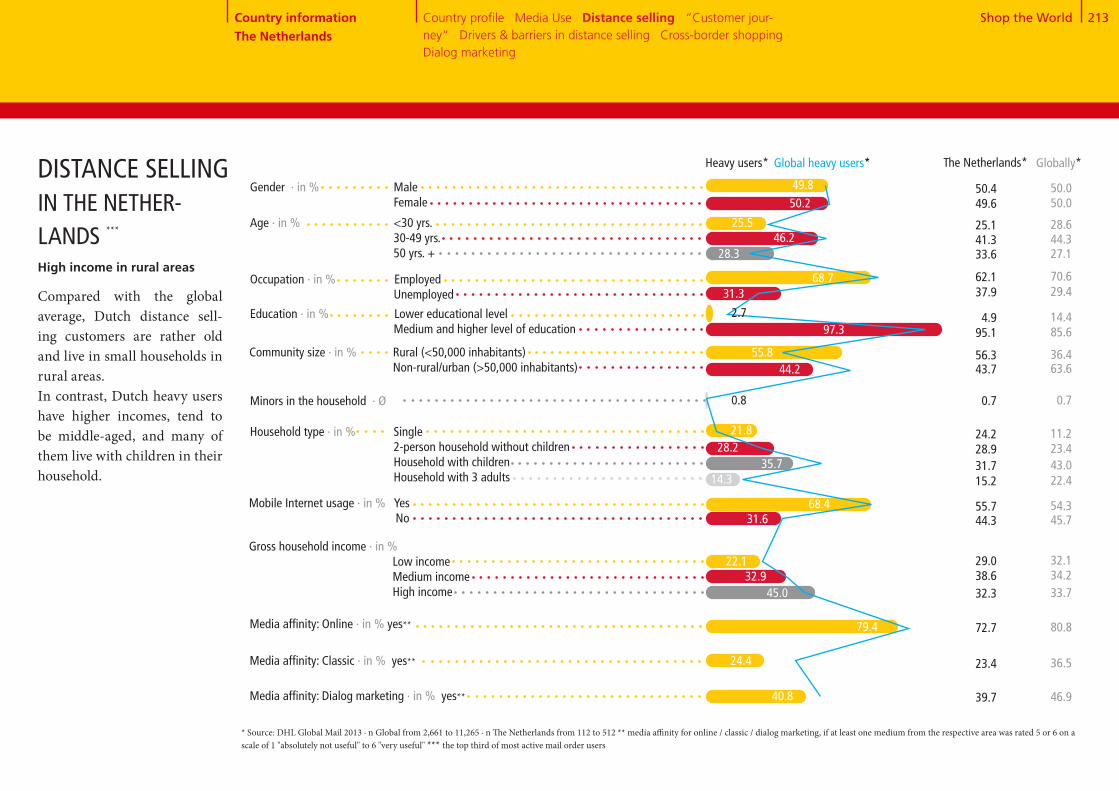

* Source: DHL Global Mail 2013 ∙ n Global from 2,661 to 11,265 ∙ n Australia from 109 to 522 ** media affinity for online / classic / dialog marketing, if at least one medium from the respective area was rated 5 or 6 on a scale of 1 "absolutely not useful" to 6 "very useful" *** the top third of most active mail order users

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

***

Globally*

40.0

Gender · in % Male Female

Age · in % <30 yrs. 30-49 yrs. 50 yrs. +

Occupation · in % Employed Unemployed

Education · in % Lower educational level Medium and higher level of education

17.1

Media affinity: Online · in % yes**

Community size · in % Rural (<50,000 inhabitants) Non-rural/urban (>50,000 inhabitants)

Minors in the household · Ø

Household type · in % Single 2-person household without children Household with children Household with 3 adults

Mobile Internet usage · in % Yes No

Gross household income · in % Low income Medium income High income

Media affinity: Classic · in % yes**

Media affinity: Dialog marketing · in % yes** 42.7

24.6

79.8

44.531.0

24.4

39.860.2

16.643.8

47.1

32.8

52.9

32.0

82.9

68.3

0.9

27.312.4

68.0

44.327.1

14.4

36.4

46.9

36.5

80.8

33.734.232.1

45.754.3

22.443.0

50.0

28.6

50.0

29.4

85.6

63.6

0.7

23.411.2

70.6

Australia*

42.628.7

15.9

31.1

40.6

29.3

73.8

36.434.828.9

44.355.7

16.344.2

49.9

28.7

50.1

36.8

84.1

68.9

0.9

25.813.8

63.2

27.1

31.7

Heavy users* Global heavy users*

Shop the World 22

“CUSTOMER JOURNEY“ – SEARCHING FOR PRODUCT INFORMATIONSearch for product information · Australia in % * Globally

34.1 35.5

53.2

24.0 23.4

35.6 44.2

22.9 23.9

45.8

49.0 42.5

24.6 25.1

11.8 15.1

16.6 15.1

8.2 9.7

39.1 37.8

Criteria for choosing a vendor · Australia in % *

Globally

Search engines

Customer ratings in blogs or forums

Product test ratings / expert test reports

Product check in a retail store

Retailer or manufacturer website

Online marketplace

Catalog

Mail advertising

Social media platforms such as Facebook and Twitter

Apps (on smartphone, iPad, or tablet)

Recommendations from friends, acquaintances, and colleagues

35.1 40.6Customer ratings on the supplier’s website

Price comparison sites

Large selection of products

Recommendation and experiences of friends, acquaintances, and colleagues

Official test seals, reviews, and test reports of independent institutions

Attractive product line

Favorable prices, promotions, & special offers

Straightforward return process

Free returns

Choice of preferred payment methods

Fast delivery

Free delivery

Good customer service

Positive customer ratings on the internet

15.1 13.7

20.7

10.1 8.8

30.0 26.6

12.0 14.9

56.9 51.7

9.6 12.9

14.4 20.8

30.6 22.6

27.5 25.7

44.0 45.2

15.4 18.5

19.9

Search engines in the leadMost Australian distance sell-ing clients use search engines to find information. Many also use retailer websites or online mar-ketplaces. They are also ex- tremely price-conscious.

* Source: DHL Global Mail 2013 ∙ n Global from 9,386 to 10,617 ∙ n Australia from 415 to 476, multiple mentioning

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

61.6

49.3

Shop the World 23

* Source: DHL Global Mail 2013 ∙ n Global from 10,218 to 10,384 ∙ n Australia from 462 to 468 ** scale from 1 "absolutely not useful“ to 6 "very useful“

Demanding target group

Persuasive advertising is a particular challenge in Aus- tralia. Online shoppers tend to perceive advertising media as unhelpful. Internet search en-gines lead the way, with 62.7% of users perceiving them as ‘very useful’.

ACCEPTANCE OF ADVERTISING MEDIA

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

Usefulness of advertising media · in % *, **

5 and 63 and 41 and 2

Ø

47.228.1 24.726.1 43.8 30.1

Online advertisingAustralia Globally

Television advertising

5 and 63 and 41 and 2

3.43.6

Ø

40.741.3 18.030.6 41.8 27.6

3.03.4

41.142.2 16.738.7 40.4 20.9Social media

Australia Globally

Advertising letters

2.93.1

32.546.2 21.333.9 37.6 28.5

2.93.4

Product suggestions in online shops

45.326.8 28.018.9 45.1 36.0

3.53.9

29.87.6 62.76.5 28.7 64.8

4.74.8

38.512.7 48.79.1 31.7 59.1

4.24.6

45.329.4 25.229.9 43.9 26.2

AustraliaGlobally

Household advertising

3.43.4

44.535.7 19.729.0 46.7 24.3

AustraliaGlobally

Advertisements in mag- azines and periodicals

3.23.4

47.338.6 14.134.8 43.1 22.1

AustraliaGlobally

Advertisements in newspapers

3.03.2

37.553.2 9.241.8 40.7 17.6

Australia Globally

Billboard advertise-ments

2.53.0

40.244.0 15.744.3 38.8 16.9

AustraliaGlobally

Radio

2.92.9

45.620.6 33.819.3 44.2 36.6

AustraliaGlobally

Catalogs from vendors

3.83.9

Australia Globally

Australia Globally

AustraliaGlobally

Internet search engines

Australia Globally

Price comparison sites

AustraliaGlobally

Shop the World 24

Australia Globally Use of different suppliers · in % *

Never Seldom Frequently / very frequently

Occasionally

* Source: DHL Global Mail 2013 ∙ n Global from 9,270 to 9,446 ∙ n Australia from 413 to 422

Online PC

Online mobile (tablet, smartphone)

By telephone

In writing (by post, fax)

By email

Order in store & delivery to home

73.2

2.7

1.7

4.2

75.0

3.2

2.1

4.4

“CUSTOMER JOURNEY“– PLACING ORDERS

Online ordering clearly prefer-red

Ordering online: Almost three-quarters of Australian distance selling clients order online using their PC. Another 15.6% use mobile devices, and 4.2% order via email.

Among the available sales channels, online marketplaces and online shops rank highly among Australians. As a result, only 9.1% and 13.8% of custom-ers have not used these mail order options in the last 12 months. The traditional print catalog loses out, with only half of customers ordering this way. Attitudes towards teleshopping are largely conservative (64.2% non-users in Australia versus 60.2% globally).

13.8 32.516.4 37.4

Australia

9.1 54.26.1 30.6

48.5 9.122.7 19.7

64.2 4.919.3 11.6

15.6

10.5

2.6

4.8

Order channels · in % *

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

Online marketplace

Mail order company from which I received a catalog

Merchant who advertises on TV

Online shop of a manufaturer or

retailer

Globally

9.9 54.38.7 27.0

38.5 12.622.8 26.1

60.2 6.617.6 15.7

15.4 31.216.8 36.6

Shop the World 25

Online payment wins

Online payment systems like PayPal are clearly preferred by Australian distance selling cli-ents: 61.9% use them frequently to very frequently (33.7% glob- ally). Unlike the global average, Australians have less of a pref- erence for payments made by invoice, cash on delivery, pre-payment, direct debit, or credit card. However, debit cards are used more often (22.7% ‘fre-quent use’ in Australia versus 18.4% globally). Installment payment/credit financing is seen only rarely in the Austra-lian distance selling business: 87.8% of customers say they never buy on credit (compared with 78.0% globally).

Cash on delivery

Prepayment

Direct debit

Credit card

* Source: DHL Global Mail 2013 ∙ n Global from 9,218 to 9,324 ∙ n Australia from 412 to 417

“CUSTOMER JOURNEY“– PAYMENT METHODS

Online payment systems

Installment purchase / financing

Debit card

Invoice

Payment options · in % *

Never Seldom Frequently / very frequentlyOccasionally

Australia

Globally

24.3 11.4 24.0 40.3

29.3 9.8 18.7 42.3

73.8 13.6 9.2 3.4

55.8 16.3 16.1 11.7

71.9 12.1 8.5 7.5

53.4 16.1 15.5 15.0

55.9 18.6 16.4 9.1

56.0 15.5 16.4 12.1

72.7 14.7 9.0 3.6

54.4 15.8 16.3 13.4

14.2 6.9 17.0 61.9

33.3 12.9 20.1 33.7

87.8 6.5 3.9 1.7

78.0 9.5 8.1 4.4

46.1 11.1 20.2 22.7

55.1 10.8 15.7 18.4

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

Shop the World 26

Australia Globally

The option of selecting the shipping company The vendor only works with reliable delivery companies

Detailed information regarding de-livery period & delivery date when ordering

Fast delivery

Free delivery

Tracking information

Delivery to a retail store

Delivery to a parcel locker or drop box

Other collection points (supermar-ket, kiosk, gas station) 3.4

3.3

2.9

5.1

4.6

5.0

3.2

4.8

4.4

Max. accepted order time · Ø in days *

3.6

3.5

3.7

5.3

4.8

5.1

3.8

4.9

4.7

* Source: DHL Global Mail 2013 ∙ n Global from 10,270 to 10,462 ∙ n Australia from 454 to 471 ** scale from 1 "absolutely not important“ to 6 "very important“

Speed is relative

Given Australia’s geography, speed is relative – as can be measured against customers’ delivery expectations. In some areas, it may take up to two days longer for a parcel to ar-rive. Expectations regarding transport are generally slightly lower compared with the global standard.

“CUSTOMER JOURNEY“ – DELIVERY

1 2 3 4 5 6

Requirements for delivery · Ø *,**

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

8.7

6.5

Australia Globally

Shop the World 27

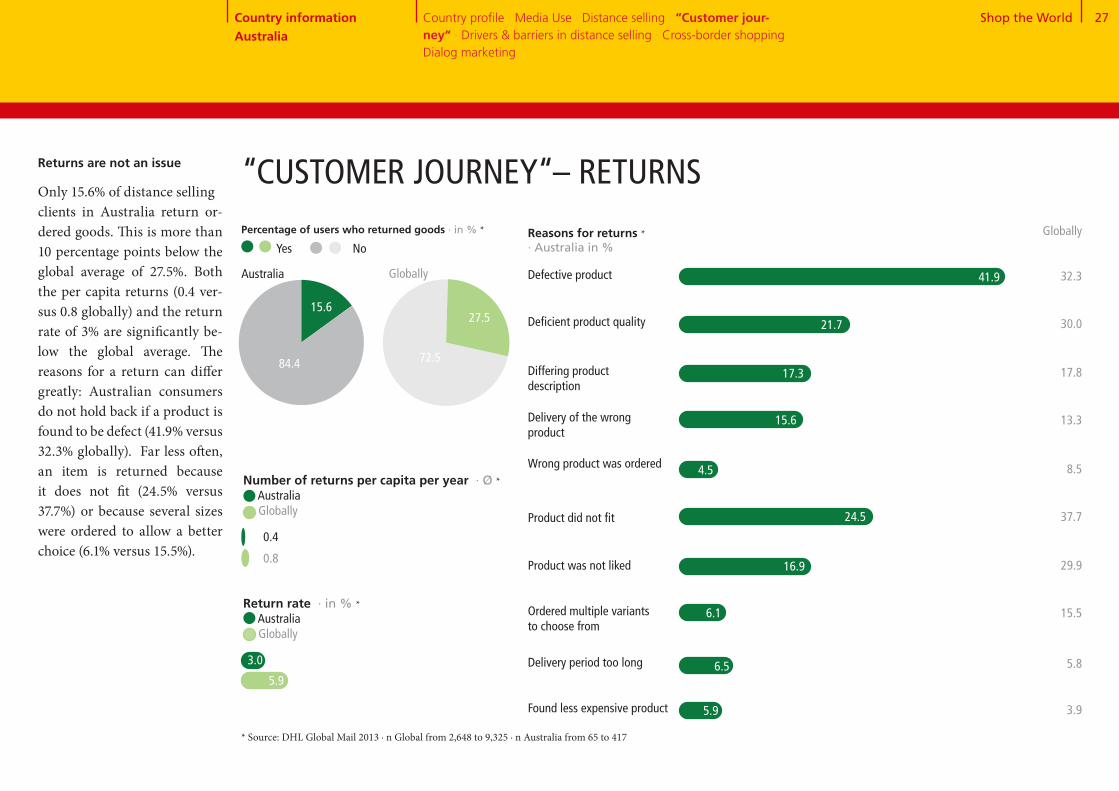

15+85Number of returns per capita per year · Ø * Australia Globally

0.8

0.4

Return rate · in % * Australia Globally

3.0

Reasons for returns * · Australia in %

Defective product 41.9

Percentage of users who returned goods · in % *

15.6

84.4

Australia Globally

Yes No

“CUSTOMER JOURNEY“– RETURNSReturns are not an issue

Only 15.6% of distance sellingclients in Australia return or-dered goods. This is more than 10 percentage points below the global average of 27.5%. Both the per capita returns (0.4 ver-sus 0.8 globally) and the return rate of 3% are significantly be-low the global average. The reasons for a return can differ greatly: Australian consumers do not hold back if a product is found to be defect (41.9% versus 32.3% globally). Far less often, an item is returned because it does not fit (24.5% versus 37.7%) or because several sizes were ordered to allow a better choice (6.1% versus 15.5%).

* Source: DHL Global Mail 2013 ∙ n Global from 2,648 to 9,325 ∙ n Australia from 65 to 417

Differing product description

Delivery of the wrong product

Wrong product was ordered

Product did not fit

Ordered multiple variants to choose from

Delivery period too long

Found less expensive product

Deficient product quality

Product was not liked

17.3

15.6

24.5

16.9

6.1

6.5

5.9

Globally

32.3

30.0

17.8

13.3

8.5

37.7

29.9

15.5

5.8

3.9

21.7

4.5

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

5.9

72+28 27.5

72.5

Shop the World 28

High delivery costs

Uncertain delivery

Concern about misuse of payment data

No demand because all products are obtainable locally

Long delivery periods

Unknown product quality

No try-on possible before purchase

Complicated return of the products

No personal advice

No personal contact person for problems

Doubts regarding data protection or the dissemination of data to third parties

Concern about counterfeited products, product piracy

DRIVERS & BARRIERS IN DISTANCE SELLING

Product can only be obtained via distance selling

Easy price comparison

Shopping 24/7

Location-independent ordering

Higher product quality

Lower prices

Greater selection

Option to deliver to a preferred location

Barriers · Australia in % *

50.8

54.6

72.6

63.5

7.8

59.1

46.0

67.3

72.3

46.4

67.4

Globally

36.6

24.2

34.4

3.9

25.8

48.5

64.9

44.1

21.5

22.0

29.8

34.1

A host of good reasons

Autonomy of time and place, pricing, and delivery options are arguments in favour of eCommerce in Australia. A noticeale drawback is con- sumers’ concern regarding unknown product quality.

Drivers · Australia in % *

Globally

* Source: DHL Global Mail 2013 ∙ n Global from 10,509 to 10,864 ∙ n Australia from 470 to 512

58.9

47.7

72.7

64.3

6.8

45.0

33.8

36.0

4.3

37.6

58.6

68.3

54.1

22.2

24.2

25.3

35.8

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“· Drivers & barriers in distance selling · Cross-border shopping · Dialog marketing

Shop the World 29

80+9+11

CROSS-BORDER SHOPPING – OVERVIEW

Previous orders abroad

Previous and future orders abroad by country · in % *

China[43.9]

Other Asian countries[17.4]

1

2

3

4

5

USA[77.4]

Great Britain[58.0]

Hong Kong[45.0]

Future orders abroad

Australia

* Source: DHL Global Mail 2013 ∙ n Global from 4,738 to 8,807 ∙ n Australia from 359 to 438 ** split into "further orders planned“ 78% Australia and "no further orders planned“ 2.1% Australia

Shopping without limits

In Australia, cross-border shopping is taken for grant-ed: 80.1% of consumers have ordered from abroad - a fig-ure far exceeding the global benchmark of 51.2%. The En- glish-speaking countries of the US and Great Britain are espe-cially popular. Orders are also placed with suppliers in Asia, primarily Hong Kong and Chi-na. Australians want to con-tinue to use these markets and are also turning to Japan for ordering abroad.

China[53.3]

Japan[34.9]

USA[85.5]

Great Britain[73.4]

Hong Kong[54.2]

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shop-ping · Dialog marketing

Use of cross-border eCommerce · in % *

Yes, already ordered **No, but future orders planned No, no future orders planned

8.6

80.1

11.3

Shop the World 30

Products not obtainable domestically

Higher quality of the products

Lower prices

Greater selection

Assurance against product counter-

feiting

Drivers for ordering abroad · Australia in % *

Barriers to ordering abroad · Australia in % *

High delivery costs Language problems

Customs clearance

Non-transparent costs

Uncertainty with problems

No demand because all products are obtainable locally

Long delivery times

Unknown product quality

Complicated return process

Concerns regarding data protection Fear of fraud Uncertain delivery

Concern about misuse of payment data

Uncertainty regarding warranty terms, payment process, legal situation, etc.

Globally

73.3

24.2

62.9

41.2

11.7

Globally

53.7

31.6

41.3

41.3

33.3

12.5

56.1

35.7

50.8

24.5

41.6

39.5

31.6

39.3

Price-driven purchase

When compared with the glob-al trend, the main driver for or-dering abroad is a lower price. In contrast, product quality (13.4% versus 24.2% globally) plays only a subordinate role. Lack of product availability on the domestic market and grea-ter selection are also key fac-tors.

CROSS-BORDER SHOPPING – DRIVERS & BARRIERS

* Source: DHL Global Mail 2013 ∙ n Global from 7,289 to 10,689 ∙ n Australia from 410 to 495

51.8

21.6

22.3

27.7

32.8

8.6

65.1

50.5

48.5

24.4

45.8

43.3

36.1

42.0

76.7

13.4

80.9

55.6

3.5

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shop-ping · Dialog marketing

Shop the World 31

Receipt of mailings and catalogs · Australia in % *

5 and 63 and 41 and 2

DIALOG MARKETING

Reading mailings and catalogs

· in % *,**

Australia

Globally

22.4 30.4 47.3

22.1 35.2 42.7

5 and 63 and 41 and 2

Response to mailings and catalogs

· in % *,**

Australia

Globally

28.1 49.1 22.8

29.0 45.8 25.3

Response channel for mailings and catalogs · Australia in % * Globally

Website visits

Visits to stores or

branch offices

Other online

response (e.g. chat,

Twitter, Facebook,

newsletter

registration, etc.)

Phone call

Business reply card

67.7 73.4

48.6

30.0

24.5

18.4

12.6

*Source: DHL Global Mail 2013 ∙ n Global from 8,788 to 11,265 ∙ n Australia from 393 to 522 ** scale from 1 "never“ to 6 "almost always“

Dialog marketing popular

Dialog marketing is widely used in Australia. At 42.6%, the number of people who receive one or more mailings and cat-alogs per week, is considerably higher than the global average of 26.9%. The approximately 11.2% of the online population that do not receive mailings is within the global average. Also, mailing recipients look forward to receiving these mails: At 47.3%, frequency in reading di-alog marketing mails is almost 5 percentage points higher than the global average. In contrast, recipients are less enthusiastic when it comes to responding via the established channels (e.g. via suppliers’ websites). They do, however, tend to go directly to an advertiser’s out-let or store (68.9% versus 48.6% globally).

Globally

One or more times per week

One or more times per month

Less than once per month

Never

26.9

33.7

27.7

11.6 68.9

19.3

16.0

17.5

6.4

42.6

24.7

21.5

11.2

Country information Australia

Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border shop-ping · Dialog marketing

Country InformationAustria

Christian

Austrian eCommerce clients are educated, young, security-conscious and live in rural areas. They love to shop abroad.

Shop the World 33

The Austrian economy *

* Source: Fischer World Almanac 2014, Germany Trade & Invest ** Source: Metropolitan areas with 1 million inhabitants and more; United Nations, Department of Economic and Social Affairs, Po-pulation Division (2012). World Urbanization Prospects: The 2011 Revision, CD-ROM Edition. *** Source: Copyright © IHS, 2013. All rights reserved **** Source: Copyright © IHS, 2013. All rights reserved

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

After a poor fiscal year in 2012,Austria’s economy continued to stagnate throughout 2013. Unlike other European coun-tries, Austria avoided falling back into a recession but the economy only grew 0.5%. The low growth rate had the greatest impact on private households: while real earnings stagnated, the unemployment rate increased one percentage point to 7.6%. Private house-holds limited their consump-tion due to the economic un-certainty and domestic demand regressed. The outlook for 2014 appears much better however - at the start of the year Austrian companies reported their order books to be fuller than in recent years.

1.3Population 0 - 15 years

COUNTRY PROFILE AUSTRIA

Number of households Ø Household sizeUnemployment rateInflation rate

0.7

Economic growth · in % ****

>

>

0.5

2.9

2011 2012 2013

Age distribution · 2013 in mn.

Population 65 years and older

Population, total · 2013 in mn. 8.4 ***

Population 16 - 64 years

· 2013 in mn.· 2013· 2013 in %· 2013 in %

3.6 2.37.62.0

5.6

1.5

Metropolitan areas with 1 million inhabitants or more · 2011 in thousands **

Vienna1,708

Shop the World 34

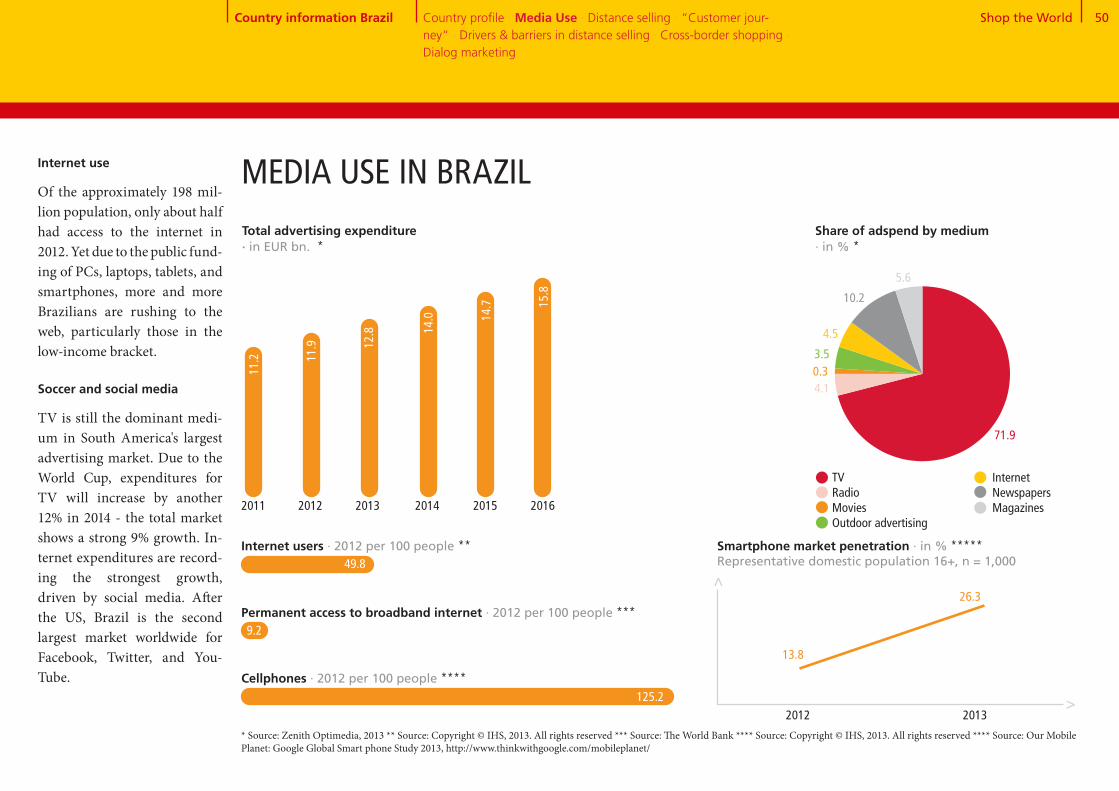

23+6+1+7+14+37+12MEDIA USE IN AUSTRIA

25.2

161.2

Smartphone market penetration · in % ***** Representative domestic population 16+, n = 1,000

35.9

Internet users · 2012 per 100 people **

Permanent access to broadband internet · 2012 per100 people ***

Cellphones · 2012 per 100 people ****

2012 2013

48.0

Share of adspend by medium · in % *

TV Radio Movies Outdoor advertising

Total advertising expenditure · in EUR bn. *

Internet Newspapers Magazines

>>

* Source: Zenith Optimedia, 2013 ** Source: Copyright © IHS, 2013. All rights reserved *** Source: The World Bank **** Source: Copyright © IHS, 2013. All rights reserved **** Source: Our Mobile Planet: Google Global Smart phone Study 2013, http://www.thinkwithgoogle.com/mobileplanet/

2011 2012 2013 2014 2015

3.4

81.0

3.3

3.3

3.3

3.3

2016

3.5

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

14.4

36.9

12.2

6.5

0.4

5.6

24.0

Internet use

The extent to which the popu-lation uses the internet is an indicator of how important it is. 81% of all Austrians had in-ternet access in 2012, while 25% had a permanent broadband connection. The future of in-ternet growth is going mobile. According to experts, "on de-mand" TV, videos and films are the greatest drivers.

In the land of newspapers and magazines

Printed advertising has an high share in Austria‘s media mix, while internet expen ditures are below the European average. Currently, the total advertising market is growing slightly at a rate of 1.2%.

Shop the World 35

Apparel and footwear

Consumer electronics,

computers + equipment

Media products (books, CDs,

DVDs, etc.)

Housewares and home furni-

shings + textiles

Food + beverages

Household and consumer

appliances

Beauty and personal care

DIY and gardening

OTC drugs and dietary supple-

ments

Traditional toys and games

House cleaning (detergent,

chastener, etc.)

Fashion and media products

Clothing and media products are bestsellers in Austria, fol-lowed by consumer electron- ics. Compared to the global average, toys are ordered more frequently, while cosmetics are less popular.

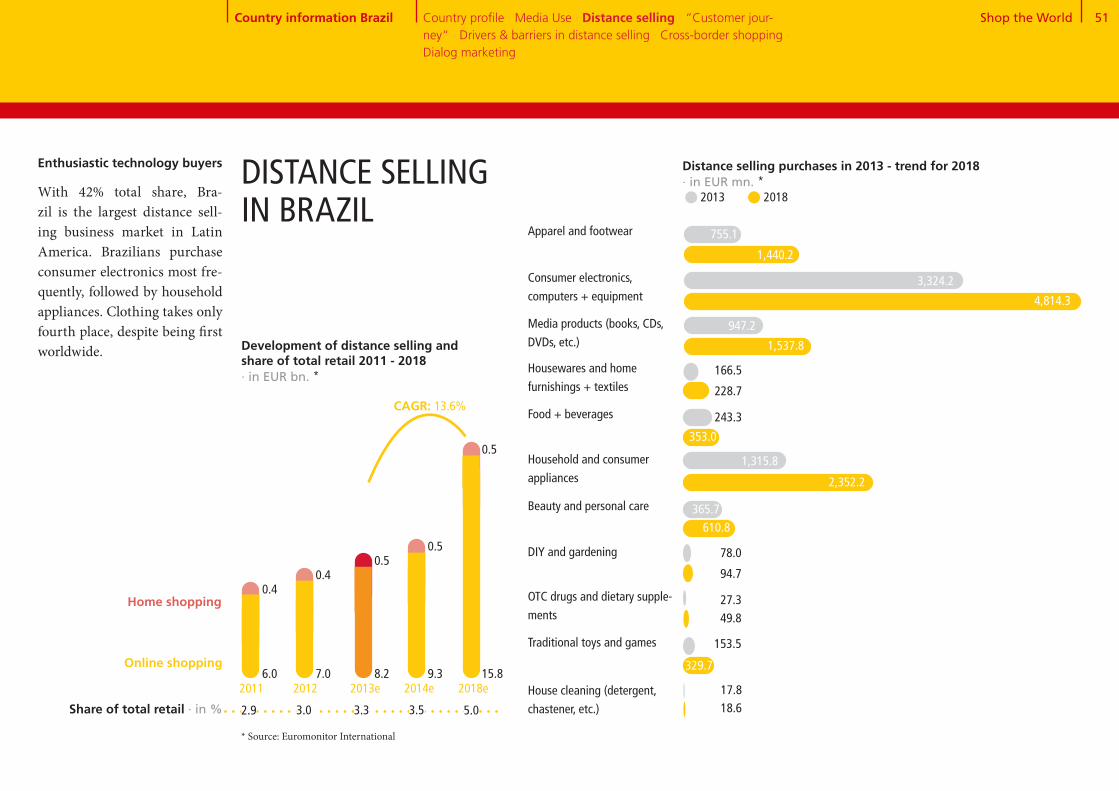

DISTANCE SELLING IN AUSTRIA

785.1

Distance selling purchases in 2013 - trend for 2018 · in EUR mn. * 2013 2018

375.4

1112.7

617.2

173.0

149.3

189.3

105.9

141.4

71.0

67.3

48.7

44.3

86.5

43.8

10.3

Development of distance selling and share of total retail 2011 - 2018 · in EUR bn. *

CAGR: 4.8%

Home shopping

Online shopping1.8 2.2 2.6

0.6

0.6

0.6

2.9 3.5

0.6

0.5

2011 2012 2013e 2014e 2018e

Share of total retail · in % 4.7 5.1 5.8 6.3 7.2

* Source: Euromonitor International

722.7

8.3

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

151.0

61.3

49.5

366.0

Shop the World 36

84+16

90+10

Top usage rates

In Austria, distance selling purchases are very common. Almost 90% are users and al-most three quarters of the non-users want to become involvedin the future.

Use of distance selling · in % *

89.8

10.2

Austria

Globally

83.5

16.5

Number of orders in the previous year · in % *

1 to 5 orders

6 to 10 orders

11 to 20 orders

No orders

21.4

39.0

17.5

10.2

11.9

20.5

35.9

15.2

16.5

12.0

Future ordering behavior (current users) · in % *

More frequently than in the last

12 months

Just as frequently as in the last

12 months

Less frequently than in the last

12 months

68.0

24.4

55.2

38.8

7.6 6.1

Non-users of distance selling - future plans · in % *

Yes73.5

Austria

Globally

Yes70.5

No26.5

No29.5

Yes No

Globally Austria Globally

DISTANCE SELLING IN AUSTRIA

* Source: DHL Global Mail 2013 ∙ n Global from 1,275 to 11,265 ∙ n Austria from 34 to 510

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

Austria

More than 20 orders

Shop the World 37

Mobile is the current trend

Active distance selling custom-ers have a unique profile in Austria: They are slightly older than the average population (78.9% over 30), live more of-ten in a rural area and also have a higher level of education. At 53.9%, the proportion of peo-ple living in smaller households (max. 2 people per household without children) is above aver-age. Consequently, this group rarely has a high household in-come. Mobile internet usage is widespread in Austria (76.1%). Traditional advertising media on the other hand is less valued than in the global average.

DISTANCE SELLING IN AUSTRIA

* Source: DHL Global Mail 2013 ∙ n from 2,661 to 11,265 ∙ n Austria from 112 to 510 ** media affinity for online / classic / dialog marketing, if at least one medium from the respective area was rated 5 or 6 on a scale of 1 "abso-lutely not useful" to 6 "very useful" *** the top third of most active mail order users

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

***

Global*

54.5

Gender · in % Male Female

Age · in % <30 yrs. 30-49 yrs. 50 yrs. +

Occupation · in % Employed Unemployed

Education · in % Lower educational level Medium and higher level of education

8.7

Media affinity: Online · in % yes**

Community size · in % Rural (<50,000 inhabitants) Non-rural/urban (>50,000 inhabitants)

Minors in the household · Ø

Household type · in % Single 2-person household without children Household with children Household with 3 adults

Mobile Internet usage · in % Yes No

Gross household income · in % Low income Medium income High income

Media affinity: Classic · in % yes**

Media affinity: Dialog marketing · in % yes** 40.0

21.4

83.4

33.040.1

26.9

23.976.1

8.737.4

47.1

21.1

52.9

28.8

91.3

34.7

0.8

33.920.0

71.2

44.327.1

14.4

36.4

46.9

36.5

80.8

33.734.232.1

45.754.3

22.443.0

50.0

28.6

50.0

29.4

85.6

63.6

0.7

23.411.2

70.6

Austria*

45.429.5

20.3

63.4

41.5

24.2

77.7

27.437.934.7

32.867.2

14.430.5

50.0

25.2

50.0

31.0

79.7

36.6

0.6

35.419.7

69.0

24.4

65.3

Heavy users* Global heavy users*

Shop the World 38

Search engines

Customer ratings in blogs or forums

Product test ratings / expert test reports

Product check in a retail store

Retailer or manufacturer website

Online marketplace

Catalog

Mail advertising

Social media platforms such as Facebook and Twitter

Apps (on smartphone, iPad, or tablet)

Recommendations from friends, acquaintances, and colleagues

Customer ratings on the supplier’s website

Price comparison sites

Large selection of products

Recommendation and experiences of friends, acquaintances, and colleagues

Official test seals, reviews, and test reports of independent institutions

Attractive product line

Favorable prices, promotions, & special offers

Straightforward return process

Free returns

Choice of preferred payment methods

Fast delivery

Free delivery

Good customer service

Positive customer ratings on the internet

Criteria for choosing a vendor · Austria in % *

“CUSTOMER JOURNEY“ – SEARCHING FOR PRODUCT INFORMATIONSearch for product information · Austria in % * Globally

33.4 35.5

53.2

27.3 23.4

44.9 44.2

22.7 23.9

48.5 45.8

50.3 42.5

23.8 25.1

17.7 15.1

9.6 15.1

5.8 9.7

35.4 37.8

Globally

54.4

48.9 40.6

7.0 13.7

20.7

9.6 8.8

22.8 26.6

15.0 14.9

46.0 51.7

19.2 12.9

36.2 20.8

31.5 22.6

23.1 25.7

42.5 45.2

14.7 18.5

23.1

Customer reviews are important

In Austria, customer reviews posted on retailer websites are extremely important when searching for information. Free returns are particularly rele-vant when selecting a product.

* Source: DHL Global Mail 2013 ∙ n Global from 9,386 to 10,617 ∙ n Austria from 453 to 489, multiple mentioning

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

Shop the World 39

* Source: DHL Global Mail 2013 ∙ n Global from 10,218 to 10,384 ∙ n Austria from 468 to 484 ** scale from 1 "absolutely not useful" to 6 "very useful“

Price checks are convincing

Distance selling clients in Aus-tria generally make purchasing decisions based on informationavailable online, mainly price comparison portals (59.4%) and search engines (57.6%). “Tradi-tional” catalogs from retailers continue to generate a great deal of interest, however.

ACCEPTANCE OF ADVERTISING MEDIA

Country information Austria Country profile · Media Use · Distance selling · “Customer jour-ney“ · Drivers & barriers in distance selling · Cross-border selling · Dialog marketing

Usefulness of advertising media · in % *, **

5 and 63 and 41 and 2

Ø43.640.8 15.6

26.1 43.8 30.1

Online advertisingAustriaGlobally

Television advertising

5 and 63 and 41 and 2

3.03.6

Ø

40.144.9 15.030.6 41.8 27.6

2.93.4

41.844.3 13.938.7 40.4 20.9Social media

Austria Globally

Advertising letters

2.93.1

33.155.4 11.633.9 37.6 28.5

2.53.4

Product suggestions in online shops

50.326.9 22.818.9 45.1 36.0

3.43.9

33.29.2 57.66.5 28.7 64.8

4.64.8

30.99.7 59.49.1 31.7 59.1

4.64.6

50.130.3 19.629.9 43.9 26.2

AustriaGlobally