shipbuilding and industrial preparedness - naval revie€¦ · training vessels (in progress), ......

TRANSCRIPT

16 CANADIAN NAVAL REVIEW VOLUME 2, NUMBER 3 (FALL 2006)

As Table 1 illustrates, the four Tribal-class destroyers came into service in 1972-73. They were the first warships in the West to be completely gas turbine powered. Since their mid-life conversions they now fill the function of task group command ships and provide long-range anti-air warfare protection. Two ships are still serving some 34 years after they came into service. Our two operational support ships (AORs) came into service in 1969-70. At over 35 years of age they are expected to operate for an-other five to 10 years before they are replaced.

In the mid-1960s the navy experimented with Fast Hydro-foil Escorts and commissioned HMCS Bras d’Or in 1968. Trial speeds as high as 63 knots were recorded. But due to a lack of money Bras d’Or was taken out of service in 1971.

Between 1992 and 1997, 12 Canadian Patrol Frigates (CPF) entered service to replace the ancient St. Laurent-class ships. These state-of-the art vessels are considered to be at the leading edge of naval warship technology. They are rapidly approaching mid-life.

Table 1 clearly shows the gap between naval building pro-grams in Canada – sometimes as long as 20-25 years. It seems obvious that one of the ways to deal with capacity and capability issues is simply to build more often.

The Commercial LinkWhat was the shipbuilding industry doing in the years be-tween naval programs? The industry was competing quite well in the years up to 1986. All manner of vessels were built, including icebreakers and oil rigs. And, like every

Canada’s shipbuilding industry is facing an unprecedent-ed domestic demand for Canadian-built government and commercial ships. The navy forecast is for construc-tion of three Joint Support Ships (JSS), eight Orca-class training vessels (in progress), up to 16 Single Class Sur-face Combatants (SCSC), and perhaps three armed ice-breakers. Life Extension Programs (FELEX) for the 12 Canadian Patrol Frigates (CPF) and mid-life refits for the four Victoria-class submarines are also on the books. And, it is estimated that replacement of the coast guard fleet will involve up to 50 vessels over the next 10 to 15 years. This has led to inevitable questions about the ca-pability, capacity, technical ability and skill levels of the industry and its people to meet the projected demand. This article will respond to these questions.

One cannot discuss the preparedness of the shipbuild-ing industry to meet the federal government’s demands in isolation of Canada’s shipbuilding policy, commercial requirements and ship repair demands. They are all part of the same whole and each is an important link in the industry chain. The interdependence is aptly alluded to in this passage from the Laws of the Navy, “On the strength of one link in the cable, Dependeth the might of the chain.”

BackgroundSince World War II the ships of the Ca-nadian Navy, with few exceptions, have been built in Canada. The St. Laurent-class destroyer escort, launched in 1951, represented the first purely Canadian design and build of a modern warship. St. Laurent was the first of 20 simi-lar ships to enter service between 1955 and 1964. Nine of these ships were either constructed or retrofitted with a hangar and flight deck to become the first anti-sub-marine warfare (ASW) ships in the world to carry and operate their own heavy ASW helicopter. All these ships served their country well, and most were in commission in excess of 30 years.

Shipbuilding and Industrial Preparedness

Vice-Admiral Peter Cairns (Ret’d)

Table 1. Canada: Major Warship ConstructionShip Class First Ship First Ship First Ship Last Ship Laid Down Launched In Service Paid Off

St. Laurent 1949 1951 1955 1998

Tribal 1969 1970 1972 Still in service

Protecteur AOR 1967 1968 1969 Still in service

CPF 1987 1988 1992 Still in service

VOLUME 2, NUMBER 3 (FALL 2006) CANADIAN NAVAL REVIEW 1�

other shipbuilding state, Canada’s shipbuilders received direct subsidies.

In 1986 all that changed. The government of Prime Min-ister Brian Mulroney rationalized the industry, thereby reducing its capacity by about 40%, and cancelled sub-sidies in anticipation of an Organisation for Economic Cooperation and Development (OECD) agreement on the elimination of subsidies worldwide. After the chang-es, the industry was left with a three-pronged policy:

1. Canadian owners who qualified and built their vessels in Canada were allowed accelerated capital cost allowance;

2. owners who wished to flag their ships Cana-dian and participate in the Canadian domes-tic trade were subject to a 25% duty on vessels imported into Canada; and

3. federal government fleets were to be con-structed, converted, refitted and repaired in Canada.

These measures are still in effect today. Unfortunately, the OECD initiative to eliminate subsidies was never ratified and Canada’s shipbuilders were left with what proved to be ineffective policies to compete in a highly-subsidized global shipbuilding industry. At the same time, Asian builders increased their capacity dramatically and global ship prices were driven to abnormally low levels – so low in fact that for a period in the 1990s they were below the costs North American and European shipbuilders paid for materials.

In 1994, Canada, the United States and Mexico entered into the North American Free Trade Agreement (NAF-TA). While this agreement has been enthusiastically en-dorsed by Canada, it did not address the protectionist measures supporting the marine industry in the United States that are contained in the Jones Act (also known as the Merchant Marine Act), passed in 1920. This legis-lation ensures that ships used in US domestic trade are owned, crewed, constructed and repaired in the United States. The failure of NAFTA to deal with the Jones Act

Halifax Shipyard.

Pho

to: C

anad

ian

Nav

al R

evie

w 2

006

18 CANADIAN NAVAL REVIEW VOLUME 2, NUMBER 3 (FALL 2006)

effectively closed the US market to Canada’s shipbuild-ers. The end result of all this was an unsubsidized Cana-dian industry fighting for survival in a subsidized market place in the West and facing vastly cheaper production costs among Asian builders.

In 2000, then Industry Minister Brian Tobin commis-sioned the National Partnership Project (NPP). Involved in this was a committee consisting of four members who were charged with finding practical ways to anchor the industry in a real and sustainable long-term market, promote innovation, skills, productivity and competi-tiveness, and suggest practical enhancements to exist-ing federal programs. The committee tabled its report – “Breaking Through” – in April 2001 and made 36 rec-ommendations.1 This report has become the foundation document for the shipbuilding industry. Of course the government did not address all of the recommendations in the report – indeed it addressed very few – but it did introduce just enough measures to give the industry some hope for the future.

Several years later, the government appointed another committee, the Shipbuilding and Industrial Marine Ad-visory Committee (SIMAC). The committee’s report was issued in October 2005. The report is entitled “Recom-mendations to the Minister for a Shipbuilding, Industry Transformative Strategy for a Duty Free Environment,” and was designed to assist the Canadian shipbuilding/repair and industrial marine industry to become self-sustaining and competitive, both domestically and in certain international niche markets.2 The defeat of the Liberal government in January 2006, coupled with what appears to be a lack of interest in this file by the new gov-ernment, raises doubts as to whether this strategy will be embraced.

A Strategy to Sustain the Shipbuilding IndustryA proposed strategy to build the base to sustain itself is outlined in Figure 1.

Figure 1. Shipbuilding Transformative Strategy

Source: The Shipbuilding and Industrial Marine Advisory Committee (SIMAC).

This strategy requires the federal government to kick-start the industry by facilitating demand. The strategy proposes the federal government look at five policy ar-eas. First, retain and improve on the key elements of the 2001 Policy Framework. Second, combine the Cana-dian ship owner’s Accelerated Capital Cost Allowance (ACCA) with the 15% Structured Financing Facility (SFF) program. At present the Canadian owner must choose between one or the other. The shortcomings of the SFF program are well documented. Third, adjust the tax policy to make it more supportive as has been done in other manufacturing industries. Fourth, investigate extended term financing for Canadians who build ships in Canada. This is common practice in several shipbuild-ing states. Last, implement government procurement policies that reduce the extreme cycles of government fleet renewal. This article will only discuss procurement

The 2006 launch of HMS Daring, the next generation of Royal Navy destroyers.

Inte

rnet

imag

e

VOLUME 2, NUMBER 3 (FALL 2006) CANADIAN NAVAL REVIEW 19

policy as it focuses directly on how the government, and particularly the navy, procures its ships.

For some time now the shipbuilding and industrial ma-rine industry has been proposing a more continuous build strategy for the navy. Assuming a navy of 16 de-stroyer/frigate vessels, as it is constituted today, build-ing one of these ships every two years would ensure no ship was ever older than 32 years (building a ship every 1.5 years would reduce the maximum age to 24 years). It would also provide considerable additional benefits to both the navy and the shipbuilding industry. The ben-efits would include:

• naval ships would be more modern and thus able to meet the changing demands of 21st century warfare;

• federal government outlays, the Department of National Defence (DND) budget and cash flows would be more predictable and manage-able;

• the maritime defence industrial base would be maintained and strengthened;

• shipbuilding and industrial marine companies would be able to maintain and build on their highly trained and specialized workforce and leverage this expertise into commercial mar-ket opportunities (see Figure 2 for an indica-tion of the learning curved involved in build-ing ships);

• continuous work would lead to increased in-dustry investment in research and develop-ment, new technology, new production pro-cesses, and workforce training and renewal;

• Canada would reap the economic and social benefits from the skilled jobs that would accrue;

• new designs and engineering changes would be iterative in nature; and

• production efficiencies would cause the cost per unit to de-crease.

Adopting a continuous build program for naval ships in Canada would require a sea change in the acquisition culture in the government and the navy. The most important change is that it would require the government to look beyond its four-year mandate and adopt a non-partisan

long-term strategy. It would not be easy but it is not im-possible.

Interestingly, the Australian shipbuilder ASC Pty Ltd (formerly the Australian Submarine Corporation) put forward a similar proposal to its government, in a docu-ment entitled “Improving the Cost-Effectiveness of Naval Shipbuilding in Australia.”3 While similar in ap-proach, its proposal goes a significant step further, with the aid of computer modeling, to show that the accepted wisdom of building a ship with a design life of 31 years is in fact the least cost-effective way to build a warship. The document shows that the last 15 years of a ship’s life are inordinately expensive, given the high cost of replacing the weapons and sensors at mid-life, and the increase in maintenance costs of the machinery with every year the ship approaches its designed end of life. It recommends that the mid-life refit be eliminated and that Australian warships be replaced after 20 years. According to “Im-proving the Cost-Effectiveness of Naval Shipbuilding in Australia”:

Replacing naval ships after 20 rather than 31 years would increase the numbers of warships built by some 50 per cent. This approach would allow for extended ship acquisition programs that would routinely produce new vessels in the flatter sections of the learning curve. As a result the unit costs of shipbuilding would be substan-tially lower.4

The Demand for Ships-2006 to 2020The demand for ships is real and it comes from all cor-ners of the Canadian shipbuilding market – navy, coast guard, commercial fleets (including Great Lakes) and

Figure 2. Typical Shipbuilding Learning Curve for a Series of 6 Vessels(with vessel #1 production hours = 100,000)

20 CANADIAN NAVAL REVIEW VOLUME 2, NUMBER 3 (FALL 2006)

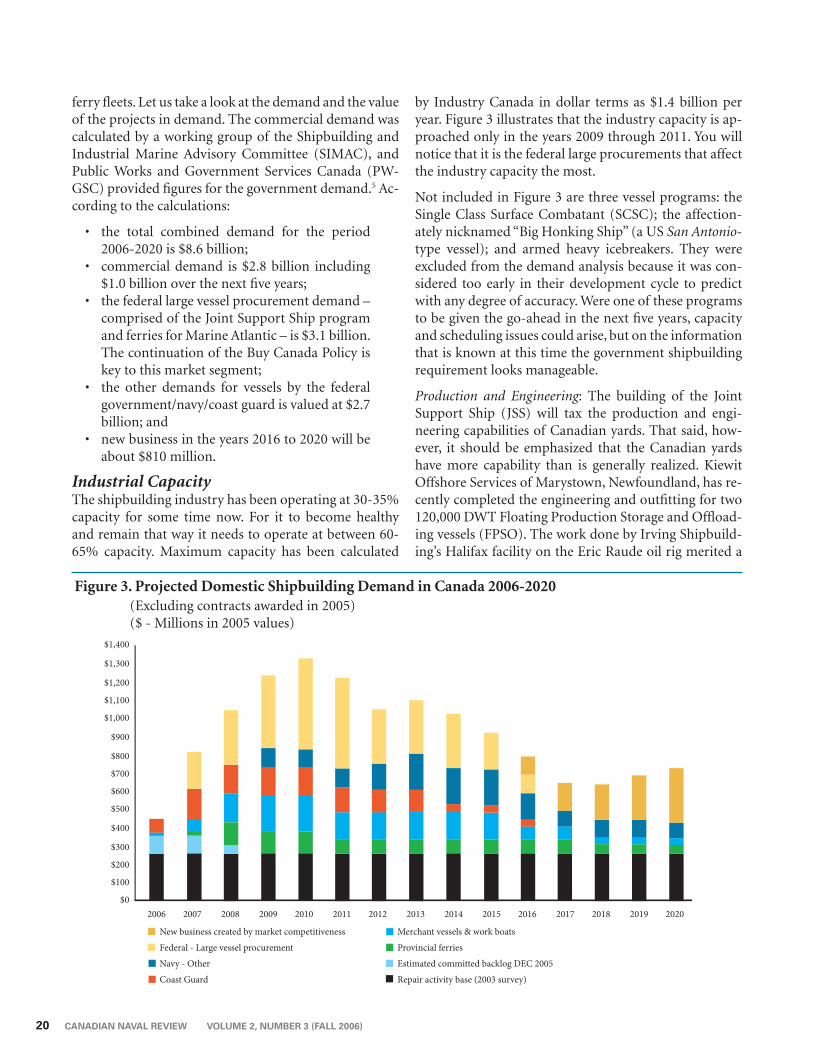

ferry fleets. Let us take a look at the demand and the value of the projects in demand. The commercial demand was calculated by a working group of the Shipbuilding and Industrial Marine Advisory Committee (SIMAC), and Public Works and Government Services Canada (PW-GSC) provided figures for the government demand.5 Ac-cording to the calculations:

• the total combined demand for the period 2006-2020 is $8.6 billion;

• commercial demand is $2.8 billion including $1.0 billion over the next five years;

• the federal large vessel procurement demand – comprised of the Joint Support Ship program and ferries for Marine Atlantic – is $3.1 billion. The continuation of the Buy Canada Policy is key to this market segment;

• the other demands for vessels by the federal government/navy/coast guard is valued at $2.7 billion; and

• new business in the years 2016 to 2020 will be about $810 million.

Industrial CapacityThe shipbuilding industry has been operating at 30-35% capacity for some time now. For it to become healthy and remain that way it needs to operate at between 60-65% capacity. Maximum capacity has been calculated

by Industry Canada in dollar terms as $1.4 billion per year. Figure 3 illustrates that the industry capacity is ap-proached only in the years 2009 through 2011. You will notice that it is the federal large procurements that affect the industry capacity the most.

Not included in Figure 3 are three vessel programs: the Single Class Surface Combatant (SCSC); the affection-ately nicknamed “Big Honking Ship” (a US San Antonio-type vessel); and armed heavy icebreakers. They were excluded from the demand analysis because it was con-sidered too early in their development cycle to predict with any degree of accuracy. Were one of these programs to be given the go-ahead in the next five years, capacity and scheduling issues could arise, but on the information that is known at this time the government shipbuilding requirement looks manageable.

Production and Engineering: The building of the Joint Support Ship (JSS) will tax the production and engi-neering capabilities of Canadian yards. That said, how-ever, it should be emphasized that the Canadian yards have more capability than is generally realized. Kiewit Offshore Services of Marystown, Newfoundland, has re-cently completed the engineering and outfitting for two 120,000 DWT Floating Production Storage and Offload-ing vessels (FPSO). The work done by Irving Shipbuild-ing’s Halifax facility on the Eric Raude oil rig merited a

Figure 3. Projected Domestic Shipbuilding Demand in Canada 2006-2020(Excluding contracts awarded in 2005)($ - Millions in 2005 values)

VOLUME 2, NUMBER 3 (FALL 2006) CANADIAN NAVAL REVIEW 21

safety award from Exxon and a full-blown documentary on the Learning Channel. Both the Kiewit and Irving projects were on time and on budget.

Washington Marine Group’s (WMG) Victoria, British Columbia, shipyard has been selected as a preferred ship-yard for refitting Holland America Cruise Ships. WMG has excellent planning capability. Cruise ship refits are about 21 days long and include the change of complete habitability modules, and inspections and repairs of hull openings and screws/pods, etc. The last refit done by WMG was completed in only 17 days, four days early, and employed some 2,000 persons working 24/7.

Each of the major yards has computer-aided design and manufacturing processes. Panels are cut and shaped au-tomatically and joined by robotic welders. Each of the

Source: Department of National Defence Chief of Review Services, Report on Canadian Patrol Frigate Cost and Capability Comparison.

Figure 4. CPF Sailaway Cost Comparison with Frigates from Seven States ($M)

Design, facility, depot spares, PMO, documentation and training costs are not included in NATO sailaway costs.

Saint John Shipbuilding showing the Canadian Patrol Frigates under construction.

Pho

to: C

anad

ian

Nav

al R

evie

w 2

006

teams has European partners that will aug-ment Canadian capabilities with expertise and transfers of technology. The partners will leave their Canadian counterparts in much better condition to tackle future projects.

Capital Investment and Research and De-velopment (R&D): The 10 years prior to 2003 were years of low business volumes. They were also years in which several ship-yards went out of business. At this stage the industry needs more emphasis on de-velopment than research. Defraying the cost of front-end engineering is crucial to being competitive.

Given the forecast building demand, it is estimated that annual capital investment will increase to 5% of revenues from the 10-year average of 2%. Similarly, R&D will in-crease from 0.6% to 2% of revenues.6

Skilled Workers: The uncertain nature of shipbuilding in Canada calls for a varying mix of skills to meet a con-stantly changing workforce requirement. In 2003 direct employment was calculated at 3,800 full-time equivalent workers but income tax forms were issued to 6,520 work-ers. This means that 6,520 workers were required to cover off the skill requirements of the industry. It is safe to as-sume that less than half of these skilled workers received a paycheck for 52 weeks of work. This is not a comment on productivity or ability but only that some necessary skills cannot, presently, be used on a full-time basis. This

VOLUME 2, NUMBER 3 (FALL 2006) CANADIAN NAVAL REVIEW 21

safety award from Exxon and a full-blown documentary on the Learning Channel. Both the Kiewit and Irving projects were on time and on budget.

Washington Marine Group’s (WMG) Victoria, British Columbia, shipyard has been selected as a preferred ship-yard for refitting Holland America Cruise Ships. WMG has excellent planning capability. Cruise ship refits are about 21 days long and include the change of complete habitability modules, and inspections and repairs of hull openings and screws/pods, etc. The last refit done by WMG was completed in only 17 days, four days early, and employed some 2,000 persons working 24/7.

Each of the major yards has computer-aided design and manufacturing processes. Panels are cut and shaped au-tomatically and joined by robotic welders. Each of the

Source: Department of National Defence Chief of Review Services, Report on Canadian Patrol Frigate Cost and Capability Comparison.

Figure 4. CPF Sailaway Cost Comparison with Frigates from Seven States ($M)

Design, facility, depot spares, PMO, documentation and training costs are not included in NATO sailaway costs.

teams has European partners that will aug-ment Canadian capabilities with expertise and transfers of technology. The partners will leave their Canadian counterparts in much better condition to tackle future projects.

Capital Investment and Research and De-velopment (R&D): The 10 years prior to 2003 were years of low business volumes. They were also years in which several ship-yards went out of business. At this stage the industry needs more emphasis on de-velopment than research. Defraying the cost of front-end engineering is crucial to being competitive.

Given the forecast building demand, it is estimated that annual capital investment will increase to 5% of revenues from the 10-year average of 2%. Similarly, R&D will in-crease from 0.6% to 2% of revenues.6

Skilled Workers: The uncertain nature of shipbuilding in Canada calls for a varying mix of skills to meet a con-stantly changing workforce requirement. In 2003 direct employment was calculated at 3,800 full-time equivalent workers but income tax forms were issued to 6,520 work-ers. This means that 6,520 workers were required to cover off the skill requirements of the industry. It is safe to as-sume that less than half of these skilled workers received a paycheck for 52 weeks of work. This is not a comment on productivity or ability but only that some necessary skills cannot, presently, be used on a full-time basis. This

The stern section of HMCS Fredericton being lowered into place at Saint John Shipbuilding Ltd.

Pho

to: S

aint

John

Shi

pbui

ldin

g

22 CANADIAN NAVAL REVIEW VOLUME 2, NUMBER 3 (FALL 2006)

anomaly could be alleviated by increased overall levels of production such as a continuous build program could bring.

Another concern is whether there will be adequate num-bers of skilled trades persons available to meet the an-ticipated demand. The average age of a shipyard worker is about 45 years. This is comparable to the other manu-facturing sectors in Canada, North America and Eu-rope. What sets shipbuilding apart is that only 6% of its workers are under age 25 as opposed to 13% in other Canadian manufacturing industries. The problem will be exacerbated by the demand for skilled workers in Al-berta that is forecast to be about 100,000 over the next 10 years. Strong training and apprenticeship programs will be absolutely necessary. We have excellent training in-stitutions in Canada that will have to be utilized to their fullest.

Cost and Delivery Schedule: It is difficult to believe that a warship can be constructed more cheaply in the United States or Europe than in Canada. Evidence suggests that the so-called premium the navy would pay to build in Canada may be largely illusory – i.e., that it would not be more expensive to build the ships in Canada. Part of the problem with making an accurate comparison of costs is

trying to determine if costs are calculated the same way in different countries. There is evidence to suggest that they are not, so comparisons can be misleading. What is important to me, as a taxpayer, is that the benefits accrue to Canada. When you build offshore they do not. Figures 4 and 5 are charts done by the Chief of Review Services while conducting a cost comparison of the Canadian Pa-trol Frigate (CPF) with other NATO frigates.

As Figure 4 illustrates, the cost of the CPFs was higher than most of the other frigates. For the most part, how-ever, the cost differential is less than 10% which for a program of this size is not of consequence. As well, a comparison of cost like this does not indicate the dif-ferences among the frigates. Figure 5 is a comparison of capability and it indicates that while the CPF may have been slightly more expensive it is clearly the most capa-ble ship of the lot. The conclusion of the Chief of Review Services’ study states “Our analysis indicates that the CPF is a world-class fighting ship and that, based on NATO costing conventions, the production cost for the last ship is reasonably competitive with other nations. The CPF exceeds the individual marine and combat characteris-tics of other ships in decidedly more instances than it is equivalent or falls short.”

Figure 5. CPF Capability Comparison with 11 Frigates from Other States

Source: Department of National Defence Chief of Review Services, Report on Canadian Patrol Frigate Cost and Capability Comparison.

VOLUME 2, NUMBER 3 (FALL 2006) CANADIAN NAVAL REVIEW 23

Ship Country Type Length (m) Weight2 Complexity Duration1

(no cargo) (tonnes)Amsterdam Netherlands AOR 166 8,100 Less 47Patiño Spain AOR 166 8,100 Less 42Rotterdam Netherlands LPD 166 8,297 Similar 48BAC Spain AOR 166 9,700 Less 63*Berlin Germany AOR 173 9,800 Less 42Galicia Spain LPD 160 11,870 Similar 33ALSL UK LSD 176 12,800 Less 48Johan de Witt Netherlands LPD 181 15,000 Similar 48*Albion UK LPD 176 17,500 Similar 72Wave Knight UK AOR 196 17,500 Less 73Ocean UK LPH 203 20,250 Similar 64JSS Canada AOR(H)/AKR 210 22,000 51*BPE Spain LHD 230 22,000 Similar 63*LPD17 US LPD 208 22,000 More 99+*Fort Victoria UK AOR 203 24,600 Similar 75T-AKE US AOR 210 30,000 Similar 58*Notes: 1. Durations are from Design & Build Order to ship entering service 2. Weights are estimates based on best available information * Assumes that the ship will be in service three (3) months after delivery

professional skills, not in repair.

However, there is one fundamental question that needs to be urgently addressed. Do Canadians and the navy want a shipbuilding industry in Canada? If the answer is yes, then it is simply a matter of giving it a priority and getting on with it. If the answer is no or I don’t know/I’m not sure, then the demise of a high-technology industry will not be long in coming.

We are presented with a once-in-a-lifetime opportunity to build a small, viable, self-sustaining shipbuilding in-dustry in Canada. It won’t come again! Notes1. National Partnership Project, “Breaking Through” (Ottawa: Government

of Canada, 2001), p. 49.

2. Shipbuilding and Industrial Marine Advisory Committee (SIMAC), “Rec-ommendations to the Minister of Industry for a Shipbuilding Industry Transformative Strategy for a Duty Free Environment” (Ottawa, 2005).

3. ASC Pty Ltd, “Improving the Cost-effectiveness of Naval Shipbuilding in Australia” (2006).

4. Ibid., p. 23.

5. SIMAC, “Canada’s Shipbuilding Industry is Here to Stay” (2005), pp. 6-9.

6. Ibid., p. 28.

Vice-Admiral Peter Cairns (Ret’d) is currently President of the Shipbuilding Association of Canada.

There is also evidence to suggest that the delivery time for a JSS constructed in Canada would not be significantly different from that of other shipyards around the world building a roughly equivalent ship. Figure 6 is a com-parison of design and build schedules. Once again there does not seem to be a significant advantage to building in another country.

ConclusionAs happened with the St. Laurent, the Tribal and the CPFs, Canada’s shipbuilders are being questioned yet again, about their capability to meet the navy’s require-ments. They have always risen to the occasion in the past and they will do it again, but there has to be a better way.

The navy can no longer dock and repair its own ships – those days are gone. The navy needs industrial sup-port. Likewise, the shipbuilding industry needs the work that the navy provides but it cannot survive on navy and coast guard repair work alone. Canadian shipbuilders need a reasonably level playing field so they can capture their fair share of the domestic commercial market. Tal-ented young engineers, naval architects and technicians want to build ships. It is in building that they hone their

Source: Department of National Defence Chief of Review Services, Report on Canadian Patrol Frigate Cost and Capability Comparison.

Figure 6. A Comparison of Design and Build Schedules