shareholder services association webinar - … · · 2017-02-24shareholder services association...

TRANSCRIPT

Shareholder Services Association Webinar: Preparing for a New Year:

Reviewing Anti-Money Laundering Rules & Ethics Guidelines

Welcome and Introduction: Abby Cowart, Executive Director, SSA

Welcome, Introduction & Moderator: Abby CowartExecutive DirectorShareholder Services Association

Presenter: Tommasina (Tomi) Olson, MS, MBALicensed FINRA Series 7, 24, 28Compliance SpecialistLifeVest Financial, Inc.

DISCLAIMERThe information provided in this webinar represents the current understanding of the presenters and the Shareholder Services Association.

It is subject to change. In no way should this information be construed or relied upon as legal or operational advice. You should consult with your own legal counsel, compliance officer and/or other subject matter experts.

2

Defining “Money Laundering”

“Any act designed to conceal or disguise the true origins of criminally derived proceeds so that they appear to be

derived from legitimate sources.”

Basis for Regulation• Bank Secrecy Act of 1970 ( BSA)

• Section 31 U.S.Css5311 & Rule17a-8 of SEC Act 1934 (the Exchange Act)*Establishes framework for AML obligations*Authorizes Secretary of Treasury to issue regulations, investigate and prosecute financial crimes.*Amended after September 11, 2001 terror attacks

Money Laundering

• Intent: to conceal either origin or intended use

• Funds may come from: charitable donations, foreign government sponsors, business ownership and personal employment

• Large sums or complex transactions not required for terrorist financing

• Can occur world-wide and cross many countries’ borders

AML crimes include:

Corruption, bribery, embezzlement, kidnaping, smuggling, arms theft, security fraud, market manipulation, tax evasion, identity theft, racketeering, check fraud.

Requirements

• All Securities firms must comply• Responsible Designee at each Firm• Records must be kept for 5 years• Firm training program for ALL employees• SARS must be filed with FINCEN• Independent Testing of AML procedures• AML rules may change quickly

Firm Training Program

• ALL EMPLOYEES must know:• How to identify suspicious transactions• What to do once risk identified: (how, when, to whom

escalate unusual customer activity)• What role each employee plays in compliance• The Firm’s record retention policy• Disciplinary consequences(civil and criminal) for non-

compliance with Bank Secrecy Act

4 Stages of Money Laundering1. Placement: illicit cash comes into the legal financial system. The objective is to avoid an audit trail. Cash is converted into cashier’s checks, money orders, bank drafts, traveler’s checks, and wire transfers.

2. Structuring: breaking up large cash transactions into multiple smaller transactions to evade reporting or recordkeeping requirements.

4 Stages of Money Laundering3. Layering: cash equivalents obtained in the placement stage purchase financial instruments, such as premiums and deposits that provide liquidity and, distribute or disburse funds in a way that appears fully legitimate. Examples: cash value life insurance and deferred annuity contracts. Often a change of ownership occurs by transferring to a third party such as a charitable organization.

4. Integration: the cleansed money is circulated back into original hands.

Recent Fines for Non-Compliance• FINRA Fines Raymond James $17 Million for Systemic Anti-Money Laundering

Compliance Failures May 18, 2016• FINRA Fines Credit Suisse Securities (USA) LLC $16.5 Million for Significant

Deficiencies in its Anti-Money Laundering Program December 5, 2016• FINRA Fines Brown Brothers Harriman A Record $8 Million for Substantial Anti-

Money Laundering Compliance Failures February 5, 2014• FINRA Fines Banorte-Ixe Securities $475,000 for Inadequate Anti-Money

Laundering Program and for Failing to Register Foreign Finders January 28, 2014• FINRA Fines Three Firms $900,000 for Inadequate Anti-Money Laundering

Programs May 8, 2013

Customer Information Procedures(CIP)

• Each Firm must have procedures for obtaining specific customer information when an account is opened for either an individual or Institution.

• DUTY TO VERIFY: procedures to assure “reasonable” reliance on info collected: consumer reporting agency, audited filings

• “Risk-based”: each Firm different• Foreign Entities/Individuals need government-issued documentation

Customer Information Procedures(CIP)

• Must collect: name, place of business, government issued ID, Articles of Organization, Trust /Partnership agreements, name of persons authorized to conduct business, their gov’t issued identification, jurisdiction in which located, nature of customer business, types of accounts opened, types of ID presented, if member of foreign political party.

Red Flags• Opening accounts BEWARE IF:• “concern” over government reporting• Reluctance to share info re business activities• False misleading source of funds• The “representative” has questionable background (news reports)• Lack of concern regarding commissions/transaction costs• Representative is acting on behalf of another• Opening of multiple accounts in different names for no apparent

reason• Representative is unable to describe the nature of the Firm• Existence of other accounts in “high risk” jurisdictions

Suspicious Activity Reports (SARS)

Note: “Willful blindness” on the part of a Firm brings severe penalties comparable to those of the Launderer.

• SARs used to Escalate a concern about an account• Evidence is not needed• Cannot tell Client or others of SAR. (BSA/criminal liability)

Foreign Institutional Clients(Foreign Corrupt Practices Act- FCPA)

Improper payments to foreign officials to gain unfair advantageValue may be free items and/or influence !• fully or partially state-owned• Includes: government administrators, departments or

agencies• Government controlled companies• International organizations (World Bank, United Nations)• Political parties including party officials, candidates for office

FINCEN(Financial Crimes & Enforcement Network)• Authorized by U.S. Patriot Act• Will issue a 314(a) • Requires IMMEDIATE search of records and 14 day response• FAQ on the website• FINCEN may Issue Special Measures against:

– Foreign Jurisdictions– Financial Institutions– International Transactions: concerned with Terrorist Money

Laundering

OFAC• Office of Foreign Asset Control• Located within U.S. Treasury • Administers and enforces economic and trade sanctions based on

US foreign policy and national security goals.• Targets: International drug smugglers; any group purveying

weapons of mass destruction• Legislative authority to impose controls on transactions; can freeze

foreign assets within US jurisdictions

OFAC• Requirements are additional to AML• OFAC Publishes lists: Countries and SDNs (Specially Designated

Nationals, & Blocked Persons)• Requires securities firms to block accounts and property of listed

countries and SDNs block /reject unlicensed trades/financial transactions from listed countries/SDNs

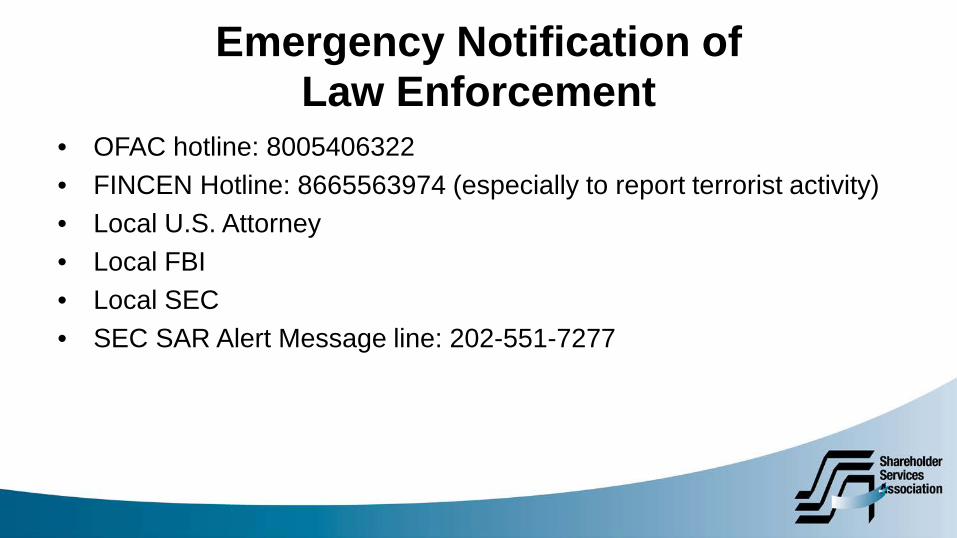

Emergency Notification of Law Enforcement

• OFAC hotline: 8005406322• FINCEN Hotline: 8665563974 (especially to report terrorist activity)• Local U.S. Attorney• Local FBI• Local SEC• SEC SAR Alert Message line: 202-551-7277

ETHICS

“A Member in the conduct of business shall observe high standards of commercial honor and justice and equitable

principles of trade.”

IOSCO

• International Organization of Securities Commissions

• SROCC (Self Regulatory Organization Consultative Committee)

• Model Code of Ethics

IOSCO

• IOSCO Model: Ethical Principles (6)– Promise keeping– Integrity and truthfulness– Maintaining confidentiality– Loyalty: managing Conflicts of Interest– Fairness to customer– Do no harm to the Customer or Profession

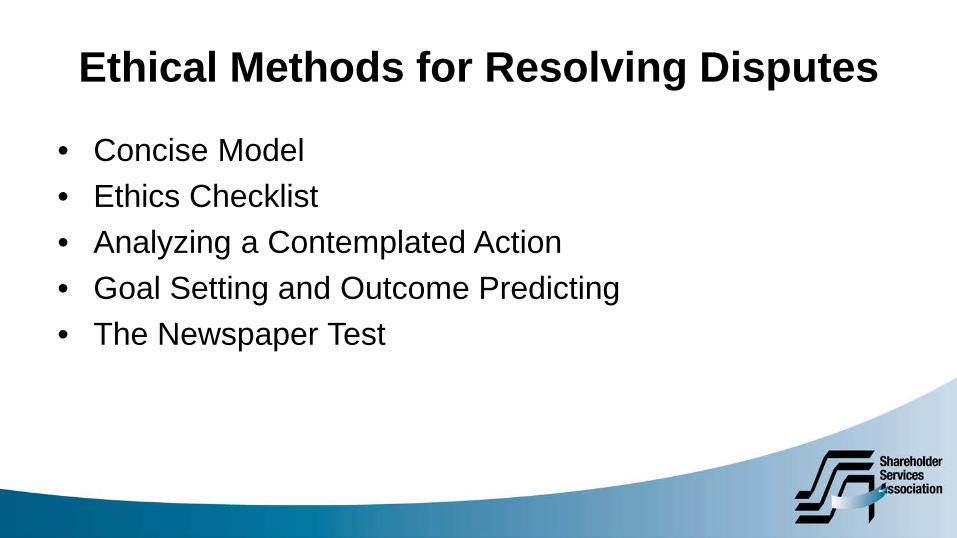

Ethical Methods for Resolving Disputes

• Concise Model• Ethics Checklist• Analyzing a Contemplated Action• Goal Setting and Outcome Predicting• The Newspaper Test

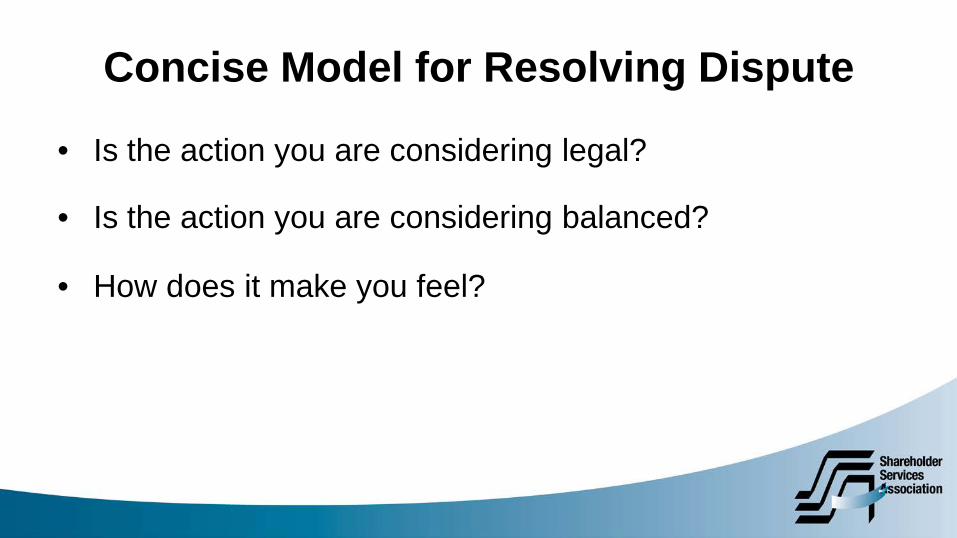

Concise Model for Resolving Dispute

• Is the action you are considering legal?

• Is the action you are considering balanced?

• How does it make you feel?

Ethics Checklist for Making Difficult Decisions

Consider the facts, the critical issues, the stakeholders, the alternatives, the ethical implications and whether there is more than one alternative.

Ethics Checklist for Making Difficult Decisions

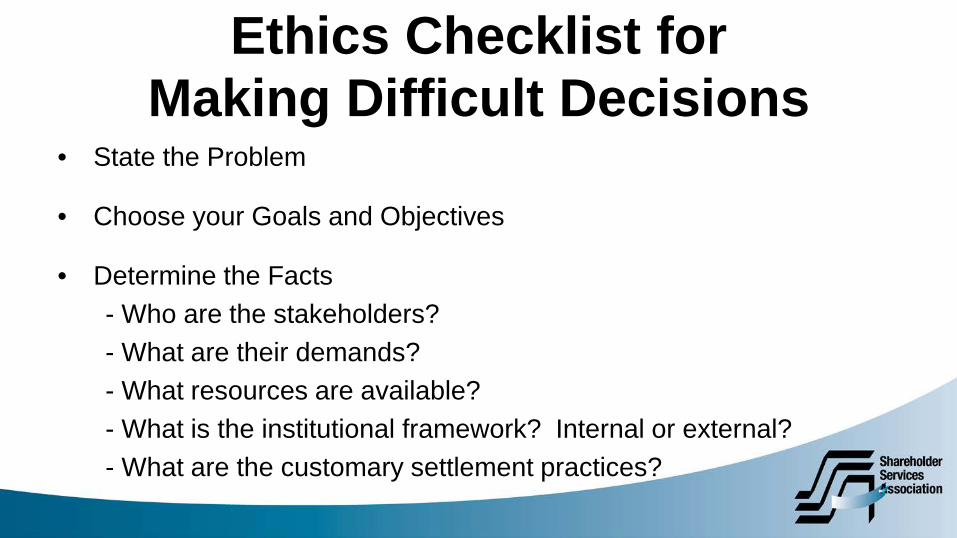

• State the Problem

• Choose your Goals and Objectives

• Determine the Facts- Who are the stakeholders?- What are their demands?- What resources are available?- What is the institutional framework? Internal or external?- What are the customary settlement practices?

Ethics Checklist for Making Difficult Decisions

• Identify obstacles: social trends ?

• Project Probable Outcomes

Ethics Checklist for Making Difficult Decisions

• Determine the Facts– Who are the stakeholders?– What are their demands?– What resources are available?– What is the institutional framework? Internal or external?– what are the customary settlement practices?– Identify obstacles: social trends ?

• Project Probable Outcomes

Analyzing a Contemplated Action

Evaluate the Various Perspectives of the decision

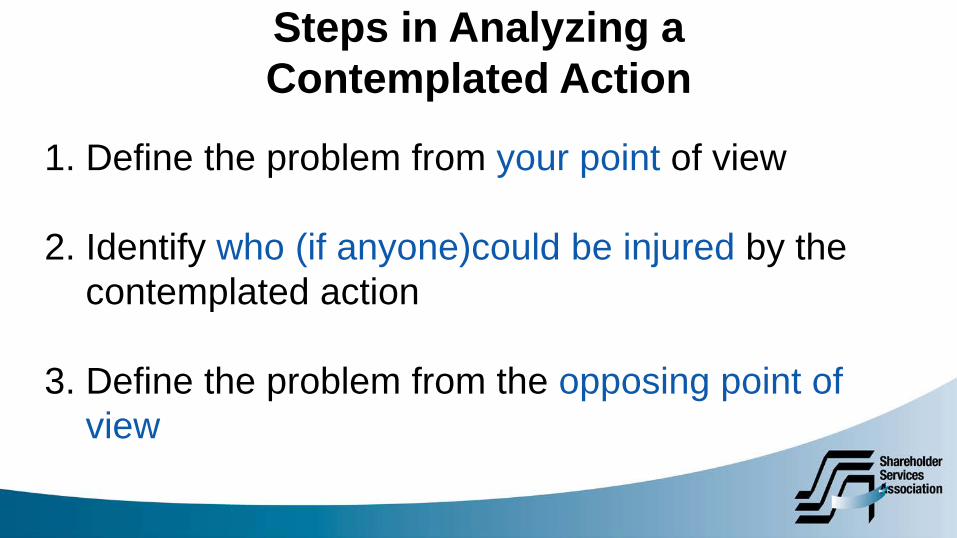

Steps in Analyzing a Contemplated Action

1. Define the problem from your point of view

2. Identify who (if anyone)could be injured by the contemplated action

3. Define the problem from the opposing point of view

Steps in Analyzing a Contemplated Action

4. Ask yourself whether you would be willing to tell others who rely on you about the planned action

5. Ask yourself if you would be willing to go public

6. After full consideration of facts and alternatives, decide what action to take.

Goal Setting & Outcome Predicting

Compare your Goals to the decision you are making and consider what might happen as a result of your action.

Newspaper Test

Consider whether you would like to see your decision described by a reporter on the front page of the local newspaper.

Conclusions

• Anti Money Laundering Programs need to be taken very seriously

• Always observe High Standards of Conduct.

Questions & Comments?

Thank you for participating!

36

Save The DatesMarch 16, 2017 12:00 pm.

SSA Luncheon & SeminarBlockchain TechnologyBattery Gardens Restaurant- New York City

April 20, 2017 1:00 pm. SSA Webinar: Medallions

2017 SSA Annual Conference

July 18-20, 2017

Bonita Springs, Florida