shamsun nahar msc (accounting and finance), uk m.b.a, b.b

TRANSCRIPT

Risk Disclosure Practices: Their Determinants and Association with Bank

Performance

Shamsun Nahar MSc (Accounting and Finance), UK

M.B.A, B.B.A (Accounting and Information system), Bangladesh

A Thesis Submitted in Fulfilment of the Requirements for the Degree of

Doctor of Philosophy

Faculty of Business and Enterprise

Swinburne University of Technology

2015

Abstract

In recent times, corporate risk disclosure has been an issue of major concern to the

global community and has gained considerable attention from stakeholders, policy

makers and regulators. This research explores risk disclosures practices, their

determinants and association with bank performance in the context of a developing

country, Bangladesh. Most existing studies on risk disclosure provide empirical

evidence from developed countries. However, the difference in institutional and socio-

economic settings between developed and developing countries might affect the extent

of corporate risk disclosure differentially. Specifically, Bangladesh makes an ideal site

in which to examine risk disclosures and their determinants within an agency and neo

institutional isomorphism conceptual framework because risk disclosures are effectively

voluntary.

This research is comprised of three interrelated Phases. Employing content analysis, the

first Phase investigates corporate risk disclosure practices by sample banks from 2006

to 2012. A comprehensive Risk Disclosure Index (RDI) is developed based on

international standards and is used as a benchmark against which to score actual risk

disclosures. The second Phase investigates determinants for such disclosures. Informed

by thematic analysis of semi-structured interviews with senior banking executives and

regulators, this Phase investigates the Risk Disclosure Index score and its association

with banks’ corporate governance and financial characteristics. The third and final

Phase uses multiple regression analysis to investigate the association between the extent

of risk disclosure and performance. Bank performance is measured using two broad

aspects: bank operating performance and bank valuation.

Overall, the Risk Disclosure Index developed in this study is of relevance to financial

institutions seeking to provide information for stakeholders and, indeed, to all relevant

parties seeking to assess or evaluate information in relation to risk disclosure. The

analysis suggests that listed banks in Bangladesh made significant improvement in risk

disclosure over time, predominantly on a voluntary basis, and this improvement is

associated with several key bank characteristics, consistent with agency and neo

ii

institutional isomorphism tenets. In addition, analysis of interview findings suggest that

institutional weakness, political interference and inadequate monitoring by the Central

Bank hinders risk disclosure practices. The findings provide evidence also that lagged

risk disclosure is positively associated with banks’ return on assets, solvency and

employee efficiency. This research should assist also accounting regulators and

legislators in developing reporting requirements that satisfy stakeholders’ demands in

relation to risk disclosure. Research implications from the findings are discussed,

together with limitations and recommendations for future research.

iii

Acknowledgement

First, I am grateful to almighty Allah for granting me strength and courage to the long,

arduous journey towards the completion of the PhD thesis.

Writing this thesis is not like making a journey alone. I would like to express my

gratitude and acknowledgement to many people for their guidance and support along

my PhD journey.

My deepest gratefulness for support and encouragement throughout my doctoral study

goes to my supervisor, Dr. Mohammad Azim. He had always been kind to me,

providing me advice and guidance throughout my entire journey. I owe him a big

gratitude.

This project could not be completed without the input and guidance provided by

Professor Christine Jubb. Her extremely valuable feedback and timely suggestions are

much appreciated. It has been my privilege to have her as my supervisor. Thank you.

I am also thankful to Dr Ron Kluvers, for all his beneficial advice and guidance. I am

sincerely pleased to the interview participants, who shared their time, knowledge and

wisdom with me and everyone who has taken part in this study. I appreciate my

distinguished colleagues in the PhD research lab at Swinburne University for their

support and friendship.

My efforts and dreams would not be materialised if Swinburne University of

Technology would not have provided me prestigious Swinburne University

Postgraduate Research Award (SUPRA) for doing PhD.

I would like to acknowledge my family- my husband, brothers, sisters, brother- in-law

and my dearest parents for having faith in my capabilities, giving me unconditional

iv

support and continuous encouragement. Very special thanks to my three-year-old ‘little

superman’ son, Rayyan, my biggest source of inspiration throughout this long journey.

Thank you.

Lastly, I wish to convey my gratitude to all my friends who always provided valuable

support, interest, and help in every possible way throughout the process of this study.

v

Declaration

This thesis contains no material that has been accepted for the award of any other

degree or diploma in any other institution. To the best of my knowledge, the work of no

other person has been used without due acknowledgement, and the thesis is not written

in collaboration with any other person.

Shamsun Nahar

June, 2015

vi

vii

Table of contents

Abstract…………. ............................................................................................................ i

Acknowledgment ............................................................................................................ iii

Declaration ....................................................................................................................... v

Table of Contents .......................................................................................................... vii

List of Tables ................................................................................................................. xv

List of Figures .............................................................................................................. xvii

List of Appendices ........................................................................................................ xix

PART ONE 1 PRELIMINARIES 1

Chapter 1: Introduction 1

1.1 Introduction ................................................................................................................. 3

1.2 Research background and motivation ......................................................................... 4

1.3 Research justification and objectives .......................................................................... 7

1.4 Key terms .................................................................................................................... 9

1.5 Research approach .................................................................................................... 10

1.6 Research contribution…………………………………………………………… 12

1.7 Thesis outline……………………………………………………………………… 12

Chapter 2: Risk Reporting as an Issue of Concern 14

2.1 Introduction ............................................................................................................... 15

2.2 Background to risk reporting .................................................................................... 15

2.2.1 Changes in business environment and emergence of risk reporting ................. 16

2.2.2 Risk reporting as an issue of concern in banking institutions .......................... 18

2.3 Risk disclosure related policies, pressures and corporate responses......................... 19

2.4 Institutional arrangements and accounting regulations ............................................. 21

2.4.1 Cadbury Report ................................................................................................ 21

2.4.2 The American Institute of Certified Public Accountants .................................. 22

2.4.3 The Institute of Chartered Accountants in England and Wales ........................ 22

2.4.4 Hampel Report ................................................................................................. 24

2.4.5 Higgs Report and Smith Report ....................................................................... 24

2.4.6 International Financial Reporting Standards .................................................... 24

2.4.7 BASEL II: Pillar 3 (Market Discipline) ............................................................ 26

2.5 Risk disclosure as a major concern in Bangladesh ................................................... 28

viii

2.6 Chapter conclusion .................................................................................................... 31

Chapter 3: Bangladesh- the Context of the Study 33

3.1 Introduction ............................................................................................................... 33

3.2 Bangladesh as the country of study ........................................................................... 33

3.2.1 Bangladesh: Country profile ............................................................................. 34

3.2.2 Political and historical context .......................................................................... 34

3.2.3 Economic context .............................................................................................. 35

3.2.4 Socio-cultural context ........................................................................................ 38

3.2.5 Legal and institutional context .......................................................................... 39

3.3 The financial system in Bangladesh .......................................................................... 43

3.4 Banking industry in Bangladesh ............................................................................... 44

3.4.1 Evolution of banking industry ........................................................................... 45

3.4.2 Structure of the banking sector in Bangladesh .................................................. 45

3.5 Financial reforms in banking sector .......................................................................... 47

3.5.1 Risk measure policy reforms in banks .............................................................. 49

3.5.2 Institutional reform of risk measures ................................................................. 51

3.5.3 Legal reform ...................................................................................................... 53

3.6 Motivation for choosing Bangladesh as the context for this study ........................... 53

3.7 Motivation for selecting listed banks in Bangladesh ................................................ 55

3.8 Chapter conclusion .................................................................................................... 57

PART TWO 59

LITERATURE REVIEW AND THEORETICAL UNDERPINNING 59

Chapter 4: Literature Review 61

4.1 Introduction ............................................................................................................... 61

4.2 Risk and risk disclosure ............................................................................................ 62

4.2.1 The concept of risk ............................................................................................ 62

4.2.2 Classification of risk .......................................................................................... 63

4.3 The concept of disclosure in accounting and economics research ............................ 65

4.4 Risk disclosure: Review of previous studies ............................................................. 66

4.4.1 Empirical studies of risk reporting by banking institutions .............................. 69

4.4.2 Empirical studies of risk reporting in other than banking institutions .............. 71

4.5 Gaps in the literature ................................................................................................. 86

4.6 Chapter conclusion .................................................................................................... 87

ix

Chapter 5: Conceptual Framework and Hypotheses 89

5.1 Introduction ............................................................................................................... 89

5.2 Theories discussed in previous disclosure studies .................................................... 90

5.3 Agency theory ........................................................................................................... 90

5.3.1 The agency problem .......................................................................................... 91

5.3.2 Agency theory and the organisational perspective ............................................ 93

5.3.3 Relevance of agency theory in this study: Development of Hypotheses .......... 95

5.4 Institutional theory .................................................................................................... 97

5.4.1Defining institution ............................................................................................. 98

5.4.2 New institutionalism ........................................................................................ 101

5.4.3 Significance of institutional isomorphism ....................................................... 102

5.4.4 Isomorphism processes .................................................................................... 103

5.4.4.1 Coercive isomorphism ............................................................................. 103 5.4.4.2 Mimetic isomorphism .............................................................................. 105 5.4.4.3 Normative isomorphism .......................................................................... 107

5.5 The relation between risk disclosure and bank performance .................................. 108

5.5.1 Employee efficiency ........................................................................................ 109

5.5.2 Solvency efficiency ......................................................................................... 109

5.5.3 Deposit concentration ...................................................................................... 111

5.5.4 Financial performance ..................................................................................... 111

5.5.5 Risk disclosure and bank valuation ................................................................. 112

5.6 Conceptual framework ............................................................................................ 112

5.7 Chapter conclusion .................................................................................................. 113

PART THREE 116

METHODOLOGY ............................................. 116

Chapter 6: Research Methodology 118

6.1 Introduction ............................................................................................................. 118

6.2 Philosophical assumption ........................................................................................ 119

6.2.1 Ontological assumption ................................................................................... 120

6.2.2 Epistemological assumption ............................................................................ 121

6.3 Research type .......................................................................................................... 122

6.4 Theoretical perspective ........................................................................................... 122

6.5 Methodology ........................................................................................................... 123

6.5.1 Quantitative research approach ....................................................................... 123

6.5.2 Qualitative research approach ......................................................................... 124

x

6.5.3 Mixed method approach .................................................................................. 124

6.5.4 Paradigm adopted in this study ....................................................................... 125

6.5.5 Designing triangulation in mixed method research ......................................... 125

6.5.6 The convergence model of triangulation ......................................................... 127

6.6 The quantitative method .......................................................................................... 129

6.6.1 Research instrument ........................................................................................ 129

6.6.1.1 Content analysis approach ....................................................................... 129 6.6.1.2 Risk Disclosure Index .............................................................................. 131

6.6.2 Reliability of Risk Disclosure Index score ...................................................... 153

6.6.3 Sample design .................................................................................................. 154

6.6.4 Data collection ................................................................................................. 154

6.6.5 The dependent variable ................................................................................... 154

6.6.6 Independent and control variables ................................................................... 155

6.6.7 Statistical data analysis techniques .................................................................. 155

6.6.7.1 Descriptive statistics ................................................................................ 156 6.6.7.2 Univariate statistics .................................................................................. 156 6.6.7.3 Bivariate analysis .................................................................................... 157 6.6.7.4 Multiple regression model ....................................................................... 157

6.6.8 Sensitivity and supplemental analysis ............................................................. 166

6.7 The qualitative method ............................................................................................ 167

6.7.1 Justification of sampling procedure ................................................................ 168

6.7.2 Designing interview protocol .......................................................................... 169

6.7.3 Designing the interview protocol .................................................................... 169

6.7.4 Data collection technique ................................................................................ 170

6.7.5 Data analysis .................................................................................................... 171

6.7.6 Reliability and validity .................................................................................... 172

6.8. Ethical clearance .................................................................................................... 173

6.9 Chapter conclusion .................................................................................................. 173

PART FOUR 174 ANALYSIS .......................................................... 174

Phase One

Chapter 7: Content Analysis of Annual Reports………………………….. 170

7.1 Introduction ............................................................................................................. 176

7.2 Trends in total corporate risk disclosure ................................................................. 177

7.2.1 Risk disclosure by key categories ................................................................... 193

7.2.2 Risk disclosure by Risk Types ........................................................................ 194

xi

7.2.3 Qualitative and quantitative disclosure ........................................................... 195

7.3 Descriptive statistics for the Risk Disclosure Index ............................................... 196

7.4 Comparison of Risk Disclosure Index over the period: Univariate analysis ......... 199

7.4.1 Significance of Risk Disclosure Index over the period: ANOVA .................. 199

7.4.2 Conventional and non-conventional banks .................................................... 200

7.4.3 Comparisons of pre- and post GFC periods .................................................... 201

7.5 Discussion of results ............................................................................................... 203

7.6 Chapter conclusion .................................................................................................. 204

Phase Two

Chapter 8: Qualitative Analysis of Interview Data 206

8.1 Introduction ............................................................................................................. 206

8.2 Risk disclosure practices and rationale for disclosure ............................................ 208

8.3 Determinants of risk disclosure ............................................................................... 210

8.3.1 Institutional isomorphism ................................................................................ 211

8.3.2 Risk governance factors .................................................................................. 214

8.4 Additional findings from interviewees.................................................................... 216

8.4.1 Institutional weakness ..................................................................................... 216

8.4.2 Political interference ........................................................................................ 218

8.4.3 Lack of central bank autonomy ....................................................................... 220

8.4.4 Lack of accountability ..................................................................................... 221

8.4.5 Lack of demand from governments ................................................................. 221

8.4.6 Lack of education ............................................................................................ 222

8.4.7 Brief and concise report .................................................................................. 223

8.5 Chapter conclusion .................................................................................................. 223

Chapter 9: Descriptive, Univariate and Bivariate Analyses 226

9.1 Introduction ............................................................................................................. 226

9.2 Sample and source of data ...................................................................................... 227

9.3 Descriptive statistics................................................................................................ 227

9.4 Univariate statistics: ANOVA and Chi-Square tests .............................................. 238

9.4.1 Significance of mean over time: ANOVA ...................................................... 238

9.4.2 Continuous variable: T tests ............................................................................ 238

9.4.3 Categorical variables: Chi-Square tests ........................................................... 239

xii

9.5 Bivariate analysis .................................................................................................... 240

9.6 Chapter conclusion .................................................................................................. 244

Chapter 10: Factors Underlying Risk Disclosure: Multivariate Statistics 246

10.1 Introduction ........................................................................................................... 246

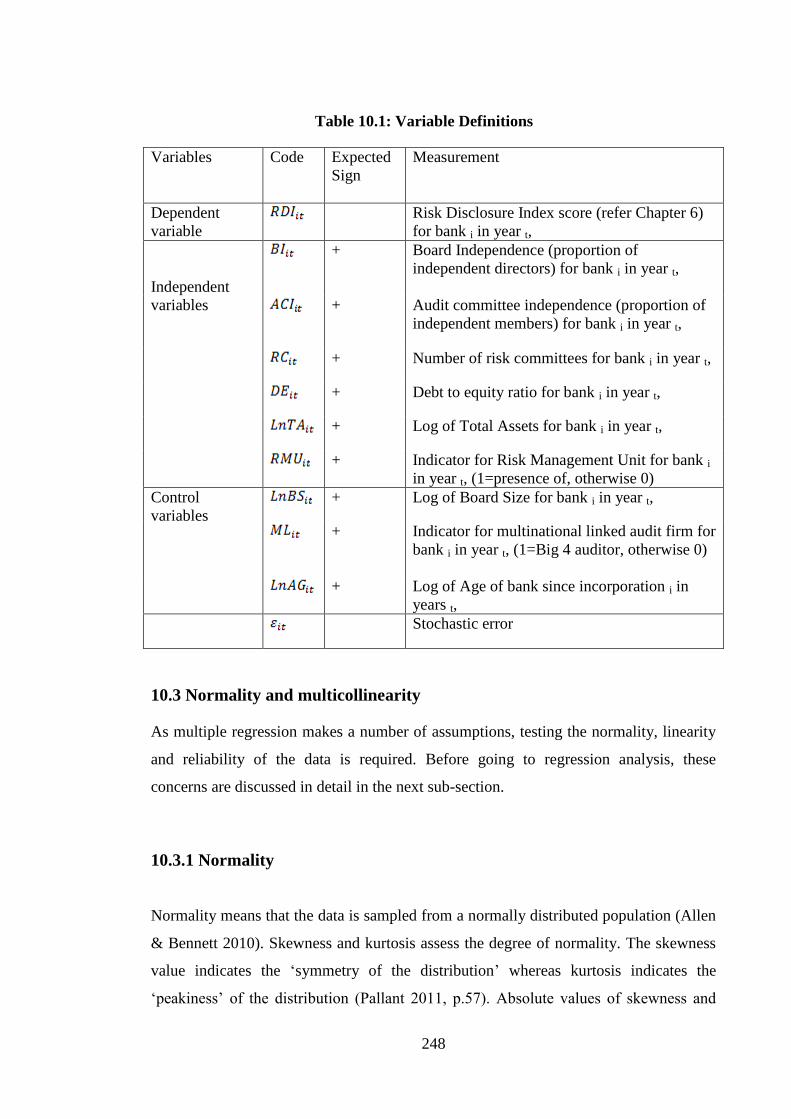

10.2 Multivariate regression model .............................................................................. 247

10.3 Normality and multicollinearity ............................................................................ 248

10.3.1 Normality ....................................................................................................... 248

10.3.2 Multicollinearity ............................................................................................ 251

10.4 Multiple regression results: Hypothesis testing .................................................... 253

10.4.1 Agency theory and Risk Disclosure Index ................................................... 255

10.4.2 Institutional isomorphism and Risk Disclosure Index .................................. 256

10.4.3 Control variables ........................................................................................... 257

10.5 Sensitivity analysis ................................................................................................ 257

10.6 Robustness check .................................................................................................. 261

10.6.1 Association of Risk Disclosure Index with profitability ............................... 261

10.6.2 Five types of Risk Disclosure ........................................................................ 263

10.7 Change in Risk Disclosure Index across the sample periods ................................ 268

10.8 Discussion of results ............................................................................................. 276

10.9 Chapter conclusion ................................................................................................ 278

Phase Three

Chapter 11: Risk Disclosure and Bank Performance 279

11.1 Introduction ........................................................................................................... 279

11.2 Descriptives, t-tests and correlations..................................................................... 283

11.3 Regression analysis ............................................................................................... 287

11.4 Supplemental analysis ........................................................................................... 291

11.4.1 Bank performance in risk disclosure groups ................................................. 291

11.4.2 Bank performance and risk disclosure in Non-Islamic and Islamic banks ... 297

11.4.3 Bank performance and Risk Types ............................................................... 300

11.5 Discussion of results ............................................................................................. 312

11.6 Chapter conclusion ................................................................................................ 313

xiii

PART FIVE 314 CONCLUSION ......................................................... 314

Chapter 12: Conclusion 316

12.1 Introduction ........................................................................................................... 316

12.2 Overview ............................................................................................................... 317

12.3 Research findings and implications ...................................................................... 322

12.4 Research contribution............................................................................................ 325

12.5 Research limitations .............................................................................................. 328

12.6 Suggestions for future research ............................................................................. 329

References .......................................................................................................... 333

Appendices ......................................................................................................... 351

xiv

xv

List of Tables

Table 1.1: Key terms ......................................................................................................... 9

Table 3.1: Economy of Bangladesh ................................................................................ 37

Table 3.2: Structure of the banking system in Bangladesh ............................................. 46

Table 3.3: Bank branches in urban and rural areas (up to June 2013) ............................ 47

Table 4.1: Classification of risk in extant literature ........................................................ 64

Table 4.2: Empirical studies of corporate risk disclosure ............................................... 77

Table 5.1: Components of institutional analysis ........................................................... 100

Table 5.2: The new and old institutionalism ................................................................. 101

Table 6.1: Paradigmatic concerns and research approaches ......................................... 125

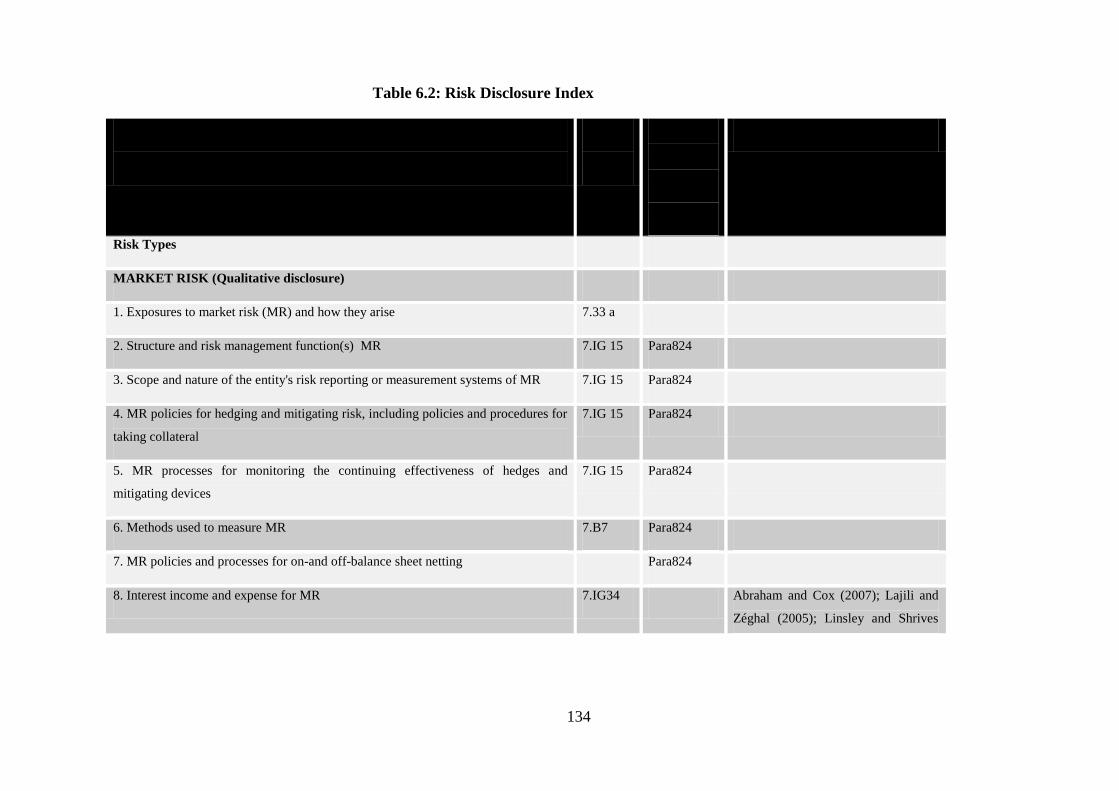

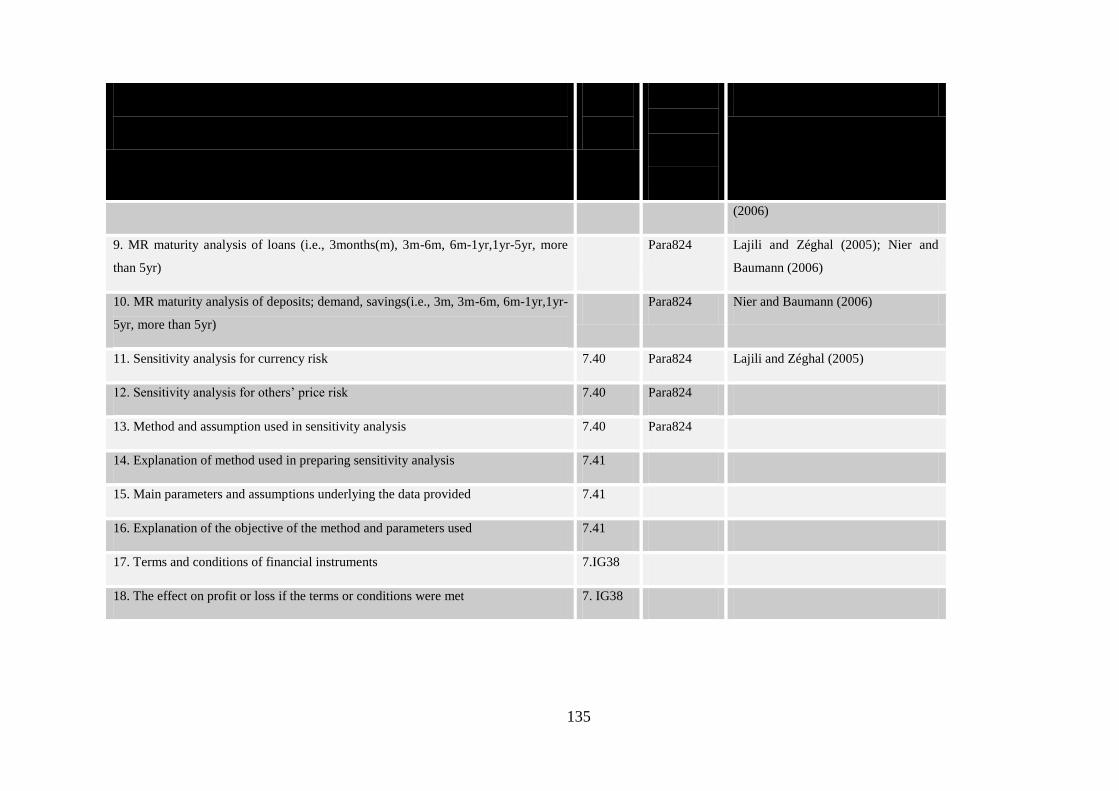

Table 6.2: Risk Disclosure Index .................................................................................. 134

Table 6.3: Reliability tests of Risk Disclosure Index comparability ............................ 153

Table 6.4: Variable definitions (Model 1)..................................................................... 161

Table 6.5: Variable definitions (Models 2-7) ................................................................ 165

Table 6.6: Variable definition ....................................................................................... 167

Table 7.1: Average Risk Disclosure Index (RDI) score .............................................. 178

Table 7.2: Mean Risk Disclosure Index score (per cent of max. possible [147]) ......... 179

Table 7.3: Mean Risk Disclosure Index (RDI) score (%) by category ......................... 193

Table 7.4: Mean Risk Disclosure Index (RDI) score (%) by Risk Type .................... 194

Table 7.5: Mean Qualitative and Quantitative Risk Disclosure Index (RDI) score ...... 196

Table 7.6: Descriptive statistics for seven key categories of Risk Disclosure Index .... 197

Table 7.7: Descriptive statistics for seven categories individually and aggregately ..... 198

Table 7.8: Risk Disclosure Index (%) by year ANOVA ............................................... 199

Table 7.9: Mean difference between conventional and non-conventional ................... 200

Table 7.10: Wilcoxon Signed Rank tests ...................................................................... 201

Table 7.11: Paired sample t tests of mean RDI (%) across discrete periods ................. 202

Table 7.12: Paired sample t-tests .................................................................................. 203

Table 9.1: Descriptive statistics by complete sample ................................................... 229

Table 9.2(Panel A): Descriptive statistics year 2006 .................................................... 231

Table 9.2(Panel B): Descriptive statistics year 2007 .................................................... 232

Table 9.2(Panel C): Descriptive statistics year 2008 .................................................... 233

Table 9.2(Panel D): Descriptive statistics year 2009 .................................................... 234

Table 9.2(Panel E): Descriptive statistics year 2010 .................................................... 235

Table 9.2(Panel F): Descriptive statistics year 2011 ..................................................... 236

xvi

Table 9.2:(Panel G): Descriptive statistics year 2012 ................................................... 237

Table 9.3: ANOVA by year .......................................................................................... 238

Table 9.4: t tests for continuous variables ................................................................... 238

Table 9.5: Pearson Chi-Square test for categorical variables ....................................... 240

Table 9.6: Pearson’s Correlations Pooled Data............................................................. 242

Table 10.1: Variable Definitions ................................................................................... 248

Table 10.2: Normality analysis for pooled data ............................................................ 250

Table 10.3: Collinearity statistics for pooled data ........................................................ 252

Table 10.4: Pooled OLS robust regression results for Risk Disclosure Index .............. 254

Table 10.5: Pooled OLS regression results for the Risk Disclosure Index ................... 259

Table 10.6: Pooled OLS regression results for Risk Disclosure Index ......................... 260

Table 10.7: Pooled OLS regression results for Risk Disclosure Index ......................... 262

Table 10.8: Pooled OLS regression results for five types of risks ................................ 265

Table 10.9: Variable definitions .................................................................................... 269

Table 10.10:Change in Risk Disclosure Index in pre and post GFC periods ............... 272

Table 10.11: Summary of significant variables from Table 10.10 ............................... 274

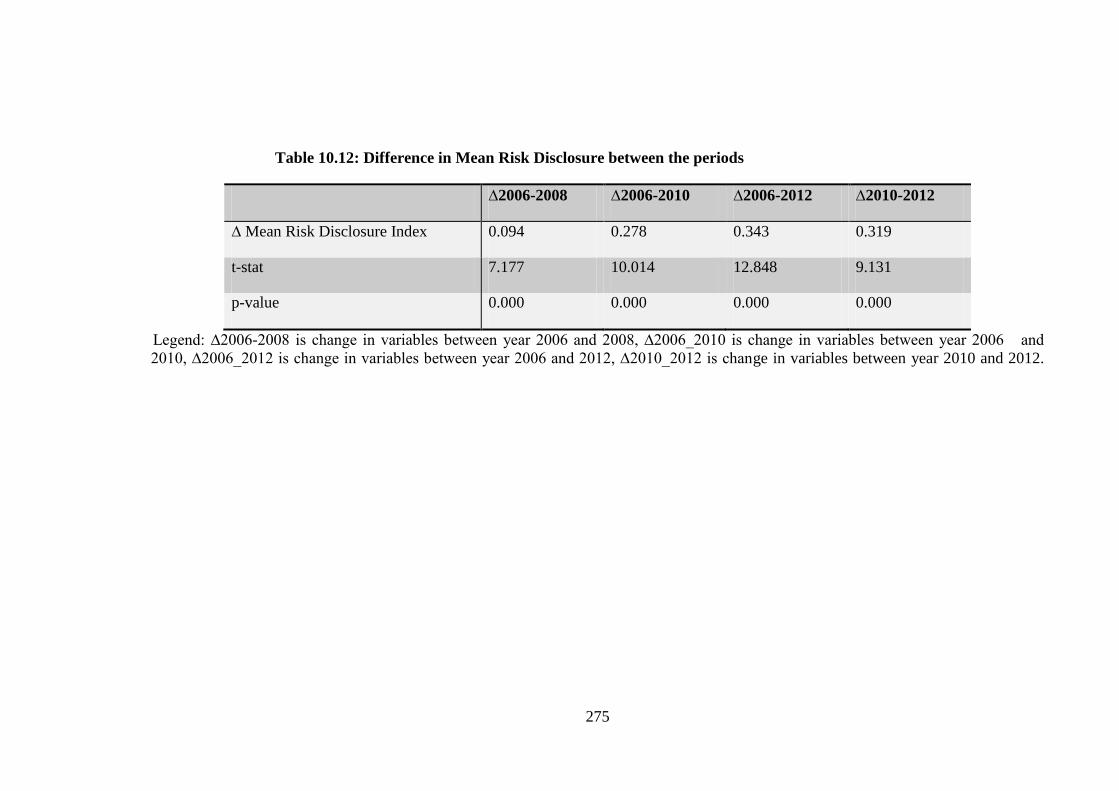

Table 10.12: Difference in Mean Risk Disclosure between the periods ....................... 275

Table 11.1: Variable definitions .................................................................................... 282

Table 11.2: Descriptive and t- statistics by complete sample ....................................... 284

Table 11.3: Pearson’s Correlations Pooled Data........................................................... 286

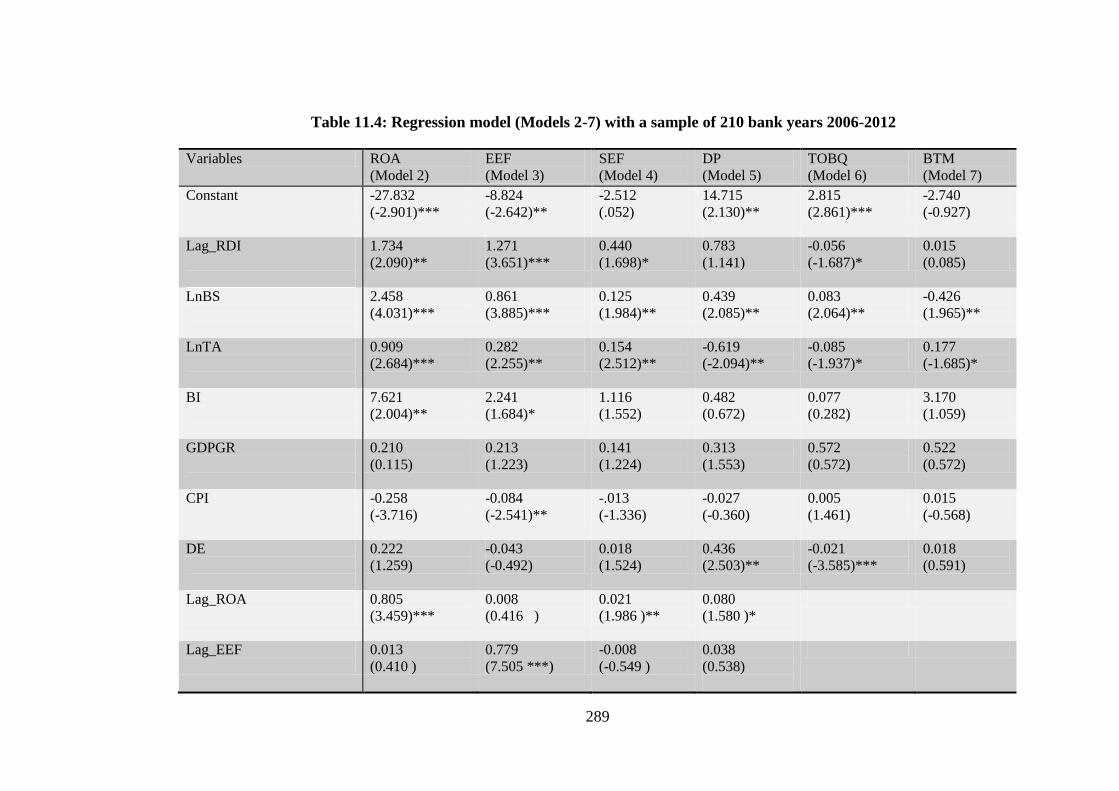

Table 11.4: Regression model (Models 2-7) ................................................................. 289

Table 11.5: Descriptive Statistics and t-tests for variables ........................................... 293

Table 11.6: Regression results for High and Low Risk Disclosure groups .................. 295

Table 11.7: Regression results for High and Low Risk Disclosure groups .................. 298

Table 11.8: Regression results -Lag_Market Risk Disclosure Index ............................ 302

Table 11.9: Regression results -Lag Credit Risk Disclosure Index .............................. 304

Table 11.10: Regression results -Lag Solvency Risk Disclosure Index ....................... 306

Table 11.11: Regression results -Lag Operational Risk Disclosure Index ................... 308

Table 11.12: Regression results -Lag Equities Risk Disclosure Index ......................... 310

Table 12.1: This thesis’ research at a glance................................................................. 318

xvii

List of Figures

Figure 1.1: Roadmap of Chapter ....................................................................................... 3

Figure 1.2: Depiction of the framework for this research ................................................. 9

Figure 1.3: Research purpose and the three Phases ........................................................ 11

Figure 1.4: Structure of the thesis ................................................................................... 13

Figure 2.1: Roadmap of Chapter ..................................................................................... 15

Figure 2.2: Factors affecting financial reporting............................................................. 17

Figure 3.1: Roadmap of Chapter ..................................................................................... 33

Figure 3.2: The national flag and map of Bangladesh .................................................... 35

Figure 3.3: Structure of the financial system in Bangladesh .......................................... 44

Figure 3.4: Bangladesh real GDP growth ....................................................................... 55

Figure 3.5: Deposits in years 2008-2012 ........................................................................ 56

Figure 3.6: Deposits in the banking sector, 2012 ............................................................ 56

Figure 3.7: Percentage share of assets (2007-2012)........................................................ 57

Figure 4.1: Roadmap of Chapter ..................................................................................... 61

Figure 5.1: Roadmap of Chapter ..................................................................................... 90

Figure 5.2: Agency theoretical perspective ..................................................................... 93

Figure 5.3: Conceptual framework for this study ......................................................... 113

Figure 6.1: Roadmap of Chapter ................................................................................... 118

Figure 6.2: Continuum of ontological assumptions ...................................................... 120

Figure 6.3: The convergence model used in this study ................................................. 127

Figure 6.4: Summary of the research design ................................................................. 128

Figure 6.5: Narratives in annual reports ........................................................................ 130

Figure 6.6: Qualitative data analysis technique ............................................................ 172

Figure 7.1: Roadmap of Chapter 7 ................................................................................ 177

Figure 8.1: Roadmap of Chapter 8 ................................................................................ 207

Figure 9.1: Roadmap of Chapter 9 ................................................................................ 227

Figure 10.1: Roadmap of Chapter 10 ............................................................................ 247

Figure 11.1: Roadmap of Chapter 11………………………………………………… 282

xviii

xix

List of Appendices

Appendix 6.1: Research paradigmatic dichotomies………………………………. 349

Appendix 6.2: Research types……………………………………………………… 350

Appendix 6.3: Summarises the prototypical characteristics of mixed method…… 351

Appendix 6.4: Interview Protocol ………………………………………………… 352

Appendix 6.5: Consent form………………………………………………………… 354

Appendix 6.6: Ethics Approval Letter………………………………………………. 356

Appendix 7.1: Tukey HSD………………………………………………………… 359

Appendix 7.2: Eta squared statistic ……………………………………………….. 360

Appendix 9.1: Presents the post hoc Tukey p values in each year………………… 361

Appendix 9.2: Eta squared statistic………………………………………………….. 364

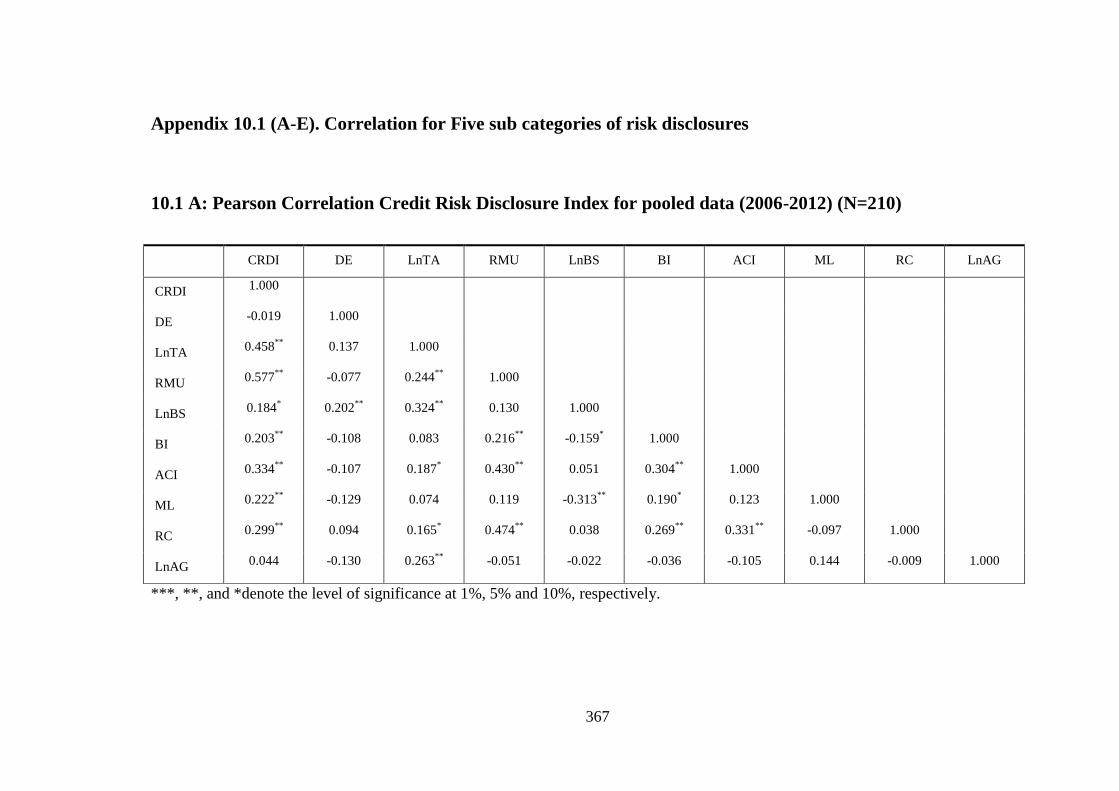

Appendix 10.1: Correlations A-E……………………………………………………. 365

Appendix 10.2: Correlations change Risk Disclosure Index 2006 and 2008………... 370

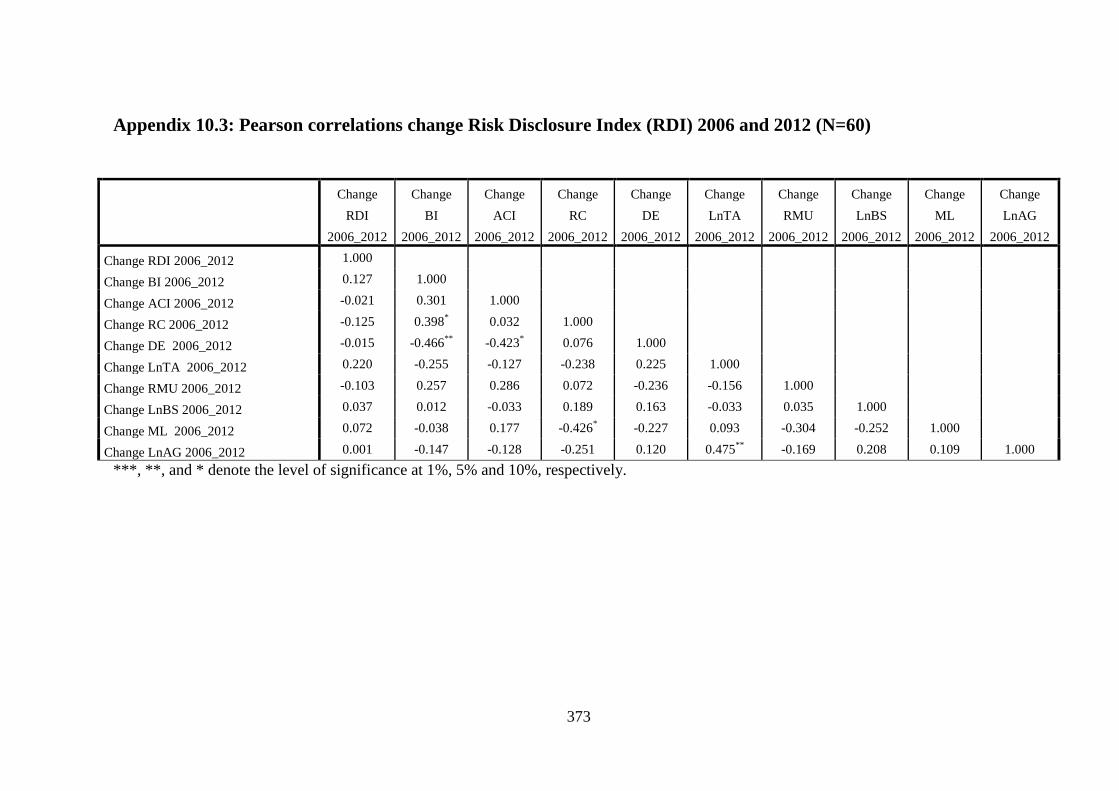

Appendix 10.3: Correlations change Risk Disclosure Index 2006 and 2012 …….. 371

Appendix 10.4: Correlations change Risk Disclosure Index 2006 and 2010……... 372

Appendix 10.5: Correlations change Risk Disclosure Index 2010 and 2012……... 373

1

PART ONE

PRELIMINARIES

Part one of this thesis introduces the research background and provides the structure of

the thesis. Chapter 1 presents an overview of the study. It starts with a brief discussion

of the background to the research, objectives of the study, research approach and

outlines the structure of the thesis. Chapter 2 provides discussion of the issue of risk

reporting in detail and Chapter 3 provides an overview of Bangladesh as a country and

why it is chosen as the location for this study.

Chapter 1: Introduction

Chapter 2: Risk reporting as an issue of concern

Chapter 3: Bangladesh – the context of the study

2

3

CHAPTER 1: Introduction

1.1 Introduction

This study extends our knowledge by undertaking an empirical investigation into

financial institutions’ corporate risk disclosure practices in an effectively voluntary

environment, the determinants of those practices and their association with financial

performance. This is an underexplored area in receipt of little attention in the financial

reporting literature.

Briefly, the study consists of three interrelated Phases under a common theme of ‘risk

disclosure practices: their determinants and their association with bank performance’.

The first Phase of the study investigates the corporate risk disclosure practices of all

listed banks in Bangladesh over a seven-year period (2006-2012). The second Phase

investigates the determinants of these corporate risk disclosure practices. The third and

final Phase of the study investigates the association of corporate risk disclosure with

bank performance. Taken together, the three Phases enhance and advance corporate risk

reporting research using various methodological lenses and perspectives. The purpose

of this Chapter is to provide an overview of the study. Figure 1.1 provides a roadmap of

this Chapter.

1Figure 1.1: Roadmap of Chapter

Introduction (1.1) Research

background and

motivation (1.2)

Introduction (1.1)

Glossary of key

terms (1.4)

Research

justification and

objectives (1.3)

Thesis outline

(1.6)

Research approach

(1.5)

4

1.2 Research background and motivation

Corporate risk disclosure has been, and continues to be, a major issue of concern to the

global community and has gained considerable attention from stakeholders (e.g. Aebi,

Sabato & Schmid 2012; Beltratti & Stulz 2012; Erkens, Hung & Matos 2012). From a

business perspective, risk disclosure assists corporations to manage changes and instruct

the path for the future (Abraham & Cox 2007). From a stakeholders’ perspective, ‘risk

profile, risk appetite, and risk management are key elements in making sound

investment decisions’ (Lajili 2009, p.94) and reducing information asymmetry (Botosan

1997; Chang 1998).

Corporate risk disclosure provides information about the company’s material risks that

help stakeholders understand and evaluate the interrelated risks, the effect of risks and

the company’s risk management strategies (Caldwell 2012). Additionally, corporate risk

disclosure lowers the cost of capital as investors achieve greater confidence in the

business operations when uncertainty is reduced (Abraham & Cox 2007; Linsley &

Shrives 2000). Compared with ill-informed investors, the confident and well-informed

investor can assess more accurately the worth of a company’s stock (Deumes &

Knechel 2008) and these (risk) disclosures bring general gains in economic efficiency

(Frolov 2004 ).

Correspondingly, corporate risk disclosure is being recognised increasingly in studies as

a fundamental of business disclosure through provision of transparent information (e.g.

Abraham & Cox 2007; Beretta & Bozzolan 2004; Cabedo & Miguel Tirado 2004;

Hassan 2009; Linsley, Shrives & Crumpton 2006). These studies investigate corporate

risk disclosure given that users of financial reports are demanding relevant risk

information increasingly in order to assess the financial position of a company (Uddin

& Hassan 2011). Moreover, the Global Financial Crisis (GFC) of 2007-2008 raised

significant concern in relation to corporate risk disclosure by banking institutions

(Beltratti & Stulz 2012; Brunnermeier 2009; Conyon, Judge & Useem 2011; Erkens,

Hung & Matos 2012; Fahlenbrach, Prilmeier & Stulz 2011; John & Fred 2009; Milne &

Wood 2008). These authors assert that this period is the worst financial phase after the

Great Depression of the 1930s.

5

Despite the growing attention on and importance of corporate risk disclosure,

considerable bodies of literature that reflect detailed academic work on disclosure and

on corporate governance, there remains limited research on corporate risk disclosure. In

particular, research linking risk disclosure with governance mechanisms, is rare

(Abraham & Cox 2007; Lajili 2009; Lajili & Zéghal 2005). According to Linsley and

Shrives (2005a), although various aspects of disclosure have been investigated in the

last 20-30 years, risk disclosure has not yet been examined seriously.

Most existing studies on risk disclosure, whether in financial or non-financial

institutional settings, provide empirical evidence from developed countries. The extant

studies focus on Anglo-Saxon countries (e.g. Abraham & Cox 2007; Deumes &

Knechel 2008; Lajili 2009; Lajili & Zéghal 2005; Linsley & Lawrence 2007; Linsley,

Shrives & Crumpton 2006; Solomon et al. 2000); European Latin countries (e.g.

Oliveira, Rodrigues & Craig 2011), French (e.g.Thuélin, Henneron & Touron 2006);

Asian countries (e.g. Mohobbot 2005); and Arab countries (e.g. Hassan 2009).

However, the difference in institutional and socio-economic settings might affect the

extent and nature of corporate risk disclosure differentially in between developed and

developing countries. For example, institutional pressure might create doubts about the

effectiveness of the Anglo-Saxon model of corporate governance when applied in

developing countries (Khan, Muttakin & Siddiqui 2013). Developing countries, which

are economically more vulnerable, many have not yet implemented international

disclosure standards from which they might benefit.

The International Accounting Standards Board (IASB) issued International Financial

Reporting Standard (IFRS) 7 (Financial Instruments: Disclosures) in 2005 to become

effective in January 2007. However, the slowdown in the global economy during the

GFC (2007-2008) and the increasing demand for risk reporting highlighted diverse risk

reporting practices, some of which were deficient, resulting in several regulatory

amendments in IFRS 7. In the banking industry, another relevant standard is Basel II:

Market Discipline (hereafter international standards), which was issued by the Basel

Committee on Banking Supervision (BCBS) in 2004. Basel II provides

recommendations on banking laws and regulations, guidelines for accounting practices

6

and disclosure and creates requirements in some countries. The implementation process

of Basel II: Market Discipline was generally slow prior to 2007-2008 until the GFC

caused a major banking crisis through default credit, mortgage backed securities, and

similar derivatives (Barth & Landsman 2010; Brunnermeier 2009). The issuance of

global guidance in relation to risk reporting, and its tightening via amendments over

time in the context of the GFC, offers the opportunity to document corporate responses

and to examine changes in reporting practices over time. Examining these changes in a

developing country is especially important since the changes are likely to be from a

comparatively low base of risk disclosure. Bangladesh, among the developing

countries, marked the beginning of a major development in its financial reporting

through implementing both of these international standards after the GFC (2007-2008).

In addition, the presence of a number of listed banks (30) in Bangladesh provides an

adequate sample for the collection of information and provides sufficient statistical

power for this longitudinal study to provide rigorous results. Moreover, the population

of banks in Bangladesh consists of both conventional (i.e. interest-based operations) and

non-conventional (Islamic Shariah based, i.e. profit/loss sharing mode) banks. The

practice of non-conventional (Islamic) banking in Bangladesh, which follows Islamic

Shariah law, might mean different levels of corporate risk disclosure compared with that

of conventional banks. For these reasons, corporate risk disclosure, particularly in the

banking industry, is deserving of greater research attention than it has received to date.

Previous studies (e.g. Abraham & Cox 2007; Dobler, Lajili & Zéghal 2011; Lajili 2009;

Linsley & Shrives 2005a) investigate corporate risk disclosures and the determinants of

these empirically by examining annual reports, however, very little is known about

regulators’ perceptions of the determinants of corporate risk disclosure. As regulators

are involved, either directly or indirectly, in the risk reporting process, it is important to

explore regulators’ insights in order to achieve a better understanding. This study

reports analysis of interviews with senior regulators and bank officials in order to

provide greater insights to evidence from empirical analysis. Access to such senior

personnel is rare and no prior disclosure studies combine evidence from multiple

sources in the way this study achieves. Briefly put, this research aims to investigate risk

7

disclosure practices, their determinants and the association of risk disclosure with

financial performance by banking institutions in a comprehensive longitudinal study

using Bangladesh as the institutional setting using both quantitative and qualitative

research methods.

1.3 Research justification and objectives

There are three objectives of this study. The first objective is to examine corporate risk

disclosure practices as evidenced in Bangladesh listed banks’ annual reports over a

seven-year period (2006-2012). The purpose of this longitudinal study is to provide a

snapshot of the volume and types of risk disclosure and examine whether the issuance

of international standards (IFRS 7 and Basel II: Market Discipline) triggered changes in

corporate risk disclosure. In addition, the lack of longitudinal studies investigating

changes in risk disclosure behaviours by banks motivates this study, which attempts to

fill a research gap and add to the existing body of knowledge on risk disclosure

practices. It is of interest to investigate how risk reporting has developed over time in

response to the development of new international standards and codes of corporate

governance (Ahsan, Skully & Wickramanayake 2009) in order to evaluate likely future

changes, for example in response to implementation of Basel III1. This is especially so

in a developing country such as Bangladesh due to implementation of Basel III in 2015

(Siddikee, Parvin & Hossain 2013).

The second objective is to identify the relationship between risk disclosure and bank

characteristics. The findings of previous studies (Helbok & Wagner 2006; Hossain

2008) reveal that the extent of risk disclosure is related to bank characteristics, however

perceptions by regulators in relation to risk disclosure determinants has been unexplored

in previous studies. This study focuses on the determinants of risk disclosure by testing

data gathered from annual reports empirically and, in addition, by interviewing

representatives from the banking regulatory sphere to identify their perceptions about

risk disclosure.

1 Basel III was initially scheduled to be implemented from 2013 until 2015; however, the implementation

process is now extended until March 2019.

8

The third objective of this study is to investigate the association of risk disclosure with

banks’ financial performance. Previous studies offer insights into the potential

usefulness and perceived benefits and cost of disclosure (Botosan 1997; Lajili 2009;

Linsley, Shrives & Crumpton 2006). These authors assert that improved disclosure

enhances corporate transparency and provides useful information to stakeholders,

lowers the cost of capital, and reduces information asymmetry. There has been limited

research on whether forces attributable to institutional theory are capable of influencing

banking operational behaviour, and more specifically, even more limited research on

this topic in developing economies. As mentioned earlier, the institutional setting of a

developing country is different from that of a developed country. Examining the

association of corporate risk disclosure with financial performance warrants research in

a developing economy setting. This study goes one-step further by examining the

association of risk disclosure with banks’ operating performance and bank valuation.

Based on the above research objectives, the research questions posed in this study are:

Research Question 1: What is the extent of corporate risk disclosure and to what extent

did banks in Bangladesh respond to the development of international standards relevant

to risk and its disclosure (IFRS 7 and Basel II: Market Discipline)?

Research Question 2: What bank characteristics and/or institutional pressures act as

determinants for disclosure of risk?

Research Question 3: Does risk disclosure have an association with bank performance?

Based on the research questions above, Figure 1.2 depicts the framework for this

research.

9

1.4 Key terms

This section highlights the definitions of key concepts and terms that are used

extensively throughout this thesis. These are presented in Table 1.1.

Term Explanation

Risk Disclosure ‘If the reader is informed of any opportunity or prospect, or of any hazard,

danger, harm, threat or exposure, that has already impacted upon the

company or may impact upon the company in the future or of the

management of any such opportunity, prospect, hazard, harm, threat or

exposure’ (Linsley & Shrives 2006, p.389).

Risk Disclosure

Index

A comprehensive Risk Disclosure Index has been developed in this study

to examine the extent of risk disclosure by listed banks in Bangladesh.

This benchmark set is based on international standards (IFRS 7 and Basel

II: Market Discipline) and an extensive list of risk disclosure items from

key previous studies. The Risk Disclosure Index consists of 147 specific

risk items in seven categories.

2Figure 1.2: Depiction of the framework for this research

1 Table 1.1: Key terms

Research Question 1 Research Question 2

Research Question 3

The extent of risk disclosure in annual

reports

Determinants of risk disclosure

Association of risk disclosure with

performance

10

Term Explanation

Voluntary and

Mandatory

disclosures

Mandatory disclosure: Any disclosure that is required by law,

accounting principles, or regulatory agencies’ regulations are

mandatory disclosure (Hassan & Halbouni 2013).

Voluntary disclosure: Any disclosure that is not classed as mandatory.

In the absence of mandatory requirements under the Bangladesh Bank

Company Act 1991 (amended in 2003), or the Companies Act 1994,

International Financial Reporting Standards (IFRS) or Bangladesh

Accounting Standards (Bangladesh Financial Reporting Standards), it is

argued in this thesis that risk disclosure effectively is voluntary for listed

banking institutions.

Determinants The key underlying factors in relation to risk disclosure in this study are

based on two underpinning theories (agency theory and neo institutional

isomorphism).

Performance Bank performance is measured using two aspects; bank operating

performance (e.g. financial performance, employee efficiency, solvency

efficiency and deposit concentration) and bank valuation (Tobin’s q and

book-to market ratio).

Global financial

crisis (GFC)

The GFC (2007-2008) raised significant concern in relation to corporate

risk disclosure as large numbers of financial institutions collapsed in the

U.K (RBS and HBOS), in the U.S (Citigroup, Lehman Brothers, Merrill

Lynch, and also in other European Countries (Dexia, Hypo RealEstate

and UBS). In Bangladesh, there is growing evidence that the post- GFC

(2007-2008) impacts are manifested in declining exports, declining

migration of labour, a growing number of sick industries, industrial

unrest, and reduced growth (Bangladesh Bank 2013b).

1.5 Research approach

As mentioned earlier, three interrelated Phases examine the research questions involved

in this study. The research method employed is detailed in Chapter 6. As shown in

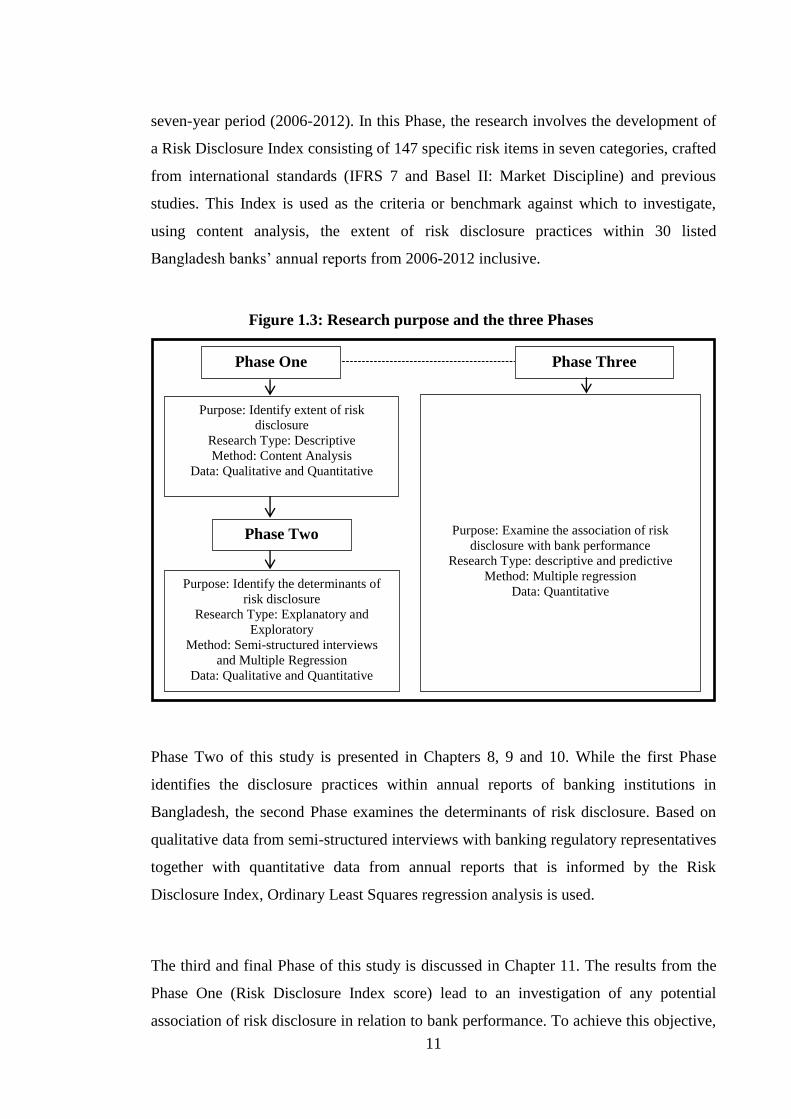

Figure 1.3, Phase One of this study, presented in Chapter 7, investigates the extent of

risk disclosure of all listed banks on the Dhaka Stock Exchange in Bangladesh over a

11

seven-year period (2006-2012). In this Phase, the research involves the development of

a Risk Disclosure Index consisting of 147 specific risk items in seven categories, crafted

from international standards (IFRS 7 and Basel II: Market Discipline) and previous

studies. This Index is used as the criteria or benchmark against which to investigate,

using content analysis, the extent of risk disclosure practices within 30 listed

Bangladesh banks’ annual reports from 2006-2012 inclusive.

Phase Two of this study is presented in Chapters 8, 9 and 10. While the first Phase

identifies the disclosure practices within annual reports of banking institutions in

Bangladesh, the second Phase examines the determinants of risk disclosure. Based on

qualitative data from semi-structured interviews with banking regulatory representatives

together with quantitative data from annual reports that is informed by the Risk

Disclosure Index, Ordinary Least Squares regression analysis is used.

The third and final Phase of this study is discussed in Chapter 11. The results from the

Phase One (Risk Disclosure Index score) lead to an investigation of any potential

association of risk disclosure in relation to bank performance. To achieve this objective,

3 Figure 1.3: Research purpose and the three Phases

Phase One Phase Three

Phase Two

Purpose: Identify extent of risk

disclosure

Research Type: Descriptive

Method: Content Analysis

Data: Qualitative and Quantitative

Purpose: Identify the determinants of

risk disclosure

Research Type: Explanatory and

Exploratory

Method: Semi-structured interviews

and Multiple Regression

Data: Qualitative and Quantitative

Purpose: Examine the association of risk

disclosure with bank performance

Research Type: descriptive and predictive

Method: Multiple regression

Data: Quantitative

12

this Phase utilises primarily quantitative financial data from the annual reports of the

banks within this study.

1.6 Research contribution

The study contributes to the literature in several ways; First, in an attempt to redress in

part the empirical scarcity in risk disclosure studies in South Asian developing

countries, this study is the first to provide knowledge of corporate risk disclosure

practices and their underlying factors. Second, it helps assess the impact of new

international standards upon the extent of risk disclosures in a weak economic period

(GFC) and beyond. Third, a comprehensive Risk Disclosure Index is developed based

on international standards and is used as a benchmark against which to score actual risk

disclosures. The Risk Disclosure Index constructed in this study is of relevance to

financial institutions seeking to provide information for stakeholders and, indeed, to all

relevant parties seeking to assess or evaluate information in relation to risk disclosure.

To the researcher knowledge, the Risk Disclosure Index developed in this study is the

first, developed for the banking industry. Finally, the Risk Disclosure Index could be

used as a guideline for corporate risk disclosure in financial reporting and could be

used as an early warning system for banking institutions in any country. In addition, the

Risk Disclosure Index, developed in this research, contributes to the literature by

quantifying the extent of risk disclosure and identifying the factors determining them.

Stakeholders, particularly depositors and investors, can use this Index in selecting

their bank of interest. A detailed discussion on research contribution is presented in

Chapter 12.

1.7 Thesis outline

Figure 1.4 depicts the structure of the study and reveals that it is organised in Five Parts.

Part One comprises three Chapters. Chapter 1, this Chapter, describes the significance

of the study, research objectives and research questions, the approach, and thesis

structure. Chapter 2 introduces risk disclosure as an issue of concern and overviews the

regulatory framework and institutional arrangements for developing a risk-reporting

framework. Chapter 3 presents the contextual background and explains the major

impetus for selecting Bangladesh as the location for this study.

13

4Figure 1.4: Structure of the thesis

Part One: Introduction and research background

Chapter 1 presents an introduction to the research study

Chapter 2 provides the background to risk disclosure concerns

Chapter 3 presents the background context of Bangladesh as the location for the study

Part Two: Literature Review and Theoretical Underpinning

Chapter 4 presents previous studies on corporate risk disclosure

Chapter 5 presents the theoretical framework, conceptual framework and development

of Hypotheses

Part Three: Methodology

Chapter 6 presents the research methodology adopted. Data collection techniques are

described in this Chapter also

Part Four: Analysis and results

Phase One

Chapter 7 reports on the content analysis of sample banks’ annual reports

Phase Two

Chapter 8 presents the thematical discussion using qualitative interview data in relation

to the determinants of risk disclosure

Chapter 9 reports the descriptive results prior to further analysis of quantitative data

Chapter 10 reports the multiple regression results for the model adopted to investigate

the association between risk disclosures and their potential determinants

Phase Three

Chapter 11 presents the multiple regression results for the model developed to examine

the association between risk disclosure and bank performance

Part Five: Conclusion

Chapter 12 comprises a summary of the findings, implications, limitations, and

recommendations for future research

14

Part Two consists of two Chapters, Chapters 4 and 5. Chapter 4 reviews relevant

literature. This Chapter also identifies gaps in the literature addressed by this study and

the applicability of risk disclosure practices within developing country contexts.

Chapter 5 presents the theoretical framework for this study and provides justification for

and an overview of the theoretical framework (agency theory and neo institutional

isomorphism) underpinning this research. This Chapter introduces the conceptual

framework underpinning this study also.

Part Three explains the methodology used in this study. Chapter 6 describes the

research design, sample, research instruments and analytical techniques and approaches.

As the research objectives of this study support a mixed method approach, the Chapter

explains both qualitative and quantitative methods of data collection and analysis

techniques. Part Four presents analysis of the data gathered from annual reports and

interviews. Chapter 7 presents the content analysis of data elicited from annual reports,

Chapter 8 thematically analyses the qualitative data and Chapters 9, 10 and 11 present

the quantitative data analysis using statistical techniques such as multiple regression.

The final Part presents the research findings, conclusions and implications. Chapter 12

provides the conclusions relating to risk disclosure practices, their determinants and

performance by banks in Bangladesh. The thesis concludes with the summary of the

findings, the research limitations and ideas for further potential research are provided.

15

CHAPTER 2: Risk Reporting as an Issue of Concern

2.1 Introduction

The primary objective of this Chapter is to introduce the issue of risk reporting as a

corporate and regulatory concern. This Chapter presents a background to and overview

of risk reporting to provide an explanation of corporate risk reporting practice.

Shareholders and other stakeholders desire banks to disclose both financial and non-

financial information for related investment, credit and other decisions. To fulfil

stakeholders’ demands effectively, financial reporting has been improving and

increasingly communicating information with regard to risk profile (Beretta & Bozzolan

2004). Moreover, the demand by stakeholders for risk reporting has been increasing

after the GFC of 2007-2008 (Lajili 2009; Michael, Kaouthar & Daniel 2011).

Before turning to discussion of the background contextualisation of Bangladesh in the

next Chapter, this Chapter addresses the key concepts underlying the research questions

identified in Chapter 1. Figure 2.1 depicts the structure of this Chapter as follows.

2.2 Background to risk reporting

Risk reporting has been of increasing importance in international policy arenas and

raised significant interest around the world (Aebi, Sabato & Schmid 2012). The

5Figure 2.1: Roadmap of Chapter

Introduction (2.1)

Background to risk

reporting (2.2)

Overview of

institutional setting

(2.4)

Policies, pressures

and corporate

response (2.3)

Risk disclosure as a

major concern in

Bangladesh (2.5)

Chapter conclusion

(2.6)

16

increasing complexity of business and need for transparency create demand for clarity

in disclosing companies’ risk profiles, risk management and risk monitoring processes

(Michael, Kaouthar & Daniel 2011). Hassan and Halbouni (2013) argue that annual

reports should provide the integral business process that communicates between the

company and key stakeholders as to whether stakeholders’ concerns have been

understood by the company. This section highlights the characteristics of the business

environment that create demand for risk disclosure and motivates regulators and

accounting professionals to enhance the quality of reporting.

2.2.1 Changes in business environment and emergence of risk reporting

The business environment has changed dramatically over the past decade, driven by

technological advancement, globalisation of markets and concentration of power in

market investors (Albrecht & Sack 2010). These changes make the business

environment more demanding for stakeholders to comprehend and similarly so for

business information without complete accompanying explanations (Beretta &

Bozzolan 2004). Figure 2.2 highlights the factors affecting reporting by companies.

Technological advancements such as computers, the internet, and data transmission

software have simplified the development of business, thereby creating opportunities

and challenges for companies. Such technological advancement has made it easier for

companies to communicate with investors. Additionally, globalisation of business has

allowed the world to become one giant marketplace with increased availability of

competitive information (Albrecht & Sack 2010). Given the differences in legal, social

and economic circumstances in different countries and also the differences in need for

accounting information among users of financial information, there have been calls by

international standard setters to harmonise accounting standards related to the

preparation of financial reporting (Beretta & Bozzolan 2004). Particularly, the

international harmonisation of accounting practices has been a central concern for

companies operating in more than one country (Marshall & Weetman 2002).

17

Source: Adapted from Albrecht and Sack (2010)

Albrecht and Sack (2010) argue that the combined forces of technology, globalisation

and market power have increased competition, regulation, financial volatility and the

level of uncertainty about business entities. Consequently, shareholders and other

stakeholders want listed companies to disclose financial as well as non-financial

information in relation to companies’ future performance (Albrecht & Sack 2010;

Beretta & Bozzolan 2004). In this sense, Beretta and Bozzolan (2004, p. 266) argue

that ‘listed companies have been improving the communication of their long-term

value-generation capabilities by increasing the amount of information disclosed with

regard to the risks faced and their expected impact on future profits’.

Moreover, many organisations have adopted rapid business expansion through either

internal development or mergers and acquisitions (Hill & Short 2009). However, such

expansion raises many challenges and concerns for investors. In addition, companies are

being confronted with frequent change in laws and regulations (Barth, Caprio Jr &

Levine 2004). Complying with these regulations is sometimes costly and adversely

affects companies’ operating cost and performance. Therefore, extant research argues

that corporate risk disclosure could be an effective monitoring system because it

provides a greater transparency and increases investors’ confidence in their decisions

6Figure 2.2: Factors affecting financial reporting

Drivers

Changes

- Technology

- Globalisation

- Concentration of Market Power

- Increased competition - Increased regulation - Financial volatility - Concentrated Market Power - Increasingly complex business - Better, quicker, and more decisive strategic actions by management - Increased focus on customer satisfaction

-Increased uncertainty and the explicit recognition of

risk

Demand for risk reporting Results

18

(Cabedo & Miguel Tirado 2004; Linsley & Shrives 2006; Solomon et al. 2000).

Deumes and Knechel (2008) argue that risk disclosure creates corporate transparency

for well-functioning markets and brings general gains in economic efficiency.

2.2.2 Risk reporting as an issue of concern in banking institutions during

financial crises

A large number of financial institutions collapsed during the GFC of 2007-2008 and

that raised significant concern in global credit markets about their performance and risk

governance (Erkens, Hung & Matos 2012; Fahlenbrach & Stulz 2011). Thereafter,

some studies have examined the performance of corporate governance and additional

attention has been paid to banks’ risk management (Adams 2012; Bebchuk 2010;

Beltratti & Stulz 2012; Erkens, Hung & Matos 2012).

Banking crises have been a common phenomenon throughout history; indeed banks are

at the centre of financial crises (Barth & Landsman 2010). To some extent, banking

crises are like periodic events that ‘unexpectedly emerge from the earth’ (Laeven 2011,

p.18). Reinhart and Rogoff (2013) count 268 banking crises over the period from 1800

through to 2008. Bordo et al. (2001) revealed that the frequency of banking crises has

been increasing in recent decades. According to Reinhart and Rogoff (2013, p.4557)

‘the historical frequency of banking crises is quite similar in high- and middle-to-low-

income countries, with quantitative and qualitative parallels in both the run-ups and the

aftermath’. The National Commission on the Causes of the Financial and Economic

Crises in the U.S. (2011; p. xvii) concluded that ‘dramatic failures of corporate

governance ….at many systematically important financial institutions were a key cause

of financial crises’.

The lack of risk management and failure of governance mechanisms are cited

commonly as the key contributing factors to the GFC of 2007-2008 (Aebi, Sabato &

Schmid 2012; Beltratti & Stulz 2012; Diamond & Rajan 2009; Hashagen, Harman &

Conover 2009; Strebel 2009). These raise several questions for regulators with respect

to corporate governance and banks and for testing the value of ‘risk governance’ and

19

‘corporate governance’ (Aebi, Sabato & Schmid 2012; Fahlenbrach & Stulz 2011).

Bebchuk (2010) suggests that excessive risk taking in the financial sector performed a

key role in the financial crisis of 2007-2008. Beltratti and Stulz (2012) argue that banks

with poor governance were involved in excessive risk taking responsible for huge losses

during the financial crisis. Goddard, Molyneux and Wilson (2009, p. 363) report ‘an

estimation of $2.7 tn (trillion) for write downs of the US – originated assets by banks

and other financial institutions between 2007- 2010 and the estimated write downs for

all mature market-originated assets for the same period are in the region of $4tn

(trillion).’

Accordingly, the financial crisis of 2007-2008 led to a slowdown in the global economy

and a further awareness of and need for appropriate risk governance structures within

banking institutions (Aebi, Sabato & Schmid 2012). It is logical that banks that identify

and analyse risks earlier than their business counterparts will be better positioned to

avoid or mitigate potential risks and can create value for investors by fostering

understanding of the risk profile of invested businesses. For example, Solomon et al.

(2000) found stakeholders strongly demand corporate risk disclosure to improve their

investment decisions. Beretta and Bozzolan (2004) argue that effective risk

communication minimises investment risks and builds opportunities for stakeholders.

Therefore, annual reporting of risk is needed to make available worthwhile disclosure to

stakeholders in making their investment decisions (Milne 2002).

2.3 Risk disclosure related policies, pressures and corporate responses

The perceived importance of corporate risk disclosure as a major financial reporting

issue has been highlighted by increased global interest, debate and discussion on the

issue of risk reporting among stakeholders since the GFC (Michael, Kaouthar & Daniel

2011). Concerns about corporate risk disclosure led bank supervisors and regulators to

rethink the rationale of banking regulations in providing transparent information and

building stakeholders’ confidence (Lajili 2009).

20

Several academic and professional reports (AICPA 1995; IASB 2007; ICAEW 1995;

Schrand & Elliott 1998), particularly in the U.S.A., U.K. and other European countries,

demand for inclusive risk information in financial reports. Acknowledging the

importance of risk disclosure, standard setters have enhanced regulatory reforms in

recent years; such as by issuing International Financial Reporting Standard 7 [Financial

Instruments: Disclosures] (IFRS 7) and BASEL II: Market Discipline, to govern

accounting practices and disclosure. Internationally, to date, the most advanced risk

disclosure regulations exist in the U.S.A., Canada, U.K and Germany (Michael,

Kaouthar & Daniel 2011). These countries require and enforce risk information in both

the notes to financial reports and supplementary management reports.

In the U.S.A., Financial Reporting Release No 48 ‘Disclosure of Accounting Policies

for Derivative Financial Instruments and Derivative Commodity Instruments and

Disclosure of Quantitative and Qualitative Information about Market Risk Inherent in

Derivative Financial Instruments, Other Financial Instruments, and Derivative

Commodity Instruments’ (FRR 48) was issued in 1997. This document requires

Securities and Exchange Commission enlisted companies to disclose market risks in the

notes and in the Management reports. Listed companies in Canada also apply FRR 48

to disclose risk information in the Management Discussion and Analysis (MD&A)

section. In the U.K, the Operating and Financial Review (OFR), issued in 1993,

necessitates disclosure of information about key risks. The Australian Securities

Exchange (ASX) issued its first version of Corporate Governance Principles and

Recommendations in 2003 (amended in 2007 and 2010) where Principle 7 pertains to