seventh multi-year expert meeting on commodities …unctad.org/meetings/en/presentation/suc...

TRANSCRIPT

Seventh Multi-year Expert Meeting on Commodities and Development

15-16 April 2015 Geneva

Near-Term Oil Outlook - 2015

By

Abhishek Deshpande Lead Oil Markets Analyst, Economic Research

Natixis

The views expressed are those of the author and do not necessarily reflect the views of UNCTAD.

15 April 2015, UNCTAD, Geneva

Dr Abhishek Deshpande

Lead Oil Markets Analyst

Economic Research

Near-Term Oil Outlook - 2015

45

55

65

75

85

95

105

115

45

55

65

75

85

95

105

115

Dec-13 Apr-14 Aug-14 Dec-14

BFOE ($/bbl)

Source: Bloomberg

2

Oil in 2014-15

Libyan output above 800,000b/d

Libyan supply back online

Russia-Ukraine crisis/July/August

Iraq-ISIS conflict intensifies in June

OPEC producing significantly more than call-on-OPEC after demand was revised downwards and after the return of Libyan oil

Libyan port deal and signs US crude exports

OPEC decided to keep total production cap unchanged at 30mn b/d

Iran & P5+1 nuclear talks extended

Physical balances had started to weaken slowly in the first half of 2014, however prices were supported by geopolitical tensions.

Supply-demand fundaments weakened further with the unprecedented increase in non-OPEC supply, further weakness in

Chinese and European demand and the paradigm shift in OPEC policy.

Large Capex cuts and fall in rig count announced Improved demand from Asia and US

4/13/2015

3

Supply disruptions

0

500

1000

1500

2000

2500

2010 2011 2012 2013 2014 2015

Supply Disruption (1000b/d)

Iraq

Iran

Libya

Source: PIRA

4/13/2015

4

Weak fundamentals

Since the start of 2014, the fundamentals in the global oil industry have deteriorated markedly.

0

0.4

0.8

1.2

1.6

2

0

0.4

0.8

1.2

1.6

2

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14

Monthly estimates of global demand growth vs non-OPEC supply growth in 2014 (mn b/d)

Demand growth

Non-OPEC Supply growth

Sources: Natixis, IEA

4/13/2015

OPEC policy results in increase in inventories!

• Crude and NGL inventories were on average 1.1% higher in 2014 than 2013-IEA • Crude inventory expected to be up 7.3%yoy in Feb15 - PIRA

OPEC’s (mainly GCC allies) refusal to cut production and let markets balance by itself - a paradigm shift in policy to maintain

market share and put pressure on marginal producers worldwide. Result: increase in crude inventories.

4/13/2015 5

0

100

200

300

400

500

600

700

800

900

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15

US, Europe & Japan Crude Stocks (mn bbls)

Spare

Japan

Europe

USA

931

Source: PIRA

Tank Capacity 931mn bbl Tank Capacity 931mn bbl

New era in oil market or just a temporary phase?

6

• Will demand pick up and will the growth be similar to the one seen in the last decade?

• What about global crude oil supply growth? Will it continue to outpace growth in demand

• Is US becoming the new marginal producer?

• If so then what happens to OPEC? Will OPEC continue to maintain its output over 30mn b/d or will it be the first to blink?

OIL DEMAND

4/13/2015 7

8

Lower oil prices are positive for global growth

• Similar to 2009, lower oil prices should help to boost global growth

• Oil consuming nations will benefit from a rise in household disposable income and/or improving government finances • Improvement of terms of trade means improvement in current balances and currencies

• Falling income in oil producing countries will reduce saving more than it cuts consumption

• A slightly positive-sum game for global growth (Keynesian balanced budget multiplier effect)

• Over time, the resultant boost to global growth should stimulate demand for oil, even where price elasticity of demand appears to be low

• IMF estimates that a 10-20% fall in oil lifts world GDP by 0.05%

0%

2%

4%

6%

8%

10%

12%

0%

2%

4%

6%

8%

10%

12%

1999 2001 2003 2005 2007 2009 2011 2013 2015

"Oil burden" - oil costs as % GDP with Brent crude averaging $64.50/bbl in 2015

Germany US

Japan China

India

Sources : Bloomberg, BP, Natixis

4/13/2015

9

Natixis near term oil demand forecasts

Note: Numbers above do not add up as the total includes other regions

Consumption of oil grew by around 700,000b/d in 2014. Demand is expected to increase by around 1mn b/d in 2015, boosted by low oil prices.

4/13/2015 9

Region OPEC IEA Natixis

Other Asia (Incl. India) +250 +430 +360

Source: Natixis, IEA, OPEC

Demand (yoy growth, 1000 b/d) - 2015

OECD +20

China +280 +280

-10 +20

+310

South America (excl. Chile) +110 +130

Middle East +180 +200

+200

+280

+1170 +990 +1000Net growth

Non-OPEC OIL SUPPLY

4/13/2015 10

11

Non-OPEC oil supply: near-term drivers

On the upside:

• US oil production is expected to rise by close to 0.74mn b/d in 2015. Output growth is expected to be greatly affected by low oil prices in 2015, given the steep decline in rig count as producers are idling rigs and capex cuts. But oil production could easily bounce back given the declining break-evens in the US.

• US NGL output is expected to rise to more than 3.8mn b/d by 2020 from current 3.07mn b/d, although growth is likely to be impacted

• Brazilian oil output expected to rise by up to 100k b/d in 2015 due to ramp up at pre-salt fields

On the downside:

• Russian oil output is expected to fall by 100k-110k b/d in 2015 due to sanctions and limited investments • Kashagan will not restart until 2016

• Lower output is expected from Middle East (Yemen) and Africa (especially Egypt, Ghana and Sudan) in 2015 • Mexican oil output is expected to decline further in 2015 by 160kb/d

Low oil prices will reduce investment in North Sea, Brazil, Canada, US and Asia, with the impact on output/growth felt as

early as second half of 2015 in some regions. We are expecting most of the non-OPEC reductions to come from North American unconventional oil supply. This supply,

unlike conventional supply, also has the ability to spring back very quickly if prices are above the required break-evens.

4/13/2015 11

12

Global Capex

• Total global Capex cuts identified in excess of $135bn

Source: Various

4/13/2015 12

-90%

-70%

-50%

-30%

-10%

10%

30%

50%

70%

Lyn

de

n E

ne

rgy

Ko

sm

os

Petr

oc

elt

icN

uvis

taO

il In

dia

Ltd

So

uth

wes

tern

En

erg

yO

NG

CG

DF

SU

EZ

Ha

llib

urt

on

PK

N O

rlen

* Q

uic

ks

ilve

r R

es

ou

rce

sD

iam

on

db

ack

En

erg

yB

eac

h E

nerg

yE

nerg

y X

XI

Na

tio

na

l F

uel C

oS

un

co

rB

lack

pe

arl

Hin

du

sta

n P

etr

ole

um

Mag

ell

an

Petr

ole

um

Co

rpo

rati

on

San

ch

ez E

ne

rgy

CN

PC

EN

IP

TT

EP

Lu

ko

ilS

tato

ilT

ota

lT

ull

ow

Exx

on

Mo

bil

BP

Ch

ev

ron

Ch

ino

ok E

ne

rgy

To

urm

alin

eP

em

ex

EQ

TP

etr

on

as

7G

en

era

tio

ns

He

ss

Cre

sce

nt

Po

int

Van

gu

ard

Na

tura

l R

es

ou

rces

LL

CB

ellatr

ixC

ab

ot

Oil a

nd

Gas

En

can

a E

ne

rgy

Dra

go

nC

an

ad

a N

atu

ral R

eso

urc

es

De

vo

n E

ne

rgy

Eco

petr

ol

CN

OO

CM

ara

tho

n O

ilP

etr

ob

ras

Ga

zp

rom

Fre

ep

ort

Mc

Mo

ran

Ch

es

ap

ea

ke

En

erg

yM

ed

co

Re

ps

ol

SM

En

erg

yG

ulf

po

rt E

nerg

y C

orp

Sin

op

ec

PD

C E

nerg

yS

ch

lum

be

rge

rW

hit

ing

Petr

ole

um

Zarg

on

Oil

an

d G

as

TA

G O

ilM

em

ori

al P

rod

ucti

on

Pa

rtn

ers

En

erg

en

BG

Co

nc

ho

Imp

eri

al O

ilL

un

din

Ne

wfi

eld

En

erg

yC

on

oco

Ph

illi

ps

Ap

ac

he

Co

rpo

rati

on

Co

ns

ol

En

erg

y In

cC

on

tin

en

tal R

eso

urc

es

Mu

rph

y O

ilO

ccid

en

tal

Pe

tro

leu

mB

ayte

xC

arr

izo

En

erg

yE

xc

o R

es

ou

rce

sN

igh

thaw

k E

nerg

yO

MV

Bo

na

nza C

reek

En

erg

yW

hit

eca

pM

ata

do

r R

eso

urc

es

Ro

se

tta R

eso

urc

es

RS

P P

erm

ian

In

cC

rew

Lo

nes

tar

Re

so

urc

es

Pen

nW

es

tT

AQ

AC

en

tric

aE

nerp

lus

En

qu

es

tE

OG

Res

ou

rce

sH

usk

y E

nerg

yN

ob

leA

nte

roA

nad

ark

oC

en

ovu

s E

ne

rgy

Pen

n V

irg

inia

Co

rpD

eeT

hre

eS

an

tos

BH

P B

illito

nL

RR

En

erg

yM

ae

rsk

Oa

sis

Pe

tro

leu

mP

ion

eer

Na

tura

l R

eso

urc

es

Ra

ng

e R

es

ou

rces

De

nb

ury

Bre

itB

urn

En

erg

y P

art

ne

rsU

nit

Co

rpo

rati

on

Ca

na

dia

n O

il S

an

ds

Co

msto

ck

Lare

do

Petr

ole

um

Ho

ldin

gs

Pre

mie

r O

ilC

hap

arr

al

En

erg

yG

len

co

reH

alc

on

Res

ou

rce

sO

ph

ir E

ne

rgy

Pare

x R

eso

urc

es

Pert

am

ina

QE

P R

eso

urc

es

San

dri

dg

e E

nerg

yS

ton

e E

nerg

yT

ran

sg

lob

e E

ne

rgy

WP

XB

on

avis

taC

ima

rex

Lin

n E

nerg

yP

ars

ley

En

erg

yP

ac

ific

Ru

bia

les

Bil

l B

arr

ett

Co

rpC

air

n I

nd

ia L

tdR

oya

l D

utc

h S

he

llV

erm

illi

on

En

erg

yA

pp

roac

h R

es

ou

rces

Ith

aca

Jo

nes

En

erg

yM

id-C

on

En

erg

y P

art

ners

Lig

hts

tre

am

Petr

oA

me

rica O

il C

orp

Ke

lt E

xp

lora

tio

nL

on

g R

un

Pain

ted

Po

ny

Go

od

ric

h P

etr

ole

um

Em

era

ld O

ilD

NO

Ge

ne

lG

ran

Tie

rra

Ult

ra P

etr

ole

um

Co

rpW

T O

ffs

ho

reS

wif

t E

ne

rgy

Str

ate

gic

Oil

an

d G

as

Co

nta

ng

o R

eso

urc

es

Ge

op

ark

Mag

nu

m H

un

ter

Leg

ac

y R

ese

rves

Tri

log

y E

ne

rgy

Man

ito

k E

ne

rgy

Ro

ck

En

erg

yA

tha

ba

sc

a O

ilS

urg

e E

ne

rgy

Source: Various

13

Natixis non-OPEC supply forecasts

Note: Numbers above do not add up as the total includes other regions

Non-OPEC supply of oil grew by 1.9mn b/d in 2014. Non-OPEC supply is expected to increase by around 760,000 b/d in 2015.

4/13/2015 13

Region OPEC IEA Natixis

Africa 0 -10 0

Source: Natixis, IEA, OPEC

Non-OPEC Supply (yoy growth, 1000 b/d) - 2015

North America +700+720+860

OECD Europe 0 +20

South America (excl. Chile) +60 +100

-40

+60

FSU -70 -110

+850 +740 +760

-130

Net growth

14

The “Key Equation”

Global demand

– non-OPEC supply

=

Implicit call on daily OPEC production

The Key Equation:

4/13/2015 14

15

Uncertainty in physical balances

With the outlook for fundamentals discussed earlier we could very well see growth in global demand exceeding growth in non-

OPEC supply by the end of 2015. However this could easily change if US output were to bounce back on high oil prices and lower

break-evens.

4/13/2015 15

0.4

0.8

1.2

1.6

0.4

0.8

1.2

1.6

Jul-14 Sep-14 Nov-14 Jan-15 Mar-15

Monthly estimates of global demand growth vs non-OPEC supply growth in 2015 (mn b/d)

Demand growth

Non-OPEC Supply growth

Sources: Natixis, IEASources: Natixis, IEA

0

0.4

0.8

1.2

1.6

2

0

0.4

0.8

1.2

1.6

2

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14

Monthly estimates of global demand growth vs non-OPEC supply growth in 2014 (mn b/d)

Demand growth

Non-OPEC Supply growth

Sources: Natixis, IEA

16

OPEC production > call-on-OPEC

With global demand expected to grow at a faster pace than non-OPEC supply , we expect the average call-on-OPEC to remain

broadly unchanged at 29.4mn b/d in 2015, as compared to 2014.

OPEC and IEA estimates for the 2015 call-on-OPEC (reported in Mar15 monthly reports) are around 0.6-0.8mn b/d below

expected average OPEC crude production for 2015. As demand exhibits seasonal weakness in 2015H1, this gap could be as high

as 1.5-2mn b/d and as low as -0.4mn b/d in 4Q15.

Call-on-OPEC (mn b/d)

2014 2015

OPEC 29.36 29.19

IEA 29.5 29.62

EIA 29.3 29.13

Sources: IEA, OPEC, EIA, Feb data

4/13/2015 16

28

29

30

31

28

29

30

31

Jul-14 Sep-14 Nov-14 Jan-15 Mar-15

OPEC: 2015 expected daily call (mn b/d)

OPEC expected daily output (OPEC)

OPEC expected daily output (IEA)

Output

Sources : Bloomberg, OPEC, IEA

17

Fiscal break-evens and “reasonable” oil price

• Our estimate for Saudi Arabia’s fiscal break-even oil price stands at around $90/bbl for 2014 and is expected to be higher in 2015. Surpluses prior to 2014 are therefore shifting to deficits.

• Saudi Arabia has acknowledged the possibility of fiscal deficits as it contemplates a period of lower output and restrained oil prices due to increased non-OPEC supply.

• To reduce fiscal break-evens would require key OPEC countries to reduce expenditure (hence subsidies)

• Middle Eastern crude exporting countries have been revising their budgetary expenditures to help them adapt in a lower cost environment. Despite these reductions all but Kuwait will be feeling pressure with current low oil prices based on recent data provided by IMF

• Further price war possible with return of Iranian oil

40

50

60

70

80

90

100

110

40

50

60

70

80

90

100

110

2009 2010 2011 2012 2013 2014 2015 2016

Weighted average oil fiscal breakevens ($/bbl)

Sources: Natixis, IMFNote: weighted average breakevens of Algeria, Iran, Iraq, Kuwait,Libya, Qatar, Saudi Arabia, UAE

0

50

100

150

200

250

-20

20

60

100

140

180

2009 2010 2011 2012 2013 2014 2015 2016

Oil fiscal breakevens ($/bbl)

Algeria Bahrain Iran

Iraq Kuwait Oman

Qatar Saudi Arabia UAE

Libya (rhs)

Sources: IMF

4/13/2015 17

NATIXIS OIL PRICE FORECAST

4/13/2015 18

19

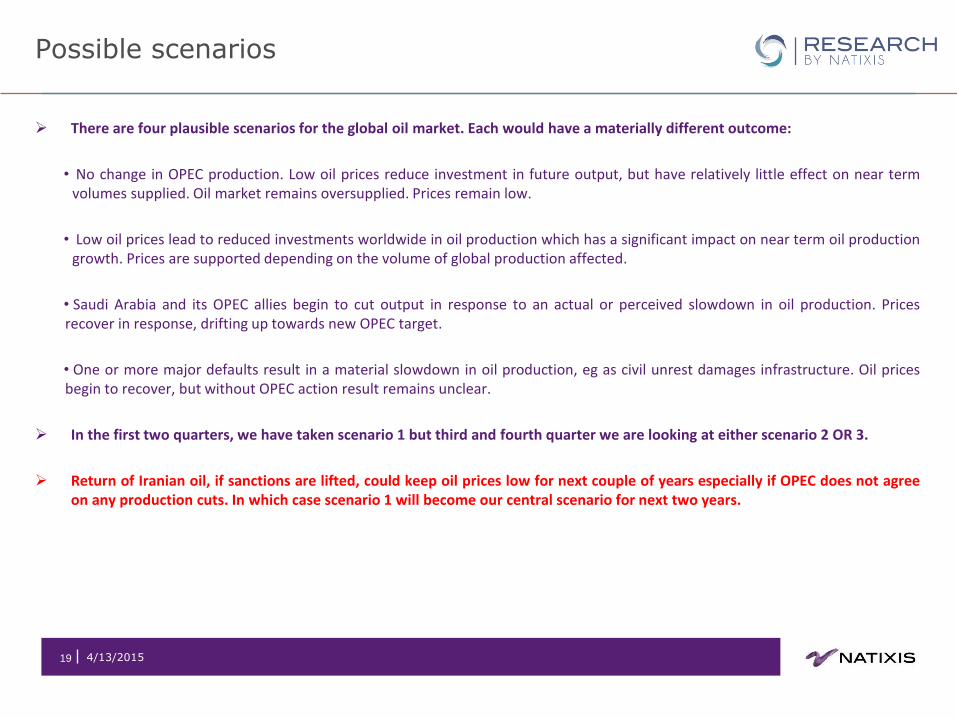

Possible scenarios

There are four plausible scenarios for the global oil market. Each would have a materially different outcome:

• No change in OPEC production. Low oil prices reduce investment in future output, but have relatively little effect on near term volumes supplied. Oil market remains oversupplied. Prices remain low.

• Low oil prices lead to reduced investments worldwide in oil production which has a significant impact on near term oil production growth. Prices are supported depending on the volume of global production affected.

• Saudi Arabia and its OPEC allies begin to cut output in response to an actual or perceived slowdown in oil production. Prices recover in response, drifting up towards new OPEC target.

• One or more major defaults result in a material slowdown in oil production, eg as civil unrest damages infrastructure. Oil prices begin to recover, but without OPEC action result remains unclear.

In the first two quarters, we have taken scenario 1 but third and fourth quarter we are looking at either scenario 2 OR 3.

Return of Iranian oil, if sanctions are lifted, could keep oil prices low for next couple of years especially if OPEC does not agree on any production cuts. In which case scenario 1 will become our central scenario for next two years.

4/13/2015 19

20

Oil price outlook

• Volatility in oil prices to remain high in 2015

• Our forecasts assume increased demand due to lower oil prices, higher seasonal demand in 2015H2, SPR demand from China

and India and a cut in oil production from OPEC or a higher than expected reduction in non-OPEC oil output growth.

• Return of Iranian oil (in the absence of OPEC cuts), would keep pressure on oil prices for longer.

• If fundamentals remain weak, we would expect oil in storage to test storage capacities - even in the US. Oil prices would come

under pressure if stocks worldwide continue to rise at current pace. Prices will have to fall further to price in floating storage.

• The more oil goes into the storage, the longer it might take for oil prices to recover.

4/13/2015 20

40

60

80

100

120

40

60

80

100

120

Apr-12 Aug-13 Jan-15 May-16

Brent price outlook - futures vs Natixis forecast ($/bbl)

Market

Natixis central scenario

Low case scenario

High case scenario

Sources : Bloomberg, Natixis

New era in oil market or just a temporary phase?

21

• Near term: Growth in global demand for oil expected to rise due to low oil prices.

• Non-OPEC supply growth will depend largely on the “new marginal producer” US supply growth. Although the

current idling of rigs suggest that US oil output is likely to reduce by end of 2015, but given the reduced break-

evens and quick turn around if prices are supported could see a rebound in US supply and hence putting a cap on

prices.

• OPEC’s paradigm shift in policy in maintaining their output at around 30mn bbl is likely to stay in place at least for

first half of this year as Saudi Arabia is looking for a sustainable solution to the over supply in the market which

would require a non-OPEC and OPEC coordination as per their latest statements.

• Medium-Long term: Growth in global demand for oil expected to rise but increase could be limited thanks to

regulations, efficiency gains and diversification.

• Reduced capex is likely to reduce supply growth in fields outside of US.

• Markets likely to be more balanced and OPEC could once again regain its position as the marginal producer

HOT MONEY NET FLOWS

4/13/2015 22

23

Hot money net flows

Speculative length has increased in Brent since February.

After cutting bullish positions for WTI, thanks to rising inventoriess in the US, net long positions have once again increased for the light crude contract.

4/13/2015 23

-20000

30000

80000

130000

180000

230000

280000

-20000

30000

80000

130000

180000

230000

280000

01Dec14 23Dec14 14Jan15 05Feb15 27Feb15 21Mar15

Total net-long non commercials

WTI (incl. other reportables)

Brent (incl. other reportables)

Managed Money (WTI net-long)

Managed Money (Brent net-long)

Sources: Natixis, CFTC

4/13/2015

24

Analyst Biography

Dr Abhishek Deshpande leads the oil and oil products research at Natixis, providing oil

strategies, price forecasts and analysis of developments across the global oil and oil product

markets. Abhishek has a doctorate in Chemical Engineering from Cambridge University and

holds Chartered Engineer status with the Institute of Engineers, UK. While pursuing his

degree, he spent time working for Indian Oil Corporation Limited.

Abhishek has appeared on BBC, CNBC, Bloomberg TV, presented at Oil & Gas

conferences and is quoted regularly by financial media globally. He has also published

articles in financial journals such as Petroleum Economics and O&G Journal. He is invited

regularly to talk at international conferences.

24 4/13/2015

This document shall only intended to eligible counterparties or professional clients or qualified investors or any similar status in another state or jurisdiction. This document is a commercial documentation for discussion and information purposes only. It is highly confidential and it is the property of Natixis. It should not be transmitted to any person other than the original addressee(s) without the prior written consent of Natixis. This document does not constitute a personalized recommendation. It is intended for general distribution and the products or services described herein do not take into account any specific investment objective, financial situation or particular need of any recipient. The distribution, possession or delivery of this document in, to or from certain jurisdictions may be restricted or prohibited by law. Recipients of this document are therefore required to ensure that they are aware of, and comply with, such restrictions or prohibitions. Neither Natixis, nor any of its affiliates, directors, employees, agents or advisers nor any other person accept any liability to anyone in relation to the distribution, possession or delivery of this document in, to or from any jurisdiction. In any event, you should request for any internal and/or external advice that you consider necessary or desirable to obtain, including any financial, legal, tax or accounting advice, or any other specialist advice, in order to verify in particular that the investment(s), transaction(s), structure or arrangement described in this document meets your investment or financial objectives and constraints, and to obtain an independent valuation of such investment(s)/transaction(s), its risks factors and rewards. It should not be assumed that the information contained in this document will have been updated subsequent to the date stated on the front page of this document. In addition, the delivery of this document does not imply in any way an obligation on anyone to update the information contained herein at any time. This document should not be construed as an offer or solicitation with respect to the purchase, sale or subscription of any interest or security or as an undertaking by Natixis to complete a transaction subject to the terms and conditions described in this document or any other terms and conditions. Any guarantee, funding, interest or currency swap, underwriting or more generally any undertaking provided for in this document should be treated as preliminary only and is subject to a formal approval and written confirmation in accordance with Natixis’ current internal procedures. Natixis has neither verified nor independently analysed the information contained in this document. Accordingly, no representation, warranty or undertaking, express or implied, is made to recipients as to or in relation to the accuracy or completeness or otherwise of this document or as to the reasonableness of any assumption contained in this document. The information contained in this document does not take into account specific tax rules or accounting methods applicable to counterparties, clients or potential clients of Natixis. Therefore, Natixis shall not be liable for differences, if any, between its own valuations and those valuations provided by third parties; as such differences may arise as a result of the application and implementation of alternative accounting methods, tax rules or valuation models. Natixis shall not be liable for any financial loss or any decision taken on the basis of the information contained in this document and Natixis does not hold itself out as providing any advice, particularly in relation to investment services. Prices and margins are deemed to be indicative only and are subject to changes at any time depending on, inter alia, market conditions. Past performance and simulations of past performance are not a reliable indicator and therefore do not predict future results. The information contained in this document may include results of analyses from a quantitative model, which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Information may be changed or withdrawn by Natixis at any time without notice. More generally, no responsibility is accepted by Natixis, nor by any of its holding companies, subsidiaries, associated undertakings or controlling persons, or any of their respective directors, officers, partners, employees, agents, representatives or advisors as to or in relation to the characteristics of this information.This document is based on public information. It should not be construed as an offer or solicitation with respect to the purchase, sale or subscription of any interest or security or as an undertaking by Natixis to complete a transaction subject to the terms and conditions described in this document or any other terms and conditions. Any undertaking provided for in this document should be treated as preliminary only and is subject to a formal approval and written confirmation by Natixis in accordance to its current internal procedures. The statements, assumptions contained in this document may be forward-looking and are therefore subject to risks and uncertainties. Actual results and developments may differ materially from those expressed or implied, depending on a variety of factors and accordingly there can be no guarantee of the projected results, projections or developments. Natixis makes no representation or warranty, expressed or implied, as to the accomplishment of or reasonableness of, nor should any reliance be placed on any projections, targets, estimates or forecasts, or on the statements, assumptions and opinions expressed in this document. Nothing in this document should be relied on as a promise or guarantee as to the future. Natixis, as part of its activities, may deal as principal in or own securities/instruments or other investments that may be the subject of opinions or recommendation discussed in this document or may advise the issuers of such securities. Natixis and its holding entities, affiliates, employees or clients may have interest or possess or acquire information in any products, markets, indices or securities mentioned in this document that could be material and/or could give rise to a conflict of interest or potential conflict of interest. This may involve activities such as dealing in, holding, acting as market makers, or performing financial or advisory services in relation to any products, markets, indices or securities mentioned in this document. Natixis is authorized in France by the Autorite de Controle Prudentiel et de Résolution (ACPR) as a Bank – Investment Services Provider and subject to its supervision. Natixis is regulated by the AMF in respect of its investment services activities. In the UK: Natixis is authorised by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and subject to limited regulation by the Financial Conduct Authority and Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and Prudential Regulation Authority are available from us on request NATIXIS is regulated by the BaFin (Bundesanstalt für Finanzdienstleistungsaufsicht) for the conduct of investment business in Germany. The transfer / distribution of this document in Germany is done by / under the responsibility of NATIXIS Zweigniederlassung Deutschland. Natixis is authorized by the ACPR and regulated by Bank of Spain and the CNMV (Comisión Nacional de Mercado de Valores) for the conduct of its business under the right of establishment in Spain. Natixis is authorised by the ACPR and regulated by Bank of Italy and the CONSOB (Commissione Nazionale per le Società e la Borsa) for the conduct of its business in Italy. Natixis is regulated throughout the European Union on a crossborder basis. Natixis is authorized by the ACPR and regulated by the Dubai Financial Services Authority (DFSA) for the conduct of its business in and from the Dubai International Financial Centre (DIFC). The document is being made available to the recipient with the understanding that it meets the DFSA definition of a Professional Client; the recipient is otherwise required to inform Natixis if this is not the case and return the document. The recipient also acknowledges and understands that neither the document nor its contents have been approved, licensed by or registered with any regulatory body or governmental agency in the GCC or Lebanon. This document is not intended for distribution in the United States or to any US person, or in Canada, Australia, the Republic of South Africa or Japan

25

Disclaimer

4/13/2015 25