session fsa

TRANSCRIPT

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 1/30

Financial Statement Analysis

Session Three

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 2/30

1–2

Introduction

• The financial health of a company can be assessedfrom two viewpoints:

– its financial statements, giving its financial position, its

operating results, and net cash flows

– capital market response to firm performance

• The basic purpose of providing two-year information

(current year and previous year) in financial

statements is to facilitate comparison

• However, simple comparison of absolute numbers in

the financial statements does not offer much insight

due to size disparity, accounting policy changes etc.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 3/30

1–3

Relation and Comparison of Data

• Accounting data in absolute terms do not provide muchmeaning – their analysis involves comparison andrelation

• Ratio analysis - Whenever one item is expressed (as afraction or a decimal fraction or an integer) in terms of

another item• Example – A firm earns a net profit of Rs. 20,000 on a

sale of Rs. 500,000. We could express this relationshipin terms of sales margin of 4%

• Comparisons could be made– With Company’s past performance– With Competing Firms– With Industry/Economy trend– With Budgets (Planning and Control)

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 4/30

1–4

Fund Flow Analysis

• Where Got Where Gone Statement

• Sources of Funds = Uses of Funds

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 5/30

1–5

Financial Ratios

• Financial ratio represents a relative measurewhere both the numerator and thedenominator are financial numbers.

• There are three class of financial ratios:

– Balance Sheet Ratio• Where both the variables are taken from the Balance

Sheet.

– Profit and Loss Ratio

• Where both the variables are taken from Profit and Loss Account.

– Mixed Ratio

• Where one variable is taken from Balance Sheet and the other from Profit and Loss Account.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 6/30

1–6

Liquidity

Efficiency

Leverage

ProfitabilityShareholders’value

Performance Analysis: Four window approach

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 7/301–7

Liquidity Ratios

• These ratios indicate the ability of the firmto meet its short-term obligations (e.g.,payment of salary, taxes, loans etc.)

• The timeframe for the expression “short-

term” is generally twelve months.• The challenge for any treasury manager is

to manage the cash flow leads and lags.

• Liquidity management essentially involveconstant monitoring of cash flow position.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 8/301–8

Liquidity Ratios

• Current RatioCurrent Assets

Current Liabilities

• Quick Ratio

Current Assets – Inventory

Current Liabilities

• Financial Slack

Cash & Bank balances *100

Total Assets

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 9/301–9

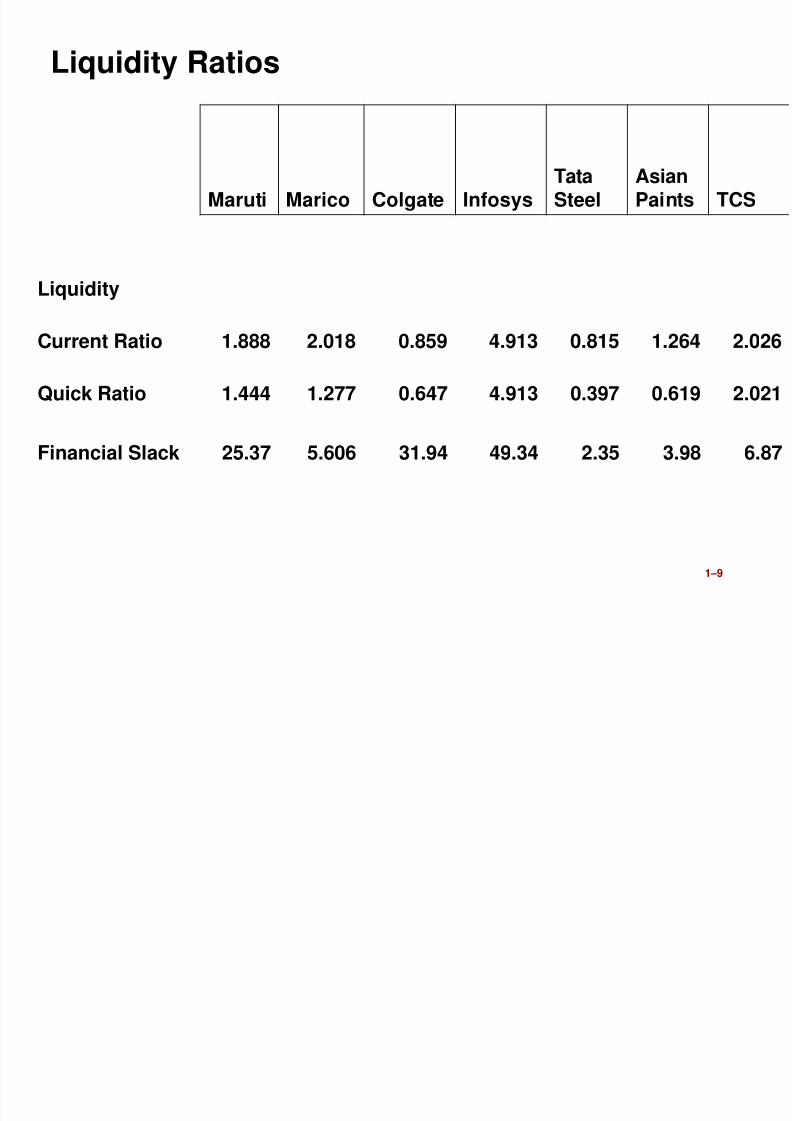

Maruti Marico Colgate InfosysTataSteel

AsianPaints TCS

Liquidity

Current Ratio 1.888 2.018 0.859 4.913 0.815 1.264 2.026

Quick Ratio 1.444 1.277 0.647 4.913 0.397 0.619 2.021

Financial Slack 25.37 5.606 31.94 49.34 2.35 3.98 6.87

Liquidity Ratios

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 10/301–10

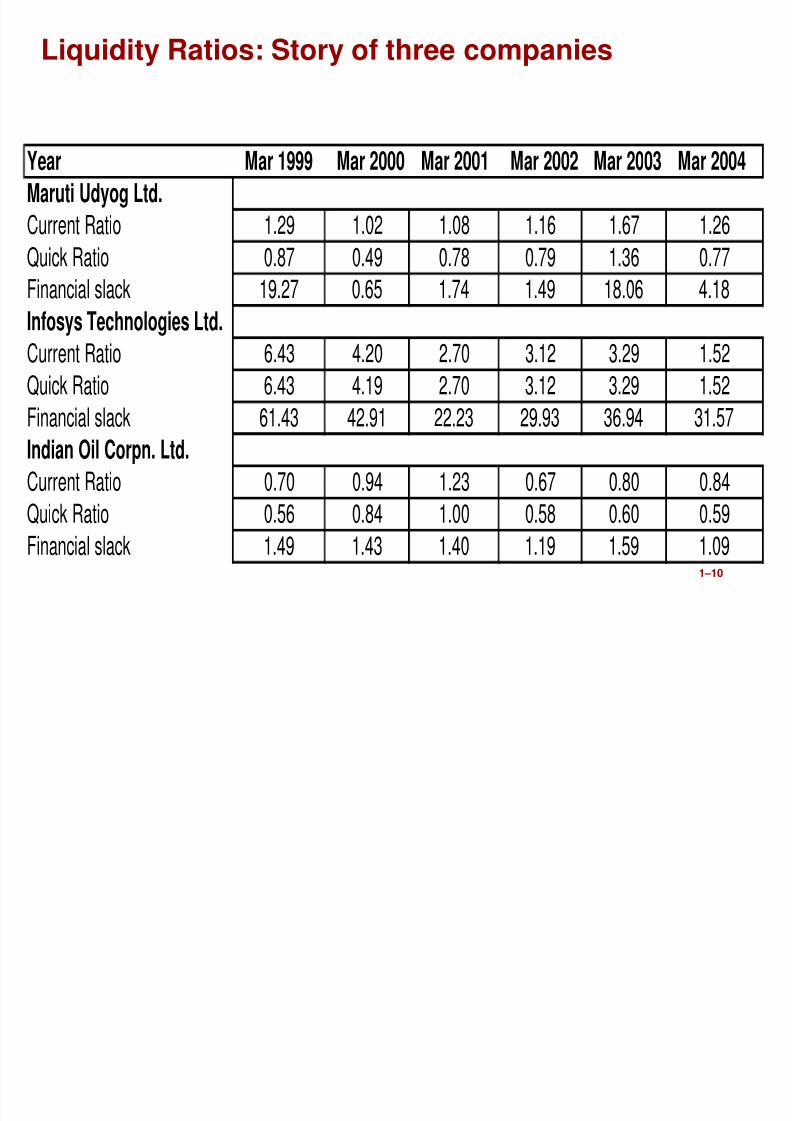

Liquidity Ratios: Story of three companies

Year Mar 1999 Mar 2000 Mar 2001 Mar 2002 Mar 2003 Mar 2004

Maruti Udyog Ltd.

Current Ratio 1.29 1.02 1.08 1.16 1.67 1.26

Quick Ratio 0.87 0.49 0.78 0.79 1.36 0.77

Financial slack 19.27 0.65 1.74 1.49 18.06 4.18

Infosys Technologies Ltd.

Current Ratio 6.43 4.20 2.70 3.12 3.29 1.52

Quick Ratio 6.43 4.19 2.70 3.12 3.29 1.52

Financial slack 61.43 42.91 22.23 29.93 36.94 31.57Indian Oil Corpn. Ltd.

Current Ratio 0.70 0.94 1.23 0.67 0.80 0.84

Quick Ratio 0.56 0.84 1.00 0.58 0.60 0.59

Financial slack 1.49 1.43 1.40 1.19 1.59 1.09

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 11/301–11

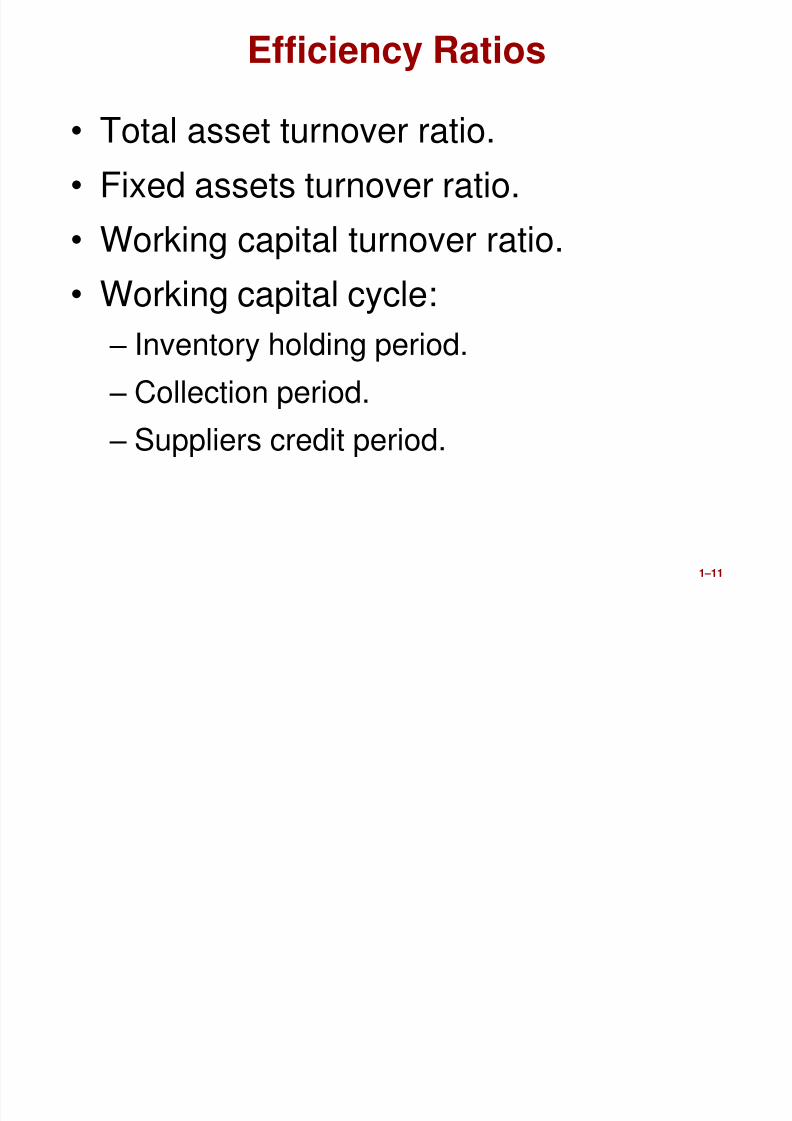

Efficiency Ratios

• Total asset turnover ratio.• Fixed assets turnover ratio.

• Working capital turnover ratio.

• Working capital cycle:

– Inventory holding period.

– Collection period.

– Suppliers credit period.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 12/301–12

Overall Efficiency Sales/Capital Employed

Fixed Assets Efficiency

(or Turnover) Ratio

Sales/(Net Block + Capital WIP)

Working Capital

Efficiency(Turnover)

Sales/ Working Capital

Inventory Turnover Cost of Goods Sold / Average Inventory

Debtors Turnover Credit Sales / (Average Debtors + Average Bills Receivable)

Creditors Turnover Credit Purchase / (Average Creditors + Average Bills Payable)

Average Inventory

Inventory Holding

Period

(Average Inventory/Cost of Goods Sold) x No. of Days/Months in a

Year

Debtors CollectionPeriod

((Average Debtors + Average Bills Receivables)/ Credit Sales) x No. of Days/Months in a Year

Suppliers Credit Period ((Average Creditors + Average Bills Payable)/ Credit Purchases) x No.

of Days/months in a year

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 13/301–13

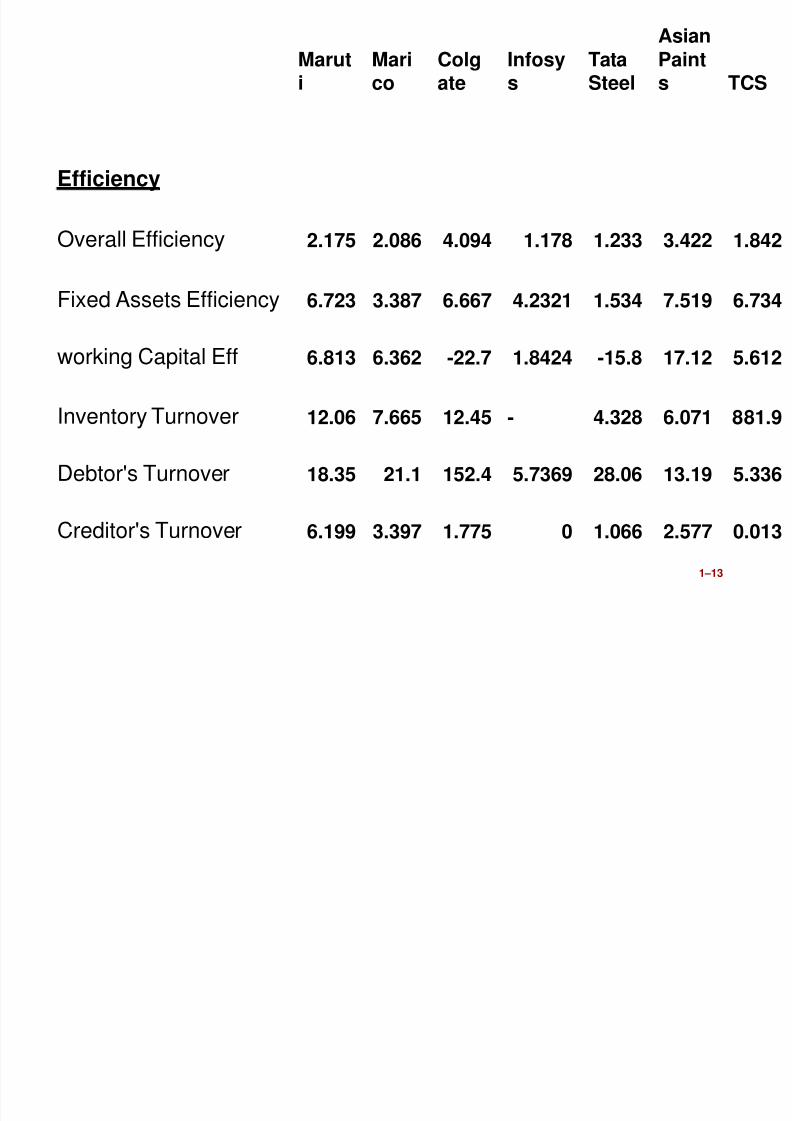

Maruti

Marico

Colgate

Infosys

TataSteel

AsianPaints TCS

Efficiency

Overall Efficiency 2.175 2.086 4.094 1.178 1.233 3.422 1.842

Fixed Assets Efficiency 6.723 3.387 6.667 4.2321 1.534 7.519 6.734

working Capital Eff 6.813 6.362 -22.7 1.8424 -15.8 17.12 5.612

Inventory Turnover 12.06 7.665 12.45 - 4.328 6.071 881.9

Debtor's Turnover 18.35 21.1 152.4 5.7369 28.06 13.19 5.336

Creditor's Turnover 6.199 3.397 1.775 0 1.066 2.577 0.013

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 14/301–14

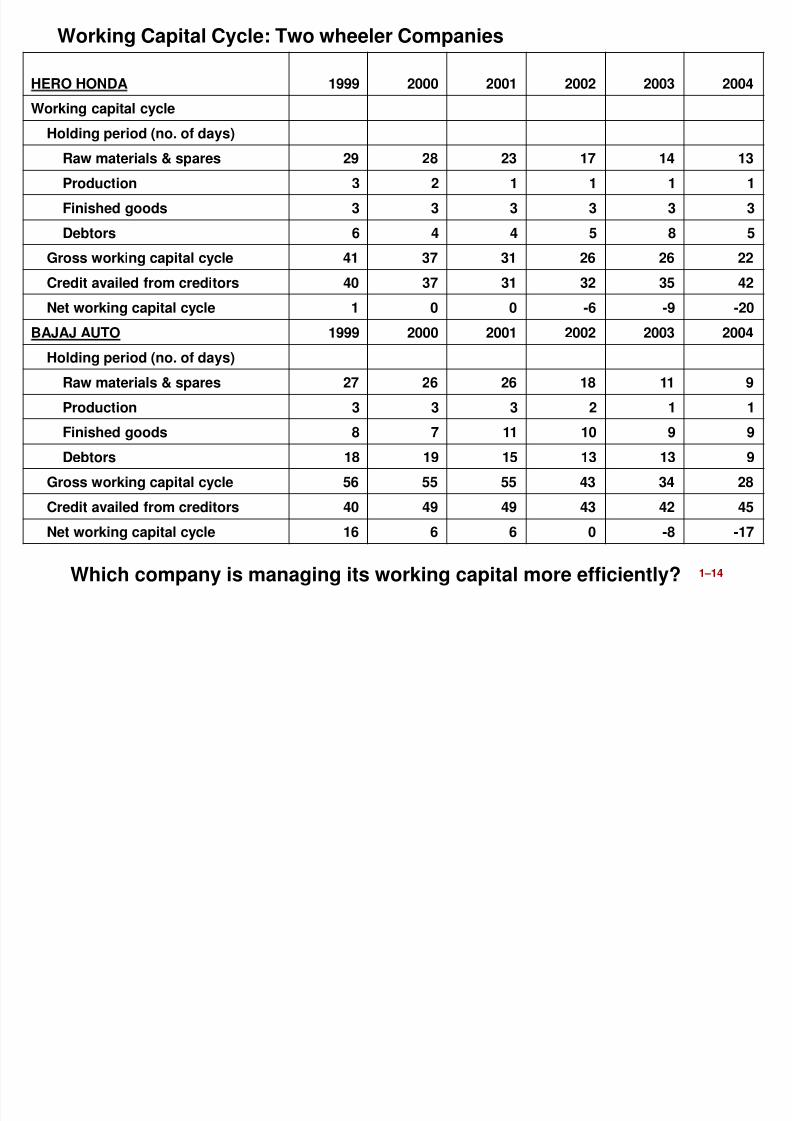

HERO HONDA 1999 2000 2001 2002 2003 2004

Working capital cycle

Holding period (no. of days)Raw materials & spares 29 28 23 17 14 13

Production 3 2 1 1 1 1

Finished goods 3 3 3 3 3 3

Debtors 6 4 4 5 8 5

Gross working capital cycle 41 37 31 26 26 22

Credit availed from creditors 40 37 31 32 35 42

Net working capital cycle 1 0 0 -6 -9 -20

BAJAJ AUTO 1999 2000 2001 2002 2003 2004

Holding period (no. of days)

Raw materials & spares 27 26 26 18 11 9

Production 3 3 3 2 1 1

Finished goods 8 7 11 10 9 9

Debtors 18 19 15 13 13 9

Gross working capital cycle 56 55 55 43 34 28

Credit availed from creditors 40 49 49 43 42 45

Net working capital cycle 16 6 6 0 -8 -17

Working Capital Cycle: Two wheeler Companies

Which company is managing its working capital more efficiently?

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 15/30

15

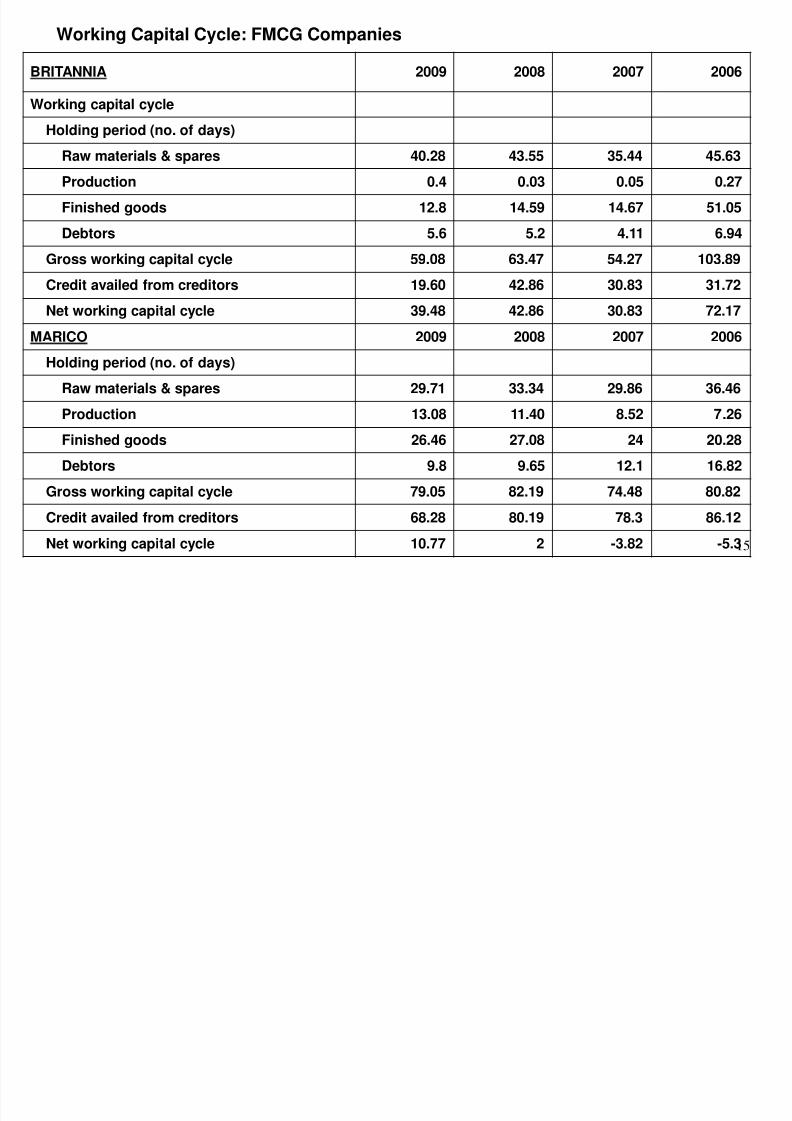

BRITANNIA 2009 2008 2007 2006

Working capital cycle

Holding period (no. of days)

Raw materials & spares 40.28 43.55 35.44 45.63

Production 0.4 0.03 0.05 0.27

Finished goods 12.8 14.59 14.67 51.05

Debtors 5.6 5.2 4.11 6.94

Gross working capital cycle 59.08 63.47 54.27 103.89

Credit availed from creditors 19.60 42.86 30.83 31.72

Net working capital cycle 39.48 42.86 30.83 72.17

MARICO 2009 2008 2007 2006

Holding period (no. of days)

Raw materials & spares 29.71 33.34 29.86 36.46

Production 13.08 11.40 8.52 7.26

Finished goods 26.46 27.08 24 20.28

Debtors 9.8 9.65 12.1 16.82

Gross working capital cycle 79.05 82.19 74.48 80.82

Credit availed from creditors 68.28 80.19 78.3 86.12

Net working capital cycle 10.77 2 -3.82 -5.3

Working Capital Cycle: FMCG Companies

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 16/30

1–16

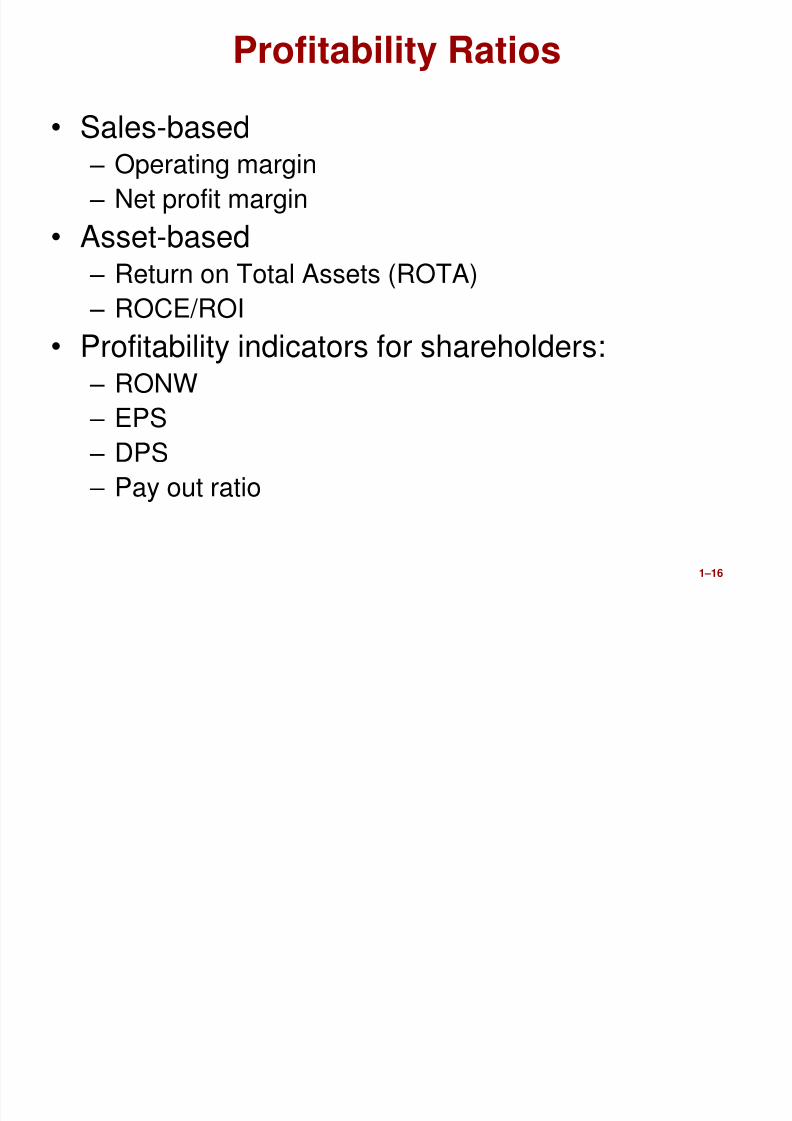

Profitability Ratios

• Sales-based– Operating margin

– Net profit margin

• Asset-based

– Return on Total Assets (ROTA)– ROCE/ROI

• Profitability indicators for shareholders:– RONW

– EPS– DPS

– Pay out ratio

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 17/30

1–17

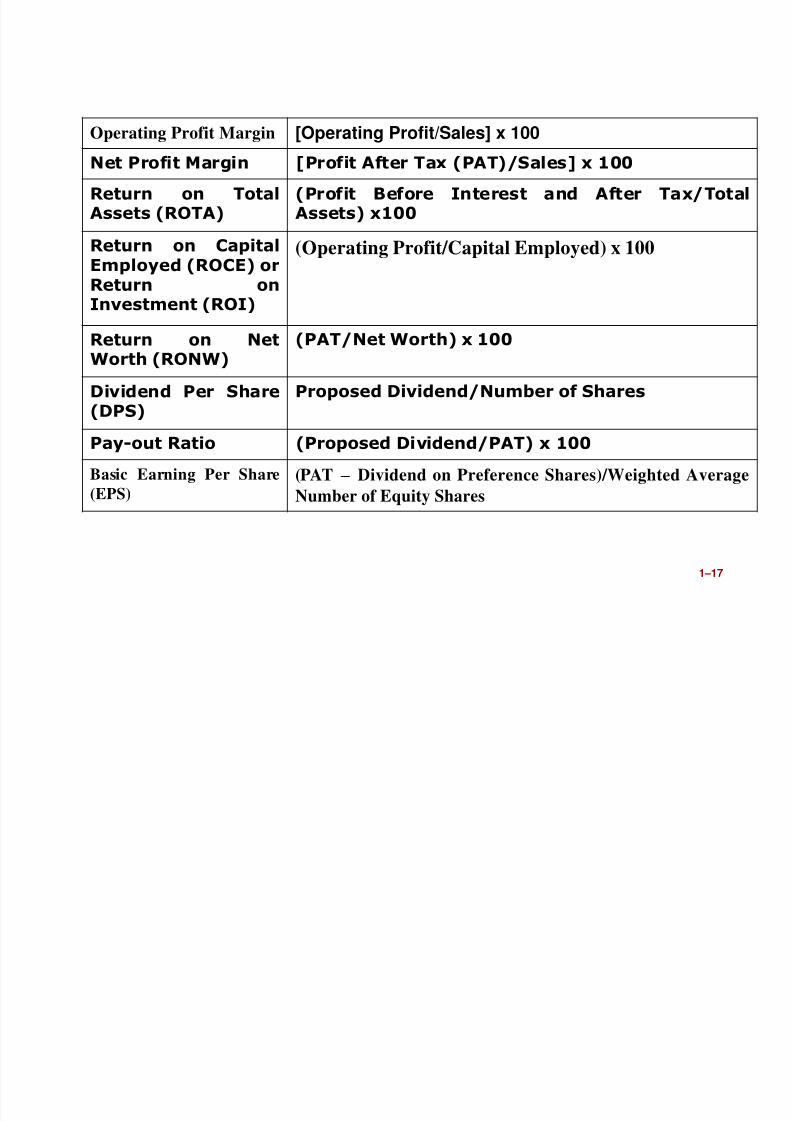

Operating Profit Margin [Operating Profit/Sales] x 100Net Profit Margin [Profit After Tax (PAT)/Sales] x 100

Return on TotalAssets (ROTA)

(Profit Before Interest and After Tax/TotalAssets) x100

Return on CapitalEmployed (ROCE) or

Return onInvestment (ROI)

(Operating Profit/Capital Employed) x 100

Return on NetWorth (RONW)

(PAT/Net Worth) x 100

Dividend Per Share

(DPS)

Proposed Dividend/Number of Shares

Pay-out Ratio (Proposed Dividend/PAT) x 100

Basic Earning Per Share

(EPS)

(PAT – Dividend on Preference Shares)/Weighted Average

Number of Equity Shares

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 18/30

1–18

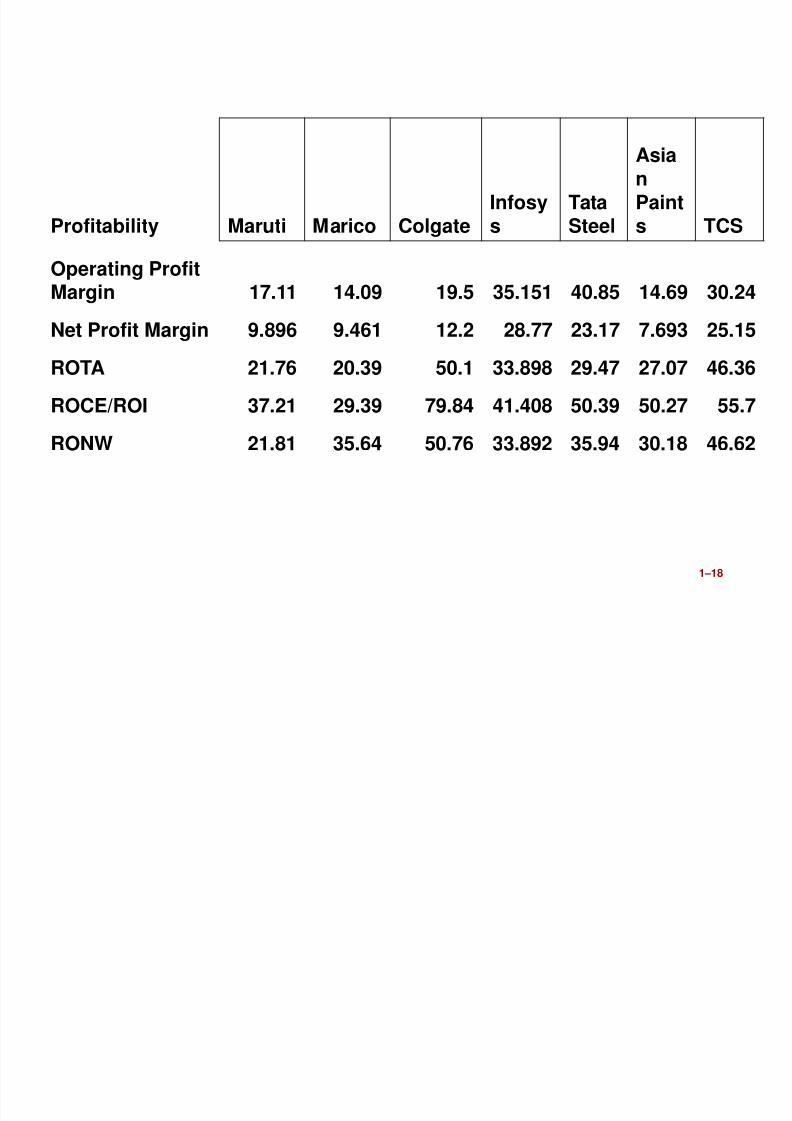

Profitability Maruti Marico ColgateInfosys

TataSteel

AsianPaints TCS

Operating ProfitMargin 17.11 14.09 19.5 35.151 40.85 14.69 30.24

Net Profit Margin 9.896 9.461 12.2 28.77 23.17 7.693 25.15

ROTA 21.76 20.39 50.1 33.898 29.47 27.07 46.36

ROCE/ROI 37.21 29.39 79.84 41.408 50.39 50.27 55.7

RONW 21.81 35.64 50.76 33.892 35.94 30.18 46.62

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 19/30

1–19

Capital Structure (or Long-term solvency)

• Debt-equity ratio.

• Interest coverage ratio.• Debt service coverage ratio.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 20/30

1–20

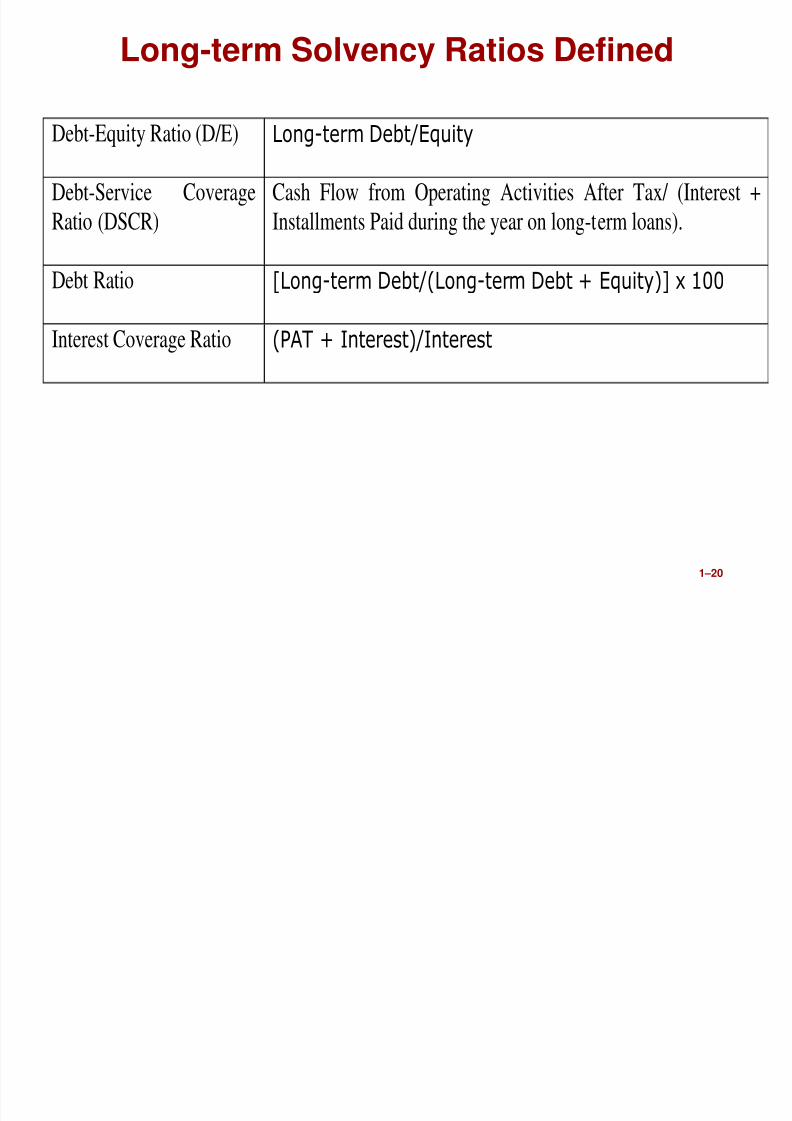

Long-term Solvency Ratios Defined

Debt-Equity Ratio (D/E) Long-term Debt/Equity

Debt-Service Coverage

Ratio (DSCR)

Cash Flow from Operating Activities After Tax/ (Interest +

Installments Paid during the year on long-term loans).

Debt Ratio [Long-term Debt/(Long-term Debt + Equity)] x 100

Interest Coverage Ratio (PAT + Interest)/Interest

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 21/30

1–21

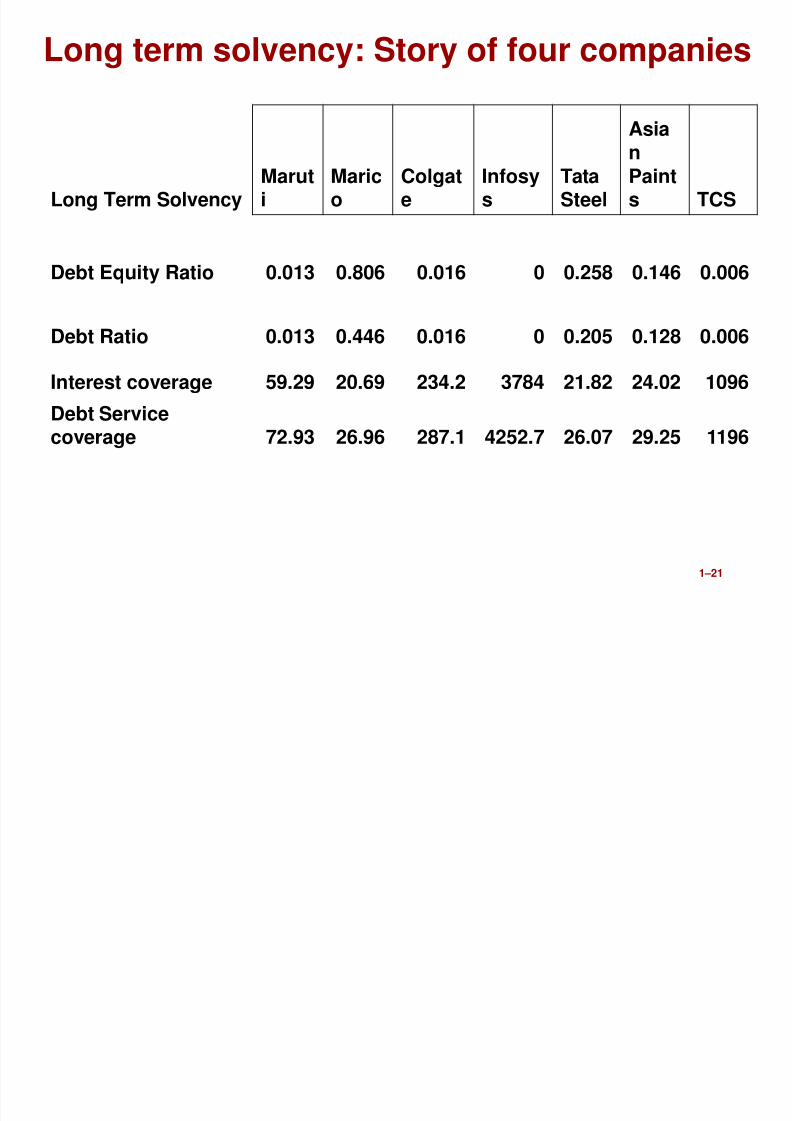

Long term solvency: Story of four companies

Long Term SolvencyMaruti

Marico

Colgate

Infosys

TataSteel

AsianPaints TCS

Debt Equity Ratio 0.013 0.806 0.016 0 0.258 0.146 0.006

Debt Ratio 0.013 0.446 0.016 0 0.205 0.128 0.006

Interest coverage 59.29 20.69 234.2 3784 21.82 24.02 1096

Debt Servicecoverage 72.93 26.96 287.1 4252.7 26.07 29.25 1196

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 22/30

1–22

Market-based ratios

• Price-earning (P/E) multiple.• Price-to-book ratio.

• Dividend yield.

• Total shareholder return (TSR)

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 23/30

1–23

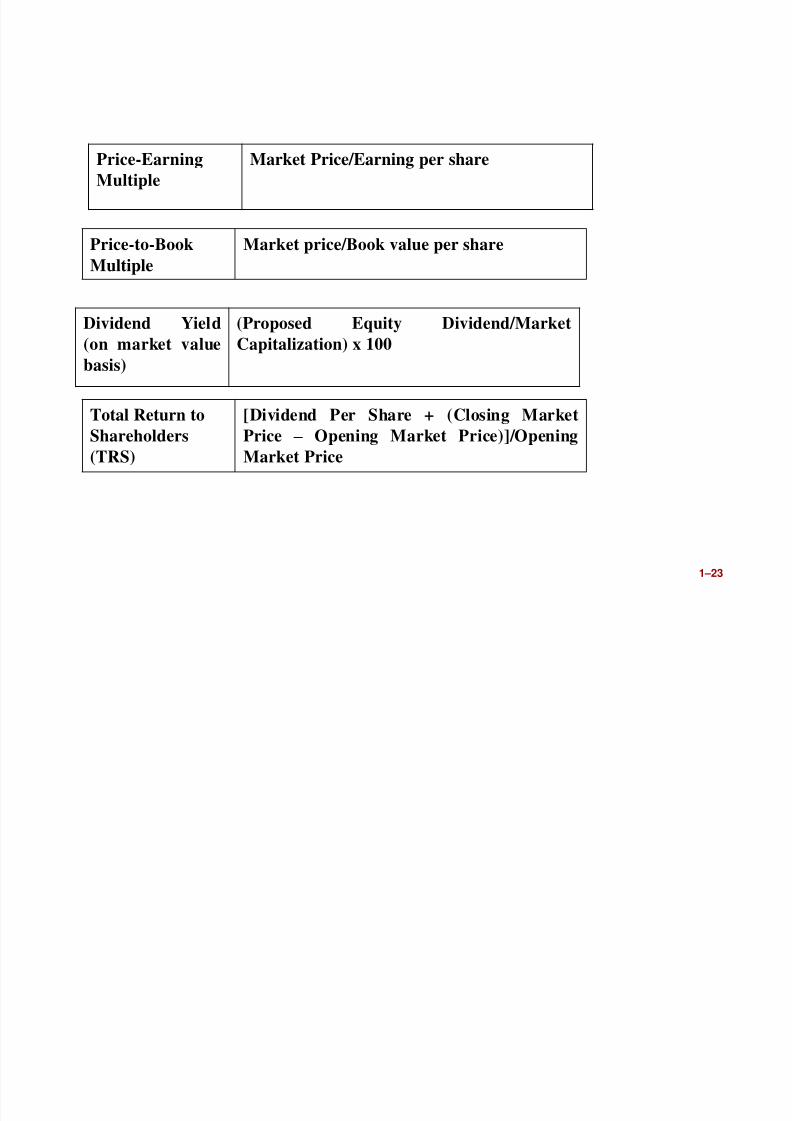

Dividend Yield

(on market value

basis)

(Proposed Equity Dividend/Market

Capitalization) x 100

Total Return toShareholders

(TRS)

[Dividend Per Share + (Closing MarketPrice – Opening Market Price)]/Opening

Market Price

Price-Earning

Multiple

Market Price/Earning per share

Price-to-Book

Multiple

Market price/Book value per share

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 24/30

1–24

Limitations of FinancialRatio Analysis

• Financial ratio analysis, however, hassome limitations:

– Comparing an organization that is in asingle line of business with an organization

that is a competitor but has multiple lines ofbusiness is likely to be a meaninglesscomparison of unlike organizations

– Even though organizations might be

comparable because they are in similarlines of business, they may use differentaccounting conventions making ratiocomparisons between the two

organizations meaningless

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 25/30

1–25

Intra-firm and Inter-firm analyses

• When the performance of a particularfirm is evaluated over a time period, it isknown as intra-firm analysis.

• When the performance of cross sectionof firms within the same industry areevaluated for a particular year or over aperiod of time, it is known as inter-firmanalysis.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 26/30

1–26

Time series and Cross sectional analyses

• The performance of a particular firmmay be observed over a time period byfollowing the trend of financial ratios.Such analysis of performance is known

as time series analysis.• When performance of cross section of

firms in the same industry is analysed

for a particular year, such analysis iscalled cross sectional analysis.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 27/30

1–27

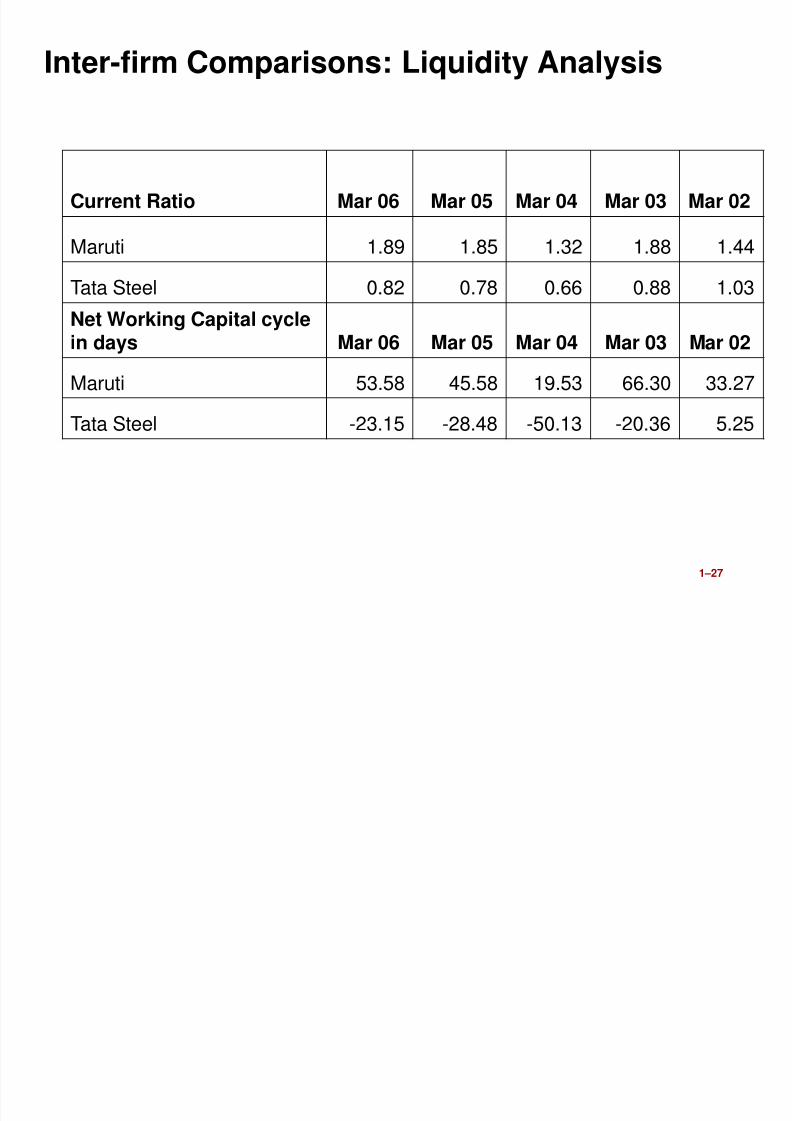

Inter-firm Comparisons: Liquidity Analysis

Current Ratio Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Maruti 1.89 1.85 1.32 1.88 1.44

Tata Steel 0.82 0.78 0.66 0.88 1.03

Net Working Capital cyclein days Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Maruti 53.58 45.58 19.53 66.30 33.27

Tata Steel -23.15 -28.48 -50.13 -20.36 5.25

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 28/30

1–28

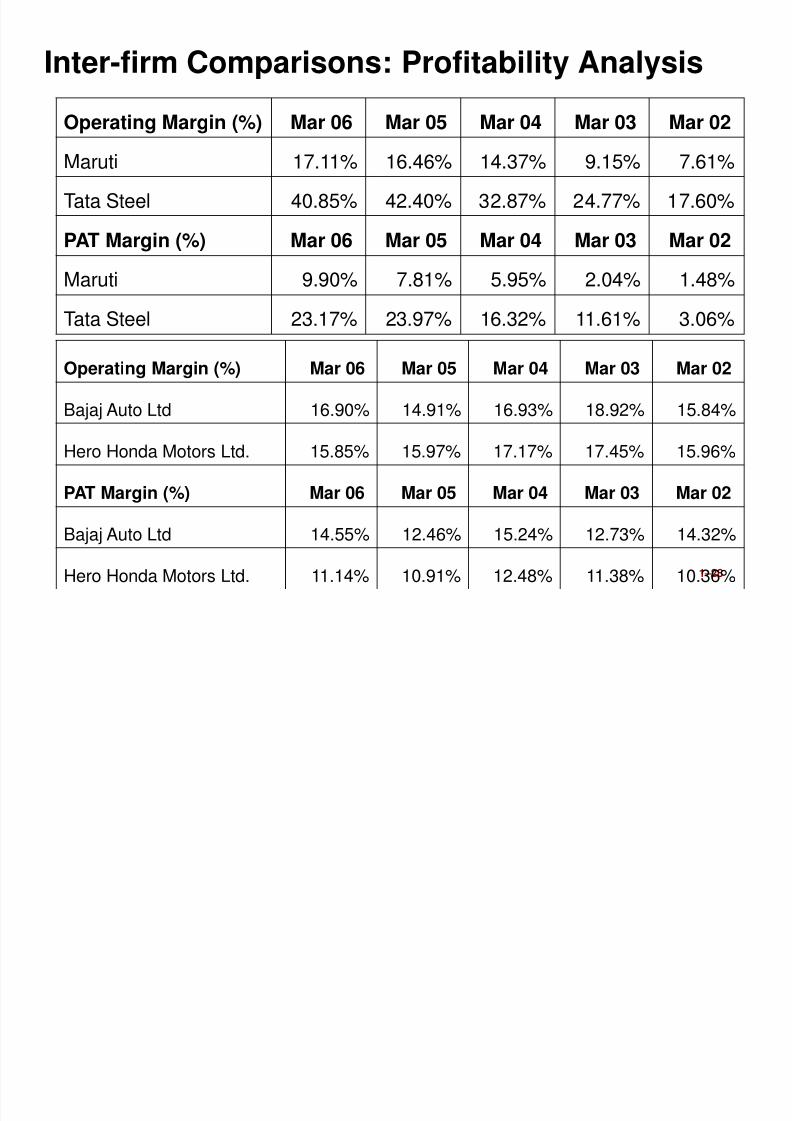

Inter-firm Comparisons: Profitability Analysis

Operating Margin (%) Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Maruti 17.11% 16.46% 14.37% 9.15% 7.61%

Tata Steel 40.85% 42.40% 32.87% 24.77% 17.60%

PAT Margin (%) Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Maruti 9.90% 7.81% 5.95% 2.04% 1.48%

Tata Steel 23.17% 23.97% 16.32% 11.61% 3.06%

Operating Margin (%) Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Bajaj Auto Ltd 16.90% 14.91% 16.93% 18.92% 15.84%

Hero Honda Motors Ltd. 15.85% 15.97% 17.17% 17.45% 15.96%

PAT Margin (%) Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Bajaj Auto Ltd 14.55% 12.46% 15.24% 12.73% 14.32%

Hero Honda Motors Ltd. 11.14% 10.91% 12.48% 11.38% 10.36%

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 29/30

1–29

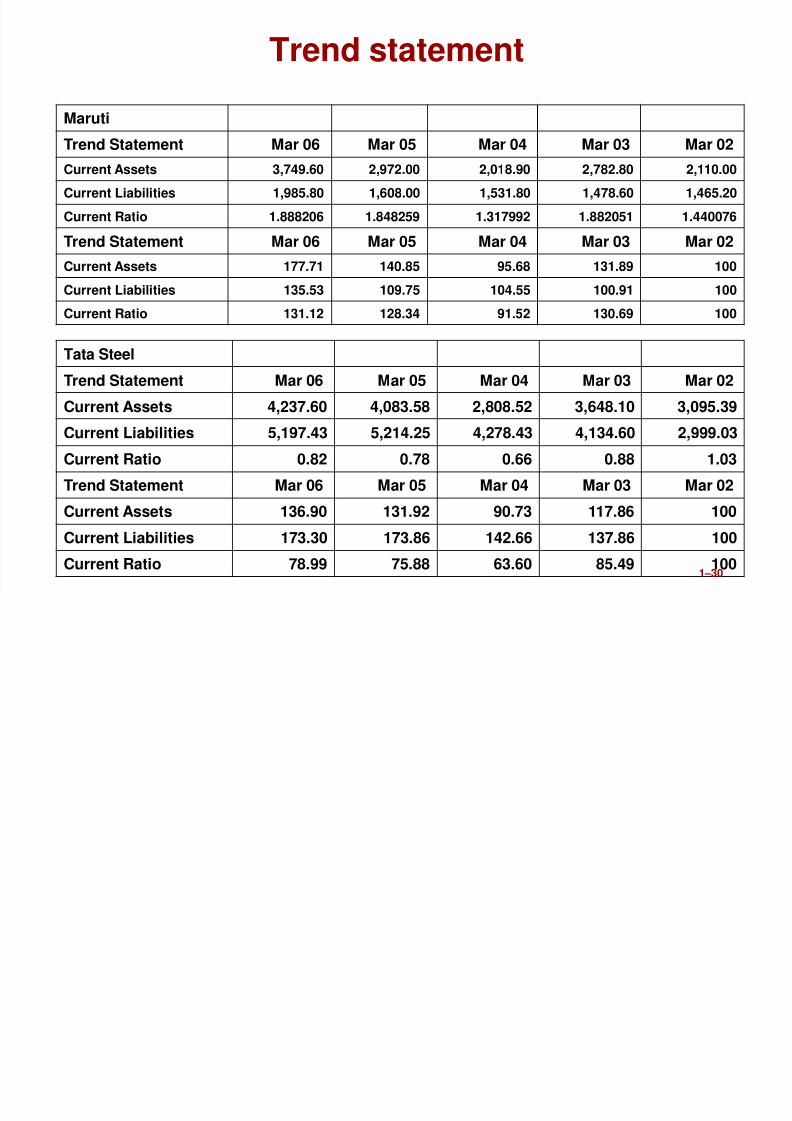

Trend Analysis

• Consider the first year of the time periodas the base year.

• The variables (e.g., ratios) in the first

year are considered as 100 andvariables of all the subsequent yearsare expressed as percentages of thebase year.

• This gives a trend line for each variable.

8/7/2019 Session FSA

http://slidepdf.com/reader/full/session-fsa 30/30

Trend statement

Maruti

Trend Statement Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Current Assets 3,749.60 2,972.00 2,018.90 2,782.80 2,110.00

Current Liabilities 1,985.80 1,608.00 1,531.80 1,478.60 1,465.20

Current Ratio 1.888206 1.848259 1.317992 1.882051 1.440076

Trend Statement Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Current Assets 177.71 140.85 95.68 131.89 100

Current Liabilities 135.53 109.75 104.55 100.91 100

Current Ratio 131.12 128.34 91.52 130.69 100

Tata Steel

Trend Statement Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Current Assets 4,237.60 4,083.58 2,808.52 3,648.10 3,095.39

Current Liabilities 5,197.43 5,214.25 4,278.43 4,134.60 2,999.03

Current Ratio 0.82 0.78 0.66 0.88 1.03

Trend Statement Mar 06 Mar 05 Mar 04 Mar 03 Mar 02

Current Assets 136.90 131.92 90.73 117.86 100

Current Liabilities 173.30 173.86 142.66 137.86 100

Current Ratio 78.99 75.88 63.60 85.49 100