session 46 panel discussion, mortality table update … 46 pd, mortality table update on the 2015...

TRANSCRIPT

Session 46 PD, Mortality Table Update on the 2015 VBT/CSO

Moderator:

Mary J. Bahna‐Nolan, FSA, CERA, MAAA

Presenters: Mary J. Bahna‐Nolan, FSA, CERA, MAAA Dieter S. Gaubatz, FSA, FCIA, MAAA

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

Joint American Academy of Actuaries Life Experience Committee and Society of Actuaries Preferred Mortality Oversight Group

Session 46, SOA Annual MeetingOctober 12, 2015

Austin, Texas

Mortality Table Update on the 2015 VBT/CSO

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 2

Agenda & Presenters

AgendaMary J. Bahna-Nolan, FSA, MAAA, CERAChair, Joint American Academy of Actuaries

Life Experience Committee and Society of Actuaries Preferred Mortality Oversight Group

Dieter Gaubatz, FSA, FCIA, MAAAChair, Underwriting Criteria Team

Presenters

2015 VBT 2015 VBT Relative Risk

Tables 2017 CSO 2017 CSO Preferred Structure

Tables Underwriting Criteria Scoring

Tool (UCS)

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 3

Mortality Development

Significant work completed to develop various mortality tables and margins to support PBR and new valuation table

Series of presentations on the various table development and impacts from prior tables via NAIC National Meetings and can be found on NAIC website VBT: Summer and Fall 2014 meetings CSO: Fall 2014 and Spring 2015 meetings UCS: Conference calls Summer 2015

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 4

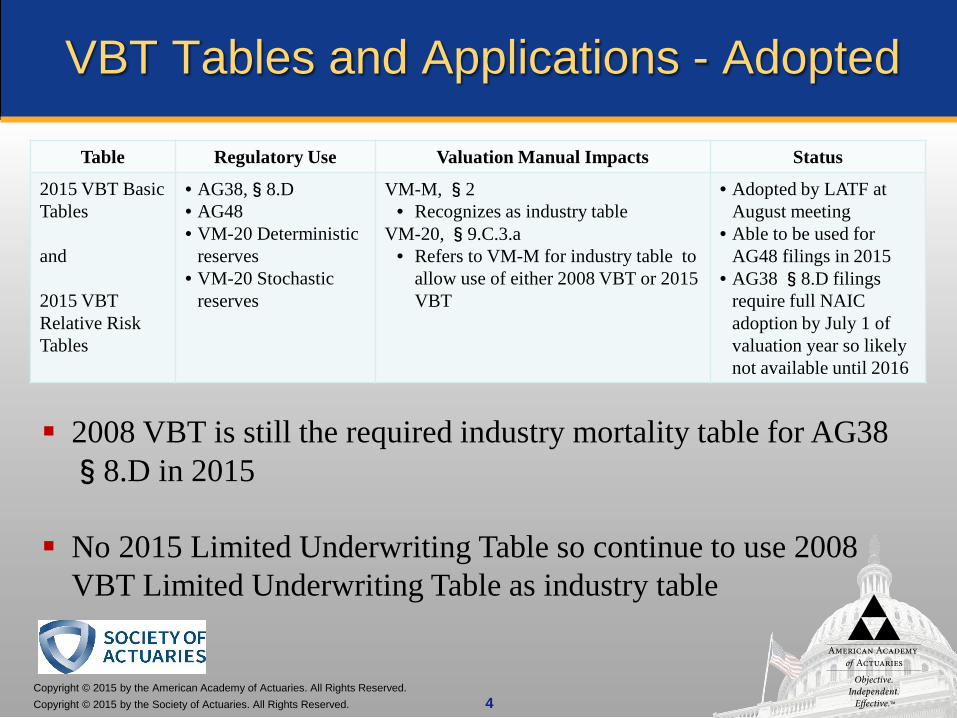

VBT Tables and Applications - Adopted

Table Regulatory Use Valuation Manual Impacts Status

2015 VBT BasicTables

and

2015 VBT Relative Risk Tables

• AG38,§8.D• AG48• VM-20 Deterministic

reserves• VM-20 Stochastic

reserves

VM-M, §2• Recognizes as industry table

VM-20, §9.C.3.a• Refers to VM-M for industry table to

allow use of either 2008 VBT or 2015 VBT

• Adopted by LATF at August meeting

• Able to be used for AG48 filings in 2015

• AG38 §8.D filings require full NAIC adoption by July 1 of valuation year so likely not available until 2016

2008 VBT is still the required industry mortality table for AG38 §8.D in 2015

No 2015 Limited Underwriting Table so continue to use 2008 VBT Limited Underwriting Table as industry table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

2015 VBT DevelopmentMary Bahna-Nolan

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 6

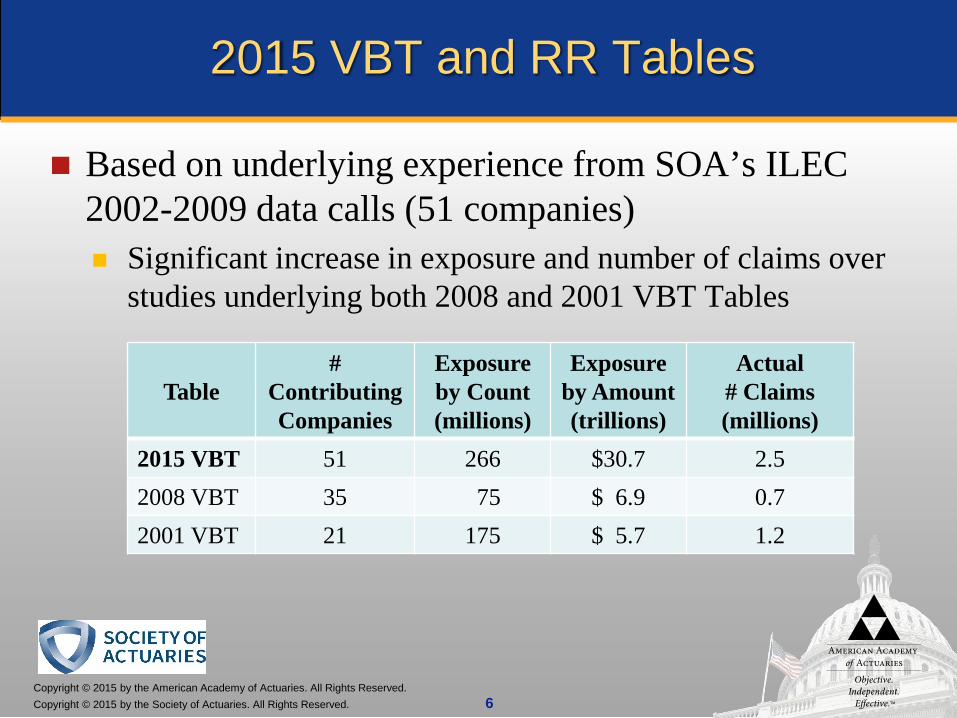

2015 VBT and RR Tables

Based on underlying experience from SOA’s ILEC 2002-2009 data calls (51 companies) Significant increase in exposure and number of claims over

studies underlying both 2008 and 2001 VBT Tables

Table#

Contributing Companies

Exposure by Count(millions)

Exposure by Amount(trillions)

Actual# Claims(millions)

2015 VBT 51 266 $30.7 2.52008 VBT 35 75 $ 6.9 0.72001 VBT 21 175 $ 5.7 1.2

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 7

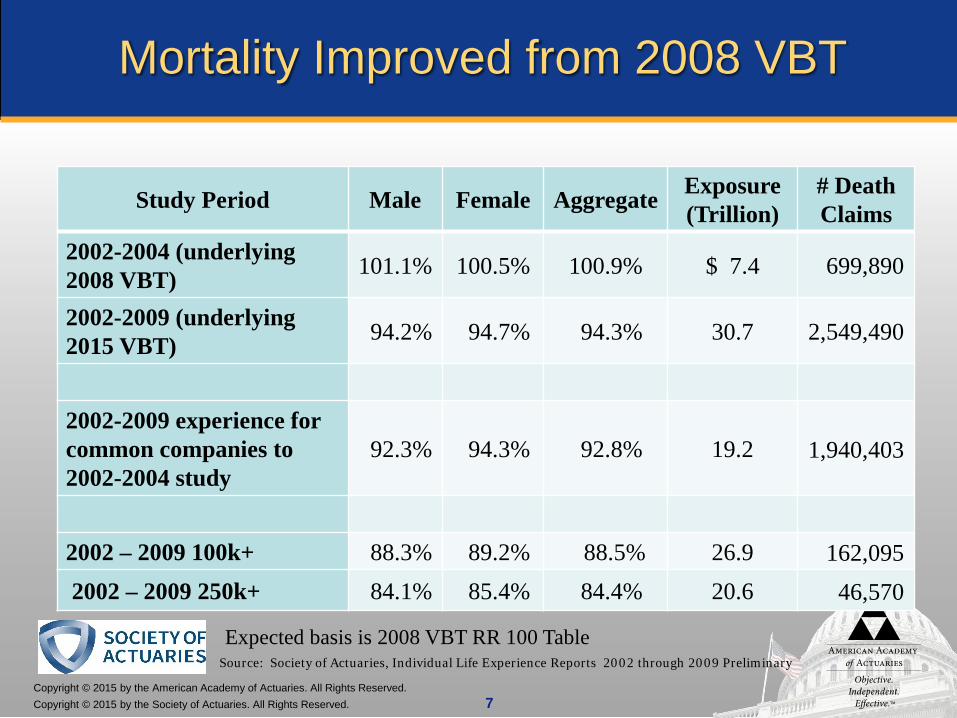

Mortality Improved from 2008 VBT

Study Period Male Female Aggregate Exposure(Trillion)

# Death Claims

2002-2004 (underlying 2008 VBT) 101.1% 100.5% 100.9% $ 7.4 699,890

2002-2009 (underlying2015 VBT) 94.2% 94.7% 94.3% 30.7 2,549,490

2002-2009 experience for common companies to 2002-2004 study

92.3% 94.3% 92.8% 19.2 1,940,403

2002 – 2009 100k+ 88.3% 89.2% 88.5% 26.9 162,0952002 – 2009 250k+ 84.1% 85.4% 84.4% 20.6 46,570

Expected basis is 2008 VBT RR 100 TableSource: Society of Actuaries, Individual Life Experience Reports 2002 through 2009 Preliminary

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 8

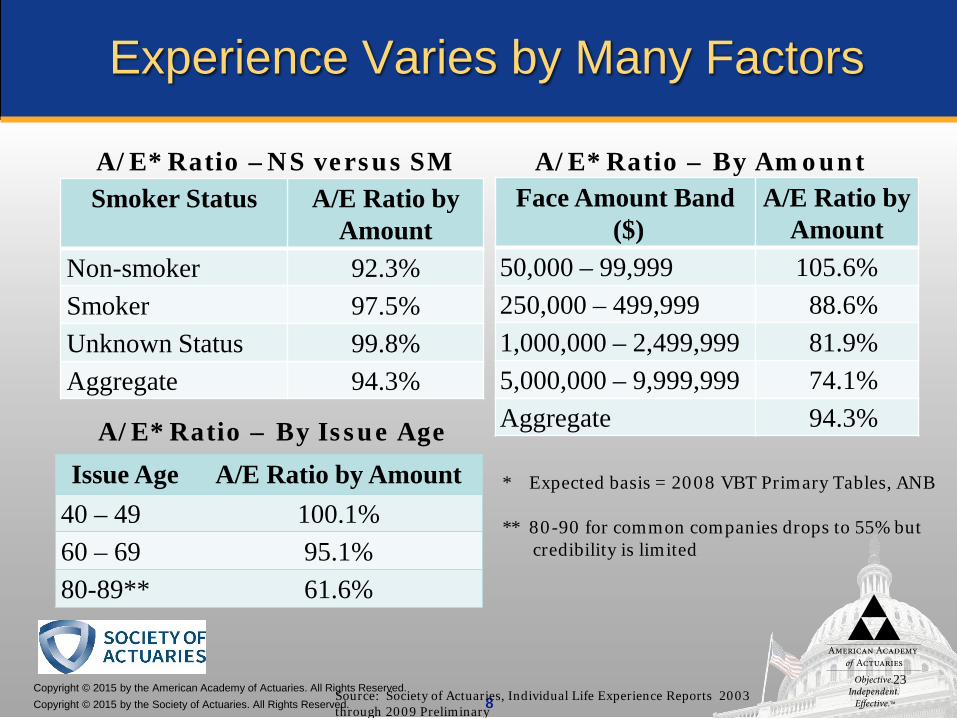

Experience Varies by Many Factors

Smoker Status A/E Ratio by Amount

Non-smoker 92.3%Smoker 97.5%Unknown Status 99.8%Aggregate 94.3%

Face Amount Band($)

A/E Ratio by Amount

50,000 – 99,999 105.6%250,000 – 499,999 88.6%1,000,000 – 2,499,999 81.9%5,000,000 – 9,999,999 74.1%Aggregate 94.3%

23

A/E* Ratio –NS versus SM

A/E* Ratio – By Issue AgeIssue Age A/E Ratio by Amount

40 – 49 100.1%60 – 69 95.1%80-89** 61.6%

* Expected basis = 2008 VBT Primary Tables, ANB

** 80-90 for common companies drops to 55% but credibility is limited

Source: Society of Actuaries, Individual Life Experience Reports 2003 through 2009 Preliminary

A/E* Ratio – By Amount

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 9

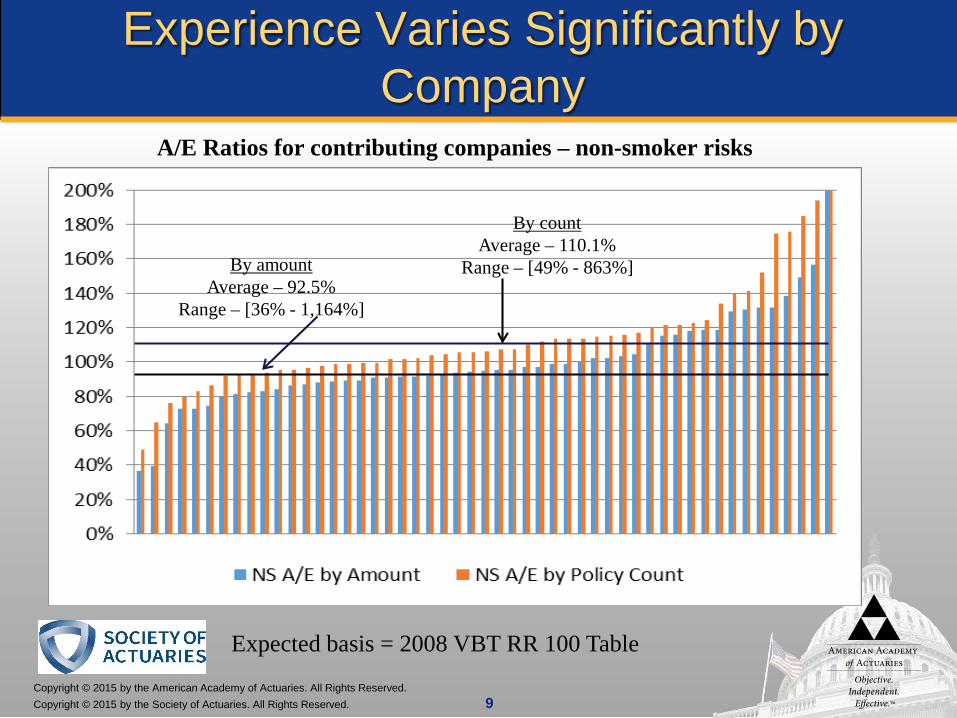

Experience Varies Significantly by Company

A/E Ratios for contributing companies – non-smoker risks

Expected basis = 2008 VBT RR 100 Table

By amount Average – 92.5%

Range – [36% - 1,164%]

By count Average – 110.1%

Range – [49% - 863%]

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 10

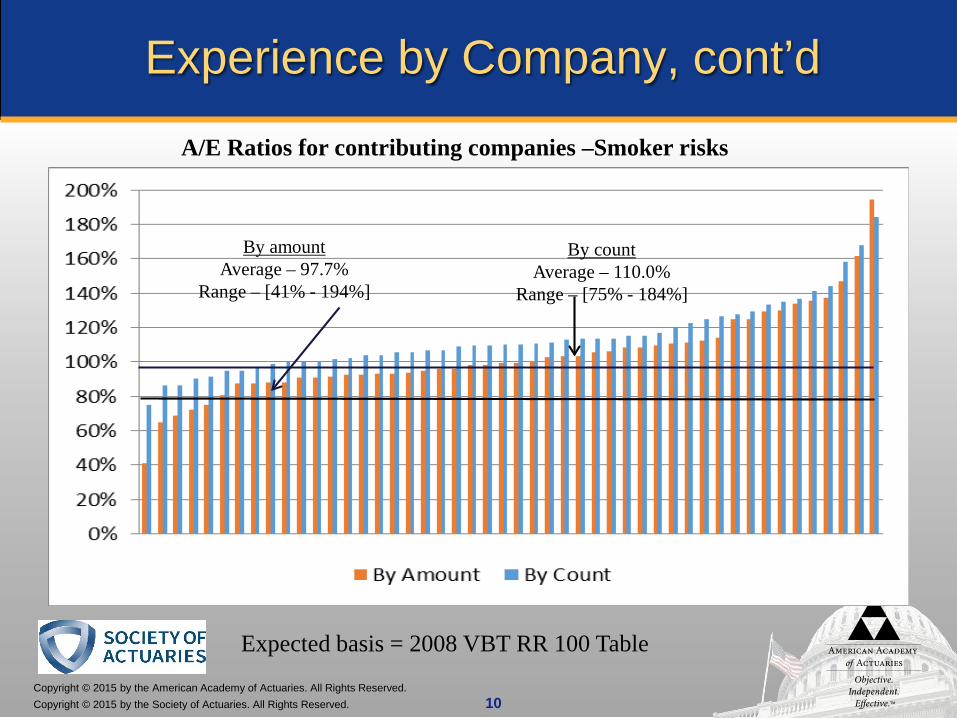

Experience by Company, cont’d

A/E Ratios for contributing companies –Smoker risks

Expected basis = 2008 VBT RR 100 Table

By amountAverage – 97.7%

Range – [41% - 194%]

By countAverage – 110.0%

Range – [75% - 184%]

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 11

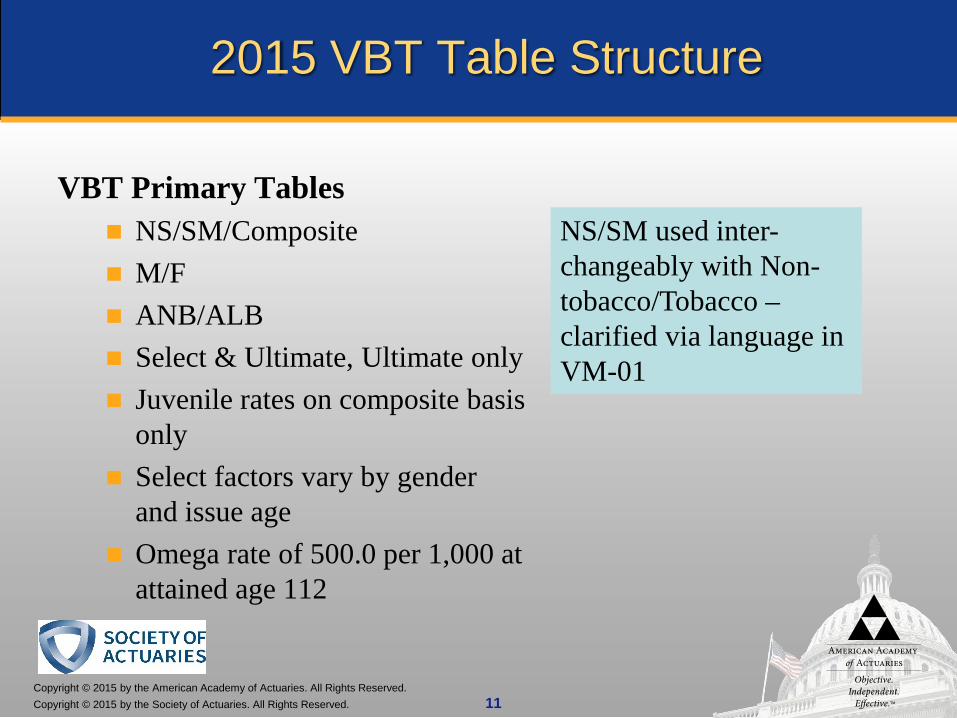

2015 VBT Table Structure

VBT Primary Tables NS/SM/Composite M/F ANB/ALB Select & Ultimate, Ultimate only Juvenile rates on composite basis

only Select factors vary by gender

and issue age Omega rate of 500.0 per 1,000 at

attained age 112

NS/SM used inter-changeably with Non-tobacco/Tobacco –clarified via language in VM-01

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 12

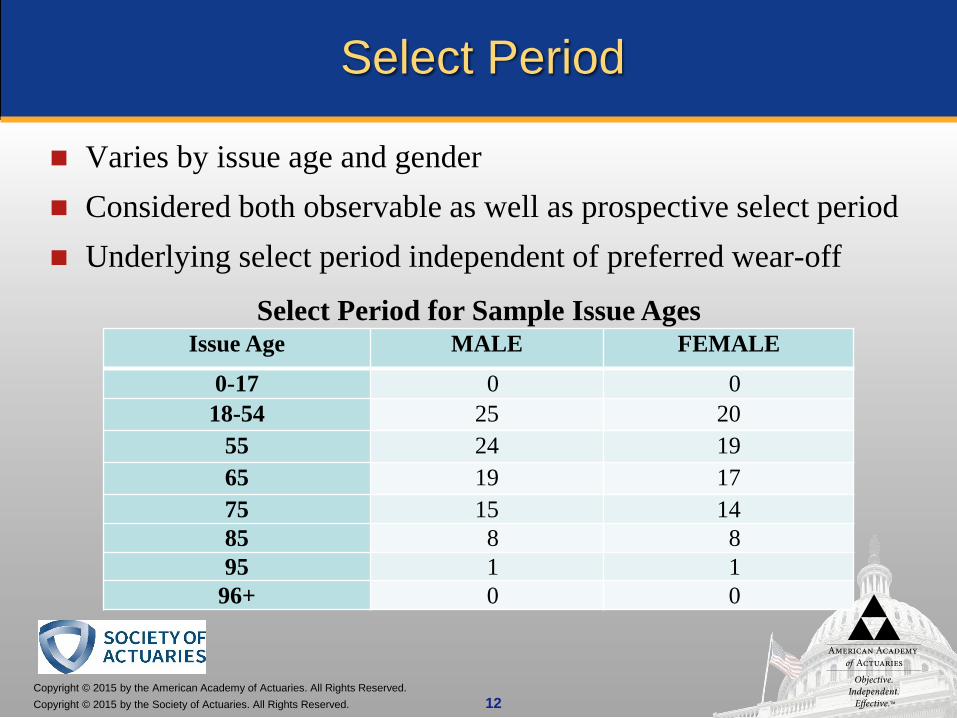

Select Period

Varies by issue age and gender Considered both observable as well as prospective select period Underlying select period independent of preferred wear-off

Issue Age MALE FEMALE

0-17 0 018-54 25 20

55 24 1965 19 1775 15 1485 8 895 1 1

96+ 0 0

Select Period for Sample Issue Ages

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 13

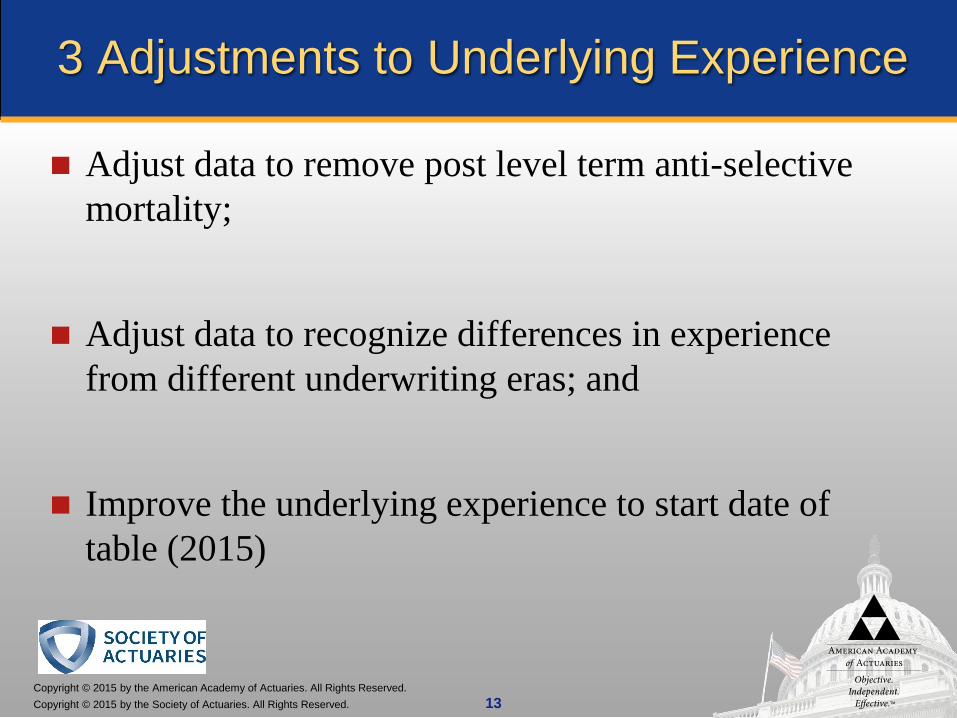

3 Adjustments to Underlying Experience

Adjust data to remove post level term anti-selective mortality;

Adjust data to recognize differences in experience from different underwriting eras; and

Improve the underlying experience to start date of table (2015)

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 14

1. Remove Effects of Post Level Term Mortality

Adjustment to decrease the total mortality rates to account for the impact of post-level term experience Analyzed A/E ratios for 10/15/20 year term plans by face

amount, issue age group and duration Recalculated A/E ratios by estimating impact of post level

term mortality

Factors vary by issue age/duration Average 2.9% at duration 13 versus 1.3% at duration 18

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 15

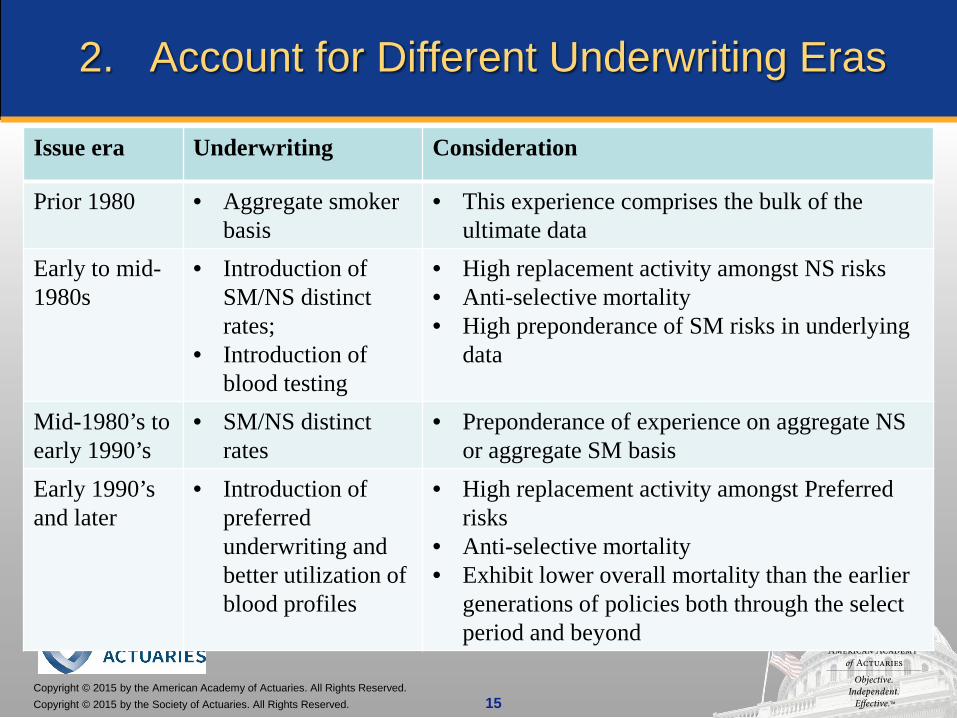

2. Account for Different Underwriting Eras

Issue era Underwriting Consideration

Prior 1980 • Aggregate smoker basis

• This experience comprises the bulk of the ultimate data

Early to mid-1980s

• Introduction of SM/NS distinct rates;

• Introduction of blood testing

• High replacement activity amongst NS risks• Anti-selective mortality• High preponderance of SM risks in underlying

data

Mid-1980’s to early 1990’s

• SM/NS distinct rates

• Preponderance of experience on aggregate NS or aggregate SM basis

Early 1990’s and later

• Introduction of preferred underwriting and better utilization of blood profiles

• High replacement activity amongst Preferred risks

• Anti-selective mortality• Exhibit lower overall mortality than the earlier

generations of policies both through the select period and beyond

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 16

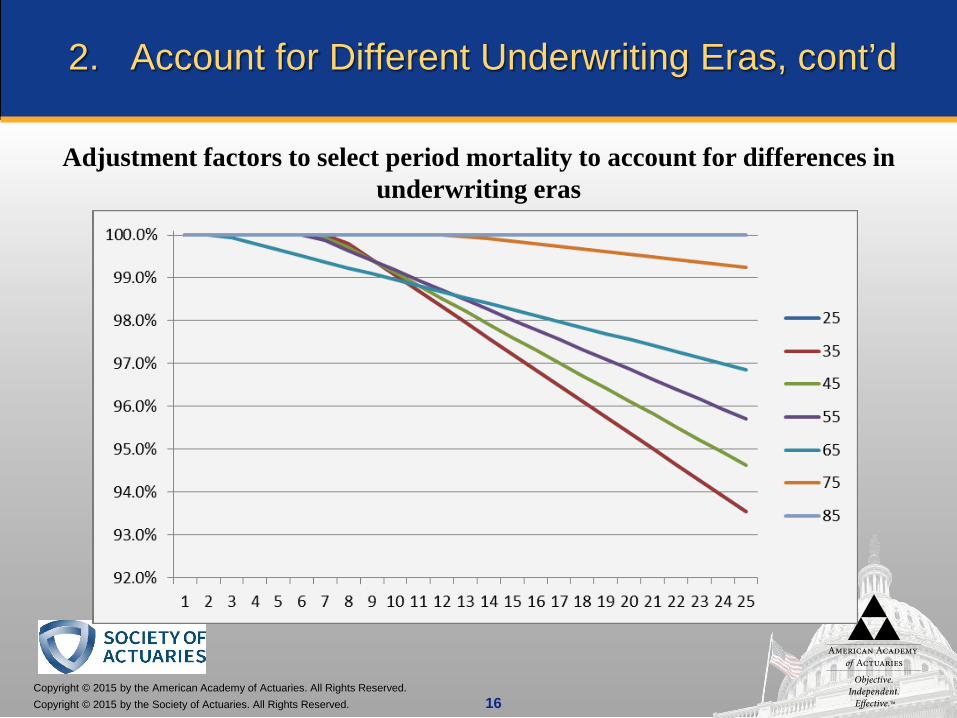

2. Account for Different Underwriting Eras, cont’d

Adjustment factors to select period mortality to account for differences in underwriting eras

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 17

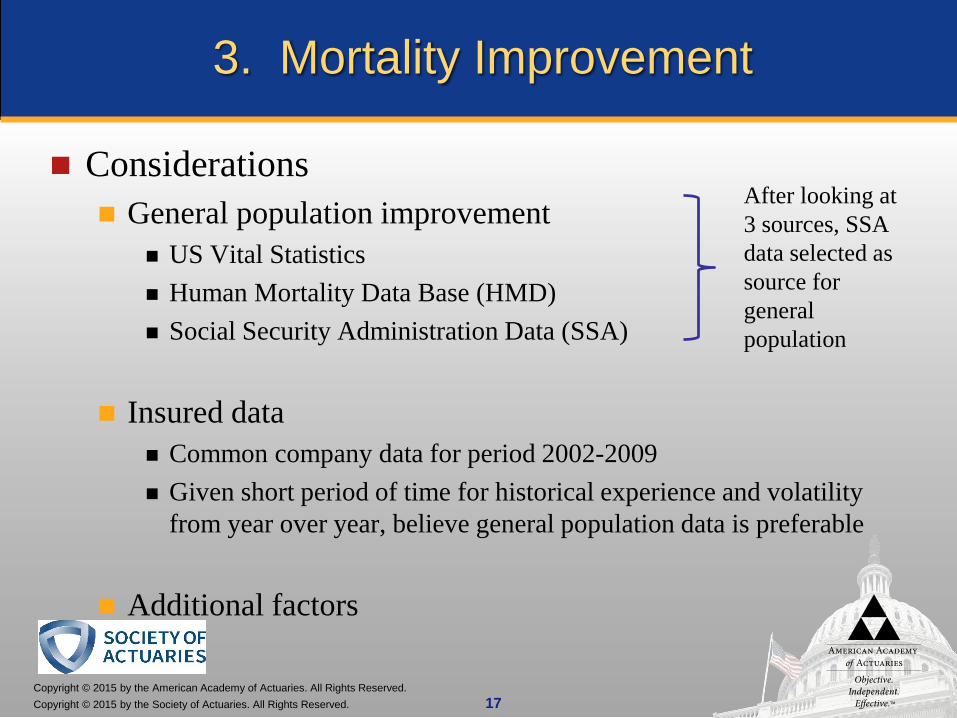

3. Mortality Improvement

Considerations General population improvement

US Vital Statistics Human Mortality Data Base (HMD) Social Security Administration Data (SSA)

Insured data Common company data for period 2002-2009 Given short period of time for historical experience and volatility

from year over year, believe general population data is preferable

Additional factors

After looking at 3 sources, SSA data selected as source for general population

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 18

3. Mortality Improvement, cont’d

Additional factors considered Gender; Attained age; Smoker status; Socio-economic status; and Differences in cause of death for insured lives vs general

population.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 19

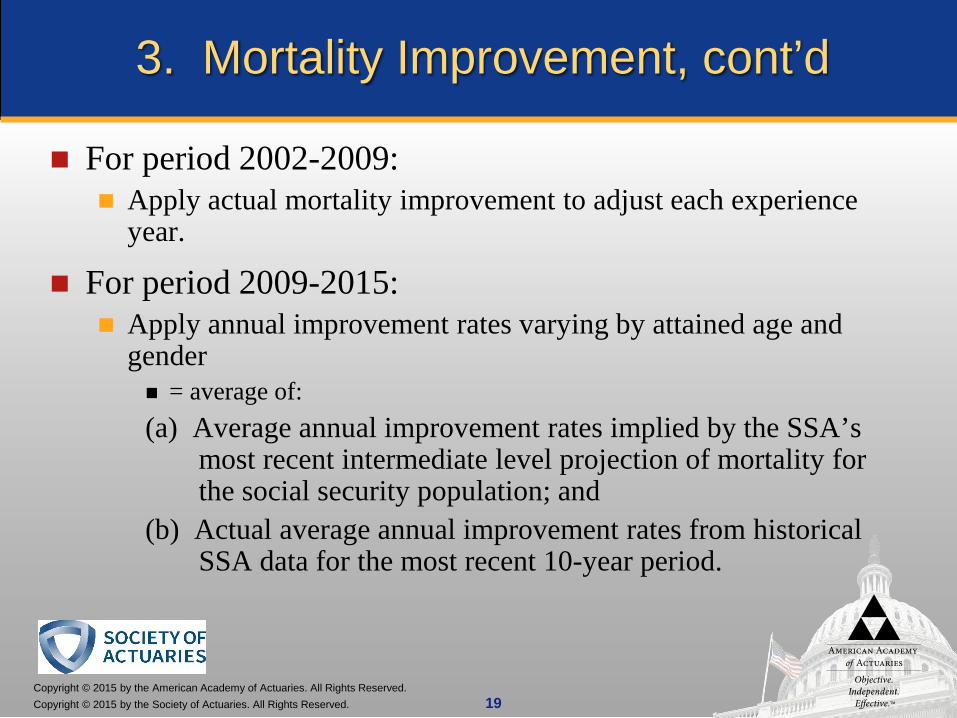

3. Mortality Improvement, cont’d

For period 2002-2009: Apply actual mortality improvement to adjust each experience

year.

For period 2009-2015: Apply annual improvement rates varying by attained age and

gender = average of:(a) Average annual improvement rates implied by the SSA’s

most recent intermediate level projection of mortality for the social security population; and

(b) Actual average annual improvement rates from historical SSA data for the most recent 10-year period.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 20

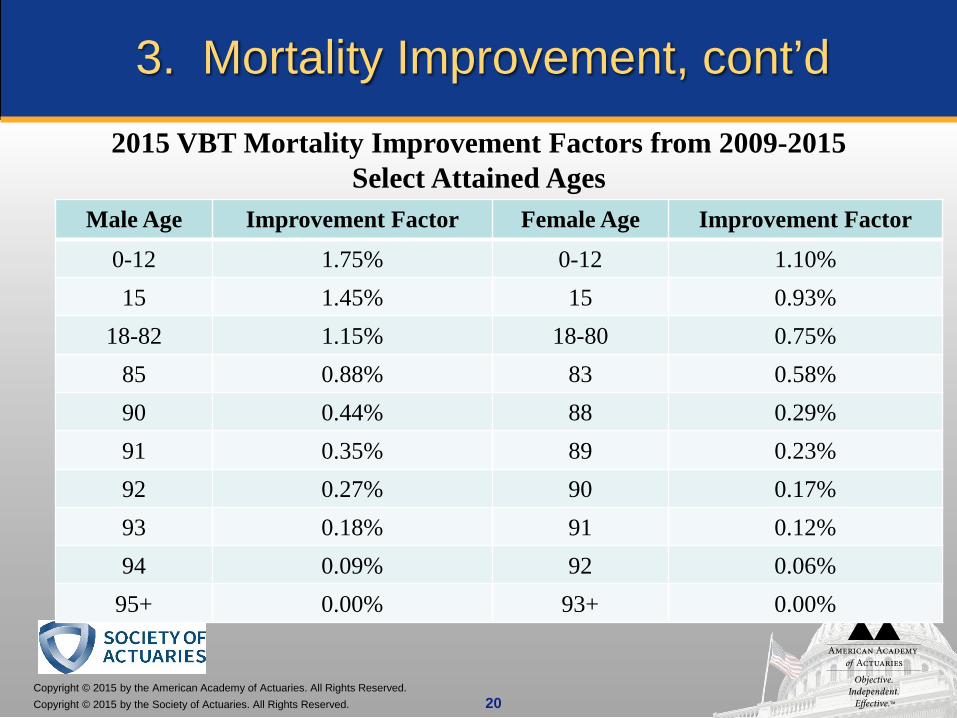

3. Mortality Improvement, cont’d2015 VBT Mortality Improvement Factors from 2009-2015

Select Attained AgesMale Age Improvement Factor Female Age Improvement Factor

0-12 1.75% 0-12 1.10%15 1.45% 15 0.93%

18-82 1.15% 18-80 0.75%85 0.88% 83 0.58%90 0.44% 88 0.29%91 0.35% 89 0.23%92 0.27% 90 0.17%93 0.18% 91 0.12%94 0.09% 92 0.06%

95+ 0.00% 93+ 0.00%

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 21

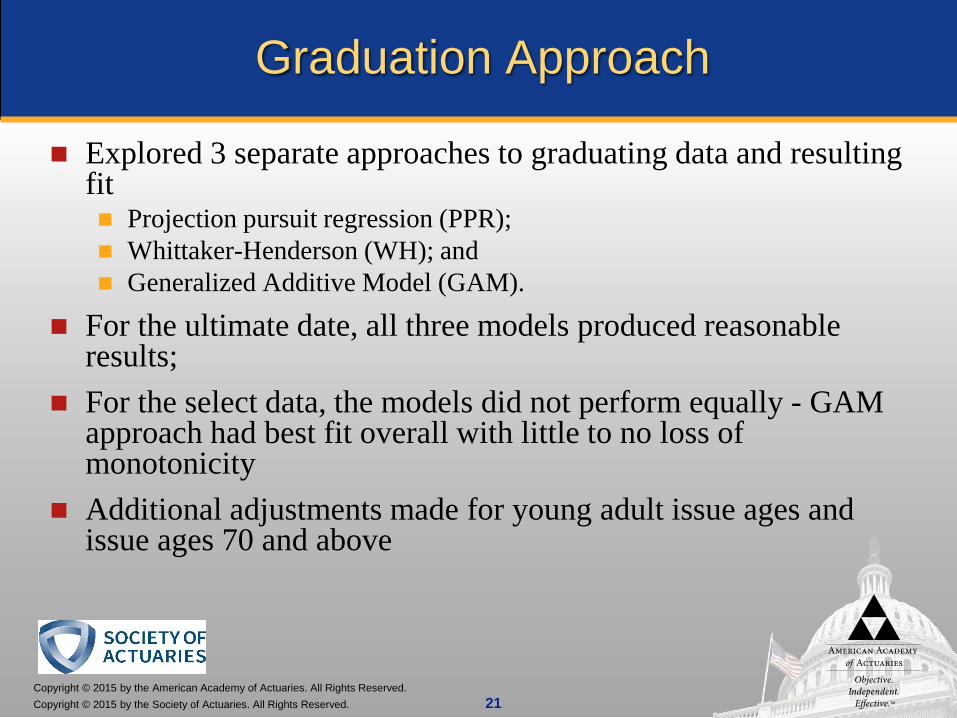

Graduation Approach

Explored 3 separate approaches to graduating data and resulting fit Projection pursuit regression (PPR); Whittaker-Henderson (WH); and Generalized Additive Model (GAM).

For the ultimate date, all three models produced reasonable results;

For the select data, the models did not perform equally - GAM approach had best fit overall with little to no loss of monotonicity

Additional adjustments made for young adult issue ages and issue ages 70 and above

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 22

Relative Risk Table Considerations

Number of tables Same as 2008 VBT for both non-smoker and smoker

Relativity amongst tables Different from 2008 VBT for non-smokers; same for

smokers

Preferred wear-off pattern Similar to 2008 VBT

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 23

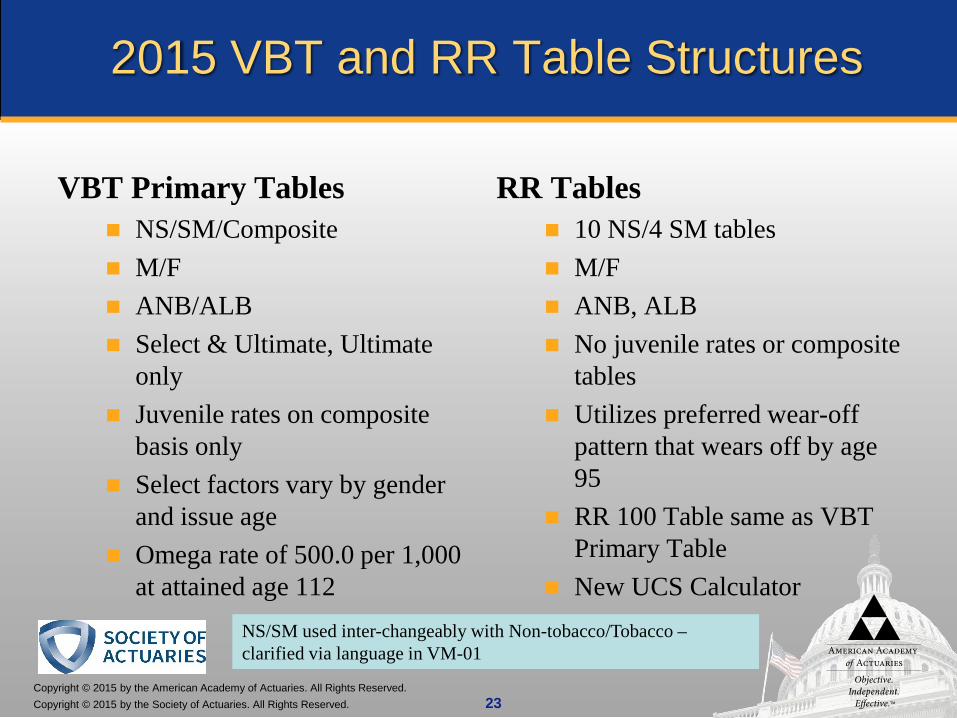

2015 VBT and RR Table Structures

VBT Primary Tables NS/SM/Composite M/F ANB/ALB Select & Ultimate, Ultimate

only Juvenile rates on composite

basis only Select factors vary by gender

and issue age Omega rate of 500.0 per 1,000

at attained age 112

RR Tables 10 NS/4 SM tables M/F ANB, ALB No juvenile rates or composite

tables Utilizes preferred wear-off

pattern that wears off by age 95

RR 100 Table same as VBT Primary Table

New UCS CalculatorNS/SM used inter-changeably with Non-tobacco/Tobacco –clarified via language in VM-01

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 24

NS = RR 50, 60, 70, 80, 90, 100, 110, 125, 150, 175

E = 2014 VBT adjusted to remove improvement to midpoint of data period for each company

02468

101214

Num

ber

of c

ompa

nies

A/E where E=2014 VBT

Range of A/Es for all NS risk classes by number of claims

50+ Claims25-49 Claims<25 Claims

Determination of Relativity for RR Tables - Nonsmoker

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 25

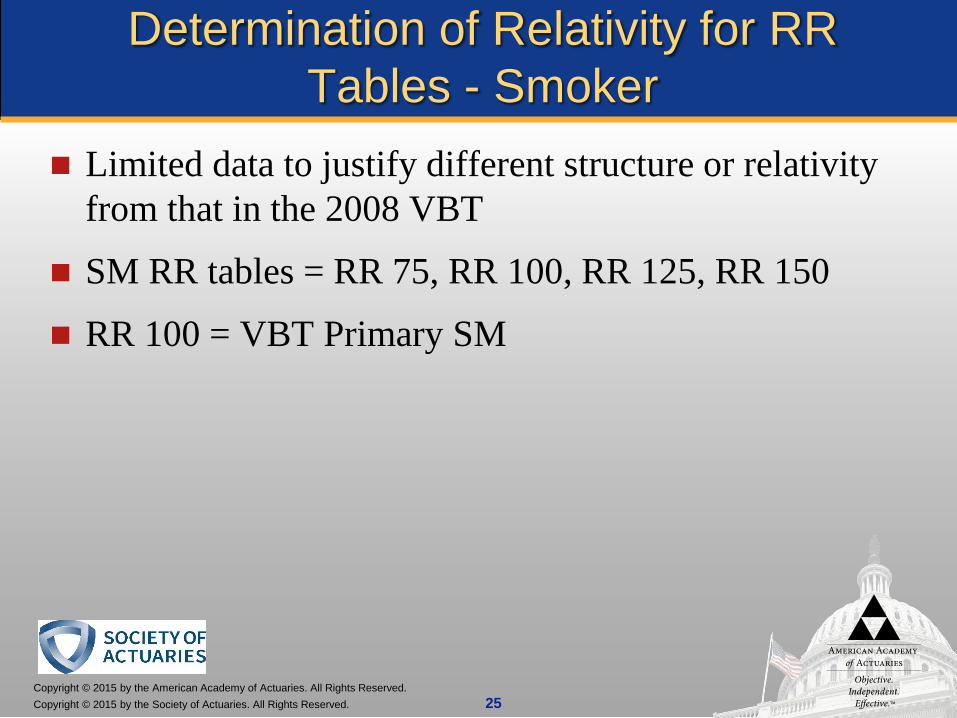

Determination of Relativity for RR Tables - Smoker

Limited data to justify different structure or relativity from that in the 2008 VBT

SM RR tables = RR 75, RR 100, RR 125, RR 150

RR 100 = VBT Primary SM

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 26

Preferred Wear-off Factors

Analyzed level of wear-off but industry experience still emerging.

There is virtually no additional information available from the 2008 VBT analysis, which was extensive.

The preponderance of aggregate NS data in early durations further complicated the analysis; therefore, also examined Milliman’s MIMSA study.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 27

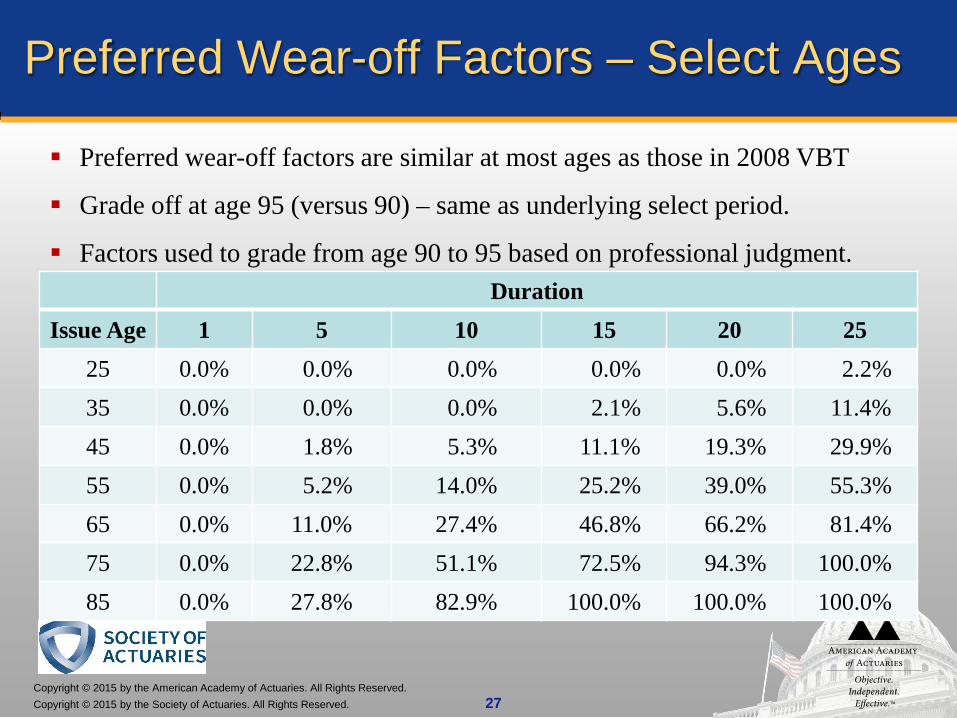

Preferred Wear-off Factors – Select Ages

DurationIssue Age 1 5 10 15 20 25

25 0.0% 0.0% 0.0% 0.0% 0.0% 2.2%35 0.0% 0.0% 0.0% 2.1% 5.6% 11.4%45 0.0% 1.8% 5.3% 11.1% 19.3% 29.9%55 0.0% 5.2% 14.0% 25.2% 39.0% 55.3%65 0.0% 11.0% 27.4% 46.8% 66.2% 81.4%75 0.0% 22.8% 51.1% 72.5% 94.3% 100.0%85 0.0% 27.8% 82.9% 100.0% 100.0% 100.0%

Preferred wear-off factors are similar at most ages as those in 2008 VBT

Grade off at age 95 (versus 90) – same as underlying select period.

Factors used to grade from age 90 to 95 based on professional judgment.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

Resulting experience – Sample Ages and DurationsMale Risks

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 29

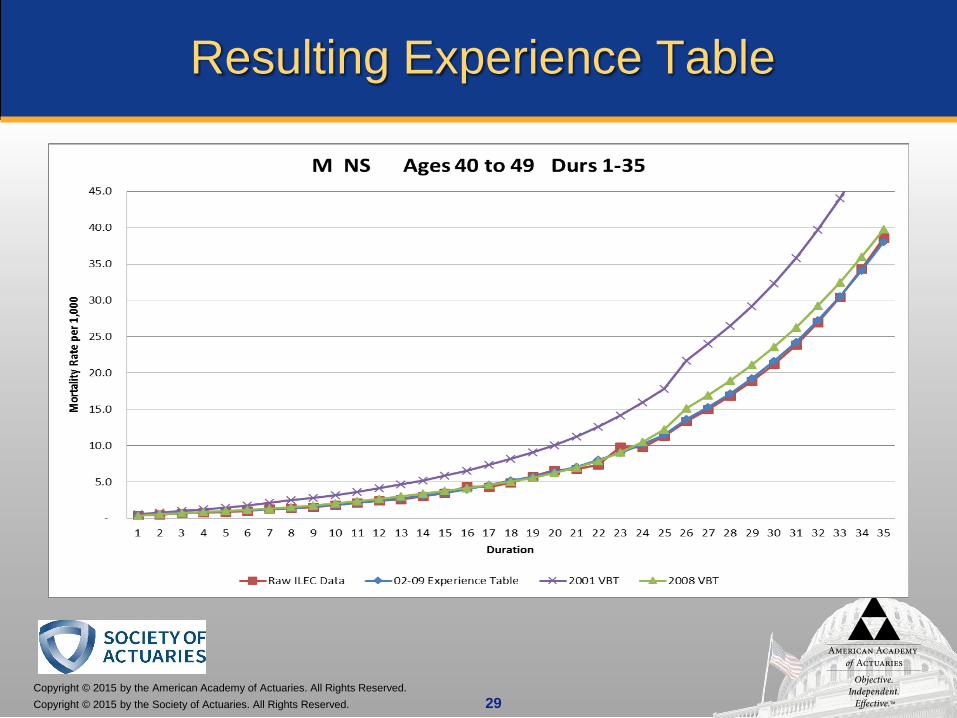

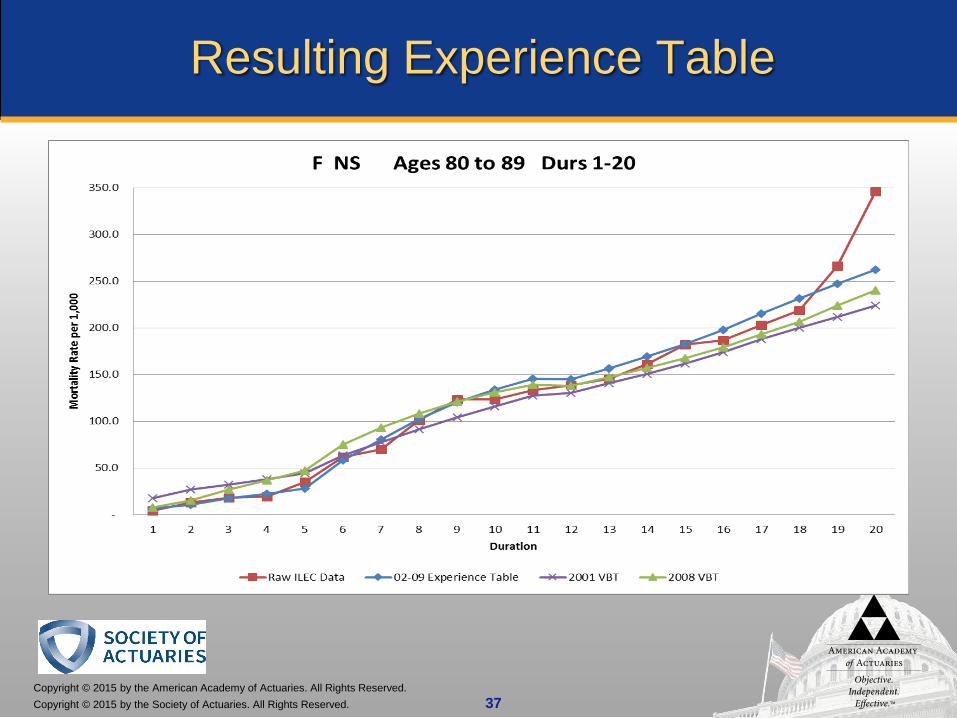

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 30

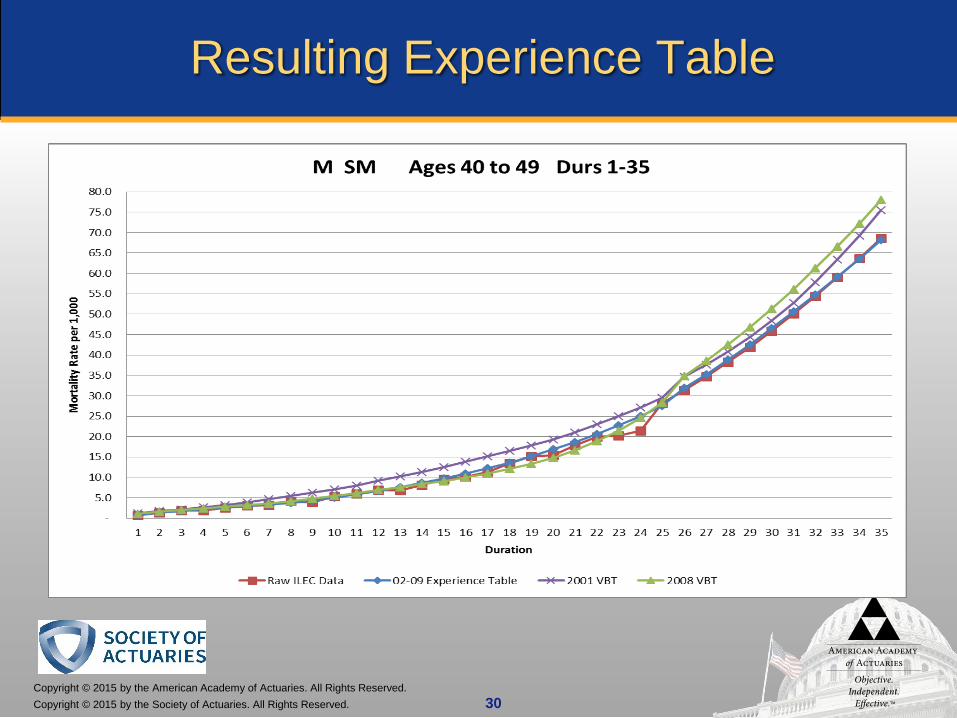

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 31

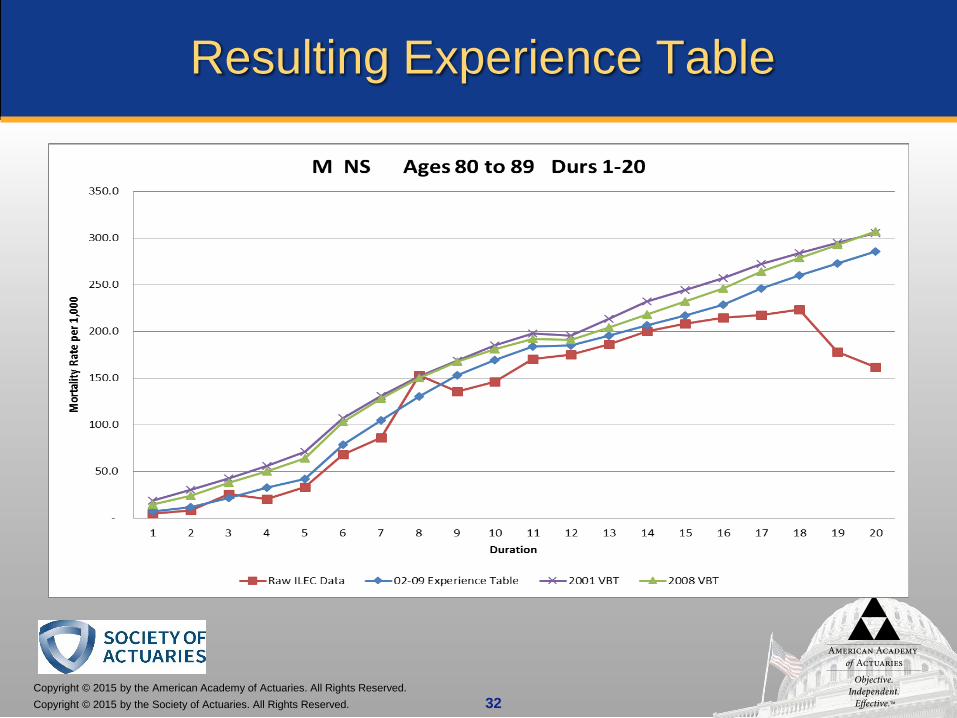

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 32

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

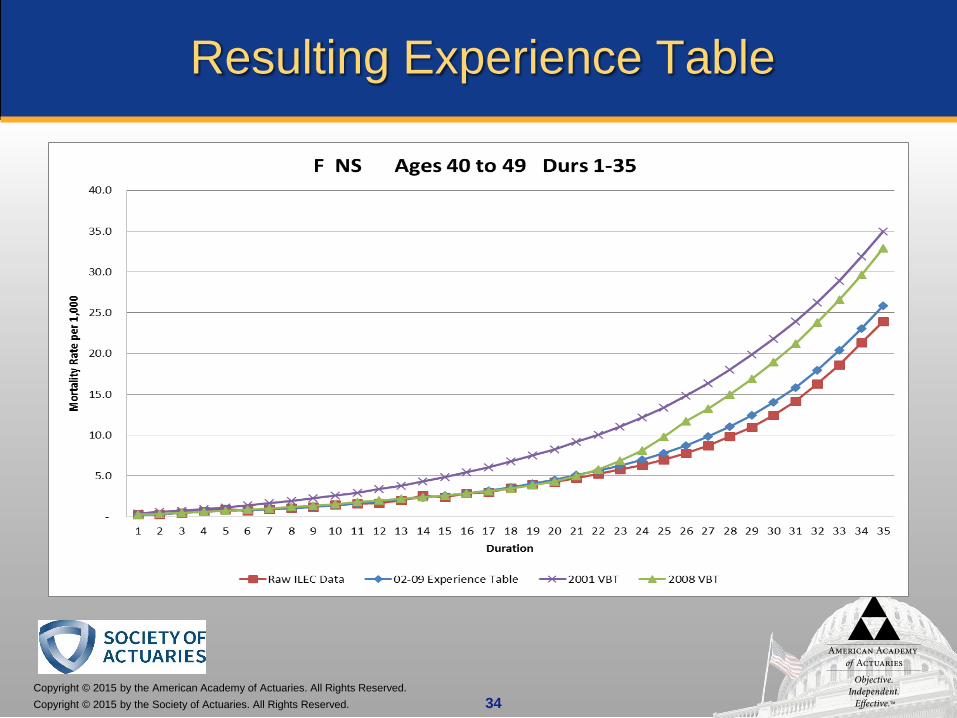

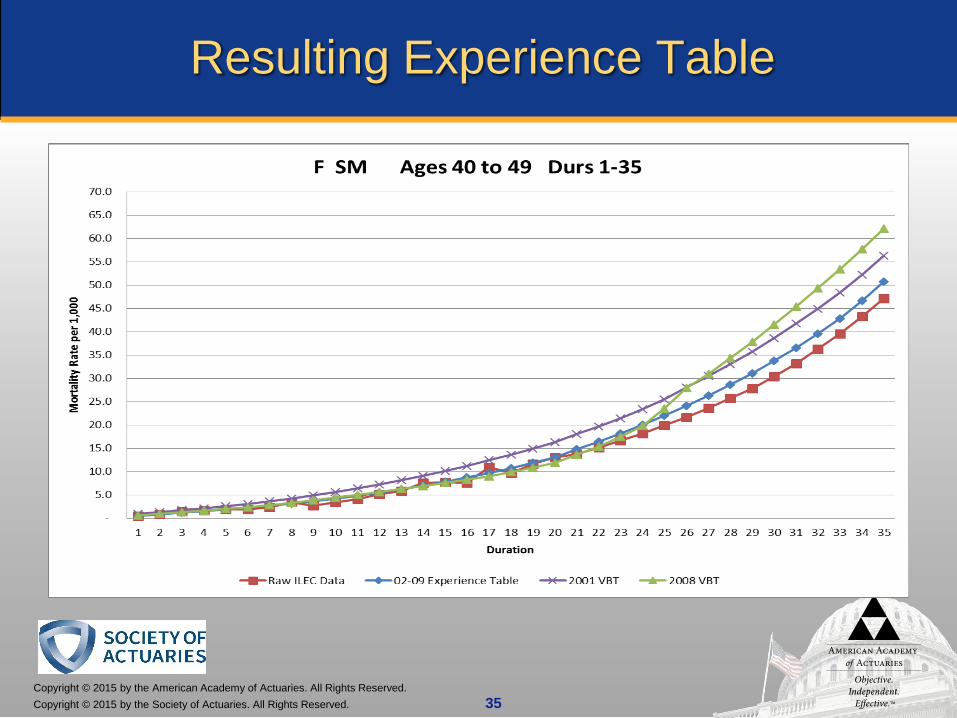

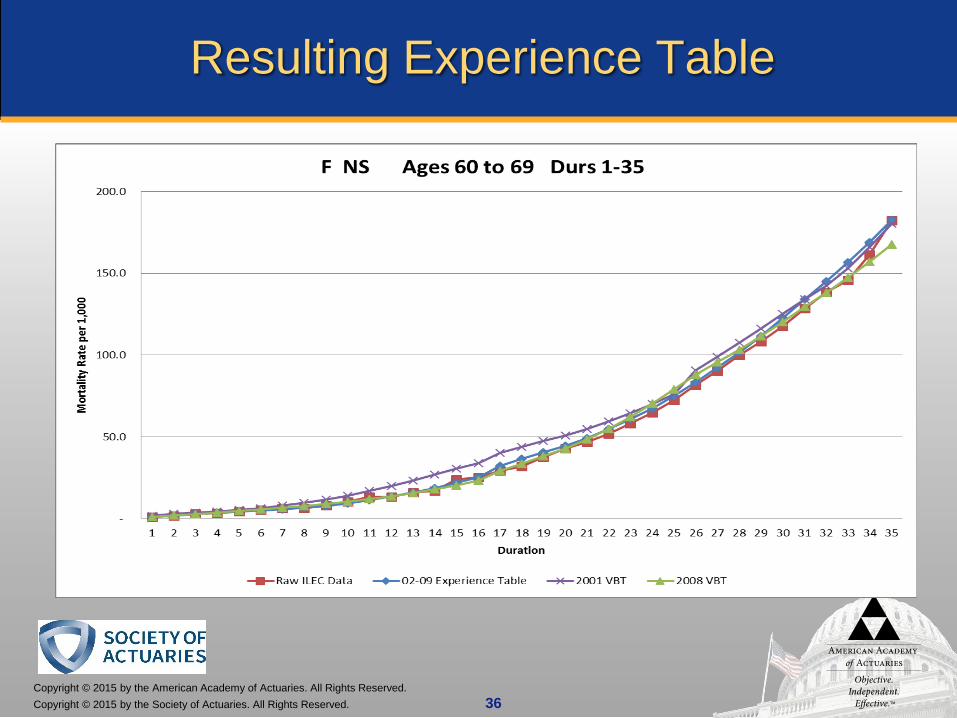

Resulting experience – Sample Ages and Durations

Female Risks

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 34

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 35

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 36

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 37

Resulting Experience Table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

2017 CSO DevelopmentMary Bahna-Nolan

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 39

Tables and Applications – Exposed, cont’d

Table Regulatory Use Valuation Manual Impacts Status

2017 CSO

and

2017 CSOPreferred Structure Tables

• Net premium reserves• Tax reserves• Non-forfeiture

determination*• Basis for 7702/7702A• Cap for universal life cost

of insurance charges

VM-00• Allows use of 2017 CSO, per conditions in

VM-20,§3 for companies that elect to defer PBR implementation

VM-02, §5.A.1-3• Recognizes 2017 CSO for non-forfeiture

and defines conditions for useVM-M, §1.H

• Defines 2017 CSO and Preferred Structure Tables for use as a valuation table

VM-20, §3.A.2 and §3.C.1• Allows use of 2017 CSO for net premium

reserve determination and defines conditions for its use

VM-20, §6• Points to mortality as defined in §3.C.1

and VM-M §1.H for which mortality to use in the stochastic and deterministic exclusion tests

VM-A• Adds Appendix A-814 to list of references

• 30-day comment period expired 09/18/2015

• Report being finalized• Vote for adoption at

upcoming LATF conference call

* Relative risk tables are not applicable for non-forfeiture

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 40

2017 CSO

Purpose of margin

Target level of margin (from regulators)

Structure of margin

Preferred structure tables

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 41

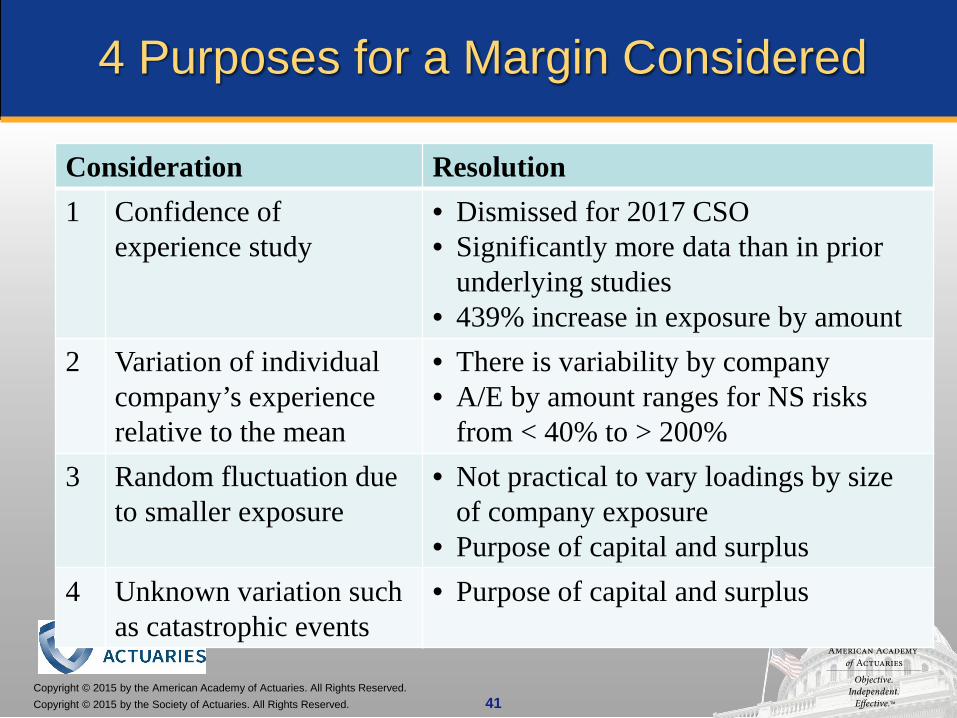

4 Purposes for a Margin Considered

Consideration Resolution1 Confidence of

experience study• Dismissed for 2017 CSO• Significantly more data than in prior

underlying studies• 439% increase in exposure by amount

2 Variation of individualcompany’s experience relative to the mean

• There is variability by company• A/E by amount ranges for NS risks

from < 40% to > 200%3 Random fluctuation due

to smaller exposure• Not practical to vary loadings by size

of company exposure• Purpose of capital and surplus

4 Unknown variation such as catastrophic events

• Purpose of capital and surplus

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 42

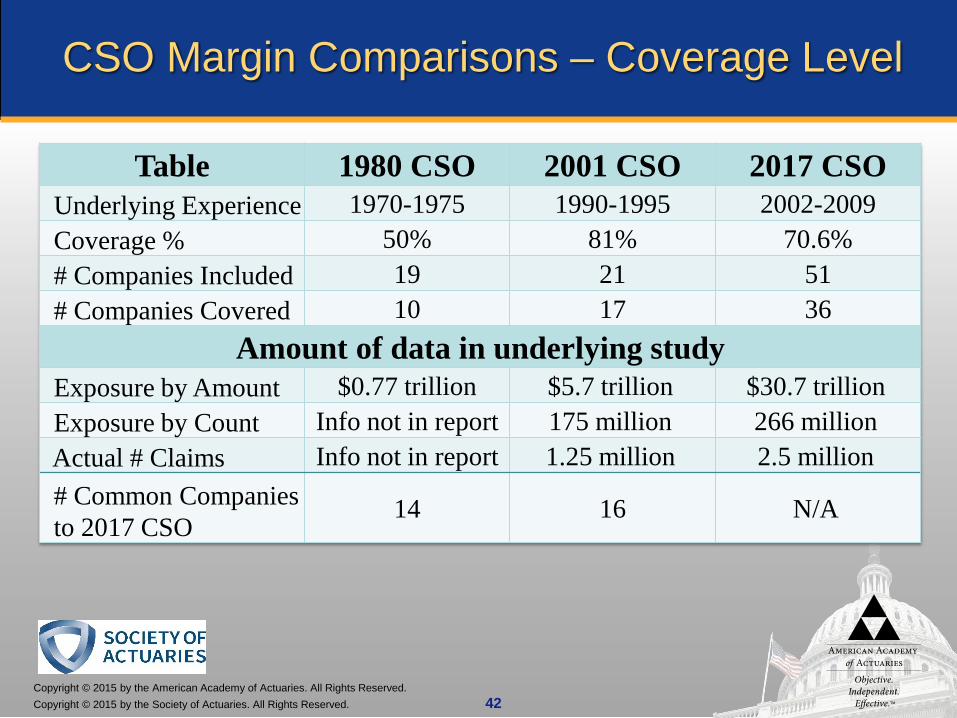

CSO Margin Comparisons – Coverage Level

Table 1980 CSO 2001 CSO 2017 CSOUnderlying Experience 1970-1975 1990-1995 2002-2009Coverage % 50% 81% 70.6%# Companies Included 19 21 51# Companies Covered 10 17 36

Amount of data in underlying studyExposure by Amount $0.77 trillion $5.7 trillion $30.7 trillionExposure by Count Info not in report 175 million 266 millionActual # Claims Info not in report 1.25 million 2.5 million# Common Companies to 2017 CSO

14 16 N/A

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 43

NAIC LATF Guidance Regarding Margin

Margins consistent with 2001 CSO

To cover the claims or mortality experience from at least 70% - 79% of the contributing companies (in the underlying mortality study)

Purpose of margin is to cover the variation of an individual company’s mortality around the mean (company variation)

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 44

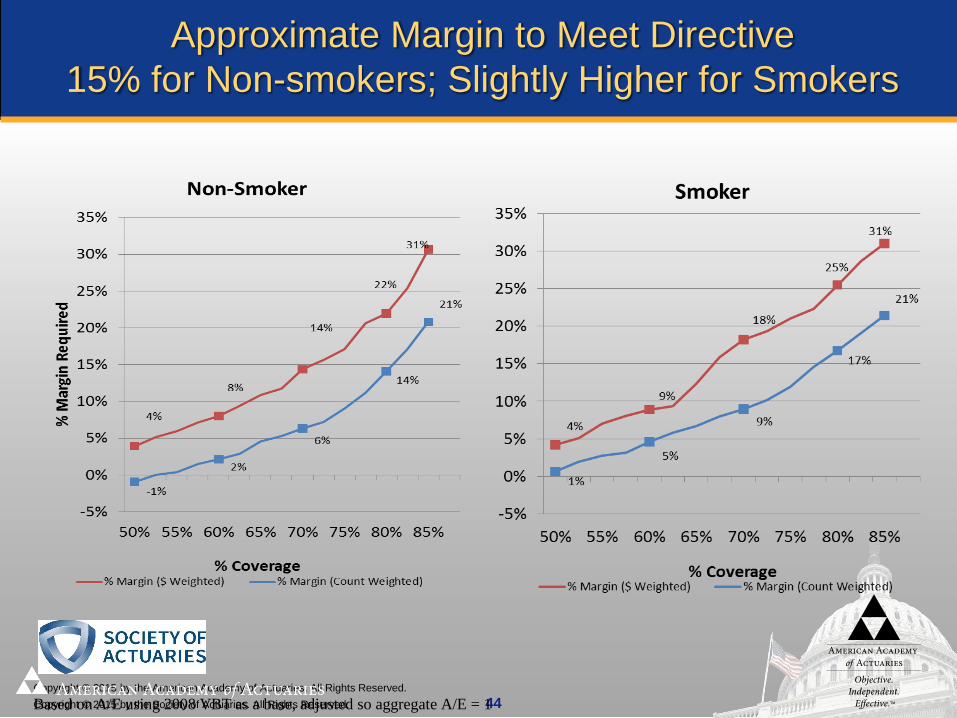

Approximate Margin to Meet Directive 15% for Non-smokers; Slightly Higher for Smokers

Based on A/E using 2008 VBT as a base, adjusted so aggregate A/E = 1

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 45

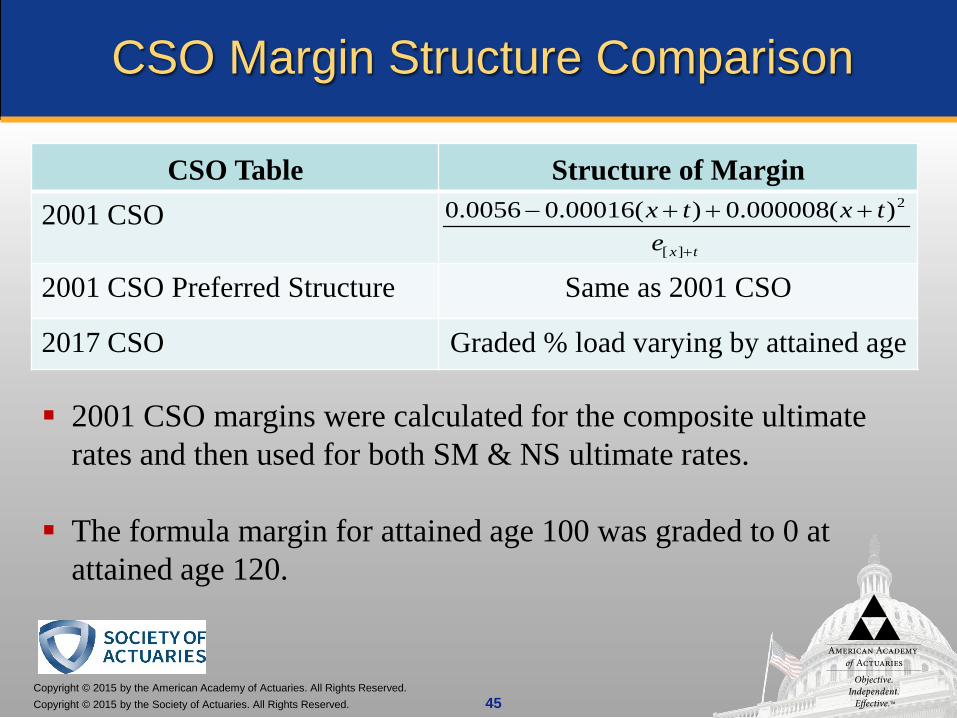

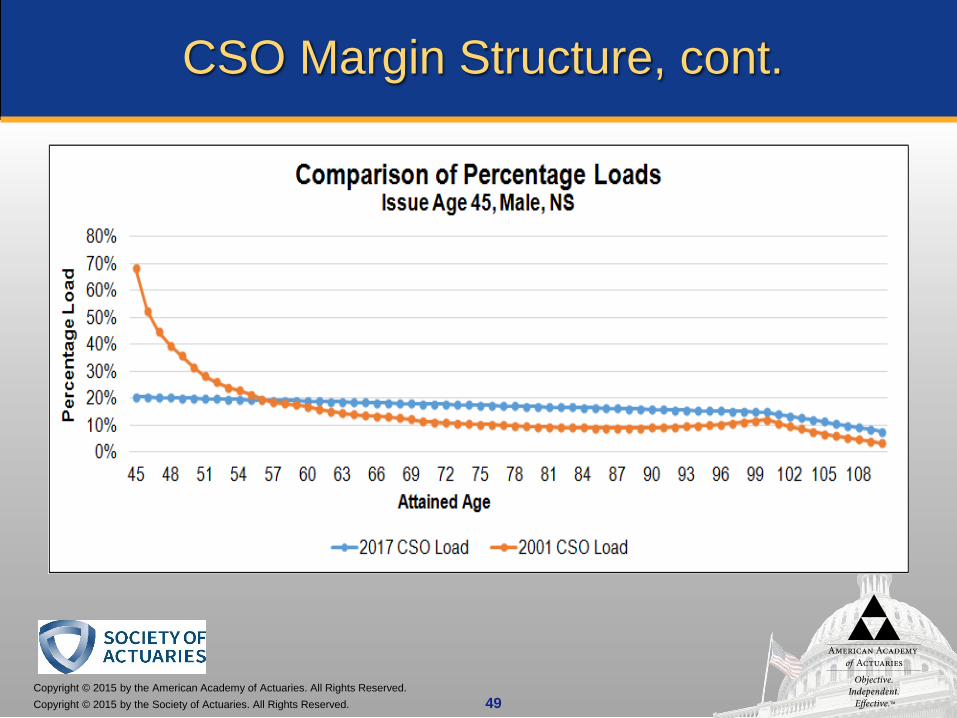

CSO Margin Structure Comparison

CSO Table Structure of Margin2001 CSO

2001 CSO Preferred Structure Same as 2001 CSO

2017 CSO Graded % load varying by attained age

2001 CSO margins were calculated for the composite ultimate rates and then used for both SM & NS ultimate rates.

The formula margin for attained age 100 was graded to 0 at attained age 120.

txetxtx

+

+++−

][

2)(000008.0)(00016.00056.0

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 46

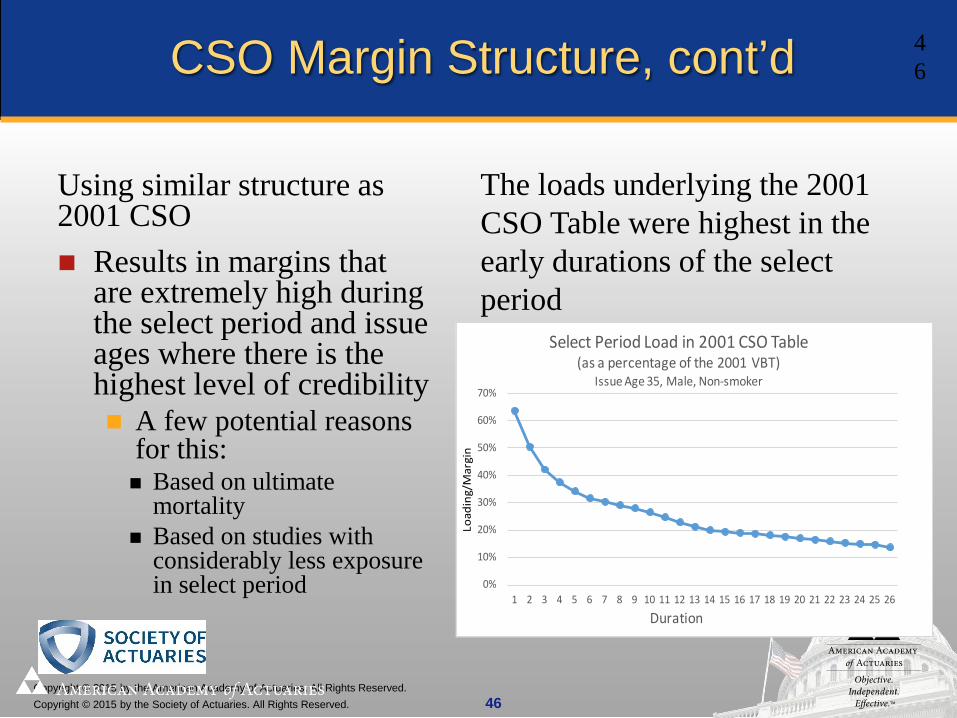

CSO Margin Structure, cont’d

Using similar structure as 2001 CSO Results in margins that

are extremely high during the select period and issue ages where there is the highest level of credibility A few potential reasons

for this: Based on ultimate

mortality Based on studies with

considerably less exposure in select period

The loads underlying the 2001 CSO Table were highest in the early durations of the select period

0%

10%

20%

30%

40%

50%

60%

70%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Load

ing/

Mar

gin

Duration

Select Period Load in 2001 CSO Table(as a percentage of the 2001 VBT)

Issue Age 35, Male, Non-smoker

46

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 47

CSO Margin Structure, cont’d

■ Developed % Load that varies by attained age with the following pattern:■ 23% below age 20, grading down to■ 17% at age 80, and further grading down to■ 15% at age 100, and further grading down to■ 7.5% at age 110 and later

■ Results in a percentage load that decreases by age and an absolute load that generally increases by age

■ Appears to result in more intuitive pattern in load by age than other methods

■ Simple to understand and administer for all the table variations■ Easier to maintain appropriate relationships between the various tables

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 48

CSO Margin Structure, cont’d

This load covers the mortality* of 70.6% of companies in the study overall 72.5% of companies for males; 76.5% for females 71.6% of the companies for male non-smokers; 74.5% for female non-

smokers 74.5% of the companies for male smokers; 78.4% for female smokers

A company’s mortality was covered if its A/E ratio by amount was below 100% where E was the loaded pure experience table before any improvement to 2014 (or 2017)

Committee believes this covers the guidance suggested by LATF to cover 70%-79% of contributing companies’ experience

* The different distributions of business within each company led to variability in which companies and how many companies experience is covered by a particular load.The coverage percentage varies by age grouping within a particular cohort.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 49

CSO Margin Structure, cont.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 50

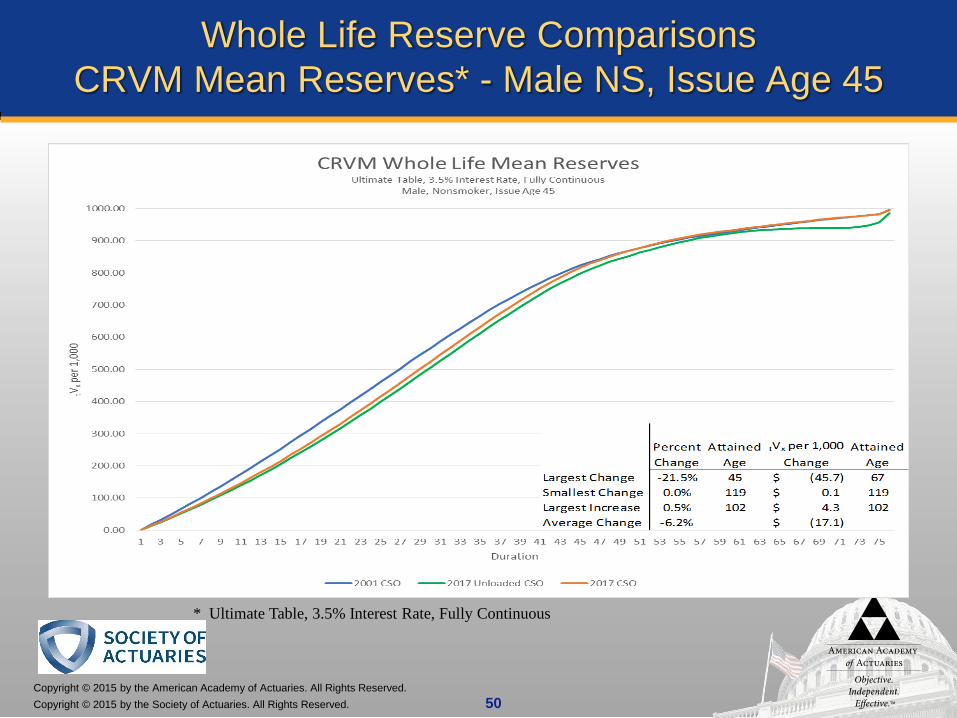

Whole Life Reserve ComparisonsCRVM Mean Reserves* - Male NS, Issue Age 45

* Ultimate Table, 3.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 51

Whole Life Reserve ComparisonsCRVM Mean Reserves* - Male NS, Issue Age 65

* Ultimate Table, 3.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 52

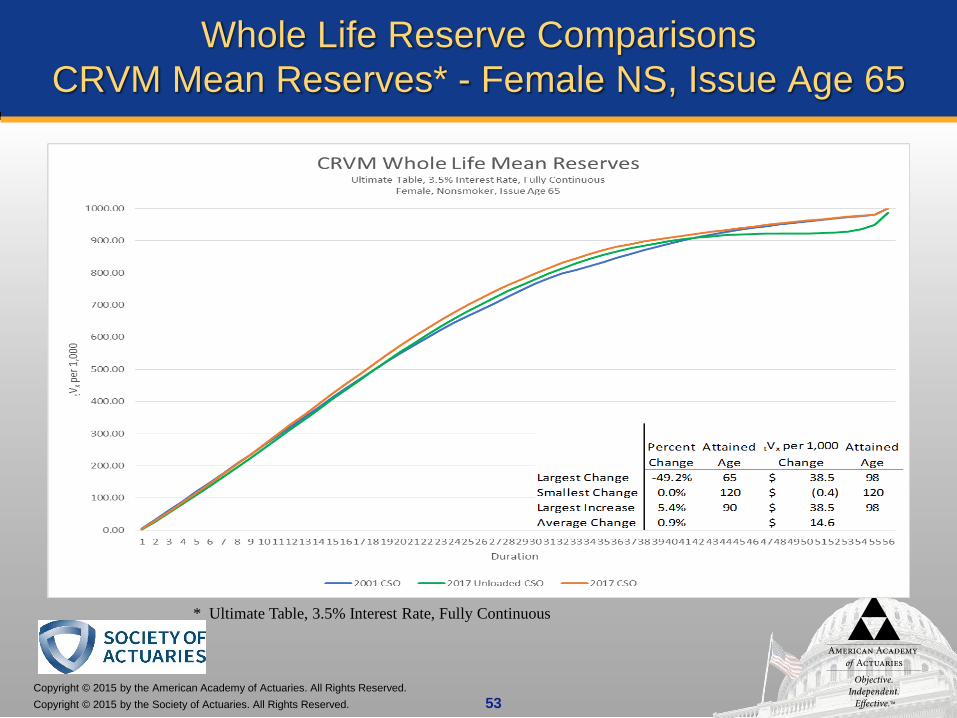

Whole Life Reserve ComparisonsCRVM Mean Reserves* - Female NS, Issue Age 45

* Ultimate Table, 3.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 53

Whole Life Reserve ComparisonsCRVM Mean Reserves* - Female NS, Issue Age 65

* Ultimate Table, 3.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 54

2017 CSO Development – Preferred Structure Tables

2015 VBT as base, projected with improvement to 2017 (referred to as Preferred Structure Basic Tables)

Similar structure as 2001 CSO Preferred Structure Tables 3 NS 2 SM

Omega age of 121 – same as 2001 CSO Rates grade to omega rate of 1.000

Load structure and load level same across all the classes

• NS and SM classes, when weighted together, equal 2015 VBT aggregate NS and SM mortality, respectively

• Tables were subsequently improved to 2017

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 55

2017 CSO Development – Preferred Structure Tables, cont’d

Step 1: Assessed preferred experience based on the 2005-09 ILEC data collected for business issued under a preferred structure basis. Business for nonsmoker risks with 3 or more classes limited

to issues since 1990 resulting in little to no data beyond duration 15

Business for smoker/nonsmoker risk structures limited to issues since 1980s

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 56

2017 CSO Development – Preferred Structure Tables, cont’d

Step 2: Mapped classes into preferred risk class structure (NS classes to Preferred Plus, Preferred and Residual Standard; SM classes to Preferred and Residual Standard) 3 class structures were mapped directly, 4 class structures mapped best class to best class, 2nd best to

2nd best, and 3rd and 4th classes to standard 2 class NS data was ignored as the experience was not

consistent with the 3 and 4 NS class structures

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 57

2017 CSO Development – Preferred Structure Tables, cont’d

Step 3: Determined a single A/E estimate for the experience by combining All available durations Male and female (because UCS scored do not distinguish

between genders)

Step 4: Determined the Relative Risk of each class, using the combined male and female A/E to point to an RR table. For example, if A/E is 72%, then use 80% of RR 70 and 20% of RR 80

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 58

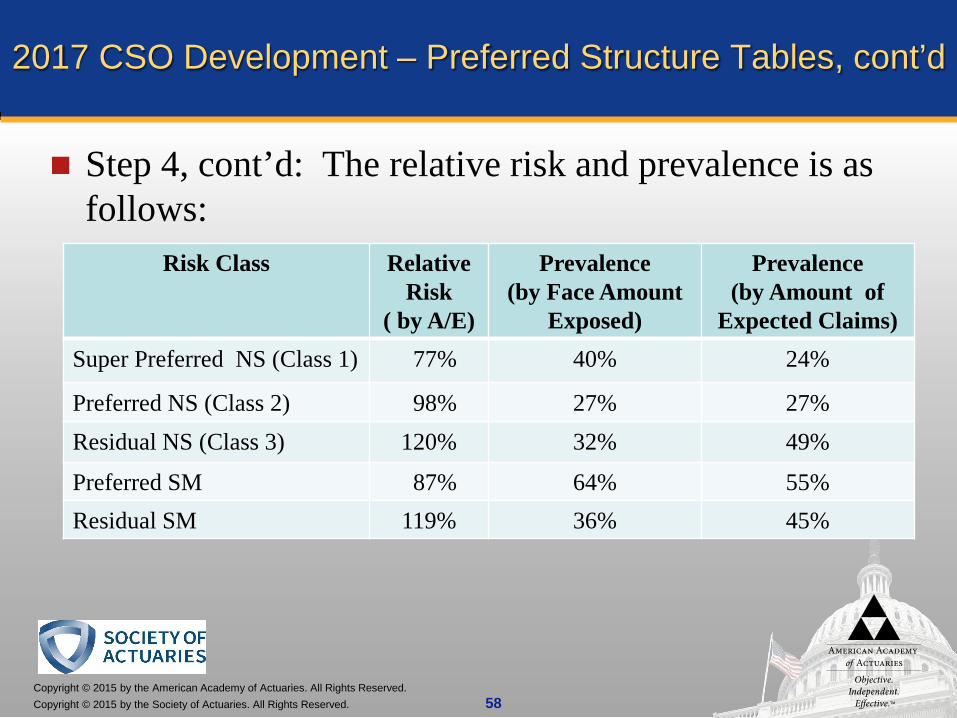

Step 4, cont’d: The relative risk and prevalence is as follows:

2017 CSO Development – Preferred Structure Tables, cont’d

Risk Class Relative Risk

( by A/E)

Prevalence(by Face Amount

Exposed)

Prevalence(by Amount of

Expected Claims)Super Preferred NS (Class 1) 77% 40% 24%

Preferred NS (Class 2) 98% 27% 27%Residual NS (Class 3) 120% 32% 49%

Preferred SM 87% 64% 55%Residual SM 119% 36% 45%

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 59

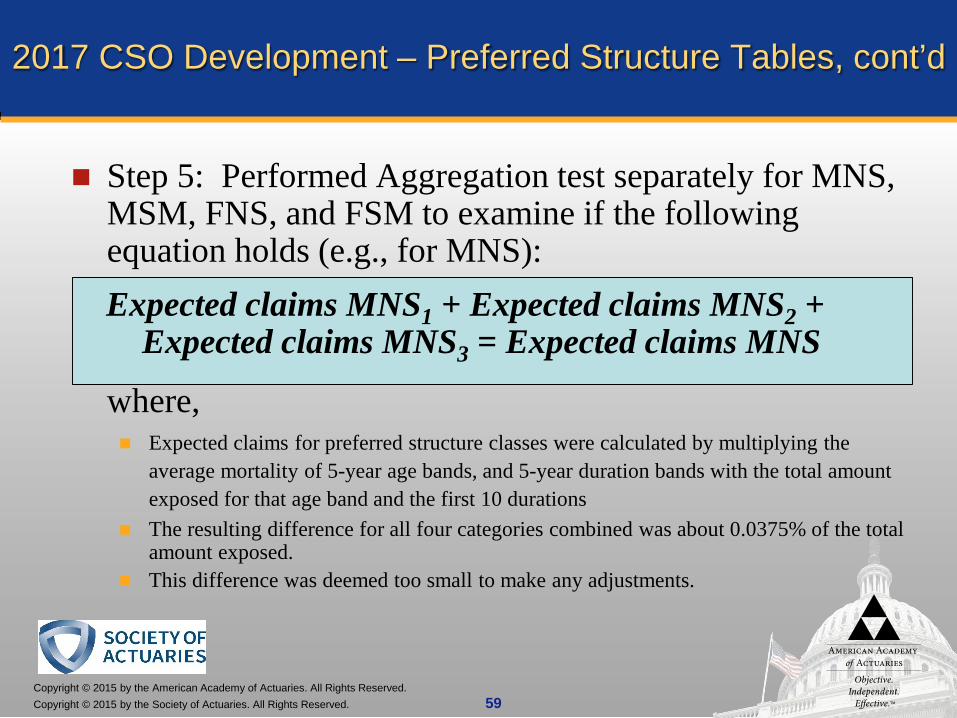

Step 5: Performed Aggregation test separately for MNS, MSM, FNS, and FSM to examine if the following equation holds (e.g., for MNS):Expected claims MNS1 + Expected claims MNS2 +

Expected claims MNS3 = Expected claims MNS

where, Expected claims for preferred structure classes were calculated by multiplying the

average mortality of 5-year age bands, and 5-year duration bands with the total amount exposed for that age band and the first 10 durations

The resulting difference for all four categories combined was about 0.0375% of the total amount exposed.

This difference was deemed too small to make any adjustments.

2017 CSO Development – Preferred Structure Tables, cont’d

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 60

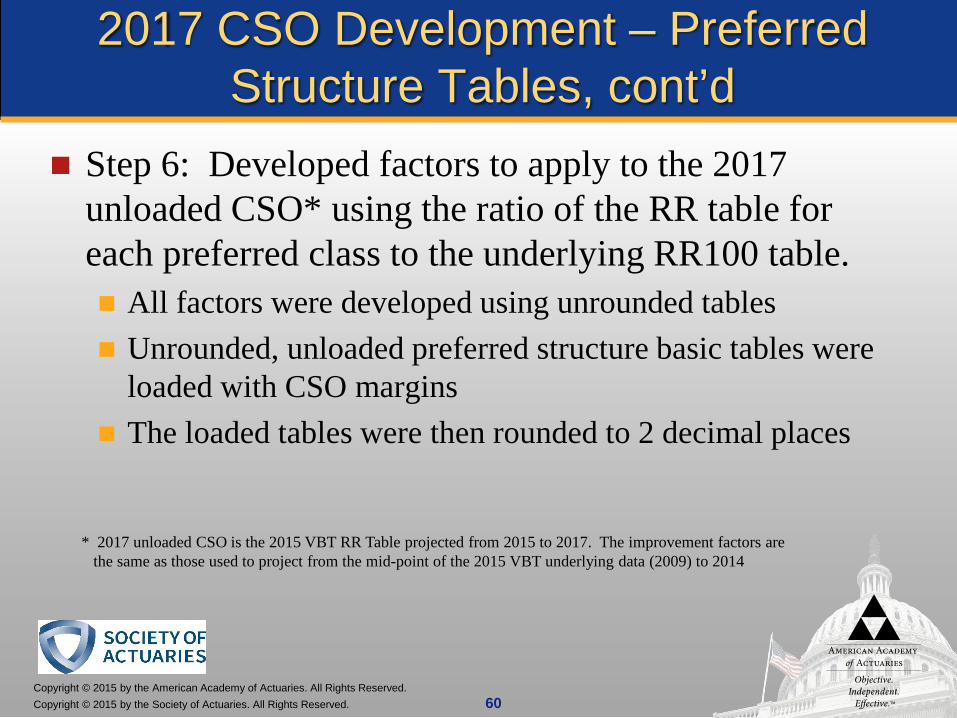

* 2017 unloaded CSO is the 2015 VBT RR Table projected from 2015 to 2017. The improvement factors are the same as those used to project from the mid-point of the 2015 VBT underlying data (2009) to 2014

2017 CSO Development – Preferred Structure Tables, cont’d

Step 6: Developed factors to apply to the 2017 unloaded CSO* using the ratio of the RR table for each preferred class to the underlying RR100 table. All factors were developed using unrounded tables Unrounded, unloaded preferred structure basic tables were

loaded with CSO margins The loaded tables were then rounded to 2 decimal places

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 61

Preferred Structure Loads

Proposed 2017 CSO preferred structure tables have same percentage load for all tables Arguments in favor of varying load by class:

Must ‘qualify’ to use the super preferred table, so lesser need for load Resulting volatility of mortality in residual class may be higher than the

aggregate CSO, suggesting potential for higher load Arguments against:

More complicated table construction Need to assure tables weight back to the aggregate CSO table

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 62

Preferred Structure Tables – Term Reserve ComparisonsSuper Preferred, Male, NS, Issue Age 40

* Select & Ultimate Table, 4.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 63

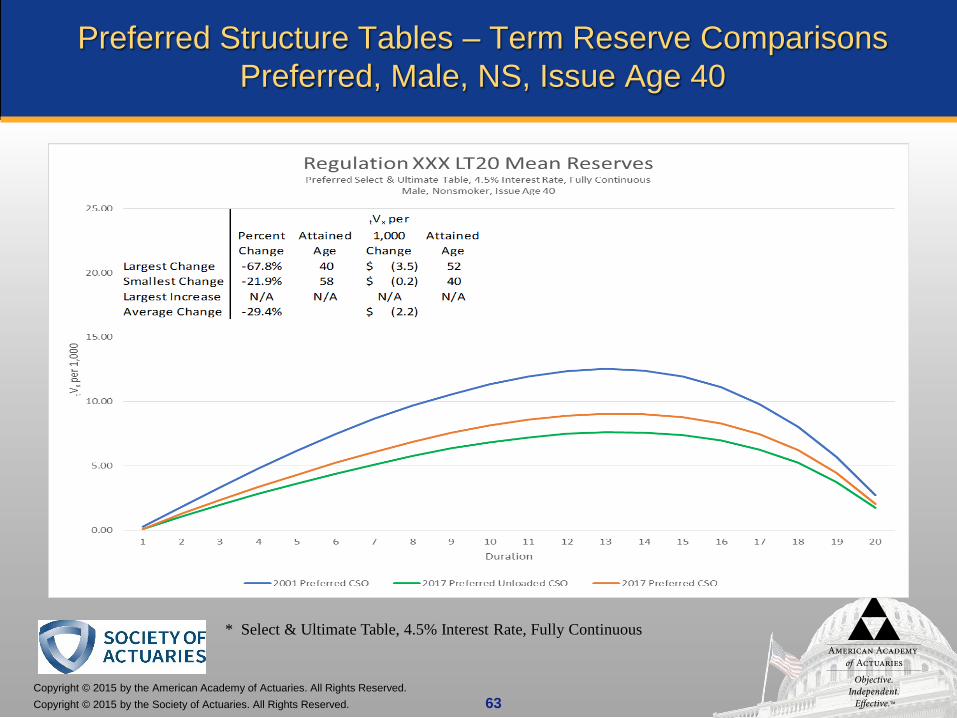

Preferred Structure Tables – Term Reserve ComparisonsPreferred, Male, NS, Issue Age 40

* Select & Ultimate Table, 4.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 64

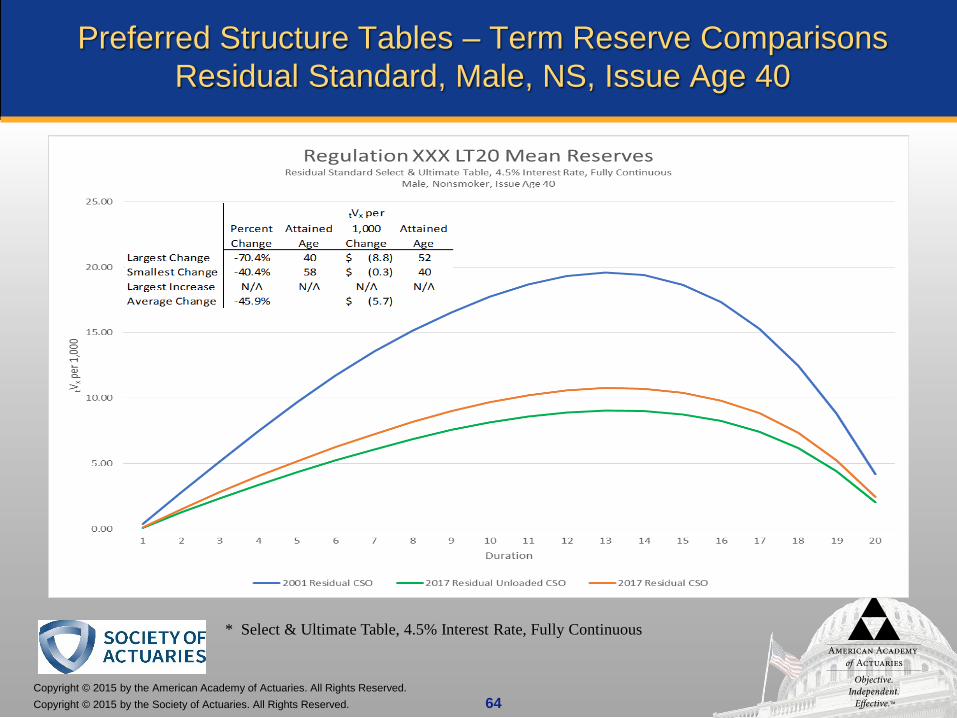

Preferred Structure Tables – Term Reserve ComparisonsResidual Standard, Male, NS, Issue Age 40

* Select & Ultimate Table, 4.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 65

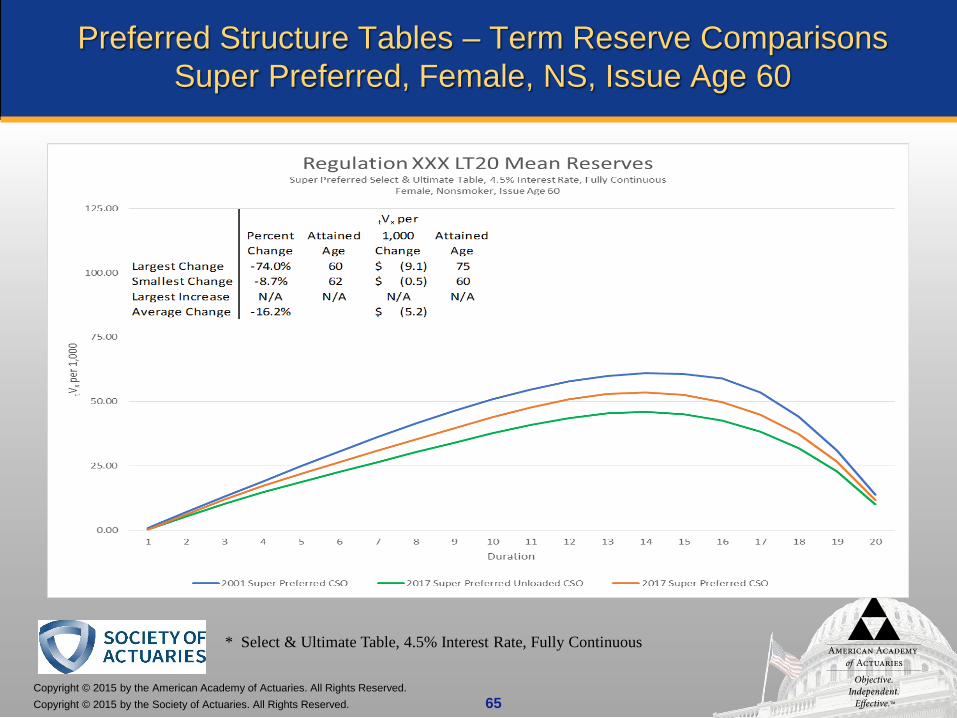

Preferred Structure Tables – Term Reserve ComparisonsSuper Preferred, Female, NS, Issue Age 60

* Select & Ultimate Table, 4.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 66

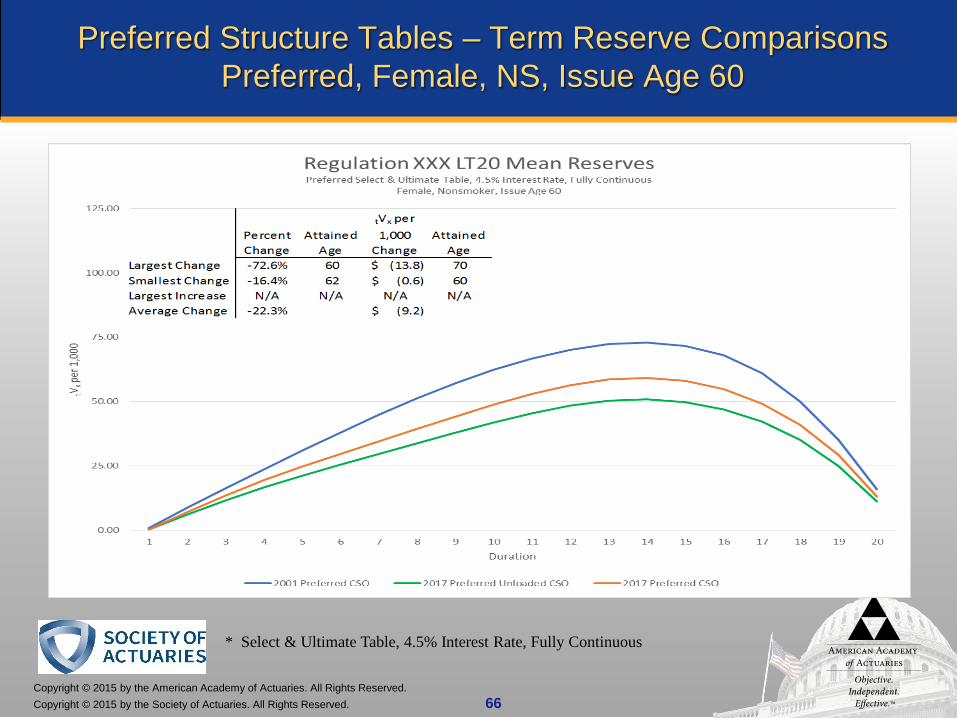

Preferred Structure Tables – Term Reserve ComparisonsPreferred, Female, NS, Issue Age 60

* Select & Ultimate Table, 4.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 67

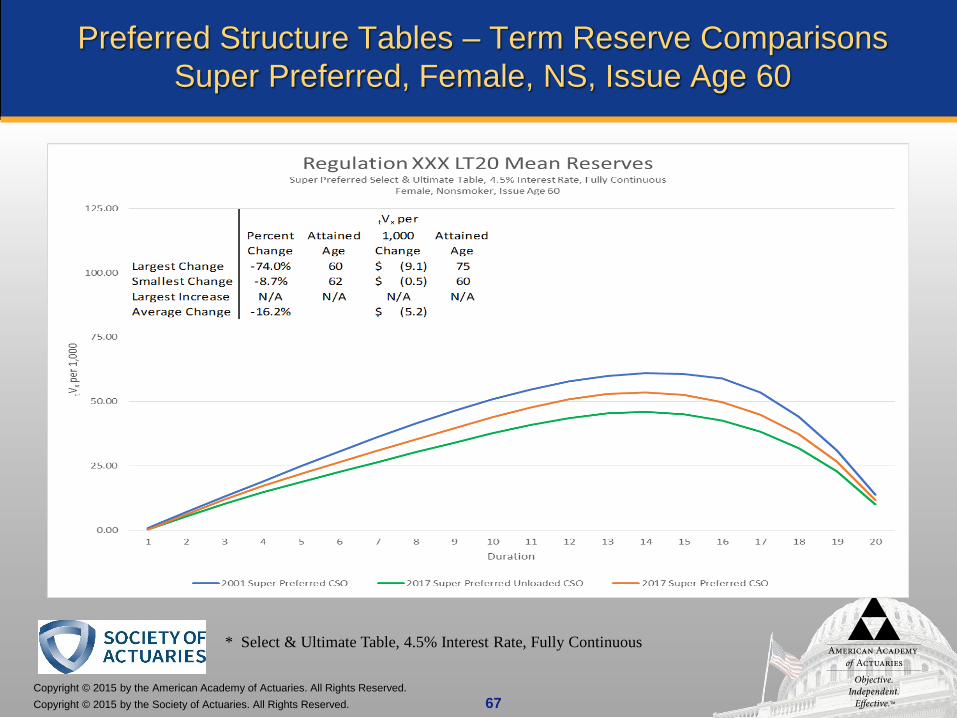

Preferred Structure Tables – Term Reserve ComparisonsSuper Preferred, Female, NS, Issue Age 60

* Select & Ultimate Table, 4.5% Interest Rate, Fully Continuous

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 68

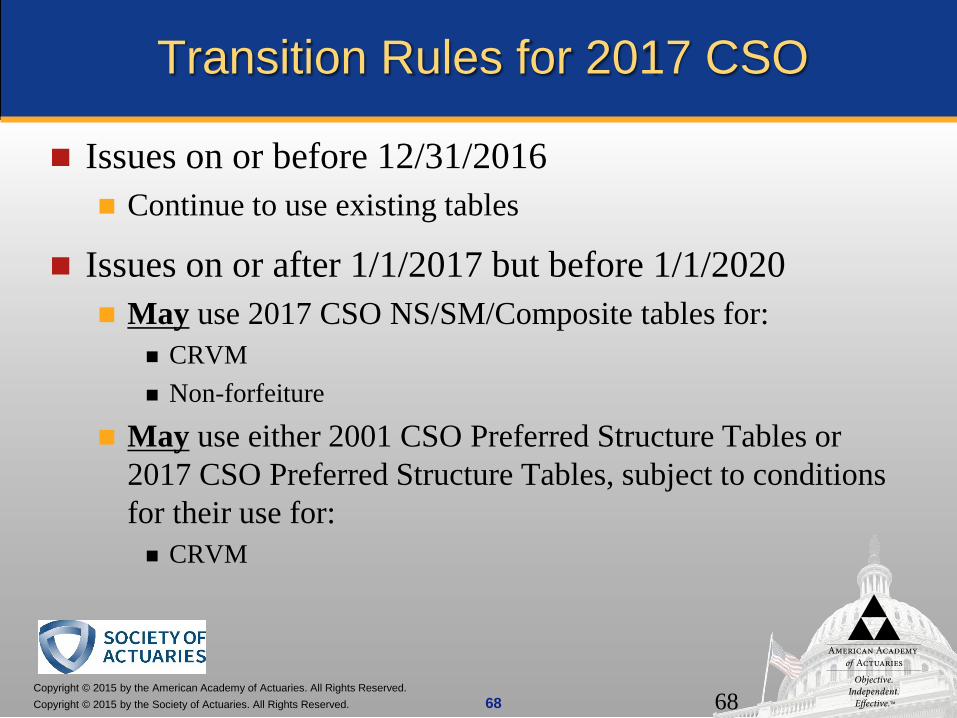

Transition Rules for 2017 CSO

Issues on or before 12/31/2016 Continue to use existing tables

Issues on or after 1/1/2017 but before 1/1/2020 May use 2017 CSO NS/SM/Composite tables for:

CRVM Non-forfeiture

May use either 2001 CSO Preferred Structure Tables or 2017 CSO Preferred Structure Tables, subject to conditions for their use for: CRVM

68

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 69

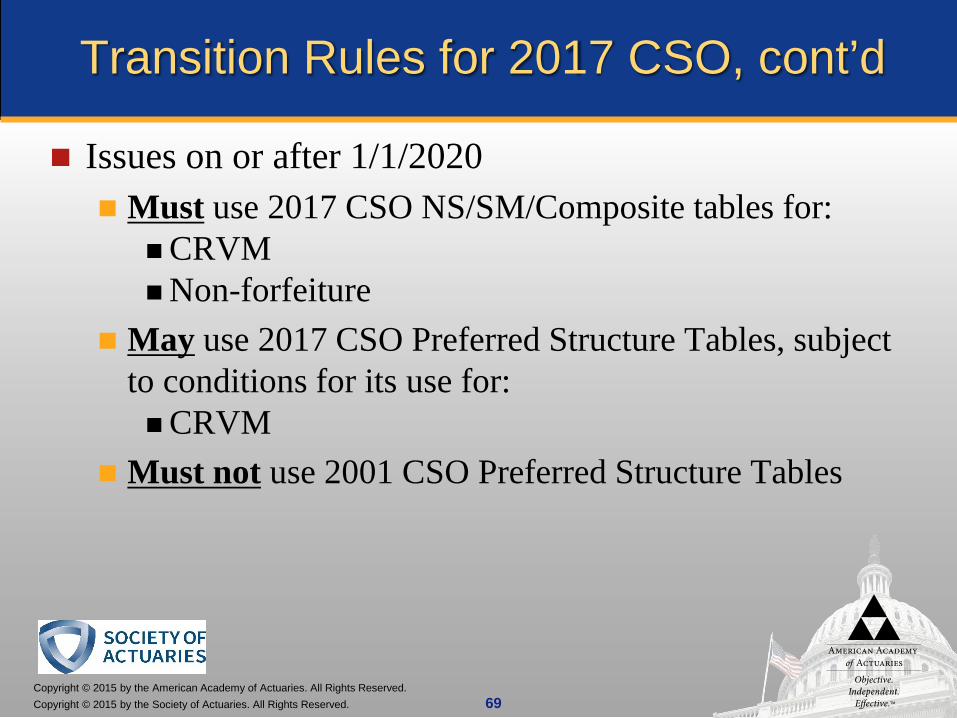

Transition Rules for 2017 CSO, cont’d

Issues on or after 1/1/2020 Must use 2017 CSO NS/SM/Composite tables for:

CRVMNon-forfeiture

May use 2017 CSO Preferred Structure Tables, subject to conditions for its use for:CRVM

Must not use 2001 CSO Preferred Structure Tables

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

Dieter Gaubatz

Underwriting Criteria Score Calculator

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 71

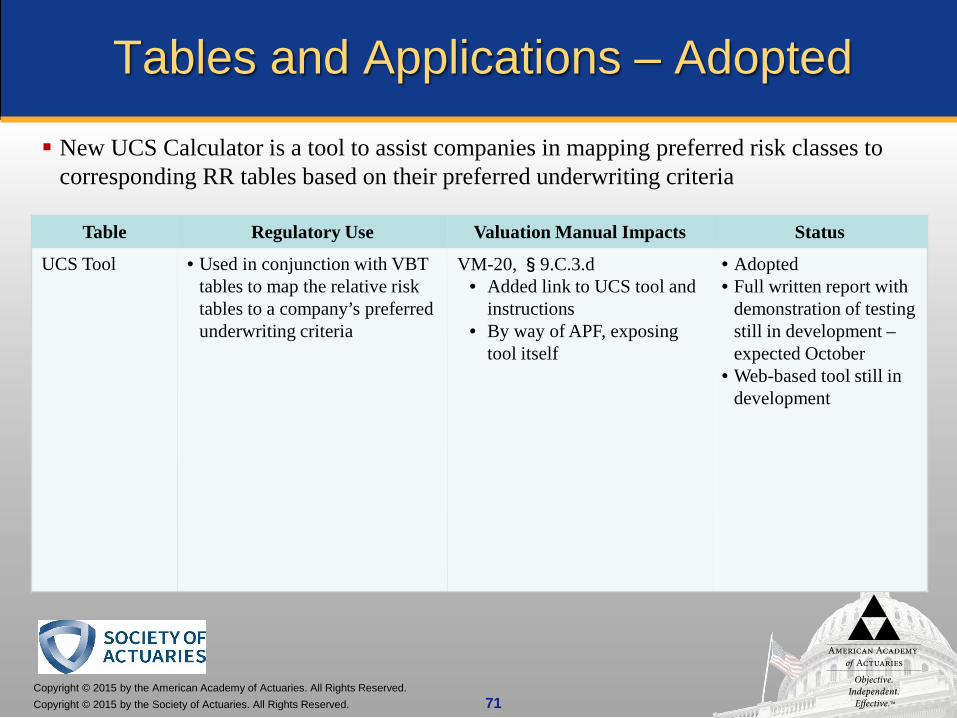

Tables and Applications – Adopted

Table Regulatory Use Valuation Manual Impacts Status

UCS Tool • Used in conjunction with VBT tables to map the relative risk tables to a company’s preferred underwriting criteria

VM-20, §9.C.3.d• Added link to UCS tool and

instructions• By way of APF, exposing

tool itself

• Adopted• Full written report with

demonstration of testing still in development –expected October

• Web-based tool still in development

New UCS Calculator is a tool to assist companies in mapping preferred risk classes to corresponding RR tables based on their preferred underwriting criteria

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 72

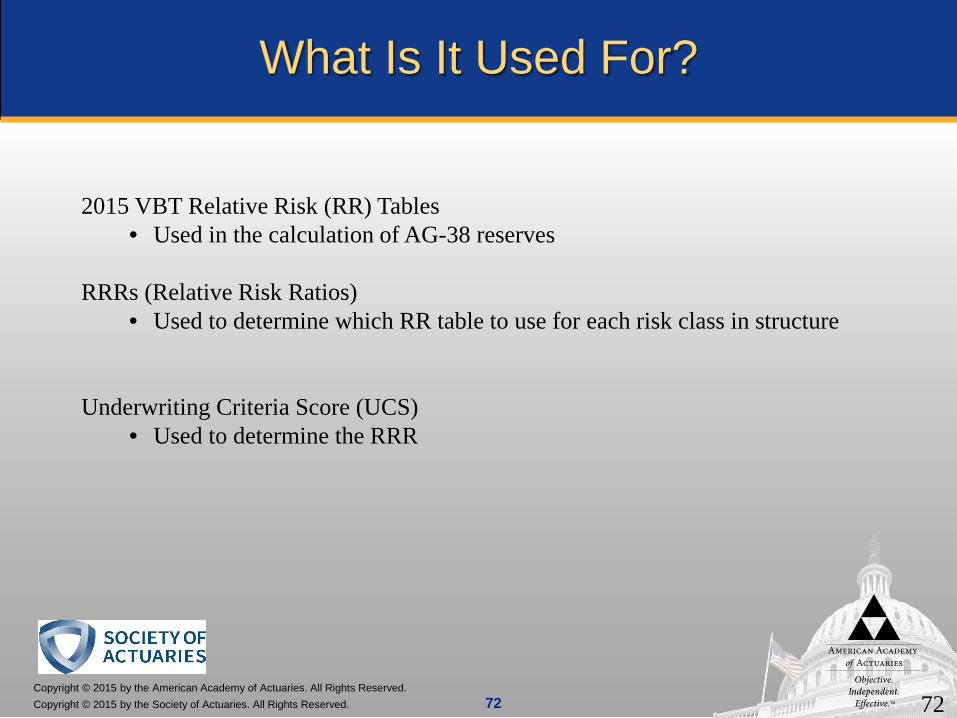

What Is It Used For?

72

2015 VBT Relative Risk (RR) Tables• Used in the calculation of AG-38 reserves

RRRs (Relative Risk Ratios) • Used to determine which RR table to use for each risk class in structure

Underwriting Criteria Score (UCS)• Used to determine the RRR

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 73

Definitions

RR(R)

• Relative Risk (Ratio)• Mortality as % of average standard mortality for a specific characteristic cell(i.e. risk class mortality compared to average mortality for a specific gender, smoking status, issue age and duration issued as a standard risk)

UCS

• Underwriting Criteria Score• Equals RRR (at issue) score for a particular risk class

• Standard definition: Not classified as sub-standard (doesn’t require a table rating or flat extra, nor declined) in the underwriting process

73

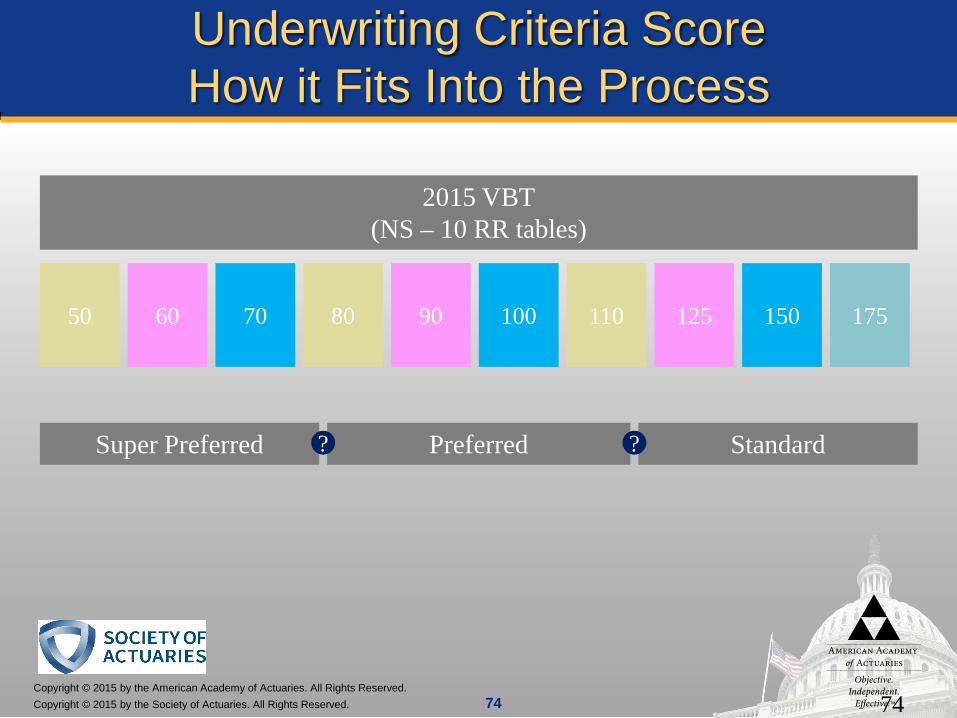

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 74

Underwriting Criteria ScoreHow it Fits Into the Process

2015 VBT(NS – 10 RR tables)

50 60 70 80 90 110 150100 125 175

Super Preferred Preferred Standard? ?

74

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 75

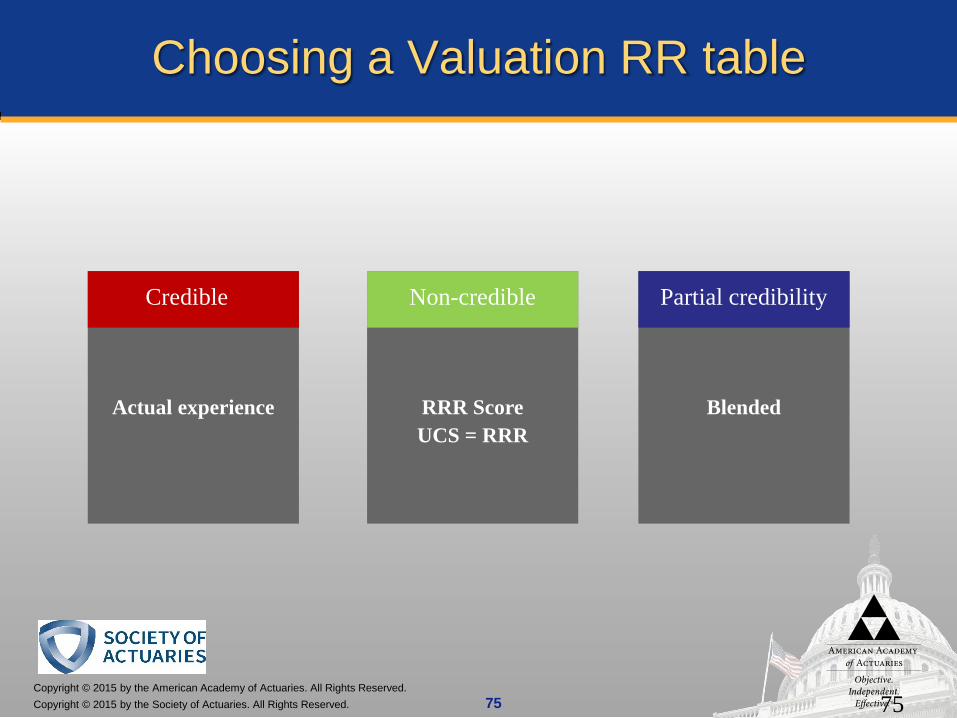

BlendedRRR Score UCS = RRR

Actual experience

Choosing a Valuation RR table

Credible Non-credible Partial credibility

75

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 76

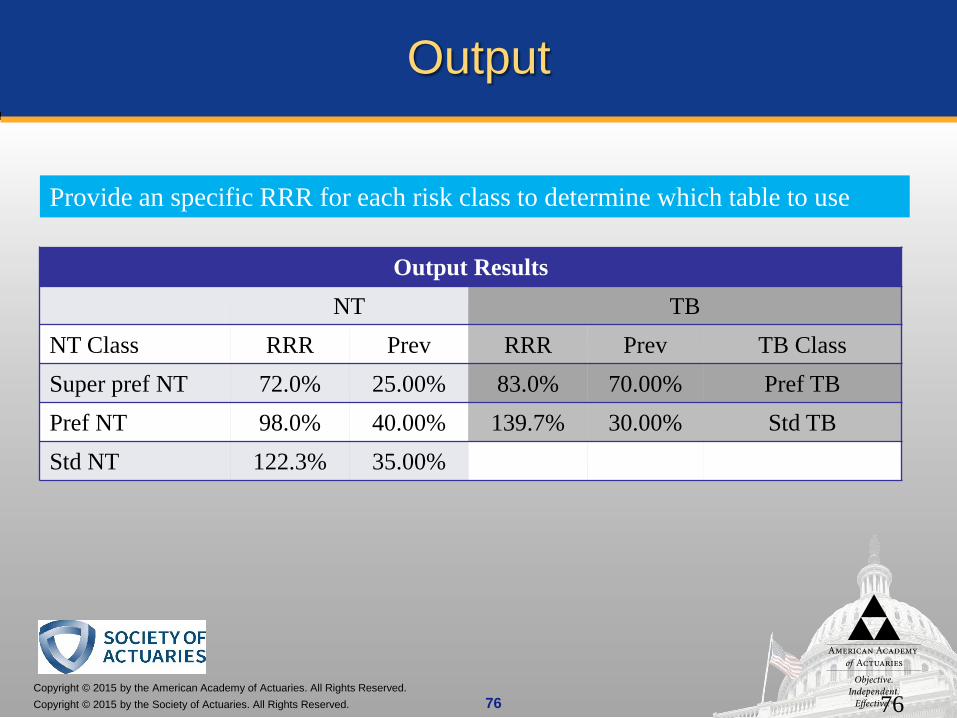

Output

Provide an specific RRR for each risk class to determine which table to use

Output ResultsNT TB

NT Class RRR Prev RRR Prev TB ClassSuper pref NT 72.0% 25.00% 83.0% 70.00% Pref TBPref NT 98.0% 40.00% 139.7% 30.00% Std TBStd NT 122.3% 35.00%

76

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 77

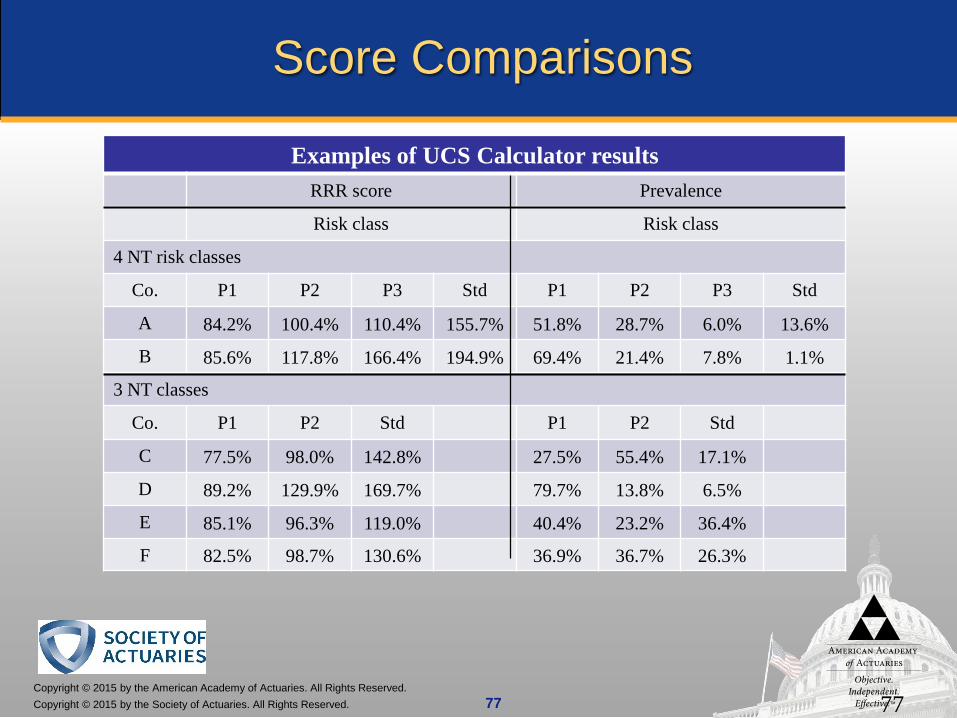

Score Comparisons

Examples of UCS Calculator resultsRRR score Prevalence

Risk class Risk class

4 NT risk classes

Co. P1 P2 P3 Std P1 P2 P3 Std

A 84.2% 100.4% 110.4% 155.7% 51.8% 28.7% 6.0% 13.6%

B 85.6% 117.8% 166.4% 194.9% 69.4% 21.4% 7.8% 1.1%

3 NT classes

Co. P1 P2 Std P1 P2 Std

C 77.5% 98.0% 142.8% 27.5% 55.4% 17.1%

D 89.2% 129.9% 169.7% 79.7% 13.8% 6.5%

E 85.1% 96.3% 119.0% 40.4% 23.2% 36.4%

F 82.5% 98.7% 130.6% 36.9% 36.7% 26.3%

77

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 78

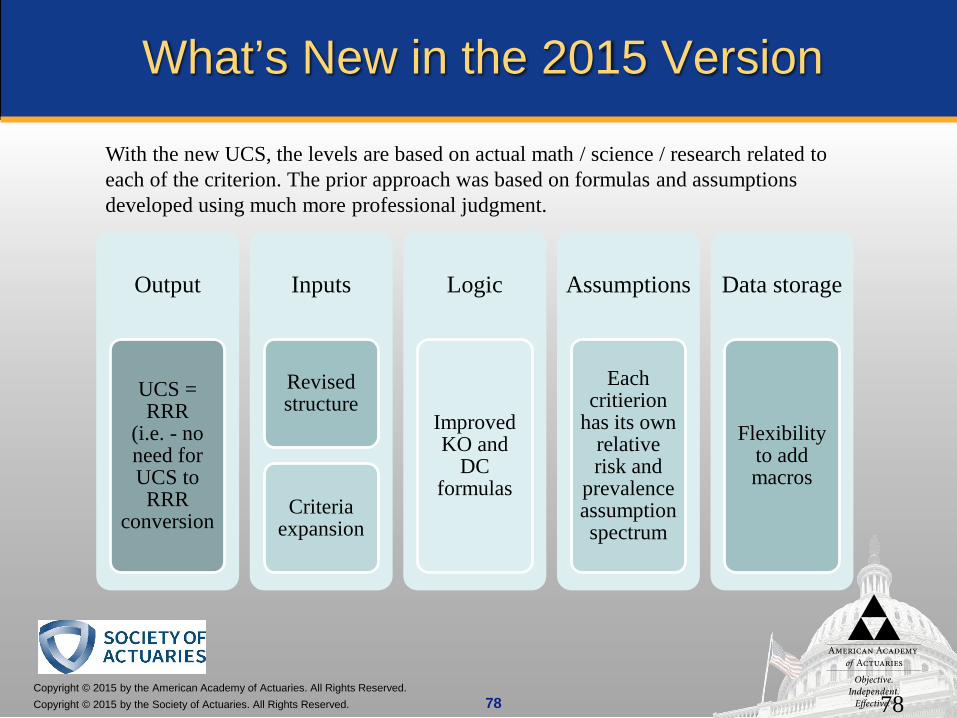

What’s New in the 2015 Version

Output

UCS = RRR

(i.e. - no need for UCS to RRR

conversion

Inputs

Revised structure

Criteria expansion

Logic

Improved KO and

DC formulas

Assumptions

Each critierion

has its own relative risk and

prevalence assumption spectrum

Data storage

Flexibility to add macros

78

With the new UCS, the levels are based on actual math / science / research related to each of the criterion. The prior approach was based on formulas and assumptions developed using much more professional judgment.

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 79

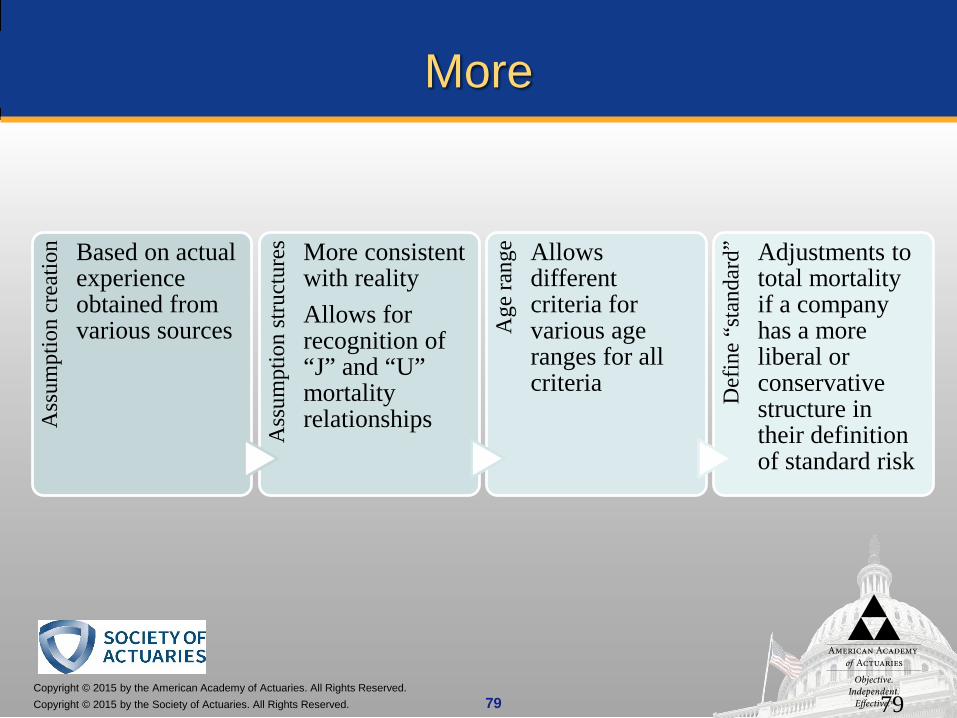

MoreA

ssum

ptio

n cr

eatio

n Based on actual experience obtained from various sources

Ass

umpt

ion

stru

ctur

es More consistent with realityAllows for recognition of “J” and “U” mortality relationships

Age

rang

e Allows different criteria for various age ranges for all criteria D

efin

e “s

tand

ard” Adjustments to

total mortality if a company has a more liberal or conservative structure in their definition of standard risk

79

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 80

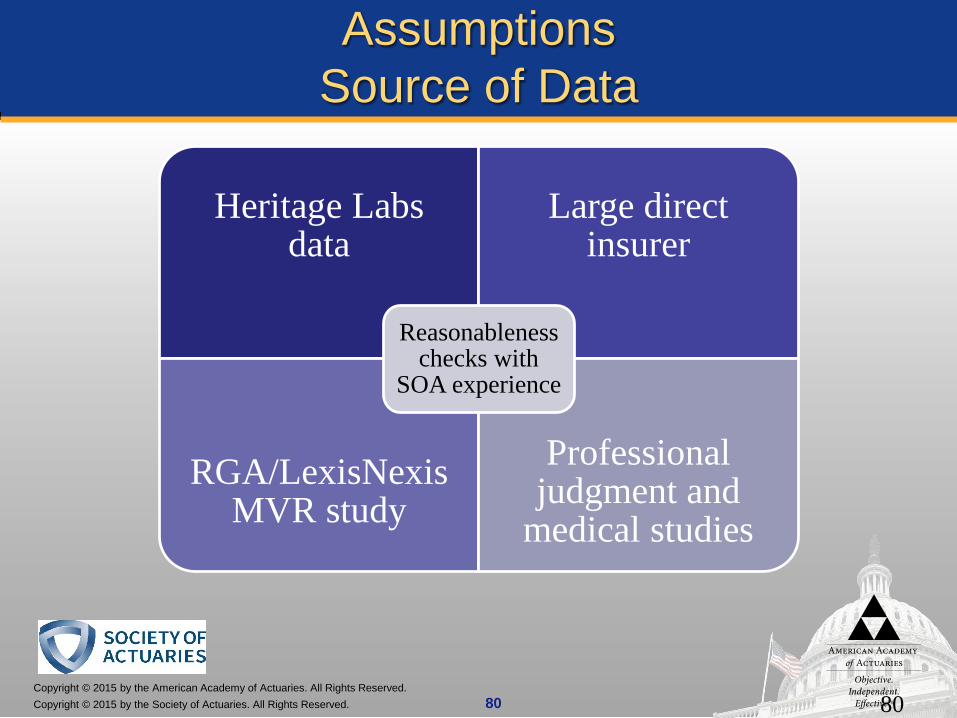

AssumptionsSource of Data

Heritage Labs data

Large direct insurer

RGA/LexisNexis MVR study

Professional judgment and

medical studies

Reasonableness checks with

SOA experience

80

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 81

0%

2%

4%

6%

8%

10%

12%

14%

0%

50%

100%

150%

200%

250%

300%

15 19 23 27 31 35 39

Prev

RRR

Prevalence

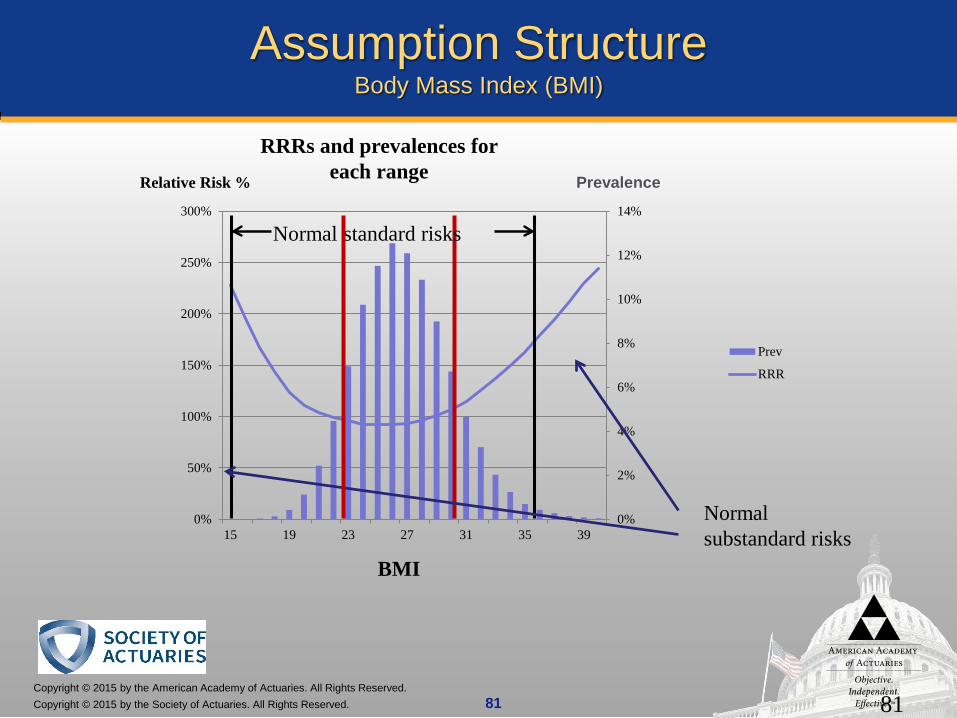

Assumption StructureBody Mass Index (BMI)

Relative Risk %

BMI

RRRs and prevalences for each range

Normal substandard risks

Normal standard risks

81

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 82

0%2%4%6%8%10%12%14%

0%50%

100%150%200%250%300%

15 19 23 27 31 35 39

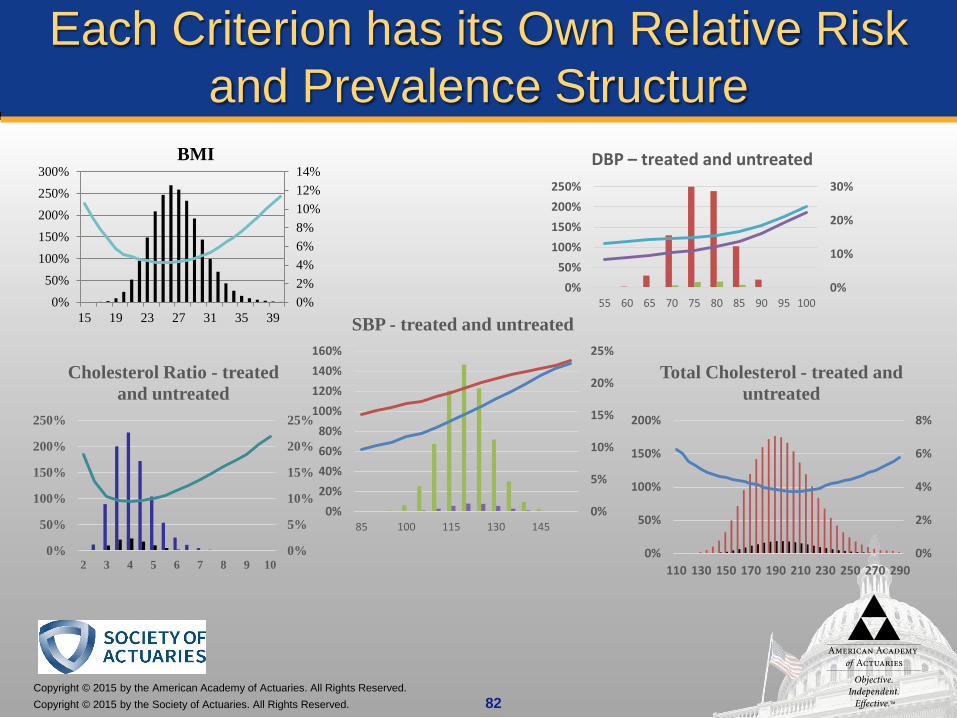

Each Criterion has its Own Relative Risk and Prevalence Structure

BMI

0%

10%

20%

30%

0%50%

100%150%200%250%

55 60 65 70 75 80 85 90 95 100

DBP – treated and untreated

0%

5%

10%

15%

20%

25%

0%

50%

100%

150%

200%

250%

2 3 4 5 6 7 8 9 10

Cholesterol Ratio - treated and untreated

0%

2%

4%

6%

8%

0%

50%

100%

150%

200%

110 130 150 170 190 210 230 250 270 290

Total Cholesterol - treated and untreated

0%

5%

10%

15%

20%

25%

0%20%40%60%80%

100%120%140%160%

85 100 115 130 145

SBP - treated and untreated

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 83

Input Changes

Criteria

Revised Structure

• Family history (coronary, cerebro)• Personal medical (coronary, cerebro, mental/nervous)

• Debit Credit and Knockout inputs combined• Flexible age banding• Multiple input structure • Conditional formatting• Separate NS/SM input worksheets

83

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 85

What’s Next?

Remaining work

Full reportWeb-based

chassis solution

85

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 86

Thanks to:Underwriting Criteria Team Members

Jaron Arboleda (MIB

representative)Jean-Marc Fix

(actuary)Kim Genik

(underwriter)Anna Hart

(underwriter)

Carl Holowaty (MD)

Doug Ingle (underwriter)

Al Klein (actuary)

Peter Komsthoeft

(underwriter)

Ev Kunzelman (underwriter)

Kevin Larsen (actuary)

Jack Luff (SOA actuary)

Cynthia MacDonald

(SOA actuary)

Brad Roudebush (actuary)

David Winsemius

(MD)David Wylde

(actuary)Dieter Gaubatz

– chair (actuary)

86

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved. 87

Calculation Logic – Combining CriteriaKnock-out

Risk Class RRR Prev

1 94% 74.1%2 109% 12.5%3 122% 13.4%

Risk Class RRR Prev

1 90% 60.0%2 105% 30.0%3 145% 10.0%

Risk Class Prev RRRBuild DBP RC Build DBP Final Build DBP Final

1 1 1 74.1% 60.0% 44.5% 94.4% 90.0% 85.0%1 2 2 74.1% 30.0% 22.2% 94.4% 105.0% 99.1%1 3 3 74.1% 10.0% 7.4% 94.4% 145.0% 136.9%2 1 2 12.5% 60.0% 7.5% 109.4% 90.0% 98.4%2 2 2 12.5% 30.0% 3.8% 109.4% 105.0% 114.8%2 3 3 12.5% 10.0% 1.3% 109.4% 145.0% 158.6%3 1 3 13.4% 60.0% 8.0% 122.1% 90.0% 109.9%3 2 3 13.4% 30.0% 4.0% 122.1% 105.0% 128.2%3 3 3 13.4% 10.0% 1.3% 122.1% 145.0% 177.1%

Build Diastolic BP

x = x =

Assumes independence

RC Prev RRR

1 44.5% 85.0%

2 33.5% 100.7%

3 22.1% 129.2%

sum

RRR is a sumproduct

© 2014 Munich American Reassurance Company. All rights reserved. 87

Copyright © 2015 by the American Academy of Actuaries. All Rights Reserved.Copyright © 2015 by the Society of Actuaries. All Rights Reserved.

Questions?Contact Information

Mary J. Bahna-Nolan, MAAA, FSA, CERAExecutive Vice President, Head of Life R&DSCOR Global [email protected](312) 544-5029

Dieter Gaubatz, MAAA, FSA, FCIA2nd Vice President, Client LiaisonMunich [email protected](770) 350-3278