session 22 equity. background on stockholders’ equity corporations are business entities...

TRANSCRIPT

Session 22

Equity

Background on Stockholders’ Equity

• Corporations are business entities authorized in accordance with state laws

• Stockholders have the right to:– Vote– Share in corporate profits– Share in any assets left at liquidation– Acquire more shares of subsequent issues of stock

• Stockholders vote to elect the board of directors

Background on Stockholders’ Equity

• A corporate proxy is a written authority granted by shareholders to have another party cast their votes at the annual meeting

• A preemptive right is the right to acquire a proportional amount of any new issue of capital stock

• Stockholders have limited liability– Creditors have claims only on the assets owned by the corporation

– Stockholders’ personal assets are not at risk

Authorized, Issued, and Outstanding Stock

• The articles of incorporation detail the number of shares and types of capital stock

• Shares can be:– Authorized—the total number of shares that can be issued

– Issued—the number of shares exchanged with stockholders

– Outstanding—the number of shares still held by the stockholders

• Treasury shares are shares of the corporation’s own stock which have been repurchased

Common Stock• Common stock represents the basic ownership

interest in a corporation. The stockholders bear the major risks and can reap the major rewards.

• Common stock frequently carries a "par value" set out in the Corporate Charter or Certificate of Incorporation. This amount is set by the Board of Directors and is typically quite small. It is irrelevant in a value sense - it does not measure value. It is set at a low value primarily for legal reasons.

• The issuing price of a share over and above the par value of the share is referred to as additional paid in capital or capital in excess of par value.

• Legal capital or contributed capital equals the par value plus additional paid in capital.

Stock values

• Par value:– A measure of protection of creditors establishing the minimum legal capital liability

• Book value– Historical accumulated accounting value of the stock (includes Additional paid-in earnings and retained earnings, and reserves...)

• Market value (FINANCE)– POSITIVE ACCOUNTING– Values the firm under completely different parameters

Accounting for Stock Issuance

• Many companies separate their contributed stock recognition into two categories:– Par value– Additional paid-in capital—the amount above par value

• If UPS issues an additional 1 million shares of its $.01 par value stock at $63, the journal entry is:

Cash 63,000,000Common stock at par 10,000

Additional paid-in capital 62,990,000

Cash 63,000,000Common stock at par 10,000

Additional paid-in capital 62,990,000

Cash Dividends

• Dividends are proportional distributions of income to shareholders

• To pay cash dividends a corporation must have:– Cash– Retained earnings

• Dividends must be declared by the board of directors—they are not automatic

Cash Dividends

• There are three important dates associated with dividends:– Date of declaration—the date when dividends are announced by the board

– Date of record—stockholders owning stock on this date receive the dividend

– Date of payment—the date the company makes payment

Cash Dividends

• A company declares a $20,000 cash dividend on September 26 to be paid on November 15 to the October 25 stockholders of record. The journal entries are:

Sept. 26 Retained earnings 20,000Dividends payable 20,000

To record the dividend declaration

Sept. 26 Retained earnings 20,000Dividends payable 20,000

To record the dividend declaration

Nov. 15 Dividends payable 20,000Cash 20,000

To record payment of dividends

Nov. 15 Dividends payable 20,000Cash 20,000

To record payment of dividends

Preferred Stock• Preferred stock offers owners different rights and preferential treatment– Dividend preference—preference over dividend claims of common stockholders

– Liquidation preference—preference to assets in the event of a liquidation

– Preferred stock does not normally have voting rights

• Par value is significant for preferred stock in cases in which the dividend is stated as a % of par and/or when the amount due at liquidation is tied to par.

• Preferred stock is accounted for in the same way as common stock.

Preference in Liquidation

• Preferred stock usually has a liquidation value– The liquidation value must be paid to preferred stockholders before distributions to common stockholders when a company is liquidated

– The liquidation value is often the same as par value

• The company must pay off all debts first

• There is less risk associated with preferred stock than common stock

Other Features of Preferred Stock

• Participating preferred stock receives a fixed dividend but can receive dividends above this amount if the company has a good year

• Callable preferred stock gives the company the right to redeem the stock at a certain call price

• Convertible preferred stock gives the owner the option to exchange the preferred shares for common shares

Stock Warrants

• Long-term call options on the issuing firm’s stock. Call options give their holders the right to buy shares of the firm at a specified price for a given period of time. These options are frequently included as part of a unit offering, which includes two or more securities offered as a package (e.g. attached to bonds or preferred stock as an "equity kicker" or "sweetener”) and issued to the general public. If the warrants are detachable a separate value is assigned and recorded by the corporation.

Employee Stock Options

• Stock options are rights to purchase a specific number of shares of a corporation's capital stock at a specific price for a specific time period

• Stock options vest when an employee remains with the company for a specific time period

• Once vested, an employee may exercise options anytime before they expire (usually about 5 years)

• Stock options are used as a form of employee compensation (expense)

Employee Stock Options

• Definitions– Grant date is the date that a company gives a stock option to an employee.

– Exercise date is the date that an employee exchanges the option and cash for shares of common stock.

– Exercise price or strike price is the price specified in the stock option contract for purchasing the common stock.

– Vesting period is the period that must expire before the employee is entitled to exercise an option to acquire the firm’s stock

Employee Stock Options

• Suppose in 2002 UPS grants options to purchase 30,000 shares of its $.01 par value common stock at $60. The estimated value of each option is $7. The options can be exercised over a 3-year period starting 5 years from the date of grant. The 2002 journal entry is:

Compensation expense, stock options 210,000* Additional paid-in capital 210,000Compensation expense, stock options 210,000* Additional paid-in capital 210,000

*30,000 x $7 = $210,000*30,000 x $7 = $210,000

Employee Stock Options

• Now suppose executives exercise all options 5 years after the date of grant. The journal entry in 2007 would be:

Cash 1,800,000*Common stock 300**Additional paid-in capital 210,000

Cash 1,800,000*Common stock 300**Additional paid-in capital 210,000

*30,000 x $60 = $1,800,000

**30,000 x $.01 = $300

*30,000 x $60 = $1,800,000

**30,000 x $.01 = $300

Restricted Stock

• Granting restricted stock is like paying employees with common stock instead of cash– Employees cannot sell the stock until it vests

– The stock is generally sold back to the company at the prevailing market price

• The company records compensation expense and an increase to paid-in capital

• Employees holding restricted stock receive dividends if declared

Stock Splits

• A two-for-one stock split involves issuing an additional share for each share currently owned

• The number of shares outstanding double and the par value decreases by 50%

• Total stockholders’ equity remains unchanged

• The market price should drop 50%• Companies split their stock in order to make their shares more affordable to small investors

Stock Dividends• Dividends paid in the corporation’s own shares of common stock

• Require the transfer of an amount from retained earnings to paid-in capital

• Result in issuance of additional shares of stock to each shareholder in proportion to their current holdings.

• Such "dividends" are issued to:– relieve pressure for cash dividends in the future or

– signal an increase in total cash dividends, if the cash dividend per share is kept constant.

• Share prices often do not fall commensurately after issuance of a stock dividend.

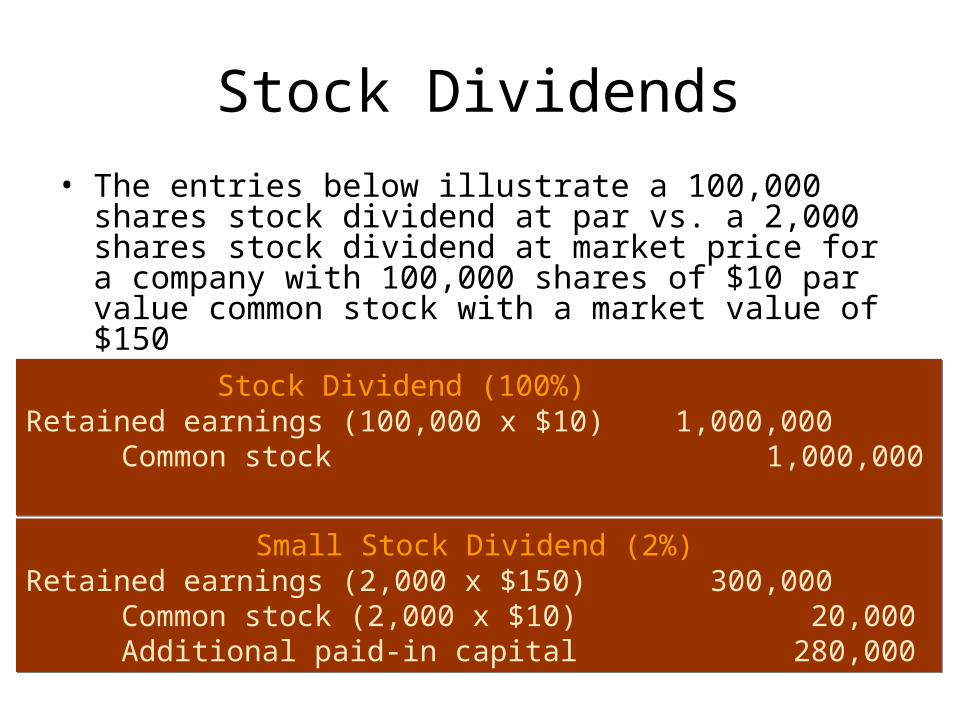

Stock Dividends• The entries below illustrate a 100,000 shares stock dividend at par vs. a 2,000 shares stock dividend at market price for a company with 100,000 shares of $10 par value common stock with a market value of $150

Stock Dividend (100%) Retained earnings (100,000 x $10) 1,000,000

Common stock 1,000,000

Stock Dividend (100%) Retained earnings (100,000 x $10) 1,000,000

Common stock 1,000,000

Small Stock Dividend (2%)Retained earnings (2,000 x $150) 300,000

Common stock (2,000 x $10) 20,000 Additional paid-in capital 280,000

Small Stock Dividend (2%)Retained earnings (2,000 x $150) 300,000

Common stock (2,000 x $10) 20,000 Additional paid-in capital 280,000

Repurchase of Shares• Companies repurchase shares because they:

– Want to retire the stock– Think the stock is undervalued by the market (“investment”)

– Want to change to proportion of debt and equity in the company

– Need shares to distribute in a stock option plan

– Want to return cash to shareholders without creating expectations for permanent increases in dividends

– Defensive measure in takeover bids.• Repurchased shares also increases EPS• Upon repurchase, the treasury stock is generally recorded at cost.

• Purchased with the intent to resell.

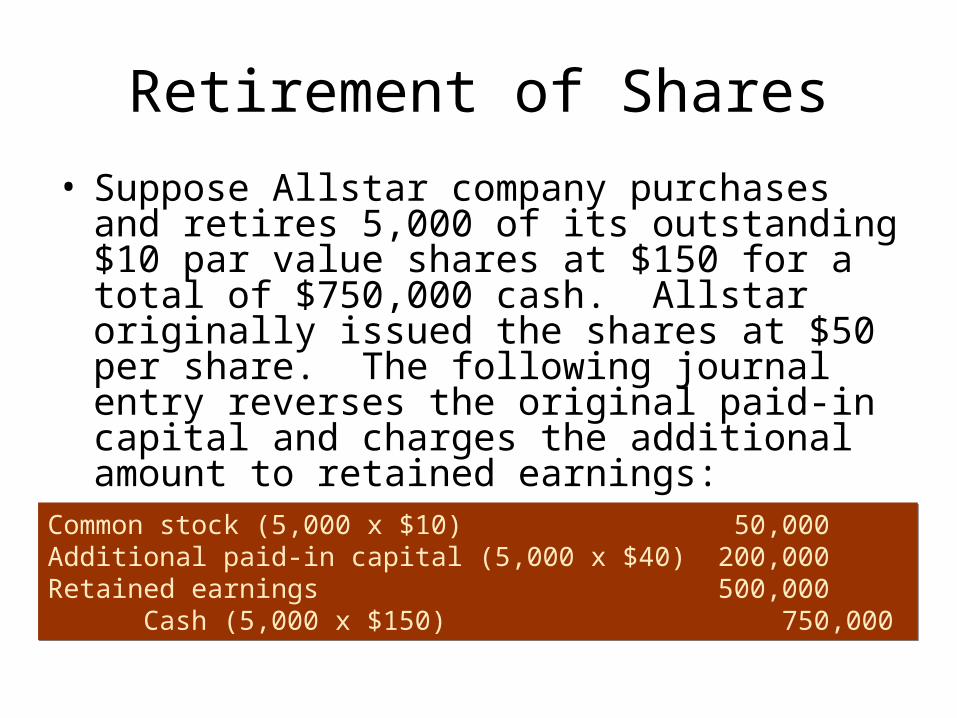

Retirement of Shares

• Suppose Allstar company purchases and retires 5,000 of its outstanding $10 par value shares at $150 for a total of $750,000 cash. Allstar originally issued the shares at $50 per share. The following journal entry reverses the original paid-in capital and charges the additional amount to retained earnings:

Common stock (5,000 x $10) 50,000Additional paid-in capital (5,000 x $40) 200,000 Retained earnings 500,000

Cash (5,000 x $150) 750,000

Common stock (5,000 x $10) 50,000Additional paid-in capital (5,000 x $40) 200,000 Retained earnings 500,000

Cash (5,000 x $150) 750,000

Treasury Stock

• Now suppose Allstar in the previous example decides to temporarily hold the repurchased shares rather than retiring them. The journal entry for the repurchase of the shares is:

• Treasury stock is a contra stockholder equity account—not an asset

Treasury stock (5,000 x $150) 750,000Cash 750,000

Treasury stock (5,000 x $150) 750,000Cash 750,000

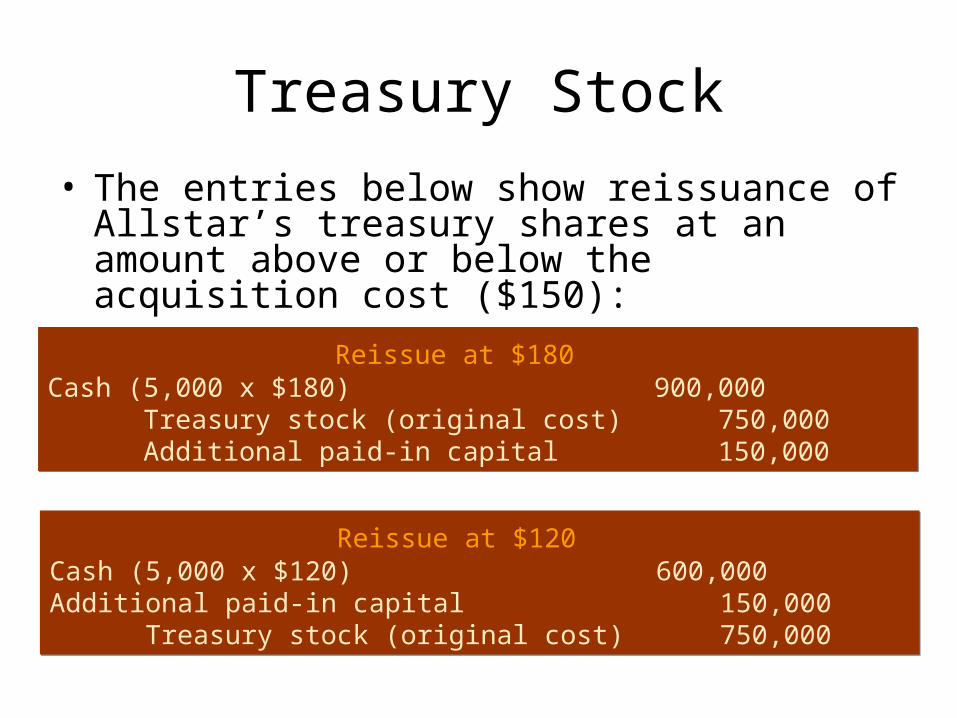

Treasury Stock

• The entries below show reissuance of Allstar’s treasury shares at an amount above or below the acquisition cost ($150):

Reissue at $180Cash (5,000 x $180) 900,000

Treasury stock (original cost) 750,000Additional paid-in capital 150,000

Reissue at $180Cash (5,000 x $180) 900,000

Treasury stock (original cost) 750,000Additional paid-in capital 150,000

Reissue at $120Cash (5,000 x $120) 600,000Additional paid-in capital 150,000

Treasury stock (original cost) 750,000

Reissue at $120Cash (5,000 x $120) 600,000Additional paid-in capital 150,000

Treasury stock (original cost) 750,000

Other Issuances of Common Stock

• Common stock is not always issued for cash

• Common stock can also be issued in:– Noncash exchanges for assets or services– Conversions of convertible bonds or preferred stock

• Common Stock can also increase through pure accounting changes:– Change some of the Retained Earnings/Reserves into Common Stock

Retained Earnings Restrictions

• State laws or contractual obligations often restrict retained earnings (and assets) for the protection of creditors

• Example: Dividends cannot be paid out to the point that retained earnings is less than the cost of treasury stock

• Companies can disclose restrictions by:– Footnotes– A line item on the balance sheet called restricted or appropriated retained earnings

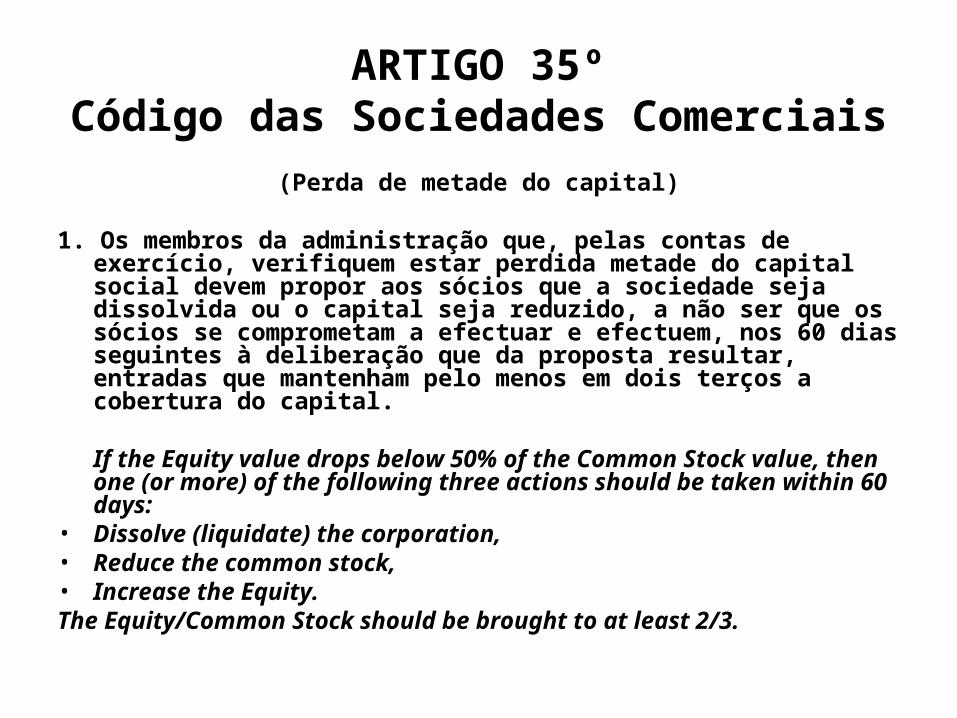

ARTIGO 35ºCódigo das Sociedades Comerciais

(Perda de metade do capital)

1. Os membros da administração que, pelas contas de exercício, verifiquem estar perdida metade do capital social devem propor aos sócios que a sociedade seja dissolvida ou o capital seja reduzido, a não ser que os sócios se comprometam a efectuar e efectuem, nos 60 dias seguintes à deliberação que da proposta resultar, entradas que mantenham pelo menos em dois terços a cobertura do capital.

If the Equity value drops below 50% of the Common Stock value, then one (or more) of the following three actions should be taken within 60 days:

• Dissolve (liquidate) the corporation,• Reduce the common stock,• Increase the Equity.The Equity/Common Stock should be brought to at least 2/3.

Convertible Bonds

• Bonds are sometimes issued with a feature that allows holders to convert the bond into common stock. Convertible bonds provide the comfort of a guaranteed return (from the bond) but allow the holder to become a common stockholder if that option becomes attractive. This conversion feature causes the bond to carry a lower interest rate.