session 2: smart electrification of end-use sectors

TRANSCRIPT

Session 2: Smart Electrification of End-Use Sectors –Implications for the Power System

Organised in partnership with EPRI

MONDAY, 05 OCTOBER 2020 • 17:00 - 20:00 (CEST)

Please make sure to mute yourself

during the session to avoid background

noise

If you have questions for our panelists, please

use the Q&A

If you encounter any technical issues, please

write your issue to Cisco Webex

Events

This session will be recorded and

recording along with the slides will be available on the Innovation Week

website

Session Overview

3

All times in Central European Standard Time (GSM+2)

Setting the Scene17:00 –17:05

Panel I: Global Experience17:05 – 17:30

Panel II: Smart Electrification at DSO Level17:30 – 18:20

Digital Break18:20 – 18:35

Panel III: Smart Electrification at the TSO Level18:35 – 19:25

Panel IV: New Power Sector Dynamics with Smart Electrification19:25 – 19:55

Closing Remarks19:55 – 20:00

Setting the Scene

Setting the scene

5

Francisco Boshell

Energy Analyst, Renewable Energy Technology Markets and

Standards, IRENA Innovation and Technology Centre

6

Innovation Week 2018: Solutions for Power Systems Flexibility

Source: IRENA (2020), Global Renewables Outlook: Energy transformation 2050

Power sector:

• Next frontier –integrating very high shares of variable renewables

• Many innovative solutions are emerging

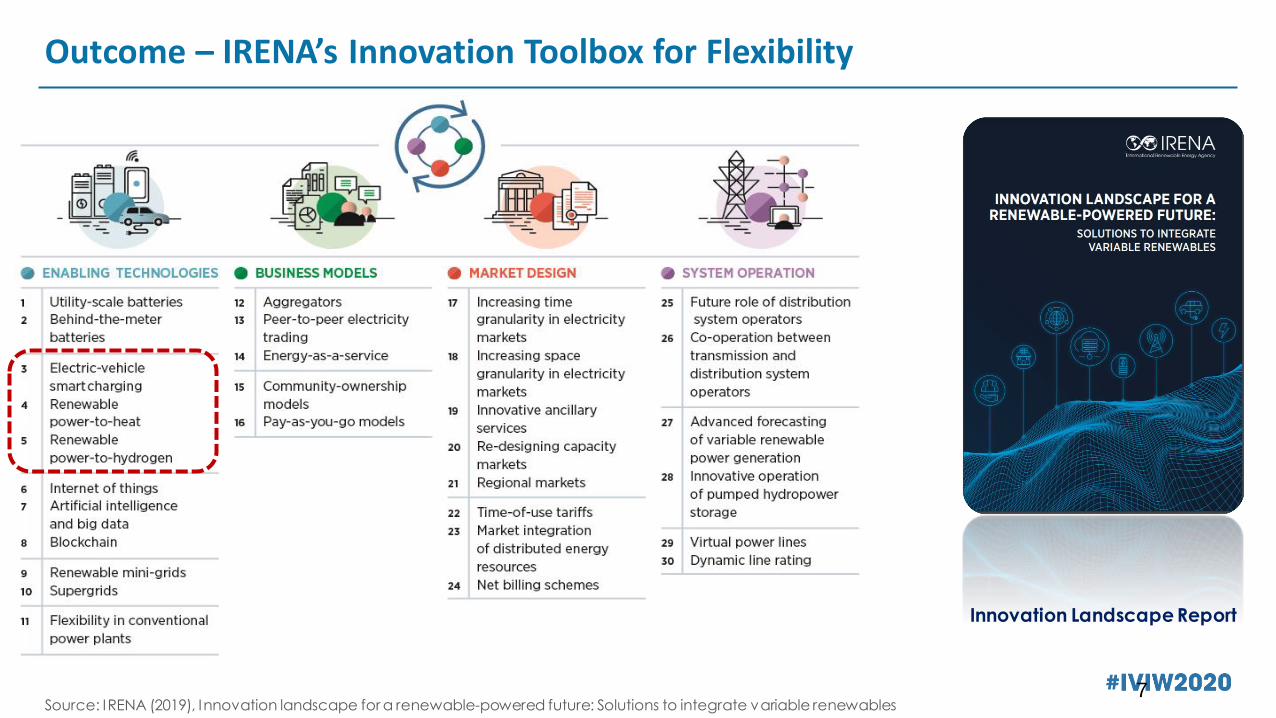

Innovation Landscape Report

7Source: IRENA (2019), Innovation landscape for a renewable-powered future: Solutions to integrate variable renewables

Outcome – IRENA’s Innovation Toolbox for Flexibility

8

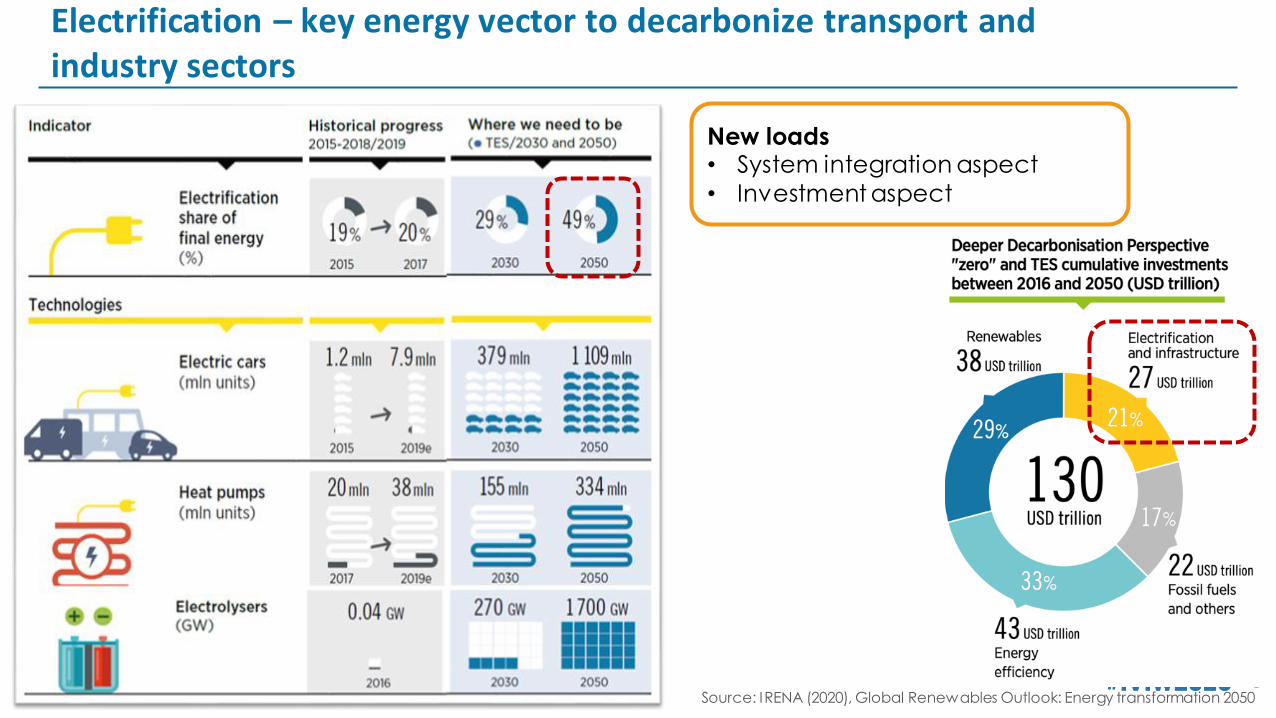

Electrification – key energy vector to decarbonize transport and industry sectors

New loads• System integration aspect

• Investment aspect

Source: IRENA (2020), Global Renewables Outlook: Energy transformation 2050

9

Smart technology resulting in smart solutions

•adapting the load profiles to the needs of consumers (demand) as well as to the conditions of the power system (supply)

What is smart electrification?

Example of smart charging for electric vehicles

Source: IRENA (2019) Innovation Outlook: Smart charging for

Electric Vehicles

10

Systemic innovation for smart electrification

Source: IRENA (2019), Innovation landscape for a renewable-powered future: Solutions to integrate variable renewables

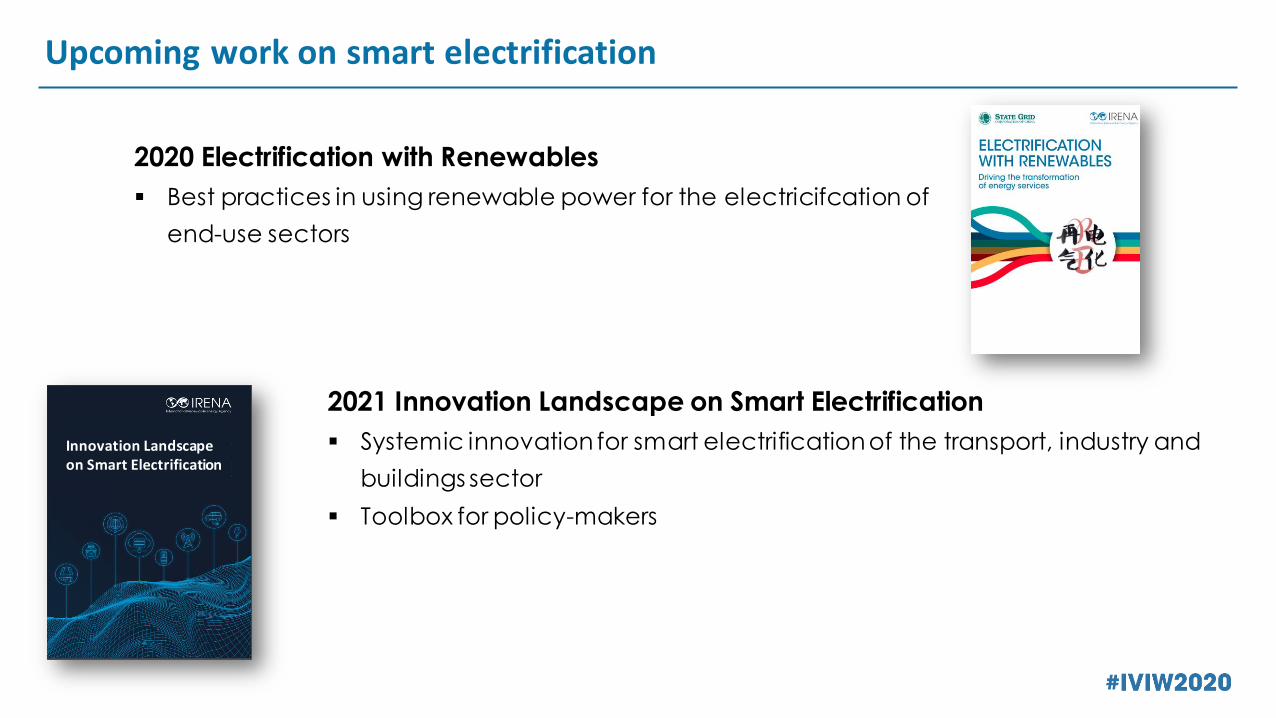

Upcoming work on smart electrification

2021 Innovation Landscape on Smart Electrification

▪ Systemic innovation for smart electrification of the transport, industry and

buildings sector

▪ Toolbox for policy-makers

Innovation Landscape on Smart Electrification

2020 Electrification with Renewables

▪ Best practices in using renewable power for the electricifcation of

end-use sectors

Panel I: Global Experience

Closing remarks

Francisco Boshell

Energy Analyst

Robert Chapman

Vice President of Electrification

& Sustainable Energy Strategy

Moderator

Kristian Ruby

Secretary General

Panelists

Dr Koshichi Nemoto

Vice President

EURELECTRICEPRIIRENA CRIEPI

Panel II: Smart Electrification at DSO Level

Closing remarks

Kristian Ruby

Secretary General

EURELECTRIC

Bastian Pfarrherr

Head of Innovation

Management

Stromnetz Hamburg

Moderator

Katie Sloan

Director of eMobility and

Building Electrificaiton

Southern California Edison

Panelists

Gregory Poilasne

Co-founder & CEO

Nuvve

Sandra Trittin

Co-Founder & CSO

Tiko Energy Solutions

Closing remarks

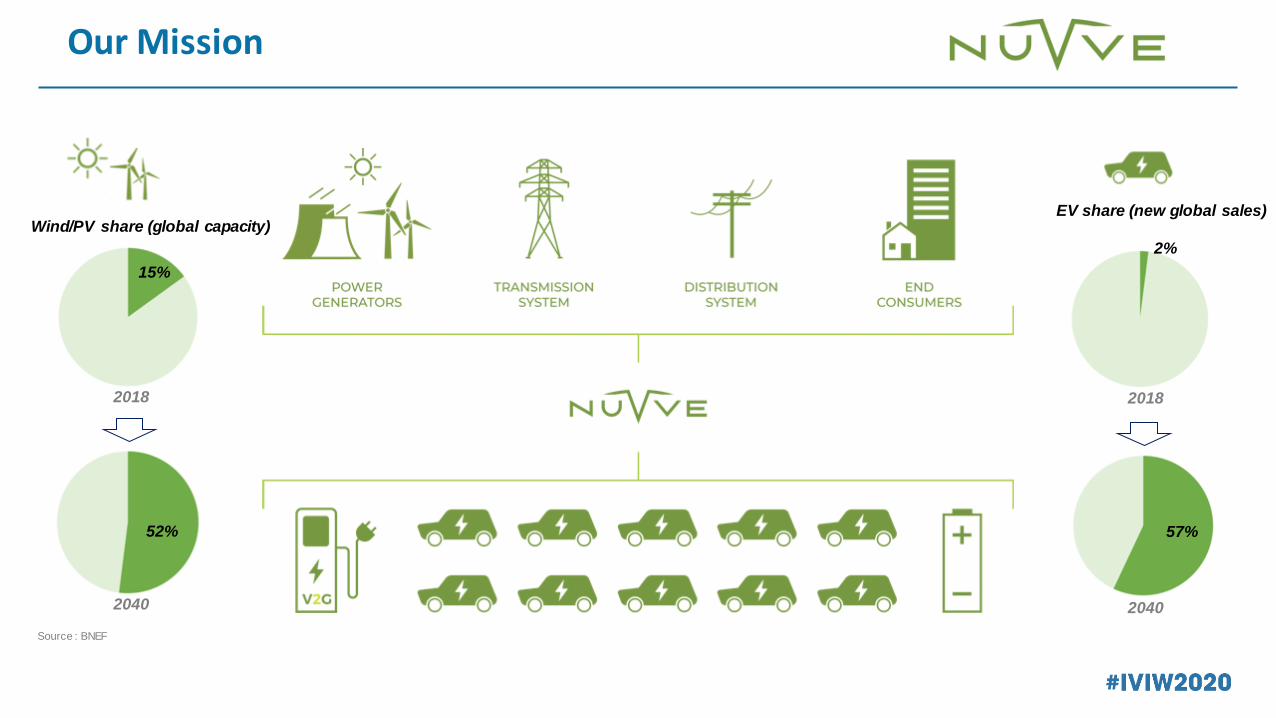

Our Mission

Wind/PV share (global capacity) EV share (new global sales)

52%

15%

2%

57%

2018

2040

2018

2040

Source : BNEF

Nuvve’s Platform and Services

Stabilizes the grid

Reduces the cost of EV

ownership, encourages EV

adoption

Guarantees vehicle use for

transportation

Optimizes and protects the

vehicle battery

Transforms electric vehicles from

unreliable resources into reliable,

dispatchable and monetizable

assets.

Enables increased renewable

penetration

Closing remarks

Kristian Ruby

Secretary General

EURELECTRIC

Bastian Pfarrherr

Head of Innovation

Management

Stromnetz Hamburg

Moderator

Katie Sloan

Director of eMobility and

Building Electrificaiton

Southern California Edison

Panelists

Gregory Poilasne

Co-founder & CEO

Nuvve

Sandra Trittin

Co-Founder & CSO

Tiko Energy Solutions

Digital BreakComing up next:

Panel III - Smart Electrification at TSO Level

Panel III: Smart Electrification at TSO Level

18:40 –19:30 (CEST)

Closing remarksNorela Constantinescu

Manager for Research &

Innovation

ENTSO-E

Anders Bavnhøj Hansen

Chief Engineer

Energinet Denmark

Pablo Mosto

Planning & Environment

Manager

UTE Uruguay

Christopher Greiner

CTO

EnergyNest

Adele Lidderdale

Hydrogen Project Manager

EMEC

Moderator Panelists

Closing remarks

Electrication needed in DK to reach national

70% climate gas reduction towards 2030 (base 1990)

North Sea Wind Power Hub scenarios investigated

DK a part in northsea windpower visions

Closing remarks

Balancing the Danish power system

23

Hub/I sland

Potential PtX-”clusters”

Hydrogen cavern storage

Potential HVDC cables

Potential AC cables

Potential hydrogen lines

Existing gas pipes-4000

-2000

0

2000

4000

6000

8000

-10

-5

0

5

10

15

20

25

140

079

911

9815

9719

9623

9527

9431

9335

9239

9143

9047

8951

8855

8759

8663

8567

8471

8375

8279

8183

80

Theo

reti

cal s

tora

ge re

qu

irem

ent

(GW

h)

Po

wer

(GW

)

Residual: Wind/solar minus basis consumption (case 2035)

Hourly imbalance (GW) Acc. imbalance (GWh)

0

20

40

60

80

100

Inve

st.

cost

, en

ergy

par

t (E

UR

/MW

h)

Investment costs for the energy storage part(NB: Exclusive input/output units)

Inve

st c

ost

, en

ergy

par

t (Eu

ro/k

Wh

)

Further information at: http://www.energinet.dk/Sys35Or E-mail: [email protected]

Closing remarks

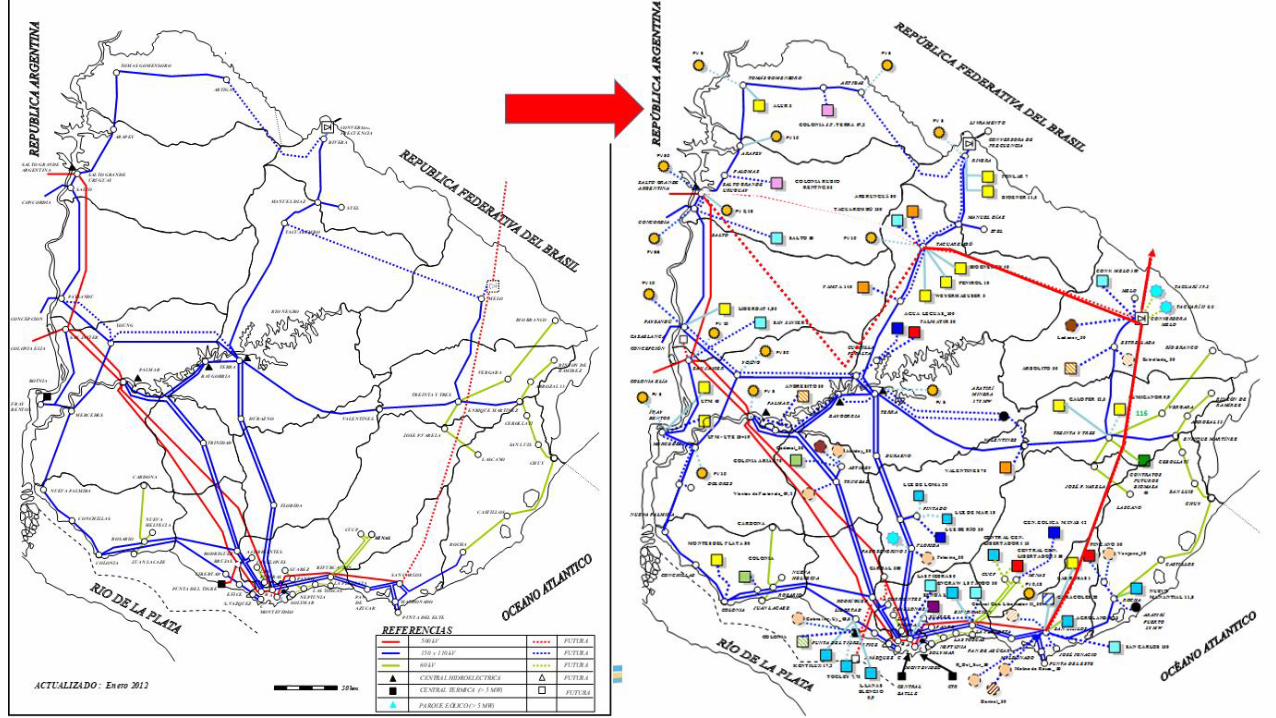

Electric power production - URUGUAY 2019 (3,5 MM inh.)

Thermal 2%

Wind Hydro

Biomass

98%RENEWABLE

Before 2010: 2.100 MW installed

2017: + 2.200 MW of NCRE

- Considering the variation onNCRE, it is economical to have a surplus (in average, near 10%).

- How to manage that resources… and their effect on the grids…

Closing remarks

Ways to manage the grids

And pass the benefits to end users

Introducing more technollogy in the operation: Automatic reconfiguration, dynamic

capacity.

Developing a new business model for a reconfiguration of the market, towards a more

flexible demand (coordinated with the supply availability).

Targets (using increasing Smart grids):➢ Better comfort for huseholds (new commercial options)

➢ Increased competitivity for productive sectors

➢ Atraction of investments (energy price levels)

➢ Better international interchanges rules

➢ Contribute to the Decarbonization in sectors like transport, heating, industries (processes

of energy substitution).

Closing remarks

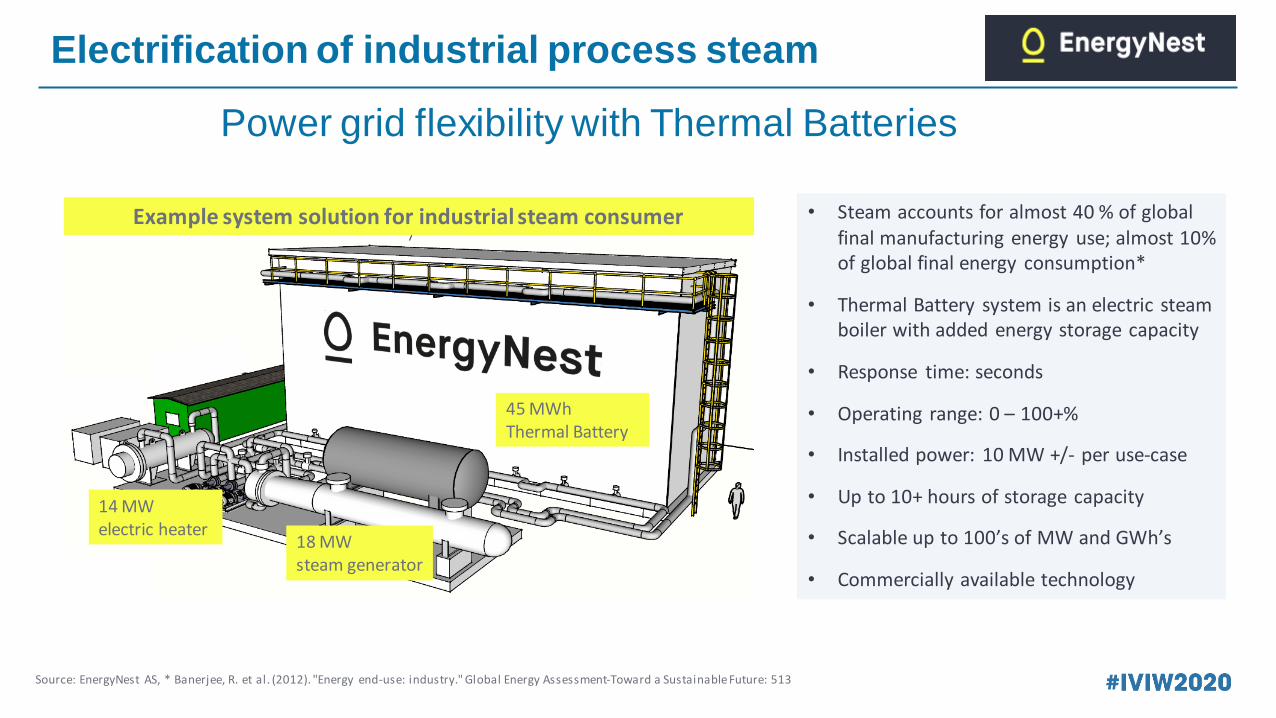

Electrification of industrial process steam

Source: EnergyNest AS, * Banerjee, R. et al. (2012). "Energy end-use: industry." Global Energy Assessment-Toward a Sustainable Future: 513

• Steam accounts for almost 40 % of global final manufacturing energy use; almost 10% of global final energy consumption*

• Thermal Battery system is an electric steam boiler with added energy storage capacity

• Response time: seconds

• Operating range: 0 – 100+%

• Installed power: 10 MW +/- per use-case

• Up to 10+ hours of storage capacity

• Scalable up to 100’s of MW and GWh’s

• Commercially available technology

Power grid flexibility with Thermal Batteries

18 MW steam generator

14 MW electric heater

45 MWh Thermal Battery

Example system solution for industrial steam consumer

Closing remarks

BIG HIT Project

Closing remarksNorela Constantinescu

Manager for Research &

Innovation

ENTSO-E

Anders Bavnhøj Hansen

Chief Engineer

Energinet Denmark

Pablo Mosto

Planning & Environment

Manager

UTE Uruguay

Christopher Greiner

CTO

EnergyNest

Adele Lidderdale

Hydrogen Project Manager

EMEC

Moderator Panelists

Panel IV: New Power Sector Dynamics with Smart Electrification

Closing remarks

Pablo Mosto

Planning & Environment

Manager

UTE Uruguay

Robert Chapman

Vice President of Electrific. &

Sus. Energy Strategy

EPRI

Bastian Pfarrherr

Head of Innovation

Management

Stromnetz Hamburg

Moderator

Katie Sloan

Director of eMobility and

Building Electrificaiton

Southern California Edison

Panelists

Anders Bavnhøj Hansen

Chief Engineer

Energinet Denmark

Closing Remarks

Closing remarks

33

Robert Chapman

Vice President of Electrific. & Sus. Energy Strategy,

Electric Power Research Institute (EPRI)

Thank you!

Coming up next:Session 3:

Green Hydrogen: Electrolysis, Ammonia and other E-Fuels

tomorrow at 8 am (CEST)

Register at https://innovationweek.irena.org/