service tax reverse & joint charge mechanism abhishek pratap singh 09/01/2015

TRANSCRIPT

Service TaxReverse & Joint Charge Mechanism

ABHISHEK PRATAP SINGH

09/01/2015

Reverse Charge Mechanism…a concept • Reverse Charge Mechanism in service tax is unique but not a new concept.

• Under this scheme, service tax is payable by service recipient instead of service provider.

• Under this charge service receiver have to register himself under service tax.

• Service receiver can not claim general exemption limit of 10 Lakh rupees. So he has to pay even on few rupees of service received.

Reverse Charge Mechanism…a concept

Reverse & Joint Charge Mechanism • The Liability To pay service Tax:

As per Sec68(1) of Finance act 1994, every person providing taxable service to any person is liable to pay service tax. Hence the liability to pay service tax is on the service provider. However an exception to the above said rule has been provided under sub section (2) of 68 of the Act., in terms of which the central government has the powers to notify services in respect of which even the service receiver shall be liable to pay service tax wholly or partially. This is termed as REVERSE CHARGE MECHANISM. Since in respect of some services both the service provider and service receiver are liable to pay service tax proportionately, it is termed as “partial reverse charge mechanism”.

• Harsh on small service receiver endwhere he has received services falls under reverse charge for only few hundred

rupees but due to it he has to register himself in service tax and have to file service tax return on prescribed interval. Moreover under service tax act Nil return is also mandatory and every registered person have to file half yearly return.

• As per notification 30/2012- Service Tax, Reverse charge is applicable from 1st July 2012 (For few services, reverse charge is applicable before 1st July 2012).

• From 01.07.2012, new services which are very common like advocate, Hiring vehicle for passenger, has been added under reverse charge.

Point of taxation

Point of taxation in Reverse Charge:• General Rule: Date of payment by service Recipient. As per rule 7 of the

point of Taxation Rules 2011(amended).

• Exception If payment is not made with in six months from the date of invoice, then the point of taxation shall be determine , as the rule does not exist . Thus the point of taxation in that case would be as per rule 3.

– a. If the invoice is issued with in the period specified (30 days) as per rule 4A of service tax rules, 1994 (w.e.f 01.04.2012) from the date of completion of service. Date of issue of invoice or receipt of payment, which ever is earlier.

– b.If invoice is not issued with in prescribed time. Date of completion of service or receipt of payment (payment date).

New Reverse charge Mechanism ( notification no. 30/2012 & 45/2012)

S.No. Description of a service % of service tax payable by Service Provider

% of service tax payable by Service Recipient

1 Service of Insurance agent to insurance company

NIL 100%

2 Goods transport service NIL 100%

3 Sponsorship service to the corporate or partnership firm

NIL 100%

4 Individual representing in arbitral tribunal to business entity.

NIL 100%

5 Individual advocate to business entity.

NIL 100%

New Reverse charge Mechanism ( notification no. 30/2012 & 45/2012)

S.No. Description of a service % of service tax payable by service provider

% of service tax payable by service recipient

6 renting or hiring any motor vehicle ( Abated value)

NIL 100%

7 renting or hiring any motor vehicle ( Non Abated value)

60% 40%

8 Manpower supply contract 25% 75%

9 Works contract 50% 50%

10 Import of Service NIL 100%

11 Director of the company ( independent Director)

NIL 100%

12 Support service by govt. Or local bodies

NIL 100%

New Reverse charge Mechanism ( notification no. 30/2012 & 45/2012) contd...

The Taxable service provided or agreed to be provided by way of renting or hiring any motor vehicle designed to carry passenger supply of manpower for any purpose works contract by any individual, Hindu Undivided Family or proprietary firm or

partnership firm, whether registered or not, including association of persons; located in the taxable territory to

any company formed or registered under the Companies Act, 1956 (1 of 1956) or a business entity registered as body corporate located in the taxable territory;

Insurance agent's Services

Insurance agent's Services Service Receiver

any person carrying on insurance businessService Provider

an insurance agent Rates : 100% by Service Recipient

Other auxiliary services provided in the field of insurance like insurance brokerage or reinsurance brokerage are not covered under the reverse charge mechanism, hence in such situations service tax has to be paid by such service providers themselves.

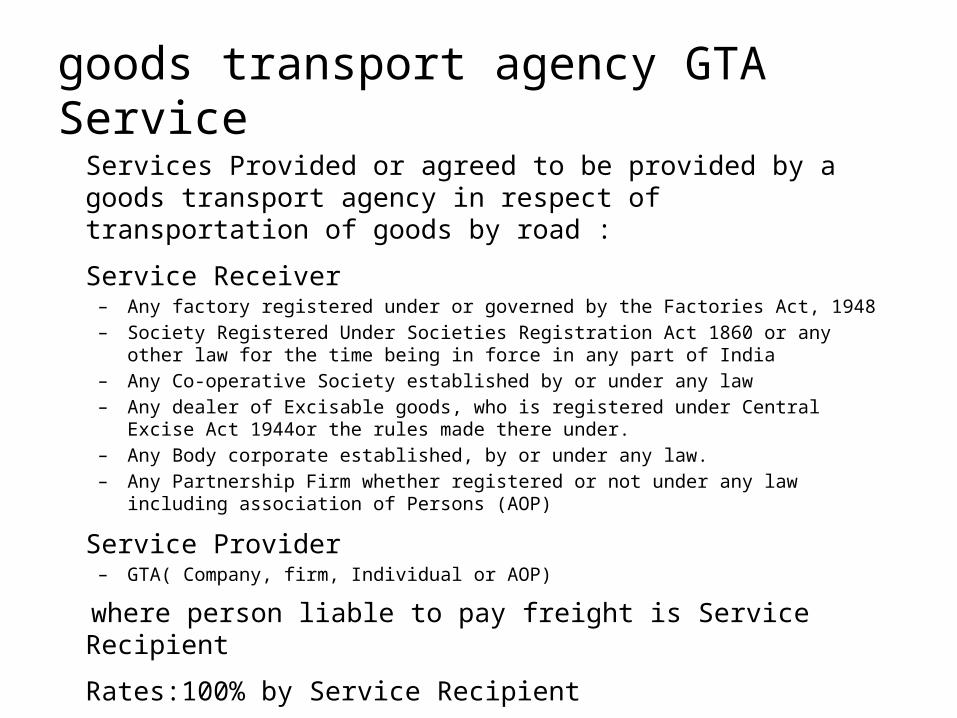

goods transport agency GTA ServiceServices Provided or agreed to be provided by a goods transport agency in respect of transportation of goods by road :

Service Receiver– Any factory registered under or governed by the Factories Act, 1948– Society Registered Under Societies Registration Act 1860 or any other law for the time being in force

in any part of India– Any Co-operative Society established by or under any law– Any dealer of Excisable goods, who is registered under Central Excise Act 1944or the rules made

there under.– Any Body corporate established, by or under any law.– Any Partnership Firm whether registered or not under any law including association of Persons (AOP)

Service Provider– GTA( Company, firm, Individual or AOP)

where person liable to pay freight is Service Recipient

Rates:100% by Service Recipient

GTA Service- contd…. If Vehicle is hired by the company, there is no service of transport of goods

hence there is no service tax liability under reverse charge mechanism. If many players involved, only transaction between the person dealing

with customer (service recipient) was a subject matter of service tax. Transportation through Hand carts, Bullock Carts, Three Wheelers and

Trams & Trolleys is not liable to service tax, but if a taxi is used for transportation of goods the same shall be liable for service tax.

Small Value Exemption Single goods carriage not exceeding Rs 1500/- Single consignment note not exceeding Rs 750/-

Exemption for Specific Goods Fruits, vegetables, eggs, milk, food grains or pulses;

Abatement An abatement of 75% can be claimed in relation to services of GTA subject to the condition that Cenvat credit has not been taken.

Sponsorship servicesSponsorship services

Provided or agreed to be provided to any body Corporate or Partnership Firm located in Taxable TerritoryService Receiver– Body Corporate– Partnership Firm

Service Provider– Any Person

Rates:100% by Service Recipient

Exemption: Services by way of sponsorship of sporting events organised,-– by a national sports federation, or its affiliates, where the participating teams/

individuals represent any district, state or zone;– by Association of Indian Universities, Inter-University Sports Board, School Games

Federation, All India Sports Council for the Deaf, Paralympic Committee of India or Special Olympics Bharat;

– by Central Civil Services Cultural and Sports Board;– as part of national games, by Indian Olympic Association; or– under Panchayat Yuva Kreeda Aur Khel Abhiyaan (PYKKA) Scheme;

Services of Arbitral Tribunal

Services of Arbitral Tribunal provided to any business entity located in India.Here The term Business Entity has been defined Under Clause 17 of Sec 65B, which means any person carrying out any activity relating to Industry, Commerce or any other business or profession. Hence, even an Individual, a proprietary firm or partnership Firm shall be construed as a business entity if such person carries out any activities relating to Industry, Commerce or Profession.

• Service ReceiverAny Business Entity carrying on Business related activities., includes:

Individuals, Proprietary firms, partnership Firms• Service Provider

Arbitral Tribunal• Rates:100% by service recipient.• Exemption: Service to

1. Any person other than business entity.2. A business entity with a turnover upto Rs. 10 Lacs in the preceding financial year.

Legal ServicesLegal Services

provided by Individual advocates or by a firm of Advocates to any business entity located In Indian Territory.

• Service ReceiverAny Business Entity carrying on Business related activities.,

includes: Individuals, Proprietary firms, partnership Firms• Service Provider

Individual or a firm Of Advocates• Rate: 100% by service recipient • Exemption

Service provided by an individual as an advocate or a partnership firm of advocates by way of legal services to,- (i) an advocate/ partnership firm of advocates providing legal services ; (ii) any person other than a business entity; or

(iii) a business entity with a turnover up to Rs 10 lakh in the preceding FY;

Legal Services – stayed by Delhi High Court

• However, High Court of Delhi vide order dated 21.09.2012 has stayed the implementation of this amendment in a petition (W.P.(c) No. 5957/2012) led Mr. A.S. Chandhiok, Sr. Adv. with Mr. Ruchir Bhatia, Adv. for Delhi Tax Bar Association. Next Hearing was scheduled to take place on 27.11.2012.

• Status as of today… No further order by Delhi High Court.. Stay order continued.

• As per our opinion / advice even with stay order by the High Court we should continue to pay the Service Tax on reverse charge basis on legal services if we are in a position to avail the Cenvat credit of it. As if afterwards the service tax liability arises, then the department will charge the amount of service tax as well as the amount of interest on it. On amount of interest no cenvat will be available. So better to pay and take the benefit of it.

Support services by Govt. or local authoritySupport services Provided by Government or local authority to any business entity located in taxable territory, excluding the following:

– 1. Renting of Immovable Property– 2. Services of Department of Post, Express Post, Life Insurance and

agency Services Provided to person other than Government.– 3. Services in relation to an aircraft or a vessel.

• Service ReceiverAny Business Entity carrying on Business related activities, includes: Individuals, Proprietary firms, partnership Firms

• Service ProviderGovernment or local authorities

• Rates:100% by service recipientThe intention is to provide level playing field to private players engaged in providing similar kind of services.Example: An small event management agency procuring police protection service from

the State government.

Renting of a motor vehicles Renting of a motor vehicles designed to carry passengers, to any person who is not in the similar line of business.• Service Receiver

– Business entity registered as Body Corporate,– located In taxable Territory

• Service Provider– Individual– Hindu Undivided Family– Partnership Firm (registered or not) or LLP– Association of Person (AOP)

• Rate:– On Abated Value:100% by service recipient– On Non Abated Value:40% by service recipient and 60% by provider

Excluding: Renting of motor vehicles to any person carrying similar line of business.

Supply of Man power or Security Services.

Supply of Man power for any purpose or Security Services.• Service Receiver

– Business entity registered as Body Corporate,– located In taxable Territory

• Service Provider– Individual– Hindu Undivided Family– Partnership Firm (registered or not)– Association of Person (AOP)

• Rate:75% by service recipient and 25% by providerImportant Points

– Direct wages paid are not covered under this category.– Payment to agency and activities of deputation of manpower are covered.– “Supply of manpower” means supply of manpower, temporarily or

otherwise, to another person to work under his superintendence or control.

Works Contract

Service Portion In the Execution Of Works Contract:• Service Receiver

– Business entity registered as Body Corporate, located In taxable Territory

• Service Provider– Individual– Hindu Undivided Family– Partnership Firm (registered or not)– Association of Person (AOP)

• Rate: 50% by service recipient and 50% by service provider

Works Contract…. Contd

Definition of Work contract {65B (54)}Works contract means a contract wherein transfer of property in goods involved in execution of such contract– Is leviable to tax as sale of goods under Vat rules and such

contract is for • the purpose of carrying out

– construction, erection, commissioning, installation, completion, fitting out,

– repair, maintenance, renovation, alteration of any movable or immovable property or

– for carrying out any other similar activity or a part thereof in relation to such property

Case Study- A Company want to paint its floor.

Painting material brought by the Company and labour is also hire by the Company

VAT is paid by the Company100% service tax is also paid by the company on the labour bill.

Painting

material br

oug

ht

by t

he

Compa

ny a

nd

pai

nti

ng c

ontract

was a

war

de

d t

o a c

ontract

or

VAT is paid by the CompanyReverse Charge on manpower supply contract so 75% liability

Contract was awarded to a contractor to purchase the painting material and to Paint

• Its a work contract

• Valuation rules apply

Valuation of Services in works Contract

Rule-2A of Service Tax Determination of Value Rules, 2006

Pay service tax on Value of services after deducting value of goods from the gross valueService portion includes

1. Labour charges

2. amount paid to a sub-contractor for labour and services;

3. charges for planning, designing and architect’s fees;

4. charges for obtaining on hire or otherwise, machinery and Tools

5. cost of consumables such as water, electricity, fuel

6. cost of establishment of the contractor relatable to supply of labour and services;

7. other similar expenses relatable to supply of labour and services; and

8. profit earned by the service provider relatable to supply of labour and services;

Where value added tax or sales tax has been paid or payable

Gross Value charged

LESS :-

Value adopted for the purposes of

payment of value added tax or sales tax, shall be taken as the value of property in goods

On balance amount service tax is paid

Rs. 100,000/-

Rs. 45,000/-

Rs. 55,000/-

Pay service tax at composite rate

•40% of the total amount charged for the works contract

Execution of OriginalWork

•70% of the total amount charged for the works contract

Maintenance or repair or reconditioning or

restoration or servicing of any goods

•60% of the total amount charged for the works contract

Service not covered above, including maintenance,repair, completion and

finishing service

“Total Amount” means the sum total of the gross amount charged for the work contract and the fair market value of all goods and services supplied in or in relation to the execution of the work contract.

Exemption to Work Contract Services

All the work contract specified in the Point 12,13 & 14 of the MegaExemption notification no. 25/2012 all are Exempt from the service tax.

Services of erection, installation, commissioning, completion, fitting out, construction, maintenance or alteration provided.

1. to government or local authority or governmental authority in relation to

specified structures like historical monuments, canal, dams etc.

2. In relation to specified structures like road, bridge, tunnel, irrigation projects etc.

3. In relation to works contract under JLNURM or Rajiv Awaas Yojana

Erection or Construction service in relation to original works pertaining to airport, port, railways or single residential unit etc.;

Import of Service

Services Provided By a person who is located In a non taxable Territory To any person located in the Taxable Territory.

• Service Receiver– Any Person Located In taxable Territory (Individual, HUF, Firms, AOP,

Body Corporates or Trusts)

• Service Provider– Any Person Located in Non Taxable Territory

• Rate:100% by Service Receiver

Here there is no provision of whether service provided for Business purposes or not, Hence it is applicable to Trusts Registered U/sec 12 A Of Income Tax Act.

Services by a Director to the Company

Services Provided By a Director of a company to the said Company:

Service Receiver– Company

Service Provider– Director of the Said Company

Rates:100% by service receiver

• However, services provided by director in employee-employer relationship do not attract reverse charge.

• Whole time director & managing director are considered as employee of company so reverse charge will not be applicable.

hidden_benefits

Case Studies

• What happens to a Society which is out of service tax ambit because of the applicability of "Negative List" but uses goods transport agency for transport of goods by road?

Society has to register to pay reverse charge tax on GTA services.

• Should liabity under reverse charge method be discharged from cenvat credit a/c by a manufacture?

Cenvat credit can be used for Service tax on any output service. Reverse charge is payable on input services . Hence liability under reverse charge can’t be discharged from cenvat credit a/c.

• Whether the service recipient can claim any credit of such service tax deposited?

Yes , service receiver can claim cenvat credit if he other wise eligible on all the service tax paid by himself or paid through service provider.

Case Studies

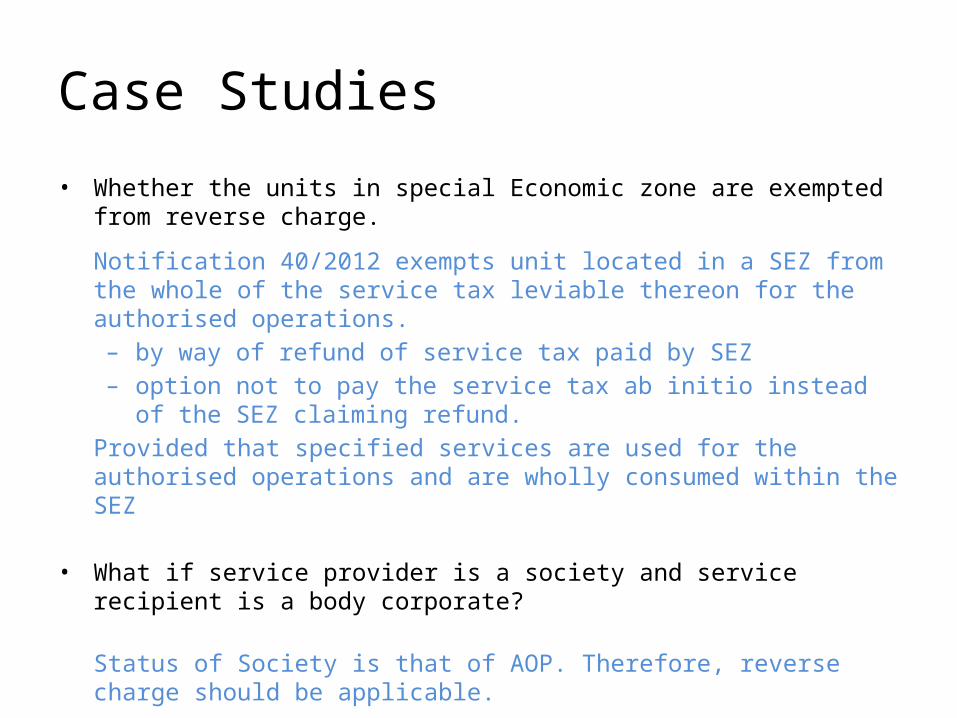

• Whether the units in special Economic zone are exempted from reverse charge.

Notification 40/2012 exempts unit located in a SEZ from the whole of the service tax leviable thereon for the authorised operations. – by way of refund of service tax paid by SEZ – option not to pay the service tax ab initio instead of the SEZ claiming refund.

Provided that specified services are used for the authorised operations and are wholly consumed within the SEZ

• What if service provider is a society and service recipient is a body corporate?

Status of Society is that of AOP. Therefore, reverse charge should be applicable.

Case Studies• Support services and manpower services of pvt ltd company rendering services to IT

company in export promotional industrial park attracts reverse ST mechanism with 25/75 ?

Reverse charge mechanism in case of following four services is applicable only if 1.works contract 2.Manpower3.Security services 4.Transport of passengers

Service provider is 1. Individual2. HUF3. Firm (registered or not)4. AOP and

service receiver is Body corporate

If service provider does not falls under above four categories and service receiver is not a body corporate then reverse charge is not applicable in case of above four services.

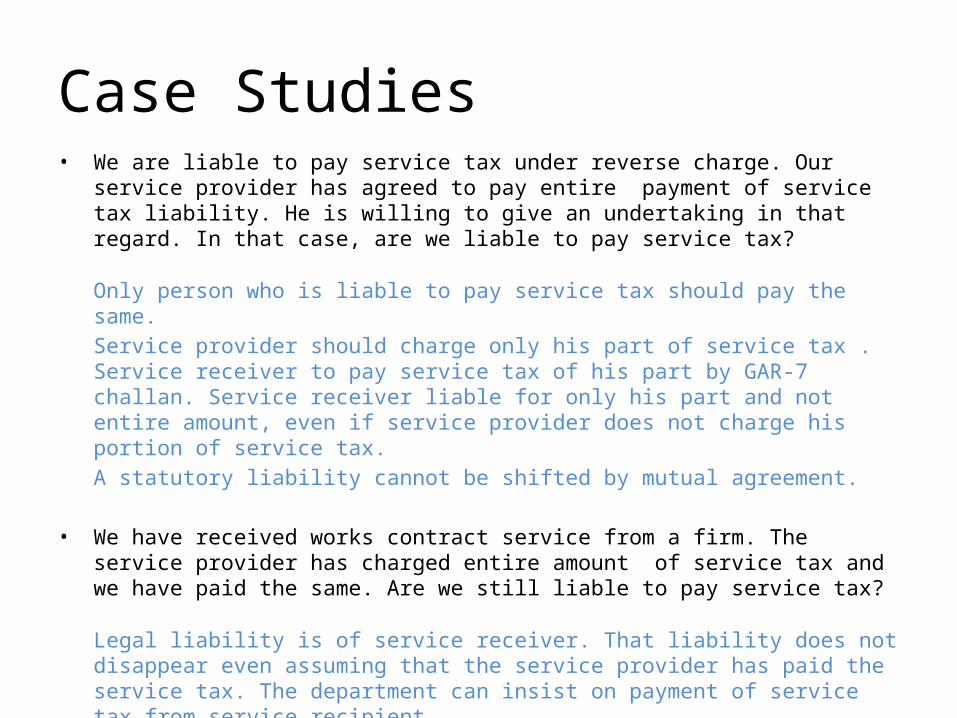

Case Studies• We are liable to pay service tax under reverse charge. Our service provider has agreed to pay

entire payment of service tax liability. He is willing to give an undertaking in that regard. In that case, are we liable to pay service tax?

Only person who is liable to pay service tax should pay the same. Service provider should charge only his part of service tax . Service receiver to pay service tax of his part by GAR-7 challan. Service receiver liable for only his part and not entire amount, even if service provider does not charge his portion of service tax. A statutory liability cannot be shifted by mutual agreement.

• We have received works contract service from a firm. The service provider has charged entire amount of service tax and we have paid the same. Are we still liable to pay service tax?

Legal liability is of service receiver. That liability does not disappear even assuming that the service provider has paid the service tax. The department can insist on payment of service tax from service recipient.

Case Studies• We are a company. Our employees engage motor vehicle on hire when they go on tour for

official purposes. On return, they claim reimbursement of the bill. Is the company liable to pay service tax under reverse charge?

Though company is reimbursing the Bill, the service receiver is the employee, if the Bill of the service provider is in name of employee [In fact, the motor vehicle operator is not likely to know that the service receiver is company and will have to charge service tax in normal course, if he is otherwise liable]. In such cases, the company will not be liable under reverse charge. However, if the bill is in name of the company, reverse charge will apply, if the service provider is individual, HUF etc.

Important Points • What is Reverse charge with condition of non-availability of Cenvat ?

In some services (e.g. GTA, renting or hire of motor vehicle designed to carry passengers), the abatement is subject to condition of non-availment of Cenvat credit by service provider (not by service receiver) A certificate should be obtained from the service provider about non-availment of Cenvat credit. Such certificate is not required in case of hire or renting of motor vehicle.

• Difference between Business Entity and Body Corporate?

“Business entity” means any person ordinarily carrying out any activity relating to industry, commerce or any other business or profession. Thus, Government, charitable organisation is not ‘business entity’. In some cases, reverse charge is applicable only when service receiver is business entity registered as ‘body corporate’. Body Corporate – Company, LLP, Cooperative Society is Body Corporate – Firm, HUF, Trust is not ‘Body Corporate’ [Society registered under Societies Act is legally not ‘body corporate’].

Important Points

• Import of Service

Service tax is payable only if Place of Provision of Service is in taxable territory (i.e. India plus 200 nautical miles inside the sea minus J&K) Service provider should be outside taxable territory and service receiver should be located in taxable territory. Service tax is payable on gross amount including TDS.

• Services of Advocate or Advocate Firms or Arbitral Tribunal to Business Entity having turnover over 10 lakhs. Then Business Entity is liable to pay entire service tax.

Important Points

• Refund of Unutilised Cenvat Credit to Service Recipients:

The Central Government has inserted a new rule 5B under Cenvat Credit Rules, 2004, providing for the refund of the Service tax paid under reverse mechanism. According to this rule, if the Service provider is unable to utilize the Cenvat credit availed of Inputs and Input services, he shall be allowed refund of such un-utilized Cenvat credit subject to safeguards, conditions and limitations.It may be noted that the refund under the above rule is available for the Provider of service who pays service tax on reverse charge mechanism. In other words, the refund shall not be allowed to service recipients who pay service tax under reverse charge wholly or Fully..

Summing Up• If you are receiving any of these services and fall under specified category of service receiver

then you must register your self for service tax.

• If you have already registered under service tax act and receiving one of new service added under reverse charge then you have to add this specific service in your service tax registration certificate.

• The service recipient is liable to pay service tax without availing the Cenvat credit of the Inputs and Input services.

• However, He can claim the Cenvat credit paid as service receiver towards the payment of service tax on other Output services and Payment of Central Excise duty on manufacture and clearance of excisable goods.

• It may be noted that in respect of renting of motor vehicles, supply of man power or security services or works contract service provided by an Individual, or HUF, or Proprietary or partnership Firm, the reverse charge mechanism shall apply only if the service recipient is a business entity registered as body corporate. If the Service recipient is not a body corporate, the reverse charge shall not apply.

Summing Up• In case of legal services provided by an individual advocate or a partnership of

Advocated, reverse charge provisions shall apply even if the receiver of such service is an Individual , HUF, Proprietary firm or partnership firm. However, such service tax shall be liable only when the gross turnover of Service receiver exceeded Rs.10lac in the preceding Financial Year.

• Other Issues relating to reverse charge – Tax should be paid under service tax registration number of service receiver

and included in his return as he is liable to pay service tax. – Service tax is payable by service receiver when actual payment is made to

service provider and not on receipt of Invoice. However, if payment is not made within 6 months, service tax is anyway payable. Interest is also payable. Exception is that when service provider outside India is Associated Enterprise (group company with at least 25% common interest), the service receiver is liable to pay service tax as soon as the account of service provider is credited in books of account of service receiver.

Leaving you thinking… about applicability of Service Tax

through Reverse Charge Mechanism.

Thank You