service tax concepts

TRANSCRIPT

BASIC CONCEPTUAL UNDERSTANDING

SAURABH MEHTA M.NO. 9920626587

CONTENTS1. Definition of Service (Sec. 65B)2. Major Change3. Declared Services (Sec. 66E)4. Valuation Rules (Sec. 67)5. Registration & Return Procedures6. SSP Exemption Provisions7. Payment Provisions8. Negative List (Sec. 66D)9. Exemptions 10. Scheme of Abatement

MAJOR CHANGEThe most important change is that the Effective rate of Service Tax has been increased from 12.36% to an all inclusive rate of 14%. The effective rate of Service Tax will go up by another 2% if and when the Central Government exercises its power to introduce a “Swachh Bharat Cess” of 2% on all or any of the taxable service.The above changes to be effective from a date to be notified by the Government.

What is SERVICE?• Definition of service u/s 65B(44) of Finance Act, 1994

Any activityCarried out by a person for anotherFor consideration, andIncludes “declared services”

• Exclusions

Transfer of title in goods or immovable property in any manner including deemed salesTransaction only in money or actionable claimService provided by an employee to an employer in the course of the employmentFees payable to court or tribunal

DECLARED SERVICESThe phrase has been specified in section 66E of the Act. The following nine activities have been specified in section 66E:

1. renting of immovable property;2. construction of a complex, building, civil structure or a part

thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration is received after issuance of certificate of completion by a competent authority;

3. temporary transfer or permitting the use or enjoyment of any intellectual property right;

4. development, design, programming, customization, up gradation, enhancement, implementation of information technology software;

5. agreeing to the obligation to refrain from an act, or to tolerate an act or a situation, or to do an act;

6. transfer of goods by way of hiring, leasing, licensing or any such manner without transfer of right to use such goods;

7. activities in relation to delivery of goods on hire purchase or any system of payment by instalments;

8. service portion in execution of a works contract;9. service portion in an activity wherein goods, being food

or any other article of human consumption or any drink (whether or not intoxicating) is supplied in any manner as part of the activity.

Services liable to Service Tax

All services are liable to service tax except –a) Activities specifically excluded in definition of service.b) Services covered under the negative listc) Services covered under Mega Exemption notification.d) Services provided outside the taxable territory (incl. Jammu

& Kashmir)e) Services received by a unit located in SEZ/STPI (subject to

conditions).

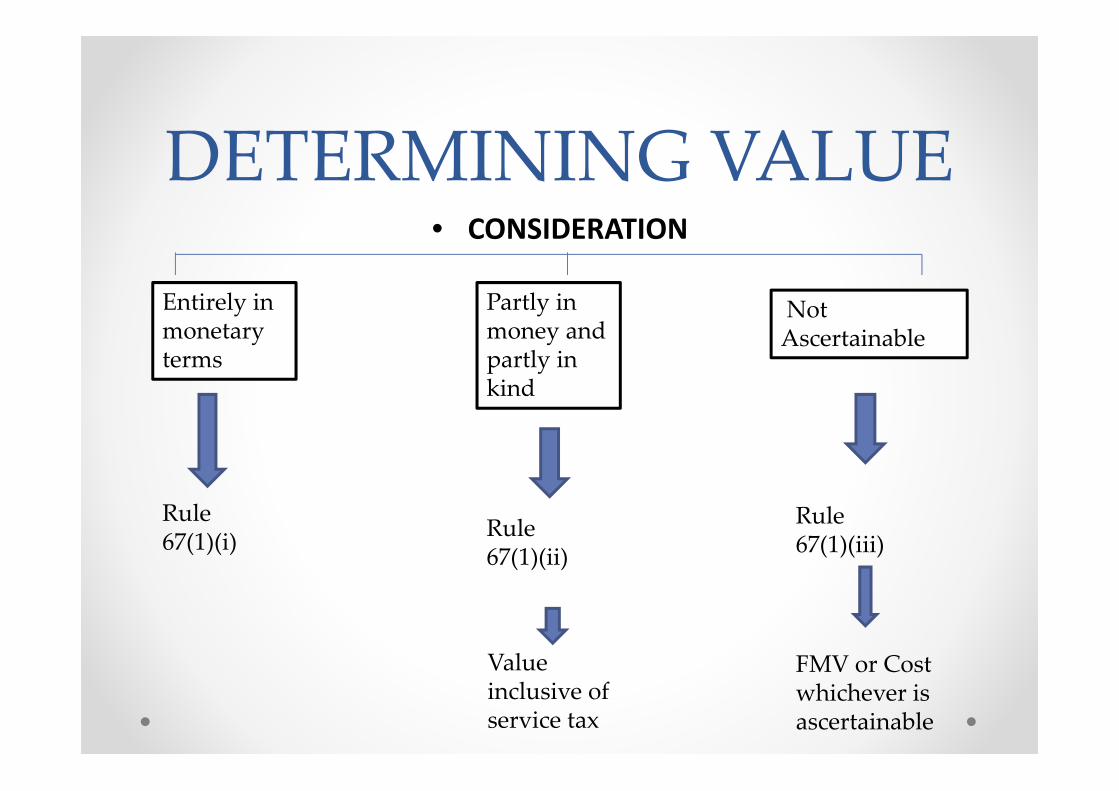

VALUATION RULES• Valuation Rules have been prescribed under Rule 67 of

Finance Act, 1994 as follows:• Service Tax will be applicable on the Gross Amount Charged or

to be charged by the Service provider.• Tax is payable as soon as advance is received without waiting

for the commencement of actual provision of service.

DETERMINING VALUE• CONSIDERATION

Entirely in monetary terms

Rule 67(1)(i)

Partly in money and partly in kind

Rule 67(1)(ii)

Value inclusive of service tax

Not Ascertainable

FMV or Cost whichever is ascertainable

Rule 67(1)(iii)

REGISTRATION & RETURNS

• FORMS

ST‐1 ST‐2 ST‐3Application for registration

Service tax registration certificate

Filing of returns

Within 30 days oncrossing threshold limit of 9 lakhs

Half Yearly

Single or centralized registration

RETURNS• DUE DATES FOR FILING

• PENALTY FOR LATE FILINGUpto 15 days = Rs. 500/‐Above 15 upto 30 days = Rs. 1000/‐More than 30 days = 1000+ Rs. 100/day Maximum

upto Rs. 20000/‐

ORIGINAL RETURN REVISED RETURN NIL RETURNH.Y. 1 = 25th OctoberH.Y. 2 = 25th April

Within 90 days of filing original return

Mandatory forassesses not providing any services during F.Y.

300000 400000600000

8000001000000

0200000400000600000800000

1000000

X 01/04/04 01/04/06 01/04/07 01/04/08Turnover

Have to pay Service tax on crossing the aggregate value of taxable service exceeding the threshold limit of Rs. 10 Lacks as per Notification No. 33/2012-ST

Have to get himself registered on crossing the aggregate value of taxable service exceeding the threshold limit of Rs. 9 Lack

Aggregate value of taxable service means the sum of first consecutive payments received during a financial year towards taxable service provided or to be provided.

9,00,000SSP EXEMPTION LIMIT

PAYMENT PROVISIONSASSESSEE PERIODICITY DUE DATE

Individual, Partnership Firm (incl. LLP)

Quarterly 6th of next month of relevant quarter/31st March for Q‐4

Others Monthly 6th of next month/ Upto 31st March

INTEREST FOR LATE PAYMENT OF LIABILITY

Upto 6 months = 18% p.a. (upto 30.09.2014 = 15%p.a.)Above 6 months upto 1 year = 24% p.a.Above 1 year = 30% p.a.

OPTION FOR INDIVIDUAL AND PARTNERSHIP FIRM

IF VOTS in P.Y. THEN in C.Y. ON=< 50 Lakh VOTS upto 50 Lakh

> 50 Lakh Receipt BasisAccrual Basis

> 50 Lakh Whole VOTS Accrual Basis

Negative List of ServicesThe services specified in the negative list go out of the ambit of chargeability of service tax. (Section 66D )1. G‐ Services by Government or a local authority excluding the

following services to the extent they are not covered elsewhere‐• (i) services by the Department of Posts by way of speed post, express

parcel post, life insurance and agency services provided to a person other than Government;

• (ii) services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport;

• (iii) transport of goods or passengers; or • (iv) any services provided to business entities; 2. R‐ Services provided by Reserve Bank of India3. D‐Services by a foreign diplomatic mission located in India

(Hint : GREAT MADE Facebook)

4. A‐ Services relating to agriculture or agricultural produce by way of‐

• (i) agricultural operations directly related to production of any agricultural produce

• (ii) supply of farm labour; • (iii) processes carried out at an agricultural farm which do not alter

the essential characteristics of agricultural produce but make it only marketable for the primary market;

• (iv) renting or leasing of agro machinery or vacant land • (v) loading, unloading, packing, storage or warehousing of

agricultural produce; • (vi) agricultural extension services; 5. T‐ Trading of goods6. M‐ Processes amounting to manufacture or production of goods

(excl. production of alcoholic liquor for human consumption)7. A‐ Selling of space or time slots for advertisements other than

advertisements broadcast by radio or television

8. T‐ Access to a road or a bridge on payment of toll charges

9. E‐ Entry to Entertainment Events and Access to Amusement Facilities not more than Rs. 500/‐ per person. (upto 01.04.2015 no such limit)

10. E‐ Transmission or distribution of electricity by an electricity transmission or distribution utility

11. E‐ Specified services relating to education by way of‐(i) pre‐school education and education up to higher secondary school or equivalent; (ii) education as a part of a curriculum for obtaining a qualification recognised by any law for the time being in force; (iii) education as a part of an approved vocational education course;

12. R‐ Services by way of renting of residential dwelling for use as residence

13. F‐ Financial sector‐ services by way of‐(i) extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount; (ii) inter se sale or purchase of foreign currency amongst banks or authorised dealers of foreign exchange or amongst banks and such dealers;

14. T‐ Service of transportation of passengers, with or without accompanied belongings, by‐

(i) a stage carriage; (ii) railways in a class other than‐(A) first class; or (B) an air‐conditioned coach; (iii) metro, monorail or tramway; (iv) inland waterways; (v) public transport, other than predominantly for tourism purpose, in a vessel between places located in India; and (vi) metered cabs , auto rickshaws;

15. T‐ Services by way of transportation of goods‐(i) by road except the services of‐(A) a goods transportation agency; or (B) a courier agency; (ii) by inland waterways;

16. F‐ Funeral, burial, crematorium or mortuary services including transportation of the deceased

EXEMPTIONMega exemption Notification 25/2012‐ST dated 20/6/12 and other exemptions‐

1. Services to United Nation and international organisations2. Health care services by a clinical establishment,

an authorised medical practitioner 3. Services by a veterinary clinic in relation to health care of animals

or birds 4. Services by Charitable Organisations in respect of specified

charitable activities only and construction of building for religious purposes for Charitable Organisation registered under section 12AA of Income Tax Act. Services imported by Charitable Organisations are also exempt from service tax

5. Services by a person by way of‐• (a) renting of precincts of a religious place meant for general

public; or• (b) conduct of any religious ceremony;6. Advocate or Advocate firm to non‐business entity or business

entity with turnover up to Rs.10 lakhs in the preceding financial year.

7. Services by way of training or coaching in recreational activities relating to arts, culture or sports

8. Services provided to or by an educational institution in respect of education exempted from service tax, by way of,‐

• (a) auxiliary educational services; or• (b) renting of immovable property;9. Services provided to a recognised sports body by‐• (a) an individual as a player, referee, umpire, coach or team

manager for participation in a sporting event organized by a recognized sports body;

• (b) another recognised sports body;

10. Services provided by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, or alteration of,‐

• (a) a road, bridge, tunnel, or terminal for road transportation for use by general public;

• (c) a building owned by a Charitable Trust;• (d) a pollution control plant11. Structure meant for funeral, burial or cremation of deceased12. Services by a performing artist in folk or classical art forms of (i) music, or

(ii) dance, or (iii) theatre, excluding services provided by such artist as a brand ambassador upto Rs. 1,00,000/‐ for the performance.

13. Services of journalists14. Hotels, guest houses with less than Rs.1,000 per day tariff15. Restaurants without AC/central heating 16. Goods transport upto Rs.750 per consignee and Rs.1,500 per vehicle and

specified agricultural commodities

18. Renting of motor vehicle to GTA19. Specified general insurance schemes exempt.20. Sub‐brokers on stock exchange21. Sub‐contractor under works contract providing service to main

contractor (who is also under works contract), when service of main contractor is exempt

22. Business Exhibition held outside India 23. Services of slaughtering of animals.24. Services from outside India to Government or Charitable Organisations25. Public Libraries26. Slump sale, sale of business, demergers27. Public conveniences like toilets, bathrooms etc.

SCHEME OF ABATEMENTS.No

Name of Service Taxable (%)

CG Input IS

1 Goods Transport Agency (GTA) (25%) 30 X X X2 Transport of goods by rail 30 X X X

3 Transport of passengers by rail 30 X X X4 Transport of goods in a vessel from one port in

India to another50 X X X

5 Transport of passengers by aira) Economy Class b) Others (40%)

4060

X X √

6 Supply of food or any other article of human consumption or any drink, in a restaurant / other premises

40 √ X (Chp. 1 to 22) √(other)

√

S.No Name of Service Taxable (%)

CG Input IS

7

Supply of food in convention centre, pandal, etc

70 √ X (Chp. 1 to 22) √(other

√

8 Accommodation in hotels, inns etc 60 X X √9 Renting of any motor vehicle designed to carry passengers

(40%)50 X X X

10 Tour Operating Service

10(a) Package Tour 25 X X X10(b) Booking accommodation 10 √ √ √10(c ) Services other than 10(a) and 10(b) provided in relation to

tour40 X X X

11 Financial leasing services including hire purchase 10 √ √ √12 Services in relation to chit (Earlier Taxable @ 30%) 100 X X X

S.No Name of Service Taxable (%)

CG Input IS

15 Construction of a complex, building, civil structure or a part thereof, intended for a sale to a buyer, wholly or partly, except where entire consideration is received after issuance of completion certificate by the competent authority,‐(a) for a residential unit satisfying both the following conditions, namely:–(i) the carpet area of the unit is less than 2000 square feet; and(ii) the amount charged for the unit is less than rupees one crore;(b) for other than the (a) above

25

30

√ X √

16 Works contracts

16(a) Works contracts entered into for execution of original works

40 √ X √

16(b) Works contracts entered into for maintenance or repair or reconditioning or restoration or

70 √ X √

16(c ) For other works contracts, not covered under sr. no. 16 and 17 , including maintenance, repair, completion and finishing services such as glazing, plastering, floor and wall tiling, installation of electrical fittings of an immovable property

60 √ X √

THANK YOU