september 2008 kraft foods...

TRANSCRIPT

September 2008

KRAFT FOODS BACK-TO-SCHOOL

2

Irene RosenfeldChairman and CEO

Forward Looking StatementsThis presentation contains forward-looking statements regarding our four strategies to get Kraft growing, specifically rewiring the organization for growth, reframing our categories, exploiting our sales capabilities and balancing cost and quality; our belief that input costs will be at least $3.3 billion, or 23%, higher in 2008 than 2006; that we're doing what we said we would and building momentum; that we’ll deliver GAAP EPS of at least $2.00 in 2009; our belief that we’re rebuilding our brand equities, and in particular, that our investments are paying off, we are reframing value proposition and leveraging our portfolio breadth; that the integration of our LU biscuits business is on track, growing strongly and accretive to EPS in 2008; that we are benefiting from decentralized structure and tightly controlling costs; that we are delivering improved financial results and improving profitability while we invest; our belief regarding our long-term EPS growth; our plan to rewire Kraft International by winning locally, leveraging globally, building management depth and focusing on specific categories, brands and markets where we believe we can win; how we plan to leverage our biscuits and snacks businesses for growth; our plan to build Oreo as a global icon, market by market and extending the brand into all channels and new countries; that we are trading up our power brands such as Milka, improving quality, increasing marketing, moving from mainstream to upper mainstream and obtaining higher margins from trading up consumers; that we are growing our Carte Noire brand and expanding into new segments and geographies and enhancing the mix of our coffee business; our belief that the best is yet to come and our long-term organic net revenue growth and margin targets; that our international business is key to our growth; our belief of what drives long-term and near-term EPS growth and our long-term EPS growth expectation; our estimates for restructuring, specifically that our savings will reach $1.1 billion in 2008 and $1.4 billion total and spending will be approximately $900 million in 2008 and $3.0 billion total; our expectation that we will continue to optimize our manufacturing network and reduce overhead costs by at least 1% of net revenue over the next few years; our 2008 guidance, in particular organic net revenue growth of at least 6%, EPS excluding items of at least $1.88 and effective tax rate of approximately 33%; our 2009 guidance, in particular organic net revenue growthof at least 4% and GAAP EPS of at least $2.00; our belief that we are improving cash flow with a $1 billion opportunity; and ourexpectation for additional cash flow improvements and our long-term target expectations for primary working capital and capital spending. These forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those predicted in any such forward-looking statements. Such factors, include, but are not limited to, continued higher input costs, pricing actions, increased competition, our ability to differentiate our products from private label products, increased costs of sales, our ability to realize the expected cost savings and spending from our planned restructuring program, unexpected safety or manufacturing issues, FDA or other regulatory actions or delays, unanticipated expenses such as litigation or legal settlement expenses, our indebtedness and ability to pay our indebtedness, the shift in our product mix to lower margin offerings, risks from operating internationally, our inability to integrate the LU biscuit business and tax law changes. For additional information on these and other factors that could affect our forward-looking statements, see our filings with the SEC, including our most recently filed Annual Report on Form 10-K/A and subsequent reports on Forms 10-Q and 8-K. We disclaim and do not undertake any obligation to update or revise any forward-looking statement in this presentation.

4

Strategic Turnaround

Operational Turnaround

Financial Turnaround

BalanceCost & Quality

ExploitSales

CapabilitiesReframe

CategoriesRewire for

Growth

1 2 3 4

5

Unprecedented input cost inflationTotal Input Costs

+$1.3Bn+$3.3Bn

vs. 2006

+23%

2006 2007 2008E

6Source: Company estimates

Doingwhat we said we would do

7

We’re building momentum

8

We’ll deliver GAAP EPS of at least $2.00 in 2009

9

Strong momentum at midpoint of turnaround

Rebuilding our brand equities

Strengthened our portfolio

Benefiting from decentralized structure

…delivering improved financial results

10

Rebuilding our brand equities

11

Reframing Value PropositionInvestments Paying Off

Leveraging our portfolio breadth

12

Solid volume/mix despite pricing

6.2%

4.0%

pp contribution 1.5%PricingVolume/Mix

7.5%

0.70.8

3.0

1.0

4.1

2.1

1.7

5.8

Organic revenue growth profile*

H1 ‘082006 H1 ‘07 H2 ‘07

13* Reported net revenue growth was 0.7% in 2006; 6.3% in H1 ’07; 10.4% in H2 ’07; 21.1% in H1 ’08. See GAAP to Non-GAAP reconciliation at the end of this presentation

Strengthened our portfolio

Exited several businesses that did not fit− VeryFine and Fruit 2O− Post cereals− European salty snacks

Acquired LU biscuits− Integration on track− Business growing strongly− EPS accretive in 2008

14

Benefiting from decentralized structure

Faster reaction to marketplace− Taking the lead on cost-driven pricing− Cutting inefficient trade spending

Tightly controlling costs

15

Improving profitability while we invest(ex items*)

16

33.7%

Q1 ‘08

36.1%

Q2 ‘08

31.2%

Q4 ‘07

Gross margin

15.3%

34.8%Adjusted**

Operating incomemargin 12.4% 13.9%

Adjusted**11.4%

Q4 ‘07 Q1 ‘08 Q2 ‘08

* Reported gross profit margin was 31.0% in Q4 2007, 33.6% in Q1 2008 and 36.2% in Q2 2008. Reported operating income margin was 10.0% in Q4 2007, 11.2% in Q1 2008 and 13.5% in Q2 2008. See GAAP to Non-GAAP reconciliation at the end of this presentation. ** Adjusted for $150 million gain related to certain commodity hedges

Returning Kraft to reliable growth

2007: Investment

2008: Sequential improvement

2009: We hit our stride− At least 4% organic revenue growth− 7%-9% EPS growth

17

18

Strategic Turnaround

Operational Turnaround

Financial Turnaround

19

Sanjay KhoslaPresident, Kraft International

International a vital part of Kraft

41%$16 Bn

Net Revenue

34%$1.7 Bn

Operating Income

202007 pro-forma estimated results including LU biscuit, excluding Post cereal.

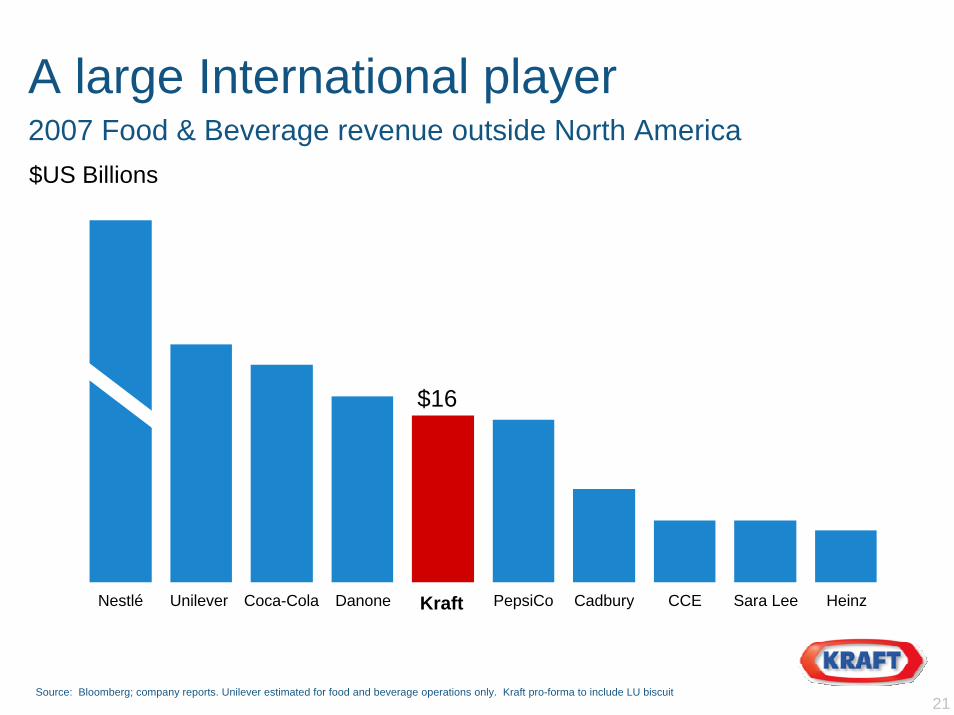

A large International player2007 Food & Beverage revenue outside North America

Nestlé Kraft

$16

Unilever Coca-Cola Danone CCEPepsiCo Cadbury Sara Lee Heinz

$US Billions

21Source: Bloomberg; company reports. Unilever estimated for food and beverage operations only. Kraft pro-forma to include LU biscuit

But not performing up to potentialKraft International

2003-2006 CAGR

2.4%Organic revenue growth*

22

(3.5)%

Operating income growthEx items*

* See GAAP to Non-GAAP reconciliations at the end of this presentation

BalanceCost & Quality

ExploitSales

CapabilitiesReframe

CategoriesRewire for

Growth

1 2 3 4

23

Three pillars to rewire Kraft International

1. Win locally, leverage globally

2. Build management depth

3. Focus where we can win

24

1. Win locally, leverage globally

Established a more flexible, decentralized business model

Empowered business units with full P&L responsibility

Linked pay structure to local results

Ensured leveraging of global expertise

25

2. Build management depth

Best of home-grown talent

Experienced international managers from the outside

Key leaders from LU biscuits

26

3. Focus where we can win

5 Categories

10 Brands

10 Markets27

5 Categories

Snacks Beverages

BiscuitsBiscuits

PowderedBev

PowderedBev

CheeseCheeseChocolateChocolate

CoffeeCoffee

Biscuits

Chocolate

Powdered Beverages

Coffee

Cream Cheese

28

Global Biscuits leader

Number 1 in key markets

More than 4X largest competitor

Seamless integration of LU biscuits

Accretive to earnings this year

29

Leveraging Biscuits for profitable growth

Increasing distribution strength in key markets

Expanding affordable nutrition platform in developing markets

Growing better-for-you alternatives in developed markets

30

Leveraging strong Snacks position for growthRevenue rank versus competition by region

EU EEMA LA APBiscuits 1 1 1 1Chocolate 3 1 2

31

Source: Euromonitor, AC NielsenKraft does not compete in this region

Strong share positions in all 5 categoriesRevenue rank versus competition by region

EU EEMA LA APBiscuits 1 1 1 1Chocolate 3 1 2Powdered Beverages 1 1 1Coffee 1 2Cream Cheese 1 1 1

32

Source: Euromonitor, AC NielsenKraft does not compete in this region

10 BrandsComposite organic revenue growth

H1 2008

14%11%

2007

6%

’03-’06CAGR

33

Building a global icon, market by market

34

Oreo in Asia for more than 10 years but not growing

Reframed into individually-wrapped, wafer forms

Extending into all channels, new countries

2007 Oreo sales +51%; +46% 2008 first half

Trading up our power brands

35

Improving quality, increasing marketing on the core

Moving from mainstream to upper mainstream

Higher margins from trading up consumers

10% growth in 2007, 18% growth 2008 first half

Growing a classic premium brand

Enhancing mix of coffee business

Expanding into new segments, new geographies

Strong organic growth in 2007, 2008 year-to-date

36

10 Markets60% of international revenue; 70% of profit

37

10 Markets4 Growth Engines

38

10 Markets4 Growth Engines6 Scale Markets

39

Three pillars to rewire Kraft International

1. Win locally, leverage globally

2. Build management depth

3. Focus where we can win

40

Gaining momentum11.7%

2.4%

03-06 CAGR

6.8%Organic RevenueGrowth*

Kraft International

2007 H1 2008

15.0%**

(3.5)%

3.0%

Operating IncomeGrowth (ex items)*

2007 H1 2008

03-06 CAGR

* See GAAP to Non-GAAP reconciliation at the end of this presentation** Organic OI growth (excluding currency and LU biscuit); See GAAP to Non-GAAP reconciliation at the end of this presentation

41

Best is yet to come

Organic Net Revenue Growth* Margin

2003-2006 CAGR

LTTarget

LTTarget

European Union (0.5) 1-3 ++

Developing Markets 7.4 8-10 +

42* See GAAP to Non-GAAP reconciliation at the end of this presentation

International is key to Kraft’s growth

Right strategy

+ Right people in the right places

+ Right focus

43

International is key to Kraft’s growth

Right strategy

+ Right people in the right places

+ Right focus

= Powerful growth engine for Kraft

44

45

Tim McLevishChief Financial Officer

46

Strategic Turnaround

Operational Turnaround

Financial Turnaround

Long-term growth model

Pricing and productivity cover input cost inflation

Volume and mix drive margin expansion

47

Long-term growth model

Organic Revenue Growth 4%+

Manufacturing, Overhead Leverage 2-3pp

Cash Flow Leverage & Tax Rate 1-2pp

Long-Term EPS Growth 7%-9%

48

Near-term drivers different

Cost-driven pricing a bigger factor

Volume and mix pressure due to pricing

Driving greater cost reductions to protect investments for long-term growth

49

Tightly controlling costs

Greater savings from Restructuring− Total program savings of $1.4 billion; +$200mm− Savings to reach $1.1 billion in 2008 − Spending $900 million in 2008; $3.0 billion total program

Savings beyond Restructuring− Costs into P&L as ordinary cost of doing business− Continue to optimize manufacturing network− Reduce overhead costs by at least 1% of Net Revenue

50

2008 Guidance update

Organic net revenue growth at least 6%

EPS excluding items at least $1.88− Adjusted downwards by $(0.04) from exiting

Post cereals in August− Effective tax rate ~33.0%

51

2009 Guidance

Organic net revenue growth at least 4%− Impact from pricing dependent on input cost trends

GAAP EPS at least $2.00− Double-digit growth from continuing operations,

excluding items− $200-300 million spending on cost-saving

initiatives− $(0.03) residual impact from exiting Post cereals

52

$1 billion annual cash flow improvement

Earnings growth− “Pay as you go” restructuring

Other opportunities over time− Primary working capital below 11% of net revenue− Capital Spending below 3% of net revenue

53

Summary

Gaining momentum at midpoint of turnaround

Strengthening our global portfolio

Driving improved financial results

54

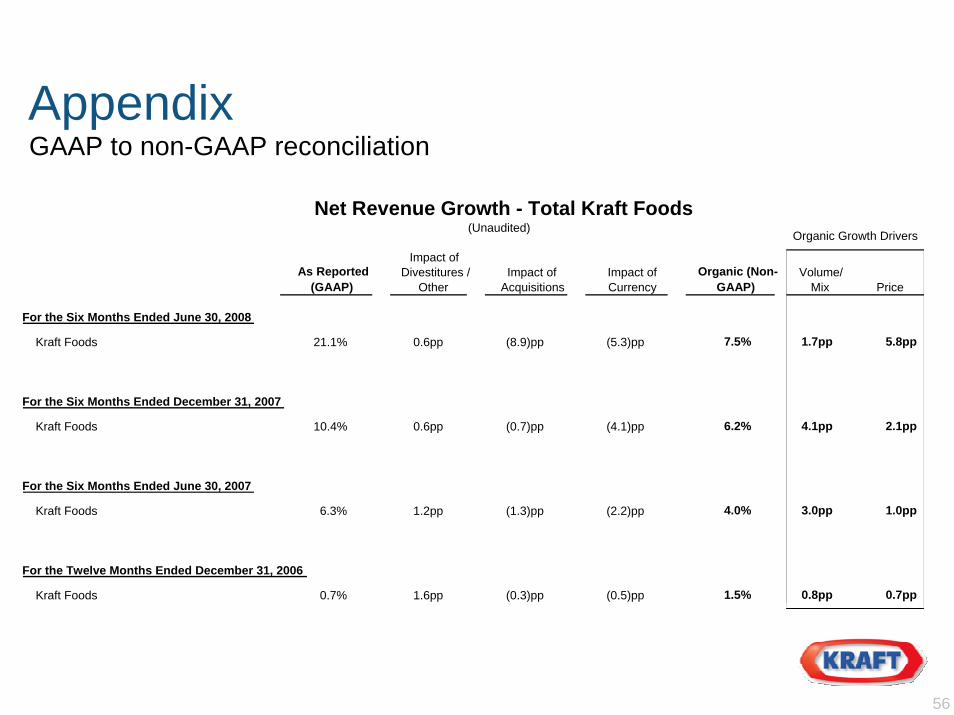

AppendixGAAP to non-GAAP reconciliation

(Unaudited)Net Revenue Growth - Total Kraft Foods

Organic Growth Drivers

56

As Reported (GAAP)

Impact of Divestitures /

OtherImpact of

AcquisitionsImpact of Currency

Organic (Non-GAAP)

Volume/Mix Price

For the Six Months Ended June 30, 2008

Kraft Foods 21.1% 0.6pp (8.9)pp (5.3)pp 7.5% 1.7pp 5.8pp

For the Six Months Ended December 31, 2007

Kraft Foods 10.4% 0.6pp (0.7)pp (4.1)pp 6.2% 4.1pp 2.1pp

For the Six Months Ended June 30, 2007

Kraft Foods 6.3% 1.2pp (1.3)pp (2.2)pp 4.0% 3.0pp 1.0pp

For the Twelve Months Ended December 31, 2006

Kraft Foods 0.7% 1.6pp (0.3)pp (0.5)pp 1.5% 0.8pp 0.7pp

AppendixGAAP to non-GAAP reconciliation

(Unaudited)Net Revenue Growth - Kraft International

Impact of Divestitures /

OtherOrganic (Non-

GAAP)As Reported

(GAAP)Impact of

AcquisitionsImpact of Currency

For the Years Ended:

2004European UnionDeveloping Markets

International

6.2%4.8%5.7%

3.2%13.9%7.0%

(0.6)%11.2%3.9%

19.2%17.1%18.4%

56.9%40.0%50.1%

2.0pp 0.0pp(0.7)pp

(10.1)pp(1.8)pp(7.1)pp

(1.9)%2.8%0.5pp

1.4pp (0.2)pp (0.2)%

2005European UnionDeveloping Markets

International

1.0pp 0.0pp (3.1)pp 1.1%0.6pp 0.0pp (4.6)pp 9.9%0.9pp 0.0pp (3.6)pp 4.3%

2006European UnionDeveloping Markets

International

0.2pp (1.7)pp0.0pp

1.4pp(2.1)pp

0.1pp

(0.7)%9.6%3.2%

0.5pp0.3pp (1.1)pp

2007European UnionDeveloping Markets

International

0.0pp (5.1)pp (10.5)pp(5.4)pp(8.5)pp

3.6%11.5%

6.8%0.0pp (0.2)pp0.0pp (3.1)pp

For the six months ended June 30, 2008:European UnionDeveloping Markets

International

1.7pp (37.2)pp (15.0)pp(9.9)pp

6.4%19.3%11.7%

0.0pp (10.9)pp0.9pp (26.4)pp (12.9)pp

Compound Annual Growth Rate, 2003 - 2006:European UnionDeveloping Markets

International

(0.5)%7.4%2.4%

57

AppendixGAAP to non-GAAP reconciliation

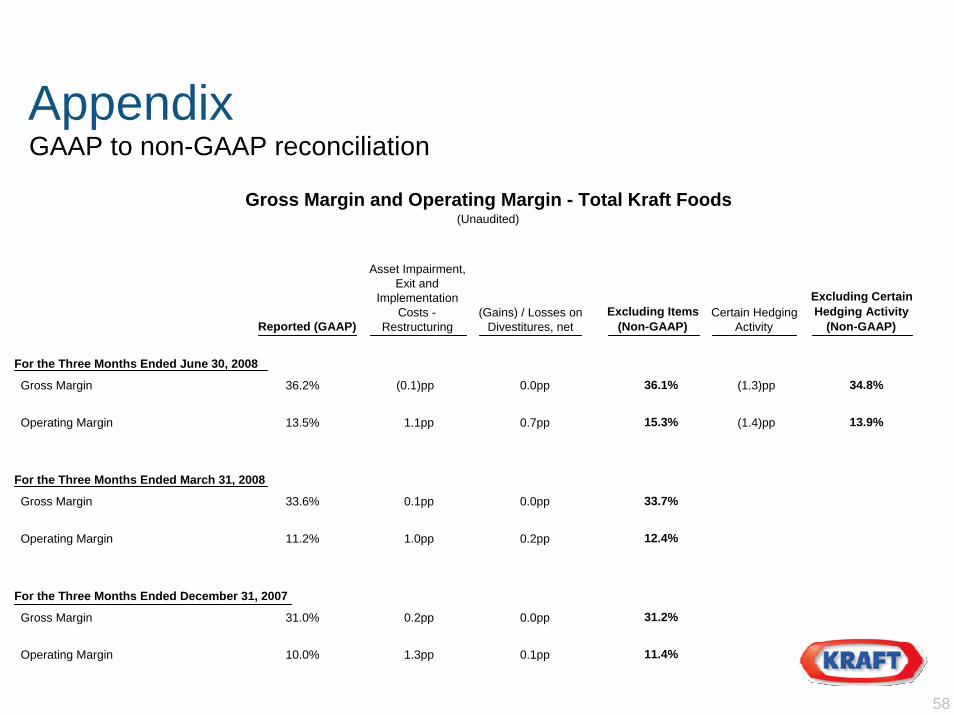

Gross Margin and Operating Margin - Total Kraft Foods(Unaudited)

Asset Impairment, Exit and

Implementation Costs -

Restructuring

Excluding Certain Hedging Activity

(Non-GAAP)Excluding Items

(Non-GAAP)(Gains) / Losses on

Divestitures, netCertain Hedging

ActivityReported (GAAP)

For the Three Months Ended June 30, 2008

Gross Margin

Operating Margin

For the Three Months Ended March 31, 2008

Gross Margin

Operating Margin

For the Three Months Ended December 31, 2007

Gross Margin

Operating Margin

36.2%

13.5%

33.6%

11.2%

31.0%

10.0%

36.1% 34.8%(0.1)pp 0.0pp (1.3)pp

15.3% 13.9%1.1pp 0.7pp (1.4)pp

33.7%0.1pp 0.0pp

12.4%1.0pp 0.2pp

31.2%0.2pp 0.0pp

58

11.4%1.3pp 0.1pp

AppendixGAAP to non-GAAP reconciliation

Operating Income Growth - Kraft International(Unaudited)

Asset Impairment, Exit and

Implementation Costs -

Restructuring

Asset Impairment and Other Costs -Non-Restructuring

Excluding Items (Non-GAAP)

(Gains) / Losses on Divestitures, netReported (GAAP)

For the Twelve Months Ended December 31, 2004

Operating Income Growth (33.0)% 15.6pp 3.4pp 2.1pp (11.9)%

For the Twelve Months Ended December 31, 2005

Operating Income Growth 20.3% (7.9)pp (4.4)pp (9.3)pp (1.3)%

For the Twelve Months Ended December 31, 2006

Operating Income Growth (14.1)% 14.2pp 14.0pp (10.7)pp 3.4%

For the Twelve Months Ended December 31, 2007

3.0%Operating Income Growth 10.2% (12.9)pp (11.2)pp 16.9pp

2003 - 2006 Compound Annual Growth Rate (3.5)%

59

AppendixGAAP to non-GAAP reconciliation

Organic Operating Income Growth - Kraft International(Unaudited)

Asset Impairment and Other Costs -

Non-Restructuring

Asset Impairment, Exit and

Implementation Costs -

Restructuring

LU Acquisition, net of

Integration Costs Organic

(Gains) / Losses on

Divestitures, net

Excluding Items

(Non-GAAP)

Impact ofDivestitures /

OtherReported (GAAP) Currency

For the Six Months Ended June 30, 2008

Operating Income Growth 43.6% 53.0% 15.0%(8.9)pp 0.7pp 17.6pp 1.6pp (11.1)pp (28.5)pp

60