senegal - world banksiteresources.worldbank.org/.../eiu_country_profile_senegal.pdf · country...

TRANSCRIPT

Country Profile 2005

SenegalThis Country Profile is a reference work, analysing thecountry’s history, politics, infrastructure and economy. It isrevised and updated annually. The Economist IntelligenceUnit’s Country Reports analyse current trends and provide atwo-year forecast.

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where itslatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

Copyright© 2005 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1352-092X

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Senegal 1

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Contents

Senegal

3 Basic data

4 Politics4 Political background5 Recent political developments8 Constitution, institutions and administration9 Political forces12 International relations and defence

14 Resources and infrastructure14 Population15 Education16 Health16 Natural resources and the environment17 Transport, communications and the Internet20 Telecommunications indicators20 Internet service subscribers21 Energy provision

23 The economy23 Economic structure24 Economic policy28 Economic performance30 Inflation30 Regional trends

30 Economic sectors30 Agriculture34 Mining and semi-processing36 Manufacturing37 Financial services38 Other services

39 The external sector39 Trade in goods40 Invisibles and the current account40 Capital flows and foreign debt41 Foreign reserves and the exchange rate

42 Regional overview42 Membership of organisations

49 Appendices49 Sources of information50 Reference tables50 Population50 Gross domestic product

2 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

50 Gross domestic product by origin51 Gross domestic product by expenditure51 Gross domestic product by expenditure52 Government finances52 Consumer prices52 Money supply, credit and interest rates53 Mineral production53 Selected tourism statistics53 Agricultural production and prices53 Fishing54 Exports54 Imports54 Key imports and exports55 Trading partners55 Balance of payments, IMF series56 Balance of payments, national series56 External debt57 Official development assistance (net)a57 Foreign reserves57 Exchange rates

Senegal 3

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

SenegalBasic data

197,161 sq km

11.66m (mid-2005; UN Population Division estimate)

Population in ‘000 (World Gazetteer estimates)

Dakar (capital) 2,352Thiès 252Kaolack 177St Louis 160

Tropical

Hottest months, September-October, 24-32°C; coldest month, January, 18-26°C;driest months, April-May, 1 mm average rainfall; wettest month, August,254 mm average rainfall

French, Wolof, other local languages

Metric system

CFA franc (CFAfr), fixed to the euro, backed by a guarantee from the Banque deFrance. It was devalued from CFAfr50:FFr1 to CFAfr100:FFr1 in 1994, thenconverted at par when France adopted the euro in 1999 to trade atCFAfr655.96:€1. Average exchange rate in 2004: CFAfr528:US$1; exchange rate onAugust 9th 2005: CFAfr532:US$1

GMT

January 1st; April 4th (Independence Day); May 1st; Christian holidays ofChristmas, All Saints, Assumption and variable dates for Easter Monday andAscension; Muslim holidays with variable dates for Maulid, Eid el Fitr (Korité),Eid el Adha (Tabaski)

Total area

Population

Main towns

Climate

Weather in Dakar(altitude 40 metres)

Languages

Measures

Currency

Time

Public holidays

4 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Politics

The Parti socialiste (PS) governed Senegal from independence in 1960, at firstunder the presidency of Léopold Sédar Senghor and then under Abdou Diouf,until 2000, when the veteran opposition politician, Abdoulaye Wade, won thepresidential election. A new constitution was passed in January 2001, allowingMr Wade to dissolve the PS-dominated National Assembly (parliament). Anearly legislative election was held in April 2001, and the electoral alliance (laternamed the Convergence des actions autour du Président en perspective du21ème siècle—CAP21) led by Mr Wade’s Parti démocratique sénégalais (PDS)obtained a large majority. The nature of the change in power enhancedSenegal’s reputation as a relatively stable African democracy. The signature of apeace accord between the government and the leaders of the rebellion inCasamance, in the south, at the end of 2004, have also helped in this regard.The government has a sufficiently solid political base to enable it to carry outfurther political and economic reforms and attempt to address Senegal’spersistent social tensions. The next legislative election is scheduled to take placein 2006 and a presidential election is due to be held in 2007.

Political background

Senegal’s recorded history dates from the 8th century, when it was part of theempire of Ghana. The settlements south of the Senegal River were regularlyinvaded by Sahelian Muslim armies until the 15th century. Portuguese tradersestablished a trading post on the island of Gorée (which later became infamousas the last staging post for the slave trade to the Americas) in the early 1500s. In1588 the Dutch ousted the Portuguese and occupied Gorée; meanwhile, theBritish and French were fighting over trading posts on the mainland. By 1641France had established a permanent presence in what is now Senegal. In 1895the country became the centre of French West Africa.

In January 1959 Senegal joined French Soudan (now Mali) to form the Federationof Mali. The federation achieved full independence from France in April 1960 butbroke up in August of that year, and Senegal became a republic with LéopoldSédar Senghor as its first president. In the mid-1960s Senegal became a de factoone-party state under the ruling Union progressiste sénégalaise (UPS). In 1974multiparty politics was restored with the recognition of two opposition parties,including the Parti démocratique sénégalais (PDS). In 1978 four officiallyrecognised political parties were permitted to compete in the legislative election,which went smoothly despite allegations of fraud from the opposition. The UPS,renamed the Parti socialiste (PS), won 82 of the 100 seats in the NationalAssembly, and the PDS won the 18 remaining seats.

In 1981 Mr Senghor retired and moved to France (where he lived until his deathin December 2001). He was replaced by his prime minister, Abdou Diouf. In thelegislative and presidential elections of 1983, the PS and Mr Diouf won aresounding victory. The 1988 elections returned Mr Diouf to the presidency andthe PS retained its large majority in the expanded National Assembly, with 103

Early history

The Senghor presidency

The Diouf presidency

Senegal 5

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

seats out of 120. This time, however, the results sparked off rioting in the capital,Dakar, amid allegations of flagrant electoral fraud. Mr Wade, the PDS’spresidential candidate, was arrested and briefly imprisoned. Political tensionseased the following year, when attention focused on a border conflict withMauritania which escalated into communal violence in both countries (seeInternational relations and defence).

Under pressure from the international community, Mr Diouf formed agovernment of national unity in 1991. Several opposition leaders, includingMr Wade, accepted ministerial posts. In 1993 Mr Diouf was re-elected under anew electoral code. The PS’s majority in the National Assembly was reduced,and the PDS increased its representation from eight to 27 seats. The oppositionagain accused the government of electoral fraud, and, when the vice-presidentof the Constitutional Court was assassinated before the announcement of theresults, Mr Wade and other opposition leaders were arrested briefly. Politicaltension continued, and in January 1994 rioting broke out in Dakar after thedevaluation of the CFA franc led to sharp price increases for many goods.

A new unity government was formed in 1995, when Mr Wade and several otheropposition politicians were given ministerial posts. Within the PS a powerstruggle arose, with Ousmane Tanor Dieng being chosen in 1996 as secretary-general of the party instead of the former minister of the interior, Djibo Kâ.Mr Kâ and other disgruntled PS leaders left the party before the May 1998legislative election to form the Union pour le renouveau démocratique (URD).Mr Wade and his colleagues resigned their ministerial posts at the same time.

Although the PS polled only 50% of the vote in the legislative election in May1998, it retained 93 of the now 140 assembly seats. The PS again chose Mr Dioufas its candidate in the February 2000 presidential election. Although severalminor opposition parties backed his candidacy, the PS itself fractured further.Most notably, Moustapha Niasse, a former PS leader, split from the party toform the Alliance des forces de progrès (AFP), and stood against Mr Diouf inthe first round.

Recent political developments

The first round of voting in the 2000 presidential election took place onFebruary 27th. Turnout was high, at 62%, and the poll was deemed to be largelyfree and fair. Mr Diouf won 41% of the vote (less than the 50% necessary toprevent a run-off), and Mr Wade—who promised social and economic sopi(“change” in Wolof) from the PS era and had stood (and lost) in everypresidential poll since 1978—was close behind, with 31%. Therefore, for the firsttime in Senegal’s post-independence history, a second round of voting washeld. Although tensions were high, the second round passed peacefully.Mr Niasse threw his support behind Mr Wade, allowing the latter to win 58.5%of the vote, compared with 41.5% for Mr Diouf. By conceding defeat well beforethe final result was announced, Mr Diouf won national and internationalpraise. Mr Wade soon formed a coalition government, including representativesof several of the parties that had supported him in the presidential race, with

Unity governments

Mr Wade wins the presidency

Power of the Parti socialistediminishes

6 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Mr Niasse as prime minister. However, political tensions rose between thevarious parties in the coalition government over the wording of the newconstitution that was to be approved in a referendum in January 2001. Themost notable dissension came from the Parti de l’indépendance et du travail(PIT), which preferred a dilution of the powers of the presidency, and this led tothe sacking of its secretary-general, Amath Dansokho, as minister of urbanplanning and housing. Tensions continued after the referendum in the run-upto the legislative election in April, leading to the departure of several partiesfrom the coalition, including Mr Niasse’s AFP.

Presidential election, 2000First round Second round

No. of votes % of total No. of votes % of totalAbdou Diouf 690,886 41.33 687,969 41.51Abdoulaye Wade 517,642 30.97 969,332 58.49

Moustapha Niasse 280,885 16.76 – –Djibo Kâ 118,487 7.09 – –Iba der Thiam 20,163 1.20 – –

Ousseynou Fall 18,676 1.12 – –Cheikh Abdoulaye Dièye 16,216 0.97 – –

Mademba Sock 9,318 0.58 – –

Source: Constitutional Court.

As was widely expected, the PS lost its ruling majority by a landslide in theApril 2001 legislative election, retaining only ten seats in the new NationalAssembly. This in effect put an end to the uneasy period of “cohabitation” thathad persisted since Mr Wade was elected to the presidency. The PDS-dominatedcoalition obtained a larger than expected majority of 89 seats in the 120-seatparliament. Whereas the PS—badly affected by its loss of the presidency, thesubsequent wave of defections to other parties, and recent evidence ofcorruption—was poised to perform poorly, the AFP seemed well positioned toundermine the gains of the PDS coalition. However, the AFP obtained only 11seats. This, together with a high turnout of 67.4%, represented a strong vote ofconfidence in Mr Wade and his party. This was further confirmed by the May2002 local government elections, although the opposition coalition, led by thePS and AFP, managed to retain control of two regions (out of ten) and aboutone-third of the municipal and rural councils.

Legislative election results1998 2001

% of votes No. of seats % of votes No. of seatsParti démocratique sénégalais (PDS) & sopi coalition 19.1 23 49.6 89Alliance des forces de progrès (AFP) – – 16.1 11

Parti socialiste (PS) 50.1 93 17.4 10Union pour le renouveau et la démocratie (URD) 13.2 11 3.7 3And-jëf/Parti africain pour la démocratie et le socialisme (AJ/PADS) 5.0 4 4.0 2

Total incl others 100.0 140 100.0 120

Source: Government press release.

Legislative election in 2001

Senegal 7

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Important recent events

March 2000Abdoulaye Wade wins 58.5% in the second round of the presidential election, withpromises of social and economic sopi (change). After a smooth transfer of powerMr Wade appoints a multiparty government, lead by his Parti démocratiquesénégalais (PDS).

April 2001

A legislative election gives the parties allied with Mr Wade a large majority inparliament.

May 2002

Local elections give Mr Wade’s coalition control of eight out of ten regions and two-thirds of municipal and rural councils.

October 2003

The vicious beating of an opposition figure, Talla Sylla, possibly by supporters of thepresident, provokes large street rallies and heightened tension between theopposition and the government.

April 2004

After months of trying, Mr Wade manages to broaden the governing coalition withthe inclusion of the opposition Union du renouveau démocratique (URD). Aconcurrent cabinet reshuffle see the replacement of Idrissa Seck as prime minister.

December 2004

The government and the separatist movement, Mouvement des forcesdémocratiques de Casamance (MFDC), sign a peace accord, 22 years after the start ofthe conflict in Senegal’s southern region, Casamance.

July 2005

Mr Seck is detained in Dakar’s central prison over corruption allegations concerningpublic-works contracts. Two weeks later the National Assembly votes to sendMr Seck before a special court for trial, and the PDS decides to expel him from theparty.

Between April 2000, at Mr Wade’s assumption of the presidency, and August2005, Senegal has had nine cabinet reshuffles and four different primeministers. In part, this has reflected changing political alignments, most notablythe departure of the AFP and the PIT to the opposition during the first year ofMr Wade’s presidency, the departure of the Ligue démocratique/Mouvementpour le travail (LD/MPT) from government in March 2005 and the URD’s shiftfrom the opposition to the government in April 2004. In addition, as somedegree of public disillusionment set in with the government’s failure to fulfil allof its ambitious campaign promises and as the opposition became more vocal,the office of the prime minister has taken on a higher political profile, shiftingfrom a non-party technocrat, Mame Madior Boye, in 2001-02, to two successivePDS heavyweights, Idrissa Seck in November 2002 and Macky Sall in April2004. This has coincided with the ruling party’s decision to go on an early

Continued instability in thegoverning coalition

8 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

campaign footing in advance of the next legislative election in 2006 andMr Wade’s re-election bid in 2007.

Several other factors also have contributed to the rapid rotation of cabinetministers. Although Mr Wade carries considerable charismatic influence withsections of the public, his style of interaction with other government and partyleaders has been arbitrary and abrupt, contributing to tensions at the top. Inaddition, there are numerous frictions between the different parties comprisingthe governing coalition, Convergence des actions autour du Président enperspective du 21ème siècle (CAP21), sometimes with leaders of non-PDSparties—including cabinet ministers—taking public positions that are critical ofcertain aspects of the government’s conduct or policies.

Some of the most intense conflicts have erupted within the PDS itself, not overideological or political disagreements, but as competing factions vie with eachother for cabinet posts, parliamentary nominations or other state offices. Thereplacement in April 2004 of the prime minister, Mr Seck—the second-highestranking PDS leader—with Mr Sall, another influential party figure, was one signof the turbulence that afflicts the ruling party, highlighting the feud betweenpro-Seck and pro-Wade factions of the PDS. The 12 rebel PDS deputies who leftthe majority parliamentary group—Libéral et démocratique (LD)—in April 2005and established an alternative group, Forces des alternances (FAL), decided torejoin the LD in June, preventing a politically damaging schism within the PDS.However, the charges brought against Mr Seck in July (of violating public tenderprocedures on public works and of breaching national security) have beenwidely perceived as politically motivated. It is likely that the case will furtherdamage the PDS, and Mr Wade’s government.

Constitution, institutions and administration

The Senegalese constitution of 1963 was progressively revised to develop asystem in which the president, as head of state, appoints the prime minister whoin turn appoints the Council of Ministers. No legislation can be passed withoutthe president’s signature. The president, elected by universal suffrage, may actindependently in particular areas, including foreign policy, defence and justice.The amended constitution, approved by referendum in January 2001, essentiallyretained these strong presidential powers. It did, however, reintroduce a two-term limit on the presidency (which had been eliminated in 1998) and reduce thelength of the terms from seven years to five. A special “transitional” provisionclarified, however, that Mr Wade could serve out his seven-year mandate.

The new revised constitution provides for a unicameral legislature, the NationalAssembly, of 120 seats. This is a reversal of the changes introduced by theprevious PS-dominated parliament, which in 1998 increased the number ofseats to 140 and set up the Senate as an advisory body. Both moves werepolitically unpopular, and were widely seen as a means to secure morepositions for disgruntled PS leaders. The amended constitution gave theNational Assembly greater authority to question the policies of the governmentand to force the cabinet’s resignation through a motion of no confidence or

A presidential system

A strengthened legislature

Intense disagreements withinruling party

Senegal 9

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

censure. It also increased the president’s power to dissolve parliament before itsmandate expires. Contrary to previous regulations, any deputy who switches toanother party now loses his or her seat, a measure intended to ensure greaterpolitical stability by making political “nomadism” more difficult. A strictlyadvisory second body, the Council of the Republic, was established in 2003.

In 1991 the Supreme Court was dissolved and its functions divided among threehigh courts, along the lines of the French judicial model. In the January 2001constitutional amendments, the number of high courts was increased to five.The Constitutional Court is empowered to adjudicate on the electoral process. Inaddition, an electoral monitoring body, the Observatoire national des élections(Onel), was created in August 1997 to observe all phases of the electoral process,from voter registration through to the announcement of results. It has beencredited with responsibility for the dramatic reduction in electoral fraud.Nonetheless, Onel was seen as insufficiently autonomous of the state and,therefore, the ruling party. The law creating the Commission électoral nationalautonome (CENA), was unanimously passed by the National Assembly in May2005. After a month’s delay, the 12 members of the CENA were appointed bypresidential decree.

Senegal’s sub-national administrative and government structures are in a stateof transition owing to efforts to decentralise central government functions tothe regions, with the help of the World Bank. In 1984 Senegal was divided intoten regions: Dakar (formerly Cap Vert), Saint-Louis (formerly Fleuve), Diourbel,Thiès, Tambacounda (formerly Sénégal oriental), Louga, Kaolack and Fatick(which previously comprised a single region, Sine-Saloum), and Kolda andZiguinchor (which previously comprised the troubled region of Casamance). InJanuary 2002 Matam, formerly a department in Saint-Louis, became a newregion. Each region is divided into three departments, with the exception ofSaint-Louis, which has four, and each of these departments is divided intoseveral arrondissements. An initial “pre-draft” of a government plan to abolishthe ten regions in favour of 35 provinces provoked such widespread oppositionthat it was quickly withdrawn.

Political forces

Although formally a multiparty democracy, with over 40 political parties and ahistory of entrenched civil liberties, Senegal was in practice a one-party statefrom independence until the March 2000 presidential election. The victory ofMr Wade changed the political scene dramatically. Although many members ofthe former ruling PS—which espoused socialism and state-control—subsequentlydefected to Mr Wade’s PDS (which describes itself as a liberal party), the latterhas not simply replaced the PS as the dominant political force, but operates in amore pluralist environment. A number of parties secured cabinet positions inthe new coalition government—this first coalition included not only partiesallied with the PDS, but also Mr Niasse’s AFP, which in March 2001 joined theopposition—and several parties formed an alliance with the PDS in the April2001 legislative election. The other party that currently forms part of the cabinetis the And jëf/Parti africain pour la démocratie et le socialisme (AJ/PADS); it

The Constitutional Court

A dramatic shift towardspolitical pluralism

The regions

10 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

originally espoused Marxist views, although over the past decade party officialshave generally referred to themselves simply as being on the left. This has notprevented AJ/PADS from forging a close political alliance with the PDS.

Nor is the opposition a coherent bloc, since the remainder of the PS mustoperate alongside several other parties, which sometimes manage to unite (asduring the May 2002 local elections) but can take quite divergent positions. Thegoverning coalition, CAP21, formed in August 2001, is not synonymous withthe government, as it includes far more parties than are actually represented inthe cabinet. The increased level of pluralism may bring greater politicaluncertainty and shifting alliances in the short term, but overall it represents asignificant deepening of Senegal’s democratic system.

Main political figures

Abdoulaye Wade

The 79-year-old leader of the Parti démocratique sénégalais (PDS) and its candidatein every presidential election since 1978, Mr Wade was elected president in March2000. He has pledged to tackle corruption, to involve the young in reconstructionefforts, and to promote the country’s economic and social development vigorously.His presidential style has drawn considerably on his personal charisma, sometimesstamping his government with an image of ad hoc decision-making.

Macky Sall

Named prime minister in April 2004, he has been active in the PDS since 1987.A geological engineer by training, he is well regarded as an able and methodicaladministrator, qualities he demonstrated when he was minister of energy, mines andwaterworks and as minister of the interior. At the same time, he carries significantpolitical clout within the PDS, and heads the party’s influential think-tank, theCellule initiative et stratégie (CIS).

Idrissa Seck

The PDS’s second-in-command since mid-1998 and prime minister from November2002 to April 2004, Mr Seck has been a source of controversy within the party andwith several of the PDS’s allies within the governing coalition, the Convergence desactions autour du Président en perspective du 21ème siècle (CAP21). The decision tohave Mr Seck tried on corruption charges by a special tribunal and to expel himfrom the PDS, suggest that Mr Wade increasingly saw his former protégé as a seriouspolitical rival.

Djibo Kâ

Mr Kâ was one of the most powerful barons in the Parti socialiste (PS) until 1996. Heleft the PS two years later to form his own party, the Union du renouveaudémocratique (URD), but secured only 7.1% of the vote in the presidential election. InApril 2004 he broke with the opposition and brought his party into the government.

Landing Savané

One of Senegal’s most articulate and radical political figures, Mr Savané leads theleft-wing And-jëf/Parti africain pour la démocratie et le socialisme (AJ/PADS). He wasappointed minister of mines in April 2000 before being moved to the Ministry ofIndustry and Crafts.

Senegal 11

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Moustapha Niasse

Mr Niasse has long been a leading political figure, serving in cabinet during thepresidency of Léopold Sédar Senghor. In June 1999 he broke with the PS andsubsequently launched his own party, the Alliance des forces de progrès (AFP). Hestood against the PS incumbent, Abdou Diouf, in the first round of the 2000presidential election, but supported Mr Wade in the second round. He was rewardedwith the prime ministership in April 2000, but was dismissed in March 2001 as hisparty prepared to stand against Mr Wade’s PDS in the legislative election. He hasemerged as a particularly acerbic critic of the government.

Ousmane Tanor Dieng

Following Mr Diouf’s failure to retain the presidency, Mr Dieng gained theleadership of the weakened PS. Intelligent but abrasive, he has managed to facedown his rivals within the PS and has sought to project the image of a “responsible”opposition leader.

Augustin Diamacoune Senghor

The central leader of the rebel Mouvement des forces démocratiques de laCasamance (MFDC), Father Diamacoune, who is in his 70s, has been pushing hisgroup towards peace, despite some challenges to his authority within themovement.

The government and opposition parties have always had to take into accountthe marabouts (spiritual leaders) of the Islamic brotherhoods (turuq), especiallywhen dealing with rural issues. The Mouride brotherhood is the mostinfluential. Other brotherhoods include the Tijaniyya (or Tidianes), theNiassiyya, the Qadiriyya and the Layenne brotherhoods. Reformist Muslimorganisations, which have a more explicitly Arabist orientation and a moreclearly defined political agenda than the traditional Islamic brotherhoods, havebeen gaining ground in Dakar and other urban areas. Until the mid-1990s the PScould count on support from the leaders of the most powerful Islamicbrotherhoods. However, the decline of the groundnut industry led to growingrural hardship and contributed to the erosion of the PS’s power. Mr Wade, adevout Muslim, has cultivated his own political ties with the marabouts (inparticular he has strong links with the Mouride brotherhood and its head,Serigne Saliou Mbacké), although he has strongly defended the secular natureof the state and the courts against those that promote sharia law.

Labour discontent was a factor in undermining electoral support for the PS,but the trade unions have also been a constant source of pressure onMr Wade’s government. Trade union membership is widespread in the urbanformal sector, although the trade union movement is weakened by the gulfbetween leaders and workers, and by corruption among union officials.Nonetheless, strike activity is commonplace, and the country’s large civilservice articulates its demands confidently, especially now that thegovernment has started to press ahead with the privatisation of major stateenterprises. The PDS failed in its effort in late 2001 to displace the pro-PSleadership of the Confédération national des travailleurs sénégalais, one of thelargest labour federations.

The Islamic brotherhoods

Trade unions

12 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

The Casamance separatists

The southern Casamance region has been a problem since colonial times. In contrast to other regions of Senegal, thedominant ethnic group, the Diola, had no social hierarchy that the French could use to administer the region. As aresult, the French used northern Senegalese to serve as local administrators. After independence, regional leaderswere absorbed into the government but, because of their lack of political influence, state investment in infrastructureand development projects in the region was neglected. In the late 1970s a land reform programme that resulted inthe transfer of land in the region to northern Senegalese sparked demonstrations and ultimately the formation of anarmed resistance movement, Mouvement des forces démocratiques de la Casamance (MFDC). In 1991 a peace accordwas signed, but the more radical southern front of the MFDC refused to lay down its arms. A new ceasefireagreement was signed in 1993. However, when the government refused to discuss the MFDC’s demand forindependence, violence resumed, increasing in intensity until late 1995. In December of that year the MFDC’spolitical leader, Father Augustin Diamacoune Senghor, issued a call to lay down all weapons, but in August 1997 theceasefire again broke down.

In 1997-98 an army offensive destroyed most of the MFDC’s bases on the Guinea-Bissau border, and Senegal’sintervention in Guinea-Bissau in June 1998 cut further supply-lines to the MFDC. In January 1999 the then president,Abdou Diouf, and Father Diamacoune met for the first time, and in December 1999 formal negotiations openedbetween the government and the MFDC. After some hesitation, the government of Abdoulaye Wade resumed thepeace process in December 2000, following Mr Wade’s election to the presidency in March 2000. By early 2004 theceasefire was holding well, some MFDC fighters had begun to demobilise and rehabilitation projects started to getunder way. The government and the MFDC signed a peace accord on December 30th 2004, 22 years after the start ofthe conflict. Hopes for the success of this agreement—compared with previous ones—are greater because of the high-level political commitment: it was signed by the MFDC’s central leader and Mr Wade himself, and has beenfollowed by detailed talks on concrete issues such as disarmament and the reintegration of ex-combatants. However,the attainment of peace will continue to be obstructed by sporadic fighting and banditry, and by serious divisionswithin the political and military leaderships of the MFDC.

International relations and defence

In exchange for helping to stop an attempted coup in The Gambia in 1981,Senegal entered into a confederation (Senegambia) with its small anglophoneneighbour. However, The Gambia dissolved the confederation in 1989, and itwas not entirely surprising that Senegal allowed a second Gambian coupattempt, in 1994, to succeed. Senegal has since normalised relations with TheGambia.

Relations with Mauritania are difficult, reflecting the tension between theArabic-speaking and black populations of that country. In 1989 a minor incidenton the border led to serious riots in both countries, in which hundreds ofpeople died. Diplomatic relations resumed in 1992, but tension flared up againin 1998, as a result of border clashes, and in 2000, when differences over acontroversial water project on the Senegal River almost led to the expulsion ofall Senegalese from Mauritania.

Relations with Guinea-Bissau have been complicated by the presence there ofmany refugees from Senegal’s Casamance region, and by the separatists’ use ofGuinea-Bissau as a base from which to conduct their operations. After civil warbroke out in Guinea-Bissau, Senegal sent 2,200 soldiers to support the

Relations with neighboursare tense

Senegal 13

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

beleaguered Bissau government in July 1998, withdrawing in March 1999 after apeace agreement was signed. The subsequent death of General AnsumaneMané, the most influential ally of the Casamance rebels in Guinea-Bissau,improved relations between the two countries. When the elected president ofGuinea-Bissau, Kumba Yala, was overthrown by a coup in September 2003,Mr Wade and several other West African leaders mediated the new junta’shandover to a civilian transitional government. Likewise, Mr Wade wasinstrumental as a mediator in the presidential election of 2005, when hepersuaded a reluctant Mr Yala to accept defeat.

Since his election Mr Wade has adopted a more active regional andinternational profile for Senegal. In December 2001 he became president ofboth the Economic Community of West African States (ECOWAS; a one-yearrotating position) and the Union économique et monétaire ouest-africaine(UEMOA). He was an initiator of the Omega Plan, which was subsequentlymerged with the Millennium Partnership for the African Recovery Programme(MAP) of the South African president, Thabo Mbeki, to become the NewPartnership for Africa’s Development (Nepad). This seeks to combine Africaneconomic development through political and economic reform with financialsupport from industrialised countries. Along with Mr Mbeki and the Nigerianpresident, Olusegun Obasanjo, Mr Wade officially launched the Nepadinitiative at the June 2002 G8 summit in Canada and has participated in allsubsequent discussions.

The International Institute for Strategic Studies estimates that Senegal’s armedforces totalled around 13,620 members in mid-2004, in addition to a paramilitarygendarmerie numbering about 5,000. The army is by far the largest element ofthe armed forces, although Senegal also has a small navy and air force. TheSenegalese army has always been loyal to the government, maintaining order—in the capital, Dakar, in particular—during turbulent elections. A special brigadeof the army has also been involved in counter-insurgency activities inCasamance since 1991.

In addition, Senegalese troops have been particularly active in regionalpeacekeeping operations, firstly under the auspices of the Organisation ofAfrican Unity, which has now been superseded by the African Union (AU), andthe UN, or by virtue of Senegal’s membership in ECOWAS (see Regionaloverview: Membership of organisations). Senegal has sent contingents toRwanda, the Central African Republic, the Democratic Republic of Congo(DRC), Côte d’Ivoire and Liberia as part of UN-led peacekeeping operations.Senegal has also sent police personnel to Sierra Leone as part of thepeacekeeping force controlled by the UN Mission in Sierra Leone. The army hasalso benefited from the presence of French army bases in Senegal, which hada contingent of around 1,130 soldiers in 2005. France gives technical assistanceto the army and conducts joint military exercises. The US has also givenfinancial and technical support to the Senegalese armed forces.

An active army

Mr Wade's proactive regionaland international stance

14 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Military forces, mid-2004Army 11,900Navy 950Air force 770

Total armed forces 13,620Gendarmerie 5,000

Source: International Institute for Strategic Studies, The Military Balance, 2004/05.

Security risk in Senegal

Senegal is widely perceived as one of the safer West African countries in terms ofcrime. This view is enhanced by the fact that there has been far less politicalinstability than in larger economies in the region such as Côte d’Ivoire or Nigeria. Amore appropriate comparison would be with Ghana. Although petty crime is aproblem, as in most developing countries, it is not a major issue. As in many Africancountries, foreigners are always a target for criminals. Although travel in most ofSenegal is safe, visits to Casamance are less so, given the long-running war betweenthe government and the separatist rebel force, the Mouvement des forcesdémocratiques de la Casamance (MFDC). Much of the fighting in recent years hasbeen at a low level of intensity, often little more than periodic skirmishes. Despitethe signing of a peace accord in December 2004, crime remains a problem and travelto Casamance is probably not advisable unless there is a pressing reason. Armedbanditry can also be a problem in rural areas and along the borders with TheGambia and Guinea-Bissau.

Resources and infrastructure

Population

Population indicatorsPopulation (mid-year; m)a 11.7Population growth rate (%)b 2.4

Fertility rate (live births per woman)b 5.1Life expectancy at birth (years)a 55.6

Population aged below 15 years (% of total)a 43.0Urban population (% of total)c 50.0

a 2005. b 2000-05 annual average. c 2004.

Source: UN Population Division.

The UN Population Division estimates for mid-2005 give a total population of11.7m, growing at a rate of 2.4% per year. The urban population is expandingmuch more rapidly, at an average of 3.9% per year. About 50% of the populationis estimated to live in urban areas, well above the regional average. The Dakarmetropolitan area contains an estimated 2m people and accounts for nearlyone-sixth of the country’s population. Despite the pace of urbanisation, formalemployment is fairly limited compared with rural employment and informal-sector activity. The total labour force was estimated at 4.6m in 2003, of whom43% were female. It is estimated that in 1990, the latest date for which figuresare available, 77% worked in agriculture, 16% in services and 8% in industry.

A swelling urban population

Senegal 15

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Around 25% of all children aged between 10 and 14 years were part of thatlabour force, employed mainly in agriculture and in informal trading and otherservices. The urban formal-sector unemployment rate has exceeded 20%.

Comparative human development indicators, 2002(% unless otherwise indicated)

Senegal Côte d’Ivoire Mali South Africa FranceHDI scorea 0.437 0.399 0.326 0.666 0.932Real GDP per head (US$; in PPPb terms) 1,580 1,520 930 10,070 26,920Life expectancy at birth (years) 52.7 41.2 48.5 48.8 78.9

Adult literacy rate 39.3 49.7 19.0 86.0 99.0Population without access to: Safe water 22 19 35 14 n/a Essential drugs 21-50 6-20 21-50 6-20 0-5 Sanitation 30 48 31 13 n/a

Population not expected to survive to age 40 27.7 51.7 35.3 44.9 n/aInfant mortality rate (per 1,000 live births) 79 102 122 52 4

Population below poverty line (1990-2001)c 26.3 15.5 72.8 7.1 n/a

a The UN Development Programme’s human development index. b Purchasing power parity. c US$1 per day.

Source: UN Development Programme, Human Development Report, 2004.

There are about 20 different ethnic groups in Senegal, the largest being the Wolof,who account for around 43% of the population. Others include Peuhl (24% of thepopulation), Serere (15%), Diola (5%) and Mandingo (or Malinké, 4%). Lessergroups are the Soninké, Toucouleur, Bassari and Dialonké. Since the countrybecame independent, Wolof language and culture have spread. Wolof is nowspoken by about 70% of the population, although French remains the officiallanguage and is used throughout the country. More than 90% of the populationare Muslim; the remainder practise Catholicism and traditional beliefs.

Education

The primary school enrolment rate stood at 85.1% in 2003, which is below theaverage for Sub-Saharan Africa of 95%, according to estimates from the UNEducational, Scientific and Cultural Organization (UNESCO) and the WorldBank. In one of Senegal’s regions it is below 50%, highlighting the noticeableinequalities in terms of access between regions and between urban and ruralareas. The literacy rate is therefore low, at only 40.2% of the adult population in2003, placing a considerable strain on the development of the country. Onlyaround 4% of those of the appropriate age are in tertiary education, but this isclose to the average for Sub-Saharan Africa. There are two universities inSenegal, Université Cheikh Anta Diop in Dakar and Université Gaston Berger inSt Louis. Despite recent increases in the budget for education—it exceeded 35% ofthe total expenditure in 2004 but is largely used for teachers’ salaries—improvements have been slow, and there have been a number of strikes bystudents and teachers.

A low literacy rate

16 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Health

Until the 1990s the number of doctors relative to the size of the population washigh by Sub-Saharan standards—12,687 per doctor in 1981 according to the WorldBank. However, successive governments made healthcare a low spendingpriority, and the number of people per doctor rose significantly to an average of18,215 in 1990 according to the World Bank, before falling to 13,133 in 1991-2004.Only about 40% of the population has access to health services, and nearlythree-quarters of all healthcare personnel are concentrated in the two largestcities, Dakar and Thiès, leaving the majority rural population poorly covered.Health problems in Senegal are compounded by inadequate nutrition:according to a 2003 report by the UN Development Programme (UNDP), 25% ofSenegalese suffer from chronic malnutrition.

HIV/AIDS profile, 2003Senegal Côte d’Ivoire

People living with HIV/AIDS 44,000 570,000

Children who have lost their mother to HIV/AIDS 17,000 310,000Deaths from HIV/AIDS 3,500 47,000

HIV prevalence rate among adults 15-49 (av; %) 0.8 7.0

Source: UNAIDS.

Hampered by insufficient resources in the past, the government has increasedinvestment in the healthcare system in recent years, in line with itscommitment to reduce poverty. The absence of updated data on death fromdisease or access to medical facilities makes it difficult to accurately assessprogress in recent years. However, increased funding going to the health sectorand increased immunisation against malaria, yellow fever, tetanus, diphtheriaand whooping cough suggest that there should be an improvement in healthoutcomes. The government has had some success with its HIV/AIDSprogramme, which has kept the HIV infection rate significantly lower than inother African countries. According to the joint UN programme for HIV/AIDS(UNAIDS), an estimated 44,000 adults and children were living with HIV/AIDSat the end of 2003, 41,000 being adults (aged between 15 and 49). The adultinfection rate was 0.8%, the lowest of all Sub-Saharan African countries forwhich data are available, and markedly below the infection rate of countriessuch as Botswana (37.2%) and Swaziland (38.8%).

Natural resources and the environment

Most of Senegal lies within the Sahelian zone, an area of irregular and uncertainrainfall and generally poor soil. Rainfall is relatively high and dependable in thesouthern part of the country, but the north has suffered in the past 25 years fromwhat appears to be a considerable climatic shift, making crop and livestockproduction increasingly difficult, even marginal. As elsewhere in the Sahel, morethan 80% of annual rainfall occurs between the beginning of July and the end ofOctober. There are a number of large rivers, including the Senegal, Saloum,Gambia, Soungrougrou and Casamance.

Healthcare is deteriorating

A dry country

Senegal 17

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Senegal has 32% forest cover and an additional 30% of other wooded land.There is a well-developed network of protected areas covering 12% of thecountry’s forested area. The vast majority of Senegal’s forests and woodlandsare open savannah, which extends through the Sudanian-Guinean, Sudanian-Sahelian and Sahelian vegetative zones. Small areas of closed forest occur inthe Casamance region. Mangrove forest blankets much of the southern coast ofthe country, particularly around the Casamance estuary. Desertification is amajor problem in northern Senegal. The country has established significantareas of plantation forest, mainly for non-industrial (fuelwood and fodder)purposes.

Senegal’s main exploited mineral deposits are calcium phosphates in Taïba andaluminium phosphates in Thiès; the opening of the Tobène deposit in 2003increased Taïba’s phosphate production capacity. Total national reserves areestimated at 100m tonnes of calcium phosphate and 60m tonnes ofaluminium phosphate. Other proven mineral reserves include iron, gold,copper, diamonds, titanium and peat, although most are not exploited. Thereare also gas and oil deposits, the extent of which has yet to be established.

Transport, communications and the Internet

Most road and rail links converge on Dakar. The city has the geographicaladvantage of being the westernmost port in Africa, and it is an importantregional and international transit hub. Owing to recent poor competitiveness, ithandled only about 9m tonnes of traffic in 2002, compared with 14.5m tonnesat the port of Abidjan in Côte d’Ivoire. However, following the rise of politicalinstability in Côte d’Ivoire, starting with the December 1999 coup and thefollowing eruption of conflict, some of the trade that had passed through Côted’Ivoire to Burkina Faso, Mali and Niger, switched to some neighbouringcountries. Senegal benefited by seeing a rise in its share of Mali-bound trade,which has been significant since September 2002. However, if peace takes holdin Côte d’Ivoire, most trade is expected to return to Abidjan, which is faster,easier and cheaper than most of the alternatives. The freight that the port canhandle will increase as the port authority, Port autonome de Dakar (PAD), isundertaking an ambitious programme to modernise and expand its facilities,with plans to build a new grain terminal, to increase capacity to handlecontainer ships and, eventually, to enlarge the port.

Senegal has one of the best road networks in West Africa, estimated to total14,500 km. It includes three primary routes: the central highway linking Dakarand Kidira (on the border with Mali); the southern route towards The Gambiaand the Casamance region; and the northern route towards Mauritania andalong the Senegal River valley. However, connections between most regions arepoor. Major road rehabilitation projects are under way, including on the mainroad link between Mali and The Gambia. Most traffic is found in the Dakarregion, or between Dakar and the groundnut-producing areas to the north andeast. Traffic in Dakar is heavily congested. The metropolitan Dakar publictransport company, Société des transports du Cap-Verde (Sotrac), was liquidatedin December 1999, following three abortive attempts to sell it to foreign buyers.

Mineral reserves

Dakar's port

Roads

Forestry

18 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

The government subsequently created a new company, Dakar Dem Dikk(“Dakar round-trip”), with 100% Senegalese ownership. It has been upgradingthe ageing fleet of taxis and buses inherited from Sotrac.

Dakar and the Malian capital, Bamako, are linked by a 1,300-km railway line. In2001 the line carried about 262,600 tonnes of freight, a volume that hasincreased since civil war broke out in Côte d’Ivoire. The railway system alsoruns north to St Louis, the country’s former capital, near the border withMauritania. Problems with the ageing infrastructure have made the rail routesinefficient and slow. In 1998 the World Bank provided assistance withrenovating part of the track in eastern Senegal. Privatisation of Senegal’s portionof the Dakar-Bamako line, originally due to have been completed in 1999, wasdelayed until 2003. After studying offers from two prospective buyers, Senegaland Mali agreed in March 2003 to sell to a Canadian company, Canac-Getma, a25-year concession for CFAfr15.7bn (US$26.7m) to run the Dakar-Bamako line.Canac-Getma pledged to invest CFAfr40bn over five years to buy new rolling-stock and locomotives, upgrade facilities, and carry out other improvements. InAugust 2003 management of the railway was handed over to Transrail, the newcompany established by Canac-Getma. Merchandise traffic has increased by75% since the start of the concession in October 2003, passing from 20,000tonnes per month to 35,000 tonnes per month in 2004, according to Canac-Getma.

The Senegal River is navigable for 220 km throughout the year, and as far asKayes, 924 km inland in western Mali, for part of the year. The Saloum Riverprovides a number of major groundnut-producing centres with a transportroute for their produce. Owing to the re-establishment of a ferry servicebetween Dakar and Ziguinchor in the 1990s, the Casamance River nowprovides an alternative route to overland travel. However, the sinking of apassenger ferry, Le Joola, in September 2002, which claimed 1,860 lives, pointedto the lack of safety in such transport. The ferry was grossly overloaded, whichcontributed to its sinking. Around 1,000 bodies remain trapped in the hull ofthe vessel, which lies on the sea bed off The Gambia. In June 2005 thegovernment hired an Indonesian passenger ferry, MV Wilis, as a replacementfor Le Joola, to ply the Dakar-Ziguinchor route.

Dakar’s Léopold Sédar Senghor international airport (based at Yoff) nowhandles in excess of 1.2m passengers annually and over 30,000 tonnes offreight, an increase over the late 1990s and reaching the level of air traffic atAbidjan airport in Côte d’Ivoire prior to the outbreak of civil war in 2002. Anew airport planned at Ndiass, 50 km from Dakar, should have more thantwice the capacity of the current one. The airport will be a build-operate-transfer (BOT) project, in which the entire cost of construction will be borne bythe private sector, which will recoup its investment by operating the airport onconcession for a period of 22 years, before it is transferred to direct governmentownership. So far there has been limited interest on the part of privateinvestors. Since 1998 St Louis has been connected by charter flight to France. Inaddition, there are 12 secondary airports at major regional centres. Originally asmall domestic carrier, Air Senegal sold 51% of its capital to Royal Air Maroc in

Railways

Air

Rivers

Senegal 19

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

late 1999 and was transformed into Air Senegal International (ASI) in 2001. Thenew airline flies to Europe and to many West African cities. ASI formed apartnership with South African Airways to fly the Johannesburg-Dakar-NewYork route twice a week. ASI’s passenger traffic increased from 125,000 in 2001to 420,000 in 2004. Many international airlines fly to Dakar, including AirFrance, Iberia, TAP Air Portugal, and Alitalia.

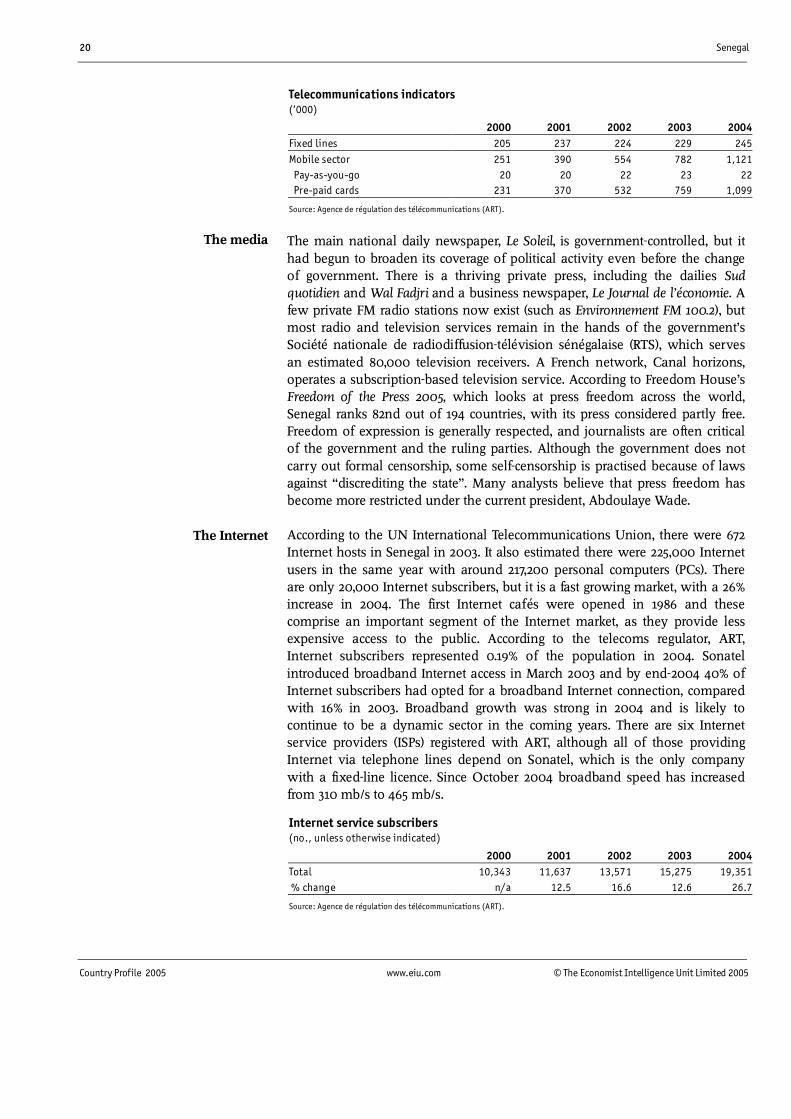

Senegal has an advanced telecommunications sector, with a digital and fibre-optic network nationally and an optic marine and satellite network inter-nationally. As a result of the quality of the network, Dakar has succeeded inattracting a buoyant call-centre industry, which has made Senegal one of thechoice destinations for off-shoring activity for France and Belgium, putting it incompetition with Morocco, Tunisia and Mauritius. The telecoms sectorrepresents about 6% of GDP and 10% of the tertiary sector, and its growth in thelast five years has averaged 18%, according to the telecoms regulator, Agence derégulation des télécommunications (ART). Total investments in the telecomssector are estimated to have exceeded CFAfr50bn (US$94m) in 2004.

In July 1997 the government sold 33% of the state-owned telecoms company,Société nationale de télécommunications (Sonatel), to France Télécom, and sold10% to the enterprise’s employees. A further 18% was sold to the public throughthe regional stock exchange, based in Abidjan. In February 1999 a capitalrestructuring increased France Télécom’s stake to 42%, reducing thegovernment’s share to 30%. A major programme to increase the number offixed lines in Senegal is under way, with a particular emphasis on expandingtelephone coverage in rural areas. According to ART, there were 244,948 fixed-line connections in the country in 2004 (compared with 205,008 in 2000),generating CFAfr175bn (US$329m) in turnover. However, growth in fixed lineshas slowed since 2000—there were 16,100 new lines in 2004, equivalent to a 7%growth rate—the year in which mobile subscribers overtook fixed-lineconnections. About 64% of fixed-lines are in Dakar, and the penetration rate offixed lines is low, at 2.3% in 2004.

Mobile telephony, using the Global System for Mobile Communication (GSM),was launched in the third quarter of 1996. By the end of 2004 the number ofmobile phone users exceeded 1m, having grown by 47.7% in that year. Annualgrowth between 1999 and 2004 averaged 70%, making it one of the mostdynamic sectors of the economy. There are two mobile operators, SonatelMobile (a subsidiary of Sonatel), which was launched in 1996 and controls 70%of the market and Sénégalaise des télécommunications (Sentel), 75%-owned by aLuxembourg-based company, Millicom International Cellular, which obtained alicence in 1998 and was launched in 1999. The mobile telephone market isdominated by pre-paid cards, which account for 98% of the sector.

Telecommunications

20 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Telecommunications indicators(‘000)

2000 2001 2002 2003 2004Fixed lines 205 237 224 229 245Mobile sector 251 390 554 782 1,121 Pay-as-you-go 20 20 22 23 22 Pre-paid cards 231 370 532 759 1,099

Source: Agence de régulation des télécommunications (ART).

The main national daily newspaper, Le Soleil, is government-controlled, but ithad begun to broaden its coverage of political activity even before the changeof government. There is a thriving private press, including the dailies Sudquotidien and Wal Fadjri and a business newspaper, Le Journal de l’économie. Afew private FM radio stations now exist (such as Environnement FM 100.2), butmost radio and television services remain in the hands of the government’sSociété nationale de radiodiffusion-télévision sénégalaise (RTS), which servesan estimated 80,000 television receivers. A French network, Canal horizons,operates a subscription-based television service. According to Freedom House’sFreedom of the Press 2005, which looks at press freedom across the world,Senegal ranks 82nd out of 194 countries, with its press considered partly free.Freedom of expression is generally respected, and journalists are often criticalof the government and the ruling parties. Although the government does notcarry out formal censorship, some self-censorship is practised because of lawsagainst “discrediting the state”. Many analysts believe that press freedom hasbecome more restricted under the current president, Abdoulaye Wade.

According to the UN International Telecommunications Union, there were 672Internet hosts in Senegal in 2003. It also estimated there were 225,000 Internetusers in the same year with around 217,200 personal computers (PCs). Thereare only 20,000 Internet subscribers, but it is a fast growing market, with a 26%increase in 2004. The first Internet cafés were opened in 1986 and thesecomprise an important segment of the Internet market, as they provide lessexpensive access to the public. According to the telecoms regulator, ART,Internet subscribers represented 0.19% of the population in 2004. Sonatelintroduced broadband Internet access in March 2003 and by end-2004 40% ofInternet subscribers had opted for a broadband Internet connection, comparedwith 16% in 2003. Broadband growth was strong in 2004 and is likely tocontinue to be a dynamic sector in the coming years. There are six Internetservice providers (ISPs) registered with ART, although all of those providingInternet via telephone lines depend on Sonatel, which is the only companywith a fixed-line licence. Since October 2004 broadband speed has increasedfrom 310 mb/s to 465 mb/s.

Internet service subscribers(no., unless otherwise indicated)

2000 2001 2002 2003 2004Total 10,343 11,637 13,571 15,275 19,351 % change n/a 12.5 16.6 12.6 26.7

Source: Agence de régulation des télécommunications (ART).

The Internet

The media

Senegal 21

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Energy provision

More than one-half of Senegal’s energy consumption comes from traditionalsources such as wood and charcoal, and this has led to serious deforestationover the years. Although the country’s industrial sector has to import most ofits energy requirements, natural gas is now being extracted from the Gadiagafield, south of the capital, Dakar.

Nearly all of the country’s electricity supply is generated thermally. Although 35%of Senegalese are connected to the national power grid, the proportion falls tojust 9% in rural areas. The national electricity company, Société nationalesénégalaise d’électricité (Senelec), has a production capacity of 415 mw andanother 90 mw is made available from the Manantali hydroelectric dam in Mali.Two diesel generators at the Cap des Biches, a private power station, wasbrought on stream in June 2003, producing 850 gwh. There is a small naturalgasfield at Diam-Niade Kabor (see below), which provides up to 20% of Senelec’sneeds. Senelec has embarked on a large investment programme, valued atCFAfr77bn (US$145m) to increase both its generation and distribution capacity.In April 2005 the government signed an agreement to buy electricity for 15years generated by Kounoune Power, a joint venture between Matelec, aLebanese company, and Mitsubishi (Japan), which will generate 67.5 mw.

In 1999 a consortium led by Hydro-Québec of Canada purchased a 34% shareof Senelec and took over its management. The agreement was abrogated inSeptember 2000, however, because the government was dissatisfied with thedelay in starting rehabilitation work and the failure to end frequent,economically damaging power cuts. Negotiations resumed in 2001 to sell amajor share of Senelec to either Vivendi of France or AES of the US. In acontext of market uncertainty and financing difficulties for the energy sectorglobally, the talks broke down, prompting the Senegalese government in July2002 to suspend Senelec’s privatisation for the time being. Since then it hasasked the World Bank to participate in a task force to examine alternative policyoptions for Senelec. The IMF, which had consistently advised that Senelec beliberalised, agreed that the government could delay privatisation for anunspecified time, provided that it carried out further reform in the electricitysector, including allowing private operators to establish new power stations.

Under a scheme administered by the Senegal River Development Organisation(Organisation pour la mise en valeur du fleuve Sénégal—OMVS), theManantali dam—on the Bafing River in Mali, a tributary of the Senegal River—provides electricity via a 1,300-km network of transmission lines to thecapitals of the OMVS member countries, Bamako (Mali), Nouakchott(Mauritania) and Dakar (Senegal), with about 90 mw supplied to Senegal. TheUS$600m project was to have begun generating electricity by 1998, buttechnical and political hitches delayed the installation of generators. Theconnection with Senegal’s grid was finally completed in July 2002, although itsinitial capacity was only 18 mw.

Thermal generation dominates

Traditional energy sources

Manantali hydroelectricstation is finally commissioned

22 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

A state-owned enterprise, Société des pétroles du Sénégal (Petrosen), wasestablished in 1981 to search for oil and to participate in external oil firms’exploration efforts. Following a call for bids in early 1990, a number ofexploration blocks in offshore waters near the Guinea-Bissau border have beenawarded. Relatively large discoveries recently made in neighbouring Mauritaniahave raised some hope that oil deposits may be found in the north of Senegal.The country’s natural gas reserves, which are estimated to be 3bn cu metres, arelocated primarily onshore. In 1999 natural gas was produced by Tullow Oil ofIreland in association with Petrosen, from the Diam-Niade Kabor field. InOctober 2002 a US independent, Fortesa, began natural gas production fromthe Gadiaga development. The Gadiaga field is currently producing around 2mcu ft/day of gas. Fortesa is also planning to carry out additional seismic work inthe area. Fortesa has a 70% share in the Gadiaga Development Area, with theremaining 30% held by Petrosen.

Oil exploration activities conducted by Benton Oil and Gas of the US in theDome Flore field continued until October 1999. The field, which was locatedoffshore southern Senegal near the border with Guinea-Bissau, had been thesubject of a boundary dispute between the two countries since the 1950s. In1995 the dispute was settled, and joint exploitation was permitted by theratification of a treaty, in which 85% of the proceeds from the activities in thearea went to Senegal and 15% went to Guinea-Bissau and the Agence deGestion et de Coopération (AGC), which was an agency created for the jointdevelopment of maritime resources in the area, was established. The field’sheavy crude reserves have been estimated to be 700m barrels (according to theUS Energy Information Administration). Among the areas covered by the jointadministration are Cheval Marin and Croix du Sud. Cheval Marin—covering anarea of approximately 6,300 sq km and extending from water depths of lessthan 75 metres to over 3,500 metres—is operated by the Italian state oilcompany, Agip. Croix du Sud, which covers an area of about 3,550 sq km andextends from water depths of less than 50 metres to over 3,550 metres, isoperated by a UK company, Sterling Energy, and the AGC. The operators arecarrying out seismic surveys.

Other firms involved in offshore exploration were Roc Oil of Australia andVanco International of the US. In October 1999 Roc Oil signed a production-sharing agreement (PSA) with Petrosen for exclusive rights to exploreCasamance offshore blocks 1, 2, and 3. The blocks are located off southernSenegal and cover a total area of 8,187 sq km. Roc Oil held a 92.5% interest inthe project, and Petrosen held 7.5%. Roc Oil, in joint venture with WoodsideEnergy (also of Australia), studied several blocks onshore and offshore andsigned a memorandum of understanding with Petrosen that proposed a workprogramme to justify the granting of prospecting rights, which would also givethem the right of first refusal to negotiate PSAs. It is understood that theagreement has lapsed.

Also in October 1999, Vanco signed a PSA with the government for the DakarOffshore Profond Permit, a deepwater block that extended from Senegal’soffshore boundary with The Gambia to its border with Mauritania. Covering7.9m acres, the Profond block is the largest concession to date offshore Senegal.

Oil and natural gas prospects

Exploration activity continues

Senegal 23

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Vanco was the operator of the concession, holding a 90% interest; theremaining 10% was held by Petrosen. In 2001 Vanco explored the south area ofthe block, identifying the Palmarin prospect. The 2D survey showed that thePalmarin prospect may be oil bearing and it was hoped that an exploratorywell could be drilled by the end of 2003. However, so far no well has been dug.

In December 2005 Al Thani Investments, which is owned by the first cousin ofthe president of the United Arab Emirates, was awarded a licence on the Cayarblock in Senegal’s shallow offshore area. Al Thani signed a contract withPetrosen, to invest CFAfr22bn (US$42m) over a period of eight years. The twoparties also agreed on an exploitation concession for a minimum of 25 years ifoil or gas is discovered. The Cayar block is considered a promising one given itsclose proximity to areas which abound in oil and gas. On December 17th,Kampac Oil, a Dubai-based oil group, signed a concession agreement forexploration and production sharing covering the Louga onshore bloc innorthern Senegal. The agreement stipulated minimum investments ofCFAfr20bn over a period of seven years. If oil is discovered, Kampac will havean exploitation concession for at least 25 years.

SENEGAL

MAURITANIA

MALI

THE GAMBIA

GUINEA-BISSAU

St-LOUISDEEP

St-LOUIS LOUGA

DIOURBELTHIES

MBOUR

SALOUM

SENEGAL SUDONSHORE

SENEGAL EAST

CAYARDEEP

RUFISQUEDEEP

SANGOMARDEEP

SENEGAL SUD SENEGAL SUD

OFFSHORE OFFSHORE

DEEP

AGC Area

SHALLOWDomeFlore

SANGOMAR

RUFISQUE

CAYAR

0 km 50 100 150 200

0 miles 50 100Source: Petrosen.

DAKAR

Senegal: oil and gas exploration blocks

24 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

The economy

Economic structureMain economic indicators, 2004Real GDP growth (%) 6.1Consumer price inflation (av; %) 0.5Current-account balance (US$ m) -742

Total external debt (US$ m)a 4,418Exchange rate (av; CFAfr:US$) 528.3

Population (m) 11.4

a 2003.

Source: Economist Intelligence Unit.

Dakar’s position as the capital of former French West Africa made Senegal oneof the most developed states in the region at independence, with a well-developed physical and social infrastructure and a relatively well-diversifiedindustrial base. In addition to having a stronger tourist sector than otherfrancophone West African countries, Senegal has remained an important hubof economic activity in the region, and the services sector is the maincontributor to GDP, accounting for 64% in 2003. Although the primary sectoraccounts for less than 20% of GDP, it remains the bedrock of the economy,supporting more than 70% of the economically active population. Groundnuts,cotton and horticulture are the main cash crops, but agricultural output is proneto changes in weather patterns. Since the mid-1980s the fish sector has emergedas Senegal’s main export earner. The industrial sector, which accounts for about20% of GDP, encompasses a variety of economic activities, but is heavilydependent on agro-industries and mining, notably phosphates and theproduction of derived chemicals (the second-largest source of export earnings).

For a long time Senegal was in the World Bank’s lower-middle income bracket,although this changed with the devaluation of the CFA franc in 1994. In 2001Senegal was formally classified by the UN as one of the world’s 49 “leastdeveloped countries” (LDCs), based on its low GDP per head, weak humanresource base and low level of economic diversification.

Comparative economic indicators, 2004a

Senegal MaliCôte

d’IvoireSouthAfrica Franceb

GDP (US$ bn) 13.1 5.1 14.7 213.2 2,047GDP growth (%) 6.1 2.2 -1.0 3.7 2.1

GDP per head (US$) 1,252 381 871 4,990 33,890Consumer price inflation (av; %)b 0.5b -3.1b 1.4b 4.3b 2.1Population (m) 11.4 13.4 16.9 42.7 60.4

Exports of goods fob (US$ bn) 1.3 1.1 6.5 48.4 425.0Imports of goods fob (US$ bn) 2.3 1.1 4.7 48.5 443.0

Current-account balance (US$ bn) -0.7 -0.2 -0.2 -7.0 -5.0

a Economist Intelligence Unit estimates. b Actual.

Source: Economist Intelligence Unit.

A sizeable economy

Senegal 25

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Economic policy

In the first two decades after independence the government professedallegiance to “African socialism”, which in practice translated into heavy stateintervention and an inward-looking economic strategy. Whereas the number ofpublic enterprises expanded, and expansionary monetary and fiscal policieswere pursued, private-sector activity was strongly regulated, and price andtrade controls spread first to agriculture and then gradually to all sectors of theeconomy. By the mid-1980s the continued deterioration of the terms of trade,induced by the overvaluation of the CFA franc and a series of droughts led tomounting fiscal deficits, highlighting the extent to which the public sector hadexpanded and the uneconomic nature of much past public-sector investment.

In 1979 the government embarked on a series of adjustment programmessupported by the IMF and the World Bank (Senegal was one of the first Africancountries to do so), but the results were mixed. Economic growth recovered,and the adjustment programmes saw the closure or privatisation of somepublic enterprises, markedly less state intervention in agriculture and cuts inthe civil service. However, the government failed to tackle deep-seatedproblems, which inhibited the diversification of the economy and the rise of adynamic private sector. Failure to trim expenditure, combined with theappreciation of the CFA franc, led to the accumulation by the government oflarge levels of debt. In the early 1990s the rate of economic growth becameerratic and low, and Senegal, in line with other members of the Franc Zone,agreed reluctantly to a 50% devaluation of the CFA franc in January 1994.

As part of the government’s efforts to reform economic policy and theeconomy, a three-year SDR130.8m (US$187.3m) enhanced structural adjustmentfacility (ESAF) was agreed with the IMF in 1994. The main challenge facing thegovernment was keeping firm control over public-sector pay. The policyconditions attached to the ESAF focused on: liberalising labour legislation,prices and external trade; agricultural reform and the stimulation of marketmechanisms; and the restructuring of the public sector, including a round ofprivatisations. A new ESAF (later renamed the poverty reduction and growthfacility, PRGF) worth US$144m, was signed with the IMF in April 1998, and itsinitial three-year duration was subsequently extended for another year, untilmid-April 2002. Under the PRGF, the government agreed with the IMF to aseries of economic targets. These included real GDP growth of 5-6% a year,inflation below 3%, and a current-account deficit (excluding official transfers)equivalent to less than 7% of GDP—all linked to implementing a programme ofagreed economic and financial reforms.

Monetary and exchange-rate policy

The central feature of Senegal’s economic policy is the pegged exchange-rate regimewhereby the CFA franc is pegged to the euro at CFAfr656:€1. This supports monetarypolicy, as determined by the regional central bank, Banque centrale des Etats del’Afrique de l’ouest (BCEAO). Accordingly, the BCEAO pursues a tight monetarypolicy similar to that of the European Central Bank (ECB). Owing to this lack ofmonetary independence, government and donors rely on fiscal policy as the main

Initial allegiance to socialism

Reforms fail to tackle problems

Renewed commitmentto reform

26 Senegal

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

instrument to achieve financial stabilisation. The BCEAO, based in Dakar, alsodictates the monetary policy in the rest of the Union économique et monétaireouest-africaine (UEMOA; see Regional overview: Membership of organisations). TheBCEAO’s main objective is to maintain the parity between the CFA franc and theeuro by using a mix of indirect and direct monetary instruments. An importantchange in regional monetary policy took place in 2002, when governmentborrowing from the BCEAO was banned and replaced by the use of Treasury bills.Advances by the BCEAO to governments have been frozen since 1998.

The president, Abdoulaye Wade, and his party, the Parti démocratiquesénégalais (PDS), generally refer to themselves as “liberal” in economic matters,although there was little change in policy following Mr Wade’s victory in the2000 presidential election, as the outgoing government had already abandonedits orientation towards state intervention. Economic reforms have concentratedon four main areas: fiscal policy, structural reforms, poverty alleviation andpromotion of the private sector.

• Fiscal consolidation and transparency: Fiscal policy remains a pivotalinstrument because Senegal’s monetary and exchange-rate policy is dictated bythe regional central bank, the Banque centrale des États de l’Afrique de l’ouest(BCEAO). The government remains committed to containing budgetaryexpenditure, strengthening revenue from domestic sources and improving taxefficiency, as well as to meeting the convergence criteria set by the regionalgrouping, the Union économique et monétaire ouest-africaine (UEMOA).

• Privatisation: The new government adopted a distinctly nationalist stanceon privatisation policy, actively seeking more openings for Senegalese investorsand taking a tougher line with foreign buyers who did not appear to be livingup to their commitments. Although the sale of the electricity parastatal, Senelec,has been delayed because of a lack of interested buyers, the IMF has advisedthat the firm should become more commercially focused, to ready itself forsome form of sale when the time is right. The sale of a majority stake in theSociété nationale de commercialisation des oléagineux du Sénégal (Sonacos),the groundnut parastatal, finally took place in December 2004.

• Poverty reduction: The poverty reduction strategy paper (PRSP; publishedon November 20th 2002) sets out the policies and strategies to tackle poverty inthe government’s anti-poverty framework. Although it is probably morecommitted than its predecessor to the promotion of the private sector, the Wadegovernment has repeatedly emphasised the importance of addressing socialconcerns such as health, education and unemployment. Mr Wade himself hasadvocated a decidedly Keynesian approach, the state having been assigned amajor role in developing Senegal’s infrastructure and in educating and trainingits workforce to compete better in global markets.

• Investment: The government has launched a series of initiatives tofacilitate and encourage private investment, both domestic and foreign. AStandard & Poor’s credit rating was commissioned, and the country wasawarded an encouraging “B+/B” in December 2000. In March 2003 Standard &Poor’s reaffirmed its B+/B issuer credit ratings. A national agency, Agencenationale pour la promotion des investissements (Apix), was established to act

Mr Wade's approachis cautious

Senegal 27

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

as a strategic advocate for foreign investors and, in particular, to facilitateadministrative procedures. The government expects some of the bigger worksprojects, such as a new international airport, expansion of the road network andport development, to be financed privately. This is especially important giventhe IMF’s warning, in its 2003 PRGF review, that the government should notundertake any “showcase projects” that could drain public finances. The IMFhas also raised doubts that the tax concessions and other investor inducementsoffered by Apix might be counter-productive.