seminario permanente de las ideas: economía, población y desarrollo

DESCRIPTION

SEMINARIO PERMANENTE DE LAS IDEAS: Economía, Población y Desarrollo. Cuerpo Académico Número 41 www.estudiosregionales.mx. 1. Public Finance and Monetary Policies as Economic Stabilizer: Unique or Universal Across Countries? DRA. ARWIPHAWEE SRITHONGRUNG Public Finance Center; - PowerPoint PPT PresentationTRANSCRIPT

1

SEMINARIO PERMANENTE DE LAS IDEAS:Economía, Población y Desarrollo

Cuerpo Académico Número 41www.estudiosregionales.mx

1

Public Finance and Monetary Policies as Economic Stabilizer: Unique or Universal Across Countries? DRA. ARWIPHAWEE SRITHONGRUNG

Public Finance Center;

Wichita State University,

Ciudad Juárez, Octubre 13 2014

2

OUTLINE

Introduction Theoretical background Methodology and data Results Discussion Conclusion

3

INTRODUCTION Motivation of the study

Does monetary policy work better than fiscal policy in developing countries?

Lack of systematic test for stabilization policy in developing countries

Non-industrialized countries Low-to medium-income levels;

Research question In what circumstances is monetary policy effective in

stabilizing an economy and in what circumstances is fiscal policy a better tool to do the same?

Theoretical arguments Asymmetric information in capital markets Stabilizing economy at the least social cost

4

THEORETICAL BACKGROUND (1) Musgrave, R. (1959): public finance functions

and roles Correct market failures

Public infrastructure Public programs Tax revenue, public budgeting, government consumption

and investment Redistribute resources from rich to poor

Social programs Income tax structure Current transfer payment

Stabilize macro-economy Fiscal policy: tax, spending and deficit finance Monetary policy: central bank interest rate

5

THEORETICAL BACKGROUND (2) Basic roles of fiscal and monetary policies

Mundell-Fleming’s (1963) IS/LM Model Sticky prices in short run Fiscal and monetary policies to change output levels

Interest rate: directly change investment and consumption level

Public spending, taxes and deficit finance: indirectly change investment and consumption by re-shuffling resources

Open economy with fixed exchange rates Fiscal policy: deficit finance and tax cut

investment/consumption change interest rate foreign investment change

Open economy with floating exchange rates Monetary policy: interest rate foreign investment - domestic

currency demands/supply export level 6

THEORETICAL BACKGROUND (3) Relax IS/LM Model by adding public debt

accumulation Two contrasting views: finite and infinite-horizon Finite-horizon assumption

Beetsma & Bovenberg, 1995; Durham, 2006; Shabert, 2004; Piergallini; 2005; Bartolomeo & Gioacchino, 2008

Fiscal policy: both fixed and floating exchange rates Economic agents:

---anticipate central bank’s inflation strategies ---assume life-cycle cost; debt is postponed to the next

generations Government liabilities affect aggregate demand and thus

generate wealth Unintentional effect of monetary policy

---agents guess central bank strategy ---cut employment and inputs without necessary reasons

Counter-cyclical fiscal policy 7

THEORETICAL BACKGROUND (4) Infinite-horizon assumption

Kirsanova, Stehn, Vines, 2005; Clarida, Gali & Gertler, 1999; Romer & Romer, 1996; Stehn & Vines, 2007

Monetary policy: both fixed and floating exchange rates Economic agents

--expect inflation and recession in the future --do not pass debt service burden to future generation --do not react to tax and government spending

Taylor rule: set nominal interest rate to target real inflation and recession

--bad times: decrease nominal interest rates for several periods, followed by deficit finance

--good times: increase nominal interest rates for several periods; followed by tax increase

Unintentional effects of fiscal policies --tax increase/surplus in early inflation period- dampens

investment; agents expect future recessions --deficit finance in early recession coupled with high debt

accumulation -- higher interest rates- force public spending cut negative impacts on employment and low-wage workers

8

THEORETICAL BACKGROUND (5)

Typically high-income Complete capital

markets—controllable cash inflows

Relatively high human development index

Relatively high institutional quality

Relatively lower fiscal burden

Mankiw, Wienzierl, Blanchard, Eggertsson, 2011; Christiano, Eichenbaum & Robelo, 2009

Relatively high public debts

Relatively low government accountability

Relatively low government credibility

Incomplete trading system, opaque national account, high level of government deficits

Imcomplete capital markets

Hasan & Isgut, 2009; Fielding, 2008; El-Shagi, 2012

OECD Countries Non-OECD Countries

9

THEORETICAL BACKGROUND (6) Fiscal and monetary policies economic growth Warren Smith (1957)

Structurally balanced economy: Full employment and production is achieved in current year In the following year, tax burden must be less than investment The ratio of private investment to GDP is greater than the ratio of

government revenue to total national income Resource allocation between public and private sectors

is optimal Business cycles create random shocks but do not

interrupt long-term growth Rarely occurs; private investment depends on

Current-year investment level and profits Profit tax Government consumption

Current year investment over optimal level- inflation Current year investment under optimal level --

recession

10

THEORETICAL BACKGROUND (7) Fiscal and monetary policies economic growth David Smith (1960),

Relaxes closed-economy assumption : In addition to domestic investment and consumption Balanced payment in national account due to a country’s levels of

export, import and disposable income Open economy allows for spillover effects

Maintaining balance of payments is key Direct policy tools, e.g., tariff taxes, import controls,

periodic exchange rate devaluation can control balance of payments

Monetary policy enhances growth Indirectly changes investment levels especially when faced with

foreign growth Fiscal policy enhances growth

Tax increases discourage consumption Cautions: in situations with incomplete capital markets

and fixed tax systems fiscal policy is more effective

11

THEORETICAL BACKGROUND (8)

Hypothesis 1: In OECD countries, fiscal policy through deficit finance and public spending is ineffective [due to economic agents’ anticipation; while monetary policy is effective because interest rates provide incentives for private investment]

12

THEORETICAL BACKGROUND (9) Capital markets / institutional quality of

government (El-Shagi, 2012) Intensity of cash inflow control Quality and intention of capital market regulation

Western/industrialized or high-income countries Capital markets designed to limit exposure to foreign risks Capital market transparency Inflow and outflow levels are compatible

Non-industrialized or medium-to low-income countries

Capital markets designed to enhance local cash supplies Capital market rules and regulation is arbitrary Transaction approvals are opaque

13

THEORETICAL BACKGROUND (10) Quality of government and ability to monetize

(Fielding, 2008; Calvo, Leiderman, Reinhart, 1996; Kaminsky, Rinehart & Vegh, 2004) Western/industrialized or high-income countries

Capital inflows rising Create domestic currency demands Foreign investments increase; generating long term growth

Non-industrialized or medium-to low-income countries

Capital inflows rising Create inflation pressure Domestic currency appreciates; dampening export

Consequences for non-industrialized and medium to low-income economies Low domestic currency demands, national saving -- inelastic

rate Public debt fails to absorb inflation, unless set extraordinary

high

14

THEORETICAL BACKGROUND (11)

Summary for monetary policy

Mankiw, Wienzierl, Blanchard, Eggertsson, 2011 monetary policy: counter-cyclical; interest rate is an effective tool to mitigate inflation

and recession Kaninsky, Rienhart & Vegh, 2004

fiscal policy tends to be cyclical coupled with the incomplete capital market problems

Easterly and Schmidt-Hebbel (1993) in developing countries, good financial management

through well-planned taxing and spending leads to growth

15

THEORETICAL BACKGROUND (12)

Hypothesis 2: In non-OECD countries, fiscal policy through public spending is effective in stabilizing economies, while monetary policy is ineffective [since current account balance does not readily adjust to reflect true levels of capital inflows]

16

METHODOLOGY AND DATA (1)

Fischer (1993):

where;

is per capita real Gross Domestic Product (GDP),

is inflation rate,

b is balance account payment,

is government spending rate,

is interest rate and

is capital accumulation rate

17

METHODOLOGY AND DATA (2)

Panel Vector Autoregression (PVAR) Endogenous system of equations Reproducing Fischer’s system

Addresses endogeneity Needs appropriate lag length to reduce errors to

white noise

18

METHODOLOGY AND DATA (3)

Sample Countries

19

OECD Member Countries (19) Non-OECD Member Country

(17)

Belgium, Canada, Denmark,

Finland, France, Greece,

Iceland, Ireland, Italy, Japan,

Netherlands, New Zealand,

Norway, Portugal, Spain,

Sweden, Switzerland, United

Kingdom, United States

Algeria, Barbados, Fiji, Hong Kong,

Jordan, Kuwait, Mauritius,

Pakistan, Paraguay, Peru,

Philippines, South Africa, Sri

Lanka, Thailand, Trinidad &

Tobacco, Uruguay, Venezuela

METHODOLOGY AND DATA (3) Summary Statistics: OECD Countries (with high

income)

20

Variables Mean

Standard Deviation

Minimum Maximum

Current Account Balance (% to GDP) ( ) -0.3 5.2 -28.4 16.5Gross Fixed Capital Formation rate (% to GDP) () 21.3 3.5 12.0 34.5

Per Capital Real GDP (Constant $ value) ( )

27,814

7,579

10,806

51,792 Government Spending Rate (% to GDP) ( ) 7.1 1.6 3.0 11.3Central Bank Discount Rate ( ) 7.5 6.0 0.0 49.0

Annual Change Central Bank Discount Rate ( -0.3 2.7 -25.0 28.0

Annual Change Per Capita Real GDP ( 429 846 -5609 4308Annual Change Government Spending Rate (% to GDP) ( 0.0 0.3 -1.4 1.8Annual Change Gross fixed capital Formation rate (% to GDP) ( -0.2 1.4 -10.5 6.2Annual Change Current Account Balance (% to GDP) ( 0.1 2.2 -12.6 16.8

METHODOLOGY AND DATA (3) Summary Statistics-Non-OECD Countries (with medium-

to low-income

21

Variables Mean

Standard Deviation

Minimum

Maximum

Current Account Balance (% to GDP) ( ) 0.41 14.35 -242.19 54.57

Gross Fixed Capital Formation rate (% to GDP) () 21.7 5.81 9.5 43.2

Per Capita Real GDP (Constant $ value) ( ) 9,617 10,382 1,170 52,502

Government Spending Rate (% to GDP) ( ) 7.76 3.45 2.82 29.40

Central Bank Discount Rate ( ) 21.96 61.03 0.00 866.00

Annual Change Central Bank Discount Rate ( -0.17 47.60 -576.00 718.00

Annual Change Per Capita Real GDP ( 158 1,172 -10,315 9,690Annual Change Government Spending Rate (% to GDP) ( -0.01 1.20 -11.15 11.62

Annual Change Gross fixed capital Formation rate (% to GDP) ( -0.17 3.27 -19.40 21.30

Annual Change Current Account Balance (% to GDP) ( 0.06 16.70 -262.53 239.92

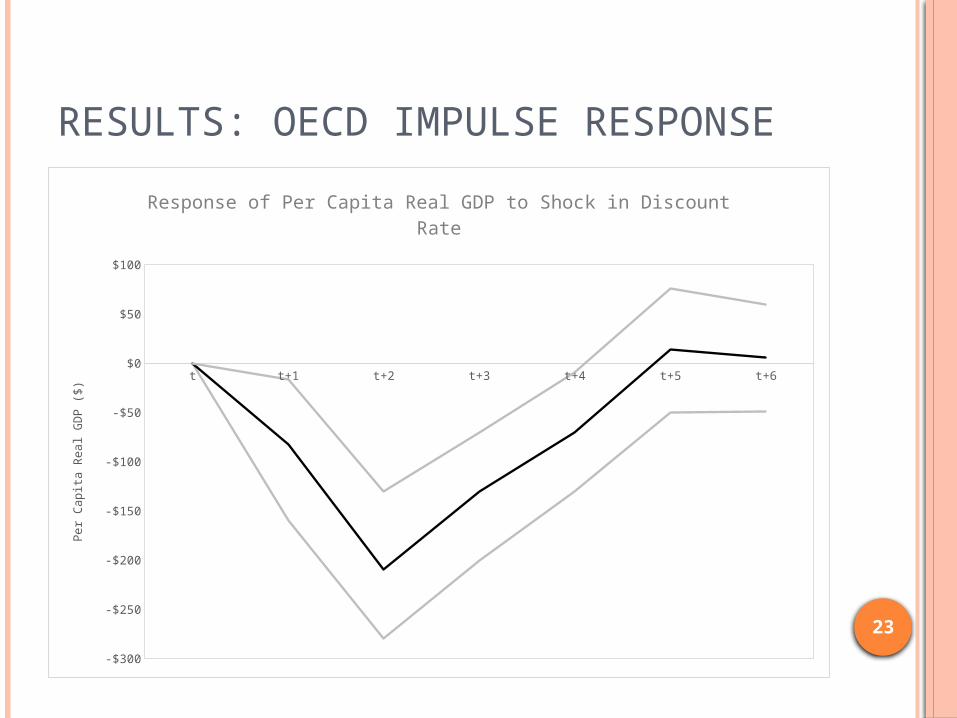

RESULTS: OECD GROUP

Variable Per Capita GDP Response Size

Year t

Year t+1

Year t+2

Year t+3

Year t+4

Year t+5

Year t+6

Cumulative Effect Across

Time

Lower Bound (95% CI) 665.4 326.4 10.5 13.4 9.6 -38.3 -32.4 $ 1,025

($846)

Point Estimate 706.6 394.8 106.8 142.2 108.4 65.9 50.6 $ 1,459

Upper Bound (95% CI) 746.6 469.7 218.1 259.8 215.4 175.7 149.7 $ 1,910

Lower Bound (95% CI) 0 -160 -280 -200 -130 -49.7 -49.5 $ (770)

(2.7%)

Point Estimate 0 -82.8 -210 -130 -70.8 13.8 5.3 $(494)

Upper Bound (95% CI) 0 -16.2 -130 -70.3 -9.7 76.3 59.1 $(226)

Lower Bound (95% CI) 0 -47.7 -18.8 17 -25.4 -21.9 -48.8 $0

(.3%) Point Estimate 0 4.3 41 84.3 45.9 31.4 9.3 $0

Upper Bound (95% CI) 0 54.8 102.1 151.3 111.2 91 66.3 $0

Lower Bound (95% CI) 0 -32.3 -160 -260 -220 -170 -120 $0

(1.4%) Point Estimate 0 58.9 -64.3 -160 -130 -110 -50.4 $0

Upper Bound (95% CI) 0 163.5 19.2 -45.4 -45.7 -36.8 11.6 $0

Lower Bound (95% CI) 0 -210 -120 -58.2 -120 -92.2 -83.5 $0

(2.2%) Point Estimate 0 -150 -38.5 56.1 -28.7 -7 -17 $0

Upper Bound (95% CI) 0 -85.5 56.5 145.4 48.1 61.3 42.1 $0

22

RESULTS: OECD IMPULSE RESPONSE

23

t t+1 t+2 t+3 t+4 t+5 t+6

-$300

-$250

-$200

-$150

-$100

-$50

$0

$50

$100

Response of Per Capita Real GDP to Shock in Discount Rate

Per

Cap

ita R

eal G

DP (

$)

RESULTS: OECD IMPULSE RESPONSE

24

t t+1 t+2 t+3 t+4 t+5 t+6

-$100

-$50

$0

$50

$100

$150

$200

Response of Per Capita Real GDP to Shock in Government Spending

Per

Cap

ita R

eal G

DP (

$)

RESULTS: NON-OECD GROUP

Variable Per Capita GDP Response Size

Year t

Year t+1 Year t+2 Year t+3 Year t+4 Year t+5 Year t+6

Cumulative Effect Across Time

Lower Bound (95% CI)

901 -36.9 172.7 -190 21.3 -74.2 -37.3 $ 1,095

($1,172)

Point Estimate 962.4 209.8 292.8 -9.9 176.5 56.8 44.8 $ 1,432

Upper Bound (95% CI)

1000 439.2 481.2 168.1 341.7 204.6 202.1 $ 1,823

Lower Bound (95% CI)

0 -41.9 -23.6 -77.4 -6 -63.3 -15.8 $ 0

(48%) Point Estimate 0 -4.5 31 -23.1 38.4 -19 18 $ 0

Upper Bound (95% CI)

0 35.7 82.2 25.6 93.8 11.6 48.7 $ 0

Lower Bound (95% CI)

0 207.7 87 15.3 5.5 6.4 3 $ 325

(1.2%) Point Estimate 0 348.3 256.1 141.4 99.3 98.6 82.4 $ 1,026

Upper Bound (95% CI)

0 507.6 453.9 367.6 267.2 269.9 240.7 $ 2,107

Lower Bound (95% CI)

0 -150 -61.9 -390 -88.8 -140 -43.3 $(390)

(3.3%) Point Estimate 0 -10.6 41.4 -230 -27.6 -50.1 8.5 $ (230)

Upper Bound (95% CI)

0 134.3 145.6 -55.3 50.8 13.8 70.5 $ (55)

Lower Bound (95% CI)

0 -200 2 -92.3 -74.4 -62.4 -16.1 $(198)

(16.7%) Point Estimate 0 -110 124.3 -24 -11.3 -13.2 20.6 $ 14

Upper Bound (95% CI)

0 -23.8 249 45.9 42.2 37.9 72 $ 225

25

RESULTS: NON-OECD IMPULSE RESPONSE

26t t+1 t+2 t+3 t+4 t+5 t+6

$0

$100

$200

$300

$400

$500

$600

Response of Per Capita Real GDP to Shock in Government Spending

Per

Cap

ita R

eal G

DP (

$)

RESULTS: NON-OECD IMPULSE RESPONSE

27

t t+1 t+2 t+3 t+4 t+5 t+6

-$100

-$50

$0

$50

$100

$150

Response of Per Capita Real GDP to Shock in Discount Rate

Per

Cap

ita R

eal G

DP (

$)

DISCUSSION (1)

OECD Countries Central bank discount rate negatively related to economic

growth

For every one standard deviation shock decrease (2.7%), real per capita GDP increases by about $495 (one standard deviation PC GDP = $846)

The monetary policy effect is persistent across 4-year period

No effect for monetary policy for the year in which the policy is introduced

No significant effect of fiscal policy 28

DISCUSSION (2) Non-OECD Countries

Government spending is positively related to economic growth

For every one standard deviation of government spending increase (1.2%), real per capita GDP increases by about $1,026 ( one standard deviation GDP = $1,172)

The fiscal policy effect on output is persistent across 6-year period

No effect of fiscal policy in the same year as the policy is introduced

Monetary policy is not statistically significant 29

CONCLUSION Three viewpoints

Currency exchange system Finite-horizon assumption/Infinite-horizon assumption Capital market and institutional quality/openness and

foreign growth and declines

Theoretical contribution To choose economic policy, it’s not only about economic

agents’ response and exchange rate systems,…………… but also quality/intention of capital market regulation

Practical contribution For developing, fiscal policy stabilizes output while shifting

wealth among sectors

Limitation The model lacks exogenous variables Fails to explain the path in which fiscal policy stabilizes

output30

31

SEMINARIO PERMANENTE DE LAS IDEAS:Economía, Población y Desarrollo

Cuerpo Académico Número 41www.estudiosregionales.mx

31