seminar on reinsurance philadelphia, pa june 3, 2003 casualty actuarial society a shps company

TRANSCRIPT

Seminar on Reinsurance

Philadelphia, PAJune 3, 2003

Casualty Actuarial Society

A SHPS Company

David OlshoFSA, MAAA

Specialty Lines:Accident & Health

A SHPS Company

3

A SHPS Company

1

3

Today’s Agenda

1. Health Care Update

2. Medical Stop Loss Marketplace

3. Consumer Directed Health Plans

4. Predictive Modeling

5. Disease Management

6. SARS

7. Society of Actuaries Large Claim Study

8. Questions

4

A SHPS Company

1

4

Health Care Update

5

A SHPS Company

1

5

0

5

10

15

20

25

Year

Perc

ent o

f GD

P

National Health Expenditures as a Percentage of GDP

* Projection** 16 Year AverageSource: Bureau of Economic Analysis, Office of the Actuary

National Health Expenditures

National Defense Expenditures**

6

A SHPS Company

1

6

-3.00%

0.00%

3.00%

6.00%

9.00%

12.00%

15.00%

18.00%

1987 1989 1991 1993 1995 1997 1999 2001 2003

% Change Health Cost % Profit Health Plans

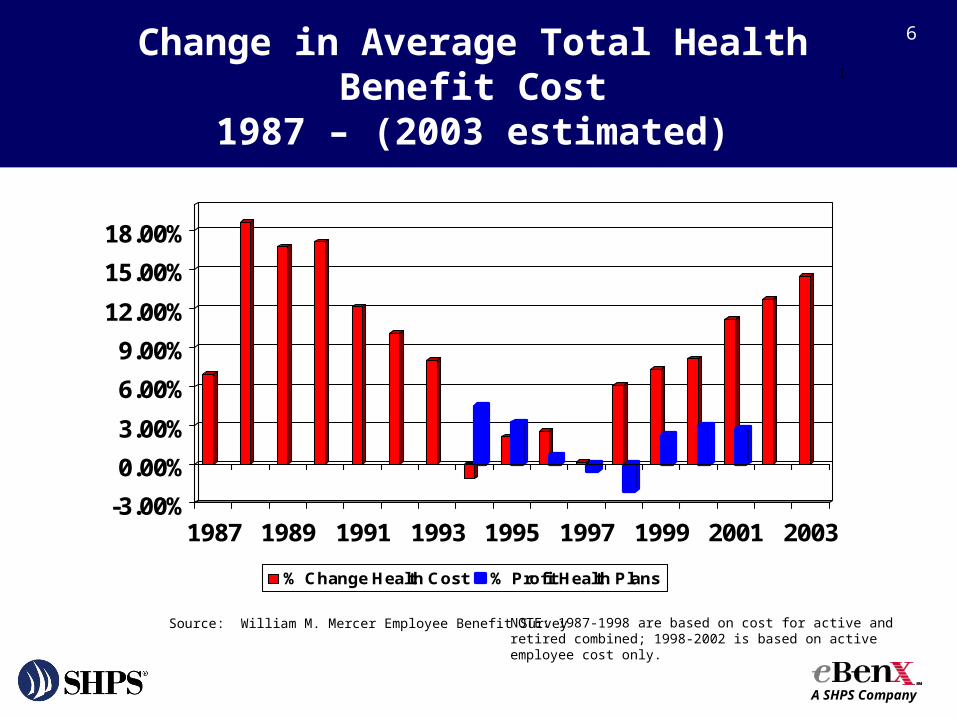

Change in Average Total Health Benefit Cost1987 – (2003 estimated)

Source: William M. Mercer Employee Benefit Survey NOTE: 1987-1998 are based on cost for active and retired combined; 1998-2002 is based on active employee cost only.

7

A SHPS Company

1

7

0% 10% 20% 30% 40% 50% 60% 70% 80%

Stock Opt.

Disability

LTC Ins.

Life Ins.

Pension

401 K

Health Ins.

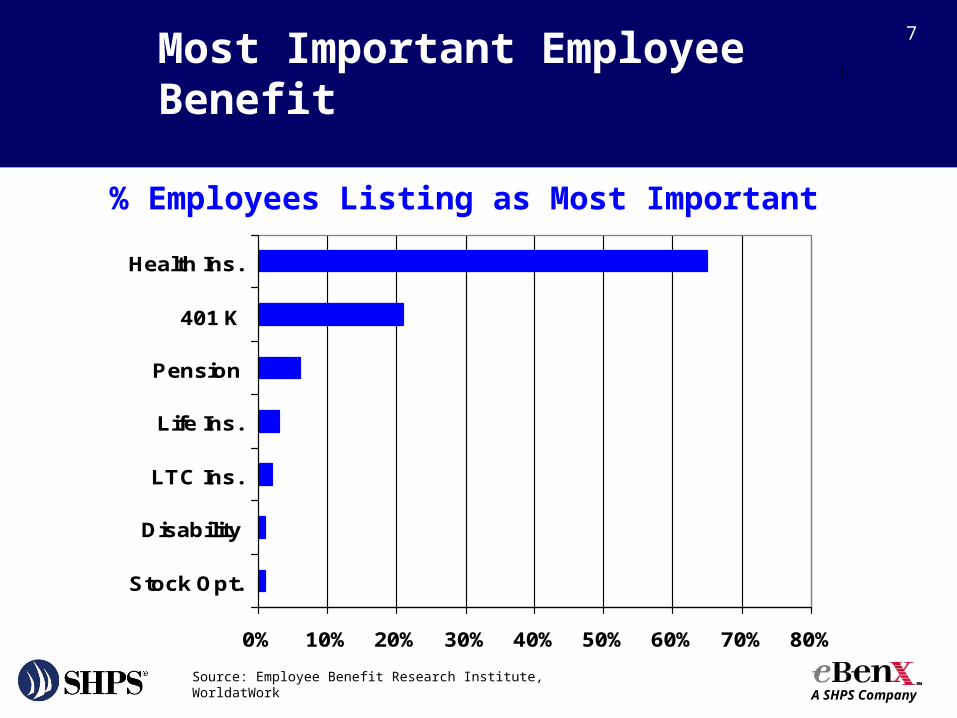

Most Important Employee Benefit

Source: Employee Benefit Research Institute, WorldatWork

% Employees Listing as Most Important

8

A SHPS Company

1

8

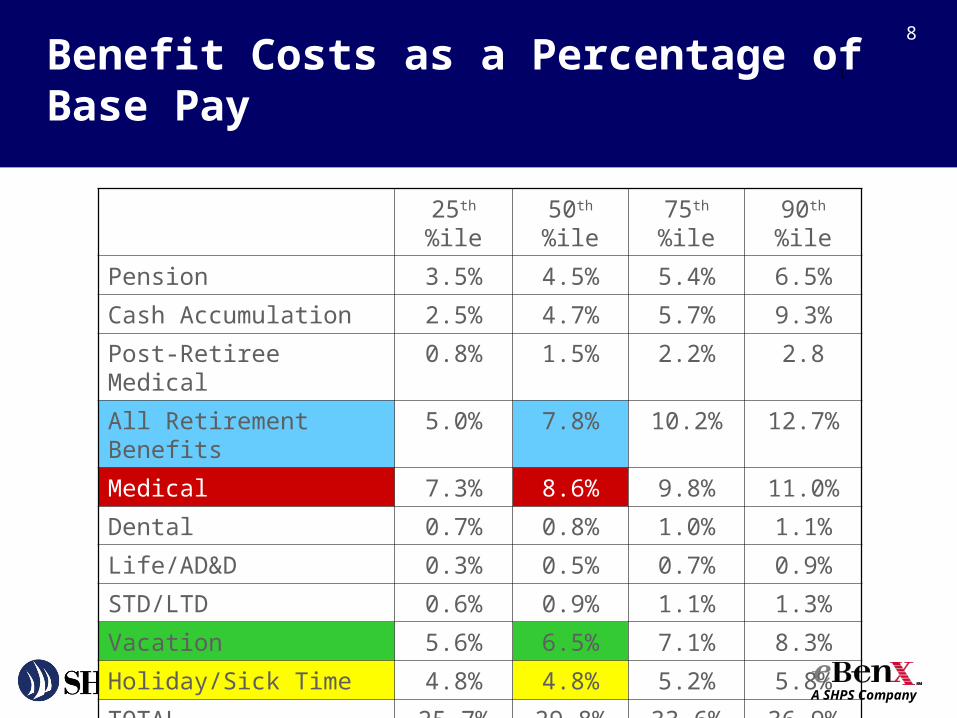

25th%ile 50th%ile 75th%ile 90th%ile

Pension 3.5% 4.5% 5.4% 6.5%

Cash Accumulation 2.5% 4.7% 5.7% 9.3%

Post-Retiree Medical 0.8% 1.5% 2.2% 2.8

All Retirement Benefits 5.0% 7.8% 10.2% 12.7%

Medical 7.3% 8.6% 9.8% 11.0%

Dental 0.7% 0.8% 1.0% 1.1%

Life/AD&D 0.3% 0.5% 0.7% 0.9%

STD/LTD 0.6% 0.9% 1.1% 1.3%

Vacation 5.6% 6.5% 7.1% 8.3%

Holiday/Sick Time 4.8% 4.8% 5.2% 5.8%

TOTAL 25.7% 29.8% 33.6% 36.9%

Benefit Costs as a Percentage of Base Pay

9

A SHPS Company

1

9

Medical Stop Loss Marketplace

10

A SHPS Company

1

10

Stop Loss Industry Results

2002- Profits Exceeded Target

Why?

Reinsurers got tough. MGUs lost their reinsurance Surviving MGUs had to write to set

RTMs

11

A SHPS Company

1

11

Stop Loss Industry Results

2002- Profits Exceeded Target 2003- Profits at Target 2004- Profits Below Target

(Losses?)

12

A SHPS Company

1

12

Stop Loss Industry Results

Why the negative trend?

Leveraged trend increase- 27%

vs

Sold trend increase- 21%

RTMs decrease

13

A SHPS Company

1

13

Stop Loss Industry Results

Why the negative trend? Increased start-up activity An underwriter at an MGU has said

“Fear has been replaced by greed.”

14

A SHPS Company

1

14

Stop Loss Industry Providers

Currently- 115 (approx)2002- asked to evaluate 1 start-up2003 (to date)- asked to evaluate 12

start-ups

15

A SHPS Company

1

15

Consumer Directed Health

Plans

16

A SHPS Company

1

16

Features:

• HRA

• High Deductible PPO Weak Discounts Weak Med Mgt

• High Administrative Fees

• Theory – Consumers seeking low cost providers will offset weak discounts and high administration fees

• Introduces “consumer cost impact”

Pre

ven

tive

Car

e 10

0%

Personal CareAccount

(Health Reimb.Account)

$1,000

Health InsurancePPO (80% IN,

60% OON)$1,500 deductible

MemberResponsibility

$500 Consumer

Directed

Consumer Directed Health Plans

17

A SHPS Company

1

17

Pre

ven

tive

Car

e 10

0%

Personal CareAccount

(Health Reimb.Account)

$1,000

Health InsurancePPO (80% IN,

60% OON)$1,500 deductible

MemberResponsibility

$500 Consumer

Directed

Internet

Provider Information Pricing Quality

Account Information Benefits Balances

General Health and Wellness Info

Health Risk Assessment

Voluntary Medical Management (“Health Coach”)

+

Consumer Directed Health Plans

18

A SHPS Company

1

18

Potential Benefits May reduce cost - May reduce unnecessary care - May reduce routine visits later in the year when HRA funds disappear

Encourages “consumerism” and the cost-effective use of services by exposing employees to cost impact

Encourages provider competition on both price and quality

Provides employees with useful information - Health risk assessments - Provider price and quality information - Nurse coaches and health interventions

Consumer Directed Health Plans

19

A SHPS Company

1

19

Potential Drawbacks

Entire premise might be flawed – not reduce cost - Not enough history for credible actuarial predictions - Very low enrollment history so far

Vendors / programs are not well established

Cost might increase - Adverse selection (only healthy people enroll) - Relatively weak discounts from “rented” networks - Employees waiving coverage historically might return to receive HRA funding - People may forego preventive care - Higher administrative fees

Consumer Directed Health Plans

20

A SHPS Company

1

20

Predictive Modeling

21

A SHPS Company

1

21

Predictive Modeling

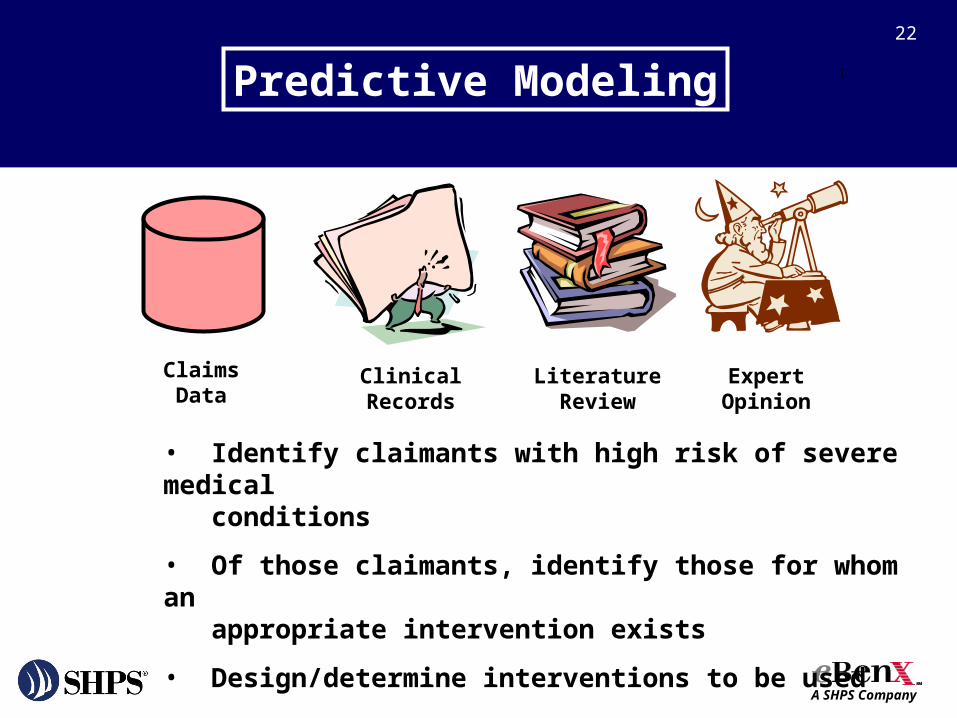

Predictive Modeling – the use of artificial intelligence or “expert systems” to predict future chronic and catastrophic claimants.

22

A SHPS Company

1

22

ClaimsData

ClinicalRecords

ExpertOpinion

LiteratureReview

• Identify claimants with high risk of severe medical conditions

• Of those claimants, identify those for whom an appropriate intervention exists

• Design/determine interventions to be used

Predictive Modeling

23

A SHPS Company

1

23

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% of Members

% o

f M

ed

ica

l Co

st

Bracket Study

62% mbrs, 3% care

87% mbrs, 41% care

99% mbrs, 69% care

Predictive Modeling

24

A SHPS Company

1

24

62%

25%

12%

1%3%

38%

27%31%

0%

10%

20%

30%

40%

50%

60%

70%

Healthy Acute Chronic Catastrophic

% Members % Cost

Claims PMPM $9.27 $179.76 $361.28 $4,790.63

Source: Aetna Healthcare

Predictive Modeling

25

A SHPS Company

1

25

Disease Management

26

A SHPS Company

1

26

Disease Management

Definition- the planned and systematic approach to caring for a population of patients with anticipatable needs and problems, typically defined by a chronic illness.

Source: Pacific Business Group on Health

27

A SHPS Company

1

27

Disease Management

Common disease management conditionsDiabetesAsthmaCoronary Artery DiseaseCongestive Heart FailureDepressionPregnancy

28

A SHPS Company

1

28

Severe Acute Respiratory Syndrome

(SARS)

29

A SHPS Company

1

29

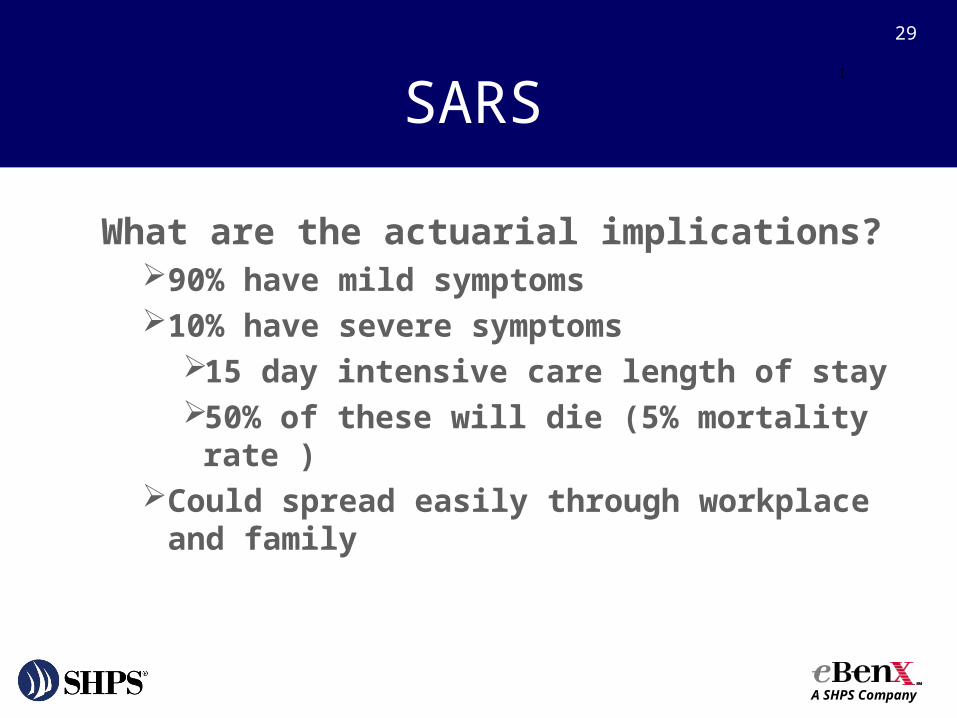

SARS

What are the actuarial implications?90% have mild symptoms10% have severe symptoms

15 day intensive care length of stay50% of these will die (5% mortality

rate )Could spread easily through workplace

and family

30

A SHPS Company

1

30

Society of Actuaries Large

Claim Study

31

A SHPS Company

1

31

Society of Actuaries Large

Claim Study

32

A SHPS Company

1

32

Society Of Actuaries Large Claim Study

New study covering 1996 to 1998 expected to be released in fall 2003

10 large insurers have contributedFollow-up to study covering 1991 to

1992, released in 1997

33

A SHPS Company

1

33

Questions ?

34

A SHPS Company

1

34

Thank You