seismic acquisition energy sector. 2 seismic acquisition companies in this industry focus on...

TRANSCRIPT

Seismic AcquisitionEnergy Sector

2

Seismic Acquisition

Companies in this industry focus on providing and using seismic technologies, including 3-D seismic acquisition, to collect data on oil and natural gas reserves. They then sell this data to their customers to receive the majority of their revenues.

These companies are operating in multiple regions of the United States and other countries by hiring and using acquisition crews for the data acquisition process.

Global Geophysical Services(NYSE: GGS)

Dawson Geophysical Co.(Nasdaq: DWSN)

Geokinetics Inc.(NYSEAMEX): GOK

TGC Industries Inc.(Nasdaq: TGE)

CGG Veritas(NYSE: CGV)

Ion Geophysical Corp.(NYSE: IO)

3

Rely on Contracts for Revenue

• Drilling Company purchases land• Need to explore and find oil and natural gas reserves

• Drilling companies offer up contracts to collect data on land• Seismic Acquisition companies offer bids • Company chooses bid to acceptLand Purchased

Contract Bids Data Collection

Drilling Begins

• Companies use 3-D acquisition to collect data on reserves• Actual value added in this step• Length of this process varies depending on certain factors

4

Energy7,726.4609B(100%)

Energy equipment and services518.7B

Seismic Acquisition$20B (0.26%)

Industry Breakdown by Market Cap($BLN)

Seismic Acquisition is Niche within Oil and Gas

Sub-Sector Breakdown By Revenue

0%

8%

16%

1%

65%

10%

5

Outlook for Seismic Acquisition Industry

Key Industry Trends

Technology Advancements

Energy IndependenceIncreasing Oil Prices

Positive Industry Rating

Technology Advancements

Energy IndependenceIncreasing Oil Prices

6

Trends

Technology Advancements Energy Independence Increasing Oil PricesTechnology Advancements Energy Independence Increasing Oil Prices

7

Investment In Technology Increases Demand

State-of-the-art equipment helps maintain and gain

contracts

• Up to 15% of revenue invested in new technology

• More channels increases accuracy and

decreases marginal cost

• ¾ of capital expenditures used for investment in

new technology

• Shift toward 4-D and autonomous equipment

• Clearer Data results in higher demand and

revenue

8

Trends

Technology Advancements Energy Independence Increasing Oil Prices

9

Energy Independence in US Increases Market Size

2005 2006 2007 2008 2009 2010 2011 2012 2013e 2014e 2015e 2016e1517192123252729

Natural Gas to reach Independence in US by 2016

Production Consumption

Trill

ion

Cub

ic F

t.• U.S. production CAGR 3.93%

• Consumption CAGR 1.98%

• Revenue increase of 1.95%

• Imports decreasing

• US production increasing

• Demand for Seismic Data increasing

2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

5

10

15

20

25

30

35

$-

$50

$100

$150

$200

$250

$300

$350

$400

Imported Natural Gas Domestic Natural Gas Revenue (MM)

Trill

ion

Cub

it Ft

Rev

enue

10

Trends

Technology Advancements Energy Independence Increasing Oil Prices

11

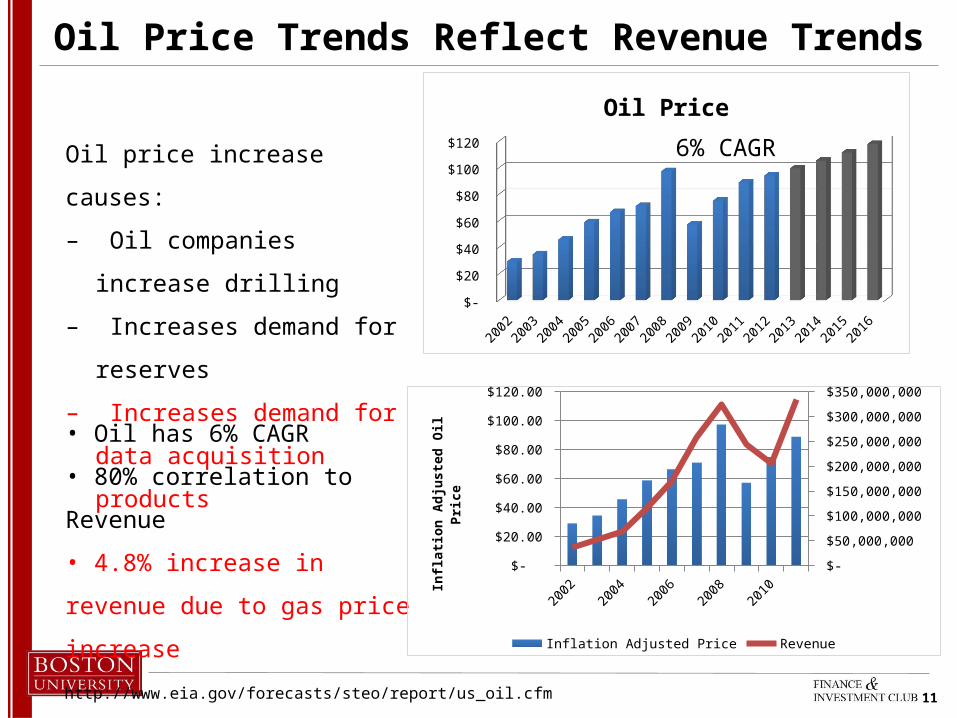

Oil Price Trends Reflect Revenue Trends

• Oil has 6% CAGR

• 80% correlation to Revenue

• 4.8% increase in revenue due to gas

price increase

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 $-

$20

$40

$60

$80

$100

$120

Oil Price

Oil price increase causes:

– Oil companies increase drilling

– Increases demand for reserves

– Increases demand for data

acquisition products

http://www.eia.gov/forecasts/steo/report/us_oil.cfm

6% CAGR

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 $-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$-

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

$350,000,000

Inflation Adjusted Price Revenue

Infla

tion

Adj

uste

d O

il Pr

ice

12

Risks

GovernmentRegulation Oil and Gas Price Drop Lack of

TechnologyGovernmentRegulation Oil and Gas Price Drop Lack of

Technology

13

Government Regulation is a High Long-Term Risk

Reasons for proposed regulation– Air and water contamination worries– Lack of disclosure of used in chemicals in fracking– EPA estimates 40% of US methane from fracking

New Legislation on regulation of fracking will:- Slow down permit process, decreasing production rates- Decrease in revenues and increase in expenses

Short-Term Risk: LOW- Would cut jobs and slow economy- Booming industry despite recession- Legislation takes time to pass

Long-Term Risk: HIGH– Water contamination is serious risk– Disclosure of chemicals already passed in many states

14

Risks

GovernmentRegulation Oil and Gas Price Drop Lack of

Technology

15

Oil and Natural Gas Price Volatility

Oil Prices on rise– Worst case projections show minimal drop– 2009 shows only drop in 10 years

Natural Gas Prices volatility due to yearly demand cycles

– Increase demand projections eliminate any major risk

– Low correlation between gas prices and revenues

– Demand increases adjust price– EIA projects price increases for upcoming

years

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 $-

$20

$40

$60

$80

$100

$120

Oil Price

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 $-

$1

$2

$3

$4

$5

$6

$7

$8

Natural Gas Price

http://www.eia.gov/forecasts/steo/report/natgas.cfm http://www.eia.gov/forecasts/steo/report/us_oil.cfm

16

Risks

GovernmentRegulation Oil and Gas Price Drop Lack of

Technology

17

Lag in Technology Loses Competitive Advantage

Invest in New Technology

Clearer Seismic Data

Higher Service Demand

Increased Revenues

• Buyer Power in Industry: HIGH

• Transitioning from 3D to 4D imaging

• Companies using 3D lose customers

18

Company % of 52 week high

Net debt/ EBITDA

TTM EBITDA Margin

ROA ROERevenue

CAGR 2009-11

Revenue CAGR

2007-2011

LTMP/E

EV/EBITDA

65.65% 6.39 0.54 8.24% 13.47% 10.99% 14.30% 9.25 2.53

50.44% 0.57 0.17 5.43% 6.72% 16.87% 6.63% 14.69 3.29

96.01% n/a 0.14 -3.30% n/a 22.26% 20.88% n/a 5.37

55.61% 0.38 0.51 14.91% 21.85% 29.23% 13.69% 7.36 3.86

46.13% 10.15 0.29 2.36% 2.58% 4.07% -0.75% 52.12 6.90

40.73% 1.61 0.37 7.74% 10.88% 0.58% -12.50% 19.33 6.20

High 96.01% 10.15 0.54 14.9% 21.9% 29.23% 20.88% 52.12 6.90

Median 46.13% 1.61 0.37 7.7% 10.9% 4.07% 10.16% 19.33 4.62

Mean 47.49% 4.04 0.39 8.3% 11.8% 11.29% 7.04% 26.27 4.69

Low 40.73% -8.17 0.14 -3.3% 2.6% 0.58% -12.50% 7.36 2.53

Source: Capital IQ

TGC Industries Financials Show Strong Company

19

Recommend TGC Industries in this Growing Industry

New Technology Raising Revenues

Energy Independence Creating

Service Demand

Revenues Rise with Oil

Prices

Government

Regulation

Oil and Gas Price Volatility

Falling Behind on Technolog

y

Trends

Risks

Positive Industry Outlook

Strong Position for Technology Investment

Highest ROE and ROA in Industry

Increasing Market

Share

20

Slide MatrixPresentationIndustry DefinitionIndustry BreakdownNatural Gas and Oil ProjectionsRevenue GenerationTechnology TrendEnergy Independence TrendOil Price TrendGovernment Regulation RiskGas and Oil Price RiskTechnology RiskComparable ChartTGC Recommendation

Backup SlidesRevenue CorrelationCOGS CorrelationGross Margin CorrelationCapEx Equipment 1CapEx Equipment 2Global Geophysical CapExGlobal Geophysical GraphDawson CapExCapEx/Revenue GraphNatural Gas and Oil PricesObama Fracking LegislationNatural Gas and Oil Projections

21

Total Revenue and Correlation

In Millions of USD (except for per share items)

12 months ending 2011-12-

31

12 months ending 2010-

12-31

12 months ending 2009-

12-31

12 months ending 2008-

12-31

Ion 454.62 444.32 419.78 679.52

CGG 2,807.98 2,708.28 2,771.74 3,221.39

Dawson 333.28 205.27 244 324.93

Geokinetic 763.73 558.13 510.97 474.6

Global Geophysical services 385.36 254.7 312.8 376.26

TGC 151.03 108.32 90.43 86.77

Gas Prices per Barrel (yearly) 105.48 80.42 63.60 99.41

* source: EIA.gov

Correlation

Ion 0.526543

CGG 0.493947

Dawson 0.807728

Geokinetic 0.522062

Global Geophysical services 0.716421

TGC 0.558636

0.604223

22

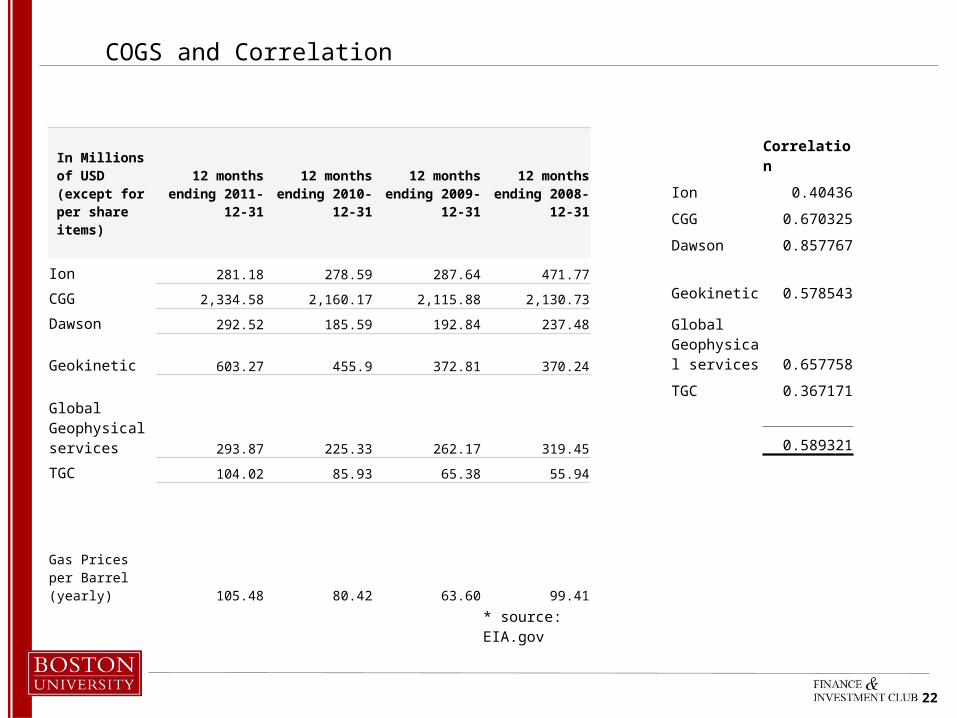

COGS and Correlation

In Millions of USD (except for per share items)

12 months ending 2011-12-

31

12 months ending 2010-12-

31

12 months ending 2009-12-

31

12 months ending 2008-12-

31

Ion 281.18 278.59 287.64 471.77

CGG 2,334.58 2,160.17 2,115.88 2,130.73

Dawson 292.52 185.59 192.84 237.48

Geokinetic 603.27 455.9 372.81 370.24

Global Geophysical services 293.87 225.33 262.17 319.45

TGC 104.02 85.93 65.38 55.94

Gas Prices per Barrel (yearly) 105.48 80.42 63.60 99.41

* source: EIA.gov

Correlation

Ion 0.40436

CGG 0.670325

Dawson 0.857767

Geokinetic 0.578543

Global Geophysical services 0.657758

TGC 0.367171

0.589321

23

Gross Profit and Correlation

In Millions of USD (except for per share items)

12 months ending 2011-12-

31

12 months ending 2010-12-

31

12 months ending 2009-12-

31

12 months ending 2008-12-

31

Ion 173.44 165.73 132.14 207.75

CGG 470.55 544.03 646.58 1,088.56

Dawson 40.76 19.68 51.16 87.44

Geokinetic 160.45 102.23 138.15 104.36

Global Geophysical services 91.49 29.38 50.63 56.8

TGC 47.01 22.39 25.05 30.84

Gas Prices per Barrel (yearly) 105.48 80.42 63.60 99.41

* source: EIA.gov

Correlation

Ion 0.816491

CGG 0.181412

Dawson 0.288426

Geokinetic 0.149726

Global Geophysical services 0.656385

TGC 0.776954

0.478233

24

CAPEX Equipment Overview

Channel – device that carries data from receiver to recorder– 500-2000 channels in 3D seismic acquisition– 120-240 channels in onshore 2D seismic acquisition

Geophone – sensors that measure ground displacement– Collect sound waves created by vibration equipment– At least one connected to each channel (the more, the better)– “Hydrophones” are the same for marine exploration

Seismic geometry – grid of seismic energy sources & receivers– Used to acquire a complete seismic survey

24

25

CAPEX Equipment Overview

State-of-the-art equipment is huge selling point– Rapid growth in imaging technology & equipment autonomy– Largest CAPEX is in multi-client libraries – only included by GGS

3D imaging still vast majority of industry– Trending toward high-density & 4D

4D “Time Lapse” Seismic Surveying– Determines changes in flow, temperature, pressure, and saturation– Important because as hydrocarbons (i.e. oil/natural gas) are extracted, pressure and

composition of field may change

Source: GGC 10-K

25

26

Global Geophysical Services (GGS)

AUTOSEIS HDR - autonomous nodal recording– Paradigm shift toward autonomy in seismic data gathering– Cuts crew size in half & increases efficiency

Recording production 3x that of traditional cable telemetry crew

Reservoir Grade 3D (RG3D) – 3D images of subsurface– High-density provides improved signal-to-noise ratio– Longer shelf life throughout geological and geophysical cycle of field– High compressional (P-wave) accuracy & allows for pre-stack analysis

Stacking – processing and consolidating data to improve signal-to noise ratio

Source: GGC 10-K

26

2012e CAPEX: $30-40M* 2011 CAPEX: $49.7M*

– $49.7M for equipment upgrades for existing crews Land nodal (AUTOSEIS) and deeper water marine technologies Developing own equipment to decrease reliance on competition

2010 CAPEX: $45.3M* 2009 CAPEX: $24.2M*

27

Global Geophysical Services (GGS)

Source: Dahlman Rose Oil Service Conference (November 2011)

27

28

Dawson Geophysical Co. (DWSN)

OYO Geospace Seismic Recorder (GSR)– High-resolution autonomous data recorder– Continuous recoding for 30+ days– Purchased 2,000 4-channel units– Purchased 25,850 single-channel units

INOVA Articulated Hydrostatic Vehicle IV 364– “Cutting-edge” seismic vibrator unit– Broad frequency bandwidth & high energy output– Stiff baseplate for low harmonic distortion– Purchased 10 in 2011; expecting another 12 in 2012

28

2012e CAPEX: $20.0M (initial budget)– Additional 12 INOVA AHV IV 364 vibrator units– Increase channel count

2011 CAPEX: $59.4M– OYO GSR single- and 4-channel units– Additional geophones– 10 INOVA AHV IV 364 vibrator units

2010 CAPEX: $20.0M

2009 CAPEX: $4.4M

29

29

30

Risk: Price drop in natural gas and oil

Jan 20

08

Apr 20

08

Jul 20

08

Oct 200

8

Jan 20

09

Apr 20

09

Jul 20

09

Oct 200

9

Jan 20

10

Apr 20

10

Jul 20

10

Oct 201

0

Jan 20

11

Apr 20

11

Jul 20

11

Oct 201

1

Jan 20

12

Apr 20

12

Jul 20

12

Oct 201

2

Jan 20

13

Apr 20

13

Jul 20

13

Oct 201

30.00

5.00

10.00

15.00

20.00

25.00

U.S. Natural Gas Prices(dollars per thousand cubic feet)

Residential priceHenry Hub spot priceComposite Wellhead price

Jan

2008

Mar

200

8M

ay 2

008

Jul 2

008

Sep

2008

Nov

2008

Jan

2009

Mar

200

9M

ay 2

009

Jul 2

009

Sep

2009

Nov

2009

Jan

2010

Mar

201

0M

ay 2

010

Jul 2

010

Sep

2010

Nov

2010

Jan

2011

Mar

201

1M

ay 2

011

Jul 2

011

Sep

2011

Nov

2011

Jan

2012

Mar

201

2M

ay 2

012

Jul 2

012

Sep

2012

Nov

2012

Jan

2013

Mar

201

3M

ay 2

013

Jul 2

013

Sep

2013

Nov

2013

0.000.501.001.502.002.503.003.50

U.S. Crude Oil Prices(dollars per gallon)

Crude Oil

31

New Legislation could add costs up to $2.5B/ year

Obama: – New Legislation on regulation of fracking

Slow down the drilling permit approval process and decrease production rates Western Energy Alliance estimates it will add $1. 2 B to costs of new wells EPA: wont add any new costs Industry: 2.5 B in added costs Bloomberg Government: $316-511 M a year (less than 1% of revenues associated with oil and gas production)

32

Natural Gas and Oil Control World Energy

25%

6%

21%

34%

14%

Coal

Nuclear

Gas

Oil

Renwables

• Oil and Gas = 54% of World Supply

• Gas expected to increase to 30% within 30 years

• Seismic Acquisition focuses on both commodities

2008 2009 2010 2011 2012 2013e 2014e 2015e

Natural Gas Consumption on the Rise

Monthly Avg Consumption CAGR: 2.38% (min CAGR = 4.97%, max = -.01%)