sefa corporate plan 2014/15 2018/19 - amazon web...

TRANSCRIPT

Sefa Corporate Plan – 2014/15 – 2018/19 Joint Portfolio Committee Meeting on Economic Development and Small Business Development

Thakhani Makhuvha

Chief Executive Officer

The Small Enterprise Finance Agency

29th July 2014

Introduction

• sefa is a wholly owned subsidiary of the Industrial Development Corporation (IDC) and provides funding ranging from R500 to R5 million via the following product / channels:

• Direct lending (50k – R5m)

• Wholesale SMME financing via retail financial intermediaries (RFIs) 50k – R3m

• Wholesale micro finance loans via micro finance institutions (MFIs) ranging from R500 to R50k

• Dedicated targeted support and lending to co-operative enterprises and support to Financial Services Co-operatives.

2

The Small Enterprise Finance Agency

(sefa) is a development finance institution

established in 2012 with a mandate to

provide access to finance to SMMEs

Government Small Business Focus

Within the context of NGP, IPAP and NDP, sefa and other development finance institutions are mandated to:

• Increase and expand the demand for goods and services produced by small businesses

• Continue to enhance efficiencies on support measures provided to SMMEs and co-operatives

• Ensure active participation of SMMEs in the industrial development programmes

• Reduce regulatory burden facing SMMEs and Co-ops

• Re-establish the Marketing Boards and Export Villages to facilitate linkages (both domestic and international) between suppliers and consumers

• Sector prioritization and promotion of SMME and Co-ops growth and development

• Upscale and fast-track the development of youth and women-owned enterprises

Specifically sefa is tasked to:

• Improve its value proposition as the primary provider of financial support to SMMEs, in collaboration with other national agencies with small business activities (e.g. IDC, NEF, Land Bank, DBSA) to particularly address market failure.

• Increase the uptake of its products and services to improve access to finance for small businesses

3

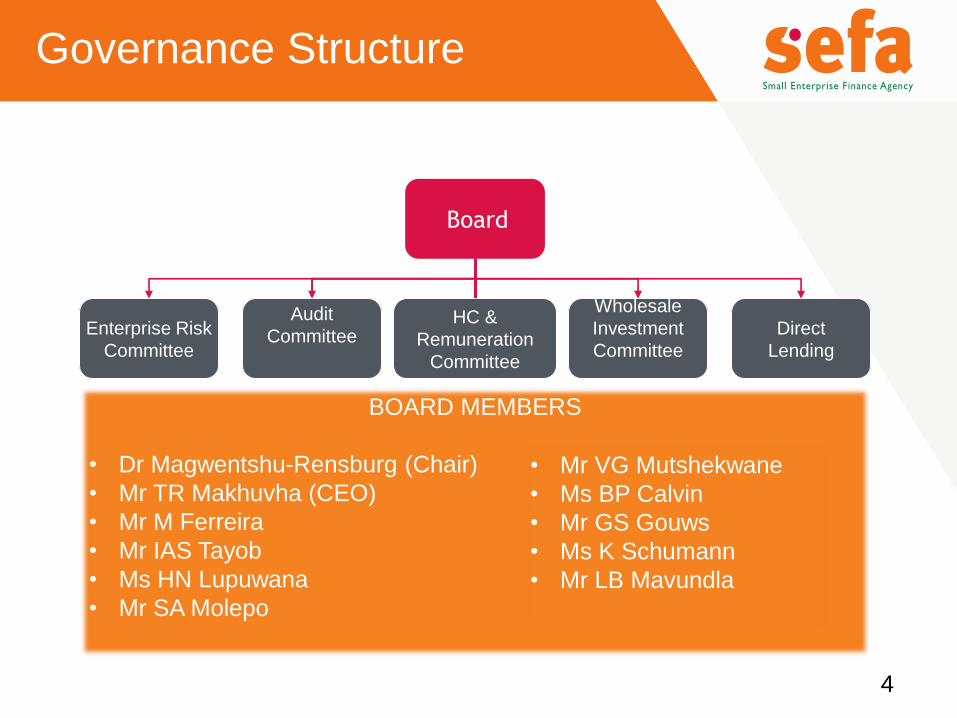

Governance Structure

4

Board

Enterprise Risk

Committee

Audit

Committee

HC &

Remuneration

Committee

Wholesale

Investment

Committee

Direct

Lending

BOARD MEMBERS

• Dr Magwentshu-Rensburg (Chair)

• Mr TR Makhuvha (CEO)

• Mr M Ferreira

• Mr IAS Tayob

• Ms HN Lupuwana

• Mr SA Molepo

• Mr VG Mutshekwane

• Ms BP Calvin

• Mr GS Gouws

• Ms K Schumann

• Mr LB Mavundla

Management Structure

5

CHIEF FINANCIAL OFFICER

Direct Lending EXECUTIVE

WHOLESALE EXECUTIVE

CHIEF RISK OFFICER

HR EXECUTIVE

Executive in CEO Office

sefa Board

CEO

Head:

Internal Audit

Company

Secretariat

5

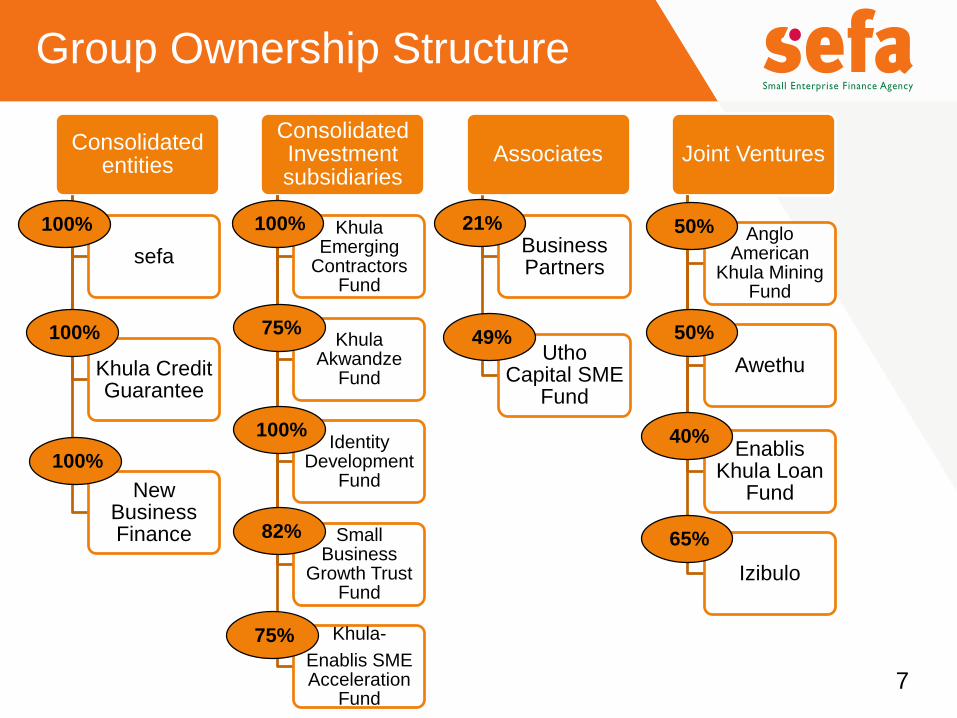

Group Ownership Structure

Consolidated entities

sefa

Khula Credit Guarantee

New Business Finance

Consolidated Investment subsidiaries

Khula Emerging

Contractors Fund

Khula Akwandze

Fund

Identity Development

Fund

Small Business

Growth Trust Fund

Khula-

Enablis SME Acceleration

Fund

Associates

Business Partners

UthoCapital SME

Fund

Joint Ventures

Anglo American

Khula Mining Fund

Awethu

EnablisKhula Loan

Fund

Izibulo

Wholly owned

subsidiaries not

consolidated:

• Khula Land

Reform

Empowerment

Facility NPC

• Khula Institutional

Support Services

NPC

Dormant

subsidiaries:

• Khula Business

Premises (Pty)

Ltd

• New Cape Equity

Fund (Pty) Ltd

• MKN Equity Fund

(Pty) Ltd

100%

100%

100%

75%

100%

82%

75%

21%

49%

50%

50%

40%

65%

100%

7

R’000 Group 2014 Group 2013

Total Assets R2,227,194 R2,179,684

Shareholders’ loan R1,175,521 R944,542

Other liabilities R158,353 R169,941

Equity R893,320 R1,065,201

Total Equity & Liabilities R2,227,194 R2,179,684

Financial Position

8

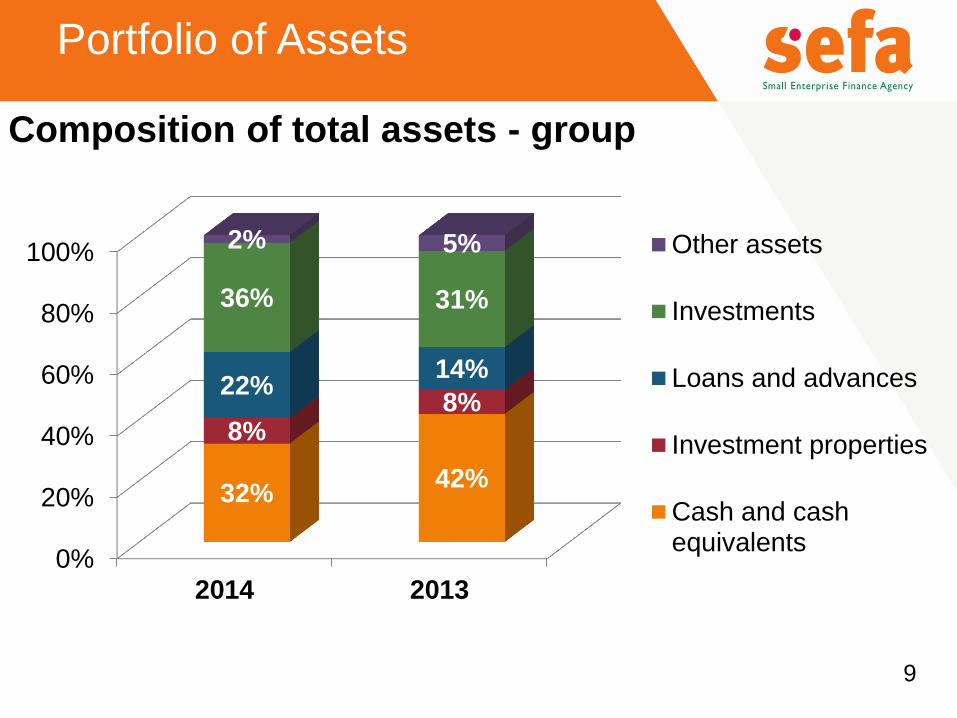

Composition of total assets - group

0%

20%

40%

60%

80%

100%

2014 2013

32% 42%

8% 8%

22% 14%

36% 31%

2% 5% Other assets

Investments

Loans and advances

Investment properties

Cash and cashequivalents

Portfolio of Assets

9

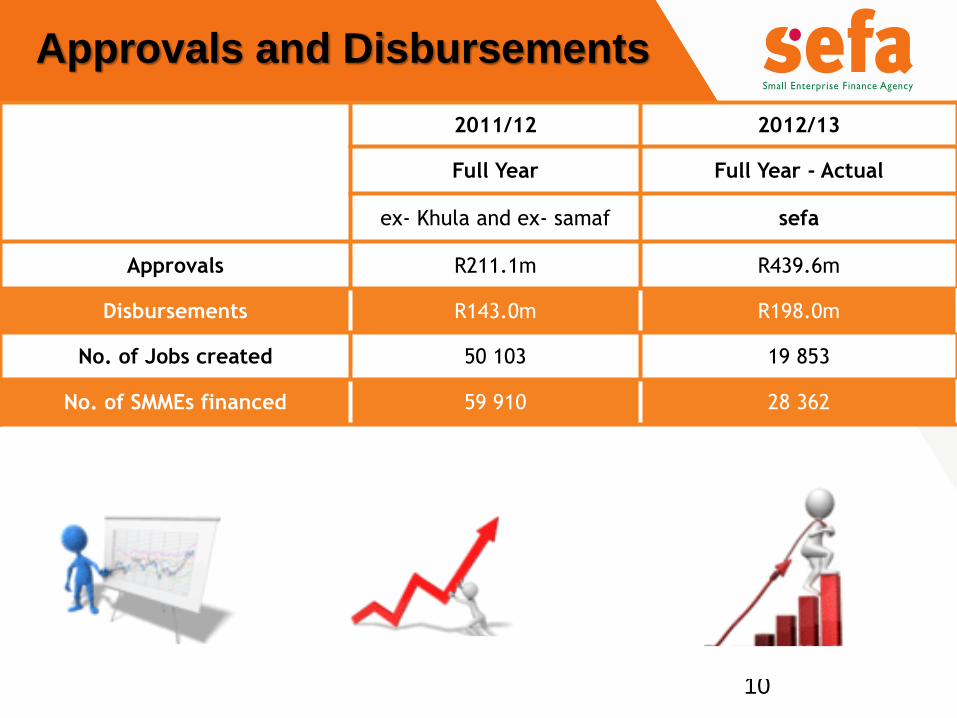

Approvals and Disbursements

10

2011/12 2012/13

Full Year Full Year - Actual

ex- Khula and ex- samaf sefa

Approvals R211.1m R439.6m

Disbursements R143.0m R198.0m

No. of Jobs created 50 103 19 853

No. of SMMEs financed 59 910 28 362

Target Market, Products and distribution channels

Target market

sefa’s target market consists of survivalist, micro, small and medium

businesses as defined in Schedule 1 of the National Small Business Act of

1996 (as amended in 2004) with specific focus on:

• Services (including retailing, wholesaling and tourism);

• Manufacturing (including agro-processing);

• Agriculture (specifically land reform beneficiaries and micro-farming activities);

• Construction (small construction contractors);

• Mining (specifically small miners).

12

• Survivalists and microenterprises – loans of between R500 and R50 000

• Small enterprises – loans between R50 000 and R1 000 000

• Medium enterprises – loans between R1 000 000 and R5 000 000

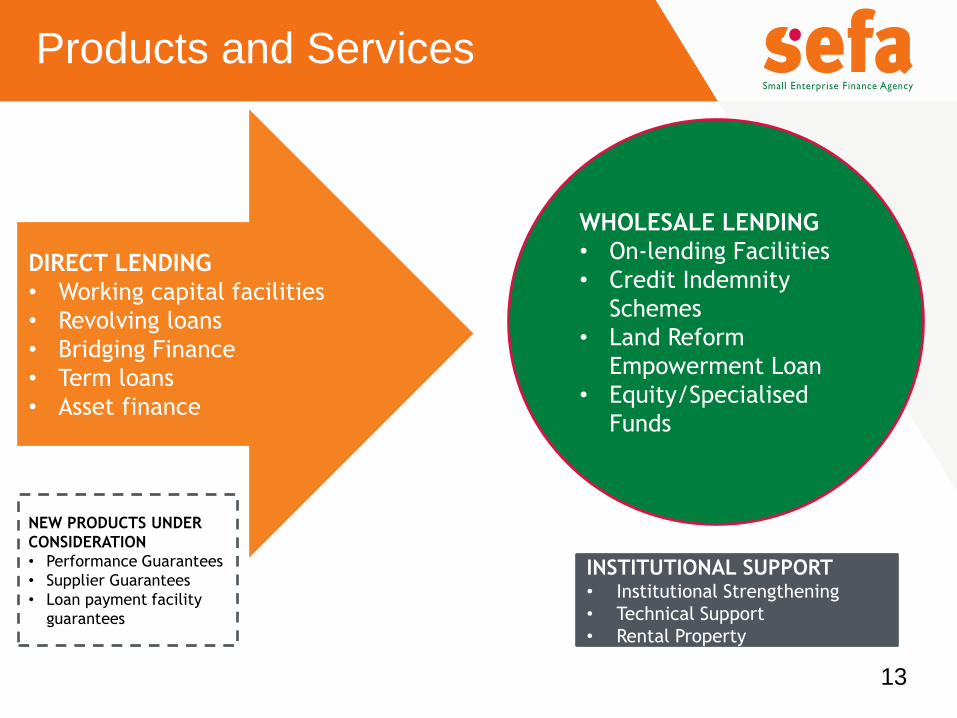

Products and Services

13

DIRECT LENDING

• Working capital facilities

• Revolving loans

• Bridging Finance

• Term loans

• Asset finance

WHOLESALE LENDING

• On-lending Facilities

• Credit Indemnity

Schemes

• Land Reform

Empowerment Loan

• Equity/Specialised

Funds

INSTITUTIONAL SUPPORT • Institutional Strengthening

• Technical Support

• Rental Property

NEW PRODUCTS UNDER

CONSIDERATION

• Performance Guarantees

• Supplier Guarantees

• Loan payment facility

guarantees

14

●

◦ ♦ ▲ 16 Micro-Finance Intermediaries

▪ 6 Retail Finance Intermediaries

∞ 3 Partnerships

*

●

●

●

●

●

●

●

● ● ●

♦

♦

♦

♦

♦

♦

♦

♦

♦

♦

♦ ▲

▲

▲

▲

▲

▲

▲

▲

▲ ▲

▲ ▲

▲ ▲ ▲

▲ 3 sefa Branch Offices

◦

◦

◦ ▪

▪

▪ ▪ ▪

▪

▪

9 sefa Regional Offices

10 Cooperative Offices

* *

* *

* *

*

*

∞ ∞ 8 Specialised Funds ∞

∞

Our Footprint

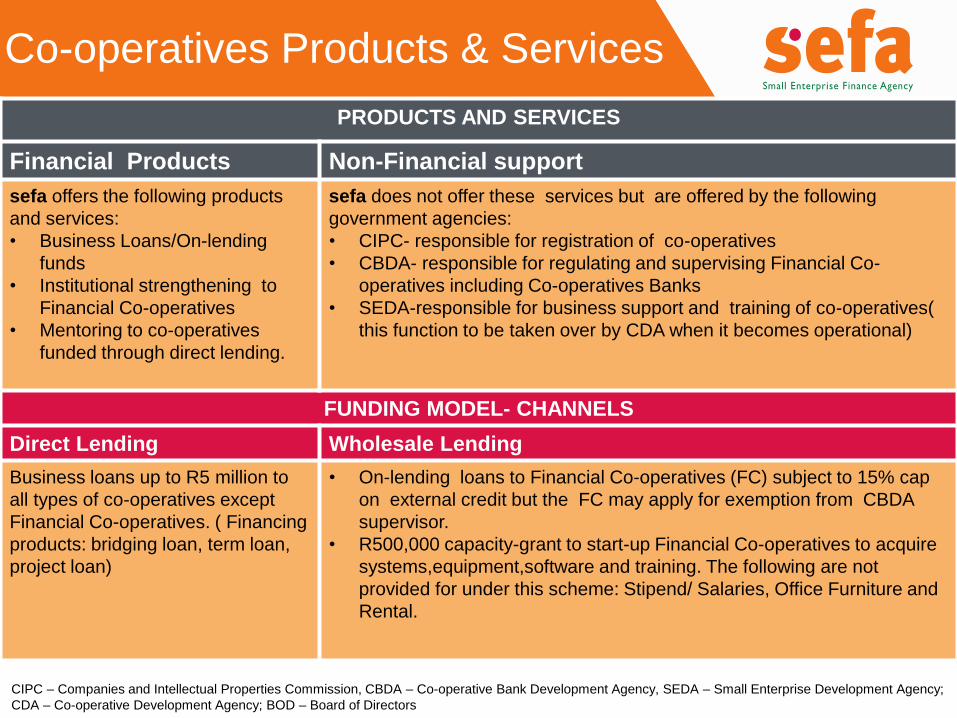

Co-operatives Products & Services

PRODUCTS AND SERVICES

Financial Products Non-Financial support

sefa offers the following products

and services:

• Business Loans/On-lending

funds

• Institutional strengthening to

Financial Co-operatives

• Mentoring to co-operatives

funded through direct lending.

sefa does not offer these services but are offered by the following

government agencies:

• CIPC- responsible for registration of co-operatives

• CBDA- responsible for regulating and supervising Financial Co-

operatives including Co-operatives Banks

• SEDA-responsible for business support and training of co-operatives(

this function to be taken over by CDA when it becomes operational)

FUNDING MODEL- CHANNELS

Direct Lending Wholesale Lending

Business loans up to R5 million to

all types of co-operatives except

Financial Co-operatives. ( Financing

products: bridging loan, term loan,

project loan)

• On-lending loans to Financial Co-operatives (FC) subject to 15% cap

on external credit but the FC may apply for exemption from CBDA

supervisor.

• R500,000 capacity-grant to start-up Financial Co-operatives to acquire

systems,equipment,software and training. The following are not

provided for under this scheme: Stipend/ Salaries, Office Furniture and

Rental.

CIPC – Companies and Intellectual Properties Commission, CBDA – Co-operative Bank Development Agency, SEDA – Small Enterprise Development Agency;

CDA – Co-operative Development Agency; BOD – Board of Directors

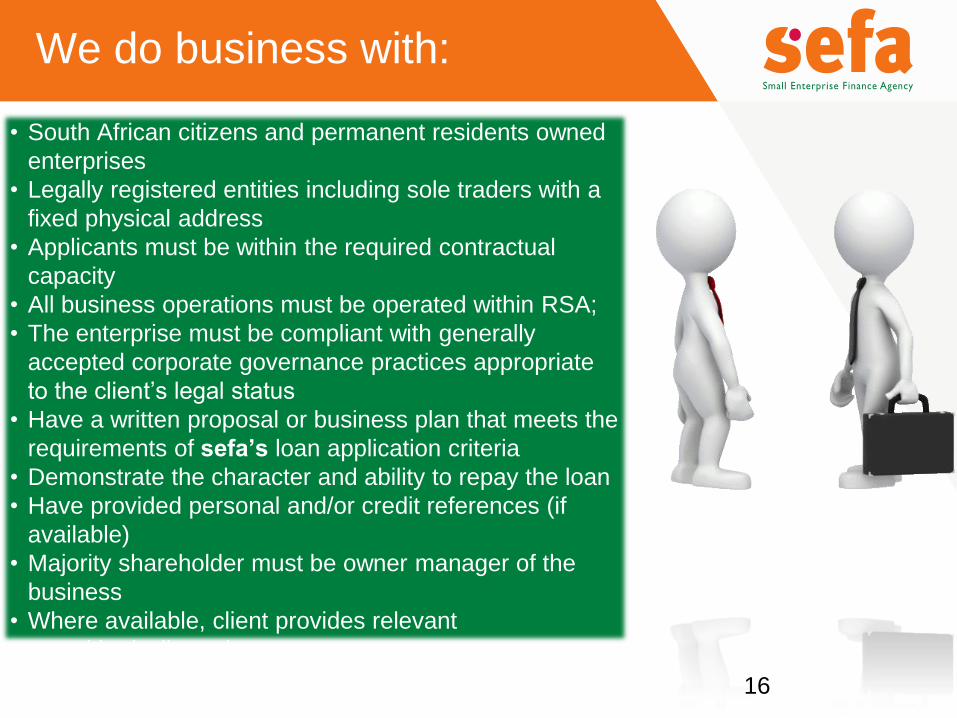

We do business with:

16

• South African citizens and permanent residents owned

enterprises

• Legally registered entities including sole traders with a

fixed physical address

• Applicants must be within the required contractual

capacity

• All business operations must be operated within RSA;

• The enterprise must be compliant with generally

accepted corporate governance practices appropriate

to the client’s legal status

• Have a written proposal or business plan that meets the

requirements of sefa’s loan application criteria

• Demonstrate the character and ability to repay the loan

• Have provided personal and/or credit references (if

available)

• Majority shareholder must be owner manager of the

business

• Where available, client provides relevant

securities/collateral

• Businesses with a valid tax clearance certificate

What makes sefa different

• Provision of capital and/or interest moratorium (Payment

Holiday) up to 12 Months

• High appetite for risk in exchange for high development

impact

• Financing SMMEs including start up businesses that are

often perceived as high risk

• Addressing the financing gap for loans below R500k

• Provision of pre and post loan business support

• Provision of funding to entrepreneurs with adverse credit

records provided they can demonstrate active remedy of

their indebtedness

• Lending not solely based on security backing – long term

sustainability potential

• Specific focus on youth owned businesses

17

What we need when applying

18

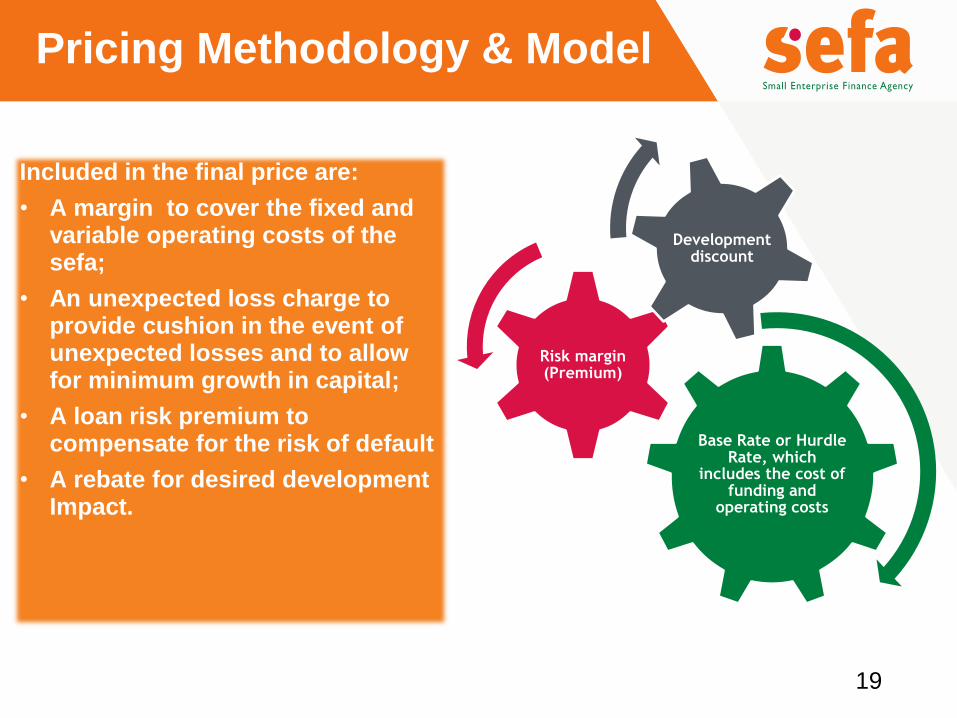

Pricing Methodology & Model

Included in the final price are:

• A margin to cover the fixed and variable operating costs of the sefa;

• An unexpected loss charge to provide cushion in the event of unexpected losses and to allow for minimum growth in capital;

• A loan risk premium to compensate for the risk of default

• A rebate for desired development Impact.

19

Base Rate or Hurdle Rate, which

includes the cost of funding and

operating costs

Risk margin (Premium)

Development discount

20

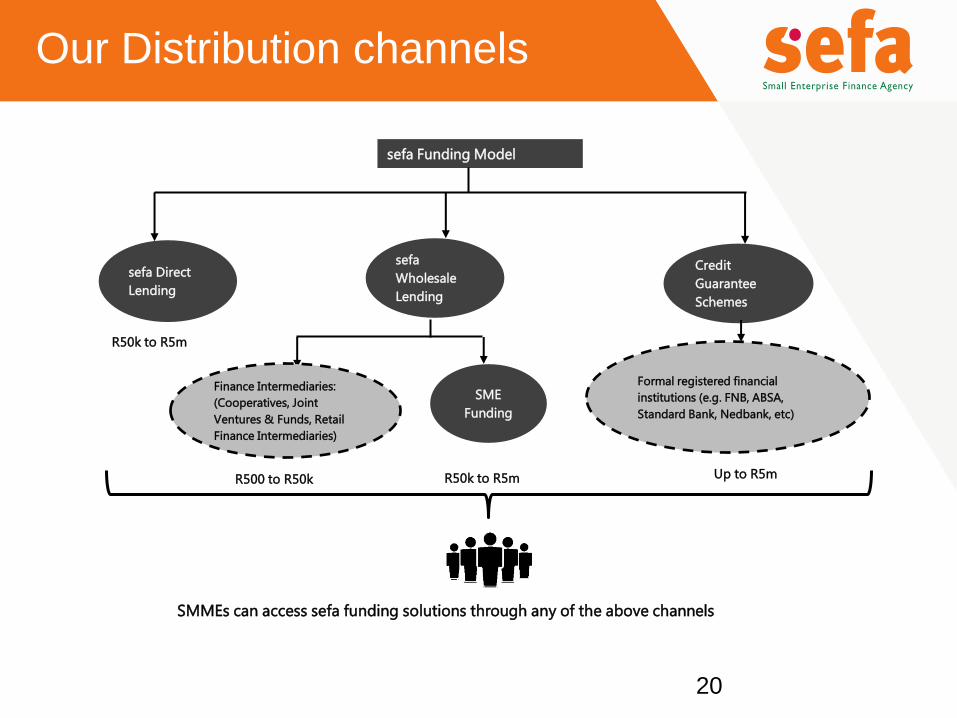

Our Distribution channels

sefa Direct

Lending

R50k to R5m

sefa

Wholesale

Lending

sefa Funding Model

SMMEs can access sefa funding solutions through any of the above channels

Credit

Guarantee

Schemes

Finance Intermediaries:

(Cooperatives, Joint

Ventures & Funds, Retail

Finance Intermediaries)

R50k to R5m Up to R5m

SME

Funding

R500 to R50k

Formal registered financial

institutions (e.g. FNB, ABSA,

Standard Bank, Nedbank, etc)

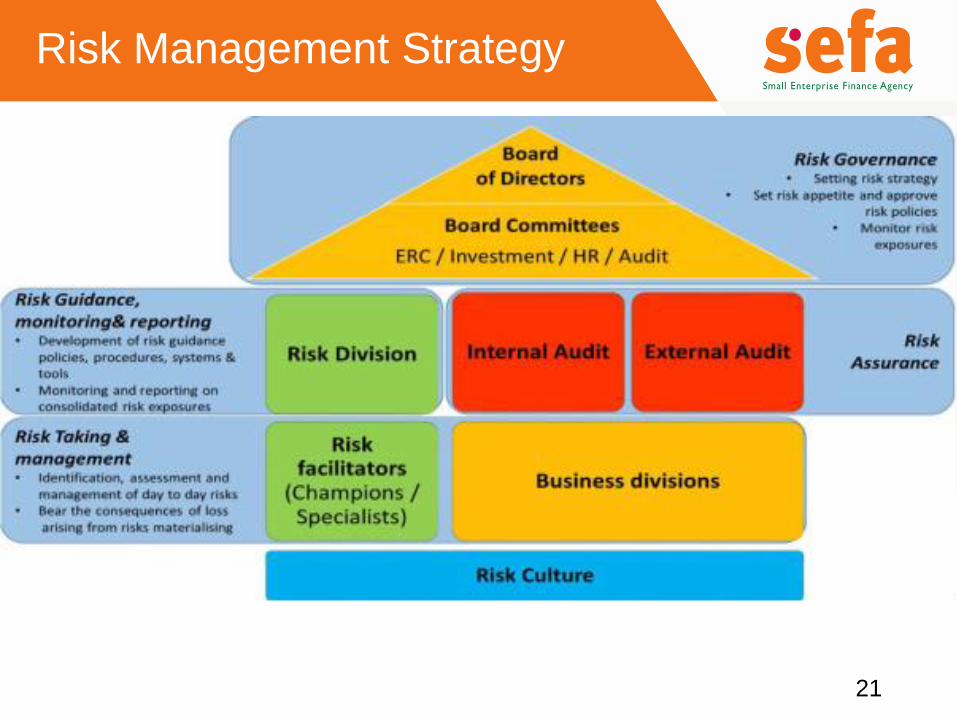

Risk Management Strategy

21

23

STRATEGIC

OBJECTIVE/

ENABLER

STRATEGIC GOAL

STATEMENT

KEY

PERFORMANCE

AREA

KEY PERFORMANCE

INDICATOR

KEY

PERFORMA

NCE

TARGET

Increase access &

provision of

finance to SMMEs

through a national

footprint &

contribute to job

creation

• Expand Direct

Lending through

partnerships

• Expand access to

Micro Enterprise

Finance

• Stronger partnerships

with RFIs in SMME

wholesale finance

• Increase utilisation of

guarantee indemnity

scheme by

commercial banks

Enable SMMEs to

access finance &

development

impact

Improve &

maintain

turnaround times

for approvals

Approvals

Disbursements

Development Impact:

R974m

R800m

SMMEs financed 37 758

Overall jobs created 57 255

Disbursements to

Youth owned 30%

Rural provinces 45%

Women 45%

People with disabilities 2%

Black-owned

businesses

70%

Facilities <R250k 40%

Approval in productive

industrial

20%

Number of day: bridging

finance

10

Number of days: term

loans

20

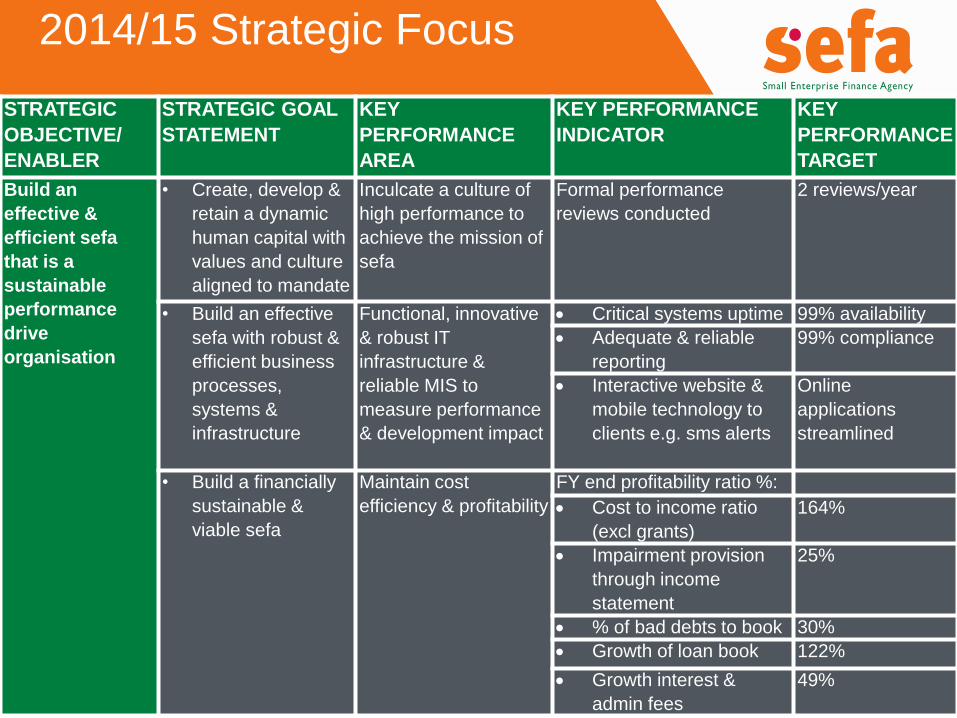

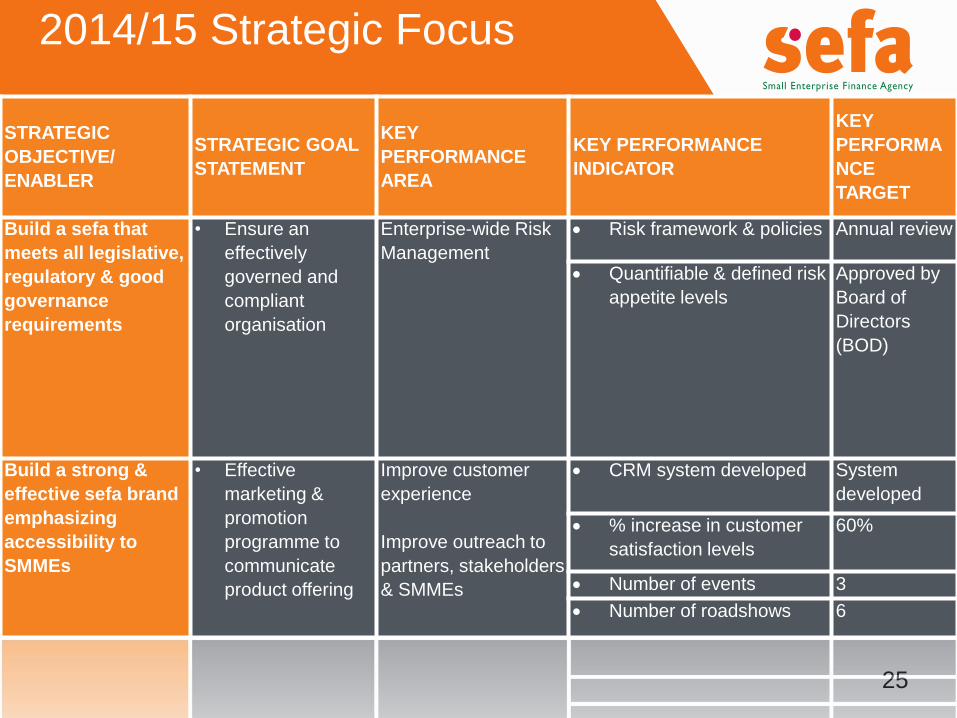

2014/15 Strategic Focus

24

STRATEGIC

OBJECTIVE/

ENABLER

STRATEGIC GOAL

STATEMENT

KEY

PERFORMANCE

AREA

KEY PERFORMANCE

INDICATOR

KEY

PERFORMANCE

TARGET

Build an

effective &

efficient sefa

that is a

sustainable

performance

drive

organisation

• Create, develop &

retain a dynamic

human capital with

values and culture

aligned to mandate

Inculcate a culture of

high performance to

achieve the mission of

sefa

Formal performance

reviews conducted

2 reviews/year

• Build an effective

sefa with robust &

efficient business

processes,

systems &

infrastructure

Functional, innovative

& robust IT

infrastructure &

reliable MIS to

measure performance

& development impact

Critical systems uptime 99% availability

Adequate & reliable

reporting

99% compliance

Interactive website &

mobile technology to

clients e.g. sms alerts

Online

applications

streamlined

• Build a financially

sustainable &

viable sefa

Maintain cost

efficiency & profitability

FY end profitability ratio %:

Cost to income ratio

(excl grants)

164%

Impairment provision

through income

statement

25%

% of bad debts to book 30%

Growth of loan book 122%

Growth interest &

admin fees

49%

2014/15 Strategic Focus

25

STRATEGIC

OBJECTIVE/

ENABLER

STRATEGIC GOAL

STATEMENT

KEY

PERFORMANCE

AREA

KEY PERFORMANCE

INDICATOR

KEY

PERFORMA

NCE

TARGET

Build a sefa that

meets all legislative,

regulatory & good

governance

requirements

• Ensure an

effectively

governed and

compliant

organisation

Enterprise-wide Risk

Management

Risk framework & policies Annual review

Quantifiable & defined risk

appetite levels

Approved by

Board of

Directors

(BOD)

Build a strong &

effective sefa brand

emphasizing

accessibility to

SMMEs

• Effective

marketing &

promotion

programme to

communicate

product offering

Improve customer

experience

Improve outreach to

partners, stakeholders

& SMMEs

CRM system developed System

developed

% increase in customer

satisfaction levels

60%

Number of events 3

Number of roadshows 6

2014/15 Strategic Focus

Corporate Targets

26

2013/14

2014/15

2015/16

2016/17

2017/18

2018/19

APPROVALS R815m R974m R1 229m R1 439m R1 708m R1 709m

DISBURSEMENT R737.5m R642m R865m R1 011m R1 189m R1 327m

NO. OF JOBS

CREATED 18 311 57 255 79 255 92 420 114 085 118 566

NO. OF SMMES

FINANCED 15 129 37 758 53 001 77 157 77 325 80 431

Corporate Targets - Approvals

27

PRODUCT

2013/14

2014/15

2015/16

2016/17

2017/18

2018/19

DIRECT LENDING R370m R485m R563m R630m R690m R725m

RFIS AND FUNDS R285m R330m R415m R470m R590m R698m

CO-OPERATIVES R20m R6,4m R8,6m R10,8m R16m R21,2m

MICROFINANCE R140m R153m R243m R329m R412m R265m

TOTAL R815m R974m R1 229m R1 439m R1 708m R1 709m

Corporate Targets - Disbursements

28

PRODUCT

2013/14

2014/15

2015/16

2016/17

2017/18

2018/19

Direct Lending R348m R388m R450m R522m R586m R616m

RFIs and Funds R293m R181m R299m R333m R421m R506m

Co-operatives R12m R2,9m R4,3m R5,4 R8m R10,6m

Microfinance R84m R71m R112m R151m R174m R195m

Total R737m R642m R865m R1 011m R1 189m R1 327m

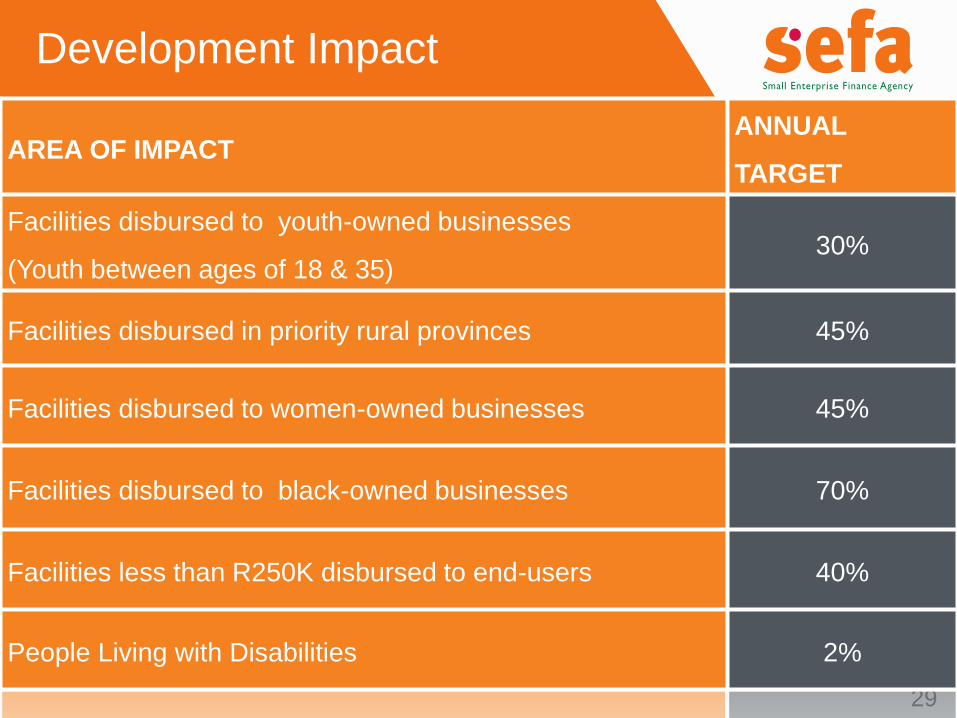

Development Impact

29

AREA OF IMPACT ANNUAL

TARGET

Facilities disbursed to youth-owned businesses

(Youth between ages of 18 & 35) 30%

Facilities disbursed in priority rural provinces 45%

Facilities disbursed to women-owned businesses 45%

Facilities disbursed to black-owned businesses 70%

Facilities less than R250K disbursed to end-users 40%

People Living with Disabilities 2%

Financial Management

30

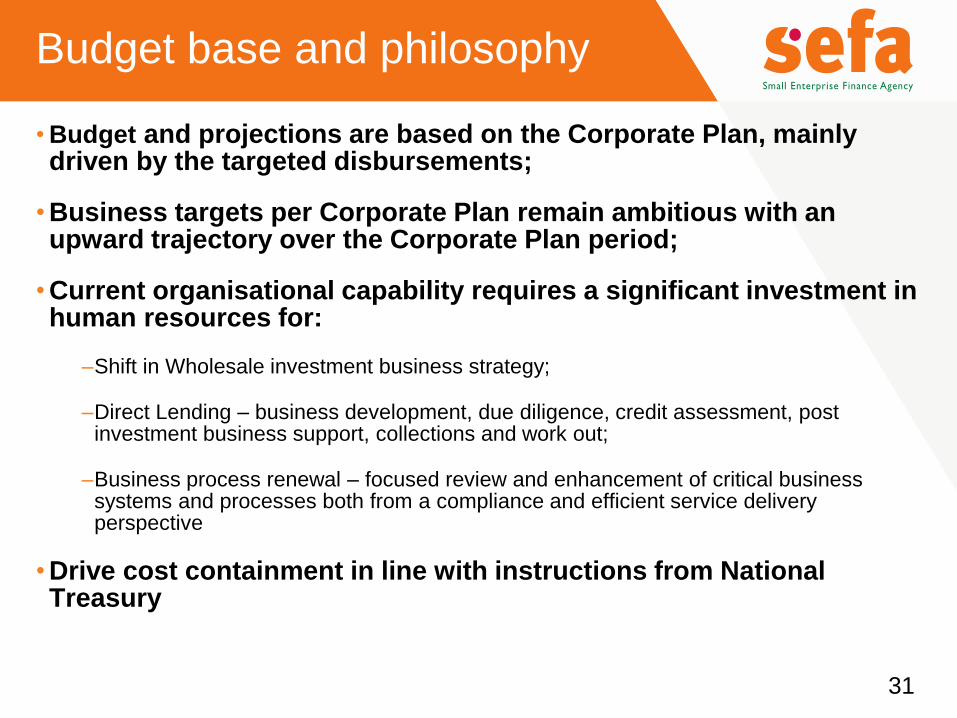

Budget base and philosophy

• Budget and projections are based on the Corporate Plan, mainly driven by the targeted disbursements;

• Business targets per Corporate Plan remain ambitious with an upward trajectory over the Corporate Plan period;

• Current organisational capability requires a significant investment in human resources for:

–Shift in Wholesale investment business strategy;

–Direct Lending – business development, due diligence, credit assessment, post investment business support, collections and work out;

–Business process renewal – focused review and enhancement of critical business systems and processes both from a compliance and efficient service delivery perspective

• Drive cost containment in line with instructions from National Treasury

31

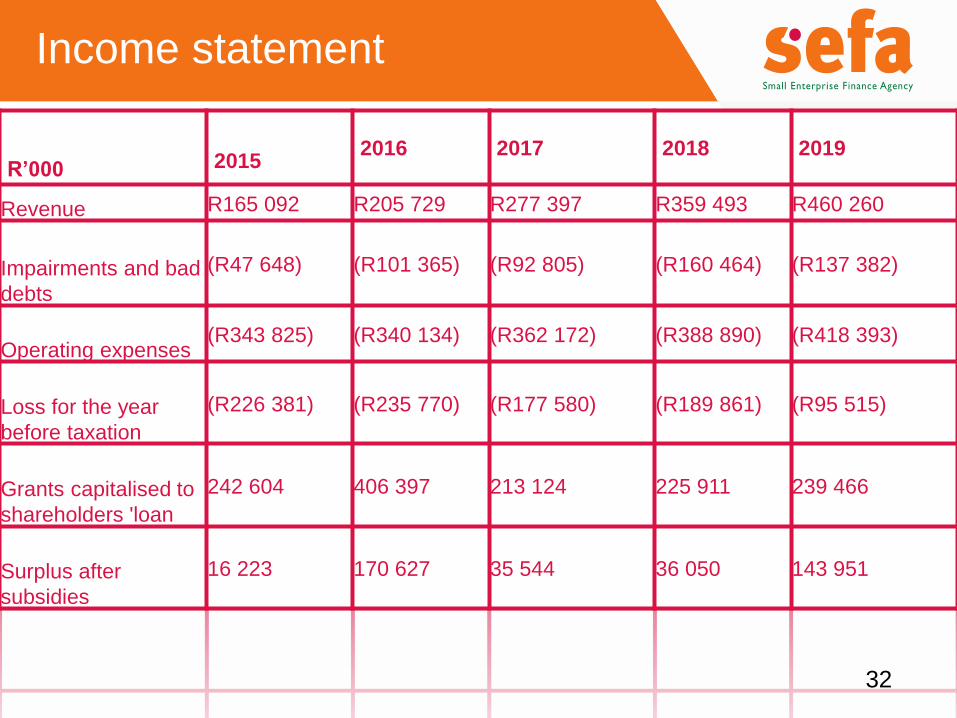

Income statement

R’000

2015 2016 2017 2018 2019

Revenue R165 092 R205 729 R277 397 R359 493 R460 260

Impairments and bad

debts

(R47 648) (R101 365) (R92 805) (R160 464) (R137 382)

Operating expenses (R343 825) (R340 134) (R362 172) (R388 890) (R418 393)

Loss for the year

before taxation

(R226 381) (R235 770) (R177 580) (R189 861) (R95 515)

Grants capitalised to

shareholders 'loan

242 604 406 397 213 124 225 911 239 466

Surplus after

subsidies

16 223 170 627 35 544 36 050 143 951

32

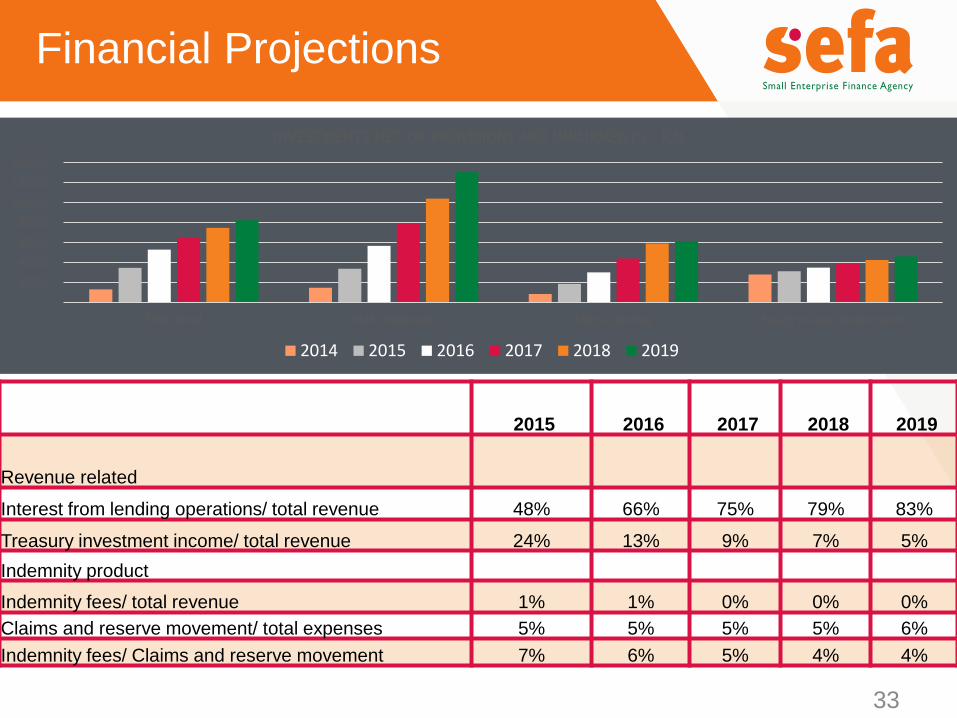

Financial Projections

2015 2016 2017 2018 2019

Revenue related

Interest from lending operations/ total revenue 48% 66% 75% 79% 83%

Treasury investment income/ total revenue 24% 13% 9% 7% 5%

Indemnity product

Indemnity fees/ total revenue 1% 1% 0% 0% 0%

Claims and reserve movement/ total expenses 5% 5% 5% 5% 6%

Indemnity fees/ Claims and reserve movement 7% 6% 5% 4% 4%

33

-

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

SME Retail SME Wholesale Micro Lending Equity related investments

INVESTMENTS NET OF PROVISIONS AND IMPAIRMENTS - R'M

2014 2015 2016 2017 2018 2019

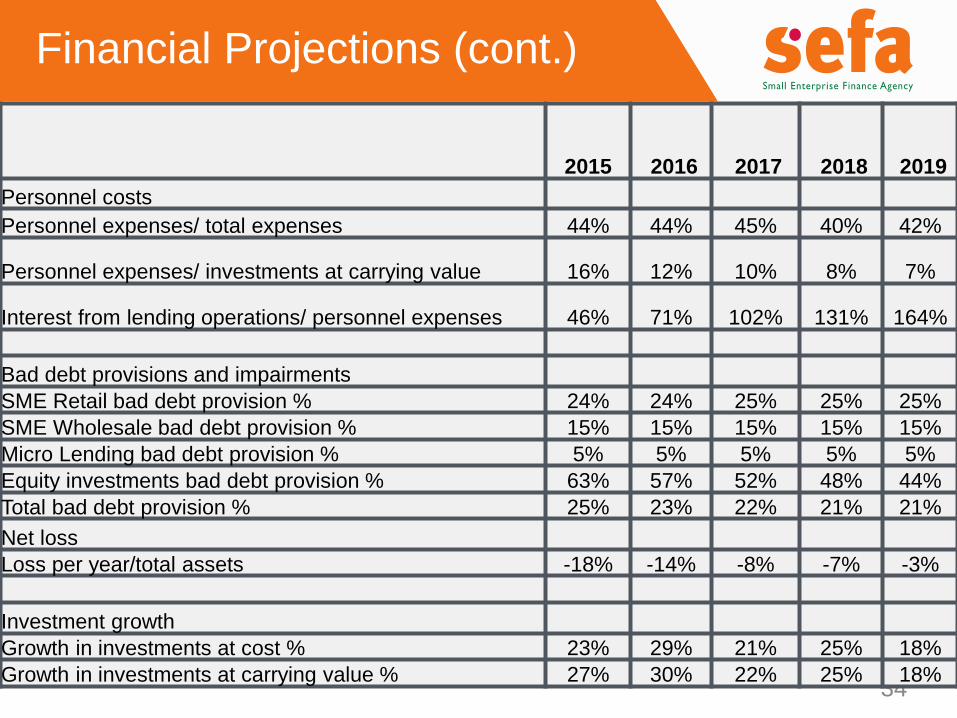

Financial Projections (cont.)

34

2015 2016 2017 2018 2019

Personnel costs

Personnel expenses/ total expenses 44% 44% 45% 40% 42%

Personnel expenses/ investments at carrying value 16% 12% 10% 8% 7%

Interest from lending operations/ personnel expenses 46% 71% 102% 131% 164%

Bad debt provisions and impairments

SME Retail bad debt provision % 24% 24% 25% 25% 25%

SME Wholesale bad debt provision % 15% 15% 15% 15% 15%

Micro Lending bad debt provision % 5% 5% 5% 5% 5%

Equity investments bad debt provision % 63% 57% 52% 48% 44%

Total bad debt provision % 25% 23% 22% 21% 21%

Net loss

Loss per year/total assets -18% -14% -8% -7% -3%

Investment growth

Growth in investments at cost % 23% 29% 21% 25% 18%

Growth in investments at carrying value % 27% 30% 22% 25% 18%

sefa Contact Details

•sefa National Call

Centre : 0860 007 332

•E-mail: [email protected]

•www.sefa.org.za

35

36