securing financing for real estate acquisitions · pdf fileforeclosure. family offices and...

TRANSCRIPT

Securing Financing for Real Estate Acquisitions

By Richard C. Wilson

Sponsored by Family Office Club

As rates continue to change, cost of debt can dramatically effect the overall viability of a project and the financial performance of a property. Securing the least expensive financing can prove to be the difference between a successful acquisition and a foreclosure.

Family offices and other experienced real estate investors take advantage of agency financing, creative structures, and competitively-sourced loans to boost the NOI of properties.

Why Financing Matters

LTV is a key number for both borrowers and lenders because it expresses the ratio between the loan and the value of the asset being acquired.

Example: Property has a value of $10,000,000; Borrower seeking loan of $8,000,000 with an additional $2,000,000 offered from the Borrower’s own money.

LTV ratio = Loan Amount Property’s Value or Purchase Price

Loan-To-Value (LTV)

Note: Recourse vs. Non-Recourse

Non-Recourse Loan: Preferred by borrowers because the lender can only seize the assets posted as collateral. Because this feature is advantageous to the borrower, the lender may charge a higher interest rate to compensate for the greater risk to his capital.

Recourse Loan: Preferred by lenders because, in the event of a default, the lender is able to seize not only the collateral but he can also pursue other means to be made whole.

So, if a borrower defaults, the lender will recover the collateral and then go after the borrower’s other assets and even sue to recover other funds such as future wages.

Lender’s Perspective

Lenders are interested in lending to borrowers that have a strong credit history (deals closed, large portfolio, pedigree) and where the loan is secured by a safe cash-flowing asset with minimal risk.

Seeking: • Low default risk• Low loan-to-value ratio• High value of collateral• High caliber borrower or sponsoring firm• High interest rate (as long as not so high to produce

default)• Recourse (if possible)• Capacity (ability of lender to make payments)• High NOI

Lender’s Perspective

What commercial mortgage lenders look for:• Cash-flow• Detailed financials showing T12 NOI and previous year NOI• Occupancy rate• Rent rolls• Details on the property (address, offering memo, history)• Details on the borrower (experience, credit history, how many

deals have you done?)• Sponsor’s existing portfolio and net worth/AUM• Desired loan and Loan to Value ratio• Timeline

Lender’s Perspective

How to secure a stronger loan offer:• Select properties in strong rental markets or where lenders are

comfortable. I.e. Houston in 2014 when the oil industry was in decline vs. Nashville where rents and property values have been appreciating.

• Don’t punch above your weight; select a property for which the loan is less than your net worth or be prepared to have a co-sponsor/co-investor.

• Maintain a healthy liquidity cushion (10+% post closing)

Strong Geographical Areas

Note: this is based solely on Bigger Pockets report and does not represent a Recommendation or suggestion as to the value of any single market or prospects for Returns or performance.Source: https://www.biggerpockets.com/renewsblog/2016-investor-market-index/

Weaker Geographical Areas

Note: this does not necessarily represent the value of properties within these markets,only that certain markets have either appreciated less or performed worse relative to other markets.Source: https://www.biggerpockets.com/renewsblog/2016-investor-market-index/

Multifamily

The vast majority of multifamily acquisitions financed by Fannie Mae are for conventional and cooperative housing but manufactured, senior, and student housing make up a not insignificant share.

Multifamily

f

Multifamily

Fannie Mae

Fannie Mae is one of the primary government participants in the mortgage market.

➢ Government Sponsored Enterprise (GSE) lender➢ Purchases and guarantees mortgages through the secondary market. ➢ Creates liquidity for banks and other lenders to continue underwriting

mortgages.➢ Strict criteria for loans to be eligible for Fannie Mae guarantee/purchase

Property Types:

• Conventional multifamily• Conventional seniors housing/healthcare• Student housing• Military housing• Manufactured housing community• Cooperative multifamily housing project• Multifamily affordable housing & low-income housing tax credit

Fannie Mae

Possible Loan Structures for Fannie Mae mortgage backed securities

• Fixed-rate and adjustable-rate• Balloon payments

• At the end of the loan period. • Fixed-rate multifamily mortgage loans usually have final balloon

maturities of 5, 7, 10, 12, 15, 18, 25, or 30 years. • The adjustable-rate multifamily loans usually have final balloon

maturities of 5, 7, or 10 years.• Fully amortizing• Partial and full-term interest only • The most common FNMA DUS structure is a 10 year balloon with 9.5

years yield maintenance (according to PNC).

Fannie Mae (DUS Model)

Fannie Mae (DUS Model)

Source for Fannie Mae info and graphics: https://www.fanniemae.com/content/fact_sheet/multifamily-business-information.pdf

Fannie Mae CriteriaEligible Borrowers and Sponsors

• Credit worthy, single-asset U.S. based borrower.• Foreign borrowers can have ownership interests but need to structure properly

Loan Terms• Ranges from 5-30 years but 5/7/10 year mortgages are most common

Amortization• Up to 30 years

LTV• Max is 80% LTV or 1.25x debt coverage

Recourse vs. Non-recourse• Non-recourse is the norm for most loans > $1.5m.

Stabilization• Most FNMA conforming loans have 90% occupancy. • Minimum vacancy and collection loss is 5%

Reports• Need property appraisal, phase 1 environmental impact assessment, physical

needs assessment.Rate Lock

• 30 to 90 day commitments. Option for Extended Rate Lock feature so borrower can lock in rate of 45 to 365 days ahead of closing.

Prepayment penalty• Prepayable but subject to defeasance, yield maintenance, or fixed %

prepayment premiums except the 90-day period to maturity. Typical prepayment protection used is yield maintenance.

Freddie Mac

Freddie Mac has a very similar mission to Fannie Mae with the largest differencebeing that Freddie Mac purchases loans from smaller thrift banks instead of just the large commercial banks that Fannie Mae works with.

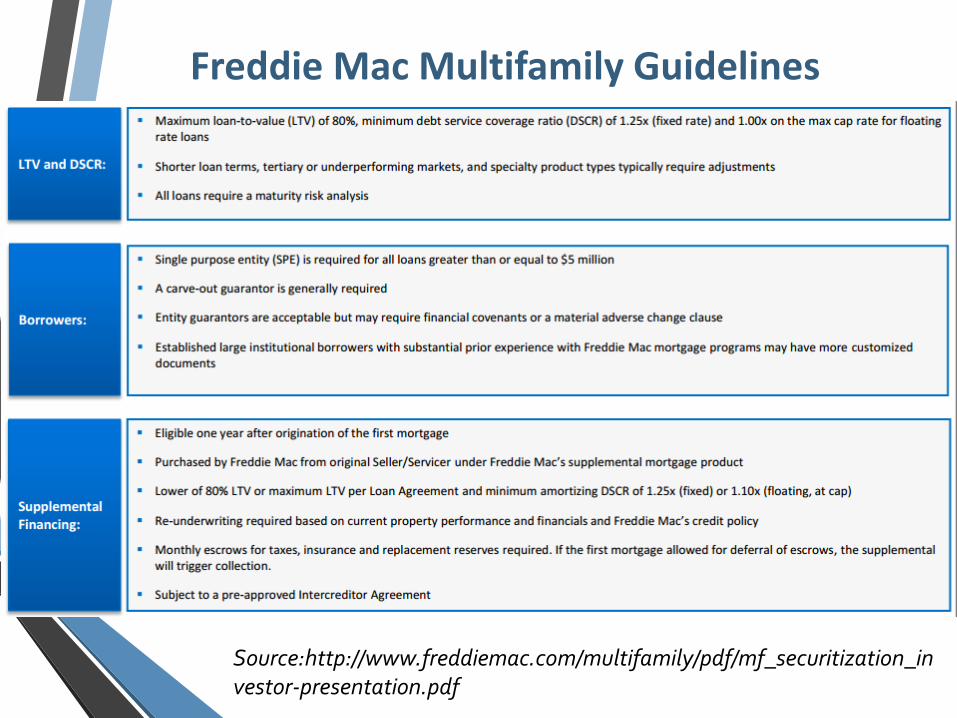

Freddie Mac Multifamily Guidelines

Freddie Mac Multifamily Guidelines

Source:http://www.freddiemac.com/multifamily/pdf/mf_securitization_investor-presentation.pdf

Freddie Mac Multifamily Guidelines

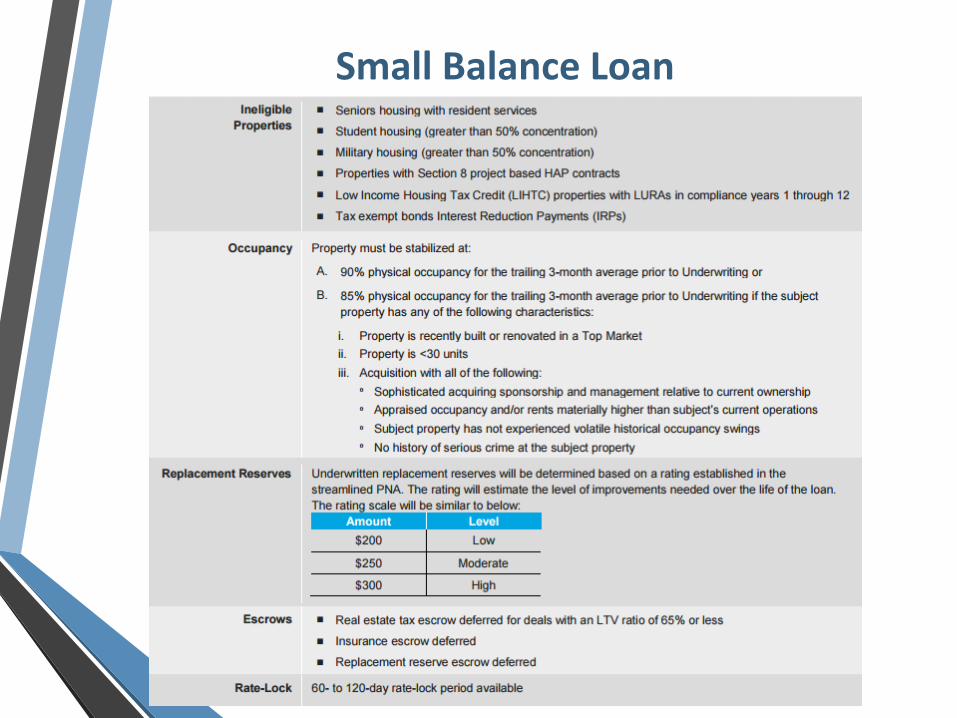

Small Balance LoanSmall Balance Loans is a program from Freddie Mac that applies to smaller loan amounts of $1 – 5m for acquisition or refinancing of multifamily housing.

Small Balance Loan

FHA / HUD Financing

The Federal Housing Administration (FHA), a division of the Department of Housing and Urban Development (HUD), acts as an insurer of certain loans so that lenders can require lower down payments, reduce closing costs, and ease credit qualification requirements.

FHA / HUD Guidelines

Borrower• Must be single asset or special purpose entity; either non-profit or for profit.

Eligible Properties• Affordable housing, subsidized housing, cooperatives, and other low-income

housing. Construction or rehab of a property must have been done 3+ years before application to HUD. Student housing must be in line with market rate multifamily comps and cash flows can’t assume multiple rents from one unit.

Non-RecourseLending limits vary by state & housing types & county in which the property is located.Interest Rate

• Subject to market conditionsMortgage Insurance Premium

• 1% due to HUD at closing and 0.6% annually going forward.

FHA / HUD Example

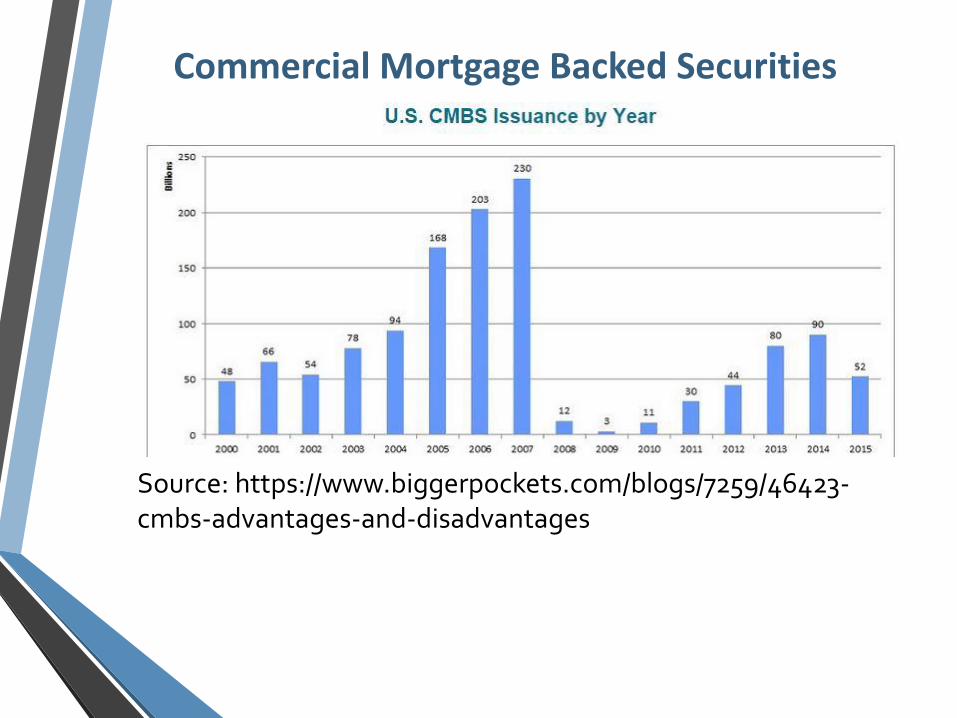

Commercial Mortgage Backed Securities

Commercial Mortgage-Backed Securities (CMBS) are bonds that are backed by commercial mortgages. Typically, these securities are backed by a pool of mortgages with different tranches separated by credit risk, yield, payment priority.

CMBS loans finance: • Apartment buildings; • Hotels;• Shopping malls & retail; • Office towers; • Warehouses;• Stabilized multifamily• Self-storage properties

Commercial Mortgage Backed Securities

Source: https://www.biggerpockets.com/blogs/7259/46423-cmbs-advantages-and-disadvantages

CMBS Benefits

Most CMBS loans are held by commercial banks and other institutional lenders.

Why CMBS? As a CMBS borrower you may be able to negotiate:• Lower overall cost of financing• Lower fixed rate for 10 year mortgage• Flexible amortization schedule, potential for initial

interest-only period (as much as 30 years)• Non-recourse (no personal liability)• Up to 75% LTV• Allows for cash-out refinancings (allows to take out

equity and avoid capital gains tax)• Minimums of $3m+ and no maximum typically

CMBS Disadvantages

Why not CMBS? Borrowers may choose to avoid CMBS loans because:

• Pre-set loan structure, can be hard to fit in CMBS box

• Prepayment: lockout for 2 years post-securitization then prepayment penalties apply.

• Defeasance can be tough to navigate and expensive with penalties.

• Volatility in pricing as spreads to Treasury change

CMBS Expenses

An example of how CMBS could potentially save vs. balance sheet loans, even withcomparatively higher lender loan fees and expenses. Source: Saratoga Springs Capitalhttp://rew-online.com/2015/09/03/benefits-of-cmbs-loans-today/

Commercial Mortgage

1. Rates are currently at historical lows; many market observers expect the new administration to implement tighter monetary policy.

2. Despite an increase to the short-term funds rate by the Federal Reserve, few expect rates to climb dramatically in short term but over the longer term we could see a major change in the cost of financing real estate.

Mezzanine

Combination of debt and equity financing

Lender typically has option to convert to equity stake in the company if loan payments are late or default.

Short-term, minimal/no collateral, and subordinate to more senior debtholders. Thus, investors charge high interest rates in 15%+ range making this an expensive form of capital.

BridgeShort-term, bridges the gap between initial need and longer-term, cheaper financing.

Provides borrower with immediate funding source to cover current obligations and secure long-term debt agreement. May be used to finance operations until the close of a round of funding.

Duration: As short as a couple of months, typically a year or less.

Used to bridge the gap in a private equity buyout until the acquisition is completed.

Key Biscayne, FL

Our Offices

Visit Our Offices

Richard C. WilsonFounder - Wilson Holding Company

Direct Line: (503) 922-181177 Harbor Drive Suite #76

Key Biscayne, FL [email protected]

Theodore O’BrienManaging Partner – Multifamily Lending Partners

Direct Line: (305) 677-333877 Harbor Drive Suite #76

Key Biscayne, FL [email protected]

Disclaimer