sectoral and skills gaps analysis report2 - tamkeen and skills gaps analysis... · tli-ap the...

TRANSCRIPT

Sectoral and Skills Gaps Analysis

Skills Gaps Research Study: Report 2

June 2009

Report to Tamkeen, Kingdom of Bahrain

Disclaimer

INFORMATION ON WHICH THE SURVEY RESULTS ARE BASED IS REPRESENTATIVE OF THE BEST INFORMATION AVAILABLE AT THE TIME OF THE STUDY’S FIELDWORK, CONSULTATIONS AND PUBLICATION. ALTHOUGH GREAT CARE WAS TAKEN TO ENSURE DATA QUALITY, LABOUR FUND (TAMKEEN) DOES NOT GUARANTEE THE ACCURACY OR COMPLETENESS OF THE SURVEY OR OF ANY INFORMATION PRESENTED HERE.

NEITHER THE LABOUR FUND (TAMKEEN) NOR ANY AGENCY THEREOF, NOR ANY OF THEIR EMPLOYEES NOR ANY OF THEIR CONTRACTORS, MAKES ANY WARRANTY, EXPRESS OR IMPLIED, OR ASSUMES LEGAL LIABILITY OR RESPONSIBILITY FOR THE ACCURACY, COMPLETENESS OR ANY THIRD PARTY’S USE OF THE INFORMATION CONTAINED IN THIS DOCUMENT.

The Allen Consulting Group ii

The Allen Consulting Group Pty Ltd

ACN 007 061 930, ABN 52 007 061 930

M elbourne

Level 9, 60 Collins St

Melbourne VIC 3000

Telephone: (61-3) 8650 6000

Facsimile: (61-3) 9654 6363

Sydney

Level 12, 210 George St

Sydney NSW 2000

Telephone: (61-2) 8272 5100 Facsimile: (61-2) 9247 2455

C anberra

Empire Chambers, Level 2, 1-13 University Ave

Canberra ACT 2600

GPO Box 418, Canberra ACT 2601

Telephone: (61-2) 6204 6500 Facsimile: (61-2) 6230 0149

Perth

Level 21, 44 St George’s Tce

Perth WA 6000

Telephone: (61-8) 6211 0900 Facsimile: (61-8) 9221 9922

Online

Email: info@ allenconsult.com.au

Website: www.allenconsult.com.au

Suggested citation for this report: Allen Consulting Group 2009, Skills Gaps Research Study: Report 2 — Sectoral and Skills Gaps Analysis, Canberra, Australia.

Disclaimer: While the Allen Consulting Group endeavours to provide reliable analysis and believes the material it presents is accurate, it will not be liable for any claim by any party acting on such information.

© The Allen Consulting Group 2009

The Allen Consulting Group iii

Contents

Glossary 1

Chapter 1 4 Introduction 4

1.1 Background to the study 4 1.2 Skills Gaps Research Study 6 1.3 Methodology for this report 8

Chapter 2 11 Bahrain’s labour market and skills 11

2.1 Bahrain’s labour market 11 2.2 Sectors of the Bahrain economy 17

Chapter 3 19 Views from graduates and education institutions 19

3.1 Overview 19 3.2 Graduate survey analysis 19 3.3 Training institution survey analysis 22 3.4 Employer survey — results by size of employer 25

Chapter 4 28 Future solutions for Bahrain’s labour force 28

4.1 Overview 28 4.2 Key findings — public services 28 4.3 Key findings — infrastructure 30 4.4 Key findings — trade and other services 33 4.5 Conclusions 37

Chapter 5 40 Education 40

5.1 Characteristics of the sector 40 5.2 Education in Bahrain 43 5.3 Skills formation in the sector 47 5.4 International trends in education 50 5.5 The future labour and skills needs 52 5.6 Skills gaps analysis 64 5.7 SWOT snapshot 66 5.8 Future skills issues 67

The Allen Consulting Group iv

Chapter 6 69

Health 69 6.1 Characteristics of the sector 69 6.2 Health in Bahrain 73 6.3 Skills formation in the sector 74 6.4 International trends in health 75 6.5 The future labour and skills needs 78 6.6 Skills gaps analysis 87 6.7 SWOT snapshot 88 6.8 Future skills issues 89

Chapter 7 91 Public Administration 91

7.1 Characteristics of the sector 91 7.2 Public administration in Bahrain 92 7.3 International trends in public sector skills and skills needs 98 7.4 The future labour and skills needs 99 7.5 Skills gaps analysis 109 7.6 SWOT snapshot 110 7.7 Future skills issues 111

Chapter 8 113 Construction 113

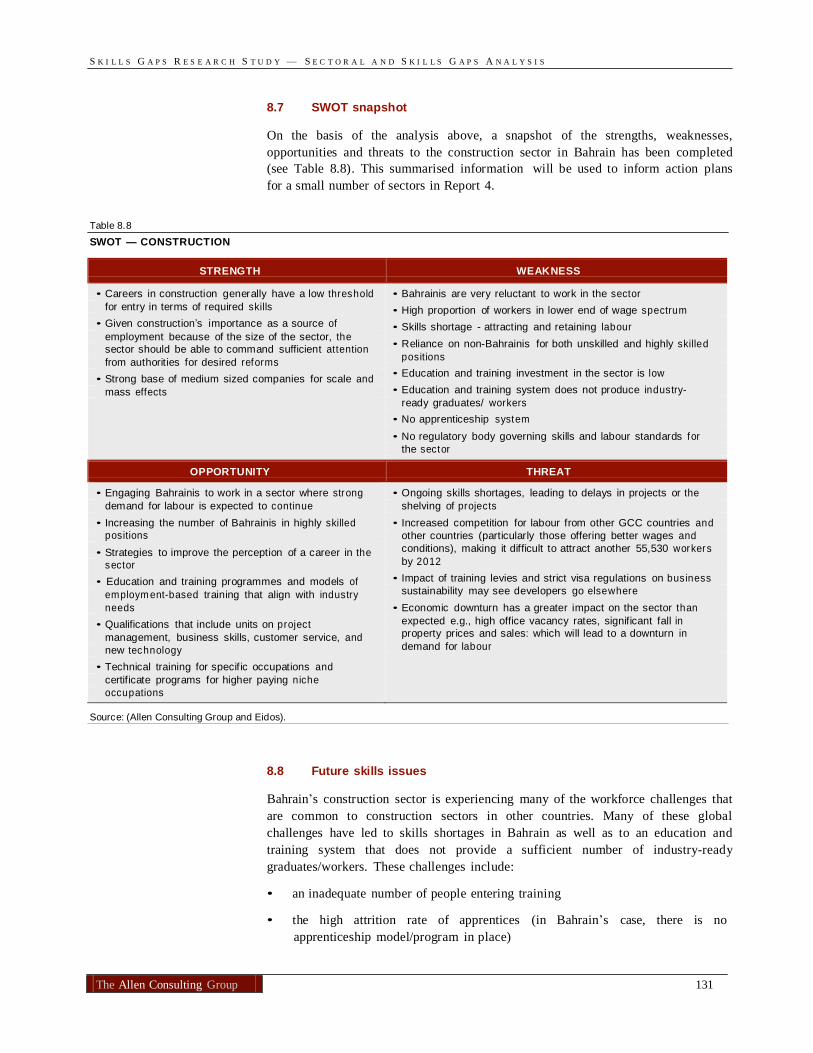

8.1 Characteristics of the sector 113 8.2 Construction in Bahrain 115 8.3 Skills formation in the sector 116 8.4 International trends in construction 117 8.5 Future labour and skills needs 119 8.6 Skills gaps analysis 129 8.7 SWOT snapshot 131 8.8 Future skills issues 131

Chapter 9 133 Information Technology 133

9.1 Characteristics of the sector 133 9.2 Information and communications technology in Bahrain 135 9.3 IT trends in Bahrain and the GCC 137 9.4 International trends in IT 140 9.5 The future labour and skills needs 140 9.6 Skills gaps analysis 151 9.7 SWOT snapshot 152 9.8 Future skills issues 152

Chapter 10 154

The Allen Consulting Group v

Telecommunications 154 10.1 Characteristics of the sector 154 10.2 Telecommunications in Bahrain 159 10.3 International trends in telecommunications 160 10.4 Future labour and skills needs in the telecommunications sector 162 10.5 Skills gap analysis 173 10.6 SWOT snapshot 174 10.7 Future skills issues facing the telecommunications sector 174 10.8 175

Chapter 11 176 Transport and logistics 176

11.1 Characteristics of the sector 176 11.2 Transport and logistics in Bahrain 180 11.3 Skills formation in the sector 180 11.4 International trends in logistics 181 11.5 The future labour and skills needs 184 11.6 Skills gaps analysis 192 11.7 SWOT snapshot 194 11.8 Future skills issues 194

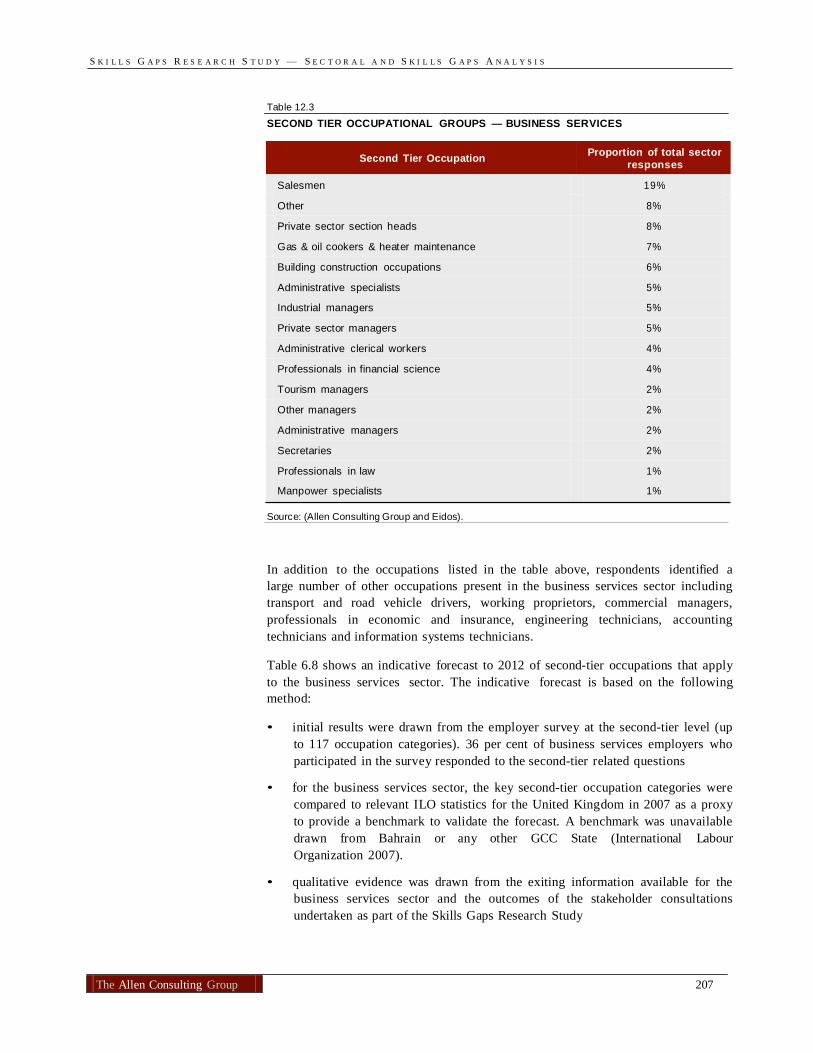

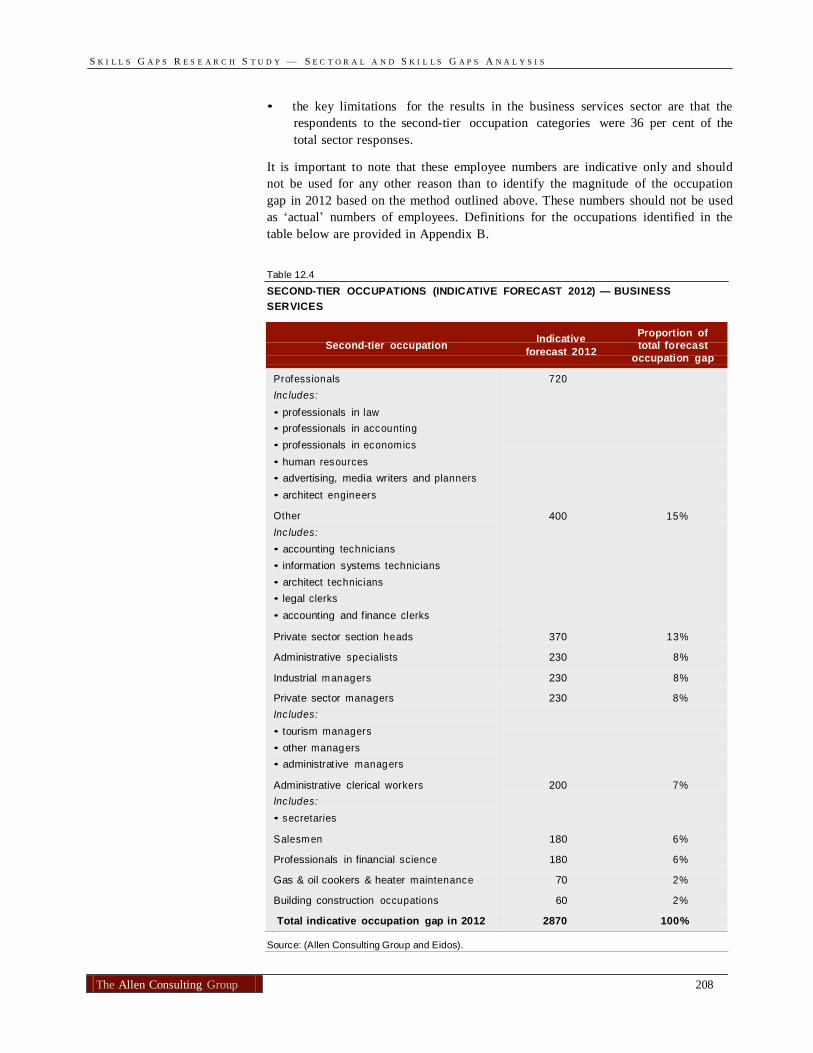

Chapter 12 197 Business services 197

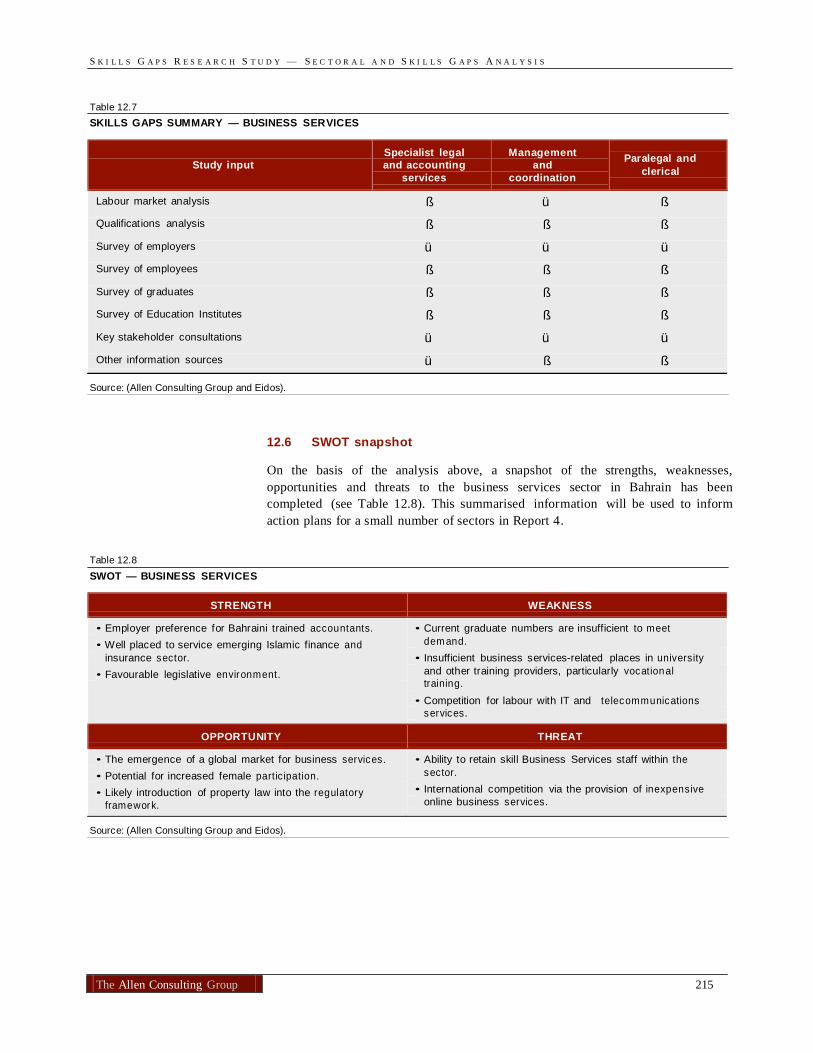

12.1 Characteristics of the sector 197 12.2 Business services in Bahrain 198 12.3 Skills formation in the sector 199 12.4 International trends in business services 201 12.5 The future labour and skills needs 202 12.6 SWOT snapshot 215 12.7 Future skills issues 216

Chapter 13 217 Manufacturing 217

13.1 Characteristics of the sector 217 13.2 Manufacturing in Bahrain 220 13.3 Skills formation in the sector 220 13.4 International trends in manufacturing 223 13.5 Future labour and skills needs 225 13.6 Skills gaps analysis 235 13.7 SWOT snapshot 236 13.8 Future skills issues 237

The Allen Consulting Group vi

Chapter 14 238

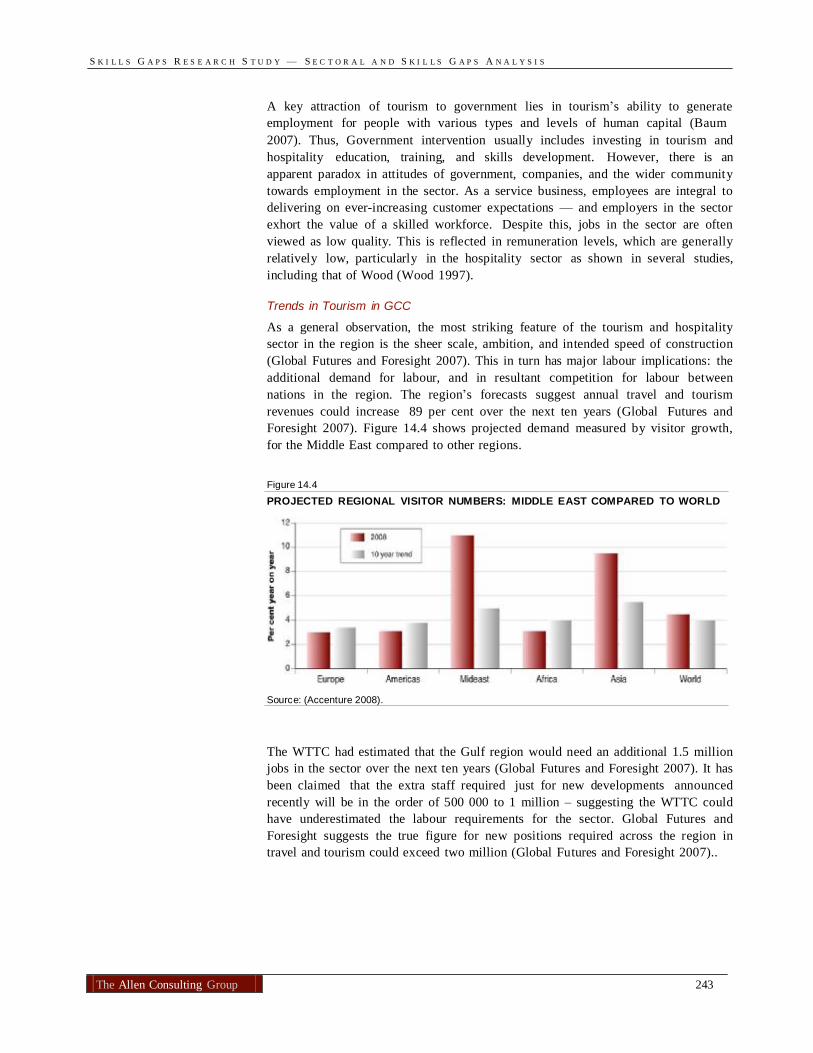

Tourism and hospitality 238 14.1 Characteristics of the sector 238 14.2 Tourism in Bahrain 241 14.3 International trends in tourism and hospitality 242 14.4 The future labour and skills needs 244 14.5 Skills gaps analysis 255 14.6 SWOT snapshot 256 14.7 Future skills issues 257

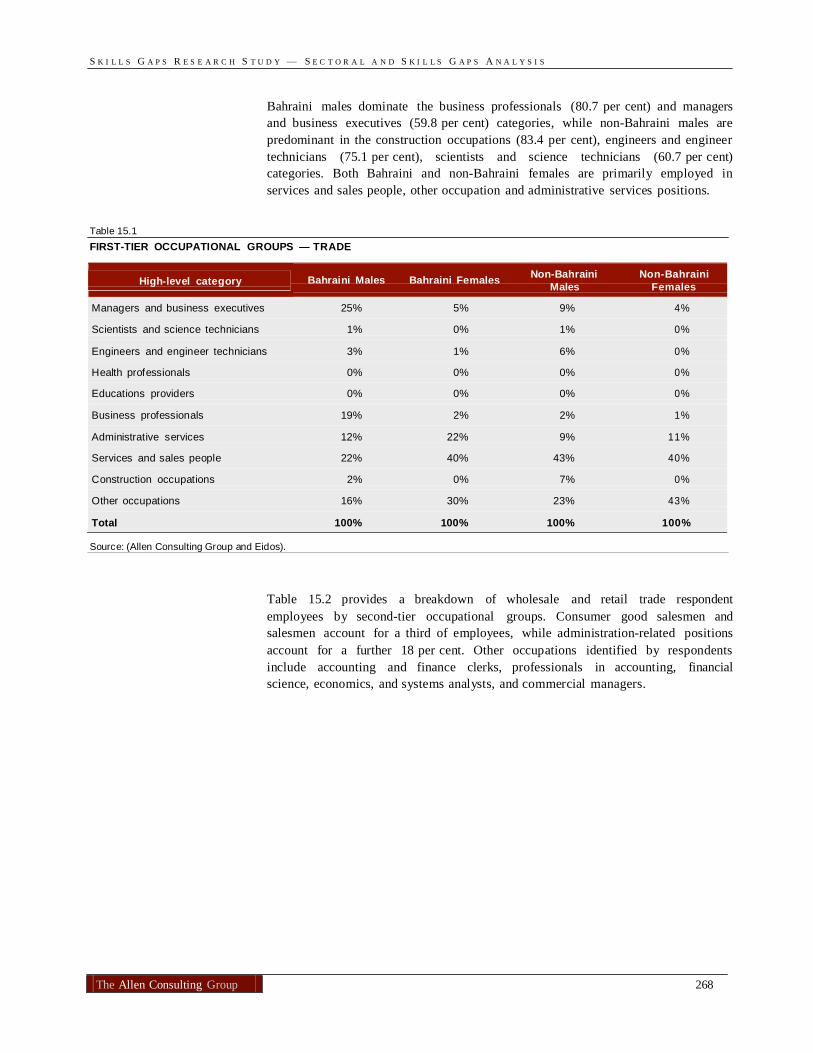

Chapter 15 258 Trade 258

15.1 Characteristics of the sector 258 15.2 International trends in trade 263 15.3 Future labour and skills needs 265 15.4 Skills gaps analysis 275 15.5 SWOT snapshot 277 15.6 Future skills issues 278

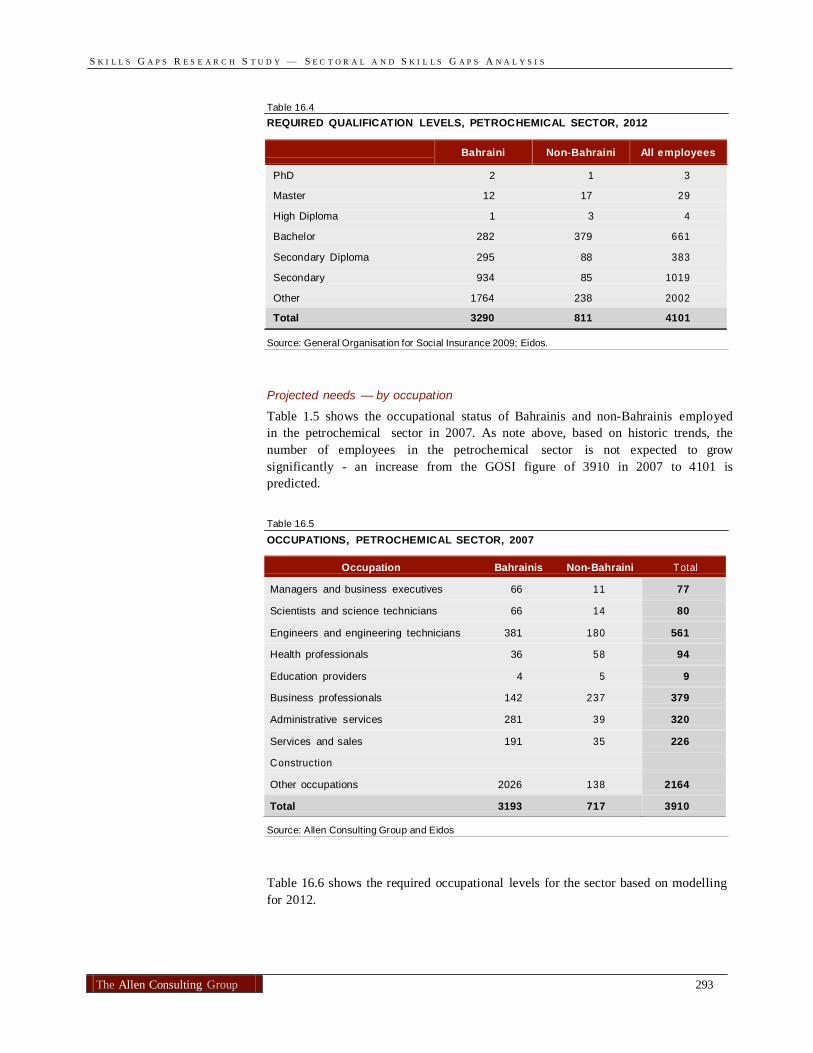

Chapter 16 280 Petrochemical Sector 280

16.1 Characteristics of sector 280 16.2 Petrochemicals in Bahrain 282 16.3 International trends in petrochemicals ⌂ 16.4 Future labour and skills needs 290 16.5 Skills gaps analysis 298 16.6 Future pressures facing the petrochemical labour market 299 16.7 Possible solutions for Bahrain 301

Chapter 17 303 Banking and finance 303

17.1 Characteristics of the sector 303 17.2 Skills formation in the sector 306 17.3 International trends in finance and banking 310 17.4 Employer survey results 317 17.5 Skills gap analysis 320 17.6 Future labour market and skills issues and possible solutions 324 17.7 325

Appendix A 326 Survey methodology 326

A.1 Baseline study review 326 A.2 Survey design 326 A.3 Data collection methodology 327

The Allen Consulting Group vii

Chapter 14 238

A.4 Employer survey 328

The Allen Consulting Group vii

A.5 Employee survey 331 A.6 Education and training providers survey 331 A.7 Graduates Survey 332

Appendix B 334 Second-tier occupation definitions 334

B.1 Second-tier occupation definitions 334

Appendix C 350 Labour market analysis — information sources 350

C.1 Sources used as part of the labour market analysis 350

Appendix D 351 References 351

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 1

Glossary

ACCA Association of Chartered Certified Accountants APICORP Arab Petroleum Investment Corporation ASRY Arab Shipbuilding and Repair Yard Company BAFCO Bahrain Aviation Fuelling Company BANAGAS Bahrain National Gas Company BAPCO Bahrain Petroleum Company BAS Bahrain Airport Services BATELCO Bahrain Telecommunications Company BCCI Bahrain Chamber of Commerce and Industry BIBF Bahrain Institute of Banking and Finance BIC Bahrain International Circuit BIHM Baisan Institute of Hospitality Management BIHR Bahrain Institute of Hospitality and Retail BIRD Bahrain International Retail Development BLZ Bahrain Logistics Zone BTI Bahrain Training Institute CAT Certified Accounting Technicians CEPIS Council of European Professional Informatics Societies CIA Central Intelligence Agency CIO Central Informatics Organisation CMA Certified Management Accountants CPHC Council of Professors and Heads of Computing CSB Civil Service Bureau CT Communications Technology EDB Economic Development Board FMC Fixed Mobile Convergence GCC Gulf Cooperation Council GDP Gross Domestic Product GOSI General Organization for Social Insurance GPIC Gulf Petroleum Industries Company HCD Human Capital Development HR Human Resources HRDF Human Resources Development Fund IATA International Air Transport Association ICSB Independent Civil Service Bureau IEA International Energy Agency ILO International Labour Organization IMF International Monetary Fund IT Information Technology KSA Kingdom of Saudi Arabia LMRA Labour Market Regulation Authority LPG Liquid Petroleum Gas LPI Logistics Performance Indicator MOU Memo of Understanding MTM Manama Textile Mills

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 2

NOGA National Oil and Gas Authority NRI National Readiness Index OAPEC Organisation of Arab Petroleum Exporting Countries OPEC Organization of Petroleum Exporting Countries PET Preliminary English Test PRM Professional Risk Managers PTTEP National Oil Company of Thailand RCSI Royal College of Surgeons, Ireland SABIC Saudi Basic Industries Corporation SEM Structural Equation Modelling TLI-AP The Logistics Institute – Asia Pacific TRA Telecommunications Regulation Authority UAE United Arab Emirates VEGA Volunteers for Economic Growth Alliance WHO World Health Organization WTTC World Travel and Tourism Council

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 3

Part 1

Sectoral and skills gaps analysis — Overview

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 4

Chapter 1

Introduction

It should be noted by the reader that the data for the Skills Gaps Research Study was collected during 2008 with the conclusions being finalised in June 2009. This data is relevant to each of the four reports in the series of the Skills Gaps Research Study.

1.1 Background to the study

Tamkeen

Tamkeen (formerly Labour Fund) was founded in 2006 with the primary objectives of developing the private sector and making Bahrainis the preferred choice for employers. Tamkeen’s goal is to create high-value added jobs for Bahrainis.

Tamkeen’s strategy focuses on:

• capitalising and developing value added Bahraini talents and skills in

rewarding careers

• supporting the development and attraction of new and emerging industries

• enhancing and leveraging existing industries.

More recently Bahrain has taken vital steps towards comprehensive labour reform aimed to develop its human capital, support the private sector and liberalise and improve inherent market systems, standards or policies.

Successful reform of Bahrain’s labour market will affect the whole economy. In particular, it will raise Bahraini living standards by challenging private and public sector establishments to improve employment services, policies and standards and the working conditions within Bahrain.

Economy in brief

Bahrain has a long history as a regional centre for trade and commerce. In more recent times, since the 1930s when oil was discovered, the country’s economic prosperity has been based largely on oil revenues. These have been the main contributors to national income over the past half-century. Oil revenues have enabled development of extensive, high quality national infrastructure, and allowed the government to provide Bahraini citizens with services such as free education and free or very low cost health care, with minimal taxation. More recently, other industry sectors — notably banking and finance — have become increasingly important.

Bahrain’s policy makers have identified the need for longer-term investment outside the oil sector, for two main reasons.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 5

Firstly, there are the dangers of natural resource income distorting patterns of economic development. Secondly, Bahrain’s oil resources are limited, and the government has prudently sought to develop a strategy for a future where the country will not be able to rely on oil as the major source of national income. Current economic development strategies and initiatives aim to mitigate the potentially significant impacts of this situation. Prominent among these to date, has been the successful effort to develop Bahrain as a regional provider of financial services and establish its position as a leader in Islamic banking and financial services.

Bahrain’s economic diversification strategy, shifting focus to non-oil sectors and industrial and commercial success, has been making notable progress over the last two decades. As a result, 75 per cent of Bahrain’s Gross Domestic Product (GDP) in 2007 was attributable to non-oil sectors(Central Informatics Organization 2008).

Among the economic successes of the nation, there remain some key issues that have the potential to act as barriers to future economic diversification. An example is that income inequality is high compared to other developed nations with few middle-income households and many low income households.

In addition, the labour market is expected to change significantly over the coming decade. These changes include:

• new Bahrainis will enter the labour market, many of whom will be recent

graduates (from either high-school or post-secondary studies)

• an increasing number of Bahraini women will enter the labour market

• those currently unemployed and lacking skills to enter the labour market will improve their skill base in order to participate in the workforce (Economic Development Board 2004).

Continuing the aim of economic diversification, Bahrain’s Economic Development Board (EDB) has been focussed on a sustainable future for Bahrain. In 2004, the EDB launched a comprehensive National Strategy for Bahrain to ensure future sustainability. This strategy aims to:

• re-capture Bahrain’s leadership position as the pre-eminent economy in the

region

• become the preferred country within the region to create and grow a business, by both nationals and foreigners

• achieve a more than two fold increase in income per capita by 2015 (Economic

Development Board 2005).

The strategy consists of three components, which are outlined in Box 1.1.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 6

Box 1.1 COMPONENTS OF THE NATIONAL STRATEGY FOR BAHRAIN

Enabling the private sector: • the removal of barriers to growth such as access to capital, land, judicial and legal

infrastructures • specific sector initiat ives to accelerate growth in strategic sectors • dedicated Small Medium Enterprise (SME) initiative and investment promotion. Transforming government: • reducing red tape • moving from owner-operator to facilitator • creating a modern civil service. Investing in people: • labour market ref orm • education system reform.

Source: (Economic Development Board 2005).

The reforms aim to ensure that the private sector is the driver of future growth in Bahrain and that Bahrainis are the employees of choice for this growing private sector (Economic Development Board 2005).

Bahrain has made a strong investment in education, skills and diversification. There has been a rapid increase in educational standards since the 1980s, and at the same time a strong increase in the size and value of the services sector. However, the reliance on foreign workers to address the shortage of skilled labour during a period of rapid growth, perpetuated by mismatches between the profile of skills possessed by Bahraini nationals and those required in the labour market, is a significant issue to be addressed.

Economic observers (including the United Nations, IMF and others) have commented on the importance of resource rich nations investing in human capital. Bahrain has adopted a far-sighted program to do exactly this. This Skills Gaps Research Study is one element of that broader strategy.

1.2 Skills Gaps Research Study

Tamkeen has commissioned the Allen Consulting Group to conduct a comprehensive study to analyse current skills in Bahrain’s labour market, as well as future and emerging skills requirements, and to assess any current or projected gaps and needs.

The study aims to build on reforms in place and improve the quality and quantity of skills being developed, in order to ensure that Bahrain maintains a strong competitive economy and high quality of life.

The project will provide an information base to underpin strategies to improve labour force participation, and responsiveness to the demand for skills using a flexible, market based approach. The objectives of this project are outlined in Box 1.2.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 7

Box 1.2 OBJECTIVES FOR THE SKILLS GAPS RESEARCH STUDY

1. To establish a detailed understanding of the current composition of the Bahraini

workforce — the deliverable at this stage will be a set of data on current labour market conditions, skills and components.

2. To provide analysis of the gaps in the current skills makeup in light of projected future demands. This will be identified on the basis of in depth analysis of the likely demands from both current employers and prospective new industry sectors.

3. To develop a strategy for overcoming such gaps. The strategy will be based on the most contemporary thinking in economics and labour market analysis.

4. Provide action plans that give clear guidance for identified priority sectors on how to implement the strategic directions proposed.

These objectives will be addressed in a series of four reports (see Box 1.3).

Box 1.3 SKILLS GAPS RESEARCH STUDY — REPORTS

Report 1: Skills Gaps Research Study: A Comparable Country Scan: This report will develop a clear understanding of the international environment in which Bahrain operates and determine Bahrain’s points of national advantage. It will also consider how other countries have aided skill development in the past. Report 2: Skills Gaps Research Study: Sectoral and Skills Gaps Analysis: This report will outline a baseline for the labour market and associated skills in eleven selected sectors, forecast the labour and skills needs for each sector into the future (assuming no predicted changes to the status quo) and identify skills gaps within each sector. It will also identify the strengths, weaknesses, opportunities and threats in terms of the labour market in each sector and associated skills gaps. Report 3: Skills Gaps Research Study: Future Skills and Workforce Needs: This report will summarise the key discussions drawn from the scenario planning exercise and the Regional Conference on Skills Gaps, conducted in Bahrain in November 2008. The report will highlight key findings that will contribute to the outcomes of the future strategy. Report 4: Skills Gaps Research Study: Final Report This report will identify the future needs of the Bahraini labour market and associated skills gaps using the information collected in each of the previous reports and incorporating economic modelling of this information. From these projections, this report will highlight a series of future scenarios that will form the base of the study’s strategy. The report will consist of a strategic skills plan for the next eight years and will include action plans that will address the future strategy.

Source: (Allen Consulting Group and Eidos).

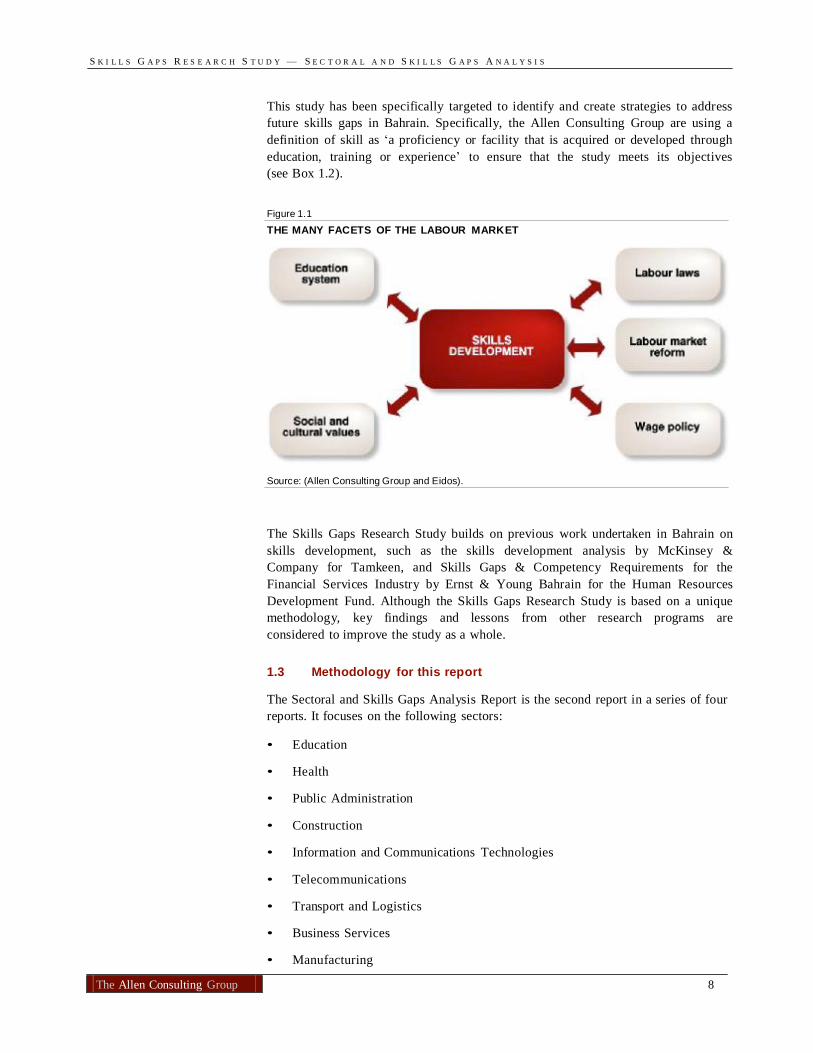

The Skills Gaps Research Study is one piece of a broader forum of issues that relate to the labour market and skill development. For example, there are key issues on labour market reform (including skill development concessions such as the current training levy scheme), wage policy, labour laws, the education system structure and Bahrain’s inherent cultural and social values that are not addressed within the scope of this study (see Figure 1.1).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 8

This study has been specifically targeted to identify and create strategies to address future skills gaps in Bahrain. Specifically, the Allen Consulting Group are using a definition of skill as ‘a proficiency or facility that is acquired or developed through education, training or experience’ to ensure that the study meets its objectives (see Box 1.2).

Figure 1.1

THE MANY FACETS OF THE LABOUR MARKET

Source: (Allen Consulting Group and Eidos).

The Skills Gaps Research Study builds on previous work undertaken in Bahrain on skills development, such as the skills development analysis by McKinsey & Company for Tamkeen, and Skills Gaps & Competency Requirements for the Financial Services Industry by Ernst & Young Bahrain for the Human Resources Development Fund. Although the Skills Gaps Research Study is based on a unique methodology, key findings and lessons from other research programs are considered to improve the study as a whole.

1.3 Methodology for this report

The Sectoral and Skills Gaps Analysis Report is the second report in a series of four reports. It focuses on the following sectors:

• Education

• Health

• Public Administration

• Construction

• Information and Communications Technologies

• Telecommunications

• Transport and Logistics

• Business Services

• Manufacturing

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 9

• Tourism and Hospitality

• Trade (retail and wholesale)

The report aims to:

• outline the baseline for the labour market and associated skills needs in eleven selected sectors

• inform the impact that the drivers of skills needs are having on the selected

sectors

• forecast the labour and skills needs for each of the eleven sectors into the future and identify skills gaps within each sector.

Across each of the eleven economic sectors the report:

• provides a snapshot of the nature of the characteristics of the sector and its

workforce

• looks at the international trends in sectors where this is relevant

• presents statistical information on labour market analysis

• evaluates some of the major factors that affect the availability of skilled workers in particular sectors.

In addition, chapters on the petrochemicals and banking and finance sectors have been included in this report, however, do not include the same level of detail as surveys of employers and employees within these sectors was outside the scope of the Skills Gaps Research Study. Further, only limited additional stakeholder consultations were undertaken with organisations within the banking and finance sector. These two chapters (Chapter 16 and Chapter 17) have been included for comparison purposes and should be considered outside the initial group of 11 economic sectors selected for the Skills Gaps Research Study.

The report has been influenced by the results of quantitative and qualitative analysis undertaken over the course of the Skills Gaps Research Study. The consultation process involved approximately 120 stakeholder meetings across the sectors, a workshop which focused on a scenario planning exercise for the Bahraini workforce and the conduct of a skills gaps conference attended by approximately 150 participants. This was supplemented by the quantitative results of four surveys carried out across the eleven sectors (an employer, employee, education institution, and graduate survey). The surveys are described at Appendix A of this report.

The report provides an overall picture of current skills gaps in the sectors and investigates the factors that will impact future skills needs. The skills gaps analysis includes a qualification gaps projection for 2012 identifying the shortage of specific qualifications by industry sector. On the basis of the skills gaps analysis a snapshot of the strengths, weakness, threats and opportunities for each of the sectors has been included.

Further, this report provides a labour market analysis across the 11 selected sectors based on historical labour market data and includes two forecasting components:

• the labour market forecast to 2012, based on the status quo for each sector

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 10

• an occupation analysis, which forecasts some key occupations required in 2012 in each of the 11 economic sectors based on the occupation-based results from the employer survey and the results of a labour market forecast based on the scenarios outlined and discussed in Report 4.

These results will be used in the final report (Report 4) to identify the future needs of the Bahraini labour market and the associated skills gaps. It will lead to the development of a strategic skills plan and will include action plans to address the future strategy.

It should be noted that data for the Skills Gaps Research Study across all four reports was collected during 2008 with the conclusions being finalised in May 2009.

Structure of Report 2

The remainder of this report is structured as follows:

Continuation of Part A— overview:

• Chapter 2 describes Bahrain’s labour market and skills. It considers the various

factor of unemployment amongst the Bahraini and non-Bahraini labour market and the participation of women in the workforce

• Chapter 3 provides an outline of key findings from two of the four surveys

(Graduate Survey and Training Institution Survey) conducted for the Skills Gaps Research Study

• Chapter 4 focuses on the key findings of the skills gaps analysis from each of

the eleven selected sectors

Part B — public services:

• Chapters 5 through 7 focus on each of the public services sectors individually — including education, health and public administration

Part C — infrastructure:

• Chapters 8 through 11 focus on each of the infrastructure sectors individually

— including construction, ICT, telecommunications and transport and logistics

Part D — trade and other services:

• Chapters 12 through 15 focus on each of the trade and other services sectors individually — including business services, manufacturing, tourism and hospitality and trade

Part E — petrochemicals and banking and finance:

• Chapter 16 and Chapter 17 discuss the petrochemicals and banking and finance

sectors for comparison purposes to the initial 11 selected economic sectors.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 11

Chapter 2

Bahrain’s labour market and skills

2.1 Bahrain’s labour market

In June 2008, the labour market in Bahrain consisted of 531 249 employees (see Table 2.1). A distinguishing feature of the Bahrain labour market (as in other GCC States) is the high proportion of non-Bahraini workers — making up 74.7 per cent of the total labour force. There has been strong growth in the labour market between 2002 and 2008 (an increase in employees of 81.6 per cent), with the majority of this growth coming from non-Bahraini workers (growth of 106.1 per cent). As a result, the level of Bahrainisation in the labour market has decreased from 34.2 per cent in 2002 to 25.3 per cent in June 2008 (Labour Market Regulatory Authority 2008b).

Table 2.1 BAHRAIN’S LABOUR FORCE — 2008 AND 2002

Indicator

2008

2002 Change from 2002 to 2008

Total employment 531 249 292 536 81.6%

Bahraini 134 468 100 007 34.5%

Non-Bahraini 396 781 192 529 106.1%

Bahrainisation 25.3% 34.2% -26.0%

Note: data for 2008 is for quarter 2 only (end June 2008). Source: (Labour Market Regulatory Authority 2008b).

The total size of the labour force and its percentage of the total population (including registered foreign nationals) has implications for the types of economic activity that can be undertaken in a nation and its capacity to achieve sustained economic growth. Nations with small pools of labour from which to draw workers, generally require a high level of participation in order to achieve economic growth.

A distinguishing feature of the Bahraini labour market is its diversity, relative to others in GCC States (as discussed in Report 1). Such diversity has important implications for the types of skills that are needed in a small labour market over the coming decades. It suggests that Bahrain will require a complex mixture of broad- based skills development (to service the vocationally-orientated sectors) and technical and professional/technical skills (to meet the needs of knowledge-based service sectors) to capitalise on a diverse range of private sector employment opportunities.

As a consequence, Bahrain will need to consider skills development in the broadest possible way. To quote the influential Leitch Review into skills development in the United Kingdom:

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 12

Skills are capabilities and expertise in a particular occupation or activity. There are a large number of different types of skills and they can be split into a number of different categories. Basic skills, such as literacy and numeracy, and generic skills, such as team working and communication, are applicable in most jobs. Specific skills tend to be less transferable between occupations. Most occupations use a mix of different types of skills (Leitch 2007).

For example, Bahrain is well-renowned for its banking and finance sector — although it only currently accounts for approximately 2 per cent of total employment — and is generally seen as an attractive sector for Bahraini citizens to seek employment (Harry 2007). In order to grow the banking and finance sectors Bahrain will require a broad range of skills that include technical, professional skills (including soft skills) and vocationally-based skills (i.e. clerical skills) to be developed. These skills will also need to be transferable across the entire sector, which is a commonly-held criticism of the employment arrangements in most GCC States (United Nations 2003)

Employment of foreign workers

A distinguishing feature of labour markets in GCC States is the high proportion of expatriate workers.

Foreign workers dominate in private sector employment, both at the skilled and unskilled level. For example, at the lower end of the employment scale, almost 25 per cent of employed non-Bahraini men are classified educationally as ‘illiterate’ compared with only 4 per cent for Bahraini men. Whereas over 35 per cent of Bahraini men have diplomas or degrees compared with 30 per cent for non-Bahraini men. However, this comparison can be misleading, with many Bahraini graduates in non-technical areas. The real dominance of expatriate workers lies in their technical and managerial skills.

The Bahrain labour market in 2008 consisted of almost 400 000 non-Bahraini workers, an increase of over 100 per cent from 2002 (see Table 2.1). This information indicates the rapid growth that has taken place in the Bahrain Labour market. It shows a number of important facts:

• most employment gains have accrued to non-Bahrainis

• as a result the process of Bahrainisation has been slowed down

• the large increase in work permit renewals signifies that foreign workers have

taken on characteristics of resident workers, in terms of quasi-permanency.

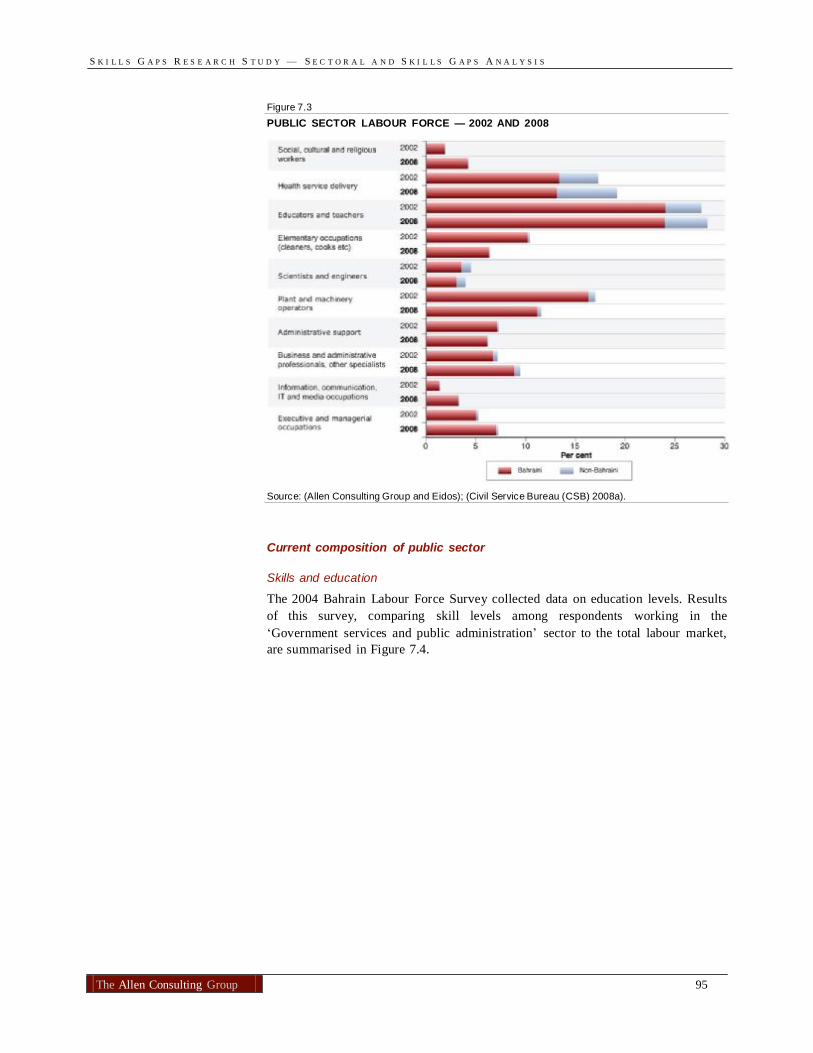

Figure 2.1 provides a yearly breakdown of total employment and employment across the broad classifications of public, private and domestic sectors over the period 2002-07. Over that period the percentage of non-Bahrainis in the labour force rose from 66 per cent to 74 per cent.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 13

Figure 2.1 ESTIMATED TOTAL EMPLOYMENT BY CITIZENSHIP AND SECTOR — 2002-07

Source: (Civil Service Bureau (CSB) 2008b; General Organization for Social Insurance (GOSI) 2008).

The process of Bahrainisation, largely driven by the employment of Bahrainis in the public sector has slowed down. While across the period Bahrainis maintained their dominance in the public sector at around 82 per cent of the workforce, private sector employment grew more rapidly than public sector employment with the result that Bahrainis lost ground in terms of contribution to the labour market.

Expatriate workers operate across the skill spectrum. They dominate the construction and heavy industry sectors by contributing the bulk of technical skills (70 per cent) and unskilled labour (over 65 per cent). However as the rapid growth in the Indian and Chinese economies has created competition for skilled labour in Bahrain (as well as the other GCC States) and has resulted in shortages in:

• structural specialists

• quantity surveyors

• planning engineers

• project directors

• design specialists

• urban surveyors.

Unemployment in Bahrain

The concept of unemployment occurs when a person who wants to work is unable to obtain a job. However, beneath this simple definition are a number of conceptual difficulties, related to job preference and reservation wage, desired working hours and spatial location of unemployment.

Unemployment data for Bahrain are superior to those available in other GCC States largely because of the Labour Force Surveys (LFS) conducted by the LMRA and the Ministry of Labour (MoL). Figure 2.2 shows data on unemployment numbers and unemployment rates by gender and split between Bahraini and non-Bahraini for the period 1981–2004. A number of features stand out:

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 14

• for Bahraini males, official unemployment rates peaked in 2004 at 12.5 per cent

• unemployment rates among Bahraini females also peaked in 2004 at 32.8 per cent

• the total (Bahraini) unemployment rate at 13.3 per cent is down from 18.5 per cent (2004) but exceeds unofficial estimates for other GCC States such as the KSA (11 per cent)

• among non-Bahraini males, unemployment is very low (0.9 per cent) but this

has traditionally been the case. The data for 2004 shows an upward movement in comparison to earlier periods

• unemployment rates for non-Bahraini females is substantially higher than

earlier periods such as 2001 and this may indicate a potentially growing problem with unemployment among guest workers (although more data points are needed to confirm this point).

Figure 2.2

UNEMPLOYMENT IN BAHRAIN — 1981-2007

Source:(Labour Market Regulatory Authority 2004; Labour Market Regulatory Authority 2007).

New entrants to the labour market

One explanation for the dominance of the young in unemployment data is the difficulty faced by new entrants to the labour market in obtaining initial work. The 2004 LFS provided data that disaggregated the unemployed into those with and without previous labour market experience.

Table 2.2

DISTRIBUTION OF UNEMPLOYED INDIVIDUALS WHO WORKED OR NEVER WORKED BEFORE — 2004

Work status Proportion

Worked before 41.6%

Never Worked 58.4%

Total 100%

Source: (Labour Market Regulatory Authority 2004)

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 15

The data in Table 2.2 shows that new entrants made up approximately 60 per cent of the total unemployed in 2004 and appears to confirm some commentary that obtaining an initial foothold in the Bahrain labour market is a contributing factor to observed unemployment. Unfortunately, no similar data are presented in the 2007 LFS to support these findings.

Duration of unemployment

The final aspect of unemployment in Bahrain relates to the duration of employment. Table 2.3 includes information on duration of unemployment. The results from the 2004 LFS (reproduced below) indicated the presence of a significant long-term unemployment problem with 54 per cent of total unemployed, 57 per cent of females and 50 per cent of males being unemployed for 13 months or more.

Long-term unemployment was a smaller problem for non-Bahrainis but the gap between Bahraini and non-Bahraini was less than in other labour market indicators.

Table 2.3 DISTRIBUTION OF UNEMPLOYED INDIVIDUALS — BAHRAIN 2004

Duration of employment

Total (%)

Non-Bahraini (%)

Bahraini (%)

Total Female Male Total Female Male Total Female Male

Less than 6 Month 22.7 19.1 26.9 35.2 32.8 39.0 20.9 16.7 25.5

7 to 12 23.3 23.9 22.7 27.9 26.2 30.7 22.6 23.5 21.7

13 to 24 23.9 23.8 24.0 18.0 22.1 11.6 24.8 24.1 25.5

Over 2 years 30.1 33.2 26.4 18.9 18.9 18.7 31.7 35.7 27.3

Total 100 100 100 100 100 100 100 100 100

Source: Derived from (Labour Market Regulatory Authority 2004).

Participation of women

A notable feature of the labour market in Bahrain has been the increased participation of females, both Bahraini and non-Bahraini, where participation is defined as the percentage of the labour force (employed plus active unemployed as a ratio of the civilian population of working age).

A number of commentators have noted the relatively low participation and level of position of women in GCC States (AL-QUDSI 1998), including such factors as low participation, occupation and segregation into lower level clerical and manual work and the service industry. For example only 1.6 per cent of women in Kuwait and 5.2 per cent in UAE hold managerial positions and 85 per cent of females in Bahrain work in the service sector. The impact of this labour market segmentation is a loss of productive labour and high allocative inefficiency, particularly in terms of education and labour market engagement.

There are social and cultural norms that impact on the participation of women in Arab society. However, theses norms have not precluded the rapid participation of women into tertiary education, where female participation (50 per cent) is significantly higher than for males (35 per cent).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 16

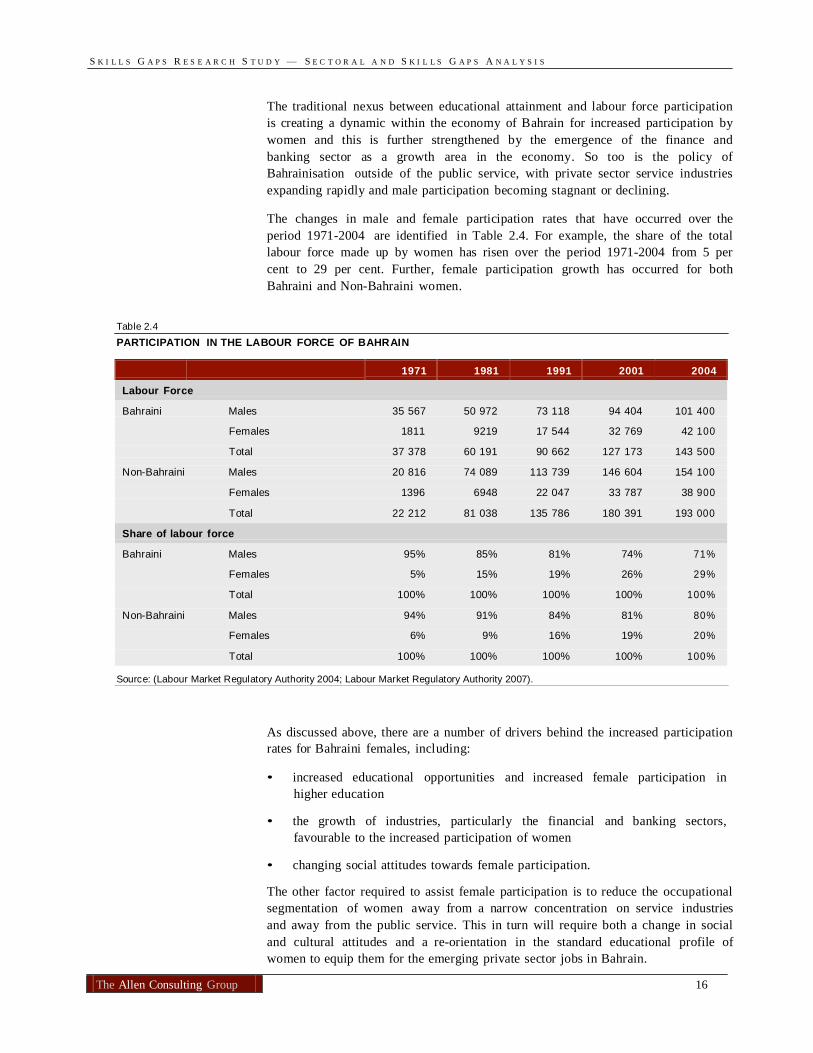

The traditional nexus between educational attainment and labour force participation is creating a dynamic within the economy of Bahrain for increased participation by women and this is further strengthened by the emergence of the finance and banking sector as a growth area in the economy. So too is the policy of Bahrainisation outside of the public service, with private sector service industries expanding rapidly and male participation becoming stagnant or declining.

The changes in male and female participation rates that have occurred over the period 1971-2004 are identified in Table 2.4. For example, the share of the total labour force made up by women has risen over the period 1971-2004 from 5 per cent to 29 per cent. Further, female participation growth has occurred for both Bahraini and Non-Bahraini women.

Table 2.4 PARTICIPATION IN THE LABOUR FORCE OF BAHRAIN

1971 1981 1991 2001 2004 Labour Force Bahraini Males 35 567 50 972 73 118 94 404 101 400

Females 1811 9219 17 544 32 769 42 100

Total 37 378 60 191 90 662 127 173 143 500

Non-Bahraini Males 20 816 74 089 113 739 146 604 154 100

Females 1396 6948 22 047 33 787 38 900

Total 22 212 81 038 135 786 180 391 193 000

Share of labour force Bahraini Males 95% 85% 81% 74% 71%

Females 5% 15% 19% 26% 29%

Total 100% 100% 100% 100% 100%

Non-Bahraini Males 94% 91% 84% 81% 80%

Females 6% 9% 16% 19% 20%

Total 100% 100% 100% 100% 100%

Source: (Labour Market Regulatory Authority 2004; Labour Market Regulatory Authority 2007).

As discussed above, there are a number of drivers behind the increased participation rates for Bahraini females, including:

• increased educational opportunities and increased female participation in

higher education

• the growth of industries, particularly the financial and banking sectors, favourable to the increased participation of women

• changing social attitudes towards female participation.

The other factor required to assist female participation is to reduce the occupational segmentation of women away from a narrow concentration on service industries and away from the public service. This in turn will require both a change in social and cultural attitudes and a re-orientation in the standard educational profile of women to equip them for the emerging private sector jobs in Bahrain.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 17

2.2 Sectors of the Bahrain economy

For the purposes of the Skills Gaps Research Study, the Bahrain labour market is being considered in two segments:

• the future labour market comprising the 11 economic sectors selected for this

study and listed in Section 1.3

• other economic sectors (including the petrochemical and banking and finance sectors) that make up the entire Bahrain labour market.

The Labour Market Regulatory Authority (LMRA) estimated the total labour market to equal 503 784 employees (both Bahraini and non-Bahraini workers) in December 2007. Of this total, 335 437 employees (around 67 per cent of the total labour force) worked in one of the 11 selected economic sectors (see Table 2.5). The remaining 168 347 employees work in other sectors of Bahrain’s economy (including the petrochemicals and banking and finance sectors.

Table 2.5 SECTORS OF THE BAHRAIN ECONOMY — 2007

Economic sector Number of employees

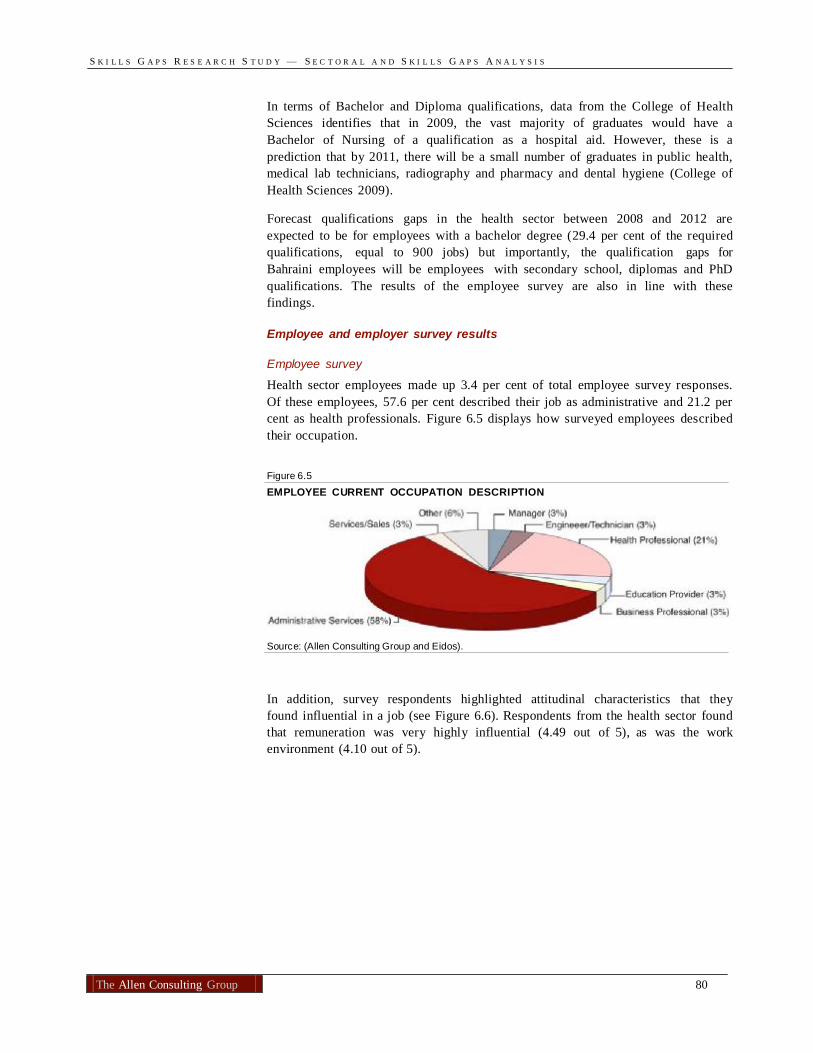

Proportion of total labour market

Education (public and private) 21 111 4.2%

Health (public and private) 9563 1.9%

Public Administration 14 119 2.8% (excluding public health and education)

Construction 115 582 22.9%

Information and Communications 3301 — Technologies

Telecom munications 2412 0.5%

Transport and Logistics 11 272 2.2%

Business Services 2822 0.6%

Manufacturing 63 439 12.6%

Tourism and Hospitality 23 518 4.7%

Trade (retail and wholesale) 71 599 14.2% 11 selected economic sectors 335 437 66.6% Other economic sectors 168 347 33.4% (including petrochemicals and banking and finance) Total labour market 503 784 100%

Note: ICT employees are a sub-sector of a number of other sectors (the majority being in the trade and manufacturing sectors). Source: (Allen Consulting Group and Eidos); (Labour Market Regulatory Authority 2008a); (Civil Service Bureau (CSB) 2008a); (General Organization for Social Insurance (GOSI) 2008).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 18

Assuming the status quo, the total labour market would be forecast to equal around 694 000 employees in 2012 (excluding ICT, for which employees are scattered across a number of the other sectors). Of this total, around 473 000 employees (68 per cent of the total labour force) are expected to work in one of the 11 selected economic sectors.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 19

Chapter 3

Views from graduates and education institutions

3.1 Overview

This chapter outlines the key findings from two surveys (Graduate Survey and Training Institution Survey) that aimed to meet the needs of the overall study to identify skills deficiencies and gaps in the Bahrain labour market. The purpose of the surveys was to collect data about the characteristics of Bahraini training institutions and characteristics and ambitions of students who are about to graduate from a range of Bahrain training institutions. This chapter also contains some overarching analysis from the employer survey, considering the differences in results across small, medium and large survey respondents.

3.2 Graduate survey analysis

A total of 270 graduates (and final year students) were surveyed as part of the skills gap analysis. Two thirds of respondents were female and around 90 per cent were born in Bahrain. As could be expected from a student population, more than half of the respondents were 20 to 24 years of age, and around 90 per cent were under 30.

The estimated monthly income of students reflects quite varied socio-economic status. Most students (61.0 per cent) reported their personal monthly income to be less than BD50. However, the results for estimated household income showed significant spread. The largest subset (27.2 per cent) of students lived in households where monthly income was more than BD1500. The next largest subsets are less than BD50 and between 1000 to BD1500 — 11.4 per cent and 11.0 per cent respectively — indicating a considerable socio-economic gap.

Educational experience

Regarding their educational experience, 72.8 per cent of respondents nominated Certificate or Diploma as the highest qualification they had completed, and another 14.4 per cent reported completing a Bachelor degree or above. It should be noted however, that not all respondents had graduated when completing the survey — some were in their final year of study.

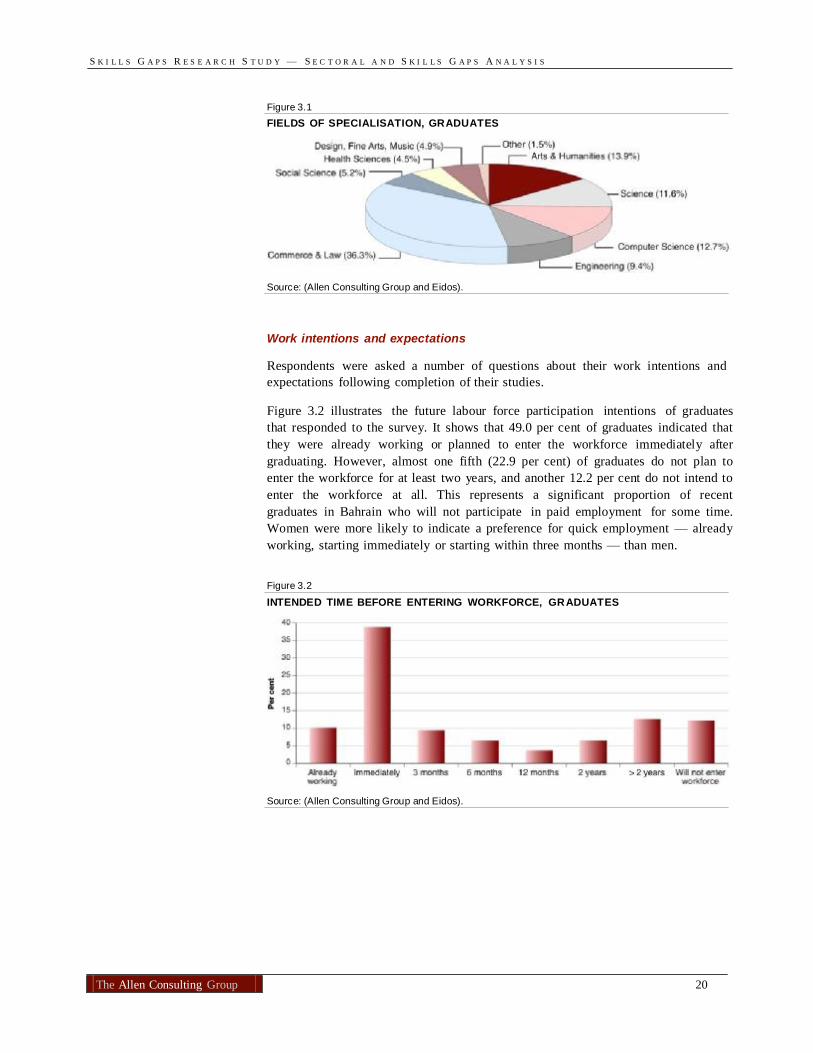

Figure 3.1 illustrates the fields of specialisation of graduate students. It shows that more than a third of students (36.3 per cent) specialised in commerce and law, significantly more than any other specialisation. Other popular specialisations were arts and humanities (13.9 per cent), computer science (12.7 per cent) and science (11.6 per cent).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 20

Figure 3.1 FIELDS OF SPECIALISATION, GRADUATES

Source: (Allen Consulting Group and Eidos).

Work intentions and expectations

Respondents were asked a number of questions about their work intentions and expectations following completion of their studies.

Figure 3.2 illustrates the future labour force participation intentions of graduates that responded to the survey. It shows that 49.0 per cent of graduates indicated that they were already working or planned to enter the workforce immediately after graduating. However, almost one fifth (22.9 per cent) of graduates do not plan to enter the workforce for at least two years, and another 12.2 per cent do not intend to enter the workforce at all. This represents a significant proportion of recent graduates in Bahrain who will not participate in paid employment for some time. Women were more likely to indicate a preference for quick employment — already working, starting immediately or starting within three months — than men.

Figure 3.2

INTENDED TIME BEFORE ENTERING WORKFORCE, GRADUATES

Source: (Allen Consulting Group and Eidos).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 21

Of those graduates who plan to work when they complete their studies, just over half (53.5 per cent) intend to work in the private sector, while the remaining 46.5 per cent would like to work in the public sector, for a government-owned business, or for a semi-government organisation. Business services (37.4 per cent) was the most popular sector in which to seek employment, followed by education (18.5 per cent), public administration (14.1 per cent) and telecommunications (10.7 per cent). Less than 10 per cent of graduates sought work in each of the remaining eight sectors.

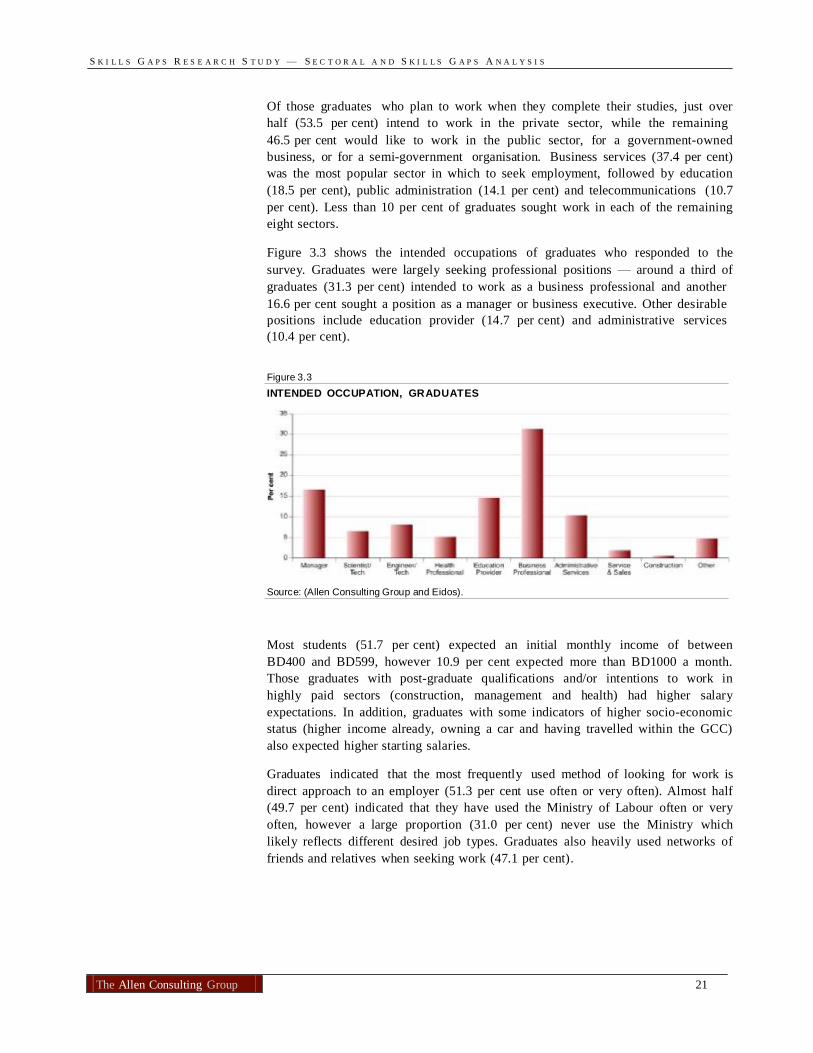

Figure 3.3 shows the intended occupations of graduates who responded to the survey. Graduates were largely seeking professional positions — around a third of graduates (31.3 per cent) intended to work as a business professional and another 16.6 per cent sought a position as a manager or business executive. Other desirable positions include education provider (14.7 per cent) and administrative services (10.4 per cent).

Figure 3.3 INTENDED OCCUPATION, GRADUATES

Source: (Allen Consulting Group and Eidos).

Most students (51.7 per cent) expected an initial monthly income of between BD400 and BD599, however 10.9 per cent expected more than BD1000 a month. Those graduates with post-graduate qualifications and/or intentions to work in highly paid sectors (construction, management and health) had higher salary expectations. In addition, graduates with some indicators of higher socio-economic status (higher income already, owning a car and having travelled within the GCC) also expected higher starting salaries.

Graduates indicated that the most frequently used method of looking for work is direct approach to an employer (51.3 per cent use often or very often). Almost half (49.7 per cent) indicated that they have used the Ministry of Labour often or very often, however a large proportion (31.0 per cent) never use the Ministry which likely reflects different desired job types. Graduates also heavily used networks of friends and relatives when seeking work (47.1 per cent).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 22

Attitudes to skills and work

Respondents were asked how important they considered certain skills to be when applying for work. As indicated in Figure 3.4, with the exception of physical skills, more than 50 per cent of respondents rated every work-related skill as very highly important. It is important to consider that many of the respondents of the graduate survey have not yet commenced work and generally identified the majority of skills as very highly important more often than the respondents to the employee survey.

Figure 3.4 ATTITUDES: WORK RELATED SKILLS, GRADUATES

Source: (Allen Consulting Group and Eidos).

Graduates were also asked about the factors that may influence their decision to take a job. Although graduates rated sufficient income and job security highly, the most influential factors stated were opportunities for promotion, working as a part of a team, good training provisions, effective resolution of work conflicts, and child tuition coverage. Graduates responded more strongly than existing employees across most factors and in particular rated alignment with traditional beliefs and the same nationality as other employees as much more important factors than existing employees. This could suggest that graduate students hold more radical views than existing employees.

3.3 Training institution survey analysis

The survey of Bahraini training institutions (TIs) was completed by 11 organisations. Of the participating TIs:

• most were private sector organisations (63.6 per cent)

• around half were universities (45.5 per cent) and the other half colleges or

other institutions providing training services (55.5 per cent)

• over half had less than 100 employees (60 per cent).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 23

Student characteristics

TIs were asked about their new enrolments and current students graduating in 2008 by gender and nationality. Bachelor degrees comprise most new enrolments (72 per cent). Although still the largest category, bachelor degrees comprised only 51.2 per cent of upcoming graduations. In contrast, certificate or diploma qualifications comprise 14.1 per cent of new enrolments compared with 39.2 per cent of graduations. This suggests that the popularity of bachelor degrees has increased in the previous few years, whilst certificate and diploma qualifications have decreased in popularity. Notably, TIs reported no doctoral degree enrolments or graduations.

It also appears that TIs are growing — total enrolments for the year were 7 562 compared with only 1 646 graduations. Even accounting for some students who do not complete their qualification, this represents a significant increase in student numbers.

More than half (57.3 per cent) of new enrolments across all qualification types were women, rising to 62 per cent of bachelor degree enrolments. Higher-level qualifications however were more male-dominated — 70.0 per cent of masters degree enrolments and 55.9 per cent of postgraduate diploma enrolments were men. The same trend was reflected in graduations — most (72.2 per cent) bachelor degree graduations were women whereas two thirds (66.7 per cent) of masters degree graduations were men.

Bahraini students significantly outnumbered non-Bahrainis in both enrolments and graduations in all qualification types with the exception of postgraduate diplomas. Overall, Bahrainis comprised 85.7 per cent of all enrolments and 79.2 per cent of all graduations. For postgraduate diplomas, most enrolments and graduations were non-Bahrainis — 78.1 and 67.2 per cent respectively.

TIs consistently reported that the professional skills most in demand from students were accountancy and information technology (IT) related skills. They reported that for potential employers, management skills were also in demand in addition to IT and accountancy. This suggests a possible shortage of supply in management skills as students attach less importance to this skill.

Bahraini TIs indicated that their students were most likely to find work in the business sector, ICT, the public sector, education and trade sectors. In addition, two institutions indicated that their students very often found jobs in the automotive industry and oil sector respectively. The health, transport and logistics, and tourism and hospitality sectors were the least likely sectors for students to attain jobs.

This is largely consistent with the industries that TIs target their qualifications to. Certificate and diploma qualifications, as well as bachelor degree qualifications were most likely to target the business services and ICT industries. Postgraduate qualifications and Masters degree qualifications were most likely to target business services with no other industry recording a high response rate across institutions. Doctoral degree qualifications were spread across most industries, rather than predominately targeted to a particular industry. For all qualification types, but particularly for the more advanced qualifications, health, transport and logistics, and tourism and hospitality industries were not popular.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 24

Employment assistance

TIs play a key role in assisting their students to find work. The methods most frequently used by TIs to assist students in finding work are direct approach to employers, career counsellors and utilising work contacts or networks. This is fairly consistent with the methods identified by graduates in the graduate survey, although few graduates (17.6 per cent often or very often) reported using career counsellors to look for work.

In addition, TIs use some specific procedures and processes to engage with industry groups or employers and most (9 of 11) target specific industries. The processes most frequently used are: obtaining employer sponsorship of programs and employer linked student placements, discussing desired qualifications and skills with industry groups and potential employers and employment expositions.

Work-related skills

TIs were asked how important they considered certain skills to be for their graduating students. Figure 3.5 shows that more than three quarters of TIs rated the more ‘traditional’ skills of literacy, numeracy, management and planning skills as very important. Overall, TIs attached less importance to the skills as a group than graduates, although they rated literacy and numeracy higher. Other clearly different views between graduates and TIs are:

• TIs rated emotional skills considerably lower — no TI considered this skill to

be very important compared with 51.8 per cent of graduates

• only 25 per cent of TIs rated persuasive skills as very important compared with 63.1 per cent of graduates

• graduates rated work communication most highly (85 per cent rated it as very

important) compared with only half of TIs.

Figure 3.5 WORK RELATED SKILLS, TRAINING INSTITUTIONS

Source: (Allen Consulting Group and Eidos).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 25

3.4 Employer survey — results by size of employer

The employer survey comprised of 804 respondents across the 11 selected economic sectors (excluding responses from the petrochemicals and banking and finance sectors). Of the total survey responses:

• 53 per cent of respondents were small employers with between 1 and 9

employees

• 35 per cent of respondents were medium employers with between 10 and 99 employees

• 12 per cent of respondents were large employers with more than 100

employees.

An overview of number of small, medium and large employers who responded to the employer survey by economic sector is provided in Appendix A.

Small, medium and large employers identified the top five skills required in the sector, which are outlined in Table 3.1. The most commonly identified skill required across all employers was communications skills (42 per cent for small employers), followed by technical skills (33 per cent for large employers). For small employers, customer service and selling skills are required, whereas for larger employers, management skills and work ethics were seen as more important skills.

Table 3.1 TOP 5 SKILLS — SMALL, MEDIUM AND LARGE EMPLOYERS

Small employers

(skill type) % of total

Medium employers

(skill type) % of total

Large employers

(skill type) % of total

Communication skills 42%

Technical skills 18%

Customer service skills 13%

Selling skills 13%

English language skills 7%

Communication skills 32%

Technical skills 22%

Customer service skills 10%

English language skills 7%

Physical skills 6%

Communication skills 38%

Technical skills 33%

Management skills 11%

Work ethics 8%

English language skills 5%

Source: (Allen Consulting Group and Eidos).

In addition, survey respondents identified the broad occupation categories where there are current vacancies (see Figure 3.6). There are significant differences in vacancies across employers depending on their size. For example, 42 per cent of vacancies for small employers were in service and sales staff. For medium employers 44 per cent of vacancies were in managers and business executive staff and for large employers, the majority of vacancies (59 per cent) were in construction occupations.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 26

Figure 3.6 CURRENT VACANCIES — SMALL, MEDIUM AND LARGE EMPLOYERS

Source: (Allen Consulting Group and Eidos).

Employers also rated the importance of work related skills on a scale ranging from not important to very highly important (see Figure 3.7). For small employers, the most important work related skill was customer communication, whereas for medium employers the most important work related skills was technical ‘know how’. For large employers, the most highly rated skills were work communication, customer communication and literacy skills.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 27

Figure 3.7 IMPORTANCE OF WORK RELATED SKILLS — SMALL, MEDIUM AND LARGE EMPLOYERS

Source: (Allen Consulting Group and Eidos).

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 28

Chapter 4

Future solutions for Bahrain’s labour force

4.1 Overview

This chapter highlights the key findings from each of the eleven selected sectors detailed further in Part B, C and D of this report. The key findings focus on the skills gaps analysis and future skills issues in each of the sectors.

Drawing on these sectoral key findings, conclusions on the skills gaps in Bahrain’s labour market are drawn and next steps are identified.

4.2 Key findings — public services

Education

Broader skills gaps areas that are direct to other industries point to skills gaps within the education sector because as previously stated, it is Bahrain’s main skills provider. These types of skills gaps include:

• higher education teaching skills — while overall there seems to be an adequate

supply of education graduates for primary education, there are skills gaps in specialised fields of education (such as early childhood, secondary, technical and higher education; curriculum and assessment; educational planning)

• technical training skills — which is reflected in the general shortage of

engineers, technologies and middle level technicians

• career development skills — including careers development issues such as careers counselling and provision of on-site training

• education administration skills — including skills required by education

managers (principals, directors, deans), and administrative skills. Applying the results from the employer survey and the current skills gaps identified in the labour market analysis allows for an approximate number of specific occupations required in 2012, including the future need for:

– 650 education providers

– 400 administrative services staff

– 350 other education related workers.

Key future skills challenges facing Bahrain’s education sector are:

• the quality of education that is hindered by problems in basic skills outcomes

from schooling

• there is an over-supply of humanities-social science graduates who often are lacking employability skills, and a shortage of science, mathematics, technology and nursing graduates

• difficulties in ensuring a supply of graduates and recruiting them into teaching

in areas where there are mismatches between supply and demand such as early childhood, VET, mathematics, science and technology.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 29

Health

Currently, health sector skills gaps fall into three main areas:

• health care specialists — a critical issue for the health system, projections of the health sector workforce show that these shortages will persist for Bahraini national employees at least for the next three years

• health management and coordination (including human resources and health

workforce planning) — cited by the WHO in 2005 and these skills will be crucial to continue to develop to maintain the current performance of the health system for Bahrain’s population

• administration — Administration training was the one aspect of training where

the number of organisations with the current capacity to provide this training in-house fell short of the number of organisations that highly prioritise this type of training.

Applying the results from the employer survey to the these skills gaps allows for an estimation of the approximate number of specific occupations required in 2012, including the future need for:

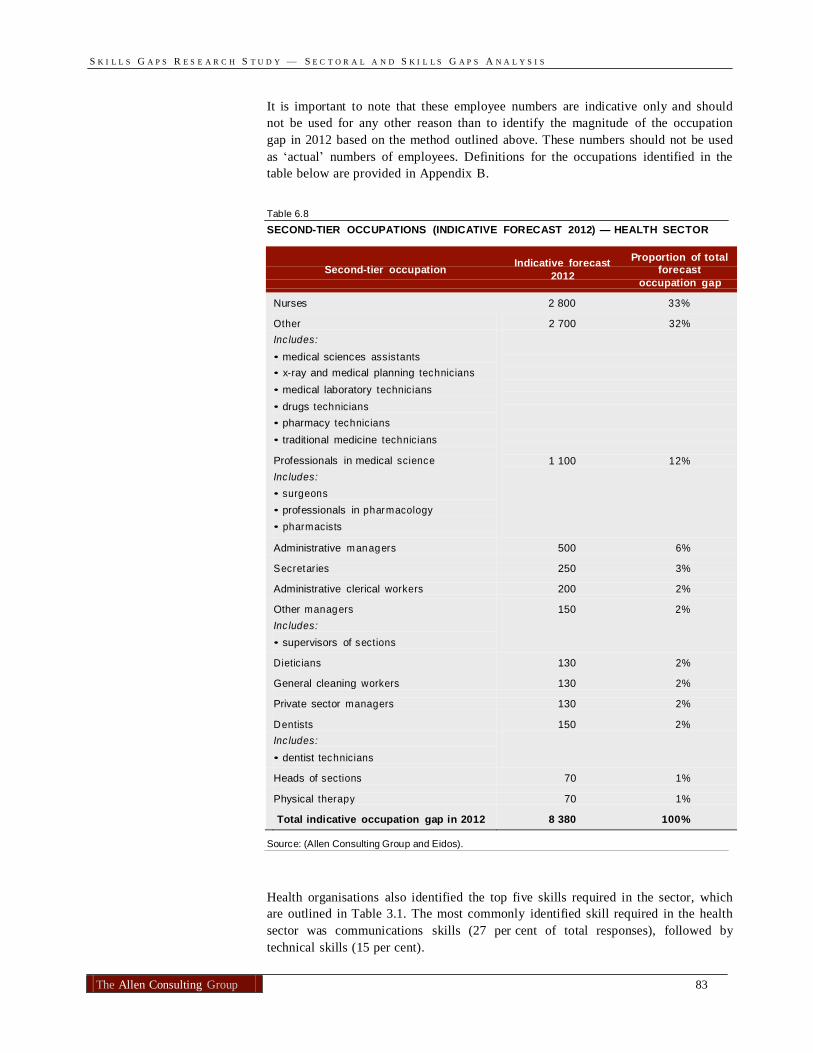

• 1 850 health professionals

• 2 500 managers

• 7 000 other health workers

• 380 administrative workers.

By 2012, it has been projected that there will be a shortage of several types of qualifications in the industry — a shortage of Bahraini staff with Diplomas, secondary education and at the PhD level and non-Bahrainis with Bachelor degrees, Diplomas, secondary education, high diplomas, masters and PhDs.

The efficacy of the health sector, given the skills gaps identified above, will be under pressure in the future — especially in a context of high incidences of non- communicable diseases in Bahrain coupled with a growing population.

• in the short term, the Bahrainisation policy may be contributing to the current

staff shortages, hindering recruitment of foreign staff where Bahrainis lack the skills for specialist position

• strong encouragement to grow the private health sector because of the benefits

it will bring to the whole of Bahrain, including tapping into the health tourism industry

• in the longer term, the key problem facing the health sector is the current

health workforce shortages in two significant areas — health specialities, including allied health positions and nurses, and heath management, human resources and health workforce planning skills

It is important to note that the health sector is ideal to target participation from the growing young female Bahraini population and alternative training and employment options could be considered to make participation in the sector more attractive.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 30

Public Administration

Primarily due to the existence and performance of the Civil Service Bureau and the high regard, which Bahrainis perceive a career in the public service, skills gaps tend to be lower in public administration compared with other sectors. Nonetheless, the labour market analysis and stakeholder comments suggest that a skills gap exists in terms of management and leadership skills. In addition, there is considerable need within the sector to accommodate an increasing number of female graduates predicted to enter the sector.

Results from the employer survey and the current skills gaps identified in the labour market analysis can be used to determine an approximate number of specific occupations required in 2012, including the future need for:

• 1 800 administrative staff

• 720 engineering/technical staff

• 171 managers (mainly at the director level).

The largest gaps in qualification between 2008 and 2012 will be for employees who have completed secondary school (35 per cent of the gap, equal to 3 614 jobs) and for employees with a bachelor qualification (26 per cent of the gap, equal to 2 685 jobs).

The main problems facing public administration in Bahrain are:

• an overly rigid (complex) system for classifying and promoting staff that does

not provide for flexible management of human resources at the agency level

• the absence of a recognised qualifications framework from which public sector organisations can make judgements about training needs, promotions, and recruitment

• an anticipated shortfall in the number of university graduates at the Batchelor

degree level and above

• inadequate data about the quality and effectiveness of public sector training

• growing number of female university graduates seeking high-level opportunities within the public sector.

4.3 Key findings — infrastructure

Construction

The Bahrain construction sector is not experiencing labour shortages alone, rather it is within the context of an international trend. In Bahrain, skills gaps lie in three key areas as discerned from the findings of the labour market analysis, surveys and other reports. These are in:

• induction, administration and technical skills for low-level workers

• tertiary and leaderships skills for high-level Bahraini employees

• human resources skills to assist entrants to jobs within the sector.

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 31

Applying the results from the employer survey and the current skills gaps identified in the labour market analysis can be used to determine an approximate number of specific occupations required in 2012, including the future need for:

• 34 000 construction workers

• 3 000 engineers/engineering technicians

• 2 100 administrative staff

• 1 250 managers.

Areas of the construction sector that could emerge as issues in the future include:

• an inadequate number of people entering training

• the high attrition rate of apprentices (in Bahrain’s case, there is no

apprenticeship model/program in place)

• a high separation from the skilled trade workforce once people are qualified, caused by low demand for skills, declining industry employment prospects, and/or better careers and conditions being offered in other industries/sectors

• difficulties in recruiting new entrants with the right level of prior education,

skills and attributes

• lack of training in particular segments of the sector because of structural issues factors such as out-sourcing or sub-contracting

• an insufficient level of activity by the existing trade workforce in upgrading

skills once initial qualifications have been attained

• addressing the issue that many employers only send employees to training courses when it does not disrupt their work and where it is vital to their firm (Libert 2004).

Despite non-Bahrainis continuing to fill the majority of unskilled and highly skilled positions, shortages in labour and delays in projects are likely to persist. Increased global competition for labour, low wages in the sector, and the impact of training levies on business sustainability may see workers and developers go elsewhere

ICT

The skills gaps in Bahrain’s ICT sector are apparent from the findings of the labour market analysis, surveys and other reports. Currently, ICT sector skills gaps fall into 3 main categories:

• ICT management and coordination skills

• certified software application technical skills

• IT strategy and planning skills.

Results from the employer survey and the current skills gaps identified in the labour market analysis can be used to determine an approximate number of specific occupations required in 2012, including the future need for:

• 1 300 service and sales staff

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 32

• 1 200 managers

• 1 100 engineers/technicians

• 650 scientists/technicians managers.

In this context, the problem of insufficient numbers of IT-trained personnel in Bahrain is expected to grow:

• it is suggests that personnel with strong fundamental IT skills and knowledge

will be able to adapt to new IT technologies more rapidly than personnel only possessing application-specific skills and knowledge

• new IT hardware and software applications are increasingly technical and

complex, requiring highly skilled personnel at both operation and maintenance levels.

Telecommunications

The extent to which the telecommunications sector in Bahrain is suffering from specific skills gaps is unclear, given:

• the relatively high levels of mobile, broadband and Internet penetration in

Bahrain

• the general absence of skills shortages identified by key stakeholders during consultations.

Nonetheless, due to the projected gradual expansion of the sector’s workforce, and the continuing convergence of the telecommunications and IT industries, there are a number of general skills areas that government and business leaders could focus on to ensure the future success of the telecommunications sector. These include:

• ICT literacy – primarily to allow for effective interaction with software linking

telecommunications devices and multi-media services

• e-business techniques – ranging from knowledge about email and VoIP to business-to-business electronic commerce

• sales and customer service.

Results from employer survey and the current skills gaps identified in the labour market analysis can be used to determine an approximate number of specific occupations required in 2012, including the future need for 120 engineers and technicians, and only a small number of administrative and sales services occupations (70 managers and 70 services and sales staff).

The main problem facing the Bahraini, telecommunications sector:

• is the constraint of a lack of local vocationally trained, work ready, graduates

to fill existing vacancies or to cater for new growth

• a sufficient supply of suitably trained employees

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 33

Transport and logistics

Currently, key skills gaps in the transport and logistics sector include:

• logistics and freight skills — future improvements in logistics and freight skills will be important to increase competence in this area of the sector. The results of the employee survey identify a need for employees with a Diploma or Bachelor qualification (approximately 1 833 jobs) in 2012

• airport services skills — required as the Bahrain International Airport

continues to grow and improve facilities, infrastructure, and in turn, activity. Specific skills include customer service and sales skills, engineering and maintenance skills, and emotional (attitudinal) skills

• airline cabin crew skills — will also be required in the future as Bahrain

increases its connectivity within the GCC and MENA regions and beyond. In addition to cabin crew skills, call centre skills for airlines will also be required.

The approximate number of specific occupations required in 2012, include the future need for approximately 7 400 positions, including:

• 6 600 general transport and logistics positions

• 800 engineers and technicians

• 670 administrative staff

• 330 managers.

Areas of the transport and logistics sectors that could emerge as issues in the future include:

• slow Bahraini employment growth — labour market analysis shows no growth

in the Bahraini workforce to 2012 in the sector

• an under utilised female workforce — given the pool of young Bahraini women that could potentially participate in the labour force, restricting and under-utilising the female workforce could be a significant human resources issue in the future

• maintaining international competitiveness in logistics — the shortage of

workers (particularly Bahraini) and skills in the logistics sector may have implications for maintaining this competitive status in the region. New infrastructure in the sector (such as the KBS port and Bahrain Logistics Zone) will further emphasis skills gaps as these projects build up to full capacity

• public transport — if improvements to the current public transport system are

considered in the future, a significant skills base will be required to expand public transport options.

4.4 Key findings — trade and other services

Business services

The skills gaps in Bahrain’s business services sector are apparent from the findings of the labour market analysis, surveys and other reports. Currently, business services sector skills gaps fall into 3 main categories:

S K I L L S G A P S R E S E A R C H S T U D Y — S E C T O R A L A N D S K I L L S G A P S A N A L Y S I S

The Allen Consulting Group 34

• specialist legal and accounting skills — primarily advisory and analysis services, targeting such business areas as Islamic banking and insurance, intellectual property and finance

• management and coordination skills — for example, resource managers,

engineering process managers, accountants and sales and marketing executives

• paralegal and legal clerical skills — miscellaneous business and legal support roles, ranging from legal assistances to receptionists and numerical clerks.

Results from the employer survey and the current skills gaps identified in the labour market analysis can be used to determine an approximate number of specific occupations required in 2012, including the future need for:

• 1 200 service and sales staff

• 900 business professionals

• 550 managers

• 400 administrative services.

The major problems facing the expansion of the business services sector include:

• labour force supply — labour market analysis suggests that the industry will

still be 68 per cent reliant on non-Bahraini’s by 2012. Unless female participation, especially of those with post-school training increases above the current rate, there may be problems in attracting sufficient domestic labour to cover even the 32 per cent predicted for Bahrainis.

• labour force skills — this is potentially the greatest problem facing the industry