sector in-depth only brief gains for ... - rio.rj.gov.br · subway operator concessão metroviária...

TRANSCRIPT

CROSS-SECTOR

SECTOR IN-DEPTH16 May 2016

Analyst Contacts

Barbara Mattos, CFA 55-11-3043-7357VP-Sr Credit [email protected]

Paco Debonnaire [email protected]

Farooq Khan [email protected]

Marianna Waltz, CFA 55-11-3043-7309MD-Corporate [email protected]

Paloma San Valentin 212-553-4111Managing Director– US and AmericasCorporate [email protected]

2016 Olympics – Rio de Janeiro

Games Offer Lasting Benefits for City butOnly Brief Gains for Brazilian Companies» The August 2016 Olympic Games will bring the city of Rio de Janeiro hundreds of

thousands of visitors, corporate marketing opportunities, lasting infrastructureimprovements and temporary business benefits. New infrastructure projectspromise the most lasting benefits to the city, while Brazil's beleaguered overalleconomy will not get a significant boost from hosting the games. The Olympics areneutral for Brazil’s sovereign credit quality, however, offering a brief economic stimulusthat will hardly budge Brazil’s still-contracting economy.

» Olympic-related investments will drive long-lasting infrastructure improvementsin public transportation and urban mobility, which the host city has supportedpartly with the help of federal transfers. The city’s debt load is set to fall despiteadditional borrowing, thanks to a likely renegotiation of its federal loans later this year.Tourists will boost Rio’s tax collections, but only temporarily, while Rio’s preparations forthe Olympics have generally been well managed, on time and on budget.

» The Olympics have generated about BRL25 billion (USD7.1 billion at May 2016rates) worth of infrastructure investments in Rio’s metropolitan area—virtuallythe same amount as the entire 2014 World Cup investment in 12 Brazilian cities.The economic benefits from investment in urban transport, toll roads, ports and energyhave already begun for project sponsors such as subway operator Metrô Rio and toll-road operator LAMSA. But both systems can expect a loss of local traffic even as touristtraffic rises.

» Total bank loans to finance infrastructure and the Cidade Olímpica athletes'village for the Rio Olympics only amount to small fractions of the outstandingloans at participating banks, and represent limited credit risks. BNDES, Brazil'sfederal development bank, has provided the most bank funding for the Olympics, but itsloans have totaled about 1.1% of its BRL700 billion loan book. Olympics-related lendingfrom Caixa represents just 0.3% of its BRL684 billion total loan operations.

» The Olympics will have little impact on most non-financial companies beyondshort-lived sales increases and intangible marketing benefits. Food and beverageproducers such as Ambev and BRF can expect a marketing benefit from theirsponsorships. Payment-processor Cielo, airlines such as LATAM and the Localiza carrental company will all benefit from a surge in tourist sales and transactions. But theBRL31 billion Olympics-related construction boom is now all but finished.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Olympic Games Offer Only Limited, Mainly Local Benefits

The August 2016 Olympic Games in the city of Rio de Janeiro (Ba2 negative) promise to bring some 10,000 athletes from more than200 countries—as well as huge marketing opportunities for corporate sponsors and temporary business benefits. New infrastructureprojects promise the most lasting benefits to the city, while Brazil's beleaguered overall economy will not get a significant boost fromhosting the games.

When Brazil (Ba2 negative) hosted the soccer World Cup in 2014, new infrastructure concentrated on airports and arenas in 12 hostcities, including Rio. By contrast, the Olympics will leave a legacy of new urban mobility projects in the city, including improvements toits international airport and the city's main Maracanã arena, on top of the urban mobility investment.

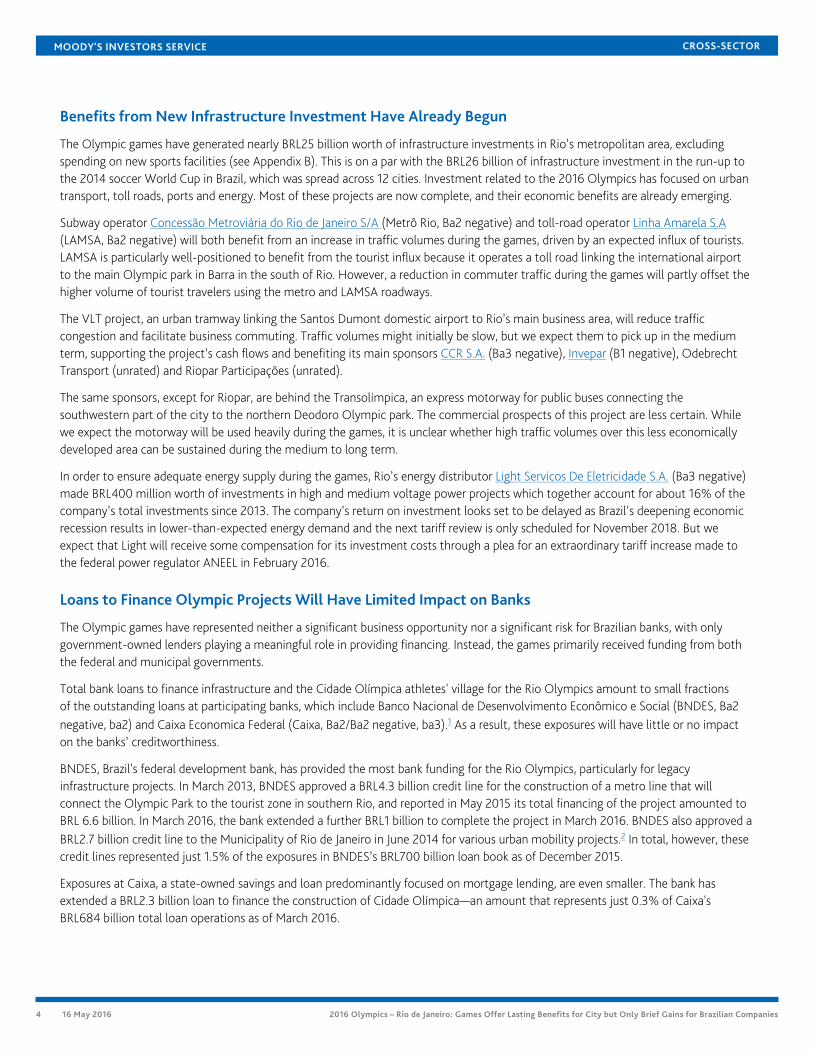

Despite a limited economic boost, hosting the Olympics will permanently improve Rio's infrastructure and labor force qualification.Improved infrastructure could eventually lead to higher supply chain efficiency and potentially lower costs for companies in the Riometropolitan area. The Olympics have generated over BRL25 billion (USD7.1 billion at May 2016 rates) in infrastructure investments forRio's metropolitan area—nearly as much as the BRL26 billion Brazil spent on the entire 2014 World Cup across the 12 host cities (seeExhibit 1).

Exhibit 1

Actual Sports-Related Costs, Olympic Games 2004-2016USD billions (2009 dollars)

Notes: Costs converted into 2009 US dollars by using local GDP deflator indices and the World Bank's National Currency Units. Cost figures exclude road, rail, airport infrastructure costsand private costs such as hotel upgrades and business investment incurred preparing for the Games.Source: University of Oxford; Organizing Committee Rio 2016; Responsibility matrix from Brazil federal government

The surrounding state of Rio de Janeiro (unrated) has about 16 million inhabitants—about 8.0% of Brazil's total population—three-quarters of whom live in the Rio metropolitan area, Brazil's second-biggest. The Olympics will give the local region the opportunityto attend the events in August, and later, to use the sports, housing facilities and infrastructure built for the Games. The competitionvenues will be clustered in four connected zones: Barra, Copacabana, Deodoro and Maracanã. Only seven of the 34 competition venueswill be temporary, while the rest were either already operational or were built for the Olympics.

The Olympics count on several sponsors and partners, which provided more than BRL3 billion of sponsorship quotes (see AppendixA). The International Olympic Committee (IOC) estimates that 52% of the Olympics' funding comes from international and nationalsponsors. It represents the main source of funding followed by IOC contribution with 25% of total resources (see Exhibits 2-3).

MOODY'S INVESTORS SERVICE CROSS-SECTOR

3 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Exhibit 2

Sources of Funding for Rio OlympicsTotal BRL7.4 billion

Exhibit 3

OCOG Expenditures for Rio OlympicsTotal BRL7.4 billion

Source: Organizing Committee for the Olympic Games, Rio 2016 Note: Organizing Committee for the Olympic Games (OCOG)Source: Organizing Committee for the Olympic Games, Rio 2016

The Olympics are neutral for Brazil’s sovereign credit quality. The games will last just one month and the associated economic stimuluspale compared to Brazil’s economy, which contracted by 3.8% in 2015. We believe Brazil's economy will contract by another 3.7% in2016 before growing anemically in 2017-18. Overall, the impact of the 2016 Olympic Games will be more meaningful at the local level,with the infrastructure work to prepare the city for the competition and the period that the event takes place, with the activities thatwill support the athletes and tourists.

Olympics to Provide Rio With Lasting Infrastructure Improvements

The key benefit of the 2016 Olympics for the city of Rio will be lasting transport infrastructure improvements. These include a fourthmetro line linking the southern part of the city directly to the main Olympic park in Barra, and the VLT light rail project, which will helprevitalize Rio’s downtown area. With the exception of the new metro line, which was largely funded by Rio de Janeiro state, the cityfinanced the new infrastructure investments through an equal contribution from its own funds and federal transfers.

Rio’s debt is set to fall despite additional borrowing to fund these upgrades, thanks to a renegotiation of the city’s federal loans that islikely to take effect later this year. This will essentially reduce the city’s debt by a third, partly reversing a 47% increase between 2013and 2015. Adjusted for this reduction, Rio’s debt/operating revenue ratio as of the end of 2015 falls to 46% from the reported 73%, thelowest debt ratio of any Moody’s-rated Brazilian regional or local government.

The Olympics will also deliver a one-off boost to the city of Rio’s tax revenues, helped by an anticipated spike in tourist numbers.However, the positive impact on tax receipts will be temporary, and will only partly counterbalance Brazil’s economic contraction,which is set to continue in 2016.

Rio’s preparations for the Olympics have generally been well managed, and have been completed on time and on budget. The recentcollapse of a seaside bicycle path that left two people dead and three injured has exposed flaws in the planning and engineering ofinfrastructure process, which raises questions regarding the sustainability of other projects as well. While such tragic events temporarilyharm Rio’s reputation, we do not think they will reduce the city’s appeal to tourists in the long term.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

4 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Benefits from New Infrastructure Investment Have Already Begun

The Olympic games have generated nearly BRL25 billion worth of infrastructure investments in Rio’s metropolitan area, excludingspending on new sports facilities (see Appendix B). This is on a par with the BRL26 billion of infrastructure investment in the run-up tothe 2014 soccer World Cup in Brazil, which was spread across 12 cities. Investment related to the 2016 Olympics has focused on urbantransport, toll roads, ports and energy. Most of these projects are now complete, and their economic benefits are already emerging.

Subway operator Concessão Metroviária do Rio de Janeiro S/A (Metrô Rio, Ba2 negative) and toll-road operator Linha Amarela S.A(LAMSA, Ba2 negative) will both benefit from an increase in traffic volumes during the games, driven by an expected influx of tourists.LAMSA is particularly well-positioned to benefit from the tourist influx because it operates a toll road linking the international airportto the main Olympic park in Barra in the south of Rio. However, a reduction in commuter traffic during the games will partly offset thehigher volume of tourist travelers using the metro and LAMSA roadways.

The VLT project, an urban tramway linking the Santos Dumont domestic airport to Rio’s main business area, will reduce trafficcongestion and facilitate business commuting. Traffic volumes might initially be slow, but we expect them to pick up in the mediumterm, supporting the project’s cash flows and benefiting its main sponsors CCR S.A. (Ba3 negative), Invepar (B1 negative), OdebrechtTransport (unrated) and Riopar Participações (unrated).

The same sponsors, except for Riopar, are behind the Transolímpica, an express motorway for public buses connecting thesouthwestern part of the city to the northern Deodoro Olympic park. The commercial prospects of this project are less certain. Whilewe expect the motorway will be used heavily during the games, it is unclear whether high traffic volumes over this less economicallydeveloped area can be sustained during the medium to long term.

In order to ensure adequate energy supply during the games, Rio’s energy distributor Light Servicos De Eletricidade S.A. (Ba3 negative)made BRL400 million worth of investments in high and medium voltage power projects which together account for about 16% of thecompany’s total investments since 2013. The company’s return on investment looks set to be delayed as Brazil’s deepening economicrecession results in lower-than-expected energy demand and the next tariff review is only scheduled for November 2018. But weexpect that Light will receive some compensation for its investment costs through a plea for an extraordinary tariff increase made tothe federal power regulator ANEEL in February 2016.

Loans to Finance Olympic Projects Will Have Limited Impact on Banks

The Olympic games have represented neither a significant business opportunity nor a significant risk for Brazilian banks, with onlygovernment-owned lenders playing a meaningful role in providing financing. Instead, the games primarily received funding from boththe federal and municipal governments.

Total bank loans to finance infrastructure and the Cidade Olímpica athletes' village for the Rio Olympics amount to small fractionsof the outstanding loans at participating banks, which include Banco Nacional de Desenvolvimento Econômico e Social (BNDES, Ba2negative, ba2) and Caixa Economica Federal (Caixa, Ba2/Ba2 negative, ba3).1 As a result, these exposures will have little or no impacton the banks’ creditworthiness.

BNDES, Brazil's federal development bank, has provided the most bank funding for the Rio Olympics, particularly for legacyinfrastructure projects. In March 2013, BNDES approved a BRL4.3 billion credit line for the construction of a metro line that willconnect the Olympic Park to the tourist zone in southern Rio, and reported in May 2015 its total financing of the project amounted toBRL 6.6 billion. In March 2016, the bank extended a further BRL1 billion to complete the project in March 2016. BNDES also approved aBRL2.7 billion credit line to the Municipality of Rio de Janeiro in June 2014 for various urban mobility projects.2 In total, however, thesecredit lines represented just 1.5% of the exposures in BNDES’s BRL700 billion loan book as of December 2015.

Exposures at Caixa, a state-owned savings and loan predominantly focused on mortgage lending, are even smaller. The bank hasextended a BRL2.3 billion loan to finance the construction of Cidade Olímpica—an amount that represents just 0.3% of Caixa'sBRL684 billion total loan operations as of March 2016.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

5 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Companies Can Expect Brief Sales Boost but No Big Change in Earnings

Overall the Olympic Games will have a minimal impact on most non-financial companies, limited to short-lived sales increases andthe intangible benefits of marketing exposure at the event’s games (see Exhibit 4). The Brazilian government expects at least 350,000people from abroad to visit Rio during the Olympics in August and the Paralympic Games in September, which compares to 470,000foreign visitors in Rio during the 2014 World Cup. Yet any benefit to Brazil’s economy and companies will depend on the actualnumbers of visitors willing to go to Rio de Janeiro in August. The slowdown in the domestic economy, with rising unemployment, highinflation and interest rates reduces consumption and travel at home, and may limit the attendance of the local population in Brazil tothe games.

Exhibit 4

2016 Olympic Games, Benefit by Corporate Sector

Source: Moody's Investors Service

Globo Gets Big Boost from Advertising Sponsorships

The Olympics will increase the audience for Brazilian broadcasters, especially for Brazil’s leading television broadcaster GloboComunicacao e Participacoes S.A. (Ba1 negative), which will broadcast all events through its channels, including open air, pay-TV, andinternet.

Globo has already sold out its 2016 Olympic Games advertising space to six sponsors: Nestlé (Aa2 stable), Coca-Cola (Aa3 stable),Procter & Gamble (Aa3 stable), Banco Bradesco (Ba2/Ba2 negative, ba2), Fiat (Ba3 stable) and Claro (unrated). Media reports sayeach of these contracts is worth about BRL250 million, totaling BRL1.5 billion in revenues during the Olympics, an amount totallingabout 10% of Globo's 2015 revenues. Globo has acquired the rights to broadcast the Olympic Games until 2032, including severaldistribution platforms such as open-air, pay-TV, internet and mobile, to be paid in installments.

Food and Beverage Producers Get Ready for Big Marketing Opportunity

The Olympics will give consumer goods companies sponsoring the event an opportunity to increase brand visibility and marketingexposure, but will not bring significant incremental changes in sales volumes for food and beverage for companies in Brazil.

Ambev S.A. (Baa3 negative) will be an official supporter of the Rio Olympics, part of an effort to help secure its share of a beer marketfacing declining sales volumes amid high inflation and lower disposable income. In 2015, Ambev’s beer sales volumes in Brazil declined1.8%, while Brazilian market volume dropped 2.0%. Even so, Ambev's revenues increased 9.6% and reported EBITDA margin increasedby 1.1% through effective marketing, pricing strategies and cost-cutting.

Although we don’t expect the Olympics to give Ambev a significant increase in sales volumes, it will offer a significant advertisingplatform to promote its core brand Skol. The core beer segment has seen the greatest drop in volume in the Brazilian beverage market,but Ambev has historically improved its sales mix and preserved profitability through its strong distribution and brand activationcapabilities.

Like Ambev, processed-foods companies such as BRF S.A. (Ba1 negative) will see little increase in sales volumes from the Olympics,but will benefit from huge marketing exposure. BRF is also an official supporter of both the Olympic and Paralympic games throughits premium brand Sadia. We expect increased brand awareness and potential market-share gains, which will likely help supportprofitability in Brazil's challenging consumer environment. The company, with a 63% share of Brazil's processed-foods market,generates 50% of its revenues in Brazil, and 51% from its processed-foods and food services portfolio.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

6 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

The Olympics will be credit neutral for restaurant operator Arcos Dorados Holdings Inc. (B1 negative). The top owner of fast-foodrestaurants in Latin America and the Caribbean and the largest McDonald's francisee worldwide is highly exposed to Brazil, where itgenerates 60% of its EBITDA. The 2014 World Cup tournament drew spectators to Arcos Dorados' quick-service restaurants in 12Brazilian cities. The Olympics will take place in only one city, which limits the company's benefit from a surge of visitors.

Foreign Visitors Will Give Payment Processors Boost

Payment processors such as Cielo S.A. (Ba1 negative) will benefit from retail activity from the Olympics, bringing extra volume intransactions, especially in foreign currency brought in by overseas tourists. Acquirers will take advantage of the event to acceleratepenetration of point-of-sale terminals to meet the demand of foreign tourists that prefer to pay for goods and services with credit anddebit cards. Brand promotion by Visa Inc. (A1 stable), an official Olympic Games sponsor, will also increase merchants' demand forpoint-of-service terminals, but market-leader Cielo will benefit most.

Flood of Travelers Will Raise Profits for Airlines and Car Rental Companies

The Olympics and Paralympics will temporarily boost demand for flights and car rentals, giving airlines and car-rental companies achance to increase prices and raising their profitability. The regional airlines have been adjusting capacity both within and to the regionto accommodate the Olympic and Paralympic spectators, and in response to Brazil's overall weak economic demand trends. TamLinhas Aereas S.A., a subsidiary of Chile's LATAM Airlines Group S.A. (B1 stable), stands to gain from brand awareness as the officialcarrier of the International Olympic Committee members. LATAM has flown officials carrying the Olympic torch in the traditional 100-day ceremony from the original flame from Olympia, in Greece, to the games in Rio.

The Olympics will reinforce LATAM's dominant market position in Latin America, with network connectivity and strategic alliances thatput them in the best position to benefit from the increased demand around the games. LATAM has the largest market share in Brazil'sinternational hubs, particularly Guarulhos in São Paulo and Brasília, Brazil's capital city—the main arrival destinations for athletes andtourists who will be visiting.

Rental car companies will also benefit from tourists' need to travel within Rio and to other Brazilian cities during their trip to Brazil.Localiza Rent a Car S.A. (Ba2 negative), the official car rental supplier of the Olympic Games, is best positioned because of its dominantmarket position. The company has strategic store locations across the country that grant access to both on- and off-airport markets.The flow of tourists and delegations of athletes that will not only be based in Rio, but also spread around the country during thetournament that according to our estimates should generate a demand for additional 1,000 cars during the Olympic Games periodrepresenting about 1.5% of the company’s car rental fleet.

Olympic Boom in Engineering and Construction is Over

Brazil's engineering and construction companies have generated about BRL31 billion in investment related to the Olympics in Rio,including the construction or renovation of arenas and stadiums, lodging for athletes, and upgrades to Rio’s logistic infrastructure andurban mobility developments. But most of the projects for these improvements began in recent years and are now completed or nearlycompleted, so the engineering and construction companies have already absorbed most of their Olympic-related benefits.

The two major Brazilian heavy construction companies, Odebrecht Engenharia e Construção S.A. (B2 review for downgrade) andAndrade Gutierrez Engenharia S.A. (B2 negative), have been involved in almost all major Olympic projects, including Parque Olímpico,Transolímpica, the Transbrasil BRT rapid bus transit system, and the renewal of the Maracanã stadium. Nevertheless, total investmentsfor Olympics-related projects comprised only about 5% of their revenues over the last three years since 2013.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

7 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Appendix A: Rio 2016 Olympic Partners and Official Providers/Suppliers

Exhibit 5

Rio 2016 Partners and Official Providers/Suppliers

Source: Organizing Committee for the Olympic Games, Rio 2016

MOODY'S INVESTORS SERVICE CROSS-SECTOR

8 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Appendix B: Key Infrastructure Projects

Exhibit 6

Key infrastructure projects

Source: Federal Government, Metro Linha 4 and VLT Carioca

MOODY'S INVESTORS SERVICE CROSS-SECTOR

9 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Moody's Related ResearchSector In-Depth Reports:

» Sector In-Depth: Sovereigns – Latin America: Evolution of Fiscal Space and Implications for Policy Response, 4 May 2016

» Corporate Liquidity - Brazil: Funding Becomes More Challenging and Liquidity Risk Increases, 2 May 2016

» Cross Sector - Brazil: FAQ on the Real Estate Market Outlook, 27 April 2016

» Banks - Brazil: Restructured Loans Mask Rising Asset Risk, 11 April 2016

» Banks - Brazil: Market Swings Raise Asset Quality and Profitability Concerns, 4 April 2016

» Banks - Brazil: Macro Profile – Moderate, 4 March 2016

» Non-Financial Corporate Sector - Brazil: Deteriorating Domestic Fundamentals Will Test Liquidity in 2016-17, 24 November 2015

» Sovereign Risk Report: Brazil’s Economic Woes Push Sovereign Risk Higher, 19 October 2015

» Credit Quality in Brazil: Economic, Political Stress Roil Issuers in Both Public and Private Sectors, 6 October 2015

» Latin America: Global Headwinds Pressure Credit Conditions in Region, 2 September 2015

» 2014 FIFA World Cup Brazil: A Quick Score for the Beverage, Travel, Construction and Broadcast Sectors, 30 March 2014

» London 2012 Olympics Provide a Short-term Boost, But No Gold Medal for Corporates, 1 May 2012

Rating Action:

» Moody's downgrades Brazil's issuer and bond ratings to Ba2 with a negative outlook, 24 February 2016

Outlooks:

» Moody's Latin America 2016 Outlook (Presentation), 6 April 2016

» Sovereigns – Latin America and the Caribbean: Mixed Rating Outlook Reflects Lower Trend Growth and Moderate Fiscal Space, 5April 2016

» Non-Financial Corporates – Latin America: 2016 Outlook - Global and Regional Stresses Strain Credit Quality (Presentation), 3December 2015

Banking System Profile:

» Banking System Profile: Brazil, 28 December 2015

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of thisreport and that more recent reports may be available. All research may not be available to all clients.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

10 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Endnotes1 These ratings represent the local currency deposit ratings for Caixa, and the senior unsecured debt ratings and baseline credit assessments (BCAs) for both

banks.

2 These projects include the BRT Transoeste; the Via Expressa Transolímpica; the connection between BRT Transolímpica-BRT Transbrasil; the surroundingsof the Olympic Park; duplicating the Elevado das Bandeiras; the Ciclovia Niemeyer; the extension of the Via Expressa to Porto Maravilha; and thesurroundings of Engenhão.

MOODY'S INVESTORS SERVICE CROSS-SECTOR

11 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1023113

MOODY'S INVESTORS SERVICE CROSS-SECTOR

12 16 May 2016 2016 Olympics – Rio de Janeiro: Games Offer Lasting Benefits for City but Only Brief Gains for Brazilian Companies

Contributors

Barbara Mattos, CFA 55-11-3043-7357VP-Sr Credit [email protected]

Paco Debonnaire [email protected]

Farooq Khan [email protected]

Alexandre Leite 55-11-3043-7353VP-Sr Credit [email protected]

Veronica Amendola 54-11-5129-2610VP-Senior [email protected]

Erick Rodrigues 55-11-3043-7345VP-Senior [email protected]

Marcos Schmidt 55-11-3043-7310VP-Senior [email protected]

Cristiane Spercel 55-11-3043-7333VP-Senior [email protected]

Sabrina Mascher DeLima

55-11-3043-7352

Associate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454