section 2.07 - freddie mac relief refinance mortgage freddie mac relief refinance mortgage sm is a...

TRANSCRIPT

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 1 of 49Broker Seller Guide

Section 2.07 - Freddie Mac Relief Refinance MortgageSM

In This Product Description

This product description contains the following topics:

Overview ....................................................................................................................... 3 Product Summary ..................................................................................................... 3 Features and Benefits .............................................................................................. 5

Related Bulletins .......................................................................................................... 5

Existing Mortgage Eligibility Requirements ............................................................. 6 Existing Investor and Servicer Requirements .......................................................... 6 Ineligible Existing Mortgages .................................................................................... 6 Existing Mortgage Payment History Requirements .................................................. 6

Loan Terms ................................................................................................................... 7 Loan Term ................................................................................................................ 7 Minimum Loan Amount ............................................................................................. 7 Maximum Loan Amount ............................................................................................ 8 Maximum LTV/TLTV/HTLTV, Primary Residence .................................................... 9 Maximum LTV/TLTV/HTLTV, Second Homes ....................................................... 10 Maximum LTV/TLTV/HTLTV, Investment Properties ............................................. 11 ARM Parameters .................................................................................................... 12 Interest Only Parameters ........................................................................................ 12 Maximum Number of Financed Properties ............................................................. 12

Eligible Transactions ................................................................................................. 13 General ................................................................................................................... 13

Eligible Transactions, Continued ............................................................................. 14 Tangible Net Benefit Requirements........................................................................ 15

Secondary Financing ................................................................................................ 16 General ................................................................................................................... 16

Geographic Restrictions ........................................................................................... 18 General ................................................................................................................... 18

Occupancy/Property Types ...................................................................................... 19 Agency .................................................................................................................... 19 Agency Plus ............................................................................................................ 21

Eligible Borrowers ..................................................................................................... 23 General ................................................................................................................... 23

Income ........................................................................................................................ 25 Income Documentation Requirements ................................................................... 25

Qualifying Guidelines ................................................................................................ 25 Qualifying Rate ....................................................................................................... 25 Qualifying Ratios – Agency .................................................................................... 26 Qualifying Ratios – Agency Plus ............................................................................ 27

Credit Requirements ................................................................................................. 28 Credit Score Requirements – Agency .................................................................... 28 Credit Score Requirements – Agency Plus ............................................................ 29 Credit History Analysis ........................................................................................... 31

Cash Requirements ................................................................................................... 32

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 2 of 49Broker Seller Guide

General ................................................................................................................... 32 Cash Reserves ....................................................................................................... 32 Gifts ........................................................................................................................ 32

Contributions by Interested Parties ......................................................................... 33 Lender Credits ........................................................................................................ 33 Temporary Interest Rate Buydowns ....................................................................... 33

Mortgage Insurance ................................................................................................... 34 General ................................................................................................................... 34

Documentation Requirements .................................................................................. 35 General ................................................................................................................... 35

Appraisal Requirements ........................................................................................... 36 General ................................................................................................................... 36

Appraisal Requirements, Continued........................................................................ 37 Home Value Explorer® (HVE) Requirements ........................................................ 37

AUS Submissions, Recommendations and Tolerances ........................................ 38 General ................................................................................................................... 38

Workflow ..................................................................................................................... 39 General ................................................................................................................... 39 Fidelity Snapshot – STM to STM Transactions ...................................................... 40 Home Valuation Explorer® (HVE) Documentation Procedures ............................. 41 **STM Internal Information ONLY**........................................................................ 41 Submission to Loan Prospector (LP) ...................................................................... 42 Pricing ..................................................................................................................... 42 Step for Determining Maximum Loan Amount ....................................................... 42 STMPartners ........................................................................................................... 42 PUD Review – STM to STM Transactions ............................................................. 43 PUD Review – Non-STM to STM Transactions ..................................................... 43 Mortgage Insurance - STM to STM Transactions .................................................. 43 Subordination of SunTrust Second Mortgages ...................................................... 43 Referrals to SunTrust’s Loss Mitigation Department - STM to STM Transactions 43 Referrals from SunTrust’s Loss Mitigation Department – STM to STM Transactions ................................................................................................................................ 43 Referrals to SunTrust’s Consumer Direct Department ........................................... 44 Principal Curtailments at Closing ............................................................................ 44

Application Disclosures and Issues ........................................................................ 45 Consumer Handbook on Adjustable Rate Mortgages ............................................ 45 Program Disclosures .............................................................................................. 45 Other Loan Application and Compliance Issues .................................................... 45

MLCS Loan Setup and Processing .......................................................................... 46 Appraisal Codes ..................................................................................................... 46 AUS Used ............................................................................................................... 46 Condominium Project Type Code ........................................................................... 46 Processing Type ..................................................................................................... 46 Program Codes – Agency ...................................................................................... 47 Program Codes – Agency Plus .............................................................................. 47 SunTrust to SunTrust Refinance and STM Refi Loan Number Fields ................... 48 Target Investor Code .............................................................................................. 48

Closing and Loan Settlement Documentation ........................................................ 49 Closing Legal Documents ....................................................................................... 49 Escrow Waiver ........................................................................................................ 49

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 3 of 49Broker Seller Guide

Overview

Product Summary

The Freddie Mac Relief Refinance Mortgage SM is a loan program created to support the “Making Home Affordable Initiative.” This loan program provides expanded opportunities for borrowers who have demonstrated an acceptable payment history on their Freddie Mac owned or guaranteed mortgage, but have not been able to refinance due to declining property values or an inability to obtain mortgage insurance. Eligible loan products available under the Freddie Mac Relief Refinance Mortgage loan program include the following: • Agency Fully Amortizing Fixed Rate, • Agency Fully Amortizing 5/1, 7/1 & 10/1 LIBOR ARMs, • Agency Plus Fully Amortizing Fixed Rate, and • Agency Plus Fully Amortizing 5/1, 7/1 & 10/1 LIBOR ARMs. Note: Loans with 10 and 40 year terms, 3/1 LIBOR ARMs, Interest Only (Fixed Rate and ARMs), and Texas 50(a)(6) loans are NOT eligible. ALL Freddie Mac Relief Refinance Mortgages MUST be processed through Freddie Mac’s Loan Prospector (LP) and receive an “Accept/Eligible” recommendation. Freddie Mac Relief Refinance Mortgage transactions that are traditionally underwritten, receive a LP “Caution” recommendation or processed through Fannie Mae’s Desktop Underwriter (DU) or SunTrust’s Custom Desktop Underwriter (CDU) are NOT eligible. Notes: • The Freddie Mac Relief Refinance Mortgage Eligibility Checklist (STM to STM)

(BRO 1380) or the Freddie Mac Relief Refinance Mortgage Eligibility Checklist (Non-STM to STM) (BRO 1415) and Freddie Mac Relief Refinance Maximum Allowable Financed Closing Costs, Financing Costs, and Prepaids/Escrows (BRO 0008) worksheet is REQUIRED to be completed and placed in the loan file to ensure that the loan is being originated within the guidelines of the Freddie Mac Relief Refinance Mortgage program.

• Borrowers who are refinancing an existing SunTrust first mortgage (STM to STM transactions) who fall outside of the Freddie Mac Relief Refinance loan parameters outlined in this product description, but are at risk of “imminent default”, should be referred to SunTrust’s Loss Mitigation Department (1-800-443-1032, Option #3) to review loan modification options. • A risk of “imminent default” may exist when a borrower has suffered a valid

hardship that impacts their ability to pay their mortgage in the near future, generally 90 days from the initial discussion with the borrower.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 4 of 49Broker Seller Guide

Overview, Continued Product Summary, (continued)

Notes, (continued) • Borrower’s who are refinancing an existing SunTrust first mortgage (STM to

STM transactions) and who fall outside of the Freddie Mac Relief Refinance Mortgage loan parameters outlined in this product description, but are NOT currently at risk of “imminent default,” should be referred to SunTrust’s Consumer Direct Department (1-800-330-4684) for further loan processing. Reference: See the “Workflow” topic subsequently presented in this product description for workflow procedures for loan referrals to SunTrust’s Loss Mitigation and Consumer Direct Departments.

Unless otherwise stated, all guidelines outlined in this product description will apply to both standard Agency and Agency Plus Freddie Mac Relief Refinance transactions. GUIDELINES NOT ADDRESSED IN THIS PRODUCT DESCRIPTION WILL FOLLOW STANDARD AGENCY LOAN PROSPECTOR (LP) GUIDELINES. Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for standard Agency LP guidelines.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 5 of 49Broker Seller Guide

Overview, Continued

Features and Benefits

Features and benefits of the Freddie Mac Relief Refinance Mortgage loan program include the following:

Feature Benefit Expanded LTVs for fixed rate transactions with a 15, 20, or 30 year loan term are available.

Provides financing opportunities for borrowers who owe more than their home is worth due to the decline in property values.

• Mortgage Insurance (MI) is not required for transactions where the original LTV was 80% or less.

• For transactions where the original LTV was greater than 80%, allows the level of MI coverage in force on the existing mortgage loan.

Note: Available for borrowers who are refinancing an existing SunTrust first mortgage ONLY (STM to STM transactions)

Flexible MI guidelines eliminate the requirement for borrowers to purchase new or additional MI coverage on the new loan.

Fixed Rate, 5/1, 7/1 and 10/1 LIBOR ARM loan products available.

Allows borrowers to obtain a more stable mortgage product to ensure long-term homeownership sustainability.

AUS eligibility Streamlined efficiencies and reduced documentation requirements of AUS processing.

Related Bulletins General

Related bulletins are provided below in PDF format. To view the list of published bulletins, select the applicable year below. • 2012 • 2011 • 2010 • 2009

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 6 of 49Broker Seller Guide

Existing Mortgage Eligibility Requirements

Existing Investor and Servicer Requirements

• The existing mortgage MUST be a Freddie Mac owned or guaranteed first lien

mortgage.

Note: The existing mortgage must have been delivered to Freddie Mac prior to June 1, 2009.

• To help determine if the loan is Freddie Mac owned or guaranteed: • Utilize the Freddie Mac Self-Service Lookup tool, or

Note: A “Match Found” response to the search in the Freddie Mac Self-Service Lookup tool means that Freddie Mac owns a loan at the address entered in the search. It does not guarantee or imply that the borrower meets all eligibility criteria for the Freddie Mac Relief Refinance Mortgage loan program.

• Contact Freddie Mac at 1-800-FREDDIE (8am to 8pm EST).

• The existing servicer may be SunTrust Mortgage, Inc. or another lender. • The Fidelity Snapshot may be accessed by a SunTrust teammate to confirm that

SunTrust is servicing the existing first mortgage in order to follow guidelines for STM to STM transactions. The Fidelity Snapshot does not guarantee or imply borrower eligibility for the Freddie Mac Relief Refinance Mortgage loan program. The Fidelity Snapshot printout must be placed in the loan file and maintained as a part of the imaged loan file.

Note: An Excel spreadsheet titled Fidelity Loan Data Retriever is used to obtain the Fidelity Snapshot. Click here to access the Fidelity Loan Data Retriever tool.

Reference: See the “Workflow” topic subsequently presented in this product description for procedures for obtaining the Fidelity Snapshot.

Ineligible Existing Mortgages

Ineligible existing mortgages include the following: • Loans delivered to Freddie Mac on or after June 1, 2009, • Mortgage loans with pending or confirmed misrepresentation, • Loans that are currently subject to any outstanding repurchase request from

Freddie Mac, • Portfolio Affordable and Doctor loans, • Reverse mortgage loans, • Second mortgage loans, • Government mortgage loans, and • Texas 50(a)(6) loans.

Existing Mortgage Payment History Requirements

Reference: See “Credit History Analysis” in the Credit Requirements topic subsequently presented in this product description for existing mortgage payment history requirements.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 7 of 49Broker Seller Guide

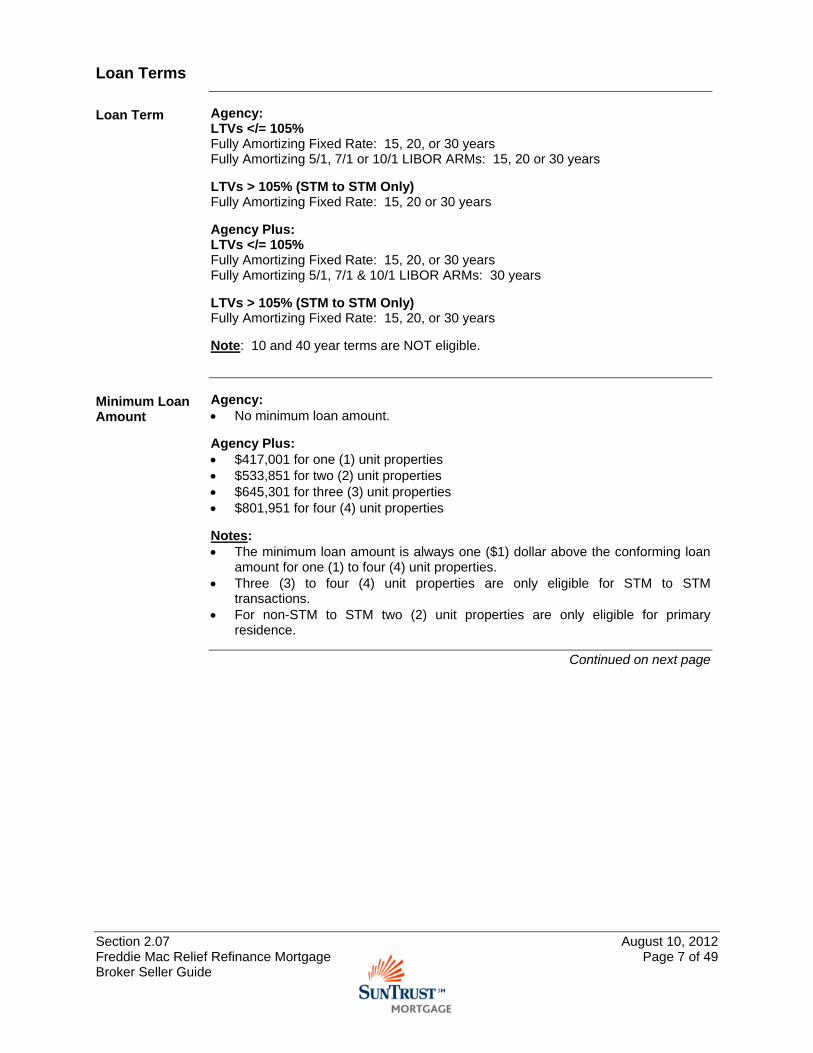

Loan Terms

Loan Term Agency: LTVs </= 105% Fully Amortizing Fixed Rate: 15, 20, or 30 years Fully Amortizing 5/1, 7/1 or 10/1 LIBOR ARMs: 15, 20 or 30 years LTVs > 105% (STM to STM Only) Fully Amortizing Fixed Rate: 15, 20 or 30 years Agency Plus: LTVs </= 105% Fully Amortizing Fixed Rate: 15, 20, or 30 years Fully Amortizing 5/1, 7/1 & 10/1 LIBOR ARMs: 30 years LTVs > 105% (STM to STM Only) Fully Amortizing Fixed Rate: 15, 20, or 30 years Note: 10 and 40 year terms are NOT eligible.

Minimum Loan Amount

Agency: • No minimum loan amount. Agency Plus: • $417,001 for one (1) unit properties • $533,851 for two (2) unit properties • $645,301 for three (3) unit properties • $801,951 for four (4) unit properties Notes: • The minimum loan amount is always one ($1) dollar above the conforming loan

amount for one (1) to four (4) unit properties. • Three (3) to four (4) unit properties are only eligible for STM to STM

transactions. • For non-STM to STM two (2) unit properties are only eligible for primary

residence.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 8 of 49Broker Seller Guide

Loan Terms, Continued

Maximum Loan Amount

Agency: • $417,000 for one (1) unit properties • $533,850 for two (2) unit properties • $645,300 for three (3) unit properties • $801,950 for four (4) unit properties Agency Plus: • Agency Plus loans are available ONLY in high cost areas (as defined by HUD). • The maximum loan amount will vary based on the location of the subject

property; however, will NEVER exceed: • $625,500 for one (1) unit properties, • $800,775 for two (2) unit properties, • $967,950 for three (3) unit properties, and • $1,202,925 for four (4) unit properties

Notes: • A copy of the applicable page from the above referenced look-up table

MUST be placed in the loan file as verification of the eligible area and the maximum loan amount.

• Three (3) to four (4) unit properties are only eligible for STM to STM transactions.

• For non-STM to STM two (2) unit properties are only eligible for primary residence.

Reference: See “Loan Terms” topic located in Section 2.03: Agency Plus Loan Program of the Broker Seller Guide for a link to the maximum loan limits.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 9 of 49Broker Seller Guide

Loan Terms, Continued

Maximum LTV/TLTV/HTLTV, Primary Residence

Agency: • LTVs </= 105%:

• Fully Amortizing Fixed Rate: 15, 20, or 30 years • Fully Amortizing 5/1, 7/1 or 10/1 LIBOR ARMs: 15, 20, or 30 years

• LTVs > 105% (STM to STM Only): • Fully Amortizing Fixed Rate: 15, 20, or 30 years

Agency Plus: • LTVs </= 105%:

• Fully Amortizing Fixed Rate: 15, 20, or 30 years • Fully Amortizing 5/1, 7/1 & 10/1 LIBOR ARMs: 30 years

• LTVs > 105% (STM to STM Only): • Fully Amortizing Fixed Rate: 15, 20, or 30 years

References: • See the “Minimum Loan Amount” and “Maximum Loan Amount” subtopics previously

presented in this product description for additional information regarding determining the minimum and maximum allowable loan amounts.

• See the “Geographic Restrictions” topic subsequently presented in this product description for additional information on state specific lending restrictions.

Loan Program

Product LTV/TLTV/HTLTV for LP Limited Cash-Out (Rate/Term) Refinance

STM to STM #

of Units

STM to STM Transactions

Non-STM to STM #

of Units

Non-STM to STM Transactions

(MI NOT REQUIRED on Original Loan)

Non-STM to STM Transactions

(MI REQUIRED on Original Loan)

Agency Fixed Rate 1-4 no max/no max/no max 1,2,3 1-4 95%/95%/95% 1,3 80%/95%/95% 1,3

Agency 5/1, 7/1 & 10/1 ARMs

1-4 105%/no max/no max1,2, 3 1-4 95%/95%/95% 1,3 80%/95%/95% 1,3

Agency Plus

Fixed Rate 1-4 no max/no max/no max 1,2,3

1 90%/90%/90% 1,3 80%/90%/90% 1,3

2 75%/75%/75% 1,3 75%/75%/75% 1,3

Agency Plus

5/1, 7/1 & 10/1 ARMs

1-4 105%/no max/no max1,2,3 1-2 75%/75%/75% 1,3 75%/75%/75% 1,3

1 LTV is the “loan-to-value” of the first mortgage to the value of the property. TLTV is the “total loan-to-value” of the first AND second mortgage to the value of the property (if second is HELOC, the outstanding balance is used to calculate the TLTV). HTLTV is the “HELOC total loan-to-value” of the first AND HELOC second mortgage to the value of the property (the total available credit line is used to calculate HTLTV). 2 There is no maximum TLTV or HTLTV limit for Freddie Mac Relief Refinance loan transactions. 3 Existing subordinate financing MUST be re-subordinated to maintain the first lien priority of the new Freddie Mac Relief Refinance Mortgage loan. New subordinate financing is NOT permitted in conjunction with the Freddie Mac Relief Refinance loan program. See the “Secondary Financing” topic subsequently presented in this product description for additional information regarding subordinations.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 10 of 49Broker Seller Guide

Loan Terms, Continued

Maximum LTV/TLTV/HTLTV, Second Homes

Agency: • LTVs</=105%:

• Fully Amortizing Fixed Rate: 15, 20, or 30 years • Fully Amortizing 5/1, 7/1 or 10/1 LIBOR ARMs: 15, 20 or 30 years

• LTVs > 105% (STM to STM Only): • Fully Amortizing Fixed Rate: 15, 20, or 30 years

Agency Plus: • LTVs</=105%:

• Fully Amortizing Fixed Rate: 15, 20, or 30 years • Fully Amortizing 5/1, 7/1 & 10/1 LIBOR ARMs: 30 years

• LTVs > 105% (STM to STM Only): • Fully Amortizing Fixed Rate: 15, 20, or 30 years

References: • See the “Minimum Loan Amount” and “Maximum Loan Amount” subtopics previously

presented in this product description for additional information regarding determining the minimum and maximum allowable loan amounts.

• See the “Geographic Restrictions” topic subsequently presented in this product description for additional information on state specific lending restrictions.

Loan Program

Product LTV/TLTV/HTLTV for LP Limited Cash-Out (Rate/Term) Refinance

STM to

STM # of

Units

STM to STM Transactions

Non-STM to STM #

of Units

Non-STM to STM Transactions

(MI NOT REQUIRED on Original Loan)

Non-STM to STM Transactions

(MI REQUIRED on Original Loan)

Agency Fixed Rate 1 no max/no max/no max1, 2, 3 1 90%/90%/90%1, 3 80%/90%/90%1, 3

Agency 5/1, 7/1 & 10/1 ARMs

1 105%/no max/no max1, 2, 3 1 90%/90%/90%1, 3 80%/90%/90%1, 3

Agency Plus

Fixed Rate 1 no max/no max/no max1, 2, 3 1 65%/65%/65%1, 3 65%/65%/65%1, 3

Agency Plus

5/1, 7/1 & 10/1 ARMs

1 105%/no max/no max1, 2, 3 1 65%/65%/65%1, 3 65%/65%/65%1, 3

1 LTV is the “loan-to-value” of the first mortgage to the value of the property. TLTV is the “total loan-to-value” of the first AND second mortgage to the value of the property (if second is HELOC, the outstanding balance is used to calculate the TLTV). HTLTV is the “HELOC total loan-to-value” of the first AND HELOC second mortgage to the value of the property (the total available credit line is used to calculate HTLTV). 2 There is no maximum TLTV or HTLTV limit for Freddie Mac Relief Refinance loan transactions. 3 Existing subordinate financing MUST be re-subordinated to maintain the first lien priority of the new Freddie Mac Relief Refinance Mortgage loan. New subordinate financing is NOT permitted in conjunction with the Freddie Mac Relief Refinance loan program. See the “Secondary Financing” topic subsequently presented in this product description for additional information regarding subordinations.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 11 of 49Broker Seller Guide

Loan Terms, Continued

Maximum LTV/TLTV/HTLTV, Investment Properties

Agency: • LTVs </= 105%:

• Fully Amortizing Fixed Rate: 15, 20, or 30 years • Fully Amortizing 5/1, 7/1 or 10/1 LIBOR ARMs: 15, 20, or 30 years

• LTVs > 105% (STM to STM Only): • Fully Amortizing Fixed Rate: 15, 20, or 30 years

Agency Plus: • LTVs </= 105%:

• Fully Amortizing Fixed Rate: 15, 20, or 30 years • Fully Amortizing 5/1, 7/1 & 10/1 LIBOR ARMs: 30 years

• LTVs > 105% (STM to STM Only): • Fully Amortizing Fixed Rate: 15, 20 or 30 years

References: • See the “Minimum Loan Amount” and “Maximum Loan Amount” subtopics previously

presented in this product description for additional information regarding determining the minimum and maximum allowable loan amounts.

• See the “Geographic Restrictions” topic subsequently presented in this product description for additional information on state specific lending restrictions.

Loan Program

Product

LTV/TLTV/HTLTV for LP Limited Cash-Out (Rate/Term) Refinance

STM to STM #

of Units

STM to STM Transactions

Non-STM

to STM #

of Units

Non-STM to STM Transactions

(MI NOT REQUIRED on Original Loan)

Non-STM to STM Transactions

(MI REQUIRED on Original Loan)

Agency Fixed Rate 1-4 no max/no max/no max1,2,3 1-4 75%/75%/75%1, 3 75%/75%/75%1, 3

Agency 5/1, 7/1 & 10/1 ARMs

1-4 105%/no max/no max1,2,3 1-4 75%/75%/75%1, 3 75%/75%/75%1, 3

Agency Plus Fixed

Rate 1-4 no max/no max/no max1,2,3 1 65%/65%/65%1, 3 65%/65%/65%1, 3

Agency Plus

5/1, 7/1 & 10/1 ARMs

1-4 105%/no max/no max1,2,3 1 65%/65%/65%1, 3 65%/65%/65%1, 3

1 LTV is the “loan-to-value” of the first mortgage to the value of the property. TLTV is the “total loan-to-value” of the first AND second mortgage to the value of the property (if second is HELOC, the outstanding balance is used to calculate the TLTV). HTLTV is the “HELOC total loan-to-value” of the first AND HELOC second mortgage to the value of the property (the total available credit line is used to calculate HTLTV). 2 There is no maximum TLTV or HTLTV limit for Freddie Mac Relief Refinance loan transactions. 3 Existing subordinate financing MUST be re-subordinated to maintain the first lien priority of the new Freddie Mac Relief Refinance Mortgage loan. New subordinate financing is NOT permitted in conjunction with the Freddie Mac Relief Refinance loan program. See the “Secondary Financing” topic subsequently presented in this product description for additional information regarding subordinations.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 12 of 49Broker Seller Guide

Loan Terms, Continued

ARM Parameters

Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for 5/1, 7/1 and 10/1 LIBOR ARM parameter guidelines.

Interest Only Parameters

Interest only transactions are NOT eligible under the Freddie Mac Relief Refinance loan program.

Maximum Number of Financed Properties

The table below provides guidelines for the maximum number of financed properties for Agency and Agency Plus Freddie Mac Relief Refinance Mortgage transactions.

STM to STM Transactions Non-STM to STM Transactions

• For primary residence transactions, there is no limit to the maximum number of financed properties a borrower may own (individually or jointly).

• For second home and investment property transactions, each borrower individually and all borrowers collectively may not own more than four (4) unit properties, including the subject property.

• Regardless of the occupancy type, the maximum dollar exposure is limited to $2.5 million.

Guidelines outlined in Section 1.20: Maximum Number of Financed Properties and Borrower Exposure of the Broker Seller Guide apply. Reference: See Section 1.20: Maximum Number of Financed Properties and Borrower Exposure, of the Broker Seller Guide, for additional information.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 13 of 49Broker Seller Guide

Eligible Transactions

General • All Freddie Mac Relief Refinance Mortgage loans MUST be originated as a

limited cash-out (rate/term) refinance transaction. • Purchase money, cash-out refinance, construction-permanent (one time and two

time closings) and streamline refinance transactions are NOT eligible. • The table below provides limited cash-out refinance guidelines for Agency and

Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

• The proceeds of the new mortgage must be only used to pay off the first mortgage (amount including only the unpaid principal balance and interest accrued through the date the mortgage being refinanced is paid off). Note: Existing purchase money subordinate financing may NOT be paid off with the proceeds of the Freddie Mac Relief Refinance Mortgage loan. All existing subordinate financing must be re-subordinated to maintain the first lien priority of the new Freddie Mac Relief Refinance Mortgage loan.

• For LTVs </= 80%, the following requirements apply: • The borrower may finance in all closing cost, financing cost and

prepaid escrows. • The borrower may receive no more than the lesser of 2% of the

balance of the new refinance mortgage or $2,000 cash back at closing.

• If there is excess cash greater than the guideline above, the loan amount must be recalculated and new documents must be drawn. Principal curtailments are not allowed regardless of the amount.

• For LTVs > 80%, the following requirements apply: • The borrower may finance up to a maximum of the lesser of 4%

of the unpaid principal balance of the mortgage being refinanced or $5000 in closing costs, financing costs, and prepaids/escrows.

• The borrower may receive up to $250 cash back at closing. • If there is excess cash greater than $250, the loan amount must

be recalculated, the loan must be re-approved and new documents must be drawn. Principal curtailments are not allowed regardless of the amount.

• The loan amount cannot exceed the maximum allowable loan amount as evidenced on the Freddie Mac Relief Refinance Maximum Allowable Financed Closing Costs, Financing Costs, and Prepaids/Escrows (BRO 0008) worksheet.

STM to STM guidelines apply.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 14 of 49Broker Seller Guide

Eligible Transactions, Continued

General, (continued)

STM to STM Transactions Non-STM to STM Transactions

Notes: • The Freddie Mac Relief Refinance Maximum Allowable Financed

Closing Costs, Financing Costs, and Prepaids/Escrows (BRO 0008) worksheet must be completed and a copy maintained in the loan file.

• Additional credit overlays may apply for transactions where existing subordinate financing is being re-subordinated.

References: • See the “Steps for Determining Maximum Loan Amount” subtopic

subsequently presented in the Workflow topic in this product description for additional information.

• See Section 1.21a: Subordinations for DU Refi Plus and Freddie Mac Relief Refinance Mortgage of the Broker Seller Guide for specific credit overlays and workflow procedures for the subordination of SunTrust second mortgages.

See previous page for information.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 15 of 49Broker Seller Guide

Eligible Transactions, Continued

Tangible Net Benefit Requirements **STM Internal Information ONLY**

The table below provides information regarding Tangible Net Benefit Requirements for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

A Tangible Net Benefit Analysis (BRO 1362) form must be completed on ALL Freddie Mac Relief Refinance transactions in order to document that the borrower is receiving a benefit in the form of either: • A reduction of the interest rate of the new first mortgage, • A reduction in the monthly principal and interest payment of the

first-lien mortgage. • Replacement of an ARM, Interest Only or a Balloon mortgage

with a fixed rate, fully amortizing mortgage, or

Note: If the mortgage being refinanced is a fixed-rate mortgage, the new mortgage may not be an ARM.

• Reduction in the amortization term of the new first mortgage.

Note: The new first mortgage may have a longer amortization term than the existing mortgage if at least one of the other requirements is met.

Note: The above referenced form must be completed by a SunTrust Underwriter.

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 16 of 49Broker Seller Guide

Secondary Financing

General

The table below provides general information on secondary financing for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

• There is no maximum TLTV or HTLTV limit for Freddie Mac Relief Refinance Mortgage primary residence and second home transactions. Note: See the “Loan Terms” topic previously presented for investment property TLTV/HTLTV restrictions.

• If subordinate financing exists, the existing subordinate financing MUST be re-subordinated to maintain the first lien priority of the new Freddie Mac Relief Refinance Mortgage loan. Note: The existing secondary financing may be an Affordable Second.

• Subordinate financing may NOT be paid off with the proceeds of the Freddie Mac Relief Refinance Mortgage loan, regardless if the subordinate financing is a purchase money second.

STM Internal Information Only Note: On MLCS, SFC 583 MUST BE entered on screen M0B (process flow 05/14) in the field labeled “AGENCY SPECIAL FEATURE CODES” to confirm a subordinate Community Second/Affordable Second.

• No increase in the unpaid principal balance of any subordinate financing is

permitted. In addition, new subordinate financing is NOT permitted in conjunction with the Freddie Mac Relief Refinance Mortgage loan program. Reference: See Section 1.21a: Subordinations for DU Refi Plus and Freddie Mac Relief Refinance Mortgage of the Broker Seller Guide for specific credit overlays and workflow procedures for the subordination of SunTrust second mortgages.

• Borrowers are permitted to pay off or pay down an existing second mortgage from their own funds.

• TLTV is the “total loan-to-value” of the first AND second mortgage to the sales price/value of the property (if second is HELOC, the outstanding balance is used to calculate TLTV). HTLTV is the “HELOC total loan-to-value” of the first AND HELOC second mortgage to the sales price/value of the property (the total available credit line is used to calculate HTLTV).

• A copy of the second mortgage note (or financing agreement terms if second is a HELOC) is required for the loan file to confirm that the terms of the secondary financing meets Freddie Mac Relief Refinance Mortgage requirements.

Note: In lieu of the second mortgage not (or financing agreement) a letter from the lender, on their letterhead, may be obtained only if the subordinate lien is reported on the credit report. The letter must disclose the terms of secondary financing and confirm if the second lien is subject to a prepayment penalty and if so, outline the terms (i.e., prepayment period).

STM to STM guidelines apply with the following EXCEPTIONS: • See the “Loan

Terms” topic maximum LTV/TLTV/HTLTV limits.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 17 of 49Broker Seller Guide

Secondary Financing, Continued

General, (continued)

STM to STM Transactions Non-STM to STM

Transactions Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for additional information on documenting a modified HELOC.

• Secondary financing payments are included in the housing ratio. • SunTrust Mortgage accepts subordinate HELOCs with a balloon payment

in less than five years after the note date of the first lien, when the following guidelines are met: • We do not require actual payoff of the account, but the borrower does

need sufficient assets available to pay off the outstanding balance in addition to the required funds to complete the transaction.

• An underwriting team lead or an underwriting manager must review these loan transactions.

• Use the account information from the credit report to determine eligibility unless other documentation in the loan file reflects information that is more current.

• Currently published LTV/TLTV/HTLTV guidelines continue to apply.

Note: Closed-end second mortgages that have a balloon payment less than five years after the note date of the first lien is not eligible.

• Secondary financing which could impose a penalty for prepayment is

NOT acceptable unless: • the subordinate loan is a home equity line of credit (HELOC), and the

amount of the prepayment penalty, prepayment fee, account closure fee, account termination fee, etc. does not exceed $500.00, or

• the subordinate loan is a home equity line of credit (HELOC), or closed-end second mortgage where the lender paid for some or all of the borrower’s closing costs and allows the lender to recoup that closing costs if the borrower pays the HELOC or closed-end second mortgage off early, or

• the prepayment penalty clause has lapsed.

Notes: • Home Equity Loans subject to prepayment penalty is NOT acceptable

secondary financing unless the prepayment penalty clause has lapsed.

• The HELOC must be in compliance with all federal, state, and local laws.

• Recouped fees may be deemed a prepayment penalty under state laws, in which case the second loan/line would not be eligible for subordination.

See previous page for information.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 18 of 49Broker Seller Guide

Secondary Financing, Continued General, (continued)

STM to STM Transactions Non-STM to STM

Transactions • Secondary financing cannot be subject to wraparound terms. • Acceptable title evidence must be obtained showing all secondary

financing recorded and clearly subordinate to the first lien. • Monthly payment must, at a minimum, meet the interest due so that

negative amortization will not occur. If the rate is variable, payments must be constant every 12 months.

• Secondary financing subject to negative amortization is not acceptable. • Variable payments are acceptable if one (1) or more of the following

applies: • the first mortgage is a fixed rate, • the first mortgage is an ARM (regardless of the initial fixed rate

period), • the second mortgage is provided by the borrower’s employer under

an employer-assisted housing program, or • the second mortgage is a HELOC.

See previous page for information.

Geographic Restrictions

General Generally, standard Agency guidelines apply with the following exception: • Agency Plus loan amounts are available ONLY in high cost areas (as defined by

HUD). References: • See the “Maximum Loan Amount” subtopic previously presented in the “Loan

Terms” topic for additional information. • See Section 2.01: Agency Loan Programs of the Broker Seller Guide for

additional information regarding standard Agency geographic lending restrictions.

• See Section 1.11: Geographic State Restrictions of the Broker Seller Guide for SunTrust specific geographic lending restrictions and state specific predatory lending restrictions that may apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 19 of 49Broker Seller Guide

Occupancy/Property Types

Agency The table below provides occupancy/property type guidelines for Agency Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

• Eligible occupancy/property types include the following: • one (1) to four (4) unit primary residences (attached

or detached), • one (1) unit second homes (attached or detached),

provided the mortgage being refinanced was a second home transaction,

• one (1) to four (4) unit investment properties (attached or detached), provided the mortgage being refinanced was an investment property,

Notes: • If the mortgage being refinanced was

previously a second home or investment property and the borrower(s) is now disclosing that the property is a primary residence (i.e., borrower(s) on the note are now owner occupants), then evidence of primary residency must be documented in the loan file.

• It is acceptable for a borrower’s occupancy to change from a primary residence to a second home or investment property.

• condominiums and units in a PUD, and • modular housing.

Notes: • A PUD review/warranty is not required on Freddie

Mac Relief Refinance STM to STM transactions. • Condominium properties must be Fannie Mae

accepted, on SunTrust Mortgage’s Approved Condominium Project List, or warranted under the SunTrust Project Review process (i.e., Limited Project Review or Full Project Review).

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for warranty guidelines.

• The Certification of Project Compliance: Condominium Lender Warranties - Agency and Non-Agency Loan Products (BRO 0212b) must be completed and included in every Freddie Mac Relief Refinance loan file.

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for additional information.

• Eligible occupancy/property types include the following: • one (1) to four (4) unit primary

residences (attached or detached), • one (1) unit second homes (attached

or detached), provided the mortgage being refinanced was a second home transaction,

• one (1) to four (4) unit investment properties (attached or detached), provided the mortgage being refinanced was an investment property, Notes: • If the mortgage being refinanced

was previously a second home or investment property and the borrower(s) is now disclosing that the property is a primary residency (i.e., borrower(s) on the note are now owner occupants), then evidence of primary residence must be documented in the loan file.

• It is acceptable for a borrower’s occupancy to change from a primary residence to a second home or investment property.

• condominiums and units in a PUD, and • modular housing.

Notes: • On attached PUDs, a PUD

review/warranty is required. • Condominium properties must be

Fannie Mae accepted, on SunTrust Mortgage’s Approved Condominium Project List, or warranted under the SunTrust Project Review process (i.e., Limited Project Review or Full Project Review).

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for warranty guidelines.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 20 of 49Broker Seller Guide

Occupancy/Property Types, Continued Agency, (continued)

STM to STM Transactions Non-STM to STM Transactions • Manufactured homes are NOT eligible. • All other standard Agency occupancy/property

guidelines (i.e., ineligible occupancy/property type guidelines) apply.

Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for standard Agency occupancy/property guidelines.

Notes: (continued) • The Certification of Project Compliance:

Condominium Lender Warranties - Agency and Non-Agency Loan Products (BRO 0212b) must be completed and included in every Freddie Mac Relief Refinance loan file.

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for additional information.

• Manufactured homes are NOT eligible. • All other standard Agency occupancy/property

guidelines (i.e., ineligible occupancy/property type guidelines) apply.

Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for standard Agency occupancy/property guidelines.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 21 of 49Broker Seller Guide

Occupancy/Property Types, Continued

Agency Plus

The table below provides occupancy/property type guidelines for Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

• Eligible occupancy/property types include the following: • one (1) to four (4) unit primary residences

(attached or detached), • one (1) unit second homes (attached or

detached), provided the mortgage being refinanced was a second home transaction,

• one (1) to four (4) unit investment properties (attached or detached), provided the mortgage being refinanced was an investment property,

Notes: • Manufactured homes are NOT eligible. • If the mortgage being refinanced was

previously a second home or investment property and the borrower(s) is now disclosing that the property is a primary residence (i.e., borrower(s) on the note are now owner occupants), then evidence of primary residency must be documented in the loan file.

Note: It is acceptable for a borrower’s occupancy to change from a primary residence to a second home or investment property.

• Eligible occupancy/property types include the following: • one (1) to two (2) unit primary residences

(attached or detached), • one (1) unit second homes (attached or

detached), provided the mortgage being refinanced was a second home transaction,

• one (1) unit investment properties (attached or detached), provided the mortgage being refinanced was an investment property,

Notes: • 3-4 unit primary residences, 2-4 unit

investment properties and manufactured homes are NOT eligible.

• If the mortgage being refinanced was previously a second home or investment property and the borrower(s) is now disclosing that the property is a primary residence (i.e., borrower(s) on the note are now owner occupants), then evidence of primary residency must be documented in the loan file.

Note: It is acceptable for a borrower’s occupancy to change from a primary residence to a second home or investment property.

• condominiums and units in a PUD, and • modular housing.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 22 of 49Broker Seller Guide

Occupancy/Property Types, Continued Agency Plus, (continued)

STM to STM Transactions Non-STM to STM Transactions

• condominiums and units in a PUD, and • modular housing.

Notes: • A PUD review/warranty is not required on Freddie

Mac Relief Refinance STM to STM transactions. • Condominium properties must be Fannie Mae

accepted, on SunTrust Mortgage’s Approved Condominium Project List, or warranted under the SunTrust Project Review process (i.e., Limited Project Review or Full Project Review).

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for warranty guidelines.

• The Certification of Project Compliance: Condominium Lender Warranties - Agency and Non-Agency Loan Products (BRO 0212b) must be completed and included in every Freddie Mac Relief Refinance loan file.

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for additional information.

• All other standard Agency Plus occupancy/property

guidelines (i.e., ineligible occupancy/property type guidelines) apply.

Reference: See Section 2.03: Agency Plus Loan Program of the Broker Seller Guide for standard Agency Plus occupancy/property guidelines.

Notes: • On attached PUDs, a PUD

review/warranty is required. • Condominium properties must be

Fannie Mae accepted, on SunTrust Mortgage’s Approved Condominium Project List, or warranted under the SunTrust Project Review process (i.e., Limited Project Review or Full Project Review).

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for warranty guidelines.

• The Certification of Project Compliance: Condominium Lender Warranties - Agency and Non-Agency Loan Products (BRO 0212b) must be completed and included in every Freddie Mac Relief Refinance loan file.

Reference: See Section 1.13: SunTrust Condominium and PUD Approval Requirements of the Broker Seller Guide for additional information.

• All other standard Agency Plus occupancy/property guidelines (i.e., ineligible occupancy/property type guidelines) apply.

Reference: See Section 2.03: Agency Plus Loan Program of the Broker Seller Guide for standard Agency Plus occupancy/property guidelines.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 23 of 49Broker Seller Guide

Eligible Borrowers

General The table below provides information on eligible borrowers for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions • A borrower may be added or removed from the

new loan provided at least one (1) borrower from the existing mortgage remains on the new mortgage. The following requirements will apply: • The borrower(s) being removed from the loan

must also be removed from the deed (i.e., title). • Evidence must be provided that the remaining

borrower(s) have been making the payments from his or her own funds for twelve (12) consecutive months prior to the origination of the new mortgage • Twelve (12) months cancelled checks or

bank statements (if automatic draft) must be documented in the loan file

• The account being used to document the twelve (12) months payments must reflect the remaining borrower(s) as the owner of the account.

Notes: • If a borrower is being removed due to death

then the following applies: • Twelve (12) month payment history is NOT

required. • A copy of the death certificate or other legal

document evidencing the borrower’s death must be obtained.

• A non-occupant borrower may NOT be added to a mortgage secured by a primary residence.

• Adding or removing a borrower is allowed when subordinating a SunTrust second mortgage (Combo Second Mortgage, EZ Two, SunTrust Equity Line or Equity Loan).

• The SunTrust second mortgage cannot be modified, regardless of whether borrower(s) are added to, or removed from, the first mortgage, and

• the borrower(s) currently obligated on the SunTrust second mortgage must remain.

• A borrower may be added to or removed from the new loan provided at least one (1) borrower from the existing mortgage remains on the new mortgage. The following requirements will apply: • The borrower(s) being removed from

the loan must also be removed from the deed (i.e., title).

• Evidence must be provided that the remaining borrower(s) have been making the payments from his or her own funds for twelve (12) consecutive months prior to the origination of the new mortgage.

• Twelve (12) months cancelled checks or bank statements (if automatic draft) must be documented in the loan file.

• The account being used to document the twelve (12) month payments must reflect the remaining borrower(s) as the owner of the account.

Notes: • If a borrower is being removed due to

death then the following applies: • Twelve (12) month payment history is

NOT required. • A copy of the death certificate or other

legal document evidencing the borrower’s death must be obtained.

• A non-occupant borrower may NOT be added to a mortgage secured by a primary residence.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 24 of 49Broker Seller Guide

Eligible Borrowers, Continued General, (continued)

STM to STM Transactions Non-STM to STM Transactions

See previous page for information.

Notes: (continued) • Adding or removing a borrower is

allowed when subordinating a SunTrust second mortgage (Combo Second Mortgage, EZ Two, SunTrust Equity Line or Equity Loan).

• The SunTrust second mortgage cannot be modified, regardless of whether borrower(s) are added to, or removed from, the first mortgage, and

• the borrower(s) currently obligated on the SunTrust second mortgage must remain.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 25 of 49Broker Seller Guide

Income

Income Documentation Requirements

The table below provides income documentation requirements for Agency and Agency Plus Freddie Mac Relief Refinance loan transactions.

STM to STM Transactions Non-STM to STM Transactions • LP will determine the level of income

documentation required.

Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for additional information.

• All IRS 4506-T requirements must be met.

Reference: See the “IRS 4506-T” subtopic in Section 1.05: Closing Information of the Broker Seller Guide for IRS Form 4506-T requirements at application and at closing.

STM to STM guidelines apply with the following EXCEPTIONS: • Self-Employed/Commission: Income must be

documented in accordance with standard Agency non-AUS guidelines.

Reference: See Section 2.01: Agency Loan Programs and Section 2.03: Agency Plus Loan Program of the Broker Seller Guide for non-AUS income documentation requirements.

STM Internal Information ONLY Reference: See the “Income Validation Procedures” for additional information on the proper documentation of tax returns.

Qualifying Guidelines

Qualifying Rate The table below provides information on qualifying rates for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

• For fully amortizing fixed rate and 7/1, and 10/1 LIBOR ARMs, the borrower(s) qualifies at the note rate.

• For fully amortizing 5/1 LIBOR ARMs, the borrower(s) qualifies at the greater of the actual Note rate plus 2% or the fully indexed rate (margin plus current index value).

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 26 of 49Broker Seller Guide

Qualifying Guidelines, Continued

Qualifying Ratios – Agency

The table below provides qualifying ratio information for Agency Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

Qualifying ratios will be determined by LP.

• The maximum debt to income ratio is 45.00%. • If the borrower’s proposed mortgage P&I

payment increases by more than 20% of the current mortgage P&I (or Interest Only) payment, then the maximum qualifying ratios are 31/45%.

Note: If the transaction includes the subordination of a second lien, the DTI ratio MUST include the second lien payment. A reduction to the credit line may be required in order to meet the TLTV/HTLTV requirements.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 27 of 49Broker Seller Guide

Qualifying Guidelines, Continued

Qualifying Ratios – Agency Plus

The table below provides qualifying ratio information for Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

Qualifying ratios will be determined by LP.

• The maximum debt to income ratio is 45.00%, regardless of the LTV.

• If the borrower’s proposed mortgage P&I payment increases by more than 20% of the current mortgage P&I (or Interest Only) payment, then the maximum qualifying ratios are 31/45%.

Note: If the transaction includes the subordination of a second lien, the DTI ratio MUST include the second lien payment. A reduction to the credit line may be required in order to meet the TLTV/HTLTV requirements.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 28 of 49Broker Seller Guide

Credit Requirements

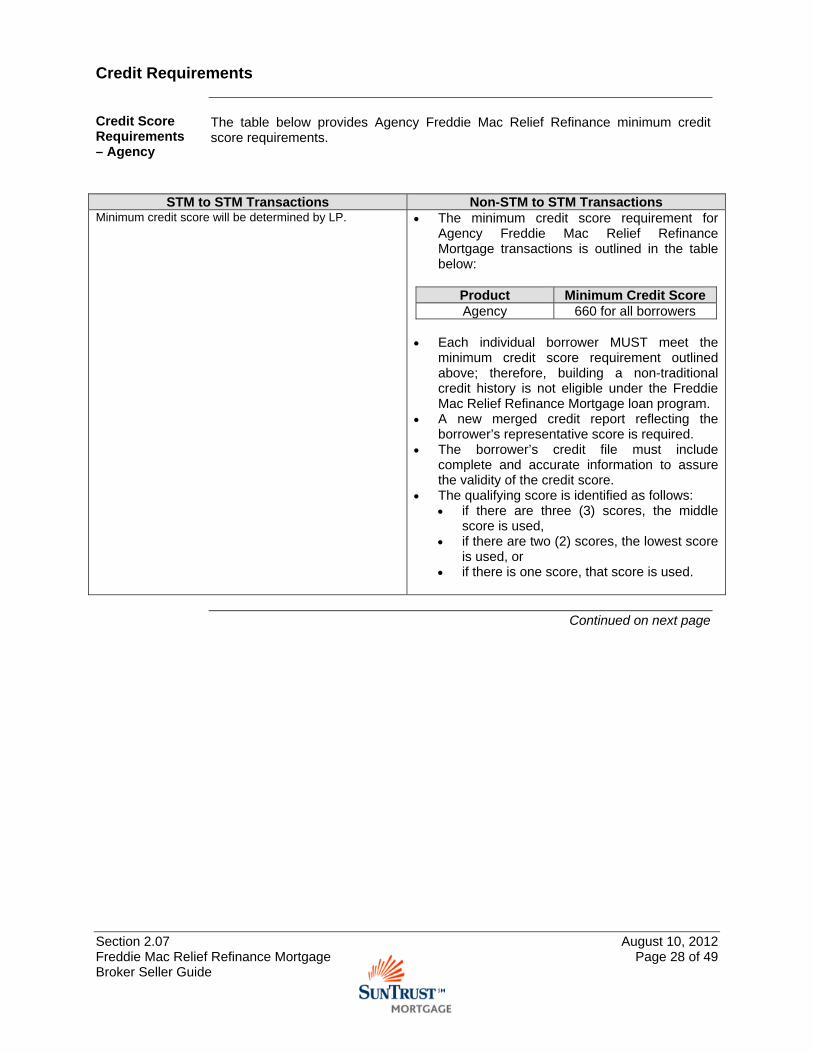

Credit Score Requirements – Agency

The table below provides Agency Freddie Mac Relief Refinance minimum credit score requirements.

STM to STM Transactions Non-STM to STM Transactions

Minimum credit score will be determined by LP.

• The minimum credit score requirement for Agency Freddie Mac Relief Refinance Mortgage transactions is outlined in the table below:

Product Minimum Credit Score Agency 660 for all borrowers

• Each individual borrower MUST meet the

minimum credit score requirement outlined above; therefore, building a non-traditional credit history is not eligible under the Freddie Mac Relief Refinance Mortgage loan program.

• A new merged credit report reflecting the borrower’s representative score is required.

• The borrower’s credit file must include complete and accurate information to assure the validity of the credit score.

• The qualifying score is identified as follows: • if there are three (3) scores, the middle

score is used, • if there are two (2) scores, the lowest score

is used, or • if there is one score, that score is used.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 29 of 49Broker Seller Guide

Credit Requirements, Continued

Credit Score Requirements – Agency Plus

The table below provides Agency Plus Freddie Mac Relief Refinance minimum credit score requirements.

STM to STM Transactions Non-STM to STM Transactions Minimum credit score will be determined by LP.

• The minimum credit score requirements for Agency Plus Freddie Mac Relief Refinance Mortgage transactions are outlined in the table below:

Note: If the existing loan required MI (i.e. if the original LTV of the existing loan was > 80% and existing MI coverage is still in force, etc.), then the maximum loan-to-value (LTV) is limited to 80% or less.

Reference: See the “Loan Terms” topic for maximum loan-to-value (LTV/TLTV/HTLTV) requirements.

• Primary Residence - Fixed Rate:

Minimum Credit Score • 1 Unit Properties:

• LTV/TLTV/HTLTV 80.01 – 90%: 720 for all borrowers

• LTV/TLTV/HTLTV 75.01 – 80%: 700 for all borrowers

• LTV/TLTV/HTLTV </= 75%: 660 for all borrowers

• 2 Unit Properties • 740 for all borrowers

• Primary Residence – ARMs:

Minimum Credit Score • 1 Unit Properties:

• 680 for all borrowers • 2 Unit Properties:

• 740 for all borrowers

• Second Homes – Fixed Rate and ARMs:

Minimum Credit Score

740 for all borrowers

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 30 of 49Broker Seller Guide

Credit Requirements, Continued

Credit Score Requirements – Agency Plus, (continued)

STM to STM Transactions Non-STM to STM Transactions

See previous page for information.

• Investment Properties – Fixed Rate and ARMs:

Minimum Credit Score

740 for all borrowers

• Each individual borrower MUST meet the

minimum credit score requirements outlined above; therefore, building a non-traditional credit history is not eligible under the Freddie Mac Relief Refinance Mortgage loan program.

• A new merged credit report reflecting the borrower’s representative score is required.

• The borrower’s credit file must include complete and accurate information to assure the validity of the credit score.

• The qualifying score is identified as follows: • if there are three (3) scores, the middle

score is used, • if there are two (2) scores, the lowest score

is used, or • if there is one score, that score is used.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 31 of 49Broker Seller Guide

Credit Requirements, Continued

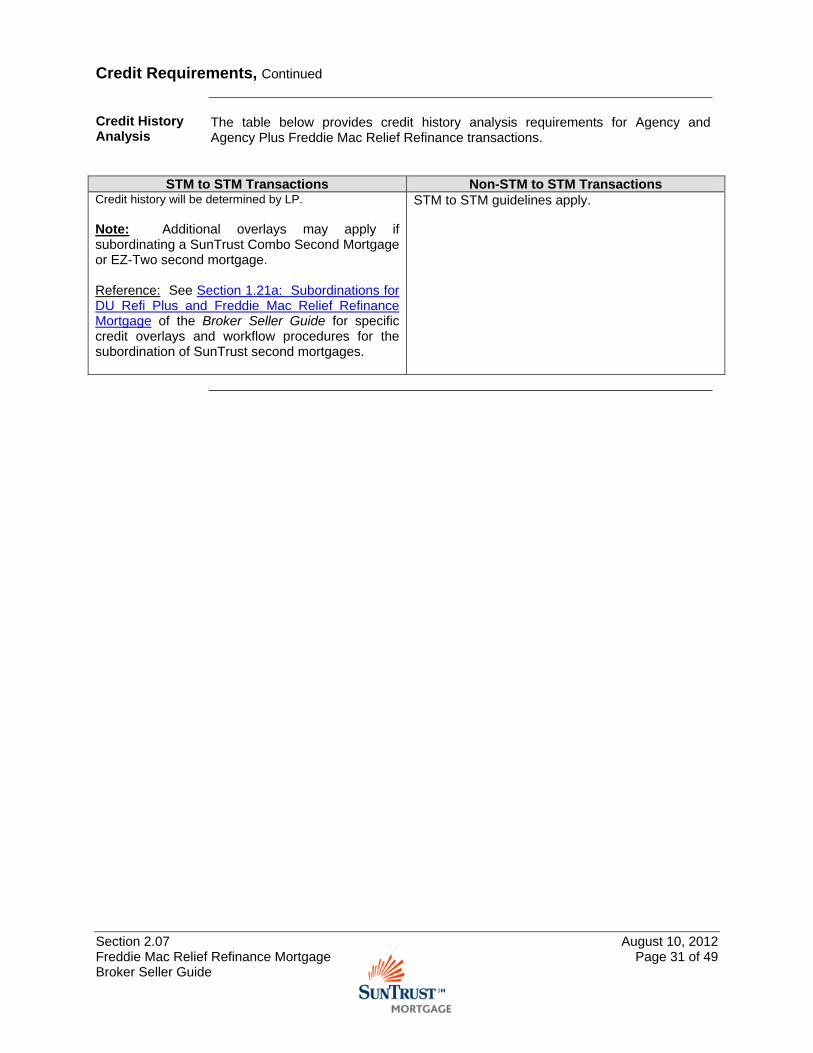

Credit History Analysis

The table below provides credit history analysis requirements for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

Credit history will be determined by LP. Note: Additional overlays may apply if subordinating a SunTrust Combo Second Mortgage or EZ-Two second mortgage. Reference: See Section 1.21a: Subordinations for DU Refi Plus and Freddie Mac Relief Refinance Mortgage of the Broker Seller Guide for specific credit overlays and workflow procedures for the subordination of SunTrust second mortgages.

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 32 of 49Broker Seller Guide

Cash Requirements

General Asset documentation will be determined by LP.

Cash Reserves The table below provides cash reserve requirements for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

LP will determine the level of reserves required. STM to STM guidelines apply.

Gifts The table below provides information on gifts for Agency and Agency Plus Freddie Mac Relief Refinance Mortgage transactions.

STM to STM Transactions Non-STM to STM Transactions

Gifts must be documented in accordance with standard Agency LP guidelines. Reference: See Section 2.01: Agency Loan Programs of the Broker Seller Guide for additional information.

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 33 of 49Broker Seller Guide

Contributions by Interested Parties

Lender Credits The table below provides information on lender credits for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

Standard Agency LP and Agency Plus guidelines apply.

Reference: See Section 2.01: Agency Loan Programs and Section 2.03: Agency Plus Loan Program of the Broker Seller Guide for additional information.

STM to STM guidelines apply.

Temporary Interest Rate Buydowns

The table below provides information on temporary interest rate buydowns for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

Temporary interest rate buydowns, including the SunTrust ARM Alternative, are NOT eligible.

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 34 of 49Broker Seller Guide

Mortgage Insurance

General The table below provides information on mortgage insurance for Agency and Agency Plus Freddie Mac Relief Refinances transactions.

STM to STM Transactions Non-STM to STM Transactions • Use the Fidelity Snapshot to determine if the existing first mortgage

has MI. The LP Feedback Certificate will also provide MI information (if applicable). Discrepancies between the Fidelity Snapshot results and the LP Feedback Certificate must be addressed.

Note: An Excel spreadsheet titled Fidelity Loan Data Retriever is used to obtain the Fidelity Snapshot. Click here to access the Fidelity Loan Data Retriever spreadsheet.

Reference: See the “Workflow” topic subsequently presented in this product description for workflow procedures for obtaining the Fidelity Snapshot.

• Section 1.08a: Mortgage Insurance - Home Affordable Refinance Program (HARP) of the Broker Seller Guide MUST be reviewed for EVERY loan requiring mortgage insurance (MI)

• New refinance transactions with LTVs </= 80% do not require MI, regardless if the existing loan has MI.

• For a loan-to-value greater than 80%, the following applies: • If the existing mortgage has MI coverage, then the same

percentage of coverage must be maintained for the new mortgage on the entire principal balance.

• Loans originated with the same level of MI coverage as on the existing loan will require a transfer and/or modification of the existing MI coverage to the new loan.

• If the existing mortgage did not have MI coverage, then no MI coverage is required for the new Freddie Mac Relief Refinance Mortgage.

• Existing loans with lender paid mortgage insurance (LPMI) are eligible.

Note: The Lender Paid Private Mortgage Insurance Notice (BRO 1305) must be signed by all borrowers at the time of loan commitment.

References: • See the “Fidelity Snapshot” subtopic located in the “Workflow”

topic subsequently presented in this product description for additional information regarding workflow procedures for obtaining MI information on the existing loan.

• See Section 1.08a: Mortgage Insurance - Home Affordable Refinance Program (HARP) of the Broker Seller Guide for additional information regarding transferring/modifying the existing MI coverage to the new loan, as well as MI data input for MLCS.

• New refinance transactions with LTVs </= 80% do not require MI, regardless if the existing loan has MI.

• If the original LTV of the existing loan was </= 80% or if the LTV was > 80%; however, the existing loan does not have mortgage insurance (MI previously canceled or terminated), then MI coverage is not required on the new loan. • The maximum loan-to-

value (LTV) guidelines for Non-STM to STM (MI NOT REQUIRED on Original Loan) must be followed.

Reference: See the “Loan Terms” topic for maximum loan-to-value (LTV) requirements.

• If the existing loan required MI (i.e., if the original LTV of the existing loan was > 80% and existing MI coverage is still in force, etc.), then the maximum loan-to-value (LTV) is limited to 80% or less. • The maximum loan-to-

value (LTV) guidelines for Non-STM to STM (MI REQUIRED on Original Loan) must be followed.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 35 of 49Broker Seller Guide

Documentation Requirements

General The table below provides documentation requirements for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

Unless otherwise outlined in this product description, Freddie Mac Relief Refinance Mortgage transactions must be documented in accordance with the requirements outlined on the Agency product description, which includes obtaining a new 1003. Reference: See the “Appraisal Requirements” topic subsequently presented in this product description for additional information regarding appraisal documentation requirements.

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 36 of 49Broker Seller Guide

Appraisal Requirements

General The table below provides appraisal requirements for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM Transactions

• Freddie Mac Relief Refinance Mortgage loan transactions must be documented with either a full appraisal (i.e., Fannie Mae Form 1004/Freddie Mac Form 70 [Uniform Residential Appraisal Report], Fannie Mae Form 1073/Freddie Mac Form 465 [Individual Condominium Unit Appraisal Report], etc), or the Home Value Explorer® (HVE) point value estimate indicated on the LP findings.

Reference: See the “Home Value Explorer® (HVE) Requirements” subtopic subsequently presented within this topic.

• The applicable appraisal code must be entered

into MLCS. References: • See Section 1.06: Appraisal Guidelines of the

Broker Seller Guide for additional information concerning appraisals and appraisal requirements.

• See the “Appraisal Codes” subtopic in the “MLCS Loan Setup and Processing” topic subsequently presented in this product description for appraisal code requirements.

STM to STM guidelines apply.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 37 of 49Broker Seller Guide

Appraisal Requirements, Continued

Home Value Explorer® (HVE) Requirements

The table below provides Home Value Explore® (HVE) requirements for Agency and Agency Plus Freddie Mac Relief Refinance transactions.

STM to STM Transactions Non-STM to STM

Transactions • Home Value Explorer is a Freddie Mac AVM tool that provides an estimated property value.

HVE reports provide a Forecast Standard Deviation and Confidence Score, indicating the accuracy of the estimated value. HVE Forecast Deviation scores of 0.20 and lower indicate that the degree of confidence in the valuation estimate is of a high or medium level. Forecast Standard Deviation scores above 0.20 indicate that the degree of confidence in the valuation estimate is low.

• For certain Freddie Mac Relief Refinance Mortgage transactions, the requirement for an appraisal may be waived. In lieu of an appraisal, the HVE value identified in the Loan Prospector (LP) Feedback Certificate is eligible to determine the subject property value.

• If an HVE value is available, the LP Feedback Certificate provides the following: • HVE value, • HVE Forecast Standard Deviation, and • HVE Confidence Score.

• To exercise the HVE option, confirm the following outside of LP: • an appraisal has not been obtained for the transaction, • the Forecast Standard Deviation (stated on the LP Feedback Certificate) is no greater

than 0.20 (corresponding to a confidence score of “H” [high] or “M” [medium]), • the property is a one-to-two unit (attached or detached) dwelling, including a unit in a

condominium or PUD project,

Note: Three-to-four units, leasehold properties, properties with rural characteristics, mixed-used properties, and properties located in a declared disaster area are not eligible for the HVE option. These properties require a full appraisal.

• the date of the HVE value (i.e., LP Feedback Certificate transaction date) is within 120 calendar days of the note date, and

• the applicable state law does not require a full appraisal • There is no fee for exercising the HVE option. • Mortgage insurance (MI) can be removed if the HVE value reduces the LTV to 80% or less. • If you resubmit a loan to LP and LP returns a higher HVE value, you may use the higher

value. • If the HVE value is greater than 120 calendar days old on the note date:

• use a more recent, unexpired HVE value, or • resubmit the loan to LP and obtain an updated HVE value.

STM Internal Information Only • An appraisal code of “A – Automated Valuation Model” must be entered into MLCS.

Reference: See the “Appraisal Codes” subtopic in the “MLCS Loan Setup and Processing” topic subsequently presented in this product description for appraisal code requirements.

• The Notice About Appraisal of Your Property disclosure, indicating that the borrower

understands his/her loan did not have an appraisal, is automatically generated in the closing package based on entering the appraisal code of “A” in MLCS.

• For STM to STM transactions, no CoreLogic Report is required. Reference: See the “Workflow” topic subsequently presented in this product description for Home Value Explore® (HVE) Documentation Procedures for additional information.

STM to STM guidelines apply with the following EXCEPTION: • For non-STM to

STM transactions, , a Mini CoreLogic Report is automatically generated.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 38 of 49Broker Seller Guide

AUS Submissions, Recommendations and Tolerances

General • ALL Freddie Mac Relief Refinance Mortgages MUST be processed through

Freddie Mac’s Loan Prospector (LP) and receive an “Accept/Eligible” recommendation.

Reference: See the “Workflow” topic subsequently presented in this product description for additional information on submissions to LP.

• Freddie Mac Relief Refinance Mortgage transactions that are traditionally underwritten, receive a LP “Caution” recommendation or processed through Fannie Mae’s Desktop Underwriter (DU) or SunTrust’s Custom Desktop Underwriter (CDU) are NOT eligible.

• The Freddie Mac Relief Refinance Mortgage Eligibility Checklist (STM to STM) (BRO 1380) or Freddie Mac Relief Refinance Mortgage Eligibility Checklist (Non-STM to STM) (BRO 1415) and Freddie Mac Relief Refinance Maximum Allowable Financed Closing Costs, Financing Costs, and Prepaids/Escrows (BRO 0008) worksheet is REQUIRED to be completed and placed in the loan file to ensure that the loan is being originated within the guidelines of the Freddie Mac Relief Refinance Mortgage program.

• The maximum number of LP submissions for the Freddie Mac Relief Refinance Mortgage loan program is limited to ten (10). Written documentation/justification must be provided in the loan file for underwriter review/approval when the number of LP submissions exceed ten (10).

Reference: See Section 1.03a: Automated Underwriting of the Broker Seller Guide for additional information.

• When the loan casefile is submitted to LP, LP will determine if the loan matches

and is an existing eligible Freddie Mac owned mortgage.

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 39 of 49Broker Seller Guide

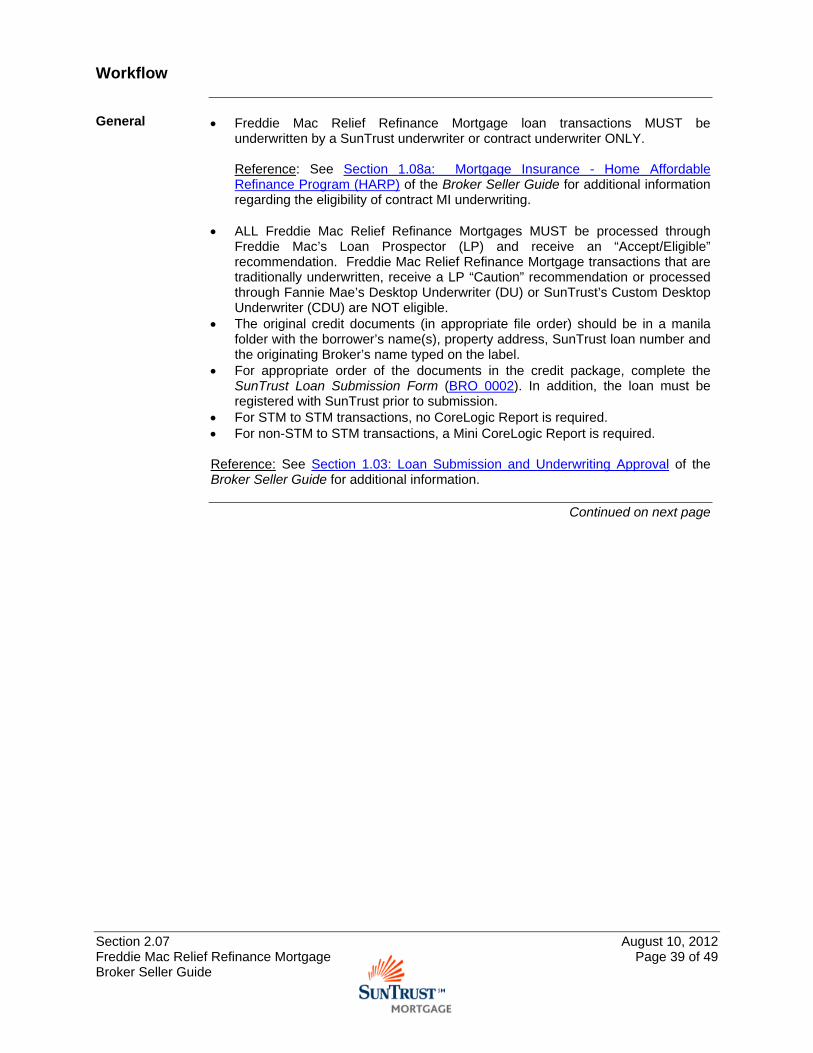

Workflow

General • Freddie Mac Relief Refinance Mortgage loan transactions MUST be

underwritten by a SunTrust underwriter or contract underwriter ONLY. Reference: See Section 1.08a: Mortgage Insurance - Home Affordable Refinance Program (HARP) of the Broker Seller Guide for additional information regarding the eligibility of contract MI underwriting.

• ALL Freddie Mac Relief Refinance Mortgages MUST be processed through

Freddie Mac’s Loan Prospector (LP) and receive an “Accept/Eligible” recommendation. Freddie Mac Relief Refinance Mortgage transactions that are traditionally underwritten, receive a LP “Caution” recommendation or processed through Fannie Mae’s Desktop Underwriter (DU) or SunTrust’s Custom Desktop Underwriter (CDU) are NOT eligible.

• The original credit documents (in appropriate file order) should be in a manila folder with the borrower’s name(s), property address, SunTrust loan number and the originating Broker’s name typed on the label.

• For appropriate order of the documents in the credit package, complete the SunTrust Loan Submission Form (BRO 0002). In addition, the loan must be registered with SunTrust prior to submission.

• For STM to STM transactions, no CoreLogic Report is required. • For non-STM to STM transactions, a Mini CoreLogic Report is required. Reference: See Section 1.03: Loan Submission and Underwriting Approval of the Broker Seller Guide for additional information.

Continued on next page

Section 2.07 August 10, 2012Freddie Mac Relief Refinance Mortgage Page 40 of 49Broker Seller Guide

Workflow, Continued

Fidelity Snapshot – STM to STM Transactions

The workflow procedures for SunTrust employees who are obtaining a “snapshot” from Fidelity for borrowers who are refinancing an existing SunTrust first mortgage (STM to STM transactions) are outlined below: • You must have a MSP (Fidelity) sign on to access. The ID starts with “AM”.

Access is requested via the FastForm for users who do not already have this access.

• The Bluezone application must be installed on your PC or laptop. This is a standard install on all SunTrust computers. • Click on Start, Programs, Bluezone to verify. • If for any reason you do not have Bluezone on your computer, you must

complete an EIS Request to obtain. • An Excel spreadsheet titled Fidelity Loan Data Retriever is used to obtain the

Fidelity snapshot. Click here to access the Fidelity Loan Data Retriever spreadsheet. • This spreadsheet should be saved to your desktop for easy access. Click

here for instructions on how to save the Fidelity Loan Data Retriever tool to the computer desktop.